Abstract

This study examines the influence of market conditions—hot versus cold—on the decision-making processes of venture capitalists (VCs). Prior research suggests that VCs prefer costly signals over cheap talk when assessing new ventures under static conditions. However, based on a cognitive perspective, we argue that the dynamic nature of market conditions alters VCs’ information processing. In cold markets, VCs prioritize signals, whereas, in hot markets, they emphasize less costly cues that resonate with prevailing optimism, often at the expense of signals. Supported by a conjoint experiment with 76 VCs, our results clarify the pivotal role of market conditions on the effectiveness of entrepreneurs’ signaling strategies.

Keywords

Introduction

For years, a deluge of cheap money kept valuations soaring, and venture [capital] firms said they spent less time on research and vetting the companies to court founders and not miss out on deals.

Entrepreneurs seeking early-stage funding often rely on signals to demonstrate the unobservable quality of their ventures (Ko & McKelvie, 2018). Ample research based on Spence’s (1973) signaling theory supports the effectiveness of signals—costly attributes or actions that low-quality ventures find difficult to imitate—as a persuasive mechanism for securing early-stage funding (Bafera & Kleinert, 2023). Emerging research, adopting a cheap talk perspective (Crawford & Sobel, 1982), also examines rhetorical cues—claims that low-quality ventures can easily fake—in new venture financing (O. Colombo, 2021). Despite the lack of a clear theoretical mechanism in cheap talk for establishing the credibility of information (e.g., Farrell & Rabin, 1996), prior research highlights its importance in influencing “less sophisticated” audiences (O. Colombo, 2021, p. 17), including crowdfunding investors who might struggle to differentiate between cheap talk and authentic signals (e.g., Anglin et al., 2018; Kleinert, 2024; Steigenberger & Wilhelm, 2018). However, the most abundant source of early-stage funding still originates from VCs, an audience known for its investment sophistication (e.g., Drover, Busenitz, et al., 2017). Whether cheap talk can also work for such sophisticated early-stage investors remains a pertinent question.

Research on cheap talk suggests that, given their sophistication, VCs should respond to signals but dismiss cheap talk as less credible (e.g., Anglin et al., 2018). However, integrating insights from cognitive science (e.g., Hallen & Pahnke, 2016; Vanacker et al., 2020), which explains how information processing by decision-makers can be constrained by cognitive limitations (Simons, 1991), provides a different perspective. These constraints can lead to selective attention, explaining why decision-makers rarely consider all available information when making decisions (Drover et al., 2018; McMullen et al., 2009; Ocasio, 1997). This cognitive perspective helps understand why less sophisticated crowdfunding investors might overlook signals (Butticè et al., 2022) or require rhetorical cues to enhance signal attention (Steigenberger & Wilhelm, 2018). Yet, cognitive limitations also affect sophisticated investors like VCs, who may exhibit overconfidence (Zacharakis & Shepherd, 2001) or rely on heuristics (e.g., Huang & Pearce, 2015), leading them to put minimal effort in judging message validity and “rely on (typically) more accessible information” (Chaiken, 1980, p. 752). This stands in contrast to the premise of signaling research, which generally assumes VCs will commit significant cognitive effort to notice and act upon any available signal (cf. Drover et al., 2018). Hence, these divergent views provide a theoretical conundrum that requires elaboration (Fisher & Aguinis, 2017): How do VCs discern and prioritize between signals and cheap talk in their decision-making processes?

We propose that VCs’ responses to signals and cheap talk depend on the prevailing market conditions—either hot or cold—that provide fundamentally different decision-making contexts (Lo et al., 2024). During periods of hot markets, characterized by an abundance of available funding for new ventures (Gompers et al., 2008), an exuberant climate fosters pronounced optimism within the startup ecosystem—often referred to as irrational exuberance (Shiller, 2015)—and intense competition among VCs for promising investments (Zhelyazkov & Tatarynowicz, 2021). As highlighted in the opening quote, during such periods, the primary concern for VCs is the fear of missing out on lucrative investments, which may lead to less thorough due diligence and a reliance on heuristic decision-making. These conditions can lead VCs to disregard signals (Drover et al., 2018), especially those related to past performance, which are less relevant to mitigating fear of missing out, in favor of salient cheap-talk cues that offer legitimizing insights in a heated market context, such as promises of substantial growth (Kleinert, 2024). In contrast, cold market phases render VCs more cautious, with a primary concern for avoiding low-quality ventures (Gulati & Higgins, 2003). Relying on extensive due diligence processes, VCs exert greater cognitive effort in the assessment of new ventures, thus prioritizing signals over cheap talk to discern high from low-quality ventures.

In this study, we develop a framework on the decision-making processes of VCs in hot and cold markets and test how market conditions moderate the effectiveness of signals and cheap talk. Given VCs’ primary objective of achieving high returns on investment, they tend to rely on financial metrics for the assessment of new ventures (Gompers et al., 2020); therefore, we examine the profitability of new ventures as a signal and growth promises as cheap talk. Achieving profitability represents a major milestone, which is difficult for low-quality ventures to imitate (Anglin et al., 2020). Promises of high growth mean that a venture claims strong revenue growth potential, which may indicate greater future return; however, it is easy to imitate (Kleinert, 2024). We expect that profitability signals will be more effective in cold markets, whereas growth promises as cheap talk will be more effective in hot markets.

To test our theory, we ran a conjoint experiment with 76 VCs. This real-time research method supports observations of decision makers as they actually make their decisions (Lohrke et al., 2010), and researchers frequently use it to study both VCs’ decision-making (Ademi et al., 2023; Shepherd & Zacharakis, 1999) and signaling effects in early-stage financing (e.g., Kleinert et al., 2022; Scheaf et al., 2018). Using a manipulation of new ventures’ attributes regarding profitability and projected growth, we test the effect of signal and cheap talk. To reliably test VC decision-making in hot and cold markets, and overcome confounding factors related to market dynamics (Cohn et al., 2015), we created between-subjects scenarios and randomly assigned VCs to assess new ventures in either hot or cold market scenarios.

This study in turn makes important contributions. First, we contribute to emerging new venture financing research on cheap talk (e.g., Anglin et al., 2018; Di Pietro et al., 2023; Kleinert, 2024; Steigenberger & Wilhelm, 2018) by clarifying its relevance for sophisticated early-stage investors. While previous research suggests that cheap talk matters for unsophisticated early-stage financiers (O. Colombo, 2021), we show that cheap talk can also be important for VCs, in particular in hot markets when uncertainties pertain to fears of missing out. In this sense, our study complements previous research that identifies receiver sophistication as a boundary condition for cheap talk (e.g., Anglin et al., 2018; O. Colombo, 2021), by highlighting that sophisticated early-stage investors also use less costly rhetorical cues for their investment decisions.

