Abstract

Voluntary environmental programs (VEPs) offer opportunities for companies and stakeholders to improve environmental outcomes valued by society in the absence of regulatory mandates. Research has addressed numerous antecedents for firm adoption of VEPs, enhancing knowledge of how stakeholders and firms engage on substantive issues of public importance. However, program adoption is dynamic, and stagnant participation rates may threaten program longevity when firms do not realize expected benefits. Prior literature has not sufficiently addressed the factors that compel firms to drop out. In this study I articulate three consequential drivers of firm commitment to VEPs—transparency, effort, and achievement—and empirically estimate their effects on firm disengagement from one such prominent program: CDP (formerly known as Carbon Disclosure Project). Findings indicate that firm transparency and effort represent powerful commitment mechanisms driving continued program participation. This study contributes to theory over multiple literatures related to VEP participation and offers practical guidance for both VEPs and firms.

Keywords

Introduction

Voluntary environmental programs (VEPs)—institutions formed to improve corporate transparency and performance on issues of broad environmental concern in the absence of government regulation—are an important, ongoing subject of scholarly research. VEPs are widely perceived as beneficial institutions, promising improved outcomes for the environment, society, and the firms that adopt them. Primary drivers of VEP adoption by firms include various institutional forces and firm-specific resources and capabilities (see Tashman et al., 2021, for a recent review). Understanding these antecedents has enabled improvements in institutional effectiveness from the stakeholder perspective (Alberini & Segerson, 2002; Borck & Coglianese, 2009).

However, for VEPs to persist, they must not only effectively serve stakeholder interests by enabling improvements in desired outcomes (which effectiveness is highly scrutinized; see Aragon-Correa et al., 2020) but also encourage continued participation among targeted firms. Firms require some private net benefit (e.g., reputation, legitimacy, reduced costs, customer traction, reduced scrutiny, or risk management) to drive continued participation. Improving our understanding of contributors to (or deterrents of) firm decisions to cease participation—to “drop out”—is important because of the potential impact on VEP effectiveness. Increasing dropout of participant firms destabilizes programs (Gaba & Dokko, 2016). VEPs that are unable to motivate continued firm participation are more likely to be disbanded (Lenox, 2006), while damages to reputation of one program may spill over to similar organizations (Grant & Potoski, 2015), reducing effectiveness of other programs across a given issue domain.

While prior research has thoroughly addressed antecedents of VEP adoption by firms, it has yet offered relatively little explanation for firm decisions to drop out. Several recent review articles and meta-analyses cover adoption of VEPs and closely related standards in various contexts and from multiple theoretical and practical angles (e.g., Aragon-Correa et al., 2020; Boiral et al., 2018; Tashman et al., 2021; Tuczek et al., 2018; Velte et al., 2020), yet reveal a lack of attention to the matter of dropout. This is an important and unresolved question, as prior theoretical work suggests observation of dropouts from a particular practice may enable more accurate inference about the value of that practice to continuing participants or prospective adopters (Terlaak & Gong, 2008). Firms have incentives to improve environmental performance (Chatterji & Toffel, 2010), but such efforts are costly and may be associated with symbolic management (Delmas & Montes-Sancho, 2010; Philippe & Durand, 2011)—providing the perception of conformance without substantive efforts or improvements. Moreover, escalating efforts by firms to conform with stakeholder expectations over environmental performance (Tetrault Sirsly & Lvina, 2019) may blind managers from value-destructive courses of action, for example, over-investing in environmental management at the risk of compromising the firm’s competitive position. Finally, while VEP features that impose excessive conformance costs have been found to discourage adoption (Tashman et al., 2021), once a firm has adopted a program the marginal costs of continued participation are often lower (Hsueh, 2019).

This tension motivates an examination of the factors associated with VEP dropout, distinct from those commonly associated with initial adoption. Continued participation by firms requires inputs to the program (e.g., costly effort or transparency; Bansal & Bogner, 2002; Hahn & Lülfs, 2014), which in turn generates outputs valued by both firms and stakeholders (e.g., recognition of performance; Fabrizio & Kim, 2019; A. A. King et al., 2005). Such outputs are often highly valued by firms as a source of legitimacy but vary to the extent that they accurately signal true firm performance. As such, a major theme in research on sustainability management concerns disentanglement of symbolic versus substantive management (Christmann & Taylor, 2006; Delmas & Montes-Sancho, 2010; Hyatt & Berente, 2017)—determining whether firms “walk the walk.” Firms may also find intrinsic benefits to VEP participation, such as increased innovative capacity (He & Shen, 2019; Prieto-Sandoval et al., 2016) and improved governance (Bui et al., 2020), but such outcomes are often difficult for firms to accurately measure and attribute (Peloza, 2009). While firms may vary in ability to recognize direct or indirect benefits from participation (Iraldo & Barberio, 2017), propensity to continue participation or to drop out may also depend on the degree to which these inputs and outcomes lead to implicit commitments to the program through factors such as heightened stakeholder awareness or establishment of organizational routines—a possibility heretofore largely overlooked.

This study takes up this challenge by examining two distinct and complementary explanations for the propensity of firms to drop out from VEPs. I develop theory on two sets of factors, the first rooted in extant literature and the second representing a novel contribution. Traditional antecedents—institutional drivers and firm-specific factors—that support continued participation are the same factors that drive initial adoption; where forces are stronger, more firms will join and fewer firms will drop out. The second set, which form the core focus of this study, are consequential factors that arise through a firm’s ongoing experience with the program and create implicit commitment to continued participation. I characterize these three factors as transparency (disclosure of participation), effort (substantive firm inputs toward meeting VEP objectives), and achievement (VEP recognition of those efforts and conformance with objectives). Regardless of substantive or symbolic intent, these factors all arguably serve to support stakeholder perceptions of firm alignment with VEP goals. These consequential factors, associated with the interactions and relationship between firm and VEP accrued through continued participation, arguably overshadow the traditional antecedents and better predict the propensity for dropouts over time. To assess these factors, I construct and analyze a data panel spanning 13 years of firm adoption of and disengagement from a prominent VEP, CDP (formerly known as Carbon Disclosure Project). CDP is a stakeholder driven VEP emphasizing information disclosure and performance along a globally relevant environmental issue (climate change), making it an ideal VEP in which to study this phenomenon. I apply a rigorous empirical approach that integrates survival analysis of firm’s VEP participation with selection bias correction and multiple imputation (MI) methods. Findings indicate that firm transparency over participation drives implicit commitment to VEP participation, overshadowing the effects of traditional antecedents established in literature on VEP adoption. I also demonstrate that greater effort—the commitment of resources toward program participation and conformance—also drives continued participation, whereas achievement effects are significant mainly in industries subject to government regulation complementary to the VEP.

This study makes several contributions to theory and practice. First, I theorize and empirically examine these consequential factors associated with continued VEP participation by firms, developing knowledge on the contributors of program dropout and thus deepening our understanding of interactions between VEP structure and firm behavior. It also contributes to broader legitimacy theory by distinguishing between types of legitimacy attained through aspects of VEP participation. The findings also contribute to a burgeoning literature on corporate carbon disclosure, highlighting the relative value of heightened information disclosure over third-party performance assessments toward program effectiveness. Finally, the findings offer important implications for practice. For VEPs, the study demonstrates the critical quality of promoting transparency and effort among participating firms to limit dropout and enhance program longevity. For firm managers, it highlights the need to consider long-term implications of VEP adoption decisions and the value in contributing substantive efforts in participation, above mere pursuit of formal recognition.

Theory

VEPs create opportunities for firms to engage with various stakeholders on issues related firm environmental impacts and related activities. VEPs have been extensively studied across multiple disciplinary literatures with a corresponding proliferation of labels and definitions. In the context of this study, I define VEPs as either centralized or decentralized institutions developed to systematically address a defined aspect of corporate environmental impacts, management, or performance, soliciting or recognizing participation by firms on a voluntary basis, with three key defining features: (1) standards of conformance prescribed by an external body, (2) some minimal level of effort by participating firms required to achieve those standards, and (3) some measure of external evaluation as evidence or recognition of achievement, which may be self-declared by firms or certified by a third party. Regarding the latter two features, this definition does not specify any particular level of stringency of standards or monitoring and enforcement of conformance, two factors established in literature as key to VEP effectiveness (Prakash & Potoski, 2012; Tashman et al., 2021). VEPs thus include institutions such as government initiatives (Delmas & Montes-Sancho, 2010; Kim & Lyon, 2011b), information disclosure programs (Etzion & Ferraro, 2010; Kim & Lyon, 2011a; Miller et al., 2017), industry self-regulatory programs (A. A. King & Lenox, 2000; Lenox & Nash, 2003), environmental management systems (Christmann & Taylor, 2006; A. A. King et al., 2005), and product or process certification programs (e.g., ecolabels; Bullock & van der Ven, 2020; Darnall & Aragón-Correa, 2014). Formal declarations or pledges (Amer, 2018), for example, do not meet this definition, as these arguably do not meet a threshold level of required effort, and often provide vague standards that prevent effective evaluation of achievement. VEPs are initiated by any of several types of institutional actors—including government agencies, industry consortia, independent standards bodies, or other ad hoc nongovernmental organizations—with varied and distinct motivations to draw stakeholder attention to corporate policies or performance on target issues and drive improvement along key dimensions of those issues.

