Abstract

Income redistribution with an efficiency loss is expected to have a twofold negative effect on support for redistribution, as it lowers egoistic support for redistribution and activates efficiency preferences. This study tests whether such a negative relationship exists, increases with the size of efficiency loss and interacts with group communication and the income position. We present a laboratory experiment in which subjects receive a randomly allocated income and must coordinate on a majority tax rate using a deliberative communication tool. The rate of money lost as a part of the redistribution process is manipulated as a treatment variable (0%, 5%, 20%, or 60%). Experimental evidence shows that efficiency loss exerts a robust negative effect on support for redistribution. The effect shows a tipping point pattern, is stronger at the lower end of the income distribution and is not fully explained by egoistic preferences. Inefficiency matters mostly for the chosen tax rate after group communication. At an efficiency loss of 60%, however, group communication does not affect support for redistribution, which implies that inefficiencies tend to play a minor role in the context of redistribution as long as they are within a moderate range.

Keywords

Motivation

Among the many factors proposed to explain why growing inequality in a democracy does not lead to increased redistribution (e.g. Alesina and Giuliano, 2011; Scheve and Stasavage, 2016), this study tests the role of efficiency loss. It is well known that transfers of income can be costly in that they can involve substantial efficiency loss. This idea is central to the work of Okun (1975), according to whom society faces an inevitable trade-off between equality and efficiency. Several studies in the wake of Okun’s (1975) “leaky bucket” explored the relationship between the size of inefficiency and acceptance of redistribution (Amiel et al., 1999; Barone and Mocetti, 2011; Krawczyk, 2010; Pirttila and Uusitalo, 2010). Much of this research focused on how individuals decide the trade-off between equality and efficiency but paid little attention to the democratic decision procedure, which is central to Meltzer and Richard (1981, henceforth MR). Experimental studies using the MR model (Agranov and Palfrey, 2015) and simplifications of it (e.g. Durante et al., 2014; Krawczyk, 2010) find that efficiency loss decreases aggregate support for redistribution, but does not account for group communication to reach an agreement on redistribution.

This study contributes to both literature strains by probing deeper on how subjects’ individual preferences and the collectively agreed level of redistribution depend on efficiency losses. Although macro-comparative evidence suggests that societies in which tax authorities are perceived to be inefficient are also less willing to reduce income inequality (Supplemental Appendix Figure 1), we cannot infer from such an observation that inefficient tax authorities are causing less support for redistribution. To identify the causal effect of efficiency loss on voters’ preferences for redistribution, we need to manipulate the actual degree of system inefficiency. Since such manipulations are neither possible nor ethically justifiable in real-world settings, this study utilizes an experimental research design. We develop an experimental design that allows us to analyze whether a negative relationship between efficiency loss and support for redistribution exists. Specifically, this study tests the individual and aggregate effect of different magnitudes of efficiency loss on subjects’ behavior when voting on a redistributive tax rate that generates a lump sum return (linear redistribution game). 1

We hypothesize that efficiency loss has a twofold effect on subjects’ vote choice: It alters subjects’ egoistically preferred tax rate and simultaneously activates their efficiency concerns, which causes them to favor less redistribution. To test these expectations in a group decision context, we collect subjects’ preferred tax rates before a phase of deliberative group communication (ideally preferred tax rate) and their decisions afterward (finally preferred tax rate). Each group votes on a proportional tax rate under majority rule. The treatment variable is the degree of inefficiency represented with 0%, 5%, 20%, or 60% of the tax revenues getting lost. We choose not to specify the cause of inefficiency, as framing such causes (e.g. civil servants’ pay, corruption) could activate preferences beyond system efficiency concerns. To mimic the public deliberation process before an election and in contrast to previous studies that use a single majority vote to determine the collective agreement, this study allows a specific form of group communication. The communication device allows subjects to make a series of tax rate proposals to coordinate the majority tax rate before making a final vote. This experimental design enables us to test the effect of system inefficiency on subjects’ preferred tax rates before and after group communication.

The study proceeds as follows. The following section reviews research regarding efficiency loss in redistribution and presents this studies’ contribution to the literature. Section 3 presents the theoretical framework and derives a set of hypotheses. Section 4 explains the experimental design followed by the presentation of empirical findings in Section 5. The final section concludes and discusses implications for further research.

Efficiency loss and voting on redistribution

Justice research shows that efficiency can be used to justify inequality (Scott et al., 2001: 751). The tension between efficiency and equality is at the center of Okun’s (1975: 55) work, in which societies face an inescapable trade-off between efficiency and equality. According to Okun (1975), there are at least four reasons why redistribution leads to lower aggregate net income, namely administrative cost of the redistribution system, changes in subjects’ work effort due to redistribution, changes in savings and investment behavior due to redistribution, and, finally, changes in voters’ attitudes towards redistribution as a result of redistributive programs (also see Gouyette and Pestieau, 1999). This study only refers to the first type of inefficiency, namely efficiency losses inherent in collecting and redistributing taxes.

The question arises of how much efficiency loss is tolerated before a redistribution program is rejected as a whole. For Okun (1975: 99), it is among the core tasks of democracy to find an agreement on how much leakage in redistribution is acceptable. As shown in survey research (e.g. Pirttila and Uusitalo, 2010) and experimental studies (e.g. Cappelen et al., 2013; Charness and Rabin, 2002; Engelmann and Strobel, 2004; Paetzel et al., 2014), a substantive share of subjects generally prefers an efficient use of resources (Scott et al., 2001: 751). Beckman et al. (2004) conduct a laboratory experiment in the US and China to test the “leaky bucket” argument. They find that the veil of ignorance has a strong effect on accepted efficiency losses. When subjects do not know their income position, leakages of 50% are rejected in three out of four cases. When the individual income is known, however, the acceptance of higher leakage rises drastically. Barone and Mocetti (2011) examine the effect of a “leaky bucket” on subjects’ tax morale—measured as an attitude towards paying taxes. They find that public spending inefficiency has a strong negative effect on citizens’ tax morale as taxpayers punish the state via tax evasion if it fails to redistribute resources efficiently (Barone and Mocetti 2011: 6).

Durante et al. (2014) and Krawczyk (2010) are most closely related to this study. Krawczyk (2010) designed a lab experiment in which he also directly manipulates the efficiency of a redistributive system that is based on a linear tax rate returning a lump sum. There is either no inefficiency or an efficiency loss of 30%. Using a very different experimental design in which participants chose different tax rates in four scenarios that could affect their own and others’ payoffs, Durante et al. (2014) distinguish between treatment conditions with no inefficiency, an efficiency loss of 12.5% or 25%. Krawczyk (2010: 135–136) finds transfer choices were significantly lower in the treatment conditions with a 30% efficiency loss. Durante et al. (2014: 135–136) find that while the average tax rate is similar in sessions with an efficiency loss of 0% and 12.5%, subjects chose significantly lower tax rates in sessions in which redistribution is associated with a 25% loss in tax revenue.

