Abstract

Do foreign investors have subnational political preferences? The political economy of foreign direct investment (FDI) involves not only choosing among host countries, but also the subnational location of the assets. However, factors affecting investors’ decisions about subnational location likely differ from the ones affecting international investment. This paper studies the effect of state-level partisanship on new FDI inflows to Mexican states. I argue that investors prefer states ruled by left-wing governors because they are more likely to invest in human capital. Statistical analyses using new data on subnational allocation of FDI in Mexican states between 1999 and 2017 support the main hypothesis. Given the persistence of authoritarian enclaves in Mexico, I also disentangle the effects of partisanship from subnational democratization. The partisan effect is independent from party turnover and political competition at the subnational level, and it is robust to different model specifications and estimation strategies. Additional evidence supports the plausibility of the argued mechanism.

Introduction

Do foreign investors have subnational partisan preferences? Foreign direct investment (FDI) has significant economic and political effects for recipient countries, but investment projects especially affect the territorial entities in which they are located (Jensen and Rosas 2007; Owen 2019). This motivates subnational entities to compete with national peers and to enter in international bids for FDI, especially in countries with federal structures of government. There are reasons to believe that explanations for international allocation of FDI may not directly apply to the subnational level, and a growing line of research analyzes the political economy of subnational foreign investment (Jensen et al. 2014; Jensen, Malesky, and Walsh 2015; Lu and Biglaiser 2020; Paul 2002; Samford and Gómez 2014). Yet, we know very little about subnational partisan dynamics that may affect investors’ decisions. This paper tries to bridge this gap by focusing on the influence of state-level partisan politics on FDI.

I argue that in labor-abundant countries that guarantee property rights, investors prefer left-leaning state governors because they are more likely to invest in human capital. In addition, given the close connection between party turnover and democratic features in developing democracies, I also distinguish the effect of partisan preferences from the impact of subnational democratization. I test my argument using the subnational allocation of new FDI among Mexican states, between 1999 and 2017. The evidence indicates that states ruled by the social-democratic Party of the Democratic Revolution (in Spanish, PRD) receive more FDI than states ruled by the centrist Institutional Revolutionary Party (PRI), or by the rightist National Action Party (PAN). This effect is robust and independent from different proxies for subnational democracy, such as party turnover and political competition.

This paper contributes to three literatures. First, it takes a deeper look at the relationships between partisan politics and international capital. In spite of recent research (Camyar 2012; Hwang and Lee 2014; Leblang and Mukherjee 2005; Pinto 2013), some scholarship on capital flows still relies on the assumption that the right is pro-business and pro-capital, and thus, the left should deter investment. The analysis presented here suggests that investors’ partisan preferences may differ for the national and subnational levels because of the kinds of policies enacted at different levels of governance. Thus, investors’ partisan preferences may be more complicated than originally thought.

Second, this article broadens our understanding of the political determinants of FDI. The relative absence of legal barriers to trade and hire across subnational boundaries, and more limited regulatory capacities than the national state, distinguish the political economy of subnational FDI from its international counterpart. These reasons suggest the importance of understanding the subnational dimension of the politics of FDI.

Finally, the paper highlights that state-level politics affect international capital mobility. In doing so, it speaks to the literature on how domestic institutions shape the impact of globalization, and on the interplay of levels of governance.

Lack of comparable data makes cross-country subnational studies challenging. Therefore, I focus on Mexico, one of the largest recipients of FDI among emerging economies (United Nations Conference on Trade and Development 2018). Furthermore, Mexico’s federal structure, its multi-party political landscape, and its uneven process of democratization result in interesting variation across its thirty-two states. In particular, increased political competition in some states permits us to disentangle the effects of partisanship in multi-party contexts, from those of democratic characteristics such as political competition and ruling parties’ turnover.

This paper also introduces some empirical innovations over previous studies. First, paper uses data on new FDI—the initial investment to carry out business transactions—instead of total FDI flows. 1 As I explain below, this is important because different FDI flows likely respond to distinct logics, and react differently to recent economic and political factors. Second, previous studies of Mexico used data that recorded the investment where the main offices of subsidiaries were located, artificially distorting the investment received by Mexico City. I use new data reflecting the actual location of investment, producing a more accurate picture of subnational dynamics of FDI in Mexico.

This paper proceeds as follows: The next section reviews the literature on subnational distribution of FDI, highlighting that factors associated with cross-national FDI do not explain subnational variation, and explaining why this should not be surprising. The theory section explains why subnational partisanship should affect FDI allocation. The section “Empirical analysis” describes the data, and presents statistical analyses that support the argument and show the plausibility of the mechanism. The last section concludes.

What Do We Know about Subnational Location of FDI?

Numerous studies identify a set of factors that explain a substantial part of variation in FDI across countries. The “baseline model” usually includes the country’s market size, development, GDP growth, and indications for political institutions and political instability (Büthe and Milner 2008; Jensen [2006] 2008; Li and Resnick 2003). It is also common to include previous levels of FDI to account for investment decisions’ temporal dependence. Additional variables respond to the research question orienting the study (Beazer and Blake 2018; Biglaiser and Lektzian 2011; Blanton and Blanton 2007; Garriga and Phillips 2014). At the subnational level, however, the factors that systematically affect FDI are less clear.

Studies of developing countries find that robust predictors of cross-national investment do not explain subnational FDI. Furthermore, many of their results are counterintuitive or contradictory among themselves. For example, contrasting with Jordaan (2008), Escobar Gamboa (2013) finds that the most important predictors of subnational FDI are years of schooling and crime. Most variables included in his models are not robust predictors of FDI. This is consistent with Garriga’s (2017) findings. Samford and Gómez’s (2014) results contradict the literature’s expectations (indicators of development and infrastructure are negatively associated with FDI, for example). They find that political competition is negatively associated with investment on some sectors. However, neither government effectiveness nor corruption is associated with subnational investment inflows. 2

These kinds of contradictions are not an exclusive characteristic of studies of developing countries. Comparable studies of the subnational determinants of FDI in the United States also present conflicting findings. State population, a common proxy for market size, is both found to be positively (Kandogan 2012) and negatively (Blonigen et al. 2007) associated with FDI. Similarly, the surrounding states’ market potential is found to deter (Blonigen et al. 2007; Halvorsen and Jakobsen 2013) and attract (Bobonis and Shatz 2007) FDI. Education has positive (Blonigen et al. 2007), negative, or insignificant (McMillan 2013) effect on investment. Unemployment is also associated with more (Kandogan 2012), less (McMillan 2013), and non-significant changes (Halvorsen and Jakobsen 2013) in FDI.

