Abstract

Voluntary nonfinancial disclosures are an increasingly relevant element of corporate sustainability strategies. Despite their importance, research is conflicted on how the transparency of such disclosures affects market and nonmarket outcomes. A possible reason is that transparency consists of multiple dimensions, each of which may be valued differently by market and nonmarket actors. Drawing on insights from attribution theory, we explore the effects that different information traits of voluntary disclosures have on market and nonmarket actors. We suggest that the completeness, clarity, and accuracy of voluntary nonfinancial disclosures affect both market (i.e., market valuation) and nonmarket (i.e., reputation risk) reactions. Using data from the Carbon Disclosure Project, we find that these actors react differently to three distinct dimensions of transparency: completeness, clarity, and accuracy. Our findings highlight the importance of the nuanced relationship between transparency and market and nonmarket actor reactions, which has implications for broader, sustainability-related outcomes.

Investors, consumers, academics, nongovernmental organizations (NGOs), reporters, and employees all have their own perspectives on what companies should and should not be doing. A company can be returning a profit to shareholders, only to find protesters at its door or lawsuits filed . . . Companies struggle to inform employees, shareholders, and stakeholders about how they are managing material, social and environmental issues (Epstein-Reeves, 2012).

Transparency—defined as the perceived quality of information disclosed by a firm (Schnackenberg & Tomlinson, 2016)—has become an increasingly critical aspect of corporate sustainability strategies as firms often struggle to understand how the release of nonfinancial information (and the quality of that information) can influence change within organizations. For instance, transparency can help external actors identify and comprehend pertinent social and environmental risks and opportunities facing the firm (Flammer, 2013). Transparency in nonfinancial disclosures is also linked to the development of trust between an organization and various stakeholders, which leads to more favorable judgments of leaders’ competency, improves the firm’s reputation, and allows firms to more quickly recover from scandals or misdeeds (Fombrun & Rindova, 2000). Because external actors often believe that firms “that are open perform better” (Tapscott & Ticoll, 2003, p. xii) and because transparency can mitigate risks associated with regulatory, social, and fiscal forces (Cheng et al., 2014; Li et al., 2019), firms often seek to increase transparency through disclosing pertinent information about their environmental practices.

Notwithstanding the importance of transparency in nonfinancial disclosures, evidence is mixed on the impact it ultimately has on firm outcomes (for a review, see Schnackenberg & Tomlinson, 2016). Although some research suggests that increased transparency can lead external actors to perceive the firm more favorably, leading to increased market value (Bushman et al., 2004) and reputation gains (Lange & Washburn, 2012), other evidence suggests that transparency is not always beneficial in generating sustainability-related outcomes. For instance, transparency may risk revealing controversial or unsustainable practices (Hahn & Lülfs, 2014), elevating the likelihood of backlash, negative publicity, and reputational damage (Briscoe & Murphy, 2012). Increased transparency may also reveal the nature of a firm’s strategic resources and reduce its competitive advantage (Vicente-Lorente, 2001).

We suggest that the explanation for the inconsistent relationship between transparency in nonfinancial disclosures and firm outcomes stems from the multidimensional nature of transparency. Although early literature typically viewed transparency as a unidimensional construct (e.g., Bushman et al., 2004; Nicolaou & McKnight, 2006), more recent work suggests that transparency may be decomposed into several dimensions, or information traits, such as the volume or completeness of information disclosed, its clarity and comprehensibility, and its accuracy (for a review, see Schnackenberg & Tomlinson, 2016). Given that firms face an increasingly diverse array of relevant actors for nonfinancial disclosure, the multidimensional nature of transparency makes it difficult for firms to be transparent in a manner that simultaneously satisfies multiple actors. External actors differ on what constitutes appropriate disclosure of information and with how they interpret and value that information (Crilly et al., 2016; Reimsbach et al., 2020). For example, nonmarket actors (such as the media and general public) concerned about the natural environment may value complete transparency with respect to a firm’s environmental actions, whereas market actors (such as shareholders) may have a more nuanced perspective. Although these market actors may value greater completeness of information disclosed because it better allows the assessment of material opportunities and risks to the firm, they may also support low levels of completeness as it limits the disclosure of proprietary information that could potentially benefit competitors. Not understanding these differences can lead to firms being punished for their disclosures, unnecessarily limiting subsequent efforts to engage in sustainable changes.

In this article, we argue that different dimensions of transparency may influence the attributions that market and nonmarket actors make in response to disclosures of information. Viewing information transparency through the lens of attribution theory can help us better understand why different actors uniquely respond to disclosures of nonfinancial information, which is an important step to understanding how nonfinancial disclosures drive real, sustainable changes both within and beyond firms (Dubbink et al., 2008; Jackson et al., 2020). We develop theoretical rationale to explain why various actors may respond differently to different information traits of nonfinancial disclosure. Attributions by external actors influence their perceptions and evaluations of a firm’s effort, ability, and intentions (Weiner, 1985). As they evaluate nonfinancial disclosures along multiple dimensions of transparency, market and nonmarket actors may make different judgments about the nature of the information as well as the firm’s motivation for disclosing the information (Bromley, 1993). These attributions can have important consequences for the risks firms face to their market value and their reputation.

We evaluate firm outcomes related to two key actors—market (shareholders) and nonmarket (the media) actors—and their responses to three distinct dimensions of nonfinancial disclosures—completeness, clarity, and accuracy—over firm management of climate change, a pressing and broadly relevant issue. Our results suggest that these actors respond differently to each dimension of transparency, which we argue is based on the attributions they make about the firm’s motivations to disclose. Furthermore, we provide evidence that responses to disclosures can be nonlinear and interactive, suggesting that the value of transparency in sustainability strategy is more nuanced than previously thought. Generally, market actors view disclosures with moderate completeness more negatively than they do for disclosures of low or high completeness, and they view low and high clarity less positively than moderate clarity. The accuracy of these disclosures provides financial value benefits for both complete and clear disclosures. Nonmarket actors, however, take a simpler view of disclosure completeness, as increasing completeness decreases the reputational risk to firms. However, nonmarket actors do not appear to value increases in clarity with voluntary firm disclosures.

In clarifying how different dimensions of transparency can influence the evaluations of market and nonmarket actors, we augment understanding of how nonfinancial disclosures can be used as a sustainability strategy (Aragon-Correa et al., 2020; Schnackenberg & Tomlinson, 2016). Utilizing elements of attribution theory, we elucidate the mechanisms by which different actors make distinct attributions about transparency efforts, resulting in varied market performance and reputational implications (Bednar et al., 2015). Building on this primary theoretical contribution, our findings have important implications for understanding when firms engage in real sustainable changes: Firms that can better address key actor expectations through nonfinancial disclosures are better able to improve financial performance and manage long-term risks. Understanding how market and nonmarket actors respond to different aspects of transparency helps firms better decide when, how, and what to report in voluntary disclosures (Reimsbach et al., 2020). This improved understanding of the feedback mechanisms provided to firms through diverse actor responses also has important implications for broader sustainability-related outcomes: Firms that engage with external actors over multiple dimensions of transparency are better able to manage for longer-term, sustainable outcomes (DesJardine et al., 2019). Thus, our findings have implications for how transparency characteristics in nonfinancial disclosures can impact real, sustainable change within organizations.

The Role of Transparency in Sustainability Strategy

Firms often increase nonfinancial transparency in response to pressure from diverse actors including investors, employees, social activists, the media, or policymakers. Disclosed information helps actors evaluate the firm’s strategic activities, exposure to risk, and the implications of its environmental, social, and governance (ESG) activities. To date, research on corporate transparency has primarily focused on transparency outcomes, such as how transparency can enhance organizational performance (Miller et al., 2017), grant enduring legitimacy and access to important organizational resources (Desai, 2018), or provide political and social support from various actors that grant firms a “social license” to operate (Henisz et al., 2014). This research is founded, in part, on the assumption that these outcomes create competitive advantage by enhancing corporate governance (Cheng et al., 2014), engendering trust in customer relationships (Lacey, 2007), or improving government relations (Frynas, 2010). Greater transparency in nonfinancial disclosures can also reduce the cost of capital (Verrecchia, 2001), increase environmental performance (Chatterji & Toffel, 2010), and improve impression management with stakeholders (Graffin et al., 2011). As organizations increase their transparency, they bring increased awareness to key strategies, which helps align the behaviors and expectations of both market and nonmarket actors of the firm (Bushman et al., 2004) and provides insurance-like benefits to a firm’s reputation (DesJardine et al., 2019; Koh et al., 2014).

However, transparency also can expose the firm to additional risk if relevant actors view the disclosed information negatively (Hahn & Lülfs, 2014). For instance, if the disclosure is viewed unfavorably, both the financial performance of the firm and its reputation may be negatively affected (Bednar et al., 2015). Greater transparency can also alert competitors to the attractiveness of specific resources, strategic or competitive fit, or production opportunities and constraints (Franke et al., 2013), enabling competitors to use that information to imitate the firm’s activities and erode its competitive advantage. In addition, transparency can expose the firm to increased risk of scrutiny from activists and other groups that may use the information to embarrass or pressure the firm into changing behavior (McDonnell et al., 2015). Thus, in order for firms to better manage the opportunities and risks of transparency, they must understand how various actors view transparency, as they may interpret disclosures in different ways (Connelly et al., 2011).

Dimensions of Transparency

Following a recent synthesis of literature on corporate transparency (Schnackenberg & Tomlinson, 2016), we examine three dimensions of transparency that may influence the attributions that stakeholders make about information disclosure: completeness of disclosure, clarity of the information, and perceived accuracy. Completeness of disclosure implies that all relevant information has been openly shared in a timely manner (Bloomfield & O’Hara, 1999). It is also related to the availability, accessibility, volume, and visibility of information (Philippe & Durand, 2011). In essence, completeness is a measure of whether the firm has provided all the necessary information to allow actors to obtain a full picture of the firm’s activities (Nicolaou & McKnight, 2006). Firms that provide complete information may be perceived as having little to hide. Conversely, a lack of completeness in disclosure may be viewed as an attempt by the firm to selectively withhold relevant information (Verrecchia, 1983).

Although completeness reflects how much relevant information was disclosed, clarity is related to how readily users can interpret the information; clarity signifies a seamless transfer of meaning from firm to the user, rather than just the amount or relevance of information shared. Clarity further suggests consistency of information that limits ambiguity (Schnackenberg & Tomlinson, 2016)—a large amount of information disclosed is not transparent if users are unable to understand the information or its significance (Briscoe & Murphy, 2012). For instance, information consisting of industry jargon (Nicolaou & McKnight, 2006) or complicated mathematical algorithms (Granados et al., 2010) is considered less transparent if actors have difficulty interpreting that information (Bushee et al., 2018). Furthermore, a firm may fully disclose all risks that it faces—such as potential litigation, environmental issues, market and economic trends, or regulatory changes—but if it does not provide clear information about the antecedents and outcomes of those risks, actors may not be able to fully comprehend the implications of those risks. Alternatively, sufficient clarity enables actors to assess the underlying significance of both large and small information disclosures (Bae et al., 2010).

