Abstract

Drawing on extensive case study evidence, this study unpacks sustainability reporting’s evolution from a moral values–based practice toward a financialized value–based one. We argue that this transition can be seen as a commensuration project. We examine the dynamics of this process and its implications for sustainability-related outcomes. We find that increased levels of commensuration have moved sustainability reporting away from an original emphasis on morality and values to a focus on strategic value creation for the firm. We theorize this process as a “crowding out of morality” that is enabled by a rigid cognitive framing of social and environmental issues (objectification) and the monetized coordination of relevant social interactions (marketization). We outline implications of our analysis for the scholarly debates on the institutionalization of sustainability reporting and commensuration.

Introduction

Sustainability reporting, defined by the Global Reporting Initiative (GRI, 2016, p. 3) as an “organization’s practice of reporting publicly on its economic, environmental, and/or social impacts, and hence its contributions—positive or negative—towards the goal of sustainable development” has gained considerable prominence. A peripheral practice at the start of the century, nowadays 80% of the largest 100 companies in 52 countries studied issue reports, as do 96% of world’s largest 250 companies (KPMG, 2020). As the idea behind nonfinancial disclosure is to improve sustainable development and combat unaccountability and non-transparency of firms (Gray, 1992; Gray et al., 1988), at first glance this institutionalization appears a success. Critics argue, however, that reporting has become increasingly captured within a discourse of business-as-usual firm-value creation (Gray, 2006, 2010; Milne et al., 2009; Spence, 2007; Tregidga et al., 2014, 2018), leading some to suggest that “the one thing that you cannot learn from a sustainability report is the contribution to/detraction from sustainability that the organization has made” (Milne & Gray, 2013, p. 17).

Prior work has looked extensively at determinants of sustainability reporting (Hahn & Kühnen, 2013; Kuzey & Uyar, 2017; Pucheta-Martínez & Gallego-Álvarez, 2020; Schreck & Raithel, 2018) and draws on institutional theory conceptualizing reporting as a purposive and strategic practice for legitimation and stakeholder management (Borgstedt et al., 2019; Comyns, 2018; Cooper & Owen, 2007; Haffar & Searcy, 2020; Higgins et al., 2018; Luo et al., 2017; van Halderen et al., 2016). Although several studies have theorized the development of sustainability reporting as a process of institutionalization (Contrafatto, 2014; de Villiers & Alexander, 2014; Etzion & Ferraro, 2010), the role of the increasing focus on measurement and financial valuation within such institutionalization processes has remained largely unexplored. However, measurement and a focus on financial value has increasingly shaped sustainability reporting (Rowbottom & Locke, 2016) and has therefore also impacted its institutionalization. Our study aims to clarify the relationship between the institutionalization of sustainability reporting and this increasing focus on measurement and financial valuation by studying reporting as a commensuration project; a project that was based on the emergent collective effort of various actors (e.g., standard setters, auditors, investors) over time.

Commensuration, viewed as “the process whereby different qualities are measured with a single standard or unit” (Samiolo, 2012, p. 383) transforms qualities into quantities and differences into sameness (Espeland & Stevens, 1998). Scholars have argued that the effects of commensuration relate to its potential to recreate social worlds (Espeland & Sauder, 2007; Mennicken & Espeland, 2019), the erasure of uncertainty (Quinn, 2008), and more generally the creation of markets (Kolk et al., 2008; Levin & Espeland, 2002). We therefore aim to answer the following research question:

We draw on a qualitative study of the history of sustainability reporting in the Netherlands, which has historically been one of the frontrunners in adopting this practice (KPMG, 2011; PwC, 2012). We use a form of historical narrative analysis (Ansari & Phillips, 2011; Leblebici et al., 1991) to map the sequences of events (Greenwood & Suddaby, 2006) that took place as sustainability reporting commensurated. Drawing on 111 semi-structured interviews and secondary data, we show that four dimensions impacted the commensuration of sustainability reporting and that these dimensions shaped different phases of reporting’s institutionalization over time. Actors first engaged in proto-commensuration—that is, they established a meaning system in which previously unrelated aspects (business and sustainability) started to become related. During proto-commensuration a moral undertone characterized the debate. Reporting was shaped by peoples’ personal convictions as well as an emphasis on corporate and societal values. Actors made the “moral case” for sustainability and hence brought business and sustainability closer together. After this, reporting moved into a phase of technical commensuration where different stakeholder groups developed standards, indicators, and benchmarks. After this technical work enabled some degree of quantification and comparability, the demarcation between financial and nonfinancial reporting started to blur and value commensuration moved the added financial value of firms’ sustainability engagements center stage. This value commensuration triggered cognitive commensuration processes in the sense that the meaning of sustainability itself was increasingly defined around capturing environmental, social, governance (ESG) issues that enhance financial firm value.

Our findings contribute to the literatures on sustainability reporting and commensuration. First, we extend the literature discussing the institutionalization of sustainability reporting. This literature has investigated the dynamics by which reporting turned into an established phenomenon within and among firms (Contrafatto, 2014). While most of this literature discusses isomorphic mechanisms and the resulting taken-for-grantedness of reporting (Aerts et al., 2006; de Villiers & Alexander, 2014; Shabana et al., 2017), our discussion shows how different dimensions of commensuration slowly enabled a focus on standards and indicators which then helped to link ESG issues with firm’s financial value. These findings complement existing insights on the institutionalization of reporting. For instance, while studies on inter-firm isomorphism (Shabana et al., 2017) have highlighted the central role of standards, our study shows how these standards emerged through commensuration work. A focus on commensuration therefore demonstrates how the emerging focus on measurement and comparability impacted how reporting practices became broadly accepted.

Second, we also extend the literature on commensuration by showing that measurement can narrow our appraisal of how value is understood. Surprisingly little attention has been devoted to the relationship between commensuration and morality (Espeland & Sauder, 2007; Espeland & Yung, 2019; Järvinen et al., 2020). As Espeland and Sauder (2007, p. 36) remark, “we do not typically associate ethics with measurement.” Our findings show that increased levels of commensuration have moved sustainability reporting away from a focus on values and morality to a focus on strategic value creation for the firm. We theorize this slow but steady “crowding out of morality” as being influenced by two processes: the rigid cognitive framing of social and environmental issues (objectification) and the monetized coordination of relevant social interactions (marketization), both of which were shaped by the four dimensions of commensuration mentioned above (proto, technical, value, and cognitive). We therefore emphasize that commensuration can favor situations in which instrumental and economic notions of value dominate at the expense of other ways of knowing. We do not suggest that a focus on financial value creation is necessarily “bad” or “wrong.” Rather, our analysis highlights that as reporting shifted from an emphasis of values toward an orientation focused on financial value creation, it became more difficult to associate ESG issues with potential moral dilemmas.

Theoretical Background

Institutionalization of Sustainability Reporting

The widespread nature of sustainability reporting, at least among larger firms, has led to the claim that the practice has become institutionalized over time (Cho et al., 2015)—that is, it has turned into a standard business practice that is taken-for-granted. The dynamics of this institutionalization process are well documented (see, e.g., Bebbington et al., 2012). Several studies have discussed the role of institutional entrepreneurs like the GRI (Etzion & Ferraro, 2010; Levy et al., 2010) as well as the role of larger epistemic communities including academics, corporations, and policymakers (e.g., Christophe & Bebbington, 1992). While several studies examined how isomorphic firm behavior spurred the diffusion of sustainability reporting at the field level (de Villiers & Alexander, 2014; Shabana et al., 2017), other research has examined how reporting has become institutionalized within firms. For instance, Contrafatto (2014) showed how a firm constructed a common meaning system around sustainability and how this system subsequently changed organizational routines and procedures. Finally, research has also discussed how the broader societal context influenced the institutionalization of sustainability reporting, such as Larrinaga and Bebbington’s (2021) argument that the societal conditions throughout the 1970s, 1980s, and 1990s provided a fertile ground for sustainability reporting to emerge.

Surprisingly little attention has been paid to the commensuration dynamics that surrounded this process. One reason for this omission is that many studies have adopted the lenses of either institutional theory (Etzion & Ferraro, 2010; Shabana et al., 2017) or legitimacy theory (O’Dwyer et al., 2011) to reflect on and explain institutionalization. We believe that including commensuration dynamics into the analysis can meaningfully extend current knowledge in this field. This is because sustainability reporting’s institutionalization was mostly driven by standards (e.g., the GRI and the International Integrated Reporting Council [IIRC]). These initiatives have attempted to reduce the complexity underlying ESG issues and tried to construct comparable disclosures. This complexity reduction was not a neutral process (Kolk et al., 2008) and hence affected the outcome of institutionalization in various ways. By studying the institutionalization of sustainability reporting from a commensuration lens, we hope to uncover how the resulting measurement and benchmarking has affected the disclosure of ESG information.

Commensuration

Commensuration “is a way to reduce and simplify disparate information into numbers that can easily be compared and this transformation allows people to quickly grasp, represent, and compare differences” (Espeland & Stevens, 1998, p. 316). It reduces the relevance of context and puts a value on and makes calculable and comparable what used to be incomparable. Commensuration thereby underpins the development of rationality and is a mechanism to study the emergence and objectification of practices (e.g., Huault & Rainelli-Weiss, 2011; Levin & Espeland, 2002; Quinn, 2008; Zelizer, 2005). It has been used to analyze a whole range of phenomena including academic rankings (Sauder & Espeland, 2009), peer reviewing (Lee, 2015), pension systems (Peeters et al., 2014), cost–benefit analyses (Lohmann, 2009; Porter, 1995; Samiolo, 2012), and the emergence of carbon measurement, accounting and disclosure (Kolk et al., 2008; Wegener et al., 2019). Commensuration is part of a growing influence of markets, comparability, transparency, and accountability in a society where measurability and reality increasingly coalesce (see, e.g., Meyer et al., 1994; Porter, 1995; Power, 1997).

