Abstract

Crowdfunding has become an established means for new ventures in search for funding and it has received increased attention from scholars and policy makers. One of the most relevant aspects of crowdfunding is to understand the factors associated with the success of a campaign. This paper addresses the issue with a novel dataset of 89 Italian campaigns. Three indicators of campaign success (funds received, funds as a share of target, and number of investors) are estimated as a function of different dimensions of human capital (team size, education, and work experience). We find that campaign success is correlated to team size, the share of members with very high education (i.e. PhD), and the share of members with business education. We also find a non-linear relation with team size, and a significant relationship with the diversification of the team's education. Our study contributes to a recent body of empirical studies on the determinants of the success of an equity crowdfunding campaign by confirming previous findings with a novel dataset and by providing new evidence on the relevance of signals of the founding team quality (e.g. diversity of education) and increasing return of funding to team size.

Introduction

Crowdfunding is a recent and growing source of entrepreneurial finance that attracts the attention of researchers and policy makers. Crowdfunding gives entrepreneurs access to online market platforms to make an open call to sell equity shares (equity-based model) or bonds (lending-based model) in the company (Howe, 2008).

Similar to other forms of alternative finance (Miller et al., 2019; Pierrakis, 2019), equity crowdfunding (ECF) responds to the financial constraints of many new ventures and provides additional benefits in terms of marketing and product development (Angerer et al., 2017; Block et al., 2018; Kleinert et al., 2020). The main difference with venture capital (VC) and business angel networks is the large number of relatively inexperienced funders who invest small amounts of money. The typical investor has limited opportunities to interact with the investee and plays a passive role after the deal. Moreover, compared with professional investors, non-professional investors lack the capacity to assess the quality of a startup. These peculiarities exacerbate the information asymmetry between investors and investees and call for a deeper understanding of the signals that affect the success of crowdfunding campaigns (Ahlers et al., 2015; Block et al., 2018; Kleinert et al., 2020; Lukkarinen et al., 2016; Piva and Rossi-Lamastra, 2018; Troise et al., 2020).

Startups’ founders use ECF when other capital sources such as bank loans and VC are either unavailable or limited. At the same time, this alternative source of capital fulfils other purposes like raising brand awareness, product testing, community building, and publicity, which in turn can attract future investors (Angerer et al., 2017; Estrin et al., 2018).

Based on the signalling theory (Spence, 1973), scholars have investigated which signals most effectively disclose information on the quality of a startup and determine the campaign success. Education, experience, knowledge and skills of founders are considered signals of quality for crowdfunding investors (Mochkabadi and Volkmann, 2020) that suggest the ability to discover and exploit business opportunities (Shane and Venkataraman, 2000) and increase future learning (Ahlers et al., 2015). Therefore, investors search for and evaluate especially the characteristics of the founder(s) as well as those of the top management team. We define the top management team (TMT) as the group of the members of the board of directors and the founders.

The literature analyses various dimensions of the TMT: i) size, ii) educational background, and iii) work experience. Extant empirical evidence generally confirms that these three factors are positively correlated to campaign success (Ahlers et al., 2015; Kleinert et al., 2020; Li et al., 2016; Piva and Rossi-Lamastra, 2018; Ralcheva and Roosenboom, 2020; Vismara, 2016). However, results are not robust across different studies, calling for further empirical analysis.

Our study is based on a new dataset on 89 ECF campaigns which appeared in four Italian platforms in 2016–2019. This is an interesting empirical setting. In 2014–2019, Italian ECF experienced rapid growth, yet the size of the Italian market remains small compared to other European countries (Ziegler et al., 2021). Various recent regulations favoure ECF to support online financing of innovative startups and small ventures, including in low-tech sectors such as food and tourism. The growth and survival rates of new venture after participation in crowdfunding campaigns are low (Osservatori Entrepreneurship & Finance, 2019), but in line with those of other new ventures (Coad, 2009).

Our study contributes to the literature on the determinants of ECF success by providing evidence on the relationship between three dimensions of TMT (size, education and experience) and campaign success (Ahlers et al., 2015; Angerer et al., 2017; Kleinert et al., 2020; Li et al., 2016; Piva and Rossi-Lamastra, 2018; Ralcheva and Roosenboom, 2020; Vismara, 2016; Vulkan et al., 2016). Our findings provide additional support to earlier works which point out the relevance of the size and the business education (Ahlers et al., 2015; Ralcheva and Roosenboom, 2020; Vismara, 2016). We also find that campaign success is correlated with the presence of members with a PhD (Ahlers et al., 2015; Kleinert et al., 2020) and TMT diverse education (Kaplan and Strömberg, 2004; Piva and Rossi-Lamastra, 2018). Unlike other studies, however, we find no evidence of the importance of entrepreneurs’ experience, i.e. working years and age (Kleinert et al., 2020; Piva and Rossi-Lamastra, 2018; Ralcheva and Roosenboom, 2020). Finally, we find that team size has a non-linear relationship with campaign success: the positive effect of TMT on campaign success increases more than proportionally as the number of members grows.

The paper is organized as follows. In Section ‘Determinants of campaign success’, we discuss the determinants of campaign success, and we review the empirical literature. Section ‘Data and methodology’ displays the dataset and the methodology, while Section ‘Analysis’ presents the results. Finally, Section ‘Conclusion’ draws the conclusions.

Determinants of campaign success

ECF is a form of funding a new venture where the investors obtain an equity share in the company with expectations of financial returns (Gleasure and Feller, 2016). Entrepreneurs make an open call to sell shares to a large group of investors who typically spend a small amount of money. Unlike other forms of venture finance, their role usually remains passive after the deal (Ahlers et al., 2015; Carbonara, 2021; Miller et al., 2019). These characteristics entail significant information asymmetry between investors and investees and make ECF more risky than other sources of financing.

