Abstract

In this paper, the increase in online grocery ordering in the UK during the COVID-19 pandemic is examined, and a prediction is made that is opposed to the balance of opinion expressed online. In their online comments, most practitioners claim that the increased use of the Internet for ordering groceries for home delivery will be sustained and will continue to grow after the risk of disease has subsided. Given the pattern of consumer behaviour in another field, discount purchasing, it seems more likely that online grocery ordering will fall back and then continue to grow at a modest pace, as it did before the pandemic.

Introduction

The COVID-19 pandemic has made consumers change their purchasing behaviour and avoid retail premises. As a consequence, online sales have increased. The focus here is on the sales of groceries online, which increased substantially with the onset of the pandemic. Practitioners anticipate retention of this increase and a further rise in sales in following years. Researchers can predict whether online grocery sales will continue to increase by using evidence on how people react in related circumstances. On this basis, it seems unlikely that practitioner claims will be fulfilled. Predictions of this sort allow us to test the robustness of our current knowledge.

UK grocery retailers have played an important part in managing the pandemic. Managements substantially increased online shopping, while retail staff worked, at some risk to themselves, to keep the nation fed. Substantial investments in equipment and staff were made to boost online sales and, despite increased sales, Morrison and Sainsbury have both reported reduced profit because of increased costs. In a world in which virtue is rewarded, customers would maintain their online purchasing post–COVID-19 and supermarket firms would then make a return from their investment. However, if online sales drop back towards the pre–COVID-19 level, much of the investment made in home delivery will lie idle and managements may then need to focus more on instore provision. Thus, it is important to use our knowledge of consumer behaviour to predict the future pattern of sales: have consumers been deflected from their normal mode of shopping, only to return to their previous pattern when the risk of infection has gone, or have they learned a new pattern of behaviour which will stay with them in the future?

The UK is surpassed only by South Korea in the use of online grocery ordering and may act as a bellwether for this channel of distribution. For this reason, there is an interest in how online sales develop in the UK.

