Abstract

The structures of ownership and governance at John Lewis, a major UK employee-owned retailer, have been commended by those who wish to recuperate capitalism and by those who seek to transform it. From a perspective of ‘critical performativity’, John Lewis is of special interest since it is celebrated as a successful organization and heralded as an alternative to more typical forms of capitalist enterprise. By examining the cooperative elements of the John Lewis structures of ownership and governance, we illuminate a number of issues faced in realizing the principles ascribed to employee-owned cooperatives—notably, with regard to ‘democratic member control’, ‘member economic participation’ and ‘autonomy and independence’.

Keywords

… it is a powerful thing to have a model which focuses on Partners, secures their experience and commitment and fosters a desire to perform, for their teams, for their customers, and ultimately through the Partnership, for themselves. We call it the Partner-Customer-Profit circle. Many businesses have something similar—the employees, customer, profit chain—but there’s a key difference. There’s a break at the end of their chain where the profit flows mainly to external shareholders. In our business it flows to our Partners and so the circle starts all over again. That’s a powerful differentiator.

Introduction

During his Party Conference in March 2012, UK Deputy Prime Minister Nick Clegg commended the retailer, John Lewis, as a model of responsible capitalism. 1 This begs a number of questions. Is John Lewis—or, to be formally precise, the John Lewis Partnership—a beacon of ‘responsible capitalism’? Or is it a cooperative organized as a Partnership? Larger questions are also invited: What degree of responsibility can be exercised in a company owned by its employees where managers are accountable to their fellow Partners but which operates in an economy dominated by capitalist priorities and practices? Does the ‘responsible capitalism’ ascribed to John Lewis affirm or transgress ‘capitalist’ principles? And what is ‘responsible capitalism’ responsible to or for? These questions speak to the perennial concerns of commentators and practitioners in search of alternatives to the capitalist corporation (Hutton, 2012), and they are especially salient in the context of multiple crises associated with modern capitalist development (Gamble, 2009).

The John Lewis Partnership (JLP) is a public limited company 2 that embraces many of the values and principles of the International Cooperatives Alliance (ICA) 3 which defines cooperatives as ‘businesses owned and run by and for their members [who] have an equal say in what the business does and a share in the profits’. 4 Defined in more rigorous terms by Webb and Cheney (2013), JLP complies, formally at least, with what these authors identify as ‘four key pillars of the co-operative business model’ with regard to ‘an internationally accepted framework of values and principles and a founding ethic of economic fairness or justice’ as well as share equity (Webb and Cheney, 2013: 5; Warhurst, 1996). 5

Many commentators on JLP, as reviewed by Cathcart (2009, 2013a, 2013b), concentrate upon specific limited aspects of its operation. Our interest, in contrast, is in whether JLP structures of ownership and governance offer a ‘critically performative’ alternative to capitalist enterprise (Spicer et al., 2009). This possibility is suggested by how, as an example of an employee-owned cooperative, JLP Partners (permanent staff 6 ) are the primary beneficiaries of income derived from assets held in trust through the vehicle of the John Lewis Partnership Trust Limited (JLPT). 7 With regard to governance, Partners are legally empowered by the JLP Constitution to participate in a range of fora and media, which includes the Partnership Council, elected predominantly (80%) by Partners, that is formally empowered to remove the Chairman and Chief Executive.

In common with many other cooperatives, JLP structures of ownership and governance do not meet the most demanding of criteria used to identify cooperatives. The Trust structure does not allow Partners, individually or collectively, to exercise ultimate control of JLP by selling their shares and, equally, there is no threat of acquisition by distant investors. JLP is a type of employee-owned cooperative (Huertas-Noble, 2010; Gios and Santuari, 2002). It is not a ‘labor managed firm’ in which ‘ultimate control rests with workers and their representatives’ (Schwartz, 2011: 14), and JLP managers are not directly elected or appointed by the Partners. Nonetheless, and unlike most organizations in which employees own some or even all of the shares (Carberry, 2011), the Constitution of the Partnership ensures that a surplus is distributed to its Partners through a common percentage increase in salary and it requires that JLP managers are accountable to the Partners. So, despite important limitations, might there not be something at least mildly ‘critically performative’ about JLP’s ownership and governance structures?

This question is prompted by how JLP’s democratic governance structures actively invite Partners’ ‘interven[tion] in managerial discourse and practice’ (Spicer et al., 2009: 544) as a means of curbing managerial autocracy in addition to how the device of the Trust closes JLP to ownership by absentee investors. Albeit imperfectly, in these respects JLP structures are designed and operate ‘to subordinate the maintenance of capital to the interests of labor and human values’ (Cheney, 1999: 39). Accordingly, scrutiny of JLP can help illuminate and interrogate issues and challenges of establishing and sustaining a post-capitalist form of organization with regard to ‘democratic member control’, ‘member economic participation’ and ‘autonomy and independence’ (principles of the ICA). In this regard, we share Hartmann’s (2014) assessment that ‘the examination of alternative organizations … counteracts a tendency in CMS (critical management studies) research to “refrain from studying alternatives” [when they] might be a better and more efficient choice or even be able compete [with capitalist enterprise]’ (pp. 13–14).

Our contention is that JLP’s ownership and governance structures offer a practical demonstration, albeit flawed, of how an alternative form of organization is sufficiently ‘efficient’ and durable to be able to ‘compete’ against joint-stock companies. These structures also suggest how the Partnership form can act to check some grosser social inequalities with regard to political domination through processes of corporate decision-making and economic exploitation arising from the separation of ownership from value-producing activity. This proposition is unfashionable and contentious as many scholarly accounts and commentaries on JLP are antagonistic to, if not dismissive of, such claims. 8 Without denying the limitations and ambivalences of JLP structures, including a pervasive paternalism and incipient managerialism, we contend, nonetheless, that, in principle, and to a degree in practice, JLP exemplifies a comparatively ‘responsible’ kind of enterprise, at least with regard to its employees and its customers. Such ‘responsibility’ is significant, if hardly earth-shattering, we argue, even when it is acknowledged that the ‘alternative’ character of JLP’s structures of ownership and governance is compromised by an instrumentalism directed at more typically ‘capitalist’ performance measures (Cathcart, 2009, 2013a, 2013b) than, say to, community well-being or ecological sustainability.

Our analysis uses secondary empirical material (e.g. JLP documents in the public domain, histories of John Lewis and recent empirical research). Our assumption is that engagement and interrogation of existing empirical work can be at least as illuminating and challenging as undertaking new studies (Moore, 2007). In addition to generating fresh insights, stimulating reflection and fostering debate, our analysis is intended to contribute to an appreciation of how structures of ownership and governance are significant in enabling and constraining practices of organizing and managing.

We begin by providing a brief history of the formation of JLP in which we address the rationale for its creation and intended operation. We then present the contours of the formal design of JLP by considering its ownership and governance structures. This fills out the relevant background and orientation for our assessment of JLP in relation to the complex practices associated with capitalist and cooperative principles of organization, and its relevance to critical performativity.

John Lewis: in pursuit of happiness

Business, objective and structure

Established in 1864, the family drapery store, John Lewis, was converted, in 1929, into a Partnership with a formal Constitution that distributed its profits to the Partners. After 25 years, the property of the Partnership was assigned to the Partners through a second Trust settlement (O’Regan and Ghobadian, 2012). At the time of writing (2013), the JLP has around 84,700 Partners (Annual Report 2013) working across the United Kingdom in 39 John Lewis stores and 290 Waitrose supermarkets. With annual gross sales of over £9.5 billion in 2013, JLP was the fourth largest non-publicly owned company in the United Kingdom measured by sales. 9

A household name in the United Kingdom, JLP is widely acclaimed for being financially and commercially successful. It is highly trusted by its loyal and generally affluent customers.

