Abstract

How does organized crime affect foreign direct investment (FDI) in developing countries? Some research examines the effects of crime, such as homicide rates, on FDI. However, we know little about how organized crime in particular might affect such investment. This paper examines organized crime and FDI in Mexican states between 2000 and 2018. This case is important because Mexico is one of the top global recipients of FDI. At the same time, criminal violence has killed hundreds of thousands of people in Mexico in recent years, and scholars seek to understand the violence’s wider effects. We explain how organized crime competition, as opposed to crime generally, should shape investors’ decisions. Analyses using original data on criminal organization territory find that higher numbers of criminal groups are associated with lower levels of new FDI. Other measures of crime, such as homicide rates or crime rates, are not associated with foreign investment.

Introduction

How does organized crime affect foreign direct investment (FDI) in developing countries? The presence of criminal organizations such as drug-trafficking groups creates a number of challenges for both governance and development (Shortland 2018). Criminal organizations can “by their very nature undermine civil society, destabilize domestic politics, and undercut the rule of law” (Williams 1994). Crime can affect political participation (Bateson 2012; Córdova 2019; Ley 2018), electoral outcomes (Alesina, Piccolo, and Pinotti 2019; Buonanno, Prarolo, and Vanin 2016), and the economy (Benton 2017; Daniele and Marani 2011).

Foreign direct investment is an important outcome of interest, although insufficiently studied regarding its possible relationship with organized crime. Foreign direct investment is crucial to economic development (Bhagwati 2007; Jensen and Rosas 2007; Jordaan 2008a), and even government stability (Malesky 2008; Owen 2019). Some studies examine how political violence may deter FDI (Powers and Choi 2012), and scholars have begun to explore relationships between criminal violence and investment. However, most of this work examines crime generally, not organized crime (Blanco, Ruiz, and Wooster 2019; Brock 1998; Brown and Hibbert 2019; Cabral, Mollick, and Saucedo 2019). Other studies stress the importance of organized crime, but almost all use proxies such as the homicide rate because more precise measures have not been available (Ashby and Ramos 2013; Ramos and Ashby 2013). These studies have reached mixed conclusions about how crime might affect FDI, if at all (Brock and Urbonavicius 2008; Ramos and Ashby 2013; Samford and Gómez 2014).

We study the relationship between organized crime and FDI using subnational data on criminal groups in Mexico. The Mexican case is important to understand given that Mexico is one of the top recipients of FDI in the world. 1 At the same time, Mexico faces substantial challenges with organized crime. The government started militarily confronting criminal groups in late 2006, and the resulting violence has killed more than 200,000 people and left tens of thousands missing (Grillo 2019). Some scholars call this violence “criminal conflict” or “criminal war” (e.g., Lessing 2015), and others argue that some models of traditional armed conflict can be applied to such bloodshed (Kalyvas 2015). Because organized crime violence is increasingly a concern in many areas, such as other parts of Latin America, West Africa, and Southeast Asia, the Mexican situation can speak to other cases.

By explaining how criminal groups’ dynamics may have distinctive effects on FDI, we add to the relatively small but growing body of work exploring political and economic consequences of criminal violence (Bateson 2012, Daniele and Marani 2011, Ley 2018). Furthermore, we unpack criminal violence with a deeper look at organizational aspects of organized crime. More than most extant work has done, we consider theoretical explanations for how organized crime competition should affect investment.

Empirically, the paper introduces a series of innovations. First, most previous studies do not include actual measures of organized crime – only crime or homicides in general. We introduce new data, counting the number of criminal groups operating in each Mexican state by year. This allows us to study the effects of the presence of organized crime independently of the effects of the violence that the states experience. Second, we study the effect of organized crime on new FDI flows. Other studies use total FDI, which includes new FDI, reinvestments, and loans between headquarters and subsidiaries. New FDI should be more sensitive to recent economic and political factors than reinvestment decisions (Coughlin and Segev 2000), which makes it a more suitable measure of investors’ reactions to criminal violence. Third, this paper uses new data reflecting the actual location of FDI. Previous studies of Mexican FDI used data that recorded the investment where the main offices of multinational corporations were located, overestimating the FDI that Mexico City received, and misrepresenting the actual distribution of investment (Comision Nacional de Inversiones Extranjeras 2019, 8-9).

Finally, the temporal span of our sample, 2000-2018, is more appropriate to study the effects of organized crime. Previous studies on the effects of crime on FDI in Mexico analyze years before Mexico’s so-called drug war began in late 2006 (Escobar Gamboa 2013; Jordaan 2008b; Madrazo Rojas 2009; Mollick, Ramos-Duran, and Silva-Ochoa 2006), or only cover the first few years of it (Ashby and Ramos 2013; Ramos and Ashby 2013; Samford and Gómez 2014). Now that the drug war has continued for more than 10 years, readers are probably curious how organized crime is associated with FDI during these years – as criminal groups have come and gone, and their territory has changed substantially.

The next section reviews research on violence and FDI. The third section presents the argument of how the presence of criminal groups, and especially competition among them, should deter FDI. The fourth section describes the data and empirical approach. We then present our analysis, which finds support for the argument. Each additional criminal group in a Mexican state is associated with less new FDI in the subsequent year. Interestingly, we do not find this deterrent effect for homicides or crime generally. We conclude with implications of the findings and suggestions for future research.

Literature Review

How does violence affect investment? Important research examines whether violence influences the decision to invest in a country. Many studies include violence under the umbrella of political risk (Barry and DiGiuseppe 2019; Busse and Hefeker 2007; Lee, Biglaiser, and Staats 2014), or the more general concept of “political instability” (Asiedu 2002, 2006; Feng 2001), and find mixed evidence that instability affects FDI.

Although a growing literature focuses specifically on how violence affects investment, the majority of these studies consider political violence, not criminal violence. 2 Regarding political violence, some studies find a negative relationship between terrorism and FDI (Abadie and Gardeazabal 2008; Bandyopadhyay, Sandler, and Younas 2013; Enders and Sandler 1996), although other evidence contradicts this result (Enders, Sachsida, and Sandler 2006; Li 2006; Li and Schuab 2004; Powers and Choi 2012). Collier (1999) finds that civil war is associated with a reduction in gross domestic product, and argues that this is because of capital flight, 3 and Jensen and Young (2008) find that recent political violence (civil or international war) is associated with higher prices for violence risk insurance. Overall, political violence seems to deter FDI, but relationships are often conditional.

Beyond political violence, the literature has examined how crime and criminal violence might affect FDI. Some global studies find a negative relationship between the homicide rate and total FDI (Brown and Hibbert 2017), or FDI in some sectors, but not others (Blanco, Ruiz, and Wooster 2019; Brown and Hibbert 2019). Country studies of crime and FDI sometimes find similar results. Gaviria (2002) shows that crime reduces firm competitiveness, and infers that this should reduce FDI inflows to Latin American countries. Research on Pakistan (Nadeem, Ahmed, and Shakeel 2017), and Russia (Brock 1998) also find a negative association between crime rates and FDI. In one of the few studies explicitly about organized crime, crime tied to the Mafia is negatively associated with FDI in Italy, but other types of crime are not related (Daniele and Marani 2011).

