Abstract

The authors study the role of redistributive policy in comparative research on the determinants of wealth. The authors argue that public redistribution affects the level of net wealth by moderating the household-level association of income and wealth. Drawing on microdata for 14 countries from the Luxembourg Wealth Study, and spending and revenue data from the Organisation for Economic Co-operation and Development, the authors use ordinary least squares models with country fixed effects. The authors find a positive moderation effect of social spending and a negative moderation effect of income taxation. Higher and lower labor incomes translate into higher and lower levels of wealth where income taxation is lower or social spending is higher. The authors complement these findings with panel information from the United States, providing further evidence supporting the cross-national results. In summary, public redistribution partially accounts for differences in the association of income and wealth across countries. The authors urge future research on the correlation of income and wealth to take public redistribution into account.

The rise of wealth-related inequalities in many contexts has spurred increasing interest in understanding its cross-national variation (Piketty 2014). Researchers find that levels of wealth inequality are largely independent from cross-country differences in income inequality (Jäntti, Sierminska, and van Kerm 2013; Pfeffer and Waitkus 2021b; Semyonov and Lewin-Epstein 2013; Sierminska, Brandolini, and Smeeding 2006), suggesting that institutions and policies that shape income inequality are potentially irrelevant when studying wealth (Semyonov and Lewin-Epstein 2013). Although national levels of wealth inequality do not conform to conventional categories in comparative political economy, average wealth levels appear to mirror variations in country-specific welfare systems (Bryant, Spies-Butcher, and Stebbing 2022; Fessler and Schürz 2018). This underscores the importance of studying policies that influence both national income and wealth, including how income translates into wealth on the household level (Kuypers, Figari, and Verbist 2021).

The absence of a correlation between income and wealth inequality at the national level is balanced by moderate correlations observed at the household level (Killewald, Pfeffer, and Schachner 2017). This correlation is most notable within the middle of the distribution and less pronounced toward the extremes (Skopek, Buchholz, and Blossfeld 2014). This disparity is driven by varying factors at the lower end (such as negative wealth due to debt) and the upper end (via inheritance, transfers, and asset appreciation). In contrast, for households in the middle of the income distribution, wealth accumulation is mostly the result of saving from (labor) income (e.g., Black et al. 2023; Waitkus and Minkus 2021), while only at the top of the income distribution inheritance and gift become more relevant (Black et al. 2023). Therefore, it is important to study how income translates into wealth in different contexts.

Although scholarly attention has centered on studying sociodemographic and socioeconomic disparities in wealth accumulation (Killewald et al. 2017), surprisingly little research has explored the impact of policy design (but see, e.g., Berman, Ben-Jacob, and Shapira 2016; Kuypers et al. 2021) and the role of public redistribution in how households translate their income into wealth across countries (Fessler and Schürz 2018; Wroński 2023).

How does public redistribution relate to the income-wealth correlations? Given that net wealth encompasses various financial and real assets minus liabilities (Davies and Shorrocks 2000; Spilerman 2000), pinpointing the taxes and transfers that potentially have the greatest influence on the income-wealth nexus is not straightforward. For example, certain countries impose taxes on net wealth levels (Limberg and Seelkopf 2022) or property taxes (D’Arcy and Nistotskaya 2022; Figari, Verbist, and Zantomio 2022), with the latter being usually levied on the local level, making cross-national comparisons challenging. Additionally, taxes on capital income or inheritance should affect those with highest levels of wealth most (Auerbach and Hassett 2015; Lierse and Seelkopf 2016a) but these have not yet been studied cross-nationally. Given that we are interested in how household income translates into wealth, it is particularly lamentable that the role of (income) redistribution in shaping wealth levels has received limited attention (but see Fessler and Schürz 2018; Kuypers et al. 2021). In this study, we aim to take a significant step in addressing this gap both across countries and over time.

To be clear, public redistribution comes in many forms, with different implications for different parts of the income distribution. For instance, welfare states redistribute incomes not only vertically (i.e., among different strata) but also horizontally (e.g., among generations). The decision whether to include or exclude pensions from welfare state measurement has far-reaching consequences as intraindividual redistribution over the life course can be a sizable proportion of public spending (Bergh 2005; Fessler and Schürz 2018). At the same time, entitlement to pension benefits is regularly tied to prior contribution, which led researchers to question its redistributive nature (Jesuit and Mahler 2010). To minimize distortion from pension generosity (see Alessie, Angelini, and Van Santen 2013 and Wroński 2023 for this perspective), we focus on income and wealth of the working age population.

Prior research on the role of redistribution in comparative studies on wealth levels offers mixed results. Whereas Semyonov and Lewin-Epstein (2013) failed to establish a direct impact of income taxes or social spending on wealth, Fessler and Schürz (2018) showed that pension and social security expenditure substitutes for private wealth accumulation, meaning countries with high public spending have lower average levels of net wealth because low-income households do not need to save precautionarily.

