Abstract

Informal care is often accompanied by a reduction or abandonment of professional activity by the caregiver. Therefore, caregiving may be associated with a lower pension for the former caregiver than for people without care obligations. There is a large gender difference in informal care responsibilities, and this may contribute to the gender pension gap. As the impact of care-related labour market decisions depends on the design of the pension system, we carry out a cross-country comparison, in which we analyse the impact of care obligations in countries with high (Luxembourg), middle (Liechtenstein, Belgium, Portugal) and low (Slovenia) gender pension gaps. Using typical-case simulation models, we examine how the impact of care-related events is mediated by pension rules, given women's labour market decisions. To what extent does working part time or interrupting one’s career at the age of 30 or 54 reduce the later pension benefit? How are these losses mitigated by pension credits that are conditional on caregiving? We find that the mitigating effects are generally strongest in Belgium, followed by Luxembourg and Slovenia. Such credits hardly exist in Portugal, while in Liechtenstein they have only a small impact. However, the consequences of either working part time or interrupting work can also be mitigated via general rules in the system that are unrelated to caregiving (such as in Portugal and Liechtenstein). They can, on the other hand, be aggravated by the existence of higher accrual rates for individuals who extend their careers, as in Luxembourg and Slovenia.

Introduction

About 44 million adults in the European Union (EU) (12% of the adult population) frequently care for a disabled or infirm family member, neighbour or friend more than twice a week (Eurofound, 2020: 7). Women are more likely than men to provide informal care and they provide more hours of informal care (OECD, 2020: 3). In the EU, 59% of adult informal carers are women, a figure which ranges from 52% in Germany to about 65% in Poland, the Czech Republic and Lithuania. The gender difference is especially large in the 45-64 age group where, in most Member States, between 10% and 30% of men and between 20% and 40% of women provide informal care (European Commission and Social Protection Committee, 2021a: 75).

Since informal care is unpaid, yet often occurs over a long period of time and can be physically and mentally demanding, it is often accompanied by a reduction or abandonment of professional activity by the caregiver (Ciccarelli and Van Soest, 2018; European Commission and Social Protection Committee, 2021a; Evandrou and Glaser, 2003; Heitmueller, 2007; Henz, 2004), a lower probability to re-enter employment (Ehrlich et al., 2020), lower future and lifelong earnings and lower-status occupations (Budig and England, 2001; European Commission and Social Protection Committee, 2021a; Gash, 2009; Van Houtven et al., 2013). Care for young children is also associated with a reduction in working hours or an interruption of employment for mothers (Hofman et al., 2020). In most EU countries, the pension received during retirement is a function of past labour market income and some social insurance benefits. As care-related effects on wage income accumulate over the life course, caregiving may be associated with a lower retirement income compared to that of people without care obligations (Fasang et al., 2013; Möhring, 2018). Therefore, the unequal distribution between genders of informal care responsibilities contributes to the gender pension gap (Bettio et al., 2013), and could also be a factor in the higher poverty risk of older women compared to older men (European Commission and Social Protection Committee, 2021b: 30).

Demographic ageing is likely to exacerbate these issues. In many EU countries, the demand for care will increase in years to come (Eurofound, 2020). If the supply of formal care work does not keep pace with population ageing, there may be pressure on women to take up even more informal care tasks than today (see also Eurofound, 2020).

Acknowledging the importance of informal care tasks, many countries have created compensating ‘care credit’ schemes for those who reduce their paid work to take up temporary care work. These schemes can provide a replacement income but can also partially compensate for the impact of reduced earnings on the later pension (Frericks, 2011; Pfau-Effinger, 2012). However, there is little evidence concerning the impact of these credits on the later pension.

To fill this gap, we use typical-case simulations (i.e. of hypothetical female individuals) to simulate the impact of taking up caring for a child (at age 30) or an older relative (at age 54). We distinguish between scenarios where caregiving results in part-time work and scenarios where it involves a full interruption of the carer’s career, both for an assumed period of six years. In the case of a full career break, we also assume that future wages are lower than they would be if the person had continued full-time work – i.e. there is a wage penalty.

We compare the impact of care activities in five European countries: Belgium, Liechtenstein, Luxembourg, Portugal and Slovenia. Teams from these countries took part in the EU-funded research project MIGAPE (MIGAPE, 2021). The primary criterion for the choice of countries within MIGAPE was that the country team should have a microsimulation model at its disposal. These countries cover only a small proportion of the European population, but as the purpose of this paper involves a comparison of pension systems, the main consideration is that there is variation in these. While Belgium, Luxembourg, Portugal and Slovenia all have Bismarckian pension systems, they differ in important respects (see the third section of this paper and European Commission and Ageing Working Group, 2021). The Liechtenstein pension system (very similar to the Swiss one) 2 is an interesting case because of its specific multipillar nature, with a highly redistributive Beveridgean first pillar and private funded pensions in the second pillar. 3 Arguably, even more important for this article is the fact (revealed in this study) that the countries vary considerably in the way they mitigate (or do not mitigate) the pension consequences of time out of work due to care responsibilities. The variation in systems also shows in their outcomes with respect to gender: the selection includes countries with a low, a middling and a high gender pension gap, and there is also variation in the gender difference in at-risk-of-poverty rates among the elderly (European Commission and Social Protection Committee, 2021b). Of course, as these outcomes reflect past employment patterns, they may turn out to be quite different in future decades.

The remainder of the article is organised as follows. The next section discusses the interplay between informal care activities, pension systems and pension accruals. It includes a brief literature review. In the third section, we present the systems of care compensation benefits, with a particular focus on rules for pension accrual during care activities. The following section describes the methodological approach of the typical-case simulations, while the fifth section is devoted to the presentation of results. The final section concludes.

Informal care activities and the pensions system

The impact of informal care on pension accrual is influenced by the degree to which pensions are dependent on labour market participation, as informal caregivers often reduce or abandon gainful employment. However, this relationship can be mitigated by the presence of redistributive elements within state pension schemes, such as care credit systems. The interplay between public and private pension provisions may also play a significant role (Möhring, 2018).

In many pension systems, including Bismarckian systems but also Beveridgean systems with strong second pillars (as in Liechtenstein), pension levels are a function of a person’s earnings and employment history. This means that interruptions in employment can lead to lower pensions. However, compensation regulations or redistributive elements in the pension system can mitigate the effects of interruptions in employment or reduced contribution payments. This can be done, for example, by basing the pension amount on a limited number of high-earning years (Leitner, 2001), or by specifying fictitious ‘pseudo-earnings’. Furthermore, interruptions or reductions in employment due to care tasks are often compensated for by the granting of care credits (Frericks et al., 2014; Pfau-Effinger, 2012).

