Abstract

The relationship between nonfinancial reporting and real sustainable change within and beyond organizations is fraught with complication. Furthermore, all facets of the relationship have not been examined equally. The contributions of this special issue made substantive progress in this regard and draw our focus to several remaining complications—in particular, the societal impacts of nonfinancial reporting. With this introduction, we seek to move the conversation forward by proposing a framework that disentangles the linkages between nonfinancial reporting and real sustainable change at multiple levels of analysis. We highlight the distinction between sustainability-related outputs and outcomes that typically materialize at the firm level, and eventually lead to sustainable impact at the societal level. Future research should advance this distinction and scrutinize the impact of real sustainable change beyond firm-level outputs, study the organizational change processes from antecedents to impacts, and examine the interrelationships between different instruments to foster real sustainable change.

Keywords

Introduction

Nonfinancial reporting, such as sustainability, corporate social responsibility (CSR), and climate reporting, has become a mainstream topic in management studies, accounting research, and business practice (Bebbington et al., 2021; Cort & Esty, 2020; Hahn & Kühnen, 2013; Shabana et al., 2017). Nonfinancial reporting is defined as information disclosed by companies about their nonfinancial performance and how they manage social and environmental challenges (e.g., European Parliament, 2014). However, the impact of nonfinancial reporting on what we define as real sustainable change, that is, actual improvements in tangible social or environmental conditions based on measurable indicators such as those derived from the 17 Sustainable Development Goals (SDGs), remains questionable. As the articles in this special issue illustrate, change toward greater sustainability is possible, but is fraught with complications. Commonly assumed factors, such as greater transparency and “what gets measured gets managed,” do not necessarily lead to real sustainable change at the societal level and therefore, need to be treated with caution to avoid detrimental consequences.

Ideally, and as often purported by reporting entities, nonfinancial reporting would help generate sustainable change, since increased transparency supposedly leads to increased accountability. However, current reporting practices seem to be more business- than society-centric, favoring the demands of reporting entities while offering new markets for advisory and auditing firms (Endenich et al., 2022; Vedula et al., 2022; Wickert, 2021). Consequently, the measurable impacts on societal well-being and other beneficiaries, such as marginalized stakeholders and ecological conditions, are if at all by-products of nonfinancial reporting (e.g., Halme et al., 2020). Research also struggles to identify causal linkages between reporting and real sustainable change (e.g., H. B. Christensen et al., 2021). Establishing such a link, however, is crucial considering increasing societal demands for information about firms’ nonfinancial performance and concomitant expectations that nonfinancial reporting helps address important social and environmental challenges (see Delmas et al., 2019). Thus, scholarly attention is needed to better understand and explain the behavior and actions related to nonfinancial reporting and its societal consequences. In fact, we know surprisingly little about whether, why, and how sustainable outputs, such as nonfinancial reports and other information disseminated to stakeholders materialize into sustainability-related outcomes, such as reduced carbon emissions, enhanced biodiversity, and improved human rights, which would ultimately lead to desirable impacts at the societal level of analysis (Bakker et al., 2020; Barnett et al., 2020; Hahn et al., 2015; Imbrogiano, 2021; Wickert & Risi, 2019).

Thus, research on nonfinancial reporting is at a crossroads. If real sustainable change is to be supported by nonfinancial reporting, scholars need to examine the mechanisms and relationships that connect inputs (e.g., data provided to compile a report) with outputs (e.g., nonfinancial reports), outcomes (in terms social or ecological performance), and impacts on social and ecological systems. For instance, we know little about the specific agendas, relationships, and decision-making processes of users of nonfinancial information within and outside reporting organizations. The matter is complicated by the heterogeneity of the addressees and users of nonfinancial information, such as equity and debt investors, media, employees, governmental actors, non-profit organizations, and pressure groups (e.g., Endenich et al., 2022). This makes it difficult for firms to decide when, how, and what to report and for whom (Bansal & Knox-Hayes, 2013; Reimsbach et al., 2020). Another complication is the specialized data vendor industry, which uses an array of measurement metrics that require correct contextualization (Berg et al., 2022).