Finally, accuracy reflects whether the information is perceived as valid or reliable enough to allow external actors to use it (Philippe & Durand, 2011). Although ensuring that disclosures are accurate can be costly, accuracy can signal that disclosures are of higher quality (Bagnoli & Watts, 2017) as inaccurate information may instead signal a lack of integrity or capability in social or environmental performance. We consider accuracy as an important moderator of completeness and clarity because of the fundamental difference in the way it affects social judgments of the firm (Granados et al., 2010). Perceptions of accuracy may affect the intensity of attributions by giving market actors added confidence in making investment decisions on the basis of nonfinancial disclosures (Reimsbach et al., 2018). Firms that provide inaccurate information are likely to draw attributions that are both internal (reflecting locus of control) and manipulative (reflecting the intentions behind the disclosure). Thus, disclosure accuracy may interact with completeness and clarity in previously unexplored ways.

As part of a sustainability strategy, transparency efforts are often aimed at two general actors: market and nonmarket. Market actors are those that have direct financial transactions with firms. Because they engage in direct transactions with firms, they can exert strong economic pressures on firm behaviors. Market actors, sometimes referred to as primary stakeholders, include buyers, suppliers, employees, and shareholders (Baron, 1995; Freeman et al., 2010). Shareholders and other investors are primarily concerned with the financial performance of the firm. Because they engage in direct financial transactions with firms, market actors tend to be more sophisticated and discriminating in their evaluations of transparency efforts (Vogel, 2005) and are often skeptical of the motives behind them (Carvalho et al., 2010; Haleblian et al., 2017), which can result in a nuanced relationship between transparency and market performance. In contrast, nonmarket actors are those that do not engage in direct financial transactions with the firm (Eesley & Lenox, 2006). They include the public, government, the media, and public institutions (Baron, 1995). Nonmarket actors, sometimes referred to as secondary stakeholders, tend to be less concerned with financial performance and more concerned with the social and environmental performance of the firm. Consequently, nonmarket actors typically indirectly engage with firms; for example, the media can shape public opinion about firm behavior or provide legitimacy and visibility for a social movement targeting the firm. These tactics indirectly affect firms financially whereas market actors’ interactions with firms directly affect firms financially. Because nonmarket actors are primarily concerned with nonfinancial aspects of firms’ performance, they are generally more embracing of greater efforts toward transparency and the motives behind them.

Actors’ Attributions

One of the reasons why transparency can lead to conflicting outcomes is that market and nonmarket actors differ in how they perceive the firm’s underlying motivations to voluntarily disclose information (Jensen et al., 2012). According to attribution theory, people seek out information to help them understand the underlying causes of an important outcome, event, or behavior (Weiner, 1985). This information is used to assign attributions about the firm’s motivations, thereby influencing the actor’s responses to the disclosure. Attributional explanations for events typically center on ability, effort, the nature of the task, and luck (Pearce & DeNisi, 1983). Thus, as actors evaluate different aspects of a firm’s transparency, they make attributions about the nature of the disclosed information and the underlying motivation for or cause of the transparency (Bromley, 1993). These attributions help actors process the information and determine how to respond.

Attribution theory identifies two key dimensions that influence how actors evaluate events or behavior—whether they are attributed as having an external or internal locus of control (Weiner, 1986) and whether intentions are attributed as altruistic or egoistic (Martinko et al., 2007). In making attributions about transparency, the locus of control helps explain whether the cause of the event or behavior is due to internal characteristics of the actor (i.e., proactive) or to external situational factors (i.e., reactive or coerced). With respect to attributions of intention, stakeholders may view the firm’s disclosure as following one of two basic motives: altruistic, to the benefit of actors outside the firm; or egoistic, to the benefit of the firm itself. Following prior research, we label these motives as either sincere or manipulative, respectively (Martinko et al., 2007). Applying the lens of attribution theory to actors’ perceptions of the different dimensions of transparency helps us better understand the varied outcomes of transparency.

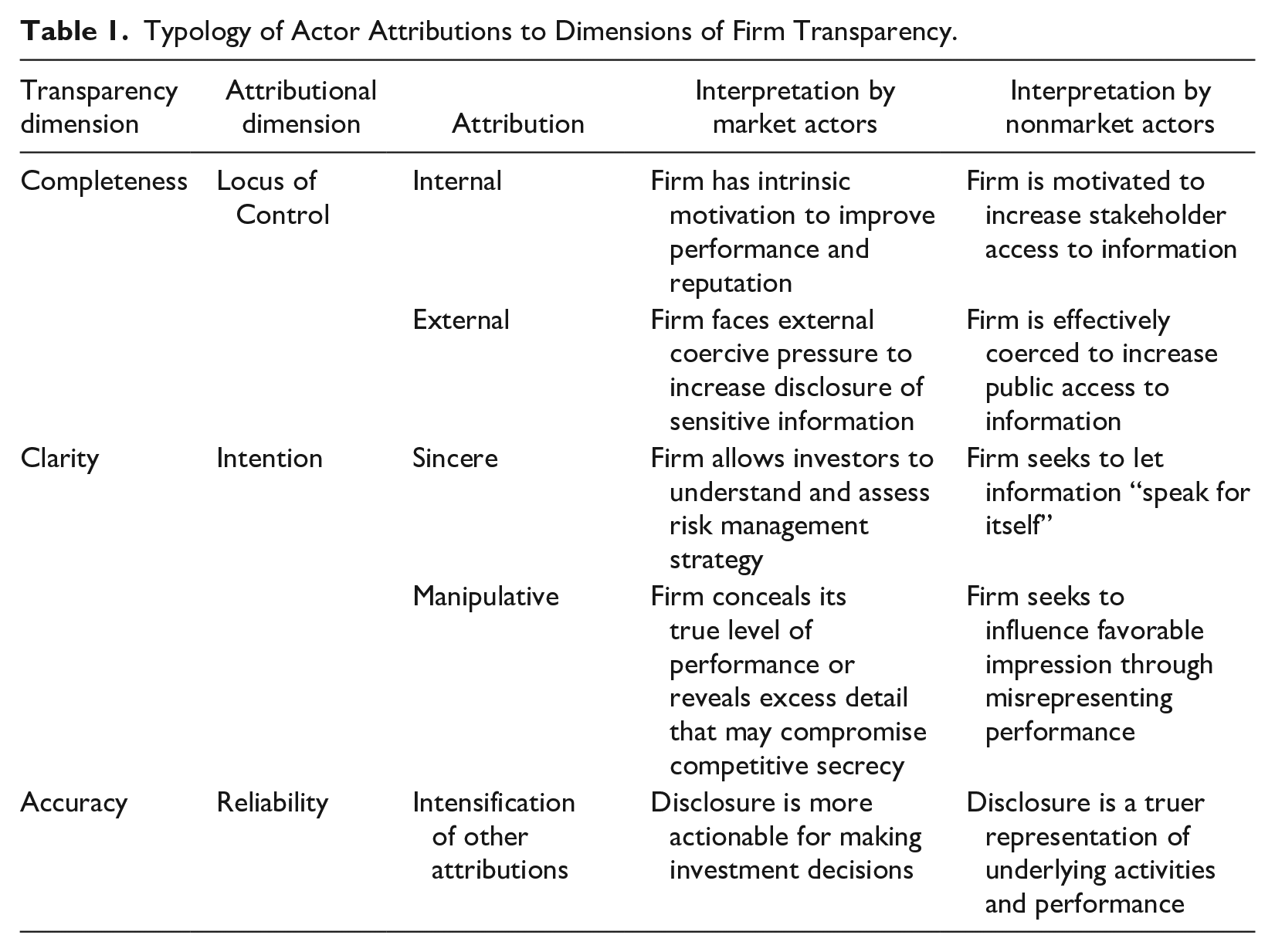

We suggest that the completeness and clarity of information disclosures primarily influence how distinct actors evaluate that information and how their evaluations then affect firm performance and reputation. We further argue that the accuracy of the disclosures moderates these relationships, as accuracy reflects the reliability of the information disclosure. Table 1 summarizes the three relevant dimensions of transparency and actor attributions, respectively, for two actors of interest—market actors and nonmarket actors. We consider how these two actors differ in how they make attributions about firms’ motivations behind voluntarily disclosing information. We consider shareholders as the most relevant market actor because unlike other market actors (e.g., customers, employees, or suppliers), nonfinancial disclosures are typically intended to provide investors access to firm information (Hahn et al., 2015) and because publicly-traded firms are legally responsible to disclose material information to market actors. We focus on the media as the most relevant nonmarket actor because while voluntary nonfinancial disclosure may address a broad range of nonmarket actors, media portrayals largely control information flow to other nonmarket actors (Graf-Vlachy et al., 2020), influencing the reputation of firms (Bednar et al., 2013). Hence, we examine how market actor’s evaluations affect firm market value and how nonmarket actor’s evaluations influence reputational risk through the transparency constructs of completeness, clarity, and accuracy.

Typology of Actor Attributions to Dimensions of Firm Transparency.

