Abstract

Concerns about climate change and energy security are driving a global shift towards renewable energy sources and green technologies such as electric vehicles (EVs), energy storage and wind turbines. This commentary analyses the policy challenges raised by the growing demand for critical metals needed for this green transition to net zero. It is crucial that the UK's strategy looks beyond merely increasing primary supply or new mining, towards strategies to ensure better stewardship of secondary mineral resources already contained in a range of products. Furthermore, creating an enabling regulatory environment for procuring key technology metals will be key to addressing future supply threats for the UK, especially post-Brexit, and that failure to do so will put the UK at significant risk of falling behind in the global race to secure supplies.

Keywords

Introduction

Concerns about climate change and energy security are driving a global shift towards renewable energy sources and green technologies such as electric vehicles (EVs), energy storage and wind turbines. However, manufacture of these green technology products, which is crucial for achieving climate change targets, depends on the ongoing availability of various critical metals (CMs). 1 The supply of CMs for the clean energy transition has been identified as one of the key policy challenges in the 2020s 2 to achieve Net Zero and address the climate challenge. As the IEA points out, clean energy technologies require far more critical minerals to build than their fossil fuel counterparts: for example, a typical electric car requires six times the mineral inputs of a conventional car and an onshore wind plant requires nine times more mineral resources than a gas-fired plant. 3 The global shift towards green technologies has, therefore, significantly increased CM demand, alongside multiple risks that could hamper CMs supply, such as uneven geological resource reserves, patchy processing distribution and lack of substitutes. Thus, effective strategies are imperative for maintaining supplies to meet the rise in demand, improving the UK's future supply chain resilience and to meet its climate change objectives. 4 While other countries have been bolstering their strategic efforts in this area for the last few years, the UK has been slower to respond. It was only in the 2021 Net Zero Strategy that the UK Government began to articulate a clearer strategy surrounding critical minerals 5 and recognised the key role these will play in achieving environmental and economic objectives. On the 22 July 2022, the UK Government took this further and released ‘Resilience for the Future: The UK's Critical Minerals Strategy’, 6 the UK's first independent policy strategy in this area.

This commentary will analyse the policy challenges raised by the growing demand for CMs needed for the transition to net zero. It is crucial that the UK's strategy looks beyond merely increasing primary supply or new mining, towards strategies to ensure better stewardship of secondary mineral resources already contained in a range of products. It is important to also ensure focus on mid-stream processing. Leveraging the UK's innovation assets can potentially unlock processing primary material from new trade partners, while also encouraging a circular economy of critical materials.

Given the imperative of the climate challenge, approaches to mitigating materials criticality also need to be cognisant of the time implications of different pathways. Mitigating against minerals criticality by developing new or alternative materials may bear fruit in the longer term, and such efforts are essential to long-term sustainability goals. However, in the short term, there is an inevitable need to mobilise greater access to primary resources, and to explore which products contain accessible stocks of technology critical metals (TCMs) that could be recycled for new manufacture. In the case of, for example, electric car batteries, it may take some years to obtain significant end-of-life battery flows, given the relative newness of EVs on the market. For other materials like rare-earth magnets, however, there already exists a supply of magnetic scrap within products that have reached end of life (old computers, motors etc.) which could potentially valorise and deliver additional material to the market.

In the first section, we outline the central importance of CMs to green technologies, and the minerals demand that will be created by the net zero transition. In the second section, we explore circular economy approaches that can supplement primary supply of CMs (e.g. through recycling and/or reuse), as well as demand reduction (e.g. through optimisation of materials use and extending product life). The last section discusses the challenges and opportunities of creating effective governance mechanisms for a CMs circular economy and for new mining. We conclude that creating an enabling regulatory environment for procuring key technology metals will be key to addressing future supply threats for the UK, especially post-Brexit, and that failure to do so will put the UK at significant risk of falling behind in the global race to secure supplies.