Commensuration limits and systematizes the amount and complexity of information to process, which reduces uncertainty by obfuscating tensions between the metric and the underlying empirical reality (Quinn, 2008) and helps to facilitate trust and control (Fligstein, 1998; Levin & Espeland, 2002; Porter, 1995). Prior research has examined various consequences of commensuration, the primary one being its potential to facilitate market creation. For instance, MacKenzie (2009) showed how different greenhouse gases were made commensurable in order for carbon markets to function, while Kolk et al. (2008) emphasized that the definition of indicators like tCO2e (tons of carbon dioxide equivalent) helped to institutionalize carbon reporting.

Whatever the exact outcomes, commensuration is a difficult and at times controversial process. It helps to establish what is considered of value and importance but at the same time it also marks what is considered irrelevant and gets silenced (Järvinen et al., 2020; Mennicken & Espeland, 2019). Fligstein (1998) and Espeland and Yung (2019) maintained that particular power relations become normalized through commensuration, whereas others get silenced. This shows that in reality not all values can be made commensurate, and unsurprisingly commensuration does get contested (Gerdin & Englund, 2019). Therefore, questions remain about the tensions between commensuration’s formal rationality and ethical systems (Povinelli, 2001). Commensuration is typically not associated with ethics as it highlights neutrality, objectivity, fairness, and rationality. This veil of formal rationality obfuscates commensuration’s potential moral complications, which warrants further research (Espeland & Sauder, 2007; Espeland & Stevens, 2008; Espeland & Yung, 2019). Our study contributes to and extends these discussions at the intersection of commensuration and morality by uncovering some of the contested consequences of the commensuration of sustainability reporting.

Dimensions of Commensuration

Commensurative work can be classified into three distinct dimensions: technical, cognitive, and value commensuration (e.g., Kolk et al., 2008; Levin & Espeland, 2002). Technical commensuration is concerned with “measuring or classifying specific characteristics or practices more accurately” (Levin & Espeland, 2002, p. 126). On one hand, this has a mechanical aspect. In their studies on carbon disclosure, Kolk et al. (2008), Wegener et al. (2019), and MacKenzie (2009) discuss the technicalities of commensurating different greenhouse gases. They discuss the technical work involved in establishing the global warming potential (GWP) for the various greenhouse gases, thereby translating different gases into a common unit of CO2 equivalents. They show that in addition to the need for proper physical equipment and technologies to set up accurate measurements, also a social factor comes into play to reach consensus.

Value commensuration typically involves a pricing or monetary component. This is achieved through attempts to quantify or even monetize key performance indicators, but also by combining disparate elements and (e)valuating firms through rankings and ratings. The aim is to ease valuations by integrating different values into a common metric. For instance, prices have been attached to a ton of CO2 (MacKenzie, 2009), air pollution (Levin & Espeland, 2002), and weather risks (Huault & Rainelli-Weiss, 2011). Value commensuration attempts to adjudicate between conflicting values and reconcile and appease their differences by constructing an overarching metric. Finally, cognitive commensuration is a “more tacit cultural accomplishment, it involves reclassifying the world in terms of categories that align more closely with the new metrics” (Levin & Espeland, 2002, p. 126). This dimension of commensuration shapes how we understand and assign meaning to the world and categorize it. Previous studies have seen cognitive commensuration as a consequence of new metrics. Järvinen et al. (2020, p. 1) show how quantification promotes commensuration and leads to “limiting the discussion to themes and questions preferred by company management.” Commensuration thus determines what we see and value and how we understand the world.

Methods

Site Selection

Our original research aim was to better understand the institutionalization of sustainability reporting in the Netherlands. However, as we explain below, it soon became apparent that the commensuration literature provided a useful theoretical angle to better understand and explain reporting’s institutionalization. We decided to focus our analysis on the organizational field that has formed around sustainably reporting (Etzion & Ferraro, 2010; Kolk, 2010; Levy et al., 2010). Actors in this field include businesses, nongovernmental organizations (NGOs), governmental agencies, professional services firms, investors, and standard setters. The focus was on sustainability reporting in the Netherlands, keeping in mind its embeddedness in a wider European and global environment. The Netherlands has been one of the early frontrunners in reporting (KPMG, 2011). Following Jennings and Zandbergen (1995), we focus on a specific country since fields of sustainable practices are often local in character (see also Adams & Kuasirikun, 2000; Kolk, 2005). Dutch reporting picked up momentum in the late 1980s. By 2020, 88% of the largest 100 companies in the Netherlands published sustainability reports and the country was a frontrunner in integrated reporting (KPMG, 2020).

Sustainability reporting is a salient case study and a good example of commensuration (Järvinen et al., 2020). Putting social and environmental aspects into indicators, ratings, rankings, and financial figures makes sustainability reporting a salient commensuration project with various spheres claiming (in)commensurability (Espeland & Stevens, 1998). As the concept of sustainability blends social, environmental, and economic aspects, it gives rise to discussions about what is of value in a corporate context. Sustainability reporting therefore offers an exemplary case of an institutionalization process that was shaped by commensuration dynamics.

Data Collection

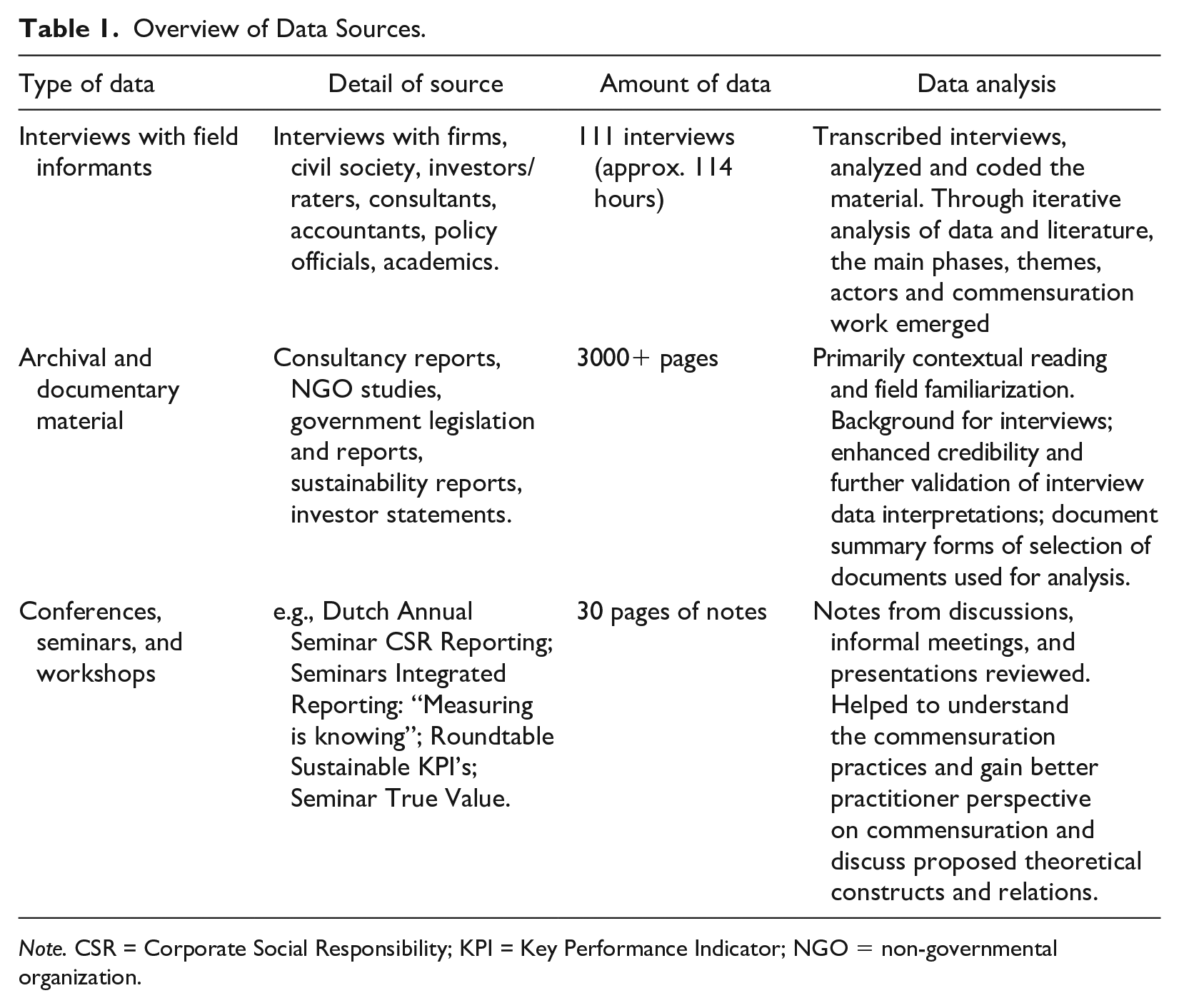

The data collection took place in several steps and relied on various data sources (see Table 1). To make ourselves familiar with the field, to test the appropriateness of the case, and to determine prospective interviewees, we closely read various documents (e.g., Dutch and European Union [EU] laws on reporting, KPMG reporting surveys, GRI Guidelines). The first author had previous contacts in the field which were also consulted. Based on this overview, a list of prospective interviewees was drawn up and interviewees were contacted. A requirement throughout the data collection process was that interviewees needed to have at least three years of experience in the field. As interviews were being conducted, the list of interviewees was continuously updated and a snowball sampling technique was applied based on recommendations of interviewees (Bryman & Bell, 2007).

