Abstract

Drawing on interviews with 27 professional investors and proceeding from a resource dependence theoretical lens, this study investigates how professional investors perceive the effectiveness of mandated approaches to increasing board independence in achieving intended governance goals in the Nigerian banking sector. We inductively identify three distinct effectiveness categories for board independence approaches: quixotic, symbolic, and practical. We further unpack seven contextual factors that influence these perceptions, namely person-specific utility; board cronyism; loss of independence over time; disconnection with business realities despite their technical competence; non-executive directors’ (NEDs’) concern for business survival; NEDs’ subservience to the major shareholder; and NEDs’ reputational standing. We provide insights that demonstrate that the mandated approaches to increasing board independence are not universally effective in achieving intended governance goals and must instead be evaluated within their institutional and contextual realities.

Introduction

Board independence refers to the extent to which a company's board of directors comprises independent, non-executive members who are not involved in the day-to-day management of the company and have no significant relationships with the company that could impair their objectivity (Solomon, 2020). On this basis, corporate governance codes across many countries embed approaches intended to increase board independence, and recent studies continue to examine their effects (Bertoni et al., 2023; Crespí-Cladera & Pascual-Fuster, 2014; Neville et al., 2018). In sensitive and highly regulated sectors such as banking, regulators prescribe specific board independence arrangements (e.g., CEO–Chair separation, the presence of independent directors and a non-executive director (NED) majority), and in some jurisdictions, mandate compliance (Neville et al., 2018; Van den Berghe & Baelden, 2005). Yet, whether ‘more independence’ benefits firms remains contested (Bertoni et al., 2023; Krause & Bruton, 2014), and qualitative evidence on how mandated approaches work in practice is limited because their effectiveness hinges on how external resource providers interpret and respond to these arrangements (e.g., conferring regulatory legitimacy and evaluating financing conditions). As directors’ substantive independence cannot be taken for granted (Crespí-Cladera & Pascual-Fuster, 2014), a persistent gap remains in understanding when and why mandated approaches to increasing board independence deliver the governance outcomes valued by regulators (legitimacy) and by professional investors (financing conditions and investability) (Black et al., 2017; Daily et al., 1999; Sur, 2014; Yu, 2023).

Prior empirical work reports mixed results on the instrumentality of board independence. Some studies associate mandated approaches to increasing board independence with reduced misconduct and litigation (e.g., Cumming et al., 2015; Shi et al., 2016), while others question its utility or feasibility (e.g., Cloke, 2009; Hambrick et al., 2015). One explanation for these mixed findings lies in how boards manage external dependencies, a challenge for all sectors (Hillman et al., 2009), but especially acute in banking, where boards contend with two powerful constituencies: regulators (focused on legitimacy, credible oversight, and compliance) and professional investors 1 (driven by financial returns) (Caprio et al., 2007; de Haan & Vlahu, 2016; Laeven & Levine, 2009; Macey & O’Hara, 2003; Mehran et al., 2011). Treating the effectiveness of mandated approaches to increasing board independence as if it were the same for regulators and investors can obscure situations where these approaches deliver regulatory legitimacy without affecting investors’ assessments and vice versa (Aluchna & Kuszewski, 2020). These tensions are likely to be pronounced in weak institutional environments, where the distance between formal codes and boardroom realities is widest and policy–practice decoupling is common (Ahunwan, 2003; Nakpodia et al., 2021). Countries characterised by weak institutions typically face poor regulatory quality, corruption, and low government effectiveness (Kaufmann et al., 2008), increasing the likelihood that prescribed mechanisms fail to deliver their intended outcomes in practice (Bednar et al., 2015). Although mandated approaches to increasing board independence are widely posited to mitigate governance problems (Bebchuk & Weisbach, 2010; Cadbury, 1992; Holder-Webb & Sharma, 2010; Uribe-Bohorquez et al., 2018), empirical evidence about which mandated approaches to increasing board independence deliver which outcomes, and under what conditions, remains scarce (Sur, 2014).

We address these gaps by examining Nigeria's banking sector. The Central Bank of Nigeria (CBN) mandates CEO–Chair separation, a minimum number of independent directors, and a majority of NEDs 2 on bank boards (Central Bank of Nigeria, 2018). We define intended governance outcomes as the stakeholder-specific governance benefits that board independence is expected to deliver. For regulators, these outcomes concern conformance with code-mandated independence and the assurance of legitimacy (de Haan & Vlahu, 2016; Macey & O’Hara, 2003; Neville et al., 2018). For professional investors, intended outcomes concern the board's ability to mobilise reputational capital and external expertise to signal credible governance, improve disclosure, and enhance the firm's financing conditions and investability (Caprio et al., 2007; Hillman et al., 2000; Holder-Webb & Sharma, 2010; Laeven & Levine, 2009). Since intended governance outcomes can differ across stakeholders, we evaluate the effectiveness of three mandated approaches to increasing board independence from the perspective of professional investors, focusing on their impact on achieving the intended governance outcomes sought by regulators (legitimacy) and by professional investors (financing conditions and investability). Guided by resource dependence theory (RDT) (Hillman et al., 2009), which emphasises how boards secure critical resources and manage external dependencies, we therefore ask: From the perspective of professional investors, in a weak institutional context, (i)) how do mandated approaches to increasing board independence perform in achieving the intended governance outcomes of delivering regulatory legitimacy and investor-relevant financing conditions? (ii) Why do these approaches diverge across these outcomes?

Drawing on in-depth, semi-structured interviews with 27 Nigerian professional investors, our study makes significant contributions. First, we demonstrate that mandated approaches to increasing board independence are not universally effective in achieving intended governance outcomes. Instead, their effectiveness is contingent on institutional conditions and the stakeholder perspective from which they are assessed. From the viewpoint of professional investors, who tend to be critical of treating independence as an end in itself, the three predominant board independence mechanisms – CEO separation or duality, the presence of independent directors, and a NED majority – are perceived respectively as quixotic, symbolic, and practical, reflecting broader concerns about whether mandated structures deliver tangible investor-relevant outcomes. Second, using a resource dependence lens, we move beyond structural counts of independence to examine how governance practices are interpreted by capital providers in a weak institutional context. This perspective helps explain why the same formal arrangements can satisfy regulators’ expectations of independence (legitimacy) yet differ in their ability to shape investor judgments about monitoring quality, information risk, and access to capital. We demonstrate how professional investors, as a critical external dependency, evaluate the effectiveness of mandated board independence mechanisms in Nigeria's banking sector. Our analysis identifies seven contextual factors shaping these evaluations: person-specific utility; board cronyism; loss of independence over time; disconnection from business realities despite technical competence; NEDs’ concern for business survival; NEDs’ subservience to the major shareholder; and NEDs’ reputational standing. Finally, we highlight the policy and managerial implications. In weak institutional environments, mandated approaches to increasing board independence that deliver tangible outcomes for investors – such as assisting in assessing a firm's viability and competitive advantage – are more attractive than those that primarily achieve symbolic legitimacy. Consequently, we suggest that policymakers broaden the definition of independence to encourage banks to leverage NED majorities. However, such measures should be accompanied by mechanisms that enable these directors to meaningfully influence board decisions, rather than merely serving as formal compliance signals. For example, regulators could enhance committee powers, require disclosure of NED contributions, and ensure qualifications that allow NEDs to exercise influence even when aligned with dominant owners, thereby safeguarding substantive independence and balancing concentrated shareholder control.

The rest of this article is organised as follows. First, we present the review of the relevant literature and theoretical framing underpinning our research inquiry. Thereafter, our methodology is presented, and the findings are discussed. Lastly, the contributions to theory and practice are outlined, and future research and limitations are highlighted.

Literature Review and Theoretical Underpinning

Board Independence and Its Effectiveness in Achieving Governance Outcomes

The literature supposes that board independence serves as one of the primary means to mitigate corporate governance problems (Langevoort, 2001). As a result, many countries have codes of corporate governance that presuppose that different approaches to increasing board independence are effective for the attainment of good corporate governance, and that the involved actors are bound by this rationality (Van den Berghe & Baelden, 2005). However, there are inconsistencies in the previous research in relation to the effectiveness of the different approaches to increasing the board's independence in achieving the expected governance outcomes (Wood et al., 2015). Board independence has been reported in the literature to be negatively associated with securities fraud, financial restatements (Cumming et al., 2015), and securities lawsuits (Shi et al., 2016). Dalton et al. (1999) noted that independent boards broaden the relationships of the company, expand the networks of said companies, increase the company's technical efficiency (Uribe-Bohorquez et al., 2018), and are a critical source of competitive advantage as they provide invaluable resources (Carpenter & Westphal, 2001; Daily & Dalton, 1994; Geletkanycz & Hambrick, 1997).

