Abstract

We examine whether and how mandatory climate reporting leads to changes in firms’ carbon emissions. Drawing on legitimacy theory and using a difference-in-differences design, we assess the effect of the Greenhouse Gas Reporting Program (GHGRP), introduced by the Environmental Protection Agency (EPA) in 2010, on the carbon performance defined as carbon intensity and absolute carbon emissions of affected firms. We find that firms affected by the GHGRP improve their carbon intensity significantly more than unaffected firms after the introduction of the GHGRP, but not their absolute carbon emissions. The results are robust to changes in the difference-in-differences design. Overall, our study contributes to research on mandatory climate reporting by assessing the GHGRP’s suitability to generate a real sustainable change in firms’ operations and reduce their negative impact on our climate.

Introduction

Firms experience increasing pressure to report on their carbon risks, strategies, and emissions (Eccles et al., 2011; Reid & Toffel, 2009). In this context, voluntary climate reporting initiatives such as the CDP (formerly: Carbon Disclosure Project) have emerged, which rely on the cooperation of firms. Although firms are major contributors to global carbon emissions and should act transparently and responsibly (Klettner et al., 2014), regulators can intervene when firms are not transparent about their commitment to national and international climate goals. To this end, national and international mandatory climate reporting regimes have been established (e.g., the Greenhouse Gas Reporting Program [GHGRP]). Comyns (2016) shows that reporting quality and quantity increase under mandatory climate reporting regimes, such as the European Union Emissions Trading System (EU ETS). Whether and how the reporting of carbon emission data also leads to a real sustainable change within firms in the form of reduced carbon emissions is still being discussed (Downar et al., 2021; Haque & Ntim, 2018; Jouvenot & Krueger, 2020; Qian & Schaltegger, 2017; Tomar, 2019). We contribute to this discussion from a legitimacy theory perspective by assessing the effect of a mandatory climate reporting regime on the carbon performance (operationalized as both, carbon intensity and absolute carbon emissions) of affected firms, operating in the country with the second-highest carbon emissions, the United States).

During the United Nations Framework Conference on Climate Change (UNFCCC, 2015) in Paris in November and December 2015, 197 parties agreed to the goal of limiting the rise in global temperature to significantly below 2°C (preferably 1.5°C) compared with the preindustrial level. This goal requires tremendous efforts to reduce carbon emissions in the public as well as the private sector. According to a special report by the Intergovernmental Panel on Climate Change (IPCC), the remaining carbon budget for a 66% likelihood of limiting global warming to 1.5°C amounts to 420 GtCO2, and about 580 GtCO2 for a 50% likelihood (Rogelj et al., 2018). In other words, carbon neutrality must be reached in about 20 years (66% chance) or 30 years (50% chance), respectively. Given the serious consequences that are expected in a scenario of unmitigated climate change (Steffen et al., 2018), the international consensus is that all parties that contribute to it have a responsibility to mitigate their carbon emissions (World Commission on the Ethics of Scientific Knowledge and Technology, 2010) and that real sustainable change is required. Thus, environmental corporate social responsibility (CSR) such as carbon emissions management has become an important aspect of societal expectations toward firms (Flammer, 2013). The increasing political and societal awareness of the serious consequences of climate change led to a growing number of regulations directly aimed at decreasing carbon emissions. Examples include the introduction of carbon taxes (e.g., Norway and Switzerland), climate-friendly mobility concepts (e.g., lowering the VAT rate on train tickets in Germany), and emissions trading systems (e.g., the EU ETS).

Drawing on legitimacy theory, we analyze whether and how a mandatory climate reporting regime, which aims at improving carbon transparency, is related to subsequent firm carbon performance improvements. Given a rising societal awareness of the consequences of climate change, mandatory reporting and the public disclosure of emissions can lead to firms being exposed to increasing societal expectations to improve their carbon performance (e.g., Deegan, 2002; Dowling & Pfeffer, 1975). Firms respond to such expectations to ensure their legitimacy, that is, their “license to operate” (Newson & Deegan, 2002). Therefore, mandatory climate reporting can trigger substantial firm carbon performance improvements.

The Environmental Protection Agency’s (EPA) GHGRP provides a unique setting to test this assumption. This mandatory climate reporting regime mandates firms to report emissions from facilities that emit 25,000 metric tons or more of carbon dioxide equivalent per year in the United States (EPA, 2020). It covers direct carbon emitters, suppliers of fossil fuel and industrial gas as well as facilities that store carbon dioxide underground for sequestration or other reasons. Certain industries such as the agricultural industry are exempt from the GHGRP. Carbon emissions are reported at the facility level annually. The EPA verifies the collected data by themselves and subsequently publishes it on its website. The aim of the GHGRP is to better understand the sources of carbon emissions in the United States and to support the development of further regulations to reduce emissions. Failure to comply with the GHGRP is considered a violation of the Clean Air Act and carries with it a fine of up to US$45,268 per day (EPA, 2021a, 2021b). The EPA (2020) estimates that the facilities covered by the GHGRP are responsible for approximately 50% of the total U.S. carbon emissions. In contrast to the EU ETS, the GHGRP is not connected to a carbon emission reduction program and pricing mechanism. Consequently, improvements in carbon performance subsequent to the introduction of the GHGRP may be directly attributable to the mandatory reporting effect, and results are not distorted by carbon pricing effects.

Covering the period from 2007 to 2016, we apply a difference-in-differences design to estimate the effect of the GHGRP on the carbon performance of affected firms after its introduction in 2010. Our results show that while there were no significant differences in the development of the carbon performance between firms affected by the GHGRP and unaffected firms prior to the introduction of the GHGRP, subsequent to its introduction affected firms show a stronger improvement in their carbon intensity. This observation is robust to changes in the difference-in-differences design and the sample composition. However, the analysis of absolute carbon emissions reveals a surprising result: Firms affected by the GHGRP did not reduce their absolute emissions as strongly as unaffected firms after the introduction of the GHGRP. Overall, our study provides evidence that the effect of the introduction of a mandatory climate reporting regulation is limited to improvements in firms’ carbon intensity (meaning improvements in the efficiency of firms’ carbon emission producing operations). That means a mandatory climate reporting regime, such as the GHGRP, can provide necessary incentives to limiting firms’ contribution to climate change, but is not sufficient by itself to reach national or international climate goals.

The contributions of our study are fourfold. First, we add to the strand of literature that discusses whether climate reporting has implications on the carbon performance of reporting firms. Existing studies mainly focus on the effects of voluntary climate reporting (Haque & Ntim, 2018; Qian & Schaltegger, 2017), of mandatory climate reporting on firms’ aggregated facility emissions falling under a certain regulation (Downar et al., 2021; Matisoff, 2013; Tomar, 2019) and of mandatory climate reporting on global firm carbon performance in a country with an existing carbon pricing scheme (Jouvenot & Krueger, 2020). We extend this scope by analyzing the impact of the introduction of a mandatory climate reporting regime on the global carbon performance of firms operating in a country without a national carbon pricing scheme. The extension to the global firm carbon performance is important because an analysis based on facility emissions that fall under a certain regulation cannot capture whether firms’ shift emissions to unregulated facilities (i.e., in the case of the GHGRP, facilities in the United States that do not fall under the GHGRP as well as facilities outside of the United States). Moreover, a carbon pricing scheme may distort the effects of the mandatory climate reporting regime. Second, we contribute to the question how mandatory climate reporting might induce a real sustainable change in firms’ operations. Drawing on and adding to legitimacy theory, we provide insight into how mandatory disclosure regimes can lead to different real outcomes compared with voluntary disclosures. Research argues that voluntary environmental reporting is used for impression management purposes to ensure firms’ legitimacy without substantially changing their operations (Archel et al., 2009; Deegan, 2002; Delgado-Márquez et al., 2017; Haffar & Searcy, 2020; Kraft, 2018; O’Donovan, 2002). Under a mandatory climate reporting regime, substantial changes in firms’ carbon emissions can be triggered, because opportunities for impression management are much more limited than under voluntary disclosure. Third, we provide new insights into the important differentiation of carbon intensity and absolute carbon emissions (Busch & Hoffmann, 2011). Although the studies by Downar et al. (2021), Jouvenot and Krueger (2020), and Tomar (2019) find improvements in both carbon performance variables, we obtain opposite results for the two variables, which underlines the need for more detailed investigations of the relationship between carbon intensity and absolute carbon emissions. Fourth, knowledge about the influence of climate policies on firms’ carbon performance and the mechanisms of improvement is essential for the future design of policies toward a low carbon economy. Previous studies have focused on carbon taxes or ETS that are similar to the GHGRP in reporting requirements but connected to a carbon price (Bel & Joseph, 2015; Haites, 2018), or consider only emissions from electricity generation in a specific region (Murray & Maniloff, 2015). Current developments in CSR reporting are moving in the direction of mandatory reporting regimes, for example, the Corporate Sustainability Reporting Directive (CSRD) in the EU, the Large Employer Emergency Financing Facility (LEEFF) in Canada, or the Business Responsibility Report (BRSR) by the Security and Exchange Board of India. We show that in the case of the GHGRP, the introduction of a mandatory reporting regime that focuses on carbon emissions has limited but nevertheless positive implications on firms’ carbon performance, contributing to the discussion whether and how the reporting of nonfinancial information can materialize into a real outcome (de Bakker et al., 2020).