Firm incentives to join, or adopt, these programs are well-documented in the literature and can be loosely categorized as institutional drivers and firm-specific factors (Tashman et al., 2021). Institutional antecedents refer to various pressures from formal institutions, such as government regulators (Matsumura et al., 2013), and informal institutional factors such as social movements (B. G. King & Soule, 2007), stakeholder demands (Flammer et al., 2019), and firm visibility (Aronson & LaFont, 2020). Firm-specific factors may also motivate adoption, such as financial and environmental performance (Prakash & Potoski, 2012), characteristics of firm executive leadership (Lewis et al., 2014), or strategic fit with extant capabilities (Dowell & Muthulingam, 2017). Industry factors such as customer requirements (A. A. King et al., 2005), competitive dynamics (DeBoer et al., 2017), and industry association pressures (Tyler et al., 2020), may straddle these two categories.

However, we know relatively little about the capacity of VEPs to drive continued participation by firms over time—demonstrated by an ongoing engagement with the VEP with commensurate effort toward maintaining conformance and/or certification. Failure to grow or maintain participation by firms may lead to disbandment of VEPs (Lenox, 2006), potentially further affecting the ability of similar or complementary initiatives to take hold (Etzion & Ferraro, 2010). VEP disbandment is of substantial concern where those programs provide valuable public goods while simultaneously enabling improved corporate outcomes. Whereas extant literature implicitly suggests that institutional and firm-specific antecedents of initial VEP adoption by firms are also relevant to continued participation, I argue that a firm’s motivations to either continue participating over the long run or to drop out are fundamentally transformed through a firm’s direct experience with its participation in the program. That is, certain consequential factors—those developed as the firm engages with the VEP over time—are more likely to explain a firm’s propensity to drop out of a VEP, barring major changes in traditional drivers over time. More specifically, ongoing efforts that increase a firm’s implicit commitment to a VEP—that is, factors that may compel a firm to continue participation through perceived costs associated with dropping out—will drive continued participation more so than institutional and firm-specific antecedents. The following discussion briefly summarizes numerous traditional antecedents of VEP adoption and how they may likewise drive continued participation (Hypotheses 1a and 1b). I then introduce and theorize on the concept of these consequential antecedents (Hypotheses 2-4).

Institutional and Firm-Specific Antecedents

Institutional Factors

Institutional pressures (e.g., mimetic isomorphism, government regulation, primary stakeholder interests, and broader social movements) contribute to the initial adoption decision and tend to continue as positive drivers toward continued participation by individual firms. For example, if a company is compelled to implement and certify an environmental management system through customer pressure, barring any dramatic change in customer makeup, that demand is likely to persist as a driver of continued participation realized through periodic recertification.

The uptake of environmentally responsible practices is often prescribed to address legitimacy concerns (Bansal & Roth, 2000); wherein firms may target pragmatic legitimacy (engaging stakeholders’ self-interest) or moral legitimacy (perceived as promoting societal welfare) through VEP participation (see Suchman, 1995). If participating firms begin to drop out from a program, then participating firms may perceive the benefits to legitimacy from ongoing VEP participation are limited (Terlaak & Gong, 2008). Many VEPs indirectly support broader social movements and thus have the potential to wield substantial influence over firm policy (B. G. King & Soule, 2007). Whereas specific social movements rise and wane over time and location (Orcos et al., 2018), the broader freedom of media and the public to speak out remains generally consistent over time in the form of legal protections and cultural norms (Marquis et al., 2016). Where such social pressure exists to drive firm adoption, that continued pressure is likely to induce continued participation. Moreover, firm visibility is commonly associated with sensitivity to institutional pressures and may influence a firm’s environmental strategy (Chiu & Sharfman, 2011). Given the heightened scrutiny of highly visible firms by media and the public, such visible firms that have adopted VEPs are more likely to continue participation over time.

Firms subject to environmental regulatory pressures are more likely to adopt a relevant VEP (Guenther et al., 2016; Reid & Toffel, 2009). VEP adoption may help forestall future regulation (A. A. King & Lenox, 2000; Lenox, 2006) or to improve government relations under existing regulations (Hong et al., 2019; Potoski & Prakash, 2005). Where regulatory pressures induce VEP adoption, ongoing regulation will drive continued participation (Seok et al., 2021). Stakeholder management concerns often drive adoption of environmental practices (Vilchez et al., 2017), as influential stakeholders may hold the power to sanction the firm if not in conformance with norms and expectations (Delmas & Toffel, 2008; Lyon & Maxwell, 2011). A firm’s primary stakeholders, notably shareholders, arguably hold greater influence over firm activities. Customers also hold substantial power to drive firms toward implementing programs and initiatives to improve environmental performance and management (A. A. King et al., 2005); employees also have a substantial role in influencing firm policies (Delmas & Pekovic, 2018; Potoski & Callery, 2018). Firm attention to those groups is associated with VEP adoption (Guenther et al., 2016) where interests are aligned. Absent major shifts in stakeholder salience, that attention is also likely to drive continued participation.

Firm-Specific Factors

Firms with superior financial performance are generally able to devote greater resources to addressing environmental concerns (Endrikat et al., 2014). Moreover, firms with governance structures more accommodating to environmental management have greater capacity for participation (Jaggi et al., 2018). Whereas VEP largely seek to improve corporate environmental performance, firms are more likely to self-select into VEPs where doing so provides an opportunity to showcase superior environmental performance to key stakeholders (Prakash & Potoski, 2012). Where new environmental programs represent a radical departure from a firm’s capabilities, firms are less likely to adopt (Dowell & Muthulingam, 2017). Conversely, firms with prior VEP experience are more likely to adopt a new VEP with similar objectives (Tashman et al., 2021).

Meanwhile, when environmental performance is perceived as inferior to stakeholder expectations, firms commonly engage in impression management at the expense of information clarity (Fabrizio & Kim, 2019). Firms that are selectively transparent—that is, selectively disclose good news while withholding bad news (Lyon & Maxwell, 2011)—seek to maintain greater discretion over information disclosure practices. As a VEP increases in relevance over time, heightened stakeholder awareness may affect the ability of selectively transparent firms to consistently manage external perceptions over multiple channels of disclosure (Marquis et al., 2016). Thus, firms that engage in selective transparency in related programs are less likely to continue VEP participation.

Consequential Antecedents

In contrast to the hypothesized temporal consistency of institutional and firm-specific antecedents of adoption, consequential antecedents of continued participation—for example, those drawing from the ongoing interaction between a firm’s resources and capabilities, values, or competitive strategy and the VEP’s goals and guidelines—tend to develop over time and are more likely to be transformed through a company’s direct experience associated with VEP participation. Firms that engage with a program on a deeper level necessarily develop associated processes and routines that lead to a more entrenched identity or status as a participant. This associative identity with the VEP serves to both drive path dependence of participation inside and influence perceptions of conformance outside firm boundaries. Arguably, a higher level of engagement through these consequential factors effectively serves as an implicit commitment mechanism for the firm to sustain participation over time. I propose three general mechanisms responsible for driving higher firm commitment to continued participation: transparency, effort, and achievement, as described below. Relative absence of these mechanisms, therefore, should lead to a firm’s higher propensity to drop out of a VEP.

Transparency

Within this context, I define a transparent firm as one that openly discloses details of its ongoing participation in a VEP. Transparency thus creates awareness among important stakeholder groups of a firm’s depth of engagement with the VEP. To the extent that such engagement is valued by those stakeholders, providing transparency over its associated activities is thus a signal of a firm’s commitment to the program (Vilchez et al., 2017) and an effective tool for legitimation (Cho & Patten, 2007). Reduction in transparency may signify to influential stakeholders that a firm has something important to hide (Lyon & Maxwell, 2011).

Many VEPs state increased transparency as a specific program objective, and so firm perceptions about the risks associated with transparency may influence the initial adoption decision. However, many VEPs leave transparency decisions to the firm, or alternately offer certifications against open standards that are only known outside the firm if directly publicized (Carlos & Lewis, 2018; Gehman & Grimes, 2017). Firms seeking to maintain dropout from the VEP as a viable future exit option are more likely to seek a lower commitment to continued participation, and corresponding reduced risk to legitimacy, by minimizing stakeholder awareness of VEP activities. Meanwhile, many primary benefits of legitimacy offered to firms through VEP participation—such as enhanced reputation (Cho et al., 2012), reduced stakeholder scrutiny (Marquis et al., 2016), or lower regulatory oversight (Hong et al., 2019)—are likely to be driven by stakeholder awareness, and so transparency decisions are often de rigeur with VEP adoption.

But firms may seek to downplay participation, particularly if initial adoption is highly stakeholder specific (e.g., investor pressure) and firms perceive little value in publicity (Kim & Lyon, 2014). Firms that maintain a private strategy for participating (Baron, 2001) may find costs of disclosure are lower when withholding public access to disclosure decisions (Verrecchia, 1983). Moreover, firms that maintain confidentiality over participation may face lower threat to legitimacy on dropout due to lower visibility and perceived level of commitment. As such, even if firms are subject to coercive pressure by limited stakeholder groups to opaquely adopt a VEP, the lack of public disclosure over participation lends a lower level of commitment to continued participation in the VEP; for example, if issue importance or participation visibility wanes over time (Delmas & Montes-Sancho, 2010). Firms that keep VEP participation proprietary thus have greater flexibility in deciding whether to drop the VEP if costs outweigh benefits in the future.