Overall, we need to know more about organizational change processes that explain how actors outside and inside disclosing organizations adjust structures and behavior to rearrange organizational strategies, practices, and procedures based on different forms of nonfinancial reporting, and the factors that may accelerate, slow down, or even block this process. This special issue of Organization & Environment has attempted to address specific aspects of this complicated relationship. The contributions of this special issue substantially advance our understanding of how real sustainable change can be achieved or complicated through nonfinancial reporting. However, much work remains to be done, which we detail in our agenda for future research.

This special issue addresses several important themes in the nonfinancial reporting literature and collectively offers a deep dive into the state-of-the-art research in this field. The first contribution by Garcia-Torea et al. (2023) reviews the literature on nonfinancial reporting; they take stock of research in the accounting and organizational studies domains. Then, contributions by Andrus et al. (2023) and Dobija et al. (2023) examine key input factors that may enable real sustainable change through nonfinancial reporting, transparency, and voluntary versus involuntary reporting. The contributions of Fu (2023), Bauckloh et al. (2023), and Crace and Gehman (2023) explicitly model a (quantitative) measure of real sustainable change as a dependent variable related to nonfinancial reporting. These studies are important as they distinguish relative from absolute levels of real sustainable change (Bauckloh et al., 2023), examine the role of negative media coverage (Fu, 2023), and scrutinize the internal versus external effects that influence nonfinancial performance (Crace & Gehman, 2023). Finally, van Bommel et al. (2023) show that reporting shifted from an emphasis on morally charged values toward a focus on financial value creation, making it more difficult to associate sustainability issues with potential moral dilemmas.

Collectively, the contributions included in this special issue significantly contribute toward a better understanding of an important mechanism in achieving real sustainable change: nonfinancial reporting. However, they also highlight the relevant questions about the relationship between nonfinancial reporting and real sustainable change that remain unaddressed. In this introduction, we illuminate the relationship between nonfinancial reporting and real sustainable change, problematize the current state of research, and highlight the ongoing struggles of scholars to link these two concepts. We then summarize and put into perspective the various contributions of this special issue. Finally, we make suggestions for future research and illustrate a research agenda that pinpoints which questions remain to be solved and how these could be best addressed.