A successful campaign brings funds, but also media exposure, marketing effects, and the attention of future professional investors. Since many platforms are based on the “all-or-nothing” system for which the venture receives the funds only if the target is achieved, campaign success implies that the project meets the target (Kleinert et al., 2020; Piva and Rossi-Lamastra, 2018). The total amount of money raised is an additional sign of success, especially when this value is significantly higher than the target. A larger number of investors is also considered a sign of campaign success; this is particularly true when a firm commercial performance relies on building a large user community or when reaching a higher audience through crowdfunding helps generate network effects.

The drivers of campaign success in ECF have been mainly discussed in the context of signalling theory. As other forms of investment, ECF entails taking decisions in a risky and uncertain context. New organizations face a high failure rate, being exposed to numerous technical and commercial challenges. In addition, new firms rarely have a record of past revenues and profit, which makes it extremely difficult to signal their quality and increases information asymmetry in the market for capital. Entrepreneurs have information on the quality of the company (e.g. the technology and the persons involved in the project), but investors lack the information for a complete assessment of their investment. While the literature on new venture financing recognizes the presence of information asymmetry between entrepreneurs and investors, ECF exacerbates this difficulty because non-professional and small investors lack the experience and expertise needed to evaluate new ventures. In a well-functioning market, entrepreneurs signal the quality of their firm to investors (Hoenig and Henkel, 2015; Spence, 1973). Drawing on signalling theory, entrepreneurs must send information about the unobserved quality of the firm to investors to mitigate information asymmetry.

Human capital

Human capital is one of the most widely investigated type of signals in ECF (Mochkabadi and Volkmann, 2020), following the well-established connection between personal traits and entrepreneurial success (Baum and Silverman, 2004; Franke et al., 2008). The underlying explanation is that human capital enhances the ability to discover and exploit business opportunities (Shane and Venkataraman, 2000) and increases future learning (Ahlers et al., 2015). Therefore, investors are supposed to search for and pay particular attention to the characteristics of the TMT in assessing the value of their investment.

The characteristics of the TMT mainly analysed in the literature are: i) team size; ii) education, and iii) experience.

Team size

In entrepreneurial literature, there is an increased awareness that the formation of new ventures is generally based on teams as opposed to single entrepreneurs and that the founding team has a strong influence on new venture success (Klotz et al., 2014). Team size may signal the “quantity” of human capital available. However, extant empirical evidence is not conclusive. Earlier works find that the number of board members (Ahlers et al., 2015; Vismara, 2016) or directors (Ralcheva and Roosenboom, 2020) positively affect campaign success. Other works report that the number of entrepreneurs in the startup is not a significant predictor of the campaign success (Piva and Rossi-Lamastra, 2018).

To the best of our knowledge, no earlier study investigates the existence of a non-linear relationship between TMT size and campaign success. Our analysis draws from entrepreneurship literature which highlights the benefits of larger TMTs in new ventures (Li et al., 2020). While in established firms larger TMT raises agency problems, in startups TMTs typically exhibit a higher level of cohesion, and a lower level of conflict (Roelandt et al., 2022). In ECF campaigns, larger teams may signal more personal external ties (Tretiakov et al., 2019), larger networks and social support (Nielsen, 2020), which may be good predictors of future firm performance. As it is documented (e.g. Estrin et al., 2022), ECF may present network effects, so that as the size of the entrepreneurs in the team (and their networks of potential investors) increases, the flow of information is amplified, and the campaign is positively affected. Hence, our prediction is that each additional member in the team amplifies the information flows and, ultimately, affects the success of the campaign. This suggests an exponential relationship between TMT size and campaign success.

Education

TMT educational background signals the quality of human capital (Ahlers et al., 2015; Kleinert et al., 2020; Piva and Rossi-Lamastra, 2018). College degrees provide specific knowledge, but also signal the capacity to commit to a purpose, the acquisition of soft skills and, especially in the case of business degrees, decisions making and leadership capacities. Ahlers et al. (2015) find that the share of board members with an MBA degree is positively correlated to campaign success, while Kleinert et al. (2020) find that the presence of founders with an MBA or a PhD is positively correlated to the success. Other studies found that only business education and education in the fields related to the startup business are significantly associated with success, while other types of education are weaker signals (Piva and Rossi-Lamastra, 2018).

The diversity of TMT educational background can also have an additional effect on campaign success. Heterogeneity may make decisions more effective by embracing different perspectives to problems. Furthermore, a diverse knowledge base may produce higher innovation and better decisions (Bantel and Jackson, 1989). However, Piva and Rossi-Lamastra (2018) fail to find a significant effect of heterogeneity in the education of founders. Therefore, the importance of educational heterogeneity is far from being well-established in empirical studies and deserves further attention.

Experience

Investors look at the work experience of startup founders (Kaplan and Strömberg, 2004), either as entrepreneurs who have developed specific knowledge and relationships, or as employees in the same industry of the startup. Earlier studies on ECF show that entrepreneurs’ work experience increases the campaign success (Kleinert et al., 2020; Piva and Rossi-Lamastra, 2018). However, other studies suggest that serial entrepreneurs positively affect campaign success only in some model specifications (Kleinert et al., 2020), while other works find that neither industry-specific or other work experience nor the heterogeneity of previous work experience of the founding team have any significant effect on campaign success (Piva and Rossi-Lamastra, 2018).

