Abstract

This study explores the signaling value of equity crowdfunding compared to grants and business accelerators in attracting late-stage venture capital (VC) funding for start-ups. Using signaling theory and a probit regression model with propensity score matching, this study analyzes how equity crowdfunding functions as a signaling mechanism for start-ups. The study's findings reveal that although equity crowdfunding provides an initial signal of quality, start-ups relying on this mechanism are less likely to secure subsequent VC funding than those supported by grants or business accelerators. Notably, including human capital in equity crowdfunding ventures narrows the funding gap between crowdfunding and grants concerning VC funding probability, though the effect remains less pronounced than in business accelerator programs. This study enhances the understanding of crowdfunding's signaling efficacy and offers practical insights for researchers and entrepreneurs navigating the evolving landscape of start-up financing.

Introduction

Start-ups often seek funding from established sources such as venture capital (VC), banks, and business angels. Recently, however, crowdfunding has emerged as a viable alternative, providing financial support to numerous start-ups during their early stages and enabling their survival and growth. Over the past decade, the crowdfunding industry has expanded significantly (Babich et al., 2021). This rapid growth has fueled scholarly interest, leading to an expanding body of literature that examines crowdfunding's impact. A significant portion of this research focuses on identifying the factors that contribute to successful crowdfunding campaigns.

Researchers have explored the roles of entrepreneurial characteristics, project attributes, and campaign dynamics in determining crowdfunding success (e.g. Ahlers et al., 2015; Lukkarinen et al., 2016; Ralcheva and Roosenboom, 2016). Additionally, recent studies have highlighted the relationship between crowdfunding and traditional funding sources. Scholars argue that crowdfunding serves as a signaling mechanism, enabling start-ups to showcase their latent quality and attract further financial backing from traditional investors (e.g. Butticè et al., 2020; Drover et al., 2017; Roma et al., 2017, 2021; Shafi and Colombo, 2020).

Building on these foundations, this study explores the signaling effect of equity crowdfunding in securing late-stage investments by comparing it with grants and business accelerators. While previous research has primarily focused on reward-based crowdfunding, equity crowdfunding has remained relatively unexplored. To address this gap, the following research question is posed: to what extent does equity crowdfunding serve as a third-party signal to start-ups seeking future funding from VCs compared to grants and business accelerators? To answer this question, signaling theory was applied, which addresses information asymmetries in markets (Spence, 1973).

Most start-ups that secure seed funding, whether through crowdfunding, angel investors, or other initial sources, generally aim to grow, which often necessitates larger-scale financing (Drover et al., 2017). This study, therefore, assumes that as ventures mature, many will seek late-stage funding from VCs, who typically specialize in financing at this scale (Drover et al., 2017; Roma et al., 2021). This assumption frames VC funding as a common goal for start-ups progressing beyond their initial seed stage.

VCs evaluate a wide range of factors beyond market potential when deciding which start-ups to fund. They seek signals of quality that go beyond market information benefits (Drover et al., 2017). To make informed decisions, VCs assess start-ups comprehensively, considering human, social, and intellectual capital. In contrast to equity crowdfunding, grants exhibit a high signaling value because awarding grants to low-quality start-ups can damage the reputation of grant agencies. Moreover, acquiring grants is highly competitive and rigorously merit-based (Hsu, 2006).

Similarly, business accelerator programs carry significant signaling value. They not only provide vital financial support during a start-up's formative stages but also offer resources for their professional development (Avnimelech et al., 2021). Considering these distinctions, it is hypothesized that start-ups obtaining equity crowdfunding may have a lower probability of securing subsequent VC funding compared to those supported by grants or business accelerators.

Despite this, equity crowdfunding presents unique advantages. First, it offers insights into a venture's market potential by reflecting investor preferences directly. Second, it allows entrepreneurs to align their projects with investor preferences by incorporating the latter's ideas into the initial development phase, potentially boosting the project's success (Drover et al., 2017; Roma et al., 2021). Furthermore, prior research (e.g. Ahlers et al., 2015; Kleinert et al., 2020; Roma et al., 2017) has demonstrated that start-up attributes, such as human capital, positively influence crowdfunding success.

Following this line of inquiry, proxies such as MBA and PhD qualifications, and the size of the entrepreneurial team were used to measure human capital, assuming that these factors reflect the quality of a start-up. Given these benefits, it is hypothesized that start-ups leveraging equity crowdfunding will send positive signals to potential investors, increasing their certification levels for future funding opportunities. To test these hypotheses, a probit regression model combined with a propensity score matching (PSM) approach was applied to account for selection effects.

This study makes several significant contributions. It addresses the calls made by McKenny et al. (2017) and Drover et al. (2017) for a deeper evaluation of emerging funding sources and their impact on traditional financing mechanisms. While recent research has extensively explored initial funding sources and their interrelationships, novel forms of start-up financing have received limited attention. Most existing studies focus on comparisons between traditional funding alternatives (Dutta and Folta, 2016).

Although prior research indicates that crowdfunding generally serves as a signaling mechanism (Drover et al., 2017; Roma et al., 2017, 2021; Shafi and Colombo, 2020), the specific ways in which equity crowdfunding functions as an effective signal remain unexplored. This paper takes an essential first step toward a more detailed examination of this phenomenon. Additionally, it investigates whether human capital variables, such as entrepreneurs with advanced degrees and team sizes, enhance the signaling effect of equity crowdfunding compared to grants and business accelerators, particularly in securing late-stage VC funding.

Theoretical background and hypotheses development

Signaling and certification in start-up financing

Investment in start-ups carries significant risk due to uncertain future outcomes and high default rates (Kleinert et al., 2020). Start-ups typically have more information about their prospects than potential investors, hindering investors’ ability to make informed decisions. This asymmetric information can prevent investors from identifying promising opportunities, leading to market failure (Akerlof, 1970). Signaling theory suggests that markets can function effectively despite such information asymmetries (Spence, 1973). The theory posits that an informed party can send an observable signal to a less-informed party, which must be both visible to the recipient and entail a cost to the sender (Shane and Cable, 2002). In entrepreneurial finance, researchers have applied signaling theory to explore how start-ups overcome information asymmetries when seeking funding (Ahlers et al., 2015; Fitza and Dean, 2016; Kleinert et al., 2020; Piva and Rossi-Lamastra, 2018).

The concept of signaling has also evolved to include third-party signaling, where an external entity provides a signal about a start-up's quality to potential investors, including late-stage VCs. For third-party signaling to be effective, the signaling entity must exhibit certain characteristics that allow investors to make credible inferences about the start-up's potential (Ralcheva and Roosenboom, 2016). Recent research on crowdfunding underscores the role of third-party certification in increasing the likelihood of securing early-stage financing. Start-ups certified by reputable crowdfunding platforms or endorsed by well-known investors are more likely to attract VC funding (Drover et al., 2017; Roma et al., 2021).

Hypotheses development

VCs view a start-up's initial financial backing as a strong signal of its potential for future growth (Drover et al., 2017). This study assumes that with maturity, start-ups will seek larger, late-stage funding from VCs, who typically specialize in late-stage financing growth (Drover et al., 2017; Roma et al., 2021). While this path is assumed for all start-ups, equity-crowdfunded ventures may have a unique trajectory, given their distinct ownership structures and investor expectations (Ahlers et al., 2015). However, it is posited that as these equity-crowdfunded start-ups grow, they, too, will likely turn to VCs to meet scaling needs (Butticè et al., 2020). Similarly, Roma et al. (2021) suggest that reward-based crowdfunding functions as a third-party signal to VCs, improving the likelihood of securing late-stage funding. Drawing from this premise, the analysis is extended to equity crowdfunding, and hypotheses are proposed to compare its signaling effect with those of grants and business accelerators.