We complement this line of research by trying to understand how income taxation and social spending moderate the relation of income and wealth, hence, enable saving in the first place. More specifically, we want to examine how income taxes and social spending moderate the link between labor earnings and net wealth at the household level across different countries. We argue that both income taxation and social spending affect net wealth only by moderating the association of income and wealth. Put differently: we are agnostic as to whether redistribution is associated with higher or lower levels of wealth but expect that redistribution is implicated in the microlevel relationship of income and wealth across countries.

To address our research interest, we rely on comparative microdata from the Luxembourg Wealth Study (LWS) database and spending and revenue information from the Organisation for Economic Co-operation and Development (OECD 2020). Using linear regression models with country fixed effects that account for unobserved heterogeneity at the country level, we assess the moderation of social spending and income taxation by interacting household labor income with the country-level policy information. To add further leverage to our results from comparative cross-sectional data, we complement our findings with longitudinal information from the United States. We draw on data from the Panel Study of Income Dynamics (PSID) (1984–2017) using individual-level fixed-effects models to estimate whether changes in market income are differently associated with changes in net wealth compared with net income. This longitudinal country-case study allows us to directly address redistribution at the household level thereby providing additional evidence supporting the moderating role of taxes and transfers in accumulating wealth through savings from income.

Our results reveal a negative moderation effect of income taxes and a positive moderation effect of social spending. To put differently: where income taxation is higher, the association between labor income and net wealth is weaker. Conversely, where social spending is higher, the association between labor income and net wealth is stronger. We run several alternate specifications of our measurements and methods and the results remain robust across specifications. Our additional longitudinal analysis showcases that changes in disposable income rather than market income are stronger associated with changes in net wealth thereby underscoring our cross-national results.

We proceed as follows. In the next section we discuss the broader literature on comparative wealth and income levels. We then discuss redistributive policies in the context of wealth accumulation and inequality. We further describe our data and analytical strategy before presenting our findings. Finally, we situate our results in the field and discuss potential avenues for future research as well as policy implications.

Theoretical Background

Despite the increasing dedication to understanding wealth differences, unraveling the origins of household’s wealth levels remains a challenge. The scholarly literature recognizes three separate pathways of wealth accumulation: wealth transfers, capital gains, and earnings from labor income (Kapelle and Lersch 2020). Wealth transfers include gifts and intergenerational transfers such as bequests and inheritance from parents or other relatives that clearly affect individual wealth (Wolff and Gittleman 2013) but particularly benefit the well off at the top of both the income and the wealth distribution. Similarly, gains arising from capital investment include interests and dividends accrued from stocks and bonds benefit the top end (Nau 2013), 1 while also encompassing rental income or different ways of capital appreciation, such as soaring housing prices (Adkins, Cooper, and Konings 2020). Last, wealth can grow through savings from earnings (Black et al. 2023).

As Hällsten and Thaning (2022:1534) noted, wealth has not necessarily a strong connection to the labor market considering that a significant portion is transferred across generations through bequests; or results from investment returns such as in housing or finance. Yet researchers struggle to precisely quantifying the contribution of labor income in wealth accumulation, partly because of the complexities of measuring jointly the role of intergenerational transmissions, asset appreciation and consumption (see Fisher et al. 2016). Hence, the individual potential to save wealth is jointly determined by earnings, transfers, returns and consumption (Schneebaum et al. 2018), although evidence from Norwegian register data suggest that income is the most consequential for wealth across the entire wealth distribution (Black et al. 2023). Although higher incomes have a higher savings potential, consumption patterns and consumption needs are similarly pivotal. Unsurprisingly, the ability to save is lower among families that cannot forgo extensive consumption expenditure (Schechtl 2022). Although social spending can increase disposable earnings, income taxes decrease the income that is available in the first place. Therefore, how strongly income and wealth correlate on the household level is moderated by both public spending and income taxation.

Within-country correlations between income and wealth are not very conclusive. For example, on the basis of different datasets for the United States, Killewald et al. (2017) found that the correlation between income and wealth ranges between .2 and .7, depending on data transformation and dataset, and further varies across time and life course. Typically, the correlation is stronger when asset income is included (Killewald et al. 2017), as well as at the top of the distribution (e.g., Killewald 2013). Although this is true for the United States, Skopek et al. (2012) showed for a set of 13 countries that the correlation between income and wealth is more pronounced at the middle of the distribution and less so at the tails and even turns negative for low-income households.

Still, intraindividual wealth accumulation is strongly connected to individual performance on labor markets and the life course. In the context of Norway, Black et al. (2023) asserted that labor income stands as the most pivotal factor of wealth across the distribution. Only among the top 1 percent do capital income and gains become more important, while inheritance and other transfers (such as gifts and inter vivo transfers) are less important than labor income. This alignment is in line with the life-cycle hypothesis (Modigliani 1966), which indicates that the bulk of an individual’s wealth is amassed during adulthood and deaccumulated during retirement.

Nevertheless, alongside these age-related effects, the relationship between individual income and the accumulation of wealth likely differs by cohort and period that are not easily disentangled from one another (Fosse and Winship 2019). It is notable, however, that younger generations seem to exhibit more responsiveness toward institutional settings concerning portfolio choices (Sierminska and Doorley 2018) and exhibit lower levels of wealth than senior households across countries (Pfeffer and Waitkus 2021a).

