Abstract

When entrepreneurs express their ambitions to achieve extraordinary financial growth, it may signal growth potential to early-stage investors. However, as this study proposes, promising overly high growth ambitions might backfire for entrepreneurs—dismissed as cheap talk and even penalized due to investors’ credibility concerns. Therefore, entrepreneurs may need to complement their high ambitions with costly signals, such as citing their rich experiences or patents. Such costly signals can serve as credibility buffers and transform high ambitions from cheap talk into credible signals. Two empirical studies, based on campaign data from an equity crowdfunding setting and a conjoint experiment, support these arguments.

“Ambition can be good. Promising a brighter future, and then trying to realise that vision, brought about computers and smartphones. But for investors, trying to separate the charlatans from the revolutionaries is a constantly evolving challenge.”

Introduction

Sustaining and growing their ventures typically requires entrepreneurs to persuade early-stage investors of their prospective success (Huang & Pearce, 2015). As a prominent theoretical lens to explain this process, signaling theory anticipates that new ventures signal their unobservable quality to resource providers by presenting observable activities or attributes (Bafera & Kleinert, 2022). According to traditional signaling theory (Spence, 1973), when such signals are costly and difficult to imitate by low-quality ventures, only high-quality ventures issue them, so signals convey credible information. But recent entrepreneurship research has extended this traditional signaling view with a modern perspective that relaxes the costliness condition (e.g., Anglin et al., 2018; Vanacker et al., 2020). This recent expansion of the theory adds the recognition that, in certain conditions—such as when objective information is scarce, audiences are less sophisticated, or behavioral norms are less explicit (Colombo, 2021)—costless, easily imitable signals can be effective too. For example, costless signals based on entrepreneurs’ rhetoric can be effective in early-stage financing contexts (Anglin et al., 2018; Di Pietro et al., 2020; Moss et al., 2015; Payne et al., 2013; Steigenberger & Wilhelm, 2018). However, such signals can be leveraged equally by any venture, regardless of its quality, such that they seem prone to misuse and may appear unreliable, according to the traditional view (Bergh et al., 2014). Because of this discrepancy between both iterations of signaling theory, ambiguity persists about costless signals, creating a puzzling conundrum for entrepreneurship signaling research: To what extent do early-stage investors perceive costless signals as credible, rather than as cheap talk?

To address this controversy and elaborate on existing theory (Fisher & Aguinis, 2017), we integrate the ideas of both traditional and modern signaling perspectives. In this effort, we introduce entrepreneurs’ expressed growth ambitions as a potentially relevant but previously neglected number-based costless signal in equity crowdfunding—a setting that combines elements of a noisy crowdfunding environment with traditional early-stage investing (Pollack et al., 2021). High ambitions are considered a hallmark of successful entrepreneurship (Baum & Locke, 2004), and because they indicate high aspirations and intentions to achieve extraordinary financial growth (Wiklund & Shepherd, 2003), growth ambitions represent an especially important consideration when new ventures seek early-stage funding. Even if early-stage investors naturally would prefer a high rate of return, new ventures suffer inherent uncertainty in terms of their growth prospects (Huang & Pearce, 2015), so entrepreneurs express their high ambitions in financial forecasts to appeal to investors (Collewaert et al., 2021). In contrast to the rhetoric-based signals, which often go unnoticed in noisy funding environments (Steigenberger & Wilhelm, 2018), growth ambitions represent quantitative, number-based signals that tend to attract attention and can even spark automatic processing by investors (Hayward & Fitza, 2017). Because objective information about new ventures’ actual growth prospects is typically not available, equity crowdfunding investors, who tend to be relatively unsophisticated (Ahlers et al., 2015), may accept entrepreneurs’ expressed ambitions as relevant information for their quality judgments. In this sense, expressed growth ambitions qualify as potentially effective, costless signals in equity crowdfunding settings.

However, due to their costless nature, we posit that their actual effectiveness is a function of opposing forces. On the one hand, higher ambitions offer positive information about higher expected returns; on the other hand, higher ambitions may appear less credible to early-stage investors. Because they do not incur any cost by making ambitious forecasts, all ventures arguably might claim great financial growth prospects (Cassar, 2010), leaving investors unable to distinguish easily between more and less appealing options. Furthermore, expressions of overly high growth ambitions might evoke investors’ skepticism and suspicions of cheap talk, which suggests that the entrepreneurs are overconfident, untrustworthy (Collewaert et al., 2021), or solely engaged in self-promotion attempts. Audiences tend to form negative judgments about self-promoters who appear self-serving or less competent (Bolino et al., 2016). Even if new ventures are sincere in sharing their high ambitions, prospective investors may view them suspiciously, because realizing such ambitions is difficult and risky, requiring both skill and viable opportunities (Wiklund & Shepherd, 2003). Such credibility issues could eclipse the positive effects of claims of strong earning potential.

It is then up to the entrepreneurs to address this tension by convincing early-stage investors of their credibility. We propose that they can do so by using a portfolio of signals, in which they combine ambitious claims with costly signals that are difficult to imitate. In particular, to overcome early-stage investors’ suspicions, we suggest that entrepreneurs should send additional, costly signals about their founders’ trustworthiness and competence, such as by citing their experience (Ko & McKelvie, 2018), or about the new venture’s competitive advantage, such as by citing granted patents (Scheaf et al., 2018). Such costly signals can function like a credibility buffer that transforms costless signals (e.g., claims of high growth ambitions) into credible signals that appeal to early-stage investors.

We test these predictions in two empirical studies. In Study 1, we gather data about 235 new ventures that ran fundraising campaigns on the equity crowdfunding portal Crowdcube (Vismara, 2016). These data include detailed financial information about historical and forecasted revenues, which provide input for a reliable measure of ambitions (Collewaert et al., 2021). Then in Study 2, a conjoint experiment with 132 equity investors, we triangulate our main findings and affirm the generalizability of our results (Stevenson et al., 2020).

In turn, we establish three notable contributions for new venture financing and signaling research. First, with a more nuanced view of the effectiveness of costless signals, this study offers a novel perspective on controversies related to signaling costs, which represent a core tenet of traditional signaling theory (Bergh et al., 2014; Colombo et al., 2019) that gets relaxed in modern versions (Clough et al., 2019; Vanacker et al., 2020). Advocates for the modern perspective anticipate positive linear effects of costless signals in nontraditional funding contexts (Anglin et al., 2018; Moss et al., 2015), but we offer evidence of a curvilinear relationship between costless signals and fundraising performance in equity crowdfunding. This evidence reveals a tension: Costless signals transmit relevant information, as predicted by modern views, but also raise credibility concerns. This initial empirical evidence clarifies that costless signals might be effective up to a threshold, beyond which they induce unintended, negative effects. Acknowledging critiques which emphasize that costless signals lack a theoretical mechanism to distinguish between high- and low-quality ventures (Bergh et al., 2014), we specify that credibility provides a critical boundary condition for their effectiveness.

Second, modern signaling perspectives seek to account for entrepreneurs’ rhetoric as a relevant means to communicate information (Steigenberger & Wilhelm, 2018), usually in the form of rhetoric-based costless signals that inform investors about “who the venture is” (Anglin et al., 2018; Moss et al., 2015; Payne et al., 2013). By focusing on entrepreneurs’ expressed growth ambitions, we move beyond rhetoric and consider another costless signal, based on numbers, that informs investors about “what the venture might become.” This extension is important for early-stage funding, where investors’ returns depend on ventures’ future growth. Compared with qualitative signals, number-based signals may also attract more attention and automatic processing from quantitatively focused investors (Hayward & Fitza, 2017).

Third, we advance limited understanding of signal portfolios (Drover et al., 2018) and, in response to recent calls (Colombo, 2021), clarify the relational structures between costless and costly signals. Building on research that shows that the positive effect of rhetoric-based, costless signals can be amplified by additional costly signals (Anglin et al., 2018; Steigenberger & Wilhelm, 2018), we add that costly signals serve specifically as credibility buffers for costless signals. Their purpose thus is to counteract the negative effect of credibility issues that arise in the presence of excessive uses of number-based, costless signals. Our study also acknowledges the risk that costless signals create portfolio inconsistencies (Bafera & Kleinert, 2022). If costless versus costly signals are inconsistent, the costly signals may not achieve their intended effect. For example, founders with great experience or granted patents that fail to match expressions of growth ambitions, produce combinations that ultimately might reduce the signal portfolio’s value.

Theoretical Framework

Before we present our hypotheses, we introduce both traditional and modern perspectives on signaling theory, as foundations for our conceptual model.

Traditional Views and Costly Signals

As introduced by Spence (1973) in an economical context, signaling theory originally suggested ways to reduce information asymmetries between job applicants and employers. Expanded applications of the theory (Spence, 2002) have implied that new ventures can intentionally or unintentionally leverage observable signals to provide pertinent information about their unobservable quality to resource providers (Connelly et al., 2011). Differentiating elements, according to traditional signaling theory, are the cost of the signal, which might be monetary or psychic expenses required to create it (Spence, 1973), such that low-quality ventures must pay disproportionally more than high-quality ventures to obtain the same signal. In turn, signals that are costly to produce create a separating equilibrium, because they are more readily available to high-quality ventures and thus represent credible information (Bergh et al., 2014). A rich history of entrepreneurship research draws on this traditional signaling perspective to outline ways for new ventures to reduce information asymmetries with resource providers (Bafera & Kleinert, 2022 for a review). Relevant distinctions of costly signals pertain to entrepreneurs’ characteristics and new ventures’ actions (Colombo, 2021). For example, founding experience is a characteristic of entrepreneurs, reflecting the founders’ individual abilities and credibility, so it is difficult to imitate (Courtney et al., 2017; Ko & McKelvie, 2018). Actions undertaken by a new venture, instead, might include patenting activity, which indicates its strong economic capabilities and likely competitive advantages (Bapna, 2019; Kleinert et al., 2021).

Modern Views and the Credibility of Cheap Talk

More recent entrepreneurship research adjusts these predictions (Vanacker et al., 2020), by accounting for the observation that less costly signals, including rhetoric, frequently provide information to prospective resource providers (Steigenberger & Wilhelm, 2018). Arguably, regardless of their cost, signals can reflect any informational characteristic that indicates a firm’s quality (Clough et al., 2019). Whereas costly signals offer objective, verifiable information (Connelly et al., 2011), costless signals mainly rely on subjective, nonverifiable claims, which underlies the common label for such signals as “cheap talk” (Colombo, 2021). Furthermore, most costly signals relate to the past, because new ventures must have previously incurred some cost to produce them (Bapna, 2019), but cheap talk can be forward-looking and related to new venture performance in an uncertain future. Entrepreneurship research that examines various costless signals focuses on the rhetoric conveyed in prospectuses and pitch decks, including positive language that emphasizes the entrepreneurial orientation, virtuousness, or emotions of the founders (Anglin et al., 2018; Moss et al., 2015; Steigenberger & Wilhelm, 2018), which can be effective means to influence resource providers.

Advocates of the modern signaling view thus argue for the importance of costless signals, due to their capacity to convey relevant information and help entrepreneurs make a good impression (Colombo, 2021), especially when they lack access to objective information, they are dealing with less sophisticated audiences, or the context lacks explicit behavioral norms (Anglin et al., 2018). In these cases, investors might believe entrepreneurs’ claims and reward them with funding, though traditional signaling theory would question this outcome, reflecting its core prediction that costless claims lack credibility and cannot distinguish high- and low-quality options (Spence, 1973). From yet another perspective, organizational research would predict that unverifiable claims used to promote performance ultimately result in negative perceptions, because of the difficulty of assessing the authenticity of such claims (Bolino et al., 2016; Jones & Pittman, 1982). Thus, subjective performance claims can look like self-promotion attempts, more widely adopted by poor performers (Gardner & Avolio, 1998), which can create a self-promoter paradox: People who overemphasize their own potential appear self-interested and less competent (Bolino et al., 2016).

These credibility concerns are particularly pertinent for entrepreneurship, because new ventures lack the operating history or reputation that incumbent companies have earned (Stuart et al., 1999). New ventures’ survival and growth depend on their ability to persuade investors (Fisher et al., 2017), so their founders might feel compelled to leverage any available means to create a favorable image—even misrepresenting facts or intentionally deceiving audiences (Benson et al., 2015; Rutherford et al., 2009; Scheaf & Wood, 2021). Assessing the trustworthiness of entrepreneurs is very challenging for early-stage investors, who mainly are interacting for the first time, before any trust-based relationship has developed (Maxwell & Lévesque, 2014). Skeptical early-stage investors want to avoid falling for misleading claims, and as such, credibility concerns could be a relevant boundary condition for the effectiveness of cheap talk signals.