Effort

Whereas participation in a VEP is often characterized as a binary choice (e.g., Lewis et al., 2014; Reid & Toffel, 2009), I define effort as an application or input of firm resources in support of the VEP. Participating firms put forth a varying degree of contribution to the program, where different VEP types elicit different degrees of effort. Effort may manifest as investment of resources in the institutional design and administration (A. A. King & Lenox, 2000; Prakash & Potoski, 2012), fulfillment of voluntary information requests (Kim & Lyon, 2014), implementation of management standards (A. A. King et al., 2005), or provision of more complete disclosure toward a voluntary transparency standard (Guenther et al., 2016).

One prominent way in which firms make implicit commitment to continued participation is in the development of formal organizational routines and processes in support of delivering on VEP objectives or requirements. Prior literature has brought to light the understanding that organizational routines offer flexibility (Feldman, 2000) yet also constrain firms (Howard-Grenville, 2005). Firms that provide a greater degree of effort toward a VEP are more likely to institutionalize practices associated with participation within the organization, allowing lower marginal costs over time and leading to stronger path dependency of participation. Internally, firms may alternately stabilize or iterate on institutionalized routines (Howard-Grenville, 2005) over organization of effort toward meeting program objectives, but the continual refinement of those routines further establishes specialization of roles and more deeply embeds the functions into organizational evolution (Sydow et al., 2009). Externally, a higher level of effort can effectively signal a firm’s commitment to the VEP and its stated goals to key stakeholders, providing further incentive to continue participation over time. Meanwhile, firms making a lower effort in support of the VEP have demonstrated lower commitment not only to the objectives of the program but also to the dedication of resources toward supporting VEP engagement. For such firms, the perceived costs of dropping out of the program are likely to be substantially lower than for firms with higher effort.

Achievement

Whereas effort refers to firm inputs in support of a VEP, I define achievement as an outcome: a formal assessment of the firm’s accomplishments in accordance with the stated objectives of the VEP. Achievement is often some measure of approval or endorsement by the VEP that the firm has fulfilled its obligations of participation, with corresponding benefits to legitimacy. For example, achievement may be signified by a product certification (Darnall et al., 2017), membership in an exclusive institution (A. A. King & Lenox, 2000), or a formally conferred status (Cho et al., 2012). Other VEPs establish commensurable performance ratings that enable comparison between firms (Fabrizio & Kim, 2019). Overall, varying indicators of VEP achievement serve to enhance firm legitimacy among key stakeholders.

Performance ratings, a commonly used VEP measure of achievement, are the result of third-party evaluative assessment of a firm’s conformance with program goals based on objective and clearly defined standards and are powerful motivators of firm behavior (Rindova et al., 2018). Firms with higher performance ratings have been duly recognized by the VEP as better fulfilling the objectives of the program. Moreover, receiving an endorsement of achievement from a credible VEP will help facilitate transfer of perceived legitimacy among stakeholders to the associated claims of the firm. Prior research has established the importance of the rating itself, more so than the underlying performance, as the primary driver of legitimacy (Lewis & Carlos, 2019; Lyon & Shimshack, 2015). Importantly, the generally positive benefits of association conferred by performance ratings provide incentives for firms to engage in impression management (Bansal & Clelland, 2004; Callery & Perkins, 2020). Firms with lower performance ratings may seek to improve that rating through increased substantive effort, potentially resulting in higher ratings (Chatterji & Toffel, 2010); however, firms may also pursue symbolic ways to enhance performance rating with minimal cost (Fabrizio & Kim, 2019). On the other hand, firms with low achievement may find that continued program engagement carries heightened risk of stakeholder scrutiny should lower performance ratings persist (Lewis & Carlos, 2019). All else equal, firms with lower achievement may find less impetus to continue to engage with the VEP over time.

Method

Data

To test these hypotheses, I analyze corporate adoption of and dropout from CDP. CDP is an information disclosure program, initiated in 2002 by a not-for-profit organization and with the backing of a substantial cadre of institutional investors, that seeks to influence corporations to make voluntary disclosure of strategy, management, and performance related to greenhouse gas (GHG) emissions and climate change risks. CDP neatly fits the three criteria of this study’s VEP definition: (1) CDP issues firms an annual disclosure questionnaire that represents the standard to which firms may voluntarily conform; (2) firms must develop formal corporate policies and strategies associated with the disclosure standards, as well as the data collection and reporting mechanisms supporting disclosure; and (3) CDP recognizes firm achievement against its standards through issuance of proprietary performance ratings.

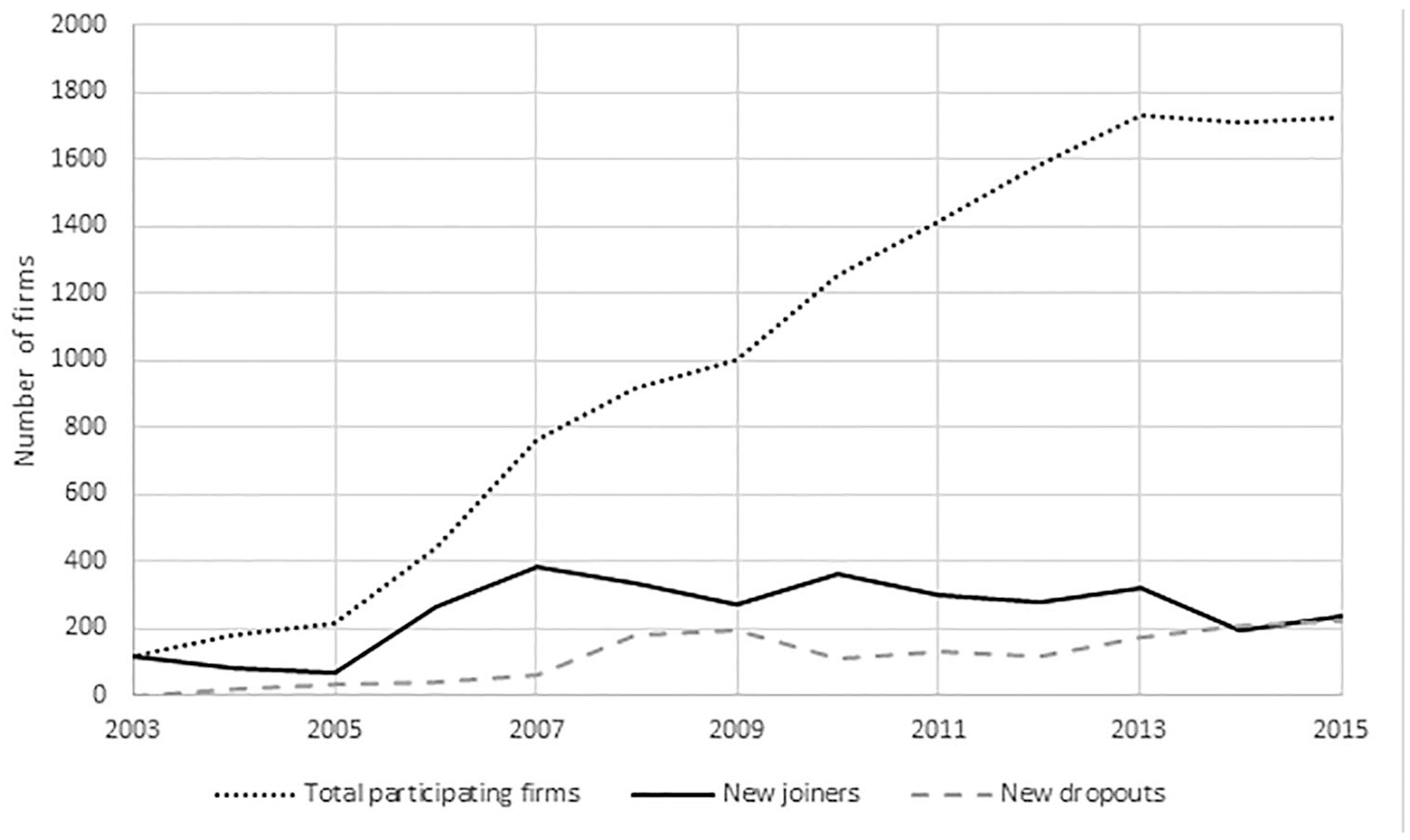

CDP is perhaps the preeminent intermediary in this domain, with a large, global pool of participant firms with varying rates of adoption and dropout. As shown in Figure 1, while the number of participating firms has grown steadily over time, so have the number of dropouts. From CDP disclosure records I assembled a data panel comprising individual firms’ adoption and dropout and other key variables for the years 2003 to 2015. The sample for the study includes 28,305 individual observations for 3,907 global firms; the subsample of firms that have adopted CDP over the course of the study period includes 6,782 observations for 1,648 unique firms. This sample is constructed by firm-year match across data sets used in the study, including CDP, Trucost, ASSET4, the World Bank, Global Reporting Initiative, and Thomson-Reuters Worldscope (described further below).

Firm participation rates in CDP by year, including new joiners and dropouts.

Dependent Variable

The dependent variable for this study represents the decisions of individual firms to “drop out” of the CDP disclosure program. I define the variable dropout as a binary indicator taking the Value 1 in the first year that a firm withdraws from CDP conditional on participation in the prior year. To validate the model (described below) according to prior research on antecedents of VEP adoption, I also define the variable join to represent the initial decision of a firm to adopt the VEP. This binary indicator variable takes the value 1 in the first year that a firm publicly discloses to CDP and 0 in all other years.