The extent to which income levels translate into corresponding wealth levels hinges on individual attributes such as age composition and household consumption patterns. How social spending and income taxation then interact to moderate the relationship between incomes acquired and wealth of individuals remains a question yet to be answered in light of the variation of wealth levels and inequality across countries (Pfeffer and Waitkus 2021b).

The moderating role of distributional efforts by the state depends on the function of wealth across countries and along the wealth distribution (Beckert 2023). Saving wealth for welfare is less prominent in contexts in which public wealth (in the form of, e.g., public pension provision, free education, and health care) is high (Wroński 2023). Therefore, Fessler and Schürz (2022) differentiated the functions along the wealth distribution: for low wealth (and income) households wealth provides additional means to spend on consumption, whereas further up the distribution wealth has a use function (e.g., the primary residence), and income function, can be bequeathed and so on. In that sense, the moderating effect of redistribution should differ across the income distribution: high public spending could strengthen the association between income and wealth for low-income households and should weaken it further up the distribution. In fact, Fessler and Schürz found that high public spending leads lower levels of wealth because low-income households save less.

Redistribution and Wealth

Figure 1 offers a streamlined representation that simplifies how redistributive policies play a moderating role in the association between income and wealth.

Conceptual framework.

The attention directed toward taxes in the context of wealth and inequality across nations has expanded in recent years. Previous research has predominantly explored historical introduction of inheritance and estate taxation (Beckert 2008; Limberg and Seelkopf 2022; Scheve and Stasavage 2012) or its redistributive capacities (Bönke, von Werder, and Westermeier 2017), as well as the possibilities of introducing (or abolishing) net wealth taxes (Roine and Waldenström 2009) and capital income taxes (Lierse and Seelkopf 2016b). Recently, Kuypers et al. (2021) described how tax redistribution affects the wealth distribution differently than the income distribution. 2

Taxes levied on income and wages profoundly influence the potential for savings originating from labor income. This is because income taxation fundamentally shapes the income distribution (Sologon et al. 2020) and further affects predistribution by incentivizing behavioral patterns in the labor market, such as households’ decisions concerning labor supply (Bronson and Mazzocco 2018). Unlike inheritance or net wealth, labor income is taxed almost everywhere (Kuypers et al. 2024).

Constituting more than 20 percent of governmental revenue on average within the OECD, taxes on labor income serve as critical means for financing public services (OECD 2020). However, the top statutory personal income tax rate varies substantially from more than 50 percent in some Scandinavian countries to less than 20 percent in many Eastern European countries. These differences in top income tax rates stem from countries with flat rates (e.g., Estonia), whereas others adopt progressive schedules, with higher incomes being subject to higher marginal tax rates. Even among countries using progressive income taxes, substantial variation persists, ranging from minimal (such as Switzerland) to highly progressive schedules (like the United States) (Prasad and Deng 2010).

Regarding wealth accumulation, previous scholars argued that the taxation of earnings would reduce the impact of income on accumulated wealth (Semyonov and Lewin-Epstein 2013). By this rationale, labor income becomes less central for wealth accumulation because other pathways (e.g., inheritance or capital income) are contributing relatively more to the accumulation of wealth than in a scenario in which labor earnings remain untaxed. Thus, our first hypothesis is as follows:

Hypothesis 1: The association of labor income and net wealth is negatively moderated by income taxes.

The role of social spending in levels of wealth and inequality across countries has received even less attention than taxes (Kuypers et al. 2021). The role of public spending can be seen as an approximation of welfare state generosity indicating how wealth serves different purposes in different contexts. Public spending should show the opposite influence of income taxation: whereas taxes decrease earnings and potentially suppress savings, social spending has the potential to increase disposable income by alleviating household pocketbooks. Public social provisions sometimes can represent a simple substitute for earnings (such as, e.g., direct cash benefits). Yet they can also take the form of in-kind provisions of goods and services, sometimes but not always targeted at sick, disabled, or unemployed individuals. The overarching idea here is that an additional dollar in labor income is more easily remunerated with an additional amount saved where the state provides for otherwise costly, private services. In fact, Fessler and Schürz (2018) found that in countries where public spending is low, net wealth levels are higher as households are incentivized to accumulate wealth to finance exactly those kinds of benefits, which in another context might be publicly financed (Skopek et al. 2014). There has been further evidence for displacement, meaning that in countries with generous pension systems, people save less (Alessie et al. 2013; Wroński 2023). Therefore, in contexts where public spending is high, households are less inclined to accumulate wealth as the buffer function of wealth. However, most transfers benefit the lower- and middle-income groups (Bergh 2005). Therefore, we our second hypothesis is as follows:

Hypothesis 2: The association of labor income and net wealth is positively moderated by social spending.

It is worth emphasizing that income taxes and social spending might be closely connected to each other. That is, revenue generated through the taxation of labor can be used to finance public transfers. However, at the same time, income taxes are only one component of public finance. What is more, as argued above, income taxation might also directly affect the association of earnings and wealth by making other types of income more attractive. In other words, although social spending and the taxation of labor are closely connected, both have the potential to independently affect the association of labor income and wealth.