A Framework Linking Nonfinancial Reporting and Real Sustainable Change

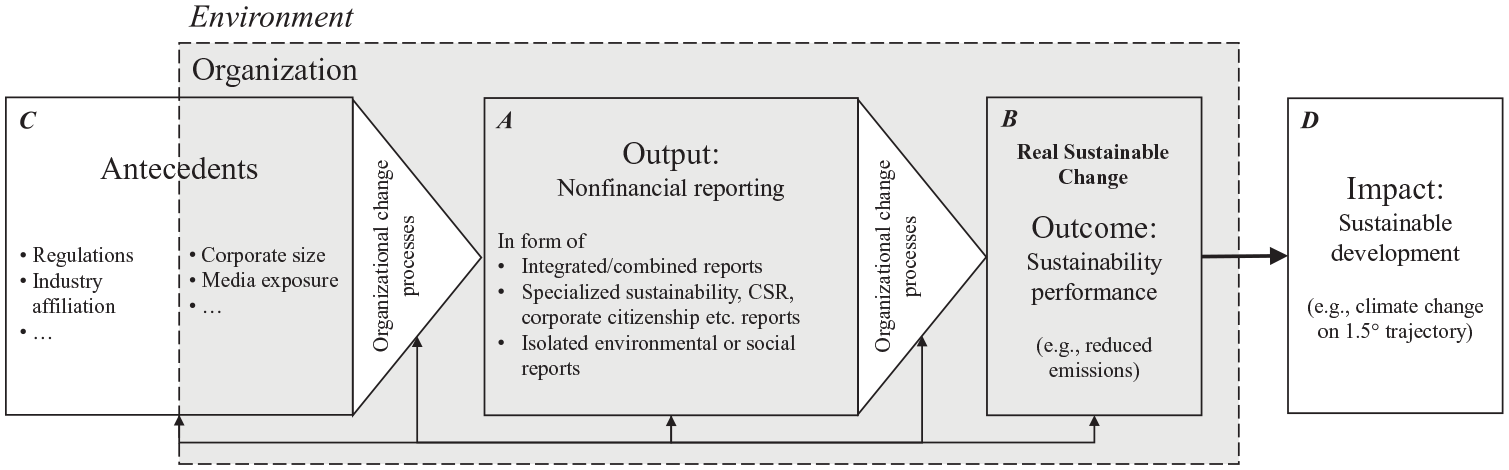

The relationship between nonfinancial reporting and real sustainable change is not straightforward. For this reason, we first conceptualize potential processes. Figure 1 schematically visualizes a framework that connects the key components of the relationship: antecedents, outputs, outcomes, and impact, all of which are interconnected by organizational change processes but may cross levels of analysis to varying degrees.

Linking Nonfinancial Reporting and Real Sustainable Change.

At the center of attention is the output of nonfinancial reporting (see A in Figure 1). Nonfinancial reporting includes a range of practices in which organizations provide and substantiate information about nonfinancial matters to stakeholders through formalized means of communication (Hahn, 2022; Laine et al., 2021). For instance, they can do so as an element in regular annual reports, a standalone nonfinancial report, or include nonfinancial information in an integrated report (Endenich et al., 2022). Terms like sustainability reporting and CSR reporting are typically used interchangeably under the umbrella term of nonfinancial reporting, despite some differences in their meanings. Through nonfinancial reporting, companies reveal how they manage social, environmental, and governance (ESG)-related challenges either holistically (e.g., in sustainability reports) or by focusing on specific issues (e.g., in climate disclosure). Just as financial reporting aims to provide a true and fair view of a firm’s financial performance, nonfinancial reporting is supposed to help stakeholders and shareholders alike to evaluate a firm’s nonfinancial performance.

One of the core goals of nonfinancial reporting is that this form of output results into an increasing level of transparency which eventually leads to the outcome of real sustainable change in the form of improved sustainability performance linked to a particular firm (B in Figure 1). Output and outcome are potentially linked through organizational change processes, where nonfinancial reporting is assumed to not only reflect existing corporate actions, but also trigger the creation of new actions as companies need to have “something to report about” (e.g., L. T. Christensen et al., 2013). From an inside-out-perspective, the (voluntary or mandated) decision to report on sustainability issues can induce companies to implement sustainability-related practices and procedures (such as setting up sustainability accounting systems to collect respective performance data; e.g., Gond et al., 2012) which enable a reporting in the first place. From a complementary outside-in-perspective, increased transparency through reporting can lead to external pressure and heightened stakeholder expectations especially for very visible companies or industries (e.g., large multinational companies), which can evoke internal processes especially if corporate reputation is at stake (e.g., Campbell, 2007).

From a societal perspective, this link between output (A) and outcome (Β) is the decisive element of the framework depicted in Figure 1. If increasing efforts in nonfinancial reporting do not induce real sustainable change, they merely represent a waste of resources. However, real sustainable change in the form of improved outcomes—sustainability performance within organizations—is not necessarily sufficient to achieve sustainable development if it does not aggregate into positive societal impacts outside the organizational sphere (D in Figure 1).

To date, research has primarily focused on the various outputs of nonfinancial reporting. The more important aspect of the outcomes (or even the impact) of nonfinancial reporting, with the exception of financial outcomes (e.g., Luo et al., 2015; Matsumura et al., 2014), have not been scrutinized adequately (Garcia-Torea et al., 2023). From the output-related stream of research, we know that different organizational or environmental antecedents (C in Figure 1) influence nonfinancial reporting. For example, research has shown that corporate size and media exposure have positive effects on the adoption and extent of nonfinancial reporting (Hahn & Kühnen, 2013). Furthermore, industry affiliation also influences reporting practices, and listed companies disclose more sustainability-related information than their private counterparts (H. B. Christensen et al., 2021; Hahn & Kühnen, 2013). Thus, there is a solid base of research on the antecedents within and outside organizations that also provides first hints about how these antecedents can lead to organizational change related to nonfinancial reporting. For example, the larger a company becomes, the more visibility it gains for different stakeholders, so managers may be inclined to disclose more nonfinancial information to meet stakeholder expectations (Schreck & Raithel, 2018; Wickert et al., 2016).