Signaling of equity crowdfunding versus grants

Equity crowdfunding offers entrepreneurs an alternative to traditional investors by enabling them to raise capital in exchange for equity shares in their ventures (Ahlers et al., 2015). This financing mechanism reduces information asymmetries for late-stage VCs through the principles of signaling theory, specifically costliness and observability. Investors bear the risk of financial loss if they back low-quality start-ups, and the open-call nature of crowdfunding ensures high observability. Additionally, crowdfunding platforms often screen for quality, rejecting subpar ventures to protect their reputation (Lukkarinen et al., 2016). This makes late-stage VCs more aware of a start-up's potential and quality, helping them make informed decisions about future investments.

Previous research underscores the applicability of signaling theory in crowdfunding and its influence on campaign success. Signals such as entrepreneurs’ equity retention (Ahlers et al., 2015; Rossi et al., 2021), founder characteristics (Piva and Rossi-Lamastra, 2018), early investor participation (Kleinert et al., 2020), and campaign features (Wasti and Ahmed, 2023) are crucial in attracting investor interest. Drover et al. (2017) and Butticè et al. (2020) further argue that crowdfunding legitimizes start-ups, facilitating late-stage VC funding.

Grants, in contrast, are financial awards provided without expectations of financial returns or ownership stakes. Typically issued by governments, foundations, or other institutions, grants aim to foster innovation and entrepreneurship. They address information asymmetries for uninformed parties, making start-ups more appealing to late-stage VCs. Signaling theory's principle of observability applies to grants since VCs recognize that start-ups have undergone a rigorous evaluation process. Costliness, another tenet of signaling theory, also applies because grant agencies face reputational and financial risks when supporting low-quality ventures. This endorsement sends a positive signal to future VCs. Furthermore, competing for grants is both time- and resource-intensive, which deters low-quality start-ups from applying (Islam et al., 2018).

Previous research further highlights the strong signaling value of grants for start-ups. Howell (2015) demonstrates that grants reduce uncertainties for start-ups, thereby increasing their likelihood of securing VC funding. Similarly, Islam et al. (2018) find that start-ups receiving grants are 12% more likely to attract VC investment. Kleer (2010) further argues that grants serve as a signal for start-ups to secure private funding, enhancing their appeal to VCs.

When it comes to comparing the strength of the signal provided by equity crowdfunding and grants, it can be argued that the former offers a weaker signaling effect because small investment amounts in equity crowdfunding lead to limited due diligence by the investors (Ahlers et al., 2015). Furthermore, the online nature of crowdfunding restricts opportunities for investors to directly evaluate start-ups, as they cannot meet entrepreneurs in person. Entrepreneurs often withhold critical information due to confidentiality concerns, further diminishing the signaling effect (Di Pietro et al., 2018). Crowdfunding investors are typically non-professionals who make decisions based on personal interests, passion, peer influence, or geographic proximity rather than through rigorous evaluation processes (Carbonara, 2021).

In contrast, grants provide a much stronger signal to late-stage VCs due to their highly competitive, merit-based selection process (Hsu, 2006). Grant-awarding agencies rely on internal scientific and technical expertise as well as external reviewers to select the most promising start-ups (Howell, 2015; Islam et al., 2018). This rigorous process ensures that low-quality ventures are excluded (Ralcheva and Roosenboom, 2016).

Based on this comparison of the signaling effects of grants and equity crowdfunding, the following hypothesis is proposed:

Signaling of equity crowdfunding versus business accelerator programs

From a signaling theory perspective, business accelerator programs significantly reduce the uncertainty surrounding nascent start-ups for future funding because business accelerators are highly selective and avoid accepting low-quality start-ups to protect their reputations. Signaling theory's principle of observability is also evident in business accelerators, as these programs provide structured training and support to start-ups over a defined period (Hallen et al., 2020). Participating in an accelerator program increases a start-up's visibility, making it more recognizable to VCs in later funding stages. Stuart et al. (1999) highlight that affiliation with business accelerator programs serves as a certification for external investors, particularly for early-stage start-ups with limited social validation.

Empirical studies reinforce the strong signaling value of business accelerators. Venâncio and Jorge (2022) argue that accelerators reduce information asymmetries by signaling unobservable quality to investors. Similarly, Hallen et al. (2014) find that accelerators enhance start-ups’ learning and network development. Additionally, accelerators also enable start-ups to differentiate themselves in the market and build relationships with key stakeholders, including customers, suppliers, and investors (Avnimelech et al., 2021).

Compared to equity crowdfunding, the signaling effect of business accelerator programs is stronger. Accelerators excel in two key dimensions of signaling theory, costliness and observability, which make them more informative for VCs. Accelerator programs not only provide financial assistance but also facilitate the professional development of start-ups (Avnimelech et al., 2021). Furthermore, accelerators assist start-ups in key operational areas, such as recruitment (Banc and Messeghem, 2020), technical support, financial management, and networking (Cohen et al., 2019).

Based on this analysis, the following hypothesis is proposed:

Equity crowdfunding interaction with human capital of start-ups

Prior research underscores the critical role of human capital in determining start-up success. High levels of human capital, including skills and capabilities, are strongly correlated with entrepreneurial outcomes (Ahlers et al., 2015). Entrepreneurs with robust human capital are better equipped to identify opportunities, secure resources, and foster organizational learning (Shane and Venkataraman, 2000). For investors, particularly VCs, management skills and prior experience are essential assessment factors (Zacharakis and Meyer, 2000). Additionally, educational credentials often serve as early-stage signals demonstrating entrepreneurial competence (Piva and Rossi-Lamastra, 2018).

This study explores whether the signaling effect of equity crowdfunding can be enhanced to rival that of grants and business accelerator programs by focusing specifically on the role of human capital. While crowdfunding facilitates the online communication of project details, it lacks the interpersonal interaction available to investors through grants and accelerator programs. However, equity crowdfunding campaigns still provide opportunities to highlight the human capital attributes of start-ups. It can be argued that human capital acts as a critical supplementary signal in crowdfunding, enhancing its signaling effect. Given that VCs rigorously examine start-ups’ foundational characteristics (Drover et al., 2017), human capital emerges as a key factor. Previous studies have similarly concluded that human capital positively impacts the success of equity crowdfunding campaigns (Ahlers et al., 2015; D’Agostino et al., 2022; Piva and Rossi-Lamastra, 2018).

In contrast, the signaling value of human capital in the context of grants and business accelerator programs may be less pronounced since these funding mechanisms already provide strong, comprehensive signals to investors. However, for equity-crowdfunded start-ups operating within higher uncertainty and information asymmetry, human capital serves as a crucial certification mechanism. This argument aligns with Roma et al.'s (2021) findings in the context of reward-based crowdfunding, which suggests that complementary signals such as human capital increase the likelihood of future VC funding. Although equity crowdfunding differs in structure and purpose from reward-based crowdfunding, both share characteristics such as virtuality, early-stage focus, and pronounced information asymmetry.

Thus, it can be argued that human capital may act as an effective signal for equity-crowdfunded start-ups. Based on this analysis, the following hypotheses are proposed:

Hypothesis 3A: Human capital reduces the funding gap between equity-crowdfunded start-ups and grant-funded start-ups in their likelihood of receiving subsequent funding from VCs.

Hypothesis 3B: Human capital reduces the funding gap between equity-crowdfunded start-ups and business accelerator-associated start-ups in their likelihood of receiving subsequent funding from VCs.

Method

Data

To test the hypotheses, data were collected from three primary sources, equity crowdfunding, grants, and business accelerators—forming two distinct samples. The first sample compared equity-crowdfunded start-ups with grant-funded start-ups (control sample 1). The second sample compared equity-crowdfunded start-ups with start-ups associated with business accelerators (control sample 2). Both comparisons focused on the second round of funding that these start-ups received from VCs.

To gather data on equity-crowdfunded start-ups, a triangulated approach involving three sources, namely Crowdcube, Crunchbase Pro, and LinkedIn, was used. Equity-crowdfunded start-ups were identified through Crowdcube; subsequently, further information, including funding history, entrepreneurial biographies, entrepreneurial team size, and start-up age, was collected from Crunchbase Pro and LinkedIn. Crowdcube, the largest equity crowdfunding platform in the UK, implements a rigorous screening process, rejecting nearly 90% of submissions. Its due diligence encompasses assessments of start-up and director backgrounds, financial performance, legal compliance, and other critical factors. Additionally, it requires campaigns to meet 100% of its funding target before funds are disbursed, ensuring high-quality standards and bolstering investor confidence (Butticè et al., 2020).