Empirical Approach

Data and Sample

In our exploration of the relationship between labor income and net wealth, we use harmonized microdata from the LWS. The LWS provides standardized, comparable data on income and wealth (Sierminska et al. 2006). The thorough harmonization of the national data renders these data ideal for comparative analysis. There are currently 18 countries in the database, with 14 possessing all required information for labor income and the different wealth components. Although some of the underlying data provided with imputations for missing wealth information, other oversample rich households. For an overview of all data and descriptive statistics, see Supplemental Appendix Table A1. 3

All monetary information is purchasing power parity–adjusted to 2017 U.S. dollars and top- and bottom-coded at the 0.1st and 99.9th percentiles. We equivalize all information on income and wealth using the per capita equivalization. The sample is limited to households whose head is aged between 20 and 59 years to prevent potential distortions arising from pension schemes generosity and the taxation of pension income. 4 Furthermore, we select only households that report positive labor income (thereby excluding households with unemployed heads).

In addition to harmonized microdata on income and wealth from the LWS, we rely on aggregated spending and tax indicators from the OECD tax database (OECD 2020). The OECD provides yearly statistics including detailed public spending, taxes on income, property and capital gains among many others that are well suited to study policy contexts across countries and have been used by various researchers (e.g., Hope and Limberg 2022; Lierse and Seelkopf 2016b).

Variables

The main dependent variable is the household’s net wealth. We use both, log-transformed net wealth as well as the inverse hyperbolic sine (ihs) transformation in our models (Pence 2006). The advantage of using the ihs transformation lies in its ability to retain negative and zero values, a feature absent in log-transformed data. Additionally, we use the log-transformed version of net wealth because of its effectiveness in handling the highly skewed distribution of wealth. 5 To ensure transparency, we present all models using both operationalizations, underscoring that our findings remain consistent across different transformation and negative wealth holdings.

The LWS net wealth measure includes financial wealth, housing wealth, nonhousing real wealth minus debts. As with most studies on wealth, we study marketable wealth, which does not include potential future pension entitlements that are usually not part of household surveys (Davies and Shorrocks 2000). 6 Considering that a significant portion of household’s wealth is stored in housing, we conduct supplementary analysis in which housing equity is excluded from our net worth measure.

Our main independent variables are the cross-level interaction of the social spending indicator and the household’s total labor income as well as the cross-level interaction of the income tax indicator at the country level and the household’s total labor income 7 (log transformed). We are interested in the inflow perspective, ignoring what is happening on the wealth side. 8 Therefore, we want to know how labor income turns into wealth through savings rather than other pathways such as capital appreciation.

Because we are interested in the moderation effect of social spending and income taxation on the association of labor income and wealth, we use the following country-level indicators from the OECD. First, we use public social spending as a share of gross domestic product in every country of our study. This variable grasps the overall level of public social expenditure in each country. Second, we use the income tax revenue as a share of gross domestic product. This variable gives us a sense of the overall significance of income taxation in each country. The second measure essentially abstracts from questions of tax incidence but provides a good proxy for the overall level of income taxation in a given country. Both indicators are included as the five-year average prior observation.

In addition, we include labor income (log) and a homeownership indicator (ownership [reference] or no homeownership) in our analyses. Finally, the following sociodemographic characteristics of the household are included: a set of dummy indicators of the type of household (single [reference], couple, couple with children, single parent, or other), highest education achieved by the household head (low [reference], medium, or high), age and squared age of the household head, gender of the head (male [reference] or female), and the number of household members.

Analytical Strategy

We apply ordinary least squares regression models with country-level fixed effects and sociodemographic controls at the household level. The main variable of interest is a multilevel interaction of the redistribution indicator at the country level (tax j ) and labor income at the household level (income i ).

Our main model takes the following form:

where net wealth

ij

is the net wealth of household i in country j,

Applying models with country-level fixed effects instead of conventional multilevel models allows to control for all unobserved heterogeneity at the country level (Möhring 2012). With this approach, no country-level variables can be included in the analysis. That is, the main effect of the redistributive indicator is absorbed by the country fixed effect. However, the multilevel interaction term still varies within countries and provides a clear estimation of the moderation effect of the redistribution indicator on the association of income and wealth. Given our limited set of countries (n = 14), conventional multilevel models suffer from the problem of not being able to include all relevant country characteristics (Bryan and Jenkins 2016). The advantage of the fixed-effects approach is that country-level heterogeneity can be better accounted for (Möhring 2012). Given our interest in the moderation effect rather than the main effect of income taxation, we prefer the fixed-effects models over the conventional multilevel models. To increase leverage, we include two survey waves for each country in our regression models, hence bringing our sample to 28 observations from 14 countries. Standard errors are clustered at the country level.

U.S. Case Study

A primary challenge in cross-national research involving the correlation between redistribution, income, and wealth is the availability of data. Consequently, we rely on external information from national accounts to proxy for the country policy system in our primary analysis in our cross-sectional comparative study. Although the cross-level interaction allows us to empirically address the role of the national redistribution indicators, a major caveat is the absence of comprehensive longitudinal data. The deficiency prevents us from effectively assessing within-unit changes over time to capture how redistribution is implicated in accumulating wealth from savings.