The age of the TMT is another dimension of experience. Older members are more likely to have more working experience. Investors may prefer a company where the TMT has some experience as they are supposed to better manage and deal with critical situations. Furthermore, older founding teams could have built a network of contacts useful for fundraising purposes, although they could also have a conservative approach to business or be less open to new market opportunities. Generally, young managers are supposed to be inclined to make riskier business decisions. Ralcheva and Roosenboom (2020) find that the average age of directors is negatively correlated to campaign success, which suggests that investors positively evaluate young (and presumably) less experienced but more innovative entrepreneurs. These nuanced findings on the relationship between TMT experience and campaign success call for further empirical analysis.

Data and methodology

Data

This study is based on a novel dataset on equity based crowdfunding campaigns launched in four Italian platforms (Crowdfundme, Mamacrowd, BacktoWork24 and 200Crowd) over the period 2016–2019.

When using the online crowdfunding platforms, companies provide several information on the company's balance sheet, business project, TMT members and the amount of money set as a target. The investors are required to register on the platform's website to access this information. These platforms are based on the “all-or-nothing” model; hence, if the campaign does not reach the target, the invested amount will be reimbursed to the investors.

The initial dataset contains information on 98 companies that have successfully completed their fundraising campaign. The data on project characteristics is provided by the four platforms. Information related to the characteristics of the TMT (founders and other top management team members) was collected through company websites, the documents uploaded in the platform, and through LinkedIn profiles. Some platforms, namely 200Crowd or Mamacrowd, provided a link to LinkedIn profiles for TMT members. When not available in the documents (e.g. CVs or company statute), we estimated the year of birth from the year of university enrolment. Because of missing information for some key variables, the final sample consists of 89 campaigns.

Dependent variables

We used three indicators of a campaign success (Ahlers et al., 2015; Kleinert et al., 2020; Lukkarinen et al., 2016; Piva and Rossi-Lamastra, 2018). The first dependent variable is funding amount, i.e., the total amount of money received by the campaign. The second dependent variable was target capital %, which indicates the total amount of funds received as a percentage of the initial target. We used the logarithmic transformation of these two variables because their distributions are highly skewed. We also considered the number of investors, which indicates the size of the audience reached by the campaign.

Human capital: Team size

The number of TMT members (nTMT) was extracted from the platforms. TMT size has been found to be positively correlated to campaign success in earlier studies (Ahlers et al., 2015; Vismara, 2016), except in a recent study (Piva and Rossi-Lamastra, 2018). A larger team may signal an abundance of human capital, and it indicates a specialization of tasks so that each TMT member does not need to perform different roles at the same time (Ahlers et al., 2015).

Human capital: Education

We collected data on the level of education including high school, bachelor, master's degree, and PhD. This data was obtained through the LinkedIn profile of the various members of the TMT or from the description of the team on the platform webpage. More rarely we had access to CVs. However, it was not possible to obtain the educational level of all team members. For 57% of the sample, we had at least one member of the TMT with missing information on education.

As indicators of education, we used the percentage of TMT members with a PhD (PhD %). A high level of university education signals the capacity to commit to a purpose, and the acquisition of hard and soft skills. Ahlers et al. (2015) find that the share of the board members with an MBA is positively correlated with campaign success, while Kleinert et al. (2020) find that the share of members with an MBA or a PhD is positively correlated with campaign success.

We use the share of team members who have earned a degree in economics or management (businessedu), which should positively affect the campaign success as it signals a greater TMT ability to identify opportunities and organize the firm to meet their goals. This is in line with previous studies (e.g. Piva and Rossi-Lamastra, 2018) which have found that the number of years in business education is positively correlated with the campaign success.

Heterogeneity in TMT may bring several benefits to the firm, and investors might positively evaluate several dimensions of diversity. However, the empirical literature on ECF has not found a significant positive association with the campaign success (Piva and Rossi-Lamastra, 2018). To test this relationship, we use a measure of education heterogeneity (edudifferent) that is the percentage of TMT members with different education backgrounds. We compute the ratio between the number of different TMT educational fields and the total number of members. The closer this variable is to 1, the more heterogeneous is the education background of the TMT. The closer the TMT members’ education backgrounds are, the closer the variable gets to zero.

Human capital: Work experience

Another dimension of the quality of human capital is experience. Data on experience were taken from the CV or LinkedIn profile of the TMT. Nevertheless, in some cases these sources were not sufficient to fill the missing information. For our estimates, we use a dummy that is equal to 1 when at least half of TMT members have more than ten years of experience (d_team_exp).

We also exploit the age of TMT member as a proxy for experience. We use a dummy equal to 1 if at least half of TMT members is less than 30-years-old (d_team_young).

Additional controls

Drawing upon previous studies, we include several controls. Premoney (taken in logs) is the valuation of the company carried out by the crowdfunding platform in collaboration with the founders. Target (taken in logs) is the minimum funding amount that a given campaign must reach in order to have access to the received funds, as set by the company (Vismara, 2016; Vulkan et al., 2016) according to the ‘all-or-nothing’ model. Minimum investment (taken in log) indicates the minimum amount of money that an investor must provide to participate in the campaign, as set by the company and the platform.

We create a dummy variable that accounts for the legal form of the companies that can have access to crowdfunding according to the Italian law. The binary variable d_innostartup takes value 1 when a company is an innovative startup, and 0 when it is an innovative SME. Differently than startup, innovative SMEs can be older than 5 years, have more than 5 million euro of revenues, can distribute profits, have externally validated balance sheets and could have been spawned by an established corporation. Clearly, innovative SMEs may constitue a less risky investment compared with innovative startups, because of a higher probability of survival.

