Abstract

Drawing on a theoretical framework associated with the cognitive perspective, we propose that investors will rely on heuristic cognitive processes when signals from entrepreneurs are congruent or imbalanced incongruent. However, when signals are balanced incongruent, investors will engage in systematic cognitive processes that incorporate additional information from the herding behavior of other investors. We find evidence supporting our hypotheses in a sample of campaigns listed on a UK equity crowdfunding platform. Further analysis employing advanced machine learning techniques reveals that investors engage more in systematic processes when signals from entrepreneurs are in a weak form of balanced incongruence rather than a strong form.

Introduction

Equity crowdfunding has recently become an alternative and important fundraising channel for entrepreneurs (Blaseg et al., 2021; Mochkabadi & Volkmann, 2020; Rossi et al., 2023). By offering shares of their firms on online platforms, entrepreneurs can raise capital from a crowd of mostly unsophisticated investors. To alleviate information asymmetry, prospective investors need to rely on different signals to assess the true quality of campaigns (Johan & Zhang, 2020; Lukkarinen et al., 2016; Mataigne et al., 2025).

Drawing on traditional signaling theory (Spence, 1973), several studies have identified various signals from entrepreneurs that investors may use in their decision-making processes, such as equity retention (Ahlers et al., 2015; Vismara, 2016), social capital (Vismara, 2016), human capital (Kleinert & Mochkabadi, 2022; Lim & Busenitz, 2020; Piva & Rossi-Lamastra, 2018), financial statement disclosure (Bogdani et al., 2022; Donovan, 2021), and environmental orientation (Vismara & Wirtz, 2025). Although the theory has been invaluable in explaining how individual cues (e.g., equity retention) reduce information asymmetry (Vismara, 2018b), it is based on the implicit assumption that signals are interpreted in isolation. However, in practice, prospective investors are rarely confronted with a single, unambiguous signal; instead, they face multiple, sometimes incongruent signals that must be cognitively processed and weighed against one another (Butticè et al., 2022; Steigenberger & Wilhelm, 2018). This creates a theoretical blind spot for traditional signaling theory: it cannot fully explain how investors process and make decisions when presented with a combination of competing signals.

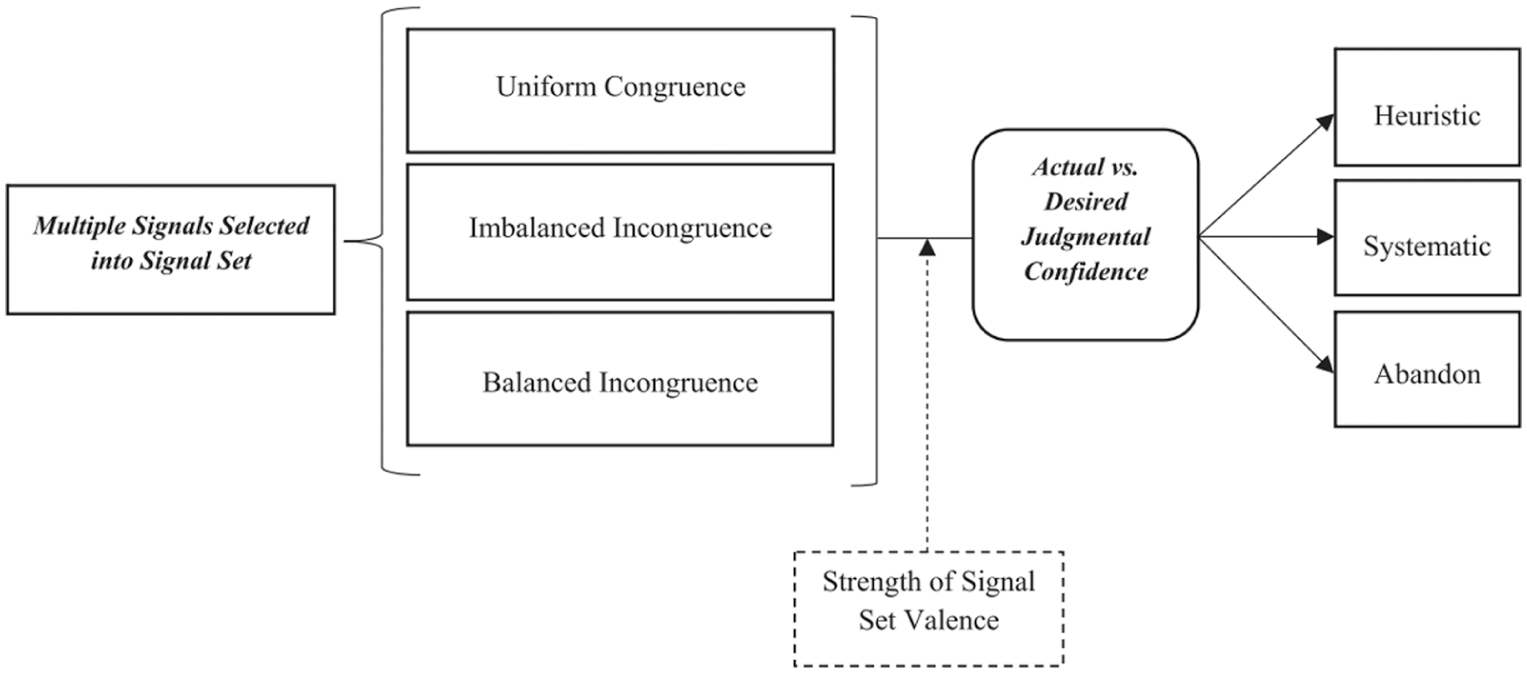

Using a novel framework drawn from the heuristic-systematic model developed by Drover et al. (2018), our paper elucidates how equity crowdfunding investors process the set of signals they receive from entrepreneurs. According to this framework, the set of signals received from entrepreneurs can form one out of three configurations: congruence, when signals communicate the same messages about the underlying quality of campaigns, either uniformly positive or negative; imbalanced incongruence, when one type of signal (either positive or negative) is predominant; and balanced incongruence, where positive and negative signals are relatively equal in strength. The model proposes that people process multiple signals via two cognitive modes: a simple (heuristic) cognitive mode and a deeper, more systematic mode. Furthermore, people tend to make decisions and judgments using low-effort rules (Drover et al., 2018), employing heuristic processes to make their decisions before considering the use of a systematic mode. Accordingly, the model predicts that when the signal set is either congruent or imbalanced incongruent, people will predominantly rely on heuristic processes as the set already provides some evidence of predominant valence (either positive or negative). However, to deal with a set of balanced incongruent entrepreneurial signals, they will need to rely on systematic processes, as the equal valence of positive and negative signals leaves them with insufficient cues to accurately assess the quality of campaigns. In this situation, interested investors may need to search for and process other relevant information and signals to make decisions. As suggested by the model, this reliance on systematic processing can be moderated by various forms of balanced incongruence. Investors tend to employ the systematic mode of processing in a weak form of balanced incongruence when competing signals are of low salience and have minimal impact on evaluation processes. Conversely, when faced with high ambiguity from highly salient competing signals in a strong form of balanced incongruence, they are more likely to abandon the systematic mode.

In the unique context of crowdfunding, where investment activities are publicly observable, prospective investors can learn more about the quality of a campaign by observing the behavior of other investors (Courtney et al., 2017; Nguyen et al., 2025). Indeed, the U.S. Exchange Act Release No. 70741 states that “A premise of crowdfunding is that investors would rely, at least in part, on the collective wisdom of the crowd to make better informed investment decisions.” Several studies (Burtch et al., 2021; Vismara, 2018a) on crowdfunding acknowledge the presence of herding as constituting the social proof of campaigns, whereby investors may use additional information to evaluate project quality. Based on these findings, we propose that the presence of herding may be important in campaigns with a balanced incongruent entrepreneurial signal set, as investors will employ the systematic mode to process further information. Conversely, the presence of herding may be less important in campaigns with a congruent or imbalance incongruent entrepreneurial signal set, as investors simply follow the heuristic mode. Our additional hypothesis posits that the impacts of herding may be more pronounced in a weak form (where investors are more likely to adhere to the systematic mode) compared with a strong form (where investors are highly likely to abandon the systematic mode) of balanced incongruence.

Our empirical analysis was conducted with a sample of 468 campaigns listed on Crowdcube, the largest UK equity crowdfunding platform, from 2014 to 2018. The core of our empirical methodology was to classify campaigns into three groups: congruence, imbalanced incongruence, and balanced incongruence—based on the predominant nature of signals from entrepreneurs in each campaign. To achieve this, we first identified a set of five signals from entrepreneurs that have a significant impact on the probability of campaign success. We then classified the campaigns into congruence when all signals are positive or negative, imbalanced incongruence when four (out of the five) signals are either positive or negative, and balanced incongruence for the remaining configurations. Following this, we utilized an advanced machine learning technique, random forest, to determine the importance of these signal scores and classified the campaigns into weak and strong forms of balanced incongruence. Subsequently, we used Li et al.’s (2022) calculation of herding intensity to measure the presence of herding, arguing that higher herding intensity is more observable and costly (Calic & Shevchenko, 2020; Connelly et al., 2011). We found evidence consistent with our hypotheses, in that campaign success is positively impacted by herding intensity in campaigns with balanced incongruent signal sets, yet there is no impact on campaigns with congruent and imbalanced incongruent signals. Consistent with the theory, we also found that the impacts of herding intensity on campaign success are more pronounced within a weak form of balanced incongruence than within a strong form. The results remained consistent across different robustness tests.

Our study makes several important contributions to the literature. First, it advances research on signaling in crowdfunding and entrepreneurial finance (Bafera & Kleinert, 2023; Colombo, 2021). Conceptually, we move beyond the conventional use of traditional signaling theory (Spence, 1973) by adopting a newly developed cognitive process model (Drover et al., 2018) to analyze signaling in equity crowdfunding. In this way, our study “speaks back” to traditional signaling theory on several important points. In particular, it reveals that the value of a signal is relative, in that it is contingent on the values of other signals. Furthermore, signals are evaluated by dynamic cognitive processes—namely, heuristics or a systematic mode in which investors may look for further signals to make their decisions.

Our study also contributes to a series of studies (Bapna, 2017; Huang et al., 2021) on the complementarity of signals by demonstrating that the complementary effect between entrepreneurial signals and social proof (i.e., interest from other investors) may depend on the nature of these signals. More specifically, our findings imply that the effect is more pronounced when entrepreneurial signals exhibit greater incongruence.

The study also makes unique methodological contributions to the research on signaling by employing machine learning techniques to estimate the relative importance of signals. This is significant as Drover et al. (2018) suggested that the valence of a set of signals is determined by the valence of each signal and its relative importance (weight) within the set. To the best of our knowledge, our study is the first in this line of literature to calculate the valence of a set of signals and conceptualize different forms of balanced incongruence using this approach.

Finally, our study contributes to the research on herding in crowdfunding (Chan et al., 2020; Dao et al., 2024; Zhang & Liu, 2012). Whereas previous studies primarily focus on establishing the existence of herding in crowdfunding, we go further by highlighting situations where herding behavior may be valuable. Specifically, we demonstrate that the herding behavior of early investors is used as a credible signal and social proof (Bapna, 2017) of campaign quality by subsequent investors when signals from entrepreneurs are mixed.

The paper is divided into five sections. Following this introduction, we review literature on signaling in equity crowdfunding in section “A Review of Literature on Signaling in Equity Crowdfunding,” and then develop the theoretical framework and hypotheses in section “Theory and Hypotheses.” Section “Research Context, Data, and Methodology” details the research context, data, and methodology. Finally, the empirical results and conclusion are presented in sections “Empirical Results” and “Conclusion,” respectively.