Overview of Data Sources.

Note. CSR = Corporate Social Responsibility; KPI = Key Performance Indicator; NGO = non-governmental organization.

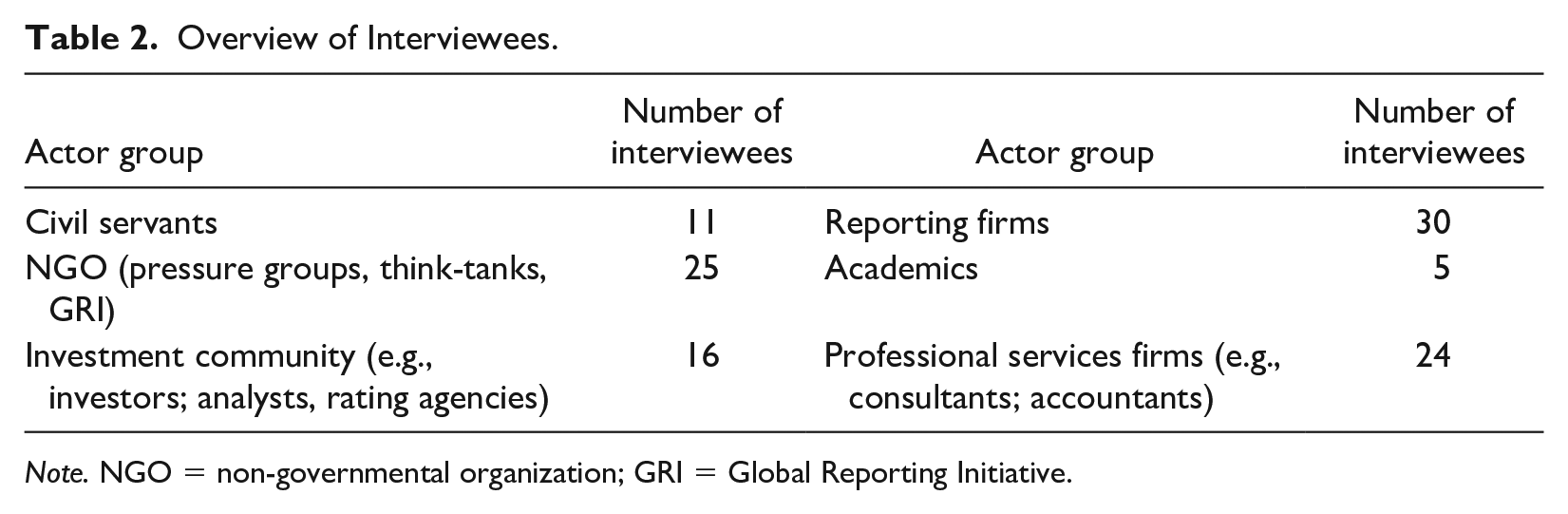

Interviews were conducted between 2011 and 2021. Data collection took place in two phases: 2011–2013 (94 interviews) and 2019–2021 (17 interviews). The first phase was part of a larger project around the institutionalization of sustainability reporting and provided insights into reporting’s historical roots, its emergence as a social practice, and its dissemination. These interviews already made clear that institutionalization was significantly influenced by standardization, quantification, and the development of measures. As time progressed, it became apparent (e.g., through informal meetings and attendance of events) that our initial observations about an increasing emphasis on standardization, measurement, and a focus on strategic value creation seemed to have advanced. We therefore decided to continue with a second round of interviews that zoomed in on these developments. Interviews during this second round focused on recent developments in the field and did not explicitly discuss reporting’s historical development as the first interview round did (hence fewer interviews in this round). Our approach allowed us to focus on contacting field actors with desired characteristics fitting the framing of the study, more akin to theoretical sampling (Strauss & Corbin, 1998). To make sure the multitude of positions present within the field were represented, and to prevent selection bias, we selected interviewees from various disciplines and positions in the field. Table 2 as well as Supplemental Appendix A and B provide further descriptive information of interviews and interviewees.

Overview of Interviewees.

Note. NGO = non-governmental organization; GRI = Global Reporting Initiative.

Interviews were semi-structured and in total 114 hours in length. Interviews were tape recorded and transcribed, with the exception of seven interviews where extensive notes were taken. These seven interviews were included in the open coding but not in the subsequent rounds of coding. For interviews that discussed the more distant history of reporting prior research was conducted (e.g., based on documents). This was done to ask specific questions, assist interviewees in structuring memories, come up with counterfactuals to test their statements, and limit the risk of retrospective bias (Eisenhardt & Graebner, 2007).

To supplement our primary data source (interviews), two other supporting data sources were consulted. First, government reports, legislation on sustainability reporting, publications of professional service firms, reports and statements of NGOs and investors, academic publications, and sustainability reports of companies were consulted. These data sources provided contextual reading and familiarization with the field, but also a form of checks and balances for the emerging dimensions and categories based on the coding of the interviews. We created document summary forms (Ansari & Phillips, 2011) that could later be used for coding alongside interview transcripts. Second, throughout the period of study we attended non-academic workshops, seminars, and conferences related to sustainability reporting (e.g., the Dutch Annual Seminar on CSR Reporting; Integrated Reporting Seminar; EU Reporting Seminar). Reflections on these events, nine in total, were recorded through field notes. This served a twofold purpose. On the one hand, these events allowed us to gain further insights into the reporting field, to track developments, and to find prospective interviewees. On the other hand, these events were also used to further triangulate the data sources.