We also control for the presence of partners (d_npartner) as provided by the company. Entrepreneurs can signal some characteristics of their firms such as affiliation with third parties (Kleinert et al., 2020), including venture capitalists, industry associations and local government (Troise et al., 2020).

We also control for the role of professional and non-professional investors (Kim and Viswanathan, 2019). The variable diff_investors % accounts for the differences between funds of professional investors and funds of non-professional investors in each campaign. Platforms provide information that allows to distinguish between the two types of investors. To generate this variable, we calculated the difference between the average investment of professionals and the average investment of non-professional investors; then, we divided this difference by the average total investment. Higher values of diff_investors % indicate a relatively higher weight of professional investors. We also used the ratio between professional investors’ funds and total funding (professional investment %).

Finally, we entered fixed effects for the platforms, which differ in size and notoriety. We control for the startup's business sector (using the national industrial classification ATECO), obtained through web search; we use the dummy high for firms operating in high-tech sectors (either manufacturing or knowledge-intensive services) 1 .

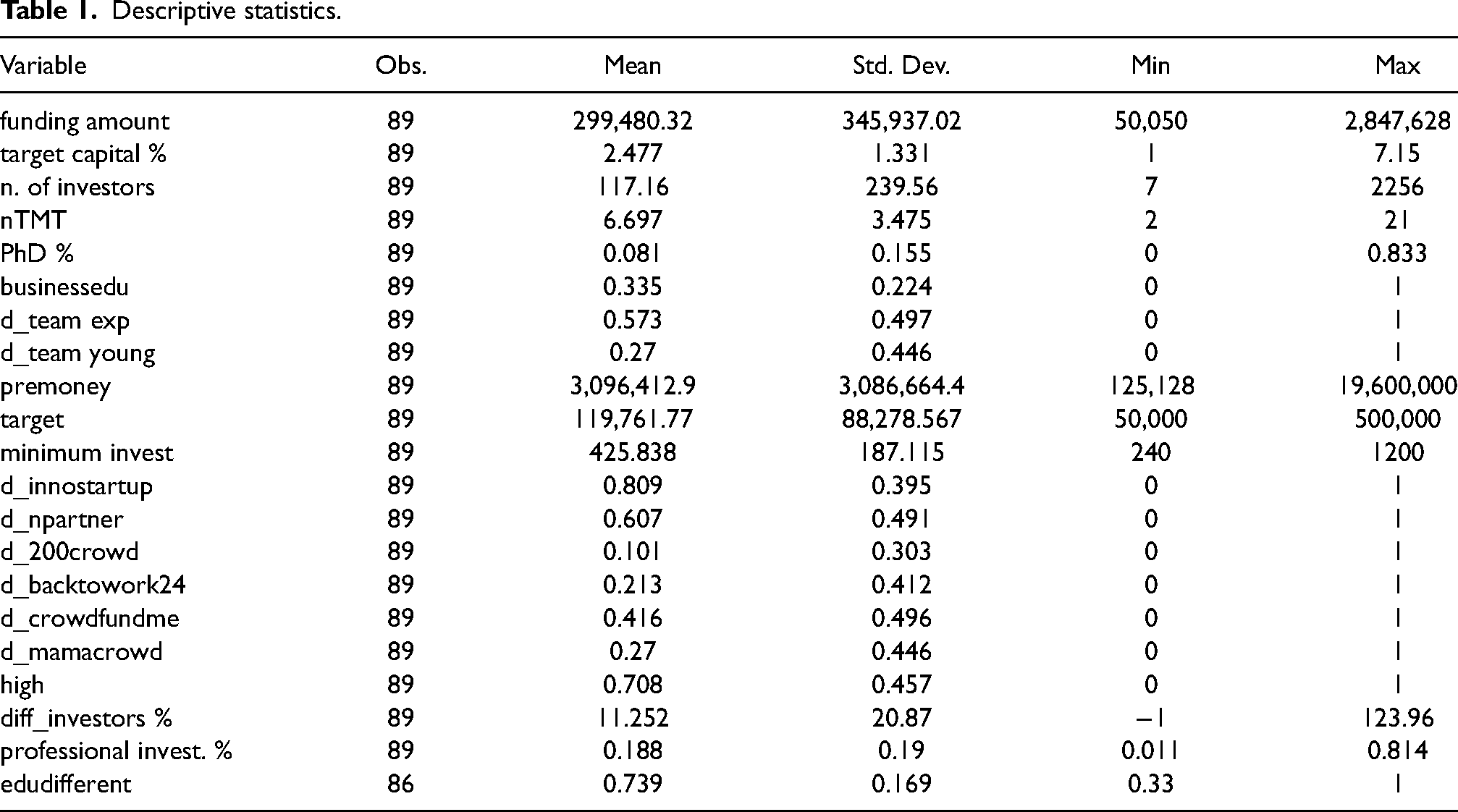

Descriptive statistics are reported in Table 1.

Descriptive statistics.

Analysis

Descriptive analysis

Crowdfundme had the highest share (41%) of campaigns in our sample, followed by Mamacrowd and Backtowork24 which accounted for roughly one-fifth each, while 200crowd accounted for the smallest share (10%).

Most companies participating in crowdfunding campaigns were innovative startups (80.9%). Innovative startups raised an average capital of € 278,473, while innovative SMEs had a larger average funding of € 388,451. Hence, since innovative SMEs presented lower risks (they are older, distribute profits and have external auditors), they were more appealing than innovative startups.

Because of their young age and missing data, revenues or number of employees were not an informative measure of firm size. We can have an idea of the firm size by looking at premoney valuation, which appeared to vary significantly across firms. Average valuation was roughly three million euros. Half of the sample was evaluated more than 2 million euro. The maximum valuation was obtained by Lovby, an innovative SME, with 19.6 million euro.