The remainder of this article is structured as follows. In “Theoretical Background, Related Literature, and Hypothesis Development” Section, we present the theoretical background, related literature and derive our hypothesis. “Research Design” section describes our research design. “Empirical Results” section presents the results of our empirical tests and is followed by a detailed discussion in “Discussion” Section. “Conclusion” section concludes our study.

Theoretical Background, Related Literature, and Hypothesis Development

Theoretical Background

Legitimacy theory describes firms as part of a broader social system, that is, the society (e.g., Deegan, 2002). Firms can only survive when society considers their operations legitimate. Suchman (1995) defines legitimacy as “a generalized perception or assumption that the actions of an entity are desirable, proper, or appropriate within some socially constructed system of norms, values, beliefs, and definitions” (p. 574). In other words, firms are considered legitimate if their activities do not violate the rules and values of the society (Dowling & Pfeffer, 1975). According to Deegan (2002), legitimacy is necessary for a firm’s survival for two main reasons. First, legitimate firms have better access to critical resources, such as human and financial capital. Second, illegitimate firms could be confronted with various forms of retribution which threatens their ability to survive (e.g., loss of sales or fines). Consequently, firms try to align their operations with the (changing) rules and values of society to ensure their legitimacy, which is seen as a “license to operate” (Newson & Deegan, 2002).

Environmental legitimacy refers to the perception that a firm’s environmental performance is congruent with society’s rules and values. In this context, climate change has become an important issue. The growing concern about the speed and consequences of global warming as documented by the IPCC (Rogelj et al., 2018) has led to regulatory measures (e.g., the EU ETS) and rising public attention. The contribution of private firms to climate change is an important aspect in this debate (Carbon Disclosure Project [CDP], 2017). Although the United States have a mixed history of climate policy, failing to ratify the Kyoto Protocol and withdrawing from the Paris Climate Accord, climate change is a legitimacy issue for firms in the United States. Twenty-four U.S. states and the District of Columbia have established their own carbon emission reduction targets (Center for Climate and Energy Solutions, 2021). Firms also need to consider public opinion to maintain legitimacy and in the United States, 75% of survey respondents support the idea to “Regulate CO2 as a pollutant,” 70% think that “Corporations should do more to address global warming” and 60% believe “The President should do more to address global warming” and these opinions have not changed significantly since 2010 (Marlon et al., 2020). In 2008, Barack Obama’s campaign also had a strong focus on climate change issues and emission reductions (Broder, 2008).

According to Dowling and Pfeffer (1975), there are three distinct approaches for firms to gain and maintain (environmental) legitimacy: first, the firm can adapt its structure by changing its goals, methods of operations and output. Legitimacy concerning a firm’s structure is referred to as institutional legitimacy (Deegan, 2019). Second, the firm can try to manipulate society’s norms and values through communication so that its practices appear legitimate. Finally, the firm can attempt, again through communication, to become associated with symbols or values, which appear congruent with the society’s norms and values. The latter two strategies are often referred to as strategic legitimacy or impression management since they aim at changing stakeholders’ perception of the firm without changing its operations (Deegan, 2019).

Related Literature and Hypothesis Development

Research has shown the examples of strategic legitimacy through the use of voluntary environmental reporting and impression management (Archel et al., 2009; Deegan, 2002; Delgado-Márquez et al., 2017; Haffar & Searcy, 2020; Kraft, 2018; O’Donovan, 2002). Some empirical studies show that poorer environmental performers are more likely to disclose nonfinancial information voluntarily to legitimize their poor performance (Cho et al., 2012; Cho & Patten, 2007; Patten, 2002). Specifically focusing on climate reporting, results are contradictory. Although Qian and Schaltegger (2017) and Siddique et al. (2021) suggest a positive relationship between carbon disclosure and carbon performance, Haque and Ntim (2018) find that firms adopting voluntary reporting guidelines, such as the guidelines from the Global Reporting Initiative (GRI), are more likely to implement carbon reduction measures, but do not improve carbon performance. Consistently, Belkhir et al. (2017) and Bernard et al. (2015) find no correlation between GRI reporting and firms’ carbon emissions. We are investigating whether the introduction of mandatory reporting leads to real changes in firms’ carbon performance, as in this scenario firms are no longer able to use reporting as an impression management tool.

Although several mandatory climate reporting regimes were implemented in recent years, investigations of their effect on firms’ carbon performance are scarce (Hahn et al., 2015). Tang and Demeritt (2018) explore the rationales for and impacts of carbon reporting by means of a systematic documentary analysis and semi-structured interviews. They find that carbon reporting has an influence on internal operations and the public image of firms but less on firms’ carbon performance. Downar et al. (2021) show for a sample of 24 firms headquartered in the United Kingdom that the introduction of the U.K. Companies Act 2006 (Strategic Report and Director’s Report) Regulations 2013 led to an improvement in the firm carbon performance. However, Downar et al. (2021) focus on facility emissions falling under a certain regulation, not on firms’ global direct emissions. Therefore, they do not control for a possible shift of emissions to facilities that operate outside of regulation. The same holds for Matisoff (2013) and Tomar (2019), who investigate the effects of different U.S. state-level mandatory climate reporting regimes (Matisoff, 2013) and the GHGRP (Tomar, 2019) and find no (Matisoff, 2013) and a positive (Tomar, 2019) effect on carbon performance. Moreover, in the setting of Downar et al. (2021), a carbon pricing mechanism, the EU ETS, already exist prior to the introduction of the new regulation, which makes it difficult to disentangle the effects of the mandatory reporting regime and the carbon pricing mechanism on carbon performance. The same applies to Jouvenot and Krueger (2020), who investigate the effect of the U.K. Companies Act on global firm-level GHG emissions.

Our study differs from these previous studies by assessing the effect of the introduction of a mandatory climate reporting regime on firms’ global carbon intensity and absolute carbon emissions without the additional effects of a comprehensive carbon pricing scheme. This is necessary to derive implications for legitimacy theory, which assumes that firms adapt their operations (i.e., at least improve their carbon intensity) to meet societal values besides being motivated by regulatory pressure. Consequently, conclusions regarding legitimacy theory are limited for most of the aforementioned studies, because they are conducted in a setting with a carbon pricing scheme (e.g., the EU ETS).

In our setting, we argue that the collection and disclosure of carbon emission data through public institutions as well as easy and free access to the data might improve the trustworthiness of the data and enable society to surveil the development of firms’ carbon performance. This leads to enhanced societal pressure on firms to improve their carbon performance.

Based on the arguments above, we formulate the following hypothesis:

Hypothesis 1 (H1): Firms affected by the GHGRP will improve their carbon performance subsequent to the introduction of the reporting regime to a greater extent than unaffected firms.

Research Design

Sample

We collect data from different sources for our analysis. We obtain carbon emission data from Trucost and cover the time period from 2007 to 2016. Trucost is a specialized provider of firm-level environmental information, which employs an “environmentally extended input-output” model that differentiates environmental impacts of 464 business activities to estimate emissions of nonreporting entities. Theoretically, in a voluntary carbon reporting environment, firms could make the choice to disclose their carbon emissions dependent on how well they perform. That means, firms which already have a good carbon performance or are on their way to achieve it will be more likely to disclose their emissions voluntarily, especially prior to the disclosure mandate. Firms with lackluster performance are more likely not to disclose. This would introduce a bias toward good carbon performers in our dataset and would make it more difficult to identify improvements in carbon performance. By using Trucost carbon emission data and including carbon emission estimations for nonreporting firms, we mitigate this bias. Busch et al. (2022b) show that the reliability and consistency of Trucost estimated Scope 1 emissions are similar to actual reported Scope 1 emissions. In addition, the inclusion of these estimations allows us to investigate carbon emissions before the respective firms started reporting or the mandatory regulation (i.e., the GHGRP) was introduced. This increases our overall sample size and helps reducing missing observations of nonreporting firms. Thus, the Trucost data are well suited as a base for our measures of carbon performance.

We exclude firms from the financial industry in our analysis, since these firms typically do not face issues in dealing with Scope 1 emissions and the unique characteristics of financial firms can skew results (Delmas et al., 2015). This leads to an initial sample of 1,458 U.S. firms with 8,017 firm-year observations. We then identify firms that own and operate facilities falling under the GHGRP by collecting facility information through the EPA Facility Level Information on Greenhouse Gases Tool (FLIGHT) and hand-match the International Securities Identification Number (ISIN) for each firm that is listed in the FLIGHT as a facility owner. In cases where a facility is not 100% owned by a single firm, we identify the firm owning the largest share as the principal owner. Using the ISIN, we then combine the carbon emission data from Trucost with the facility ownership information from the FLIGHT system. This allows us to split our full sample into a treatment sample of firms that own facilities subject to the GHGRP (i.e., regulated firms) and a control sample of firms that do not own such facilities (i.e., unregulated firms). The treatment sample contains 263 firms with 1,910 firm-year observations and the control sample 1,195 firms with 6,107 firm-year observations. We combine these carbon emission data with financial information from Refinitiv Datastream. Due to data availability, we arrive at a final sample of 1,454 firms and 7,961 firm-year observations. We winsorize all continuous variables in our analysis at the highest and lowest 1% level to curb the effect of potential outliers in the data.