Transparency and Financial Performance

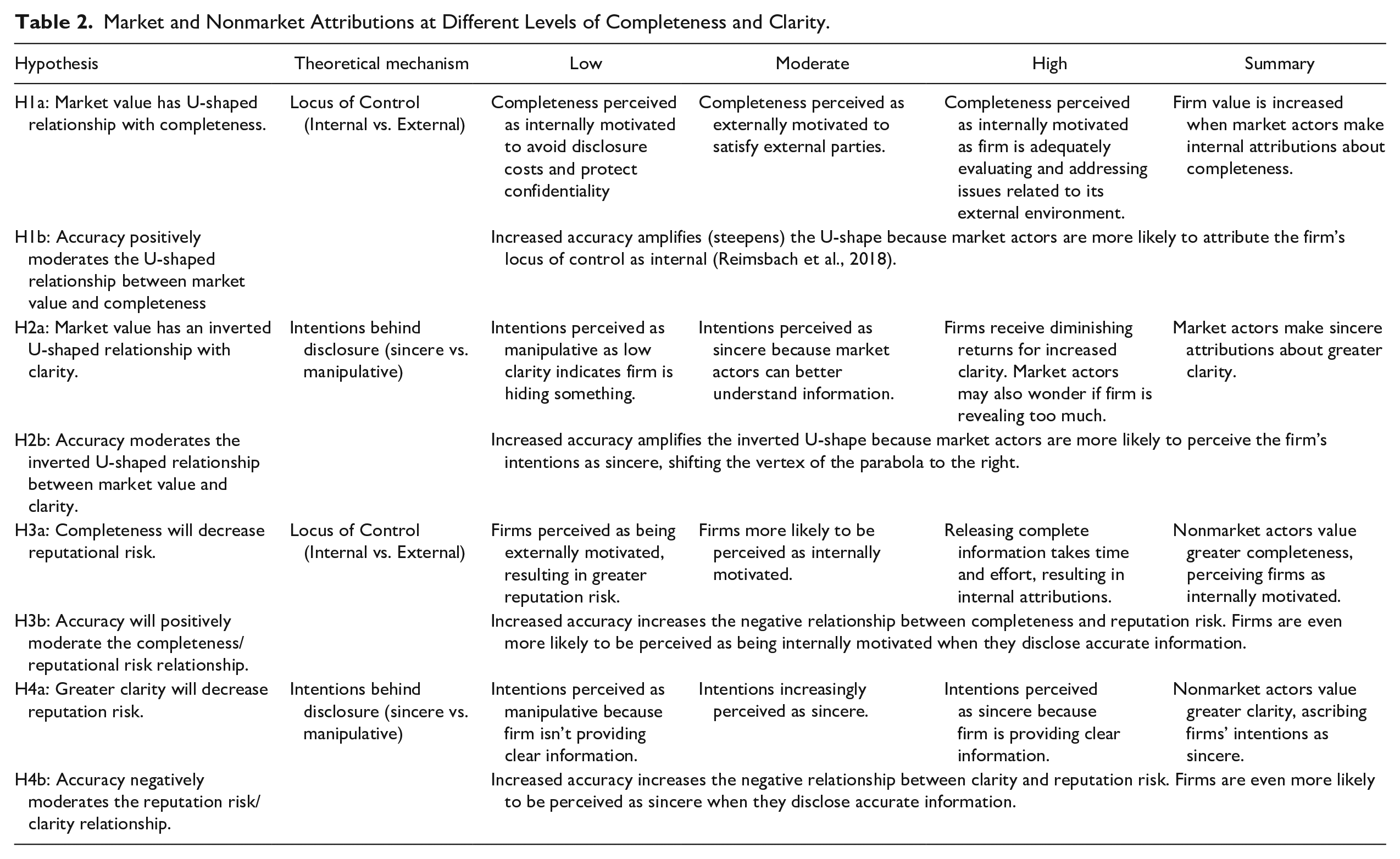

Nonfinancial disclosures are of primary interest to market actors because the information helps them assess future financial performance (Eccles et al., 2011). Increased transparency in these disclosures—particularly nonfinancial disclosure of sustainability-related information—benefits the financial value of firms. For example, transparency can increase access to capital (Barnett & Salomon, 2012; Cheng et al., 2014) and reduce regulatory scrutiny (Li et al., 2019); however, the empirical evidence directly linking transparency and financial performance is weak (Peloza, 2009). One reason for this may be a lack of consensus on the mechanisms behind market actor’s responses to information disclosure. For example, some research suggests that managers may seek their own self-interest by engaging nonmarket actors at the expense of market actors (Marquis et al., 2007), whereas other work suggests that firm leaders engage and manage both actors to more effectively craft and execute firm strategies (Barnett & Salomon, 2012). We suggest here that the completeness, clarity, and perceived accuracy of the information may influence market actors’ causal attributions about the disclosures, thereby affecting financial performance. Table 2 summarizes the hypothesized relationships between dimensions of transparency and the evaluations of market and nonmarket actors, which we describe in detail in the following text.

Market and Nonmarket Attributions at Different Levels of Completeness and Clarity.

Effect of Completeness on Financial Performance

Completeness of disclosure affects the ability of actors to assess important elements of firm activities, such as the firm’s exposure to risk and the financial, social, and environmental implications of its activities (Madsen & Rodgers, 2015). Although nonfinancial disclosure has historically been largely voluntary, mandatory disclosure and other coercive pressures are increasingly prevalent (Aragon-Correa et al., 2020; Grewal et al., 2019), suggesting that completeness of disclosure may be influenced by both proactive and reactive motivations. Market actors may thus attribute differences in disclosure completeness to the perceived locus of control of a firm’s disclosure decision.

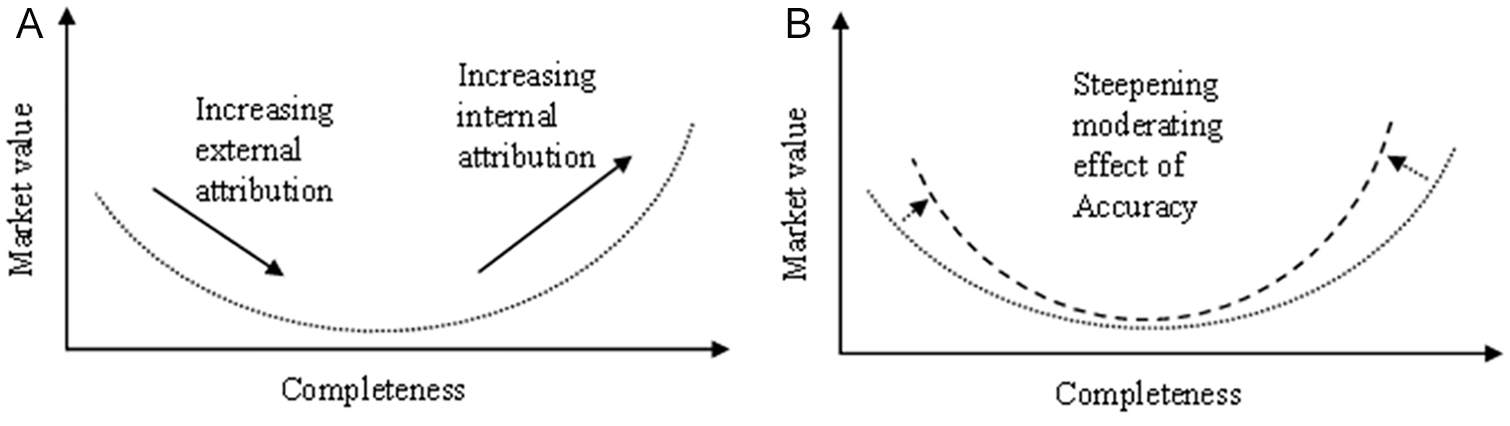

In general, attributions of an internal locus of control lead to more favorable valuations, whereas attributions of an external locus of control lead to less favorable valuations and these attributions are likely to be affected by different levels of completeness. Figure 1 shows that internal attributions dominate at low and high levels of completeness (resulting in more favorable attributions), resulting in a U-shaped relationship between completeness and market value. Low completeness indicates that the firm provided a very small amount of information in its disclosure. This may be perceived by market actors as an internally motivated strategic decision by firms to avoid the costs associated with disclosure and to protect confidentiality, both of which may help the firm’s competitive position. Low levels of disclosure completeness may also serve to preserve competitive secrecy (Contractor, 2019) or protect firms from unwanted scrutiny (Cappellaro et al., 2021; Carlos & Lewis, 2018). Because the firm is intentionally choosing to withhold information, thereby saving the firm money and improving its competitive position, market actors are likely to respond favorably to low levels of completeness.

Hypothesized Attributional Relationships Between Completeness and Market Value. (A) Locus of Control Attributions. (B) Moderating Effect of Accuracy.

In the case of high completeness, the firm provides an ample amount information in its disclosure. In this case, market actors are also likely to attribute the firm’s actions to internal motivations because a disclosure that is high in completeness requires the firm to collect and thoroughly vet a large amount of information before disclosing it. This process requires the firm to study and understand several dimensions associated with its social and environmental impacts, which can benefit the firm through reduced resource consumption (Matisoff, 2013) and better mitigation of risks (Jacobs et al., 2016). Although this can be expected when a disclosure is mandatory, an effort of this size is unlikely to be undertaken voluntarily without good reason. Market actors may attribute such extensive efforts and expense for a voluntary disclosure as an attempt to better position the firm to identify opportunities for improvement and to manage for long-term growth.

High levels of completeness also drive internal attributions by demonstrating to market actors that the firm is adequately evaluating and addressing issues related to its external environment. A complete disclosure helps reduce the information asymmetry for analysts who provide earnings forecasts and other types of information for market actors (Luo et al., 2015). Disclosures related to environmental issues lead to more precise earnings forecasts from analysts (Aerts & Cormier, 2009), as it helps them better assess the extent of the natural (e.g., flood, drought, climate change) and regulatory risks the organization faces (Luo et al., 2015). To market actors, a firm that has undertaken the challenge and costs associated with thorough information disclosure more thoroughly understands its competitive environment and should be able to better help investors understand the risks associated with investing in the firm.

Conversely, market actors may make external attributions when they perceive disclosure as a reactive response to coercive forces with limited benefit to firm value (Husted & De Jesus Salazar, 2006). This is most likely to occur when firms provide information with a moderate level of completeness. Moderate levels of completeness suggest the amount of information is disclosed is neither protective of firm competitive positions nor indicative of a genuine motivation to provide market actors with ample information about market risks or long-term growth. Rather, market actors may view disclosures with moderate levels of completeness as a reluctant effort to compromise with external constituent demands—such as regulators or activist groups—to disclose information, thus sacrificing secrecy to maintain external legitimacy. In addition, a moderate level of completeness may suggest to market actors that firms are selectively releasing some information, while hiding potentially damaging information that a more complete disclosure may include (such as poor social and environmental performance). Moderate levels of disclosure are linked to efforts to mislead market actors and may draw greater scrutiny of the firm’s motivations (Marquis et al., 2016).

Taken together, the increasing value from internal attributions and decreasing value from external attributions may result in an aggregate nonlinear response in disclosure completeness. Consistent with research on market value associated with corporate social responsibility (CSR) performance (Brammer & Millington, 2008), we hypothesize a U-shaped relationship between completeness and market perceptions of the firm.

Hypothesis 1a (H1a): Market value has a U-shaped relationship with disclosure completeness.

We expect the accuracy of disclosures to amplify the U-shaped relationship between disclosure completeness and market value as it provides an important signal about the reliability of the information disclosed (Reimsbach et al., 2018), as market perceptions can be undermined by low accuracy information (Dando & Swift, 2003). Accuracy affects the confidence market actors have in their attributions of the motivation behind the disclosure: lower accuracy reduces their confidence and higher accuracy increases their confidence. On average, the greater an actor’s confidence in the accuracy of the disclosure, the stronger their attribution of the locus of control: more accurate disclosures are associated with a steeper U-shaped relationship because it enhances market actors’ belief in their internal and external locus of control attributions.

Hypothesis 1b (H1b): Disclosure accuracy will positively moderate (steepen) the U-shaped relationship between market value and disclosure completeness.