Companies were concentrated in few industrial sectors. Drawing on 2-digits ATECO classification (25 sectors), 78.6% of the firms belonged to the service sectors, mostly software (J62, accounting for 32.5% of the sample) and IT services (J63, which accounted for 14.6% of the sample). Computer and electronic components (C26) were the manufacturing sector with the highest presence in the sample (7.8% of firms). 63 firms (70.8% of sample) were classified in high-tech sectors, of which 14 were manufacturers and 49 were knowledge-intensive services.

Campaign success

The average number of funds received was 299 thousand euros and vary from a minimum of 50 thousand euros (EXEPT) to a maximum of 2.8 million euros (StartupItalia). The average number of investors per campaign was 114.5. The company that had the fewest investors was Tiassisto24 (7), while the company that enjoyed the largest number of contributors was StartupItalia with more than two thousand investors. Finally, the sample companies received on average as much money as 2.5 times the target. There were 3 companies that just matched the target and about half of the sample at least doubled the objective.

Human capital

On average, teams were made of 6.6 people and no firm had less than two persons in TMT. Generally, TMT members had higher education. On average, 8% of the team members had a PhD (PhD %). In terms of the percentage of TMT with a master's degree or a PhD, the average was 76.4% across firms, and 32.5% of companies had all TMT members with a university degree (not shown in Table 1). Most companies had a team made up of members with different educational background. The mean value of diversity of fields (edudifferent) was 73.8%, while on average one-third of TMT members had a degree in business or economics (businessedu).

In terms of experience, the majority of companies had relatively inexperienced members. More than eighty percent of the firms had at least a member with less than 10 years of work experience, while only twenty percent had at least a member with more than 30 years of experience. When looking at age, sixty percent of firms had at least a young member (less than 30-year-old), while 36% had at least a member older than 51 years.

Econometric analysis and discussion of results

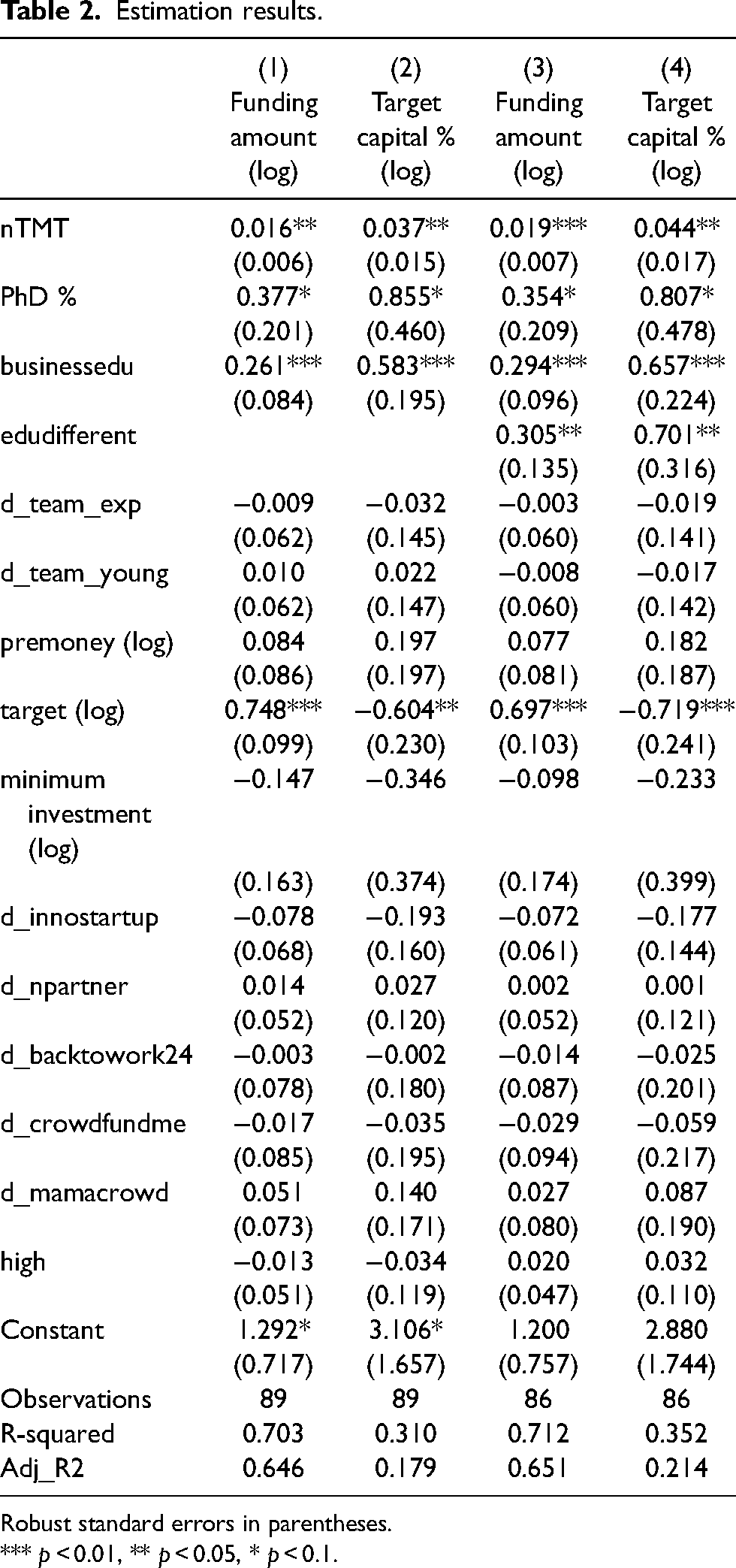

Firstly, we checked the pair correlation for multicollinearity for the variables used in the estimations. The correlation between target (log) and funding amount (log) was the only one of a certain concern (0.75) 2 .