A Review of Literature on Signaling in Equity Crowdfunding

Spence (1973) developed the most important theoretical framework for understanding how signals and signaling operate in the context of equity crowdfunding. 1 Recent studies (e.g., Ahlers et al., 2015; Vismara, 2016; among others) adopted the theory to identify different signals from entrepreneurs that may be used by investors to evaluate the underlying quality of a campaign. First, Ahlers et al. (2015) identified equity retention and risk disclosure among entrepreneurs as effective signals about the quality of a campaign. Subsequently, Vismara (2016) confirmed the equity retention signal and further highlighted the importance of entrepreneurs’ social capital. In a more recent study, Kleinert and Mochkabadi (2022) identified entrepreneurs’ human capital as another crucial signal.

The development of literature has seen recent studies (Bapna, 2017; Butticè et al., 2022; Colombo et al., 2019) investigating the interactions among signals rather than focusing solely on the impacts of isolated signals. For instance, a study of signal sets in equity crowdfunding by Bapna (2017) revealed the complementary effects of product certification by expert intermediaries and prominent customers, and also product certification and social proof (investment of other investors in this venture). Specifically, investors were 72% (65%) more likely to invest if they were able to view the combination of product certification and prominent customers (product certification and social proof) than those who did not receive any of these signals. A recent study by Butticè et al. (2022) also revealed that investors in equity crowdfunding perceive signals from entrepreneurs in a set. In the relevant context of equity financing (Initial Public Offering (IPOs)), Colombo et al. (2019) examined the role of multiple signals and found that these do not necessarily substitute for one another but rather complement each other. They argued that firm quality in biotech IPOs is a multidimensional construct, as investors evaluate both the scientific potential of the technologies and products under development and their market potential. Given that different signals address diverse types of uncertainty and information asymmetry, investigating signal sets within the context of equity financing provides valuable insights.

In combination, these extant studies proved to be important in identifying different effective signals in equity crowdfunding and how they interact; however, traditional signaling theory provides only a limited understanding of how investors make decisions when signals are incongruent. We therefore adopted a novel theoretical framework to investigate investors’ decisions when signals from campaigns are noisy.

Theory and Hypotheses

The Theory of Cognitive Processing of Signals: A Dual Process Framework

Recent developments in signaling research expand the boundaries of traditional signaling theory by drawing on insights from cognitive science (Evans, 2006, 2008), within which the dual processing theory states (Epstein, 1994; Evans, 2007; Frankish & Evans, 2009) that the human mind processes information and forms judgments through two different systems. One system is intuitive thinking, which is a low-effort mode of information processing used to make rapid judgments, while the other relies on analytic thinking—a high-effort mode of information processing using logical reasoning to make thoughtful judgments (Franzoni & Tenca, 2020). This analytic thinking system requires evidence to gauge the validity of given information and ultimately believe or disregard it. Franzoni and Tenca (2020) demonstrated that system 2 (analytic thinking system) draws on all pieces of relevant information to make decisions based on a logical and deductive analysis.

Based on the perspectives from cognitive research, Drover et al. (2018) developed a heuristic-systematic model theorizing how people will process multiple signals (signal set) from organizations. Specifically, it proposes that signals will be processed via two cognitive modes, the first of which involves fast, simple, and almost subconscious (heuristic) cognitive processes, while the second relies on slow, deep, conscious, and deliberate (systematic) processes. Another key tenet of the model is the desired level of confidence among decision-makers, conceptualized as the degree of confidence about organizations that one aims to achieve from interpreting the signals. Importantly, the comparison between the level of desired confidence and the actual judgmental confidence gained from processing relevant signals and information about the organization will determine the signal processing mode that follows low-effort decisions (Drover et al., 2018). Specifically, if decision-makers can achieve their desired judgmental confidence level through the heuristic mode of interpreting signals, they will save cognitive energy by not using the systematic mode. The systematic cognitive mode will, however, be used when the heuristic mode cannot lead to the desired level of confidence.

Following the model illustrated in figure 1, Drover et al. (2018) were able to explain how people process sets of multiple signals. They suggested that when signals are uniformly congruent, that is, signals unanimously communicate the same information regarding organizational quality (either positive or negative), or imbalanced incongruent, where one type of signal (either positive or negative) is dominant, decision-makers are more likely to rely on heuristic processing due to the large positive–negative valence gap. However, when the signal set is balanced incongruent, that is, where positive and negative signals are relatively equal in valence, the heuristic mode may not be sufficient to achieve the desired level of confidence. Consequently, decision-makers will need to trigger the systematic mode, engaging in a more in-depth analysis to make sense of these signals.

Theoretical framework of cognitive processing.

Within the framework of the model, investors’ decision-making in contexts of balanced incongruence—when adopting a systematic approach—is inherently complex and may be shaped by the characteristics of competing signals within the set. Drover et al. (2018) distinguished two forms of imbalanced incongruence: (a) the weak form, where competing signals have relatively low salience and minimal impact on the evaluation processes; and (b) the strong form, where highly salient competing signals—both positive and negative—are present. Specifically, when the balanced incongruent signal set is in a weak form, the cognitive requirement is significant but manageable; hence, investors will rely more on systematic processing. However, when the signal set is in a strong form, the ambiguity is too high. Thus, it is likely that investors will ultimately abandon further systematic processing.

Hypotheses

Entrepreneurial Signal Set, Herding, and Investor Behavior

The novel model by Drover et al. (2018) provides the essential theoretical framework for investigating the decisions made by investors in equity crowdfunding when interpreting the collection of signals from entrepreneurs. Following the framework, we argue that when signals from entrepreneurs are congruent or imbalanced incongruent, investors in equity crowdfunding will use heuristic cognitive processing to interpret the signal sets. However, when entrepreneurial signals are balanced incongruent, that is, signals convey conflicting messages about the quality of campaigns (mix of an equal number of positive or negative signals), investors may need to rely on all relevant information (Franzoni & Tenca, 2020) and use the systematic mode of processing to come to their decisions.

Within the unique context of crowdfunding, investors may be able to learn about campaign quality by observing the behavior of their peer investors (Chan et al., 2020; Li et al., 2022; Vismara, 2018a; Zhang & Liu, 2012). Indeed, Vismara (2018a) noted that “…late investors make decisions based not only on the observable characteristics of the campaigns and their proponents, but they also consider of previous investors” (p. 477). Courtney et al. (2017) contended that opinions from other backers can be seen as a third-party endorsement of campaign quality and founder credibility. Following Li et al. (2022), we argue that the presence of herding can be seen by investors as a credible signal about the quality of campaigns. Indeed, herding is widely seen as social proof of a campaign (Bapna, 2017; Burtch et al., 2013, 2021), whereby investors believe that the herds “may know something better” (Bernstein et al., 2017; Hornuf & Neuenkirch, 2017; Song et al., 2020). More importantly, herding is inherently different from signals from entrepreneurs as it represents unintentional and objective opinions from other investors (Milosevic, 2018) and can be observed at a different (later) time.

Based on such theories, we argue that when signals from entrepreneurs are congruent or imbalanced incongruent, investors will save their “cognitive efforts” by predominantly relying on entrepreneurial information. The presence of herding will not have any impact on investors’ decisions and the probability of campaign success. When positive and negative signals from entrepreneurs are balanced, investors will need to process all relevant information, including that from previous investors, to make their decisions. Therefore, the presence of herding will be a decisive factor in determining the probability of those campaigns being successful. Accordingly, our hypotheses were as follows.

Weak Form and Strong Form of a Balanced Incongruent Signal Set

To further determine whether the heuristic-systematic model helps to explain the decisions of investors when processing an entrepreneurial signal set, we investigated the impact of herding on the likelihood of crowdfunding campaigns being successful within balanced incongruent entrepreneurial signal sets. Given the two forms of balanced incongruence, investors are more likely to rely on systematic processing in the weak form, whereas in the strong form, they tend to abandon systematic processing due to heightened ambiguity. Thus, we contend that the presence of herding may have more pronounced impacts on the likelihood of crowdfunding campaigns being successful when investors face balanced incongruence in a weak form rather than in a strong form.

Research Context, Data, and Methodology

Research Context

Equity crowdfunding is characterized by high levels of information asymmetry where entrepreneurs may know more about campaign quality than investors (Johan & Zhang, 2020; Lukkarinen et al., 2016; Vismara, 2016). In the context of Crowdcube—a prominent equity crowdfunding platform in the UK, entrepreneurs who intend to raise funds from the crowd need to provide different information about their campaigns, such as a description of the business, entrepreneurial team, and the offerings (Vismara, 2018b) publicly available on the platform at the beginning of fundraising campaigns (Nguyen et al., 2019). All potential investors have access to the information (signals) from entrepreneurs, based upon which they can make their investment decisions anytime during the typical 30-day fundraising period.

A unique feature of an online fundraising platform like Crowdcube is that potential investors and visitors can observe the investment activities of other (previous) investors. Investors in the final few days of the funding campaign may therefore combine the signals from both entrepreneurs and previous investors to make their decisions.

Data

Data were collected by scraping daily funding information from campaigns listed on Crowdcube in the period from January 2014 to January 2018. From the initial sample, we removed campaigns with no information on daily funding, as this information was essential for our measurement of herding intensity. The same applied to debt fundraising campaigns, as our focus was on equity fundraising. After dealing with outlier values (removing campaigns which had fewer than 5 fundraising days—too short—or more than 100 days—too long—as they may have had different stories or characteristics), we were left with 468 campaigns, comprising 172 that were successful (36.75%) and 296 that had failed (63.25%). For our analysis, we also excluded the days during the overfunding period, namely the period after the campaign successfully reached its original funding target, as the motivations of investors in this period are fundamentally different from those in the funding period. We supplemented data on campaigns scraped from the platform with information about companies collected from the Orbit Database and Intellectual Property Office 2 for trademark status.