Second, by elaborating on cognitive perspectives within entrepreneurship signaling research (Bafera & Kleinert, 2023; Butticè et al., 2022; Drover et al., 2018; Kackovic & Wijnberg, 2022; Vanacker et al., 2020), we address controversies surrounding investors’ decision-making processes. Previous research suggests a dichotomy: investor decisions driven by cognitive shortcuts (e.g., Huang & Pearce, 2015; Steigenberger & Wilhelm, 2018) versus those arising from detailed analyses (e.g., M. G. Colombo et al., 2019; Hoenig & Henkel, 2015). Our study suggests that decision-makers like VCs alternate between these modes of information processing contingent upon the prevailing market conditions. Specifically, in cold markets, VCs conduct extensive due diligence and employ signals to resolve information asymmetries, whereas in hot markets, they are inclined toward heuristic-based decisions, which can lead to the overlooking of signals and increased reliance on cheap talk. Our study thus clarifies the pivotal role of market conditions for the effectiveness of entrepreneurs’ signaling strategies.

Theoretical Background

Venture Capitalists and Information Asymmetries

For new ventures seeking to accelerate their growth, venture capital is the go-to source of early-stage equity finance (Drover, Busenitz, et al., 2017). Yet only few new ventures ever raise venture capital because of the selective due diligence processes of VCs—experts within private equity firms that specialize in identifying and investing in high-potential new ventures (Pahnke et al., 2015). For example, Gompers et al. (2020) report that VCs screen approximately 100 investment opportunities before finalizing a single deal. This rigorous selectivity underscores VCs’ investment rationale, who consider only a small fraction of new ventures as relevant investment cases. This rationale is rooted in the understanding of VCs that a predominant portion of new ventures fail, with the majority of investments resulting in a total loss of the original investment amount. Hence, any single investment in a startup is expected to have the potential to generate returns sufficient to recoup the entire fund (Nanda et al., 2020). The structure of venture capital funds, which are typically organized as limited partnerships, further intensifies their selective nature. In this structure, VCs manage the funds and make investment decisions, while limited partners (LPs)—often institutional investors like pension funds, banks, and insurance companies—provide the capital (Hellmann & Puri, 2000). The performance of these funds critically depends on the VCs’ ability to garner substantial returns by investing in high-quality ventures. Hence, selecting high-quality ventures is directly related to the remuneration of VCs and whether LPs will continue to invest or divert their capital (Vanacker et al., 2020); however, this process is complicated by prevalent information asymmetry concerns.

Information asymmetries mean that entrepreneurs (agents) hold private information about their venture’s quality that VCs (principals) lack (Jensen & Meckling, 1976; Mishra et al., 1998). This imbalance creates a situation where self-interested entrepreneurs might overstate their value, making it hard for VCs to judge the venture’s true quality (Eisenhardt, 1989). These concerns can cause adverse selection and market inefficiencies as described in Akerlof (1970). To overcome these challenges, new ventures need to find ways to persuasively communicate their value to VCs.

Signaling Theory and the Cheap Talk Perspective

Signaling theory (Spence, 1973) serves as a foundational framework for addressing information asymmetries and has been extensively applied in management and entrepreneurship research (Bafera & Kleinert, 2023; Connelly et al., 2011). It explains how new ventures can credibly show their value through observable signals—costly actions or attributes—because high-quality ventures can afford these actions or attributes more easily than low-quality ventures. The nature of these costs varies from upfront investments of money, time, or effort, to penalties for dishonest signals, labeled as default-independent and default-contingent signals respectively (Kirmani & Rao, 2000). For example, the process of obtaining a patent is challenging for any new venture, but especially so for lower quality ones; hence, patents effectively function as a signal (Hoenig & Henkel, 2015). Signals thus correlate with a venture’s unobservable quality and lead to a separating equilibrium, where new ventures that send signals outperform those that do not (Bergh et al., 2014).