Variables

In our analyses, the dependent variable is carbon performance. We operationalize this variable as a process-based measure, carbon intensity (Scope 1 Intensity), and as an outcome-based measure, absolute total emissions (Log Scope 1). Scope 1 Intensity is calculated as Scope 1 emissions (in metric tons) divided by total assets (in US$1,000). It captures firms’ efforts to reduce carbon emissions in their operations, while controlling whether firms are expanding/reducing their operations (Busch et al., 2022a). The measure of intensity based on total assets captures the overall efficiency in firms’ operations; however, it does not account for fluctuations (e.g., a “bad year” where sales decreased but assets remain unchanged). Log Scope 1 is measured as the logarithm of a firm’s total Scope 1 emissions. Taking the natural logarithm allows for better comparison between firms, since, for example, firms with high emission can also reduce their emissions more in absolute terms. In contrast to process-based measures, outcome-based measures like Log Scope 1 are often not able to fully capture managerial efforts aimed at reducing carbon emissions, since they disregard changes in the amount of firms’ operations (Busch & Hoffmann, 2011). However, absolute emissions are an important factor when it comes to evaluating any policy aimed at addressing climate change. Emission intensity and absolute emissions are thus complementary measures of firm carbon performance.

Both dependent variables, Scope 1 Intensity and Log Scope 1, build on the emissions targeted by the GHGRP, which are Scope 1 (direct) emissions. Although Scope 2 and 3 (indirect) emissions are important in certain industries, they are under the reporting firms’ discretion to a much lesser degree than Scope 1 emissions and instead depend on other external factors, like energy prices or the availability of renewable energy providers in the reporting firms region. Therefore, we only focus on emissions that are directly affected by the regulation (i.e., Scope 1 emissions). Firms’ total Scope 1 emissions are a good basis for our analysis because they are not affected if firms shift production (and, thereby, carbon emissions) from facilities falling under the GHGRP to other facilities (these can be facilities within the United States, which do not reach the threshold value of the GHGRP, or facilities outside the United States). Moreover, carbon emission data on facility level are only available after the GHGRP introduction, while firms’ Scope 1 emissions are already available before the introduction. This enables us to measure changes in facility-based emissions around the GHGRP introduction. In our sample, direct facility-level emissions constitute the main portion of firms’ Scope 1 emissions. On average, Trucost Scope 1 emissions of sample firms regulated by the GHGRP consist of 80% facility-level emissions, which are covered by the GHGRP and 20% other emissions (i.e., outside the GHGRP).

In our analysis, we investigate the effect of the GHGRP introduction on U.S. firms’ carbon performance through a difference-in-differences estimation. With the introduction of the GHGRP in 2010 (i.e., the treatment), it became evident to firms that the data collected by the EPA would eventually be made public, and thus reporting high emissions might threaten a firm’s legitimacy. Accordingly, we analyze effects following the treatment by creating a dummy variable Post. The variable takes the value of 0 for years before the treatment in 2010 and the value of 1 starting with the treatment year. We use a dummy variable Treat to capture firms affected by the GHGRP. Treat takes the value of 0 for firms that are not directly affected by the GHGRP (i.e., firms which do not own regulated facilities) and the value of 1 for firms that own regulated facilities and are thus directly affected. The interaction of Post with the Treat variable allows us to measure the difference in the carbon performance development between affected and unaffected firms after the treatment. For further analyses, we also create a subsample where treatment and control firms are limited to industries characterized by a high-emission intensity in the following sectors: Oil & Gas (ICB 0001), Basic Materials (ICB 1000), Industrials (ICB 2000), and Utilities (ICB 7000).

We also control for several other factors that could explain firms’ carbon performance. The amount of property, plant, and equipment (PPE) indicates the extent to which a firm relies on physical production assets in its business. We measure PPE Intensity as the ratio of the net value of PPE to total assets. A high PPE Intensity indicates that a firm relies more heavily on physical production processes, which typically causes more carbon emissions compared with a firm, for example, from the service industry, which requires less PPE in its production processes (Trinks et al., 2020). Therefore, we expect PPE Intensity to be positively correlated with carbon intensity and absolute carbon emissions. We use a firm’s total assets as an indicator of firm size (variable Total Assets, denominated in billion US$), which we expect to be negatively related to carbon intensity, because larger firms can have efficiency gains due to economies of scale (Clarkson et al., 2008) and positively correlated with absolute carbon emissions. We control for risk, operationalized as Leverage and calculated as the total long-term debt to common equity ratio. The reporting of carbon emissions is an essential indicator for a firm’s environmental performance and the legitimacy of its ongoing operations in which debt-holders are particularly interested (Dhaliwal et al., 2014). Thus, we expect a positive correlation between leverage and carbon performance. Finally, we control for firms’ profitability measured as the ratio of income before extraordinary items and total assets (ROA) (Barth et al., 2017), since profitable firms have more opportunities and resources available to implement measures to improve their carbon performance. This variable also controls for negative events, like a sharp decline in a firm’s profitability (e.g., due to a sudden decrease on a firm’s net sales).

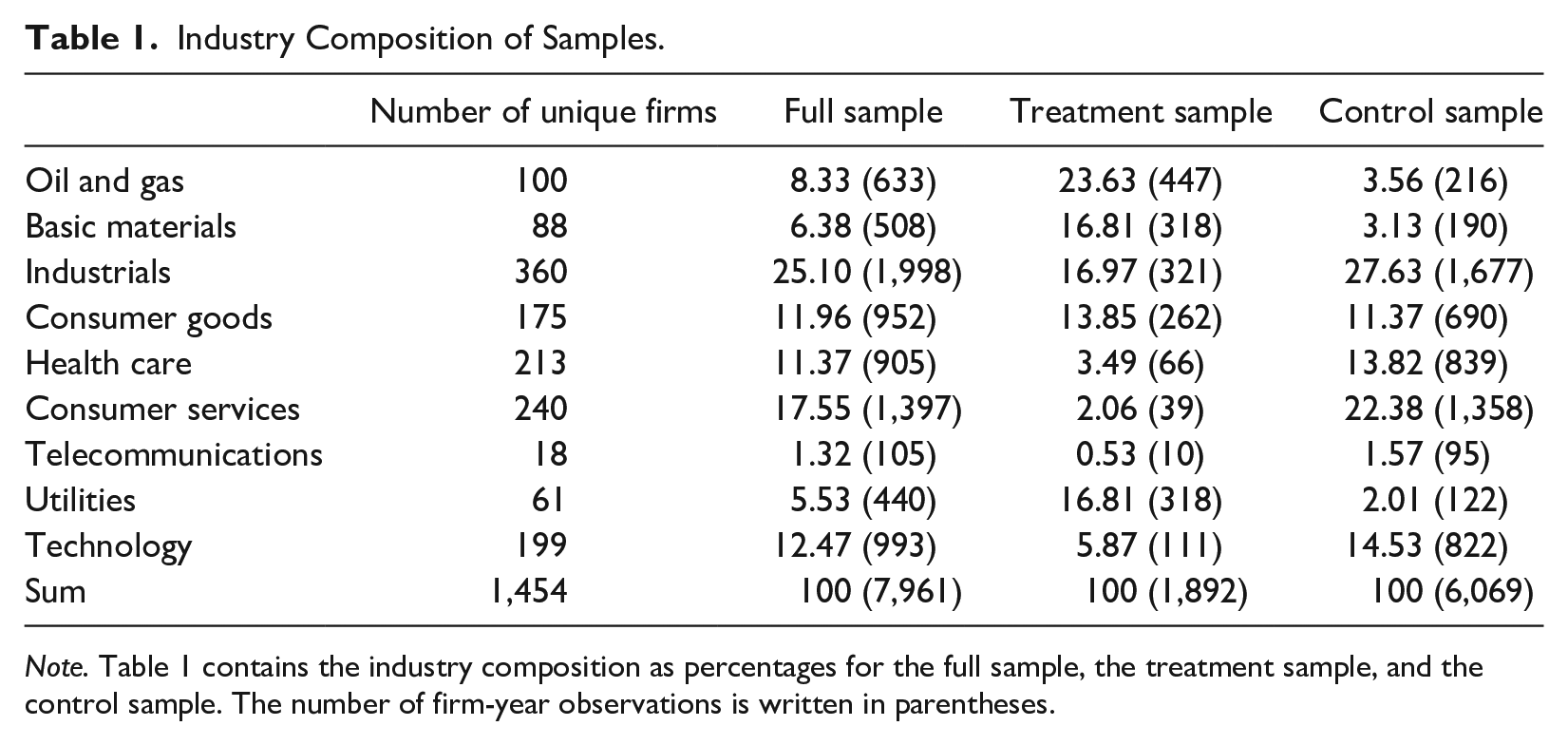

Table 1 shows the industry distribution in percent of our sample. The treatment sample (i.e., firms that own regulated facilities) shows more firms from industries with a high-emission intensity (specifically Oil and gas, Basic materials, and Utilities) compared with the control sample (i.e., firms that do not own regulated facilities). This is unsurprising because the GHGRP targets specific high-emission facilities which are typically found in these industries. Although firms in other industries also started addressing the issue of carbon emissions before 2010 (e.g., Dell in 2002; Goldman Sachs in 2006; Nike in 2008 or Pfizer in 2002), a treatment sample consisting of more high-emission firms may introduce a bias because these firms could be more motivated to reduce emissions due to greater public attention.