Effect of Clarity on Financial Performance

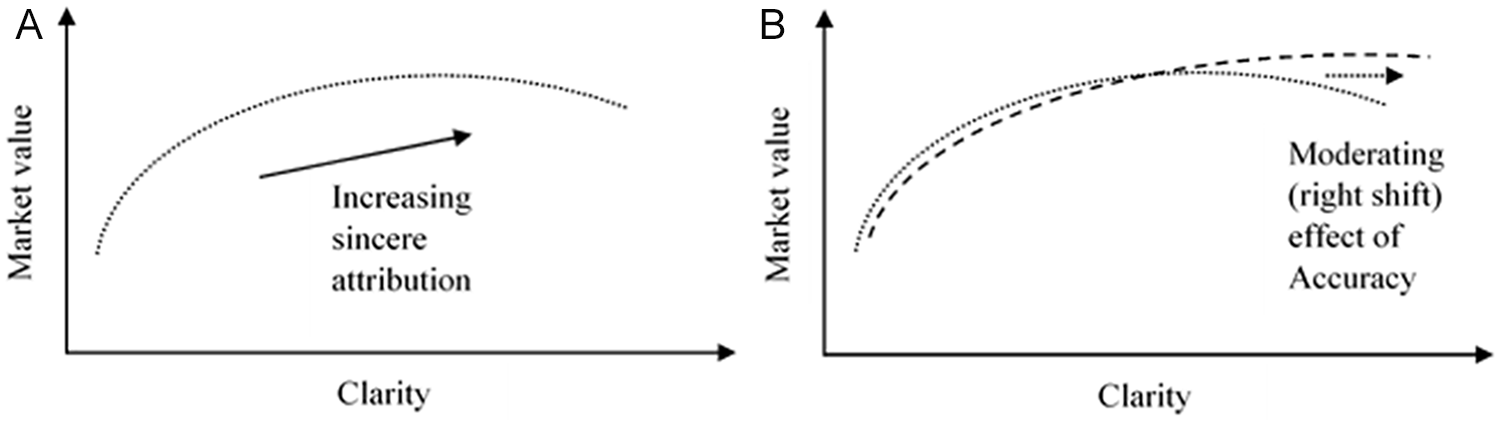

Although the completeness of disclosure refers to how much of all the available information is released, clarity of disclosure is related to how clear the information is, allowing the meaning of the information to be adequately transferred from sender to receiver (Schnackenberg & Tomlinson, 2016). Thus, although a firm may disclose information completely, it is possible that the receivers are not able to comprehend or interpret the information in a meaningful way. We assert that clarity of disclosure conveys information about the firm’s intentions behind the release of information by providing a channel through which the sender may either strive to enhance an actor’s understanding of the information or manipulate the meaning of the information for its own benefit. In attribution theory, intentions are determined based on whether the receiver perceives that the sender is sincere or engaging in manipulation (Weiner, 1995). In general, manipulative intentions, which dominate at low levels of clarity, are negatively perceived while sincere intentions, which dominate as clarity increases, are perceived favorably by the market, although the returns diminish at higher values. As a result, we expect clarity to have an inverted U-shaped relationship with market value for reasons we explain below (see Figure 2).

Hypothesized Attributional Relationships Between Clarity and Market Value. (A) Intentionality Attributions. (B) Moderating Effect of Accuracy.

Low levels of clarity result in market actors perceiving the firm’s intentions as manipulative for several reasons. First, market actors may fear that the firm is engaging in decoupling or symbolic management, reaping the benefits from symbolically adopting a practice without actually implementing it (Carlos & Lewis, 2018). In such cases, firms do little to actually address material social and environmental risks, which may not be well-received by market actors. Furthermore, unclear disclosures can indicate that the firm is obfuscating a lower level of environmental performance, which may be an important financial risk to the firm (Fabrizio & Kim, 2019). When market actors attribute manipulative intentions to a firm’s disclosure, the market value is likely to decrease. However, as clarity increases—making it easier for market actors to understand the information—market actors react more positively as they attribute the intentions behind the disclosure as sincere efforts to provide interpretable information that help investors correctly value a firm. Such attributions reflect the increased ability of market actors to better understand the firm’s priorities and intentions (Godfrey, 2005) from an environmental perspective. Greater clarity also allows market actors to more effectively judge the firm’s efforts to manage emergent risks and opportunities. Thus, greater clarity of disclosure is expected to enhance market value.

In addition to the increased costs that firms incur from preparing disclosures that have a high level of clarity, sincere attributions may provide diminishing returns as clarity reaches higher levels for two primary reasons. First, high clarity may imply excessive commitment about a firm’s environmental position. This commitment can limit the firm’s flexibility to adjust its strategic position in the future (Wagner et al., 2009). Moreover, a clear commitment on causes important to nonfinancial stakeholders may give rise to perceptions of resource mismanagement or heightened financial risk. For example, the editorial board of The Wall Street Journal recently highlighted the financial risks that businesses such as Delta Air Lines and The Coca-Cola Company face because their CEOs were taking a public stand on a contested social issue in the southeastern United States (The Wall Street Journal, 2021). In situations such as these, disclosures with higher levels of clarity risk overcommitting the firm to a potentially controversial position, or risk being seen as hypocritical in trying to exploit a cause for the benefit of nonfinancial stakeholders (Carlos & Lewis, 2018; Wagner et al., 2009). Such concerns may soften or otherwise counteract positive attributions by market actors, leading to decreased market value (Lange & Washburn, 2012).

The second reason higher clarity may provide diminishing returns is because it may put firms at greater risk of being targeted by activists should they misbehave in the future (King & McDonnell, 2015). Firms voluntarily disclosing environmental information that is too clear may also be viewed as seeking public approval, heightening the risk of sanctions in the event of future negative events that contradict sanctimonious declarations (Ashforth & Gibbs, 1990). This is especially likely with voluntary environmental disclosures, as the environmental behavior of firms often contradicts the values they publicly espouse (Lyon & Maxwell, 2011). In aggregate, these different attributions suggest an inverted U-shaped relationship of disclosure clarity to market performance. Low levels of clarity result in market actors perceiving firm intentions as manipulative, whereas greater clarity leads to sincere attributions and greater market value, although firms benefit less at high levels of clarity.

Hypothesis 2a (H2a): Market value has an inverted U-shaped relationship to disclosure clarity.

Accuracy moderates the inverted U-shaped relationship between disclosure clarity and market value. External verification or endorsement of information has been found to increase the credibility of information in the eyes of important actors (Sethi et al., 2017) thereby affecting whether or not the information release is judged as sincere or manipulative. Hence, accuracy can strengthen market actors’ sincere attributions of higher clarity because it acts as an external verification or endorsement that signals greater credibility (Connelly et al., 2011). As a result, the turning point where higher clarity provides diminishing returns to market value will shift rightward. Disclosures perceived as accurate (and more credible), are more likely to draw sincere attributions, thus lowering perceived risk of future exposure of hypocrisy through social or environmental crises or misdeeds.

Hypothesis 2b (H2b): Disclosure accuracy will positively moderate (shift rightward) the inverted U-shaped relationship between market value and disclosure clarity.

Transparency and Reputation Risk

In addition to the financial benefits of increasing transparency, firms may also gain reputational benefits with nonmarket actors, such as news media and the general public. Corporate reputation is developed over time as firms make strategic choices that provide information to stakeholders, which the stakeholders use to form impressions and judgments about the firm (Rindova et al., 2006). Enhanced reputations can serve as a critical resource that improves the firm’s relationship with important nonmarket actors and increases competitive advantage (Fombrun, 2015). Reputation may also serve an important risk-management function. Although prior work suggests that actions such as voluntary information disclosures and CSR can help firms with financial risk management (Kölbel et al., 2017), such actions can also reduce the risk to firm reputation. Managing reputation risks includes understanding both what creates risk as well as how to manage it (Andersen & Bettis, 2015). Firms face risks not only to their financial performance but also to their reputation with nonmarket actors. Given that a reputation is a perception or judgment of an organization, any changes in these collective judgments put the firm’s reputation at risk (Lange et al., 2011). As a result, managing the risk to a firm’s reputation is an important responsibility of firm leaders (Fombrun et al., 2000). For instance, prosocial activities such as CSR may provide insurance against risks to a firm’s reputation (Godfrey et al., 2009), and events such as involuntary product recalls may threaten a firm’s reputation (Rhee & Valdez, 2009).

Completeness and clarity in voluntary disclosure can play an important role in how stakeholders will perceive the locus of control and intention of a firm’s nonfinancial disclosure. For instance, firms perceived to be fully disclosing information related to CSR, and in a manner that is readily understood, were more likely to be perceived by the public as being unselfish in their disclosure (Godfrey et al., 2009). We develop arguments below about how each type of transparency can influence attributions made by nonmarket actors such as the media, thus leading to variations in firm reputational risks (Suddaby et al., 2017).

Effect of Completeness on Reputation Risk

As with market actors, disclosure completeness helps nonmarket actors determine whether a firm is acting in response to external or internal influences. Because collecting and disseminating information requires costly effort, firms that voluntarily release more information (i.e., more complete disclosure) are more likely to have nonmarket actors attribute transparency efforts to internal motivations rather than to external, situational factors. As a result, internal attributions will decrease reputational risk (Koh et al., 2014). Furthermore, more complete disclosures reduce the information asymmetry between firms and nonmarket actors. Thus, nonmarket actors can better anticipate negative actions or events, which also leads to a reduction in the likelihood that nonmarket actors attribute responsibility for a negative event to the firm, effectively limiting the subsequent risk to the firm’s reputation (Godfrey et al., 2009).

Meanwhile, firms are often faced with substantial external pressure to increase disclosure completeness (Lyon & Shimshack, 2015), as media portrayals and activist campaigns are frequently directed toward improving firm transparency on important social issues (McDonnell et al., 2015). Although increased disclosure completeness may also be the direct result of coercive pressure by nonmarket actors, these actors tend to view greater completeness of disclosure as a successful outcome (Marquis et al., 2016). Thus, even when the attributions about a firm’s nonfinancial disclosure are external, nonmarket actors still react positively. Because nonmarket actors are less likely than market actors to be concerned about reactive disclosure to external pressure, in general, they view complete disclosures more favorably, suggesting a negative linear relationship between the completeness of disclosure and reputational risk.

Hypothesis 3a (H3a): Greater disclosure completeness will decrease firm reputational risk.

Greater accuracy signals increased integrity and reliability of information disclosures and allows external actors to make more sophisticated inferences about the actual level of a firm’s sustainability activities (Bagnoli & Watts, 2017). Nonmarket actors, therefore, are more likely to believe that accurate disclosures are more credible and a more complete representation of firm activities and performance. We expect that greater accuracy will steepen the negative relationship between completeness and reputation risk, such that more accurate and more complete disclosures will be associated with lower reputation risk.

Hypothesis 3b (H3b): Disclosure accuracy will positively moderate (steepen) the relationship between disclosure completeness and firm reputational risk.

Effect of Clarity on Reputational Risk

Whereas the completeness of disclosure is negatively related to firm reputational risk, we suggest that the clarity of the information disclosed exhibits a more nuanced relationship with reputational risk. Clarity allows nonmarket actors to better comprehend or translate the information disclosed into meaningful judgments about the activities or events related to the firm. As with market actors, clarity speaks to the intentions of a firm’s motivations, as it allows nonmarket actors to make attributions about whether the information disclosure is sincere or manipulative. At low levels of clarity, nonmarket actors are more likely to attribute the firm’s intentions as manipulative because the disclosure is more difficult to understand, suggesting the firm is obfuscating its activities. For example, firms may hide poor environmental performance by disclosing information as a means of reputation management, thus creating an appearance of consistency between the firm’s practices and actors’ expectations (Elsbach & Sutton, 1992). Prior research suggests that firms may also manipulate the clarity of their disclosures to distort nonmarket actors’ perceptions of the firm’s activities (Merkl-Davies & Brennan, 2007). That allows firms to highlight more favorable data and obscure negative elements by manipulating visual or thematic presentations of information to present an idealized image of the firm (Talbot & Boiral, 2018). However, this may lead to greater reputational risk as nonmarket actors are more likely than market actors to attribute lower clarity as manipulative (Crilly et al., 2016).