High Growth Ambitions as Cheap Talk

Promising high ambitions is a salient, costless signal in early-stage financing and equity crowdfunding. Entrepreneurs’ ambitions reflect their aspirations to achieve venture growth, especially financial growth (Cassar, 2006); they thus constitute important considerations in early-stage financing, because early-stage investors operate predominantly according to an economic return logic (Fisher et al., 2017) and look for new ventures that promise extraordinary returns (Huang & Pearce, 2015). Returns depend on future growth, which is highly uncertain for new ventures and depends on their capabilities and motivation to grow (Bapna, 2019). Therefore, it seems logical for entrepreneurs to express high ambitions that, in turn, promise strong growth, significant exit potential, and high rates of return. For example, in financial outlook reports provided to early-stage investors, entrepreneurs frequently boast about their venture’s positive financial growth prospects (Collewaert et al., 2021). Such claims are costless, but in the absence of objective information, early-stage investors likely rely on and react to such claims—especially equity crowdfunding investors, who generally are unsophisticated (Ahlers et al., 2015). Because this context also features high levels of noise, these unsophisticated investors also struggle to assess the objectivity of information (Butticè et al., 2021). They might overlook qualitative information, which is more difficult to comprehend in noisy environments (Steigenberger & Wilhelm, 2018). Reflecting their quantitative mindsets, early-stage investors might automatically and unconsciously notice and process number-based cues (Hayward & Fitza, 2017). Reasonably, high growth numbers should evoke a sense that the venture holds promise; low growth numbers likely lead them to anticipate low return potential. Accordingly, growth ambitions may serve as a relevant signal for future revenue potential that early-stage investors perceive favorably in an equity crowdfunding context.

As noted, though, controversy remains. According to three opposing arguments, higher stated growth ambitions should raise credibility concerns. First, entrepreneurs know that early-stage investors prefer high growth prospects, so they have clear financial incentives to meet these expectations, or at least claim to be able to do so. There are no direct costs for boasting about future sales; entrepreneurs can easily overstate their financial growth prospects (Cassar, 2010), such that they might just offer cheap talk (Ahlers et al., 2015). For early-stage investors, it is difficult to distinguish realistic and fake growth prospects, so they worry about the veracity of high ambitions. Some might ignore absurdly ambitious claims; others even could penalize such displays, due to the high value they place on trustworthiness. Worried that an entrepreneur is exhibiting trust-violating behaviors, such as one who “deliberately misrepresents or conceals critical information” (Maxwell & Lévesque, 2014, p. 1063) to appeal to them, early-stage investors likely suspect too high ambitious growth claims (Pollack & Bosse, 2014; Rutherford et al., 2009) and punish this attempt for its trust-violating effect. Collewaert et al. (2021) concur, suggesting that overstated revenue growth undermines trust and causes early-stage investors to question entrepreneurs as a whole.

Second, new ventures might evoke a self-promoter paradox (Bolino et al., 2016), such that sharing overly ambitious growth goals creates negative impressions of the entrepreneurs’ motives, performance, or competence. Self-promoters appear selfish and motivated to take credit (Berman et al., 2015); in response, observers often discount self-promotion claims as exaggerated, with the skeptical belief that unverifiable performance claims are more common among underperforming actors (Bolino et al., 2016; Jones & Pittman, 1982). Entrepreneurs who boast about very high ambitions thus may appear less competent, leading to lower performance expectations, as summarized by a venture capital-backed entrepreneur interviewed by Collewaert et al. (2021, p. 4): “if you give them too high numbers … that may turn into ‘these guys don’t know what they are talking about’… it can create a negative perception on you as a team.”

Third, realizing expressed high growth ambitions is an uncertain process. Actual growth requires not just ambitions but ability and viable opportunities (Wiklund & Shepherd, 2003). Achieving massive growth is especially demanding; pursuing this ambitious goal might distract the new venture from its core business operations or increase organizational complexity (Mishina et al., 2004). Growing too fast too soon creates a severe failure risk (Cressy, 2006); financially constrained new ventures can only afford a certain, constrained level of growth, and exceeding it represents a primary cause of insolvencies (Probst & Raisch, 2005). Early-stage investors might be unwilling to bear this risk, especially if they are not fully confident in the entrepreneurs’ abilities or opportunities.

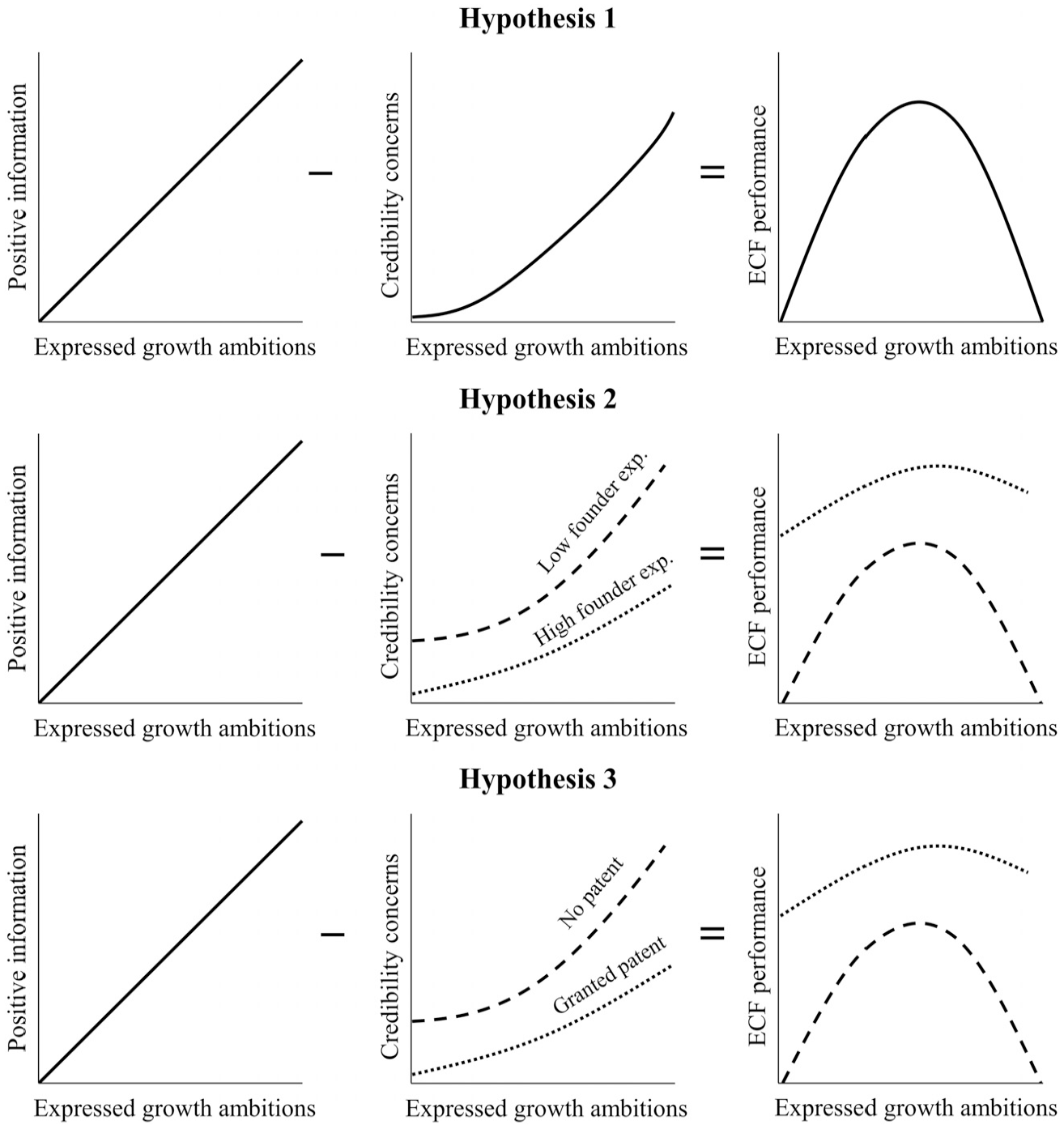

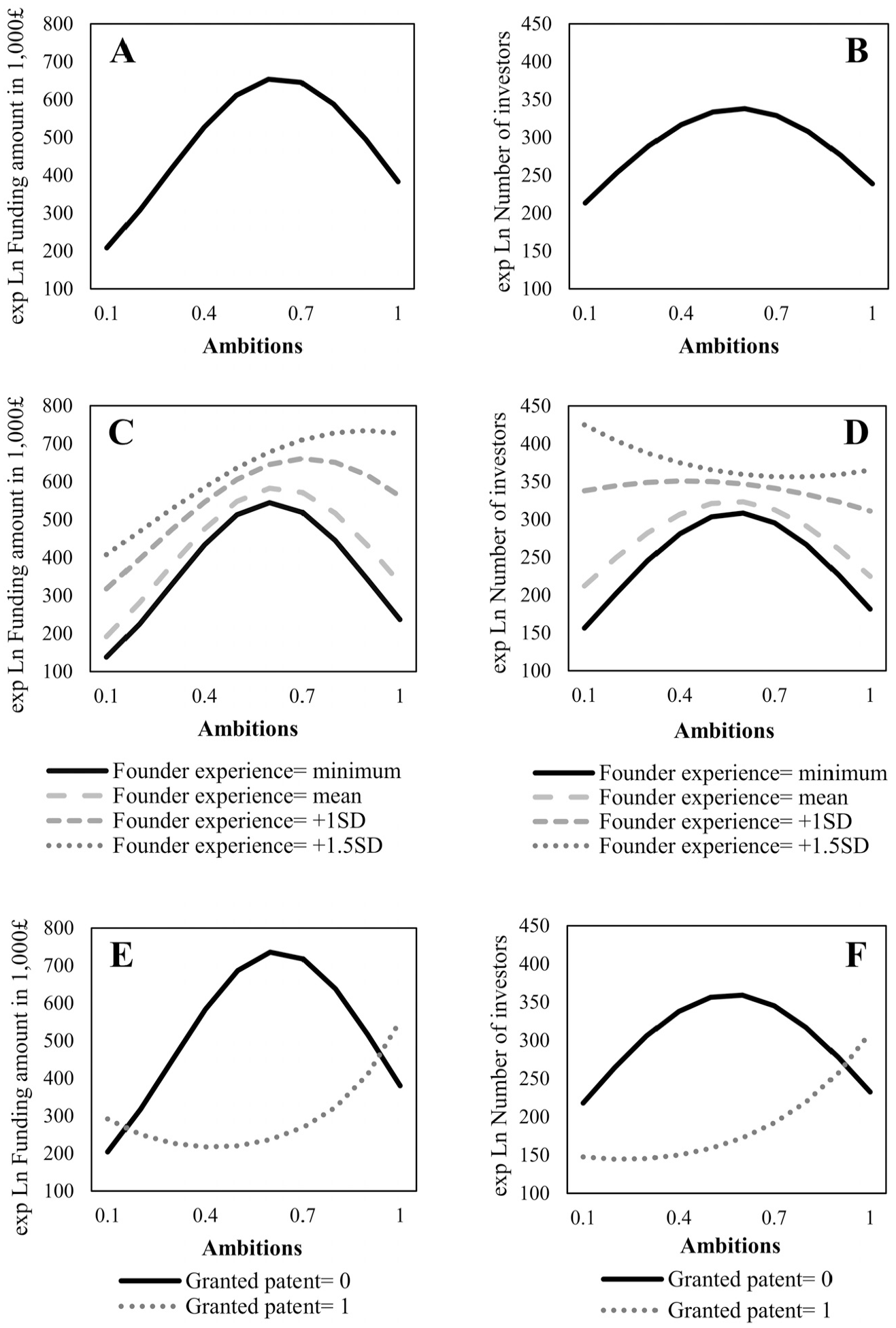

On balance, these divergent views suggest a curvilinear, inverted U-shaped relationship: Expressed growth ambitions may have a positive effect on a new venture’s fundraising performance up to a point, after which further increases in growth ambitions reduce fundraising performance (Figure 1, first row). Thus, the following hypothesis is proposed:

Theorized main and moderation effects.

Moderating Influence of Costly Signals

If complementary, costly signals can provide a credibility buffer, they might resolve the tension between positive information about return potential and diminished credibility. Specifically, we propose that the entrepreneurs’ experience and new ventures’ patents serve as relevant, costly signals that indicate the credibility of higher expressed growth ambitions.

Costly Entrepreneur Signals: Founder Experience

Founder experience refers to entrepreneurs’ prior experience as founders and managers; it is perhaps the most relevant entrepreneur-related costly signal in early-stage financing contexts (e.g., Hoenig & Henkel, 2015; Ko & McKelvie, 2018; Lim & Busenitz, 2020), because it indicates entrepreneurs’ abilities, competence, and trustworthiness (Plummer et al., 2016). It thus might offset credibility concerns and increase early-stage investors’ confidence that new ventures can realize their high growth ambitions.