To provide further leverage supporting our interpretation we therefore additionally draw on long-running information from the PSID. We use household-level net wealth as provided by the PSID in the years between 1984 and 2017. 9 We additionally rely on microlevel market and net income information simulated through TAXSIM as provided through the Cross-National Equivalent File data (Frick et al. 2007). The PSID thus allows us to estimate the effect of changes in household market vs net income on changes in household net wealth holdings. In this manner, the role of redistribution, understood as the difference between market and net income, can be addressed directly.

We apply household-level fixed-effects models that account for any unobserved heterogeneity between households. In short, exploiting only over-time variation within households, the model tells us in how far a microlevel change in income is associated with a microlevel change in wealth. Here, we therefore only include a parsimonious set of time-varying controls next to market and net income (log): in education (yes or no), age, age squared, number of household members, and marital status. We cluster standard errors at the household level. Mirroring our cross-national approach, we transform net wealth using the ihs.

Results

We present our findings in several steps. We first show the wealth-income correlations in each country (i.e., the coefficient of the correlation between labor income and net wealth). We go on to explore the bivariate association of the correlation coefficients and our tax and spending indicators across countries. We then turn to the results of our fixed-effects regression models. Finally, we present results from the U.S. case.

Wealth-Income Correlations

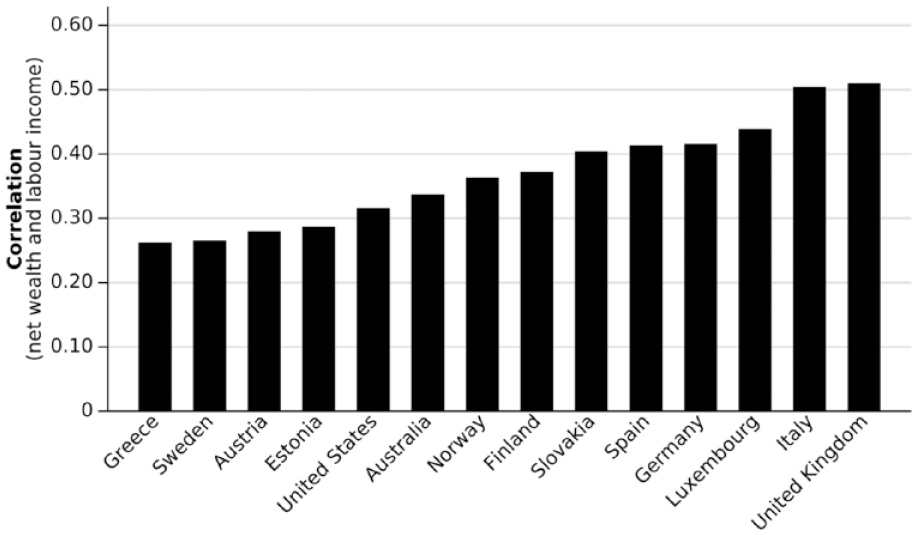

Figure 2 displays the correlation coefficients for labor income and net wealth (log) for every country in our study applying log transformations. The correlations are largely in line with findings from previous literature (Killewald et al. 2017; Skopek et al. 2012). However, countries differ substantively in their income-wealth correlations, with coefficients ranging from less than 0.3 in Austria and Sweden to about 0.5 in the United Kingdom and Italy.

Wealth-income correlations by country.

Although labor income and wealth are correlated, this correlation varies, for instance, across asset types or age groups (Killewald et al. 2017). If wealth is accumulated through income, the number of years in paid employment clearly determines the accumulative potential of income and, thus, the correlation of income and wealth. Therefore, a weak correlation might reflect the distinct nature of wealth as a stock accrued over the life course and would be stronger, if we could measure permanent income instead of income in a given year (Killewald et al. 2017). Could differences in redistributive systems account for different income-wealth correlations?

We are interested in the relevance of social spending and income taxation in shaping the association of labor income and wealth. As mentioned earlier, we expect wealth-income correlations to be higher where social spending is high, and weaker where income taxes are high. Figure 3 plots the correlation coefficients against our tax indicators. The figure shows the association of the wealth-income correlation and public social spending (left), and the relationship of the correlation coefficient and income taxation (right).

Bivariate relationship of the wealth-income correlation across countries and redistributive indicators.

Both measures are weakly associated with the wealth-income correlation coefficient. In other words, in countries with higher income taxation we see a weaker correlation of household’s income and net wealth, whereas in countries with higher social spending, we see a stronger correlation of household’s income and net wealth. However, in both cases the bivariate association is very limited. Some countries have high wealth-income correlations while indicating redistributive measures at the cross-national average, such as the United Kingdom.

We further plot the indicators against median wealth-income ratios to approach whether countries with lower income taxes or higher social spending also show higher wealth levels. We express median net wealth as its ratio to median income because countries differ in their economic development. Figure 4 depicts that countries with lower tax measures have higher median wealth-to-income ratios. Put differently, in countries where income taxes are higher, net wealth as a ratio of labor income is lower. However, the public social spending indicator shows no association. Does this macrolevel explorative figure also translate to the microlevel?