10

The ‘ultimate purpose’ of JLP, as stated in its Constitution, is

the happiness of all its members, through their worthwhile and satisfying employment in a successful business. Because the Partnership is owned in trust by its members, they share the responsibilities of ownership as well as its rewards—profit, knowledge and power. (Cox, 2010: 272, emphasis added)

This overarching purpose is one to which all JLP Partners are held accountable, and to which all Partners are able to make direct appeal, as do JLP Registrars (see later) who are appointed to act as the guardians of the company Constitution.

The architect of JLP, who was John Spedan Lewis (J.S.L.), one of the sons of the firm’s founder, who bequeathed the company to its employees. In a British Broadcasting Corporation (BBC) poll, in 2002, J.S.L. was voted Britain’s top business leader, ahead of Andrew Carnegie, Joseph Rowntree and William Lever. 11 J.S.L.’s bequest followed his disenchantment 12 with a more conventional and deeply entrenched philosophy and operation of capitalist enterprise, as exemplified by the business practices of his father. J.S.L. voiced his disillusionment in a talk aired by the BBC in April 1957, where he recalls how his father ‘seemed to have all that anyone could want’, and yet spent ‘no more than a small fraction of his income’ (Lewis, 1957). For his father’s staff, in contrast, ‘any saving worth mentioning was impossible. They were getting hardly more than a bare living’ (Lewis, 1957). Commenting upon the impact of capitalism upon working people, J.S.L. first remarks that ‘capitalism … has done enormous good and suits human nature far too well to be given up as long as human nature remains the same’ (Lewis, 1957). But he immediately adds that it is ‘all wrong to have millionaires before you have ceased to have slums’ (Lewis, 1957)—a state of affairs that he describes as ‘a perversion of capitalism’ (Cox, 2010, emphasis added).

In J.S.L.’s eyes, the ‘perversion’ was widespread in business practices, and especially in the treatment of employees, that were unjustifiably inegalitarian, socially divisive and ultimately self-destructive. J.S.L. set himself the challenge of (re)constructing the family business in a form compatible with his conception of ‘human nature’ and consistent with retaining the capacity of capitalism to do ‘enormous good’ so that its (performative) effect is to reduce unnecessary suffering rather than needlessly producing or perpetuating it. Conveyed in the subtitle of his book Fairer Shares (Lewis, 1954), J.S.L. regarded the model enacted in the Partnership as ‘A possible advance in civilization and perhaps the only alternative to Communism’.

Commentary

Whether intended or not, the formation and maintenance of the Partnership is simultaneously a direct and practical intervention in debates around ‘alternative forms of organization’—alternatives which have been defined primarily in relation to the expansion and domination of the joint-stock company. The slump of the late 1920s (Schwartz, 2011) re-ignited discussion of the relevance of ideas about collective and cooperative, rather than capitalist, organization ‘as the best way to create a better society’ that continued into the early 20th century (Cathcart, 2009: 96–97; Goglio and Leonardi, 2010: 12). It also fuelled moral concern about the damaging and degrading consequences of unbridled capitalist expansion in which, established institutions (e.g. family and state) were becoming progressively harnessed to, and reshaped by, its priorities.

J.S.L.’s vision of a Partnership, governed by a Constitution setting out very detailed rules for its day-to-day operation, was apparently inspired primarily by an offended morality tinged with a philanthropic paternalism than it was animated by any political allegiance or agenda. Considered from a more contemporary vantage point, the creation and longevity of JLP may be seen as a practical demonstration of how

the economy [does] not have to be thought as a bounded and unified space with a fixed capitalist identity. Perhaps the totality of the economic could be seen as a site of multiple forms of economy whose relations to each other are only partially fixed and always under subversion. (Gibson-Graham, 1996: 12, emphasis added)

Capitalist relations are ‘under subversion’ (Gibson-Graham, 1996) in diverse ways. The accumulation of capital by entrepreneurs and/or their family members affords them the option of becoming absentee shareholders in joint-stock companies in which, unlike the Partnership form, their liability for losses is legally limited to their share holdings. In such companies, salaried managers are hired to act as custodians of the assets of the company as the ex-owners spread their risks and smooth their returns within diversified investment portfolios. It is the rise of the joint-stock company that Marx (1981) describes as a ‘negative’ (p. 572) form of transition within capitalism (to be discussed below). And it was this (joint-stock) trajectory of capitalist development that J.S.L. sought to escape, and perhaps also to forestall, by establishing and demonstrating the viability of an alternative ‘form of economy’ (Gibson-Graham, 1996: 12) involving the use of a Trust to convert the family business into a Partnership.

Ownership and governance

Structures of ownership and governance define the broad parameters of the operation of companies. These structures are of critical importance as they facilitate but also restrict the practices that comprise corporate activity (see Appendices 1 and 2).

JLT ownership: voting rights and types of shares

The locking down of JLP assets in a Trust (JLPT) prevents the dilution of equity, as it forbids its acquisition by non-Partners. 13 The device of the Trust frustrates the attentions of ‘carpetbaggers’ and thereby protects the benefits (e.g. employment) enjoyed by future as well as present Partners. 14