First, entrepreneurs gain important knowledge, competencies, and skills from their past experiences in founder roles; entrepreneurs without such experiences lack these resources (Shepherd et al., 2000). Through their past founding experiences, entrepreneurs learn to select better opportunities and commercialize products (Ko & McKelvie, 2018), implying better chances that they can realize their high growth ambitions. Because they have accumulated knowledge about what must be done and how, these experienced entrepreneurs should be more effective and efficient in growing ventures (Dencker & Gruber, 2015). For example, they might better understand the risks associated with developing a successful venture and could be less likely to make fatal mistakes that prevent the attainment of high growth (Ucbasaran et al., 2010). As empirical evidence has indicated, entrepreneurs with more experience tend to achieve higher revenue growth (Dencker & Gruber, 2015; Stuart & Abetti, 1990; Wiklund & Shepherd, 2003).

Second, through their prior managerial roles, experienced entrepreneurs may appear more trustworthy and less likely to offer just cheap talk to comply with investors’ return expectations. In their prior roles as managers, entrepreneurs should have built a professional reputation (Shane & Cable, 2002), which they should be loath to jeopardize by being dishonest. Experience in management positions also offers a signal to labor markets, such that the opportunity costs of starting a new venture would be higher for entrepreneurs who have invested time and effort to gain such valuable experience. In turn, they strive for higher growth than less experienced entrepreneurs do (Cassar, 2006). Early-stage investors can be more confident in the ability of such experienced entrepreneurs to calculate realistic financial growth prospects, because in their past management roles, they likely have learned how to issue precise revenue forecasts (Hayward & Fitza, 2017). With this relevant experience, they can undertake foresighted planning that incorporates risks of environmental changes (Shepherd et al., 2000).

Overall then, founder experience should give entrepreneurs “a more realistic view of the new venture growth process” (Capelleras et al., 2019, p. 6) and tacit knowledge about managing organizations, including financial planning (Dencker & Gruber, 2015). Accordingly, ambitions expressed by experienced entrepreneurs should seem like more trustworthy proxies for future revenue potential. That is, because experience lends credibility to growth ambitions, expressing high ambitions provides a credible signal when it comes from experienced entrepreneurs. Early-stage investors even might expect experienced founders, with their rich expertise, to express high ambitions. Instead, if experienced founders express lower ambitions, then investors may perceive inconsistency between the new venture’s costless and costly signals (Bafera & Kleinert, 2022). Thus, the inverted U-shaped relationship between expressed growth ambition and equity crowdfunding performance should be flatter for new ventures run by more experienced entrepreneurs (Figure 1, second row). Conversely, we anticipate a steeper inverted U-shaped curve for inexperienced founders. They should be penalized more for both high ambitions, due to stronger credibility concerns, and for below-average ambitions, due to investor concerns that entrepreneurs who lack both experience and ambition cannot offer sufficient return potential. On the basis of this reasoning, we hypothesize the following:

Costly New Venture Signals: Granted Patents

Granted patents represent credible information about product quality and competitive benefits (Audretsch et al., 2012; Scheaf et al., 2018). Earning a patent is costly and can only be obtained by high-quality new ventures that have developed a novel invention (Kleinert et al., 2021). In turn, a patent suggests that the new venture is an engine of innovation (Ahlers et al., 2015), which represents a critical antecedent of new venture growth and survival (Baum et al., 2001). Furthermore, patents provide competitive advantages to their holders (Ahlers et al., 2015), due to the temporary monopoly rights they gain, which exclude competitors from using or selling the same offering (Farre-Mensa et al., 2020; Scheaf et al., 2018). New ventures might even leverage their patents to obtain first-mover advantages (Lieberman & Montgomery, 1988) and establish a dominant design (Abernathy & Utterback, 1978). New ventures with granted patents thus are more likely to exploit their competitive benefits to realize high growth ambitions. Research confirms that a granted patent “sets a start-up on a growth path,” on which they pursue higher quality innovations and achieve, on average, 80% higher sales growth (Farre-Mensa et al., 2020, p. 642). Thus, early-stage investors should perceive higher ambitions as more credible and likely to be realized if new ventures own patents.

Earning patents further demands significant intellectual and personal investments by the entrepreneur (Scheaf et al., 2018), so early-stage investors are less likely to dismiss expressions of higher ambition as cheap talk and instead should view them as trustworthy. For example, earning a patent requires a significant commitment of resources, such as effort, time, and patent application fees (Hsu & Ziedonis, 2013). In turn, patents “enable entrepreneurs to recoup investments made developing the invention” (Scheaf et al., 2018, p. 724). Early-stage investors thus might perceive higher growth ambitions as a logical consequence of the efforts evidently taken by patent-holding new ventures and regard them as credible and reasonable.

Overall then, patents offer increased likelihood of realized and trustworthy growth ambitions. But if patent-holding new ventures appear insufficiently ambitious, early-stage investors may perceive conflicting information or suspect that the venture is not driven enough to exploit its competitive advantage. Accordingly, we expect granted patents to flatten the inverted U-shape of expressed growth ambitions (Figure 1, third row). Conversely, for ventures without patents, the inverted U-shape should be steeper. In this latter case, overly high ambitions appear more implausible; below-average ambitions also are particularly concerning, because investors sense that the new ventures lack both ambition and competitive benefits (i.e., patents). In other words, for new ventures without patents, the initial reward of expressing higher ambitions should increase more rapidly, whereas overly high ambitions prompt greater penalties. Collectively, we hypothesize the following:

Overview of Studies

We use a multimethod, multistudy approach to test the effect of expressed ambitions and complementary costly signals on equity crowdfunding performance. In Study 1, we draw on campaign-level data from a leading equity crowdfunding platform, such that we examine real investment decisions by early-stage investors (Vismara, 2016). These data are unique; they provide detailed financial information about new ventures. In Study 2, an experimental conjoint analysis, we measure decision-making by early-stage investors (Drover et al., 2017) and overcome some limitations of observational data (Hsu et al., 2017); with Study 2, we replicate the key findings of Study 1 in an experimental setting. By combining different research methods, we address recommendations of prior entrepreneurship research and can establish generalizable findings (Williams et al., 2019).

Study 1: Campaign-Level Data from Equity Crowdfunding

Sample

We identified a sample of 245 new ventures that launched equity crowdfunding campaigns on the U.K. Crowdcube platform between April 2017 and mid-July 2018. Crowdcube has facilitated more than £1 billion in funding since its founding in 2010, more than any venture capital firm in the United Kingdom (Beauhurst, 2020). New ventures seeking funding on Crowdcube provide a public project description, then share confidential business plans and financial information on request to registered members. We requested and obtained these data; detailed financial information is especially critical for our research but rarely available for early-stage finance studies. Nine ventures did not document their financial data and one venture employed an atypical accounting practice; they were excluded, leaving a final sample of 235 new ventures.

Variables

Dependent Variables

To measure equity crowdfunding performance, we rely on two variables: funding amount and number of investors (Kleinert et al., 2020; Vismara, 2016). The funding amount refers to the total amount invested in a new venture (in £) during the equity crowdfunding campaign. The number of investors refers to the total number of investors. Similar to prior research, we use the natural logarithm of both variables to account for the measures’ high degree of skewness (Taeuscher et al., 2021).

Explanatory Variables

To construct an ambitions variable, we draw on detailed, self-reported financial data from the new ventures. It equals the difference between the revenues forecasted for the post-campaign year and the revenues generated in the year prior to the campaign, divided by the sum of both values (Cassar, 2010; Collewaert et al., 2021), such that it takes values between 0 (extremely low ambitions) and +1 (extremely high ambitions). 1 It can be interpreted as the percentage of forecasted revenues that would be new, compared with prior revenues; stated differently, it indicates how much of forecasted revenues were not earned as past revenues. A forecast of £1,000,000 for the post-campaign year and revenues of £50,000 in the pre-campaign year produce a score of 0.9, indicating high ambitions; a forecast of £50,000 and historical revenues of £50,000 produce a score of 0, reflecting extremely low ambitions. Because this measure considers both forecasted and historical revenues, it accounts for how ambitions relate to deviations from the present state so that the past serves as a benchmark. Furthermore, by dividing by the sum of both values, we reduce susceptibility to extreme values, as frequently occur in new venture forecasts (Collewaert et al., 2021). We deliberately choose a constant, 1-year time horizon, to account for the potentially different lengths of the forecast horizons provided by new ventures and the decreasing informative value of forecasts of more distant futures (Collewaert et al., 2021). Overall, this measure is well-suited for our study context and theoretically consistent with prior research.

With regard to the predicted moderators, we create a count variable founder experience, using the professional business network LinkedIn and the team description in the business plans to identify relevant past managerial and founder roles for each entrepreneur. Similar to Plummer et al.’s (2016) study, our measure reflects a count of the number of other businesses that the founders have owned or principally managed (e.g., as founders, CEOs, directors). Furthermore, following Ahlers et al. (2015) and Scheaf et al. (2018), we denote granted patent as a dichotomous variable, indicating whether a new venture reports that it owns any patent (1) or not (0).

Control Variables

We control for several team and venture characteristics. The number of founders is an integer variable that counts the number of founders; larger teams might benefit from their greater human capital, compared with single founders (Ko & McKelvie, 2018). To account for gender bias in entrepreneurial finance and the possibility that female founders tend to express lower growth intentions (Sweida & Reichard, 2013), we also create a share female founders variable that reflects the share of women among the number of founders. Entrepreneurs’ education can create positive perceptions among investors (Kleinert et al., 2020), so we denote a dichotomous education of founders variable, indicating whether at least one of the entrepreneurs holds an MBA or PhD (Ahlers et al., 2015). Some new ventures benefit from the advice and social capital of nonexecutive directors, which we control for with another dichotomous variable (Vismara, 2018). When new ventures have obtained prior funding, they also attain financial and reputational benefits (Kleinert et al., 2020), such that we control for whether new ventures are venture capital-funded; whether they obtained government funding, using a dichotomous grant variable (Islam et al., 2018); and whether they were equity crowdfunded before. We use a binary exitplan variable to indicate whether a new venture mentions an exit plan (Ahlers et al., 2015). As continuous variables, equity offer is the percentage of equity offered to investors in the pitch page, and funding goal (in £100,000) is the target capital requested by entrepreneurs (Vismara, 2016). We control for the age of the new venture in years since its founding, because older ventures might be better developed (Stuart et al., 1999). Finally, we use a dummy variable to control for technology venture and indicate if the firm operates in a technology sector (Plummer et al., 2016).

Results

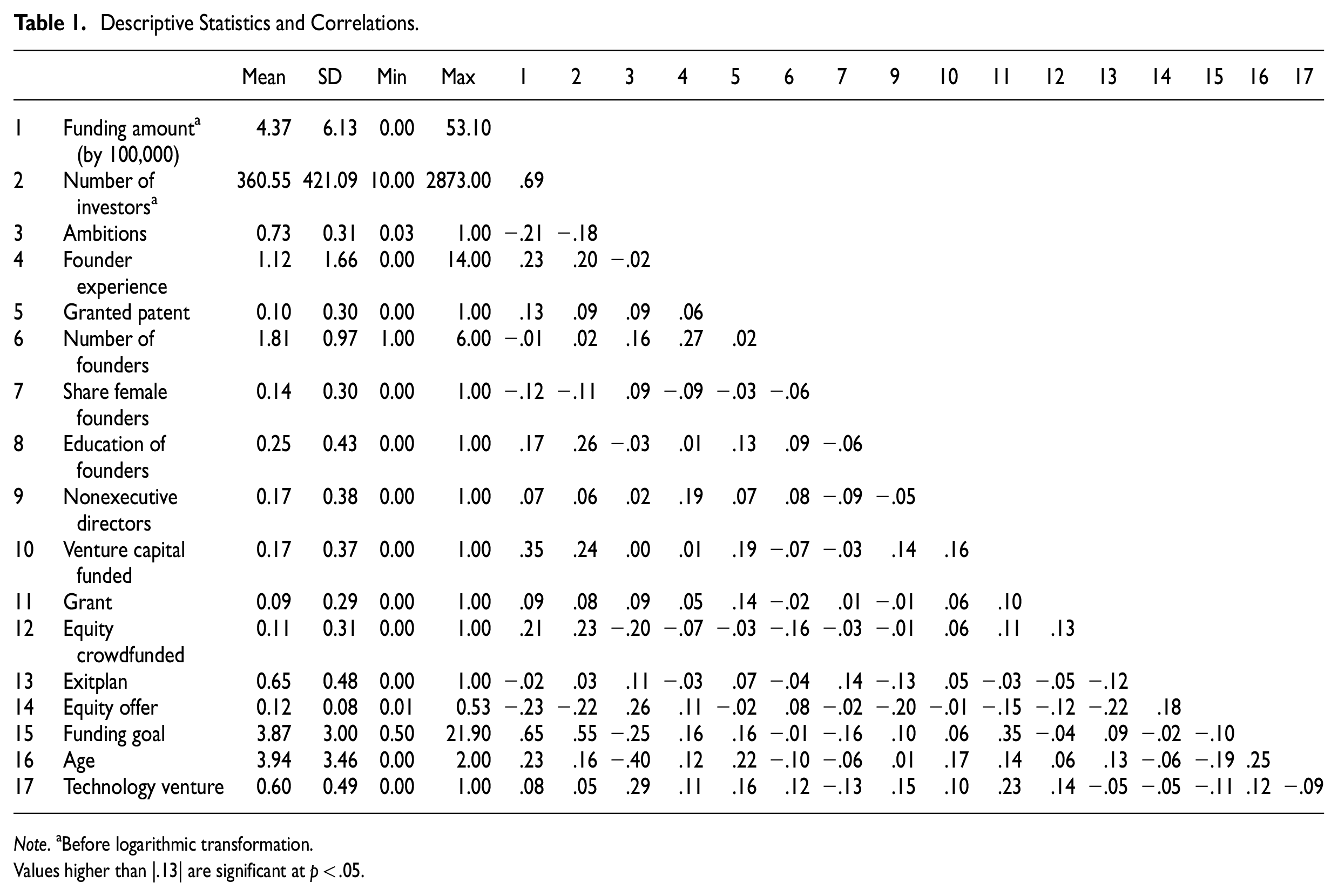

Table 1 contains the descriptive statistics and correlations. The minimum value of our ambitions variable equals .03, suggesting that all ventures predict at least some growth ambitions. The mean value is 0.73, meaning that entrepreneurs generally express high ambitions. This finding is not surprising; entrepreneurs have strong incentives to predict ambitious growth, as we have theorized.