Subnational studies of Mexico find mixed evidence regarding a possible relationship between criminal violence and FDI. Some research finds that crime in general is negatively associated with FDI (Escobar Gamboa 2013), or with only resource-seeking FDI (Samford and Gómez 2014). Regarding homicides, some studies show that they are negatively associated with most types of FDI (Ashby and Ramos 2013; Cabral, Mollick, and Saucedo 2019; Madrazo Rojas 2009; Ramos and Ashby 2017). Other studies, however, find that homicide is positively associated with either total FDI (Brock and Urbonavicius 2008), or FDI from countries that have a high amount of crime (Ramos and Ashby 2013). Moderating factors, such as the type or origin of the FDI also seem to matter (Garriga 2017; Ramos and Ashby 2013; Witte et al. 2016).

Overall, there is some evidence in the literature of a negative relationship between crime, particularly violent crime, and FDI. However, the above studies have limitations. Almost none of the studies include measures of strictly organized crime violence. 4 The analyses of FDI in Mexico usually rely on relatively coarse proxy measures for organized crime. Additionally, as noted earlier, most of the studies have covered few or no years of the serious organized crime situation since 2007 in Mexico. Should we expect a relationship between organized crime and FDI?

Theory: Organized Crime Competition and FDI

While crime seems likely to affect FDI allocation decisions, this paper focuses on the influence of organized crime competition on investment decisions. Inter-group competition is a regular aspect of criminal group life. One reason for this is that criminal organizations generally seek to control markets or territory, to have a monopoly over a certain area (Schelling 1971; Varese 2010). 5 Competition varies considerably in areas where criminal groups operate. At one extreme, some cities or regions have many groups fighting amongst themselves, a highly competitive environment. At the other extreme, a single group has a monopoly, and no competitors exist. Within this spectrum are many degrees of competition, but perhaps the most commonly occurring dynamic is several groups that compete for market share, with sometimes-surging rivalries and fleeting alliances (Atuesta and Pérez-Dávila 2018; Descormiers and Morselli 2011).

Criminal group competition is likely to have unique deleterious effects for foreign investment. Competition suggests violence, often extreme and visible. A great deal of research shows that increasing competition among criminal groups is associated with increased violence – whether in Italy (Moro, Petrella, and Sberna 2016), Latin America (Atuesta and Pérez-Dávila 2018; Berg and Carranza 2018; Durán-Martínez 2015; Rios 2013), Russia (Volkov 2002), the United States (Block 2000), or elsewhere. Gambetta (1993, 40) argues that competition is probably the most common reason for organized crime violence. While there generally seems to be a relationship between competition and violence, we emphasize that competition can affect the quality of violence. Competition leads to extreme and predatory violence, though mechanisms we discuss below, and this is likely to concern foreign investors.

Organized crime violence becomes especially serious when criminal groups are competing for territory (Guerrero Gutiérrez 2011; Rios 2013). When a single group has a monopoly over territory, it might leave legitimate businesses alone, especially if the group is primarily focused on trafficking. This would provide stability that would be attractive to investors. An example of this is the southern state of Campeche, where the Zetas were largely unchallenged in the mid-2010s. Campeche received much more new FDI during years of only the Zetas present compared to years with multiple groups. 6 Alternately, if the single group is small, it might be too weak to substantially affect businesses, especially powerful foreign corporations. Either way, a single group in an area might not necessarily be detrimental to investment. When multiple groups are present, however, they often try to take each other’s territory – and threaten those in their way.

Competition between criminal groups can lead to extreme and public violence. For example, when Mexican cartels fight over territory, they frequently block roads with burning cars in what are called “narcobloqueos,” or narco roadblocks, in order to show their power (Peña 2019; Phillips 2018). 7 Such public and indiscriminate violence could make foreign firms alarmed about the safety of their workers and property, raising concerns about how their products are to be safely transported. Consistent with this, a 2018 survey of foreign executives in Mexico found that that 14% of respondents reported that their companies suspended operations in certain states for security reasons (AmCham Business Security Survey 2018). Respondents indicated substantial concern about Tamaulipas, a northern state affected by violence related to inter-cartel disputes in recent years (Parish Flannery 2018).

The notion that competition-induced violence on its own could deter FDI is consistent with some research on Mexico (Madrazo Rojas 2009; Ashby and Ramos 2013). In 2012, the then-president, Felipe Calderón, acknowledged that crime is likely to deter FDI (Caldwell 2012). JP Morgan’s chief Mexico economist stated in 2011: “We are seeing a geographic change in new investment plans from hotspots of violence to safer cities” (Cattan 2011). Analysts frequently use criminal violence to gauge the safety in the country – particularly related to its favorability as an investment location (Estevez 2014).

Our primary emphasis is on competition, but competition is intimately related to fragmentation – a frequent source of criminal group competition. 8 Fragmentation refers to groups breaking into smaller organizations, whether it is a single group splintering off and the original group remaining mostly as it was, or the original group dissolving into smaller organizations. Fragmentation can result from government interventions, such as when security forces kill a group leader (Atuesta and Pérez-Dávila 2018; Atuesta and Ponce 2017; Durán-Martínez 2015). Groups also break up as a result of inter-group fighting (Locks 2015) – thus fragmentation is both a cause and consequence of competition. Resisting fragmentation is important for criminal groups, as intra-group cohesion is associated with group survival over time (Ouellet, Bouchard, and Charette 2019). Yet fragmentation is widespread among criminal organizations (Atuesta and Pérez-Dávila 2018; Guizado and Restrepo 2000).

Beyond affecting violence, competition and fragmentation often lead to predatory criminal organizations. In the Mexican case, the fragmentation of drug trafficking groups has generated smaller groups too weak to transnationally traffic drugs. These new groups turn to “easier” businesses like extortion, kidnapping, and robbery (Guerrero Gutiérrez 2011; Locks 2015). The extortion rate in Mexico tripled between 2001 and 2009, and security experts attribute this to criminal group fragmentation (Guerrero Gutiérrez 2011, 58-59). 9 Predatory crimes like extortion have serious negative implications for businesses (Konrad and Skaperdas 1998). Attacks by armed groups are associated with domestic firm exit from areas in Colombia (Camacho and Rodriguez 2012), and it makes sense that the logic would apply to foreign firms, since they seem to be sensitive to crime generally (Gaviria 2002; Nadeem, Ahmed, and Shakeel 2017). Research on Italy suggests that extortion and related crimes are associated with less FDI (Daniele and Marani 2011).

In Mexico, criminal groups are probably more likely to target domestic firms (Celis 2018), but they also attack foreign companies (Gonzalez 2012). For example, “heavily armed commandos” kidnapped a PepsiCo executive in June of 2015 in the southern state of Guerrero (Parish Flannery 2015). Both Pepsi and Coca-Cola scaled back operations in the state that year after a series of kidnappings and arson attacks apparently related to extortion. In 2018, Pepsi completely withdrew from the Guerrero city of Altamirano, blaming extortion and robbery, and laid off 70 employees (Sin Embargo 2018). In 2015, someone set fire to a Tabasco branch of the U.S. oil services firm Key Energy Services, and the Mexican government speculated that the attack was extortion-related (Grillo 2015). Many more such cases probably exist, but crimes like extortion are usually unreported (e.g., Barrera González 2019). The threat of predatory crimes has caused foreign firms to close operations in a variety of states, and spend more on security (AmCham Business Security Survey 2018).