Industry Composition of Samples.

Note. Table 1 contains the industry composition as percentages for the full sample, the treatment sample, and the control sample. The number of firm-year observations is written in parentheses.

Model and Measurement

We test our hypothesis through a difference-in-differences analysis, where Post identifies the pretreatment and treatment period and Treat captures whether a firm is affected by the GHGRP. Therefore, our regression model has the following form:

We employ an ordinary least squares (OLS) regression with firm-clustered standard errors. The clustered standard errors help account for within-cluster correlation and heteroscedasticity (Gow et al., 2010; Petersen, 2009). We also test the parallel trend assumption that is underlying the difference-in-differences estimation method. We follow Chen et al. (2018) and apply a timing approach where we substitute our interaction term (Post*Treat) with timing variables, year−1 and year+1, which we individually interact with our treatment indicator to track the effect of the regulation over time compared with the benchmark year 2010. If the introduction of the regulation and the publication of carbon emission data have a causal effect on carbon performance, we should not see significant effects before each respective treatment. We test the parallel trend immediately around the introduction of the regulation to exclude other events that could influence firms’ carbon performance. For example, the 2008 oil price drop or the release of the new IPCC Assessment Report in 2014 can influence firms and industries to different degrees and direct more attention toward the issue of climate change. Such events could potentially introduce confounding factors.

Empirical Results

Descriptive Statistics

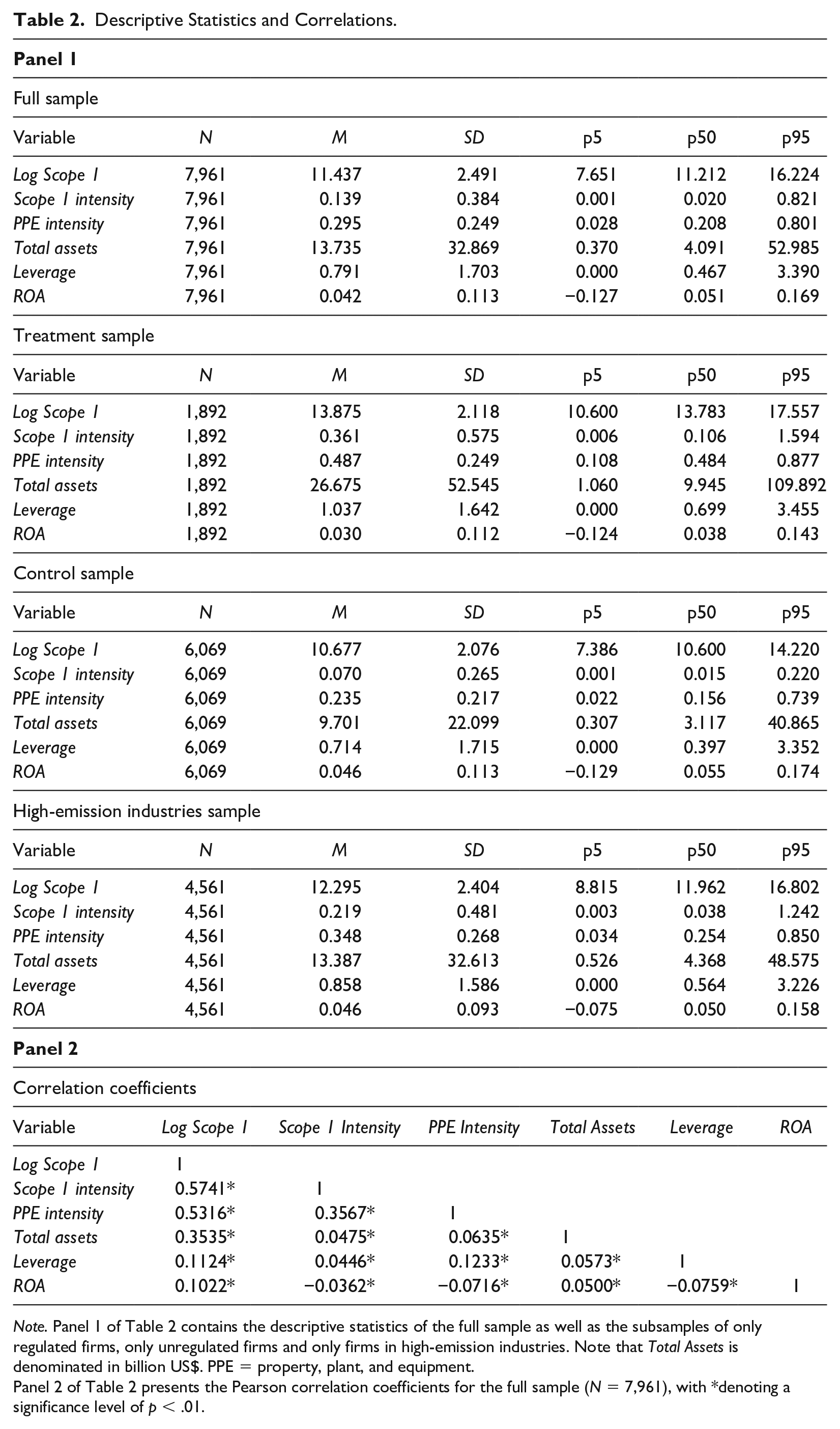

Panel 1 of Table 2 shows the descriptive statistics of all the variables in our model after winsorizing at the highest and lowest 1% level. In the full sample, on average, firms have carbon emissions of 0.139t per 1,000 US$ in total assets and value their total assets at 13.7 billion US$. This translates to roughly two million tons of carbon emissions per year (0.139*13.7). They also own, on average, 0.295 US$ in PPE per US$ of total assets. In the sample comparison between regulated and unregulated firms, we find that carbon emissions (Log Scope 1) are higher in the treatment sample than in the control sample. Scope 1 Intensity is also higher in the treatment sample (an average of 0.361t of carbon emissions per 1,000 US$ in total assets) compared with the control sample (an average of 0.070t of carbon emissions per 1,000 US$ in total assets). The Industry Classification Benchmark (ICB) classifies listed firms according to their main source of revenue. Table 1 highlights the industry composition and the predominant industries of our U.S. treatment sample (i.e., the regulated firms). When comparing the full sample with our sample of firms in high-emission industries, we see that on average firms in the high-emission industries sample have a higher Scope 1 Intensity than the full sample (0.219t of carbon emissions per 1,000 US$ in total assets compared with 0.139t in the full sample) but perform better than the sample of only firms regulated by the GHGRP. Although firms in the high-emission industries sample show similar Total Assets as the full sample firms, their PPE Intensity is substantially larger. Furthermore, more than 5% of firm-year observations have a leverage of 0.

Descriptive Statistics and Correlations.

Note. Panel 1 of Table 2 contains the descriptive statistics of the full sample as well as the subsamples of only regulated firms, only unregulated firms and only firms in high-emission industries. Note that Total Assets is denominated in billion US$. PPE = property, plant, and equipment.

Panel 2 of Table 2 presents the Pearson correlation coefficients for the full sample (N = 7,961), with *denoting a significance level of p < .01.

Panel 2 of Table 2 also shows the Pearson correlation coefficients of our variables. Although all coefficients are significant at p < .01, the correlation coefficients are typically low. Even the highest coefficient values (correlation of Log Scope 1 and Scope 1 Intensity; Log Scope 1 and PPE intensity) do not exceed 0.6. Therefore, we do not expect issues with multicollinearity.