Descriptive Statistics and Correlations.

Note. aBefore logarithmic transformation.

Values higher than |.13| are significant at p < .05.

We use ordinary least square regressions to test our hypotheses related to the funding amount and number of investors and calculate all models with robust standard errors to account for heteroskedasticity. Prior research uses the same approach to examine these dependent variables and potential curvilinear relationships (e.g., Taeuscher et al., 2021). As recommended for the tests of curvilinear relationships (Cohen et al., 2014), we mean-center our ambitions measure to address the extreme multicollinearity associated with interaction terms of the same predictor. The results are mathematically equivalent for centered and raw data (Haans et al., 2016), but mean-centering remains useful for facilitating interpretations of lower-order terms, which then reflect the effect at the average level of the variable (Cohen et al., 2014), equivalent to the average linear effect of our ambitions variable. In our research setting, the main effect of ambitions thus indicates whether the average new venture in our sample benefits from its expressed ambitions or specifies too high ambitions. Before reporting our results, we check the variance inflation factors (VIFs) in our regression models, which confirm that multicollinearity is not a concern (maximum individual VIF is 5.5), consistent with the generally low correlations across our explanatory variables (Table 1).

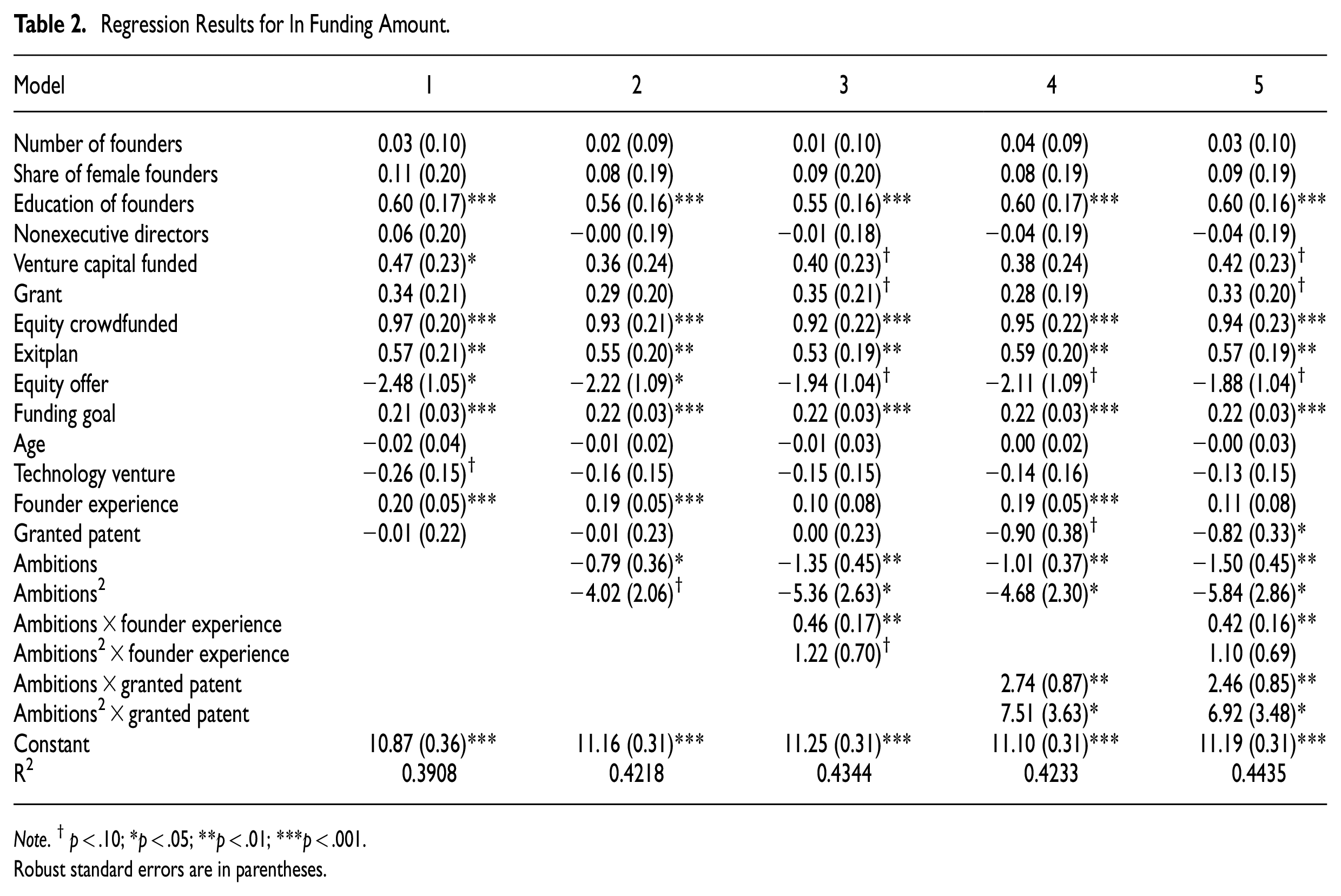

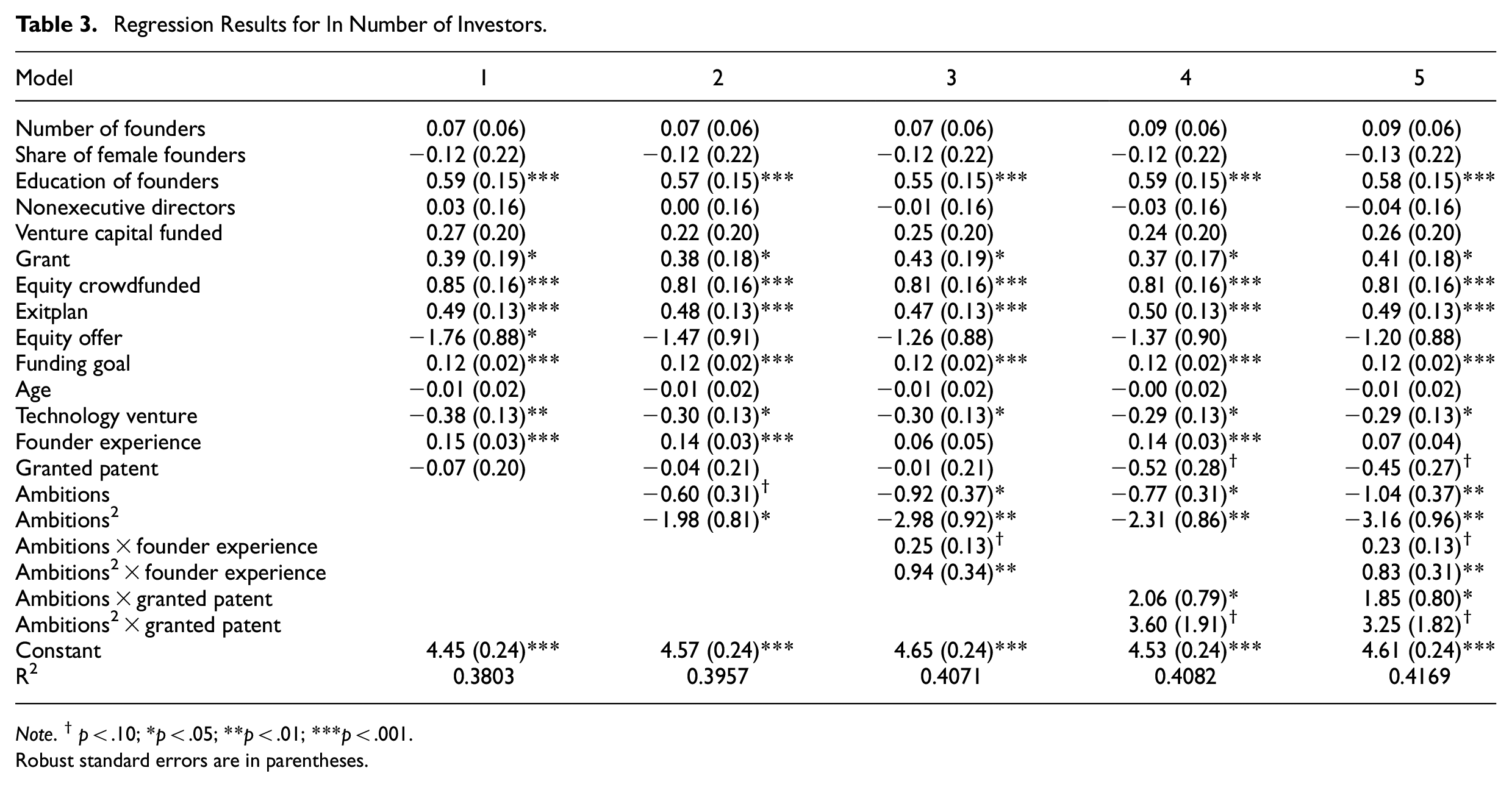

The regression results for the funding amount are in Table 2; those for the number of investors are in Table 3. Models 1 include the control variables only and echo prior results (e.g., Kleinert et al., 2020; Vismara, 2016). Models 2 introduce the ambitions variable and its squared term. The results support H1, in that the squared term of ambitions negatively affects funding amounts (β = −4.02, p = .053) and the number of investors (β = −1.98, p = .015). The negative, significant coefficient of the squared ambitions variable is a necessary condition to confirm a curvilinear relationship; we test additional conditions to affirm support for the inverted U-shape though (Haans et al., 2016). Following the procedure suggested by Lind and Mehlum (2010), 2 we first confirm that the slope of the curve is steep enough at both ends of the data range. That is, we test whether the slope is significant and positive at low levels of ambitions (=.05) and negative at high levels (=.95). The results confirm this condition for funding amounts (β = 4.7, p = .070; β = −2.54, p = .031) and number of investors (β = 2.11, p = .025; β = −1.46, p = .016). Second, we check whether the turning point is located within the observed data range and confirm that it is: The turning point for ambitions is 0.63 for the funding amount and 0.58 for the number of investors, and both their 95% confidence intervals are within the observed data range. Average expressed ambitions thus are above the turning point. Because we use mean-centered values, the coefficients of the linear effects for funding amounts (β = −.79, p = .030) and the number of investors (β = −.6, p = .053) are negative. We thus conclude that, on average, ventures communicate overly high ambitions that may render investors more skeptical. Our finding of an inverted U-shape for ambitions supports H1. Using the calculated average marginal effects in Model 2, we graph the curves for the funding amount in Figure 2a and the number of investors in Figure 2b; for illustrative purposes, they reflect non-mean-centered ambition values.

Regression Results for ln Funding Amount.

Note. †p < .10; *p < .05; **p < .01; ***p < .001.

Robust standard errors are in parentheses.

Regression Results for ln Number of Investors.

Note. †p < .10; *p < .05; **p < .01; ***p < .001.

Robust standard errors are in parentheses.

Main and moderation effects, Study 1.

The interactions between the squared term of ambitions and founder experience, as reported in Models 3, also offer support for H2, in that the interaction is positive and marginally significant for the funding amount (β = 1.22, p = .080) and highly significant for the number of investors (β = .94, p = .007). These positive coefficients indicate flattening of the curves (Haans et al., 2016). We calculate the average marginal effects for the interaction at different levels of founder experience (i.e., minimum, mean, +1SD, +1.5SD) and depict the effect sizes in Figure 2c and d. These results affirm that high levels of ambition can produce higher fundraising performance than moderate levels, as long as founder experience is sufficiently high. It is worth emphasizing that the negative effect of average expressed ambitions also can become positive at high levels of founder experience, according to the linear interaction terms (funding amount β = .46, p = .007; number of investors β = .25, p = .062).