In terms of antecedents outside organizations, one of the most crucial environmental factors influencing nonfinancial reporting are standards and regulations (H. B. Christensen et al., 2021). Although nonfinancial performance has become a central concern for many managers, investors, and consumers over the years, no universal approach for measuring and reporting nonfinancial performance exists. Rather, we face a “plethora of names and frameworks” (Eccles & Mirchandani, 2022) that have been promoted recently through a variety of actors. In terms of reporting frameworks, these include, among others, the Global Reporting Initiative (GRI), the Sustainability Accounting Standards Board (SASB), the Task Force on Climate-related Financial Disclosures (TCFD), and more recently, the International Sustainability Standards Board (ISSB) and the European Financial Reporting Advisory Group (EFRAG). Moreover, also rating agencies who draw on information provided by nonfinancial reports influence how reporting might lead to real sustainable change. While it can more generally be assumed that the pressure exerted on companies to achieve favorable ratings, the picture is complicated because as recent research shows different rating agencies possess proprietary evaluation schemes that tend to either measure different things, or measure the same things differently (Berg et al., 2022). Only time will tell whether and how the different initiatives and standards will co-exist, and what impact they will have on nonfinancial reporting on the output level and corporate sustainability performance from an outcome perspective.

Against the background of such fragmentation, the literature has examined the role and design of nonfinancial reporting standards (e.g., Grushina, 2017; Rawhouser et al., 2018). Other studies have questioned the efficiency and effectiveness of the diverse nonfinancial reporting landscape where voluntary guidelines exist alongside mandatory reporting regimes (e.g., Aragòn-Correa et al., 2020; H. B. Christensen et al., 2021; Eberlein, 2019). Research has also critically examined how and why national standards coexist and compete with international frameworks (e.g., Einwiller et al., 2016). Overall, a paradigm shift from reliance on market forces to (globally) mandated nonfinancial reporting standards is currently developing, while the efficacy of one or the other approach remains contested (Eccles, 2021). The extent to which such a globally unified approach enables or hinders real sustainable change will also depend on the range of nonfinancial topics that are considered material and mandated to be reported. This materiality debate (i.e., the question of which kind of information matters for whom and thus should be reported) is still ongoing (e.g., Eccles & Mirchandani, 2022; Reimsbach et al., 2020).

The example of regulations is illustrative of the complicated organizational change processes that link antecedents to output and outcomes. For example, if a new regulation forces companies to report on human rights risks, management could react by implementing due diligence processes along its supply chain to gather the necessary information to be reported. This links the antecedents of nonfinancial reporting (C) with output (A). Owing to the increased transparency of human rights risks, the same company would then feel pressured to set specific targets on human rights issues for its suppliers to reduce risks in the next reporting period. Such structural changes could lead to behavioral changes if the reporting process induces changes in individual or collective behavior within an organization or among its suppliers. However, if a company merely introduces ceremonial or symbolic changes (Lyon & Montgomery, 2015) to fulfill regulatory requirements, the respective antecedents would lead to changes in output (reporting) but not outcome (real sustainable change).

Such organizational change processes thus represent crucial elements linking the elements of our framework, because they illuminate the causal mechanisms underlying the assumed relationships. These change processes most likely have repercussions, feedback loops, path dependencies, and cross levels of analysis. Therefore, actions taken in relation to output management influence the actions taken related to outputs and impacts. These effects are indicated by arrows at the bottom of Figure 1. However, researchers have just begun to disentangle these organizational change processes related to nonfinancial reporting, specifically those related to outcomes. While many questions remain, the contributions to this special issue collectively make a major contribution that accelerates our understanding of the complicated relationship between nonfinancial reporting and real sustainable change. We summarize these contributions in greater detail below.