Critical materials and green technologies

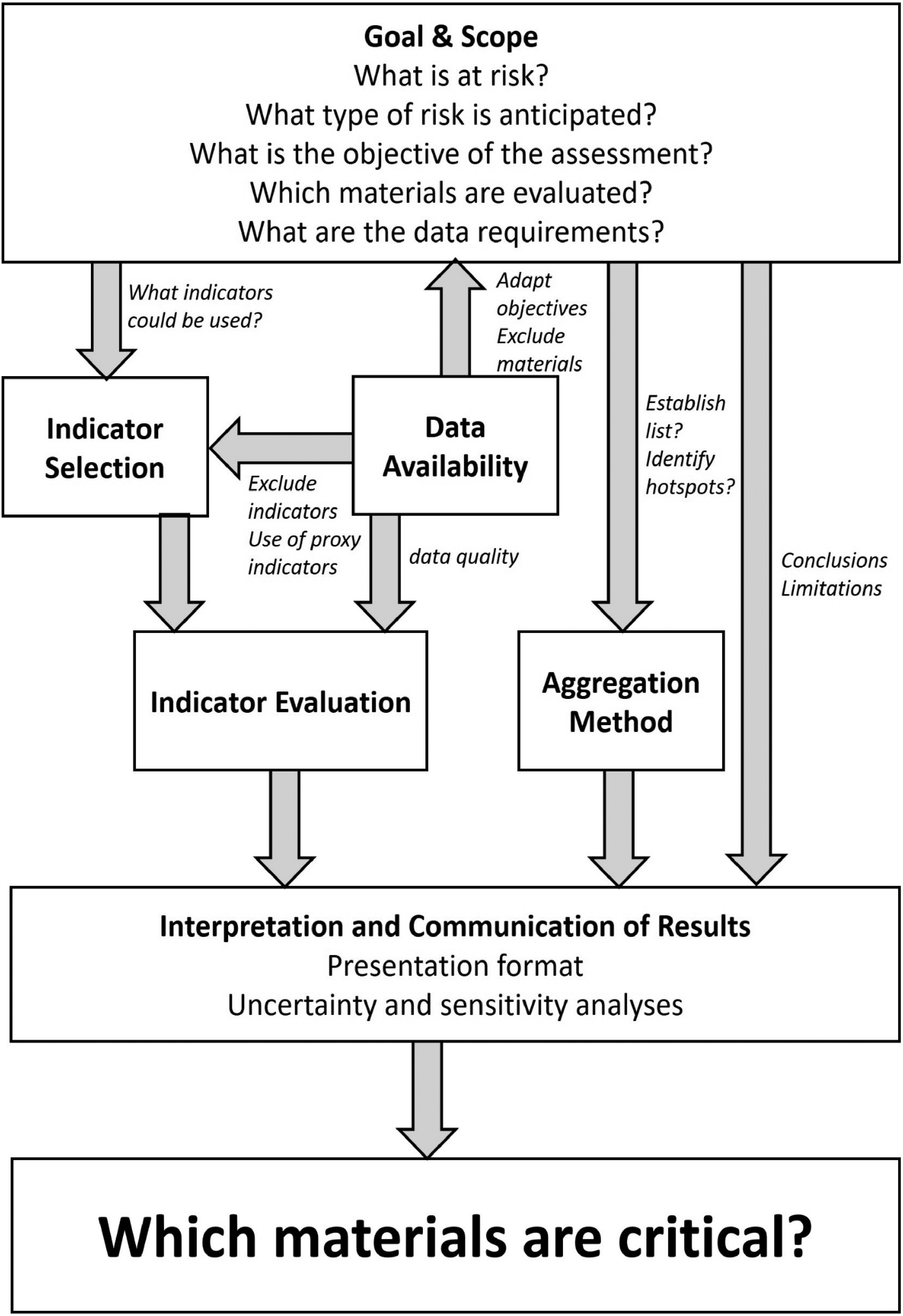

Methods for assessing material criticality vary and are usually based on a range of inputs, including data or expert judgement. 7 There are a number of definitions and terminologies for TCMs, 8 with supply risks and economic importance ranking amongst the foremost criteria for assessing criticality. 9 Figure 1

How the goal and scope influences which materials are critical. Redrawn from the original. 98

A material may be considered critical if it has properties (such as being magnetic or emitting light) that are essential for a product and cannot readily be provided by other materials, (which therefore makes it economically important) and is at risk of supply disruption. 10 In 2020, the EU has published regular lists of ‘critical materials’ which are deemed to have crossed this threshold. 11 Within ‘Critical Materials’ an important subset of materials is ‘TCMs’. This is a more specific and narrow term that focuses exclusively on metals important for technology applications. This term would exclude, for example, materials such as ‘Natural Rubber’ even though this is included in the EU critical materials list. Many of the chemical elements embedded in green technologies are strategically important and becoming increasingly vulnerable to supply risks; these are sometimes referred to broadly as ‘strategic elements’. Critical minerals is another widely used term, although the term ‘minerals’ can be perceived as focussing on primary supply and mining.

Additionally, there are other materials which, whilst not defined as ‘critical’, are still seen as materials of concern. For example, with the growing need for nickel in battery manufacturing, it was identified by the EU as a ‘material of concern’ to keep a watching brief over. 12 Current political events in Ukraine have further escalated concerns over nickel supply. Interestingly, the UK Government's new strategy, discussed below, positions itself as a ‘Critical Minerals’ (as opposed to the EU's critical materials) Strategy. This new Critical Minerals Strategy in the UK 13 has a smaller list of key resources listed than the EU's Critical Materials Communication. The main reasons for the differences in lists are the scope of the list, methodologies applied and the geographical location of the assessor.