Models 4 represent the interaction between ambitions and granted patents. In support of H3, the interaction between the squared term of ambitions and granted patents is positive and highly significant for the funding amount (β = 7.51, p = .040) and marginally significant for the number of investors (β = 3.6, p = .060). We calculate the average marginal effects and graph the curves in Figure 2e and f, which illustrate how high growth ambitions lead to more positive outcomes when combined with patents, whereas patents have no effect in the case of lower growth ambitions. Here again, the linear interactions are more positive than the negative main effect of ambitions (funding amount β = 2.74, p = .002; number of investors β = 2.06, p = .010). Thus, at an average level of ambitions, the negative effect gets reversed by ownership of patents.

Robustness Checks

Alternative Statistical Model

We rerun all our models from Tables 2 and 3 with negative binomial regressions, 3 which are appropriate for our dependent variables (Cameron & Trivedi, 2013), though they offer less straightforward tests of (inverted) U-shapes and their respective moderation effects (Haans et al., 2016). But even with this distinct approach, we find effects similar to those that result from our main analysis, with a few differences in the significance of the explanatory variables. In particular, the main effect of squared ambitions loses significance for the number of investors in the main model (β = −1.22; p = .110), but it remains significant in all other models and for the funding amount as the dependent variable (β = −1.79; p = .031). We also observe slight variations in the moderation effects. For example, with regard to funding amounts, founder experience has a significant, positive, linear interaction with ambitions, whereas moderation by squared ambitions turns nonsignificant. For the number of investors, we find a significant, positive, linear interaction between ambition and patents but no significant interaction between patents and squared ambitions. However, as Haans et al. (2016) note, such significant coefficients are neither necessary nor sufficient conditions to confirm curvilinear effects and their moderations in negative binomial regressions. We therefore also consider graphical representations, based on marginal effects, which confirm the similar effects and shapes of all the curves, relative to our main analysis (results available on request).

Ambitions Measure

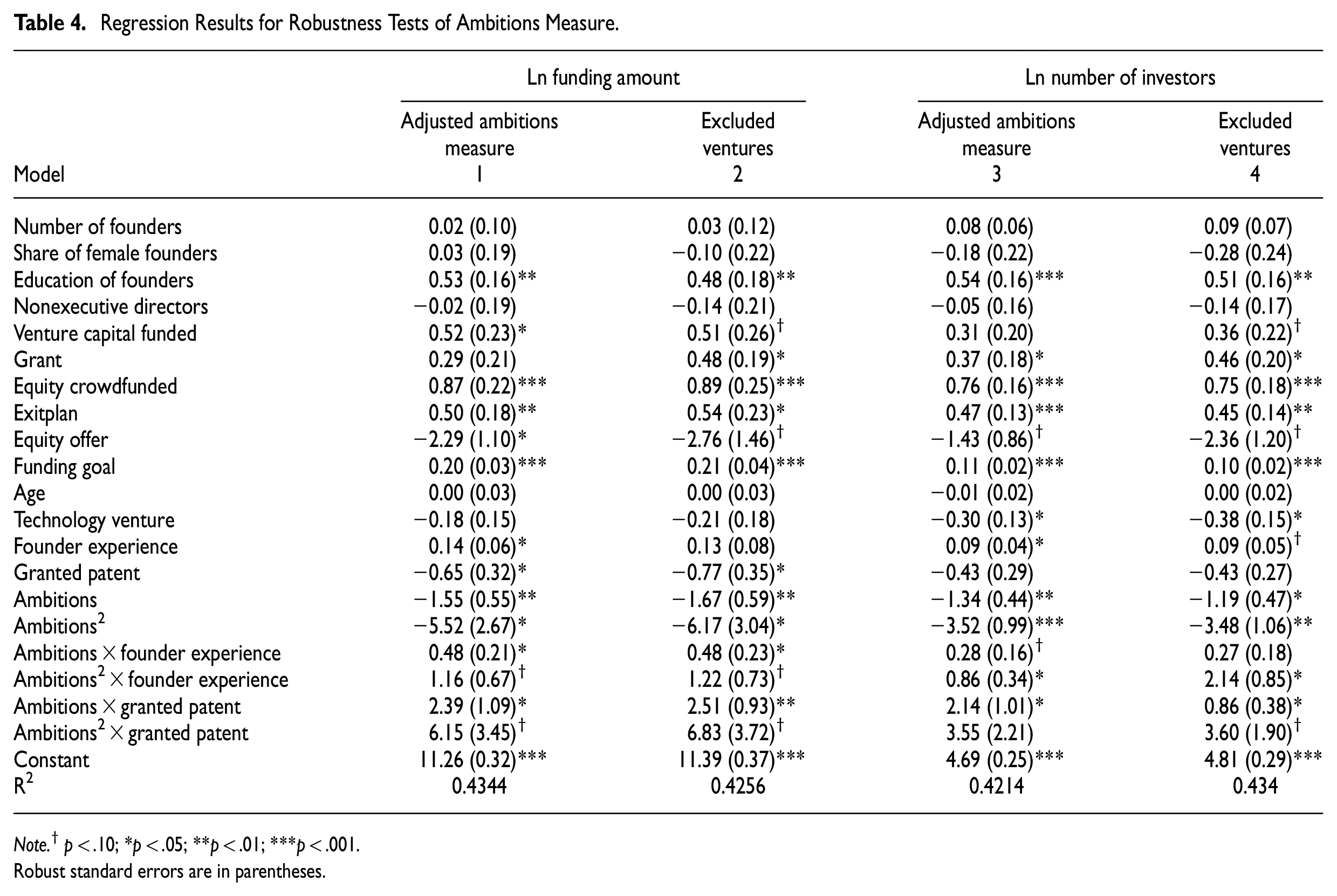

In our main analysis, new ventures that had not yet generated any revenue but forecast them for the coming year were ranked as extremely ambitious (ambition = 1). Such ventures were not even operational yet, which represents a crucial hurdle (Cassar, 2010). Early-stage investors likely perceive such ventures as very ambitious, because all their forecasted revenues are new and must be generated from new customers. However, such ventures also might forecast lower versus higher future sales, and our main analysis cannot account for this difference. Therefore, we conducted two robustness checks. First, we ran another analysis in which we assume all ventures had earned at least £10,000 in prior revenues (i.e., added 10,000 to all observations if their prior revenues were equal to 0). Table 4, Models 1 and 3, contains these results and confirms the findings of our main analysis. Second, we exclude ventures without prior revenues if they also forecast revenues below the threshold of £500,000, such that we retain only those new ventures that express clearly ambitious goals. 4 The results for this analysis are in Table 4, Models 2 and 4, and also confirm our results.

Regression Results for Robustness Tests of Ambitions Measure.

Note. †p < .10; *p < .05; **p < .01; ***p < .001.

Robust standard errors are in parentheses.

Founder Experience Moderation

With another robustness check, we replace the count variable of founder experience from the main analysis with a dummy variable (mean = .52). These results still confirm the main effects.