Using retrospective data, previous literature analysed the impact of informal care activities or childrearing across the life cycle on the retirement income of current pensioners (Bonnet et al., 2012; Evandrou and Glaser, 2003; Evandrou et al., 2009; Kuivalainen et al., 2020; Möhring, 2018; Veremchuk, 2020). These results capture the complexities of people's lives and the evolving pension systems in which they were insured throughout their working lives. Still, given the changes in pension legislation over the past two decades, it is not clear how informative they are about the impact of current care activities on future pensions. Since later generations of retirees have different education and employment patterns, and have lived in different institutional environments, the relevance of results based on retrospective data may be limited (Sefton et al., 2011).

There are fewer forward-looking studies of the impact of care responsibilities on later pensions. The European Commission's 2021 Pension Adequacy Report (European Commission and Social Protection Committee, 2021b) assesses the impact of three years of childcare on future pensions (for a person starting her working career in 2019) in the form of so-called theoretical replacement rates (TRRs; see also OECD, 2019). Its analysis – limited to childcare activities – is related to our approach, although we do not focus on replacement rates and assess, in addition, the impact of care responsibilities later in life. We also employ more detailed earnings trajectories in our analysis. Halvorsen and Pedersen (2019) use a stepwise analysis to investigate how various components of the Norwegian pension regime, including the child credits system, impact the gender pay gap and general inequality of pension income for one cohort of pensioners. Contrary to our study, the authors do not include tasks caring for elderly people. Frericks et al. (2008) make a detailed comparative assessment of care credits in France and Germany. They, however, do not assess the impact of working part time or interrupting work in the absence of these credit systems.

This study contributes to the existing literature by examining how either childcare at a younger active age, or care for an older adult at an older active age, affects the later pension, allowing for mediating roles of (a) pension rules, (b) women's care-related labour market decisions and (c) varying levels of earnings.

Pension systems and care compensation schemes in various countries

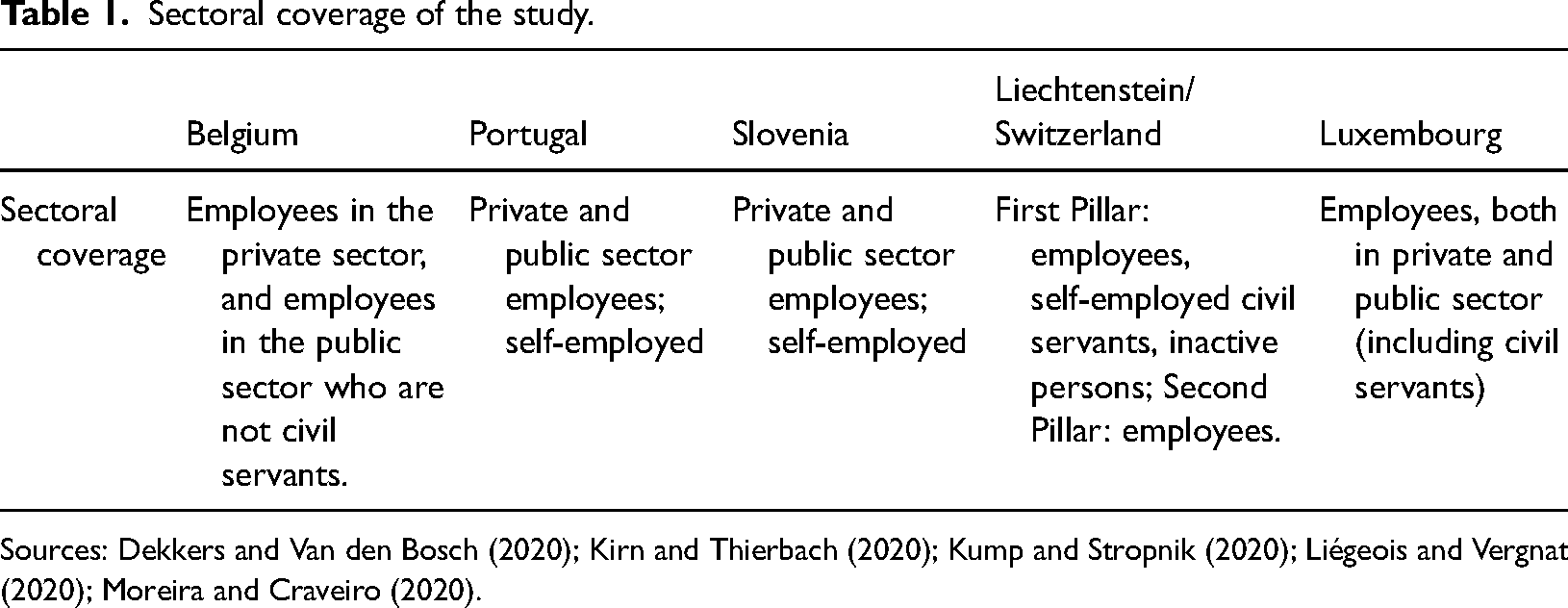

Four of the countries under consideration – Belgium, Luxembourg, Portugal and Slovenia – have Bismarckian pension systems; Liechtenstein has a Beveridgean system complemented by extensive second pillar pensions. Since Beveridgean systems are likely to have a zero or small gender gap in public pensions and a wide gender pay gap in the second pillar, the second pillar is also included in our analysis of Liechtenstein. For the other countries, the second pillar (which is less important) could not be covered due to a lack of data. The statutory retirement age is currently 65 in Slovenia and Luxembourg; it will be 67 in Belgium from 2030 on and is expected to become 69.5 in Portugal, where it is linked to the evolution of life expectancy.

In Belgium, Luxembourg and Portugal, there are different pension schemes for different sectors (Table 1). To simplify the analysis, we considered the modalities of the most prevalent scheme in each country. In Portugal, Slovenia, Luxembourg and Liechtenstein, the general pension scheme covers both private and public sector employees and the self-employed. In Belgium and Luxembourg, civil servants have their own scheme, while in Belgium there is also a separate system for the self-employed. The pension system for new civil servants in Luxembourg is very similar to the general system for employees, so that simulations in Luxembourg describe the system for the private sector and civil servants, but not for the self-employed (who make up about 6% of the work force in 2017)

Sectoral coverage of the study.