On the other hand, some scholars (e.g., Hambrick et al., 2015) have questioned the ability of board independence to accomplish much in terms of monitoring internal company activities, with researchers such as Cloke (2009) considering the idea of self-regulation as projecting an ‘economic wonderland’. Others have still questioned the extent to which any given director is truly independent and what conditions must be met to determine one's independence (Veltrop et al., 2018). Most existing studies describe board independence effectiveness in probabilistic terms (Uribe-Bohorquez et al., 2018), while some studies argue that beyond certain thresholds, board independence becomes excessive and can be counter-productive (Bertoni et al., 2023). Therefore, although most board directors view themselves as independent and strategic partners and believe that their independence is important for attracting positive outcomes for the company (Boivie et al., 2021), the literature does not provide unambiguous practical evidence of the effectiveness of mandated approaches to increasing board independence to achieve the intended governance outcomes (Black et al., 2017; Daily et al., 1999; Sur, 2014; Yu, 2023).

These mixed findings suggest that ‘effectiveness’ may not be a universal quality of board independence, but rather contingent upon context and perspective. Boards manage critical stakeholders whose expectations differ (Aluchna & Kuszewski, 2020; Hillman et al., 2009). In banking, two critical stakeholders are regulators and professional investors (de Haan & Vlahu, 2016). Regulators confer legitimacy through visible conformance with code-mandated independence and accountability, while professional investors supply capital and value independence for its potential to reduce information risk and influence financing conditions (Caprio et al., 2007; de Haan & Vlahu, 2016; Holder-Webb & Sharma, 2010; Laeven & Levine, 2009; Macey & O’Hara, 2003; Mehran et al., 2011). Treating the effectiveness of mandated board independence mechanisms as if it were the same for all stakeholders’ risks obscuring these differences and may partly explain the inconsistencies in prior research (Aluchna & Kuszewski, 2020).

Effectiveness of Mandated Approaches to Increasing Board Independence and Professional Investors

According to the literature, approaches to increasing board independence, which includes the absence of CEO duality (Dalton & Dalton, 2011), the presence of more non-executive (or outside directors) than executive (or inside directors) on the board (Hillman et al., 2009), and having independent directors (Hillman et al., 2000) are useful influences on the stakeholders’ perspectives about the company. We discuss the effectiveness of these mandated approaches to increasing board independence from the perspective of professional investors. 3

Board independence is vital for the professional investors’ investment decision-making (McKinsey, 2002), partially due to institutional pressures (Schnatterly & Johnson, 2013). However, how and why the different mandated approaches to increasing board independence are (in)effective in achieving intended governance outcomes is less understood (Boivie et al., 2021). Board independence, although prescribed as being a good corporate governance driver (Adegbite, 2015), might be illusionary (Cloke, 2009). This is because the environmental constraints encountered by board directors in a given context can result in the decoupling of policy from practice (Nakpodia et al., 2021). Hence, while regulators justify the effectiveness of mandated board independence mechanisms as visible safeguards of legitimacy, their effectiveness for professional investors rests on whether they improve financing conditions through credible monitoring and reduced information risk (Caprio et al., 2007; de Haan & Vlahu, 2016; Laeven & Levine, 2009; Macey & O’Hara, 2003; Mehran et al., 2011). In what follows, we summarise the rationales for each mechanism.

CEO–Chair Separation or Non-CEO Duality

The literature suggests that the absence of CEO/Chairperson duality promotes efficiency (Black & Kim, 2007; Filatotchev et al., 2007). This assumption is based on the notion that when a single individual holds both the CEO and Chairperson positions, they may exert an excessive influence over the company (Ahunwan, 2003; Kisfalvi & Pitcher, 2003). From this perspective, CEO duality can lead to adverse outcomes, such as a decline in a firm’s earnings quality (Alves, 2023). Consequently, the separation of these roles, or non-CEO duality, has been conceptualised as a strategy to enhance board independence (Dalton & Dalton, 2011), a practice that is generally perceived favourably by stakeholders (Rodriguez-Dominguez et al., 2009). However, the empirical research has not always supported non-CEO duality as the gospel for board independence (Lewellyn & Fainshmidt, 2017; Yu, 2023). Yu (2023) conducted a systematic review of 314 studies on the CEO duality–performance relationship, showing that the research findings are mixed due to different company performance measurements, research designs, sampling practices and approaches to dealing with endogeneity issues. The mixed results in the literature make it even more complex to ascertain the effectiveness of non-CEO duality to deliver stakeholder-specific intended governance outcomes. This suggests that the effectiveness or otherwise of non-CEO duality is reinforced or compensated for by other types of power and discretion arising from the context in which the CEO is embedded (Lewellyn & Fainshmidt, 2017). Despite this ambiguity, the theoretical expectations are that non-CEO duality is instrumental in relation to positive governance outcomes for stakeholders, as some evidence suggests that ‘boards use the separate board leadership structure as a substitute for other governance mechanisms’ (Krause et al., 2014, p. 277). However, the perception of professional investors on the effectiveness of non-CEO duality in achieving its stakeholder-specific intended governance outcomes remains undocumented in the literature (Wang et al., 2019).

Independent Directors

Some countries (e.g., the USA and Nigeria) have mandated that boards have government-imposed independent directors as members (Neville et al., 2018). The argument is that the absence of governmental direction encourages certain shareholder abuses commonly attributed to the separation of ownership and control in large corporations (Adegbite, 2012; Eisenberg, 1976; Rodriguez-Dominguez et al., 2009). Consequently, corporate governance reformers proposed a more activist governmental role in mandating the high ethical standards of board practice (Adegbite, 2012). The government assumes this more active role by ensuring that at least some directors are chosen based on their ability to ratify managerial decisions, monitor strategy implementation, and mete out rewards and penalties based on managerial performance. However, some studies (e.g., Garg, 2007; Mishra, 2023) on the role of independent directors have shown that having board independence (proxied by the presence of independent directors) does not guarantee improved positive outcomes due to the poor monitoring roles of independent directors. Independent directors may be adversely influenced by the dominant politically-connected person on the board (Chen et al., 2023). There is the possibility that independent directors can negatively affect a company's performance (Mishra, 2023). Yet, the convention is that the presence of independent directors will make the board independent and less prone to misconduct (Alves, 2023; Neville et al., 2018; Rodriguez-Dominguez et al., 2009). Uribe-Bohorquez et al. (2018) argue that the effectiveness of independent directors is greater when companies operate in countries with a greater extent of law and enforcement. Given the lack of clarity, especially from the perspective of external stakeholders, we argue that the effectiveness of independent directors in achieving stakeholder-specific governance outcomes in a weak institutional country requires a contextual, retrospective understanding.

Presence of Majority NEDs

NED refers to an individual who is appointed to the board of a company to be responsible as part of the board for the success of the company, but does not have executive responsibilities within the company and is not an employee of said company (Tricker, 2015). Awan (2012), Baranchuk and Dybvig (2009), and Dehaene et al. (2001) posit that having a majority of NEDs on a board leads to improved performance. The role of NEDs is to provide creative, independent oversight and a constructive challenge to the executive directors (EDs) (Dehaene et al., 2001). It is generally accepted that NEDs make essential contributions to the proper functioning of companies and, more broadly, to the economy as a whole (Boivie et al., 2021).

Some studies (e.g., Klein et al., 2004; MacAvoy & Millstein, 2003) show that the traditional role and overbearing influence of family ownership in the appointment of board members limit the oversight function and independence of NEDs. Boivie et al. (2016) posit that the effectiveness of having more NEDs than EDs is limited because of the other job demands of the NEDs and the norms of deference. In fact, the work of NEDs is inherently paradoxical (Pina e Cunha et al., 2024). As a result, in order to guarantee board independence, Adegbite (2015) proposed that NEDs should come with experience and have a reputation to protect, so they can be instrumental in decision-making outcomes. The effectiveness of NEDs in achieving stakeholder-specific governance outcomes, as viewed by professional investors, is not well documented.

From the arguments above, it is evident that the contextual reality of the effectiveness of board independence mechanisms is often taken for granted. Yet board independence does not operate in a vacuum: its effectiveness depends on how external constituencies interpret and value these governance arrangements. The RDT provides a suitable lens because it conceptualises boards as boundary-spanning bodies that mediate critical external dependencies. This perspective allows us to explain why the same formal independence mechanisms can secure legitimacy from regulators while failing to reassure investors about monitoring quality, information risk, or access to capital.

RDT Perspective on Board Independence Arrangements

The RDT explains how organisations design and use boundary-spanning structures to secure critical external resources, notably regulatory legitimacy, capital and decision-useful information (Hillman et al., 2009; Pfeffer & Salancik, 1978). In the banking sector, mandated board-independence mechanisms (e.g., CEO–Chair separation, independent directors, NEDs majority) are commonly justified as arrangements through which boards manage dual dependencies on regulators (licensing/oversight) and professional investors (financing) (Hillman et al., 2000; Luoma & Goodstein, 1999; Neville et al., 2018). RDT is, therefore, a premier framework for understanding firm-environmental relations as it supposes that firms critically depend on their stakeholders and the environment for the provision of vital resources and that this dependence is often reciprocal (Drees & Heugens, 2013). RDT supposes that firms must manage their dependencies to survive and maintain autonomy (Drees & Heugens, 2013; Pfeffer & Salancik, 1978). RDT's central premise is that firms cannot be studied in isolation; the flow of resources and the power of external stakeholders shape organisational structures, strategies and decision-making (Drees & Heugens, 2013). In this study, we adopt RDT because it provides a theoretical lens to examine how banks’ governance mechanisms, mandated to manage these dependencies, perform in achieving intended outcomes. In the banking sector, critical dependencies include regulatory legal authorisation and supervision for banks to operate (legitimacy), and professional investors’ monitoring due to the supply of capital (finances) (Drees & Heugens, 2013; Hillman et al., 2009; Pfeffer & Salancik, 1978).