Disentangling the Complicated Relationship Between Nonfinancial Reporting and Real Sustainable Change: Contributions of the Special Issue

The first contribution of this special issue is Garcia-Torea et al.’s (2023) literature review on nonfinancial reporting and real sustainable change based on a cross-disciplinary perspective that includes accounting and organization studies. The authors show that accounting researchers have been exploring the transformative potential (i.e., the links between C to A to B in Figure 1) of social and environmental reporting since its inception, whereas researchers from the organization studies domain have only recently developed interest in this issue. Importantly, the review stresses that nonfinancial accounting and reporting “can initiate change, albeit of a limited nature” but also “inhibit sustainable organizational change” (Garcia-Torea et al., 2023, p. 8). This is an important insight on the link between output (A) and outcome (B). Importantly, this literature review outlines multiple bridges for generative conversations in an interdisciplinary research field on the link between nonfinancial reporting and real sustainable change. The authors specifically highlight several important broader avenues that should receive more attention, such as scrutinizing the direction of causality between nonfinancial reporting and organizational change.

Departing from this generative review of the literature, this special issue delves into the empirical complications that characterize the link between nonfinancial reporting and real sustainable change, with two contributions zooming in on the role of external stakeholder pressures through the media to report on attempts to achieve real sustainable change. First, Andrus et al. (2023) examine the uneven returns of transparency in voluntary nonfinancial reporting and, in doing so, question the performance implications of reporting. Motivated by conflicting findings in the literature, the authors examine how different dimensions of transparency of reporting are perceived, and thus rewarded, by market and nonmarket actors. Based on data from the CDP (formerly the Carbon Disclosure Project) and drawing on attribution theory, they show that firms that successfully address key stakeholder expectations through nonfinancial reporting are better able to improve their financial performance and manage long-term risks. Specifically, the findings suggest that the completeness, clarity, and accuracy of voluntary nonfinancial disclosures affect both market (i.e., market valuation) and nonmarket (i.e., reputation risk) reactions, thereby shedding light on the factors that influence the relationship between antecedents and outputs (C to A in Figure 1).

Second, based on an analysis of stakeholder-initiated communication on social media, Dobija et al. (2023) contrast voluntary with involuntary reporting, with the latter often being mobilized by stakeholders through social media. The authors analyzed more than 100,000 Twitter replies from seven companies to identify their responses to involuntary nonfinancial reporting practices. They found that company responses ranged from active communication to almost complete silence. However, those companies that engage in communication with their stakeholders do so in a mostly one-way manner, where mortification or dissent are the likely response strategies. According to the study, while stakeholders generally do not engage in corporate communications, they are likely to respond when companies deny the information revealed by involuntary disclosure. Overall, the results suggest that involuntary disclosures are unlikely to be a mechanism through which meaningful communication between companies and stakeholders develop, thus complicating the achievement of real sustainable changes in corporate behavior. Therefore, their study examines factors along the pathway from antecedents to outputs and whether these will materialize into outcomes (C to A to B in Figure 1).

The next three contributions by Fu (2023), Bauckloh et al. (2023), and Crace and Gehman (2023) model real sustainable change as an explicit dependent variable, uncovering important complications with its relationship to nonfinancial reporting. Fu (2023) mobilizes signaling theory to examine how negative media coverage affects real sustainable change in the form of firm nonfinancial performance (C to A to B in Figure 1). This study finds that negative media coverage on corporate social irresponsibility (CSiR) is costly yet effective external feedback to firms’ current social signaling, inducing firms to report and improve their nonfinancial performance. Furthermore, the study results show that organizational search for innovation augments the impact of negative media coverage on firms’ nonfinancial performance by virtue of its incentive and competency to improve this type of performance.

In their study on how mandatory climate reporting leads to changes in firms’ carbon emissions, Bauckloh et al. (2023) also question the implications of nonfinancial reporting on real sustainable change. Drawing on legitimacy theory and using a difference-in-differences design, the authors assessed the effect of the Environmental Protection Agency’s Greenhouse Gas Reporting Program (GHGRP), introduced in 2010, on carbon performance, defined as the carbon intensity and absolute carbon emissions of affected firms. In doing so, Bauckloh et al. (2023) make an important yet underemphasized distinction between relative and absolute emissions, namely that nonfinancial reporting may help reduce relative emissions (i.e., carbon intensity, defined as the efficiency of firms’ carbon emission-producing operations), but not necessarily absolute carbon emissions. However, a reduction in absolute carbon emissions at a global level is crucial for achieving global climate targets. Thus, their research underscores that mandatory climate reporting regimes, such as the GHGRP, can provide the necessary incentives to limit firms’ impacts on climate change, but are not necessarily self-sufficient to reach national or international climate goals (Bauckloh et al., 2023). Thus, caution should be exercised when considering outcomes (relative vs. absolute) with sustainability-related outputs (A to B in Figure 1) based on different regulatory backgrounds (C to A in Figure 1).