For control samples 1 and 2, data were obtained from Crunchbase Pro and LinkedIn. Crunchbase Pro is a comprehensive database that includes detailed information on start-ups, investors, funding history, and founder profiles. It is widely used in venture financing research (e.g. Butticè et al., 2020; Roma et al., 2021). LinkedIn was consulted to fill the gaps in educational data available on Crunchbase Pro.

The study classified small firms as start-ups if they were incorporated after 2000, received initial funding between 2011 and 2020, were located in the UK, and had aspirations for commercialization. Start-ups that are inactive, operate as non-profit organizations, or lack complete information were excluded from the analysis. The first sample included equity-crowdfunded start-ups, with control sample 1 (grants) comprising 1187 (537 equity-crowdfunded and 650 grant-backed) start-ups. The second sample included equity-crowdfunded start-ups, with control sample 2 (business accelerators) comprising 829 (537 equity-crowdfunded and 292 business accelerator-backed) start-ups.

Variables

Dependent variable: The study adopted the definition of the dependent variable from Roma et al. (2021), categorizing VC funding as a dummy variable. This variable was assigned a value of 1 if a start-up secured VC funding by the end of 2022, following initial funding through equity crowdfunding, grants, or business accelerators during the observation period (2011–2020). If not, the variable took the value of 0. This measure assumes that VC funding is a common next step for maturing start-ups seeking further growth.

Independent variables: This study's primary independent variables were dummy variables: equity crowdfunding versus grants (labeled as CF vs. Grants) and equity crowdfunding versus business accelerators (labeled as CF vs. BA). The variable CF vs. Grants took the value of 1 if a start-up received equity crowdfunding and 0 if it obtained funding via grants. Similarly, the variable CF vs. BA was assigned a value of 1 if the start-up received equity crowdfunding and 0 if it secured funding through business accelerators. These variables were used to test Hypotheses 1 and 2.

To test Hypothesis 3A, CF vs. Grants was interacted with human capital variables: MBA, PhD, and Size of the entrepreneurial team. Each human capital proxy was individually interacted with CF vs. Grants. To measure the first interaction term (CF vs. Grants*MBA), a dummy variable, MBA, was used, whose value was 1 if at least one member of the entrepreneurial team held an MBA degree, regardless of the initial funding source; the value was 0 otherwise. For the second interaction term (CF vs. Grants*PhD), PhD was defined as a dummy variable of value 1 if at least one team member held a PhD degree, irrespective of the initial funding source; the value was 0 otherwise. PhDs signify advanced expertise and problem-solving skills, which are particularly valuable for early-stage start-ups. Although rare, they serve as robust proxies for human capital when analyzing the signaling effects on fundraising (Hsu, 2007). To measure the third interaction term (CF vs. Grants*Size), the entrepreneurial team's size was used, defined by the number of team members occupying key positions such as founders, CEO, COO, CFO, or other managerial roles. Previous studies have used MBA, PhD, and Size as valid indicators of human capital (e.g. Ahlers et al., 2015; Kleinert et al., 2020). To test Hypothesis 3B, human capital variables were interacted with CF vs. BA, thus measuring the effect of human capital together with equity crowdfunding on subsequent VC funding.

Control variables: Control variables were employed to account for factors that may influence the likelihood of start-ups receiving subsequent funding from VCs. First, the effect of professional investors (i.e. Angelpre and VCpre) and PastGrant was controlled, which may affect VCs’ decision to fund equity-crowdfunded start-ups (Butticè et al., 2020; Islam et al., 2018). These variables were binary, taking a value of 1 if the start-up received support from professional investors or grants before equity crowdfunding and 0 otherwise. Second, the direct effect of human capital was accounted for by employing the three proxies: MBA, PhD, and Size. Third, London 1 is included as a city-level dummy variable due to its prominence as a financial center with a high concentration of start-up funding activities (Butticè et al., 2020; Wasti and Ahmed, 2023). Fourth, the age of the start-up was controlled for (Age). Fifth, the time lag between the end of the initial funding period (2020) and the VC funding event (up to 2022), denoted as Lag_years, was accounted for. Finally, unobserved fixed effects were controlled for by including Years and Industries.

Results

Descriptive statistics

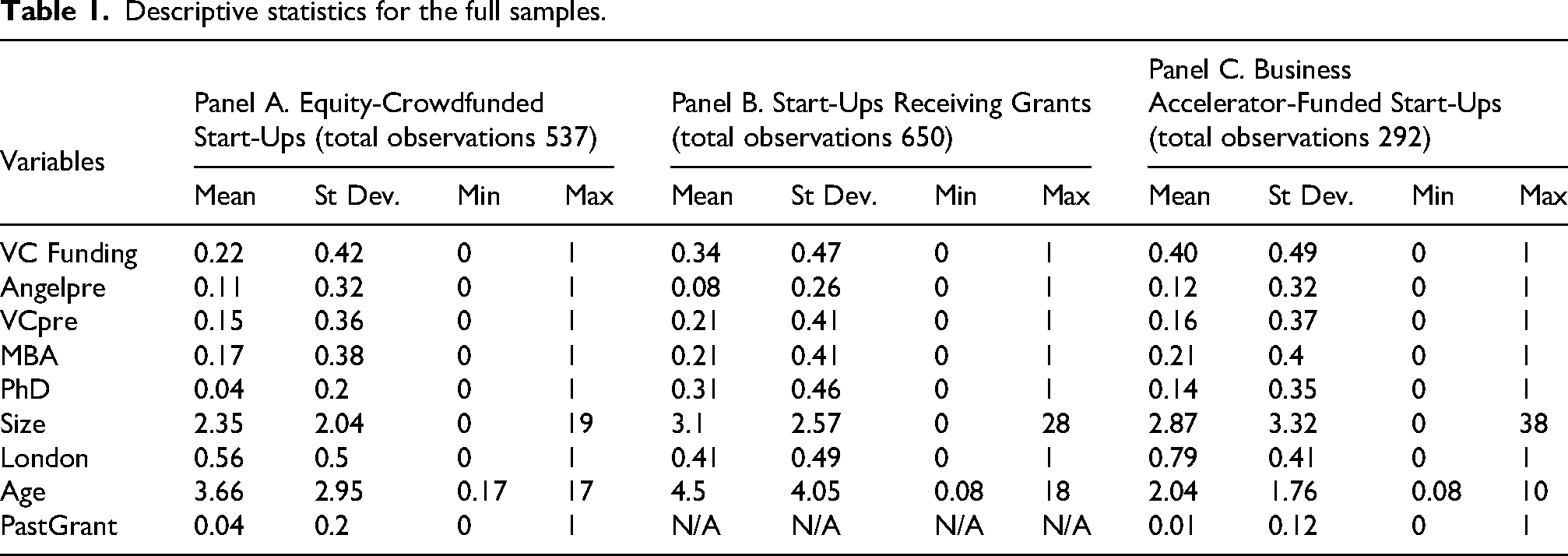

The descriptive statistics in Panels A, B, and C of Table 1 provide preliminary insights into the signaling effects of equity crowdfunding compared to grants and business accelerators. The correlation matrix for the samples indicates no significant correlation among the variables. 2

Descriptive statistics for the full samples.

Matched sample

Descriptive statistics reveal that grant-backed or accelerator-affiliated start-ups generally exhibit higher quality and attract more VC funding than their equity-crowdfunded counterparts. This suggests that late-stage VCs may prefer high-quality start-ups supported by grants or accelerators to relying solely on signaling effects. This study faces selection bias, as start-up funding sources are not randomly chosen; to address this, a matching method used by previous research (Butticè et al., 2020; Roma et al., 2021) was employed.

