Abstract

Plastics have become an indispensable part of our daily lives. From food packaging to advanced medical applications, life in the 21st century would not be the same without them. The exponential increase in the production and use of plastics does, however, have significant negative environmental impacts that range from emissions and other pollution associated with the production of plastic, through to the impacts of improper disposal and direct leakage on the environment. The plastic packaging tax (PPT) was introduced in the UK in 2022, with the aim of providing a clear incentive for businesses to enhance a circular plastics economy by using recycled materials in production processes, as well as to motivate businesses to consider climate impact at every stage of the product lifecycle. This paper exposes some of challenges associated with the application of the PPT while proposing several policy options as to how to best address these challenges.

Keywords

Background

Plastics have become an indispensable part of our daily lives. From food packaging to advanced medical applications, life in the 21st century would not be the same without them. The exponential increase in the production and use of plastics does, however, have significant negative environmental impacts that range from emissions and other pollution associated with the production of plastic, through to the impacts of improper disposal and direct leakage on the environment. Single-use plastic packaging represents approximately 40% of plastics produced and hence interventions that can reduce the volume of virgin plastic that is used in these applications and help drive towards a circular economy are highly desired.

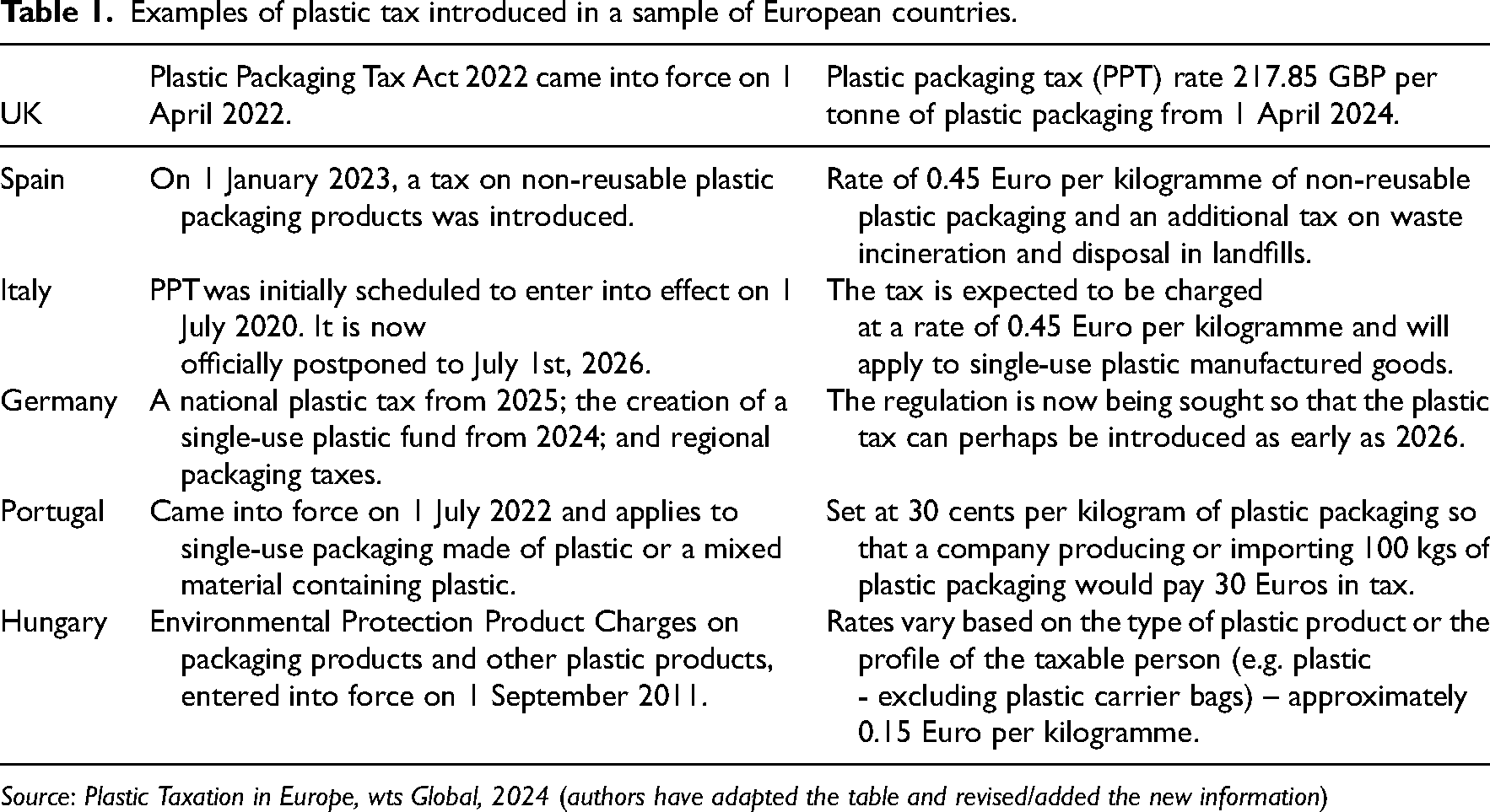

The plastic packaging tax (PPT) was introduced in the UK in 2022, with the aim of providing a clear incentive for businesses to enhance a circular plastics economy by using recycled materials in production processes, as well as to motivate businesses to consider climate impact at every stage of the product lifecycle. Similar tax arrangements have been introduced in other European countries (see Table 1), coupled with other measures such as extended producer responsibility (EPR) schemes which, in countries such as Hungary and the Netherlands, include heightened fees built into the EPR system where the plastic packaging is non-reusable. Note that there are important variations in the schemes currently applied in different countries. For example, in the UK, plastic packaging that contains at least 30% recycled plastic is exempt from tax, whereas in Spain, for example, all of the non-recycled content is subject to tax. Although this would seem to provide a stronger incentive to use recycled plastics, as we explain below, whether this is so depends on the availability and market price of recycled plastic.

Examples of plastic tax introduced in a sample of European countries.

Source: Plastic Taxation in Europe, wts Global, 2024 (authors have adapted the table and revised/added the new information)