Meanwhile, as clarity increases, reputational risk is mitigated as nonmarket actors attribute increased clarity to a more sincere effort by the firm to provide information that better allows evaluations of the firm. Because nonmarket actors can better understand the disclosure, they will have higher confidence in the firm’s efforts to improve environmental performance (Philippe & Durand, 2011), improving the firm’s ability to manage future crises or scandals (Coombs, 2007). Thus, higher disclosure clarity will be associated with lower reputational risk.

Hypothesis 4a (H4a): Greater disclosure clarity will decrease firm reputation risk.

Disclosure accuracy is also likely to negatively moderate the relationship between clarity and reputation risk as more precise and reliable information makes obfuscation and reputation management tactics less effective (Hahn & Lülfs, 2014; Marquis et al., 2016). Nonmarket actors who see that the firm is providing accurate information are less likely to make manipulative attributions and instead make sincere attributions about the firm’s intentions. Thus, we expect that accuracy will more often lead to sincere attributions at any level of clarity, reducing reputation risk even when information is difficult to understand.

Hypothesis 4b (H4b): Disclosure accuracy negatively moderates the relationship between reputation risk and clarity.

Method

We evaluate these hypotheses using analysis of corporate disclosures through a prominent information disclosure program (IDP) called CDP. CDP (formerly the Carbon Disclosure Project) is a London-based, not-for-profit organization supported by more than 800 institutional investors. CDP aims to increase transparency among corporations around the world by asking them to voluntarily disclose information about their greenhouse gas emissions and mitigation strategies as well as about the risks and opportunities they face with respect to climate change. This is an ideal context in which to examine issues surrounding transparency and nonmarket strategy because carbon disclosure is a complex issue that embodies multiple dimensions of transparency (such as completeness, clarity, and accuracy) as well as serving multiple types of stakeholders (market and nonmarket actors). Reporting to CDP has become standard practice among many companies, with more than 1,997 global companies representing 55% of global market capitalization voluntarily reporting to CDP as of 2015 (CDP, 2015, p.7).

Dependent Variables

Market value represents shareholder evaluations of corporate financial performance. In line with prior literature, we use Tobin’s q as a measure of relative market value, as it both considers total firm capital (equity and debt) and provides an asset-relative measure, such that acquisition or divestiture effects do not distort investor evaluations of financial performance over the sample period. We use the Chung and Pruitt (1994) method to approximate Tobin’s q using data from Thomson-Reuters Worldscope.

We use a constructed measure of media accounts to represent nonfinancial stakeholder evaluations of firm reputation risk. Media accounts are commonly used to measure the frequency (Lamertz & Baum, 1998) and valence (Bansal & Clelland, 2004) of exposure and conversations about firms among general public, consumer, and government stakeholders. We obtain our measure of reputation risk from RepRisk AG, a private organization that screens global media reports, NGOs, and governmental agencies for information about ESG performance of companies (Kölbel et al., 2017; Luo et al., 2015). The RepRisk Index (RRI) is a proprietary metric of monthly changes in reputation risk based on the relative severity of issues reported, the reach or influence of the source, and the novelty of the issue. The RRI, calculated on a scale from 0 to 100, is unique to each firm and updated daily as new media articles are released. Notably, RRI decays over time should there be no new risk events reported. For the first 2 weeks after a risk incident, RRI remains constant. After that time period, if the RRI is between 25 and 100, it decays at a rate of 25 every 2 months until it reaches 25. Once it reaches 25 (or if its below 25), it decays at a rate of 25 every 18 months until it reaches the value of 0. Firm’s RRI will gradually decay toward zero in the absence of media attention. Companies with little prior exposure would be more severely impacted by a new event, whereas companies that have a lot of past events would be less impacted by a new event. Generally, most multinational firms would have a RRI between 25 and 49. Our measure, which we label RepRisk, takes the average RRI value over the course of each calendar year as a proxy for general stakeholder evaluation of risk to ESG performance reputation.

Independent Variables

Completeness is based on CDP’s quantitative assessment of firm disclosure: the completeness of a firm’s response to CDP’s questionnaire. According to CDP, this score “assesses the completeness and quality of a firm’s response” and “signals that a company provided comprehensive information” about its climate change strategy and risk management (CDP, 2015, p.12). CDP assigns each firm a score on a scale from 0 to 100. Firms accrue points by responding to specific questionnaire items; a high score indicates that the firm provided all relevant information requested by CDP. Because stakeholders are more likely to assess firm financial performance and ESG performance within the context of the specific industries in which firms operate, we transformed this score into industry-relative values. Values are the focal firm’s score minus the average score of all scored firms operating in the same GICS (Global Industry Classification Standard) Industry Group (4-digit code). Thus, the variable Completeness is an industry-relative score for each firm-year observation.

Our Clarity score is based on CDP’s evaluation of how well the firm is “measuring, verifying and managing its carbon footprint” (CDP, 2015, p.12). CDP employs analysts that manually review the text of each firm’s response and assess how readily interpretable the information is, 1 as set forth in CDP’s scoring methodology (CDP, 2016). Our measure of Clarity represents CDP’s aggregate score from these questionnaire items distributed into six rank-ordered groups. As with Completeness, we transformed Clarity into an industry-relative measure. To measure Accuracy, we assign a binary indicator taking the value 1 for firms that provide evidence of obtaining third-party assurance of Scope 1 emissions inventory in their CDP disclosure, and 0 otherwise. Because CDP disclosures are voluntary and unaudited, external actors are more likely to perceive as accurate firm disclosures accompanied by formal verification from a certified assurer.

Control Variables

In line with prior research examining market value effects, we control for several corporate financial factors. Larger firms tend to have greater public visibility and are often subject to greater scrutiny regarding environmental impacts. We use ln Assets, which is the log-transformed value of total assets, as a relevant measure for firm size. Firm profitability is associated with greater resources and capacity for attention to CSR. We use the return on assets (ROA) measure of accounting profits. Firms carrying greater financial risk may be discounted by investors or perceived negatively by stakeholders; we use the debt-to-assets ratio (Debt Ratio) as a control for financial risk. We also control for firm Revenue Growth (annual percentage change in sales). All corporate financial data are obtained from Thomson-Reuters Worldscope.

Finally, we use the Thomson-Reuters ASSET4 equal-weighted ESG performance rating (ASSET4 Rating) to control for firm performance along issues broadly relevant to various stakeholder groups. We also considered individual ASSET4 dimensions corresponding to firm orientation to specific stakeholder groups (e.g., employees, customers, shareholders, and natural environment) but found the aggregate rating to provide a more parsimonious model according to the Bayesian information criterion.

Analytical Approach

We employ a panel data estimation to determine how the completeness, clarity, and accuracy of firm disclosures are related to market value and reputational risk. Tests for H1 and H2 use the natural log of Tobin’s q as the dependent variable Market value,

2

and tests for H3 and H4 use the RepRisk Index as the dependent variable RepRisk. To account for high correlation between the two main independent variables, we first transform Completeness and Clarity using the Gram–Schmidt orthogonalization technique (Sine et al., 2006),

3

which includes mean centering Completeness and Clarity. RepRisk is also included as a control in the market value models. Our baseline empirical model (with Tobin’s q as dependent variable) is provided in Equation 1, where subscript i denotes an individual firm and t denotes year.