Three elements of the theory are central to our study. First, uncertainty about resource flows compels firms to create boundary-spanning arrangements, including the board of directors, that can reduce dependence and safeguard autonomy (Hillman et al., 2000). Under conditions of high resource concentration and environmental volatility, boards coordinate relationships among internal and external stakeholders, negotiate access to scarce capital and information, and supply the legitimacy that allows the firm to act despite uncertainty (Drees & Heugens, 2013; Pfeffer & Salancik, 1978). In the Nigerian banking context, such uncertainty is acute: licensing power is concentrated in the CBN while investable funds are concentrated among a small pool of professional investors, making the board a pivotal boundary-spanner that must simultaneously pacify regulators and reassure markets.

Second, the composition of a board must match both the type of resource sought and the expectations of the specific providers who control it (Hillman et al., 2009). Regulated industries typically add more NEDs with specialist credentials to signal probity to regulators (Luoma & Goodstein, 1999; Pfeffer & Salancik, 1978), whereas firms seeking diversification appoint business experts or community influencers who can open doors to new funding or markets (Certo et al., 2003; Jones et al., 2008). In our setting, the CBN values directors who embody compliance expertise, while investors favour non-executives whose reputations and networks promise insight and the ability to hold management accountable. This creates a dual and sometimes conflicting set of stakeholder demands that shape both the number and the profile of ‘independent’ seats. Accordingly, banks add non-executives with compliance and control credentials to reassure regulators (legitimacy), whereas investors favour non-executives whose reputations and willingness to challenge improve the company's financial position (Hillman et al., 2009; Luoma & Goodstein, 1999).

Third, the symbolic value of these arrangements (for legitimacy) and their substantive capacity (for control of resources) may diverge, especially in volatile environments. Boards may satisfy formal codes yet fail to curb insider dominance, leading to a gap between policy and practice that external actors quickly detect (Hambrick et al., 2015; Maitlis, 2005). Such decoupling is common in weak institutional environments, where legitimacy requirements are mandated by law, but enforcement is uneven and investors rely on informal cues – such as director reputation – to judge whether independence is real (Klarin & Sharmelly, 2021; Nakpodia et al., 2021; Samdanis & Lee, 2019). Our analysis centres on how professional investors interpret informal cues. This allows us to examine whether mandated structures that satisfy regulators also provide substantive protection for investors’ capital. Where enforcement is uneven, formal adherence can produce legitimacy without shifting investors’ financing judgements; our analysis traces when such decoupling persists and the informal conditions that reverse it.

We adopt RDT because it provides a lens to understand how banks navigate dual dependencies and how mandated board independence mechanisms perform in achieving governance outcomes from the perspective of a critical external stakeholder: professional investors. The RDT principles are particularly very useful for our empirical context. Banks rely on two external players who supply different critical resources: the CBN, which confers regulatory legitimacy, and professional investors, who provide finance. The CBN, therefore, presses for visible indicators of propriety – non-CEO duality, CBN-approved independent directors and a non-executive majority – while investors judge whether those same structures actually curb insider opportunism and protect their capital. Board independence thus becomes a pivotal arrangement through which banks attempt to balance and navigate these dual dependencies, making this setting an ideal testbed for resource-dependence theorising. To gain insights into how to interpret the effectiveness of the mandated approaches to increasing board independence in achieving intended governance outcomes, it is instructive to take into consideration the discrepant thoughts of active socio-economic players, such as professional investors, and to obtain their perceptions on their lived experiences in a particular context (Dogui et al., 2013; Maitlis & Christianson, 2014).

Research Methodology

Mandated Approaches to Increasing Board Independence in the Nigerian Banking Context

Situating our study in the Nigerian banking sector is vital for two main reasons. First, the banking sector is typically the bedrock of any country's economic and social development (King & Levine, 1993). Second, the banking sector is the most active sector in Nigeria, and it mimics the Global North's standards (Abdulkadir, 2012). The nature of today's business world assumes that an independent board of directors is critical to a company's functioning (Neville et al., 2018). Our context is, therefore, apt for this study since the banking sector in Nigeria is regulated by the CBN, and board independence is a compulsory governance requirement. To prevent heavy sanctions, which can include the withdrawal of the banking licence, all banks in Nigeria must always be legally in compliance with the CBN-mandated board independence mechanisms.

As banks occupy a sensitive and important fiduciary role in the economy, the CBN has mandated the separation of the roles of the Chairperson and the CEO. However, many CEOs, upon retirement, become the Chairperson and continue to maintain a strong influence over the bank (Adegbite, 2015). This situation is common, especially as many Nigerian CEOs are the majority (or strong minority) owners of their bank's shares, which enables the easy transmutation of CEOs into the Chairmen of companies (Ahunwan, 2003). In the context of this study, independent directors are non-related directors appointed by the CBN (Adegbite, 2012). The CBN Code of Corporate Governance of 2018 specifically recommends that banks must have a minimum of two independent directors. A CBN circular (2007, p. 1) defines an independent director as ‘a member of the board of directors who has no direct material relationship with the bank or any of its officers, major shareholders, subsidiaries and affiliates; a relationship which may impair the director's ability to make independent judgments or compromise the director's objectivity in line with corporate governance best practices’. In order to improve board independence, the CBN prescribes and mandates that over 50% of the bank board seats must be held by NEDs.

Despite the formal assumptions of increased board independence in the banking sector, in the Nigerian environment, institutions are weak, hence policy–practice decoupling is prevalent (Nakpodia et al., 2021). Thus, the practical dependency obtainable from the mandated approaches to increasing board independence arrangements might be limited. Invariably, the governance mechanisms in Nigeria are copied from developed countries without giving due consideration to the Nigerian context where they are applied (Alhababsah & Yekini, 2021). Hence, our argument is that professional investors are able to parse out any conflicting signals and offer clarity on the effectiveness of the different mandated approaches to increasing board independence to achieve the intended governance outcomes.

We proceeded from the notion that semi-structured interviews with experts can be used to understand idiosyncratic reasoning as it pertains to the Nigerian context. Therefore, our study's use of semi-structured interviews allowed us to gain insights into a phenomenon yet to be fully explored (Gioia et al., 2012). The subjective perceptions of Nigerian professional investors provide a rich and valuable source of information for our research inquiry (Bryman, 2015). All professional investors interviewed are aware of the CBN-mandated approaches to increasing board independence. During the interviews, we clarified relevant terminology and definitions where necessary. Consistent with our theoretical framing, we were careful not to interfere with the interviewees’ reflexive stance (Millo et al., 2023).