Care activities and pension compensation

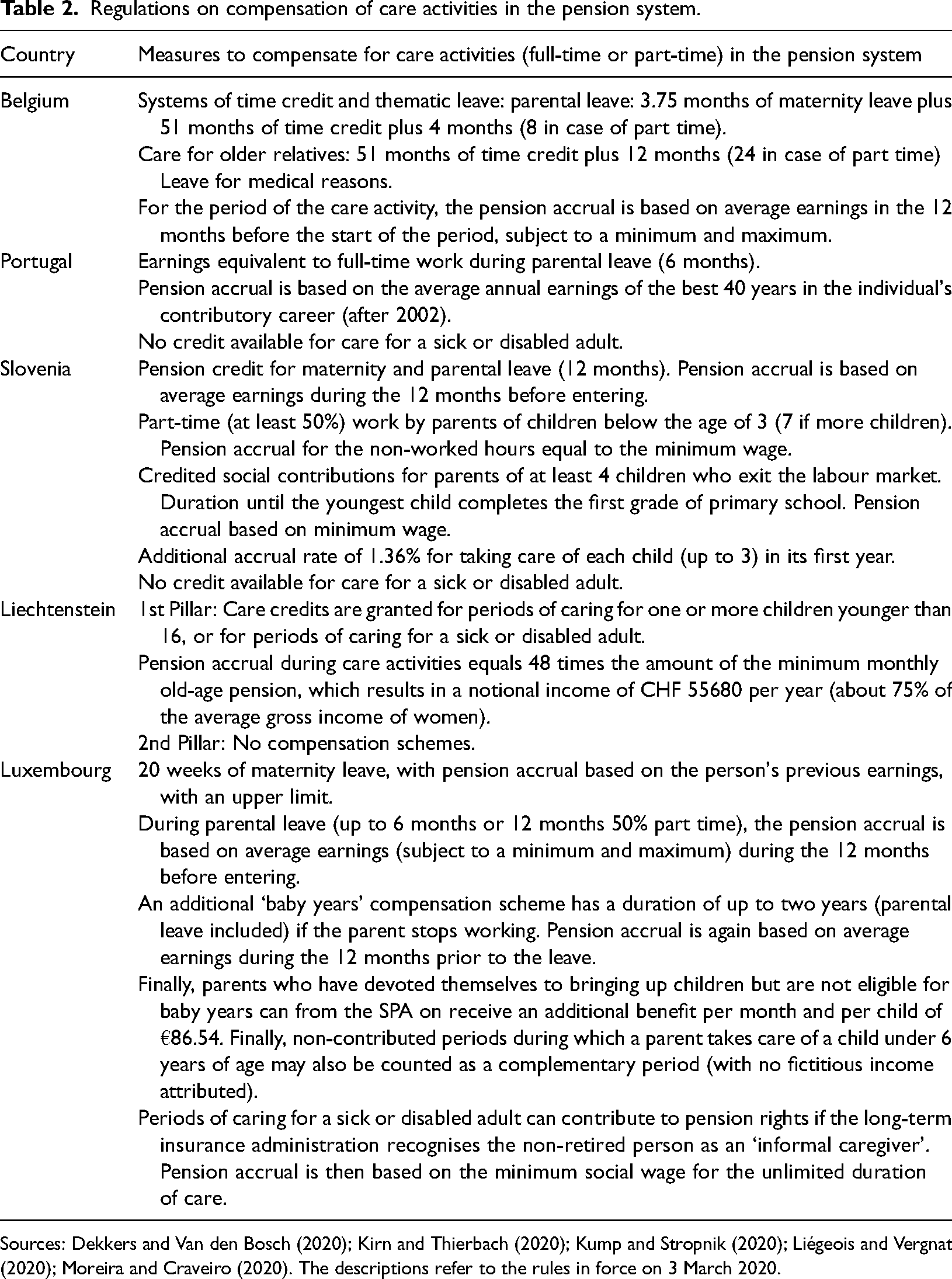

All five countries have policies in place to compensate for lost pension accrual during time spent caring for children, but systems crediting care for older relatives exist only in Belgium, Liechtenstein and Luxembourg, not in Slovenia or Portugal. This, however, does not necessarily mean that taking up these care tasks would result in pension reductions; as we will see later; other, more general, redistributive characteristics of the pension system can take over the role of ‘care credit’ schemes.

The key elements of the care compensation systems are summarised in Table 2. Pension accrual during time off for childcare is covered in all five pension systems. However, there are large differences when it comes to the period for which childcare is covered by pension accrual. It ranges from a maximum of six months in Portugal up to 16 years in Liechtenstein.

Regulations on compensation of care activities in the pension system.

Sources: Dekkers and Van den Bosch (2020); Kirn and Thierbach (2020); Kump and Stropnik (2020); Liégeois and Vergnat (2020); Moreira and Craveiro (2020). The descriptions refer to the rules in force on 3 March 2020.

In Slovenia, part-time work due to childcare (at least 50%) can be compensated for in the pension system for up to two years (in the case of one child below the age of three). In Belgium, the combined time credit and thematic leave systems (including the mandatory maternity leave) provide pension credits for at most four years and 9.5 months in the case of full interruption of work, and five years and 1.5 months if working part time at 50%. In Portugal, compensating care credits are provided for the duration of parental leave, which is six months at most. In Luxembourg, in addition to the 20 weeks of maternity leave, parental leave can be taken: up to six months full time, one year if working part time at 50%, or 20 months if working part time at 80%. Furthermore, an additional compensation called ‘baby years’ can be added to the parental leave up to two years after maternity leave or birth if the parent stops working. If the parent is not working and not eligible for ‘baby years’, childrearing periods can be added to the total career length, as long as the child is under six years of age. Liechtenstein has the most generous system of the five countries in terms of the period for which the credit system applies: child credits are available for up to 16 years, to people both in and out of employment. However, this system only applies to the first pension pillar, while the second pillar of the pension system does not include care credits.

In Belgium, Luxembourg and Slovenia (during the period of parental leave and the ‘baby years’ in Luxembourg), pension accrual is based on the earnings received during the last 12 months, subject to a minimum and maximum. In Luxembourg, childrearing periods only add to the total career length. In Slovenia, in the case of part-time work after the parental leave (second and third year after childbirth), pension credits are based on the minimum wage. 4 In Liechtenstein, the first pillar pension is built up on the basis of earnings and care credits. Since compulsory (albeit small) contributions must be paid in the event of interruptions in employment, there is no loss of contribution years. In Portugal, the pension credits accumulated during parental leave are based on the ‘reference earnings’, equal to the average annual earnings of the best 40 years in the individual's contributory career (since 2002).

In Slovenia and Portugal, there is no pension compensation mechanism in place for caring for a sick or disabled older relative later in working life. In Luxembourg, the long-term care insurance administration can agree to cover the pension contributions (up to a maximum) of a non-retired caregiver who has reduced his/her professional activity to provide care to a dependent person. In this case, no explicit maximum duration of the care credit system is imposed. Likewise, in Liechtenstein, there is a programme to compensate for lost pension contributions for the duration of the care period. In Belgium, the maximum duration is five years and three months in the case of a full career interruption, and six years and three months in the case of part-time work at 50%.

Other relevant aspects of the pension systems

All five countries have minimum pensions in place, which apply in some scenarios. Maximum pension amounts (or assessment bases) also exist in most countries. The exception is Portugal, where, instead, the pension accrual rate decreases for higher wages.