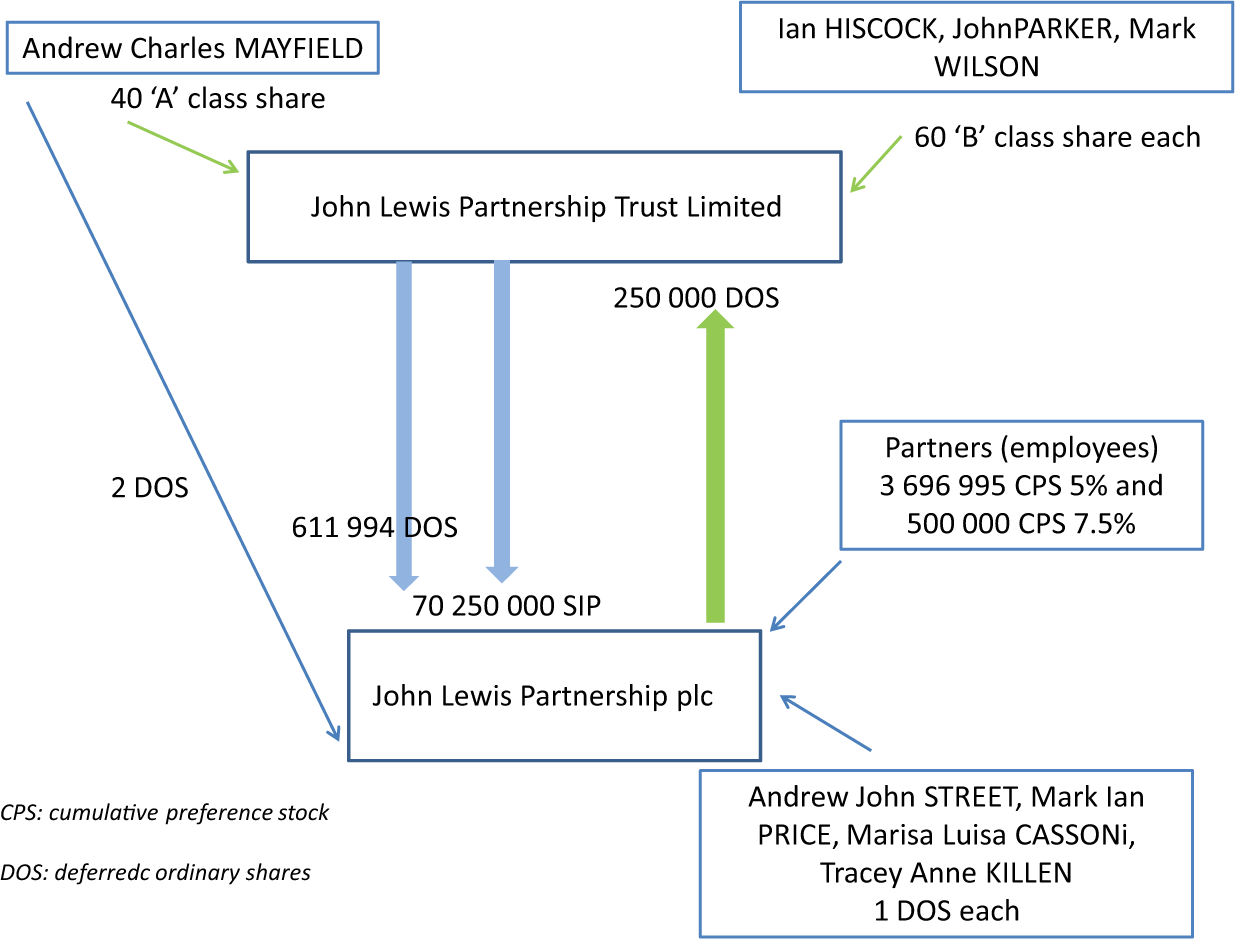

JLP is organized around two main structures: a Trust and a Partnership (John Lewis Partnership Plc—JLPplc), with cross-holding. This cross-holding is organized with the support of different kind of shares.

At the Trust level, there are three types of share, but only one share, owned by the Chairman, has full voting rights. JLPplc owns the majority of the shares but with no voting rights, just dividend rights, call Deferred Ordinary Shares (DOS).

At the Partnership level, there are also three kinds of shares but only one, owned by JLPT, has full rights attached (DOS—which are different to those of the Trust). The Cumulative Preference Stocks (CPS) 15 have priority on dividends and are owned by the employees (the Partners). JLPT also owns Share Incentive Plan (SIP) shares that have only dividend rights. The position is summarized in Figure 1.

Overall ownership structure.

Commentary

The salient points are as follows:

Partners have the benefit of dividends paid by the CPS. But they have no other rights with regard to voting, and so on, and they cannot sell CPS. This stock simply underwrites giving priority to a minimal level of annual bonus paid to Partners.

The Trust (JLPT), and not individual partners except Directors, owns DOS and the SIP. Only the former have full voting rights and neither can be sold.

It is a cross-holding organization linking JLPT and JLPplc.

JLP is a wholly employee-owned cooperative Partnership. Since the financial beneficiaries of the Trust are solely JLP employees, it is relevant to consider how this structure differs from that of non-cooperative organizations where (a) there is some employee ownership but neither extensive ownership and/or control (Ben-Ner and Jones, 1995; Doucouliagos, 1995) and (b) cooperatives are founded by their members. A typology devised by Pendleton (2011) distinguishes (a) ‘worker cooperatives’, (b) firms with minority share plans and (c) ‘firms that are substantially or wholly worker owned’ (p. 315). Applying this typology, JLP is a ‘business succession firm’ 16 in which the motive ascribed to the divesting owner is ‘to protect the firm they have built up’ (Pendleton, 2011: 323), presumably from external investors who might seek to control or acquire it, and ‘a paternalist desire to protect the interests of their workforce’ (Pendleton, 2001: 323, 2011). Indeed, Pendleton explicitly refers to JLP which he includes among employee-owned firms that ‘adopt cooperative principles of equality of ownership, even though they do not register as fully fledged cooperatives’ (Pendleton, 2011: 320) with regard to direct ownership by employees accompanied by full voting rights. JLP is, in very many respects, close to Pendleton’s ‘worker cooperative’ but, notably, in the Partnership, at the Trust level, the ownership of shares with full voting rights is limited to the Chairman. 17

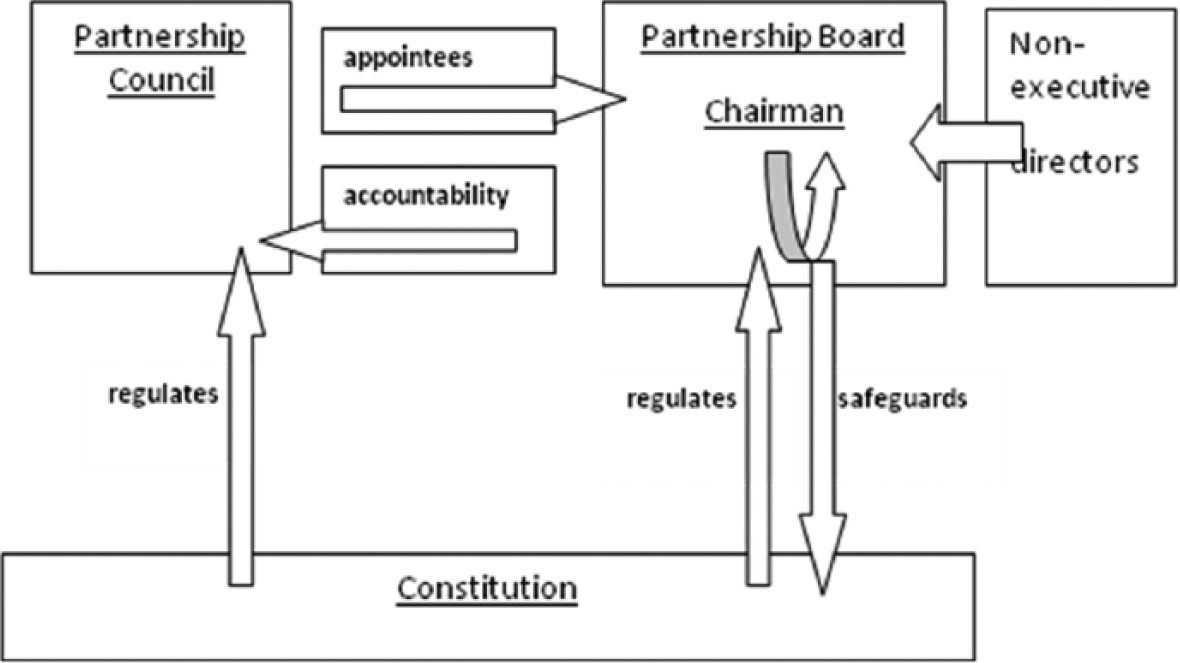

JLT governance: constitution, ‘Critical Side’, board and council

Three key elements characterize the governance structure of JLP: The ‘Critical Side’, the Partnership Board and the Partnership Council.

The Critical Side is a novel and significant feature of the JLP governance structure included within its Constitution. Its purpose is to counterbalance and check the ‘Executive Side’, and thereby, in J.S.L.’s memorable formulation, ‘safeguard the Executive from inadvertence’ (Lewis, 1948: 425). The ‘Critical Side’ comprises ‘independent’ advocates of the JLP Constitution—and of Partners’ rights within it and obligations to it—who are found across branches of the Partnership. Called Registrars, their role, is to ensure that all forums and committees comply with the employee input and representation functions, as set out in the Constitution. A Chief Registrar, who is often elected by Partners to the Board (considered below), oversees the ‘Critical Side’. Additionally, there are ‘independent’ Partners’ counsellors at HQ who engage with the Registrars across the branches whose responsibility it is to ensure that employment and work practices are consistent with Partnership values (e.g. the ‘happiness’ of Partners). The most senior within this intricate governance structure, the councillors provide a further constitutional counterweight to the ‘Executive Side’ in relation to complaints of, and grievances between, Partners.