Predation resulting from organized crime competition and fragmentation can also deter investment through effects on local law enforcement. As criminal groups compete for control of territory, they often get municipal police to not only tolerate their actions, but actually affiliate with particular criminal groups (Moro, Petrella, and Sberna 2016; Morris 2013). There are many cases of Mexican police working for one group and attacking or arresting its rivals, and hundreds of police officers are killed each year by criminal groups – often for not cooperating (Hope 2018; Monroy 2021; Semana 2021). It is difficult to know to what extent the participation of local police in organized crime is voluntary or coerced. The result, however, is local authority in the hands of organized crime. This suggests challenges for foreign investors. When local police are controlled by criminal groups, foreign firms will be on their own regarding security provision and unable to depend on local authorities if victimized by crime. In general the literature finds mixed relationships between corruption and FDI (Cuervo-Cazurra 2008; Wei 2000), but this particular type of corruption – local police serving predatory criminal gangs, often to attack rivals – seems especially discouraging for foreign investors.

Overall, organized crime competition should provide a unique set of challenges for foreign investors. Although risk insurance could hedge economic costs imposed by some criminal activities on business, the cost of such insurance is not negligible, and can deter investment. 10 Furthermore, criminal violence generates additional costs that are seldom covered by risk insurance. For example, the American Chamber of Commerce in Mexico estimates that “security costs business as much as five percent of operating budgets. Many companies choose to take extra precautions for the protection of their executives. They also report increasing security costs for shipments of goods” (United States Department of State 2019). British investors highlighted that criminal violence caused “a logistical nightmare and a costly slap in the face after all their investment in Latin America’s number-two economy” (Webber 2017).

In brief: competition often leads to qualitatively extreme violence and group fragmentation, fragmentation produces groups likely to engage in predatory crimes and further compete in the same territory, and all these issues concern investors. While crime or homicide in general might deter FDI, it seems likely that organized crime dynamics, particularly inter-group competition, should have especially adverse consequences for foreign investment. This suggests the following hypothesis: Higher levels of organized crime competition are associated with lower levels of FDI.

Note that this hypothesis is not necessarily intuitive. Regarding the Mexican case, some analysts have looked at overall increases in FDI in Mexico and argued that the drug war is not scaring investors. Headlines like “Crime explodes – but an economy booms” (Caldwell 2012) and “Lego is not afraid of Mexico’s drug war” (Thomson 2011) suggest no relationship. This is consistent with the comments of the CEO of a Canadian mining company, who said that drug cartels usually left his business alone (Grillo 2015). Overall, however, the notion of competition suggests that organized crime should generally deter investment.

Empirical Strategy

Data

The dependent variable is new FDI measured as the natural logarithm of the state’s yearly FDI inflows in constant 2012 U.S. dollars. 11 We use new FDI because new investments are more likely to reflect recent evaluations of the host state – as opposed to reinvestment decisions, for example. The data come from the Mexican government (Gobierno de Mexico 2019). In 2015, the Mexican Secretary of Economy revised the methodology to register FDI. The new subnational data record the actual location of the investment, instead of where the headquarters of the company are located in Mexico (Comision Nacional de Inversiones Extranjeras 2019). The new data start in 1999 and are not systematically correlated with previous releases of official data. The last year with official data is 2018. Unfortunately, Mexican official data do not allow users to distinguish the sector that receives new FDI (sectoral data is available only for total FDI), or whether this investment is greenfield or brownfield, which limits additional analyses.

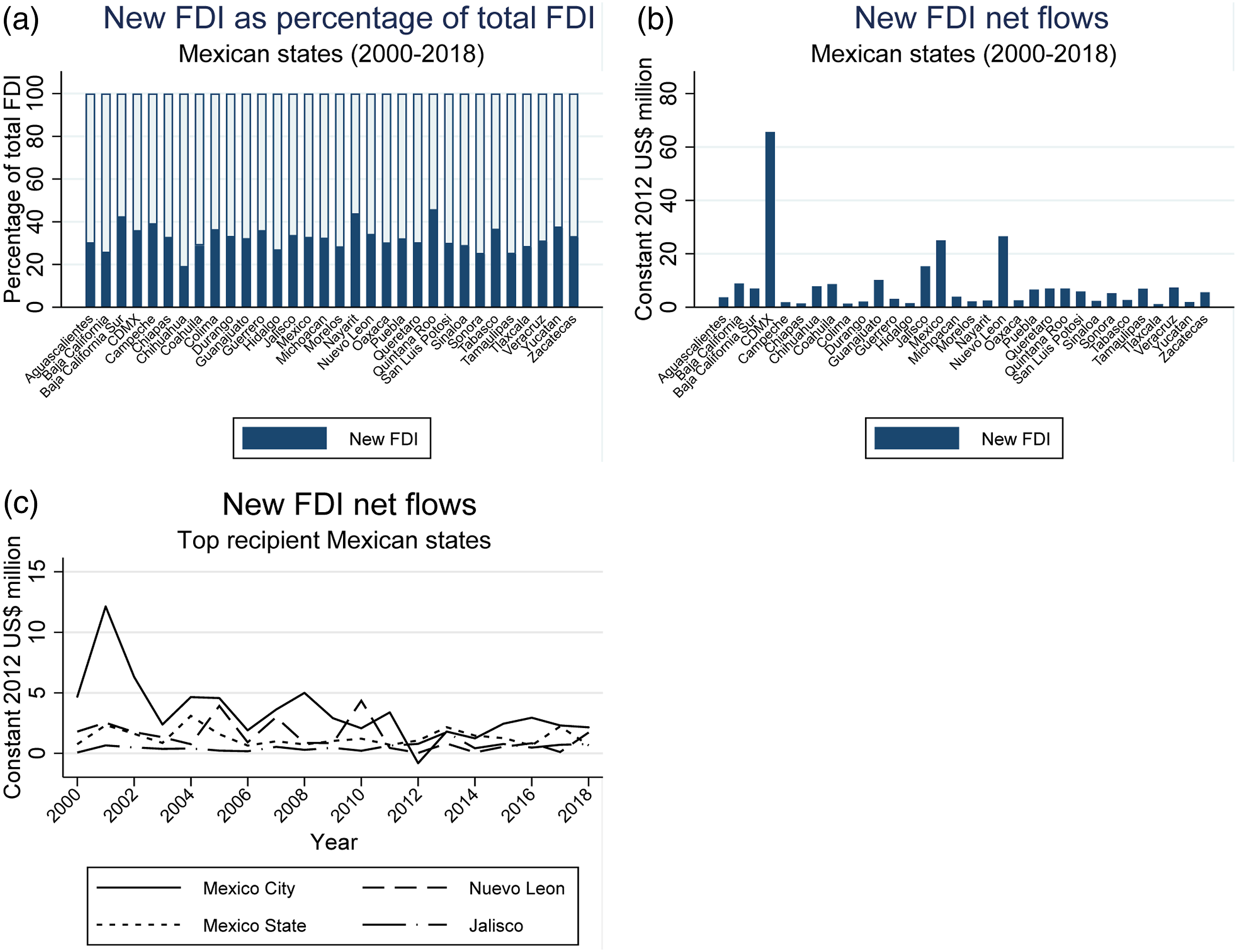

New FDI accounts for between 20 and 45% of the total FDI received by each Mexican state between 2000 and 2018 (see Figure 1a). As Figure 1b shows, there is substantial variation throughout the 32 Mexican states in FDI. During the 2000-2018 period, the top recipient state was Mexico City (25.2% of the country’s new FDI). Other top FDI recipients include Nuevo Leon (10.2%), the state of Mexico (9.6%), and Jalisco (5.9%). There is also substantial temporal variance within states (Figure 1c). New foreign direct investment to Mexican states. Descriptive data.