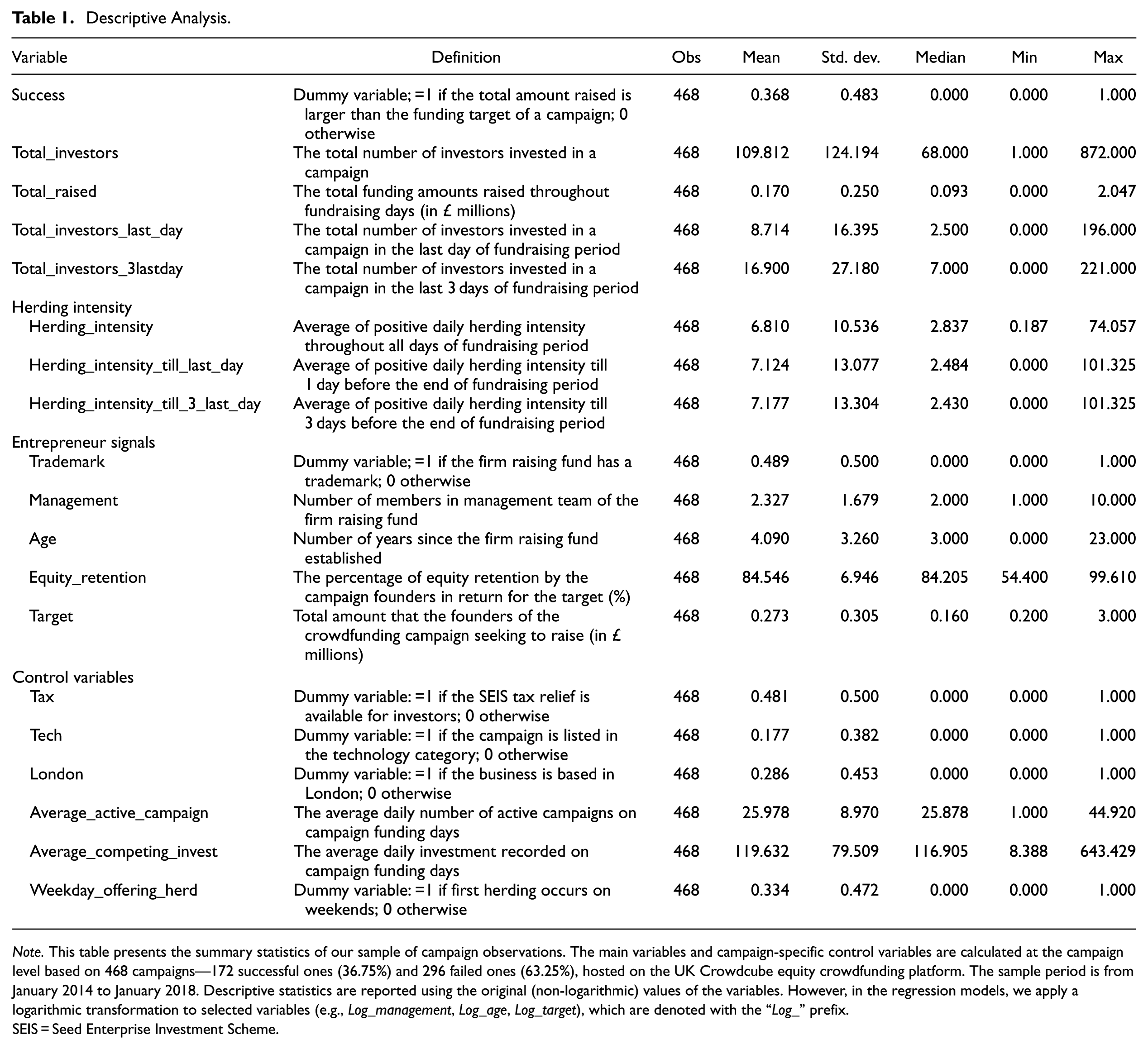

Table 1 presents descriptive statistics along with definitions of the variables used in our study. Our analysis revealed that the average total number of investors across all 468 campaigns was 109.81—slightly higher than the average of 84 reported by Vismara (2016). The campaigns in our sample, on average, attracted £170,408 in funding, with some campaigns raising over £2 million. In terms of entrepreneurial characteristics, approximately half of the campaigns possessed intellectual capital and trademarks. Our sample included firms raising funds that have small management teams with an average of 2.33 members and a maximum of 10. The firms in our sample were also in the early stages of their business lifecycle, with an average age of 4 years and a maximum age of 23 years. Founders retained an average ownership of 84.55%.

Descriptive Analysis.

Note. This table presents the summary statistics of our sample of campaign observations. The main variables and campaign-specific control variables are calculated at the campaign level based on 468 campaigns—172 successful ones (36.75%) and 296 failed ones (63.25%), hosted on the UK Crowdcube equity crowdfunding platform. The sample period is from January 2014 to January 2018. Descriptive statistics are reported using the original (non-logarithmic) values of the variables. However, in the regression models, we apply a logarithmic transformation to selected variables (e.g., Log_management, Log_age, Log_target), which are denoted with the “Log_” prefix.

SEIS = Seed Enterprise Investment Scheme.

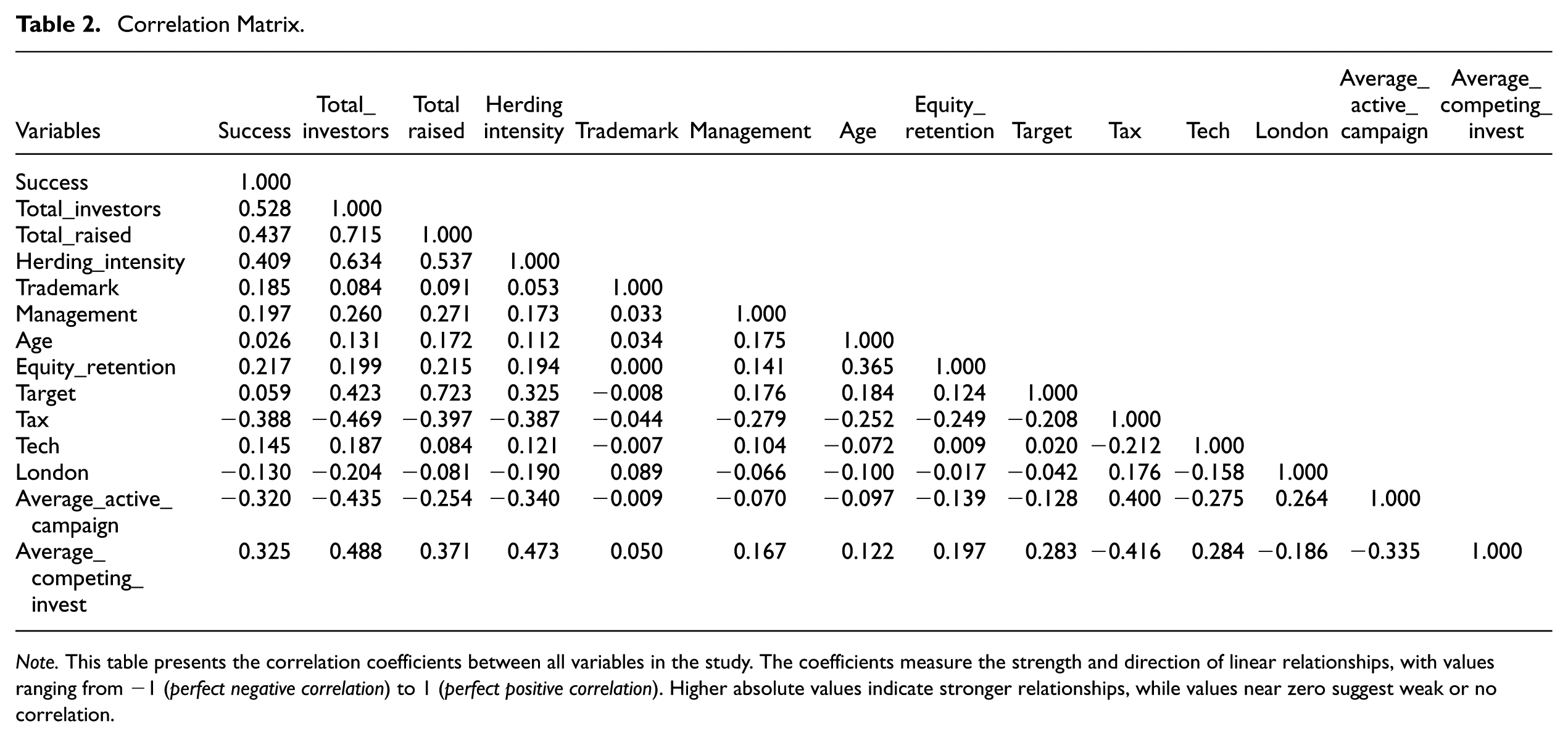

The results of the correlation matrix among independent variables are depicted in Table 2. Multicollinearity among variables was unlikely to be a concern, as all statistical results were lower than 0.5. We also conducted variance inflation factors analysis, the results of which confirmed the validity of the variable sets.

Correlation Matrix.

Note. This table presents the correlation coefficients between all variables in the study. The coefficients measure the strength and direction of linear relationships, with values ranging from −1 (perfect negative correlation) to 1 (perfect positive correlation). Higher absolute values indicate stronger relationships, while values near zero suggest weak or no correlation.

Methodology

Congruent and Incongruent Sets of Signals From Entrepreneurs

To empirically test our hypotheses, we needed to be able to identify campaigns with congruent and imbalanced/balanced incongruent signals from entrepreneurs. Our empirical strategy was as follows. First, we followed the literature (Ahlers et al., 2015; Lim & Busenitz, 2020; Vismara, 2016) to identify the set of potential signals from entrepreneurs. 3 In particular, based on the theoretical framework used in Ahlers et al. (2015), we used management team size as the signal of human capital and social capital of entrepreneurs, and possession of a trademark as the signal of intellectual capital. Ahlers et al. (2015) and Vismara (2016) argued that entrepreneurs’ willingness to invest in their own business can effectively signal their venture quality. We thus used equity retention as the signal of venture quality. Firm age may also be an effective signal from entrepreneurs, as investors may perceive such firms as having higher growth potential and being more dynamic (Lawless, 2014). Moreover, although a higher target may signal strong growth ambition, suggesting that the entrepreneur has an expansive plan for scaling the business, it may also raise concerns about higher risk, particularly regarding the entrepreneur’s managerial capability and ability to efficiently allocate and utilize the requested funds.

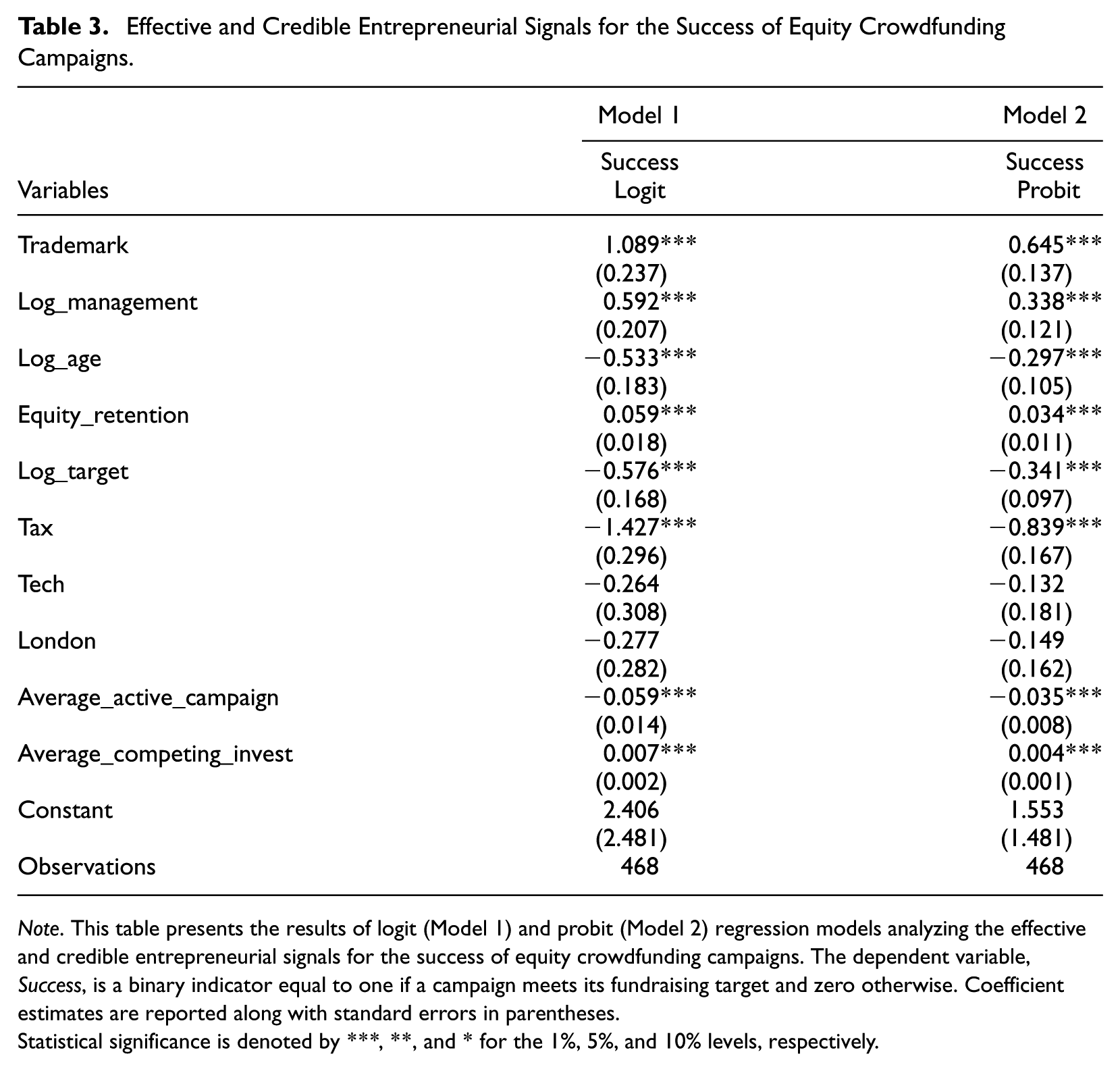

After selecting these signals from their theoretical foundation, we assessed their empirical validity in our specific sample by examining their impacts on the likelihood of campaign success. Specifically, we ran a regression with Success as the dependent variable—a dummy variable with a value of one if campaigns were able to reach the target set by entrepreneurs at the beginning of the campaigns and zero otherwise. 4 Because Success was a dummy variable, we employed logit (and probit) regression with robust standard error to estimate the effectiveness of different entrepreneurial signals on the likelihood of campaign success. The results from empirical models reported in Table 3 confirm the empirical validity of these signals as all the selected signals had statistically significant impacts on success at a 1% level. 5

Effective and Credible Entrepreneurial Signals for the Success of Equity Crowdfunding Campaigns.