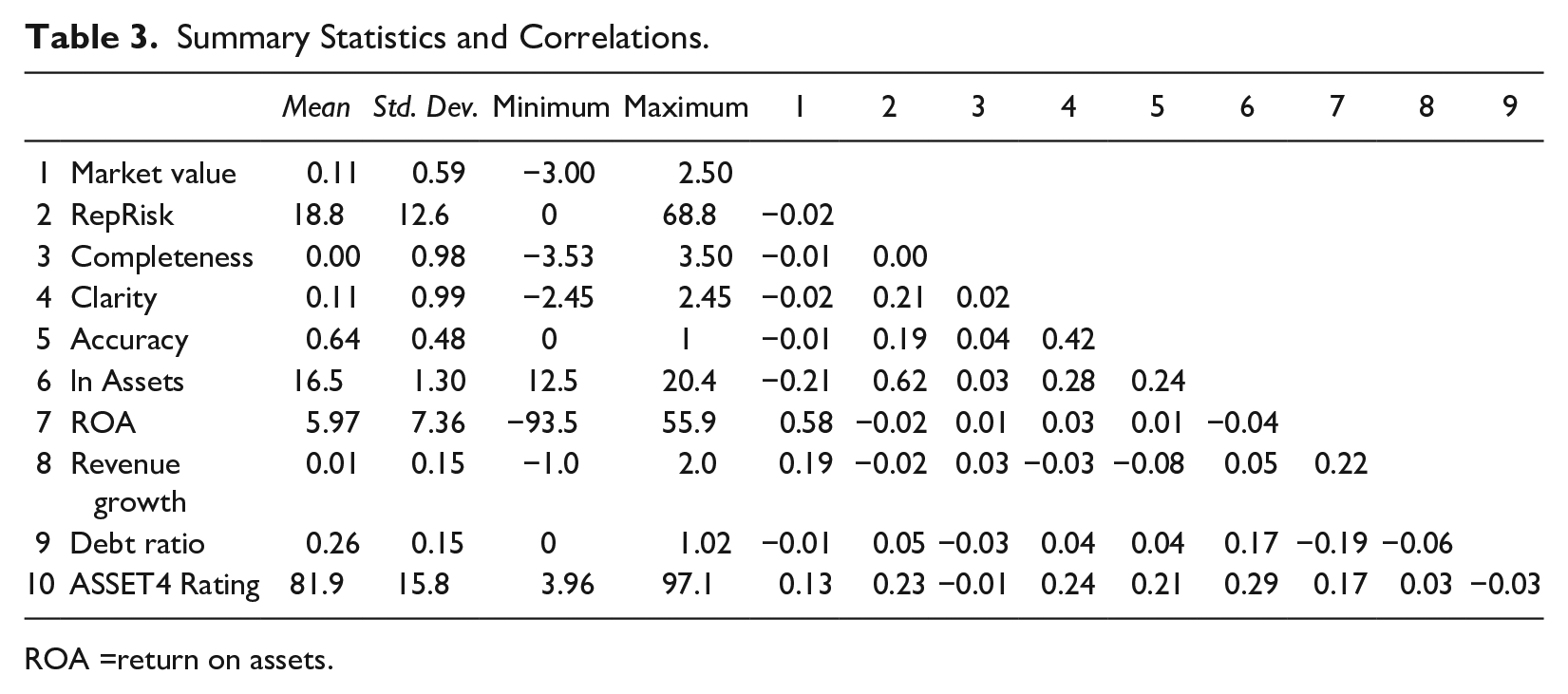

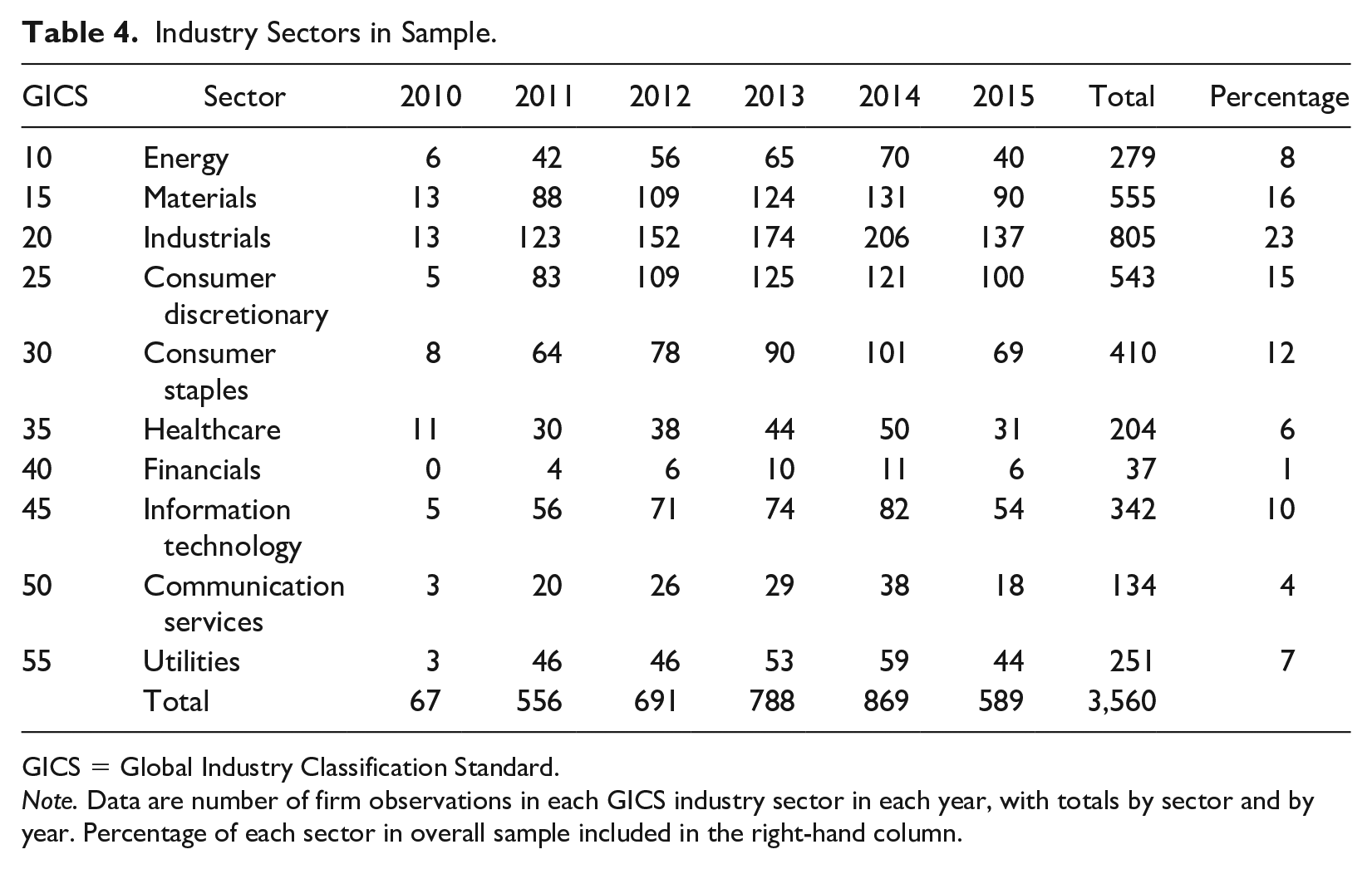

Table 3 lists summary statistics and correlation coefficients for the variables used in our analysis. Most correlations are significant at the 95% confidence level; a test of variance inflation factors (VIFs; all individual VIFs <2.0; model VIF = 1.27) indicates that multicollinearity is not a concern. To account for unobserved, time-invariant, firm-specific factors, we use firm-level fixed effects, with robust standard errors clustered on individual firms. We also include a set of year dummies to control for unobserved market trends and synchronous shocks. The final sample consists of 3,560 firm-year observations from 1,026 individual firms over the years 2010 to 2015. 4 Relative to major firm indices (e.g., S&P 500), industry composition of the sample is slightly overweighted to environmentally sensitive industries (e.g., Energy, Materials, Industrials, and Utilities) and consumer-facing industries, likely owing to the sectoral focus of CDP (see Table 4).

Summary Statistics and Correlations.

ROA =return on assets.

Industry Sectors in Sample.

GICS = Global Industry Classification Standard.

Note. Data are number of firm observations in each GICS industry sector in each year, with totals by sector and by year. Percentage of each sector in overall sample included in the right-hand column.

As a robustness check, to account for potential sample selection bias (i.e., we sample only on firms that disclose to CDP), we employed a Heckman selection model employing multiple exclusion restrictions. Although results of this analysis are not reported here, we found that Heckman’s lambda (the inverse Mills ratio) was not significant, nor did including the first step regression change any of the focal results, indicating that selection bias is not an issue.

Results

Market Value

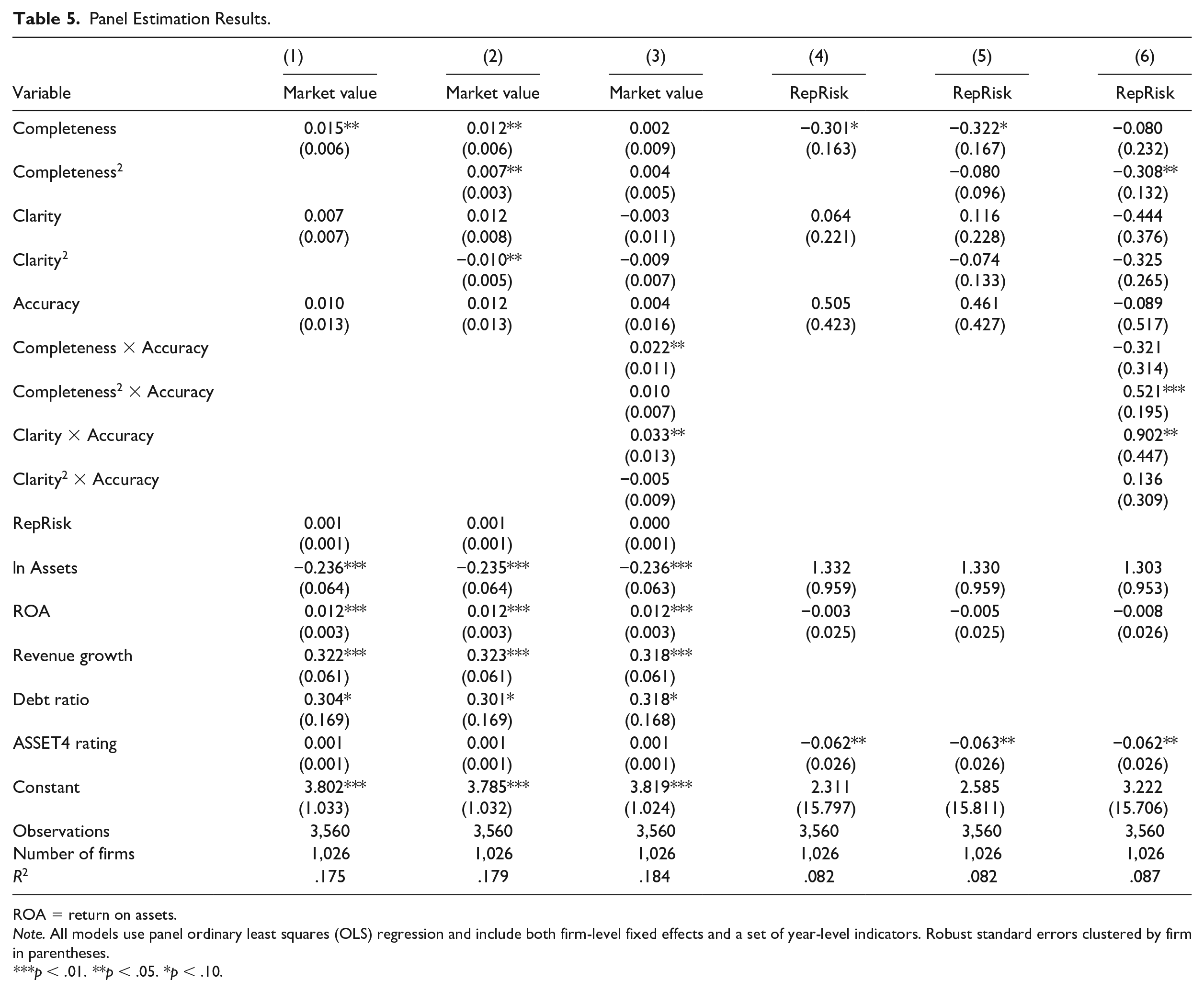

Table 5 displays the results of regression models testing the study hypotheses. Models 1 and 4 include linear functions of the independent variables Completeness and Clarity, Models 2 and 5 include quadratic terms, and Models 3 and 6 include interaction terms with Accuracy.

Panel Estimation Results.

ROA = return on assets.

Note. All models use panel ordinary least squares (OLS) regression and include both firm-level fixed effects and a set of year-level indicators. Robust standard errors clustered by firm in parentheses.

p < .01. **p < .05. *p < .10.

Model 1 results indicate that market actors value greater completeness of disclosure, although clarity of information appears not to be significantly related to firm value (p = .35). The coefficient of 0.015 (p = .02) suggests that a one-standard deviation increase in completeness corresponds to a 1.5% increase in market value, all else equal. Including quadratic terms of the explanatory variables (Model 2) provides a more nuanced picture. Completeness has a significant, positive quadratic relationship with firm value (p = .04), indicating support for H1a (U-shaped relationship). Moreover, Clarity has a significant, negative quadratic relationship with market value (p = .03), indicating support for H2a (inverted U-shape). Next, in Model 3, we interact all independent variable quadratic terms with Accuracy; linear coefficients of these moderator terms are significant (β = 0.022, p = .05; β = 0.033, p = .01), whereas the unmoderated coefficients are all not significantly different from zero, suggesting higher market value associated with perceived accuracy in disclosure. These results clearly indicate a complex, nonlinear relationship between market value and transparency.