It is difficult to make definite estimations of the quantities of different minerals that will be required in the future, as the mineral demands vary by technology, and thus could be affected by factors such as technological innovations, optimisation of materials usage and climate policies. A good illustration is EV batteries, which currently rely on cobalt, but the ongoing development of low-cobalt battery technologies could lead to a future decline in cobalt demand. 14 However, all analyses agree that deployment of clean energy technologies will ‘supercharge’ the demand of critical materials. 15 Demand for metals and minerals needed for EVs and battery storage is projected to grow from between 10 times to 30 times the current demand by 2040. 16 Lithium, nickel, cobalt, manganese and synthetic/high-grade natural carbon will be the predominant materials needed in the EV sphere. In a recent report, the IEA noted that the world would need 50 more lithium, 60 more nickel and 17 times more cobalt by 2030 if countries around the world were to deploy sufficient green technologies to meet their pledged emissions scenarios. 17

The growth of green hydrogen is expected to lead to a significant rise in demand for nickel and zirconium. The growth in wind power will lead to a manifold increase in need for materials such as copper and rare-earth elements (REEs) such as neodymium, dysprosium and terbium. These REEs are essential to manufacture the high-strength magnets contained in offshore wind generators and high-performance motors for EVs. 18 Platinum group metals (such as platinum and palladium) are used in vast quantities in catalytic convertor emission abatement systems. Materials such as rhenium and tantalum will be essential for aerospace applications and the future electrification of air transport. Materials such as arsenic, gallium, indium, tellurium and germanium are needed for solar energy devices. Further, assessments around critical materials demand for low-carbon technologies often miss the need for digital and grid technology deployment. The low-carbon energy transition needs ‘smart grids’ to make the new system work effectively. Again, materials demand is often missed when the focus is only on the specific generator or PV panel.

The primary resources from which many TCMs are derived are not uniformly distributed around the globe. The challenge for many countries in the West is the dominance of China in supply chains for many of the key materials. Moreover, the processing capacity needed to transform these raw materials into refined products for industrial use is also not uniformly distributed. Furthermore, disruptions to global supply chains resulting from the Coronavirus pandemic 19 have posed a challenge to what has been a prevailing narrative of globalisation in the latter half of the twentieth century. The pandemic has highlighted the fragility of global supply chains, 20 and many manufacturers are considering the advantages of ‘reshoring’ 21 operations. After a period of growth of global value chains, momentum appears to have stalled 22 and structural shifts appear to point to a new emerging narrative where manufacturers are considering the resilience that can be offered through more domestic capacity. 23 There are other factors that are also influencing this trend. For example, a growing middle class in countries where labour was hitherto cheap now command higher wages, which diminishes the relative advantages of offshoring operations.

Development of new renewable technologies required for environmental objectives, coupled with supply issues, have resulted in more prominent discussion of material requirements of the energy transition amongst policymakers and energy experts. 24 Critical materials supply for the clean energy transition has been identified as one of the key policy challenges in the 2020s 25 and measures to tackle this are essential to climate change goals. 26 The IEA recently published a dedicated report on the topic. 27 A number of recent reviews focus on the resilience of the material supply chains and identify the energy transition as one of the most important factors driving rapidly growing demand. 28 Time is scarce and the relatively late realisation of the importance of materials supply and demand means that the scope for incremental changes may have passed.

Legal and policy context in the UK

The UK was the first country to set out legal targets to reduce greenhouse gas (GHG) emissions. With the entry into force of the Climate Change Act in 2008, 29 the UK Government was charged with legally binding targets to reduce GHG emissions by at least 80%, compared to a 1990 baseline, by the year 2050. This was followed by many subsequent strategies across different policy areas that contribute to emissions of GHGs. 30 Although this was an ambitious target at the time, the UK Government soon decided to extend its target further; partly to meet global pledges but also to position the UK as a global actor in climate action. In its 2019 Net Zero report, the Climate Change Committee recommended that rather than setting ‘a 97% target that leaves a small residual amount of emissions’, it would be more appropriate to set a net zero target. 31 Accordingly, section 1 of the Climate Change Act was subsequently amended in 2019 so that the target was now to achieve net zero GHG emissions by 2050.

In the same vein, the UK Government launched a Ten Point Plan for a Green Industrial Revolution in 2020. 32 This Plan aims not just to address climate change, but also to enable the UK to ‘transform its economy, deliver jobs and growth across the country’. 33 This will be underpinned by the UK's ability to capitalise on low-carbon technologies, in the expectation that investing in clean technologies will help position the UK as a global leader in green technologies. 34 This discourse clearly maintains that technology is the primary driver not only for environmental change, but also for economic growth. 35 Out of 10 points, seven points directly rely on the use of particular technologies to drive the change.