To investigate the relationship between campaign success and explanatory variables, we firstly ran four models where funding amount (log) and target capital % (log) were estimated as a function of human capital (size of the team, education, and experience). The results are illustrated in Table 2. As for the size of the team (nTMT), the estimates showed a positive and significant relationship. Hence, human capital expressed in terms of the number of team members was a good signal of the potentials of the startup, in line with the empirical literature on ECF at the project level (Ahlers et al., 2015; Vismara, 2016).

Estimation results.

Robust standard errors in parentheses.

*** p < 0.01, ** p < 0.05, * p < 0.1.

The second dimension of human capital we accounted for is education. Higher education of TMT members was supposed to attract more investors and funds. The share of TMT with a PhD (PhD %) was positively correlated with the total funding and the funds-to-target ratio, albeit at a low significant level (p < 0.10). This was partially in line with Kleinert et al. (2020) who found that a founder with an MBA or a PhD is positively correlated with campaign success. Since we did not have information on MBAs, we only accounted for the PhD 3 .

We also accounted for the share of members with a management or economic degree (businessedu) which were supposed to signal a greater ability of the TMT to identify business opportunities and organize the firm to meet their goals. In line with earlier work (Piva and Rossi-Lamastra, 2018), businessedu was positive and significant, hence there was a positive correlation with the total amount of money raised and the share of funds over the target. These findings confirmed that education (PhD % and businessedu) played an important role for the campaign success in terms of total funding and the funds-to-target ratio.

The third dimension of human capital we explored is experience measured with two dummies, working experience (d_team_exp) and age (d_team_young). None of these variables were significant. Although earlier works on ECF show that the presence of experienced entrepreneurs increases the probability of the campaign success (Kleinert et al., 2020; Piva and Rossi-Lamastra, 2018), as discussed before, the empirical evidence has not reached clearcut conclusions. Earlier studies find that what matters is entrepreneurial experience, while work experience in the same industry of the startup or in any other industry does not have a significant effect on the campaign success (Piva and Rossi-Lamastra, 2018). Our study confirmed that TMT work experience was not relevant for the campaign success.

Target (log) entered significantly in both funding amount (log) and target capital % (log) equations, although with opposite signs. A higher target was more likely to yield a larger amount of funds collected. This was due to the fact that our sample included only projects which met the target; hence, total funding was proportional to the target that was set. The negative correlation with target capital % was driven by the fact that a higher target will limit the likelihood of overfunding (i.e. the amount of capital raised over the target) 4 .

Other controls – premoney (log), minimum investment, the presence of partners, the dummy for innovative startup, and the dummy for high-tech sectors – did not have statistically significant correlation with the campaign success.

In Table 2 (models 3–4) we explored another dimension of education, i.e. heterogeneity. The variable edudifferent was positive and significant for both indicators of campaign success. This result differed from Piva and Rossi-Lamastra (2018), where heterogeneous education of team members was not significant. The inclusion of this variable did not alter the main results reported in models 1–2.

We ran additional specifications by including the role of professional investors. We used the variable diff_investors % and professional investment %. The inclusion of these variables did not alter the main results, and they were not statistically significant 5 .