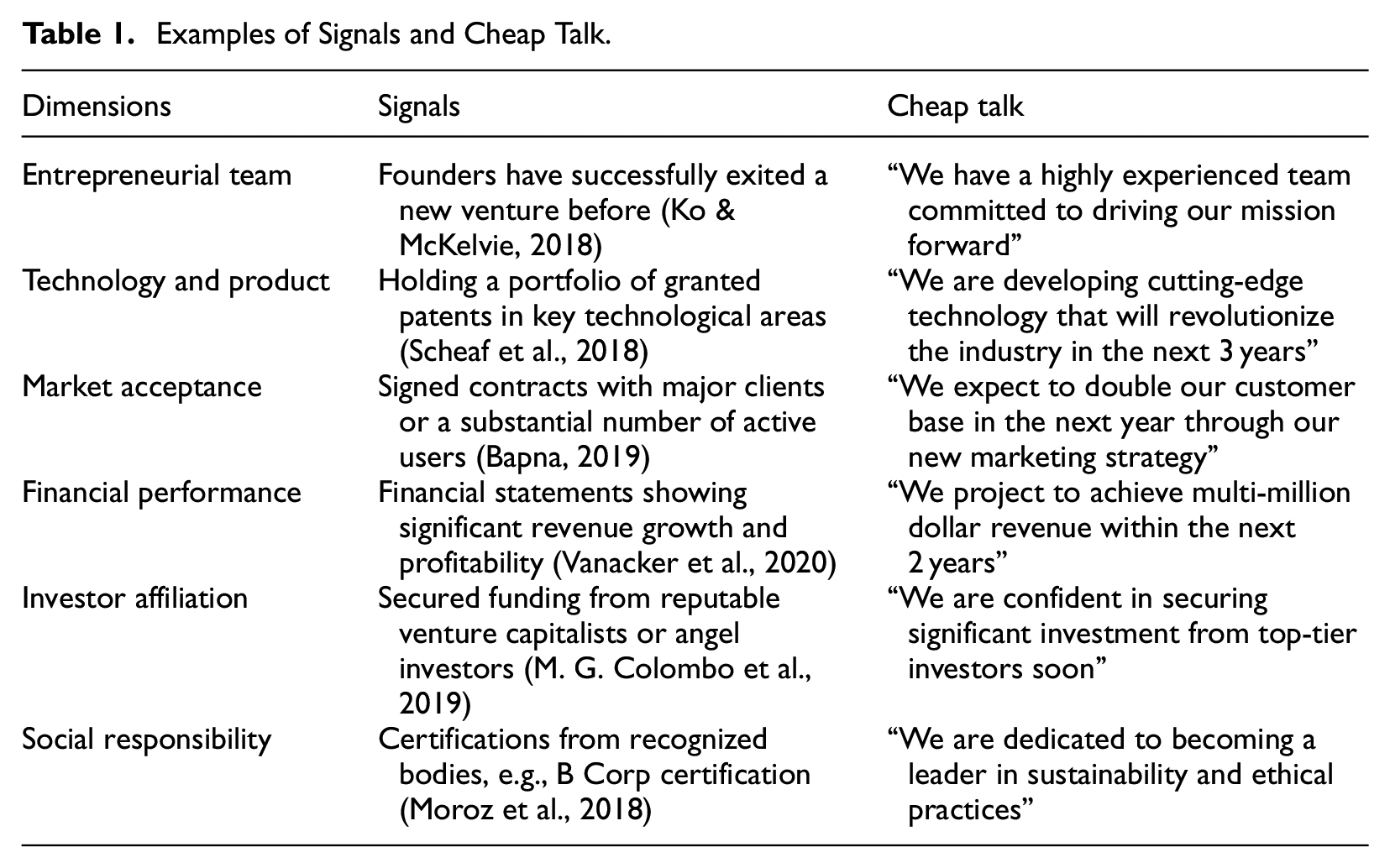

Although the literature robustly validates the role of signals in reducing information asymmetries in venture capital and new venture financing contexts (e.g., O. Colombo, 2021), the role of cheap talk—costless, unverified communication—is more controversial (Farrell & Rabin, 1996). Cheap talk has been introduced in economics as an alternative mechanism for strategic information transmission (Crawford & Sobel, 1982), recognizing that “most information sharing is not done through Spence-style signaling” and “talk is cheap, but given that people respond to it, talk definitely affects payoffs” (Farrell & Rabin, 1996, p. 104). For example, to inform about technological capabilities, new ventures might claim: “We are developing cutting-edge technology that will revolutionize the industry in the next 3 years.” Such cheap talk, though theoretically less effective in differentiating quality, has thus been highlighted as a less universally applicable but still persuasive means to convey information to decision-makers (e.g., Chakraborty & Harbaugh, 2010; Farrell & Rabin, 1996). 1 We provide additional examples that distinguish signals and cheap talk in Table 1. 2

Examples of Signals and Cheap Talk.

Growing entrepreneurship research examines how variations of cheap talk can complement signals in resource acquisition contexts and tends to confirm its relevance (O. Colombo, 2021). Prior research has primarily focused on cheap talk as rhetorical cues, such as psychological capital language (Anglin et al., 2018), virtue rhetoric (Payne et al., 2013), or claims about growth ambitions (Kleinert, 2024). Steigenberger and Wilhelm (2018) propose a useful distinction of such rhetoric based on Aristotle’s appeals of logos (logic), pathos (emotions), or ethos (credibility). They suggest that for instance logos appeals “convey information about a focal economic activity,” such as a new product to be developed, and thereby reduce activity-related information asymmetries for investors (Steigenberger & Wilhelm, 2018, p. 532). The effectiveness of such cheap talk remains less clear-cut than signals in new venture financing, and their persuasive power can be compromised if perceived as exaggerated (Kleinert, 2024). Yet research also shows that when paired with signals, cheap talk can help, adding information or drawing attention (Steigenberger & Wilhelm, 2018). However, our current understanding of the role of cheap talk in new venture financing is based on less savvy audiences like crowdfunding who lack the experience to deal with potentially easily manipulated cheap talk and do not conduct formal due diligence (Ahlers et al., 2015). As such, research emphasizes constraints of the receivers as a main reason and boundary condition for the relevance of cheap talk, and it remains unclear to what extent cheap talk also plays a role for VCs as sophisticated early-stage investors (O. Colombo, 2021). To understand why cheap talk should work at all and potentially also for VCs, a deeper exploration of decision-makers’ cognitive processes is necessary.

A Cognitive View on Information Processing

Emerging research combines a cognitive view with signaling theory to explain how decision-makers in early-stage financing attend to and interpret signals (e.g., Butticè et al., 2022; Steigenberger & Wilhelm, 2018; Vanacker et al., 2020). Cognitive research recognizes the subjectivity in how information is processed, highlighting that decision-makers’ cognitive capabilities are bound by limitations (Simons, 1991) and a limited attention span (Ocasio, 1997). Such limitations can lead to misinterpretation of information and selective attention, resulting in biases (Tversky & Kahneman, 1974; Zacharakis & Shepherd, 2001), or a focus on specific signals or cues to the exclusion of others (Drover et al., 2018). Dual processing theory from cognitive science provides a framework for understanding how these cognitive limitations affect decision-making (e.g., Chaiken, 1980). According to this theory, cognitive processes are divided into two categories—intuitive thinking and analytical thinking—between which individuals switch for information processing (Evans, 1984; Evans & Stanovich, 2013).

In the intuitive thinking mode, known as System 1, decision-makers “exert comparatively little effort in judging message validity” (Chaiken, 1980, p. 752) and decide based on heuristics and emotions (Epstein, 1994). System 1 is invoked by experience and operates automatically and quickly, relying on memory-based associative processes and readily available information cues. It is typically engaged under heavy cognitive loads or in familiar contexts, enabling rapid decision-making through heuristics or cognitive shortcuts (Tversky & Kahneman, 1974). Although System 1 can lead to accurate judgments, it is also highly susceptible to biases (Morewedge & Kahneman, 2010). In contrast, in the analytical thinking mode, known as System 2, decision-makers “exert considerable cognitive effort in performing [a] task” and “actively attempt to comprehend and evaluate the message’s […] validity” (Chaiken, 1980, p. 752). System 2 involves detailed and systematic processing of information. It is slow, effortful, and requires concentration and the conscious allocation of cognitive resources. System 2 is typically engaged when the stakes are high, and the decision-maker has the time and capacity to conduct a thorough analysis of options and consequences (Kahneman & Frederick, 2002).