Institutional Factors

Institutional factors studied include mimetic isomorphism, regulatory pressure, social movements, stakeholder pressure, and firm visibility. Firm-specific factors include financial performance, environmental performance, and prior experience with related VEPs. Because this study uses multiple measures representing different factors jointly corresponding to Hypotheses 1a and 1b, we are interested in which of these are most relevant within the study context (CDP) and secondarily whether they are jointly significant.

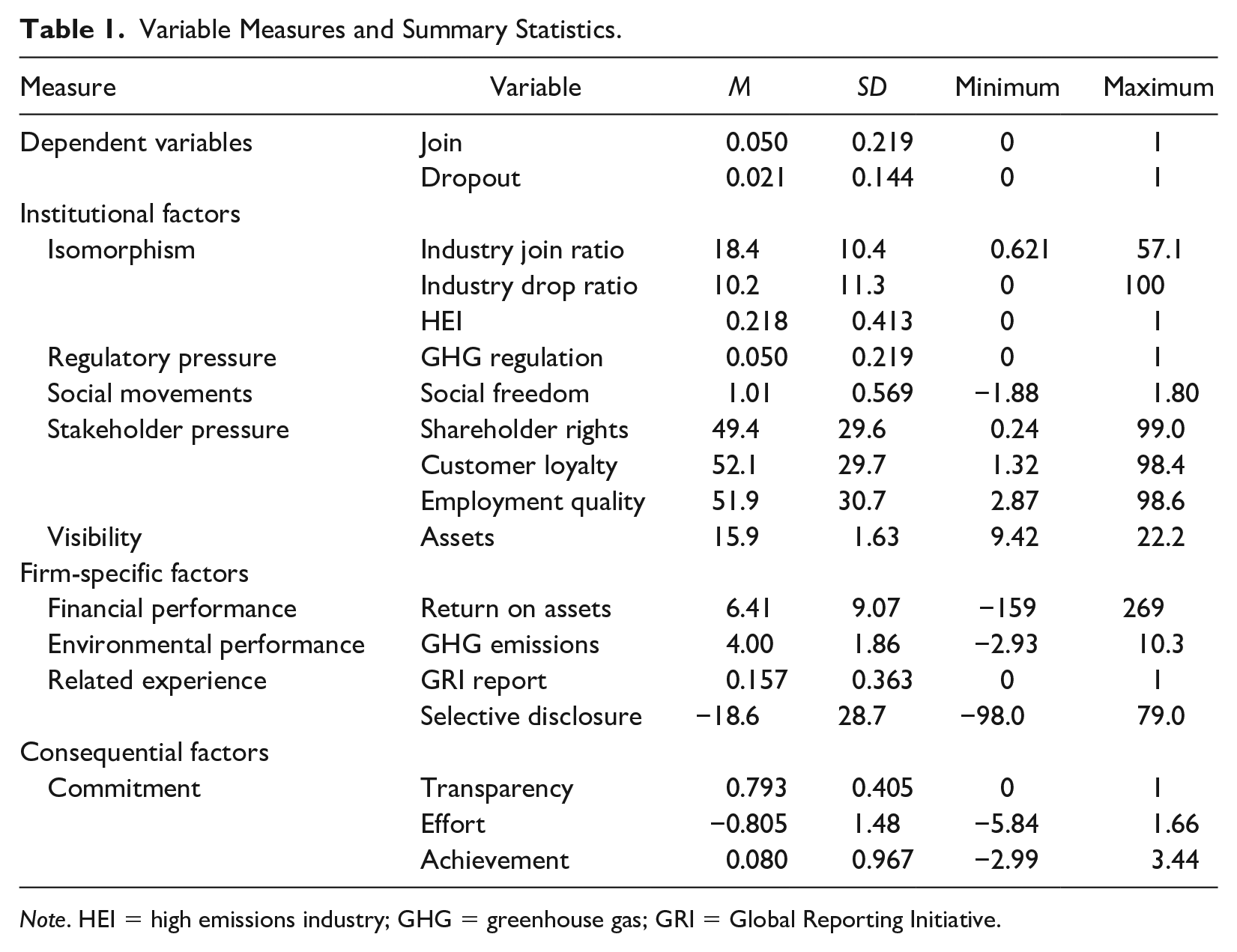

To measure mimetic effects, I compute two variables: industry join ratio is the ratio of CDP adopter firms to total firms within a common industry group in the sample each year, and industry drop ratio is the ratio of dropouts to ongoing participants in each industry. Observations are lagged one year to indicate current year firm response to prior year industry peer adoption. Both measures use Global Industry Classification System industry group (four-digit code). To control for industry effects, I assign the binary indicator variable high emissions industry (HEI) to signify presence in a high-emissions intensity industry, covering firms in the top quartile of industries by GHG emissions intensity (i.e., Scope 1 and 2 emissions per unit revenue): utilities, materials, energy, and transportation. To measure regulatory pressure, GHG regulation, is a binary variable taking the value 1 for firms subject to carbon emissions regulation, 0 otherwise. I use the World Bank’s World Governance Indicators (WGI) data (voice & accountability dimension) for the variable social freedom to measure the degree to which social movements (and by extension, the media and general public stakeholders) in a particular country are allowed freedom of voice and have the ability to hold institutions accountable for actions and impacts. I measure firm orientation to three primary stakeholder groups—shareholders, customers, and employees—using variables from Thomson Reuters ASSET4 data. The three ASSET4 category scores used to measure these factors (on a scale from 0 to 100) are shareholder rights, client loyalty, and employment quality, respectively. I take firm size, measured by the natural log of total assets, as a measure of visibility. All financial data is obtained from Thomson-Reuters Worldscope.

Firm-specific factors

I use return on assets as an accounting measure of financial performance. As a measure of environmental performance relevant to the VEP being studied, I include the natural log of total GHG emissions per unit revenue, using data provided by Trucost. To measure related experience with similar VEP, I assign the indicator variable Global Reporting Initiative (GRI) report with value 1 for observations in which firms submitted a corporate sustainability report in accordance with GRI standards (data obtained from the GRI), 0 otherwise. Finally, I derive the variable selective disclosure from Trucost data, following the method of Marquis et al. (2016). Effectively, the measure describes the relative magnitude of actual environmental impacts to disclosed impacts, where a positive number indicates greater degree of selective disclosure.

Consequential factors

The three hypothesized consequential antecedents—transparency, effort, and achievement—are taken from CDP data. The CDP climate change disclosure questionnaire comprises more than 250 individual questions covering several broad categories of information related to company management of issues related to climate change. Starting in 2010, CDP developed and compiled two separate quantitative scores for each firm based on content of disclosure and overall GHG emissions and climate change management performance. The CDP disclosure score rates firms on overall completeness of information provided over a 0 to 100 integer scale. The variable effort is derived from this score. Active participation in the program requires firms to measure, assess, and monitor information on dozens of performance indicators, develop and implement policy and strategy to manage risks, plan and execute programs and initiatives to address performance, and others. Firms that input a higher level of effort into the various tasks required to complete the questionnaire may attain a higher CDP disclosure score.

Achievement is based on the CDP performance score, a categorical rank score that places firms in one of six performance bands based on CDP’s assessment of overall climate change management, with higher scores awarded to firms demonstrating a greater overall achievement in addressing climate change through disclosed actions, policies, and results. As disclosure and performance scores are highly correlated (ρ = 0.69), to consistently identify the relative contribution of each to a firm’s likelihood of dropout I applied the Gram–Schmidt orthogonalization to the two raw scores. The variable achievement is the orthogonalized value of CDP performance score.

Importantly, CDP allows responding firms the choice to make its disclosure publicly available or keep it private. CDP enables public access to all public responses (on a limited basis or unlimited by paid subscription), whereas a private response is not released to the public (CDP’s institutional investor signatories are granted access to all responses, public and private). I assign the binary indicator variable transparency with value 1 to observations of firms that allow public access to questionnaire responses in the given year, and 0 otherwise.