To further explore variation in foreign investment, Figure 2 indicates the average amount of new FDI each Mexican state received per year between 2000 and 2018. Note that FDI is not concentrated only in the north, near the U.S. border, or only in beach areas to exploit tourism opportunities. Geographically there is a great deal of variation, with some of the top-earning states in the center of the country (Mexico City and Mexico State), north (Coahuila and Nuevo Leon), or northwest (Baja California). Yearly average of new foreign direct investment received per state, 2000-2018.

Our key independent variable is Criminal groups. This is a count of the number of criminal groups active in the state that year, to proxy the notion of criminal group competition. We assume that group competition is likely to increase as the number of groups operating in a state grows. The data are a temporally-extended version of a variable published by Phillips (2015) that originally covered 2006-2012. For that paper, Phillips used Mexican news reports, government reports, and other sources such as STRATFOR maps to identify the geographic territory of criminal groups in Mexico. 12 For the current paper, we followed the coding description in Phillips (2015) and gathered new data using the same types of sources. The new variable covers 2000-2018.

This variable is a direct measure of criminal group presence, and is therefore a better measure of organized crime than counts of crimes, as many crimes are perpetrated by actors unaffiliated with organized crime. This is the case with homicides, many of which in Mexico are not connected to organized crime.

13

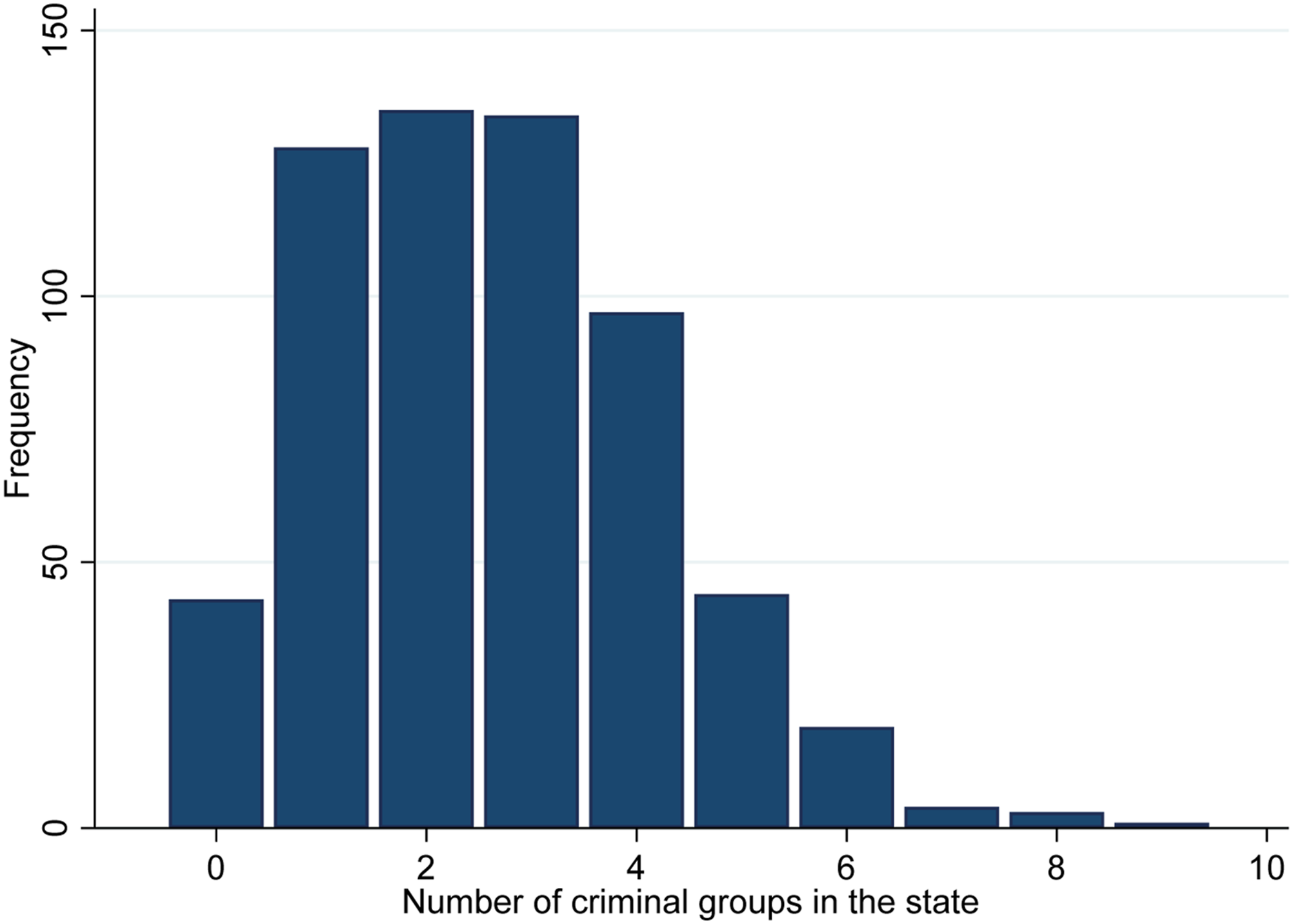

Criminal groups is a good measure of competition because additional groups suggest additional opportunities for competition. In the study of comparable groups, such as dissident or terrorist organizations, counts of groups in a geographic area are often used to indicate competition (Belgioioso 2018; Conrad and Greene 2015). A broad range of research, including studies of street gangs, finds higher number of groups in an area associated with more violence and qualitatively different types of violence (Block 2000; Conrad and Greene 2015; Dowd 2019). The variable ranges from 0 to 9, with a mean of 2.9 criminal groups per state, and a median of 2. States with high numbers (>5) of criminal groups during various years include Guerrero, Jalisco, Mexico City, Mexico State, and Michoacán. Figure 3 shows the distribution of this independent variable. Number of criminal groups per state in a given year.

Our baseline model includes a series of controls, all lagged 1 year: We include a measure of homicides per 100,000 inhabitants (natural log) using data from the Mexican Institute of Statistics (INEGI). Homicide rate is correlated with Criminal groups at 0.42, indicating some overlap between the two. However, they are not highly correlated, which suggests they are distinct phenomena. Homicides are sometimes used as a proxy for organized crime violence, since data on other crimes (e.g., kidnapping, extortion) is markedly incomplete. However, since many homicides are unrelated to organized crime – but to domestic violence or small-scale robberies, for example – it is not a precise measure of organized crime. Market size is the log of the state’s population as in Ramos and Ashby (2013). Development is the log of GDP per capita, in constant 2012 U.S. dollars. Contrary to expectations from cross-national studies, sub-national analyses of Mexico either find GDP per capita is not related to FDI (Ashby and Ramos 2013; Garriga 2022; Mollick, Ramos-Duran, and Silva-Ochoa 2006; Ramos and Ashby 2013), find mixed results (Escobar Gamboa 2013), or find that GDP per capita is negatively related to FDI. Growth is the state’s real GDP growth. Road density is the length of roads, divided by the state’s area. We include a year lag of the dependent variable because there is evidence that even new investment decisions use information produced from companies in the field, especially if both companies share national origin (Garriga and Phillips 2014; Mody, Sadka, and Razin 2003). 14

The quality of institutions may affect investors’ decisions, thus we include a proxy for subnational democracy. The literature suggests the “alternation rule” as an indicator of democratic competition – that is, besides holding elections, incumbents need to lose elections to be considered democratic (Przeworski et al. 2000). Mexico was ruled for 72 years by the Institutional Revolutionary Party (PRI). Although the PRI lost the 2000 national election, the PRI has never lost control of the executive power in many states, which is considered an indicator of subnational authoritarian enclaves (Benton 2008; Garriga 2022). Democracy is a dichotomous variable coded 1 if the PRI has lost the state governor elections at some point in the past; and zero otherwise. The baseline model also includes year-fixed effects.