In the context of venture capital and early-stage investments, one might expect a predominance of the analytical mode of System 2, given the substantial risks associated with startup investments. Yet, research shows that early-stage investors often resort to the quick, heuristic-based judgments characteristic of the intuitive mode of System 1 (e.g., Chan & Park, 2013; Huang & Pearce, 2015; Zacharakis & Shepherd, 2001). In this way, they can “preserve effort by relying on highly accessible information” (Hallen & Pahnke, 2016, p. 1538)—a tendency common in situations that demand great cognitive effort such as when evaluating new ventures and interpreting multiple signals (Drover et al., 2018). Such reliance is especially pronounced when decision-makers are overwhelmed with an abundance of information, such as in early-stage financing settings or crowdfunding where numerous companies emit signals simultaneously (Plummer et al., 2016; Steigenberger & Wilhelm, 2018). Accordingly, early-stage investors frequently employ the intuitive mode of System 1 processing, and although it can enable proficient decisions by experts (Huang & Pearce, 2015), this heuristic-driven approach risks missing crucial signals and yielding to biases.

Empirical studies confirm that these cognitive processes can lead investors to overlook important signals (Butticè et al., 2022)—unless they are counterbalanced by attention-boosting rhetoric (Steigenberger & Wilhelm, 2018)—or to prioritize promises of future performance that qualify as cheap talk (Vanacker et al., 2020). The cognitive perspective can thus explain why cheap talk might matter in early-stage financing, though prior research tends to view cognitive constraints either as a general feature of decision-making in specific settings like crowdfunding (e.g., Steigenberger & Wilhelm, 2018) or inherent to specific audiences like less experienced crowdfunding investors (Butticè et al., 2022). We advance this perspective with a dynamic model in which cognitive processes vary across different market conditions, such as in hot and cold venture capital markets and explain why even sophisticated early-stage investors such as VCs occasionally draw on cheap talk.

The Decision-Making of Venture Capitalists in Hot and Cold Markets

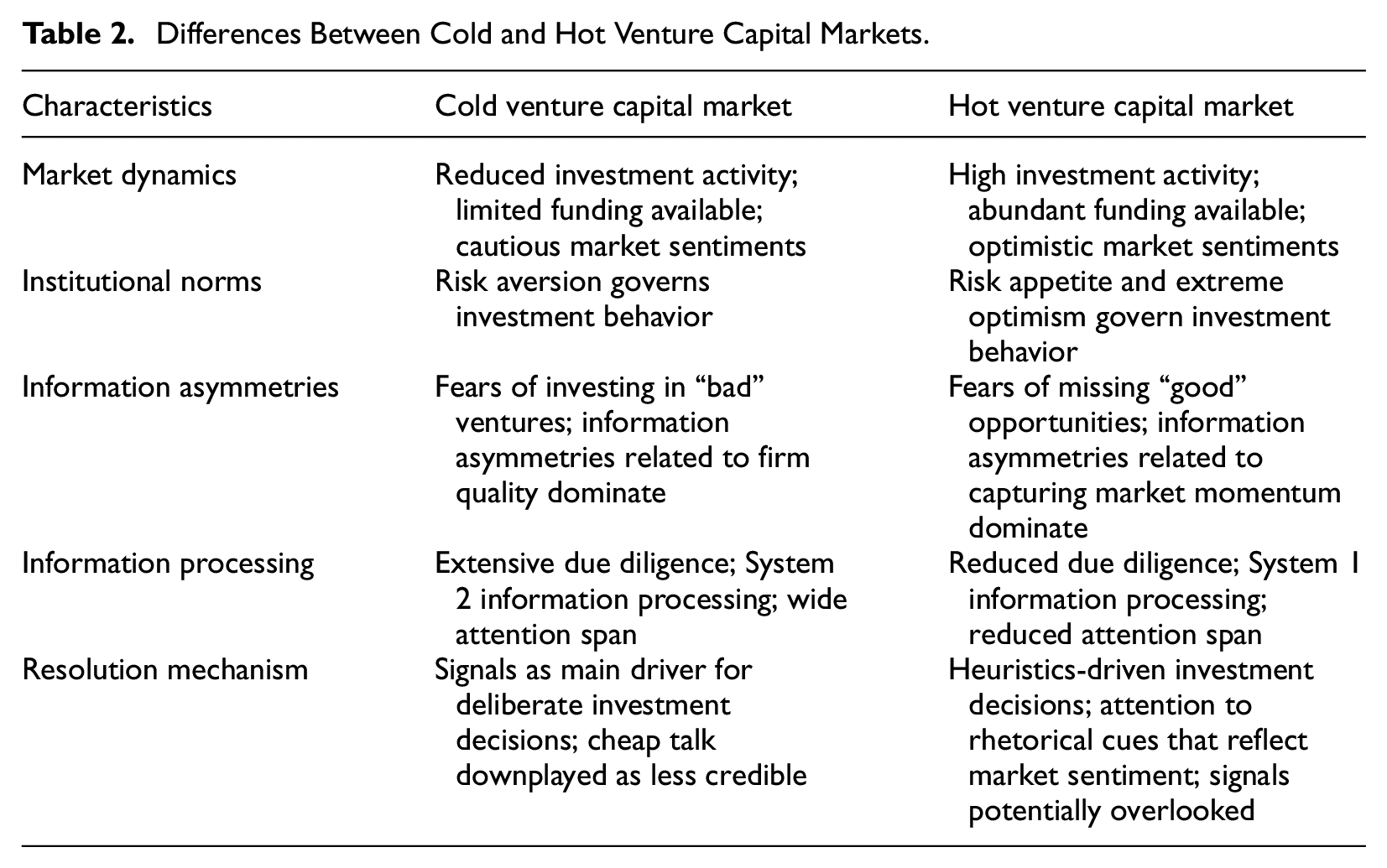

Financial markets go through cycles of hot and cold conditions (Ozmel et al., 2017), as suggested by prior research in the IPO context (e.g., Ibbotson & Jaffe, 1975; Ritter, 1984) and venture capital markets (e.g., Lo et al., 2024). We propose that these market conditions create fundamentally different decision-making contexts for VCs, influencing their behavioral norms, information processing, and, consequently, the effectiveness of signals versus alternative cues, such as cheap talk. Table 2 summarizes the main differences, which we discuss in the following.

Differences Between Cold and Hot Venture Capital Markets.