Patent Moderation

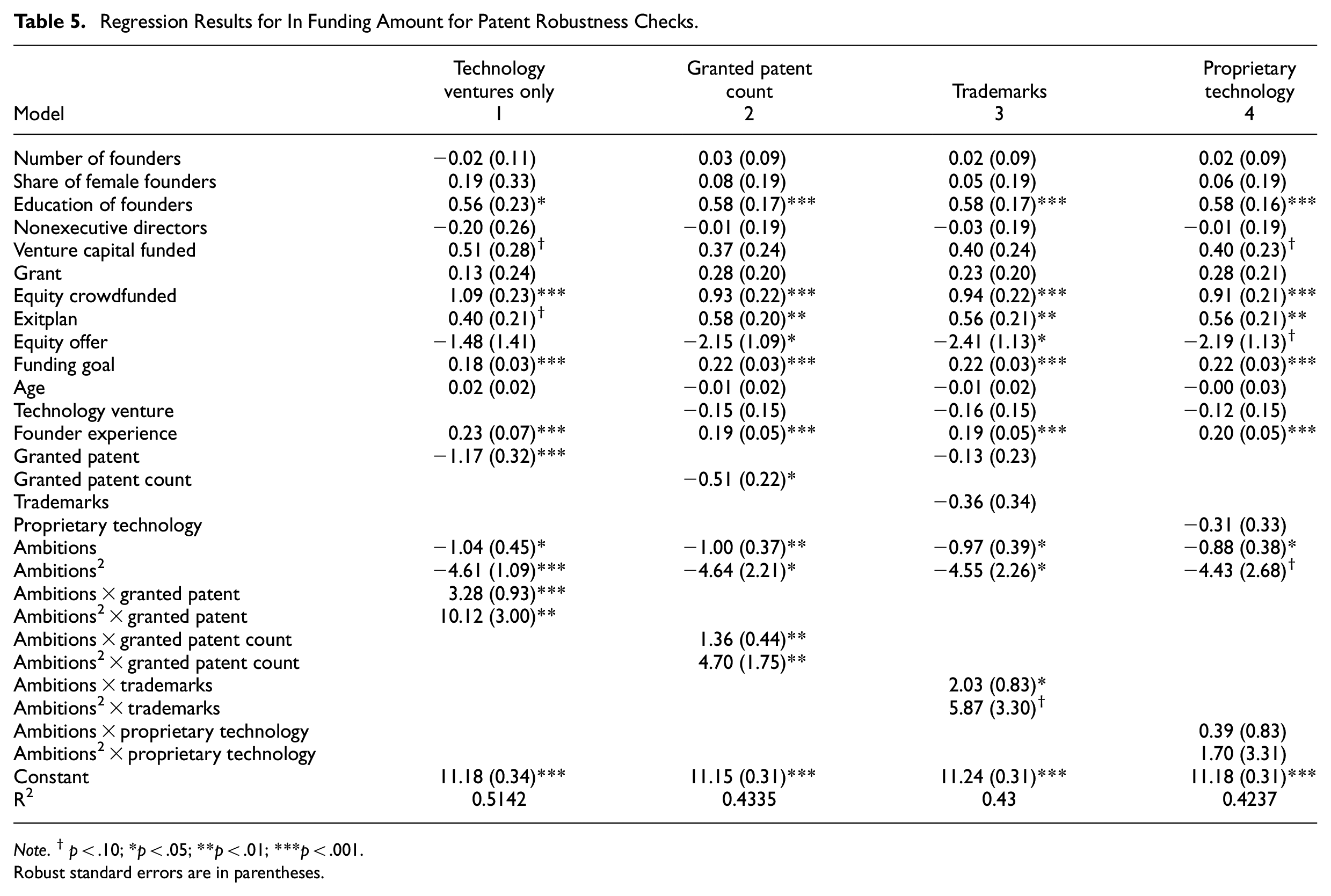

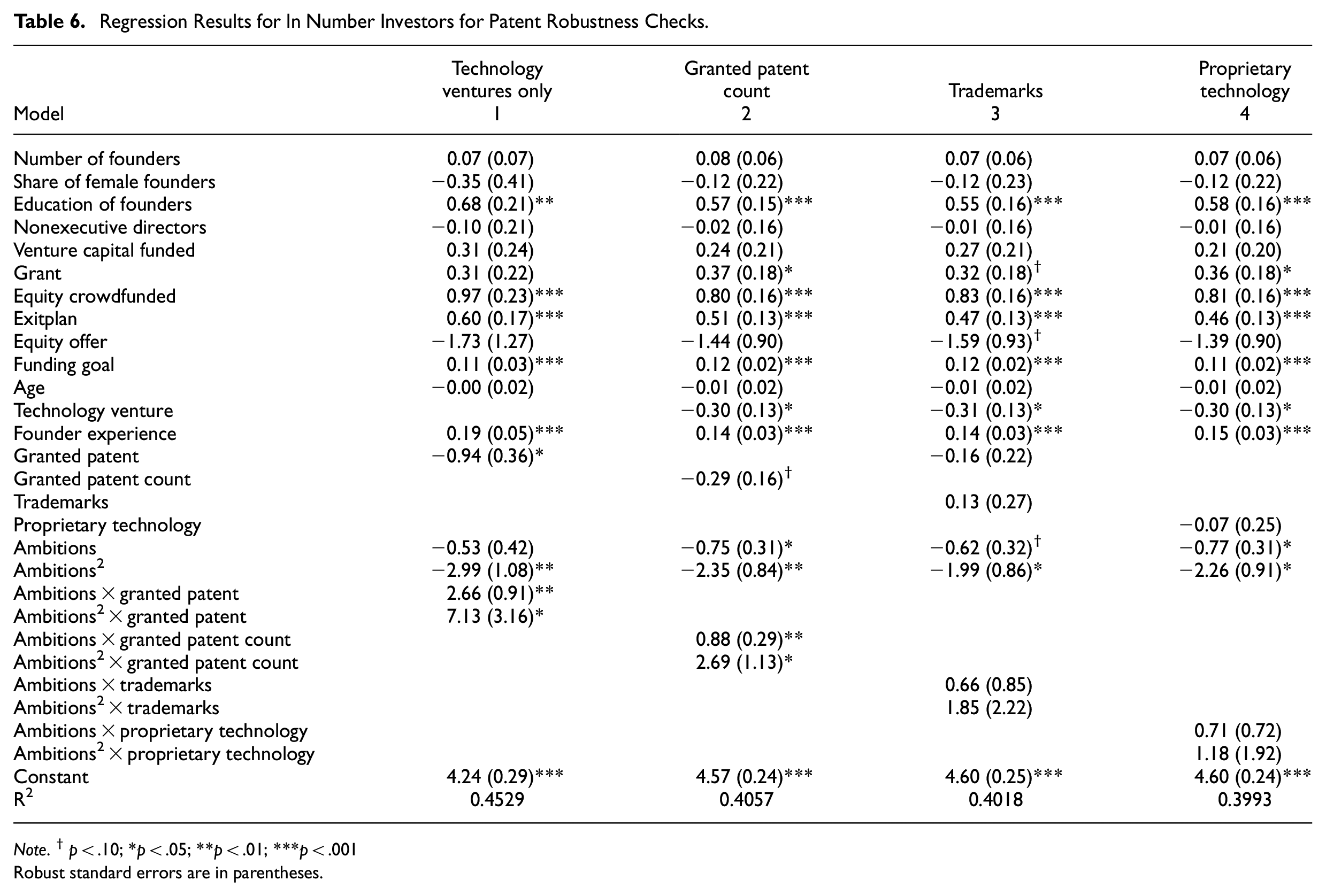

We conduct several robustness tests for our patent moderation effect, which we report in Table 5 for funding amounts and Table 6 for the number of investors. First, granted patents may be more important for technology ventures, so we conduct a robustness check with a subsample of technology ventures (Models 1). As expected, the moderation effect between granted patents and squared ambitions grows more significant and powerful for both dependent variables. However, we do not find that the main effect of granted patents turns positive in either the full model or the (unreported) main effect model. Second, we run robustness tests using patent counts, instead of a binary variable. New ventures with patents hold, on average, 2.2 patents, with a maximum of 11 patents in our sample. The results (Models 2) confirm a positive and significant interaction effect with squared ambitions, which is in further support of H3. Third, we employ alternative intellectual property variables that could provide signaling mechanisms similar to granted patents (Fisch et al., 2022). When we rerun the analysis with a dummy variable, indicating whether new ventures own trademarks (mean = .11), as indicated in their business plans, the results (Model 3) support a marginally significant positive interaction of trademarks and squared ambitions for the funding amount (β = 5.87; p = .077) but not the number of investors. We also consider whether new ventures have proprietary technologies (mean = .23), such that we denote this dummy variable as equal to one if a new venture indicates that it exclusively owns a technology, such as, if it has developed an application, tool, or software. This variable shows a high correlation with granted patents (.63), but we do not find any significant interaction effects with ambitions (Models 4). Proprietorship of a technology, seemingly has a much weaker signaling effect than patents, potentially because it distinguishes less clearly between the quality and uniqueness of technologies.

Regression Results for In Funding Amount for Patent Robustness Checks.

Note. †p < .10; *p < .05; **p < .01; ***p < .001.

Robust standard errors are in parentheses.

Regression Results for ln Number Investors for Patent Robustness Checks.

Note. †p < .10; *p < .05; **p < .01; ***p < .001

Robust standard errors are in parentheses.

Alternative Gender Measure

We reran all our regressions with an alternative gender measure, that is, whether the lead entrepreneur was female (Yang et al., 2020). In mixed gender teams, we considered the entrepreneur who holds the CEO position as the lead entrepreneur. The alternative gender measure is nonsignificant, and our results remain unchanged.

Study 1 Discussion

Our results support H1 and demonstrate an inverted U-shape of ambitions, such that too low and too high expressed ambitions can harm fundraising performance in equity crowdfunding. Expressions of low ambitions are less common in our data; in general, entrepreneurs display ambitions, which is both consistent with prior research (Cassar, 2010) and unsurprisingly, given that they are aware of early-stage investors’ return expectations. Accordingly, the most relevant case is the thin line between moderate ambitions and overly high ambitions. The former tends to be viewed favorably and enhances entrepreneurs’ fundraising success; expressing overly ambitious predictions of growth instead evokes penalties from early-stage investors. The average level of expressed ambitions in our sample already lies beyond the point that investors perceive as favorable. Thus, on average, entrepreneurs appear to be overshooting their ambitions and being penalized for it. Our results also support H2 and H3: Founder experience and patents accomplish similar purposes and lend credibility to expressions of high ambitions. The magnitudes of these effects are substantial and reveal that the negative effects of high ambitions can be reversed in the presence of costly signals. When entrepreneurs signal their high levels of experience, their high ambitions can even yield the best funding outcomes. Another interesting result emerges: Patents seem to have negative effects when new ventures express very low ambitions.

The design of Study 1 is consistent with prior equity crowdfunding research that uses campaign-level data (e.g., Ahlers et al., 2015; Vismara, 2016, 2018), but because equity crowdfunding platforms prescreen new ventures, these data may suffer from endogeneity concerns (Kleinert et al., 2021). Platforms might even select more ambitious new ventures so that our sample would be biased. To address these concerns, as well as increase the validity of our findings, we adopt an experimental design for Study 2.

Study 2: Conjoint Analysis with Equity Investors

Conjoint Design

To confirm the main findings of Study 1 in an experimental setting and increase the generalizability of our results (Stevenson et al., 2020), we conduct a metric conjoint experiment in Study 2. As a decomposition research method, conjoint analysis is well-suited to examining early-stage investors’ judgments (e.g., Drover et al., 2017; Murnieks et al., 2011), and it overcomes limitations associated with other research methods (Hsu et al., 2017). Because it can support data collection based on when respondents make decisions, it offers reliable insights into individual decision-making preferences (Green & Srinivasan, 1990). Respondents assess a set of hypothetical venture profiles which differ on manipulated attributes; in this study, we manipulate two levels each of ambitions, founder experience, and granted patents.

We focus on moderate and high levels of ambitions in our effort to confirm both the negative main effect of expressions of overly high ambitions and the positive moderation effects of complementary, costly signals. This design reflects three intentional choices. First, we learned that few new ventures express low levels of ambition, and the average entrepreneur expressed growth ambitions beyond the identified turning point, which produced negative effects. Thus, the range between moderate and high ambitions is particularly relevant. Second, the inflection points of the ambition variable in Study 1 were 0.63 and 0.58, so two levels of ambition, before and after these inflection points, are sufficient to validate our results. Third, as theorized and shown in Study 1, the credibility-buffering effect of complementary, costly signals should be particularly important for new ventures that express high ambitions, which suffer most from credibility problems. Accordingly, considering two levels of ambition is appropriate to replicate the main findings from Study 1.

Sample

We recruited 150 equity investors from the U.K. Prolific platform, which is a frequently used, reliable source of input from early-stage and equity crowdfunding investors (Butticè et al., 2021; Zunino et al., 2021). The participants received fair compensation, in line with Prolific.co guidelines. To ensure a representative sample (Butticè et al., 2021; Van Balen et al., 2019), we required respondents to have experience in some form of equity and early-stage investments (e.g., angel syndicates, stock market, venture capital fund). To mirror the Study 1 context, we sought only U.K. respondents. We excluded 18 respondents who did not respond correctly to an attention question (“What was the product offered by the start-up?”) or were among the 2% of outliers who completed the survey very quickly or very slowly (cf. Younkin & Kuppuswamy, 2018). The final sample consists of 132 respondents who made 1,056 decisions. Their median age is between 31 and 40 years, most are men, and they generally have undergraduate degrees.

Experimental Design

The design follows best practices from previous conjoint studies in a new venture financing context (Drover et al., 2017; Kleinert et al., 2021), with three stages: description of the task and reference setting, conjoint profiles, and post hoc survey questions. At the start, we explained the decision-making task and setting and asked respondents to take an equity crowdfunding investor’s perspective to evaluate a set of new venture financing opportunities. To match the Study 1 context, we also presented respondents with the same information that registered members on Crowdcube receive before investing (e.g., procedure, return and risk potential). The baseline start-up characteristics also matched, such that the respondents have the same venture in mind when assessing the different profiles (Hoenig & Henkel, 2015). In detail, we obtained a pitch proposal from Crowdcube (see Figure A1 in the Appendix) and adjusted it slightly so that it resembled a typical venture from Study 1 (e.g., 3 years old, two entrepreneurs, 10% equity on offer). Before participants could continue, they completed an instruction check that asked whether they understood the task and setup (Scheaf et al., 2018).

Next, to gather their evaluations of a set of hypothetical ventures, we used a full-factorial design with two levels of each of the three attributes (ambitions, founder experience, and patent), resulting in eight unique conjoint profiles (see Drover et al., 2017; Murnieks et al., 2011). This design ensures orthogonality (i.e., zero correlation among attributes) and enables us to test main and interaction effects. Respondents were randomly assigned to different survey versions, in which the order of the eight profiles and the attributes within profiles both were random, which reduces the potential for order effects (Hsu et al., 2017).

We performed several measures to ensure the validity of our experiment. First, the experimental setup (task description, reference setting, attributes) reflects a real venture and platform from the Study 1 context. Second, the sample of respondents is representative of investors from previous equity crowdfunding studies (Butticè et al., 2021; Zunino et al., 2021). Third, we interviewed two equity crowdfunding experts, to check the clarity of the scenario and attributes. They affirmed the high validity of our design, and we used their feedback to make minor changes in the wording of the attributes and reference setting.

Variables

Dependent Variable

To match Study 1 and previous conjoint studies (Fu & Tietz, 2019; Murnieks et al., 2011), we use two dependent variables, based on 7-point Likert scales, to examine funding performance. The variables are the funding amount, measured as the likely amount that the respondent would invest (lowest to highest possible amount), and investment likelihood, measured as the probability that the respondent would invest in the proposed venture (very low to very high).