In sum, contrasting with the findings about international allocation of FDI, there is mixed evidence regarding the existence and direction of a relationship between FDI and variables such as subnational market size, development, and growth. Regarding political determinants of subnational FDI, in developing countries, studies of subnational FDI either do not include political variables (Escobar Gamboa 2013; Jordaan 2008), or include them as mere controls (Garriga 2017; Samford and Gómez 2014; Wattanadumrong, Collins, and Snell 2010).

Theory

Why Should Subnational FDI Be Different?

I argue that factors affecting investors’ decisions about subnational location should differ from the ones affecting international investment for several reasons. First, in contrast with the international arena, there are normally no legal barriers to the mobility of goods, labor, or capital across subnational states. Lack of substantial legal or administrative obstacles for trading or hiring across subnational boundaries reduces concerns about local market’s relative size or human capital. 3 Second, trade and capital openness to other countries tends not to differ by geographical location within the country. 4 Two additional differences discussed below derive from the more limited and qualitatively different subnational regulatory capacities vis-à-vis national authorities, and the fact that the ultimate decision over property rights is in the hands of national authorities. These differences condition subnational governments’ ability to compete against peers and may further distinguish the political economy of subnational FDI from its international counterpart.

Does State-Level Partisanship Matter?

Partisanship matters to the extent that it can be associated to policies that affect foreign investment. For example, an extensive literature on the distributional effects of economic policies explains what sectors they are more likely to benefit from them (Frieden 1991) and shows that political parties tend to enact international economic policies that benefit sectors at the core of their constituencies (Bearce 2003; Boix 2000; Garrett 1995), and that partisanship may influence citizens’ preferences for FDI (Pandya 2014). Thus, investors can use the government’s party identification to infer what policies would likely be enacted. In particular, the literature shows that investors associate right-leaning governments with more property rights protection, and with lower risks of expropriation (Weymouth and Broz 2013). Although some expect investors to prefer a right-leaning government because of its inclination to enact free market policies, others predict the opposite effect in certain economic sectors (Pinto 2013).

I argue that the reasons that make partisanship matter at the national level may not apply or work in different directions at the subnational level. First, research suggests that partisanship of the national government may affect—or be perceived to affect—property rights and expropriation (Li and Resnick 2003; Weymouth and Broz 2013), regulation (Pinto 2013; Pinto and Pinto 2008), labor reforms (Murillo 2005), or taxation (Hart 2010). However, decisions on these matters are normally not under the authority subnational governments: even in federal countries in which subnational authorities have important powers, subnational states lack the regulatory or legislative attributions implied in most of the arguments that explain investors’ partisan preferences at the national level. This distinguishes my argument from previous research (Pinto 2013; Pinto and Pinto 2008).

Second, subnational authorities are rarely in position to affect the ultimate protection of property rights. Even if subnational authorities decided to expropriate investment, 5 the final decision on these matters lies ultimately in the hands of federal courts (Biglaiser, Lee, and Staats 2017; Johns and Wellhausen 2016; Staats and Biglaiser 2012). All these reasons make the subnational level substantially different from an international scene characterized by much higher legal market isolation and wider regulatory asymmetries. Thus, the effect of subnational partisanship on foreign investors’ decisions may reflect other kinds of considerations.

The Left Attracts FDI

Pinto and Pinto (2008) study the association between partisanship and sectoral FDI at the national level. Their descriptive data suggest that most economic sectors received more FDI in the United Kingdom and in the United States under the Labor and Democratic Party governments, respectively. Yet, multivariate analyses show that in Organisation for Economic Co-Operation and Development (OECD) countries, partisanship is significantly associated with FDI in only five out of seventeen economic sectors: mining, food, automotive, and financial intermediary industries receive more FDI under left-leaning governments, and the construction sector receives more FDI during right-leaning governments.

Pinto (2013) argues that FDI alters the relative demand of local factors. Because the core constituency of the Left is labor owners, left-leaning governments promote FDI-friendly regulation in sectors that employ their constituencies, and therefore, receive more FDI (Pinto 2013, 61). Both Pinto’s theory and evidence focus on the national level. But, as mentioned, the subnational level exhibits fewer regulatory asymmetries than those observed among countries—even in countries with strong federalist structures (Benton 2009). This is especially true in developing countries with weak institutions, in which the national government tends to centralize decisions. These considerations make a direct application of Pinto’s theory to subnational FDI problematic.

I argue that in labor-abundant countries, investors will prefer left-leaning governments at the subnational level because left-leaning governments are more likely to invest in human capital. This argument builds on an important literature showing that left-leaning governments are more prone to implement redistributive policies that contribute to human capital formation (Havrilesky 1987; Iversen and Soskice 2006), and to spend more on public works (Cusack 1997). Left-leaning governments tend to spend on projects that benefit labor, either because labor owners constitute the core of their constituency, or because they are more likely to compensate for negative effects of international openness (Kaufman and Segura-Ubiergo 2001; Walter 2010). There is also evidence that social spending and human capital development has a positive effect on FDI inflows at the national level (Blanton and Blanton 2007; Garriga 2016; Hecock and Jepsen 2013). Therefore, it is reasonable to expect that subnational partisanship signals to investors the kinds of policies that will be enacted. The expectation of policies—and corresponding spending—that correlate with improving human capital, both in the short term (for example, health investment or spending) and in the long term (for example, investment in education) should attract more FDI, holding other things constant.

From the previous reasoning, I expect a significant effect of partisanship on FDI flows to subnational entities. In particular, I test the following hypothesis:

Hypothesis 1: Left-leaning subnational governments attract more FDI

Support for this hypothesis should rule out two alternative arguments that exist in the literature. First, the idea that states ruled by the right should receive more FDI. Samford and Gómez (2014) stress that the right-leaning PAN became the pro-market alternative to the PRI. They find that states ruled by the PAN receive more FDI than states ruled by the centrist PRI, but no statistical differences between right- and left-ruled states.

Second, this evidence would counter the argument against investors’ subnational partisan preferences. In the United States, Halvorsen and Jakobsen (2013) argue that both Republicans and Democrats enact development policies. The parties differ in their policies’ orientation—investment- and consumption-driven policies, respectively. However, because investors value both sets of policies, multinationals should not prefer one party over the other. Fox (1996) makes a similar argument, but she finds that Democrat-ruled states host more foreign companies. Focusing on the demand side of FDI, Pandya (2010) finds that partisanship does not have a significant effect on Latin American voters’ preferences toward FDI. 6

Empirical Analysis

Dependent Variable

The dependent variable is New FDI, measured as net new FDI received by the state in a given year, as a percentage of its GDP, following the literature on subnational FDI (see Supplemental Appendix 1). 7 FDI refers to the construction of a new factory or the purchase of an existing one in a given state. Mexico records three kinds of flows: New FDI is the initial investment to carry out business transactions; or the purchase of at least 10 percent of the stocks with voting power of existing Mexican companies. Profit reinvestments include earnings not distributed as dividends that increase the foreign investor’s capital. Finally, accounts between companies include all transactions between headquarters and subsidiaries, including loans and payment advances (Secretaría de Economía 2013).