Online Sales

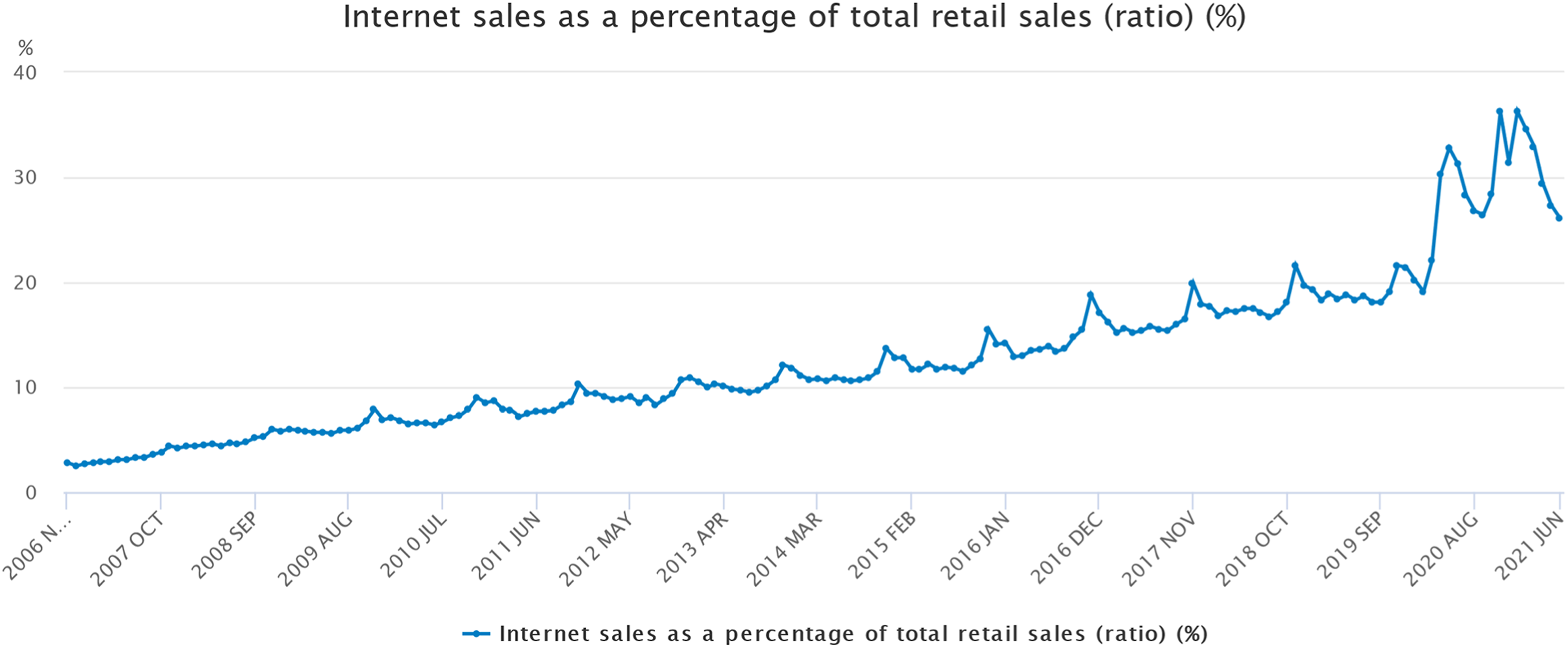

In the UK, the Office for National Statistics reported an increase in all Internet sales from less than 20% to approximately 33% at the beginning of the pandemic; in 2021, the increase fell back as shown in Figure 1 (ONS, 2021). Internet sales as a percentage of total retail sales (Office for National Statistics).