Of particular importance for this discussion are the three points of the Ten Point Plan which outline UK ambitions to promote technologies which are fundamentally reliant on a steady supply of technology metals. Firstly, the UK Government is committed to advancing offshore wind, its ambition is to ‘quadruple our offshore wind capacity so as to generate more power’. 36 By 2030, the UK aims to produce ‘40GW of offshore wind, including 1GW of innovative floating offshore wind in the windiest parts of UK seas’. 37 In 2018, nearly all of the offshore wind turbines deployed in Europe used permanent magnet motors 38 containing rare-earth materials. Wind turbines require around 0.5kilotons of magnets per GW. 39 As wind turbines scale up and become larger, they make more efficient use of materials. In order to fulfil this ambition, the UK would need to secure around 20 kt of rare-earth magnet material if this demand was to be fulfilled using permanent magnet machines. Secondly, the shift to EVs is another important objective and the UK aims to accelerate the shift to electric mobility by adopting more stringent phase-out deadlines: the sale of new diesel and petrol cars will now end by 2030, while achieving 100% zero emission from 2035. 40 As with offshore wind technology, electric cars are heavily dependent on CMs. The fact that other countries are also announcing similar plans and policy measures to move to electric transport means that global competition for EV battery materials is likely to intensify further. Global demand for lithium, for example, is predicted to grow by over 20% a year in the next decade. 41 Finally, the growth of low-carbon hydrogen relies on platinum group metals; thus, the access to these metals will be necessary for the UK to achieve its ambition to develop ‘5GW of low-carbon hydrogen production capacity by 2030’. 42

The 2021 Net Zero Strategy sets out a clearer strategy surrounding critical minerals and recognises these as key to the growth of clean energy technologies. 43 Due to different risks that may hamper their supply, the Strategy recognises that it is critical to maintain flow within supply chains and improve the UK's future economic resilience. 44 Equally, the Net Zero Strategy acknowledges the importance of the mining sector, vouching to support engagement in new and existing markets as well as to facilitate investment and collaboration in extraction and processing opportunities. 45 However, some stakeholders have reservations over the use of the term ‘minerals’ in the Strategy as it appears to focus on increasing metals mining or primary supply, and this alone will not be sufficient to address the anticipated short-term demands. Nor would an emphasis on increasing supply solely through increased mining align with environmental and circular economy goals. An environmentally sound strategy, we contend, should also equally emphasise sustainable options to address supply risks. As discussed further in the section Challenges and opportunities surrounding technology metals, primary mining must be supplemented by efforts to increase secondary supply (e.g. through recycling), as well as demand reduction (e.g. through optimisation of materials use and extending product life).

On 04 July 2022, the UK launched the Critical Minerals Intelligence Centre (UKCMIC), 46 its first-ever centre to analyse stocks and flows of critical minerals to support and inform the delivery of the 2022 UK Critical Minerals Strategy. 47 The Centre, based in Nottingham, will be run by the British Geological Survey and governed by the Department for Business, Energy and Industrial Strategy (BEIS). Funding is available for the CMIC over 3 years, to provide criticality assessments and aid evidence-based policymaking in relation to CMs. The first list of materials considered a high criticality risk for the UK include antimony, bismuth, cobalt, gallium, graphite*, indium, lithium*, magnesium, niobium, palladium, platinum, REEs, silicon, tantalum, tellurium, tin*, tungsten* 48 and vanadium. 49 The UK has several critical minerals resources. 50 Whilst this presents an opportunity, there are also a number of ongoing challenges that will be discussed in the next section.

Challenges and opportunities surrounding technology metals

Building effective governance frameworks for new mining

A demand-led response to the challenge of minerals criticality for each Government globally would entail securing access to growing quantities of primary raw materials to feed rising demand for key technology metals through increased mining and processing. This would involve import of those materials, as well as exploring domestic production. However, potential environmental harms from mining must be mitigated by robust governance to ensure high levels of environmental protection. Actions to boost supply over the period up to 2030 and beyond would be crucial, for example by facilitating geological exploration and mining projects or improving recycling facilities and waste collection. 51 In the UK context, the main question is whether these materials are available domestically, in particular lithium and tungsten of which there is growing evidence to suggest potential geological reserves. Exploration is currently underway in Cornwall for tungsten, tin and hard rock lithium. 52 Globally significant levels of lithium deposits have been found in Cornish hot springs and a number of exploration and extraction projects for battery-grade lithium from tin and copper mines are underway. 53

However, the ongoing renaissance of UK mining (such as the exploration work currently being carried out by a number of companies in Cornwall) 54 will need to be underpinned by a supportive planning and permitting process that ensures prevention of environmental harm while also remaining mindful of the growing need for a domestic UK mining industry to achieve climate change goals. Outdated mining laws and cumbersome minerals rights regimes are a significant barrier to environmentally sustainable UK mining. Mineral rights in the UK are historically complex, often dating back hundreds of years to the manorial rights of large landowners and the Church; these rights can be owned separately from surface rights in land and were often retained even when land title was transferred. 55 As there is no regulatory requirement to register minerals ownership in the UK, these rights can often remain unknown and undocumented in land registry transactions. 56 This lack of clarity and uncertainty presents a threat for potential investors and is an important barrier to exploration and mining in the UK. By contrast, countries such as Canada and Australia have regulated systems whereby the state grants exploration licences. 57 This opens up a question about best ways to simplify and facilitate the identification of the minerals ownership system in the UK if the potential of lithium and other geological reserves is to be actualised. Various options need to be examined, from nationalisation of mineral rights to compulsory registration of those rights. Each solution needs to be carefully considered both in terms of how it affects property rights of individuals and in terms of time and resources required to implement any new solution. Finally, this issue is closely linked to the question of environmental liability which also needs to be considered as a part of the reform.