Despite the shared interest in how inefficiency affects preferences for redistribution, many of our study’s experimental design choices are subtly different from previous research. First, while Krawczyk (2010) used only a single measure of efficiency loss (30%) but varies subjects’ endowment (random vs real-effort), this study keeps subjects’ endowments exogenous but varies the size of efficiency losses (5%, 20%, or 60%). Moreover, there is robust evidence showing that voting behind the veil of ignorance, as implemented in Krawczyk (2010), elicits decisions closer to subjects’ fairness preferences than decisions after lifting the veil (Nicklisch and Paetzel, 2020). We elicit preferences for redistribution exclusively after getting the information of their own income and the income distribution in their group. In this respect, our study tests whether previous experimental results on the effect of efficiency loss on support for redistribution are still robust in alternative design choices.

Second, this study’s voting procedure is different from previous research (e.g. Krawczyk 2010 uses a random selection of one vote; Barber et al. 2013; Durante et al. 2014; Esarey et al. 2012a, 2012b, use the median vote). A key difference concerns the communication device that enables groups to coordinate on a majority tax rate before making a final vote. In democratic societies, voters’ decision for or against redistribution is preceded by a phase of deliberation and coalition formation. The group communication stage captures an essential aspect of the political decision-making process. Research in political science has a long history of analyzing the importance of deliberation (e.g. Gutmann and Thompson, 1998; Hole, 2011; Landwehr, 2010) and coalition dynamics (Iversen and Soskice, 2006) in redistribution contexts. 2 From a theoretical perspective, group communication can have a twofold effect on voting for redistribution (e.g. Sauermann, 2020). First, it enables coalitions to arrange a common voting strategy and agree on distributing benefits among their members. Second, it strengthens prosocial orientations and fairness in groups (Bicchieri, 2002; Ostrom, 1998; Sally, 1995). In contrast to previous research, which compares treatments with and without group communication, we identify group communication’s effect on support for redistributive taxation by measuring subjects’ preferred tax rate before and after group communication, with and without efficiency loss.

Third, for the theoretical reason outlined above, the technical implementation of group communication deviates from previous research, which relies, for example, on a chat-box function. Our group communication tool restricts the messages participants can send only to contain numbers and is organized in a sequential table format rather than an unstructured chat protocol. These restrictions have been chosen to enable coordination on the exact same tax rate but avoiding any loaded language that can emerge from open chat-based communication. Individual factors, such as the ability to use moralizing or emotionalizing language, can be problematic in open chat-based communication, while at the same time, coordination on the exact same tax rate is more demanding if communication is unrestricted. This study’s deliberative communication tool is highly structured as each group member has to enter a number (tax rate) 10 times. In the last step of the sequential communication process, most group members should have agreed on a coalition and then make their final decision. The operationalization of the deliberative communication tool will be explained in more detail in the next section. 3 Measuring subjects’ preferred tax rate before (ideal tax rate) and after group communication (final tax rate), enables us to identify whether group communication alters the effect of the leak size on support for redistribution.

Fourth, another branch of the literature analyzes whether and to what extent the source of inequality impacts the acceptance of redistribution (Cappelen et al., 2013; Liebe and Tutic, 2010). Conducing a large-scale social preference experiment among Americans and Norwegians, Almås et al. (2020) show that costly redistribution is more accepted if inequality is based on luck instead of productivity differences. Besides that critical finding, Almås et al. (2020) also show that if inequality is based on luck, efficiency considerations play a minor role in explaining inequality acceptance. Hence, efficiency considerations appear to be less critical than fairness considerations in the context of redistribution. This study enables us to test whether inefficiency suppresses the effect of group communication, which is believed to activate fairness consideration, in the context of redistribution.

Theoretical framework and hypotheses

Egoistic preferences

Before we continue theorizing about the effect of efficiency loss on subjects’ preferences for redistribution, we present the linear redistribution mechanism borrowed from the MR model and explain how an efficiency loss is implemented in this mechanism. The redistribution mechanism consists of a proportional tax rate that is imposed on all incomes. The tax revenue is distributed in equal shares among all group members. Depending on the size of the tax rate, this mechanism redistributes income from those with gross incomes above the mean toward those with gross incomes below the mean. The single-dimensional conflict over the size of the proportional rate is decided through majority rule. Under the premise of fully rational and egoistic agents, the group member with the median gross income is pivotal. The redistribution mechanism for N individuals with gross incomes x1,. . ., xN can be defined as:

where yi is the net income of individual i under tax rate τ. The average gross income is denoted

Individuals with a gross income above mean income after redistribution through the leaky bucket (xi > (1−λ)

Efficiency concerns

Human behavior is rarely exclusively guided by egoistic preferences. When deciding upon redistributive taxation, subjects’ vote choice tends to depend on multiple, even conflicting motives, including fairness (Almås et al., 2020; Cappelen et al., 2013; Nicklisch and Paetzel, 2020), social identity (Klor and Shayo, 2010; Paetzel and Sausgruber, 2018), inequality aversion (Tyran and Sausgruber, 2006) and the framing of the vote choice (Lorenz et al., 2017; Paetzel et al., 2018). Laboratory research on the MR model (Agranov and Palfrey, 2015) and simplifications of it (e.g. Barber et al., 2013; Esarey et al., 2012a, 2012b) also suggest that egoistic preferences do not fully determine subjects’ behavior. Subjects tend to eschew voting for extreme net income distributions, as τ = 0% and τ = 100% hardly occur. Instead, subjects with a gross income above

Avoidance of efficiency loss may provide another explanation for why support for redistribution falls below egoistically expected levels. Introducing an efficiency loss to the redistribution mechanism (represented by λ) is expected to decrease support for redistribution for two reasons. First, under the premises of subjects having egoistic preferences, efficiency loss involved in the redistribution mechanisms decreases support for redistribution. For each magnitude of efficiency loss, we can determine a corresponding egoistically preferred tax rate (see Figure 1). Second, if subjects have genuine efficiency concerns, they are predicted to prefer less redistribution when redistribution comes with an efficiency loss. Contrary to the egoistic prediction, there is no need to presume a strict proportional relationship between the size of fiscal leakage and a consequent reduction in preferred taxation if we presume that subjects voting behavior is affected by their efficiency preference.