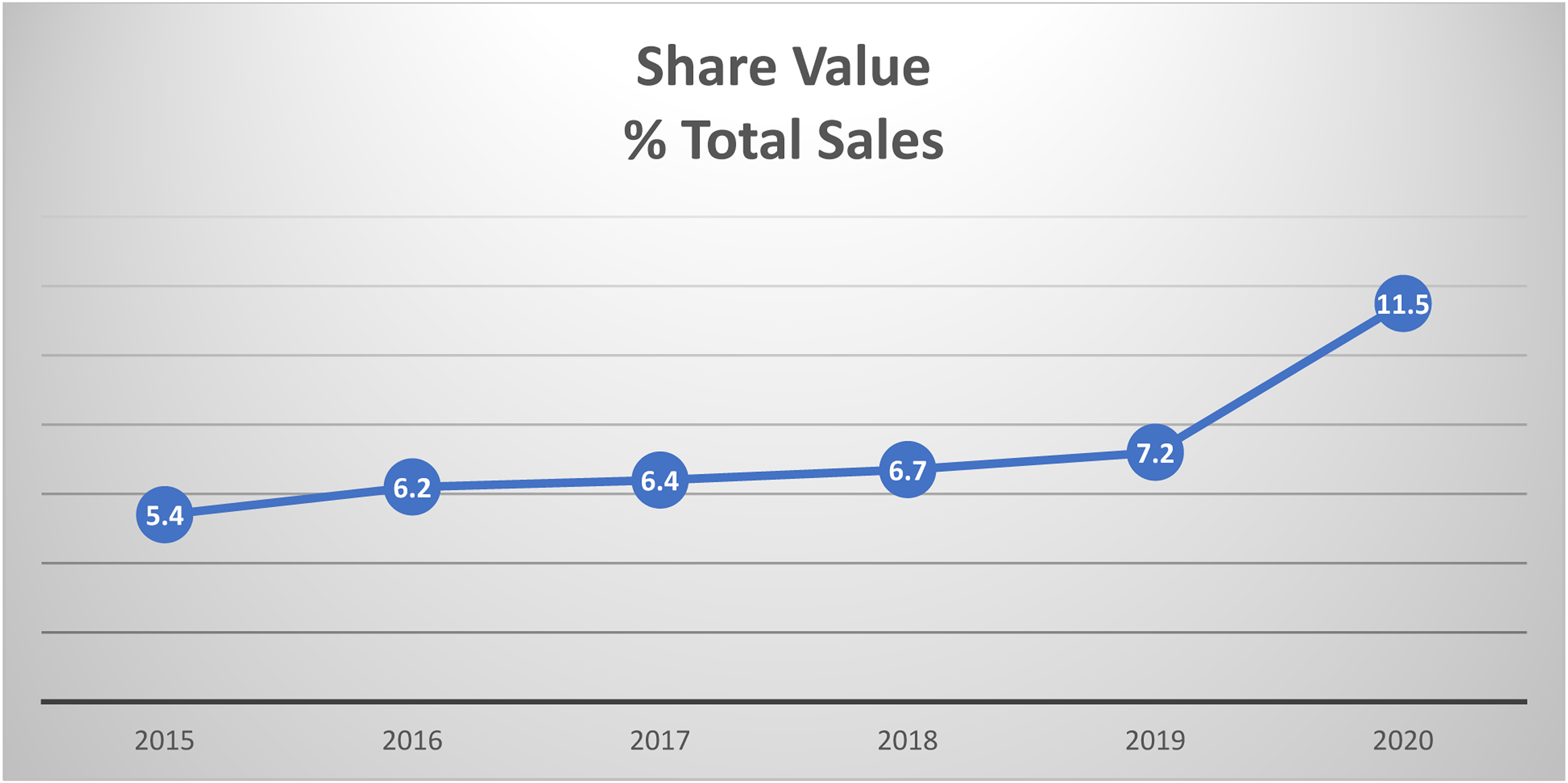

This raises a question about the future of online grocery sales: will the increase hold in the post-pandemic period or will sales tend to return to the pre-pandemic pattern? Five years of online grocery sales in the UK, reported by NielsenIQ is shown in Figure 2. This shows increases in sales from 2015 to 2019. In 2020, online sales took off and, in the last quarter (not shown), the share was 13.1%. The figure shows that although the year-on-year percentage increases in the pre–COVID-19 period were quite large, the online share was quite small. Internet grocery share value as a percentage of all grocery sales (Data supplied by Nielsen Homescan, 2021).

A UK Statista (2021) survey of online grocery shoppers indicated that there would be some post-pandemic decline in sales. When shoppers were asked about their prospective online shopping after the pandemic, 42% expected to maintain their level, 33% to use online less often, 18% would probably stop and 7% expected to increase their level. However, practitioners expect online grocery buying to continue at the level reached during the pandemic. Davey (2020) refers to a Reuters report on this matter and cites Ocado CEO, Tim Steiner, who foresaw the online market doubling in the next few years and believed that online would eventually become the major channel. Ocado are specialists in the design of online fulfilment systems, and the Ocado share price, in March 2021, was approximately twice its pre-pandemic level and ten times its level in 2017. Steiner’s enthusiasm for online is supported by others. Goldsmith (2021), citing work by NielsenIQ, expressed similar expectations. In Europe, McKinsey & Co (2021) were more cautious and expected a muted post-pandemic return to the stores, but noted that the online experience was less satisfactory in continental European countries where this channel was less used before the pandemic. In the USA, the Mercator Advisory Group (2021) expected online grocery sales to be maintained after the pandemic, and Supermarket News (2020) expected online to more than double by 2025.

Further evidence on online grocery sales in August 2021 shows that the situation remains equivocal. A report using NielsenIQ data on May sales in 2021 indicated that Internet grocery purchase was holding up (Skeldon, 2021). However, a report based on Kantar data found a minimal decline from 13.4% to 13.3% in the 4-week period before June 11th compared to the equivalent period a year before (Kantar, 2021). However, at this time, infections were still rising, which was not conducive to a return to the physical stores.

Related Evidence

New markets that succeed usually show an S-shaped growth curve, accelerating initially, reaching a maximum rate of growth, and then slowing down as potential new customers become fewer (Bass, 1969; Rogers, 2003). There is no evidence in Figure 2 of any acceleration in online grocery sales before the pandemic began despite the resources that were devoted to this channel by the major retailers. On this evidence, we should not expect rapid growth in online sales after the pandemic has ended.