Cold venture capital markets—characterized by a reduced venture capital activity and limited funding for new ventures—may arise from market volatility and economic downturns (Gompers et al., 2008). These conditions typically shift investor sentiments toward caution, diminishing confidence in the startup ecosystem and making it challenging for VCs to raise capital for their funds. In such environments, new ventures might postpone fundraising to avoid the unfavorable investment terms common in cold private equity markets (Helwege & Liang, 2004). Cold market conditions have severe implications for the decision-making of VCs. First, VCs adopt a more risk-averse behavior in cold markets, given the heightened challenges associated with exiting investments and securing subsequent funding for their funds. This heightened caution is further reflected by LPs, who adjust their expectations accordingly, fostering a climate of risk aversion among VCs (Cohn et al., 2015; Zhelyazkov & Tatarynowicz, 2021). Hence, in cold markets, VCs employ a risk averse institutional logic—beliefs regarding the legitimacy of new ventures (Pahnke et al., 2015)—where VCs’ main concern is investing in “bad” new ventures (Gulati & Higgins, 2003). In turn, they perceive new ventures as legitimate that can credibly reduce such investment risks. Second, the scarcity of funds is causing VCs to pursue fewer, more carefully selected deals, while less favorable investment terms deter new ventures from seeking venture capital (Gompers et al., 2008). This scenario requires and enables VCs to conduct extensive and thorough due diligence on new ventures. Consequently, in cold markets, VCs are more likely to utilize analytical processing (System 2), affording the time and capacity for such in-depth analysis. Driven by a focus on risk mitigation, their main goal is filtering out low-quality ventures so that signals become pivotal in differentiating the quality of new ventures. Hence, VCs will actively look for such reliable indicators of a startup’s economic viability and because of the heightened attention span enabled by System 2 processing (Drover et al., 2018), VCs will readily notice signals. Therefore, signaling theory emerges as the key framework for resolving information asymmetries in cold markets.

In hot markets, characterized by high investment activities and abundant capital, the landscape shifts dramatically compared to cold markets. These conditions, fueled by strong economic growth, high-profile IPOs (Zhelyazkov & Tatarynowicz, 2021), or hype around specific industries (Jain et al., 2008), create an ideal backdrop for new ventures seeking capital. Such an environment may lead to irrational exuberance among investors—extreme optimism and enthusiasm about market success (Shiller, 2015)—known from heated stock and IPO markets (Ritter, 1984) where investors may even disregard the results of their own due diligence to follow prevailing market sentiments (Banerjee, 1992). Against this backdrop, VCs adopt a more risk-taking and optimistic institutional logic, aligning with the collective expectations of exceptional returns and quick exits among LPs and the VC community (Lo et al., 2024). This optimism propels VCs to find new ventures as legitimate that resonate with the heated market sentiment and capitalize on the prevailing momentum. At the same time, “too much money will chase too few deals” (Gulati & Higgins, 2003, p. 130), leading to intense competition among VCs for promising investments and sparking a fear of missing out (Zhelyazkov & Tatarynowicz, 2021). To accelerate decision-making speed, VCs may abandon the rigorous due diligence characteristic of cooler markets and instead, shift toward the heuristic-driven decision-making associated with System 1 processing. This approach allows VCs to effectively evaluate the large number of new ventures seeking funding in hot markets, though at the cost of reduced and more selective attention (Drover et al., 2018). Guided by extreme optimism and fear of missing out, VCs’ main goal is to identify ventures that promise significant returns amidst the favorable market conditions (Zhelyazkov & Tatarynowicz, 2021). In this context, conventional signals—often reflective of past achievements (Di Pietro et al., 2023)—lose their edge in distinguishing ventures that may or may not thrive on the prevailing market optimism. Consequently, VCs will not actively seek out these signals, and instead focus on cues that align with the current market excitement, even if such cues are based on less reliable information sources like cheap talk. Hence, we anticipate a diminished role for signaling theory in addressing information asymmetries in hot markets, with VCs more likely to rely on salient cues indicative of current market optimism as their key decision-making anchor.

Hypotheses

Our theorizing provides a concrete framework that we use to develop hypotheses about VCs’ responses to signals and cheap talk in hot and cold markets. To this end, we focus on the profitability of new ventures as signal, and their growth promises as cheap talk, for two reasons. First, VCs tend to embrace a quantitative focus, and their primary goal is to achieve a high return on investment (Amit et al., 1998)—financial performance in particular is a key quality dimension considered in such settings (Vanacker et al., 2020). Accordingly, profitability and growth are often considered central financial metrics by VCs (e.g., Collewaert et al., 2021; Puri & Zarutskie, 2012; Shepherd et al., 2000). Second, both are potentially relevant in different market conditions. Profitability is a more conservative measure—reflecting a past achievement (Block et al., 2019)—and could therefore be a suitable signal for the cautious sentiment in cold markets, whereas promises of high growth—reflecting future growth potential (Kleinert, 2024)—match the optimistic sentiment in hot markets.

Profitability as Signal in Hot Versus Cold Venture Capital Markets

New ventures that have achieved profitability signal their financial sustainability (Anglin et al., 2020; Shepherd et al., 2000). It is a difficult and resource-intensive process that requires a solid business model, effective management, and a competitive advantage (Jain et al., 2008). Low-quality ventures cannot easily imitate this critical milestone. Being profitable thus clearly distinguishes between high- and low-quality ventures and constitutes a signal that is relevant for reducing VCs’ uncertainties about the economic quality of a new venture. 3 We expect profitability to be effective in cold markets but less so in hot markets.

First, signals about economic firm quality like profitability are more relevant for reducing information asymmetries in cold markets, where fears of investing in bad ventures dominate (Gulati & Higgins, 2003). If a new venture is profitable, VCs perceive that it has already achieved one of the central milestones in its life cycle—which many new ventures never achieve (Jain et al., 2008). Profitability thus constitutes an effective proxy of a new venture’s success, which increases the likelihood of survival in the long run (Delmar et al., 2013) and considerably reduces VCs’ investment risk (Block et al., 2019; De Rassenfosse & Fischer, 2016). Consistent with their risk-aversion in cold markets, VCs will therefore view profitable new ventures as legitimate and lower risk investment opportunities. Profitability may be less relevant for reducing information asymmetries in hot markets when uncertainty shifts the focus from concerns about investing in low-quality ventures to fears of missing out on promising opportunities (Gulati & Higgins, 2003). In particular, profitability does not provide any meaningful insight into whether new ventures can actually exploit the market momentum and turn into an outstanding and successful exit (e.g., acquisition, IPO), which VCs strive for in hot markets, but which also depend on sustained growth (Jain et al., 2008). Hence, although profitability aligns with the risk aversion of VCs in cold markets, it does not align with the irrational exuberance sentiment of VCs in hot markets.