For models without state-fixed effects, we include Ports, a dichotomous variable indicating the existence of commercial ports; Mexico City is a dichotomous variable individualizing Mexico City, the largest recipient of FDI in the country, and distance from the state to the closest U.S. border crossing (data from Jensen and Rosas (2007)).

Methods

We estimate the following regression

The literature suggests that the dynamic nature of the panel is especially relevant: current FDI is affected by its past values (Ashby and Ramos 2013; Sánchez-Martín, de Arce, and Escribano 2014). Therefore, our benchmark specification is a dynamic panel model with fixed effects. A lagged dependent variable could introduce a bias (Nickell 1981). We address this issue in two ways. First, we remove the lagged dependent variable (equation (2)). However, this would cause equation (2)’s point estimates to be less precise due to a specification error (Mizon 1995).

We do not estimate an error-correction model as our benchmark specification for several reasons: the series are stationary, the time series are too short, and lack of data on new FDI stock However, we re-estimate the model in changes, and results are substantively the same (see online Appendix 1).

Second, we use Generalized Method of Moment (GMM) dynamic panel data estimators (Arellano and Bond 1991; Arellano and Bover 1995; Blundell and Bond 1998), which allows us to address the issues of joint endogeneity of all explanatory variables in a dynamic formulation, while mitigating potential biases induced by fixed effects. Our data is consistent with two main assumptions of this approach: we do not find serial correlation in the second order differences, and Sargan and Hansen tests show the validity of the instruments. This approach has limitations. The instrument count can easily grow large relative to the sample size (Roodman 2009), risking to overfitting endogenous variables, and biasing coefficient estimates. To address this, we estimate models including Windmeijer’s (2005) correction for limited samples, 15 and we limit the construction of our instruments to the first lag of all variables but our main independent variables (second lag), and omit year fixed effects. We specify population and geographic controls as instruments. An additional specification also includes time-invariant variables controlling for the most relevant state-level features that could affect the FDI a state receives. Nevertheless, given the risks of bias in our estimates, we use equation (1) as our benchmark specification and substantive interpretation.

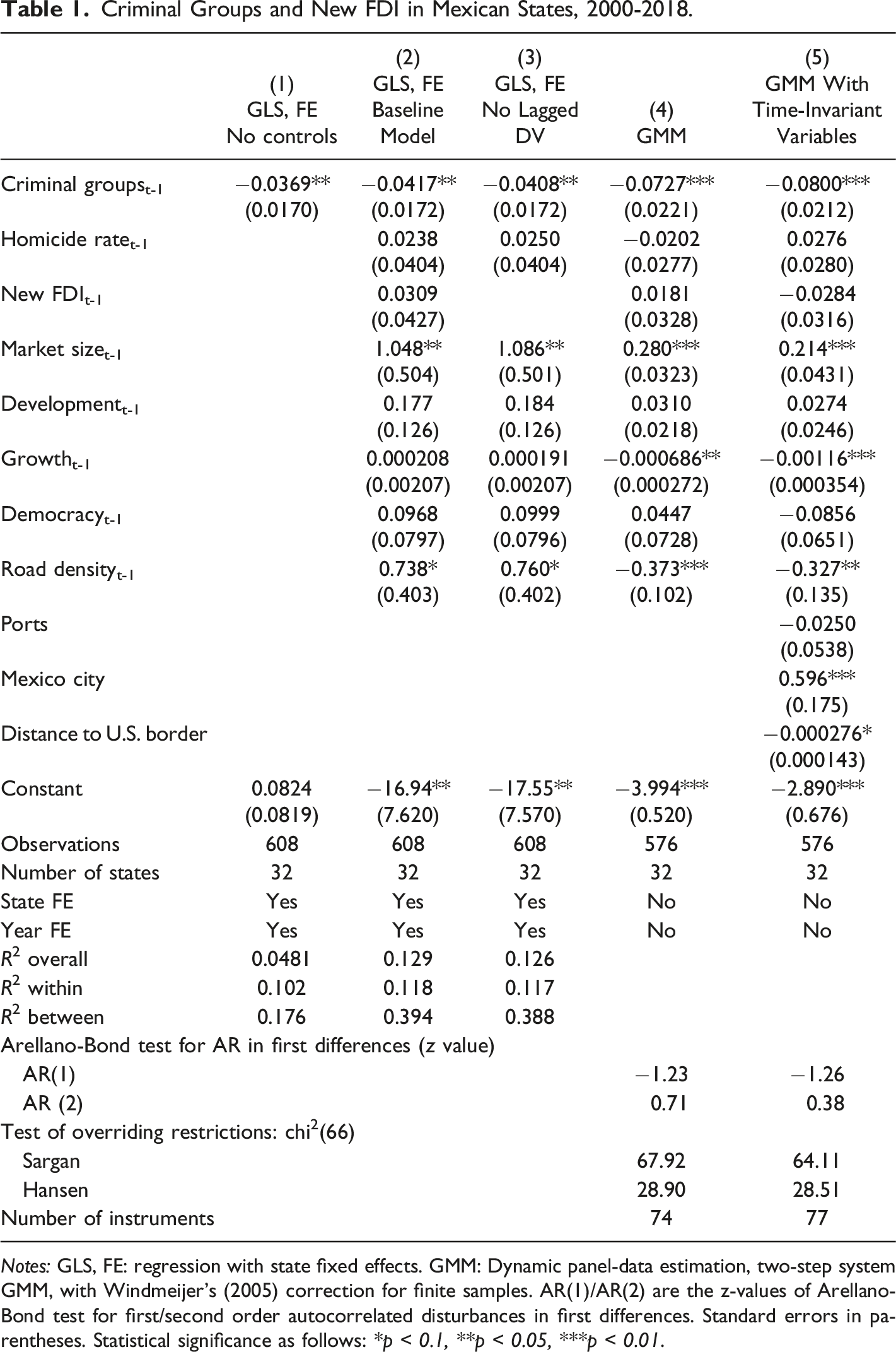

Results

Criminal Groups and New FDI in Mexican States, 2000-2018.

Notes: GLS, FE: regression with state fixed effects. GMM: Dynamic panel-data estimation, two-step system GMM, with Windmeijer’s (2005) correction for finite samples. AR(1)/AR(2) are the z-values of Arellano-Bond test for first/second order autocorrelated disturbances in first differences. Standard errors in parentheses. Statistical significance as follows: *p < 0.1, **p < 0.05, ***p < 0.01.