There are several specificities of the pension systems which have particularly important implications for our results. The pension system in Liechtenstein is a two-pillar system. The first pillar is a highly redistributive pay-as-you-go system for old-age, survival and disability insurance. The interaction of several factors ensures a relatively effective compensation for periods of care. First, compulsory contributions prevent contribution gaps in the event of non-employment. Second, childcare credits are granted for a long time (16 years), including to those in employment. Thus, in the case of a temporary reduction in employment, the loss of contributions can be offset, although care credits are not linked to previous income and are fixed at around 75% of the average gross wage for women. Thirdly, income and care credits are revalued comparatively generously when determining the relevant income. As the first pillar is of a Beveridgean character with a fairly low cap on the maximum pension, the maximum pension can also be reached by someone who has had caring responsibilities. However, as the maximum pension from the first pillar is below the level of social assistance, the income from the second pillar is needed to maintain the standard of living. In terms of the average pension, the second pension pillar is far more important than the first pillar. The second pillar is a funded, mandatory occupational pension insurance, and there is no compensation for caring periods. Consequently, a loss of earnings due to caring leads to a lower pension in the second pillar, but not in the first pillar. The differences in simulated pension income are therefore due to differences in second pillar pension income.

In Portugal, the 40 years with the highest earnings are taken into account, so for long careers, years of caring may ‘drop out’ from the pension base calculation and have no impact at all on the later pension. In Slovenia, only the best 24 consecutive years of earnings (indexed annually to the average nominal growth in wages) serve as the basis for the final pension assessment. Still, years of caring have a strong impact on the later pension, because the accrual rate per year is increased for those who work at an older age after a long career. The regular accrual rate of 1.36% per year is increased to 1.5% (for three years at most) for each six months of work beyond the age of 60 with at least 40 years of pension contributions. The implication is that shortening the contributory period (as is done in some of the scenarios presented) for those (otherwise) eligible for this higher accrual rate can have a strong negative impact on their pension outcome. For those not eligible for higher accrual rates, there is still a negative impact on their pension outcome, but it is weaker. The pension system in Luxembourg also provides some degree of bonus accrual to encourage people to extend their working life. In 2020, the earnings-related part of the annual (new) pension is based on an accrual rate of 1.8% of total career earnings. The accrual rate is increased by 0.013 (with a cap of 2.05%) for each year in which the sum of the retirement age and the career length exceeds a specific threshold (94 in 2020). As in Slovenia, this may mean that reductions or interruptions of work early in the career have a negative effect on the pension, disproportional to the loss in total earnings.

Methodology and pension models

We used typical-case simulation (also called standard or model person simulation) to analyse the impact of current institutional settings on future pension benefits (Burlacu et al., 2014). A well-known example of this technique are the prospective theoretical replacement rates (TRRs) published by the OECD (2019) in ‘Pensions at a Glance’. Standard simulations are calculations of income packages (or other outcomes) for a hypothetical individual, solely based on the applicable tax and benefit rules and the characteristics of the individual. The stylised assumptions make interpretation of the results easier but come at the price of limited representativeness. We addressed this issue by simulating several scenarios. The simulations were carried out applying the pension modules of existing microsimulation models, which were used and validated in earlier studies (Dekkers et al., 2022).

Our basic scenarios involved wage profiles for three levels of educational attainment: up to lower secondary education (ISCED 0-2), medium (upper and post-secondary, ISCED 3-4) and higher education (tertiary, ISCED 5+). All scenarios involved individuals born in 2000. These hypothetical persons were assumed to work full time and continuously from the time they leave school until the statutory retirement age (see the previous section), except for the periods of care. The age of entering the labour market and starting the pension accrual differed by educational attainment, varying between 19 and 24. Alternative scenarios were differentiated by a) the kind of care involved (childcare at the age of 30 or care for an older relative at the age of 54) and b) the labour supply response (part-time work 50%, or a complete career break with wage penalty). All interruptions were assumed to last for six years at ages 30 and 54, after which the person resumed full-time work. 5 We furthermore assumed that the person met any eligibility conditions for care compensation schemes, both in terms of employment history and in terms of the relationship to, and characteristics of, the person cared for. These schemes were used to the maximum extent where possible.