The taxation of plastic packaging has faced challenges arising from diverse origins, including external factors such as pricing (for instance through competition with low-cost virgin materials) and inadequate supply of recycled content. In addition, there are considerable difficulties surrounding compliance and verification. This brief contribution exposes some of these challenges while proposing several policy options as to how to best address these challenges. Before exploring these questions and potential solutions, the paper briefly discusses the available taxation models to address reduction of plastic pollution by reference to the point at which the tax is levied.

Available taxation options

Policymakers have a number of taxation models available to address plastic packaging; each carrying its own advantages and disadvantages. There are three main options that could be deployed to address plastic packaging. The first option, currently adopted in the UK, entails taxing materials at the point at which they are utilised, which for plastics is as they enter first use (at the industrial rather than consumer level). This model attempts to reduce virgin product by encouraging packaging containing recycled plastics. There are positive and negative consequences associated with this option. It could increase business overheads at least in the short term, so that the UK would need to consider the trade implications and review what competitor countries are doing in this space (see Table 1). On the other hand, the tax may have the effect of encouraging research and development into secondary plastics or alternative packaging materials. Stimulating the growth of the recycling sector in this way may be advantageous to the UK in a global market for recycled plastics. This objective behind the tax may lead to a switch away from plastic, but this switch may not necessarily be to more sustainable types of packaging but, for example, to packaging the production of which generates a much higher carbon footprint, so transitions in production will need to be monitored and assessed.

The second option is a tax on consumption. This tax could be applied at the point of purchase of consumer goods which are packaged using non-recycled plastic. There are however some difficulties here related to consumer choice i.e., are non-plastic options available that would allow consumers to avoid the tax? If not, there is little consumer incentive to change, and whilst the tax may raise some revenue., it risks doing so without reducing plastics in circulation. There are further complexities. VAT is the ordinary consumer tax and changes to PPT could clash with this. One option would be to implement a rise in VAT on plastic-packaged goods and reduce it if more sustainably packaged, however this would be hard to effectively track and administer. Moreover, defining what constitutes a more sustainable option and even what might constitute a plastic in this context could prove challenging.