At the same time, relevance is not enough to effectively resolve information asymmetries—a signal must also be noticed (Butticè et al., 2022; Drover et al., 2018). This is less of a problem in the cold market phase, where VCs conduct extensive due diligence and their detailed analyses of potential investments lead to a high attention span—relevant information is unlikely to be missed under these conditions. Conversely, in hot markets, the urgency among VCs to close a deal quickly—before they miss the opportunity—leads to reduced due diligence, such that VCs might not thoroughly evaluate the risks and potential pitfalls associated with their investments. Accordingly, hot markets considerably disrupt VCs’ attention spans (Zhelyazkov & Tatarynowicz, 2021), rendering them more susceptible to overlooking signals that convey the profitability of a new venture, which might not be the most relevant performance benchmark during these periods (Jain et al., 2008). For example, research on emerging internet companies in the 2000s suggests that investors by and large ignored credible performance benchmarks when assessing newly public companies in hot IPO markets (Mudambi & Treichel, 2005). When they adopt heuristics, investors tend to attend only to the information for which they actively look (Drover et al., 2018), and in hot markets, when VCs seek cues that align with the prevailing gold rush sentiment, they are likely to overlook profitability signals, which reflect a more conservative financial outlook. We therefore hypothesize:

Growth Promises as Cheap Talk in Hot Versus Cold Venture Capital Markets

When new ventures promise high revenue growth, it might suggest an investment opportunity with high return potential to VCs. Promises of high growth thereby represent a logos appeal (Steigenberger & Wilhelm, 2018), suggesting that the venture will undertake relevant activities to secure future growth. However, because any new venture can do so, promises of high growth do not distinguish between high- and low-quality ventures and reflect cheap talk (Kleinert, 2024). We expect that high projected growth will still be relevant for the decision-making of VCs in hot markets, but less so in cold markets.

High-growth projections address the main uncertainty of risk-seeking VCs in hot markets—whether new ventures can exploit the current market momentum and potentially turn into a quick exit. For VCs, a singular successful investment can offset numerous unsuccessful ventures (Nanda et al., 2020), positioning a high-growth venture to potentially dominate the market. As Sorenson and Stuart (2008, p. 271) note, in hot markets, “unsure precisely how to evaluate them, VC firms nonetheless rush into them with the hope of seizing time-sensitive opportunities for supra-normal profits.” This eagerness to capitalize on unique prospects makes VCs more receptive to claims of high-growth potential, despite their less credible nature. Additionally, the phenomenon of irrational exuberance in hot markets may lead VCs to overrate the success prospects of new ventures (Goldfarb et al., 2007; Nofsinger, 2005). Thus, VCs may display overconfidence (Lo et al., 2024) so that they do not question exaggerated promises of high growth from new ventures (cf. Kleinert, 2024). For example, driven by optimism (Sorenson & Stuart, 2008), VCs might assume that growth will be easier to achieve as new ventures leverage hot market dynamics to attract essential resources for their expansion. Moreover, with their investment horizons in mind, VCs seek timely returns (Bacon-Gerasymenko et al., 2020), and in hot markets, new ventures with significant growth have enhanced prospects for lucrative exits such as acquisitions or IPOs (Jain et al., 2008). Thus, in a hot market, new ventures that promise high growth appear highly legitimate to VCs.

While VCs may worry about missing out on good investment opportunities (Zhelyazkov & Tatarynowicz, 2021), the growth potential is a salient indicator that the opportunity is relevant under current market conditions. Accordingly, even with a limited attention span in hot markets, high-growth promises are likely to command special attention. For example, in the hot market of the internet boom, post-IPO investors followed the “growth at any cost” mantra, in which investors overemphasized signs of growth over any other performance benchmark (Jain et al., 2008). Thus, in their heuristically driven decisions in hot markets, VCs may actively search for cues about growth potential, which increases their attention to appeals consistent with this search for growth (Drover et al., 2018). The combination of little due diligence and a high tolerance for risk reduces VCs’ tendency to question the credibility of cheap talk. As a result, in hot markets, the salience may matter more than the credibility of information. High-growth promises emerge as a salient cue that can help VCs filter through the clutter and identify new ventures that are consistent with the current optimistic market sentiment (Sorenson & Stuart, 2008). That is, promises of high growth likely become a convenient cognitive anchor in VCs’ heuristics in hot markets.

In cold markets, on the other hand, as a result of their extensive due diligence, VCs also notice the growth promises of new ventures but can readily differentiate cheap talk from credible signals. Given the increased difficulty for new ventures to secure funding in cold markets (Gulati & Higgins, 2003), VCs may be particularly skeptical of dishonest and exaggerated growth projections. Therefore, in cold markets, they should be more likely to perceive growth claims as less credible and be less willing to overemphasize such claims as a relevant factor in their decisions. We thus hypothesize:

Methodology

Metric Conjoint Experiment with Between-Subjects Variation

To test our hypotheses, we combine a metric conjoint experiment with a between-subjects design. The metric conjoint experiment allows us to observe the influence of signals and cheap talk on VCs’ decision-making, and the between-subjects design allows us to effectively test VCs’ decision-making in either a hot or cold market environment.

Metric conjoint experiments constitute a decomposition-based research method to analyze decision-making (Green & Srinivasan, 1990; Shepherd & Zacharakis, 1999). Participants assess hypothetical profiles consisting of a set of theoretically grounded attributes (Lohrke et al., 2010). In new venture financing research, these attributes often relate to new venture characteristics, such as signals, which can be varied between high and low levels (Kleinert et al., 2022; Scheaf et al., 2018). Using participants’ assessments of these profiles, conjoint analysis allows researchers to deconstruct the importance of different attributes in the decision-making process.

Conjoint analysis is one of the most commonly used methods to analyze VCs’ decision-making (see Petty et al., 2023 for an overview) and is appropriate for our study for several reasons. First, VCs’ screening decisions are inherently difficult to observe because of the sensitivity of the diligence process and because public data typically do not contain the detailed information new ventures use in their persuasion process (cf. Petty et al., 2023). Historically, research on VCs’ decision-making has therefore relied on surveys and interviews, but conjoint analysis has emerged as a more widely used method since the early 2000s (Petty & Gruber, 2011) and continues to maintain its relevance (e.g., Drover, Wood, & Zacharakis, 2017; Hoenig & Henkel, 2015; Warnick et al., 2018). Its advantage over other methods is that conjoint experiments use real-time data, thus circumventing many of the limitations associated with post hoc research methods (Lohrke et al., 2010; Petty & Gruber, 2011). For example, questionnaire or interview data can be highly susceptible to retrospective or recall bias and hinder accurate interpretations of causal factors (Shepherd & Zacharakis, 1999). Specifically in our context, VCs may downplay the role of market cycles when asked directly in a survey (Gompers et al., 2020). Previous research also highlights the external validity of conjoint experiments by establishing that they can effectively replicate decision environments and that estimated decision behavior is significantly correlated with actual observed behavior (Shepherd & Zacharakis, 2018). Therefore, metric conjoint experiments are well-suited to derive insights into underlying decision processes; they also have proven highly relevant for studying complex decisions in various entrepreneurial contexts (Lohrke et al., 2010), especially early-stage financing (Drover, Wood, & Zacharakis, 2017; Murnieks et al., 2011). For example, conjoint experiments have been instrumental in investigating how early-stage investors evaluate investment opportunities (Ademi et al., 2023), assess entrepreneurs’ characteristics and attitudes (Warnick et al., 2018), and interpret new ventures’ quality signals (Scheaf et al., 2018). In turn, a metric conjoint experiment is appropriate to investigate the impact of signals and cheap talk on VCs’ decision-making.