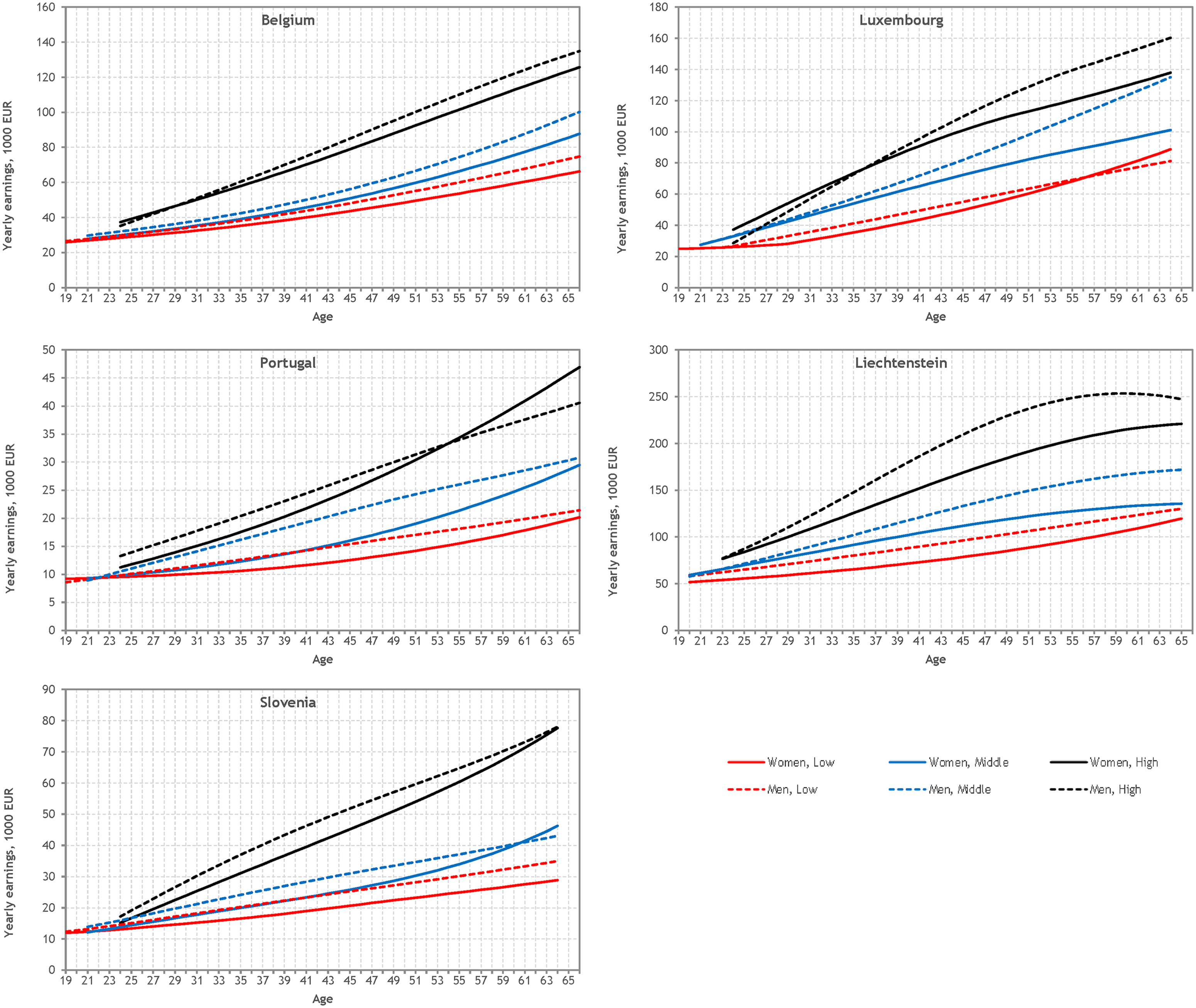

The earnings profiles over the model individuals’ lifetimes were estimated using cross-sectional data for recent years on working women: EU-SILC data for Portugal and Luxembourg and administrative data for Belgium, Slovenia and Liechtenstein. The wage profiles were smoothed by using simulated values from regression equations of full-time equivalent gross earnings for the individual's age and age squared. Separate equations were specified for the three educational attainment levels referred to above. This resulted in three different earnings trajectories for full-time continuous employment, based on education. Finally, these simulated cross-sectional age-earnings profiles were adjusted for real wage growth over the period 2020–2067, using the projections of average wages produced by the Ageing Working Group of the European Council’s Economic Policy Committee (European Commission and Ageing Working Group, 2021). Figure 1 illustrates the estimated and uprated wage profiles, together with, for comparison, those of men.

Projected age-wage curves by gender and level of education of persons born in 2000. Sources: Belgium: Administrative data from the Datawarehouse Labour Market and Social Protection, 2011; Portugal: EU-SILC 2018; Slovenia: Structure of earnings statistics 2016; Luxembourg: EU-SILC 2016; Liechtenstein: 2015 Census and 2016 wage statistics; Amt für Statistik. All graphs are based on own calculations.

Women with a higher level of education start from somewhat higher wage levels than those with low or medium education, and in addition tend to experience much steeper wage growth during their first 20 years in work. This has implications for the relative impact of care activities across earnings trajectories.

The wage curves show income by age in the case of full-time continuous employment. In the periods of caring, earnings are adjusted in proportion to the reduction in working time. After the caring period, earnings are assumed to revert to the original wage curve in the case of part-time work. In the scenarios with a full interruption and a wage penalty, earnings remain below the level they would have reached had there been no interruption.

The above profiles differ from the previous studies discussed earlier. In the theoretical replacement rates, wage profiles are not specified by age, but represent the projected average earnings of the corresponding year. The OECD (2018) does use wage profiles by age, but does not uprate the wages to future years. Hence, their approach is cross-sectional and not prospective, unlike that taken in this study.

Modelling the wage penalty

A so-called wage penalty, also referred to as wage scarring, is an important component of the impact of care responsibilities on the later pension, in addition to the earnings foregone during the period of care. Caregivers may earn a lower wage than men and women without care responsibilities once they return (full time) to the labour market (e.g. Blau and Kahn, 2017; Earle and Heymann, 2012; Van Houtven et al., 2013). Following the birth of their first child, women's wages are markedly lower than those of men; and this effect lasts more than 10 years after the birth (Angelov et al., 2016; Kleven et al., 2019). The wage differences are driven by a loss of job-related skills during career breaks (Budig and England, 2001), a lower accumulation of experience due to fewer working hours or an interruption of employment (Aisenbrey et al., 2009), or by employers’ perception that these workers are less committed to their work (Gregg and Tominey, 2004; Nielsen and Reiso, 2011; Staff and Mortimer, 2012). England et al. (2016) find that highly skilled women, who have a higher rate of return due to experience and a steep wage trajectory, face a higher wage penalty when they lose work experience due to childrearing. The wage penalty – which we model as persistent over the life course – results in lower pension accrual. Moreover, since wages increase most strongly at younger ages, the opportunity cost of caregiving varies over the life course.

In modelling the wage penalty, we assume that during the interruption of employment, the hypothetical person does not accumulate age-specific wage increases, which is equivalent to assuming no gain in experience or seniority. However, the person's potential wage still increases with the average economy-wide growth in wages (e.g. because of collective wage agreements). After the interruption, it is assumed that the wage will increase at the same rate as that of a person of the same age with an uninterrupted career (see Dekkers and Van den Bosch, 2020). 6