Data Analysis

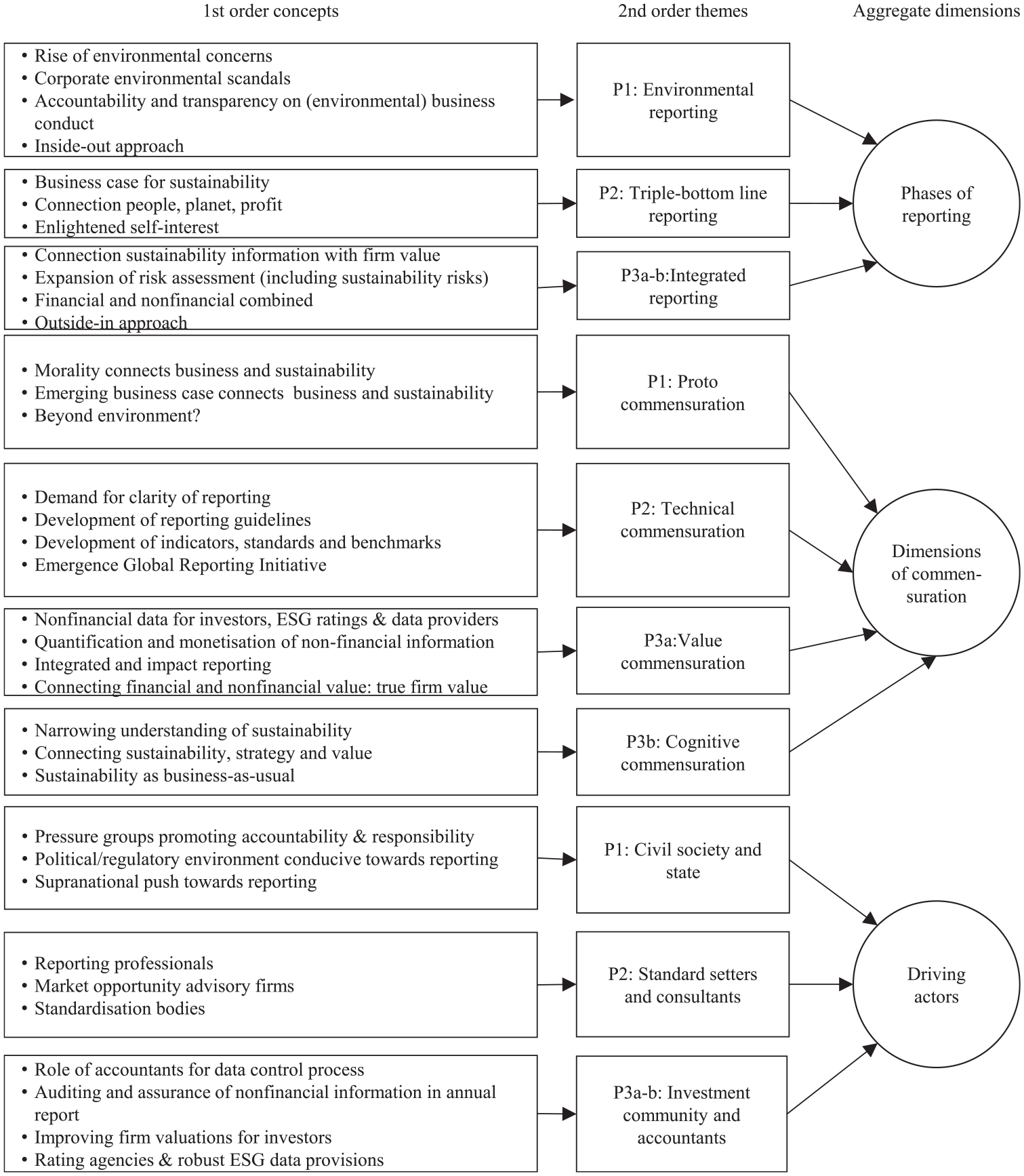

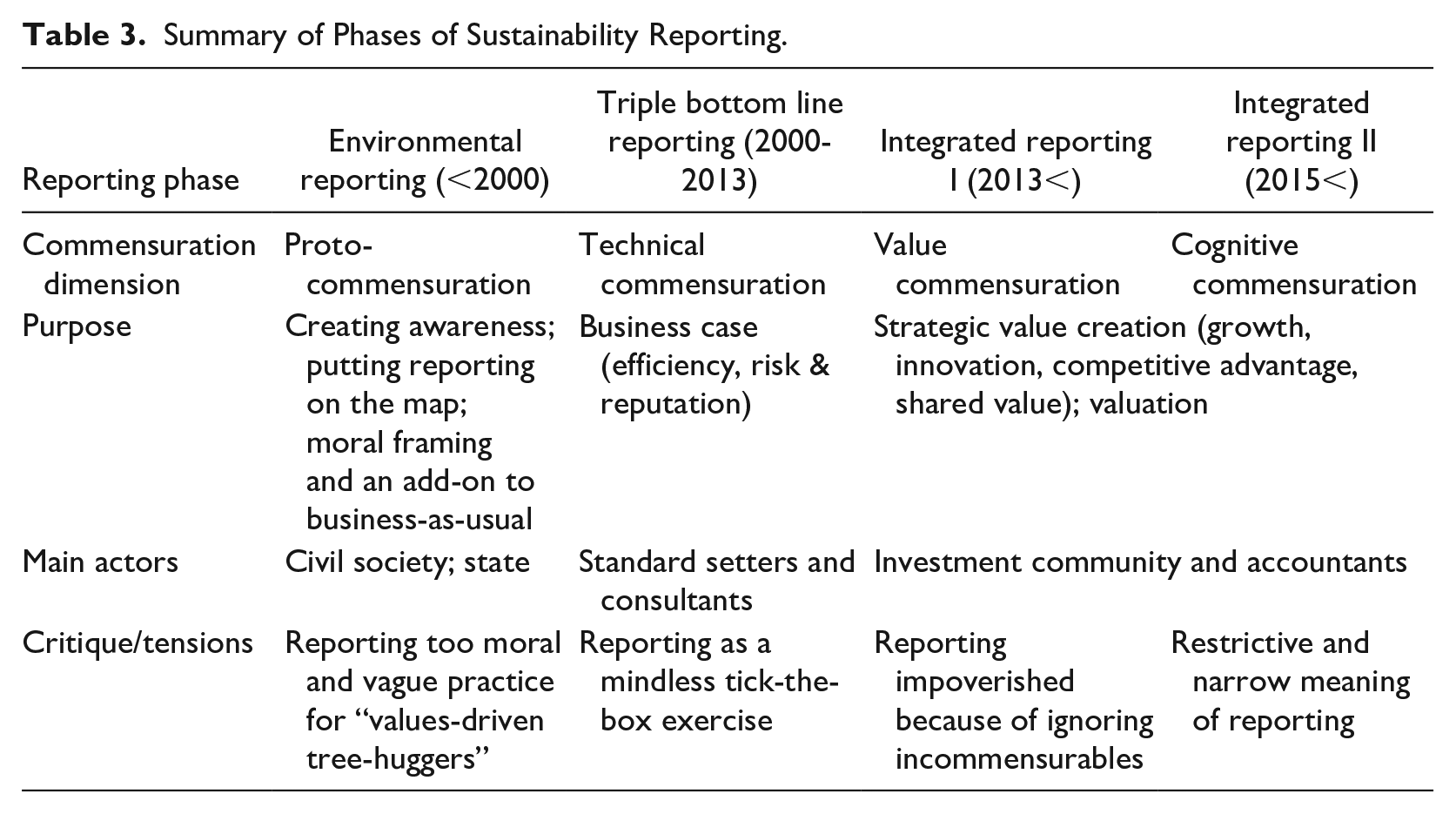

The data analysis was based on an inductive approach with frequent iteration between the empirical material, literature, and emerging theory (Strauss & Corbin, 1998). We relied on a historical narrative analysis, an approach taken in previous studies (Ansari & Phillips, 2011; Etzion & Ferraro, 2010; Leblebici et al., 1991; Scott et al., 2000), that “presents an account of the linkages among events as a process leading to the outcome one seeks to explain” (Roth, 1988, p. 1). We combined this approach with a temporal bracketing strategy as we observed “a certain continuity in the activities within each period and [. . .] certain discontinuities at its frontiers” (Langley, 1999, p. 703), which is explained below. We based our data analysis and coding primarily on the interview data, supported by document summary forms and field notes of attended events. The analysis took place in three stages, with concurrent data collection and analysis. Figure 1 shows the data structure, Table 3 offers a summary of main outcomes, and Table 4 offers a table with illustrative quotes.

Stage 1: The initial aim of the project was to examine how sustainability reporting had institutionalized over time. This shaped our approach to data analysis. First, we carefully analyzed the empirical material collected and exploratively coded the data around general questions of the (1) what? (e.g., events, actions, initiatives); (2) who? (e.g., actors involved, new entrants; incumbents); (3) why? (e.g., motivations, intentions, drivers); (4) how? (e.g., tactics, strategies, mechanisms); and (5) when? (e.g., what point in time?) of sustainability reporting. This first coding round was only minimally driven by theory and resulted in a large number (200+) of a diverse range of 1st order codes (Gioia et al., 2013).

Stage 2: We reread the empirical material and analyzed the assigned codes, but now trying to trace how reporting emerged and subsequently gained momentum and spread. Two issues became apparent. (A) We observed a chronology of key reporting types and actors, which made it apparent that the empirical data contained a temporal element, which led to the demarcation of three stages of sustainability reporting’s development (see also, e.g., Tregidga et al., 2014), which we labeled environmental, triple bottom line, and integrated reporting. (B) Recurrent references to the need for, criticism of and moves toward standardization, comparability, quantification, and monetization became apparent. Practices such as rankings, ratings, benchmarks, and performance indicators came up frequently as well. This warranted a more theoretical explanation. At this point in the data analysis, when a stronger theoretical grounding was called for, we followed Gioia et al. (2013, p. 23) who argued that “upon consulting the literature, the research process might be viewed as transitioning from ‘inductive’ to a form of ‘abductive’ research, in that data and existing theory are now considered in tandem” (Alvesson & Kärreman, 2007). Hence, we started to consider the commensuration literature since it appeared from the various codes that commensuration was potentially an insightful theoretical lens to explain how the observed phenomena contributed to reporting’s institutionalization. The data were thus again analyzed and (re)coded, this time zooming in on commensuration aspects. By consulting the data and informants, we identified examples of commensuration and these were classified along the dimensions of value, cognitive, and technical commensuration. Inductively, we found a new dimension (“proto-commensuration”) that preceded the other three dimensions.

Stage 3: As part of our temporal bracketing strategy, we tracked the role of the commensuration dimensions and relevant actors throughout the history of reporting to see whether there was temporal variation. The analysis suggested that the various dimensions of commensuration developed differently over time (see also Figure 1 and Tables 3 and 4), and that commensuration work took place against a background of shifts in type of reporting, purpose of reporting, and main actors involved. In fact, the twin-tracked analysis of reporting phases and commensuration dimensions showed a lot of overlap over time, making it possible to relate the dimensions of commensuration to the phases of reporting. Whereas a typical Gioia data structure does not easily allow for showing such temporality (but see Kroon et al., 2021), we marked the various phases in the data structure (see Figure 1) to show the linkages between the core dimensions and themes over time. An overview of these phases and their specific characteristics was iteratively discussed and validated throughout the interviews.

Data Structure.

Summary of Phases of Sustainability Reporting.