Finally, the third option involves taxation at the point of disposal. It is possible to levy tax at the point of disposal, as happens with landfill tax, which might need, in this case, to be extended to include other disposal options such as incineration, since the fate of much plastic packaging is in energy from waste (EfW) installations. This leads to complexity as to what is a disposal option and what amounts to recovery. It raises the question of whether incineration in a waste-to-energy plant amounts to an exempt recovery operation, or would it attract tax, and, if so, at what rate? Such taxes target the end of the plastic waste pipe and while they might lead to more recycling, they do not tax plastics in circulation until the end of life and may therefore have little effect on minimisation of plastic usage. One significant question concerns who would be liable for a plastic disposal tax since one would not wish to provide disincentives to collecting plastic packaging waste. If the burden is put on (say) householders, in order to avoid tax, other even less sustainable solutions may be taken to avoid tax—such as fly tipping or open burning of waste.

All of the above options involve complex interplays and potential consequences. The above consideration of the available taxation options strongly suggests that, at present, retention of tax levied on production, as adopted by PPT, constitutes the most efficient policy solution. Nonetheless, ongoing review of policy options can help ensure that the most efficient and effective tax structures are pursued, particularly because strategies of tax avoidance may create a dynamic policy environment. This may mean that the application of the tax can be refined and improved over time. There are good reasons to calibrate the tax carefully: to ensure that supply of recycled plastic can meet demand; to encourage greater use of recycled content; and to ensure better implementation and recovery of the tax. All these steps would greatly increase the effectiveness of PPT. The following section reviews the immediate challenges associated with the current UK tax approach (PPT) and how these might be addressed in order to refine and improve the existing approach to the taxation of plastic packaging.

Challenges associated with the current tax

PPT requires persons liable to be registered for the tax, provided they meet the following prescribed requirements:

“expect to import into the UK or manufacture in the UK 10 tonnes or more of finished plastic packaging components in the next 30 days; have imported into the UK or manufactured in the UK 10 tonnes or more of finished plastic packaging components in the last 12 months”.

1

The environmental benefits of PPT are many-fold. First, beyond the reduction of plastic waste entering the environment where it may cause environmental and human health concerns, retaining polymeric carbon as polymeric carbon is also beneficial as it reduces the demand for raw materials and energy inputs, and pollution associated with the extraction of raw materials and manufacturing of virgin plastics. 2 Secondly, whilst incineration of used plastic, or conversion into chemicals for fuel will release that energy and provide useful byproducts, downstream more energy and raw materials must be invested into the manufacture of new replacement plastic. This suggests that while incineration combined with EfW is a convenient method for the disposal of waste, it is less efficient than recycling and likely to create greater externalities. Finally, PPT may lead to a reduction in plastics’ consumption, and to better adoption of reuse strategies in food transport and packaging, which will lead in turn to lower levels of demand and use of virgin plastic through a longer lifetime of use. The intention of PPT and related policies is to encourage the use of recycled content, however, it is currently only achieving limited success in this regard.