Note. This table presents the results of logit (Model 1) and probit (Model 2) regression models analyzing the effective and credible entrepreneurial signals for the success of equity crowdfunding campaigns. The dependent variable, Success, is a binary indicator equal to one if a campaign meets its fundraising target and zero otherwise. Coefficient estimates are reported along with standard errors in parentheses.

Statistical significance is denoted by ***, **, and * for the 1%, 5%, and 10% levels, respectively.

Importantly, from the results we were able to categorize each of these five effective signals of a particular campaign into positive or negative valence. For instance, the results indicate that if everything else is kept equal, campaigns possessing a trademark are more likely to be successful than campaigns without such a trademark. Possessing a trademark conveys a positive signal about a campaign’s quality to investors. Thus, when a campaign (does not) possess a trademark, its signal valence of trademark will be (negative) positive. For other signals (i.e., size of management team, equity retention, firm age, and target), we used the median value of the sample to determine the valence of the signals. Specifically, compared with the median value of all campaigns, a larger number of members in the management team, higher equity retention, lower firm age, and lower target were considered positive signals and vice versa. For each campaign, we assigned signals with positive (negative) valence a valence score of one (−1).

We were then able to separate projects into congruence, imbalanced incongruence, and balanced incongruence based on the valence of individual signals. Specifically, a campaign was classified as congruent if all entrepreneurial signals shared the same valence. A campaign was deemed imbalanced incongruence when the majority (four) of its entrepreneurial signals shared the same valence, either predominantly positive or negative. Conversely, a campaign was categorized as balanced incongruence if its entrepreneurial signals were a mix of positive and negative, such as three positive signals and two negative ones (or vice versa). Following this method, we were left with 158 campaigns that had congruent or imbalanced incongruent signal sets and 310 campaigns that had a balanced incongruent signal set.

Imbalanced Incongruence in a Weak and Strong Form

To distinguish between the two forms of balanced incongruence, we employed an advanced method to assess the importance of each signal. This is essential because, within a mix of positive and negative signals, the salience of each signal can differ under systematic assessment, with certain signals having a more significant impact on investors than others. We employed an advanced machine learning technique, random forest, to measure the relative importance of each signal (see e.g., Cao et al., 2019, Wang et al., 2022). Random forest was adopted due to its advantages in ranking signals compared with other conventional methods, including leveraging multiple trees rather than individual trees, and handling missing data and non-linear relationships. Unlike linear models, which assume a fixed relationship between inputs and outputs, random forests leverage an ensemble of decision trees to uncover hidden patterns and interactions and dynamically measure feature (signal) importance.

To assess the relative importance of each signal, we implemented a Random Forest model using Python’s Scikit-Learn package. This model consists of an ensemble of multiple decision trees, where each tree is trained on a randomly sampled subset of a larger sample. For our research, a single decision tree was constructed using a sample of 314 crowdfunding campaigns (corresponding to a training set size of 67% and a test set size of 33%), randomly selected from our full sample of 468 campaigns, as input data.

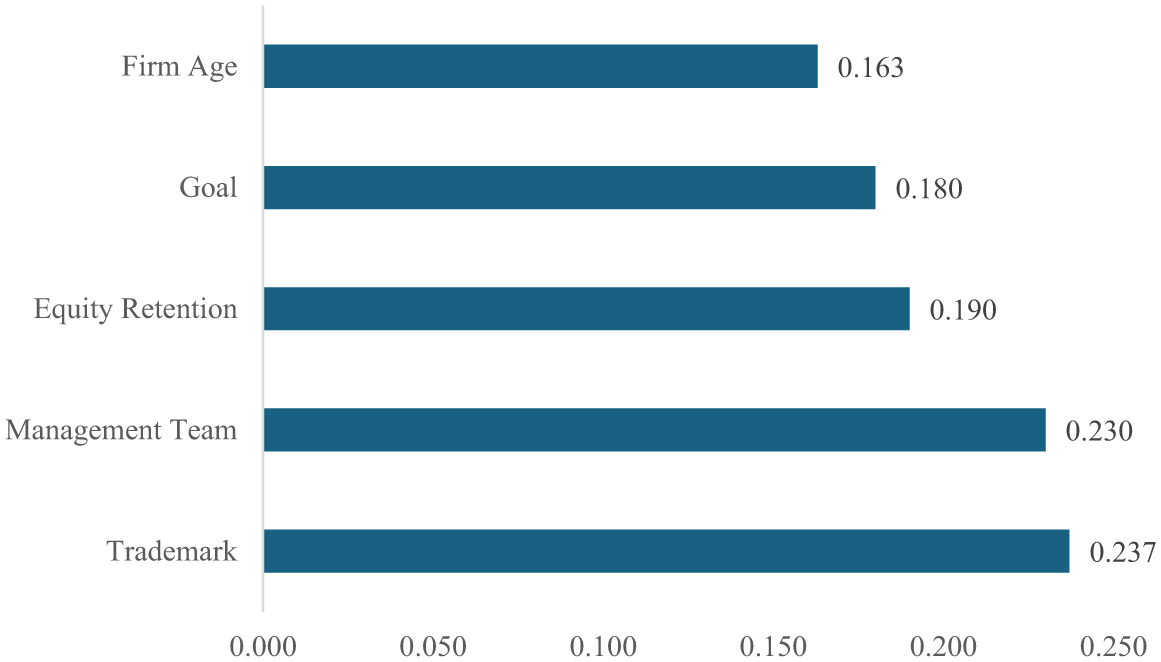

Within each decision tree, the model creates nodes using the five signals—equity retention, firm age, patent, management team size, and funding target—as splitting variables. Each node in the tree represents a decision rule that divides the campaigns into two groups (i.e., high equity retention—positive signal valence; low equity retention—negative signal valence). The goal of each split is to choose a signal that makes the resulting subgroups more homogeneous, as measured by the reductions in Gini impurity, 6 with respect to the outcome variable—crowdfunding success or failure. At the first node (root node), the model calculates the reductions in Gini impurity for each signal; following this, the signal with the largest drop in Gini impurity is selected because it is the most effective (the most important signal) in separating successful from unsuccessful campaigns. The process then continues with other nodes to determine the importance of (other) signals until the tree reaches its maximum depth. Each time a signal (e.g., equity retention, firm age) is used to separate campaigns in a node, the model records this reduction in Gini impurity. This value is then weighted by the ratio of the number of campaigns separated by that signal over the total number of campaigns in the tree and then summed across all trees in the forest to compute the overall importance of the signal. Finally, the importance scores are normalized so that they sum to one, enabling direct comparison across features. The resulting signal importance values are reported in Figure 2.

Signal importance score.

Using the signal valence score and signal importance score, the signal set salience score is calculated as:

Following Equation (1), the signal set salience score will range from −1 (all negative signals) to 1 (all positive signals). Accordingly, a campaign is allocated to a strong form if its score belongs to the top 75th or bottom 25th (large salience) percentiles. A campaign is placed in a weak form if its score is between the 25th and 75th (small salience) percentiles. Following this method, in 310 campaigns of balanced incongruence, 137 campaigns belonged to balanced incongruence in a weak form, and 173 campaigns belonged to balanced incongruence in a strong form.

Measuring Signals From Herding

According to signaling theory (Spence, 1973), the presence of herding can generate (more) effective signals about a campaign’s underlying quality to subsequent investors when it is more observable and costly. We proxied the observability and costliness of herding through the measurement of herding intensity, as in Li et al. (2022). Following Lakonishok et al. (1992), herding intensity, denoted as Lakonishok, Shleifer, and Vishny (LSV) measure, was calculated as the difference between the observed deviation in daily trading activity and the expected deviation under the assumption of no herding behavior. 7 Given that daily funding amounts follow a Poisson distribution (Li et al., 2022), the mean and expected deviation can be derived accordingly and incorporated into the original LSV formulation. From the calculation, a higher herding intensity implies a greater level of abnormal daily funding, making herding behavior more visible and noticeable to other investors. Furthermore, higher herding intensity requires larger contributions from investors, thus making herding intensity more costly to attain. Specifically, the daily herding intensity of campaign i at day t is estimated as follows.

where R i,t denotes the number of daily funding amounts of campaign i at day t, and the mean of the Poisson distribution is estimated as follows:

A larger daily LSV i,t indicates stronger herding intensity, while a non-positive LSV i,t signifies no herding on the day. For each campaign, a herding signal is constructed by averaging the positive daily LSV during the campaign period.

Estimation Model

We empirically examined our hypotheses by estimating the impacts of our measure of herding intensity on the likelihood of campaign success with different configurations of signal sets from entrepreneurs. Because the presence of herding may also be driven by signals from entrepreneurs, we used the system of two stages developed by Vismara (2016). Accordingly, in stage 1, we estimated the effect of entrepreneurial signals and other control variables (campaign listing characteristics) on herding intensity, while in stage 2, we investigated whether success probability is influenced by both herding intensity and the same set of these signals and control variables. The stage 2 results will answer our research question.

For the estimation method, we adopted generalized structural equation modeling (GSEM), which has previously been used in a study by Vismara (2016) on crowdfunding. Although traditional structural equation modeling can handle continuous dependent variables, GSEM offers various treatments. While OLS was used in stage 1 due to herding intensity being a continuous dependent variable, stage 2 was tested using a logit estimation, focusing on the probability of those campaigns being successful.

To ensure the validity of two-stage models, we employed an instrumental variable (Weekday_offering_herd), which took a value of one if the first herding occurs on weekends and zero otherwise. We argue that the instrumental variable is valid as it influences the level of herding intensity but does not have any effect on campaign success, either directly or through other channels. First, regarding the relevance of the instrument, we follow the theoretical justification from Vismara (2018a) to argue that if first herding occurs on weekends, investors will pay less attention to this signal, leading to lower herding intensity than when first herding occurs on weekdays. We empirically confirmed the relevance of the instrument by reporting a first-stage F-statistic of 20.35, exceeding the conventional threshold of 10. Second, our instrument satisfies the exogeneity condition. Indeed, the occurrence of the first herding is essentially random and independent of any strategic decision-making on the part of the entrepreneur, such as the timing of the launching day, which could influence campaign outcomes. Furthermore, there is no theoretical background or empirical evidence to suggest that the timing of the first herding may affect a campaign’s success. Therefore, any effect of the instrument on campaign success operates solely through its impact on herding intensity, ensuring the exogeneity of our variable.