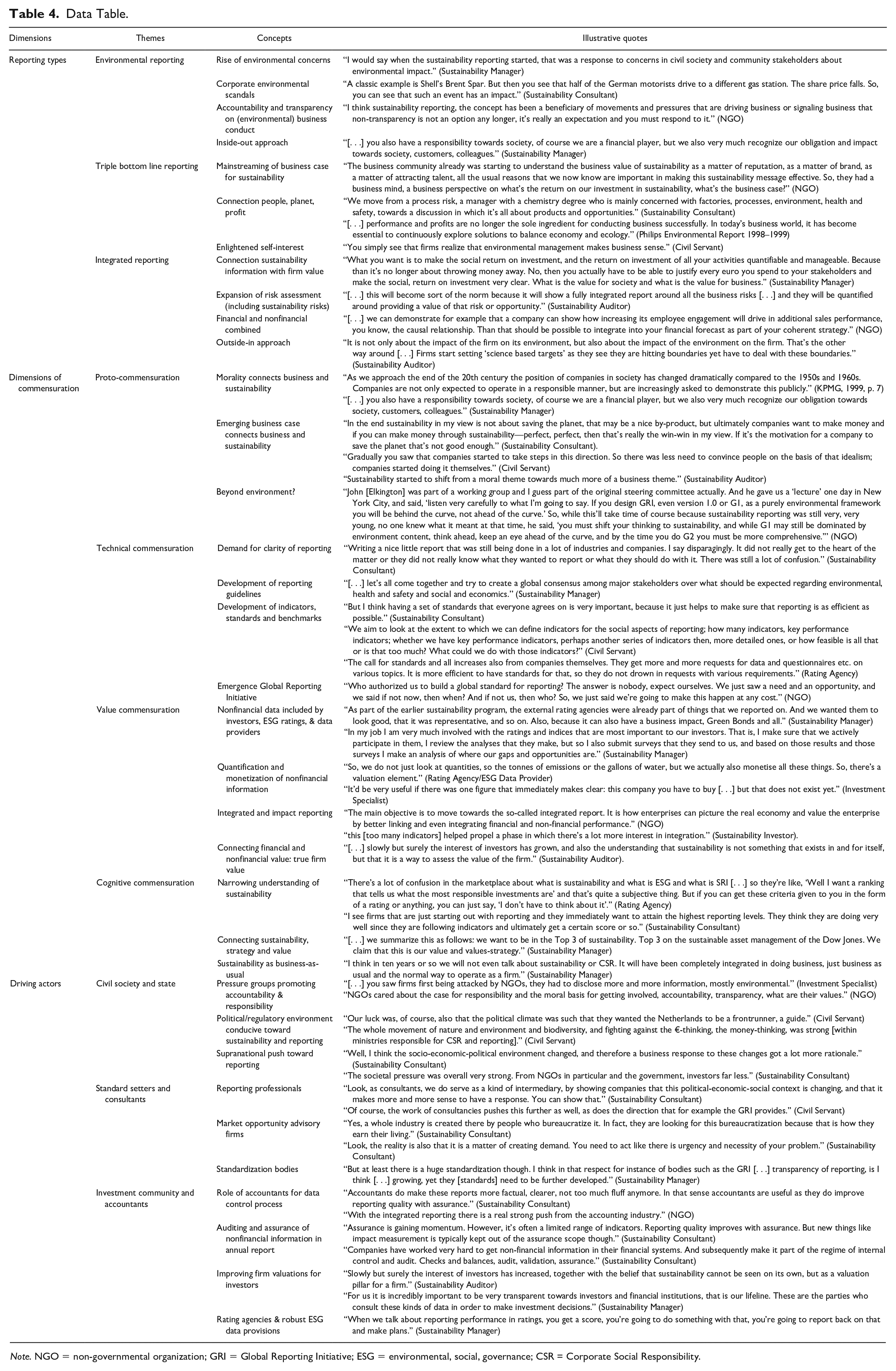

Data Table.

Note. NGO = non-governmental organization; GRI = Global Reporting Initiative; ESG = environmental, social, governance; CSR = Corporate Social Responsibility.

Findings

Our analysis is structured around three main reporting phases in which we highlight four sequential commensuration dimensions. These phases and dimensions should not be treated as abrupt and absolute demarcations, but rather as transition periods in which one reporting phase and commensuration dimension gets gradually taken over by a new one. Moreover, while we identify a dominant commensuration dimension in each phase, this does not imply that no other types of commensuration exist during that phase (e.g., the work of the IIRC in phase 3a relies strongly on value commensuration, but still requires technical commensuration). Table 3 offers a summary and Table 4 additional details and supporting empirical evidence.

Phase 1 (<2000): Environmental Reporting and Proto-Commensuration

Prior to the 2000s, reporting was primarily focused on environmental issues and driven by a combination of emerging regulation and pressure from civil society, not the least due to corporate scandals such as Shell’s Brent Spar incident or Nike’s sweatshop controversy. Reporting had little connection with firm value and “early reports contained a lot of ‘hurray’ stories” (NGO). Reports focused on the impact organizations had on their environment and were framed around how transparency was part of being a good corporate citizen. Business and (environmental) sustainability were at first largely unconnected, yet gradually a meaning system emerged that saw them as two sides of the same coin, a process we label proto-commensuration.

At first, morality was the connecting element in establishing the business-sustainability link. NGOs and the Dutch government emphasized the failings of firms and their moral obligation to become more responsible, accountable, and transparent. The reasoning was that “transparency is not an option any longer, it is really an expectation and you must respond to it” (NGO). Helped by the 1992 Earth Summit’s Agenda 21 plan (United Nations, 1992, p. art. 30.10), which contained a recommendation urging firms “to report annually on their environmental records, as well as on their use of energy and natural resources,” a push for reporting started to emerge. The Dutch Environmental Protection Act stated that starting from 1999 around 300 companies (mostly heavy polluters) were required to report. Still, this only affected a small number of companies and exactly how to report remained ill-defined.

Notwithstanding these limitations, in the words of a civil servant involved, the societal norm that as an organization “you were morally obliged to pursue these sustainability goals and reflect and report on them” slowly started to take hold. This push urging companies to report “had a very ethical and normative viewpoint” (Investment Specialist) and remained relatively unconnected from business strategies and processes. The message to companies from (civil) society was summed up as follows: “You ought to be doing this. You have a responsibility to address these issues!” (Sustainability Consultant). According to a civil servant at the time, the reasoning behind reporting was quite morally inspired: “you go to a company and tell them that CSR is a very moral issue and that it is actually your moral obligation to pursue these environmental goals.”

Responses by corporations differed, as “firms were not used to disclose information that had no, or a very limited, financial component. They found that soft and irrelevant” (CEO, MNC). Resistance was visible as some firms argued: “we should not start doing this! We put too much responsibility upon ourselves” (Sustainability Consultant) and typical resistance was framed around “we don’t need it, it’s technologically impossible, it’s too complex, it’s going to be too expensive, it doesn’t add any value [. . .] or the other thing is it’s not mandated, so why should we do it?” (Sustainability Consultant).

Still, some early adopters responded to this moral obligation, or in some cases had their own more personal conviction toward sustainability and contended that in a changing society “firms simply are expected to behave in a certain way, and rightfully so. An aspect of this is a more ethical form of business in which there is a place for accountability and reporting” (Sustainability Manager). For instance, Philips in its 1998 Environmental Report argued, “we have long been aware of the responsibility we have towards society and the environment.” An environmental manager phrased the spirit as follows: “we want to be more than just a profit-pursuing entity. We want to offer our people a good work environment; contribute to [solving] environmental challenges. We find that important and therefore we want to report about such things.” Hence, a moral undertone characterized the debate, mostly because reporting was shaped by showing good corporate citizenship in touch with societal norms and corporate values: “When I started working on sustainability it was more like: you need to do good. You have to do business decently and ethically. You have to show that in your management and also report on it” (Sustainability Auditor).

However, environmental reporting remained a fringe practice supported mostly by some bigger firms. These companies adopted an inside-out approach to reporting. That is, at first the focus was on the impact of companies on their environment, and how they could minimize the negative impact and maximize the positive rather than considering how sustainability could positively or negatively affect the company and use reporting as an internal management tool. (Sustainability Auditor)

Overall, early reports remained both limited in numbers, rather vague, and “a lot about doing good, giving something back to the world” (Sustainability Consultant). Moreover, “there was no set format that could measure success” (NGO) and “everybody was trying to find out: What is sustainability and what does it mean for reporting? Can we actually report? What do we have to report on and how?” (Sustainability Manager).

As this call for more guidance and standards emerged, a gradual transition took place toward the turn of the century: The initial moral undertone started to become supplemented by some firms recognizing the potential (financial) benefits of addressing sustainability. This was pushed by some stakeholders, as they argued that “it helps as a means of pressure if companies have to start reporting on things they’ve never thought about before, then systems are going to be set up” (NGO). Within firms, the idea emerged that “yes, there may have been an ethical aspect here, but that is a difficult starting point for us, we need to link it to the business” (Sustainability Manager). The 1999 Shell Report (p.1) argued, “Sustainable development is a way of developing and safeguarding our reputation and it will help us develop our businesses in line with society’s needs and expectations,” and a manager involved in reporting during this period observed that “gathering the data helped us to run a better, more disciplined business.” Hence, the business case for sustainability started to emerge, though it was not mainstreamed yet.

In short, at first morality was the linchpin between business and sustainability, but gradually the business case became the connecting element. A meaning system slowly emerged in which previously unconnected aspects (i.e., business practices and sustainability) started to become related concepts. We label this dimension of the commensuration process proto-commensuration, which functioned as an enabler for subsequent commensuration activities. In the next phase, this new meaning system would develop further and give rise to the technical work needed to develop common reporting standards and indicators.

Phase 2 (2000–2013): Triple Bottom Line Reporting and Technical Commensuration

As firms increasingly started to wonder “What is the scope, what are we talking about? What are the themes? What are the KPIs?” (Sustainability Manager), the second phase emphasized technical commensuration through the development of indicators. Now that a link between business and sustainability was more established, reporting became increasingly about building a business case. A partner of a Big Four firm captured the new spirit as “[s]ustainability is a topic that is important in the world. That’s no ethics or morality. It is simply that if I don’t pay attention now, I’ll have a problem later on.” There was a strong notion that reporting “had to become formalized and was expected to be concrete, measurable, comparable and quantifiable” (Civil Servant). Technical commensurative work was required to remove uncertainty around reporting and make it more concrete and manageable. This type of commensuration was driven primarily by standard setting bodies, who together with companies and consultants started to give the rather complex and messy sustainability reporting some hands and feet.

Standard setting happened through the development of the multi-stakeholder GRI guidelines, a project that required extensive technical commensuration as it aimed to develop “a general global agreement on the sorts of non-financial information or social and economic information that companies should report,” according to a GRI employee at the time. The reasoning behind developing the guidelines was “instead of having 50 different standards, let’s all come together and try to create a global consensus among major stakeholders over what should be expected regarding environmental health and safety and social and economics” (NGO). The work of the GRI had a considerable technical dimension as it aimed to develop relevant indicators, which was typically done in working groups in which different stakeholders discussed the indicators. Developing such indicators was not an easy task. As one informant, who was closely involved in the GRI standard-setting process, argued, “They were very difficult discussions at times, when even some of the stakeholders said I am ready to walk away from the table.” While disagreements and tensions were common, agreement could often be reached as a more neutral rather than normative stance on indicators was sought: “You may not think it is a perfect idea, you may not be able to agree to the exact language and the indicators that we’re developing, but can you live with it?” (NGO).

As a GRI employee of the time recalled, an important aspect was tapping into existing knowledge by “trying to involve technical expertise with some of the people who are familiar with financial reporting, assurance issues.” Notwithstanding agreement that “especially on the social side we need to make it more comparable because it’s too soft and too mushy” (Sustainability Manager), the development of indicators for social aspects remains up to this day more controversial than the development of environmental indicators: “The problem was that the people in the social groups weren’t used to metrics and did not know how to design them or what they will do for you” (Sustainability Manager).