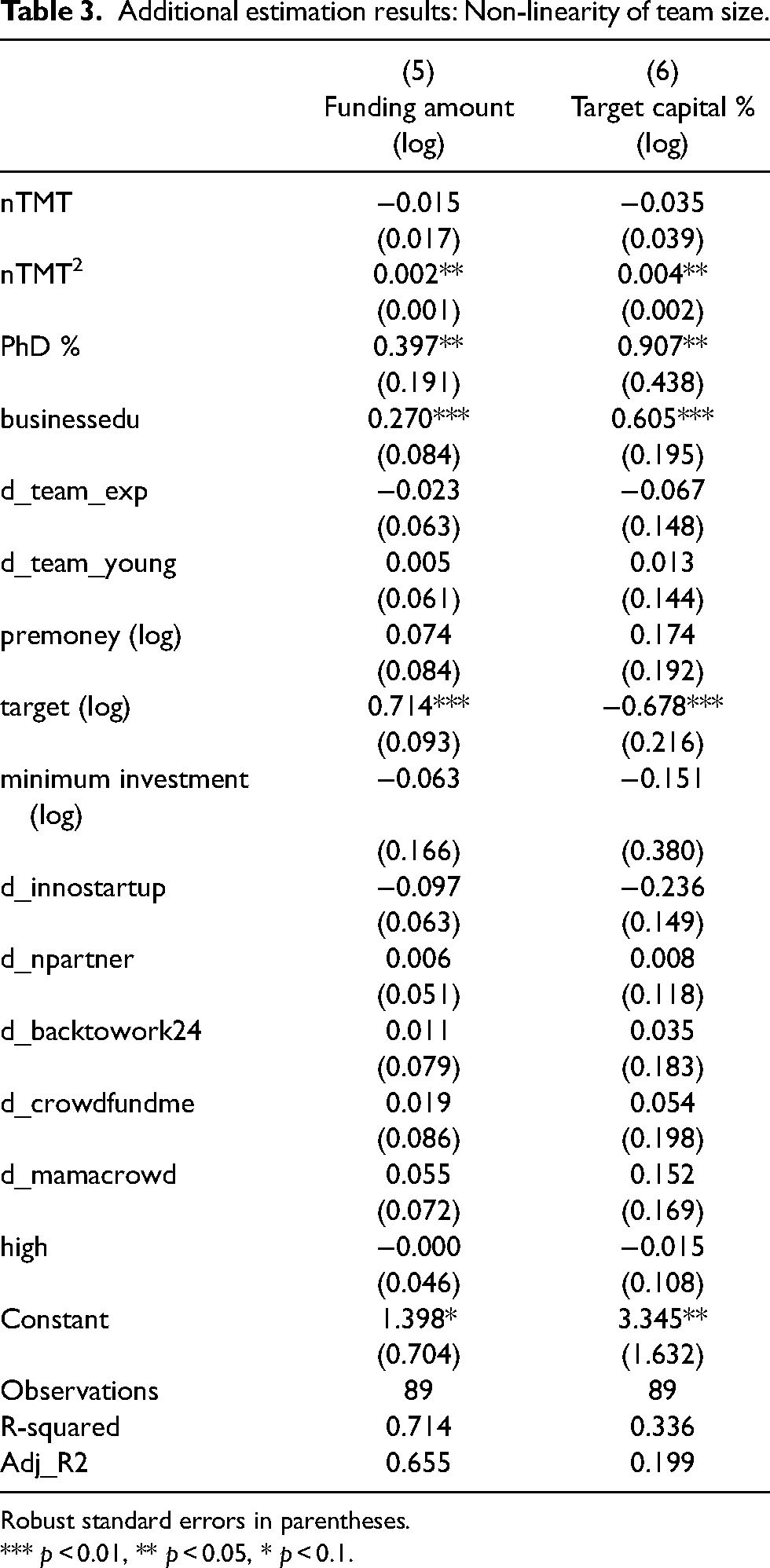

We also explored the possibility of a non-linear relationship between team size and campaign success, as shown in Table 3. The squared term (nTMT2) was positive and significant, while nTMT lost its significance. Following a three-step procedure to test for a quadratic relationship (Haans et al., 2016; Lind and Mehlum, 2010), we found that both funding amount (log) and target capital % (log) increased more than proportionally with team size.

Additional estimation results: Non-linearity of team size.

Robust standard errors in parentheses.

*** p < 0.01, ** p < 0.05, * p < 0.1.

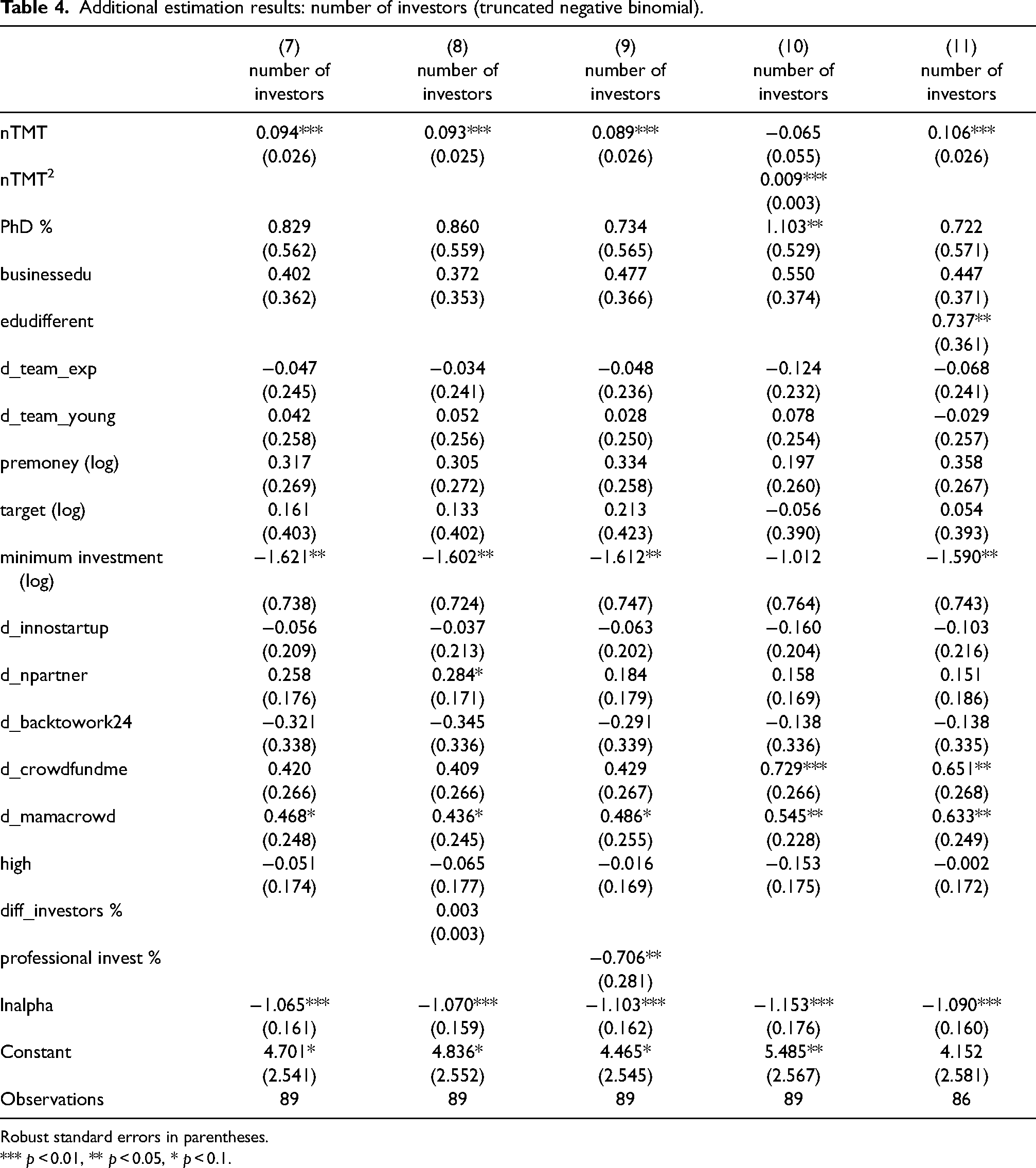

To conclude our analysis of crowdfunding performance, we considered the number of investors as a measure of the campaign success.