We employed two specifications to unpack the impact of herding on different configurations of the entrepreneurial signal set. First, we adapted the interaction model (Specification A) in Equation (4.1) by adding a new binary variable, Imbalanced_Incongruence, which was assigned a value of 1 if the campaign belongs to imbalanced incongruence and 0 otherwise. Second, we used a subgroup (Specification B) with Equation (4.2) in two separate samples: (a) congruence and imbalanced incongruence and (b) balanced incongruence.

Specification A (Interaction Model)

Specification B (Subgroup Model)

Regarding the interaction models (Specification A), hypothesis 1a and hypothesis 1b are supported when

Following the literature (Nguyen et al., 2019; Vismara, 2018a), a range of variables (

Empirical Results

Main analysis of Herding and Different Configurations of Entrepreneurial Signal Sets

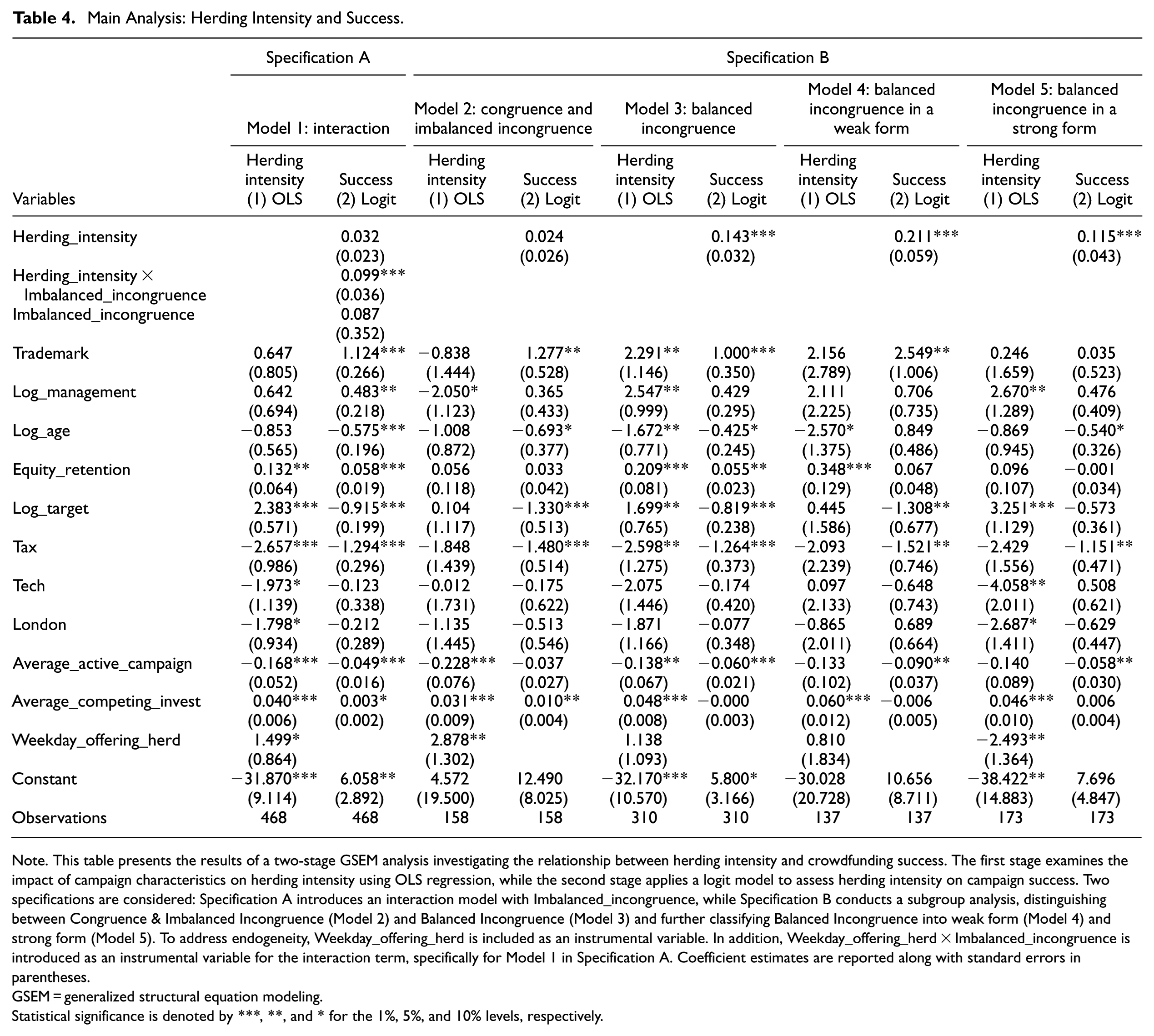

We report the main results in Table 4 for both interaction models (Model 1) and subgroup models (Models 2 & 3). Because we utilized the GSEM approach, which involves two stages per model, we report both the two distributions of dependent variables and their corresponding results. First, we focused on interaction models to test whether there is a difference in effect between (a) congruence and imbalanced Incongruence and (b) balanced incongruence. The positive and significance interaction terms between the dummy variable Balanced_incongruence and Herding_intensity revealed that herding has a significant and stronger positive effect on the balanced incongruence group than on the congruent group and imbalanced incongruence group. This result supports hypothesis 1b.

Main Analysis: Herding Intensity and Success.

Note. This table presents the results of a two-stage GSEM analysis investigating the relationship between herding intensity and crowdfunding success. The first stage examines the impact of campaign characteristics on herding intensity using OLS regression, while the second stage applies a logit model to assess herding intensity on campaign success. Two specifications are considered: Specification A introduces an interaction model with Imbalanced_incongruence, while Specification B conducts a subgroup analysis, distinguishing between Congruence & Imbalanced Incongruence (Model 2) and Balanced Incongruence (Model 3) and further classifying Balanced Incongruence into weak form (Model 4) and strong form (Model 5). To address endogeneity, Weekday_offering_herd is included as an instrumental variable. In addition, Weekday_offering_herd × Imbalanced_incongruence is introduced as an instrumental variable for the interaction term, specifically for Model 1 in Specification A. Coefficient estimates are reported along with standard errors in parentheses.

GSEM = generalized structural equation modeling.

Statistical significance is denoted by ***, **, and * for the 1%, 5%, and 10% levels, respectively.

We then examined subgroup models, Model 2 and Model 3, and observed that herding does not appear to play any key role in the progress of an investor’s assessment in the congruence and imbalanced incongruence group, as demonstrated by the non-significance of Herding_intensity_till_last_day in stage 2 of Model 2. This finding aligns with hypothesis 1a, which posits that when investors face congruent and imbalanced incongruent signal sets, they adopt heuristic cognitive processes and do not necessarily rely on herding signals to make funding decisions. However, regarding the balanced incongruence group, we identified the significance and positive sign of Herding_intensity in stage 2 of Model 3. Specifically, economic significance is illustrated by the fact that one unit increase in herding intensity would lead to a 14.3% increase in success probability, ceteris paribus. These results indicate that herding may contribute to attracting more funding in balanced incongruence groups. This line of results supports hypothesis 1b, which proposes that when investors face a balanced incongruent signal set, they adopt systematic cognitive processes and rely on herding signals to make funding decisions.

The empirical results in Models 4 and 5 (Table 4) support hypothesis 2, as they demonstrate that the presence of herding will have a more pronounced effect on campaign success when investors face balanced incongruence in a weak form rather than in a strong form. Specifically, herding intensity is significant in both models. Furthermore, the coefficient for herding intensity in a weak form of balanced incongruence is 0.211, which is substantially higher than the 0.115 coefficient observed in a strong form of balanced incongruence.

Taken together, the results from our main analysis are consistent with the theoretical framework of cognitive processing for signal sets, as illustrated by Drover et al. (2018). We endorse the argument of Franzoni and Tenca (2021) regarding two-step cognitive processing of investors in relation to crowdfunding: intuitive thinking (heuristic processes) and analytic thinking (systematic processes). Thus, crowdfunding investors may utilize step two (analytic thinking, systematic processes) when thinking about the value of the signal set delivered by entrepreneurs. We found that herding may bring credible third-party endorsements to investors, in line with numerous studies (Bernstein et al., 2017; Burtch et al., 2013, 2021; Hornuf & Neuenkirch, 2017; Song et al., 2020), resolving investors’ conflicting views of the entrepreneurial signal set.

Extending the Analysis

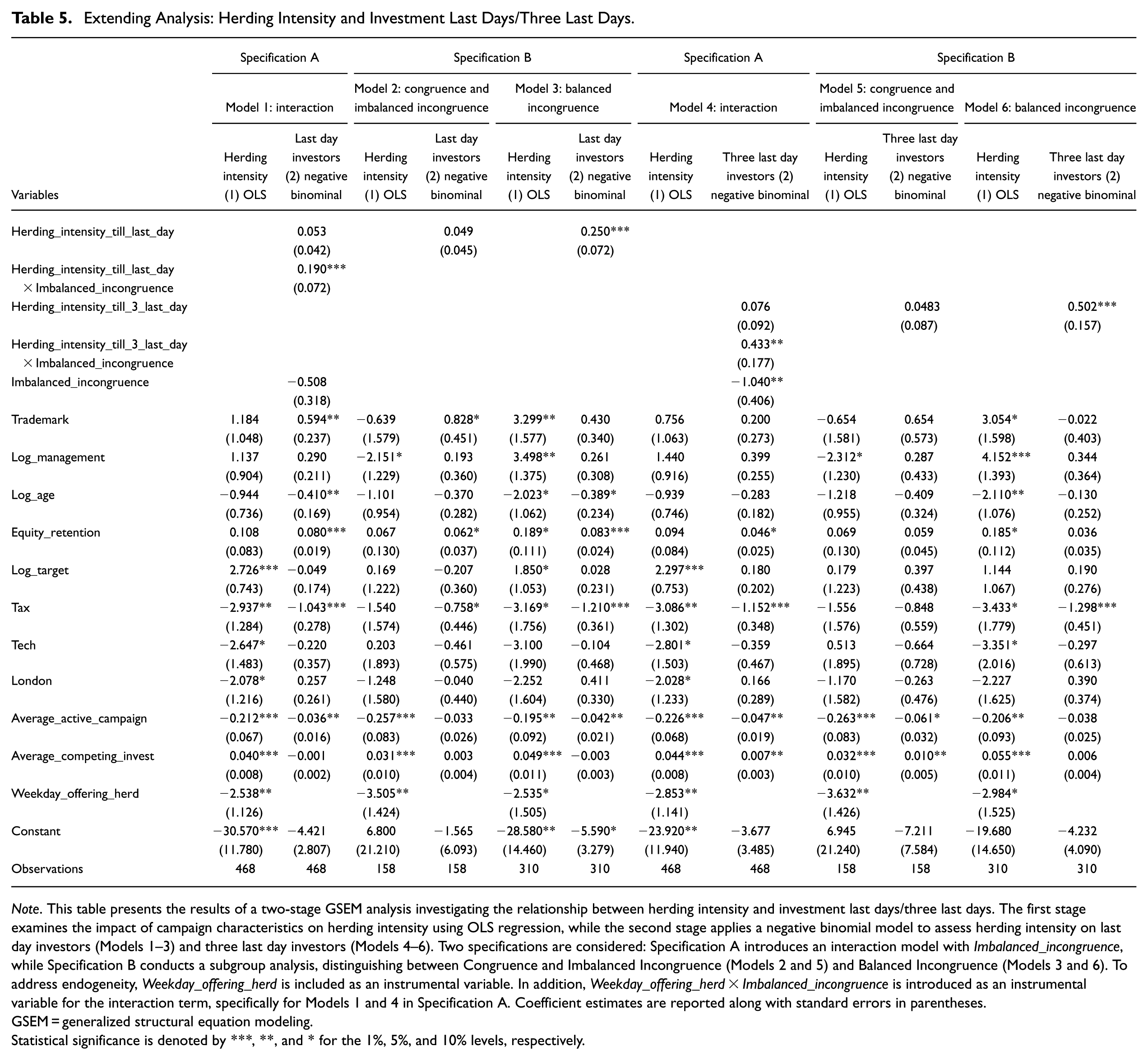

One concern arising from the results is that the measurement of herding intensity may correlate with the number of investors in campaigns, which will impact their probability of success. We confirmed the robustness of our results by extending our analysis to investigate whether the measurement of herding intensity (in previous days) impacts different measures of investment activities in the final days of campaigns.