This article focuses on new FDI. I assume that the logic underlying new investment decisions is different from the one driving reinvestment or loans between headquarters and subsidiaries. Reinvestment decisions are more likely to respond to long-term disbursement plans—tend to be more path dependent (Coughlin and Segev 2000; Wren and Jones 2009). The literature suggests that reinvestment decisions are based less on expectations about the host country—that heavily influence new investment—and more on financial performance of the firm, scale of the firm, and other firm-specific factors (e.g., Bercovitz and Mitchell 2007; Cull and Xu 2005). One important idiosyncratic characteristic of reinvestment is the “escalation of commitment” (McCarthy, Schoorman, and Cooper 1993). Both the dependence on the initial decision and escalation bias make reinvestment decisions less correlated with the general political or economic environment than new investment. 8 In contrast, new FDI should be more sensitive to recent economic and political factors than reinvestment decisions. 9

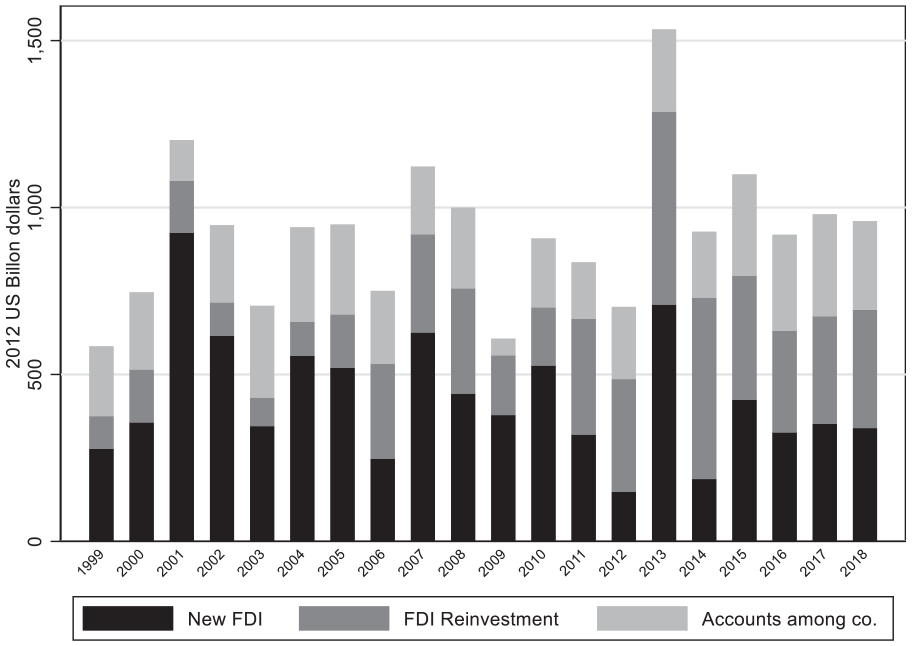

In the past decades, FDI grew dramatically in Mexico as a result of changes in international investment flows, and of domestic reforms. In particular, the 1993 Foreign Investment Law that eliminated restrictions to investment in many economic sectors, the signing of the North American Free Trade Agreement, and increasing confidence in Mexican political institutions spurred FDI. Between 1999 and 2018, Mexico received 920.8 billion dollars in FDI, averaging 46 billion dollars per year. 10 During this period, 46.8 percent of total FDI net flows were new investments; 28.6 percent and 24.6 percent corresponded to reinvestments and accounts between companies, respectively. Mexican data show that the three kinds of FDI flows, and that their contribution to total investment, significantly vary through time (see Figure 1).

FDI net flows, by type.