A further question is whether the increase in sales brought about by the pandemic will be retained, as practitioners have predicted. A study by Hand et al. (2009) noted that the first use of online grocery purchase was usually driven by particular circumstances but this study also found that people often discontinued online ordering once the initial trigger had disappeared. On this evidence, shoppers could go back to shopping in the store when the trigger of disease prevention is removed. Lacking direct evidence on this, we consider the effect of sales promotions which also produces a surge of extra sales. Ehrenberg, Hammond and Goodhardt (1994) found that the normal pattern after the promotion has finished is for sales to revert to the pre-promotion level. One factor here is that shoppers have usually bought the discounted item before – it is in their repertoire – so no new learning occurs when they buy it on discount. In the same way, it is likely that many households were familiar with online ordering before COVID-19 and simply raised their level of usage during the pandemic. McKinsey & Co report that only 15% of respondents to a European survey used online grocery ordering for the first time during the pandemic, indicating that few people acquired new experience of this channel. The lockdown periods in the UK were more sustained than a promotion period, but this does not mean that shoppers found that online ordering was more attractive than previously or that the store was less agreeable after the pandemic.

We should not forget that many shoppers like bricks-and-mortar stores. A Which? review of a YouGov survey noted that 51% stated that they enjoyed supermarket shopping and that people like to assess quality themselves and enjoy the social contact of instore shopping (Train, 2017). They may also use the sight of goods on the shelves to remind themselves of what they need or to suggest new purchases. In addition, visits to the supermarket can be combined with shopping for items in other stores or markets. Some of the modest proportion of shoppers who used online shopping for the first time during the pandemic will have discovered advantages and may stay with this method of buying, but others may dislike the time taken for ordering and the cost of slots when these have to be purchased. They may also find that, after the pandemic, it is difficult for them to be at home for deliveries.

Supermarket Strategy

On this evidence, it seems likely that any post-pandemic carryover of online shopping will be limited. If this is the outcome, the store groups will not recoup their investment in online service rapidly. It was fortunate that the major UK store groups had invested in online service because this allowed them to play an important role in servicing customers at particular risk from COVID-19. However, from a commercial standpoint, this effort probably returned little profit since order picking and delivery raises the cost of fulfilling online orders. It seems likely that one of the reasons for the substantial investment in online provision in the UK was that managements were reluctant to lose shares. However, if online sales give lower margins than instore selling, managements should look again at ways of strengthening the appeal of traditional shopping.

Managements can increase the range of services offered instore and make the store environment more entertaining. In the first half of the week, large stores are less patronised and can put on functions that will draw more customers and keep those that do come for longer so that they spend more. Supermarkets with underused space can entertain with cooking and new product demonstrations; they can engage more with the local community, advertise jobs, provide samples, play enjoyable music and enhance the café so that it offers a more exciting experience. At certain times of the day, there could be entertainment for toddlers; at other times, for those who are retired. The car park could host second-hand markets. They might even take a leaf out of Amazon’s book and host competitors such as farmers’ markets. The loss of instore trade to such competitors could be more than covered by the extra sales from increased footfall. Facilities of this sort would help the major supermarkets to compete with the online channel and would aid competition with the deep discounters which lack the space, either inside or outside the store, to create much enhancement of the shopping experience. Store groups such as Tesco that have shopper databases from their loyalty programmes can easily communicate such changes to shoppers.

Seasoned store managers may see these suggestions as cosmetic and unlikely to have much effect on sales but they would do well to note the evidence from store atmospherics research. This field is concerned with the impact on sales when stores alter shoppers’ sensory experiences. To consider just one area, music: if you play French accordion music in a wine store, you sell more French wine (North, Hargreaves and McHendrick, 1999); if you play classical music, more expensive wine is chosen (Areni & Kim, 1993); if you play slow-tempo music in supermarkets, customers slow down and buy more – quite a lot more, 38% in Milliman’s (1982) study. Effects like this are not cosmetic and suggest that a store group can change the instore experience in ways that produce substantially more sales.

Conclusion

The prediction made here that online grocery purchase will fall back in the post-pandemic period is conditional on an effective end to the pandemic. It seems likely that infections will continue but that vaccination will reduce their frequency and mitigate their effects. In these circumstances, the pandemic may not fully end, but if there is a general relaxation in precautionary measures, it seems likely that there will be a reduction in online grocery sales and a return to the growth pattern that applied before the pandemic. In this event, supermarket managements will need to revise their strategy on online fulfilment and take steps to enhance the store experience.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.