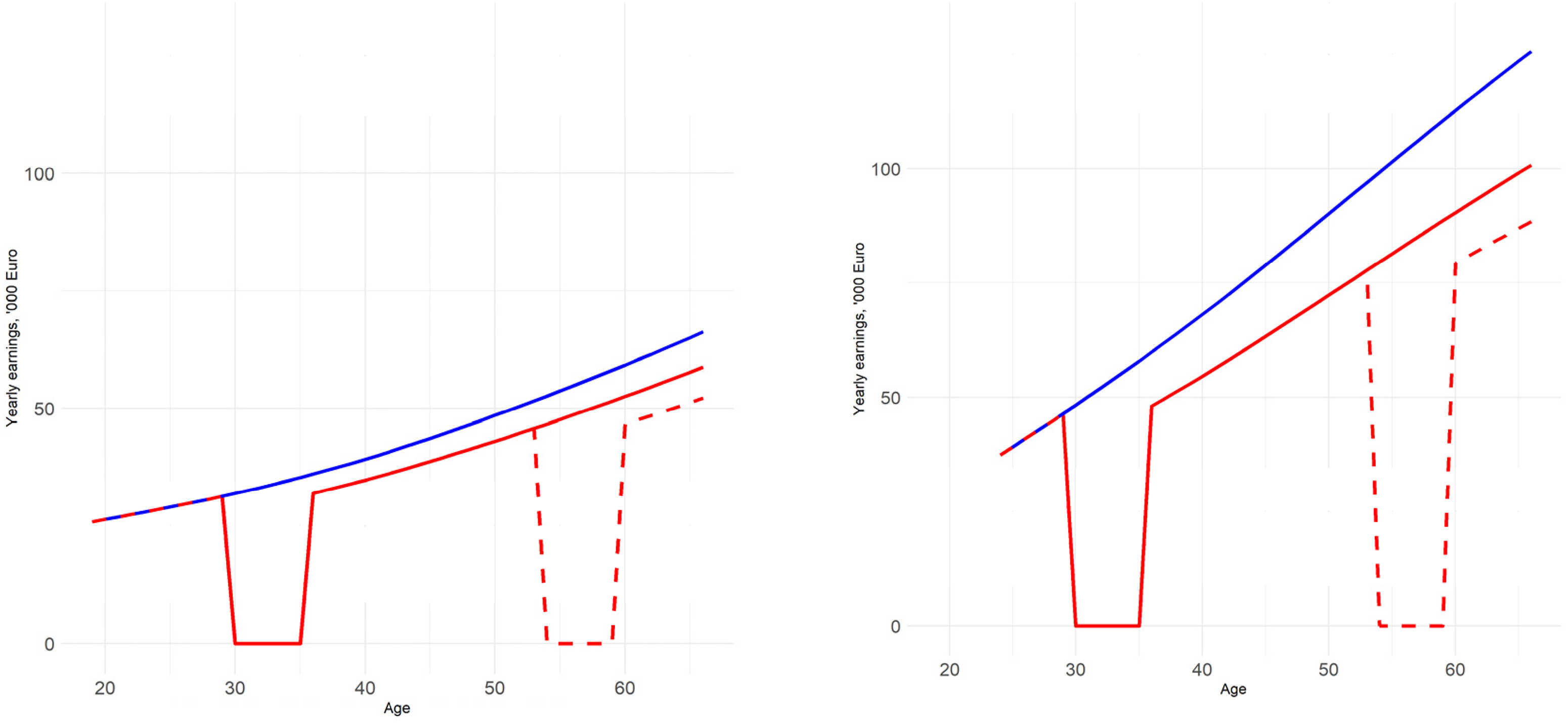

Figure 2 illustrates the impact of the earnings penalty on simulated earnings trajectories in the case of model individuals with low (left-hand side) and high (right-hand side) levels of education in Belgium. The curves indicate the size of the wage penalty for one six-year career interruption at age 30 (full red line) and with an additional six-year career interruption at age 54 (dashed red line). As the lines indicate, the impact of an interruption is assumed to be persistent throughout the remaining working life and thus to affect pension income. The impact of the wage penalty is greater for women with a higher level of education, since their wage curve is steeper.

The wage penalty for individuals with low and high educational attainment in Belgium. Source: Own calculations based on estimated earnings trajectories for Belgium. Note: The figure shows the estimated full-time earnings trajectories (blue line) for a woman with low (ISCED 0-2) (left) and high (ISCED 5+) (right) education. The full red line shows the impact on the earnings trajectory of full-time childcare from age 30 to age 35 when an earnings penalty is applied (see main text). The dashed red line shows the impact on the earnings trajectory of full-time childcare from age 30 to age 35 and full-time caring for an older relative from age 54 to age 59 when an earnings penalty is applied.

Our modelling of the earnings penalty is necessarily ad hoc. The main goal is to analyse the relative effect of an earnings penalty on pensions, rather than the exact mechanisms behind the earnings penalty. Given the wage profiles and our assumptions regarding the wage penalty, total relative loss in annual earnings over the six years at age 30 is around 10% for a woman with a lower level of education and 20% for a woman with a higher level of education. Kleven et al. (2019), who studied the impact of having a child on women’s wages, report earnings losses of between 20% and 60% in six countries (Denmark, Sweden, Germany, Austria, UK and the USA); these persist for 10 years, with little evidence of a mitigation of the earnings loss over time. Our modelled earnings losses, therefore, are near the lower end of their reported range.

Results

We present results for a number of scenarios with varying care activities and care duration. The base scenario refers to women with three different levels of education working full time and continuously between the age of leaving school and the statutory retirement age. The various scenarios consist of six-year spells of part-time work or interruptions of work, either at the age of 30 (in the case of childcare) or 54 (in the case of care for an older relative), or both. Finally, in the case of a full-time interruption, we assume a wage penalty after the woman returns to the labour market. 7

Childcare scenario

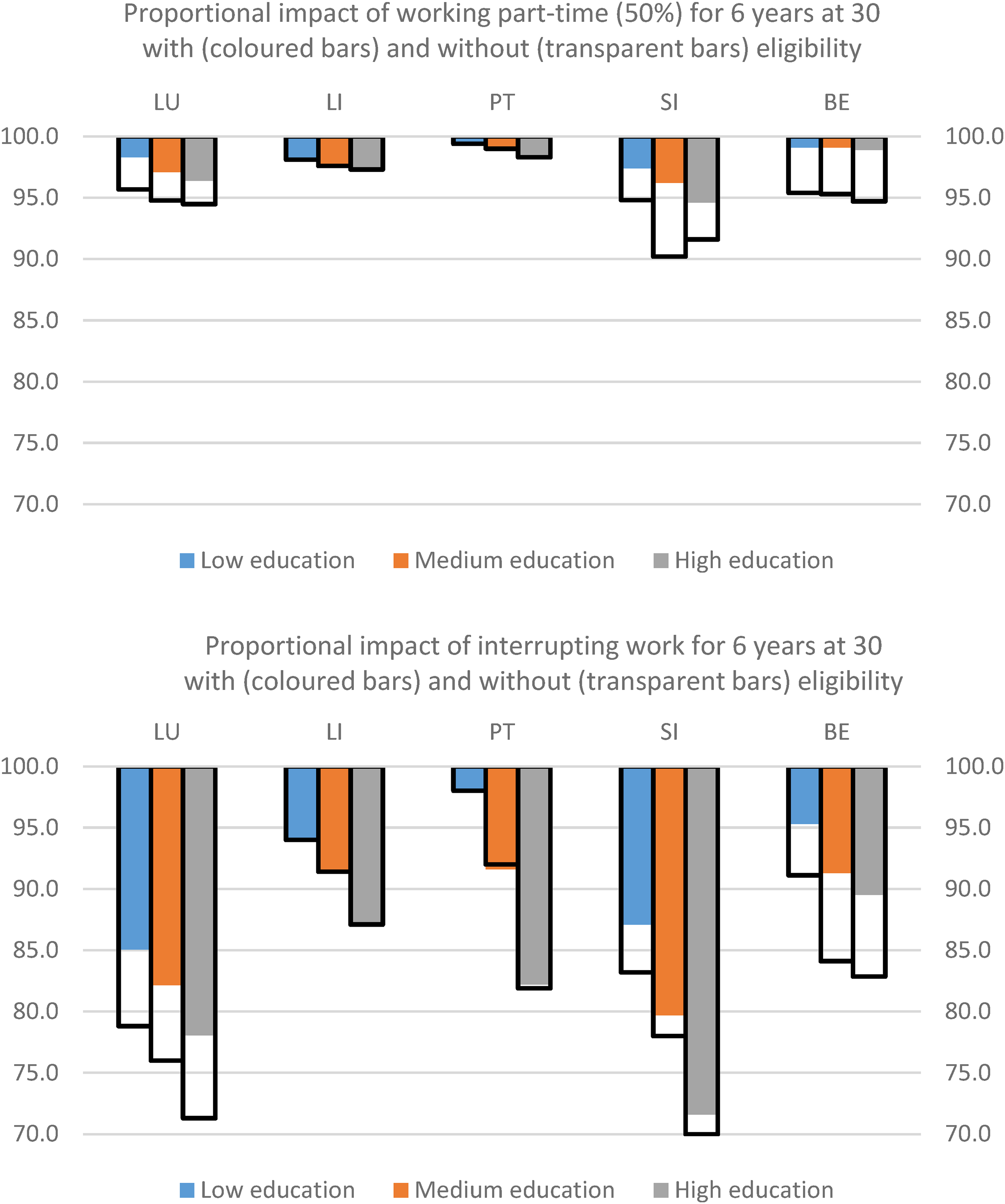

We first look at the variants in which the woman decides to interrupt her work, partially or completely, to focus on childcare for six years at the age of 30. In the case of part-time work, the model person’s wages are reduced proportionally during the period when they are aged 30 to 35, whereafter earnings return to the level of the estimated earnings trajectory for the relevant age. When the model person stops working entirely, their wage during the interruption period is reduced to zero. Upon returning to work at age 36, the person is then subject to a wage penalty. Figure 3 displays the findings.