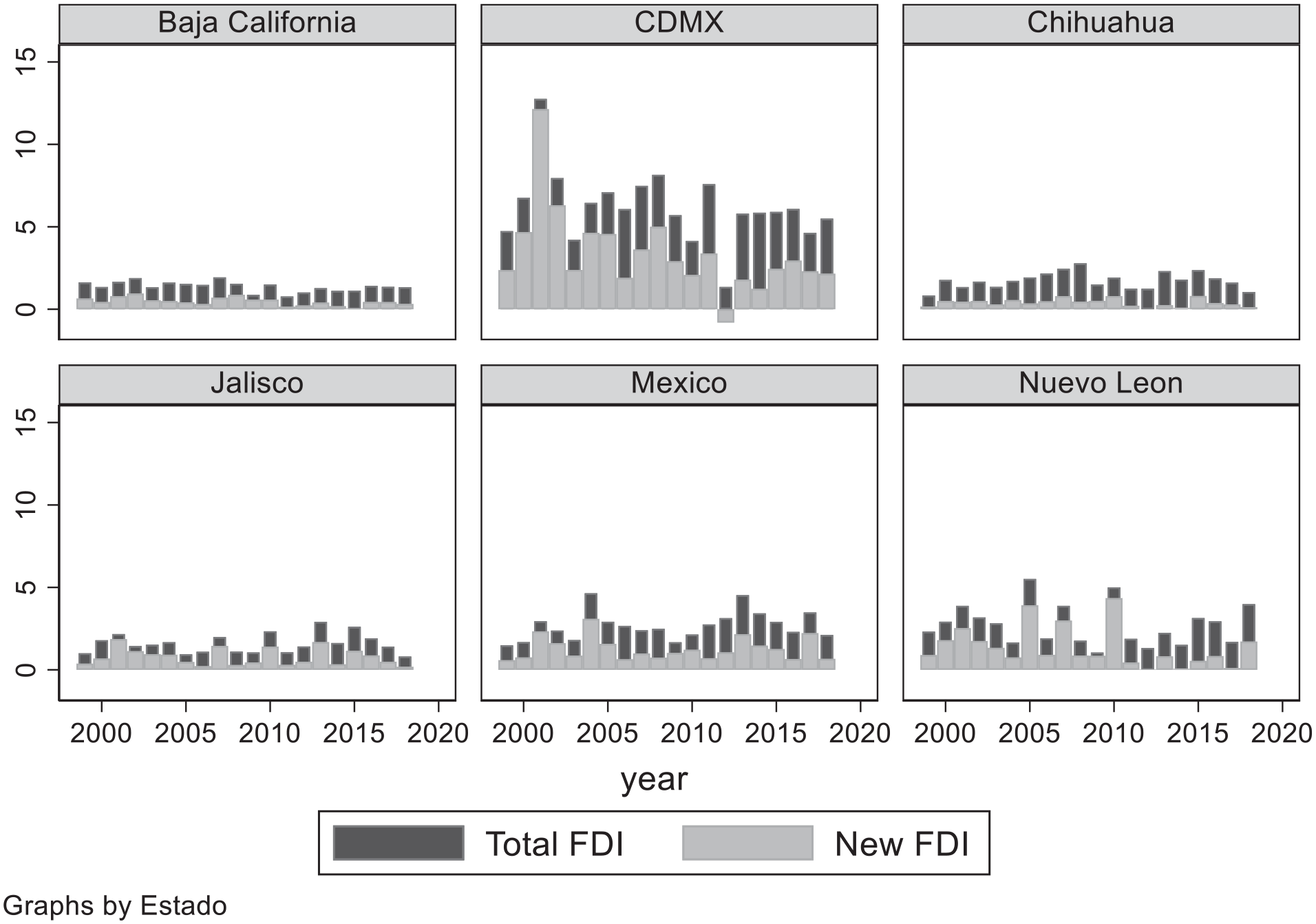

National aggregate data conceal important subnational variation. First, there is great variance in the allocation of investment in the national territory. Between 1999 and 2018, five states received 52 percent of the national FDI inflows (Mexico City, Nuevo Leon, the State of Mexico, Chihuahua, and Jalisco). Second, temporal patterns of FDI also differ across states. For example, although the country received record net FDI in 2013, those flows were not evenly distributed across states. In fact, Mexico City received the largest FDI inflows in 2001, as did Nuevo Leon in 2005 and 2010, the State of Mexico in 2004, and Chihuahua in 2008. This suggests subnational dynamics that differ from national trends. Finally, there is also subnational variation regarding new FDI and other FDI flows. Although at the national level 48 percent FDI flows to Mexico during this period were new investments, the relative importance of new FDI is different across subnational units. As an illustration, most of the FDI Quintana Roo and Nayarit received was new (83% and 77%, respectively), versus 24 percent and 33 percent in Chihuahua and Tamaulipas, respectively. Figure 2 illustrates different temporal dynamics and FDI flows composition in the top recipients of FDI. Supplemental Appendix 3 shows all other states.

FDI net flows.

Until 2014, national statistics attributed FDI to the state where the multinational subsidiary was located, even if the exploitation or actual factory was in a different state. Therefore, previous data wrongly attributed to Mexico City more than half of total FDI (the actual figure is 21% on average). Between 2014 and 2017, the Secretary of Economy corrected the data, and released updated series for 1999 to the present. This paper uses the new data, which may explain contrasting findings with previous literature.

Independent Variables

The main independent variable is the state Governor’s partisan orientation. Mexico has three major political parties, which can be located from left to right in the ideological spectrum: the leftist Party of the Democratic Revolution (PRD), the Institutional Revolutionary Party (PRI), with centrist and populist positions, and the rightist National Action Party (PAN). Except for three observations, 11 all states included in the sample are ruled by one of these three parties alone, or as the major leader of a coalition. Therefore, a set of four dichotomous variables (PRD, PRI, PAN, and Independent) codes whether Governor belongs to either party (or independent), and zero otherwise. Between 1999 and 2017, 16.8 percent of the observations (102 state-year observations in eleven states) 12 were under PRD rule, and 25.2 percent, 57.5 percent, and 0.5 percent were under PAN, PRI, and independent rule, respectively. Alternative specifications include coalitions as a separate independent variable.

The baseline model includes the lagged dependent variable for theoretical reasons: even new investment decisions use information produced from companies in the field, especially if both companies share national origin (Garriga and Phillips 2014; Mody, Sadka, and Razin 2003), and companies observe investment trends as signals of host markets’ promise. I also include Market size, Development, and Growth, measured as the log of states’ population and GDP per capita, and real GDP growth, respectively. Infrastructure is another likely determinant of FDI. However, studies of subnational allocation of FDI disagree on which are the relevant infrastructure indicators and find mixed or counterintuitive results. I include Road density (the length of roads in kilometers, divided by the state’s area) and the existence of commercial ports (Port) as more direct proxies for production and commercialization infrastructure—these variables are insignificant or negatively associated with FDI in other studies (Jordaan 2008; Mollick, Ramos-Duran, and Silva-Ochoa 2006).

Geography is especially important for the Mexican case. First, I include a control for Mexico City (CDMX) because it concentrates 21.6 percent of the FDI the country receives. Second, I control for distance to the United States, the largest market for Mexican exports including the minimum distance to border crossing points, in miles (Jensen and Rosas 2007). Models include a variable absent in previous research, National new FDI. The total flows of new FDI to Mexico allows us to control for domestic and international factors that affected FDI flows to the country and, therefore, may affect the subnational allocation of FDI. Having the same value for all states in the same year, this variable works as an informative “year-fixed effect.” Supplemental Appendix 4 shows data sources and descriptive statistics. 13

I estimate models on a sample of all thirty-two Mexican states between 1999 and 2017. The study begins in 1999, when the Mexican government changed its methodology to register and classify FDI. The last year with official data is 2018, but some economic controls have official data not subject to corrections until 2017. The data are stationary. 14 I estimate general least squares regressions, with correction for AR1 disturbances, 15 and random effects to allow the inclusion of time-invariant variables. Furthermore, Hausman tests suggest that random effects produce consistent estimates (Greene 2011, Chapter 11) (see Supplemental Appendix 5).