Macrolevel bivariate association of country indicators and wealth-income ratios.

The Moderation of Income Taxes

We expected our tax measure to negatively moderate the association of labor income and net wealth and our spending measure to positively moderate this association. Where taxes on labor are higher, the decisiveness of labor income for wealth accumulation should be lower (hypothesis 1). Conversely, where social spending is higher, labor income should translate into wealth more easily (hypothesis 2). We examine these expectations in linear regression models with country fixed effects and an interaction term of labor income and the two different indicators of redistributive context. For descriptive statistics on our main variables, please see Table A1 in the Supplemental Appendix. Table 1 displays the main results (see Supplemental Appendix Table A2 for the full regression results). Note the difference in the underlying sample size emerges because of retained zero and negative values in the ihs-transformed model that are excluded in the log-transformed model.

Ordinary Least Squares Regression Models of Net Wealth and the Moderation Effect of Redistributive Indicators (Country Fixed Effects).

Source: Author’s calculation on the basis of Luxembourg Wealth Study data.

Note: Values in parentheses are standard errors. All models control for the following sociodemographic characteristics: labor income (log transformed), highest education, age, squared age, gender (reference male), number of household members and dummies for the type of household (reference single), and homeownership. Standard errors are clustered at the country level. GDP = gross domestic product; ihs = inverse hyperbolic sine.

p < .05. ***p < .001.

In the first model, we show results from linear regression with country fixed effects, drawing on log-transformed net wealth. The second, otherwise identical model uses ihs-transformed net wealth. We interact the household’s labor income with our country-level indicators of social spending and income taxation. Both models control for labor income, homeownership status and other sociodemographic characteristics. Both measures of the moderation effect of redistributive policies are statistically significant associated with net wealth. As expected, public social spending positively moderates the association of income and wealth. Conversely, income taxation negatively moderates said relationship. Put differently, labor income is less determinative for net wealth where income taxes make up for a greater share of the economy, yet labor income is more determinative for net wealth where public social spending is more substantive.

The moderation effects of both indicators are significant and provide novel insights into the institutional determinants of wealth. Countries with either particularly high-income tax reliance or above average levels of social spending are among the most studied countries in wealth-related research. Wealth data from the Scandinavian countries such as Sweden are frequently used to examine the relationship of income and wealth. Yet our results suggest that findings from such a high–income tax context should be generalized only carefully to other settings. What is more, income-wealth correlations from U.S. data—among the widest studied countries in contemporary social science—indicate a very particular underlying context where comparatively high reliance on income taxes is combined with low social spending. Drawing any generalized conclusions regarding the association of market income and net wealth from such a context might be considerably problematic in the light of our results above.

U.S. Case Study

In our main analysis, we relied on external information from national accounts to proxy for the country policy system. The cross-level interaction informed us about the context moderation of the microlevel association of labor income and wealth. Unfortunately, we lack extensive microlevel longitudinal information on market income and net earnings as well as wealth holdings that would allow us to address within-unit changes over time across countries. We thus further draw on case study evidence from long-running panel data in the United States to provide additional support for our argumentation.

By combining low social spending with high reliance on income taxation, the U.S. case is in itself interesting. On the basis of our cross-national results, the United States should be a least likely case in the sense that high income taxation and low public social spending should render the association of market income and net wealth quite weak. In other words, guided by our cross-national analysis, we expect market income to be substantively weaker associated with wealth compared with the association of net income and wealth.