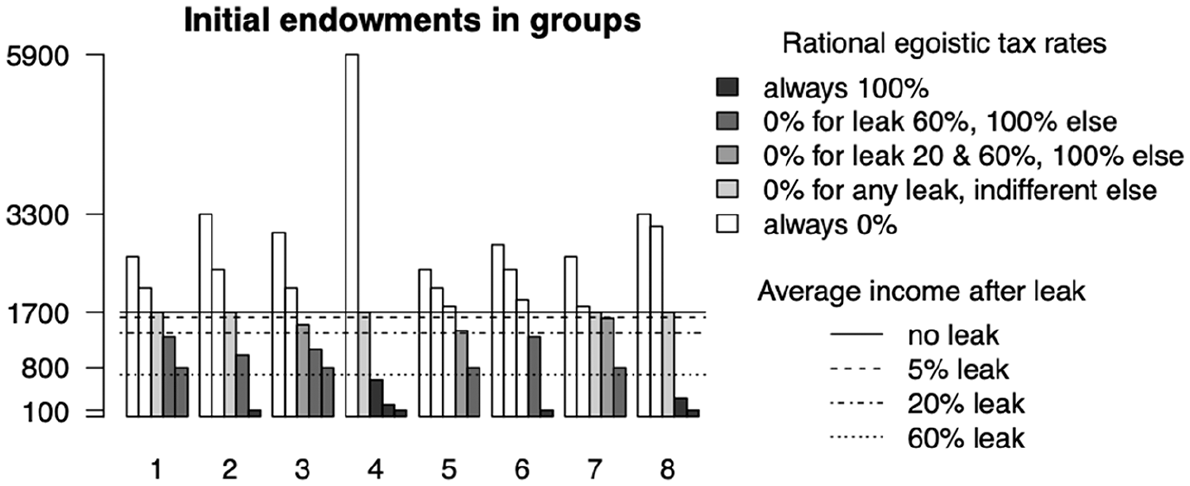

Distributions of endowments. The x-axis represents eight different gross income distributions (D1–D8). The horizontal lines show the average income after redistribution with a “leaky bucket.”

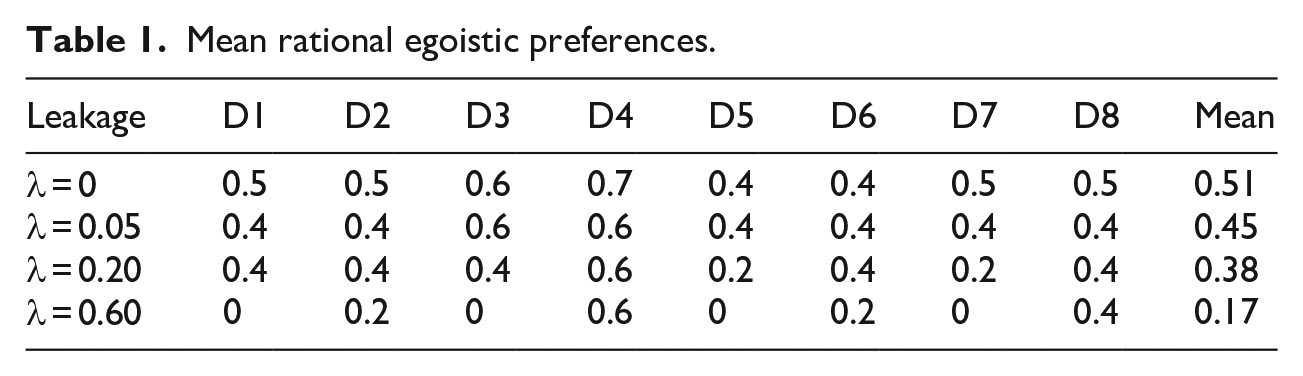

Previous research by, for example, Cappelen et al. (2013), Charness and Rabin (2002), or Almås et al. (2020) integrated efficiency preferences into subjects’ utility function. Regardless of their specific focus and modeling choices, these models predict that if subjects have efficiency preferences and redistribution causes inefficiency, subjects prefers less or no redistribution. Instead of deriving another one-directional prediction, we are interested in analyzing the sensitivity of support for redistribution towards different degrees of inefficiency. Efficiency preferences might matter only if the efficiency loss is above a certain subjectively “accepted” threshold. For that reason, we introduce three different sizes of leakage into the redistribution mechanism; small, λ = 5%, medium, λ = 20%, and large λ = 60%. The values for λ are, to some extent, arbitrary (also see Durante et al., 2014; Krawczyk, 2010), yet these values are believed to offer enough range to mimic a small, medium, and large efficiency loss (Beckman et al., 2004). Although based on different microeconomic assumptions, both efficiency preferences and egoistic preferences suggest a negative effect of efficiency loss on support for redistribution.

Furthermore, the effect of efficiency loss on support for redistribution is expected to depend on subjects’ income position. Egoistic subjects with a gross income above (1−λ)

A matter of particular relevance for assessing the merits of democracy refers to whether the effect of system inefficiency on subjects’ vote choice, as summarized in H2 and H3, disappears in the political decision-making process or whether it persists and thereby affects the collectively agreed tax rate. Like economists who believe that interactions in markets will correct individual irrationality (e.g. Fehr and Tyran, 2005), political scientists tend to show an implicit hope that deliberation could make collective agreements less vulnerable towards individual bias and vested interest. The “wisdom of crowds” literature, for example, suggests that social groups can be remarkably knowledgeable when their average decisions are compared with the decisions of individuals (Surowiecki, 2005). However, Lorenz et al. (2011) show that a “social influence effect” diminishes the diversity of the crowd without improvements of its collective error, leading to a state of herd irrationality. Such a “bandwagon” effect is also known from experimental voting literature in economics (e.g. Tyran, 2004). It remains an open empirical question of how group communication affects subjects’ efficiency preferences and their egoistic preferences in voting on redistribution. Communication can create and maintain a coalition that imposes a tax rate that is most beneficial for its members, while at the same time, it can strengthen fairness within groups. Assuming the latter, and there is some experimental evidence to do so (see Sauermann, 2020 for review), group communication could activate preferences that suppress efficiency loss’ negative effect on support for redistribution.

Experimental design and procedures

Building on previous experimental work on the redistribution mechanism outlined above (e.g. Barber et al., 2013; Esarey et al., 2012a, 2012b), we use the redistribution mechanism of equation (2) to test the impact of a “leaky bucket” with different degrees of inefficiency in a laboratory democracy.

Experimental vehicle

In each of the eight rounds, subjects were randomly assigned into groups of five. In each round, subjects received endowments from the pre-specified distributions D1–D8 as displayed in Figure 1 via a random assignment. Figure 1 presents the eight distributions. For each of the eight distributions, the individual gross incomes of the five group members are displayed. The sequence of the eight distributions was randomized only once for all sessions to allow comparability between treatments. Each distribution has an average endowment of

Mean rational egoistic preferences.

The laboratory experiment was conducted with z-tree Fischbacher (2007) and consisted of the following stages:

(1) Information about endowments and individually preferred tax rate: Subjects were informed about their endowment and the endowment of all other group members. In this stage, subjects were privately asked to enter their ideally preferred tax rate. The upper part of Supplemental Appendix Figure 2 presents a screenshot of the ideal tax rate elicitation. In this non-incentivized decision, strategic concerns should play no role. In fact, we argue that a not monetarily incentivized decision is appropriate to elicit what subjects think is their ideal level of redistribution (Gaertner and Schokkaert, 2012; Konow, 2003). We analyze both subjects’ none-incentivized decision (ideally preferred tax rate) and the tax rate (finally preferred tax rate) that is used to determine the collective decision and subjects’ payoffs.