Base Analysis

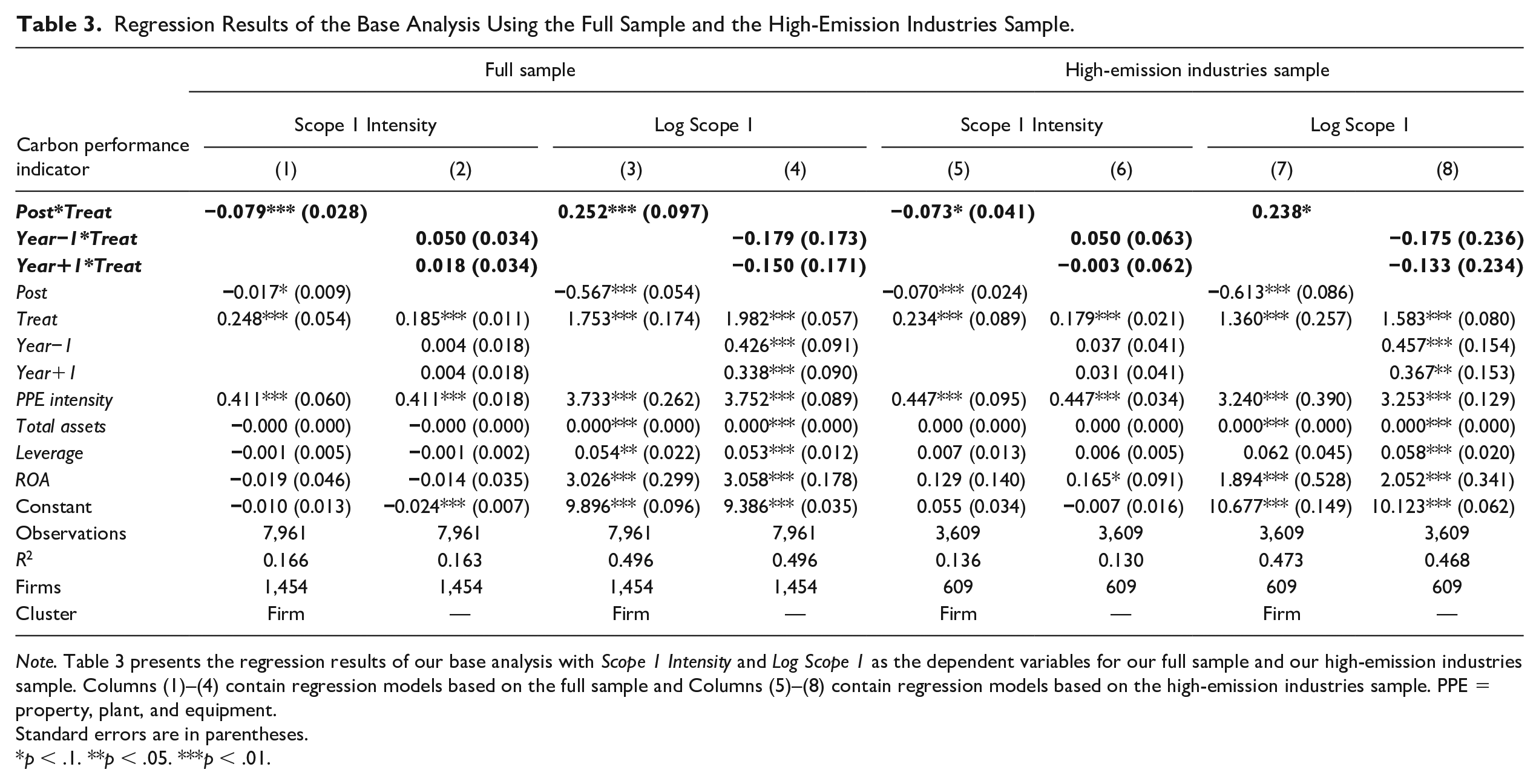

The results of our base analysis, presented in Table 3, are in line with our hypothesis. Column (1) shows a significantly negative coefficient for the interaction term Post*Treat (coefficient: 0.079; p < .01). That means, after the introduction of the GHGRP in 2010, firms in the treatment sample improve their carbon intensity significantly more than firms in the control sample. In addition, Post is also significantly negative (−0.017; p < .1) indicating that all firms improved their carbon intensity to some degree. This result also means that firms in the treatment sample reported a total change of Scope 1 Intensity of −0.096 after the GHGRP introduction (0.017–0.079). More specifically, based on the average Scope 1 Intensity for treatment firms in the pretreatment period (0.427), 1 the total reduction of Scope 1 Intensity translates into an improvement in carbon intensity of around 22.5% (0.096/0.427), while the improvement attributable to being affected by the GHGRP still amounts to around 18.5% (0.079/0.427).

Regression Results of the Base Analysis Using the Full Sample and the High-Emission Industries Sample.

Note. Table 3 presents the regression results of our base analysis with Scope 1 Intensity and Log Scope 1 as the dependent variables for our full sample and our high-emission industries sample. Columns (1)–(4) contain regression models based on the full sample and Columns (5)–(8) contain regression models based on the high-emission industries sample. PPE = property, plant, and equipment.

Standard errors are in parentheses.

p < .1. **p < .05. ***p < .01.

We also investigate whether the introduction of the GHGRP had an effect on firms’ absolute carbon emissions. The idea behind introducing legislation on firm carbon emissions is to counteract and prevent climate change. Achieving this goal requires an absolute reduction of carbon emissions. In Table 3, Column (3), Post has a significantly negative coefficient (−0.567, p < .01) for Log Scope 1, which means that control firms have 43.3% less emissions in the posttreatment period on average than in the pretreatment period. 2 Post*Treat is significantly positive (0.252, p < .01) indicating that treatment firms reduced their emissions significantly less than control firms, that is, 28.7 % = exp (0.252) – 1. More specifically, treatment firms decreased their absolute emissions following the GHGRP introduction by only 14.6% (−43.3% + 28.7%) compared with the 43.3% reduction of control firms. Note, while the reductions seem large at first, they represent the average improvement during the treatment period (2010–2016). Therefore, the effects on absolute carbon emissions are contrary to those by Jouvenot and Krueger (2020), who find a 12.19% reduction in global Scope 1 emissions relative to a control group during a treatment period from 2013 to 2016. This observation might be attributable to differences in the experimental settings, because in the study of Jouvenot and Krueger (2020), the carbon pricing scheme of the EU ETS might provide an additional incentive to reduce carbon emissions. For our sample of firms in high-emission industries, we find a similar treatment effect in the Post*Treat interaction term as in our full sample (−0.073, p < .10). The total change in Scope 1 Intensity for treatment firms in this subsample was −0.143 (−0.070–0.073) and the total change in Log Scope 1 is −18.9%, that is, exp (−0.613) – 1+ exp (0.238) –1.