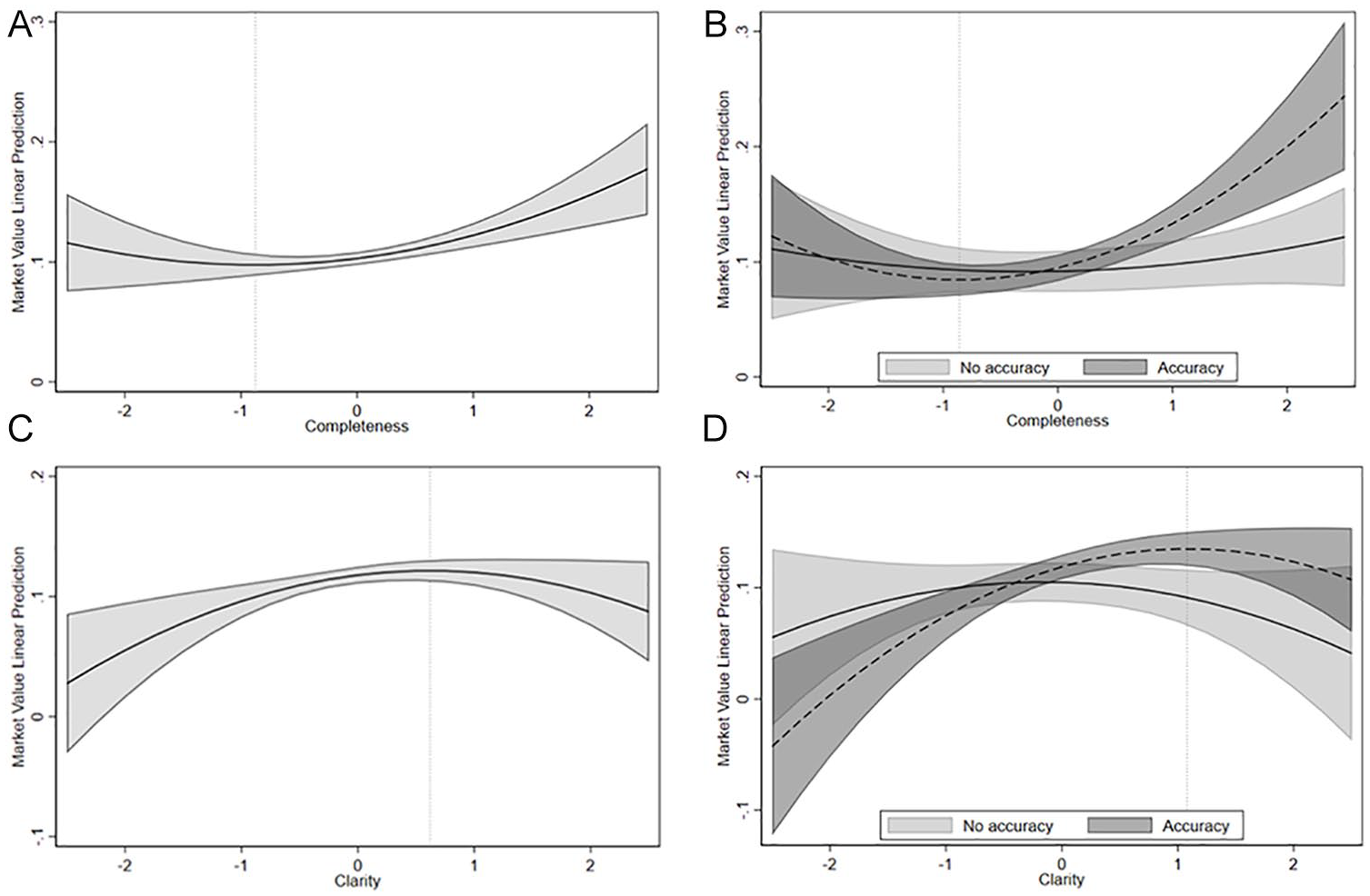

To better comprehend the nature of these relationships, we plotted the marginal effects of each independent variable on market value, shown in Figure 3. Figure 3(A) displays the relationship between completeness and market value. The horizontal axis indicates the orthogonalized (i.e., standardized) value of Completeness; zero indicates disclosure equivalent to industry group average, and positive values indicate higher completeness, with each integer increment corresponding to one standard deviation. The vertical axis is the model-predicted value of the dependent variable (Market value) computed at the sample means of all other covariates. Shaded areas represent 90% confidence intervals, and the vertical dotted line indicates the turning point (extremum) of the quadratic function. Figure 3(A) indicates that firms that increase disclosure completeness near and above their industry average are rewarded with higher market value, all other factors held constant, suggesting a favorable, internal attribution by market actors. 5 Figure 3(B) displays the moderating effect of Accuracy, indicating a steepening of the relationship between Completeness and Market value. Figure 3(C) indicates Market value gains for increased Clarity up to and beyond industry mean, with a slight Market value penalty at higher levels of Clarity, whereas Figure 3(D) indicates rightward shift (vertical dotted lines show the turning point) of this relationship for perceived accuracy in disclosure.

Marginal Effects of Standardized Values of Completeness and Clarity on Market Value. (A) Effect of Completeness on Market Value. (B) Effect of Completeness on Market Value, Moderated by Accuracy. (C) Effect of Clarity on Market Value. (D) Effect of Clarity on Market Value, Moderated by Accuracy.

To statistically verify the observed U-shaped relationships, we performed multiple tests of the significance of the quadratic relationship (Haans et al., 2016). First, the U-shaped relationship is valid if the local extremum lies within the range of the x-axis variable; Figure 3 plots include vertical dotted lines marking the locations of the extrema. We use the Fieller method (Lind & Mehlum, 2010) to compute confidence intervals of the respective extrema. Both Clarity and Completeness have 80% Fieller confidence intervals fully bounded by the working range of the variables, indicating support for the hypothesized U shapes. 6 Second, for an observed U-shaped relationship to hold, the slopes of the response curve at the upper and lower limits of the explanatory variable range must be significantly different from zero. We employ the Sasabuchi (1980) test of the joint significance of the slopes at upper and lower limits (Fernhaber & Patel, 2012) and confirm that both Clarity (p = .05) and Completeness (p = .07) have slopes at the range limits significantly different from zero. Finally, we follow Haans et al. (2016) method for verifying the significance of moderator relationships; the significance of linear interaction terms indicates Accuracy leads to an upward shift (but no steepening) in the relationship of Completeness to Market value; moreover, the slopes of accurate and “inaccurate” response curves are significantly different (p<.01), providing partial support of H1b. Meanwhile, we observe a significant shift rightward (p=.08) in the relationship of Clarity to Market value (see vertical dotted lines in Figure 3(C) and (D)), supporting H2b.

Reputation Risk

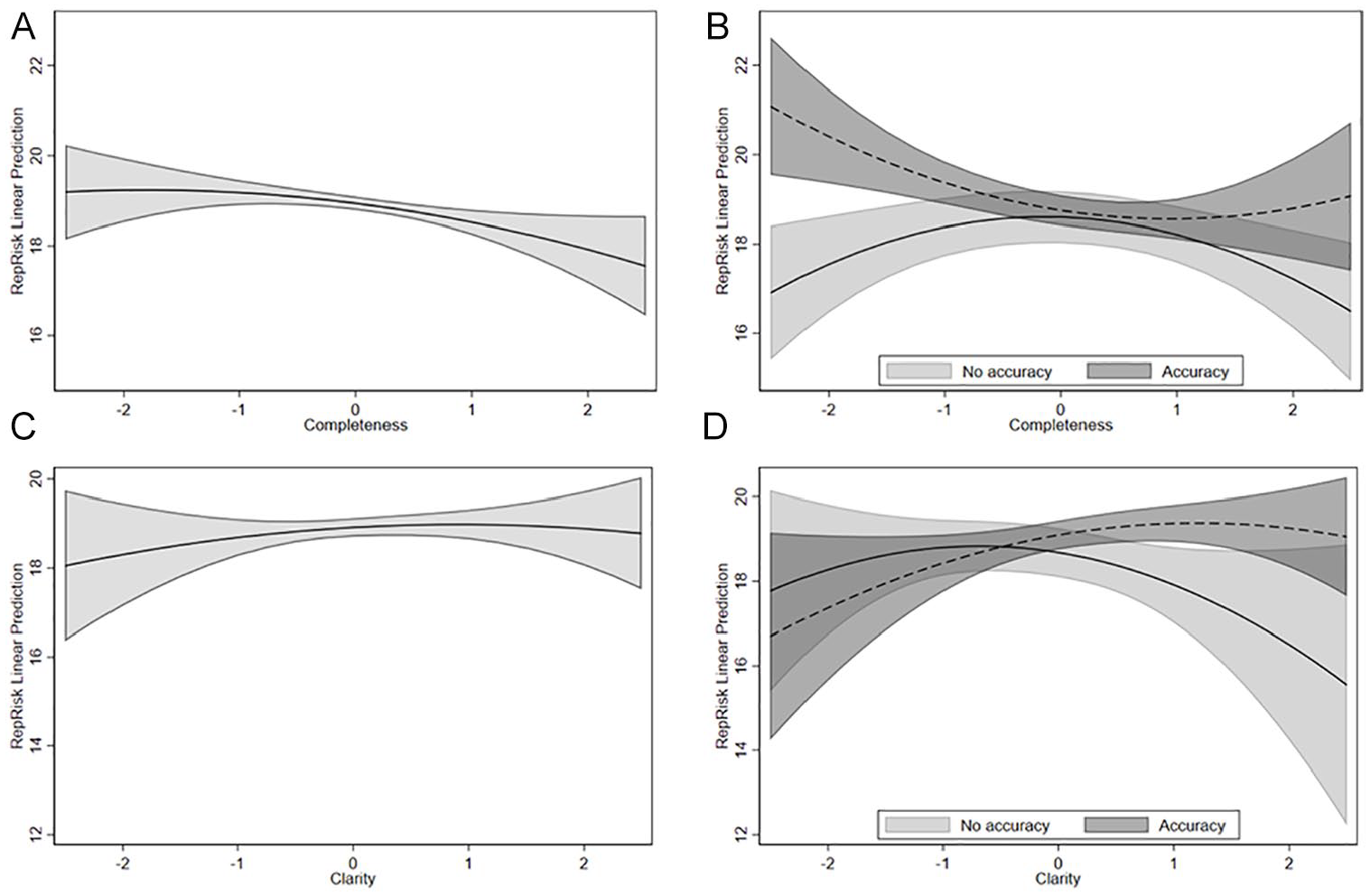

With respect to reputation risk, Models 4 and 5 results indicate that nonmarket actors attribute lower reputation risk to firms with greater Completeness, supporting H3a. A one-unit increase in Completeness results in a 0.3 unit decrease in reputational risk (p = .06). Meanwhile, neither quadratic nor linear coefficients on Clarity are significant, failing to support H4a. Including interactions with Accuracy again indicates more nuanced relationships (Model 6); opposite signs of quadratic term coefficients on Completeness signify opposing nonlinear effects of Accuracy, suggesting nonmarket actors make different locus of control attributions depending on perceived disclosure accuracy. Figure 4 illustrates these relationships graphically; Figure 4(B) displays the opposing attributions of Completeness (standardized) over Accuracy, suggesting perceived accuracy of incomplete disclosures is associated with greater reputation risk, partly contradicting H3b. Meanwhile, Figure 4(D) displays a slightly heightened reputational risk attributed to accurate disclosures at higher clarity (standardized), contradicting H4b. Although tests for significance of U shapes (Haans et al., 2016) in these moderated relationships are not supported (p>.15), we do find a significant steepening of the effect of Completeness on RepRisk by Accuracy (p<.01). Table 6 shows a summary of each hypothesis and whether it was supported to help clarify the results of our analysis.