(2) Group communication stage: The upper part of Supplemental Appendix Figure 2 presents a screenshot of the communication stage. Each subject had to make ten proposals which appeared in a five-column table visible to all group members. The first proposals appeared in the table after the last group member confirmed their proposal. All other proposals appeared in real-time after confirmation by the specific subject. The tax rates that subjects enter during this stage of numerical communication are forwarded to subjects’ group members but have no consequences. Only the tax rate a subject enters in the collective decision stage is used to determine the final group tax rate. The endowments were displayed throughout the whole communication stage. Subjects could only communicate with numbers to coordinate their final decisions. We argue that the communication tool allows members of a society to deliberate and reach an agreement, respectively create majority coalitions before they cast their final vote. Bearing in mind, however, that proposals are not binding.

(3) Collective decision stage: After the tenth proposal, a decision box appeared where subjects had to enter their final decision privately. A group decision was achieved when at least three subjects decided on the same number (majority rule). The net income was then computed using the redistributive mechanism explained in Section 2. If the group failed to reach a collective decision, their income was 50% of the endowment or 850 (50% of the average endowment), whichever was lower. 6

(4) Information payoff: Subjects were informed on the result of the collective decision and their resulting net income from the eight periods at the end of the eighth period. Although subjects are randomly re-matched into groups of five after each period, we choose to present subjects’ net income at the end of the experiment to ensure that there are no carry-over effects like emotions or indirect reciprocity. The payoff in Euros was defined by a subject’s average earnings over eight periods. The exchange rate was: one experimental token = 0.005 Euro.

Experimental procedures

The experiment started with the incentivized social preference elicitation task introduced by Balafoutas et al. (2012) and applied in for example, Paetzel et al. (2014). 7 Then the main experiment started. Subjects played eight different gross income distributions (rounds). After the eighth round, subjects completed a questionnaire consisting of questions on their political attitudes, socio-demographic background (age, gender), and field of study. Subjects’ partisan orientation is measured on a 1 to 10 scale, where 1 represents an extreme right-wing orientation, and 10 represents an extreme left-wing orientation.

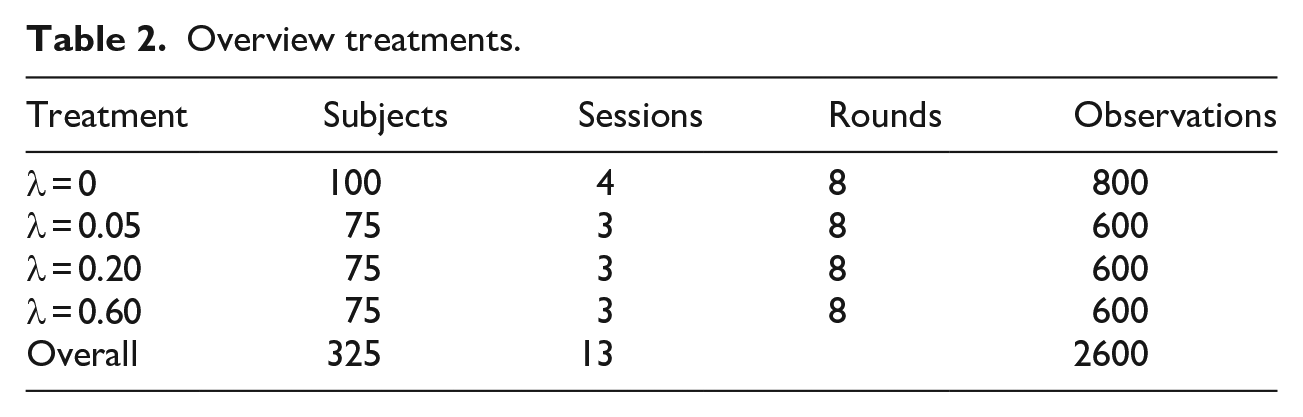

Subjects were recruited from the University of Oldenburg and the University of Hamburg using the software ORSEE (Greiner, 2015) and hroot (Bock et al., 2014). Using a between-subjects design, 100 subjects played the no leakage condition, 75 subjects played the 5% leakage condition, 75 subjects the 20% leakage condition, and another 75 subjects played the 60% leakage condition. With 325 subjects in total and eight rounds per subject, the dataset contains 2 (ideal and final) × 2600 observations. The written instructions can be found in Supplemental Appendix C. Table 2 provides an overview of treatments and observations.

Overview treatments.

Data analysis

Fractional logistic regressions are used to estimate the effect of efficiency loss on the two dependent variables, subjects’ ideally preferred tax rate and subjects’ final vote on the tax rate after group communication. The tax rate is measured on a 0–1 scale. 8 Fractional logistic regressions are particularly suitable for analyzing proportions such as tax rates (Papke and Wooldridge, 1996). We estimate cluster-adjusted standard errors to account for the fact that we have repeated observations for our 325 subjects. 9

Each model includes a set of dummies specifying the leakage’s size (λ = 5%, λ = 20%, or λ = 60%). The no leakage treatment serves as the reference category. Subjects’ egoistic preference is operationalized either categorical or a continuous measure. Models using the categorical measure include two dummy variables accounting for whether subjects should vote for τ = 100% or τ = 0%. The rational prediction “indifferent” serves as the reference category. This categorical operationalization of subjects’ egoistic vote rests on the assumption that subjects decide perfectly rationally when they choose their tax rate and only consider tax rates of 0% or 100%. A more realistic presumption is that participants take into account the relative costs and benefits from redistribution. This is taken into account by our continuous measure of subjects’ egoistic preference. We created a measure of subjects’ relative distance from the groups’ average gross income. Esarey et al. (2012a) have used a similar measure for example. The continuous operationalization of subjects’ egoistic vote is defined as r

Testing the effect of the leak size and the egoistic preferences on subjects’ vote choice before and after group communication has implications for preparing the dataset for the statistical analysis. First, subjects ideally preferred tax rate and their finally preferred tax rate after group communication could be seen as independent vote choices and thus should be analyzed separately. Secondly, the two choices (ideally and finally preferred tax rate) can be set up in a multi-panel dataset, which then includes a dummy variable indicating whether a particular tax rate has been entered before (ideal) or after (final) the group communication stage. This approach has the advantage of testing the direct and conditional effect of group communication in a single model. In the following, we will present estimation results from fractional logistic regressions conducted on a single sample (Table 3) and on separate samples (Table 4). Both approaches provide similar results.

Determinants of subjects’ vote choice.

Fractional logistic regression. Dependent variable: tax rate {0, 0.1, 0.2, . . .,1}. Standard errors in brackets adjusted for 325 subjects.

p < 0.10. **p < 0.05. ***p < 0.01.

Ideally and finally preferred tax rate on split samples.

Fractional logistic regression. Dependent variable: ideally preferred tax rate {0, 0.1, 0.2, . . .,1}. Finally preferred tax rate Standard errors in brackets adjusted for 325 subjects.

p < 0.10. **p < 0.05. ***p < 0.01.