Findings

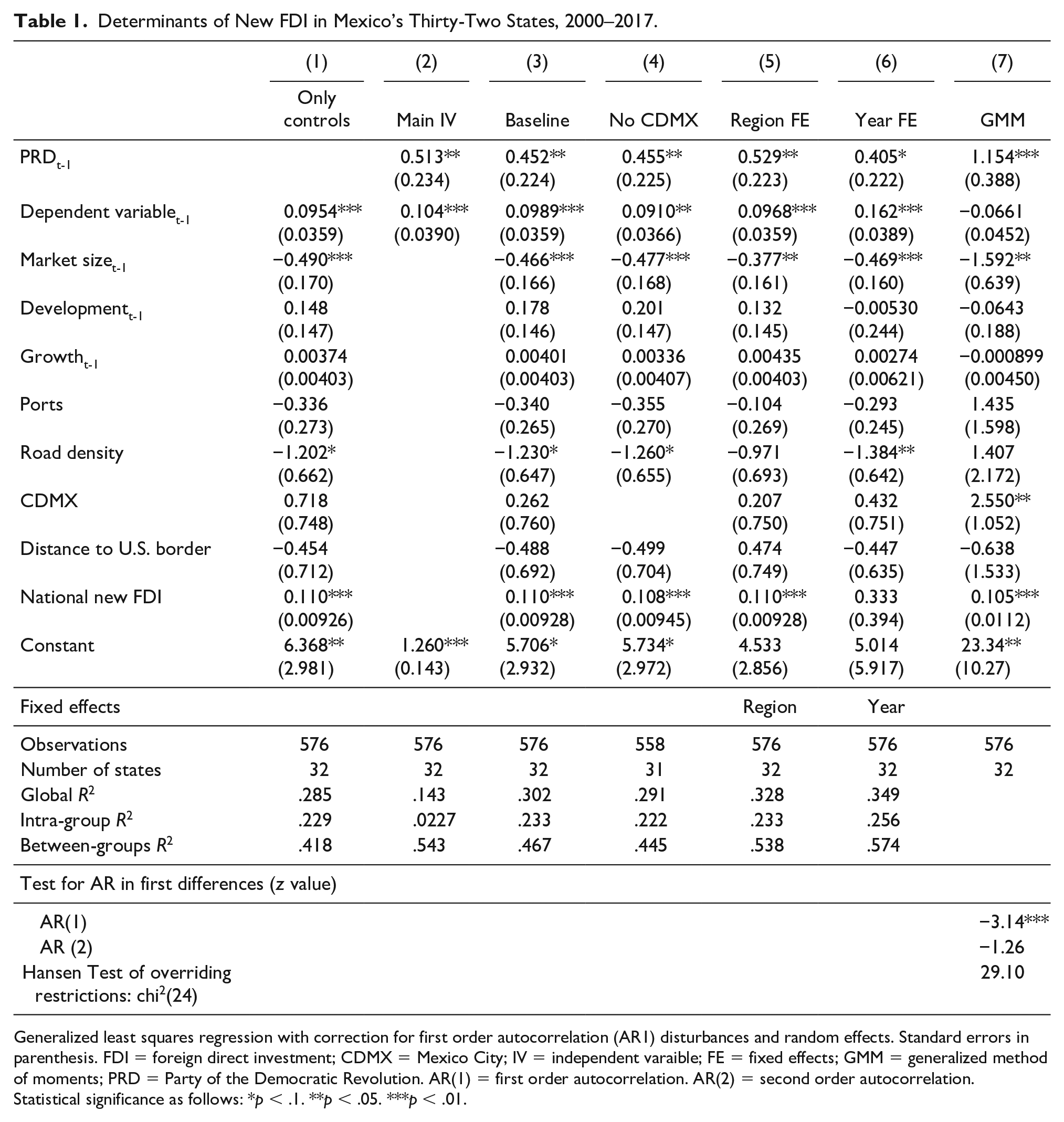

Table 1 presents the regression results. The first column shows the baseline model, without political variables for comparison purposes. Model 2 includes the PRD and lagged dependent variables, and Model 3 includes the other controls. In models 2 and 3, the coefficient associated with PRD is positive and statistically significant, as expected. Among the control variables, previous levels of new FDI and the total amount of FDI Mexico receives in a given year are positively associated with new FDI to a Mexican state. The coefficient associated with the lagged dependent variable is not very large—especially in comparison with the lagged dependent variable in studies of total FDI. This suggests that an informational effect might affect new investment decisions, but that new FDI flows are not largely path dependent. National new FDI is also positively associated with the FDI states receive and is statistically significant.

Determinants of New FDI in Mexico’s Thirty-Two States, 2000–2017.

Generalized least squares regression with correction for first order autocorrelation (AR1) disturbances and random effects. Standard errors in parenthesis. FDI = foreign direct investment; CDMX = Mexico City; IV = independent varaible; FE = fixed effects; GMM = generalized method of moments; PRD = Party of the Democratic Revolution. AR(1) = first order autocorrelation. AR(2) = second order autocorrelation.

Statistical significance as follows: *p < .1. **p < .05. ***p < .01.