Participant Selection

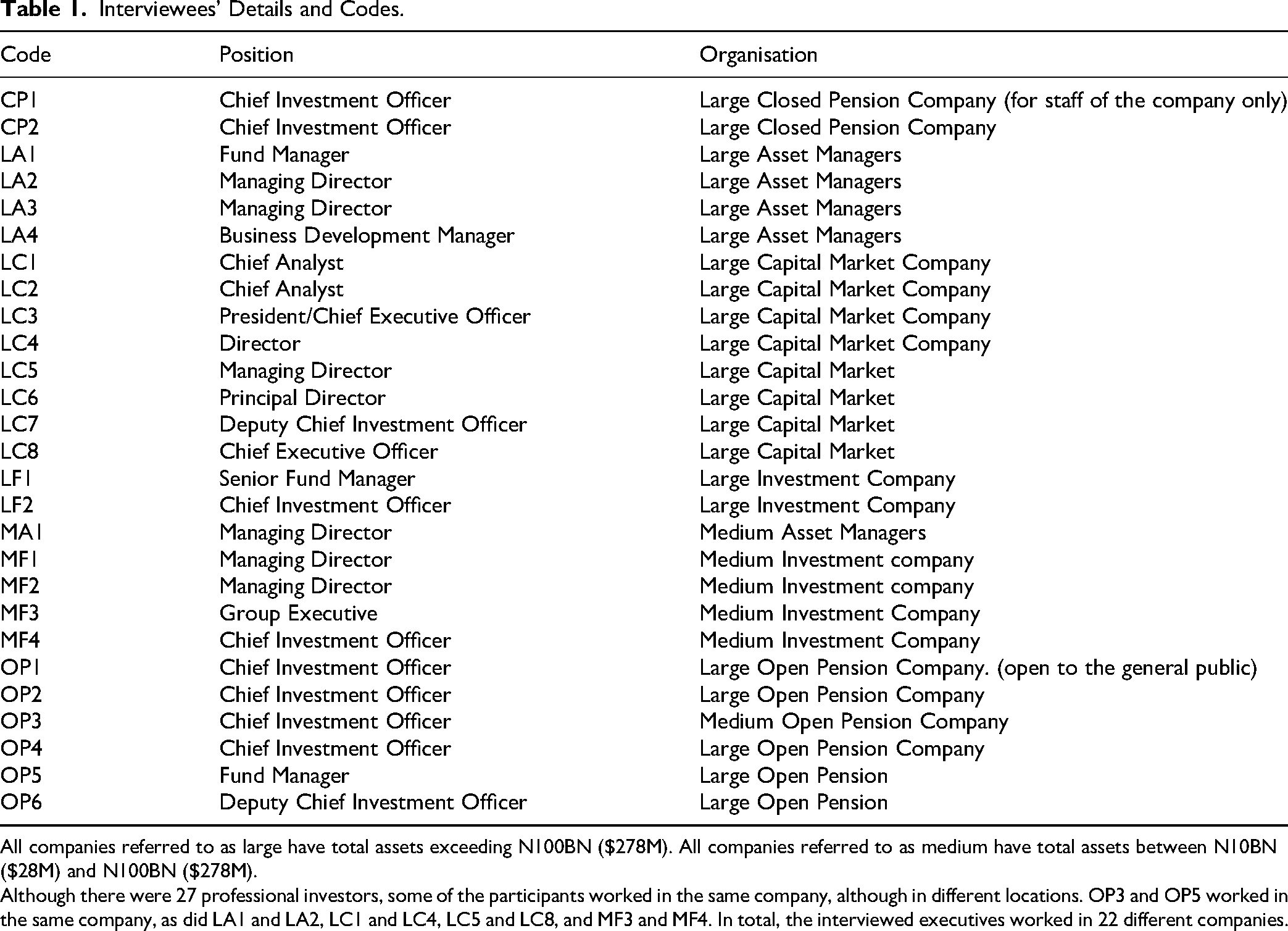

We gained exceptional access to professional investors, including managing directors, chief investment officers, asset managers, and fund managers (see Table 1), from 22 pension funds and asset management companies in Nigeria.

Interviewees’ Details and Codes.

All companies referred to as large have total assets exceeding N100BN ($278M). All companies referred to as medium have total assets between N10BN ($28M) and N100BN ($278M).

Although there were 27 professional investors, some of the participants worked in the same company, although in different locations. OP3 and OP5 worked in the same company, as did LA1 and LA2, LC1 and LC4, LC5 and LC8, and MF3 and MF4. In total, the interviewed executives worked in 22 different companies.

All our interviewees had over fifteen years of investment experience. The enriched data obtained from these knowledgeable experts served as a control mechanism within which the different views were assessed and compared with one another (Adegbite, 2015). The interviewees were contacted via email and telephone calls, outlining the research agenda. After exhausting personal contacts, the snowballing technique proved beneficial in gaining access to these high-calibre respondents (Denscombe, 2010; Stigliani & Ravasi, 2012). The respondents’ biased position (Miller et al., 1997) was minimised by selecting only respondents who satisfied the purposive sampling requirement of competence (Adegbite, 2015; Hughes & Preski, 1997). As a result, 24 face-to-face interviews were initially conducted until saturation 4 in depth and breadth was achieved, but we proceeded with three additional interviews to confirm data consistency. There was a very high degree of agreement amongst the respondents’ comments. All interviews were conducted and recorded in Lagos (Nigeria's financial capital) or Abuja (the national capital).

Data Collection and Analysis

In this study, in-depth semi-structured interviews (see Appendix A for questions) were conducted over a 4-week period between December 2017 and January 2018. This approach, while encouraging two-way communication, also offered us more latitude to ask further questions as a reaction to what is considered to be a significant response. Thus, the information generated from our semi-structured interviews not only provided us with answers but also offered reasons for those answers (Flick, 2014). Each interview lasted an average of 45 minutes. Our interview methodology is consistent with the previous studies on corporate governance drivers (Adegbite, 2015; Ashiru et al., 2023; Cullen & Brennan, 2017; Goyal et al., 2024; Merendino & Sarens, 2020; Nakpodia & Adegbite, 2018).

The recorded interviews were transcribed manually to aid ‘data immersion’ – a process that involves rereading the transcribed text (Bradley et al., 2007). The transcribed interviews were reviewed for completeness, and any errors were corrected. In total, the transcripts generated 337 pages of text. Given the extensive literature on board independence, this research acknowledges the established concepts in the field (Graebner et al., 2012). Building on this foundation, we rely on professional investors’ understanding of the CBN-mandated approaches to increasing board independence. The interview data collected for this study was analysed with the help of the NVivo 11 application package, which allowed for the subjective interpretation of the content of the text data through a systematic classification process of coding and identifying themes or patterns (Hsieh & Shannon, 2005). Unlike conventional content analysis, thematic qualitative analysis is not restricted to frequency counts (Schreier, 2012). As Mayring (2000) suggests, analysis via NVivo 11 provides a medium for exploring core themes. These features, in addition to their considerable link with interpretivist features (see Flick, 2014), were crucial to their adoption in this study.

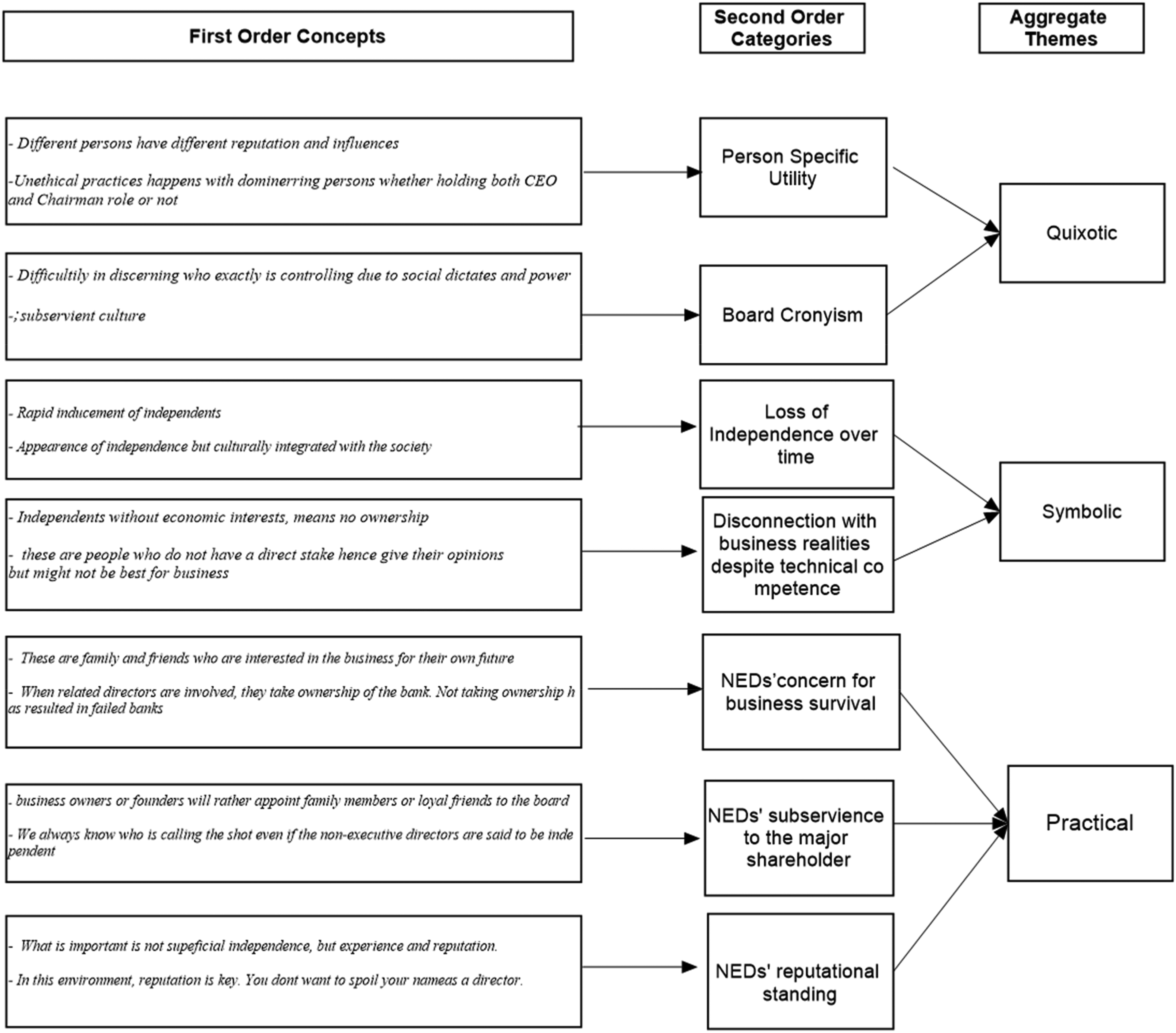

The first stage of our interview data analysis involved generating first-order codes (which are basic concepts that emerge directly from our raw data) followed by second order codes to make sense of the data. This stage ensured that the many words of the transcribed material were classified into much smaller content categories (Weber, 1990). This process generated themes which represent the second order codes, such as corruption prevalence, environmental influences, the passion of the NEDs, willingness to be on the board, and the dominant principal's reputation, as factors influencing the effectiveness of the mandated approaches to increasing board independence in Nigeria. The second stage of our analysis involved the generation of generic categories where the second order codes were grouped under higher order headings (Burnard, 1991). The objective of this stage was to reduce the number of second order codes by collapsing those that are similar or dissimilar into broader higher order categories (Dey, 2003). This second stage was labelled according to our study concepts of interest (Non-CEO Duality, Presence of Independent Directors, and Presence of More NEDs than EDs) and generated second order categories such as loss of independence over time, presence of persons of repute, and person-specific utility. In this stage, we analysed the emerging patterns in our data until adequate conceptual themes emerged (Eisenhardt, 1989). In the final stage, an abstraction procedure was followed to generate an overall description of the research problem (Nakpodia & Adegbite, 2018; Polit & Beck, 2012), which formed the basis of our theorising and the generation of aggregate themes.