Limits of demand-led approaches

The UK's current strategy appears to be demand-led, rather than exploring the potential for demand side management 58 alongside new minerals extraction. However, it is important to look beyond mining ever-greater quantities of CMs and shift the focus towards circular economy approaches which focus on resource efficiency and therefore greater environmental sustainability. In the short term, supply threats could be mitigated through interventions aimed at reducing demand, such as extending the life of products and investing in scientific research to substitute CMs with other alternatives. 59 Whilst critical materials undoubtedly impart unique qualities to the technology devices that contain them, there are many approaches to reducing the quantity demanded by our economy, such as technical innovation to develop products that make better use of materials and improving manufacturing efficiencies to reduce waste in the manufacturing process. Redesigning products to last longer, as well as extending life through repair, refurbishing, and remanufacturing will be crucial to a sustainable circular approach.

In addition, there are also social approaches to help reduce demand. For example, private vehicles are a poorly optimised asset which spend most of their time parked up. By pivoting to public transport, cycle hire and shared transport 60 , much more efficient use can be made of vehicles and their constituent materials. Business models based on product leasing, or ‘products as a service’ models can also make a significant contribution to better resource management, and there is growing interest in this approach. 61 Such innovative business models would be particularly beneficial for products that contain significant quantities of critical materials, such as EV batteries, 62 as this would facilitate more effective collection, takeback and recycling/reuse at the end of life.

Developing enabling recycling regulation

Recycling as a part of the circular economy model of critical materials will be a key approach for ensuring stewardship of material resources, as opportunities for increasing primary supplies through new mining will necessarily be limited by geological, environmental and social factors. In addition to being a resource opportunity, recycling is also essential to ensure correct management of waste at the end of life. Moreover, growing volumes of waste are expected as new technology products reach their end of lives. The UN forecasts, for example, that e-waste (electronic and electrical waste) volumes are likely to rise from 50 million tonnes in 2019 to 120 million tonnes in 2050. 63 Current recycling rates for REEs are only around 1%. 64 While we are used to recycling materials like glass, paper, plastics and metals like steel, recycling pathways for CMs are less well-developed. Improving CM recycling efficiencies will require substantial improvements in product design, recycling technology and recycling infrastructure. People are now familiar with the need to sort certain materials in order to avoid contamination and to ensure that the properties of the recycled product are preserved. However, electronic and electrical products containing critical technology metals do not yet have the advantage of mature recycling routes and high public awareness.

Further, given the functional nature of critical materials, purity is especially important, and given that small quantities of these critical materials are often dispersed through large products, efficient minerals recovery is particularly difficult. Research efforts need to aim at developing low-cost recycling technologies, improving recycling efficiencies, recovering better quality and high-value recycled content.

Under current UK regulations, many recycling efficiency targets focus on setting percentage targets by overall weight of product. That is, the regulations usually stipulate that a certain percentage by weight of the overall product should be recycled. However, this is a somewhat crude and inadequate approach for critical materials, which are usually found in relatively small quantities in technology devices, making them costly to recover. In the absence of regulatory drivers, recyclers often have little incentive to bear the costs of recovering these critical materials. Recycling obligations are, therefore, often met by recycling of relatively low-value material that is easier to recover, while critical minerals may be lost. The new EU Batteries Regulation 65 takes a more well-considered approach to critical materials circularity, by setting specific recovery targets for minerals of particular concern, such as cobalt, lithium and nickel. It stipulates, further, the amount of recycled material that must be included in future batteries. These escalating targets should serve to drive the efficiency of the recycling process and focus recovery efforts on high-value critical minerals. Such governance mechanisms, focussed on critical materials recovery and underpinned by circular economy principles, have significant potential to achieve a secure and sustainable critical materials supply chain.

Eco-design standards

The dominant approach in the recycling industry for materials recovery is to shred products to liberate the materials that they contain, and then recover the materials that are the product of this shredding process using carefully selective processes. 66 However, more efficient recycling processes might focus on ‘disassembling’ products and recovering materials with more care to reduce contamination. This then enables the subsequent chemical processing steps to be much simpler, as they do not need to be as selective. This means that simpler, less energy-intensive chemistries can be employed. The back end "chemical complexity" is reduced, but this comes with the requirement of greater mechanical front end "mechanical complexity" in disassembling devices. However, this has enormous potential to increase materials recovery and reduce environmental impact. To achieve this, eco-design becomes essential to making products easier to recycle, but recycling is often an afterthought. Products are designed for manufacture, but little thought is given to ‘unmanufacturing’ at the end of life. Design for recycle has the potential to aid in optimising materials recovery at the end of life. 67 Unhelpfully, products are often stuck together with glues and adhesives, which hampers their recycling and makes the process all the more difficult: particularly hazardous for potentially explosive products such as EV batteries. 68 Eco-design of products to facilitate reuse or recycling by designing for disassembly and materials recovery has long been a goal of EU policy makers. Regulatory interventions or standards in regard to eco-design can significantly aid circularity.