Arguably, the unique operation of equity crowdfunding platforms implies that late investors in equity crowdfunding make decisions based not only on observing signals from campaign founders but also by considering the investment activities of previous investors (Vismara, 2018a). Thus, herding, a signal from previous investors, will be more likely to influence the decisions of these late investors. We used investors on the last day and the final 3 days of the funding period as two proxies for late investors. We empirically examined this hypothesis by estimating the impacts of our measure of herding intensity before the final 3 days and before the last day on investment activities in the final 3 days and last day of funding campaigns, respectively.

Following the estimation in the main analysis, we used the two-stage system to address potential endogeneity issues that arise, given that herding intensity may also be driven by signals from entrepreneurs. A key difference from the main analysis is that our calculation of herding intensity did not include investment activities in the last few days; this ensured that the correlation was not influenced by the estimation methods of these variables.

Table 5 shows results that are consistent with the main analysis, in that the funding decisions of later investors are driven by herding in the balanced incongruence group (Models 3 and 6), but not the congruence and imbalanced incongruence group (Models 2 and 5). We identified positive and significant interaction terms in Models 1 and 4. While Models 3 and 6 showed a positive and significant effect of herding (balanced incongruence group), the herding variable in Models 2 and 5 (congruence and imbalanced incongruence group) was not significant. More specifically, in terms of economic significance, one unit increase in herding intensity on previous days leads, on average, to a 25% increase in the number of investors in the last day and a 50% increase in the final 3 days, respectively. These results suggest that when faced with conflicting signals, later investors pay attention to herding to resolve these conflicts and invest more when a stronger herding signal is observed.

Extending Analysis: Herding Intensity and Investment Last Days/Three Last Days.

Note. This table presents the results of a two-stage GSEM analysis investigating the relationship between herding intensity and investment last days/three last days. The first stage examines the impact of campaign characteristics on herding intensity using OLS regression, while the second stage applies a negative binomial model to assess herding intensity on last day investors (Models 1–3) and three last day investors (Models 4–6). Two specifications are considered: Specification A introduces an interaction model with Imbalanced_incongruence, while Specification B conducts a subgroup analysis, distinguishing between Congruence and Imbalanced Incongruence (Models 2 and 5) and Balanced Incongruence (Models 3 and 6). To address endogeneity, Weekday_offering_herd is included as an instrumental variable. In addition, Weekday_offering_herd × Imbalanced_incongruence is introduced as an instrumental variable for the interaction term, specifically for Models 1 and 4 in Specification A. Coefficient estimates are reported along with standard errors in parentheses.

GSEM = generalized structural equation modeling.

Statistical significance is denoted by ***, **, and * for the 1%, 5%, and 10% levels, respectively.

Robustness Analysis

Alternative Proxies

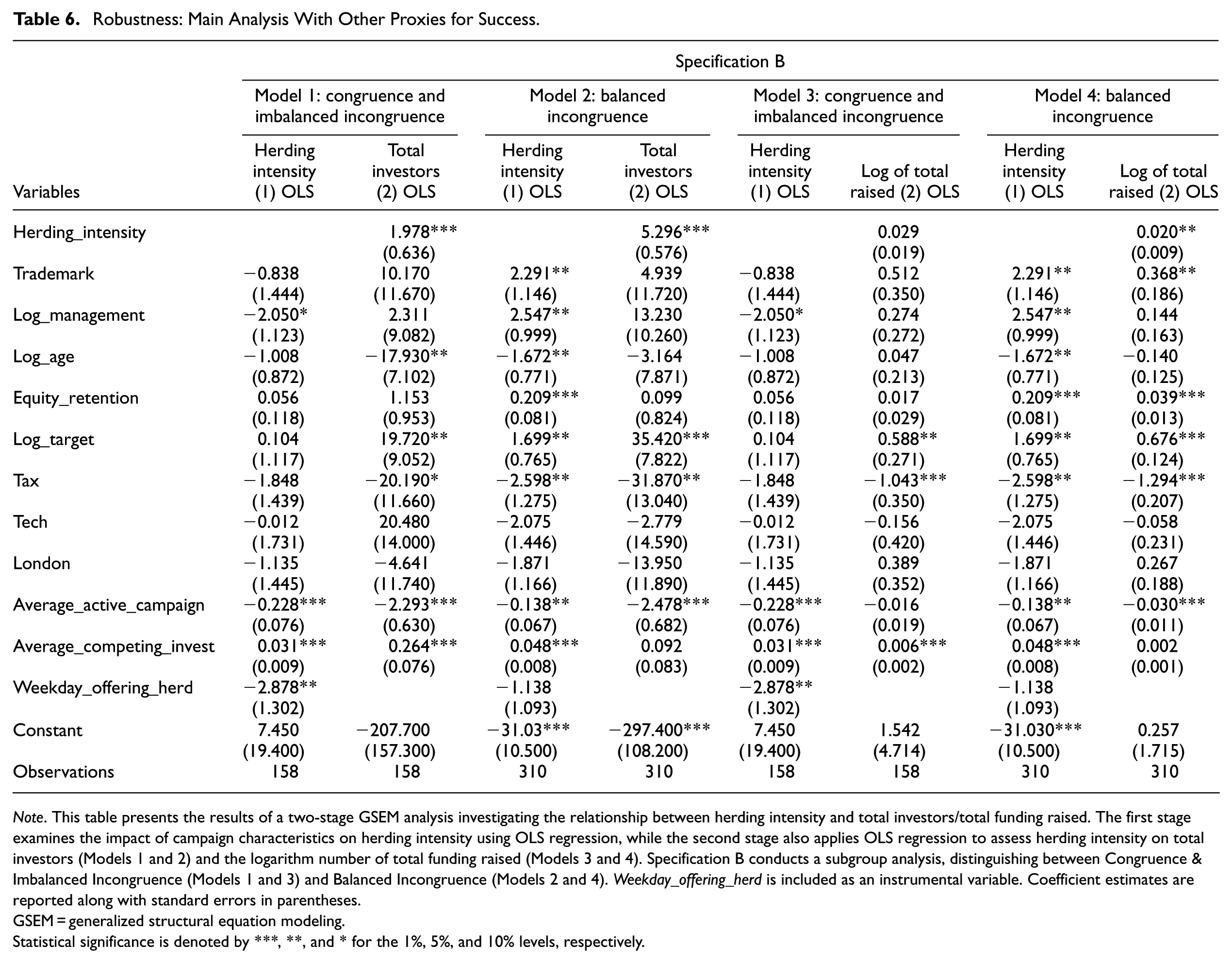

To further ensure the robustness of results, we replicated the main analysis (Table 4) by using other proxies for success; namely, total number of investors and total amount of funding raised, the results of which are reported in Table 6b. These two proxies are consistent with numerous studies on equity crowdfunding (e.g., Ahlers et al., 2015; Vismara, 2018a). The results indicate that the impacts of herding on the total number of investors in the balanced congruence group are significantly stronger than in congruence and imbalanced incongruence group. Moreover, regarding the total amount of funding raised, herding intensity continued to be positive and statistically significant in the balanced incongruence group, thereby corroborating the consistency of the primary findings.

Robustness: Main Analysis With Other Proxies for Success.

Note. This table presents the results of a two-stage GSEM analysis investigating the relationship between herding intensity and total investors/total funding raised. The first stage examines the impact of campaign characteristics on herding intensity using OLS regression, while the second stage also applies OLS regression to assess herding intensity on total investors (Models 1 and 2) and the logarithm number of total funding raised (Models 3 and 4). Specification B conducts a subgroup analysis, distinguishing between Congruence & Imbalanced Incongruence (Models 1 and 3) and Balanced Incongruence (Models 2 and 4). Weekday_offering_herd is included as an instrumental variable. Coefficient estimates are reported along with standard errors in parentheses.

GSEM = generalized structural equation modeling.

Statistical significance is denoted by ***, **, and * for the 1%, 5%, and 10% levels, respectively.

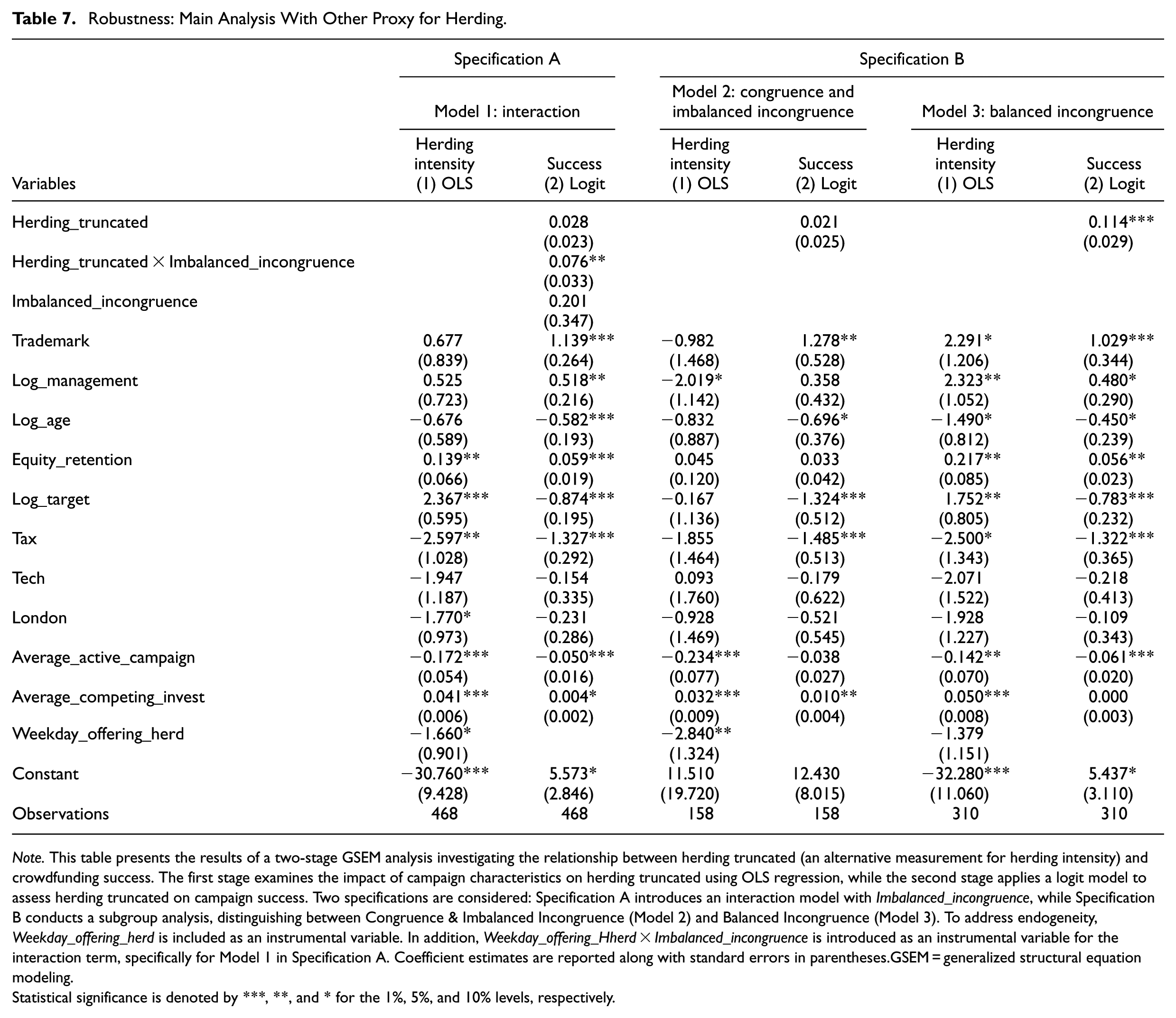

Alternative Measurement of Herding Intensity

To advance from Li et al. (2022)’s measurement of herding intensity, we propose a new proxy to test robustness. While Li et al. (2022) used a Poisson distribution, our research applied a zero-truncated Poisson distribution to exclude the effect of multiple zero funding days. This is also consistent with several previous studies on herding in crowdfunding which have suggested the presence of thin trading volumes dominated by many days across the entire funding campaign with no investment activity (Nguyen et al., 2019; Vismara, 2018a). The results in Table 7 are consistent with a new proxy for herding intensity. The formula for calculating daily LSV following a zero-truncated Poisson distribution is as follows:

where R i,t denotes the number of funding amounts of campaign i at day t, and the mean of zero-truncated Poisson distribution is calculated as:

Robustness: Main Analysis With Other Proxy for Herding.