Overall, our inductively derived insights were refined using the theoretical insights from the existing literature (Bell et al., 2022). To improve the trustworthiness of our data, the researchers independently reviewed the data coding and the assignment of codes to the respective categories (Campbell et al., 2013). We discussed the codes, meanings and categorisation until an acceptable level of reliability was achieved. Wherever there was disagreement, the categories were modified and intercoder reliability was maximised (Gioia et al., 2010; Krippendorff, 2004). Figure 1 show our coding structure. This article's supplementary file contains further quotes for each aggregate dimension and second order theme. In the following section, we present our findings using anonymised quotes from our interviews.

Coding structure.

Findings

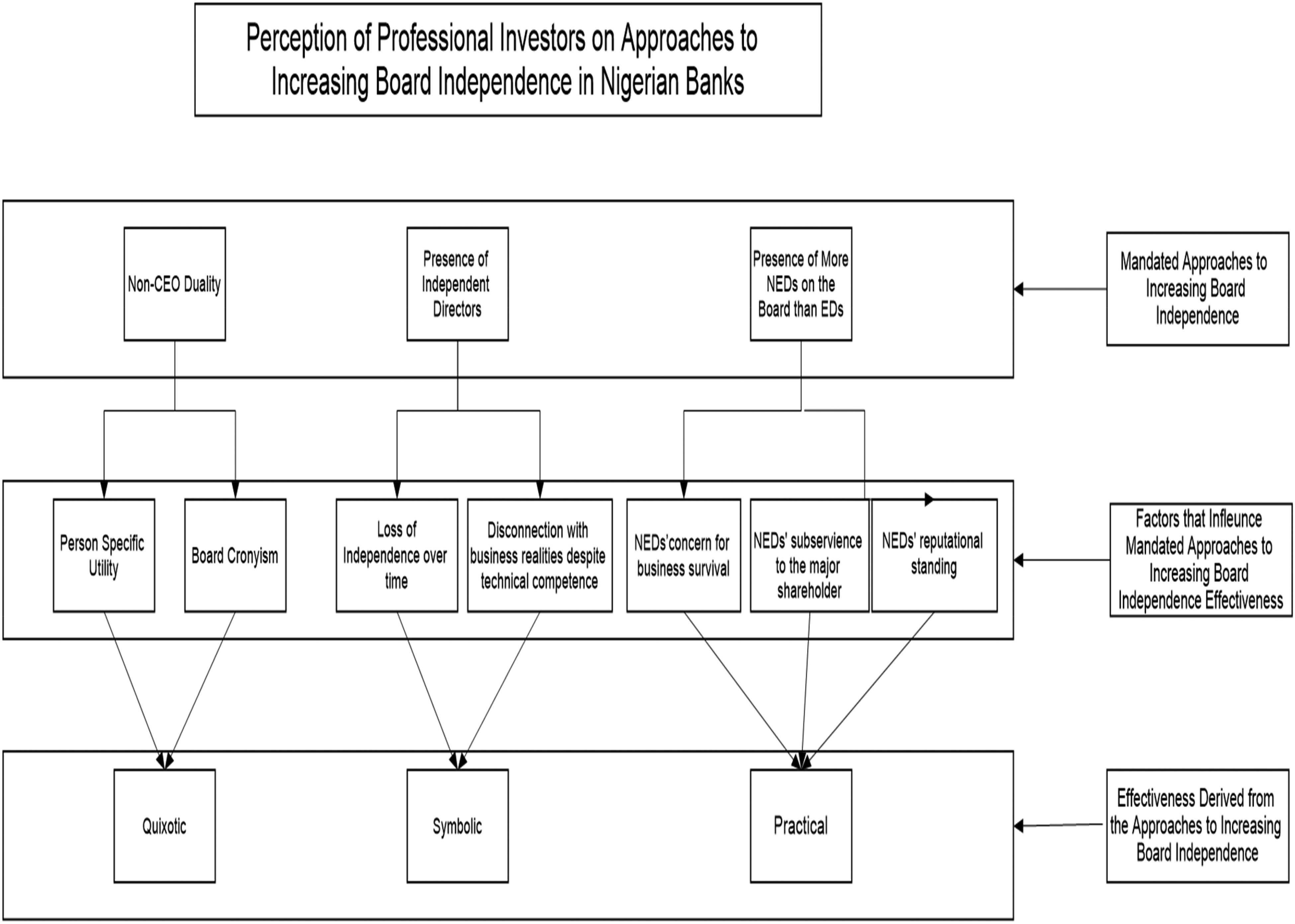

During our interviews, professional investors engaged in discursive constructions of reality to interpret the mandated approaches to increasing board independence and their effectiveness in achieving governance outcomes. In our findings, these interpretations were framed against two distinct sets of stakeholder outcomes: regulatory legitimacy, valued by the CBN, and favourable financing conditions, valued by professional investors. By applying an RDT lens, we moved beyond a superficial acceptance of the CBN's mandated board independence policy. Instead, we drew on professional investors’ interpretations of practice to uncover deeper meanings and situate the mechanisms within their institutional context. This approach is particularly relevant in Nigeria, a weak institutional environment where policy–practice decoupling is prevalent. The RDT lens is especially useful here, as it highlights how interest-driven interpretations by professional investors shape the perceived effectiveness of board independence mechanisms in achieving governance outcomes. Figure 2 shows our concept map.

Concept map.

Professional Investors’ Views on Board Independence

Our interviewees acknowledged that in Nigeria's weak institutional environment, board independence mechanisms can, in certain cases, positively shape how the board operates as a governance mechanism. According to interviewee LC2, (Board independence) to a large extent means that there's high transparency … in terms of how the institution is run with expectations that there is strong alignment between the board and the minority shareholders as well and not too much of a link between the board and management but clearly showing a strong proper representation of minority investors on the on the board of the institution.

Supporting this view of independence, interviewee MA1 highlights that, [an] independent board means that the board has separate thinking, the activities of the board is separate from that of the company. In terms of conflict, the company is trying to ensure that there is no conflict of interest.

Further supporting this view, interviewee LC5 posits that independence means, The situation which will arise that will make the board have a conflict of interest is almost zero. So, that includes any kind – the board members should not have a stake in the company in terms of loans, they should not be suppliers, they should not have anything that can make the managing director (of the bank), or anybody blackmail them, or arm twist them into any unethical decision.

However, some interviewees questioned the concept of board independence. For example, interviewee MA3 wonders if ‘board independence is real or even needed’ (MA3), while interviewee LC8 suggests that ‘board independence is forced upon companies’ (LC8). In the Nigerian environment, where banks are still controlled by dominant individuals, ‘dominant owners might prefer to have their trusted nominated directors since such trusted director will not rock the boat on board’ (LC8). Considering Nigeria's weak institutional environment, where policy–practice decoupling is common, contextual interpretations of the effectiveness of approaches to increasing board independence in achieving the intended governance outcomes become even more necessary. Our interviewees’ critical perspectives demonstrate that mandated independence mechanisms may satisfy regulatory legitimacy requirements without necessarily delivering substantive investor-relevant benefits, emphasising the importance of considering both stakeholder-specific outcomes when evaluating board independence effectiveness. Accordingly, we proceed by identifying the factors that explain the (in)effectiveness of the mandated approaches – CEO duality, the presence of independent directors, and a board composition with more non-executive than EDs – in relation to achieving the intended governance outcomes.

Effectiveness of the Mandated Approaches to Increasing Board Independence to Achieve the Intended Governance Outcomes

Quixotism of Non-CEO Duality

The professional investors’ perception is that non-CEO duality does not assure them that their intended governance outcomes have been achieved in Nigeria. From our data, two factors – i. Person-Specific Utility and ii. Board Cronyism – were identified as being those responsible for the professional investors’ description of non-CEO duality as a quixotic governance arrangement in Nigeria. The quixotism of CEO non-duality refers to the perception that non-CEO duality, while idealistic in principle, is often impractical for achieving professional investors’ intended governance outcomes in the Nigerian context.