In the next contribution, Crace and Gehman (2023) ask why there is large heterogeneity in nonfinancial performance between firms. To address this question, they disentangle the antecedents of firm-level performance on nonfinancial aspects across an array of positive and negative ESG indicators, thus examining the pathway from antecedents to outputs and outcomes (C to A to B in Figure 1). Their research shows that variation in nonfinancial performance, and thus a company’s ability to achieve real sustainable change, is more due to asymmetrical internal (e.g., firm, CEO) than external (e.g., industry, year, state) effects, and differs significantly depending on which nonfinancial aspects are considered. Furthermore, they show that disaggregation of the multidimensional ESG construct significantly shifts the salience of the factors, revealing the importance of the external environment (i.e., industry and year) in explaining ESG concerns. Importantly, as Crace and Gehman (2023) show, the observed strong industry effect indicates that a one-size-fits-all reporting approach, for instance, as manifested in regulations for mandatory reporting, may not be uniformly effective across industries when attempting to stimulate real sustainable change. However, differentiated reporting frameworks may have stronger effects.

Finally, while the above contributions bring us closer to understanding the complicated relationship between nonfinancial reporting and real sustainable change, van Bommel et al. (2023) take us a step back and allows for reflection on some potentially unintended consequences. Drawing on extensive case study evidence, van Bommel et al. (2023) delve into the ethical dimension of nonfinancial reporting and show that it has metamorphosed from a value-based practice into a monetized one, thus leading to a crowding out of morality in favor of strategic and instrumental considerations of reporting firms. The authors’ analysis highlights that as reporting, based on a process described as commensuration, shifted from an emphasis on moral values toward a focus on financial value creation, it became more difficult to associate nonfinancial issues with potential moral dilemmas.

Collectively, these contributions further our understanding of the relationship between nonfinancial reporting and real sustainable change in multiple significant ways. While providing answers to a range of critical research questions, they also provide the space to ask new questions about many of the unresolved issues where scientific advancements are still needed. Taking the contributions of this special issue as a starting point, we outline important areas for future research.

A Research Agenda on How to Create Real Sustainable Change With Nonfinancial Reporting

Departing from the insights that the contributions to this special issue have generated, we now sketch some important avenues for future research and outline suggestions on ways to address them methodologically and conceptually. We propose three broad yet interrelated areas in need of attention. First is to analyze the impact of real sustainable change beyond outputs. Second is to examine the organizational change processes that span the entire spectrum of our framework, from antecedents to impact. Third is to study the potential interaction effects between nonfinancial reporting and other measures intended to achieve real sustainable change.

Analyzing the Impact of Real Sustainable Change Beyond Outputs

Normatively speaking, real sustainable change in organizations is meaningless if it does not ultimately materialize into societal impacts that improve key social and environmental conditions. Research should disentangle the complicated nature of sustainability-related outcomes that business aims are expected to deliver and examine their relationship with impact. Thus, we encourage future research to explore the missing links among the key components of our guiding framework. In fact, outcomes are often long-term, nonlinear, and in many cases not easily measured, specifically when they relate to social outcomes (Barnett et al., 2020; Kühnen & Hahn, 2018). To tackle the elusiveness of respective issues, such as human development, we advocate interdisciplinary research collaborations, for example, at the intersection of business and sociology. Furthermore, for aspects of ecological sustainability, similar interdisciplinary collaborations may be beneficial to connect business outcomes with impacts in the realm of the natural sciences.