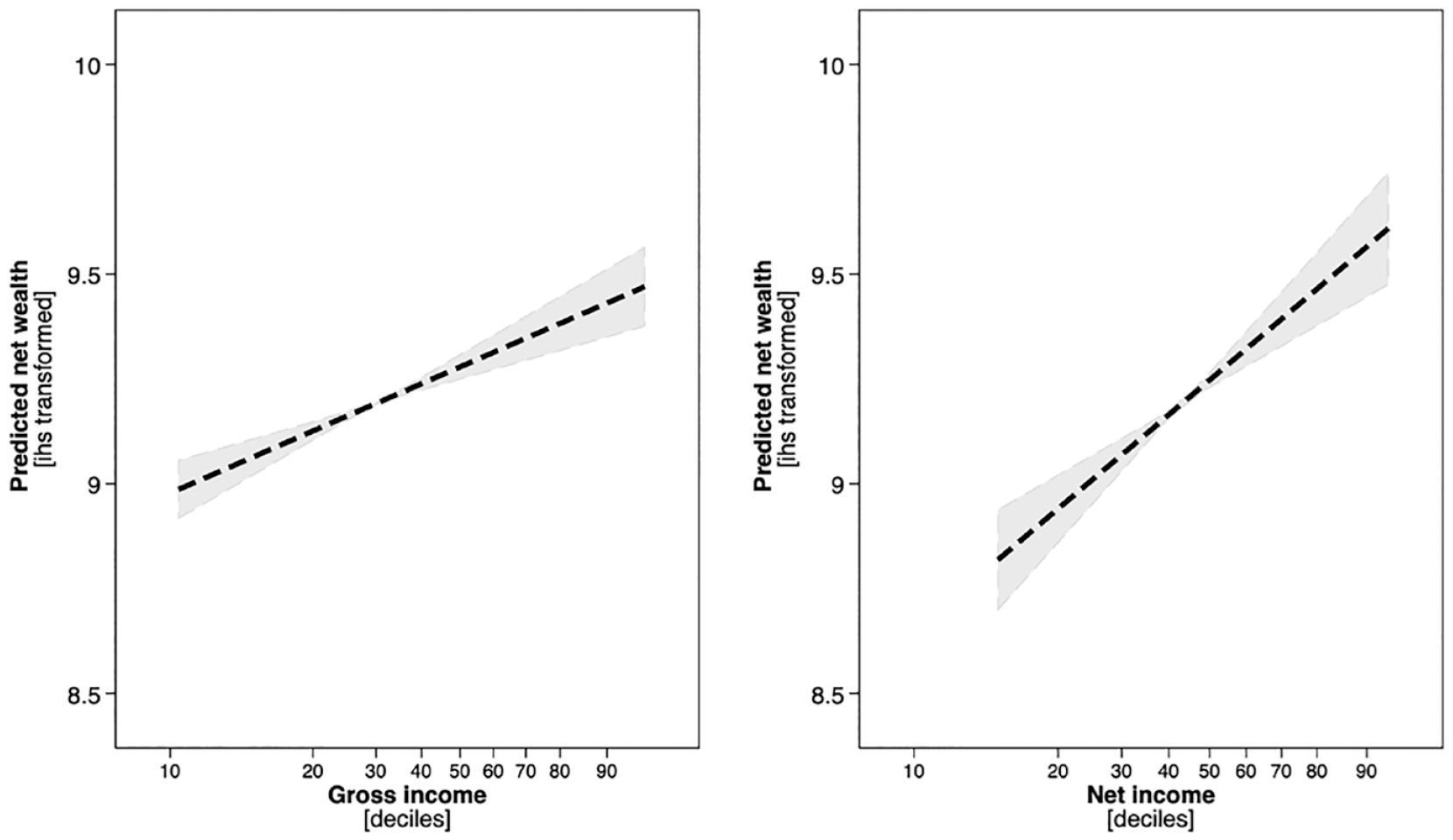

Figure 5 shows linear predictions of net wealth on the basis of household fixed-effects linear regressions covering several decades of PSID data. These models discharge any heterogeneity between households and thus only exploit variation within households over time, thereby allowing us to better approximate the cumulative nature of wealth. Figure 5 indicates predicted net wealth (ihs transformed) across the market income distribution (left) and the net income distribution (right). Consistent with our main analysis, market and net income are associated significantly differently with net wealth. To be clear, market and net income are both positively associated with net wealth, yet net income is significantly more so. In other words, a marginal increase in net income translates into a larger marginal increase in net wealth compared with a marginal increase in market income. Public redistribution matters for how income translates into wealth. 10

Linear predictions of net wealth from household fixed-effects models.

Supplementary Analyses

Wealth Source

Previous literature emphasized the central role of housing for net wealth. Although we accounted for tenure status in our models, the choice of net wealth (which includes housing wealth) could still affect our findings. The inclusion of housing wealth might particularly obscure our interest because housing prices recently became widely decoupled from trends in income in many countries (Adkins et al. 2020). Thus, we replicate the main analysis with financial wealth rather than net wealth. Supplemental Appendix Table A4 shows that the moderation effects of social spending and income taxation are robust to this additional specification.

Income Source

We were particularly interested in the tax moderation of the association of labor income and wealth. However, in some countries, other income components beyond labor (e.g., capital income) are also subject to income taxation. Thus, we also estimate our main models with combined household labor and capital income rather than labor income alone (Supplemental Appendix Table A5). Interestingly, including capital income eliminates the weak, but negative moderation we estimated for income taxation when looking at ihs-transformed wealth. All other models are consistent with previous specifications. We further replicate our main models excluding the self-employed. Our results are robust to this alternative specification (Supplemental Appendix Table A7).

Empirical Strategy

We argued that regarding our research interest, ordinary least squares models with country fixed effects are superior to conventional random-effects multilevel models. Most important, the fixed-effects approach allows us to discharge country-level heterogeneity. Yet our approach might entail biased standard errors because the level 2 n is very small. To provide further support for our main analyses, we additionally ran a meta-regression. To this end, we first estimated linear regression models for each country. We then recovered coefficients and standard errors from these models and ran a regression including our redistributive indicators using Stata’s metareg routine (Harbord and Higgins 2008). Findings presented in Supplemental Appendix Table A6 yield a positive yet insignificant coefficient for the spending indicator and similar results to the main analysis for the income tax indicator, thus providing some additional support for our argumentation.

Discussion

Wealth is a central dimension of economic well-being, and its level and accumulation are the consequences of demography, labor markets, education, housing, and many other factors. Yet policy design, be it welfare state generosity or tax policy, might be similarly decisive. Among these, the relevance of social spending and income tax policy remains scarcely examined from cross-national comparative research.