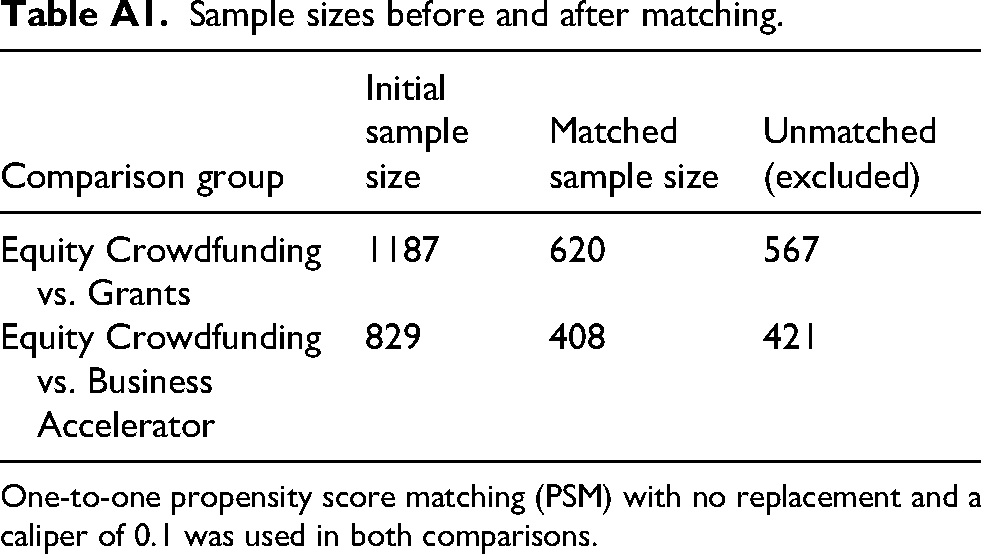

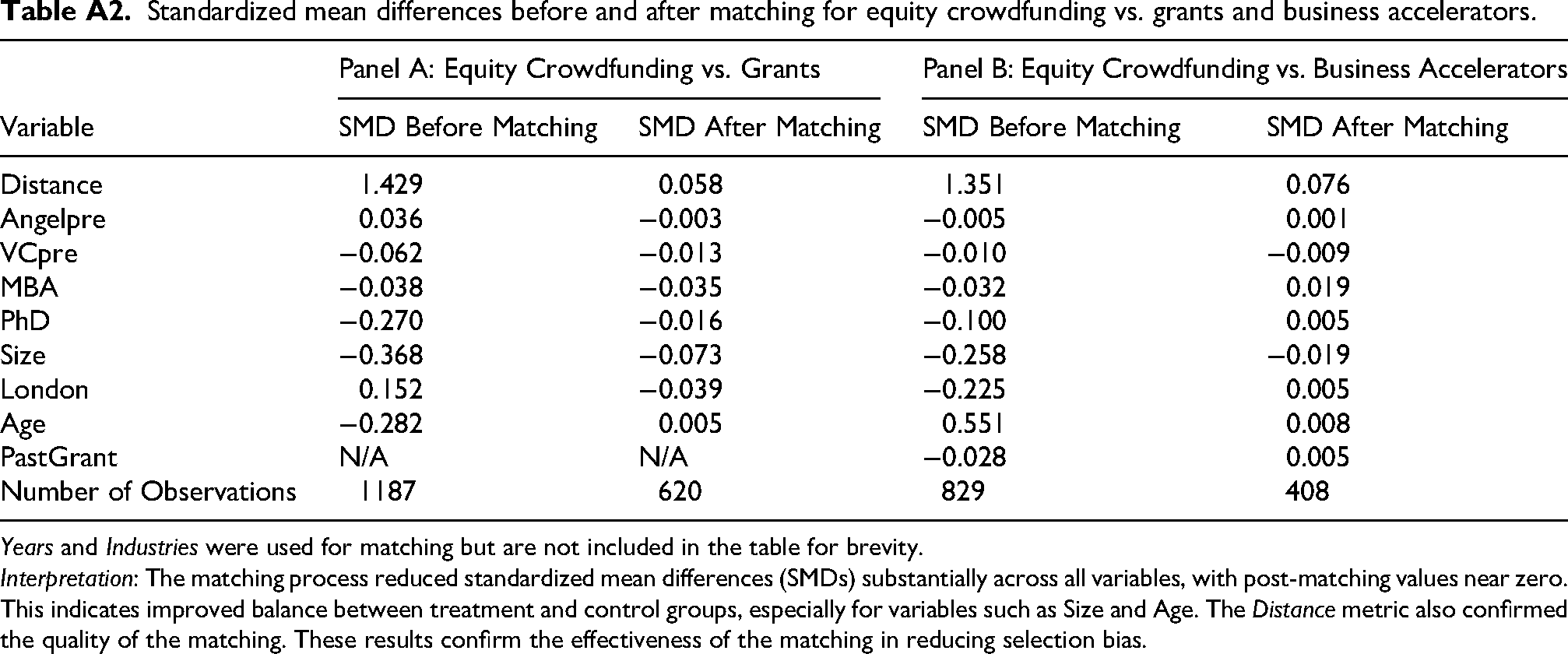

Matching: The propensity score matching (PSM) algorithm proposed by Heckman et al. (1997) was used to match treated and non-treated units across multiple dimensions. In this context, treated units are defined as start-ups funded through equity crowdfunding, while the control group comprises start-ups initially funded by grants or associated with business accelerators. The matching dimensions include variables such as human capital, age, previous funding sources, team size, location, industry, and funding years. A one-to-one matching procedure with no replacement and a caliper of 0.1 was employed to ensure accurate and reliable matches (Butticè et al., 2020). A summary of the matching procedure, including initial sample sizes, matched observations, and unmatched cases, is provided in Appendix Table A1. To assess the effectiveness of the matching process, balance diagnostics based on standardized mean differences (SMD) were conducted before and after matching, as shown in Appendix Table A2.

The robustness of this procedure depends on its underlying assumptions. The PSM procedure assumes that it can account for the unobserved characteristics of start-ups by leveraging observed characteristics for matching (Roma et al., 2021). In this study, this assumption is expected to hold true, given the inclusion of various control variables. These variables capture critical aspects of start-ups that VCs commonly use to assess quality (Ahlers et al., 2015; Hsu, 2007). If unobserved characteristics correlate with observed ones in VCs’ evaluations, the matching process can minimize disparities in both observed and unobserved traits between equity-crowdfunded start-ups and those funded by grants or affiliated with business accelerators (Roma et al., 2021). By aligning equity-crowdfunded start-ups with comparable non-equity-crowdfunded start-ups, the matching process facilitates the identification of those that are likely to attract VC funding.

Results of main effects

Given the binary nature of the dependent variable, this study employed a probit model, which is appropriate for modeling non-linear relationships and constrains predicted probabilities within the 0–1 range (Bowen and Wiersema, 2004). The probit model assumes a normal distribution of the error term, which aligns closely with this study's theoretical framework and context, which examines nuanced decision-making processes influenced by signaling theory. This model is also widely used in entrepreneurial finance research (e.g. Butticè et al., 2020; Roma et al., 2021; Rossi et al., 2021). While logistic regression is another common approach for outcome variables, its assumption of a logistic error distribution typically yields similar results to probit in practice. As a robustness check, this study's analysis was conducted using a logit model, and the results were consistent with those of the probit model, further supporting the methodological choice. The linear probability model was also considered but deemed unsuitable due to its unbounded probabilities, which can lead to unrealistic estimates.