Each model controls for age, gender, subjects’ field of study, and self-reported right-left partisan orientation. Each model includes a dummy variable accounting for subject pool effects, since the experiments were conducted at two laboratories. 10 As part of the robustness analysis, we also controlled for social and efficiency preferences, utilizing the distributional-preferences elicitation from the first part of our experiment. Taking into account these measures does not alter any of the substantive findings presented in the next section.

Empirical results

Basic results

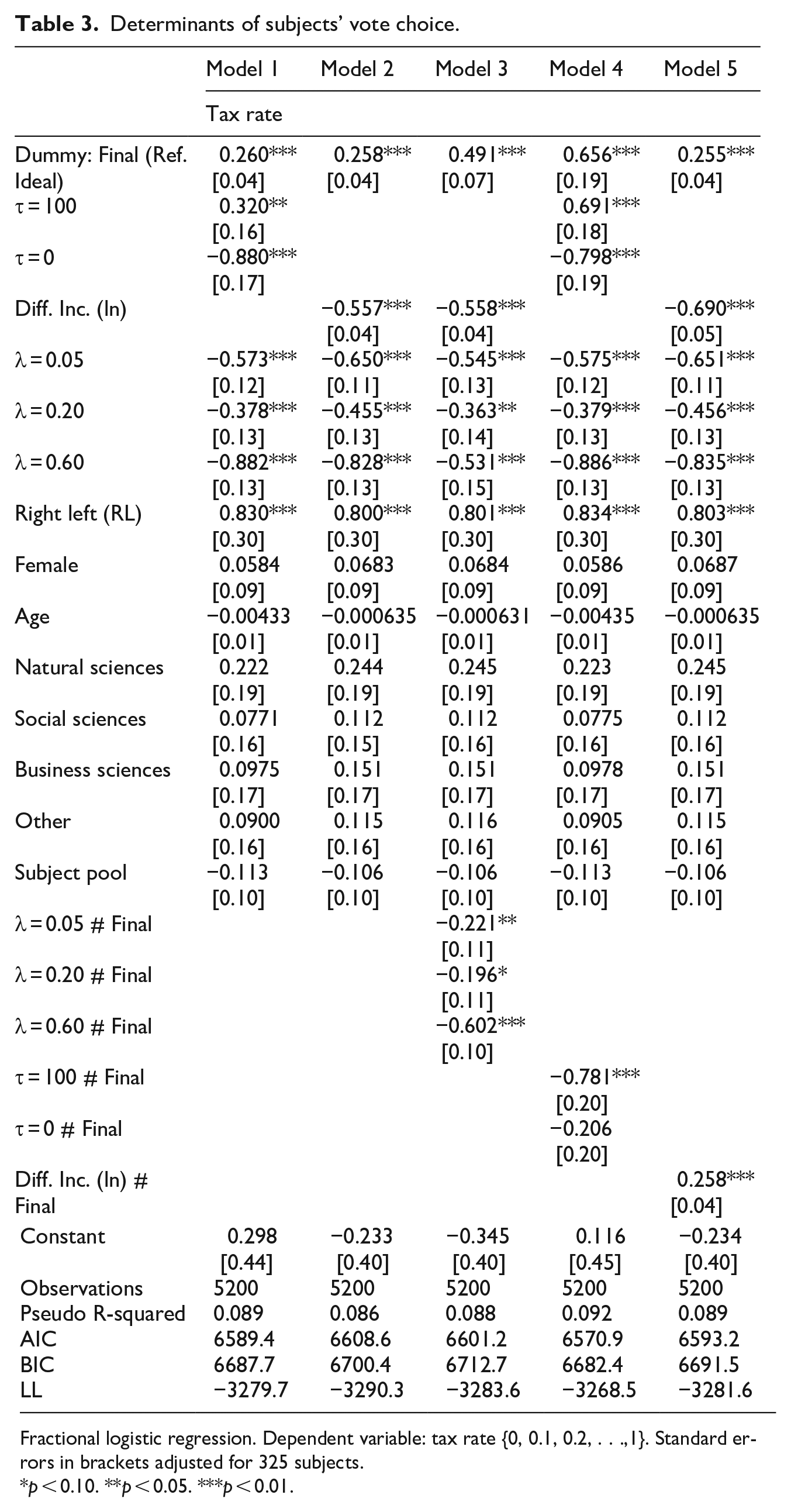

Models 1 and 2 from Table 3 report the direct effect of the egoistic prediction (categorical and continuous measure), the leak size, and the communication stage on subjects’ vote choice. The dummy final indicates subjects finally preferred tax rate. Subjects’ ideally preferred tax rate serves as the reference category. Model 3 includes a set of multiplicative interaction terms between the three leakage dummies (λ = 5%, λ = 20%, or λ = 60%) and the dummy indicating subjects’ final decision to tests whether the group communication stage conditions the effect of the leak size on support for redistribution. Models 4 and 5 include similar interaction terms between the egoistic prediction and the group communication stage to test whether the effect of the egotistic preference on support for redistribution is conditioned by group communication. To ease the interpretation of these regressions, we plot the predictive margins and the average marginal effects in Figures 2 and 3. Using averages from the raw data yields similar results. The predicted effect plots have the advantage of taking into account the effect of control variables and thereby provide a more precise representation of the treatment effect.

Average tax rate by treatment conditions. Based on Model 3 from Table 3.

Findings from Models 1 and 2 in Table 3 show that group communication positively affects redistribution. This means that on average, subjects’ finally preferred tax rate is higher than their ideally preferred tax rate. Second, the set of leakage dummies negatively affects support for redistribution, although in substantive terms, the negative effect for λ = 5% is stronger than for λ = 20%. Third, egoistic preferences matter, regardless of their operationalization. The coefficients for the τ = 100% dummy and τ = 0% dummy show effects in the predicted direction, just like the coefficient for Diff. Inc. (ln)