Person-Specific Utility. The majority of our interviewees assert that there are ambiguities on the effectiveness of non-CEO duality in achieving the intended governance outcomes in Nigeria. On the one hand, the interviewees suggest that in an ideal world, the spirit behind the non-CEO duality regulation can be deemed reasonable. For example, LC3 and CP1 posit that: Regulation supports that I do not recommend investment in a company that has the MD (Managing Director)/CEO as the Chairperson and I understand the spirit behind this. (This is) because control is definitely weak across the board (if there is CEO duality). Corporate governance is weak. Control is weak and objectivity has been thrown to the bush. (LC3) The presence of such domineering persons (someone holding both CEO and Chairperson roles) in a bank can lead to unethical practices. (CP1)

On the other hand, the interviewees believe that the potency of the non-CEO duality regulation is generally undermined in Nigeria. Interviewee MF1 highlights that: In this (Nigerian) environment, we have seen people who left as MD, who are owner founder of banks, or owner-manager and the situation is not that different. When they leave (retire) as maybe Chairperson or managing director, they still find a way to run the organisation behind the scenes. So, what you see is that underneath they still call the shots, even though they are not managing directors, or they are not a Chairperson. So, typical outgoing managing director that is the owner manager is so powerful that he can sit in the comfort of his home and call the board meeting into this house.

For most of our interviewees, the key consideration is the character and competence of the CEO and Chairman. These qualities can make the non-CEO duality arrangement a potentially effective approach to increasing board independence, supporting both sets of governance outcomes: regulatory legitimacy, valued by the CBN, and favourable financing conditions, valued by professional investors. According to interviewee OP1, In this environment, we (professional investors) know that the CEO is still dominant and usually appoints a chairman he can control. So, the policy is still bypassed. So, what do we look out for … the character of the CEO or Chairman.

Some of the interviewees suggest that CEO duality might be favourable depending on the individual holding both roles. According to interviewee LC5, Whether you like it or not, what I have noticed is that in many cases, I prefer to see that controlling CEO. For example, in XXX Bank, we know that the CEO dominates and, in reality, is the only voice that matters. To be fair, this (dominant voice) is common in many banks. But I like it. He takes ownership of his business. It's important to him. This way, I am also confident to invest.

Our findings suggest that, from the perspective of professional investors, the effectiveness of non-CEO duality is largely contingent on the character, influence, and intentions of key individuals, who are the CEO or Chairperson. In Nigeria, despite regulatory efforts to separate these roles, powerful CEOs often retain informal control, undermining the intended governance outcomes of the regulation.

Board cronyism. Our interviewees agreed that socio-economic disparities (heritage, status, wealth) in Nigeria constrain the benefits of the non-CEO duality regulation. This is primarily due to the significant divide between the elites and the general population, which fosters a phenomenon we refer to as board cronyism. We describe board cronyism as a situation where an individual appointed to a critical position (such as the role of chairperson) by a dominant person (usually the CEO) must operate by permission of the dominant person, as opposed to by right, had the position earned by merit.

In Nigeria, the expectation is that ‘you do not bite the hands that feed you’ (OP2). Thus, this leads to subservience to benefactors, which casts doubts on the effectiveness of non-CEO duality as an approach to increasing board independence which can assist in achieving the intended governance outcomes. Interviewee LF5 posits that if the CEO was influential in the appointment of the Chairman, then the Chairman would be unable to hold the CEO accountable (LF5).

Importantly, our data shows that the institutional weakness in Nigeria supports a situation where non-CEO duality is not necessarily a good outcome. Professional investors argue that, in many instances, there is an existential risk to a company when there is no powerful driving force behind it (LF5). In Nigeria, when the dominant principal makes important decisions, then the business continuity of the company is usually more assured (LF5). Hence, the interviewees believe that in the Nigerian environment, non-CEO duality is more of a game banks play to fulfil regulatory requirements while the bank is still controlled by the dominant shareholder (LC4). Interviewee OP2 describes the situation as follows: …we have seen in Nigeria, a number of CEOs who then became board Chairperson and basically, it's still the same person in charge. In any case, despite not quite being a case of being both CEO and Chairperson at the same time, has from our perspective not impeded the level of transparency and has not brought in a level of conflicts of interest. So, we have had figurehead CEOs essentially and we have had chairmen who appear to be more Chairperson and CEOs at the same time, yet the organisation is thriving.

Overall, professional investors consider non-CEO duality a desirable feature of board design, as it is intended to limit the concentration of power and enhance board independence. However, they note that in practice, it does not always achieve these objectives or support their governance outcomes related to monitoring and protecting capital. Given Nigeria's weak institutional environment, many interviewees view non-CEO duality as challenging to implement effectively and suggest that, under certain circumstances, CEO duality might better align with the operational realities of banks and investors’ monitoring needs.

Symbolic Presence of Independent Directors

Professional investors perceive that in Nigerian banks; the presence of independent directors does not reliably ensure that intended governance outcomes are met. Independent directors are seen as largely symbolic rather than substantive, especially from the perspective of investors focused on governance outcomes related to financing conditions and investability. For example, interviewee MF2 notes: When you have two independent directors, it presupposes that you have two directors that do not have any economic interest in that organisation. Ideally, they are there to ensure that the corporate governance codes are respected and that they are implemented as designed and where they are not being followed or respected, they bring them to the surface and insist that that they must be implemented. The reality is different. (MF2)

Our findings indicate that two key factors contribute to the perception that the regulation of independent directors is merely symbolic, rather than substantive, in increasing board independence to achieve professional investors’ intended governance outcomes: (i) loss of independence over time and (ii) a disconnect from the business realities despite their technical competence. These two factors are discussed below.

Loss of independence over time: According to the interviewees, in Nigeria, independent directors, even though previously unaffiliated with the bank, lose their independence over time because they are swiftly absorbed into the bank's culture and operations. Interviewee LC2 posits that: On paper, independent directors on board look ideal, but so far in the Nigerian example or experience, we (professional investors) have not really seen that differentiated business performance or accountability they inspire. This is because the independent directors are blended into the bank's system quickly.

Interviewees attribute this loss of independence to the corrupt practices in the Nigerian environment where independent directors are quickly induced (through bribes and favours) by the Nigerian banks upon appointment (MF4).

Disconnection with business realities despite their technical competence: According to our interviewees, in situations where the independent directors are only technical, they are disconnected from a lot of business realities and are excluded by core management in business considerations (LC5). Also, the dominance of elites in Nigerian society means that the ability of independent directors to prevent unethical practices by dominant shareholders can be doubtful since these elites are very influential (LA1). According to interviewee OP1, For Nigeria specifically, a lot of times you still have three or four independents that are handpicked and nominated by one person, usually the dominant shareholder in alliance with regulatory officials. It's not really about the number of independent directors but really how they got there, how they are selected, who influenced it?

Nonetheless, most interviewees believe that appointed independent directors can understand technical issues such as accounting, control or auditing and thus might reduce managerial opportunism and stamp out unethical employee behaviour within the organisation (OP1). For instance, interviewee LF2 notes thus, It (the presence of independent directors) gives you more comfort because then you have technical people who do not have a direct stake in the business, and they are happy to give their opinions. They can give you their expert views without holding back. Again, it helps me as an investor because it means that you have people from the outside who can see the company in lights different from how people inside view the company. In terms of sharing feedback with management, they can give feedback, undiluted feedback hundred percent without fear of losing their jobs or anything negatively impacting them.

Our interviewees suggest that the presence of independent directors regulation is only symbolic, as that (presence of independent directors) in itself is not the silver bullet and is not enough reason to make the board independent (CP1) but they (independent directors) are typically very useful in technical aspects of the accountability of banks (LA1).

These findings reveal that the effectiveness of appointing independent directors in order to achieve governance outcomes tends to become symbolic over time in the Nigerian context.

Practicality of NEDs Majority Our data show that professional investors value directors who provide independent strategic insight and resources to the board. According to investors, the CBN requirement that banks have NEDs majority is a practical approach – not necessarily because it increases board independence, but because it supports firm performance and, consequently, investors’ governance outcomes (financing conditions and investability). From our data, three factors – i. NEDs’ concern for business survival, ii. NEDs’ subservience to the major shareholder, and iii. NEDs’ reputational standing – explain why professional investors perceive having more NEDs than EDs as practical for achieving investor-relevant governance outcomes, even if, from their perspective, it may have limited impact on actual board independence.

NEDs’ concern for business survival: The majority of our interviewees agree that the presence of more NEDs than EDs on the board means that there is better management business practice, more strategies and other ideas flowing on the board (OP4). Professional investors argue that the business exigencies in the Nigerian environment demand that the majority shareholder dictates the bank's board composition and appoints loyal people. Interviewee OP4 posits that, There is some management that can wreck your business. Look at the Nigerian business environment, for example, if you set up a business, you put somebody to oversee the business. (Having) somebody who does not have shares in the business and financial risks can wreck you. So, you as the owner acts as control and are supposed to be directly involved or deciding. Ordinarily, in an ideal world, in an ideal situation there should not be this issue, but you know we humans in this part of the world will always have our own selfish interests at heart.