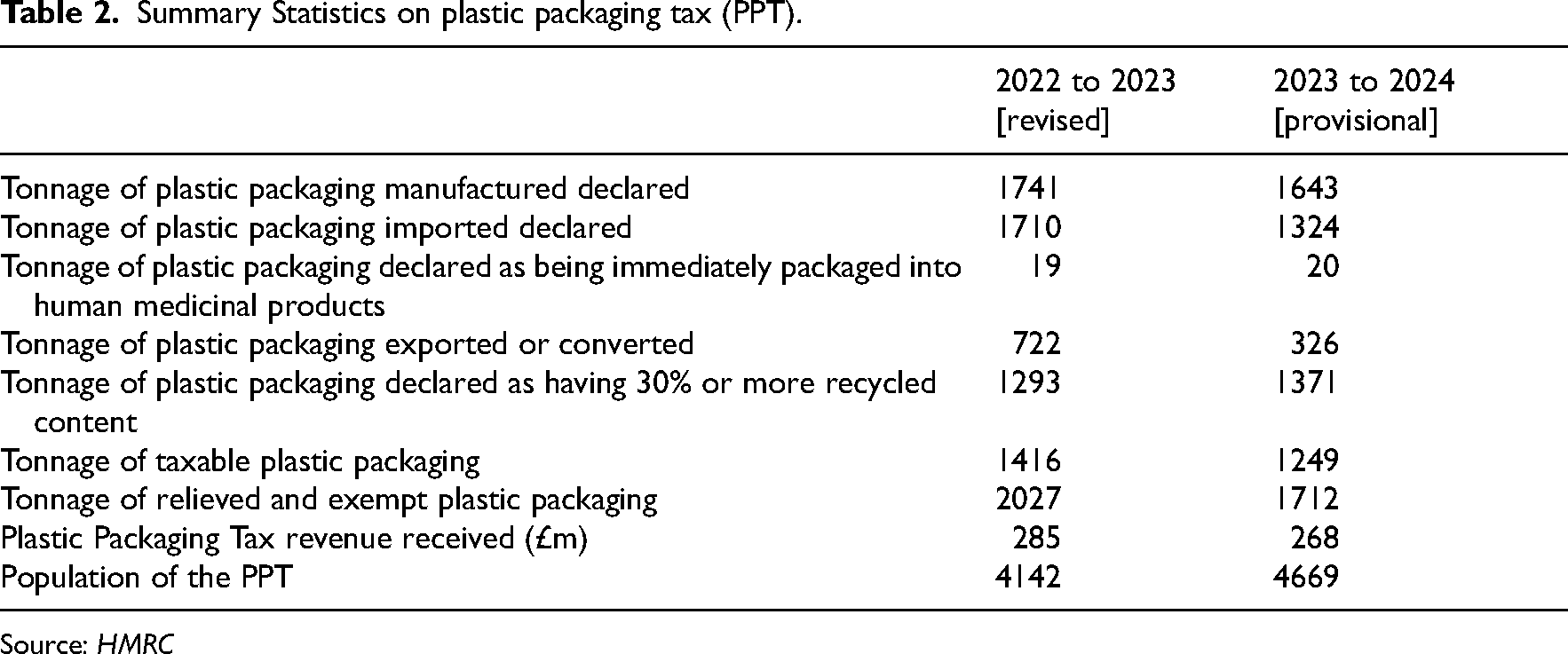

According to HMRC, as of July 24, 2024, there were 4669 businesses registered for PPT, an increase from 4142 registered at the time the previous year's data was released. 3 This is considerably less than an expected 20,000 manufacturers and importers of plastic packaging suggesting that businesses are unaware of the scope of the tax. 4 This is a persistent problem in registration schemes as evidenced by EPR regulations. 5 For example, in 2024, Budweiser Budvar was found never to have registered as a packaging producer in spite of 18 years of beer sales in the UK. 6

HMRC statistics also show that there is a 6% reduction of the generated revenues of PPT from £285 million in 2022–2023 to £268 million in the year 2023–2024. 7 This difference indicates that the total volume of plastic packaging produced and imported into the UK declined over the past year. An estimated 5 million tonnes of plastic is used in the UK every year, of which almost 2.25 million tonnes consists of packaging. 8 It is worth bearing these figures in mind when reading the summary statistics on PPT in Table 2. As for imports, these decreased from 1710 tonnes in 2022–2023 to 1324 tonnes in the most recent year. Moreover, the volume of plastic packaging containing 30% or more recycled plastic has increased in real terms, rising by almost 6% from 1293 tonnes to 1371 tonnes. This suggests that PPT may be having some early impact, though compliance with recycling targets will drive down the levels of tax take.

Summary Statistics on plastic packaging tax (PPT).