The work of the GRI was instrumental in advancing technical commensuration and was further reinforced by the technical work undertaken on developing indicators for simultaneously established indices and rankings such as the Dow Jones Sustainability Index (DJSI), the FTSE4Good Index, and the Dutch Transparency Benchmark. The technical work of these initiatives at times overlapped. As a GRI employee recalled, we did take very seriously the FTSE4Good and the same with the DJSI, and worked very hard to try to capitalize on the inroads they were making with companies on transparency [. . .] we tried to make reporting as easy as possible by mapping, where possible, the overlapping indicators [. . .] and we had a deal and we said “hey look, can we get you to say to firms ‘yes, we’ll accept your GRI report.’”

Reporting’s technical commensuration was not without contention though as it turned out to be a double-edged sword. In the words of one consultant, “True, reporting became more business-focused, more factual, more figures, objectives, evaluation of objectives, you name it. However, companies started asking ‘Are we not over-bureaucratizing? The reports are thicker than the annual financial reports!.’” Some companies had started to blindly follow the new standards and hence lacked reflection on reporting. One interviewee duly noted, “you need to be careful that sustainability and sustainability reporting do not become checklists. That is, for my part, they become checklists, but then you have to see that you are working on something very restricted” (NGO). In short, as a sustainability manager commented, “GRI has been a great help [. . .] when we made our first sustainability report it was very nice to have some point of reference. Back then it was simply tick-the-box of the indicators.” Reporting by ticking boxes and following rankings and benchmarks ran the risk of not anchoring it to the core of the business. The idea that “sustainability will only be really relevant when it is a strategic theme that is managed by the Board of Directors” (Sustainability Consultant) took hold, which meant “don’t report on everything. Look at what items are material” (Sustainability Manager) as following standards blindly “actually takes them [companies] away from what they should be doing, namely looking at sustainability in the context of their own organization and putting together good strategies” (Sustainability Consultant).

Phase 3a (2013<): Integrated Reporting and Value Commensuration

From 2013 onwards, sustainability reporting saw the emergence of integrated reporting and an increased focus on firms’ financial value. We have split this phase into two parts, with at first value commensuration becoming more important (3a) and, as a consequence, some years later also cognitive commensuration (3b).

As sustainability reports became “obese with indicators” (NGO), the investment community (investors, data providers, rating agencies) and accountants increasingly emphasized determining the true value of a firm, which required integrating financial and nonfinancial aspects. Such integration, however, required reducing reporting to its core and having a clear picture of how sustainability affects the company, instead of only vice versa. You say to a firm “You better take a look at some of those so-called non-financial issues, because it just impacts your business. It impacts your finances.” (Sustainability Auditor)

Captured succinctly by a CSR think-tank: We can continue to improve reporting by fine-tuning these KPI’s, that is one big agenda, but to us the biggest agenda [. . .] is the connection with financial aspects that counts. That is going to reconcile within the company the financial and non-financial to picture the real economy of your enterprise.

Hence, reporting’s connection to firm value (e.g., through monetized KPIs and integrated reporting) became important. The aim was to improve firm valuation by integrating the technical sustainability indicators with firms’ strategic thinking.

Investors became increasingly interested in “developments such as the Paris Agreement and SDGs and wanted to understand what they mean and their effects on firms and value. These days I have almost weekly conversations with pensions funds and investor relations” (Sustainability Manager). However, investors had a specific mindset as they regarded nonfinancial information increasingly important for a functioning market and making sound investment decisions: Forget about the accountability of companies. If you like, forget about the company’s own business case; let’s talk about the efficient allocation of capital. Do investors have access to the kind of information in the right kind of format for them to be able to make correct valuations of companies? (Civil Servant)

Consequently, data requirements started to change as “non-financial data has grown in importance comparable to financial data, and with that has come the expectation around that data being of the same quality like financial data, the same level of reliability” (Sustainability Manager). In short, “now you see that the financial world is looking at it, and it suddenly becomes a lot more serious” (Sustainability Consultant).

Alongside the investment world, accountants also got more involved. As a Big Four partner argued, accountants have noticed that sustainability reports get ever closer to the core operations of the firm and therefore become also relevant for them [. . .] they are starting to realize that non-financial information involves more than just sustainability and that it is important for the valuation of the organization.

Big Four accounting firms all started auditing integrated reports, engaged in thought-leadership, and organized seminars and workshops on integrated and true value reporting (EY, 2016; KPMG, 2014; PwC, 2019). Still, this also caused some tensions, as shown by one informant (NGO) who argued, “I don’t consider the accounting industry authoritative in the social performance area, but they will say well, we’re authoritative in accounting. Well, I’m not sure that’s the same thing.”

A salient commensuration example was the International Integrated Reporting Council (IIRC) that launched its reporting framework in December 2013. IIRC defined an integrated report as a “concise communication about how an organization’s strategy, governance, performance and prospects, in the context of its external environment, lead to the creation of value over the short, medium and long term” (IIRC, 2013, p. 7). Integrated reporting was not primarily about developing technically valid and reliable indicators, but more about putting prices or values on these indicators as “the more distant you get from the factors that can be readily monetized, the more difficult it is to create a meaningful framework for comparison” (NGO). The view took hold that the only way to make sure sustainability or QHSE [quality, health, safety and environment] information has an impact within the firm is by letting it flow into the financial reports. After all, those reports are actually being read! So, you will have to translate sustainability information into financial reports. (Investment Specialist)

However, critics started to worry that with integrated reporting, “is there still sufficient space left for reporting about sustainability, or is this aspect hidden somewhere in the corner?” (NGO).

Phase 3b (2015<): Integrated Reporting and Cognitive Commensuration

As reporting’s commensuration continued, a particular understanding of the meaning of sustainability and what it meant to be counted as a reporting company emerged. Firms started to pay attention to a much narrower selection of (quantified) strategic indicators. This emerging dimension of cognitive commensuration, or “reclassifying the world in terms of categories that align more closely with the new metrics” (Levin & Espeland, 2002, p. 126), further highlighted some tensions. Reporting became even more associated with (financial) value creation and a focus on material (i.e., strategically important) topics. As mentioned in KPMG’s (2020) biannual reporting survey (p. 8), “We predict a further tightening of focus of nonfinancial reporting on investors’ needs, more harmonized reporting based on common metrics and further coalescence towards a global corporate reporting system. The time has come.” This made sustainability more attractive to executives and investors, yet at the same time it also led to tensions and discomfort by other stakeholders because questions around the integrity of reporting firms were increasingly sidelined. An NGO said, “Some stakeholders argued that reporting ought to be about understanding better the performance of companies, whilst for other stakeholder groups it is more about the transparency and integrity of companies” (NGO). This highlights the difficulties in bringing together people primarily interested in sustainability and those more embedded in finance and accounting: People in the world of sustainability reporting tend to be values driven, tend to be mission orientated. In their hearts they’re social change people. [. . .] Financial reporting is very much a mechanical exercise that’s getting the numbers in the right columns and getting the accounts straight and the balance sheets and income statements. (NGO)

Cognitive commensuration highlighted the standardization of the meaning of sustainability reporting. A reporting company was one that showed how social, environmental, and economic value could be integrated with each other. A consultant argued that companies “bring back sustainability in their reports to its strategic core, which also means that there is only one way to report, and that is integrated reporting” (Sustainability Consultant). This led reporting to “develop from a kind of tick-the-box exercise towards reporting that is more relevant for the corporate strategy” (Investment Specialist). Even more than before “the ultimate goal of sustainability reporting and moreover integrated reporting is to evaluate and value the quality of the firm” (Investment Specialist). The Sustainability Accounting Standards Boards (SASB) provided firms with industry-specific “materiality maps” and thus an overview of material ESG indicators. Hence, questions such as “Which factors really have a relation with financial value? Which factors are determinant of true value of the firm?” (Sustainability Auditor) became paramount. As this new meaning of sustainability became more accepted by field-level actors, the “industry” behind sustainability started to further grow. A consultant said in this context: “a whole industry is created by people who bureaucratize it [sustainability]. In fact, they are looking for this bureaucratization because that is how they earn their living.”

With investor interest on the rise, ESG rating agencies and data providers also gained influence as they started to commercially feed data to investors. Again, some voices argued “ESG information has become big business!” (NGO). On the one hand, ratings referred to value commensuration: “We have a large number of indicators per profile and we put a weight on each indicator and you get a score on each indicator. Ultimately, that culminates in a number between 0-100, a company gets a mark” (ESG Data Provider). On the other hand, ratings also had a cognitive effect in the sense that they helped to determine what is considered material sustainability information. As explained by a sustainability manager, We find Sustainalytics a very important rating. Recently they told us we need to report on our Gender Pay Gap, which we had not done before. So, now we have added a disclosure on our Gender Pay Gap. That is very useful for us internally, as these ratings function as a stick that can help you set things in motion within the organization.

The commensurative work undertaken also positioned sustainability as “something that people in the top-level of the firm can understand. [. . .] When you see that your transparency [. . .] score goes from 60 to 70 than everybody understands that you have improved” (Sustainability Consultant). With this strategic and financialized focus, sustainability had become an easier message because rather than talking about sustainability—I mean I very, very rarely use that term—I go in to talk to clients and I will talk about risk, I will talk about opportunity, cost, and as a result of that you talk the language of business. (Sustainability Auditor).

Ultimately, the boundaries between business and sustainability started to disappear, or as one rating analyst argued: “I think that as long as [. . .] sustainability can be externalized and be something that is additive, it can be called sustainability. Once it is integrated into the business, people stop calling it sustainability.”