The Partnership Board is the body ultimately responsible for fulfilling the purpose of the Partnership. In addition to the Chairman, the membership of this Board comprises three non-executive directors, five directors elected by the Partnership Council and a further five directors appointed by the Chairman. Members of the Partnership Board are responsible for managing JLP strategy, the quality of its financial statements, and the direction and reputation of its commercial activity (John Lewis Constitution, 2012, article 38). 18

In the organization and work of the Partnership Board, the role of the Chairman—a position first occupied by J.S.L.—is pivotal. Not only is he or she responsible for deciding who should be admitted and retained in the Partnership, and for maintaining the Constitution to the satisfaction of the Partnership Council (considered below), but the Chairman has sole responsibility for the appointment of his or her successor (Constitution, article 41), and as noted above, he or she has full voting rights (Appendix 1). Additionally, the Chairman is charged with ultimate responsibility for reconciling conflicting pressures between, for example, (a) re-investment of surpluses to develop the business, (b) Partners’ desire for a good quality of working life but also the receipt of a substantial bonus and other benefits and (c) the competitiveness of JLP with regard, for example, to staffing costs and increasing employee productivity. When drawing up the Constitution, J.S.L. reports that he agonized over the contradictions between his advocacy of industrial democracy (e.g. election of 80% of the Partnership Council, see below) and the autocracy vested in the role of the Chairman. Whether his motivations were self-interested (recall that he appointed himself as the first Chairman) or more altruistic, J.S.L. justified this structural design by reference to fear of the ‘disastrous’ consequences that might result from its abolition (Cathcart, 2009: 46).

The Partnership Council is the third element of the governance structure which, in effect, is the General Assembly of JLP. In all, 80% of Council members are elected by the Partners on the basis of one person-one-vote, with the remaining 20% of the Partnership Council being appointed by the Partnership Board. Members of the Partnership Council are required to ‘represent Partners as a whole and reflect their opinion’ (John Lewis Constitution, 2012, article 7). The Partnership Council discusses and makes recommendations on the development of policy, and it shares responsibility with the Board and the Chairman for making decisions about the governance of the Partnership. The Partnership Council can ask for explanations from the Board; it can propose strategy, and the Board and its Chairman are obliged to respond to such proposals and requests. However, the Board is not required to respond if this would, in the Board’s opinion, damage the Partnership’s interests. The relationships between the Constitution, the Board and the Council are summarized in Figure 2.

Constitution, council and board.

We now introduce a comparative framework in which we contrast, capitalist with cooperative structures of ownership and governance before applying this framework to illuminate and interrogate those of the Partnership, as sketched above. A key question is whether JLP can be credibly regarded as a critically performative alternative to capitalist enterprise.

Enterprises: capitalist and cooperative

Conditions of possibility

To explicate the organization of work within different (e.g. tendentially) ‘capitalist’ or ‘cooperative’ structures of ownership and governance, it is important to appreciate that structures per se are impotent: the catalyst of human agency is required to enact their reproduction or transformation. Attentiveness to agency serves to recall how, for example, ‘efficient markets’ and organizational hierarchies are, on the whole, forged and protected by emergent or entrenched elites and then are reproduced (and transformed) by the masses. Agency is obfuscated when, for example, the determination of prices, including the terms and conditions of labour, are abstracted from the political (re)construction of seemingly impersonal market forces. But, equally, the ‘agency’ of organizational members is conditioned by their situatedness and participation in ‘structure(s)’, even if their ‘agency’ is not reducible to, or determined by, the ‘structure(s)’ in which it is embedded.

In work organizations, structures of ownership and control are maintained or transformed through day-to-day struggles wherein agents (e.g. employees) introduce, absorb, question, reject, moderate or reproduce those structures. J.S.L., for example, reflected upon structures and associated employment practices typical of his day, and he determined to establish an alternative, Partnership structure capable of fostering and sustaining substantially different practices. In JLP today, governance bodies, including the Partnership Council,

19

are arenas of day-to-day struggle where, by virtue of the Constitution and its guardians (the Registrars), the exercise agential powers of governance is facilitated but also restricted, resulting in the preservation, or the alteration, of work practices and benefits (e.g. pensions provision).

20

In this context, it is salutary to recall Marx’s (1981) observation that

Capitalist joint-stock companies as much as cooperative factories should be viewed as transition forms from the capitalist mode of production to the associated one, simply that in the one case the opposition is abolished in a negative way, and in the other in a positive way. (p. 572)

Marx’s reflections suggest that, as a ‘transition form’, cooperatives are on the margins of an opposition between capital and labour. It is an assessment echoed by Pendleton (2005) when commenting upon employee share ownership which, he notes, modifies the ownership relationship but ‘does so by making the worker a capitalist rather than by changing the capital-labour relationship fundamentally’ (Pendleton, 2005: 77, emphasis added). In effect, without more radical, extensive politico-economic change, employees in cooperatives become mini-capitalists who, it may be said, participate in their own ‘self-exploitation’. 21

It is unsurprising to find that the historical and ongoing processes of ‘positive transition’ (Marx, 1981: 572)—from a family owned capitalist enterprise into an employee-owned cooperative enterprise—are permeated by constraints, contradictions and compromises with regard to issues and processes of governance as well as ownership. There are, nonetheless, structural differences of ownership and governance between JLP and its earlier form as a family business. Of greater contemporary relevance, there are differences between the structures of JLP and the joint-stock form of enterprise. They facilitate but also restrict distinctive complexes of practices that articulate an embeddedness in dynamic and, to a degree, open historical and cultural contexts. This dynamism and openness is symptomatic not only of the volatility and instability arising from the capitalist ‘imperative’ of creative destruction but also of the dependence of this imperative upon the catalyst of human agency. As the formation of JLP demonstrates, what is accepted and apparently enduring today may be challenged and overturned tomorrow.

Capitalist enterprise: the joint-stock company and disempowering governance

Capitalist enterprise, in its joint-stock variant, is here conceived as tendentially organized to prioritize and safeguard the concerns of investors. This predilection is accomplished by the exclusion of sellers of labour power and other stakeholders from direct ownership of assets (e.g. buildings, raw materials, tools, etc.). Sale of goods generates a surplus which, in the form of dividends or capital gains, is privately appropriated by investors. With the exception of senior managers, who may also possess substantial stock options, wage labour has no significant, formal involvement in determining or reforming the structures of ownership or governance. 22 The accountability of senior executives (e.g. through audit and analysts’ reports) is primarily to financial institutions through financial markets.

Understood in these terms, capitalist enterprise is considered to be systematically exploitative and oppressive (Weeks, 2010). Economic exploitation and political oppression exist irrespective of claims about the ‘progressive’ or ‘enlightened’ character of particular practices—with regard, for example, to employee involvement and employee share ownership schemes, or even token worker directors. Capitalist practices are, however, rarely represented, or even consciously experienced, as either exploitative or oppressive since, commonsensically, the terms ‘exploitation’ and ‘oppression’ are reserved for their most extreme and abhorrent forms—such as slavery, child labour or trafficking. Sanctified by bourgeois economics, economic exploitation and oppression are normalized in value-orientations that many employees learn to accept and defend. In common with J.S.L., poverty and misery are considered to harboured or engendered by capitalism only in their (most) ‘perverted’ forms. Everyday contractual exchanges between purchasers and sellers of labour power are deemed to be fair, not exploitative. That is because ‘prices’—which include the prices in labour and capital as well product markets—are regarded as a result of impersonal and impartial forces rather than the outcome of relations of power and domination through which elites make markets and maintain hierarchies (Böhm and Land, 2012; Orleans, 2011). In financial markets that have been spawned by the rise of the joint-stock form of capitalism, shares and indeed companies are traded speculatively, as commodities, by absentee investors who often have only a short-term interest in maximizing the value of their holdings. Investors’ preference is to finance companies in which they, and not other parties such as employees, can collectively exert a majority, controlling grip. Their concerns are then prioritized through the disciplining operation of capital markets.