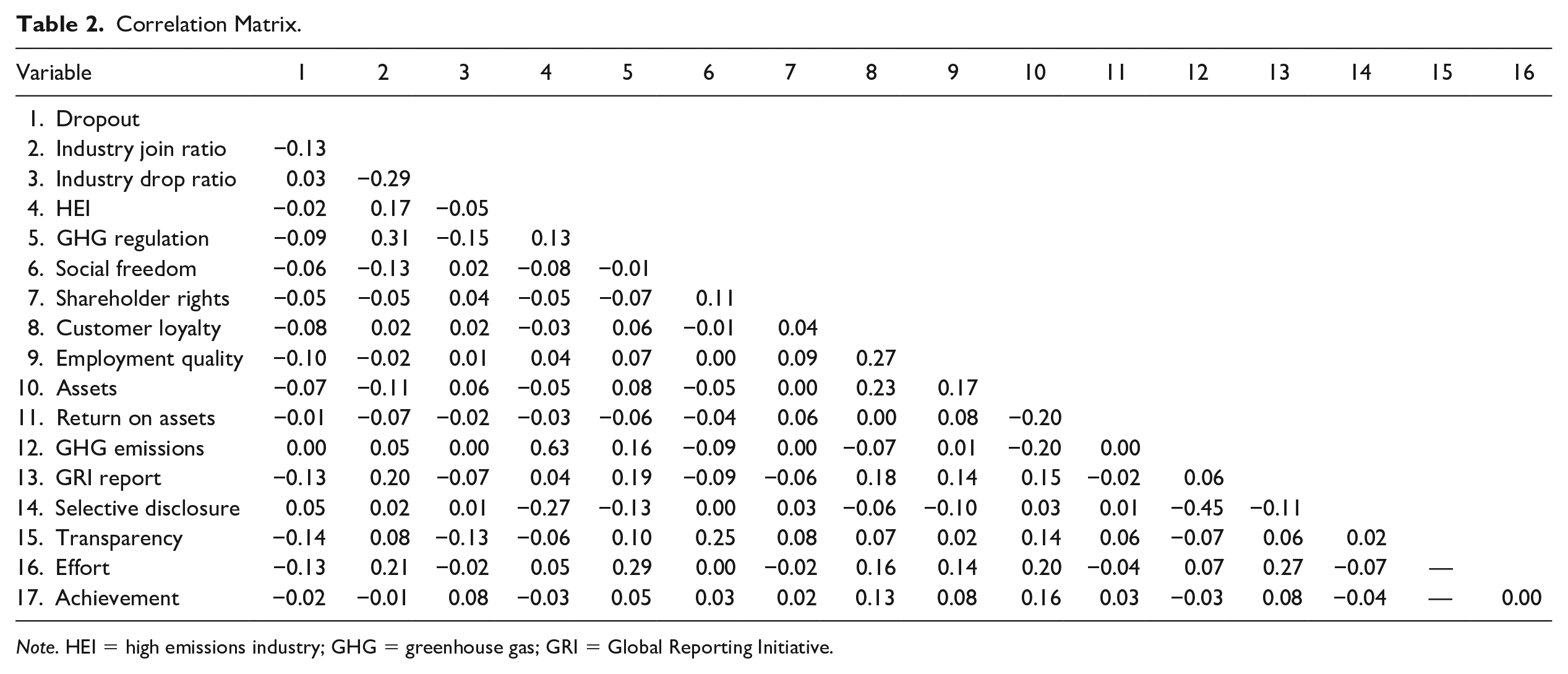

Summary statistics are displayed in Table 1; covariate correlations are displayed in Table 2. In Table 1, note that sample means for indicator variables are based on relevant subsample available. Also note several relatively high correlation coefficients due to largely structural relationships (e.g., GHG emissions with HEI). Mean variance inflation factor (VIF) for a maximal model is 1.25 with no individual VIF greater than 2.10, indicating collinearity is not a concern.

Variable Measures and Summary Statistics.

Note. HEI = high emissions industry; GHG = greenhouse gas; GRI = Global Reporting Initiative.

Correlation Matrix.

Note. HEI = high emissions industry; GHG = greenhouse gas; GRI = Global Reporting Initiative.

Empirical Approach

To analyze effects on dropout, I use survival analysis using Cox proportional hazards regression (Cox, 1972). This method estimates the hazard that an individual experiences an event (e.g., drops out of a VEP) over time, dependent on both time-varying and time-invariant factors. I employ the discrete-time Cox model, as decisions to drop out of CDP are effectively realized on an annual basis and not in continuous time. As noted above, I also estimate effects of traditional antecedents on join to validate the survival model approach in accordance with the findings of prior literature on antecedents of VEP adoption.

Dropout models estimate the hazard of dropping out after initial adoption. Each firm enters the dropout sample in the year it first joins CDP (i.e., staggered entry model); the survival time extends from this entry year to the first year in which the firm drops out of CDP; only the first entry and exit events for each firm are used. All models are right-censored at 2015, the last year in the sample. Firms are unable to “exit” the study, aside from acquisition or dissolution (which are independent of CDP participation decisions), satisfying the independent censoring assumption.

There are two types of unobserved (i.e., missing) data for the key independent variables: a selection and a truncation. First, estimating effects of effort and achievement is potentially subject to selection bias in the current setting: by definition, levels of effort and achievement are only observed for firms that choose transparency. There may be unobserved factors that affect a firm’s choice of transparency that are also related to its levels of effort and achievement. For example, a company may choose to keep its response private if it expects certain stakeholders will react negatively (Lyon & Maxwell, 2011) or otherwise develop unreasonable expectations for future firm performance (Carlos & Lewis, 2018). Second, for some observations of transparent firms we observe effort but not achievement. CDP does not compute a performance score for firms with effort below a specified threshold (i.e., CDP disclosure score less than 50). Omitting these firms from the sample will bias estimated achievement effects, considering high correlation between raw CDP disclosure and performance scores noted above.

Selection Effects

Regarding the selection concern, a complete case analysis (CCA) approach (listwise dropping of observations with missing data) is appropriate. Whereas researchers commonly specify (and misspecify) Heckman’s selection correction model for such cases, the Heckman model is prescribed only where selection leads to unobserved instances of the dependent variable (Certo et al., 2016). In the study sample, the dependent variable (dropout) is observed in all cases, whereas the independent variables of interest (effort and achievement) are not observed when firms do not select transparency. MI methods are commonly used to address such missing variables; however, given the selection concern, the unobserved effort and achievement for nontransparent firms is clearly “missing not at random” (MNAR), for which MI methods are less appropriate. Where an MNAR mechanism depends on the outcome, CCA yields biased estimates (White & Carlin, 2010). However, insofar as the MNAR mechanism is dependent only on the missing data and other covariates, CCA may produce unbiased estimates (Hughes et al., 2019). Noting that MNAR mechanism (i.e., nontransparent firms) is logically dependent on the missing values of effort and achievement (firms may choose nontransparency to either restrict disclosure of low ratings or prevent elevated stakeholder expectations from high ratings) but arguably not dependent on the outcome of interest (dropout), I take a CCA approach to estimate effort and achievement effects for transparent firms.

Missing Data and Multiple Imputation

Because one can empirically observe the correlation between effort and achievement, the second type of missing data (unobserved achievement due to low effort) is more likely to bias estimates in a CCA approach. To properly address the MNAR mechanism, I combine MI with a Heckman selection model as in Galimard et al. (2016). The first stage estimates a probit model on the missingness mechanism (achievement not observed for transparent firms); in the second stage I employ MI by chained equations (MICE) using panel data techniques to impute missing values of achievement. I then use multiple imputed data sets to estimate the baseline survival model, using Rubin’s rules (Rubin, 2004) to aggregate coefficients and standard errors. Note that this MI approach is applied only to the missing achievement data on firms with low effort.

Results

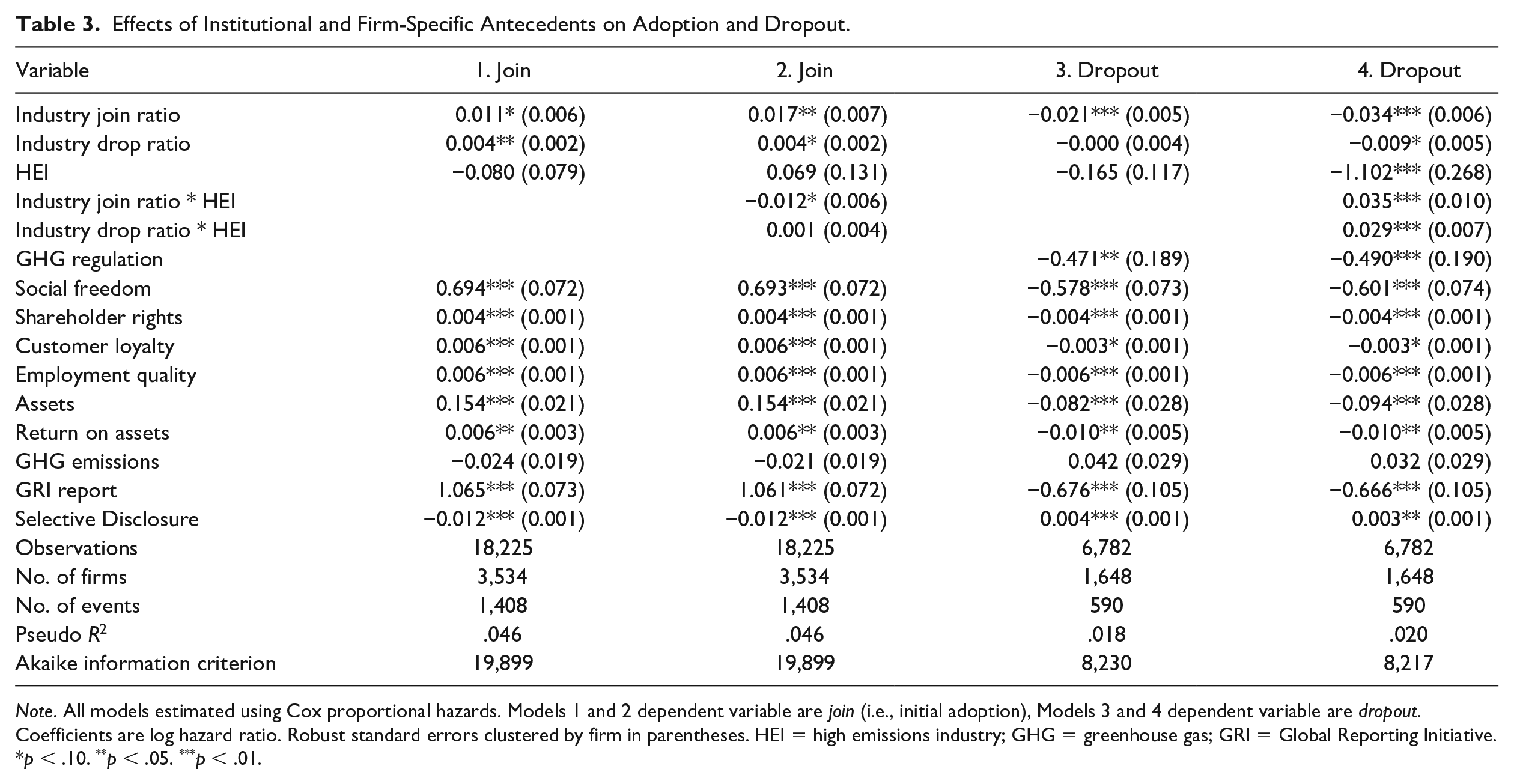

Table 3 presents results from Cox proportional hazards survival analysis of institutional and firm-specific factors that alternately explain the propensity to join and drop out of the VEP. The coefficients are parameter estimates (i.e., natural log of hazard ratio), such that positive, significant coefficients represent factors associated with increased propensity to join or drop out, respectively. A Schoenfeld residuals test indicates the proportional hazards assumption is valid for all models. I also test independence of survival times (dropout) by industry identifiers, which yields a nonsignificant result (p = .17), indicating the independent observations assumption is valid. Note the survival analysis omits all firm-year observations that occur after the corresponding event (i.e., join for Models 1 to 2 and dropout for Models 3 to 4), as indicated by the number of firms and observations Table 3.