Despite this indication of early impact, a number of key challenges remain. First, pricing is crucial to the success of PPT. The price of recycled plastic is on the rise and prices of virgin and recycled plastics are generally volatile in part due to the overheads of collection, energy, and treatment of used plastics. Global market trends have a significant impact on prices of virgin plastic, so the availability of recycled plastic is not entirely within the control of the UK. If the cost of recycled plastic rises beyond that of its virgin equivalent, then companies may choose to revert to virgin plastic and pay the tax. This may necessitate raising the tax on virgin plastics until a balance is reached between supply and demand. Moreover, as industries have moved from the use of virgin materials to products that contain a minimum of 30% recycled, the availability of recycled plastic materials has become incredibly tight. The British Plastics Federation (BPF) suggests that around 28% of the plastic packaging used in the UK is then recycled in the UK. 9 Despite the amount of plastics recycling increasing over time, there is not enough recycled plastic to meet demand. Of note is the fact that the UK does not have adequate reprocessing capacity to produce the necessary amount of recycled plastic to respond to the shortfall and meet the demand, 10 making it more cost-effective to use virgin materials and absorb the tax impact. In this scenario, sustainable behaviour is not incentivised and there is insufficient evidence of the necessary behavioural change strategies required to improve circularity of plastics packaging. This is true across all businesses, and in relation to a wide range of activity including possibilities of collection in the store and the return of plastic packaging. There is significant appetite from various stakeholder groups for money raised by HMRC and the PPT, to be reinvested into UK recycling and waste management, since it is not currently hypothecated. Comparatively, in EU Member States, moneys collected at a member state levy are then paid over to the EU budget to meet the EU Plastics Levy. 11

Second, defining plastic plays a key role. PPT is broadly applied to plastic packaging, in which plastic is defined as a polymer material to which additives and substances may have been added. The only notable exemptions relate to cellulose-based polymers that have not been chemically modified. Compostable, biodegradable, or oxo-degradable plastics are specifically included in the definition of plastic. 12 If the tax is expanded beyond packaging to other single-use plastics (as is proposed in some EU countries, see Table 1) the lack of exemption for compostable and biodegradable plastics could affect areas where single-use is unavoidable and there are limited options for replacement, and sometimes no option to recover for recycling (i.e., food waste bags). Moreover, PPT is agnostic to the source of the polymer, i.e., fossil- and bio-sourced plastic are treated equally. While most fossil-derived plastics can be manufactured from bio-based starting materials, their end-of-life fates remain the same. Nonetheless, without well-thought-out exemptions, PPT could potentially stifle innovation of environmentally beneficial solutions to the wider plastics sustainability challenge.

Third, there are potential unintended consequences of taxation, in the form of negative externalities, which need to be considered, (e.g., bans on disposable plastic shopping bags leading to rise in use of thicker plastic bags). 13 End users of plastic packaging will likely incur some or all of the PPT indirectly as suppliers are likely to pass on a significant portion of the extra costs from the tax to consumers, pulling against the intention of PPT to reduce the quantity of virgin plastic being used. Equally, there is a danger of regrettable substitution, moving to products which have potentially worse environmental and health impacts than plastics, such as paper straws coated in materials containing Per- and polyfluoroalkyl substances, to avoid taxes and levies on a specific material i.e., plastic. 14

Fourth, the wider compliance framework faces several challenges. Firstly, the current verification/certification system that confirms whether a package contains the required 30% recycled plastic is not robust 15 and has the potential to create more difficulties, particularly for SMEs. 16 Related to this are challenges in recording necessary data that form part of the certification process. Data management may create substantial administrative headaches for businesses and supply chains. Some businesses already choose to outsource reporting duties which may be resource efficient but is not resource free. The certification challenges are also linked closely to the point of enforcement as there are concerns that the existing model of verification has a knock-on effect on compliance. 17 A lack of monitoring of imported plastic packaging and recycled feedstock may ultimately lead to fraudulent claims and could disadvantage British business.

Fifth, PPT may need to take into account the regulatory limitations that restrict the use of recycled content, for instance, where certain types of plastic packaging are essential in the food sector, in terms of product safety, quality, and shelf life. 18 On the other hand, under the UK's EPR programme, businesses are likely to be accustomed to covering the costs of collecting and recycling their packaging and are well versed in the possibility of eco-modulation fees for less sustainable options. 19

Ways forward for the PPT?