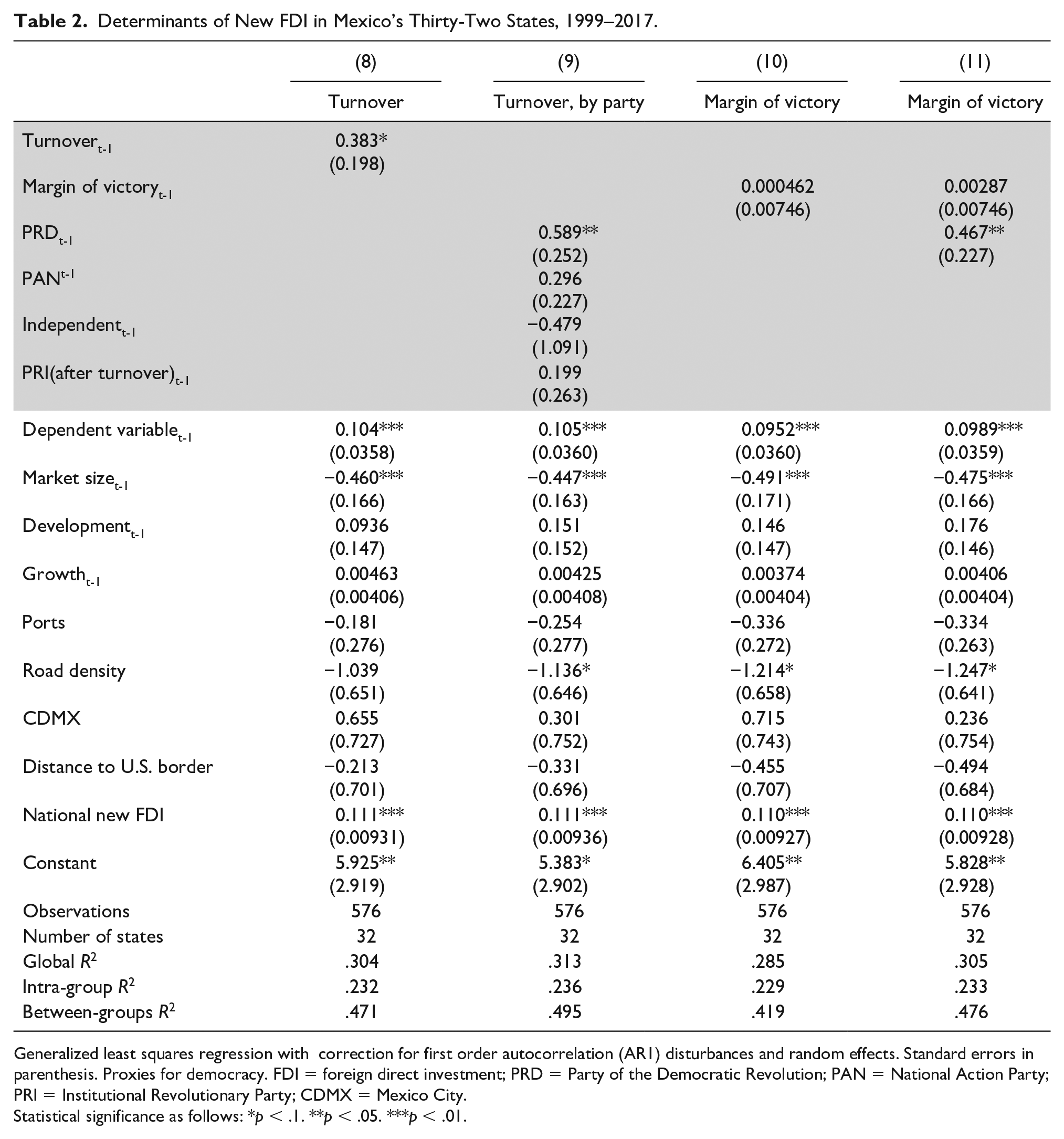

Determinants of New FDI in Mexico’s Thirty-Two States, 1999–2017.

Generalized least squares regression with correction for first order autocorrelation (AR1) disturbances and random effects. Standard errors in parenthesis. Proxies for democracy. FDI = foreign direct investment; PRD = Party of the Democratic Revolution; PAN = National Action Party; PRI = Institutional Revolutionary Party; CDMX = Mexico City.

Statistical significance as follows: *p < .1. **p < .05. ***p < .01.

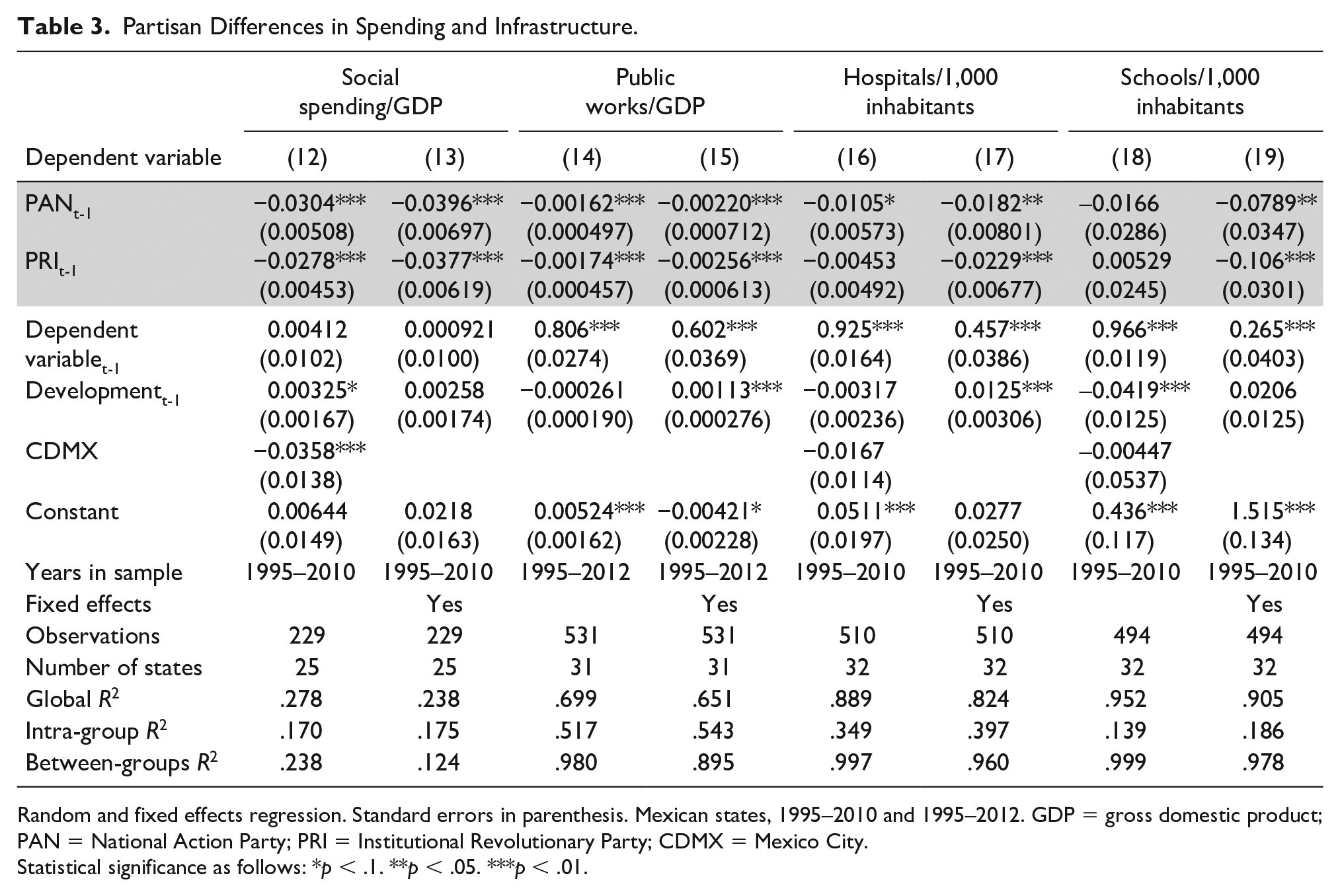

Partisan Differences in Spending and Infrastructure.

Random and fixed effects regression. Standard errors in parenthesis. Mexican states, 1995–2010 and 1995–2012. GDP = gross domestic product; PAN = National Action Party; PRI = Institutional Revolutionary Party; CDMX = Mexico City.

Statistical significance as follows: *p < .1. **p < .05. ***p < .01.

Interestingly, two controls are negatively associated with new FDI. The negative sign of Market size may result from a large volume of investment that does not target consumption in local markets—for example, maquila investment targets foreign markets, and extractive industries do not depend on local consumption. Furthermore, relative absence of barriers to trade across states allows locating domestic oriented companies in less populated states, especially if other considerations—price of land, lower wages, for example—offset transportation costs. The negative sign for Road density, although puzzling, is consistent with previous findings (Jordaan 2008; Mollick, Ramos-Duran, and Silva-Ochoa 2006). Neither Development nor the dynamism of the local economy is significantly associated with higher levels of FDI, a result consistent with other studies (Escobar Gamboa 2013). The lack of significance of Mexico City (CDMX) contrasts with previous studies, which is likely a consequence of the corrected methodology to assign subnational FDI to the states where the production takes place, instead of the headquarters located in Mexico City.