Cooperative enterprise: employee ownership and collective governance

Employee-owned cooperatives are here conceived to be tendentially organized to prioritize and safeguard the concerns of employees—notably by establishing and maintaining majority ownership and by democratizing governance. In employee-owned cooperatives, where its members are majority shareholders, there can be no systematic exploitation of labour by a different group, or class. Ownership of the assets of cooperative enterprise is normally through the investment of members or supporters in enterprise shares supplemented by other sources of finance, such as grants and loans. Cooperative members are either directly responsible for enterprise governance, including strategic and operational decision-making, or managers are appointed by and/or held accountable to the membership. Labour is no longer commodified even if the domination of exchange value persists in the economy as a whole (Weeks, 2010). In cooperatives, there are no dividends distributions, so the surplus value is dedicated to improving wages and conditions in addition to re-investment and creating reserves, and there is no opportunity to speculate on their future value as this is fixed.

When operating in an economy dominated by joint-stock companies and financial markets established to serve them, cooperative work organizations are financially disadvantaged so that their members struggle to achieve competitive economies of scale or scope. Nonetheless, their members opt to create or join such organizations where they are able to exercise a greater degree of autonomy and independence with regard to their governance. Notably, they are able to exercise democratic control over the goods or services that they produce and also over how they are produced. In employee-owned cooperatives, governance is not confined to the activities of an elite of board members but extends to decision-making across the organization in a way that assumes trust and commitment, and so also risks its abuse. In principle, decisions are either directly determined by cooperative members or they are scrutinized through mechanisms of accountability where managerial decisions are subject to challenge and potential reversal (Paranque, 2014).

Commentary

Our presentation of capitalist and cooperative enterprise, as comprising tendentially distinct practices, has served to highlight the significance of structures of ownership and governance in conditioning employment relations and the organization of work. But those structures are impotent without the catalyst of agency. The presence of agency accounts for why, in their day-to-day operation, practices of organizing and managing rarely mirror the structural features ascribed to them. Members of cooperatives, for example, may turn a blind eye to ‘free-riding’ by members whose commitment to principles of working together and inclusiveness is, at best, partial. It is to such recalcitrance that J.S.L. may have been alluding when, reluctantly, 23 he concludes that reducing the power of the Chairman ‘would open the door to troubles that might be disastrous’ (Lewis, 1948: 369).

As anticipated by Marx (1981), the formation of cooperatives may signal ‘the first examples of the emergence of a new form’ (p. 571), but they also ‘naturally reproduce in all cases, in their present organization, all the defects of the existing system, and must reproduce them’—by which we understand Marx to refer inter alia to forms of self-interested behaviour as well as self-exploitation and work degradation. Marx conceives of cooperatives as foreshadowing a ‘new’ form of work organization in which the opposition between capital and labour is abolished ‘even if at first only in the form that the workers in association become their own capitalist, i.e. they use the means of production to valorize their own labour power’ (Jossa, 2005: 5, citing Marx, 1981: 571, emphasis added). 24 Here, Marx might be describing the situation at JLP where the social division between capital and labour is abolished, at least with regard to external owners. Cathcart’s (2009) study of JLP echoes Warhurst’s (1996) observation that ‘management as an occupational group [within the kibbutz system] is becoming more coherent and consistent’ (p. 434), and in this sense, it comprises a fraction within the Partnership that is in some tension with the more unified spirit of the JLP Constitution. In this light, ‘economic sites’ (Gibson-Graham, 1996: 18) that are widely represented as ‘homogeneously [cooperative] may be re-envisioned as sites of economic difference where a variety of [cooperative and non cooperative] class processes interact’ (Gibson-Graham, 1996: 18).

An exclusive focus upon the political economy of enterprise courts the danger of reducing relationships to ones of economic ownership versus economic non-ownership. While political economy is vital—we have stressed the importance of structures of ownership—this emphasis can overlook the heterogeneity of corporate practices. It may fail to appreciate how, for example, even within joint-stock enterprises, relations may be pervaded by, and depend upon, other (e.g. cultural) relationships, including friendship, family and community (Grey and Sturdy, 2007). Those ‘informal’ relations may, of course, be more or less purposefully harnessed by management to smoothing or intensifying the capital-labour relationship, but they are rarely reducible to that single objective. Analysis which considers only the expansive tendencies of capitalism to colonize and commodify ever wider areas of social life risks conveying an indefensibly totalizing picture in which the economy is left ‘theoretically untouched’ (Gibson-Graham, 1996: 38), or, at least, the abstraction of the economic from the cultural is inadequately interrogated and problematized so that sites are (mis)represented as homogeneously capitalist or cooperative.

Discussion

We now assess JLP as an example of critical performativity with respect to its structures of ownership and governance and its relevance for moving ‘beyond capitalism’.

Ownership and JLP

When employees are the shareholders, the systematic exploitation of one class by another is, by definition, excluded within the company. If this logic is accepted, then in employee-owned cooperatives there is no logical justification for a distinctive, potentially oppositional, employee voice. And yet, even where, as in the case of JLP, the opposition of capital and labour is formally abolished, and a comparatively democratic structure of governance is established, its day-to-day operation may be conditioned or even dominated by other (e.g. financial) considerations.

Unlike many employee-owned cooperatives, JLP is in an enviable position of being minimally reliant upon external sources of capital. Even so, the ‘professionalization’ of JLP management has been accompanied by the importation of financial performance conventions and by a managerially encouraged emphasis upon running the business to deliver the annual bonus paid to Partners. These considerations inform decision-making within the Partnership, including discussion of governance reforms and proposals to change the terms and conditions (e.g. extension of trading hours) of Partners.

The absence of a directly oppositional employee voice, which JLP shares with certain cooperatives (e.g. Mondragón), may be taken to reflect the abolition of the social division between capital and labour. But it may also indicate the latent influence of a shareholder ideology and associated discourse of shareholder value creation (Pendleton, 2005: 76). JLP staff may then identify themselves primarily as recipients of dividends rather than as Partners committed to the ‘happiness’ of all members, where ‘happiness’ is not conflated with the ‘self-exploitation’ required to deliver a substantial bonus. The dividend paid to shareholders and the Partners’ bonus may function in a similar way when each encourages, or induces, the generation of a surplus in a manner that does not, and perhaps cannot, readily countenance, accommodate or fulfil other, non-financial objectives (e.g. sustainability), except perhaps by promoting higher margin ‘green’ products in its stores, thereby improving financial returns. If Partners’ identification with the ethos of Partnership is shallow or eclipsed by other priorities, their relationship to (fellow members of) the cooperative becomes less distinguishable from the alienated labour found more typically in capitalist enterprises.

In capitalist enterprise, it is the concerns of investors rather than other stakeholders that are prioritized. This follows, in substantial part, from (mis)ascribing to shareholders ownership of residual rights (claimants) on the assets of the enterprise when, legally, they own no more than the shares traded on financial markets. This (mis)ascription leads to an agency-theoretic (mis)representation of executives as ‘agents’ of the ‘principals’ (i.e. shareholders). For, legally, executives are guardians of the assets of the enterprise, not of the ‘principals’ of a going-concern in which diverse parties, including shareholders, make a contribution and have a stake. In JLP, the (mis)ascription of ownership of the assets is avoided. It is clear that the Partners derive a share of the surplus produced from the productive use of those assets. The role of managers is, however, less well defined beyond a rather vague notion of their responsibility for ‘the happiness of all [the Partnership’s] members, through their worthwhile and satisfying employment in a successful business’ (Cox, 2010: 272). The question begged is the meaning of ‘happiness’, ‘satisfaction’ and ‘successful’ and whether, managerially, it might be framed in relation to service to the community, for example, or to the size of the bonus.