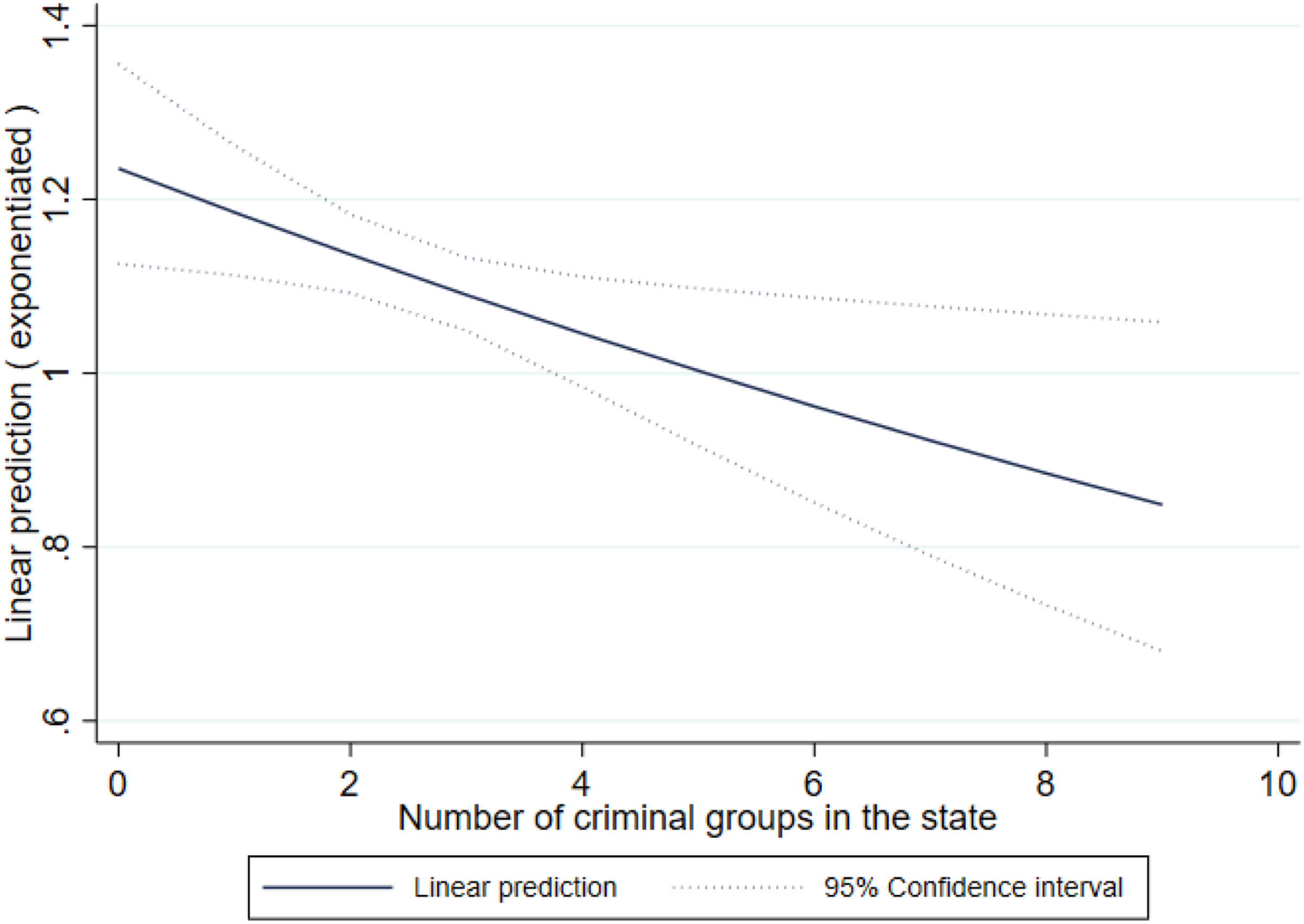

Figure 4 plots the marginal effects of Criminal groups.

17

Holding other variables at their mean, the model predicts that a movement from the minimum to the maximum levels in Criminal groups (0–9) is associated with a 31% reduction in new FDI. In other words, a state with no criminal activity would receive $1.235 billion, but if there were 9 criminal groups, it would receive $849 million. Predictive margins of criminal groups on new foreign direct investment (billions of 2012 U.S. dollars).

A comparison of the standardized effect of statistically significant variables, with other variables held at zero, shows that the substantive effect of Criminal groups is sizable: a standard deviation-increase in criminal groups (1.617 groups) is associated with a $1.687 billion reduction in FDI. This represents 77.5% of the effect of a standard deviation change in Market size (US$ 2.176 billion), and 461% the effect of a standard deviation of Road density (US$ 366 million). 18

Homicide rate does not achieve statistical significance in any of the models. This contrasts with some previous studies that find a negative association between crime and total FDI (either by sectors or in total). We further analyze the effect of this variable in the robustness analysis section. However, this result suggests support for our argument: new FDI seems to be dissuaded by the set of issues represented by additional criminal groups, but it is apparently not deterred by criminal violence generally.

Regarding other control variables, Market size (population) has a significant and positive effect on new FDI inflows in all four models. Road density has a positive and marginally statistically significant effect in models with fixed effects, suggesting that improvements in road infrastructure attract FDI. This variable has a negative statistically significant effect in GMM models. The negative sign is unexpected, but in models without fixed effects, this variable could be influenced by the size of the state (a between-effect) instead of being a reliable proxy for improvements in infrastructure (within-effect). The lack of significance of other independent variables is consistent with a number of subnational studies, including those of Mexico (Ashby and Ramos 2013; Escobar Gamboa 2013; Garriga 2022; Samford and Gómez 2014), and suggests important differences between cross-national and within-country studies of FDI.

Model 5 includes several time-invariant variables. Only Mexico City is statistically significant and positive, capturing the fact that holding other things constant, this federal entity receives more foreign investment, relative to the other 31 Mexican states. Ports and Distance to U.S. border are statistically insignificant, as they are in some other studies (Jordaan 2008b; Mollick, Ramos-Duran, and Silva-Ochoa 2006). Although one could expect more FDI near ports and the U.S. border, FDI is distributed throughout the country in areas such as tourist beaches and mines, as well as central Mexico, so apparently ports and the border are not uniquely important.