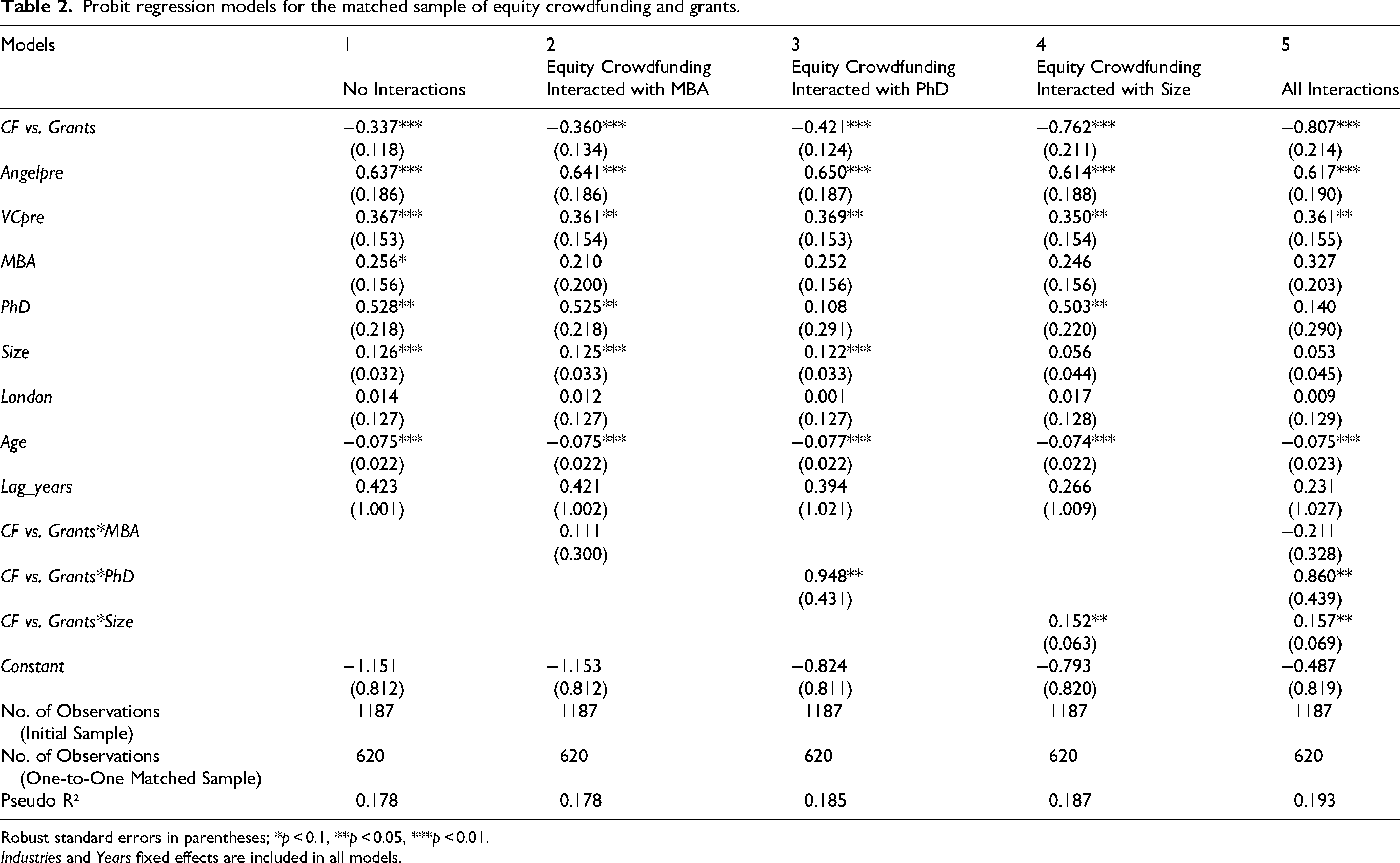

Table 2 presents the analysis based on a matching sample composed of equity-crowdfunded start-ups and start-ups receiving grants. To test Hypothesis 1, the variable CF vs. Grants was introduced, along with control variables, in Model 1. This variable's sign was negative and statistically highly significant (p < 0.01). The negative sign indicates that start-ups initially funded through equity crowdfunding are less likely to secure subsequent VC funding than start-ups that receive grants, thus supporting Hypothesis 1. The expected signs and significance of the control variables align with prior studies. Angelpre, VCpre, MBA, PhD, and Size show positive and significant relationships with late-stage VC funding, extending the findings from campaign-phase crowdfunding research (Ahlers et al., 2015; D’Agostino et al., 2022; Kleinert et al., 2020) to the post-campaign stage. Additionally, London as a location for the start-up is insignificant, while a start-up's age shows a significant negative relationship with securing late-stage VC funding.

Probit regression models for the matched sample of equity crowdfunding and grants.

Robust standard errors in parentheses; *p < 0.1, **p < 0.05, ***p < 0.01.

Industries and Years fixed effects are included in all models.

Interaction variables in Models 2–5 test Hypothesis 3A, and the results are consistent across all models. Even with all interaction terms included in Model 5, the main variable CF vs. Grants remains negative and highly significant (p < 0.01). While the interaction term for MBA is positive but insignificant, PhD and Size significantly moderate the effect of equity crowdfunding on subsequent VC funding (p < 0.05). Overall, Hypothesis 3A is partially accepted, with support from the human capital variables PhD and Size.