Commensuration resulted in a specific, yet unavoidably partial, understanding of what it meant to be a reporting company. The value-driven understanding of sustainability reporting troubled critics. One sustainability consultant commented, “The topic of sustainability is currently being hijacked by the accountants, KPMG-type of people, and the raters and ISO-folks. I do understand where the desire comes from: clarity, measurability, thinking in absolute terms, yet it has limitations.” Some NGOs viewed the emerging understanding of sustainability reporting as being focused on value creation as problematic: They [NGOs], of course, didn’t care about the business case, they cared about the case for responsibility and the moral basis for getting involved, accountability, transparency, what are their values, and they thought this [reporting] would be an instrument for advancing those values. (NGO)

Although these concerns were mostly raised by NGOs, they were also recognized by other actors. A partner of a Big Four firm emphasized the tricky nature of the connection between financial firm value and individual values: We are used to looking at everything from a financial perspective and we try to make connections with the financial elements. That is the basis and everything that falls outside of this you try to bring inside of this domain. We as humans are able to set various types of value against each other. We say that we create value by doing interesting and worthwhile work, but by doing so [we] cannot be with our family which destroys value. Still, we do not turn this into monetary terms but are somehow able to juggle these types of value. However, firms are quite bad at managing this value complexity. It forces firms into a dilemma thinking mode which includes thinking in terms of ethical elements and they are typically not very able or willing to do so.

In sum, risks loomed of firms neglecting to think about individual values and what sustainability meant to them. Instead, firms followed guidelines, indicators, rankings, and understood reporting as one important driver of value creation. Yet “if you restrict yourself to reporting the standardized information, and I think that is cause for concern, at least for me, then you risk that you stop the thinking” (Sustainability Auditor). This highlights the risk of firms failing to think through what being a sustainable firm actually means and the dilemmas that accompany the journey toward sustainability.

Discussion

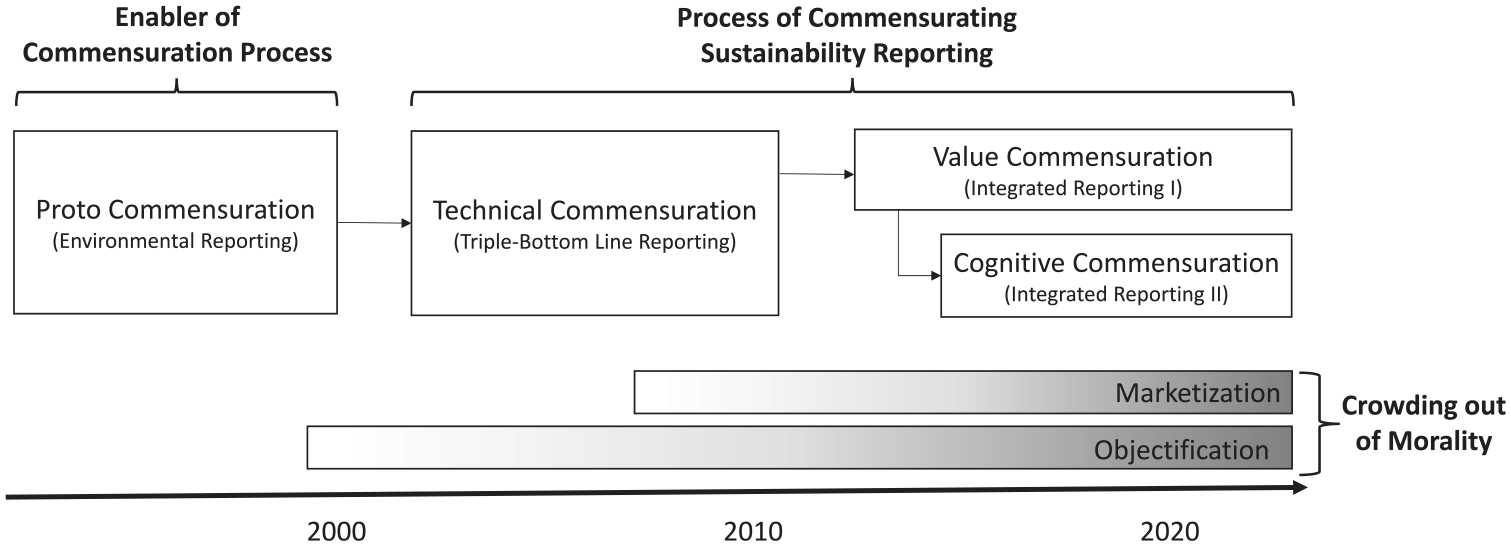

Our findings show that the different dimensions of commensuration supported sustainability reporting’s institutionalization from a rather fringe practice shaped by a moral undertone to a taken-for-granted practice mainly focused on the creation of firm value. While the literature has described the overall institutionalization process well (Aerts et al., 2006; Contrafatto, 2014; de Villiers & Alexander, 2014), it has not yet linked the commensuration dynamics underlying this process to the dissemination of sustainability reporting as a social practice. Our study therefore complements this literature by uncovering a so far neglected effect of commensuration on sustainability reporting: the “crowding out of morality.” Early reporting practices served as a ground for “doing good” and were connected to personal convictions and corporate values. Increasing levels of commensuration rendered the moral nature of sustainability issues less visible, as technical, value, and cognitive commensuration processes shifted the focus toward minimizing negative ESG impacts on companies (e.g., through risk management) and maximizing their financial value. In the following, we explain why and how this “crowding out of morality” happened and how the different elements of our argumentation hang theoretically together. Our starting point is the theoretical model depicted in Figure 2.

The Commensuration of Sustainability Reporting and the “Crowding Out of Morality”.

Figure 2 shows how the four discussed dimensions of the overall commensuration project relate to each other. Three of these dimensions (technical, value, and cognitive commensuration) reflect the actual process of commensurating sustainability reporting, while the fourth dimension (proto-commensuration) acts as an enabler of the entire project. The four dimensions of commensuration jointly influenced two processes—the objectification and marketization of sustainability. We maintain that, together, objectification and marketization created one outcome: a “crowding out of morality” within discussions of corporate sustainability. In the following, we discuss how objectification and marketization influenced this “crowding out of morality.”

Objectification

Following McKinley (2011), we understand objectification as a process through which certain phenomena achieve the status of things over time—that is, they are increasingly viewed as “given” and appear detached from their human origin. In our study, especially technical and value commensuration objectified relevant parts of social reality. These processes turned subjective moral concerns around social and environmental problems into decontextualized indicators that were mostly linked to financial value. Commensuration created order out of chaos and made the complex practice more manageable and easier to understand for a larger audience. It also shifted the emphasis from more narrative accounts of firms’ sustainability practices to formal codifications and countability (Hasselbladh & Kallinikos, 2000). The objectification of sustainability through reporting took away a lot of the tacitness and ambivalence related to social and environmental issues and instead created a simpler and seemingly rational and objective approach. The development of numerical indicators made it possible to know and judge sustainability without access to detailed contextual particularities (Merry, 2011).

The objectification of sustainability also led to higher degrees of depersonalization. Research in social psychology suggests that depersonalization leads to a situation in which the moral status of something is either completely withdrawn or at least neglected more easily (Loughnan et al., 2010). Moral disengagement becomes easier because people feel less involved in ethical dilemmas when seeing sustainability through the lens of formal codifications and technical indicators instead of semantically richer narrative accounts. Such moral disengagement is caused by the application of cognitive frames (Palazzo et al., 2012). People use such frames “to impose structure upon information, situations, and expectations to facilitate understanding” (Gioia, 1992, p. 385). Our study shows that commensuration influenced such frames (mostly through cognitive commensuration) and hence controlled which aspects of sustainability were emphasized and which ones were obscured. The indicators, standards, ratings, KPIs, and measurement systems that resulted from technical and value commensuration shaped peoples’ perception in a way that sustainability was increasingly framed in economic and instrumental terms.

These developments become visible when looking at cognitive commensuration where data providers and rating agencies pushed mostly those data items that were of special value for investors. The dominant frame for analyzing the “worth” of sustainability information was economic reasoning (e.g., Does this information help to improve the management of market risks and opportunities?). Prior research suggests that such cognitive frames are rigid in the sense that people do not shift easily between them (Schoemaker & Russo, 2001). Cognitive frames, which are influenced by commensuration processes, are likely to be particularly rigid, as sustainability metrics contain high levels of codification. Research on the sociology of numbers confirms this. Porter (1995), for instance, showed that indicators might be perceived as contingent at first; however, once they are in place they become resilient and take on a permanent existence as a form of knowledge that is difficult to challenge or change.

Marketization

Our findings also demonstrate that the crowding out of morality was supported by marketization processes. Marketization refers to the “expansion of market coordination into non-market coordinated social domains” (Ebner, 2015, p. 369). Commensuration and the formation of markets are known to go hand in hand (Levin & Espeland, 2002; Mennicken & Espeland, 2019). While our findings support this, as commensuration contributed to the creation of a market around sustainability reporting, our results also show that commensuration enabled the dissemination of the market system into a domain which at least some perceived as consisting of incommensurable issues. Following White (1981, p. 518), we understand markets as “self-reproducing social structures among specific cliques of firms and other actors who evolve roles from observations of each other’s behaviour.”

Over time, different forces and actors contributed to the formation of a market around sustainability reporting: Standard setters (like the GRI) provided a common language and technical benchmarks during technical commensuration, while the Dutch government and the EU provided hard and soft regulatory measures. Investors increasingly demanded “hard data” on sustainability (e.g., to manage ESG funds). This is also visible in the world of data vendors, as shown by Eccles et al. (2020) in their account of how MSCI opted to use Innovest’s financial value-driven methodology rather than KLD’s values-driven methodology. Accountants, on the other hand, refocused reporting to a more strategic core to merge sustainability into the business and offered assurance services for firms’ reports. Firms were motivated to demand assurance, as this often opened the door to participate in rankings and indices (e.g., the DJSI). All of this contributed to the formation of market mechanisms around sustainability reporting.