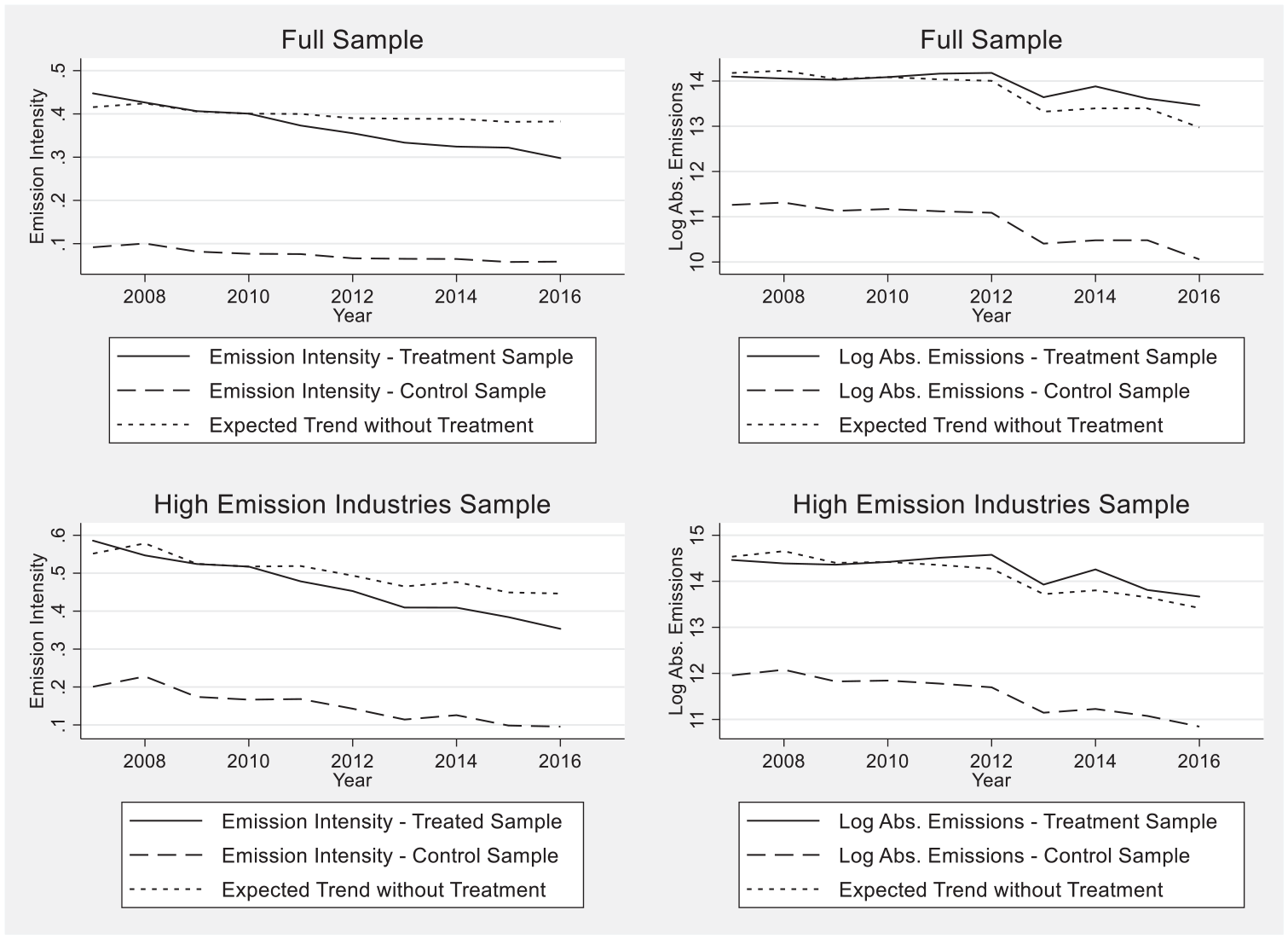

For our control variables, we see that firms with a higher PPE Intensity have a significantly higher carbon intensity and significantly higher absolute emissions. Our base analysis is also tested for parallel trends. Results are presented in Columns (2), (4), (6), and (8), showing no significant effects before or after the respective treatment year (variables: Year−1*Treat and Year+1*Treat). We, therefore, conclude that our results indeed measure the hypothesized event and its effect on carbon performance. This can also be observed in a graphical representation of the parallel trends in emission intensity (Figure 1). The continuous line represents the treatment firms and the dashed line the control firms. The dotted line shows the expected development of emissions if the treatment did not have any influence on the treatment firms and the parallel trend continued after the treatment.

Graphic Representation of the Parallel Trend Assumption.

Overall, we interpret the results as an indication that firms forced to disclose their facility-level emissions to the EPA perceive this requirement as a potentially legitimacy-threatening issue to which they respond with substantial efforts to improve carbon intensity. Therefore, the mandated disclosures can play a role in motivating firms to assume responsibility to mitigate their carbon emissions (World Commission on the Ethics of Scientific Knowledge and Technology, 2010). Our findings show that a mandate to disclose carbon emissions—even if it is restricted to the facility level—improves firm-level carbon intensity, but at the same time reduces the motivation to decrease absolute carbon emission. This is in line with studies showing that the relation between disclosure and carbon performance is not consistently confirmed by empirical literature (Belkhir et al., 2017; Bernard et al., 2015).

Furthermore, our results for carbon intensity are in line with studies confirming carbon performance improvements based on facility emissions falling under a mandatory disclosure regulation (Downar et al., 2021; Tomar, 2019). But we show that such improvements are not consistent across different definitions of carbon performance (i.e., intensity measures vs. absolute measures) on a global carbon emission level and in the absence of a national carbon pricing scheme.

Additional Analyses

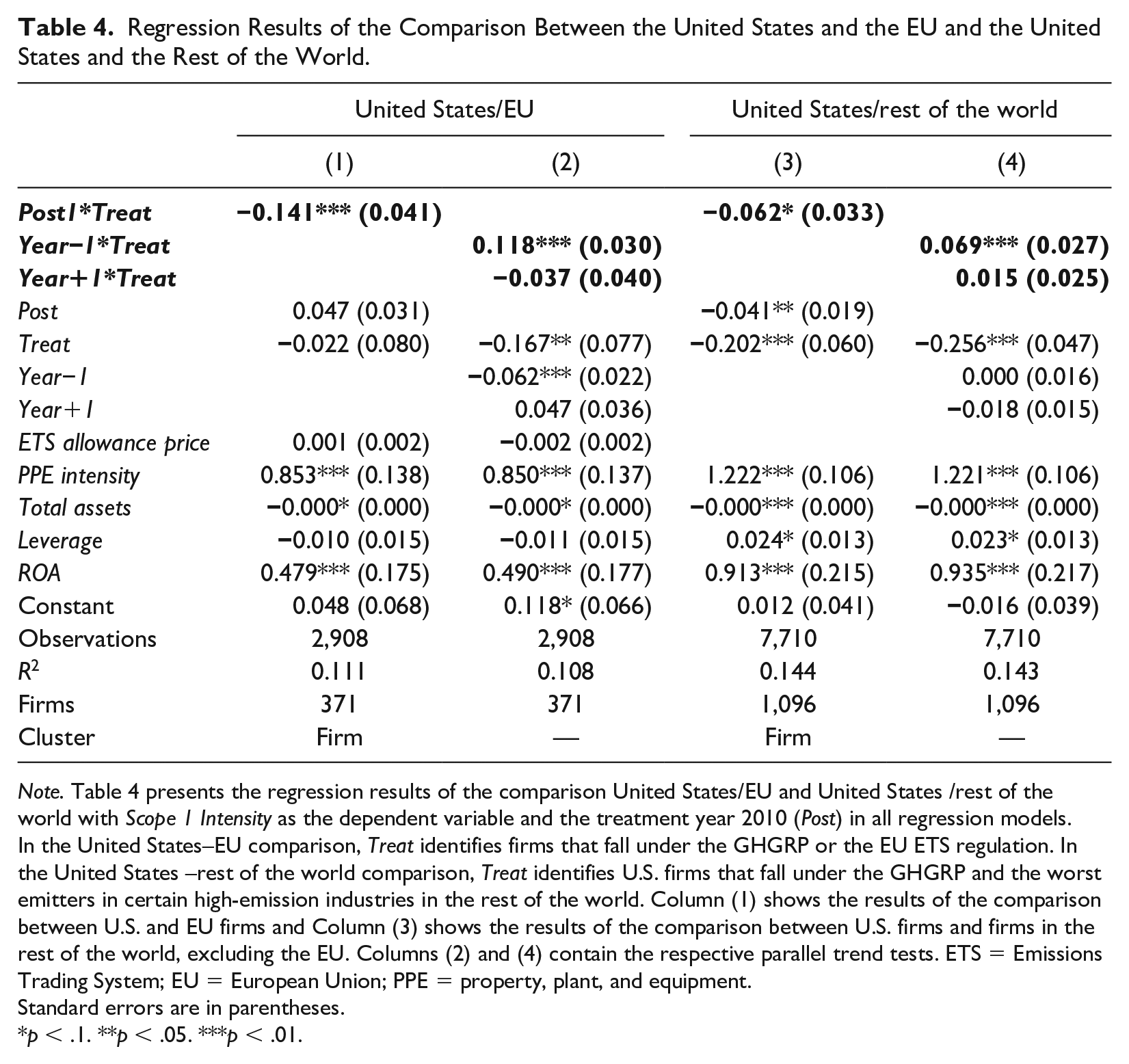

First, in the U.S. setting, we compare firms directly affected by the GHGRP with firms that are not affected. The GHGRP focuses on firms in high carbon-emitting industries, and despite our efforts to create a comparable sample using only high-emitting industries, the results could also be affected by other events in the same years, which affected the carbon performance of the treatment firms more than the carbon performance of the control firms. For example, from 2009 to 2010, the oil price increased considerably. Therefore, our first additional analysis focuses on a comparison of the treatment firms within the United States with firms outside the United States, which have similar characteristics to the treatment firms. We use firms from the EU, which are affected by the EU ETS, for comparison, because the EU ETS focuses on similar firms (i.e., high-emitting firms). Indeed, both regulations are similar in their focus on facilities with emissions above an annual threshold of 25,000 metric tons. However, the EU ETS is connected to a price on carbon and it was introduced in 2005. That means, comparable EU firms do not undergo significant changes in EU ETS regulation between 2009 and 2010 because they have already undergone these changes. Early opportunities for carbon emission reductions would have been realized a while ago and firms under the EU ETS have had several years of experience with the regulation and reporting at the time the GHGRP was introduced in the United States. Since we can thus expect that firms in the EU are on a stable trajectory in terms of carbon emissions and should not show sudden reactions, they are a suitable control group for U.S. firms that face a new regulation.

We gather information about firms affected by the EU ETS similarly to those affected by the GHGRP. We collect the facility-level carbon emission data from the database Carbon Market Data and use the database’s matching of facilities to firms and additionally add ISIN identifiers manually, where they are missing. Afterward, we use the same model as in our previous analysis to calculate the difference-in-differences between U.S. and EU firms that are subject to a mandatory reporting regime. We also collect monthly carbon price information from the European Energy Exchange and calculate annual average EU ETS allowance prices, which we use as an additional control variable (ETS Allowance Price).