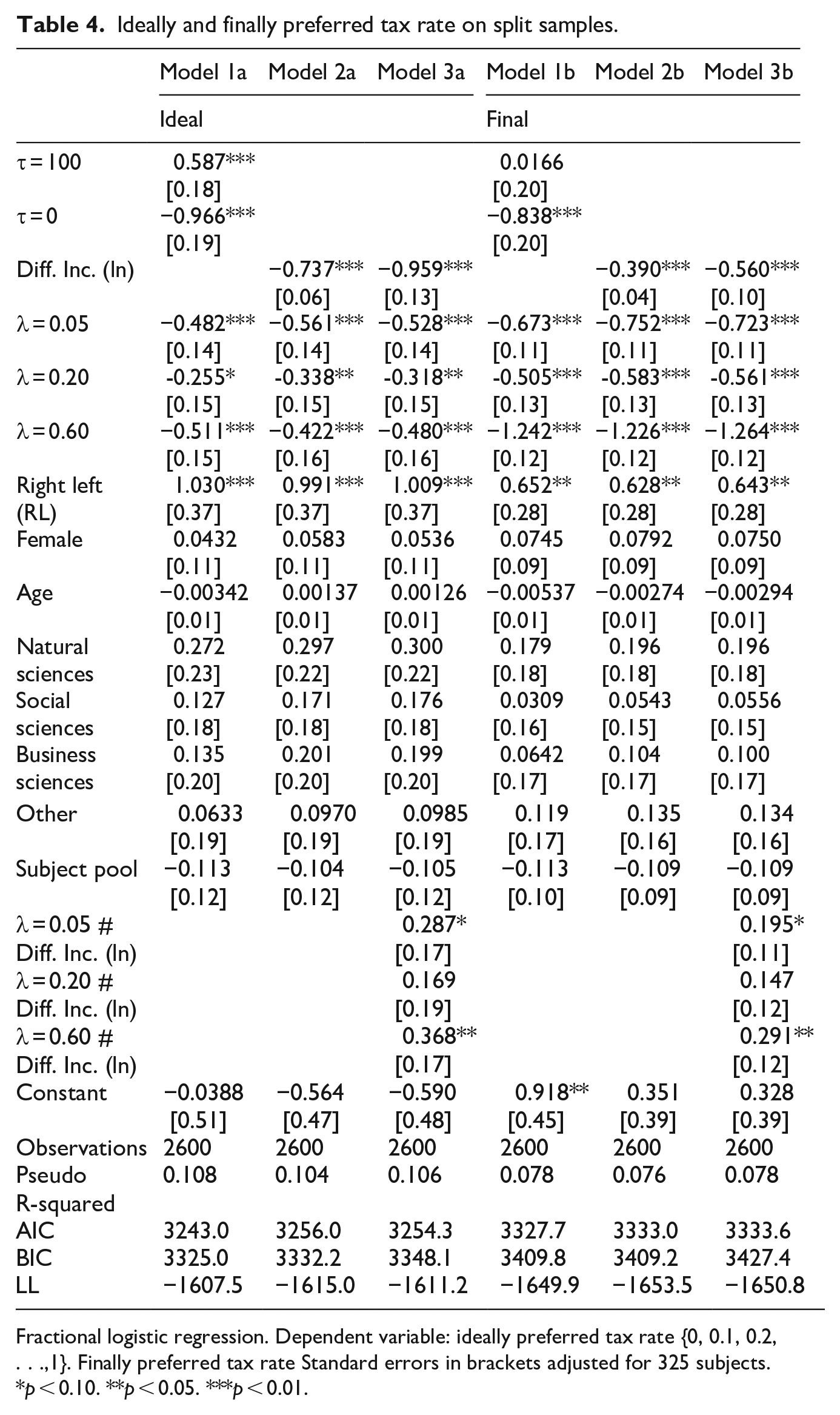

Figure 2 provides a visualization of estimation results from Model 3 in Table 3. The panel on the left compares the rational median voter prediction (see Table 1) and subjects’ actual behavior for the leakage treatments (λ = 0, 0.05, 0.2, and 0.6), before and after group communication. The rational median voter prediction expects 51% as the average tax rate for λ = 0, 45% for λ = 0.05, 38% for λ = 0.2, and just 17% for λ = 0.6. The panel on the right shows the average marginal effect before and after group communication. Findings from Figure 2 can be summarized in three points:

First, concerning the rational prediction, we see that in each treatment condition, the average tax rate is above the predicted average tax rate for leaks of λ = 0, 0.2 and 0.6. Except for the treatment λ = 0.05, the ideally and finally preferred tax rates are close to the rational prediction. Second, the existence of an efficiency loss is associated with a reduction in support for redistribution. The reduction is the strongest in the 60% leakage condition. A 5% and a 20% leakage both trigger a substantial reduction of the average ideally preferred tax rate and the tax rate after numerical communication compared to the situation without leakage. Surprisingly, the reduction is slightly stronger for the 5% leakage. Third, there is a substantive variation of the leakage effect before and after group communication. It seems that what matters in choosing the ideal tax rate is just whether the inefficiency is present or not rather than its actual size. This conjecture is empirically confirmed when the control treatment is removed from the analysis (Supplemental Appendix Table 4). The degree of inefficiency appears to matter most over the decision of the final tax rate. Figure 2 also shows that in treatment conditions with leaks of λ = 0.05 and λ = 0.2, the average tax rate after group communication is higher than the average ideal tax rate before group communication. Only with λ = 0.6, the difference in means is no longer statistically significant, as shown in the right panel of Figure 2, reporting the average marginal effects. In the treatment with the highest leakage (λ = 0.6), group communication seems to protect the electorate from “wasting” money. In other words, the efficiency loss is “unacceptably” high and outweighs the positive effects of communication on support for redistribution.

In total, Figure 2 shows that efficiency loss decreases support for redistribution and the decreasing effect shows a tipping-point pattern for the size of efficiency loss, which supports H2. The overall level of redistribution is still above the rational median voter prediction, before communication and even more so after group communication. Group communication increases support for a moderate redistribution level as long as the efficiency loss has an “acceptable” size.