Effects of Institutional and Firm-Specific Antecedents on Adoption and Dropout.

Note. All models estimated using Cox proportional hazards. Models 1 and 2 dependent variable are join (i.e., initial adoption), Models 3 and 4 dependent variable are dropout. Coefficients are log hazard ratio. Robust standard errors clustered by firm in parentheses. HEI = high emissions industry; GHG = greenhouse gas; GRI = Global Reporting Initiative.

p < .10. **p < .05. ***p < .01.

Results demonstrate support for Hypotheses 1a and 1b. Institutional antecedents—mimetic effects (industry join ratio), social freedom, stakeholder orientation (shareholder rights, customer loyalty, and employment quality), and visibility (assets)—are all negatively associated with dropout. Firm-specific antecedents—financial performance (return on assets) and related experience (GRI Report and the negative complement of selective disclosure)—are likewise. Wald tests of joint significance on both sets of factors rejects the null hypotheses that coefficients are equal to zero (p < .001). Note that relevant environmental performance (GHG emissions) is not significantly associated with either. In terms of effect sizes, for example, the coefficients on industry join ratio suggest a 10% increase in proportion of industry peers joining CDP, all else equal, corresponds to a 12% greater hazard of initial adoption (Model 1) and a 19% lower hazard of dropout (Model 3), conditional on having previously adopted. Meanwhile, firms that have previously published a GRI-conforming sustainability report are nearly three times more likely to adopt CDP (Model 1) and are 49% less likely to drop out of CDP once joined, all else equal. Also note, with minor exceptions, the magnitude of dropout effects is dampened relative to adoption effects, suggesting the presence of additional (i.e., consequential) factors explaining dropout.

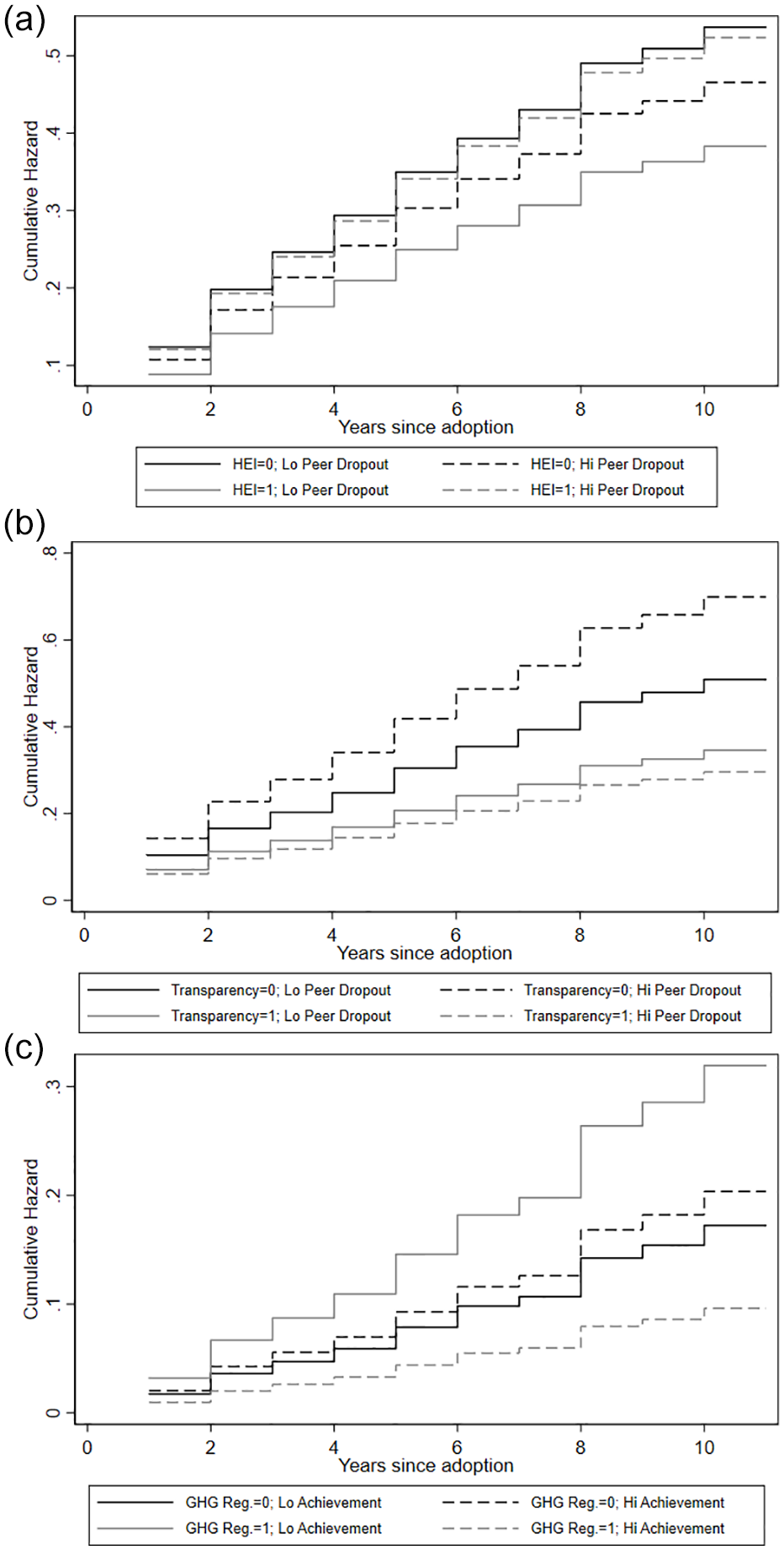

To estimate industry effects, Models 2 and 4 include interaction terms between HEI and mimetic factors industry join ratio and industry drop ratio. In Model 2, the negative interaction term coefficient indicates that mimetic effects of adoption are not significant in emissions-intensive industries (suggesting that other institutional and firm-specific factors predominate in those industries), and mimetic effects of dropout are small and independent of industry. The former effect is roughly replicated in Model 4 (dropout). However, the interaction-combined coefficient for industry drop ratio is positive and significant (calculated β = .020, p < .001), indicating that the mimetic dropout effect is much larger in emissions-intensive industries. Figure 2a displays a cumulative hazard plot to better illustrate the HEI moderating effect of this “negative” mimetic pressure on hazard rate of dropout. Gray lines correspond to HEI firms, black lines to other industries. Solid lines correspond to low dropout rates (one standard deviation [SD] below the mean), dashed lines to high dropout (+1 SD). Here the significant reduction in hazard rate for HEI firms with lower industry peer dropout, with no industry effect under high peer dropout.

Cumulative hazard plots show interaction effects on dropout of key predictor variables moderated by other antecedents: (a) effect of industry dropout rate on focal firm dropout hazard positively moderated by presence in emissions-intensive industry; (b) effect of industry dropout rate on focal firm dropout hazard positively moderated by firm transparency; (c) effect of achievement on dropout hazard unique to regulated firms.

Consequential Antecedents

Table 4 displays results from survival analyses of consequential factors. Model 1 shows significant negative effects of transparency on dropout, providing support for Hypothesis 2. Per Model 1 results, the coefficient of −0.642 (p < .001) corresponds to a hazard ratio of 0.53, suggesting that transparent firms, all else equal, have a 47% lower dropout hazard than nontransparent firms, and industry mimetic effects are not significant. In consideration of the industry effects noted above (Table 3), I also add interaction terms between transparency and industry join and drop ratios here (Model 2). Results are striking: the transparency effect is not significant for industries with low dropout rates, while the transparency effect is significant for industries with high dropout. Figure 2b displays cumulative hazards for this moderating effect; note the negligible difference in cumulative hazard for transparent firms from low to high industry dropout (−1 to +1 SD), and the significantly lower overall hazard for transparent firms. This result adds nuance to the support for Hypothesis 2: transparency serves as an important commitment device primarily for firms subject to higher mimetic pressures to dropout.