Is social spending and income taxation moderating the association between labor earnings and net wealth? Drawing on harmonized microdata from the LWS, we indeed find support for a negative moderation of income taxation and a positive moderation of social spending. Thus, where income taxes are higher, the positive relationship between labor earnings and net wealth is weaker. Conversely, where social spending is higher, the positive relationship between labor earnings and net wealth is higher.

Our study is of utmost interest for any comparative research on the determinants of wealth. More specifically, we add to the ongoing discussion on the weak correlation of income and wealth by highlighting the crucial role of the redistributive policy context. Our findings stand in contrast to previous research that suggested social expenditure and income taxes are unrelated to levels of wealth (Semyonov and Lewin-Epstein 2013). Here, we argued that it is crucial to understand both as policy dimensions that moderate the relationship of income and wealth, rather than by directly affecting levels of wealth or inequality (Kuypers et al. 2021). Although previous research has established that welfare spending leads to lower levels of wealth (Alessie et al. 2013; Fessler and Schürz 2018; Wroński 2023), we complement this line of research by showing that the welfare state kicks in when labor income is translated into wealth levels. We find that when income from labor earnings is taxed higher, revenue from other sources gain in relative importance for the accumulation of wealth although labor income remains positively associated with wealth. Conversely, where public social spending provides for otherwise costly private services, labor income translates into accumulating savings more easily. Although this notion is difficult to tackle in single-country studies, the comparative approach enables us to compare different institutional settings and thereby assess the relative weight of the redistributive system.

Several limitations of this study are noteworthy. First, our sample consists of only 14 countries in two waves. As with most research on wealth, data availability is a major constraint. Although data restrictions provide a clear limitation for generalizing the findings, we argue that our results indicate findings from case-country studies in wealth research are even more problematic. This might be particularly the case as most wealth data are from countries with either high levels of social spending (e.g., Sweden, Finland) or countries that rely heavily on income taxation (e.g., the United States). Studies highlighting the lack of correlation between income and wealth positions might fail to acknowledge the exceptional relevance of social spending and income taxation in their country context.

Second, the function of wealth differs across countries that potentially affects the income-wealth correlation: In countries with low public pension entitlements the correlation might be stronger as people save up income for cover income losses in retirement (Skopek et al. 2014). This is less the case in Scandinavian welfare states with generous coverage and less need for wealth accumulation, which is reflected in our cross-country correlations (Figure 2).

Finally, the cross-sectional correlation presented here says little about a causal relationship. Ideally, we would thus rely on over-time variation within countries to estimate the change in the association of income and wealth in light of changes in income taxes. However, first, redistributive systems are characterized by substantive rigidity over time. That is, over-time differences within countries are dwarfed by differences between countries. Second, and more important, accumulating wealth through income is a time-consuming endeavor. It is unlikely that a change in social spending or the income tax will be observable in changing wealth holdings even years after. Here again, we simply lack cross-national microdata covering a reasonably extended timespan.

This study opens way for a multitude of future research projects. First, the relevance of redistributive context in determining the potential to accumulate wealth over the life course across different institutional settings is puzzling. For such a project, harmonized panel data from multiple countries, such as the Cross-National Equivalent File and the Comparative Panel File, are needed (Frick et al. 2007; Turek, Kalmijn, and Leopold 2021). Second, researchers could engage in examining the macrolevel association of income redistribution and income-wealth correlations by investigating a wide range of policy characteristics. Finally, extending our approach to other spending categories and taxes, and other income sources, should be a particularly insightful endeavor.

Our study speaks directly to recurrent policy debates. For instance, throughout the last decades, many countries introduced policies of asset-based, private ways to insure against insecurities, mostly by encouraging private savings as a complementary social safety net. This article highlights the simple fact that asset-based security ultimately reproduces income-based inequalities but that the strength of such reproduction will be moderated by income taxation and public social spending. The same is true for other policy debates evolving around different functions of wealth, such as policy measures that encourage homeownership.

All told, this study provides evidence in favor of a moderation of social spending and income taxes on the positive association of labor earnings and wealth. Where income taxes are higher, the relative weight of income in determining net wealth declines. Conversely, where social spending is higher, labor income turns into accumulated wealth more easily.

Supplemental Material

sj-docx-1-srd-10.1177_23780231241261599 – Supplemental material for Where Income Becomes Wealth: How Redistribution Moderates the Association between Income and Wealth

Supplemental material, sj-docx-1-srd-10.1177_23780231241261599 for Where Income Becomes Wealth: How Redistribution Moderates the Association between Income and Wealth by Manuel Schechtl and Nora Waitkus in Socius

Footnotes

Acknowledgements

We would like to thank Davide Gritti, Tobias Rüttenauer, Philipp Lersch, Julian Limberg, Maximilian Longmuir, and Nhat An Trinh for helpful comments and suggestions on earlier versions of the article.

Funding

This publication is part of the project “Varieties of Wealth” with the project number VI.Veni.221S.161 of the Talent Programme financed by the Dutch Research Council (NWO). Manuel Schechtl’s research was funded by the Support Network for Interdisciplinary Social Policy Research of the German Federal Ministry of Labour and Social Affairs.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.