This marketization of reporting supported the crowding out of moral concerns. Marketization made it harder for firms and other actors to make sustainability the subject of moral reflection, because the associated commensuration dynamics contributed to a process in which the instrumental reasoning of the market system became so predominant that it limited the possibility to raise normative concerns (see also Habermas, 1987, p. 355). More precisely, it was the monetization of social interactions around sustainability reporting that was driving the money-mediated market system into the domain of sustainability and made it more difficult to distinguish between what is (in an economical sense) and what ought to be (in a moral sense) (see also Espeland & Sauder, 2007). Monetization sidelined moral concerns especially during value and cognitive commensuration in two ways: (1) by limiting reporting to those topics that could be framed in monetary terms (e.g., when standard setters required “material” sustainability issues that are relevant to firm value) and (2) by making social interactions around reporting subject to economic exchanges (e.g., when accountants “sell” assurance or when investors “buy” information on sustainability-related risks). These two developments made it more difficult to coordinate social interactions based on shared values and hence to allow for reflecting on moral concerns. For instance, commensuration enabled the integration of ESG data into information platforms used by investors. While this allowed for material sustainability issues to be embedded into market transactions (e.g., valuation of companies), it also rendered all those sustainability issues invisible that were not categorized as material.

Contributions and Conclusion

This study showed that four dimensions (proto, technical, value, and cognitive) impacted the commensuration of sustainability reporting over time. Together, these four dimensions shaped different phases of the evolution of sustainability reporting and contributed to its institutionalization. The four dimensions shaped two processes (objectification and marketization) which moved reporting from a practice with an initial moral undertone to a practice with a high concern for firm value. The outcome of these two processes was a “crowding out of morality” that was driven by the rigid cognitive framing of ESG issues through sustainability reporting (objectification) and the increasingly monetized coordination of social interactions in the context of sustainability disclosures (marketization).

Our argument is not that the commensuration of sustainability reporting completely denies morality in corporations, but that the moral status of sustainability was marginalized and not much reflected upon over time. We believe that our analysis is important, not only because commensuration is a prevalent phenomenon but also because it spreads into different spheres of life. The commensuration of sustainability reporting has created effects that are increasingly relevant in other societal domains. NGOs as well as public sector organizations, for instance, are increasingly asked to attach specific (often financial) indicators to measuring their work. Furthermore, it is important to keep the Dutch context in mind when interpreting our study results. While our study is not a comparative one, specific elements that may have influenced reporting’s trajectory are: a relatively strong governmental involvement, albeit in particular in the earlier stages; the GRI being based in Amsterdam and possible spillover effects this may have caused; the sustainability consulting industry in the Netherlands developing quite early and being large considering the size of the country; and the consensus-seeking nature of Dutch (business) culture which may have influenced the responses to pressures and demands.

Theoretical Contributions

Our study contributes to two sets of literatures: (1) studies discussing the institutionalization of sustainability reporting and (2) commensuration studies.

We supplement the existing literature on the institutionalization of sustainability reporting by highlighting the relevance of commensuration within this process. Prior work has helped us to understand that sustainability reporting’s institutionalization was driven by analogies (Etzion & Ferraro, 2010), isomorphic firm behavior within industries (Aerts et al., 2006; Shabana et al., 2017), professional networks (de Villiers & Alexander, 2014), and the reinforcement of intra-organizational structures and processes (Contrafatto, 2014). Our study has shown the relevance of commensuration within this process in two different ways. First, commensuration work, such as the definition of technical indicators and standards, helps to unpack some of the processes that enable and drive institutionalization. For instance, coercive isomorphism in the context of sustainability reporting depends on the existence of predefined standards and indicators provided by technical and value commensuration (Shabana et al., 2017), while companies’ widespread internalization of norms around reporting (de Villiers & Alexander, 2014) depends on the professionalization of the field and the creation of common meaning systems that are impacted by cognitive commensuration processes. Second, a focus on commensuration confirms that the institutionalization of reporting has given rise to an imbalance between (a) a domination of a managerialist understanding of reporting and (b) the declining importance of an approach that takes individual values seriously (Milne & Gray, 2013; Tregidga et al., 2018). Our results allow for a more fine-grained understanding of this observed imbalance. While prior analyses have cautioned that at least some reporting remains detached from ethical reflection (see, e.g., Maniora, 2017), our study has unpacked the role of commensuration in creating such detachment.

Our findings also contribute to those parts of the commensuration literature that discusses the role of morality in the context of incommensurables. Ethical dilemmas are often perceived to include incommensurable values. Our analysis complements this literature by showing that commensuration was a successful undertaking in the context of sustainability reporting because it crowded out moral concerns and thereby reduced the likelihood of long “philosophical” debates about intangible worth, which could have resulted in claims about incommensurability. Many social and environmental problems could potentially be seen as incommensurable, because they occur at the intersection of different institutional spheres where modes of valuing clash (Espeland & Stevens, 1998). For instance, although scholars have argued that human rights should be measured in principle, they have also pointed out that the achievement of rights cannot be measured without running into ethical dilemmas (Merry, 2011). The commensuration of sustainability reporting helped to overcome the seemingly incommensurable nature of “business” and “sustainability” by replacing moral debate with technical expertise.

Our analysis also extends the literature on commensuration by highlighting a so far neglected dimension: proto-commensuration. While current studies on the dimensions of commensuration (Kolk et al., 2008; Levin & Espeland, 2002; MacKenzie, 2009) highlight the necessity of technical, value, and cognitive commensuration, we show that proto-commensuration precedes any technical commensuration work by relating so far unconnected aspects of social life. In our case, proto-commensuration was inevitable, as it helped to overcome the seemingly incommensurable nature of sustainability and business reasoning, first by viewing businesses contributions to sustainability as a moral obligation and later through the emerging business case for sustainability (see Phase 1 above). While technical commensuration contained technical work in terms of quantifying sustainability issues and designing relevant measurement systems (MacKenzie, 2009; Wegener et al., 2019), proto-commensuration involved the work of overcoming cognitive distance—i.e., a distance that prevented the discussion of the possibility of expressing two issues in relation to each other. Hence, proto-commensuration acted as an enabler of technical commensuration. We believe that proto-commensuration is particularly important in commensuration processes that deal with seemingly incommensurable things, such as when the intrinsic value of nature or human rights are at stake (see also Taylor, 1981).

Future Research Directions

We see three promising directions for future research. First, we need to know more about how mundane practices related to sustainability reporting’s commensuration can potentially influence moral disengagement. Our analysis operated at the field level and hence it was not concerned with the role of specific practices. To better understand this “how” question of commensuration, insights derived from institutional theory are beneficial (Canning & O’Dwyer, 2016; Lawrence & Suddaby, 2006). Such research could ask questions such as: Which institutional logics frame and channel demands for the monetary valuation of sustainability issues, especially in cases where institutional logics conflict each other (Gisch et al., 2021)? In how far are relevant practices deliberately framed as being morally neutral? How do actors create new ways of visualizing sustainability issues (e.g., through Infographics), and what effects does this have on their moral engagement with an issue?

Second, future work can discuss the applicability of our results in other research contexts. Our study was concerned with the commensuration of sustainability issues appearing in the context of firms reporting. This research context is characterized by high levels of ambiguity, for instance, because the precise link between certain social and environmental values and corporations’ strategic value is not always easy to establish. Yet this ambiguity is not present in all cases of commensuration. The described interactions between commensuration, sustainability reporting, and the crowding out of morality are most likely to arise when claims about incommensurables are strong, for instance, “at the borderlands between institutions, where what counts as an idea or normal mode of valuing is uncertain, and where proponents of a particular mode are entrepreneurial” (Espeland & Stevens, 1998, p. 332). Future research needs to show in how far our insights also hold for less contentious commensuration processes.

Finally, there is need to investigate the consequences of the shift from values toward value. We believe it is important to study whether there might be some displacement of moral concerns within organizations (e.g., reporting firms or investors). Moral reflections might be moved to other (and maybe less visible) parts of the organization because an organization’s sustainability team may be seen as being primarily concerned with securing financial value. Prior studies of commensuration in the context of rankings (Espeland & Sauder, 2016) have emphasized the displacement of moral decisions in the sense that mid-level administrators became responsible for key moral dilemmas of organizations. Future scholarly work needs to clarify whether such displacement happens in the context of sustainability reporting and which possible consequences exist.

Overall, the ongoing commensuration of sustainability reporting reminds us of the power and usefulness of numbers. However, as Espeland and Sauder (2016, p. 198) remark, “useful is not the same as good.” Therefore, we hope that future studies will further examine if and how commensuration can be a force for substantive sustainable change.

Supplemental Material

sj-pdf-1-oae-10.1177_10860266221086617 – Supplemental material for From Values to Value: The Commensuration of Sustainability Reporting and the Crowding Out of Morality

Supplemental material, sj-pdf-1-oae-10.1177_10860266221086617 for From Values to Value: The Commensuration of Sustainability Reporting and the Crowding Out of Morality by Koen van Bommel, Andreas Rasche and André Spicer in Organization & Environment

Footnotes

Acknowledgements

We thank the guest editors of this special issue and four anonymous reviewers for their helpful feedback and guidance. A special thanks to Kyllian ten Kate for his valuable help with the interviews.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Author Biographies

![]() .

.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.