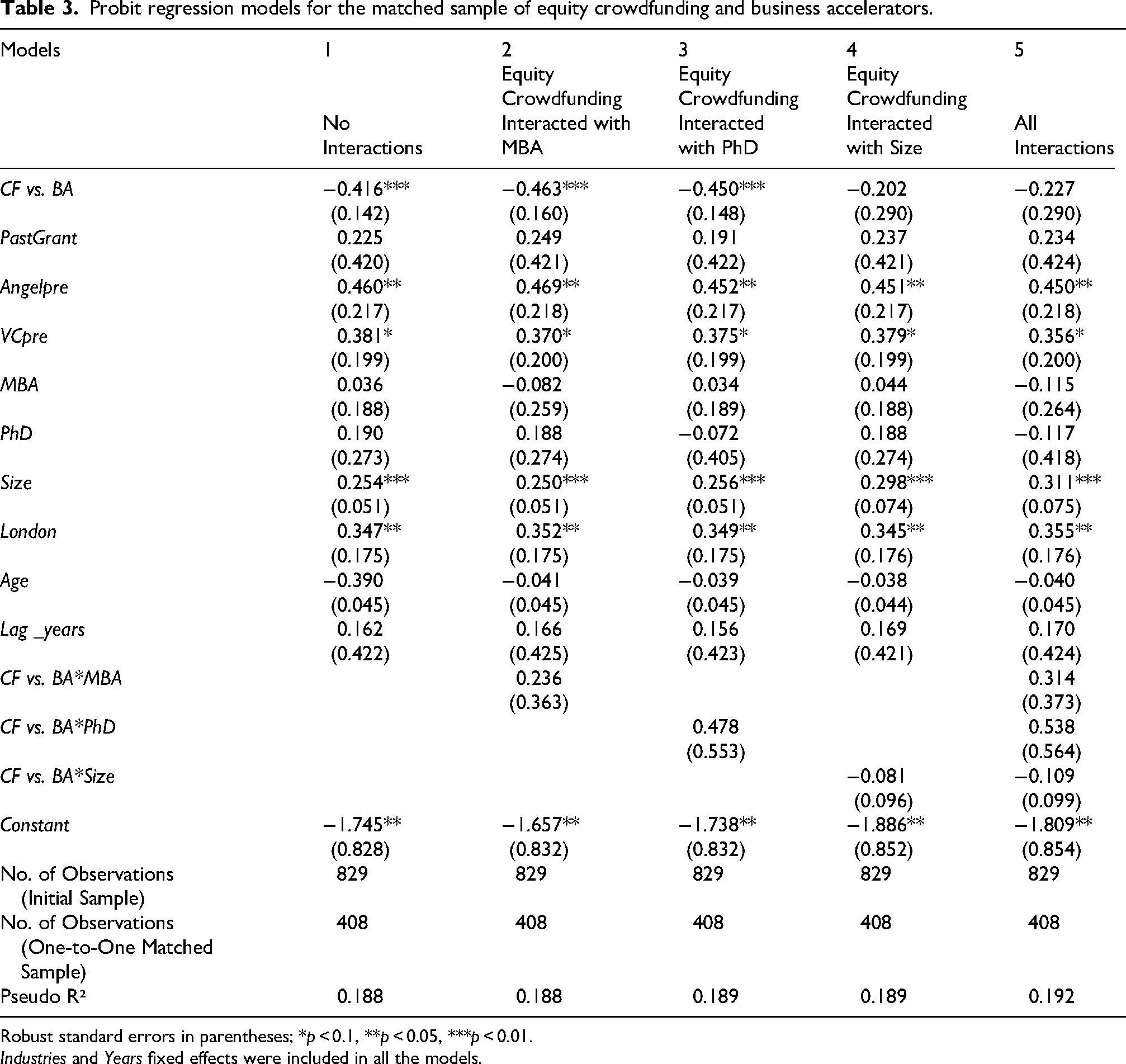

The same approach was utilized for control sample 2 with the variable CF vs. BA, comparing equity-crowdfunded start-ups with those associated with business accelerators. In Table 3, Model 1 shows a negative sign for the variable CF vs. BA, indicating that equity-crowdfunded start-ups are less likely to receive subsequent VC funding compared to those associated with business accelerators, thus supporting Hypothesis 2 (p < 0.01). Interaction variables in Models 2–5 test Hypothesis 3B, but the results are insignificant. The interaction terms for MBA and PhD show positive but insignificant effects. Similarly, the interaction term for Size is also insignificant, with a negative coefficient on subsequent VC funding. Therefore, Hypothesis 3B cannot be supported based on the interaction terms.

Probit regression models for the matched sample of equity crowdfunding and business accelerators.

Robust standard errors in parentheses; *p < 0.1, **p < 0.05, ***p < 0.01.

Industries and Years fixed effects were included in all the models.