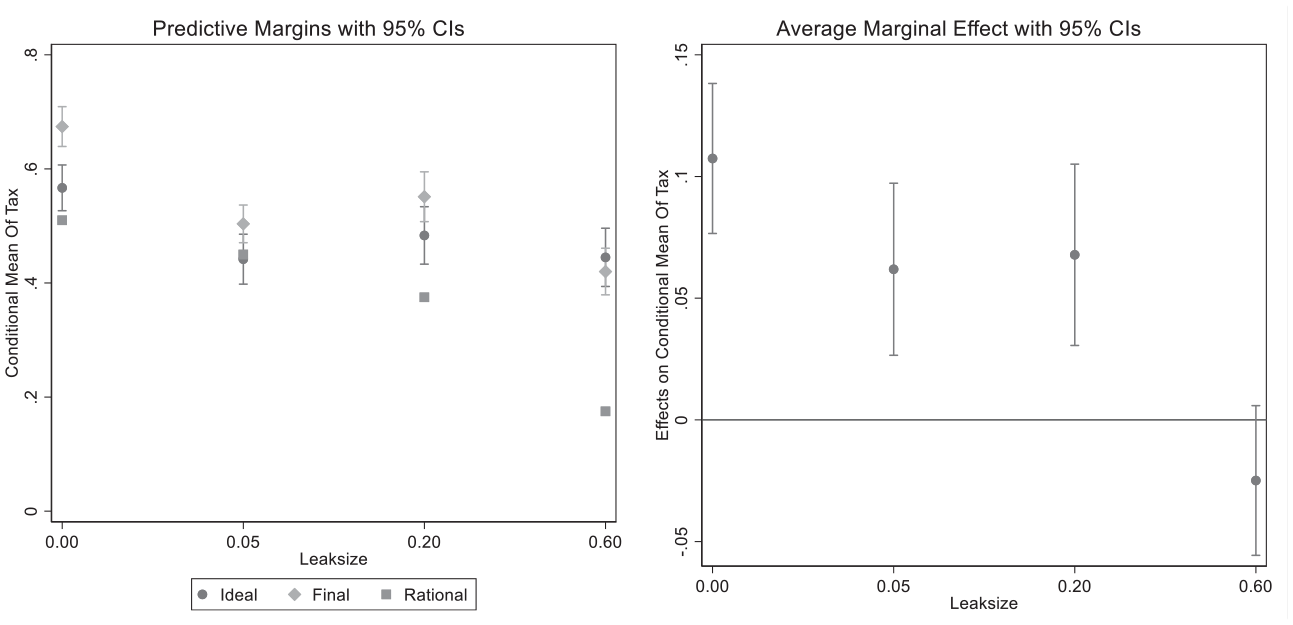

Figure 3 provides more detailed information on the effect of the egoistic prediction on subjects’ vote choice before (ideally preferred) and after (finally preferred) group communication. The upper left panel of Figure 3 shows the predicted effect using the categorical operationalization for the egoistic preferences (Model 4 from Table 3). The upper right panel reports the corresponding average marginal effect. The lower left panel shows the predicted effect for the relative gross income measure r (Model 5 from Table 3). The lower right panel reports the corresponding average marginal effect.

For the categorical measure, we find that the individually preferred redistribution is about twice as large for subjects whose rational prediction is to vote for maximum redistribution (about 70%) than for subjects who favor no redistribution according to their rational prediction (about 35%). This means that subjects whose egoistic preference is to vote for τ = 0% vote for too much redistribution, while subjects whose egoistic preference is to vote for τ = 100% vote for too little redistribution. Group communication increases support for redistribution among subjects whose egoistic preference is to vote for τ = 0% and those predicted to be indifferent, while it has no effect among those whose egoistic preference is to vote for τ = 100% (see average marginal effects). Nevertheless, in qualitative terms, these results are consistent with H1. The egotistic prediction remains to be an important determinant of subjects’ vote choice. Estimating the effect of the two dummies for the rational vote choice for the ideally preferred tax rate and the finally chosen tax rate without any controls yield an overall R2 of 22.8 (ideal) and 12.5 (final).

Using the continuous measure r to operationalize subjects’ egoistic preferences provides similar results. Bearing in mind that r is defined as

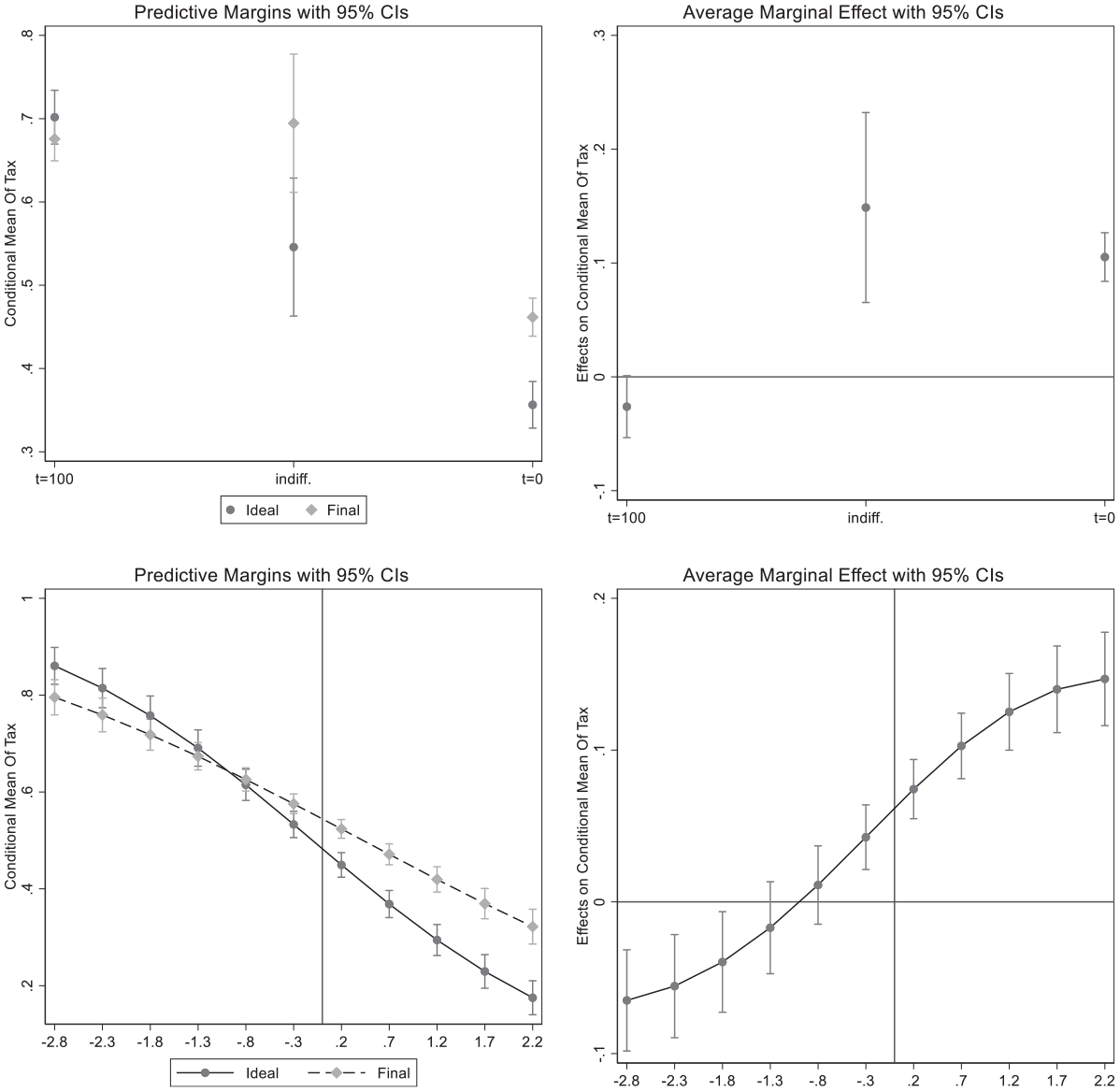

Figure 4 is dedicated to the analysis of H3. It shows the ideally preferred tax rate (left panel) and the finally chosen tax rate as a function of the relative income (r) for each inefficiency (λ = 0, λ = 0.05, λ = 0.2, or λ = 0.6). In general, we see that the “leaky bucket effect” is stronger for subjects with an income below the mean than for those with an income above the mean. The interaction of the leakage with the relative income r in Model 3a and 3b in Table 4 show that this effect is significantly stronger for the treatments with a leakage of 5% and 60%. The negative effect of inefficiency on support for redistribution is stronger with an increasing relative income distance r. With high values of r, leakage has a declining effect on subjects’ ideal vote choice, which means that leakage does not affect subjects who have a strong incentive to vote for τ = 0% based on their distance. The opposite can be observed for subjects who have a strong distance-based incentive to vote for τ = 100%. In line with H3, these subjects consider the inefficiency of the redistributive system and favor less redistribution with a higher efficiency loss.