Explanatory Variables

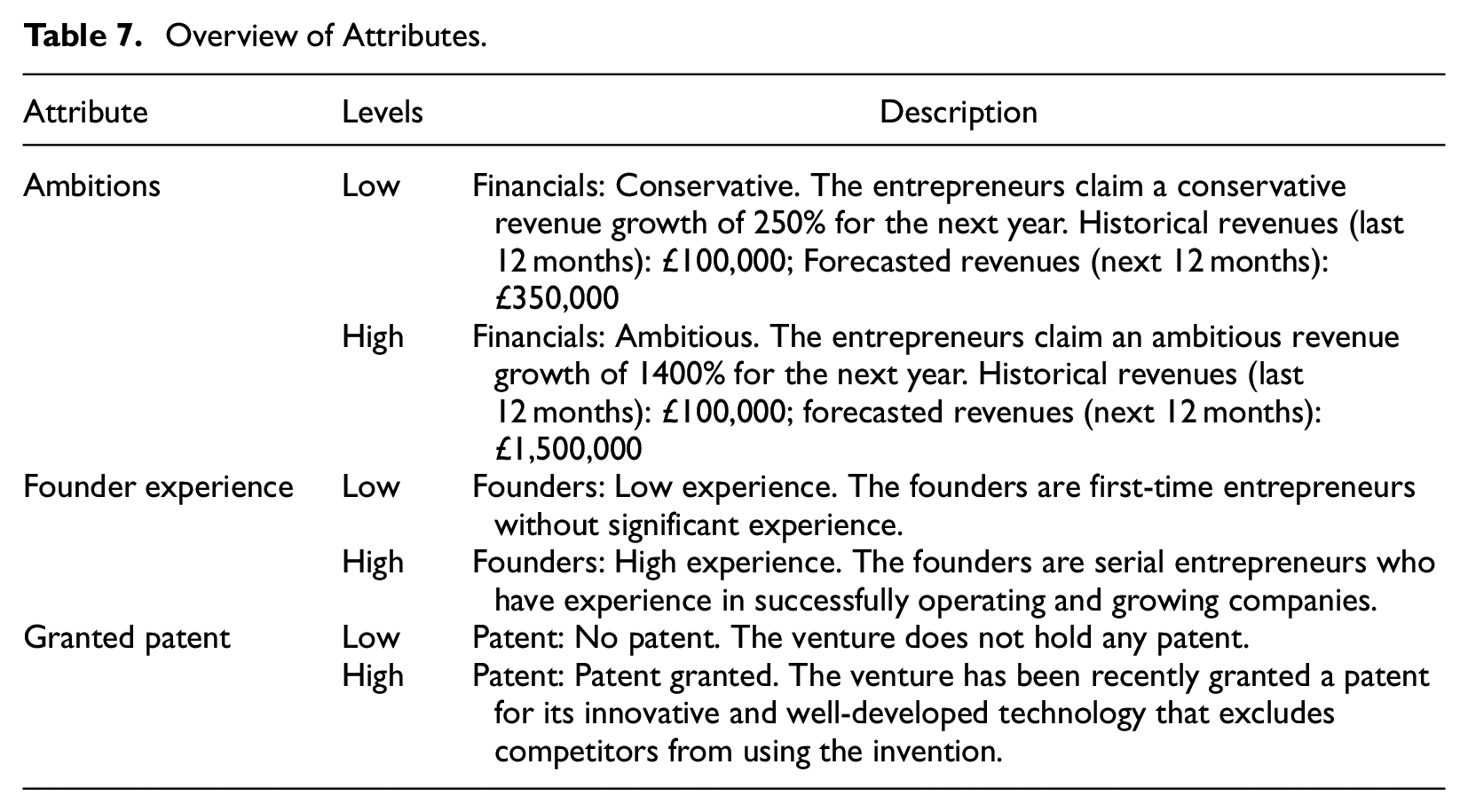

The manipulations of the attributes match the Study 1 variables (see Table 7). The main focus of this conjoint study is to confirm the negative effect of overly high ambitions and the respective positive interaction effects of costly signals. Accordingly, we examine two levels of ambition. In both the low- and high-level conditions, new ventures generated historical revenues of £100,000 (near the median value in Study 1). In the low-level condition, a new venture’s financial forecast was described as conservative, predicting revenues of £350,000, whereas in the high-level condition, the financial forecast was described as ambitious and predicted revenues of £1,500,000. The low-level condition would thus equal to 0.56, whereas the high-level condition would be 0.88, for the index variable we used in Study 1. These values translate into realistic, even numbers, and they are below and above the inflection point, respectively, of our ambitions measure from Study 1. As in Study 1, the ambitions attribute is presented as part of the financials, in a typical tabular format, as obtained on Crowdcube, together with a brief caution that financial forecasts are not reliable indicators of future performance. The founder experience attribute appears in the team description, referring to low or high experience (Plummer et al., 2016). In the low experience condition, we define founders as first-time entrepreneurs; in the high experience condition, they are serial entrepreneurs. Consistent with Study 1, the attribute reflects either the minimum founder experience (i.e., 0 in Study 1) or the mean of founder experience (i.e., 1 in Study 1). Finally, the granted patent attribute cites no patent for the low level and a granted patent for the high level (Scheaf et al., 2018). All three attributes are dummy variables, with low-level conditions as reference groups.

Overview of Attributes.

Control Variables

We captured several relevant control variables in a post hoc survey (Fu & Tietz, 2019; Murnieks et al., 2011; Van Balen et al., 2019). Respondents indicated their gender, age group, education (five options, up to postgraduate), entrepreneurial background (having founded a company before), investment experience (very low to very high), and willingness to take risks (not at all to very willing).

Results

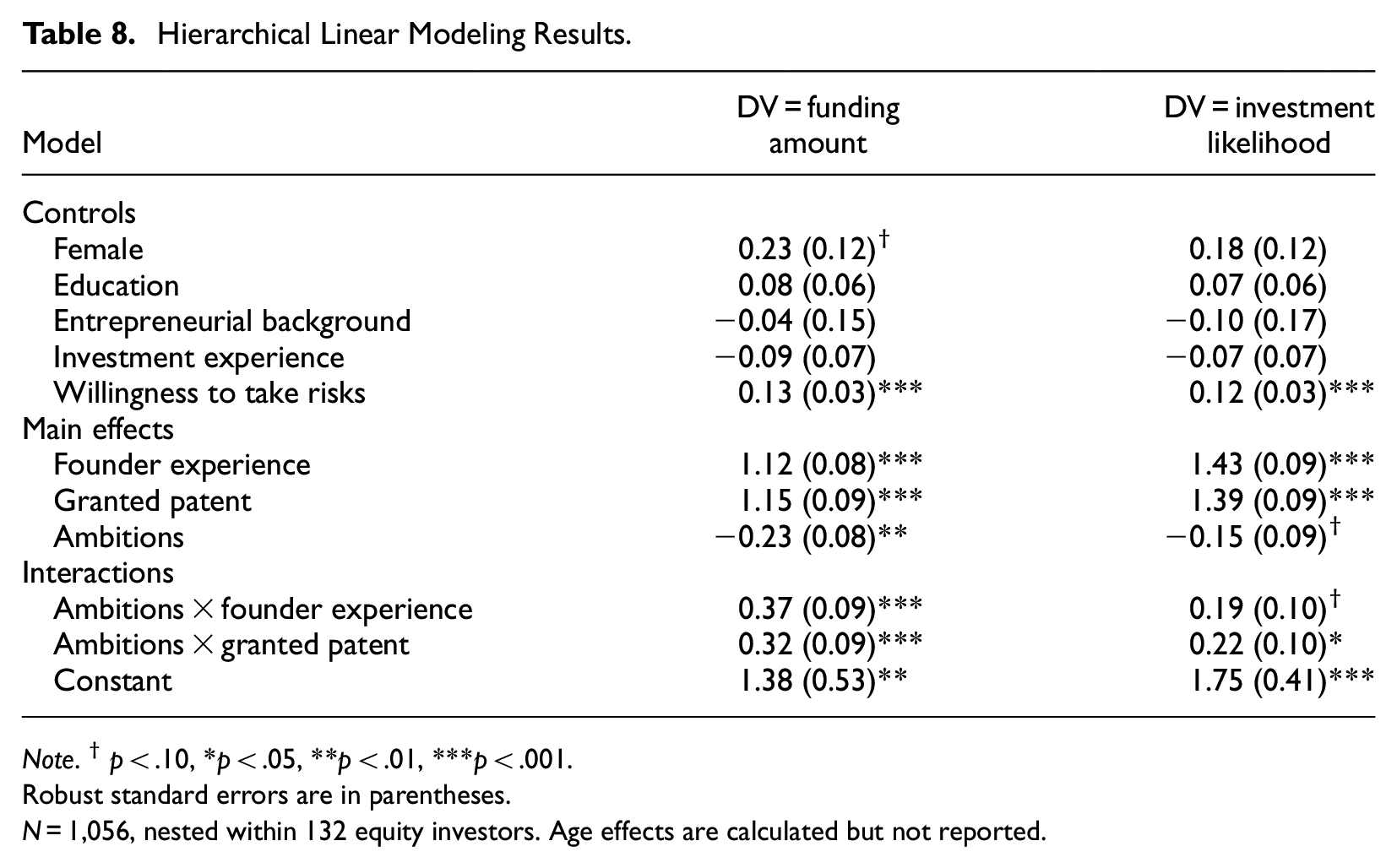

We use hierarchical linear modeling (HLM) to analyze the conjoint data, as is standard in conjoint studies (Lohrke et al., 2010). It accounts for the nested data structure; multiple conjoint profiles (level 1) can be assessed by individual respondents (level 2). In HLM, respondents become the controls for their decision-making preferences, so we can control for unobserved individual-level effects (Hsu et al., 2017). The coefficients can be interpreted as the change in the dependent variable for a 1-unit increase in the independent variables (Drover et al., 2017). In Table 8, we provide the HLM results; due to the orthogonal conjoint design and in line with previous research, we report the full models (Drover et al., 2017; Murnieks et al., 2011).

Hierarchical Linear Modeling Results.

Note. †p < .10, *p < .05, **p < .01, ***p < .001.

Robust standard errors are in parentheses.

N = 1,056, nested within 132 equity investors. Age effects are calculated but not reported.

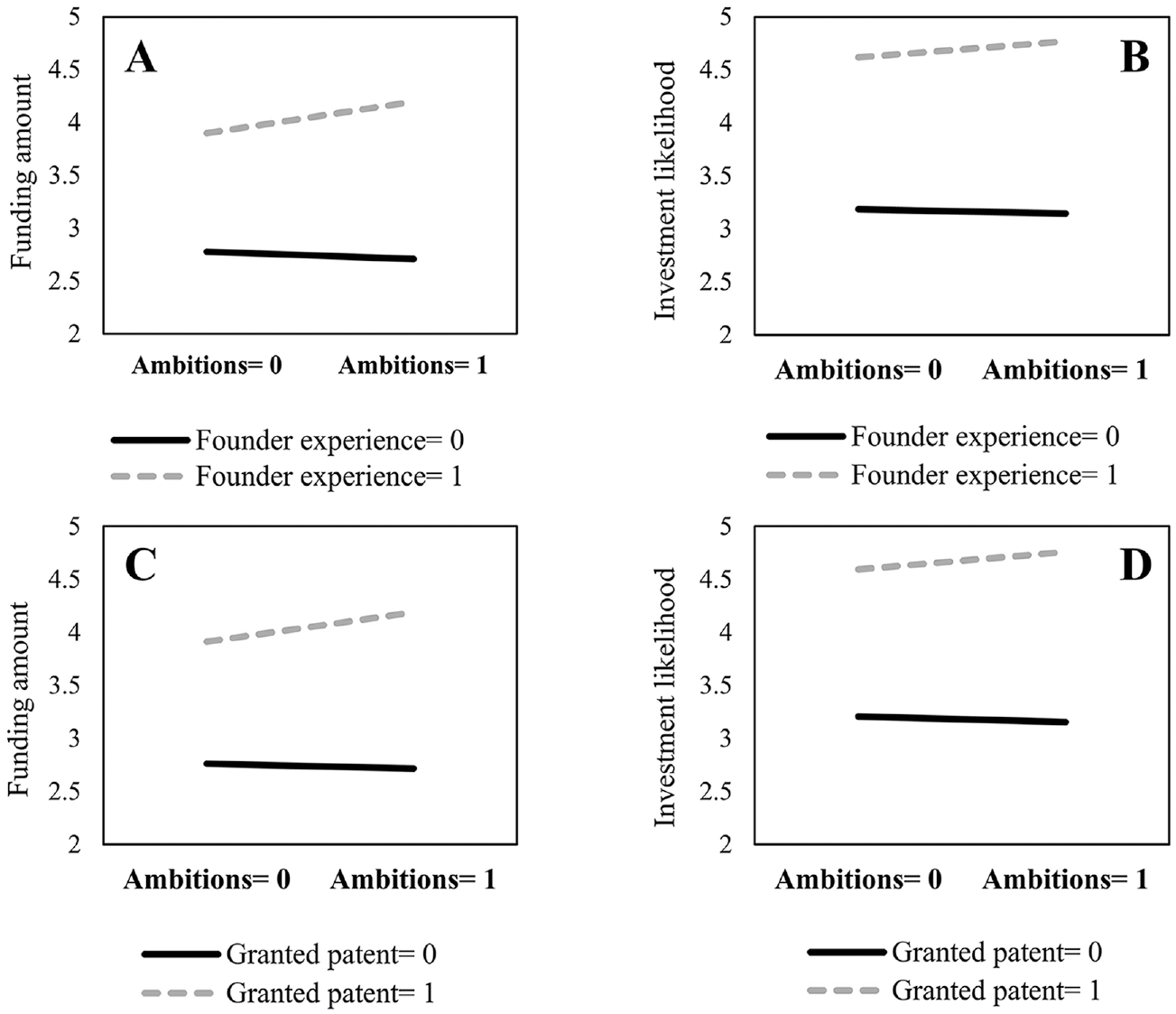

In support of our Study 1 results, the coefficient of the ambitions variable is significant and negative, though this effect is more significant and negative for the funding amount (β = −.23; p = .004) than for investment likelihood (β = −.15; p = .096). The negative effect for both dependent variables also is smaller than the respective interaction effects, so the negative effect of ambitions appears conditional on the absence of costly signals. We find support for the moderating effects of costly signals: The interactions between ambitions and founder experience (funding amount β = .37; p = .000; investment likelihood β = .19; p = .053) and between ambitions and granted patents (funding amount β = .32; p = .000; investment likelihood β = .22; p = .038) are significant and positive for both dependent variables. Using the calculated average marginal effects, we depict the moderating effects of founder experience in Figure 3a and b and those of patents in Figure 3c and d.

Interaction effects, Study 2.

As is true of all conjoint studies, interpreting the practical meaning of the effect sizes requires caution, because investors evaluated the new ventures on a 7-point Likert scale (Murnieks et al., 2011). To gauge the meaning of these effect sizes, we can compare them with effect sizes reported in prior, similar conjoint studies (Aguinis & Harden, 2010). The effect sizes we find compare favorably to previously reported ones in conjoint studies involving early-stage investors (e.g., Drover et al., 2017; Murnieks et al., 2011). 5

Discussion

A key challenge for entrepreneurs is to convince early-stage investors about their prospects of success (Huang & Pearce, 2015). Despite a general agreement that entrepreneurs need to send signals in such situations (Bafera & Kleinert, 2022), a controversy has arisen regarding whether such signals must be costly to be perceived as credible (Colombo, 2021). With this study, in an effort to elaborate on existing theory (Fisher & Aguinis, 2017), we analyze the extent to which expressed growth ambitions, as a salient, number-based costless signal, induce favorable responses in the early-stage financing context of equity crowdfunding. Our results suggest that expressed growth ambitions convey relevant information about a new venture’s earning potential to early-stage investors, but they also can evoke countervailing credibility problems. Above a certain threshold, expressed growth ambitions start to have negative effects. On average, entrepreneurs in our sample express overly high ambitions and get penalized for it. To establish a credibility buffer and reverse the negative effect, they need to send complementary, costly signals that can transform high growth ambitions from cheap talk into credible signals. In leveraging these findings, we next discuss our work’s theoretical and managerial implications, boundary conditions, limitations, and directions for further research.