Robustness checks

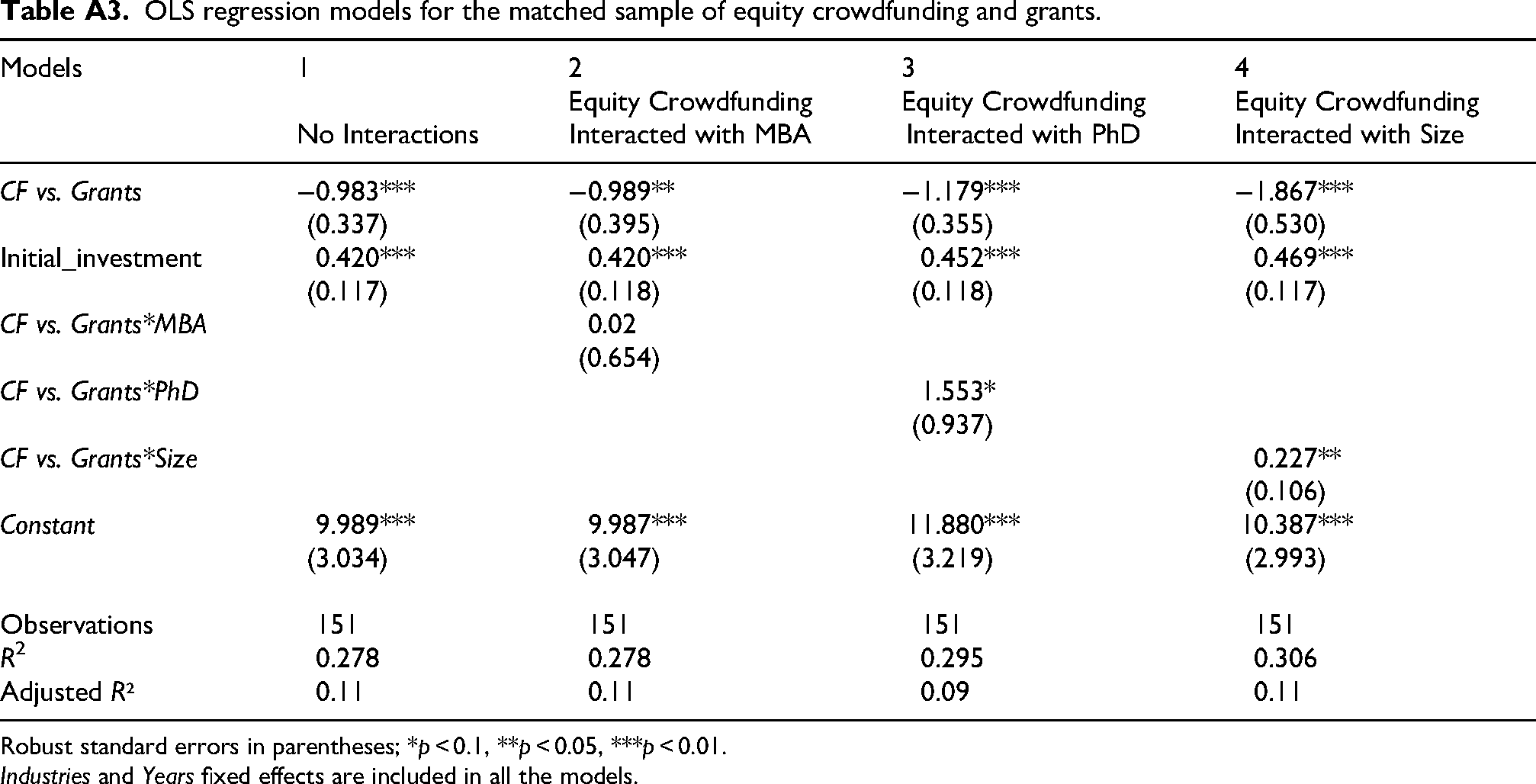

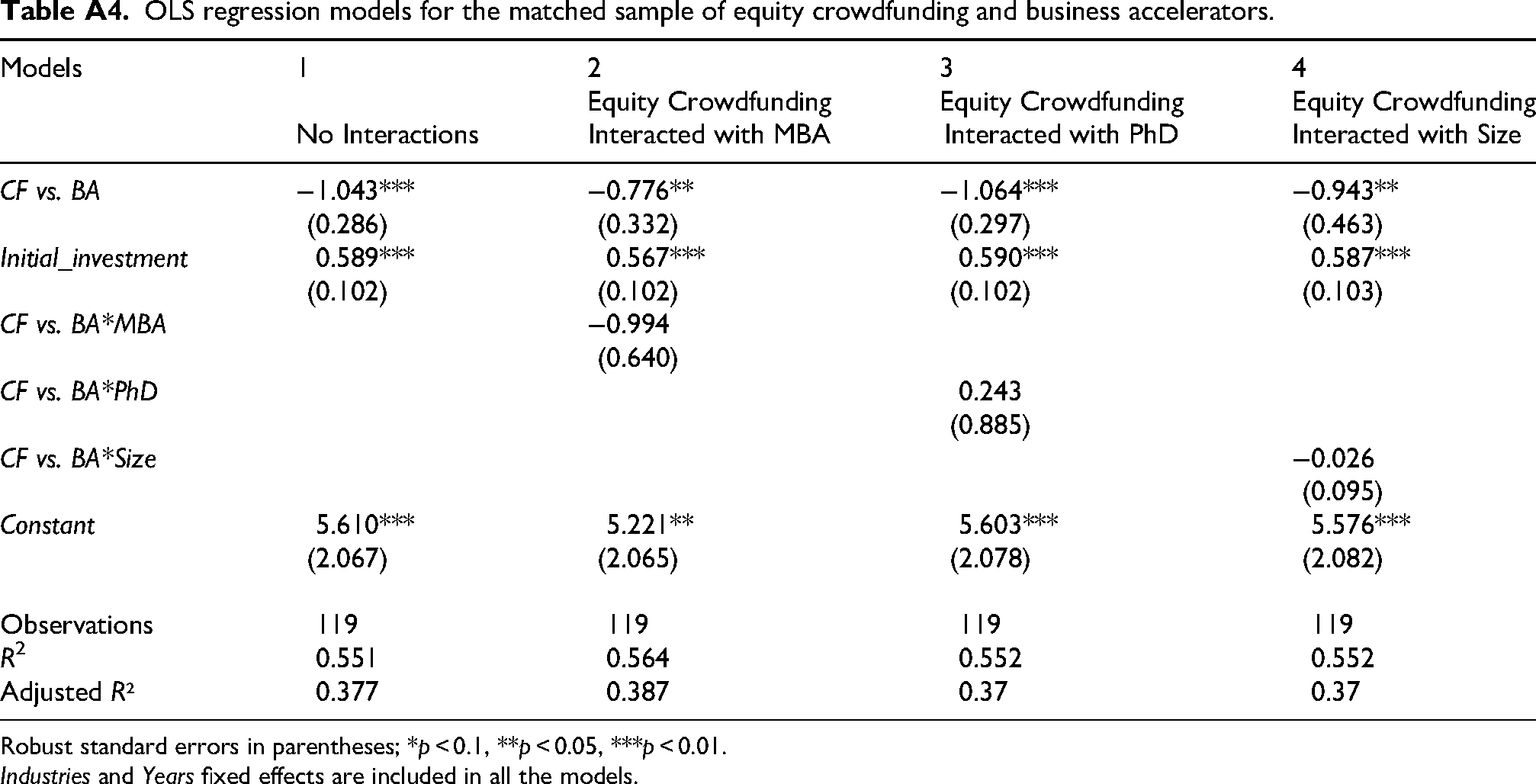

This study assumes that with maturity, start-ups seek VC funding as a next step for growth. Although not all start-ups may pursue this, the initial results are based on the assumption that all start-ups aim to secure VC funding. To further validate these results, an additional analysis was conducted as a robustness check, focusing on a sample of start-ups that had actually obtained VC funding. By using this refined sample, it was ensured that all included start-ups clearly wanted to pursue VC funding. For this sample, a different dependent variable, the amount of VC funding received, was used allowing for the assessment of equity crowdfunding's signaling effect compared with that of grants and business accelerators for start-ups that clearly wanted VC funding.

The robustness results (see Appendix Tables A3 and A4) align with the main findings. Start-ups initially backed by equity crowdfunding received lower subsequent VC funding amounts than those supported by grants or business accelerators, with negative and highly significant coefficients for CF vs. Grants and CF vs. BA (p < 0.01). Initial_investment (funding raised from early sources like crowdfunding, grants, or accelerators) was included as a control to account for the impact of early funding, and it showed a positive, significant effect across models, while other controls remained consistent. Interaction effects also reinforce the main results, with significant positive coefficients for CF vs. Grants*PhD and CF vs. Grants*Size (p < 0.1 and p < 0.05, respectively), indicating that entrepreneurs with PhDs and team size enhance the signaling value of equity crowdfunding.

Additionally, a sensitivity analysis was conducted to address potential concerns about time lags in VC funding. Observations from 2019 and 2020 were excluded from the initial funding samples (i.e. equity crowdfunding vs. grants and equity crowdfunding vs. business accelerators) to ensure that all included start-ups had sufficient time to secure subsequent VC funding by the end of 2022. The results were consistent with the main findings and are not included in this paper to avoid redundancy. However, they further confirm the robustness of the analysis.

Discussion

Equity crowdfunding addresses information asymmetries in start-ups by providing signals of observability and costliness. These platforms showcase start-ups’ quality by presenting their business ideas online, signaling their potential for future success. Platforms such as Crowdcube enhance the credibility of start-ups by hosting only those with high potential, thereby boosting investor confidence (Kleinert et al., 2020). Additionally, as outlined in the data section, equity crowdfunding platforms face reputational risks when selecting low-quality start-ups, while investors risk capital on uncertain ventures (Butticè et al., 2020; Lukkarinen et al., 2016).

The results in Tables 2 (Model 1) and 3 (Model 1) show that equity-crowdfunded start-ups are less likely to receive subsequent funding from VCs than start-ups that receive grants or are associated with business accelerators. This finding aligns with previous research by Roma et al. (2021), who compared third-party signaling between reward-based crowdfunding and early-stage VCs, concluding that reward-based crowdfunding does not effectively signal to late-stage VCs. However, they suggest that reward-based crowdfunding signaling, when complemented by patent certifications and a track record of success in the founding team's prior ventures, can match the signaling of early-stage VCs in securing late-stage VC funding. Similarly, Butticè et al. (2021) compared the signaling of equity-crowdfunded start-ups with business angels for late-stage VC funding, finding that equity crowdfunding's signaling is weaker than that of business angels but strengthens with a nominee shareholder structure. Additionally, Drover et al. (2017) found no significant signaling from equity crowdfunding to VCs. Therefore, this study contributes to the ongoing discussion about the signaling of new funding sources, such as equity crowdfunding, grants, and business accelerators, and their impact on traditional funding mechanisms, such as late-stage VCs, as highlighted by McKenny et al. (2017) and Drover et al. (2017). While previous studies have primarily compared traditional funding alternatives (Dutta and Folta, 2016), this study focuses on equity crowdfunding as an emerging funding source.

The findings in Tables 2 (Model 1) and 3 (Model 1) suggest that the signaling effect of equity crowdfunding is less effective than that of grants and business accelerators in attracting subsequent VC funding. Several factors may explain this discrepancy. While equity crowdfunding provides initial capital to start-ups, it often lacks the mentorship and expert guidance that late-stage VCs may look for when evaluating signals of start-up quality (Roma et al., 2021). The weaker signal from equity crowdfunding primarily stems from its less experienced and lower-stakes investor base, which may not evaluate or monitor start-ups rigorously. Consequently, VCs may perceive equity-crowdfunded start-ups as carrying a lower-quality signal compared to those supported by grants or business accelerators. Additionally, the online and dispersed nature of equity crowdfunding means that investors often base decisions on personal knowledge, interest, passion, or geographic proximity (Carbonara, 2021). In contrast, grants and business accelerators typically involve more structured, expert-driven evaluations, which may lead VCs to view them as stronger quality signals than equity crowdfunding.

Furthermore, the results in Table 2 (Model 1) highlight that grants act as an effective signaling mechanism, enabling start-ups to secure funding from late-stage VCs. This observation aligns with the findings of Islam et al. (2018) regarding the signaling efficacy of grants. Similarly, Table 3 (Model 1) shows that business accelerators provide a strong signal for start-ups to attract future funding, corroborating previous research on the signaling role of business accelerators (Hallen et al., 2014; Venâncio and Jorge, 2022).

To enhance the signaling value of equity crowdfunding compared to grants and business accelerators. MBA, PhD, and Size were considered as moderating variables. The results in Models 2–5 of Table 2 reveal that start-ups with at least one PhD entrepreneur significantly improve the signaling effect of equity crowdfunding compared to grants. This finding aligns with previous studies (D’Agostino et al., 2022; Kleinert et al., 2020), which identified a direct and significant signaling effect of PhD qualifications on crowdfunding success. It also extends prior research by demonstrating that entrepreneurs with PhDs enhance the likelihood of securing late-stage VC funding through interaction effects.

Similarly, the size of the entrepreneurial team strengthens the signaling of equity crowdfunding relative to grants. This result supports earlier findings by Ahlers et al. (2015) and D’Agostino et al. (2022), which reported a direct positive relationship between team size and equity crowdfunding success. These findings suggest that larger entrepreneurial teams increase the likelihood of subsequent VC funding for equity-crowdfunded start-ups through interaction effects, further expanding on prior research. However, the presence of at least one MBA-qualified entrepreneur in equity-crowdfunded start-ups does not show a significant moderating effect on signaling value compared to grants. Nonetheless, when treated as a direct control variable, the presence of an MBA entrepreneur significantly enhances the likelihood of obtaining VC funding. This result is consistent with previous findings by Ahlers et al. (2015) and Kleinert et al. (2020).