In this context, NEDs contribute independent resources and expertise to the business, but their presence primarily ensures that those aligned with the company's survival (often family or loyal associates of the majority shareholder) remain involved. Consequently, while more NEDs may support board functioning and business performance, they do not necessarily guarantee substantive board independence from majority shareholder influence.

NEDs’ subservience to the major shareholder: From the professional investors’ perspective, many NEDs are loyal and subservient to the major shareholder. This subservience can facilitate quick business decision-making, even if it limits their formal independence. The volatile nature of business in Nigeria means that business owners or founders will rather appoint family members or loyal friends to the board for efficiency (MF1).

Some interviewees note the limitations of having subservient NEDs, particularly when their motivation are for self-interest (MF1, CP1). As interviewee MF1 observes: Some people who are appointed to the board, but who cannot contribute anything meaningful to the business performance. In the first place, their coming to the board is more or less like (the dominant principal saying) oh! I have settled

5

you.

Nevertheless, the majority of our interviewees contend that many NEDs whose interests align with the dominant owner still add value. While they may be loyal to the shareholder, NEDs often hold perspectives that differ from day-to-day management, enabling them to provide useful checks on managerial decisions and mitigate insider opportunism, even if their substantive independence is limited. Interviewee OP1 summarises thus: We want to see more non-executives (because they facilitate business), and we (also) want to see the separation of roles. But we realise that there is a whole lot more grey than black and whites in this market, so we spend a lot of time looking at the grey areas (when considering the effectiveness of approaches to increasing board independence).

NEDs’ reputational standing: Our interviewees suggest answers to questions such as Who are these NEDs? What have they done before? What is their track record? What is the market noise about them? (OP1) determines the value of the NEDs. Professional investors generally perceive Nigerian bank boards’ NEDs as reputable, so the presence of more reputable NEDs serves as a positive signal.

According to interviewee LF1: For an independent board, you expect to have a larger number of non-executive members. So, that is again looking at the numbers in terms of the reputation of the non-executive directors in the composition. So, that to some extent will balance the power and make the board to a large extent (more) independent and strategic.

From investors’ perspectives, a board with more reputable NEDs is valued as a practical mechanism that can support governance outcomes, such as monitoring management and protecting capital, without necessarily increasing substantive board independence. According to interviewee LA1 even though independence is limited in practice, …at least from the perspective of more reputable external directors, it means there is a certain level of independence the board has (in day to day management).

In furtherance of the above, interviewee CP1 posits that: Independence is not really about the form, all right, or the framework. It is really about the substance that you see. But you cannot have the substance without the framework, or we cannot have the substance without the form. So, a few things come to mind. In this environment, I would love to see practical things like strong individuals

6

on the board, especially in the non-executive capacity.

The perspectives of our interviewees are that NEDs with a reputation to protect generally bring different strategic perspectives to a company's board based on (the NEDs’) backgrounds and orientations (OP1).

In sum, while the interviewees suggested that an appropriate proportion of NEDs to EDs can positively influence performance – especially when the directors are ethical and reputable -, they also indicated that this mandated approach does not necessarily mean increased board independence. In our setting, many NEDs are appointed by or aligned with dominant owners, making them independent of day-to-day management but not of the owner, which constrains substantive independence. Accordingly, investors view a NED majority as practical because it can enhance firm attractiveness, even when board independence remains limited. By contrast, this mandated approach is unlikely to achieve the regulators’ intended governance outcomes, such as promoting accountability.

Discussion and Conclusion

In this study, we examine how professional investors perceive mandated approaches to increasing board independence and how these perceptions relate to the achievement of stakeholder-specific governance outcomes – namely, regulatory legitimacy and investor financing conditions and investability. We recognise that investors’ assessments are not neutral, as they are shaped by their own resource interests and can diverge from regulators’ expectations or from abstract ideals of independence. A resource dependence perspective allows us to explain why such stakeholder-specific biases matter, since boards must navigate these competing interpretations in order to secure both legitimacy and access to capital. Accordingly, our research questions are: From the perspective of professional investors, in a weak institutional context, (i) how do mandated approaches to increasing board independence perform in achieving the intended governance outcomes of delivering regulatory legitimacy and investor-relevant financing conditions? (ii) Why do these approaches diverge across these outcomes?

Implications for Theory and Research

We grounded our analysis in RDT (Hillman et al., 2009; Pfeffer & Salancik, 1978), framing mandated approaches to increasing board independence as arrangements through which firms manage external dependencies (access capital and secure legitimacy). This theoretical lens allows us to interpret the professional investors’ perspectives on the (in) effectiveness of these approaches in achieving the stakeholder-specific intended governance outcomes.

On the effectiveness of non-CEO duality, the literature (Adegbite, 2015; Bertoni et al., 2023; Filatotchev et al., 2007) suggests that consolidating the roles of the CEO and the Chairperson into one position amounts to an undue concentration of power in one individual, impinging on board independence. However, in Nigeria, similar to the findings by Pucheta-Martínez and Gallego-Álvarez (2020), some professional investors believe that CEO duality can aid company performance. The perspective of professional investors in Nigeria is that non-CEO duality, while an ideal policy that might have been desirable as an effective board arrangement, is not always practical. In resource dependence terms, person-specific utility and board cronyism frequently render the separation formal rather than substantive: the visible split satisfies regulators and therefore secures legitimacy, but investors do not relax financing constraints because effective monitoring does not improve, and information risk remains elevated. This aligns with the literature (Daily & Dalton, 1994; Holder-Webb & Sharma, 2010; Peng et al., 2007), which suggests that CEO duality (a unity of command) might be effective in complex transition economies where efficiency and speed are the differentiating factors needed for effectiveness and improved performance. However, our findings offer a different perspective to studies such as Alves (2023), which suggest that CEO duality drives negative consequences, including decreased earnings quality. We find that professional investors believe that the effectiveness of non-CEO duality as an approach to increasing board independence is quixotic due to person-specific utility and board cronyism.

On the effectiveness of the presence of independent directors, the professional investors reveal that in Nigeria, independent directors are quickly initiated by management into the routine of ‘how things are done’ within the banking sector. The perspectives of our interviewees are consistent with those of Chen et al. (2023), who assert that over time, independent directors are compromised due to the adverse influences of dominant board members. Thus, while the presence of independent directors assists in holding internal company actors in technical departments (such as control, risk or audit functions) to account, it is more symbolic. Thus, mandatory independent directors requirements may satisfy legitimacy concerns, but they do little to enhance investors’ decision-useful information, since independent directors’ influence is often confined to technical committees rather than strategic oversight. The belief of professional investors is that independent directors bring their expertise to bear in select aspects of the company's transparency (such as the board's audit committee), where they can dispassionately provide some important insights that can benefit external stakeholders. Although this finding corroborates Uribe-Bohorquez et al. (2018) and Alves et al. (2023), who argue that independent directors enhance a company's technical efficiency, our evidence also shows that their loss of independence over time and disconnection from business realities, despite their technical competence, cause them to be regarded as merely symbolic in strengthening board independence.

Finally, our data shows that while having NEDs majority on the board does not necessarily ensure substantive independence, investors regard a NED majority as practical because it can support firm performance and investment attractiveness. Where NEDs are reputable and well connected, boards signal enhanced capacity and benefit from external insight; information flows to investors improve and investability increases, even though owner alignment tempers the autonomy signal and can make legitimacy cues mixed. This corroborates prior research (e.g., Baranchuk & Dybvig, 2009; Dehaene et al., 2001; Libman et al., 2020), which supports the notion that the NEDs majority on a board leads to improved performance. However, our findings diverge from much of the corporate governance literature (e.g., Dalton et al., 1999; Neville et al., 2018) that treats independence primarily as a mechanism of accountability or regulatory legitimacy. In our setting, many NEDs are independent of day-to-day management but aligned with dominant owners. This dual position allows them to check managers while still facilitating decisive action in line with owners’ interests – an arrangement professional investors often value, even though it constrains full board autonomy. Accordingly, investors appraise a NED majority instrumentally for finance (performance/attractiveness), rather than as a route to increased independence or regulator-intended accountability. This is consistent with the inherently paradoxical nature of NEDs’ roles in a weak institutional context (Pina e Cunha et al., 2024). For our interviewees, the experience of NEDs might be more valuable than their independence (Boivie et al., 2021).