Effect on retirement pension of working part time (50%) or interrupting work for six years due to childcare, relative to the pension in the case of continuous full-time work, with and without eligibility for care compensation schemes. Source: Typical-case simulations, see text. Note: The coloured bars show pension outcomes by average earnings for three educational attainment groups for a woman working part time (upper graph) or interrupting work (lower graph) for six years from age 30 and caring for a child, as a percentage of the pension outcomes in the case of uninterrupted full-time work. It is assumed that pension credits for childcare are applied as per the current legislation. The transparent monochrome bars show the equivalent impact in the case of non-eligibility, i.e. when the woman does not take up an eligible care task.

If the person is not eligible for care compensation schemes, their pension losses (indicated by the transparent bars) due to working half time for six years are limited in Liechtenstein and Portugal, around 5% in Belgium (which is nearly proportional to the loss in life-time earnings) and Luxembourg, and relatively high in Slovenia (up to 10%). In both Luxembourg and Slovenia, a bonus accrual at the end of the working life is lost if the career is reduced. In Liechtenstein, the loss is relatively small due to the redistributive mechanisms of the first-pillar pension scheme, in particular the revaluation factor. This means that the maximum pension from the first pillar is reached whether the woman works part time or not, and the limited pension loss is only due to the second-pillar pension. The Portuguese old-age pension is calculated on the basis of the 40 career years with the highest wages, and therefore (in our scenarios) the years with half-time wages are replaced by earlier or later years with full-time wages, resulting in only a minor loss in pension.

The pattern of pension losses across countries is rather different if the person is eligible for compensating measures (coloured bars). The loss is then small in Belgium (around 1%), Portugal (less than 2%) and Liechtenstein (less than 3%), somewhat larger in Luxembourg (between 2% and 4%), and Slovenia (up to more than 5%). The difference between the transparent and the coloured bars indicates the compensating impact of the pension credits related to care compensation schemes. In Belgium, this compensating impact is large because care compensation schemes can come into play for a maximum of 59 months. Furthermore, the pension credits related to the care compensation scheme during the period of part-time work are based on the last full-time wage. In Slovenia, this compensating impact is smaller than in Belgium, because the pension credits are based on a shorter period (second and third year after childbirth), but also because they are based on the minimum wage. In Luxembourg, pension credits (related to maternity leave, parental leave, ‘baby years’ and ‘education’ periods) compensate for about half of the loss in earnings. Finally, in Liechtenstein and Portugal, eligibility for compensatory measures has little or no dampening effect. Parental leave in Portugal lasts only six months. In Liechtenstein, as described above, the redistributive mechanisms of the first-pillar pension scheme mean that working part time for six years for any reason whatsoever has no impact on the later first-pillar pension. On the other hand, there is no provision for childcare in the second pillar. Differences in pension income are therefore entirely due to differences in second-pillar pension income.

The bottom graph in Figure 3 shows that interrupting one’s career for six years at the age of 30, which entails a wage penalty, results in larger pension losses than changing to part-time work. For a woman with low education not eligible for care-related pension credits, the loss varies between only 2% in Portugal and 21% in Luxembourg. In all countries, the losses are greater for a woman with a higher level of education who is not eligible for a compensatory scheme, suggesting that the impact of the wage penalty is severe for this category of women (see the discussion of Figure 2). For such women, the loss in pensions is very high in Luxembourg (29%) and Slovenia (30%). In both countries, the pension accrual rate increases when one works longer at an older age and after a long career. This additional accrual is missed if the career is interrupted without eligibility for pension credits.

In Liechtenstein and Portugal, the impact of pension credits related to care compensation schemes remains non-existent or very small, for the same reasons as for the part-time scenario. In Belgium, Luxembourg and Slovenia, however, although these impacts are considerable, they are proportionally smaller than if the person works part time. This suggests that the losses are partly driven by the wage penalty that the woman suffers after her return to the labour market, which is not offset by pension credits.