Egoistic prediction conditioned by efficiency loss.

Among the control variables, only subjects’ self-reported right-left orientation helps to explain support for redistribution. There is robust evidence that subjects who consider themselves left-leaning vote for higher redistributive taxation (coefficient RL is always significant in Tables 3 and 4). Subjects’ self-reported ideological orientation exerts a persistent effect on subjects’ vote choice. Probing deeper, we find no evidence that the size of the efficiency loss conditions the effect of subjects’ self-reported partisan orientation on support for redistribution. This means that even a strong partisan orientation does not immunize subjects against the fiscal leakage effect. However, concerning the effect of group communication, we find that group communication does not affect support for redistribution among subjects reporting the highest level of left-leaning attitudes (Supplemental Appendix Figure 3). These subjects favor redistribution regardless of deliberative group communication.

Discussion and conclusions

This study explores the effect of different magnitudes of efficiency loss on subjects’ voting behavior in a linear redistribution game before and after group communication. In theoretical terms, we draw on Okun’s (1975) idea of redistribution with a “leaky bucket” and test the effect of different sizes of efficiency loss on individual and aggregate support for redistribution in majority voting. We hypothesize that efficiency loss has a twofold effect on subjects’ vote choice: it alters subjects’ egoistically preferred tax rate and simultaneously activates their efficiency concerns, both of which causes them to favor less redistribution. To test these expectations in a group decision context, we collect subjects’ preferred tax rate before a phase of numerical group communication and their decisions afterward. Each group votes on a proportional tax rate under majority rule. The treatment variable is the degree of inefficiency represented with 0%, 5%, 20%, or 60% of the tax revenues getting lost.

First, concerning H1, subjects with a gross income above (1−λ)

Second, concerning H2, the experimental evidence shows that efficiency loss significantly reduces the individual and aggregated support for redistribution. This result is consistent with theoretical predictions that larger efficiency losses lead to smaller governments (Becker and Gary, 2003) and with previous experimental research by Durante et al. (2014) and Krawczyk (2010) despite the design differences. The negative effect of efficiency loss remains even after controlling for rational egoistic preferences and self-reported ideological orientation. What is more, efficiency loss shows a tipping-point pattern and matters more in the final vote choice. An efficiency loss of 5% and 20% results in the same negative effect (17% points), while an inefficiency of 60% reduces the support by twice as much (35% points). Additionally, when λ = 60%, group communication fails to increase support for redistribution, indicating that the efficiency loss has reached such a magnitude that even communication is no longer able to create support for redistribution. This tipping point pattern for the effect of different sizes of leakage on lowering individual and aggregate support for redistribution hints towards the idea that what prevents subjects from voting in favor of redistribution is not a genuine efficiency preference, but rather social preferences for moderate levels of redistribution. We interpret these findings in line with Almås et al. (2020). They find using a large-scale international social preference experiment with a simpler redistribution game tested in both the US and Norway, that fairness considerations are more fundamental for inequality acceptance than efficiency considerations.

Third, the negative effect of efficiency loss on subjects’ support for redistribution is conditional on their income position (H3). The effect is stronger for those subjects whose rational egoistic preference would be to vote in favor of redistribution. In this income domain, efficiency loss suppresses egoistic preferences in favor of redistribution.

This study explored the effect of different sizes of efficiency loss on support for redistribution with an exogenous endowment, before and after group communication. Previous research, however, indicates that support for redistribution is affected by whether endowments are earned or randomly assigned (Durante et al., 2014; Krawczyk, 2010). This poses the question of whether the effect of efficiency loss would change with endogenous endowments. With earned endowments, it could be that some participants would see it as a greater shame to let some of the joint payoff go to waste, and Krawczyk (2010) finds some tentative evidence for this expectation. Endogenously determined endowments are expected to lower the ideally preferred, and the implemented level of redistribution but not alter the effect of different sizes of efficiency loss on support for redistribution. In order to avoid any contamination, we thus choose to keep the type of endowment allocation constant.

Using exogenous endowment might also explain why subjects’ self-reported ideological right-left placement is such a robust predictor for voting on redistributive taxation in this study compared to Esarey et al. (2012a). The latter were using endogenous endowments and find no such effect. From a procedural justice perspective, random assignment of endowments rather than earned endowments creates an unjust allocation of pre-tax income. Such concerns about the cause of inequality are reflected in subjects’ right-left placement (Mair, 2007). Leftists vote in favor of redistribution to compensate the losers in the random allocation of endowments.

Finally, we would like to discuss the limitations of this study. First, the positive and robust effect of group communication on support for redistribution could also be reinforced by the communication stage design, which implicitly sanctions groups that fail to coordinate on a majority tax rate. Although this design has proven beneficial to identifying the effect of communication on support for redistribution, future research might alter the sanction rule to explore its effects on majority coordination and aggregate redistribution. Second, this study examined the effect of inefficiency, defined as a loss in the process of redistribution, and did not give any further background information on why the loss occurs. Subjects could experience such a loss as being “expropriated” by the experimenter. Although we cannot rule out that some subjects feel that way, we believe that such reactions should be stronger with endogenous endowments, which is not the case here. For this study, we used a neutral loss frame to keep the influence of other preferences outside. However, little is known about whether the effect of efficiency loss on support for redistribution is sensitive towards the cause of inefficiency. Future research might address this limitation, for example, through the introduction of “bureaucratic” subjects, whose task is to transfer the money and who must be paid for their service.

Findings from this study may have important policy implications. Efficiency can be used to justify inequality (Hayek, 1976; Nozick, 1976). However, the efficiency with which welfare programs transfer income from rich to poor is usually hard to measure. Despite this, as made apparent in our results, voters respond to inefficiency in the context of redistribution. Skillful politicians might take advantage of the difficulties of having valid information on the efficiency of redistribution programs and understate their efficiency to stir voters’ fear of system inefficiency to make voters, that should egotistically be in favor of redistribution, vote against it. Thus, from a policy-making perspective, presenting and reproducing a participial negative image of the redistributive system’s efficiency can be an effective measure to make voters irrationally vote against redistribution. However, manipulations are only possible within the set of “moderate” levels of redistribution. We favor interpreting our findings as evidence for a strong societal preference for moderate levels of redistribution even if such a level comes with high efficiency costs.

Supplemental Material

sj-pdf-1-rss-10.1177_10434631211015514 – Supplemental material for Efficiency loss and support for income redistribution: Evidence from a laboratory experiment

Supplemental material, sj-pdf-1-rss-10.1177_10434631211015514 for Efficiency loss and support for income redistribution: Evidence from a laboratory experiment by Markus Tepe, Fabian Paetzel, Jan Lorenz and Maximilian Lutz in Rationality and Society

Footnotes

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by German Research Foundation (DFG, LO-2024/2-1) “Opinion Dynamics and Collective Decision” and German Research Foundation (DFG, FOR 2104, TE1022/2-1) study group on “Need-Based Justice and Distributive Procedures.”

Data and code availability

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.