Our approach enables us to make three important contributions. First, our research contributes to the debate on the effectiveness of mandated approaches to increasing board independence by offering a more nuanced, context-driven perspective. Prior studies (e.g., Adegbite, 2015; Dalton & Dalton, 2011; Hillman et al., 2000; Neville et al., 2018) have largely assumed that formal governance mechanisms, including CEO non-duality, the presence of independent directors, and a NED majority, enhance board effectiveness and firm legitimacy. However, our findings challenge this assumption by revealing that board independence is not universally effective, but rather highly contingent upon institutional and contextual realities. In response to our first research question, which asks ‘how do mandated approaches to increasing board independence perform in achieving the intended governance outcomes of delivering regulatory legitimacy and investor-relevant financing conditions?’, we provide empirical evidence that formal proxies of board independence, as mandated by regulators, do not always translate into substantive governance effectiveness – particularly in weak institutional environments where compliance mechanisms can be undermined. In unravelling this effectiveness, we classify three mandated approaches to increasing board independence into distinct categories: CEO non-duality is quixotic – though theoretically sound, it is practically ineffective due to entrenched power structures; the presence of independent directors is symbolic – providing a veneer of compliance but failing to ensure substantive oversight as independence erodes over time; and NEDs majority is practical – valued by professional investors because it contributes to business survival and provides strategic resources, even when subservient to major shareholders. By highlighting these distinctions, our study advances the discussion initiated by scholars such as Krause and Bruton (2014) and Bertoni et al. (2023) on mandated board-independence approaches, demonstrating that formal prescriptions alone are insufficient to ensure effective board oversight.

Second, addressing our research question on why these approaches diverge across outcomes, our findings extend the application of RDT by showing that resource dependencies do not translate directly into governance design choices or effectiveness when mechanisms are mandated. Instead, we demonstrate that the practical, symbolic, or quixotic value of board-independence arrangements is contingent on how different dependencies (e.g., regulatory legitimacy and investor capital) interact with weak institutional conditions and stakeholder priorities. In this way, we reframe RDT's broad proposition that organisations design or adopt governance mechanisms to manage interdependence over critical resources. In institutionally weak contexts, mandated governance structures are interpreted and enacted differently by resource providers, so the same arrangements may secure regulatory legitimacy without improving investors’ financing terms or reducing information risk. This is the pattern our findings document for CEO–Chair separation, the presence of independent directors, and a NEDs majority, highlighting the challenge of delivering stakeholder-specific intended governance outcomes.

Drawing on the unique perspective of professional investors, we identified seven informal dynamics, including person-specific utility, board cronyism, loss of independence over time, disconnection from business realities despite technical competence, NEDs’ concern for business survival, subservience to the major shareholder and reputational standing. These dynamics explain how mandated board independence mechanisms translate differently into stakeholder-specific governance outcomes: regulatory legitimacy for regulators versus financing conditions and investability for investors. They do so by determining whether mandated board independence mechanisms operate in substance or merely in form. In the case of CEO–Chair separation, person-specific utility and board cronyism preserve informal insider control, allowing regulators to grant legitimacy but leaving investors unconvinced that monitoring or information risk has improved – hence financing constraints remain. Independent directors, while often losing independence over time, continue to provide technical value in areas such as audit and risk, which sustains legitimacy but does little to enhance capital access or decision-useful information. By contrast, a NED majority can be substantively valuable when reputational NEDs broker external insight and discipline: here, investability improves through better financing conditions, even if concentrated ownership tempers the legitimacy signal. In doing so, we extend the application of RDT in two ways: we demonstrate that the potency of boundary-spanning governance structures hinges on actors’ interpretations of those structures, and we specify context-specific conditions under which ostensibly similar boards vary in their capacity to control external dependencies. Our evidence offers empirically substantiated boundary conditions for RDT in weak institutional settings, clarifying when formal structures secure legitimacy without unlocking capital and why. Crucially, for the board independence literature (e.g., Bertoni et al., 2023; Boivie et al., 2016; Crespí-Cladera & Pascual-Fuster, 2014), our evidence shows that professional investors are not merely assessing independence differently from regulators; they are explicitly critical of treating independence as a governance outcome in itself. They evaluate mandated structures instrumentally: independence matters only insofar as it delivers credible monitoring, decision-useful information, and performance, while simple headcount-based proxies are discounted. From a resource dependence perspective (Drees & Heugens, 2013; Hillman & Dalziel, 2003; Hillman et al., 2009; Pfeffer & Salancik, 1978), this reframes board independence from a universal prescription to a contingent mechanism whose value depends on context and whose interests are at stake, for example, regulators’ legitimacy versus investors’ capital. Accordingly, we argue that governance effectiveness should not be inferred from structural indicators alone but from whether arrangements deliver the outcomes valued by the relevant stakeholders in that context.

Finally, we contribute to the board-independence literature (Crespí-Cladera & Pascual-Fuster, 2014; Neville et al., 2018; Uribe-Bohorquez et al., 2018) by specifying the conditions under which formal indicators, that is, CEO–Chair separation, presence of independent directors, and NEDs majority, do or do not correspond to substantive independence as understood by capital providers in weak institutional settings. Prior work links independence to lower misconduct and better conduct outcomes (Neville et al., 2018) and shows stronger effects where laws and enforcement are robust (Uribe-Bohorquez et al., 2018), but it also documents problems of construct validity and excess independence (Bertoni et al., 2023; Black et al., 2017) and the limits of boards’ monitoring capacity (Boivie et al., 2016). Our evidence explains these mixed findings by showing that the same structures have divergent resource consequences: CEO–Chair separation often delivers regulatory legitimacy without improving financing conditions because person-specific utility and cronyism sustain insider control; independent directors provide technical assurance yet rarely shift strategic oversight as independence erodes; and NEDs majority is practically valuable when reputable NEDs import external ties and insight that investors price as investability, even when alignment with dominant owners tempers formal autonomy.

This resource-centred reading sharpens the independence construct within the literature. Independence must be assessed relative to whose influence is being checked (management versus dominant owners), to its durability over tenure and socialisation (cf. Veltrop et al., 2018), to the provenance of appointments (owner-nominated or regulator-approved), and to whether influence extends beyond audit and risk committees into strategy and CEO evaluation (Boivie et al., 2016; Hillman & Dalziel, 2003). By situating our study in Nigeria, we contribute to the growing body of work on governance in emerging economies (e.g., Adegbite, 2015; Ahunwan, 2003; Ashiru et al., 2025), where institutional weaknesses and policy–practice decoupling undermine the effectiveness of conventional governance prescriptions (Nakpodia et al., 2021). Our study specifies the boundary conditions under which formal rules travel poorly across contexts and identifies contextual indicators and informal dynamics – such as reputational standing and the ability to channel external information into board deliberations – that make NED majorities consequential even when formal autonomy is limited. In doing so, we clarify when board independence mechanisms are likely to be symbolic and when they can be relied upon as evidence of substantive oversight (Crespí-Cladera & Pascual-Fuster, 2014; Neville et al., 2018), depending on stakeholder-specific governance outcomes.

Implications for Policy and Practice

Our study also has implications for corporate governance policy and practice. First, we highlight the inherent tensions in board independence constructs. Managers should be aware that in a weak institutional environment, regulators’ interest is legitimacy whereas professional investors’ interest is finance/performance. Accordingly, professional investors do not value independence as an end in itself; they rather assess mandated approaches to increasing board independence instrumentally, that is, whether they credibly improve monitoring, reduce information risk and support performance and competitive advantage. This implies that some mandated approaches to increasing board independence may raise regulatory legitimacy without advancing investor-valued outcomes and can reduce firm attractiveness when perceived as symbolic (Bertoni et al., 2023). Meanwhile, firms that only symbolically comply with board independence requirements can still secure legitimacy and, in some cases, perform well; however, such compliance does not by itself enhance access to capital. Our findings, therefore, guide investors, domestic and foreign, in Nigeria and similar weak institutional contexts to prioritise the substance of board practices over formal counts when assessing independence.

Second, we draw the attention of regulators to the perceived negligible influence of the imposition of independent directors. Since these imposed independent directors operate in a social context and are influenced by their environment (Scott, 1995), their presence on the boards of banks in Nigeria is perceived as symbolic and creates some measure of bureaucracy and increased transaction costs. Although it is acknowledged that the presence of qualified independent directors is effective for certain board functions, it might be necessary to reduce the tenure they spend on the board to prevent a situation where their independence becomes compromised. Finally, our findings indicate that the regulatory definition of board independence may benefit from reconsideration to account for the ways professional investors perceive board effectiveness. While our data show that investors value NEDs majority for their contributions to firm performance and strategic oversight, we do not assume that their preferences should be directly adopted as policy. Rather, our analysis highlights that simply increasing NED numbers does not guarantee substantive independence. Broadening the NED majority could, in principle, help align regulatory governance outcomes (e.g., compliance and ethics) with investor-relevant outcomes (e.g., assessment of firm viability and competitive advantage). Any such consideration should be accompanied by mechanisms that enable NEDs to meaningfully influence board decisions, such as strengthened committee powers, enhanced disclosure of contributions, and ensuring NEDs have qualifications for effective oversight – even when aligned with dominant owners. These suggestions are intended as insights derived from our analysis and should be evaluated critically by policymakers in light of institutional context and governance objectives.

Implications for Future Research and Limitations