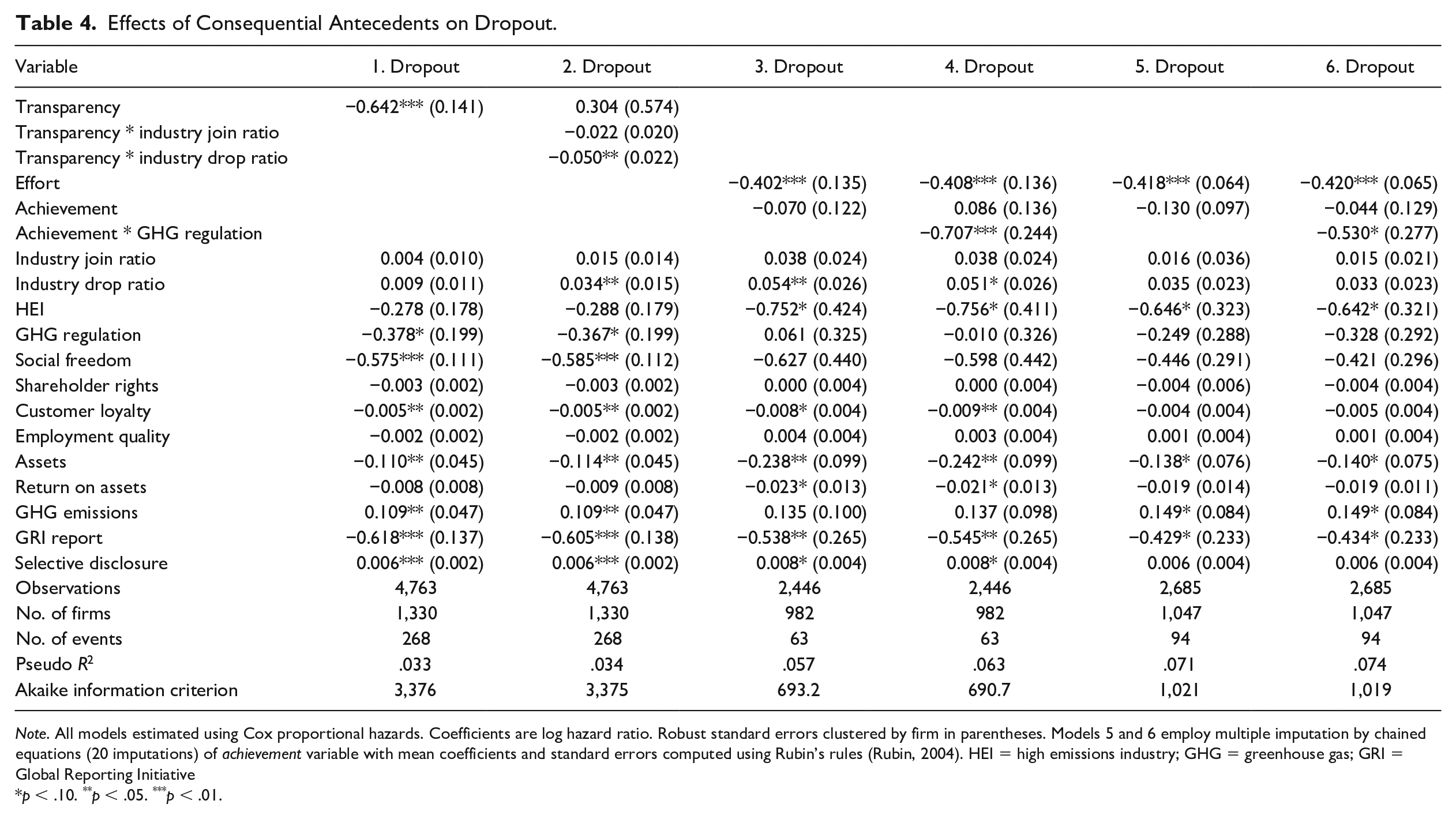

Effects of Consequential Antecedents on Dropout.

Note. All models estimated using Cox proportional hazards. Coefficients are log hazard ratio. Robust standard errors clustered by firm in parentheses. Models 5 and 6 employ multiple imputation by chained equations (20 imputations) of achievement variable with mean coefficients and standard errors computed using Rubin’s rules (Rubin, 2004). HEI = high emissions industry; GHG = greenhouse gas; GRI = Global Reporting Initiative

p < .10. **p < .05. ***p < .01.

Model 3 displays results for effort and achievement, conditional on transparency. Results indicate a significant negative effect of effort on hazard of dropout, providing support for Hypothesis 3. The coefficient of −0.402 (p = .003) corresponds to a hazard ratio of 0.67, indicating that a 1 SD increase in effort (approximately 13 points on the CDP disclosure score scale), all else equal, is associated with a 33% lower dropout hazard. Meanwhile, there is no significant effect of achievement on dropout hazard, failing to provide support for Hypothesis 4. Recognizing that GHG emissions performance is of material importance to firms subject to carbon emissions pricing regulations, I interacted achievement with GHG regulation. Model 4 results show that higher achievement firms subject to carbon pricing regulation are significantly less likely to drop out, whereas there is no such achievement effect for unregulated firms. The coefficient of −0.707 indicates that for a given level achievement, regulated firms have roughly 50% lower dropout hazard than nonregulated firms, all else equal. This relationship is illustrated in Figure 2c; note the substantial drop in hazard rate for high achievement, regulated firms relative to low achievement, regulated firms (dashed and solid gray lines).

Models 5 and 6 (Table 4) display the results of MI analysis using 20 imputations of a MICE algorithm applied to the panel data structure. Coefficients on effort are more negative, suggesting the CCA method may bias the results toward zero (null), while the interaction coefficient on achievement is slightly less negative and still significant. Perhaps more interesting, coefficients on many of the traditional antecedents are smaller in magnitude, indicating that the consequential factors analyzed here are of primary relevance in explaining propensity for dropout.

Discussion and Conclusion

The following discussion first examines how the core empirical findings of this study support theory articulated above on consequential antecedents of continued participation as sources of implicit firm commitment to VEPs, then highlights the implications for both management theory (namely, legitimacy theory and the growing literature on carbon disclosure) and practice (from perspectives of both firm strategy and sustainability of voluntary institutions). I add commentary on generalizability of findings and study limitations, as well as outline opportunities for future research on the subject of VEP dropout.

Baseline results show that traditional antecedents associated with VEP adoption (joining) are also strongly associated with continued participation, largely consistent with the cumulative findings of the VEP adoption literature (Tashman et al., 2021). Industry moderating effects are more illuminating. Industry peer adoption rates intuitively had a significant, positive effect on both initial adoption and continued participation for some industries, but that effect was not significant for firms in emissions-intensive industries. This moderating effect may indicate that VEP adoption is a more powerful driver of legitimacy than mimetic effects in environmentally sensitive industries. Moreover, it is surprising that while higher peer dropout is positively associated with focal firm dropout in emissions-intensive industries, that effect was reversed in other industries. This suggests that VEP participation is a stronger driver of legitimacy in sectors where VEP goals are more material, while the relationship of participation to legitimacy in low impact industries is less instrumental; this offers an interesting avenue of future research. Finally, note that the smaller effect sizes on dropout (relative to join) suggest the influence of other, consequential factors, which comprise the core contributions of the study as discussed below.

The analysis of consequential factors highlights the important role of transparency and effort in continued participation. Transparency can serve as a powerful commitment device by creating an expectation among stakeholders for continued transparency, threatening legitimacy for transparent firms that drop out. More precisely, transparency appears to offset susceptibility to mimetic effects in industries with higher dropout rates; results as illustrated in Figure 2b demonstrate this notion. A VEP may consider efforts to promote transparency by its participant firms as another tool to enhance the long-term viability of the program through encouraging continued participation. Moreover, by controlling for institutional and firm-specific factors we find that social pressures and firm visibility (among others) remain significant predictors of continued participation (see Table 4), suggesting heterogeneity among stakeholder groups in attributions of legitimacy. Post hoc analysis (results not shown) indicates social freedom and visibility effects are positively moderated by transparency, further suggesting the capacity of transparency as a commitment device to maintain public trust. Developing a deeper understanding of how different stakeholder groups respond to changes in different aspects of transparency offers a fruitful line of future research. Findings also indicate that greater effort is associated with substantially lower dropout hazard. Moreover, controlling for effort (Table 4, Models 3-6) yields multiple institutional and firm-specific factors not significant, yet slightly magnifies the dropout hazard associated with lower visibility and higher selective disclosure. Overall, these findings signify the nature of a firm’s commitment to visible and procedural actions, supporting the notion that sustainability practices are predominantly oriented toward maintaining legitimacy (Schaltegger & Hörisch, 2017).

However, findings suggest that while higher achievement may promote continued participation by regulated firms, achievement (i.e., performance rating in the study context) is largely irrelevant for unregulated firms. This is surprising both because firm environmental performance tends to be associated with financial performance (Endrikat et al., 2014; Flammer, 2013) and because higher achieving firms may leverage CDP’s positive assessment to enhance legitimacy with influential stakeholders. In the current context, a firm’s identity as a VEP participant may be a more powerful signal of commitment to the VEP and its objectives than the actual perceived level of performance or achievement. In other VEP contexts, both transparency and achievement may be highly subjective (Aragón-Correa et al., 2016). Prior research suggests some stakeholder groups gravitate toward simple, summary metrics, and disregard the nuanced details of underlying information (Lyon & Shimshack, 2015). Moreover, mere visibility of achievement may weigh more heavily in external perceptions than the level of achievement itself (Lewis & Carlos, 2019). Aggregate measures of firm achievement may be manipulated through linguistic obfuscation (Fabrizio & Kim, 2019) or false accounts (Callery & Perkins, 2020). Recent research has also questioned whether certain assessments carry any significance at all for a range of stakeholder groups (Silva et al., 2019). Future research may examine more closely how different stakeholders filter, interpret, and act on information provided by firms.