The effect of the PRD variable is sizeable. Holding other things constant, a state ruled by the PRD receives additional new FDI equivalent to 0.45 percent of its GDP. This effect is larger than a standard deviation increase in the lagged dependent variable (0.18%), Market size (0.36%), Road density (0.21%), but smaller than a standard deviation increase in the total new FDI Mexico receives that year (0.64%).

These results are robust to changes in the sample, different model specifications, and estimation techniques. First, an important concern is whether Mexico City, the richest, most populated state, and largest recipient of FDI, ruled by the PRD since 1997, is driving the PRD result. The results hold if I exclude the observations pertaining to Mexico City (model 4). Jackknife estimations show similar results (Supplemental Appendix 6). Second, results are robust to the inclusion of region fixed effects (model 5), and of year fixed effects (model 6, in which the PRD coefficient is smaller, and the statistical significance drops to .055). Results are also robust to the exclusion of the lagged dependent variable, and to the inclusion of controls for violence (homicide rates), international migration (international emigration and net migration; Leblang 2010), election year (t and t-1), corruption, and labor disputes. None of these controls are statistically significant, and the main results hold. I also control for human capital. In these models, years of schooling and PRD are positive and statistically significant. This suggests that PRD is not a proxy for human capital. All these models are in Supplemental Appendix 6.

Model 7 deals with an additional concern: the possibility that PRD rule is endogenous to new FDI. I run a dynamic panel-data estimation (one-step system GMM) using lags 1 to 4 of the independent variables (Arellano and Bond 1991; Arellano and Bover 1995; Blundell and Bond 1998). 16 Hansen tests of overriding restrictions (H0: overidentifying restrictions are valid) and the difference-in-Hansen tests of exogeneity of instrument subsets (H0 = the instruments are endogenous) fail to reject the null hypotheses. Results hold. To further test the possibility of reverse causality, models predicting PRD government suggest that lagged values of new FDI are negative, and generally not significantly associated with PRD (Supplemental Appendix 7). Finally, models instrumenting PRD rule show similar results (Supplemental Appendix 8). In all, these results provide support to hypothesis 1.

The role of coalitions

The Mexican political landscape shows a peculiarity: in the period under study, seven states were ruled at some point by a PRD-PAN (left-right) coalition. In the previous models, I coded these cases according to the partisan affiliation of the governor elected. However, as an additional robustness check, I further disaggregate the data, separating the observations that were under this kind of coalition, and recoding the PRD variable. 17 Models in Supplemental Appendix 9 show that after separating the coalitions from the other cases, states ruled by left-leaning governments still receive more FDI, but the alliance PRD-PAN is not statistically significantly associated with new FDI. Additional models show that there is no statistical significance between PRD-ruled states and those ruled by PAN-PRD coalitions.

The role of state legislatures

I re-estimate the main model replacing the governor’s partisanship with the largest party in the legislature. 18 Results in Supplemental Appendix 10 are consistent with the high correlation between the partisanship of the executive and legislative branches: the coefficient associated with PRD legislatures is positive, statistically significant, and of a larger magnitude than the PRD coefficient in the baseline model. I also explore the effect of the cases in which the governor and the legislature majority belong to different parties. The coefficient associated with a dichotomous variable indicating divided government is negative and marginally significant, suggesting that those cases receive less FDI. The other results hold.

Timing of investment decisions and party turnover

The one-year lag is a conventional way of modeling FDI inflows in the literature. However, it does not map the timeline of the decision-making process of foreign investors to make an initial investment 19 —although it may be realistic regarding the decision to halt previously planned investment. I run additional models with deeper lags of PRD, collapsing the data per period, and including the number of years of PRD rule in the past ten years. In all cases, the coefficient associated with PRD is positive and statistically significant. I also interact PRD (and non-PRD government after PRD rule) with the time in power. The marginal effect of PRD is positive and statistically significant since the third year in power, and increases in magnitude over time. The coefficient for non-PRD after PRD rule is negative and insignificant (see Supplemental Appendix 11).

Other FDI flows

I re-estimate the main model on total FDI and the two other components of FDI (reinvestment and accounts). Because the determinants of these component flows are in theory different from new FDI, and empirically these variables are not highly correlated, it is not surprising that partisanship does not show a significant correlation with reinvestment decisions. The coefficient is significant for total FDI and for accounts (see Supplemental Appendix 12.)

Partisanship or Democracy?

As noted above, most models explaining FDI include institutional variables reflecting the degree of democratization or institutional quality. Democracy is understood as a source of credibility for investors, although evidence at the national level is still mixed (Li, Owen, and Mitchell 2018). In developing countries—especially, in federal systems—some subnational entities might be less democratic than others (Gervasoni 2010; Giraudy 2013; Lawson 2000).

The Mexican case requires disentangling the effects of partisanship from the potential effects of subnational democracy. First, in Mexico there is a high correlation between authoritarian enclaves and the persistent rule of the PRI—that is, non-PRD governments. Therefore, the effect I find for left-leaning governments could be an artifact of a direct relationship between democracy and FDI in which states that are more democratic are more likely to attract FDI, and more likely to have PRD governments—due to increased political competition and turnover. Second, confounding the effects of partisanship and subnational democratization would be especially problematic within the framework of my argument, given that there is some evidence of a positive association between democracy and social spending, “particularly on items that bolster human capital formation” (Avelino, Brown, and Hunter 2005; Kaufman and Segura-Ubiergo 2001). The Mexican case allows us to test the independent effect of these competing dynamics.

Measuring democratization at the subnational level presents several challenges. The literature uses turnover or alternation in power as a proxy for the effective political competition that should characterize democratic environments. This is consistent with the “alternation rule” that prevents from considering democratic a country that holds elections, but in which incumbents never lost elections (Przeworski et al. 2000, 27). I include Turnover to control for states that escaped the PRI control at some point, and following the literature, I expect a positive relationship with FDI.

In model 8, the coefficient associated with Turnover is positive and marginally statistically significant. This result, however, does not let us disentangle the possible effect of democratization from partisanship. Because of the correlation between PRD and alternation (and PRI and lack of alternation), 20 it is not possible to include partisan variables together with Turnover. In model 9, I replace Turnover with a set of partisan variables that disentangle which party rules after at least one turnover: PRD, PAN, Independent, and PRI after turnover—the reference category is non-turnover. Only PRD is statistically significant, which suggests that the result of Turnover is driven by left-wing governments, and not by alternation in power.

Model 10 proxies subnational democracy with increased electoral competition. Margin of victory is the percentage-point difference between the winner and the second most voted party in the previous elections for governor. The assumption is that smaller electoral margins indicate more political competition, and thus, more democratic states (Benton 2012; Giraudy 2010). Based on previous literature, if democracies attract more FDI, Margin of victory should be negatively associated with FDI. However, Margin of victory is associated with positive but statistically insignificant coefficients. When the PRD variable is included (model 11), its coefficient has a similar magnitude, statistical significance, and direction as in the main models. Overall, these results suggest that the effect attributed to the left subnational rule is independent from the effect of subnational democratization.