To explore the moderating effect of different market conditions, we integrated a between-subjects design into the conjoint experiment, in which we randomly assigned VCs to evaluate ventures in either a hot or cold market. Incorporating a between-subjects design into the conjoint experiment provides methodological advantages (Hsu et al., 2017) that help shed light on the complex interplay between external market factors and investment evaluations. First, capturing market dynamics is inherently challenging because many other factors intertwine with financial cycles (Cohn et al., 2015). By integrating a between-subjects design, our study systematically isolates the effects of market conditions (hot or cold) on VCs’ responses to signals. Second, randomly assigning VCs to different market conditions creates an experimental setting that reflects real-world variation in venture capital sentiment. Within-subject designs are useful to account for VCs’ holistic evaluations of new ventures that include multiple criteria simultaneously (Block et al., 2019), but market conditions remain constant over a certain time frame. Integrating a between-subjects design avoids the potentially confounding carryover or order effects that are prevalent in within-subject scenarios such as conjoint experiments (Hsu et al., 2017). Thus, our design avoids exposure to both market environments, minimizing the risk that prior exposure will bias or influence responses, and ensures a more unbiased assessment of how each market environment independently influences decision-making.

Experimental Setup

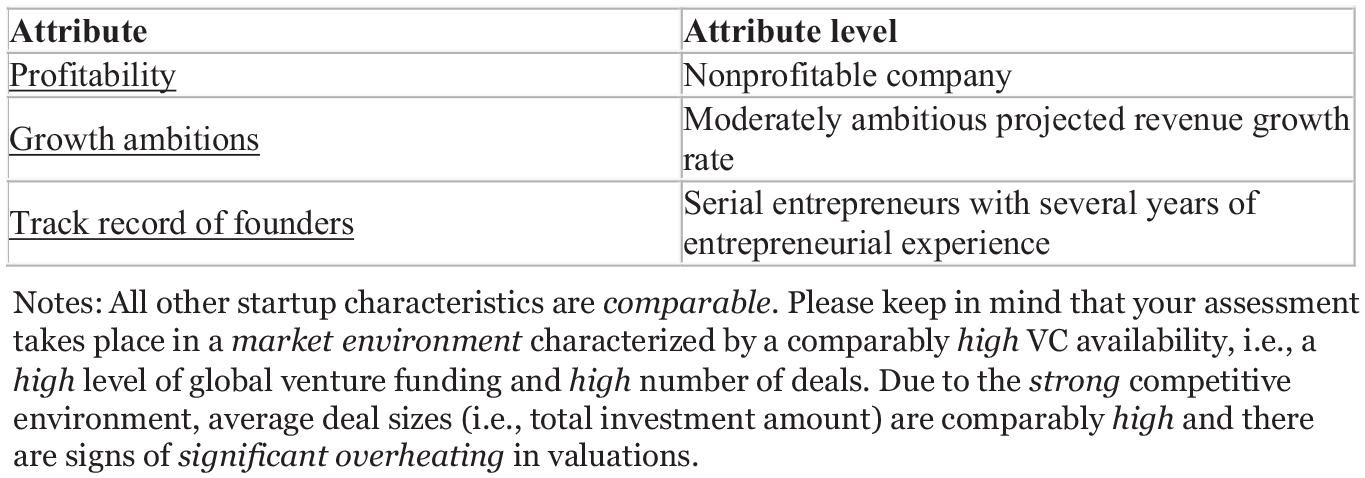

We distributed the conjoint experiment to VCs through a survey that consisted of detailed instructions, the conjoint task, and a post hoc questionnaire. In a first step, VCs read the instructions, in which we explained to participants that the task was to evaluate a set of startups as potential investment opportunities, which differ only with regard to the indicated attributes. Because it is important to specify the context in which judgments are being made (Shepherd & Zacharakis, 1999) and to ensure that participants think about the same ventures when evaluating investment opportunities, we presented respondents with a reference scenario that defined a common set of characteristics (Figure 1). As in previous research (Kleinert et al., 2022), we clarified that the new venture would match the VC’s general preferences and defined prototypical characteristics of an early-stage new venture. For instance, we highlighted that the new ventures were from the tech industry and had multiple paying customers. We further showed VCs definitions of the attributes used in the conjoint experiment.

Reference scenario.