Even allowing for how, in Marx’s (1981) words, the formation of cooperatives may reproduce ‘the defects of the existing system, and must reproduce them’ (p. 571) (as illustrated earlier), if JLP structures of ownership and governance were to be widely adopted, there would be far-reaching consequences. Capital/labour divisions would be very considerably eroded and the conditions of possibility of the (mis)ascription of asset ownership to shareholders, and the associated mantra of shareholder value maximization, would be silenced. Private wealth could still be accumulated by loaning capital without voting rights, but external shareholders could not engage in trading their shares or entire companies without regard to those who create the assets from which capital is privately accumulated.

Given the radical implications of any widespread adoption of the JLP model, as commended by the UK Deputy Prime Minister, it is surprising that John Lewis is routinely presented, and indeed is celebrated, as an icon, and perhaps a saviour, of ‘true’ capitalism—that is, ‘responsible capitalism’. On the other hand, and in common with employee-owned cooperatives, such as Mondragón, JLP poses no direct threat to the ‘free market’ principles of capitalism, and it offers no succour for the nationalization of enterprises. Indeed, the inspiration for establishing the Partnership lay in demonstrating the viability of ‘responsible’ capitalism, and not in engineering a replacement for it. Even the aspiration to counteract and reduce the pathological effects of ‘free markets’ can prove difficult to fulfil—as is evident from how members of the Mondragón cooperative reportedly regard their relation to it ‘less as citizens and more as consumers’. 25 This consumerist orientation, which finds echoes among the Partners of JLP has been interpreted as an effect of how ‘the cooperatives themselves [have] imported managerial regimes that privilege constant orientation towards the customer/client’ (Asparagus et al., 2012: 79). Had a survey equivalent to that administered at Mondragón been undertaken in JLP, it would probably elicit similar responses. That said, it is undoubtedly easier for a retailer to preserve such principles than it is for a producer cooperative that faces intense international competitive pressures.

Governance and JLP

Partners do not own JLP, only a specific right to a minimal level of dividend, and so they are prevented from exerting direct pressure upon JLP managers through the market for corporate control. Instead, Partners are obliged to control managerial decision-making through an elaborate governance structure. Their capacity to resist managerialism flows from the powers of governance bestowed upon them by the Constitution, and not from their property rights as shareholders. It is Partners’ election of a majority (80%) of the Partnership Council that, ultimately, empowers them to influence strategy as well as operational decisions, 26 and even to remove the Chairman.

In direct contrast to joint-stock enterprise, JLP institutionalizes a recognition of the productive engagement of labour in the creation of assets and guards this in its Constitution. That said, and as Pendleton (2011) has noted of ‘post-conversion governance structures’ similar to JLP, they are ‘likely to be especially influenced by [the ex-owner(s)]’ (p. 332). Bequeathing the assets of a company to employees, as J.S.L. did, tends to place them in the position of passive beneficiaries, rather than active advocates and practitioners, of a cooperative ethos. An indicator of such passivity is the way ‘employee involvement in governance is typically kept clearly distinct from day-to-day management’ (Pendleton, 2011: 332). The JLP governance structure is extensive in its design and scope, but it can prove difficult to operate effectively on a day-to-day basis. Historically, the various channels of representation have tended to be disproportionately populated by managers and time-serving, institutionalized staff (Cathcart, 2009; Erdal, 2011). The governance structure may, consequently, deliver only a weak, and perhaps ritualistic, form of accountability. Participants may be complicit in managerial decision-making rather than watchful and questioning of it (Cathcart, 2009; 2013a)—a posture that reflects Partners’ exclusion from share ownership and, more specifically, their powerlessness to exert pressure upon JLP managers through the market for corporate control in the form of their collective divestment.

Managers’ accountability to Partners is indirect and collective through the Partnership Council and its associated bodies. The day-to-day approach to managing JLP tends to be predominantly technocratic, with decisions being rationalized post hoc by justifying their compliance with Partnership principles, and thereby minimizing the risk of challenge by the Partnership Council or its sub-committees (Cathcart, 2009). Managerial authority is thus exercised by virtue of specialist knowledge and/or previous experience, and not primarily through a democratic mandate. Qua managers, rather than Partners, their status and expertise provides them with a platform for articulating and influencing the ‘interests’ of the Partners in a way that is congruent with a managerialist agenda. 27

JLP and ‘beyond capitalism’?

Finally, we relate our discussion of JLP’s structures of ownership and governance to the question of how capitalism might be transformed into a less divisive and destructive political economy. Directly pertinent to this issue is Wolff’s (2009) thesis that the prospects of such transformation are impeded by structures of ownership and governance that are entrenched, though not immutable. Wolff argues that capitalist structures bestow monopoly power upon boards of directors, drawn from a narrow elite, whose decision-making has increasingly become exclusively geared to maximizing shareholder value, and so intensifies the economic exploitation and political oppression of labour by capital. The broad-brush remedy proposed by Wolff (2009) is for

workers inside enterprises to displace their boards and become their own collective boards of directors … As people once dethroned kings in favour of universal suffrage, workers can abolish boards of directors in favour of receiving and distributing the surpluses/profits themselves … [In this process, employees are understood to become] their own surplus/profit appropriators … [and are] … more personally invested in the quality of their work. (pp. 14, 15)

Wolff (2009) is silent on the question of how boards are to be ‘dethroned’, except to say that it will somehow be accomplished by workers. JLP offers an alternative kind of ‘dethronement’ in the form of abdication. Relinquishing ownership by gifting the assets of the company to present and future employees does, however, present significant challenges in terms of worker/Partner ‘investment’ in post-capitalist, cooperative enterprise. Wolff’s ‘new strategy of “reform plus”’ is, nonetheless, to a degree foreshadowed in the Constitution and structures of JLP. JLP admittedly falls short of Wolff’s vision, 28 but it is important to recall, once again, that few cooperatives fully exemplify cooperative principles and/or wholly embrace all aspect(s) of Wolff’s ‘reform plus’. Taking this into account, Wolff’s ideas are relevant for conducting a thought experiment where a transition occurs in which enterprises are incentivized, or required, to adopt JLP structures of ownership and governance. 29 With this change, as Wolff (2009) anticipates, ‘capitalist boards of directors’ would be deprived of the resources and incentives to ‘shape political processes … to secure their situations’ (Wolff, 2009: 16). There would, as he anticipates, be a major politico-economic shift as ‘the absence of economic democracy inside enterprises [would no longer] systematically undermine political democracy outside them’ (Wolff, 2009: 16). Such a possibility connects to wider debates. Those debates include discussions circling around the notion of critical performativity within CMS. Their focus is upon on how a transition towards a less divisive and destructive post-capitalist political economy might develop that is not premised upon abolition of capitalist privately owned means of production (assets) and/or planning and command by the state. We have seen how, in the JLP model, the assets of the organization are held in Trust for the benefit of its present and future employees/Partners. And we have shown how, despite lacking the ultimate means of sanctioning managers by selling their shares, the JLP governance structure permits, but does not compel, Partners to exercise some control of management as vouchsafed by the Constitution.