On this basis, future research should specifically determine the relevant outcome indicators in relation to social and ecological goals. Here, the work of Bauckloh et al. (2023) provides an important starting point, as they show the critical difference between relative and absolute outcomes in the context of greenhouse gas emissions. Researchers can identify this distinction and examine how and why organizations would achieve one or more types of outcomes. Presumably, firms may focus on “easy to achieve” relative outcomes, such as energy efficiency, to disguise potentially negative absolute outcomes, including overall emissions of their fleet or sites. Thus, research should examine the factors that promote the establishment of absolute outcome indicators as meaningful measures of real sustainable change, not only for climate-related or other ecological issues but also in the area of social sustainability, which is often even more difficult to measure (Kühnen & Hahn, 2019).

However, prospective studies should pay close attention to outcome changes not only at the company level, but also at the industry and field levels to avoid potentially flawed conclusions. For example, researchers may find that improved relative outcomes (e.g., carbon emissions per revenue) accompany worsened absolute outcomes (e.g., total carbon emissions) for specific firms. If such a result is an industry-wide outcome of certain reporting practices, it would have a detrimental effect on climate change. However, increasing absolute and decreasing relative emissions at some companies could also be the result of increasing market shares of less polluting companies at the expense of more polluting companies, which could be the case in emissions trading schemes such as the Regional Greenhouse Gas Initiative (RGGI) in the United States or the Emissions Trading Scheme (EU ETS) in the European Union. Thus, increasing absolute emissions at the firm level does not necessarily have to result in increasing absolute emissions at the industry level.

Studying the Organizational Change Processes From Antecedents to Impact

In addition to questions regarding outcomes and impacts, the actual organizational change processes underlying the links between the key components of our framework are still poorly understood, specifically because they are often influenced by factors that cross levels of analysis. For example, research struggles to explain causal linkages from outcomes attributable to corporate sustainability activity to the impacts these activities might create and how this can be linked to specific products and services a company offers. In terms of nonfinancial reporting, an important question would be to examine which actors, internal and external, use what kind of information in relation to outputs, outcomes, and impact, and how this is related to organizational change processes. The study by Fu (2023) is a good starting point, for it argues that negative media coverage encourages firms to undertake organizational changes to send positive response signals through improved nonfinancial performance. Future research should explicitly analyze and model these change processes and embrace a variety of research methods to do so (Lewis & Carlos, 2022).

Longitudinal process studies, such as ethnographic observations and multilevel studies, may be particularly suitable to study the underlying change processes in the entire pathway from (internal and external) antecedents to outputs, outcomes, and impact, for instance, through single or multiple comparative case studies. Here, researchers should pay particular attention to the interdependencies between possible structural and behavioral changes that may occur in organizations and how those either accelerate or deccelerate real sustainable change. With respect to behavioral change, researchers could analyze how the internal dissemination and transparent usage of nonfinancial reporting and concomitant data affect behavior, while structural change might be affected by specific outputs like nonfinancial reports being mandatory or voluntary.

In this regard, recent regulatory developments are likely to be especially relevant for future research. In March 2022, for example, the SEC proposed new rules on climate-related reporting, and the International Sustainability Standards Board (ISSB) published a proposal for reporting on sustainability-related financial information. Only 1 month later, the EU’s Corporate Sustainability Reporting Directive (CSRD) with exposure drafts by the European Financial Reporting Advisory Group (EFRAG) was published. One important element in this regard is that not all nonfinancial issues fall under the scope of each initiative, as their understanding of materiality differs significantly. While the ISSB follows the interpretation of “single materiality” where information is material if it financially matters for investors, the CSRD has a broader “double materiality” mandate that covers issues that can either be financially material or affect other stakeholders. Considering these regulatory developments, we are yet to see how the relationship between nonfinancial reporting and real sustainable change will develop under future reporting regimes. Generally, given the rapid pace at which new regulations are being developed and will most likely continue to develop in the future, we urge scholars to pay attention to state-of-the-art regulatory regimes and to reflect upon how effective and efficient policy making would look like.