Note. This table presents the results of a two-stage GSEM analysis investigating the relationship between herding truncated (an alternative measurement for herding intensity) and crowdfunding success. The first stage examines the impact of campaign characteristics on herding truncated using OLS regression, while the second stage applies a logit model to assess herding truncated on campaign success. Two specifications are considered: Specification A introduces an interaction model with Imbalanced_incongruence, while Specification B conducts a subgroup analysis, distinguishing between Congruence & Imbalanced Incongruence (Model 2) and Balanced Incongruence (Model 3). To address endogeneity, Weekday_offering_herd is included as an instrumental variable. In addition, Weekday_offering_Hherd × Imbalanced_incongruence is introduced as an instrumental variable for the interaction term, specifically for Model 1 in Specification A. Coefficient estimates are reported along with standard errors in parentheses.

GSEM = generalized structural equation modeling.

Statistical significance is denoted by ***, **, and * for the 1%, 5%, and 10% levels, respectively.

Alternative Specifications

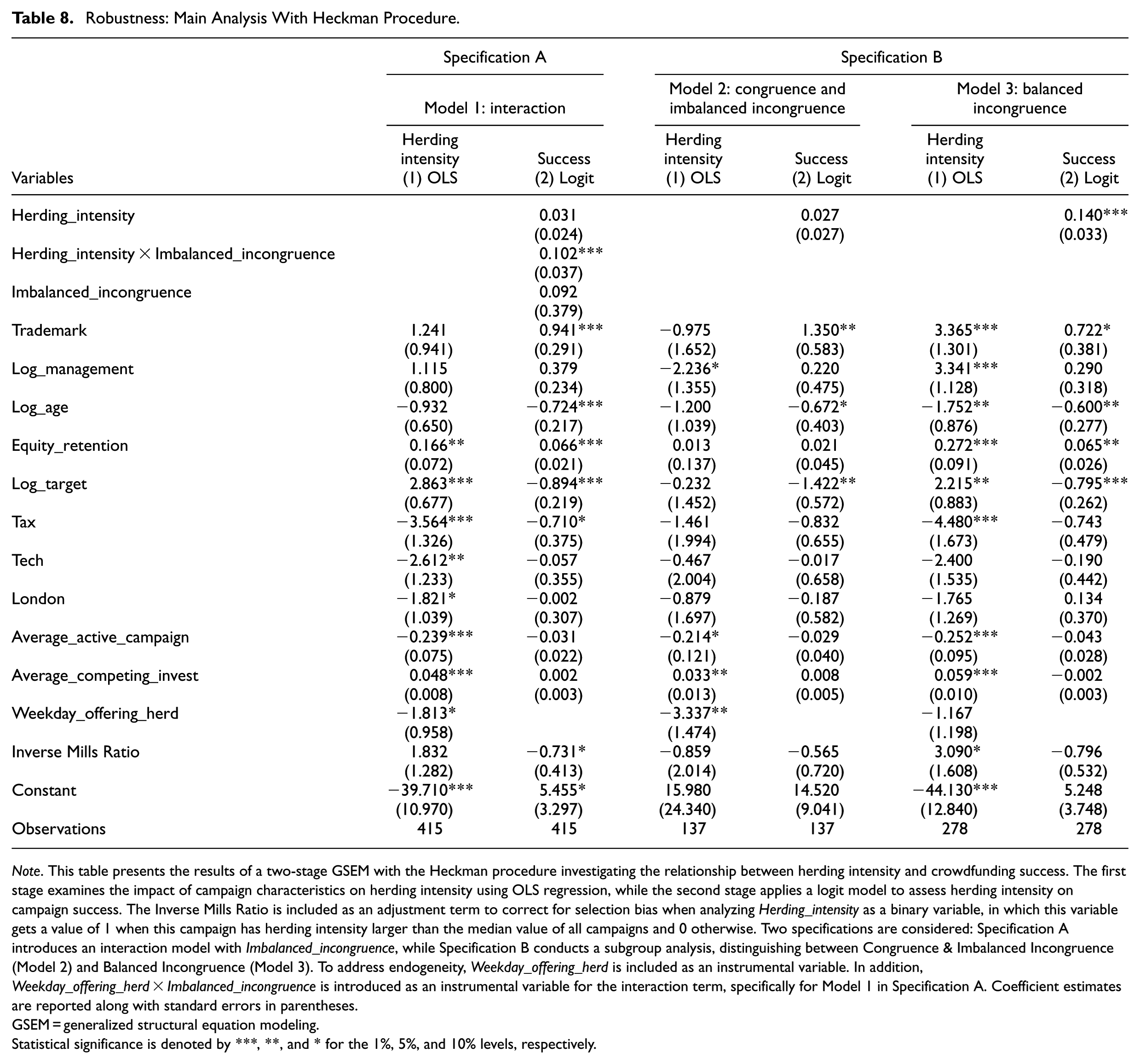

In addition to GSEM, we also adopted the two-stage Heckman procedure to treat selection bias and unobserved heterogeneity. This method was used by Courtney et al. (2017) in a study of signaling in crowdfunding. The selection bias arises when different unobserved features of campaigns are present, which may have impacts on herding intensity. Following this method, we needed to specify one variable: high herding, which was assigned a value of 1 when a campaign had a herding intensity larger than the median value of all campaigns and 0 otherwise. We estimated the first-stage probit model to determine the probability that a campaign has high herding, then calculated Inverse Mill’s ratio as an adjustment term for selection bias to use in the second stage of the GSEM model in the main analysis. When Inverse Mill’s ratio was included in the model, the results continued to be robust (Table 8).

Robustness: Main Analysis With Heckman Procedure.

Note. This table presents the results of a two-stage GSEM with the Heckman procedure investigating the relationship between herding intensity and crowdfunding success. The first stage examines the impact of campaign characteristics on herding intensity using OLS regression, while the second stage applies a logit model to assess herding intensity on campaign success. The Inverse Mills Ratio is included as an adjustment term to correct for selection bias when analyzing Herding_intensity as a binary variable, in which this variable gets a value of 1 when this campaign has herding intensity larger than the median value of all campaigns and 0 otherwise. Two specifications are considered: Specification A introduces an interaction model with Imbalanced_incongruence, while Specification B conducts a subgroup analysis, distinguishing between Congruence & Imbalanced Incongruence (Model 2) and Balanced Incongruence (Model 3). To address endogeneity, Weekday_offering_herd is included as an instrumental variable. In addition, Weekday_offering_herd × Imbalanced_incongruence is introduced as an instrumental variable for the interaction term, specifically for Model 1 in Specification A. Coefficient estimates are reported along with standard errors in parentheses.

GSEM = generalized structural equation modeling.

Statistical significance is denoted by ***, **, and * for the 1%, 5%, and 10% levels, respectively.

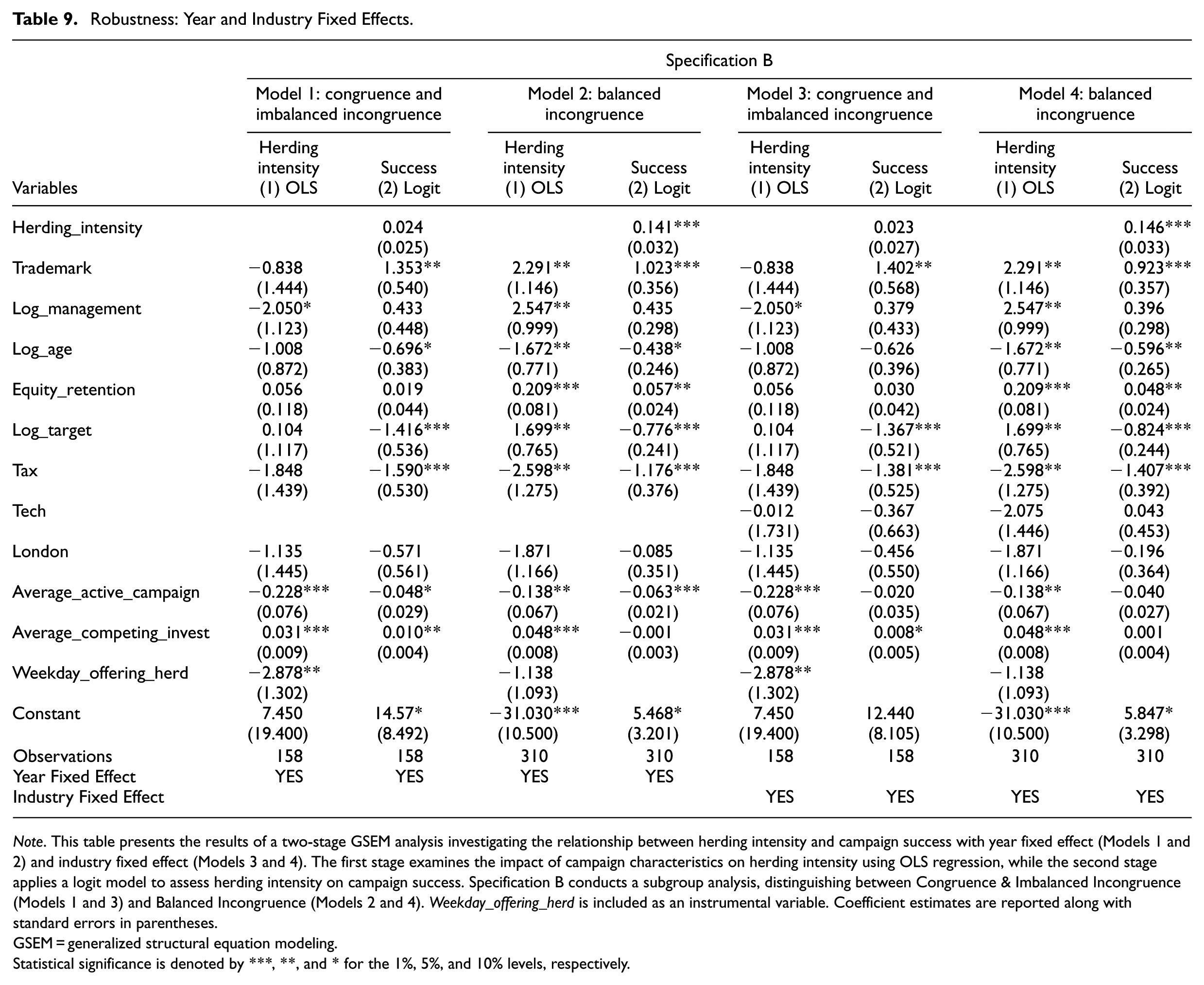

Industry and Time Fixed Effect

To ensure the robustness of our findings, we re-estimated our main results using year- and sector-fixed effects, rather than relying solely on the technology sector dummy variable. Overall, we had information on nearly 30 specific sectors, with technology sectors (Technology Hardware & Equipment, and Computer Software) representing approximately 20% of all campaigns (83 projects). Other dominant sectors were Business Services, Food & Tobacco Manufacturing, Online Applications, Travel, Personal & Leisure, and Wholesale. Based on the characteristics of each sector, we merged all sectors and categorized them into four main groups: Technology (17.74%), Manufacturing (11.75%), Services (52.78%), and Others (17.74%). The results presented in Table 9 remain consistent with our main findings, further reinforcing the robustness of our analysis.