Research and investment

Any UK strategy on critical materials should be coupled with the ability to attract large-scale strategic private investments for supply chain development of technology – CMs both at home and abroad. To this end, the UK is seen as one of the most attractive locations in Europe for inward investment, 69 with the UK attracting the second most inward-investment projects in Europe, but closing the gap with the leader, France. 70 The Strategy echoes the Beddington Report 71 in suggesting using the leverage of the City of London as a world-class financial hub to create the context for investment in critical minerals development. 72 That said, the UK trails the EU in attracting investment in clean technology and this is a key area for improvement. 73 Securing access to key TCMs and their supply chains will help significantly in aiming to make the UK an attractive destination for clean technology development.

The United Kingdom does have a number of unique strengths, with a unique cluster of research and development capabilities. However, furthering research and scientific collaboration between the UK and international partners is a foundation stone of scientific progress. It will be important to ensure that close collaboration with EU-based partners continues, especially in the light of the outcome of Horizon Europe Associated Partnership Agreement. Many EU-based university and research and technology organisations have a strong track record on research, innovation and education on critical materials; it would be advantageous to the UK to foster and build on ongoing links with these. There are also significant advantages to collaborating with mineral-rich nations outside Europe, like Canada, Australia and the USA. From a legal and regulatory perspective, there are many things that could make the UK a more attractive destination concerning researcher mobility, and it is important to ensure this is as easy as possible.

Concluding remarks on the way forward

As the UK Government moves from its initial Critical Minerals Strategy and begins to translate this into action, wider consideration of product-relevant policies that contain those critical materials is needed to maximise recovery of CMs at the end of product life. This may prove to be an onerous task, as the UK is faced with rapid economic challenges and a shifting geopolitical landscape. Moreover, most other nations around the world are competing for access to the same resources. The geopolitical picture is complicated by conflicts, as some resources and their processing capacity are owned by nations under sanctions, aiming to provide leverage in ongoing geopolitical events. However, in turn these sanctions provide further challenges for the countries imposing them in terms of their own materials security. In developing the delivery plan for the new strategy on critical materials, the UK Government needs to forge new international trade alliances and consider approaches taken by other countries, including environmental and labour safeguards in trading partner countries. Such an approach would build on the lead taken in COP26 and could set a benchmark internationally. The Strategy already considers the actions necessary to achieve international collaboration on critical minerals and considers Environmental & Social Governance (ESG) of materials as one of the key pillars of future critical minerals policy. 74

UK policy on critical materials has needed to adapt following leaving the European Union. There are multiple implications for UK Critical Materials Strategy which need careful and informed evaluation. UK critical materials policy as well as product standards that contain those materials were previously developed as a part of EU policy. Although the UK is now free to independently formulate its own policy by creating a new governance regime that may diverge from the EU regime, this may not be an optimal approach. The UK market is highly integrated into the EU market which has consistency of standards and practices. Therefore, any greater regulatory divergence would create market barriers and increase trade friction, neither of which would help the UK economically. In turn this could hamper the UK's efforts to develop sustainable critical materials policies.

Equally important are the timescales needed to develop any new strategy, which can take decades to develop and embed, as seen in the cases of the EU and USA. Given the pressing nature of the climate challenge, it is essential to put in place approaches to mitigate against materials criticality that can be more rapidly implemented and prioritise regulatory intervention accordingly.

At a time when a clear and workable plan is needed to secure global supplies of the TCMs needed by British industry, the UK's plan has been further beset by challenges from unprecedented global events and domestic distractions. 75 For some TCMs such as lithium and tungsten, there is the potential to develop indigenous primary sources, for many others there are not. Whilst the mineral wealth under UK soil is defined, the UK can make careful, informed choices to improve supply chain resilience. There is potential to build domestic processing capacity for a range of materials, and the UK should explore the synergies between primary (mined) and secondary (recycled) material inputs into these supply chains. 76 In many cases, the same processing technologies exist for both, and if set up correctly, both should be leveraged to support the downstream supply chain. 77