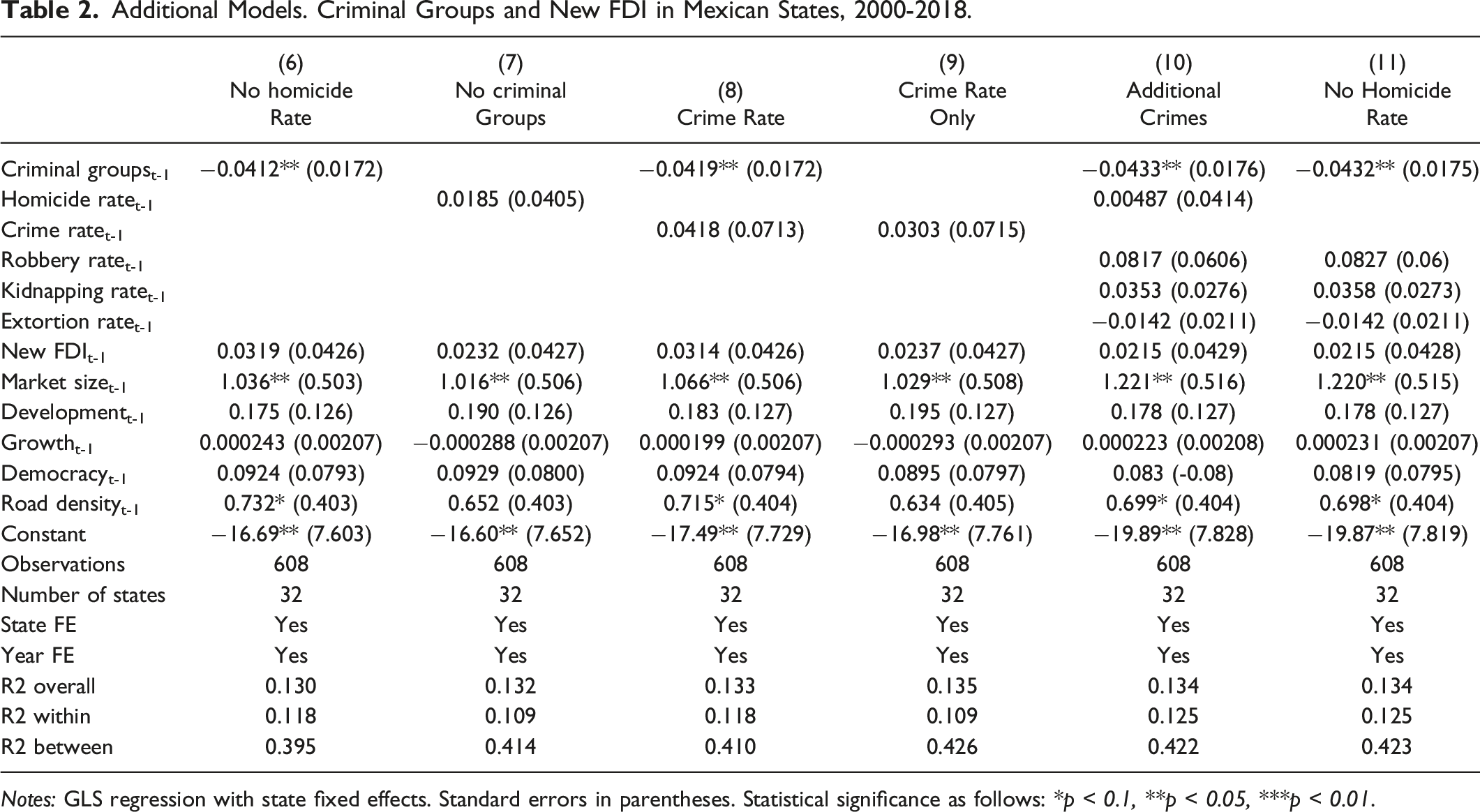

Additional Models. Criminal Groups and New FDI in Mexican States, 2000-2018.

Notes: GLS regression with state fixed effects. Standard errors in parentheses. Statistical significance as follows: *p < 0.1, **p < 0.05, ***p < 0.01.

Models 8 and 9 include an alternate measure of crime, Crime rate, which includes all crimes, including and excluding our measure of Criminal groups. As with homicide rates, the coefficient on Crime rate is statistically insignificant in both models. Models 10 and 11 include measures of the robbery rate, kidnapping rate, and extortion rate in each state-year – Model 11 excludes the homicide rate measure, since it is correlated with kidnapping at 0.55. These variables are included because higher rates of these crimes might deter foreign investment. The coefficients on each of these variables are statistically insignificant in both models. However, as noted earlier, kidnappings and extortions are significantly underreported, and it is probably not randomly missing. The (non-)results on these coefficients should be taken with some caution, and for that reason we do not include the variables in all models. Regardless, our main result holds. The lack of relationship between homicides or crime and FDI might seem surprising. However, a great deal of crime does not directly affect foreign firms.

State Interventions Against Crime

Our baseline model does not account for state interventions against crime. Models 12 and 13 include two additional indicators: Security spending is the percent of a state’s budget that is spent on public security. 19 It could be that states providing more public security draw more foreign investment. This variable is missing information for some state-years, so models only have 479 observations – a reduction of more than 20% of observations. For this reason, we do not include Security spending in our baseline model. The coefficient on Security spending is positively signed, but statistically insignificant. Model 13 includes a count of the number of criminal group leaders arrested or killed by authorities in the state-year, which could proxy both state capacity and willingness to confront organized crime. 20 The coefficient is negatively signed and marginally significant (p < 0.10). More criminal leaders caught in a state are associated with less new FDI the following year. This could be the result of the widely-noted phenomenon where pressure on criminal groups can backfire, leading to instability, fragmentation, and predatory crime (Atuesta and Ponce 2017). Again, however, other results are robust to the inclusion of this variable. The number of criminal groups in a state-year is robustly associated with less new FDI in the state in the subsequent year, even when taking into consideration many alternate factors such as specific crimes and government security approaches.

External Shocks

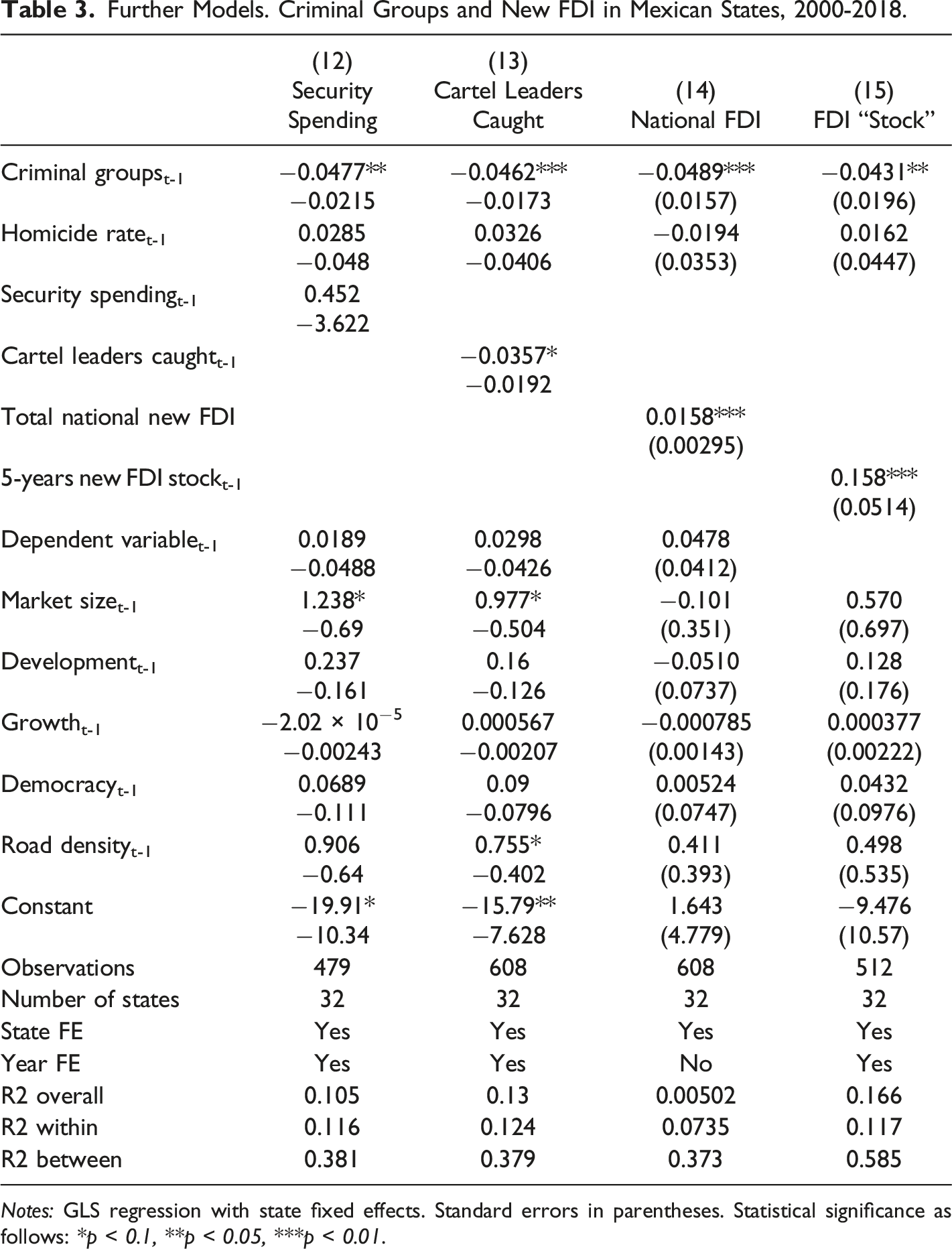

Further Models. Criminal Groups and New FDI in Mexican States, 2000-2018.