Marginal Effects of Standardized Values of Completeness and Clarity on Reputation Risk. (A) Effect of Completeness on Reputation Risk. (B) Effect of Completeness on Reputation Risk, Moderated by Accuracy. (C) Effect of Clarity on Reputation Risk. (D) Effect of Clarity on Reputation Risk, Moderated by Accuracy.

Summary of Analytical Results.

We employed several robustness checks. To evaluate potential higher order effects, we included cubic terms of the two main independent variables and found the curvilinear response to be largely unchanged. Alternately controlling for emissions-intensive industries and including a set of industry indicators (i.e., industry fixed effects) likewise had no significant impact on results. To check for the influence of outliers, we also winsorized financial variables at 5% and 95% levels, again finding only minor impact to results. Using nonorthogonalized versions of the independent variables yielded modest changes in results, though we also observed that alternately removing each variable from regression models yielded unstable coefficients, a key indicator that multicollinearity is confounding results, and supporting our use of orthogonalized variable measures. Finally, as noted above, correcting for potential selection bias using Heckman’s method did not change results.

Discussion and Conclusion

The core finding of our study is that different actors respond differently to distinct dimensions of transparency in corporate nonfinancial disclosures which has implications for how these disclosures can impact real, sustainable change within organizations. Because sustainability-related changes within an organization often depend on the behavior of external actors who deploy nonfinancial information (Sharma & Henriques, 2005), our study enhances the understanding of the relationships and interdependencies of different users of nonfinancial disclosures. Prior research on the outcomes of transparency has been mixed: while transparency sometimes offers benefits to the firm (Lange & Washburn, 2012; Philippe & Durand, 2011), its influence is not always beneficial (Briscoe & Murphy, 2012). In this study, we provide an explanation for these mixed results by offering evidence that two dimensions of transparency—disclosure completeness and clarity—are viewed in different ways by market (i.e., shareholders) and nonmarket actors (e.g., the media and the general public), resulting in different market and nonmarket outcomes. We also find that a third dimension of transparency reflecting the reliability or quality of the information—accuracy—moderates these effects. These findings advance our understanding of the critical linkages between nonfinancial disclosure and actor-specific firm outcomes, which have important implications for sustainability-related firm behavior (Dubbink et al., 2008; Jackson et al., 2020).

Our findings provide evidence that market actors view transparency in a more nuanced way than previously understood. Firms with high levels of disclosure completeness obtain higher market value, whereas firms with low to moderate levels of completeness receive no significant benefit from—and are possibly penalized for—increasing disclosure completeness as shown in Figure 3(A). We suggest that market actors may make more positive attributions if firms disclose very little, as such firms may be perceived as having superior information strategies, as being more effective at protecting proprietary information, or as better managing costs of transparency. However, market actors may perceive incremental increases in disclosure completeness from low-transparency firms as a reaction to external coercion, which comes at the risk of losing advantages from competitive secrecy. This finding supports the value of practice opacity (Briscoe & Murphy, 2012) and highlights the notion that increased transparency is not always perceived to be in the best interest of firms. However, our findings clearly suggest that accuracy amplifies positive attributions for more complete disclosures, which is shown in Figure 3(B), resulting in higher market value. This suggests that increasing the accuracy of disclosures may be an effective approach for transparent firms but has little value for less transparent firms.

Market actors react to disclosure clarity in a very different way than for disclosure completeness, as shown in Figure 3(C). In disclosures with low clarity, market actors may perceive firms as intending to manipulate their performance or exposure to risk. As clarity increases, market actors increasingly perceive the firm’s motivation as sincere and can better gauge the firm’s activities. In line with our arguments, the upper bound of the inverted U-shape relationship is weakly significant and thus indicative of decreasing marginal returns to clarity; while additional clarity does not appear to dramatically hurt firm value, there is a point of diminishing returns for the effort to provide complete information. We also find that the turning point in the curvilinear relationship is greater for accurate disclosures—shown in Figure 3(D), demonstrating the value of improving credibility of information, which is consistent with our findings on completeness and accuracy.

The contrast between how market and nonmarket actors respond to these two dimensions of transparency is revealing. Our finding that market actors prefer firms they perceive as being proactive rather than reactive supports prior research (Husted & De Jesus Salazar, 2006). Furthermore, our analysis suggests overall that nonmarket actors value greater transparency as it provides them with a better understanding of the risks the firm faces (Vicente-Lorente, 2001). Nonmarket actors view transparency in a much simpler way than market actors as they see more complete disclosures as an important corporate responsibility; yet, on the surface, they do not similarly attend to the level of clarity in disclosure. As theorized, the greater the completeness of disclosure, the more likely nonmarket actors are to make internal attributions of firm transparency, leading to decreased reputational risk. This suggests that greater completeness leads nonmarket actors to view firms as trustworthy or as reliable corporate citizens because such firms are willing to publicly disclose more comprehensive information about their activities. Whereas the decreasing relationship is strong and significant, the interaction with accuracy reveals nonlinear effects in this relationship, as shown in Figure 4(B). Findings indicate little benefit to perceived accuracy at high completeness, while accuracy is instead associated with greater reputation risk at low completeness. This surprising result suggests that perceived accuracy intensifies nonmarket actors’ external (rather than internal) attributions of disclosure completeness—highlighting the superior ability of specialist stakeholders to recognize decoupling (Crilly et al., 2016) and challenging the notion that costly signaling of accuracy improves actor perceptions (Bagnoli & Watts, 2017).

Meanwhile, the null result for disclosure clarity and reputation risk is surprising in light of prior findings that nonmarket actors may hold higher expectations and subject firms to greater scrutiny when claims of performance are made clearer (Carlos & Lewis, 2018; Marquis et al., 2016). Moreover, whereas accuracy is associated with greater reputation risk at low completeness, it is also weakly associated with greater risk at high disclosure clarity, as shown in Figure 4(D). This nonintuitive result suggests sincere attributions may carry an unwelcome side effect: Firms that cultivate a virtuous image and high-performance expectations are more likely to be targeted by nonmarket actors because even a small misstep becomes more noticeable and damaging to firm reputation (King & McDonnell, 2015). In such cases, nonmarket actors are more likely to punish the firm for misdeeds (Carlos & Lewis, 2018). Overall, our findings suggest that simply disclosing more information may send a stronger signal of overall transparency, whereas higher clarity may put firms at greater reputational risk.

Overall, our findings help illuminate boundary conditions to the relationship between nonfinancial disclosure and actor reactions. Different dimensions of transparency affect the perceptions and decisions of key actors external to the firm. Our primary contribution is the application of attribution theory to provide a relevant and appropriate perspective for understanding the mixed findings on how key actors view transparency in firm disclosures. Our findings that both market and nonmarket actors hold distinct views of disclosure completeness, clarity, and accuracy suggest that firms must carefully weigh the relative influence of different stakeholder groups when determining the appropriate levels of disclosure (Mitchell et al., 1997).

We also make several important empirical and methodological contributions. First, we contribute to the understanding of corporate reputation by exploring the impact of firms’ reputational risk rather than the magnitude of reputation, which has already been studied (e.g., Philippe & Durand, 2011). Furthermore, we highlight the role of IDPs (Miller et al., 2017) by calling attention to the way these programs can influence actor attributions of firm transparency. Whereas many stakeholder groups are challenged to interpret and infer truthfulness of proprietary voluntary disclosure by firms (e.g., independent corporate sustainability reports), IDPs offer standard disclosure formats and evaluative ratings that simplify stakeholder assessments. IDPs thus provide valuable services, akin to financial reporting standards, that enable more uniform judgments of firm transparency and other relevant performance metrics. Finally, our quadratic model specification reveals the nuanced relationship described here, one that was not evident from a simple linear estimation. These results highlight the importance of model specification in understanding multidimensional effects, particularly in areas with ambiguous market value implications, such as transparency in nonfinancial matters.

Future Research and Limitations

This study highlights several new paths for future research. Although we examined firm transparency around climate change strategy and risk management, our approach is generalizable to other modes of nonfinancial disclosure. A primary opportunity is to consider how the reactions of external actors to these disclosures subsequently impacts future firm actions such as their environmental performance. Future studies might also seek to learn more about how the managers of disclosing organizations adjust the information dimensions of transparency to suit different actors and respond to resistance they may face (Wickert & De Bakker, 2018). Regarding reputation risk, we still know little about the relationship between reputation risk and reputation; future work may explore mechanisms by which increased reputation may mitigate or exacerbate reputation risk, and the associated dimensions of firm reputation. Next, we know little about the direction of causality with reputational risk and reporting. For example, are firms with higher reputational risk driven to disclose more, or do firms that disclose more invite more scrutiny? We also know little about whether these relationships vary between categories of reputation (i.e., governance, environmental, and social). Finally, from a methodological standpoint, this study highlights the importance of considering alternative functional forms of empirical relationships to provide an accurate estimation of firm outcomes; we hope future research will follow this lead to improve overall methodological rigor.

An important limitation of our study is that our measures of market and nonmarket actor perceptions are based on market value for market actors, and on media perceptions for nonmarket actors. We recommend that future research examine other measures of performance because stakeholder expectations may vary in ways that are not easily captured by market value or media attention. For example, recent work shows that stakeholder expectations of firm nonfinancial performance evolve over time (Hawn et al., 2018), especially as emerging third-party disclosure mechanisms stabilize and become institutionalized. In addition, our arguments suggest that there is little benefit to firms for disclosures that are low in clarity, as both market and nonmarket actors view these disclosures negatively. As a result, we believe that future research should explore the conditions under which firms can successfully use low clarity disclosures to improve their standing with external actors.

In conclusion, understanding external attributions of transparency is increasingly important to firms that voluntarily disclose nonfinancial information about their social and environmental activities and performance. Our study provides evidence that market and nonmarket actors react to different components of transparency (i.e., completeness, clarity, and accuracy) in unique and more nuanced ways than previously understood. This result is important in helping firms understand that the release of this information can send very different signals to market and nonmarket actors, as they may attribute different types of transparency in distinct ways. As external constituencies other than shareholders become increasingly important mechanisms for social control, understanding the way that nonmarket actors attribute firm motivations of nonfinancial disclosure will help firms not only improve financial performance and mitigate reputational risk but also better align social and environmental performance with societal expectations.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.