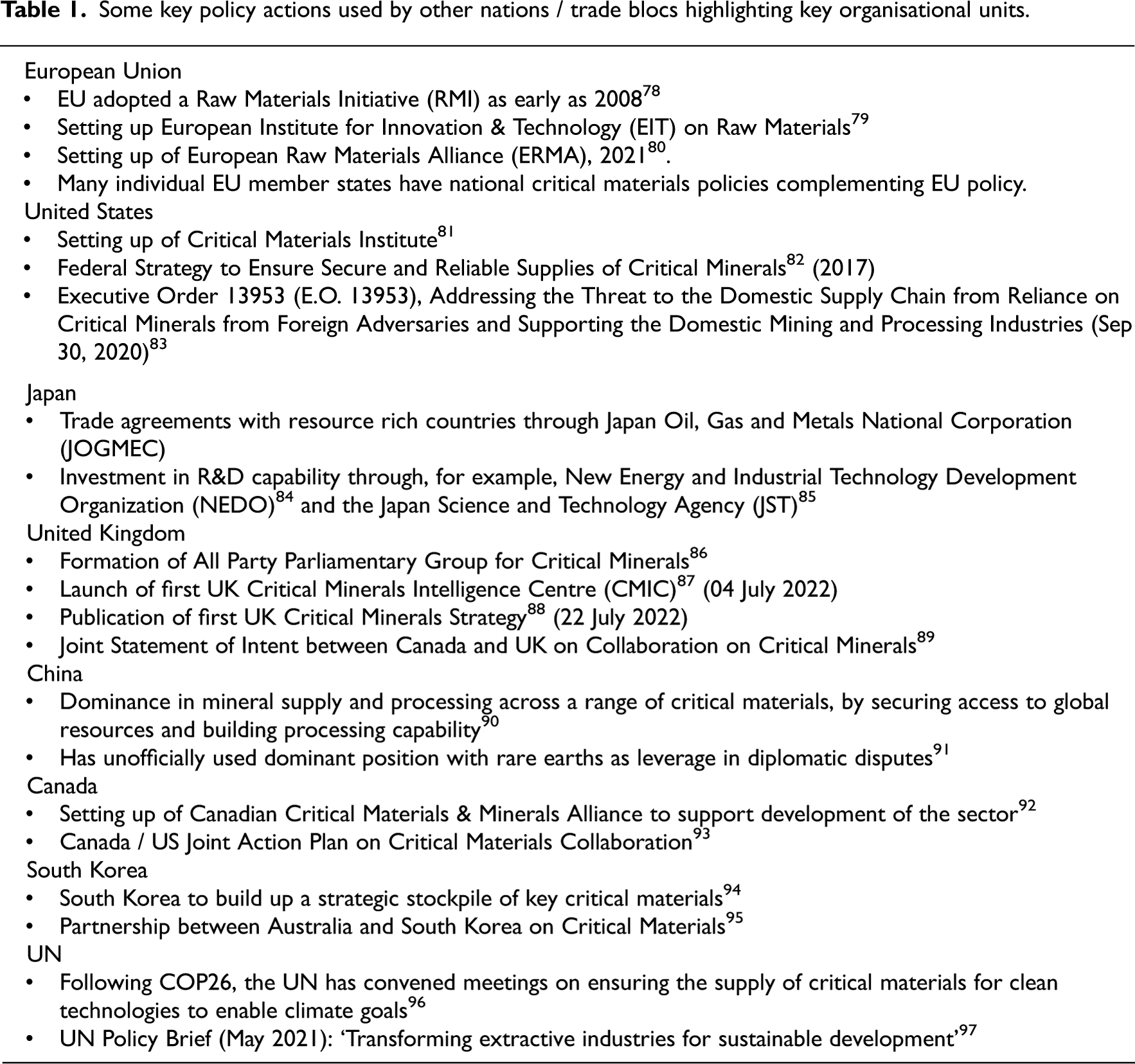

However, there is a risk that the UK will fall behind in the race to secure critical materials, as it competes against other larger, more powerful, nations and economic blocks with mature and established policy and governance structures in this area. The UK has released its Critical Minerals Strategy in 2022 and is in the process of establishing the attendant infrastructures to support the delivery of this strategy. States and regional bodies in many other parts of the world have already created institutions and governance bodies to conduct concerted research and development for building the socio-technical infrastructures to address challenges of materials criticality. The table below contains some examples of measures taken across a range of jurisdictions in recent years (however, this is by no means an exhaustive list) Table 1.

Some key policy actions used by other nations / trade blocs highlighting key organisational units.

Finally, social interventions and circular business models are crucial to reduce our demand for critical materials. A proportion of our technology metals demand will be needed for the energy transition, but some demand could be mitigated through better-informed user interventions. This will in the first instance require raising public awareness about critical materials and how they are key to achieving net zero targets. More importantly, consumer habits will need to change through more functional use of products containing critical materials and more accessible recycling schemes for consumers. This will require putting in place a range of regulatory approaches through various product and quality standards and softer approaches through information policies and voluntary schemes that should inform consumers when making their purchase choice and encourage eco-management scheme attractive for large polluters. Currently this demand management is absent from the UK Strategy.

Footnotes

Author note

David Peck is currently affiliated with Delft University of Technology.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

This study was (part) funded by the UK Research and Innovation (UKRI) Interdisciplinary Circular Economy Centre for Technology Metals (Met4Tech) (EP/V011855/1).

This study was (part) funded by the UK Research and Innovation (UKRI) Interdisciplinary Circular Economy Centre for Technology Metals (Met4Tech) (EP/V011855/1).

1.

L. Grandell, A. Lehtila, M. Kivinen, T. Koljoen, S. Kihlman, L.S. Lauri, ‘Role of Critical Metals in the Future of Green Technologies’ (2016) 95 Renewable Energy 53–62.

2.

3.

4.

5.