Theoretical Contributions

Our study contributes to the emerging research on costless signals (Anglin et al., 2018; Di Pietro et al., 2020; Steigenberger & Wilhelm, 2018) and offers a deeper understanding of how they relate to fundraising performance. Rather than assuming linear relationships between costless signals and new ventures’ fundraising performance, we predict and provide initial evidence of an inverted U-shaped relationship. This insight is crucial; it suggests a tension between the transmission of relevant, positive information and credibility issues as two opposing mechanisms that drive the effectiveness of costless signals. Accordingly, our study indicates a threshold, up to which the relevant information of costless signals prevails, before credibility issues dominate and investors dismiss costless signals as cheap talk.

Unlike prior research that has focused on rhetoric that conveys positive psychological capital, virtuousness, or emotions of entrepreneurs as costless signals (Anglin et al., 2018; Moss et al., 2015; Payne et al., 2013), we investigate expressed growth ambitions as number-based signals that convey future-oriented information. Building on constructive critiques that indicate rhetoric may be insufficiently addressed by traditional signaling theory (Steigenberger & Wilhelm, 2018), we consider the role of number-based costless signals, which may be uniquely relevant in noisy environments, such as crowdfunding, in which investors may overlook qualitative information (Steigenberger & Wilhelm, 2018). Such number-based signals tend to evoke more automatic processing by investors (Hayward & Fitza, 2017), even in noisy fundraising environments. The introduction of number-based costless signals is therefore an important extension of prior research, but may also constitute a boundary condition for our findings regarding the inverted U-shaped effects. As we have theorized herein, because entrepreneurs have much to gain from overpromising, and growth ambitions are difficult to validate, entrepreneurs might sense few inhibitions about engaging in cheap talk. Thus, number-based signals that predict future growth might seem like “too much of a good thing,” interpreted as manipulative attempts to meet early-stage investors’ expectations. To what extent our results are generalizable to rhetoric remains an open question. We suspect that also rhetoric-based costless signals may at a certain point be perceived as disingenuous attempts to create a positive impression. For example, excessive uses of virtue rhetoric (Payne et al., 2013) or overly positive rhetoric about the founders’ psychological capital (Anglin et al., 2018) may no longer appear credible and could be penalized by investors. Because we do not control for rhetoric-based costless signals in our study, we cannot infer the relative effectiveness of number-based versus rhetoric-based signals either. We hope our results provide new impetus for research designed to study how different costless signals vary in their effectiveness and potentially stop working at certain thresholds.

Furthermore, in line with recent calls for research (Colombo, 2021), we offer new insights into the concept of signal portfolios (Bafera & Kleinert, 2022; Drover et al., 2018) and the relationship between costless and costly signals. Both costless and costly signals can provide complementary functions in a new venture’s signal portfolio; as Anglin et al. (2018) show, when new ventures use costly human capital signals, it strengthens the positive effect of their rhetoric-based costless signals. Steigenberger and Wilhelm (2018) find that entrepreneurs can leverage rhetoric-based costless signals to complement costly signals if the rhetoric offers additional relevant information or enhances their visibility. We add to this research stream by providing the novel insight that costly signals might be not just complementary but requisite. They are necessary to buffer the credibility of costless signals and resolve the tension between relevant information and credibility issues. Accordingly, costly signals offer little additional value for costless signals presented at lower or moderate levels, because these costless signals do not raise severe credibility concerns. Their ability to lend credibility to a number-based costless signal at a high level is powerful though; as we show, high expressed growth ambitions have negative implications in isolation, but additional costly signals reverse this effect. Although both founder experience and patents, as costly signals, can provide such benefits, the moderating effect of founder experience is more pronounced. Together with very high ambitions, it can create the best configuration. Perhaps founder experience is an especially strong signal in the early-stage funding context (Ko & McKelvie, 2018); it offers pertinent information about entrepreneurs’ credibility and thus the trustworthiness of otherwise cheap talk. Patents instead might offer signals about the firm’s economic capabilities (Audretsch et al., 2012), but not so much about the credibility of the entrepreneurs expressing their ambitions.

Another important theoretical consideration, related to the interplay of costly and costless signals in a portfolio, involves the rarely considered concept of signal conflicts (Bafera & Kleinert, 2022). When signals conflict, it likely reduces the value of a signal portfolio as demonstrated by prior work in the initial public offering (IPO) context (Wang & Song, 2016). We identify this effect in relation to costless signals in early-stage funding. For example, patents alone do not seem to attract equity crowdfunding investors, such that their effect is positive only when combined with expressions of high ambitions, as a costless signal. 6 As a logical explanation, we posit that investors expect high growth from patent-holding ventures, so expressions of lower ambitions contradict patent ownership and imply insufficient dedication to exploiting the competitive advantage that the patent offers. This more nuanced view clarifies how costless signals can inform the effectiveness of costly signals, as well as how their inconsistency might jeopardize the value of a signal portfolio. This evidence, in turn, indicates the need to consider the interplay of various costless and costly signals in a portfolio carefully.

In relation to entrepreneurship signaling theory, this study contributes new insights to the ongoing controversy about whether signals need to be costly (Steigenberger & Wilhelm, 2018; Vanacker et al., 2020). Traditional signaling theory requires that, for signals to be effective, they must be costly, which prevents inferior ventures from imitating them (Connelly et al., 2011). But modern versions relax this costliness condition, with an implicit assumption that resource providers might believe even unverifiable claims by new ventures. This strong assumption does not account for severe credibility concerns in entrepreneurship contexts (Maxwell & Lévesque, 2014), nor the widespread evidence of intentional lies, camouflaging, and misrepresentation as common practices by entrepreneurs (Benson et al., 2015; Rutherford et al., 2009; Scheaf & Wood, 2021). In nontraditional fundraising contexts though, costless signals still might be required, because the environments tend to feature noise and less sophisticated audiences (Anglin et al., 2018; Steigenberger & Wilhelm, 2018). As we show in the hybrid equity crowdfunding context, which includes environmental conditions of both crowdfunding and traditional early-stage funding, investors obtain relevant information from costless signals too. Yet we theoretically challenge the universal effectiveness of costless signals and empirically show that investors sometimes penalize them. We thereby offer entrepreneurs a novel insight and recommendation: Their excessive, unverifiable performance claims, if presented without any credibility buffer, can produce adverse consequences. By detailing how costless signals work, we introduce an entrepreneur’s credibility as a critical boundary condition for the effectiveness of costless signals to this line of research.

Accordingly, we argue that credibility, conveyed through a reasonable quantity of the costless signal or additional costly signals, provides a hitherto missing theoretical mechanism for explaining why costless signals transform from cheap talk into effective signals. Noting our equity crowdfunding research context though, we acknowledge some unique characteristics that might represent constraints on the generality of our findings (Simons et al., 2017). First, our results may not generalize to other crowdfunding types. For example, in reward crowdfunding or microloan markets, resource providers often operate with a social or community logic (Anglin et al., 2020; Fisher et al., 2017), rather than an economic return logic (Cholakova & Clarysse, 2015). Thus, they may be less suspicious and more inclined to believe entrepreneurs’ claims. The relevance of credibility in these nontraditional funding contexts represents an exciting question for continued research. Second, we note constraints on the generality of our findings to other traditional early-stage financing settings (Huang & Pearce, 2015). While venture capitalists or business angels embrace return logics similar to investors in equity crowdfunding, they tend to be more sophisticated and confront less noisy environments. They also invest larger sums, hold more control rights, and employ other agency mechanisms to manage their risks even after the investment; they might interpret information (i.e., costless and costly signals) differently than equity crowdfunders. Arguably then, venture capitalists or business angels might not even consider costless signals; we suspect that they might rely on costless signals if they become convinced of the entrepreneurs’ credibility. Still, we cannot draw conclusions about the extent to which our results are generalizable to these other early-stage investors. Therefore, an important direction for research is to investigate costless signals and credibility as potential boundary conditions across various new venture financing contexts.

Managerial Implications

Entrepreneurs often overstate growth figures in their existing relationships with venture capitalists (Collewaert et al., 2021); if they do so in the early stages, when trying to attract prospective equity crowdfunding investors, on average, they get penalized. These early-stage investors demand financial outlooks though, so entrepreneurs must recognize the consequences of their ambitious claims and realize that expressing high growth ambitions might backfire. Even if equity crowdfunding investors expect growth ambitions, entrepreneurs would be ill-advised to overpromise, because it carries significant risk and could be perceived as cheap talk or a trust violation that then limits the new ventures’ access to early-stage funding. Especially novice entrepreneurs who have not yet developed any credentials should be cautious. However, these recommendations change if entrepreneurs can demonstrate credibility. In doing so, they encourage leaps of faith by investors, such that their unverifiable claims can evoke positive reactions, to the extent that they can benefit more from expressions of high growth ambitions. Thus, entrepreneurs who have strong performance records should realize they are expected to be ambitious. For example, a patent-holding venture may raise suspicions if it does not signal that it seeks high growth.

Limitations and Further Research

Some limitations of our studies provide room for further research. First, the ambition measure we use reflects revenues, which is appropriate because higher revenues are critical antecedents of returns for investors (Bapna, 2019) and provide key financial information in early-stage investment contexts (Collewaert et al., 2021). However, entrepreneurs can signal their ambitions in other ways too, such as with descriptions of internationalization plans or employee growth (Cassar, 2004). Research opportunities thus exist with regard to other measures of growth ambitions. In particular, it might be interesting to combine our quantitative measure with other qualitative measures to investigate complementary effects.

Second, in line with prior research, we conceptualize costless signals as requiring no implementation costs (Anglin et al., 2018). Such signals still might theoretically separate higher from lower quality ventures, because disingenuous signals could lead to penalty costs when they turn out to be false ex-post (Bafera & Kleinert, 2022). While we cannot fully account for this explanation, this scenario seems relatively unlikely in equity crowdfunding, where investments are anonymous, and entrepreneurs and investors rarely interact beyond the funding round (Ahlers et al., 2015). But in other contexts, such as venture capital, it becomes a plausible scenario, because close working relationships and stronger governance mechanisms make it easier for investors to verify and penalize previously issued signals (Collewaert et al., 2021). Then entrepreneurs might worry about failing to obtain follow-up investments from venture capitalists. Additional research should address signals that are costless in some contexts, like equity crowdfunding, but potentially costly in others, like venture capital.

Third, our multistudy, mixed-methods approach achieves consistent findings in support of the hypotheses, but each individual study remains subject to limitations. Study 1 draws on campaign-level data from a leading equity crowdfunding portal (e.g., Kleinert et al., 2020; Vismara, 2018), which preselects new ventures (Kleinert et al., 2021), such that it might exclude those without any growth ambitions. The surprising, nonsignificant main effect of patents in Study 1 also could be explained by data factors; perhaps high-performing firms with patents prefer to turn to other sources of available financing (Walthoff-Borm et al., 2018). Furthermore, in Study 1, some of the effects are only marginally significant, possibly due to the relatively small sample size. Confirmatory research thus is needed. Study 2 addresses some of the concerns with an experimental design (Van Balen et al., 2019; Zunino et al., 2021), but conjoint analysis creates its own limitations (Murnieks et al., 2011). Because respondents evaluate hypothetical instead of real ventures, conjoint designs inherently feature some artificiality (Hsu et al., 2017). To reduce this concern, we used a realistic reference setting, based on a real venture description from Crowdcube, and ensured the validity of our attributes by drawing on real venture information from our Study 1 data and interviews. The triangulation of different methodological approaches (Stevenson et al., 2020) and the consistency of our findings increases confidence in the generalizability of the findings, but further tests could reaffirm it.

Conclusion

We elaborate on signaling theory in entrepreneurship research by recognizing that stating growth ambitions, as a costless signal, enters into an inverted U-shaped relationship with equity crowdfunding performance. Overly high stated growth ambitions can be ineffective and harmful to entrepreneurs. Entrepreneurs’ credibility emerges as a boundary condition for effective costless signals. The empirical results, relevant for both theory and practice, provide new empirical evidence that entrepreneurs can make their costless signals work, either by expressing them at an optimal, credible level or by complementing them with costly signals.

Footnotes

Appendix

Acknowledgements

I thank the editor and the anonymous reviewers for their numerous helpful and constructive comments. I am further grateful to Diemo Urbig, Martin Carree, René Belderbos, and Julian Bafera for their comments on earlier versions of this manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.