Care-for-an-older-relative scenario

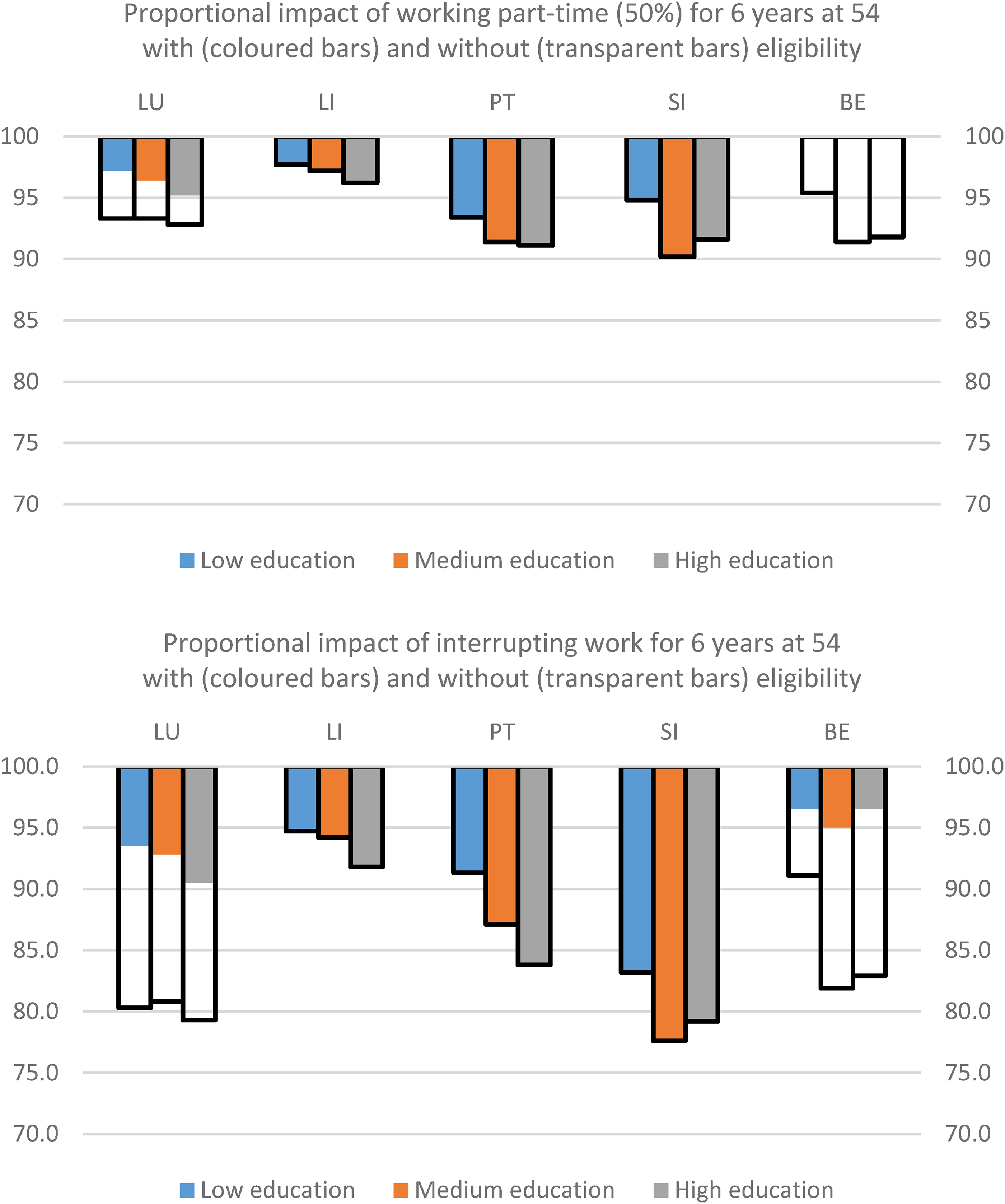

Now we turn to the scenarios involving care for an older relative, at the age of 54 (Figure 4).

Effect on retirement pension of working part time (50%) or interrupting the career for six years due to care for an older relative, relative to the pension in the case of continuous full-time work. Women, by education level (% levels). Source: Typical-case simulations, see text. Note: See Figure 3 for an explanation.

In Liechtenstein, if the person is not eligible for care-related credits, six years of half-time work at age 54 has only a small impact on their pension. The pension losses are larger in the other countries, ranging from 5% (a woman with low education in Belgium and Slovenia) to 10% (a woman with a middle level of education in Slovenia). If the person is eligible for compensation, these losses are virtually eliminated in Belgium and much reduced in Luxembourg. The reasons are that the period of eligibility covers the entire six-year period of interruption, and also that the fictitious wage taken into account for the pension calculation in Belgium is quite close to the wage of someone who has continued working full time, whereas in Luxembourg it is equivalent to the minimum social wage. By contrast, there are no compensating systems for someone caring for an elderly person in Slovenia and Portugal. There is such a system in Liechtenstein, but due to the redistributive impact of the first pillar (described above), it has no impact on the pension in our scenarios.

The bottom graph in Figure 4 shows that fully interrupting one’s career for six years without eligibility for care-related pension credits has a substantial impact on the later pension. However, a comparison of the bottom graphs in Figures 3 and 4 indicates that the costs of interrupting one’s career are often lower when this interruption occurs at age 54 than at age 30. The reason for this is that the effects of the earnings penalty are smaller – mainly because the number of remaining career years during which one will suffer this penalty is lower, but also because the earnings curve is flatter at higher ages, thereby reducing the penalty per year.

In Belgium the dampening impact of compensatory measures for someone taking up eligible caregiving at age 54 is large, even more so than at age 30. Apart from the smaller effect of the wage penalty, the reasons are the same as for half-time work, explained above. In Luxembourg, all periods devoted to care for an older person are offset (though at a lower level of fictitious earnings) by the care-related pension credits, whereas only part of them are compensated for when caring for a child at age 30.

Discussion and conclusions

This article is about the impact of childcare and care for an older relative on a person’s future gross pension in five European countries, given the pension legislation in force in the first half of 2020. We have studied this using the typical-case method. Several main findings stand out. First, it is clear that in Belgium, Slovenia (especially in the case of part-time work) and Luxembourg, the pension credits obtained by beneficiaries of care compensation schemes for childcare are important in mitigating the effects on the later pension of working part time or interrupting one’s career. However, other features of the pension system (such as revaluation factors which uprate the care credits, as in Liechtenstein, or consideration only of the years with the highest earnings, as in Portugal) can also mean that interrupting or reducing work has a relatively small impact on the later pension. These other features are not necessarily less effective than pension credits. Conversely, other features (such as missing out on higher accrual rates for longer careers, as in Slovenia and Luxembourg) can aggravate the negative impact.

Secondly, increased accrual rates for those with longer careers, as are available in Luxembourg and Slovenia, can strongly increase the loss in pension, for example when people interrupt their career to take up caring responsibilities. One solution to this problem, applied in Luxembourg, is to include some of these years as career years.

Third, the dampening effect of pension credits in Belgium, Luxembourg and Slovenia on losses due to a career interruption for childcare depends on the way these credits are calculated. If they are derived from a minimum wage (as in Slovenia). instead of from last actual earnings (as in Belgium and Luxembourg), then the mitigating effect is smaller. Imposing a restrictive ceiling on the last-earned income (Luxembourg) also results in a more limited mitigating effect.

Fourth, in Belgium, Liechtenstein and Luxembourg (the only countries under scrutiny that have pension credits related to elderly care), the dampening impacts of these systems is stronger than in the case of childcare at the age of 30. This is partly due to the conditions linked to these systems. In Belgium and Luxembourg, the coverage period for elderly care extends over the entire six years, whereas it is more limited in time for childcare. In Belgium, the pension credits are based on the last earnings, while in Luxembourg they are based on the minimum wage. Another factor, independent of the regulations, is the age at which the care-related pension credits are accessed in our scenarios. At age 54, the wage penalty after resuming work has much less impact than at age 30. Finally, in Liechtenstein, a combination of care-related pension credits and the highly redistributive first pillar of the pension system mitigates care-related losses of first-pillar pension income.

There are several limitations to our results, apart from the usual qualifications that have to be made for any study using standard simulation on hypothetical cases. Note that the focus on women is not really a limitation. As pension legislation is formally gender-neutral in all countries (except for maternity and paternity leave), the results apply also to men if they have the same wage profiles. One limitation is that we have left out the important question of contemporary support for care activities, that is, to what extent the state supports childcare and care for older people at the time of caring needs. To assess the overall support given to care activities, we would need to combine the results we have presented with a comparative analysis of the generosity of childcare benefits (e.g. Cascio et al., 2015) and benefits related to caring for older relatives (e.g. Riedel and Kraus, 2016). Another important limitation is that we simulate only first-pillar pensions (except for Liechtenstein). Adding the second- and third-pillar pension savings would exacerbate the impact of caring periods on the total pension outcomes, as in these funded pension systems, no credits are generally given for periods of caring. Finally, the study covers only five countries, two of which are tiny and are also exceptionally rich. A follow-up study involving more countries and pension systems is therefore recommended.

Footnotes

Acknowledgements

We are grateful to Simon Gstöhl of the Liechtenstein Statistical Office for the estimation of the Liechtenstein wage profiles, to Vera Hoorens of the KU Leuven for stimulating discussions on the research proposal and to an anonymous referee for useful comments which have improved the paper.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship and/or publication of this article: this work was supported by the Directorate-General for Justice and Consumers (grant number 820798).