The results reported in Table 4 indicate that TMT size was positively and significantly correlated with the number of investors, which probably reflected the effect of the perceived quality and the importance of social links that clearly increased with the number of TMT. The positive sign on the squared term (nTMT2) confirmed that the TMT size effect increased more than proportionally with the TMT size.

Additional estimation results: number of investors (truncated negative binomial).

Robust standard errors in parentheses.

*** p < 0.01, ** p < 0.05, * p < 0.1.

In addition, two platforms (Crowdfundme and Mammacrowd) were positively correlated to campaign success, with 200crowd platform as the baseline. These effects reflected differences across platforms in the number of visitors and network effects, marketing, and social networking strategies.

The share of professional investors (professional investment %) had a negative correlation with the dependent variable (number of investors). The presence of professional investors induced a reduced participation of non-professional investors, which in turn implied a reduction in the amount of investment by non-professional investors. Instead, the difference between professionals and non-professionals (diff_investors %) funds was not significant.

Finally, as far as education is concerned, the variety of educational background was confirmed as a good signal to attract a larger number of investors (model 11); at the same time, the measures of the quality of high education (PhD % and businessedu) failed to be important factors to attract investors across all models, except for PhD % in model 10.

Conclusion

In line with previous studies, we find that the team size is positively correlated with the success of crowdfunding campaigns. In addition to previous works, our findings show a non-linear relationship between TMT size and three measures of performance. This novel contribution points to increasing returns to TMT scale: after a certain threshold, the productivity gains of a larger set of capabilities and network ties increase more than proportionally with the number of additional team members. Moreover, we find that the share of TMT members with a PhD increases the campaign success measured by total funding and the ratio of total funding to the target capital. This novel result is consistent with the large share of sample companies operating in high tech sectors, where scientific and technical capabilities are important determinants of innovation and business performance.

Our findings corroborate earlier works (e.g. Piva and Rossi-Lamastra, 2018) by showing that companies with higher shares of TMT members with an economics or management degree obtain more funding and a larger ratio of total funding to the target capital. We also test whether heterogeneity of educational background may be positively related to the success. Unlike previous studies (e.g. Piva and Rossi-Lamastra, 2018), we find that the diversity of educational background positively correlates with all indicators of success. Finally, we do not find evidence of any significant correlation with experience (measured by work experience and age). In line with previous studies on ECF (e.g. Kleinert et al., 2020; Piva and Rossi-Lamastra, 2018; Ralcheva and Roosenboom, 2020), our analysis suggests that the difficulties in capturing the experience dimension of human capital require new measures.

This paper contributes to the literature on the role of human capital in ECF by suggesting that different dimensions of human capital prove to be an effective signal and facilitator of information flows that reduce information asymmetry between investors and entrepreneurs (Estrin et al., 2022; Mochkabadi and Volkmann, 2020; Piva and Rossi-Lamastra, 2018; Troise et al., 2020). Our findings provide further evidence that investors will evaluate those characteristics as a good proxy for a new venture's future performance (Colombo and Grilli, 2005; Hambrick, 2007). We also contribute to the literature on the role of networks in EFC as facilitator of information flows; as the curvilinear effect of team size suggests, larger teams bring about a broader network of social ties, which probably favors the access to a larger set of potential investors (Estrin et al., 2022; Troise et al., 2020).

The managerial implications of our study are straightforward. Entrepreneurs who wish to achieve a successful crowdfunding campaign should invest in the following dimensions to signal the quality of their venture to crowdfunding investors: larger teams, a higher share of members with business education and higher share of PhDs, especially for startups active in high-tech industries, and a diversified educational background.

However, our results must be taken with caution, since our paper is not without limitations and should be interpreted as a preliminary exploration of a novel dataset. The first limitation is the small sample size and a relatively short time horizon. Secondly, our dataset does not allow for identification of causal relationships. However, we believe that the correlations discussed in the paper provide various useful suggestions for future research. Third, we do not consider firms that do not achieve the target. This problem could be important especially for firms excluded from our sample that get close to the target and that may have characteristics very similar to sample firms that barely match the target.

Our study points to several directions for future research. First, other dimensions of heterogeneity such as gender and ethnicity should be considered, especially as females and second-generation entrepreneurs increase (Kleinert and Mochkabadi, 2021). Second, further attention should be devoted to the interplay between specific fields and levels of education of TMT, for example in terms of whether PhD is more effective in STEM fields or other fields like general management and economics. Digging deeper into different combinations of educational fields could be useful to identify synergies or skill combination patterns and their implications for crowdfunding success in different industries. Third, it could be useful to understand whether the non-linear effect of TMT size varies with different dimensions of TMT heterogeneity (e.g. education, experience, age, and gender); for example, network effects may be more likely to emerge for older or more experienced members or TMT with a more diversified educational background that can draw from a variety of social networks. Fourth, future research could consider more thoroughly the role of partners or professional investors in affecting the decision of non-professional investors.