Notes: GLS regression with state fixed effects. Standard errors in parentheses. Statistical significance as follows: *p < 0.1, **p < 0.05, ***p < 0.01.

Reverse Causality

The GMM approach (models 4 and 5) may not ease concerns regarding the possibility of FDI driving organized crime numbers. To alleviate these concerns, we estimate models predicting Criminal groups and Homicide rates. Both past values of new FDI in the previous year and the total of the past 5 years are negative, but neither variable achieves statistical significance (see online Appendix 2). This suggests that FDI is not driving increases in criminal groups or homicides.

Other FDI Flows

One could expect different sensitivity or elasticity to criminal violence depending on the kind or origin of FDI (Blanco, Ruiz, and Wooster 2019; Brown and Hibbert 2019; Witte et al. 2016). 22 Unfortunately, as mentioned above, new FDI data is not disaggregated in any of these dimensions. Using sectoral total FDI is not a satisfactory proxy for several reasons: First, new FDI is not a constant share of total FDI. Second, total FDI includes an important proportion of reinvestment; third, reinvestment and new FDI are not highly correlated. Finally, we argue that the logic driving new and reinvestment decisions are different – for example, security concerns may halt new investment, but force companies to not distribute profit and “reinvest” to protect the investment already made. This contrasting logic should make data on total FDI a poor proxy for new FDI. Online Appendix 3 shows that the determinants of new FDI have different effects for reinvestment and total FDI, which suggests that the logic behind different forms of FDI may be different and should be theorized separately.

Diminishing Returns

We also explore the possibility of a diminishing impact as the number of criminal groups increases. We interact the change in groups with the number of groups and find that, although an additional group is always associated with less FDI, the first additional group (from 0 to 1) is associated with a $1.109 billion (constant 2012 U.S. dollars, holding other variables to zero) reduction in expected FDI, while the “last” additional group (from 8 to 9) is associated with a $724 million reduction in expected FDI. See online Appendix 4.

Conclusions

How does organized crime affect FDI in developing countries? This question is puzzling because the news media and academic research present conflicting expectations. Some news sources present accounts of crime deterring foreign corporations (Parish Flannery 2015), but other reports indicate that companies are not substantially affected by crime – organized or otherwise (Caldwell 2012). At the same time, some research suggests a deterrent effect of crime on FDI (Ashby and Ramos 2013; Escobar Gamboa 2013), but other work suggests complicated or mixed relationships, if at all (Ramos and Ashby 2013; Samford and Gómez 2014). Almost none of this work uses measures of organized crime in particular. Furthermore, there is often little discussion of the specific causal mechanisms through which organized crime might concern investors.

This paper sought to address these issues by presenting an argument about organized crime competition, a process that involves multiple criminal groups fighting and often engaging in predatory behavior. This seems likely to deter foreign investors. Empirical analyses of Mexican states from 2000-2018, using new data on the presence of criminal groups in each state, suggests support for the argument. State-years with higher numbers of criminal groups receive lower levels of new FDI the following year. Interestingly, neither the homicide rate nor the crime rate is associated with foreign investment, suggesting a process unique to organized crime.

There are several important implications of these findings. Despite some news media and government suggestions that investors are ambivalent about organized crime, there seems to be a deterrent effect. This suggests yet another reason that governments – including those of the firms that invest abroad – should be concerned about organized crime. Foreign direct investment often has positive effects on recipient countries (Bhagwati 2007; Jensen and Rosas 2007), so declining investment is cause for alarm. Governments of FDI “sending” countries might be ambivalent about organized crime in the countries where foreign investment occurs, but these governments should realize that organized crime has potential implications for their own economy as well. In other words, the paper’s findings suggest international consequences of organized crime.

Additionally, the attention to the problem of multiple criminal groups in a particular space – and fragmentation specifically – raises questions about the policy of “decapitation” many governments use toward criminal groups. State security forces sometimes put substantial emphasis on “wanted” lists of criminal group leaders, and the loss of leaders causes the remaining groups to fragment into multiple new organizations (Atuesta and Ponce 2017; Durán-Martínez 2015). This is obviously not the only factor behind fragmentation (Locks 2015), but it is one apparently spurred by government policy. The phenomenon has been noted in Colombia and Mexico, for example (Pachico 2015). This paper’s results suggest that this decapitation focus should be reconsidered, or governments that use the policy should prepare for economic consequences among others.

Our findings suggest steps for future research. First, should we expect the same relationships between criminal groups and FDI to be present elsewhere? It seems reasonable to expect similar dynamics in other countries with multiple prominent criminal groups, such as Colombia, El Salvador, or Italy. Second, which crimes associated with criminal groups are the most deleterious for FDI? The theory section mentioned extreme and visible crimes such as narco-roadblocks, as well as predatory crimes like extortion. Analysis of these specific crimes would be interesting for shedding light on precise causal mechanisms. Data on some specific crimes, such as extortion or kidnapping, is often unreliable, at least in Mexico (e.g., Barrera González 2019). However, analysis of countries where crime data is more reliable would be a helpful contribution.

Third, beyond FDI, what other economic phenomena might organized crime affect? Previous work has looked, for example, at how crime affects firm performance (Gaviria 2002), domestic investment (Camacho and Rodriguez 2012, Singh 2012), and economic growth (Detotto and Otranto 2010). How does organized crime affect these outcomes? Given the predatory nature of organized crime as discussed earlier, it seems likely that organized crime would affect domestic firms, both in terms of their closure/exit and investment. However, it might be more difficult to identify a direct relationship between criminal groups and economic growth more broadly. Multi-stage modelling could be helpful in this regard. Regardless, the data introduced in this paper can contribute to additional research on consequences of organized crime. Overall, the finding that increasing numbers of criminal groups seems to deter foreign investment suggests important implications for theory and policy, and lays a foundation for substantial future research as well.

Supplemental Material

Supplemental Material - Organized Crime and Foreign Direct Investment: Evidence From Criminal Groups in Mexico

Supplemental Material for Organized Crime and Foreign Direct Investment: Evidence From Criminal Groups in Mexico by Ana Carolina Garriga and Brian J. Phillips in Journal of Conflict Resolution

Supplemental Material

Supplemental Material - Organized Crime and Foreign Direct Investment: Evidence From Criminal Groups in Mexico

Supplemental Material for Organized Crime and Foreign Direct Investment: Evidence From Criminal Groups in Mexico by Ana Carolina Garriga and Brian J. Phillips in Journal of Conflict Resolution

Footnotes

Author’s Note

Previous versions of this paper were presented at APSA, ISA-FLACSO, and REPAL annual meetings, and at CIDE.

Acknowledgements

We thank Pablo Pinto for comments. We also thank Karina Aguilera Romo, David Blanc Murguía, José Miguel Olvera Puentes, Manuel Pérez Aguirre, and Giovanna Rodríguez García for research assistance. Replication data will be available at the authors’ websites.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.