Wolff’s ‘reform plus’ proposal invites further reflection on the critical performativity of JLP. If Partners’ ‘happiness’ is framed primarily in terms of self-centred concerns, such as working conditions, it displaces any more extensive concern for diverse stakeholders and the natural environment. When the ‘happiness’ of Partners and a ‘successful’ business is defined in terms of financial performance and increasing the annual bonus, there is a more tenuous basis for ‘shar[ing] common interests with surrounding communities’, let alone for paying greater attention to ‘air, water, ground and other pollution by the enterprise’ (Wolff, 2009: 15). JLP structures of ownership and governance are currently myopic with respect to stakeholders other than Partners, and to wider considerations—such as sustainability. While this myopia could be ascribed to the timing of JLP’s formation, and its history as a business succession firm, it is also evident in more recently established cooperatives where employees directly own the shares, such as Mondragón. The primary and overriding aim of Mondragón is confined to serving the people and culture of the Basque region. In common with Mondragón, JLP structures of ownership, and especially governance, require radical revision if their current emphasis on financial performance for the benefit of an inner circle of Partners is to be re-oriented to facilitate participation by a wider constituency of stakeholders, deep commitment to sustainability and/or respect for the commons.

Summary and conclusion

Our examination of the ownership and governance structures of John Lewis is intended to advance and deepen reflection and debate upon possibilities for a ‘critically performative’ transformation of capitalism, and not just its recuperation. We have noted that the ownership structure of JLP protects future as well as current Partners from the attentions of distant investors. We have also shown how the JLP governance structure makes managers formally accountable to Partners through a range of channels. Endorsement of these progressive, putatively post-capitalist features of JLP has been qualified by reference, respectively, to the infantilizing and managerially colonizing effects of its structures.

The very existence of JLP is, nonetheless, significant as it presents a direct challenge to the necessity of what has become normalized as the joint-stock form of capitalist enterprise. Since 1928, JLP has delivered comparatively secure employment, good working conditions and generous fringe benefits to its Partners. The vitality and longevity of the Partnership is attributable, at least in part, to its transgression of Marx’s dictum that ‘co-operative societies … are of value only insofar as they are the independent creations of workers and not protégés either of governments or of the bourgeoisie’ (Jossa, 2005: 8, citing Marx, 1875: 94). JLP demonstrates that it is possible to develop and sustain a highly successful business without recourse to the ownership and governance structure of the joint-stock form of capitalist enterprise. Yet, JLP’s philanthropic formation and its paternalistic structures of ownership and governance also make its cooperative status, and its emulation as an alternative model of enterprise, somewhat problematical, but without rendering its claim to offer an alternative, even a critically performative one, wholly indefensible or irrelevant. JLP is not an ‘independent creation of workers’ (Marx, 1875). Indeed, and in common with most cooperatives, it does not comply with the more idealized principles ascribed to them. But, in a market context, dominated by joint-stock enterprises, JLP’s limitations may also be a source of strength or at least of durability.

What, then, are the ‘critically performative’ credentials of JLP? JLP scores comparatively highly on the cooperative principles of ‘member economic participation’ (e.g. through bonuses and benefits) and ‘autonomy and independence’ (JLP operates independently of external shareholders). The JLP Constitution confers considerable formal powers on Partners and protects them from the control of JLP assets by distant investors. But its Constitution also assumes, or at least leaves unquestioned, the legitimacy and continuation of capitalism as a politico-economic system. There is an assumption that the JLP Constitution can be faithfully enacted in an economy dominated by joint-stock enterprises. But whether or not that supposition is supportable, the very existence of the Trust form tacitly challenges and frustrates the development and expansion of capitalism by ruling out the control of JLP assets by external shareholders.

Turning to the question of how JLP incorporates ‘democratic member control’, its scope has been circumscribed from the outset. Managerial decision-making is accountable to Partners through a range of mechanisms and media, but, crucially, managers are not appointed or elected by the Partners: J.S.L.’s vision of the Partnership was not one of collective self-determination. Symptomatic of this deficit, the most influential person in JLP—the Chairman—nominates his or her successor subject to the approval of the Partnership Board but without any formal consultation with Partners. Within the JLP governance structures, there is also vulnerability to over-prioritizing conventional commercial objectives, such as retaining or expanding market share, without equivalent or greater regard to their democratic determination or endorsement. Those pressures are especially difficult to resist when strong financial performance is a prerequisite of meeting Partners’ expectations, including receipt of a substantial annual bonus on top of funding an exceptionally generous package of fringe benefits. For those committed to the cooperative values of the Partnership, the challenge is not ‘simply’ to demonstrate the viability as its business model but, above all, to nurture and strengthen a strong counter-ideology capable of resisting pressures to circumvent or compromise ‘democratic member control’ and thereby translate formal accountability into its substantive operation.

Despite its Partnership Council and the ‘Critical Side’, the JLP governance structure operates, with an occasional challenge, to facilitate and legitimate Partners’ loyal and largely passive participation in the pursuit of a managerial elite’s (benevolent) priorities, which this elite represents as imperative to ensuring the future ‘happiness’ of the Partners (Cathcart, 2009, 2013a). Since Partners have no direct power to shape the financial strategy of the firm through the market for corporate control, they can only endeavour to convince different boards and committees to heed and adopt their preferences. JLP Partners are, in principle, collectively sovereign but, in practice, JLP’s structures of ownership and governance co-opt and colonize, as well as facilitate, Partners’ powers of self-determination.

These observations signal our ambivalence about JLP as an example of ‘critical performativity’ (Spicer et al., 2009). JLP can be read as a ‘subversive intervention’ (Spicer et al., 2009: 538) insofar as it denies absentee investors access to, and control of, its assets. If the UK’s Deputy Prime Minister’s advocacy of a ‘John Lewis economy’ was to be realized, then opportunities for the reproduction and further enrichment of the capitalist class would be significantly curtailed. Currently, however, even the critical performative potential of the Partnership model is impeded by its paternalist structures. Exclusion of Partners’ participation in the market for corporate control is reflected in, and compounded by, a weak form of ‘democratic’ governance, where managers are accountable to Partners but not controlled by them.

For these reasons, it is implausible to characterize JLP as an unequivocally progressive or emancipatory form of organization. It is deeply infused with paternalism and the narcissistic spirit of contemporary capitalism. Its ownership and governance structures are dedicated primarily to mitigating needless ‘perversions’ of capitalism, rather than their eradication. Moreover, such mitigation is pursued without regard to the inclusion of other stakeholders, such as suppliers, and to the consideration of socially responsible objectives, such as sustainability. For variety of reasons, it is doubtful that the JLP model ‘offer(s) a powerful response to today’s and tomorrow’s economic, social, and environmental needs’ (Webb and Cheney, 2013: 24). Framed within a Constitution that pays little regard to other stakeholders, let alone to the natural environment, JLP presents a ‘response’ to ‘ environmental needs’ that is highly partial, rather than ‘powerful’.

What, then, might be done to tackle these and other structural limitations of the JLP model? Empirical research is undeniably helpful in generating findings with which to probe and challenge received understandings (e.g. Cathcart, 2013a, 2013b). Yet, as such evidence is inescapably theory-dependent, generating additional data will not resolve interpretive differences except disingenuously through evidence-based fiat. Indeed, focussing scholarly effort primarily on conducting further empirical studies may inadvertently (or perhaps intentionally) displace or obscure the structural conditions of possibility of the practices being investigated. Such conditions include the structures of ownership and governance which support but also circumscribe those practices.