Robustness: Year and Industry Fixed Effects.

Note. This table presents the results of a two-stage GSEM analysis investigating the relationship between herding intensity and campaign success with year fixed effect (Models 1 and 2) and industry fixed effect (Models 3 and 4). The first stage examines the impact of campaign characteristics on herding intensity using OLS regression, while the second stage applies a logit model to assess herding intensity on campaign success. Specification B conducts a subgroup analysis, distinguishing between Congruence & Imbalanced Incongruence (Models 1 and 3) and Balanced Incongruence (Models 2 and 4). Weekday_offering_herd is included as an instrumental variable. Coefficient estimates are reported along with standard errors in parentheses.

GSEM = generalized structural equation modeling.

Statistical significance is denoted by ***, **, and * for the 1%, 5%, and 10% levels, respectively.

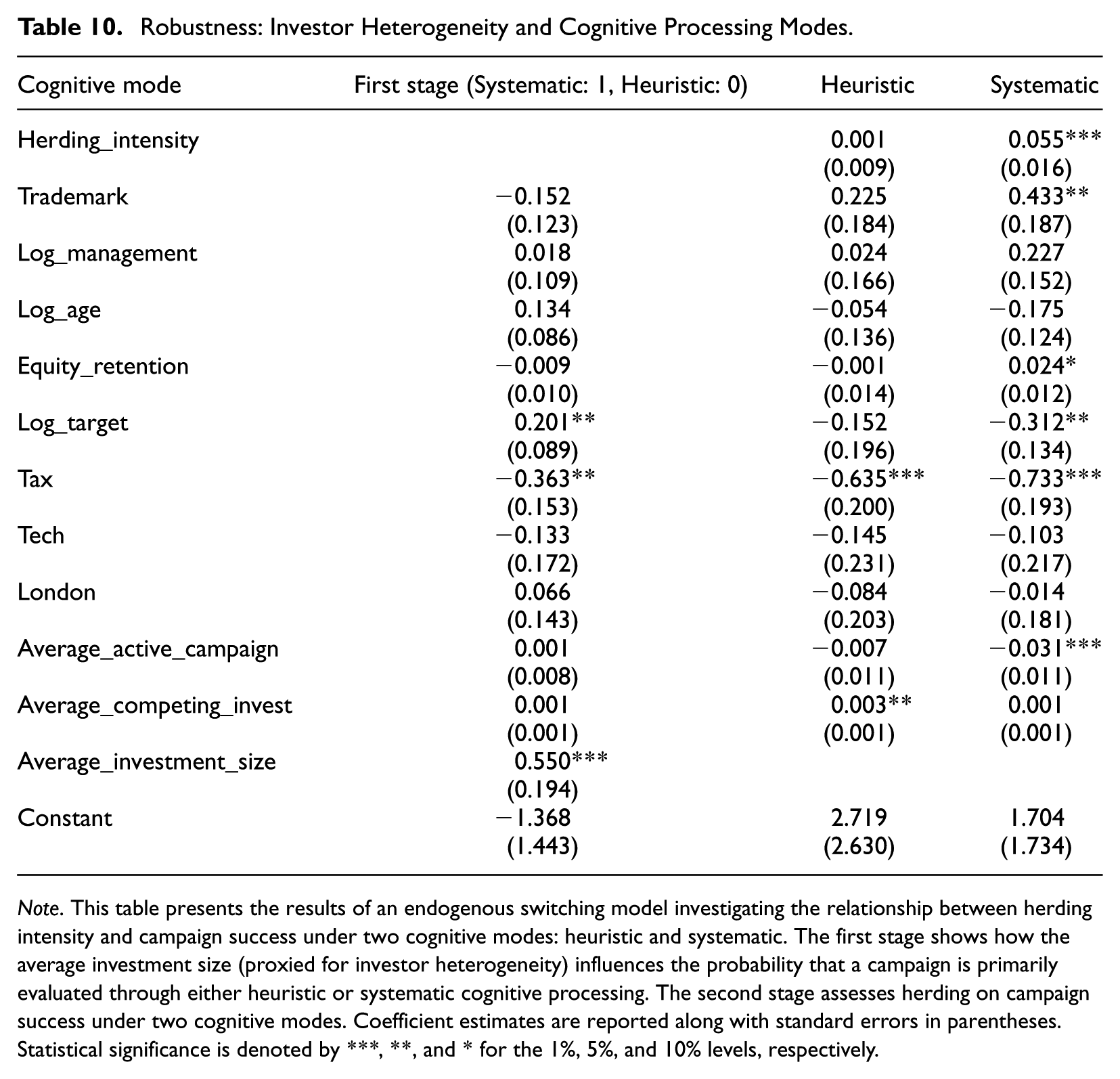

Accounting for Investor Heterogeneity and Cognitive Processing Modes

One potential issue with our research design is that the cognitive processing choice of investors may be influenced by the heterogeneity of their experience and prior knowledge (Butticè et al., 2022). We addressed this issue by employing an endogenous switching model to predict investors’ cognitive choices based on their heterogeneity. As a proxy for investor heterogeneity, we used average investment size, measured as the logarithm of the average funding amount per investor for each campaign. We argue that this measure can capture the differences in investor type and, by extension, their experience and investment behavior (Wallmeroth, 2019).

Using the endogenous switching model, we first estimated how the average investment size influences the probability of adopting either heuristic or systematic cognitive processing. The first-stage results, reported in Table 10, show that average investment size is positively associated with the likelihood of adopting systematic processing, which is consistent with the notion that larger investors are more likely to engage in deeper, analytic evaluation. Based on these estimated probabilities, we classified campaigns into heuristic and systematic regimes and re-estimated our main model within each group. The results from the second stage, also presented in Table 10, remain consistent with our baseline findings in that herding significantly influences campaign success under systematic processing, but has no statistically significant effect under heuristic processing.

Robustness: Investor Heterogeneity and Cognitive Processing Modes.

Note. This table presents the results of an endogenous switching model investigating the relationship between herding intensity and campaign success under two cognitive modes: heuristic and systematic. The first stage shows how the average investment size (proxied for investor heterogeneity) influences the probability that a campaign is primarily evaluated through either heuristic or systematic cognitive processing. The second stage assesses herding on campaign success under two cognitive modes. Coefficient estimates are reported along with standard errors in parentheses.

Statistical significance is denoted by ***, **, and * for the 1%, 5%, and 10% levels, respectively.

Conclusion

Practical Implications

Our study has two significant implications for practice. First, by employing advanced machine learning techniques, we identified a set of effective signals and their relative importance. This finding will be helpful in enabling entrepreneurs to strategically select and present the information they communicate with investors. Moreover, with respect to communication, entrepreneurs can also use the relative importance of signals to allocate limited resources more effectively—focusing on the most influential signals that resonate with investors. This is a particularly important consideration given the significant resource constraints that entrepreneurs often face (Bapna, 2017).

Second, our study sheds light on how investors process information, underscoring the role of herding behavior in equity crowdfunding. In particular, for entrepreneurs whose signal portfolios may appear inconsistent or weakly aligned (incongruent signals), leveraging herding dynamics, such as creating early momentum (Mataigne et al., 2025) to initiate the mechanisms of information cascade (Vismara, 2018a), can help compensate for signal ambiguity and enhance perceived legitimacy among later-stage investors. Equity crowdfunding platforms may further amplify herding effects by displaying charts on daily fundraising and/or the number of investors, thereby making the fundraising dynamics and progression more visible to potential investors.

The findings also have notable implications for investors, particularly new participants in equity crowdfunding markets. Specifically, by identifying the relative importance of different entrepreneurial signals, our results will help investors understand how others interpret and respond to the signals provided by entrepreneurs. This insight is especially useful as investors generally prefer to invest in successful campaigns; hence, it will be valuable for them to have a data-driven clue concerning how others interpret and respond to the signals provided by entrepreneurs.

Moreover, our findings imply that investors may benefit from observing herding behavior in cases where entrepreneurial information is ambiguous or incongruent. The actions of early backers can serve as an additional signal of perceived campaign quality, helping later investors make more informed decisions in the face of uncertainty. In this way, herding acts as a social filter, potentially improving the accuracy of investment decisions when direct evaluation of signals may be difficult.

Limitations and Future Research Directions

It is important to acknowledge the limitations of our study and suggest potential directions for future research. First, our study used the findings of previous studies and econometrics methods to identify effective signals used by investors. To extend the set of signals, future studies could use different methods, such as direct interviews with investors. In addition, it is important to advance the methodology to measure the importance of signals so that campaigns can be allocated more accurately into groups comprising congruent and incongruent signals.

A second limitation of our study is that we relied solely on data from Crowdcube, a UK-based equity crowdfunding platform. This may affect the generalizability of our findings, as Crowdcube operates within a specific regulatory environment and attracts a particular investor base and certain types of campaigns; hence, it may differ from platforms in other countries such as the United States (e.g., Cumming et al., 2025), Europe (e.g., D’Agostino et al., 2024), or Australia (e.g., Ahlers et al., 2015). Future research could expand on our findings by examining cross-country comparisons, assessing how regulatory frameworks, investor profiles, and cultural differences influence signal processing in equity crowdfunding.

Third, recent studies (Belavina et al., 2020; Cumming et al., 2023; Mataigne et al., 2025; Meoli & Vismara, 2021) document evidence of false and misleading signals in crowdfunding, which may have vital implications for our study. For instance, these studies provide evidence suggesting that entrepreneurs and platform members may manipulate early investments to create momentum and then withdraw their funds, leading to spurious herding (Bikhchandani & Sharma, 2000). This implies that even a careful and rational approach to decision-making (i.e., using systematic processes to incorporate additional signals from herding) may result in misinterpretation and flawed investment choices. Future research could therefore extend our study by investigating the effects of false signals and spurious herding on investor decision-making, particularly with regard to distinguishing between genuine and misleading signals in equity crowdfunding.

Fourth, investor heterogeneity may influence the cognitive processing of signals (Butticè et al., 2022). For instance, more experienced investors are likely to engage in systematic processing, carefully evaluating signals before making decisions. Future research could adopt experimental designs, similar to those used by Butticè et al. (2022), to better capture investor heterogeneity and assess its impact on decision-making in equity crowdfunding. 8

Finally, crowdfunding campaigns operate within a complex signaling environment in which investors are also impacted by other sources of information, such as discussions on online crowdfunding platforms or social media (Jiang et al., 2018; Lee and Lee, 2012; Xiao et al., 2021). It will therefore be useful to extend our research by investigating whether and how investors are influenced by various signals in such environments.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.