Table 4 shows results of the US-EU difference in difference model. Column (1) presents a significant coefficient for Post*Treat (−0.141; p < .01), indicating that U.S. firms improve their carbon intensity significantly more than their European counterparts after the GHGRP was introduced. This is consistent with our expected effect of the GHGRP regulation. Although EU firms could have experienced earlier opportunities to reduce emissions after the introduction of the EU ETS, these effects should no longer play a role in 2010. This is also what we find empirically. Although firms affected by the EU ETS show a better carbon intensity compared with GHGRP firms (0.259 vs. 0.427) and lower average emission levels (6.76m tCO2e vs. 7.12m tCO2e) before 2010, after the GHGRP introduction, U.S. firms caught up and improved carbon intensity to 0.339 and average emissions 6.20m tCO2e (these figures are not reported in the tables of this study). This might seem to be a surprising result at first, because the EU regulation affects the same industries and has an additional carbon price attached to it. However, we do not see a significant effect from the allowance price in our regression analysis, which is consistent with the common assessment that the early phases of the EU ETS failed to incentivize investments in emission-reducing measures, due to an oversupply of emission allowances and thus too low allowance prices (Edenhofer et al., 2017). In fact, during our sample period, the average allowance price fluctuated around 10€ per metric ton of carbon emissions, with 12.65€ in 2009 and 16.28€ in 2010.

Regression Results of the Comparison Between the United States and the EU and the United States and the Rest of the World.

Note. Table 4 presents the regression results of the comparison United States/EU and United States /rest of the world with Scope 1 Intensity as the dependent variable and the treatment year 2010 (Post) in all regression models. In the United States–EU comparison, Treat identifies firms that fall under the GHGRP or the EU ETS regulation. In the United States –rest of the world comparison, Treat identifies U.S. firms that fall under the GHGRP and the worst emitters in certain high-emission industries in the rest of the world. Column (1) shows the results of the comparison between U.S. and EU firms and Column (3) shows the results of the comparison between U.S. firms and firms in the rest of the world, excluding the EU. Columns (2) and (4) contain the respective parallel trend tests. ETS = Emissions Trading System; EU = European Union; PPE = property, plant, and equipment.

Standard errors are in parentheses.

p < .1. **p < .05. ***p < .01.

Although the EU and U.S. firms affected by their respective regulation can be expected to be very similar, the setting is not ideal for a difference-in-differences analysis because our control firms (EU firms) are not free of any treatment (they just received the treatment much earlier). Therefore, we add a second analysis, and compare U.S. firms affected by GHGRP to high carbon-emitting firms located in the rest of the world which are not affected by the GHGRP. We use the same identification strategy as in our high-emission industries subsample. Thus, we identify firms that should operate similar facilities to their U.S. counterparts in the most emission-intensive industries. We then proceed, as previously, by conducting a difference-in-differences analysis, including a test for parallel trends. Results in Table 4, Column (3), contain a significantly negative coefficient for Post*Treat (−0.062; p < .01), meaning that U.S. firms improved their carbon intensity significantly more than similar firms outside the United States. This finding further confirms our base analysis results and supports the notion that mandatory climate reporting is an effective tool to improve firm carbon intensity.

We also perform a number of additional robustness tests. First, when there are concerns that the treatment sample is not randomly selected, which typically is the case in real world settings, propensity score matching can be used to make the treatment and control samples more comparable regarding the observable variables (Chen et al., 2018). By matching treatment with control firms using the variables from our base analysis, we generate a sample that allows us to compare firms, which are similar in their emissions and firm characteristics in the pretreatment period (2009) but differ in whether they are affected by the GHGRP. Applying an OLS regression model to the propensity score-matched sample leads to qualitatively similar results as our base analysis. Second, we apply a fixed effects regression model with firm-clustered standard errors, which helps control for omitted variable bias. Firm fixed effects allow us to control for unobserved firm-specific characteristics, whereas year fixed effects control for overall time series effects like additional confounding events. The fixed effects models confirm our initial hypothesis tests. Third, we test a specification of our base model without control variables to see if our results hold. Fourth, we test our base model using the Huber–White sandwich estimators, which are robust to heteroscedasticity (White, 1980). Fifth, we also use both, metric tons of Scope 1 emissions and Scope 1 intensity, calculated as the ratio of Scope 1 emissions to PPE and the ratio of Scope 1 emissions to sales, as alternative dependent variables for our base model. Sixth, we test our parallel trend assumptions for all analyses using different variations of placebo years and estimation methods. Finally, we limit our sample period to the years directly surrounding the introduction of the GHGRP in 2010 (sample limited to 2008–2012). All of these tests show qualitatively similar results to our base analysis.

Discussion

In case of voluntary environmental reporting, extensive literature has argued that it could be used for impression management purposes to gain or maintain (strategic) legitimacy (Archel et al., 2009; Deegan, 2002; Delgado-Márquez et al., 2017; Haffar & Searcy, 2020; Kraft, 2018; O’Donovan, 2002). Consequently, firms may disclose their environmental performance to manipulate society to obtain its support and approval because it is often easier to manage a reputation than to make real sustainability improvements (Dowling & Pfeffer, 1975; Lyon & Maxwell, 2011; Neu et al., 1998). In line with that, some studies find that poorer environmental performers are more likely to disclose nonfinancial information voluntarily to legitimize their poor performance (Cho et al., 2012; Cho & Patten, 2007; Patten, 2002) and that voluntary carbon reporting is not followed by improvements in carbon performance (Belkhir et al., 2017; Bernard et al., 2015; Haque & Ntim, 2018). Some researchers even argue that voluntary reporting might negatively affect social progress, that is, firms’ sustainability performance (Deegan, 2019). Our study cannot fully confirm this observation for mandatory carbon reporting. Although the smaller reduction in absolute carbon emissions suggests that firms required to report under the GHGRP are reducing their efforts to decrease absolute emissions, the results also show increasing efforts to improve carbon intensity. It appears that firms do not or cannot use mandatory reporting entirely as an impression management tool. This could be due to the fact that, in contrast to voluntary reporting, the mandatory reporting under the GHGRP does not allow firms discretion in the selection of data to be reported and in its presentation, which would be necessary in the context of impression management and strategic legitimacy (Deegan, 2019). Firms can no longer control the “story” under the GHGRP, because the data are made available to the public in a standardized form on the EPA website. Without the opportunity to manipulate society, to communicate a certain carbon performance to the outside, firms are forced to increase at least certain aspects of carbon performance to act in accordance with society’s expectations.

The success of the Toxic Release Inventory (TRI) in the United States confirms this reasoning and serves as anecdotal evidence of the effect of an environmental reporting regulation. Since its implementation in 1988, the TRI tracks the management of certain toxic chemicals that may pose a threat to the environment (EPA, 2019). U.S. facilities in different industries must annually report how much of each chemical they release into the environment or manage through recycling, energy recovery, and treatment. The reporting is mandatory when the use of these chemicals exceeds established levels. Currently, the TRI covers more than 650 different toxic chemicals. In 1995, 7 years after its implementation, the release of covered chemicals declined by 45% (Fung & O’Rourke, 2000). In their assessment of the TRI, Fung and O’Rourke (2000) attribute its success, among other things, to the possibility for citizens to inform themselves about toxic chemical releases and the resulting public pressure on polluting firms. Both, the TRI and the GHGRP, are pure mandatory reporting regimes, in the sense that they are not explicitly linked to any reduction programs.

A key feature of our study is the use of two measures of carbon performance, namely carbon intensity and absolute carbon emissions. The advantage of process-based measures (carbon intensity) over absolute measures (absolute carbon emissions) is that the former take into account changes in the scale of firms’ operations and thus capture the efficiency of operations while the latter do not (Busch & Hoffmann, 2011). Our results confirm that firms affected by the GHGRP improve their carbon intensity more than firms in the control sample. As argued above, this indicates that the introduction of the GHGRP motivates real changes in the efficiency of operations. However, at the same time, we find a significantly smaller percentage reduction in absolute carbon emissions for reporting firms compared with nonreporting firms. At first sight, this may be a consequence of increasing business operations. However, we address this issue through a number of control variables such as PPE intensity, firm size, leverage, and profitability. Alternatively, firms with high carbon emissions might be able to show impressive absolute emission reductions, which are still relatively smaller than for firms with lower carbon emissions. For example, a firm with 10 million tons of yearly Scope 1 emissions reports a decrease of an impressive 500,000 tons, which would mean a 5% decrease. At the same time, a firm with one million tons of yearly Scope 1 emissions reports a decrease of 90,000 tons, which would amount to a 9% decrease. 3 Therefore, the reporting scheme might increase the motivation to report large absolute emission reductions, but it might not extend to also achieve large relative improvements. Considering that especially for carbon-intensive sectors entirely decoupling carbon emissions from business activities is often difficult, firms might deem it sufficient to show at least some improvements to secure their legitimacy (e.g., Haberl et al., 2020). Therefore, our study emphasizes the importance to consider both types of variables, intensity and absolute measures, when evaluating a legislative measure to address climate change. However, while absolute emissions show firms’ progress toward reaching the overall important goal of net zero emissions, carbon intensity shows their progress on the transition toward this target. In the short term, it is thus not necessarily negative if firms with improving carbon intensity, at the same time, show no improvements in total emissions. This could mean that their business is growing, crowding out competitors with inferior carbon intensity, thus contributing to the overall reduction of a given sector’s emissions.