PPT has been levied in the UK for the last two years and it has a wide remit in applying to plastic packaging manufactured or imported to the UK. As expected, PPT has faced some challenges in its early implementation, and it becomes imperative to keep possible revisions to the tax under review. This is supported by data generated since the launch of the PPT. For example, data from the BPF indicates that many UK recyclers experienced a decline in sales in 2023 compared to 2022. If the use of recycled materials in packaging is indeed rising, this suggests that the materials are either being diverted from other sectors or imported. Thus, the BPF concluded that the current legislation is not effectively reducing plastic waste. As a result, some organisations such as BPF are calling for changes to the tax to help the legislation meet its original objectives. 20

We argue that moving forward PPT should achieve three main objectives. First, to focus on encouraging the use of recycled content and preventing regrettable substitution. To achieve this, despite the different taxation models explored here, we consider it advisable to retain the current system of one taxation method where materials are taxed at the point of first utilisation or, in the case of plastics, as they first enter use (at the industrial, rather than consumer level). However, it would be beneficial to consider taxing all packaging based on their respective environmental impacts rather than just focusing more generically on plastic packaging. Bearing in mind some challenges faced by certain sectors such as the food industry, the PPT rate and recycled content threshold should be kept under annual review on a sectoral basis to ensure the tax delivers its objective. One might attempt to generate a sliding scale of taxation to link the rate of tax to the price of virgin or recycled plastic to remove the volatility and uncertainty with defined inflection points to encourage adoption of recycled content over virgin plastics. Whether or not this could be fully achieved, it may prove necessary to periodically raise tax on virgin plastic, in addition to any changes for CPI-based inflation, 21 to ensure that a balance is reached between available supply of and demand for recycled polymer.

Second, to improve mechanisms for the assessment of PPT to encourage uptake and to create a level playing field for UK producers. Achieving this would involve several measures starting with the reconsideration of reporting requirements that, depending how they are implemented, may either reduce or increase administrative and compliance challenges for SMEs. This is closely linked to a more robust certification system which would remove the burden of complex reporting based on due diligence obligations. A better option would be some centralised standard to validate the recycled content in packaging. It is worth considering certification models in different jurisdictions, such as the Spanish model or deployment of Recycled Content Verification System as proposed by the BPF, together with RECOUP 22 . Another aspect related to this is the need for robust scrutiny of imported plastic packaging, including packaging imported as part of goods. 23 This needs to be coupled with a further refinement of accountability/penalty mechanisms for non-compliance. 24 Canada, for example, considers the possibility of prohibiting non-compliant companies from engaging in public procurement tendering. 25

Thirdly, stimulating the green economy through the creation of more recycled content. One way to achieve this is to apply mass balance accounting 26 when calculating the recycled content of chemically recycled plastic which was recently approved by the Government 27 . As it was noted earlier, the UK needs to build adequate reprocessing facilities which might require innovation funding and cooperation between business and research institutions. This comes at a time when the new Government has just concluded a consultation on a new Industrial Strategy ‘Invest 2035: the UK's Modern Industrial Strategy’ which commits to facilitating economic growth and green transition. 28 To that end, the Strategy is branded as pro-business by engaging with complex issues relevant for that sector including driving and supporting infrastructure and research development which are key in more effectively reducing and recycling plastic.

Conclusion

To conclude, these policy recommendations have a significant role in furthering refining the UK PPT which has already proved effective in achieving its main objective of reducing the demand for virgin plastic. However, further refinement is required to ensure that UK PPT is achieving its goals. PPT is one taxation method within a suite of other policy and incentivisation measures. The way in which these measures work together to deliver their goals, alongside ensuring UK business competitiveness is important to the long-term success of PPT. These measures include, but are not limited to packaging EPR, packaging recovery notes (PRN/PERN) and the emissions trading scheme. Of course, the ultimate success of the PPT should lead to it becoming largely obsolete as the market moves towards the recovery and use of recycled plastic content. In this way, a successful PPT would present an example of how a taxation method could help to move a market towards a more sustainable and circular economy that can be applied to plastics, and other materials, in other sectors of the economy; thus promoting sustainable options in while promoting innovation of environmentally beneficial packaging solutions for the future.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.