Apart from event studies and natural experiments that take advantage of the introduction of new regulations worldwide, we also encourage researchers to further leverage the broad range of experimental methods that analyze the behavioral aspects of change (processes). A few examples of more traditional laboratory experiments exist in the realm of nonfinancial reporting and behavioral change (e.g., Martin & Moser, 2016), but they primarily focus on the associated economic effects. We suggest that other experimental methods such as factorial survey experiments, a hybrid approach combining elements of survey research and classical experiments (e.g., Oll et al., 2018), and field experiments that take the “controlled” setting from the laboratory to the field (e.g., Delmas & Aragon-Correa, 2016), are more suitable for testing questions related to real sustainable change beyond the economic focus. For example, factorial survey experiments could be used to address customer preferences in response to nonfinancial reporting, while employee behavior following the initiation or change of nonfinancial reporting could be studied experimentally in the field.

Studying Interrelationships Between Different Instruments to Foster Real Sustainable Change

While this special issue focused on nonfinancial reporting, other instruments that seek to foster real sustainable change within organizations exist. When considering carbon emissions, for example, carbon reporting as a subcategory of nonfinancial reporting is only one possible instrument in the toolset of regulators and sits next to, for example, market-based instruments for carbon prices (e.g., Stiglitz, 2010). At the organizational level, this could be accompanied by managerial incentive systems, including carbon performance measures. There is reason to believe in the mutually reinforcing mechanisms of these instruments. High carbon prices could lead to increased corporate carbon reduction efforts, especially in a setting of transparency generated by carbon reporting, further propelled by the inclusion of carbon performance into incentive systems. However, scientific evidence for such interactions is scarce. Future research should therefore examine the interdependencies between different instruments geared toward real sustainable change, as well as toward how and why some measures may jointly influence organizations. More generally, nonfinancial reporting typically goes along with sustainability strategy, changes in leadership, commitment to achieve more advanced levels of sustainability implementation, and membership in a sustainability or multi-stakeholder initiative. Collectively, these instruments may have a stronger effect on real sustainable change, but they also create more complexity in organizations that are costly to administer.

Qualitative studies are ideally suited to, for instance, examining the perceptions and decision-making of actors tasked with managing one or more of these instruments and analyzing how they juggle interdependencies. Here, comparative case studies seem particularly insightful if they examine organizations that have shown different combinations of instruments that materialize into different types and/or levels of outcomes and impacts. Quantitative studies, in turn, could investigate the effect sizes on real sustainable change when organizations employ one or more of the abovementioned instruments. Here, an important detail is to further investigate how the forms of nonfinancial reporting—a standalone sustainability report or an integrated report (Reimsbach et al., 2017)—may be better suited to stimulate real sustainable change.

Finally, the proposed chain of effects from increased transparency through reporting to improved sustainability performance can only materialize if the respective reporting practices provide a true and fair view of a firm’s nonfinancial performance. If regulation is weak and standards are largely voluntary, companies may be incentivized to engage in greenwashing (e.g., Delmas & Burbano, 2011; Kim & Lyon, 2015). Building on legitimacy theory (e.g., Suddaby et al., 2017), Hummel and Schlick (2016) show that poor sustainability performers engage in low-quality reporting to disguise their weak performance. Future research could investigate incentives to engage in truly transparent reporting and scrutinize the user’s perspective of nonfinancial reporting. An interesting question would be, for example, how users of nonfinancial reports such as investors react to different qualities of reported information and how such reactions, in turn, affect organizational decisions to improve sustainability performance (or not).

Conclusion

In this introduction to the special issue on nonfinancial reporting and real sustainable change, we have taken stock of how this collection of articles has advanced our understanding of this complicated relationship. Yet, as we have outlined above, more research is needed to explain how and why important instruments such as nonfinancial reporting drive progress toward real sustainable change. One important step is to move away from sustainability-related outputs that many business firms are typically quite good at delivering, toward sustainability-related outcomes and ultimately impacts. While it is challenging to achieve this shift, progress in sustainable development fundamentally depends on it. Consequently, we call for change that may push firms into uncomfortable self-examinations and unfamiliar domains of activity. This imperative for redirection is not limited to firms, however, as researchers must also recognize the imperative to reorient their scholarship toward more meaningful outcomes.

Footnotes

Acknowledgements

We thank Robert Eccles for his company and valuable advice during the process of editing this special issue. We are furthermore grateful to editor Mike Russo for his continuous support. Most of all, we thank all authors included in this special issue for their contributions.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.