On the Mechanism

I argue that in labor-abundant countries, investors will prefer left-leaning governments at the subnational level because left-leaning governments are more likely to invest in human capital. This section shows the plausibility of this argument for the case of Mexico. 21

Although state-level data do not individualize spending in human capital, 22 I test partisan differences in spending and infrastructure related to human capital. All models include the lagged dependent variable, the party ruling the state, 23 Development measured as the log of GDP per capita. I show results with and without fixed effects. Because I am interested in showing partisan differences, I include variables indicating non-PRD partisanship, omitting PRD for comparison purposes. These models’ samples differ from the main models due to data availability.

The dependent variable in models 12 and 13 is state social spending as a percentage of the state’s GDP. The models show that PAN and PRI governors spend significantly less than the PRD in this concept—about between 0.03 and 0.4 percentage point less than the PRD, which is sizeable given that the sample average for Social Spending/GDP is 0.11. I find a similar result if the dependent variable is spending in public works. PRD governments spend 0.002 percentage-points more of their GDP in public works. Although small, this figure represents almost 3 percent of the sample mean. Regarding actual infrastructure, only models including fixed effects show significant partisan differences. Models 17 and 19 suggest that states ruled by the PRD build relatively more hospitals and schools than states rules by other parties. The magnitude of these differences is small, and the indicators used here are indirect measures of actual spending. However, they suggest that the different spending patterns is a plausible mechanism.

Finally, I test whether PRD rule is associated with improvements in human capital in the longer run, proxied as average years of schooling of the population aged fifteen or more. Improvements in schooling take longer time, and depend on the magnitude and effectiveness of public investment, and also on state characteristics. For these reasons, I include a measure of the number of years under each party’s rule in the state in the previous ten years. Simple regressions on the level and change in years of schooling including fixed effects and state’s GDP per capita indicate that, holding everything else constant, more years under PRD rule are associated with higher levels and larger increases in the average years of schooling (Supplemental Appendix 13). In those models, the coefficients associated with PAN rule are negative, and those associated with PRI rule are positive, but much smaller that the PRD coefficients (almost half the size of the PRD coefficients).

Conclusions

This paper analyzes whether foreign investors have subnational political preferences and argues that we should expect a preference for subnational entities ruled by leftist governments. On a sample of all Mexican states, between 1999 and 2017, I find that partisanship has an effect on the subnational allocation of FDI and that left-leaning governments attract more FDI than centrist or right-leaning states. These results extend research by Pinto and Pinto (2008), and Pinto (2013) to the subnational level. However, I argue that the mechanism connection partisanship and FDI at the subnational level is different from the one operating at the national level for two reasons: the relative absence of legal barriers to trade and hire across subnational boundaries, and the more limited regulatory capacities of subnational authorities. Although I do not provide a direct test of the mechanism, the literature and descriptive data suggest that left-leaning governments seem to direct their spending toward human capital in a distinct manner, and simple analyses show a correlation between PRD rule and improvements in human capital in the longer term, which could explain the partisan differences in foreign investment flows. Micro-level data could provide direct evidence on how investors evaluate these factors. In addition, more refined data on new FDI would allow to explore sectoral differences (Hecock and Jepsen 2014). Unfortunately, those data are not available to date.

The partisan effect is robust, and it seems not to be driven by more democratization that correlates with alternation between the PRI and the PRD. Furthermore, results do not support that enclaves that are more democratic receive more FDI. Alternation in government seems to matter, but only when the Left enters in power. Political competition, the other proxy for subnational democracy, does not seem to be associated with new FDI. An important caveat, however, is that these two proxies are far from ideal measures of subnational democracy. Better measures of democracy or of institutional quality may have a significant effect on FDI.

This article presents another contribution by developing a parsimonious baseline model suitable for the study of subnational allocation of FDI. Previous studies are based on international FDI allocation model specifications, without considering that some of the factors that affect FDI across countries may play a different (or no) role in subnational FDI allocation—and possible, FDI retention—decisions. In addition, they do not include controls for national FDI or international shocks. Finally, some studies include predictors that do not vary across states or that are very highly correlated with each other, such as education and wages. The model presented here satisfactorily explains variation among states, and global variation in FDI.

The empirical evidence draws from a single but very important case. The Mexican case is critical to understand given the amount of FDI it receives. Regarding generalizability, it is likely to contribute to our understanding of the political economy of FDI in other federal countries. Furthermore, it may help understanding investors’ strategies when evaluating competing regions—in different countries—that will host their companies. So far, research on regime shopping suggests that investors do not follow a consistent strategy regarding environmental or labor regimes (Traxler and Woitech 2000), and other factors seem to play more important roles in the choice of FDI subnational location. Including the partisan dimension to these analyses may provide a more complete explanation of investors’ strategies. Another important caveat is that the empirical evidence corresponds to years of centrist and right-leaning national governments. In December 2018, the left-wing candidate Anders Manuel Lopez Obrador assumed office as president of Mexico. Unfortunately, there is no data to assess whether a change in the national-level partisanship affects the dynamics studied here. However, holding other things constant, my theory would not lead to expect a different logic for the subnational allocation of FDI.

This study helps to bridge research on comparative politics and on international political economy. The evidence suggests international effects of subnational partisanship and of a greater magnitude than economic factors. Furthermore, the direction of some findings suggests that subnational and national institutions may play different roles in investors’ decisions. These results highlight the importance of integrating domestic politics—national and subnational—to the analysis of international phenomena (Caporaso 1997). Partisan politics seem to matter, and other aspects of subnational electoral competition may matter, too (Beer and Mitchell 2004; Gibson and Suarez-Cao 2010). In this sense, this research also speaks to work analyzing the local effects of investment policies (Jensen and Rosas 2007; Owen 2019) and potential feedback effects between globalization and local politics (Ezrow and Hellwig 2014; Hellwig and Samuels 2007; Rommel and Walter 2017). A further step in this direction is to provide a unified framework linking national and subnational politics to fully understand investment decisions and their consequences.

Supplemental Material

sj-pdf-1-prq-10.1177_10659129211030331 – Supplemental material for International Capital and Subnational Politics: Partisanship and Foreign Direct Investment in Mexican States

Supplemental material, sj-pdf-1-prq-10.1177_10659129211030331 for International Capital and Subnational Politics: Partisanship and Foreign Direct Investment in Mexican States by Ana Carolina Garriga in Political Research Quarterly

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

Supplemental Material

Supplemental materials for this article are available with the manuscript on the Political Research Quarterly (PRQ) website.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.