Ibid. at 237.

6.

7.

8.

In this article, we largely use the term ‘Critical Metals’ as the supply of these is the focus of our concern; however, ‘critical materials’ is a broader umbrella term that also encompasses critical minerals and metals.

10.

See ‘Access to Critical Materials’ above n. 7.

11.

12.

Ibid.

13.

See HM Government, ‘Resilience for the Future’ above n. 6.

14.

15.

International Energy Agency, ‘The Role of Critical Minerals in Clean Energy Transitions’ above n. 3.

16.

17.

18.

P. Alves Dias., S. Bobba., S. Carrara, B. Plazzotta, ‘The Role of Rare Earth Elements in Wind Energy and Electric Mobility’ (2020) EUR 30488 EN, Publication Office of the European Union, Luxembourg, ISBN 978-92-79-27016-4. Available at: doi:10.2760/303258, JRC122671 (last accessed 27 November 2021).

19.

20.

21.

22.

23.

24.

25.

See D. Ainalis et al. above at n. 2.

26.

J. Acton and others., ‘Addressing the Climate Challenge’ (University of Birmingham, September 2021). Available at: DOI: 10.25500/epapers.bham.00003451 (last accessed 16 February 2022).

27.

International Energy Agency, ‘The Role of Critical Minerals in Clean Energy Transitions’, above at n. 3.

28.

See Y. Liang above n. 24.

30.

Not just Carbon Dioxide CO2, but also other greenhouse gases including Methane CH4, Nitrous Oxide NO, Chlorofluorocarbon-12 (CFC-12) CCl2F2, Hydrofluorocarbon-23 (HFC-23) CHF3, Sulphur Hexafluoride SF6, Nitrogen Trifluoride NF3).

31.

32.

33.

Ibid. at 4.

34.

Ibid. at 5.

35.

See for example Communication from the Commission to the European Parliament, the European Council, the Council, The European Economic and Social Committee and the Committee of the Regions: The European Green Deal, COM/2019/640 final.

36.

See HM Government, ‘Ten Point Plan’, above n. 32 at 8.

37.

Ibid. at 8.

38.

See P. Alves Dias et al. above n. 18.

39.

40.

See HM Government, ‘Ten Point Plan’ above n. 32.

41.

See ‘Access to Critical Materials’ above at n. 7.

42.

See HM Government, ‘Ten Point Plan’, above n. 32 at 10.

43.

See HM Government, ‘Net Zero Strategy’, above n. 4.

44.

Ibid. at 235.

45.

Ibid. at 237.

46.

47.

HM Government, ‘Resilience for the Future’, above n. 6.

48.

The asterisk has been used to denote a significant opportunity for UK domestic primary production.

49.

HM Government, ‘Resilience for the Future’, above n. 6.

50.

51.

See P. Alves Dias et al., above n. 18.

52.

See Houses of Parliament, ‘Access to Critical Materials’, above n. 7.

53.

BBC News, Cornwall Lithium Deposits 'Globally Significant' (17 September 2020). Available at: https://www.bbc.co.uk/news/uk-england-cornwall-54188071 (last accessed 09 May 2022); National Geographic, In Cornwall, ruinous tin and copper mines are yielding battery-grade lithium![]() (last accessed 9 May 2022).

(last accessed 9 May 2022).

54.

55.

56.

57.

See Financial Times, above n. 55.

58.

See HM Government 'Resilience for the Future’ above n. 6.

59.

P. Alves Dias et al., above n. 18.

60.

61.

62.

63.

64.

See Alves Dias et al. above n. 18.

65.

Regulation (EU) 2023/1542 of the European Parliament and of the Council of 12 July 2023 concerning batteries and waste batteries, amending Directive 2008/98/EC and Regulation (EU) 2019/1020 and repealing Directive 2006/66/EC, PE/2/2023/REV/, OJ L 191, 28.7.2023. Available at: EUR-Lex - 32023R1542 - EN - EUR-Lex (europa.eu) (last accessed on 10 September 2023).

66.

D. Thompson, C Hyde, JM Hartley and others, 'To Shred or Not to Shred: A Comparative Techno-Economic Assessment of Lithium-Ion battery Hydrometallurgical Recycling Retaining Value And Improving Circularity In LIB Supply Chains’ (2021) 175 Resources, Conservation and Recycling 105741.

67.

68.

L. Gaines, ‘The Future of Automotive Battery Recycling: Charting A Sustainable Course’ (2014) 1–2 Sustainable Materials and Technologies 2, at 6.

69.

70.

Ibid.

71.

72.

See HM Government, ‘Resilience for the Future’, above n. 6.

73.

Ibid.

74.

Ibid.

75.

76.

77.

A. Walton, P. Anderson, G. Harper et al, ‘Securing Technology-Critical Metals for Britain’ April 2021, University of Birmingham, Birmingham Centre for Strategic Elements & EPSRC Critical Materials & Critical Elements and Materials (CrEAM) Network 2021. at 13.

87.

above, n. 46.

88.

see above, n. 6.