Taken together, these findings offer important implications for VEPs in the context of legitimacy theory. Perceived stakeholder value in transparency and effort are indicative of a pragmatic legitimacy, wherein a firm attends to the self-interest of its audience (Suchman, 1995); whereas a lack of perceived value in a higher recognition of achievement contradicts the notion of moral legitimacy, wherein firms are judged on accomplishments (Suchman, 1995). Moreover, the institutional drivers traditionally associated with legitimacy (Bansal & Roth, 2000) are largely attenuated by consequential factors—transparency and effort are key vehicles by which firms seek legitimacy through VEP participation (Qian & Schaltegger, 2017), and by this study’s findings differentially subsume the original institutional drivers, while firm-specific drivers are still present and in some cases amplified (see Table 4). This suggests that once a firm has joined a VEP, the nature of its participation may drive its legitimacy calculus, though perhaps still through a pragmatic focus. Recent research highlighting the tension between pragmatic and moral legitimacy in VEP research (Bowen, 2019) argues that moral legitimacy has not been sufficiently studied. Where moral legitimacy is addressed, prior literature has tended to focus more on normative assessments of moral legitimacy (Boiral, 2007, 2013) than on firms’ perceptions of legitimacy from an audience perspective. These findings suggest a more nuanced view that firms may perceive respective audiences as more responsive to appeals for pragmatic legitimacy than moral legitimacy, an interpretation arguably consistent with the view that some VEPs are challenged to effectively convey a moral legitimacy through induced firm disclosure (Wijen, 2014). Analyzing audience responses to various aspects of perceived firm commitment to VEPs represents a compelling opportunity for future research.

The tensions noted above are also relevant within the specific context of voluntary carbon disclosure as addressed in this study. Given the heightened attention to this phenomenon in recent years (Hahn et al., 2015; Qian & Schaltegger, 2017; Velte et al., 2020), I highlight this study’s contributions to this growing literature. A primary focus of the carbon disclosure literature is on the relationship between disclosure and performance; this study addresses perceived performance (i.e., recognition of achievement) as measured by a rating scheme rather than realized performance (i.e., carbon emissions reductions). Findings indicate that firms (notably in non-emissions intensive industries) are more attentive to external perceptions of transparency and effort than that of achievement, suggesting a relationship between participatory effort and realized performance. While recent research has elucidated the contingencies of the relationship between carbon disclosure and emissions performance (Bui et al., 2020; Dahlmann et al., 2019), the study’s findings point to the need for future research to address the effectiveness of programs contingent on varying participation. Improving our understanding here may lead to further advancements in identifying best practices for VEP effectiveness in the field of carbon disclosure.

The study also contribute to literature on VEPs more generally, with emphasis on implications for program longevity. I identify key factors representing implicit commitment that determine whether a firm remains engaged with a program over time. The nature of these commitments has important implications for our understanding of how firms use transparency and effort in VEPs to improve private outcomes (Fabrizio & Kim, 2019; Marquis et al., 2016), as well as the longevity of VEPs that seek to generate outcomes that benefit both participant firms and broader society (Etzion & Ferraro, 2010; Lenox, 2006). Etzion and Ferraro (2010) employed an institutional entrepreneurship lens to discuss the capability of VEPs to switch identifying frames to promote distinctiveness once the VEP is firmly established among stakeholders. This theory suggests a path for VEPs to be perceived as “indispensable” once established; the concept of firm commitment supports this notion. Emergence of alternate programs in such stakeholder-critical domains (e.g., in the case of climate change: government-mandated emissions reporting or alternative frameworks such as SASB, IIRC, or TCFD) may threaten VEP indispensability by shifting firms’ commitments to an alternate intermediary. When a voluntary program can be subverted to mislead (Callery & Perkins, 2020) stakeholders may lose trust in the intermediary, exposing it to substitution by new entrants. Future research can examine firm propensity to shift commitments among competing disclosure vehicles and associated effects on institutional longevity.

Finally, the study highlights important implications for practice from the perspective of both VEP sponsors and participant firms. Collective action among participants is critical to certain VEP forms (such as industry self-regulation, e.g., Bowen, 2019; Lenox, 2006); findings suggest that independent VEPs such as CDP may yet leverage participant incentives beyond basic institutional factors (e.g., mimetic or coercive) by fostering a perceived need to continue participation in the interest of program sustainability. This has important practical implications for VEP design, suggesting that VEPs may incentivize firm transparency and effort to drive continued participation; for example, a common limitation of some VEPs (e.g., ecolabels) is a lack of transparency over required firm effort (Darnall et al., 2017; Prieto-Sandoval et al., 2016). If firms are allowed to join and drop out at will, the flux in participants may hamper VEP credibility and potentially limit effectiveness. Moreover, as the depth and breadth of data available to investors and other stakeholders grows, the relevance of summary performance ratings may be on the decline (Chatterji et al., 2016) as organizations are able to integrate big data into performance monitoring and investment algorithms. For example, both CDP and Trucost offer data products to institutional investors that generate imputed values of emissions performance for nonadopters based on other disclosure channels and proprietary input–output models. Noting also that commensurable performance ratings may promote competitive intensity between participants that encourages decoupling or symbolic disclosure (Luca & Smith, 2015), smaller programs targeting collaborative interactions between participants may reduce competitive positioning (Bowen et al., 2018; van der Heijden, 2020) that may enhance moral legitimacy of firms as perceived by concerned stakeholders. Thus, the ability to formally recognize top performers may offer relatively less utility for stakeholders, suggesting VEPs may focus on more effective commitment mechanisms.

Firms considering VEP adoption may select those expected to maintain relevance. While prior research suggests that increased stringency of VEP standards deters firms from initial adoption, it is associated with higher firm legitimacy (Tashman et al., 2021). While the study does not specifically address stringency, findings suggest firms seeking to provide a distinct signal of quality and prepared to demonstrate effort of participation may choose a VEP with greater institutional credibility. However, stringency may also lead to interest divergence between sponsors and participants (Wijen & Chiroleu-Assouline, 2019), leading to proliferation of standards with varying levels of perceived effectiveness (Schleifer et al., 2019). Firms may better secure legitimacy for VEP participation by selecting VEPs that reward long-term commitment by recognizing substantive effort. Furthermore, while institutional factors may compel firms to reduce decoupling strategies (Marquis et al., 2016), transparency and achievement concerns may lead firms toward greater decoupling (Fabrizio & Kim, 2019; Hahn & Lülfs, 2014). This study adds nuance to these observations by considering the possibility of dropout as an evolutionary disclosure strategy; firms may exit voluntary mechanisms where risk of stakeholder scrutiny becomes too great relative to the risk of stakeholder sanctions over dropout. Surely, stakeholder attendance to firm dropout depends on the perceived credibility of the VEP and the expectations formed around a firm’s continued participation. Building on points made above, examining stakeholder responses to firm dropout in different VEP contexts represents an encouraging area for further research.

Given that the study examines a single VEP (CDP) in a specific domain (climate change information disclosure), there are potential limitations in generalization of findings. For example, transparency is closely associated with achievement for other VEP types wherein the ostensible purpose of firm participation is to attain some formal recognition (e.g., an ecolabel or other certificate of conformance) that can be presented to stakeholders as evidence of performance. In such contexts, achievement is typically a binary outcome, and effort may be ascribed to VEP characteristics (Darnall et al., 2017) but unobservable on a firm-specific basis. The current findings are more relevant to programs where transparency is a stated VEP goal (e.g., other information disclosure programs) or limited stakeholder awareness may be of value to participant firms (e.g., see Carlos & Lewis, 2018; Gehman & Grimes, 2017). Future research may compare the relation of these important VEP mechanisms (stringency of standards and sanctions for nonconformity) and firm dropout across multiple VEPs of a specific type. As comparative studies of VEP stringency have examined the implications for VEP adoption and effectiveness (Tashman et al., 2021), my findings are relatively agnostic to institutional expectations for effort and achievement. Also note that transparency likely carries different significance among stakeholders for different VEP types; to understand the effectiveness of transparency as a signal of legitimacy requires a specific analysis of stakeholder responses, as noted above. Additionally, to limit the scope of this study I take an agnostic view of symbolic versus substantive management (an area that has been studied extensively in prior research), instead focusing on the value of VEP participation for legitimacy. The interaction between dropout and symbolic versus substantive management represents an interesting avenue for future research.

In conclusion, this study addresses a current lack of understanding of factors associated with firm dropout from VEPs. First I theorized, and largely demonstrated empirically, that certain institutional and firm-specific factors of a VEP-firm relationship that are commonly associated with initial adoption are also associated with continued participation. I further theorized a series of consequential, or experience-driven, factors—transparency, effort, and achievement—that are based in implicit firm commitments to continued participation in a VEP. Empirical results indicate that transparency and effort represent powerful firm commitment mechanisms leading to continued participation, while achievement obligates similar commitment only where firms are subject to complementary regulations. The study contributes to legitimacy theory in the VEP context, extend literature on corporate carbon disclosure, and offer implications to enhance the longevity of voluntary institutions and drive substantive participatory effort by firms.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.