The moderating variables—MBA, PhD, and Size—presented in Models 2–5 of Table 3 do not significantly enhance the signaling value of equity-crowdfunded start-ups compared to those affiliated with business accelerators. This discrepancy arises from the fundamental differences between equity crowdfunding and business accelerators as funding sources. Business accelerators not only provide financial support but also deliver comprehensive professional development for start-ups, addressing a wide range of business needs beyond enhancing human capital (Avnimelech et al., 2021). Consequently, the human capital of start-ups, as measured by MBA, PhD, and Size, does not appear sufficient to elevate or equalize the signaling effect of equity crowdfunding to match that of business accelerator programs.

Implications of the results

This study empirically examines the interconnectedness of financing sources for entrepreneurial start-ups, especially equity crowdfunding, grants, and business accelerators. While prior research has primarily focused on the success of equity crowdfunding campaigns (D’Agostino et al., 2022; Kleinert et al., 2020; Lukkarinen et al., 2016; Ralcheva and Roosenboom, 2016), this study expands the conversation by exploring how these funding sources interact as mechanisms of certification or endorsement, (Butticè et al., 2020; Drover et al., 2017; Roma et al., 2021). Furthermore, it sheds light on the moderating role of human capital in the context of equity crowdfunding, grants, and business accelerators, an area often directly examined for crowdfunding success (Ahlers et al., 2015; D’Agostino et al., 2022; Kleinert et al., 2020; Piva and Rossi-Lamastra, 2018). This research advances the application of signaling theory (e.g. Ahlers et al., 2015; Fitza and Dean, 2016) by demonstrating that equity crowdfunding, grants, and business accelerators serve as signaling mechanisms for start-ups to showcase their quality. However, the signaling strength of these mechanisms is not equal when considered collectively.

From a practical perspective, the findings highlight that entrepreneurs can leverage various initial funding sources to launch their projects and attract late-stage VCs for commercialization. Initial funding sources, such as equity crowdfunding, grants, and business accelerators, provide avenues for entrepreneurs to signal the value of their businesses. However, the legitimacy and perceived quality of these signals differ. In this study, the signaling effect of equity crowdfunding is shown to be weaker compared to grants or business accelerators. For start-ups seeking to secure VC funding, strengthening other critical attributes, such as human capital, could enhance the signaling value of equity crowdfunding.

Limitations and future research

This study has several limitations. First, it focuses exclusively on one equity crowdfunding platform (Crowdcube) and is limited to the UK. While this provides valuable insights into the UK context, future research could expand the scope by examining other platforms and countries to determine whether these findings apply across different regulatory and cultural environments. Second, the study concentrates on the signaling effects of initial funding sources on late-stage VC funding without considering how entrepreneurs’ motivations or behavioral traits influence their initial funding choices. Future research could investigate the impact of these factors on funding preferences and subsequent VC funding outcomes. Third, this study evaluates equity crowdfunding as the sole form of crowdfunding. Future studies could explore the broader signaling effects of crowdfunding as a whole by comparing it with other initial funding sources. Additionally, it would be valuable to differentiate the signaling effects among various types of crowdfunding, such as equity crowdfunding versus reward-based crowdfunding, to access their relative appeal to potential investors. Fourth, to measure the moderating effects on VC funding, this study examines only human capital as a moderating factor. Future research could incorporate additional factors, such as equity retention and intellectual property rights, to assess their impact on the signaling value of equity crowdfunding. This approach could provide a more comprehensive understanding of how different elements influence subsequent VC funding outcomes compared with other initial funding sources.

Conclusion

This study evaluates the signaling value of equity crowdfunding for start-ups compared to grants and business accelerators in attracting late-stage VC funding. Drawing on signaling theory, the findings reveal that start-ups initially funded through equity crowdfunding are less likely to secure VC funding than those supported by grants or affiliated with business accelerators. However, human capital partially mitigates the funding gap between equity crowdfunding and grants in terms of the likelihood of obtaining VC funding, though its influence is less pronounced than that of business accelerator programs.

Footnotes

Acknowledgments

The author thanks Associate Professor Markus Fitza (Nord University, Norway, and Frankfurt School of Finance & Management, Germany) and Associate Professor Irena Kustec (Nord University, Bodø, Norway) for their valuable comments and insights during the development of this article. The author also thanks Associate Professor Tom Vanacker (Ghent University, Belgium) for his helpful comments and suggestions during the research stay, as well as the two anonymous reviewers for their valuable feedback on earlier versions of this paper.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Notes

Appendix

Sample sizes before and after matching. One-to-one propensity score matching (PSM) with no replacement and a caliper of 0.1 was used in both comparisons. Standardized mean differences before and after matching for equity crowdfunding vs. grants and business accelerators. Years and Industries were used for matching but are not included in the table for brevity. Interpretation: The matching process reduced standardized mean differences (SMDs) substantially across all variables, with post-matching values near zero. This indicates improved balance between treatment and control groups, especially for variables such as Size and Age. The Distance metric also confirmed the quality of the matching. These results confirm the effectiveness of the matching in reducing selection bias. OLS regression models for the matched sample of equity crowdfunding and grants. Robust standard errors in parentheses; *p < 0.1, **p < 0.05, ***p < 0.01. Industries and Years fixed effects are included in all the models. OLS regression models for the matched sample of equity crowdfunding and business accelerators. Robust standard errors in parentheses; *p < 0.1, **p < 0.05, ***p < 0.01. Industries and Years fixed effects are included in all the models.

Comparison group

Initial sample size

Matched sample size

Unmatched (excluded)

Equity Crowdfunding vs. Grants

1187

620

567

Equity Crowdfunding vs. Business Accelerator

829

408

421

Panel A: Equity Crowdfunding vs. Grants

Panel B: Equity Crowdfunding vs. Business Accelerators

Variable

SMD Before Matching

SMD After Matching

SMD Before Matching

SMD After Matching

Distance

1.429

0.058

1.351

0.076

Angelpre

0.036

−0.003

−0.005

0.001

VCpre

−0.062

−0.013

−0.010

−0.009

MBA

−0.038

−0.035

−0.032

0.019

PhD

−0.270

−0.016

−0.100

0.005

Size

−0.368

−0.073

−0.258

−0.019

London

0.152

−0.039

−0.225

0.005

Age

−0.282

0.005

0.551

0.008

PastGrant

N/A

N/A

−0.028

0.005

Number of Observations

1187

620

829

408

Models

1

2

3

4

No Interactions

Equity Crowdfunding

Interacted with MBA

Equity Crowdfunding

Interacted with PhD

Equity Crowdfunding

Interacted with Size

CF vs. Grants

−0.983***

−0.989**

−1.179***

−1.867***

(0.337)

(0.395)

(0.355)

(0.530)

Initial_investment

0.420***

0.420***

0.452***

0.469***

(0.117)

(0.118)

(0.118)

(0.117)

CF vs. Grants*MBA

0.02

(0.654)

CF vs. Grants*PhD

1.553*

(0.937)

CF vs. Grants*Size

0.227**

(0.106)

Constant

9.989***

9.987***

11.880***

10.387***

(3.034)

(3.047)

(3.219)

(2.993)

Observations

151

151

151

151

R

2

0.278

0.278

0.295

0.306

Adjusted R²

0.11

0.11

0.09

0.11

Models

1

2

3

4

No Interactions

Equity Crowdfunding

Interacted with MBA

Equity Crowdfunding

Interacted with PhD

Equity Crowdfunding

Interacted with Size

CF vs. BA

−1.043***

−0.776**

−1.064***

−0.943**

(0.286)

(0.332)

(0.297)

(0.463)

Initial_investment

0.589***

0.567***

0.590***

0.587***

(0.102)

(0.102)

(0.102)

(0.103)

CF vs. BA*MBA

−0.994

(0.640)

CF vs. BA*PhD

0.243

(0.885)

CF vs. BA*Size

−0.026

(0.095)

Constant

5.610***

5.221**

5.603***

5.576***

(2.067)

(2.065)

(2.078)

(2.082)

Observations

119

119

119

119

R

2

0.551

0.564

0.552

0.552

Adjusted R²

0.377

0.387

0.37

0.37