Future research could provide additional insights into the discrepancy between intensity and absolute emission measures. For example, future research might analyze how firms approach carbon emission reduction efforts through improving operational efficiency, outsourcing, offsetting, or adapting business models and how these in turn affect absolute emissions and emission intensity. It may also prove useful to explore how society’s expectations are perceived by firms in the United States and what repercussions are expected or experienced for noncompliance. The GHGRP provides firms in the United States with a standardized framework by which they can compare their own carbon performance with that of their peers. Whether this information could lead to firms reducing their emission reduction efforts because the urgency to act is actually lower than anticipated could be explored in a future study.

Conclusion

We analyzed whether and how the introduction of a mandatory climate reporting regime leads to improvements in firms’ carbon performance. A reason for firms to improve carbon performance might be the need to secure legitimacy, given the public disclosure of carbon emission data and increasing societal expectations that firms limit their contribution to climate change. In our setting, we use the GHGRP, which was introduced in 2010. We find that the carbon intensity of U.S. firms affected by the GHGRP improved significantly more than the carbon intensity of unaffected U.S. firms. At the same time, regulated U.S. firms reduced their absolute carbon emissions less than unregulated U.S. firms. These seemingly contradictory results may be worth further exploration. Although we control for several possible explanations, such as changes in firm size, leverage or profitability, there may be additional unobserved differences, like specific firm-level differences in the ability to decouple emissions from production. However, a mandatory reporting regulation leads to real sustainable change in firms’ operations and can be a stepping stone for further regulation. The detailed emission information of the GHGRP, including location, could create pressure, particularly from U.S. states that have set individual emission reduction targets, like California, which in 2018 passed legislation toward achieving carbon neutrality by 2045 (Executive Department, State of California, 2018) or New Mexico, which in 2019 committed to reducing carbon emissions by 45% below 2005 levels (Executive Office, State of New Mexico, 2019).

To achieve any climate goals, firms must improve their carbon performance including their absolute emissions. Tomar (2019) has shown that individual facilities reduce their absolute carbon emissions subsequent to the GHGRP introduction, because managers in these facilities learn and profit from experience of surrounding businesses in terms of carbon management. Our results suggest that carbon management experience from individual facilities can translate to improvements in the efficiency of operations throughout the entire firm and decrease carbon intensity. However, results for absolute carbon emissions suggest that learnings from individual facilities on how to decrease carbon emissions do not enable firms to fundamentally disconnect their business growth from the amount of absolute emissions.

Our study and its results contribute to research in four ways. First, we add to the discussion whether climate reporting has implications on firms’ carbon performance. Literature on voluntary climate reporting identifies either no or limited effects on firms’ carbon performance (Haque & Ntim, 2018; Qian & Schaltegger, 2017). Existing studies of the effect of mandatory climate reporting focus on firms’ aggregated facility emissions falling under a certain regulation (Downar et al., 2021; Matisoff, 2013; Tomar, 2019) or on the global carbon performance of firms headquartered in a country with an existing carbon pricing scheme (Jouvenot & Krueger, 2020). We contribute to this literature by showing that the introduction of a mandatory climate reporting regime has a positive impact on the global carbon intensity of firms headquartered in a country without a national carbon pricing scheme. Second, we explain how mandatory climate reporting might lead to a sustainable change in firms’ operations, drawing on and contributing to legitimacy theory. We argue that, opposed to voluntary reporting, under mandatory reporting firms cannot rely on strategic legitimacy and impression management, but are motivated to show real changes in firms’ operational efficiency (institutional legitimacy) leading to an improved carbon intensity. Third, we provide new insights into the important firm-level distinction between carbon intensity and absolute carbon emissions. Downar et al. (2021) and Tomar (2019) find improvements for both carbon intensity and absolute carbon emissions calculated based on firms’ aggregated facility emissions falling under a mandatory climate reporting regulation. However, we show that this is not the case when carbon intensity and absolute carbon emissions are calculated based on firms’ global emissions. Although firms in our sample reduce their absolute carbon emissions after the GHGRP introduction on average, regulated firms do so to a lesser degree than unregulated firms. The same is true when only looking at high-emission industries. The reduction of absolute emissions is an essential measure for firms because it relates to the remaining global carbon emission budget that is left, according to the IPCC assessments, to have a chance of staying below 1.5°C global warming. Thus, the reduction of the overall carbon emissions in the economy is key to mitigate climate change. In the short term, firms with superior carbon intensity can contribute by crowding out competitors with inferior carbon performance, but in the long term, most likely, reductions in absolute emissions will be required. Although Aragòn-Correa et al. (2020) argue that mandatory regulation typically has a strong positive effect on firms’ sustainability performance, it is important to consider the specific nature of the climate change problem. Due to the finite nature of the remaining carbon budget to remain under 1.5°C or 2°C a positive change in individual firms’ carbon intensity may be a step in the right direction but is in itself not enough to solve the problem. Fourth, we add to the literature about the effectiveness of policy designs aimed toward a low carbon economy (Bel & Joseph, 2015; Haites, 2018; Murray & Maniloff, 2015). We show that mandatory climate reporting contributes directly to improved carbon performance and, therefore, deserves political consideration. Thereby, we also contribute to previous literature on the real effect of mandatory disclosure (Chen et al., 2018; Christensen et al., 2017). Although previous literature shows significant improvements in firms’ sustainability performance after the introduction of respective disclosure mandates, our results also show that such improvements cannot be expected across the board. Given the current international development toward more mandated disclosures, such as the CSRD in the European Union, the inclusion of climate disclosure requirements in Canada’s COVID-19 release program, the LEEFF, or the requirement to disclose a BRSR by the Security and Exchange Board of India, future research can build on many opportunities to analyze the effectiveness of different systems in safeguarding capital markets and improving firms’ sustainability performance.

Some limitations of our research design are worth mentioning because they highlight the potential for further research, and they emphasize careful interpretation of our results. The nature of a mandatory climate reporting regime is to target high-emitting facilities. Thereby, our sample is not based on a random assignment of firms to the treatment and control samples. That means, as in many real-world cases, we cannot create a perfect experimental setting. However, we address this issue through a number of control variables, the propensity score matching, and additional analyses to the best extent possible. With a general tendency toward more climate reporting, there are more opportunities to analyze the effectiveness of mandatory climate reporting regimes in different institutional contexts. In addition, due to the nature of our setting, there is no information about firms, which do not voluntarily report firm-level carbon emissions. We rely on estimates from Trucost for these firms. Therefore, if Trucost’s estimation process is systematically flawed, this would affect our results. However, according to Busch et al. (2022b), the consistency and reliability of estimated emissions are not significantly different from reported carbon emission data. Furthermore, due to the nature of the GHGRP and its focus on facility-level emissions, we have used Scope 1 emissions to measure carbon performance. Although Scope 1 emissions, especially in high-emission industries, are an important factor in combatting climate change, the implications we draw do not necessarily hold true to the same extent for Scope 2 and Scope 3 emissions. Especially, Scope 3 emissions are, however, another key factor to achieve climate goals.

Further research can analyze whether mandatory climate reporting regimes affect the negative firm value effect of carbon emissions (Grewal et al., 2019; Griffin et al., 2017; Matsumura et al., 2014). Moreover, our research is focused on the GHGRP, a regulation specific to the United States and only targeting certain high-emission facilities. Therefore, our results do not necessarily translate to other regulatory settings. Future research can address whether other regulatory settings or current policy developments, such as the EU taxonomy on sustainable activities, can better motivate firms to identify critical processes to improve their absolute carbon emissions in alignment with Paris Climate Accord. Considering our somewhat surprising results that the GHGRP does not motivate regulated firms to reduce their absolute carbon emissions proportionally more than unregulated firms, future research can also analyze the underlying reasons. For example, it remains unclear why firms can improve their carbon intensity but are unable to disconnect their operations from absolute carbon emissions. Finally, while this study focuses on whether and how mandatory climate reporting has implications on firms’ carbon performance, further knowledge about the causal chain that connects mandatory nonfinancial disclosure to sustainability-related outcomes, and how managers adapt their behaviors and transform organizational policies, practices, and procedures is needed (Wickert & Risi, 2019).

Footnotes

Acknowledgements

We are grateful for valuable and insightful comments from seminar and conference participants at the University of Hamburg, the University of Kassel, the Catholic University of Eichstätt-Ingolstadt, the 36th EGOS Colloquium, the 23rd Annual Financial Reporting and Business Communication Conference, the 25th Annual Conference of the European Association of Environmental and Resource Economists and the 2nd Summer School on Sustainable Finance of the European Commission Joint Research Centre. The authors gratefully acknowledge funding from the German Federal Ministry of Education and Research and the Mercator Foundation. We are grateful to Thomas Cauthorn for language editing and proof reading. All remaining mistakes are our own.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors gratefully acknowledge funding from the German Federal Ministry of Education and Research (project number 01LA1820) and the Mercator Foundation via the project “Rahmenprogramm Sustainable Finance” (grant number 19026202).