Returning to the question of whether JLP offers an example of ‘critical performativity’, our answer is, with many reservations, cautiously affirmative. Crucially, the Trust, unlike the joint-stock enterprise, safeguards the assets created by employees among other contributors, and makes them, rather than absent shareholders, the primary beneficiaries. It also makes Partners the custodians of JLP assets through a comparatively democratic form of governance. The ownership and governance structures designed by John Spedan Lewis have proved remarkably practical and resilient. They have provided some restraint upon tendencies towards ‘perversion’, whether those arise from the avarice of owners or the unchecked power of managers. And, it may just be that areas of deficit, especially with regard to democratic member control, have facilitated the survival of JLP in a context where it faces intense competition from joint-stock enterprises that are not ‘hampered’ by the restrictions upon access to capital and upon managerial prerogative faced by JLP.

Finally, it is relevant to recall that JLP was bequeathed to its Partners, and that the conversion of joint-stock enterprises into equivalents of JLP would require a comparable and rather improbable act of philanthropic generosity on the part of their shareholders, perhaps facilitated by appropriate tax breaks. With regard to governance, it has been noted how its structures tend to infantilize its Partners and co-opt them, as passive participants, within practices that accommodate managerialism even if they also curb its worst excesses. So, would disestablishing the Trust better instantiate or advance ‘critical performativity’? It is by no means self-evident that its dismantlement would be advantageous for future employees or for other stakeholders (customers, suppliers, the wider community or natural environment). Its dissolution would risk distant investors gaining control of John Lewis which, in turn, would likely result in its governance structures being weakened or even dismantled rather than strengthened and extended. If, instead, the Partnership structure were somehow to replace every joint-stock company, there would be a substantial reduction in the external pressures which currently frustrate the democratization of work organizations. There would, of course, remain concerns about the infantilizing effects of the Trust and the coherence of its governance model (e.g. the role of the Chairman and the exclusion of Partners from the process of hiring managers). But latent potentials within the JLP Constitution and its structure of governance might be leveraged to build a more radical, outward-looking, 21st-century company 30 in which a revised Constitution could ensure not only that managerial appointments are collectively determined by Partners but that other stakeholders and ecological considerations become central, rather than peripheral, to JLP’s strategy and operations. Whether the retention of JLP’s existing structures of ownership and governance, or a push for their radical reform, would save capitalism, or bury it, is question to which we have offered no unequivocal answer. By leaving the question open, our intention is to stimulate further reflection and debate on the possibilities of ‘critical performativity’ and the degree to which the JLP model does, or could potentially, advance it.

Footnotes

Appendix

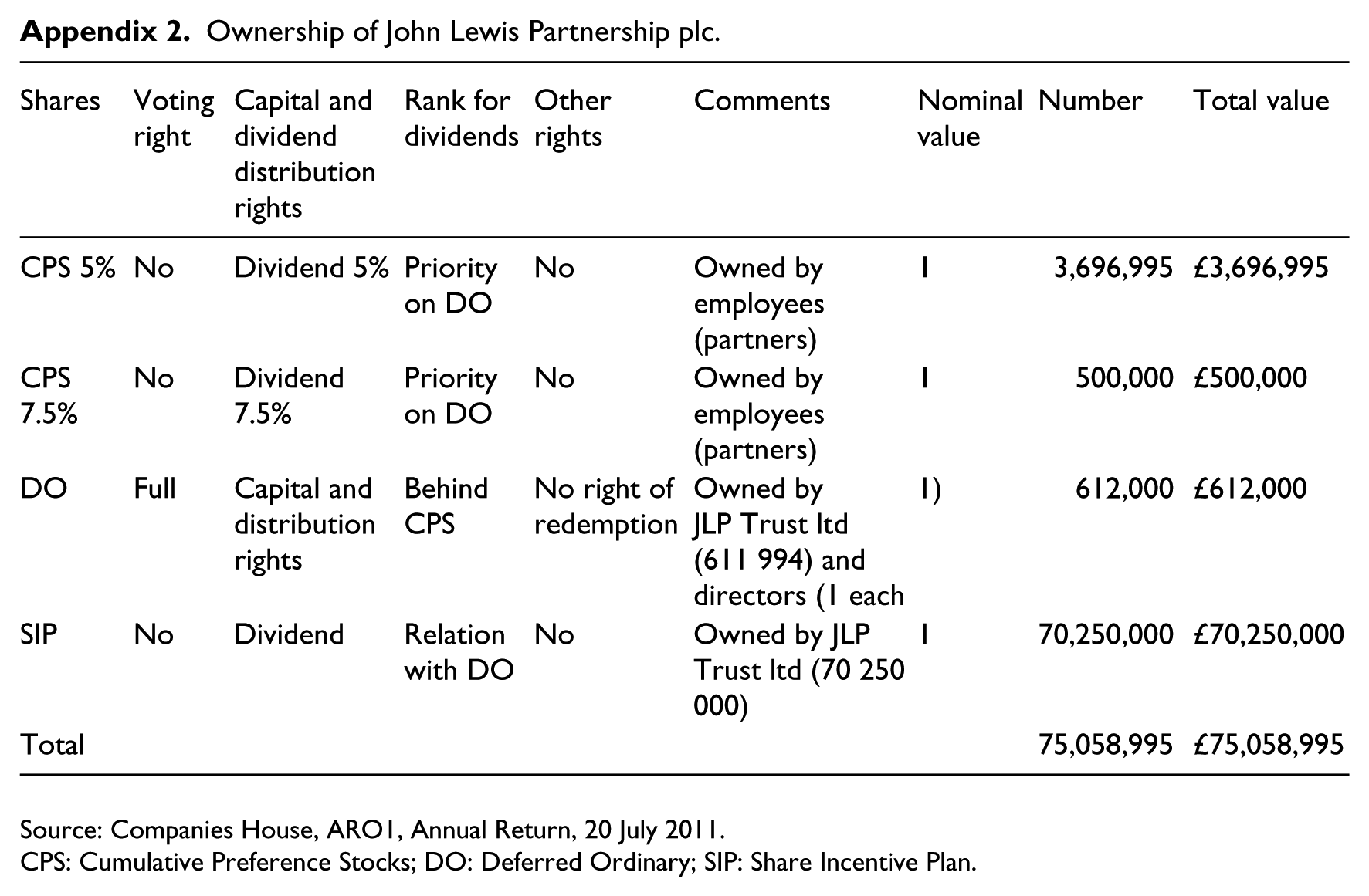

Ownership of John Lewis Partnership plc.

| Shares | Voting right | Capital and dividend distribution rights | Rank for dividends | Other rights | Comments | Nominal value | Number | Total value |

|---|---|---|---|---|---|---|---|---|

| CPS 5% | No | Dividend 5% | Priority on DO | No | Owned by employees (partners) | 1 | 3,696,995 | £3,696,995 |

| CPS 7.5% | No | Dividend 7.5% | Priority on DO | No | Owned by employees (partners) | 1 | 500,000 | £500,000 |

| DO | Full | Capital and distribution rights | Behind CPS | No right of redemption | Owned by JLP Trust ltd (611 994) and directors (1 each | 1) | 612,000 | £612,000 |

| SIP | No | Dividend | Relation with DO | No | Owned by JLP Trust ltd (70 250 000) | 1 | 70,250,000 | £70,250,000 |

| Total | 75,058,995 | £75,058,995 |

Source: Companies House, ARO1, Annual Return, 20 July 2011.

CPS: Cumulative Preference Stocks; DO: Deferred Ordinary; SIP: Share Incentive Plan.

Acknowledgements

Many thanks to Abby Cathcart, Peter Cox, Richard MacVie, Ewan McGaughey and Peter Smith (Partner Constantin) as well as to participants in the ‘Cooperatives’ UMASS-Boston CMS Paper Development Workshop held in August 2012, for their very useful help and comments in the preparation of this article. All errors remain ours.

Funding

This research received support from AG2R LA MONDIALE Chair “Finance Reconsidered”.

Notes

Author biographies

![]() .

.

![]() .

.