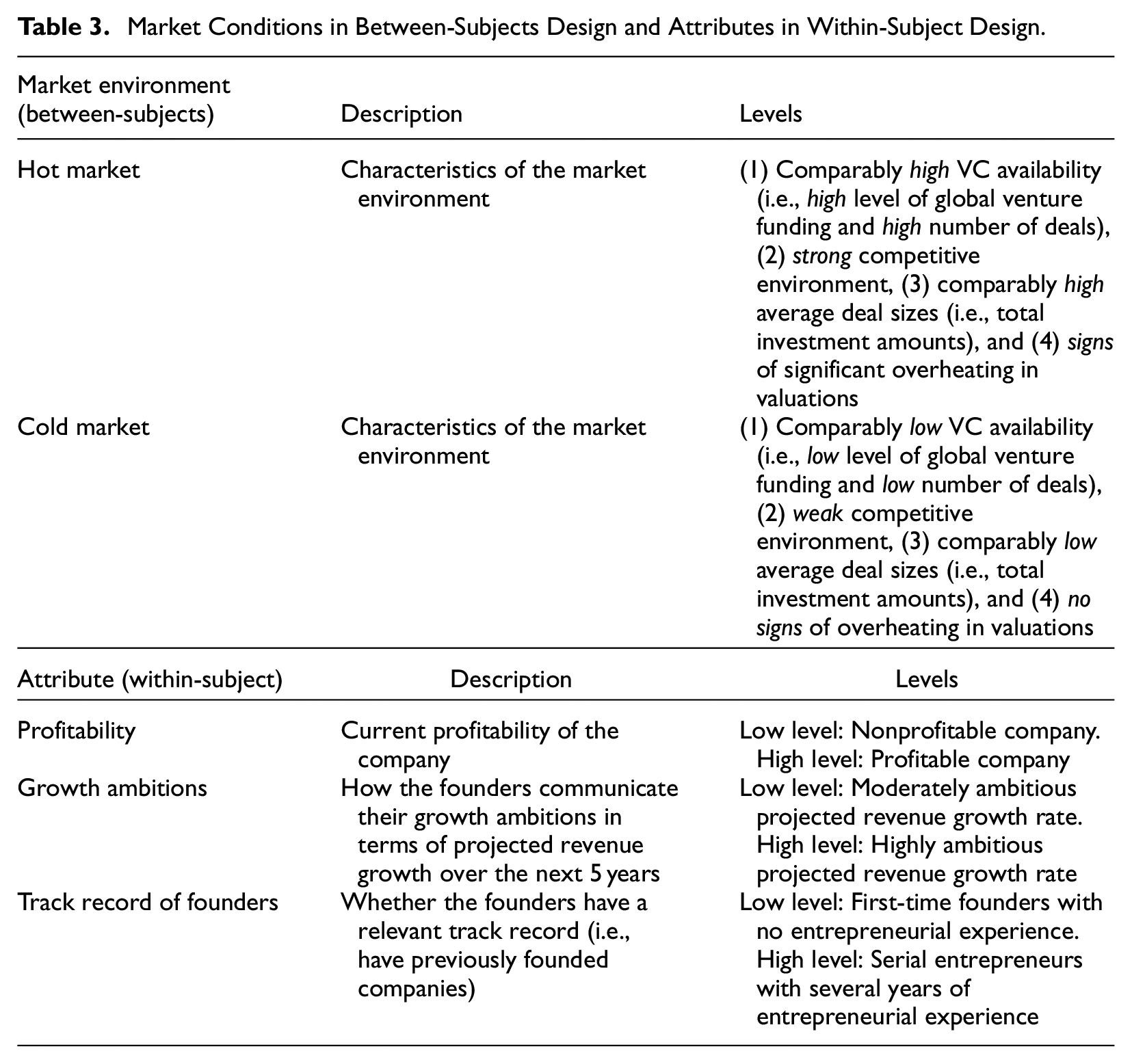

We randomly assigned respondents to different market conditions, so participants learned in the instructions that they were to evaluate the new ventures in either a hot or a cold market phase. In the hot market condition, participants read that market conditions were characterized by a high level of venture capital availability, a high level of global venture capital funding, a high number of deals, a strong competitive environment, a high number of average deals, and signs of overheated valuations. In the cold market condition, they read a description of a contrasting market phase. The market phase definitions are based on previous research on hot and cold markets (Gulati & Higgins, 2003; Zhelyazkov & Tatarynowicz, 2021) and, like the manipulated attributes in our conjoint analysis, were agreed on in preliminary interviews with five VCs. Table 3 contains the exact definitions of the market phases, as presented to respondents and the descriptions of the attributes as shown to VCs. After familiarizing themselves with the instructions and the task, participants indicated whether they understood the task and agreed to participate, which all confirmed.

Market Conditions in Between-Subjects Design and Attributes in Within-Subject Design.

In the next step, participants continued with the conjoint experiment, in which they evaluated eight profiles of new venture as investment opportunities. To ensure that they considered the respective environment during the evaluation, we included in each profile a note that new ventures were seeking funding in the respective market condition. Except for the indication that it was a hot or cold market phase, all VCs assessed the same set of attributes and profiles. We manipulated three attributes related to the new venture: profitability, growth ambition, and founder track record. We measured each of these attributes on two levels, yielding a total of eight (23) profiles, that is, each of the eight profiles has a unique combination of the three attributes. This well-established orthogonal full-factorial design ensures zero correlation among the attributes (Drover, Wood, & Zacharakis, 2017; Murnieks et al., 2011). The design is also consistent with the maximum number of attributes and decision tasks recommended to avoid respondent fatigue (Shepherd & Zacharakis, 1999). The attributes of profitability and growth ambitions allow us to test our hypotheses, and we included the founder’s track record as an additional attribute. It is one of the most important criteria for VCs’ decisions (Gompers et al., 2020; MacMillan et al., 1985) and supports a meaningful trade-off within the experiment. The attribute formulations are consistent with previous research on profitability (Block et al., 2019; De Rassenfosse & Fischer, 2016), growth ambitions (Kleinert, 2024), and founder track record (Ko & McKelvie, 2018). Table 3 lists the attribute definitions by level. Figure 2 illustrates an exemplary profile for an assessment taking place in hot markets, with notes about the corresponding market condition. Apart from the notes, the experiment (including the presented profiles and the questions) was identical for both conditions.

Example profile for hot market condition.

We used several measures to increase the validity of our experimental setup (Anderson et al., 2019). First, to increase the external validity of our conjoint experiment (Warnick et al., 2018), we conducted interviews with five VCs who provided insights about how to label and construct the market conditions and attributes, as well as feedback on the instructions and the clarity of the setup. Using their feedback, we ensured that the descriptions were realistic and the information relevant for VCs—all five VCs affirmed relevance and clarity. Second, to minimize the risk of respondents attaching importance to the attributes merely because they were presented with a decision scenario, we ensured that the decision attributes were well-grounded in theory (Lohrke et al., 2010). Specifically, we grounded our three attributes in signaling theory and aligned them with prior conjoint experiments studying similar attributes (Block et al., 2019; De Rassenfosse & Fischer, 2016; Kleinert, 2024). Third, a frequent concern in within-subject designs involves order effects; the sequence in which conditions are presented to participants might influence their assessments (Hsu et al., 2017). To mitigate this risk, we fully randomized the order of the presented profiles within the experiment.

Sample and Data Collection

Between May 2022 and March 2023, 4 we invited early-stage VCs to participate in our study. As in previous research, we considered VCs only as those who worked at institutional venture capital funds—thus, angel investors or other types of private equity funds were not included (see Gompers et al., 2020 for a similar approach). We focused on VCs in the DACHNL countries (Germany, Austria, Switzerland, and the Netherlands), where the authors’ networks facilitated data accessibility. Given the heterogeneity of VCs’ investment practices across countries (Bertoni et al., 2015; Manigart et al., 2002), we decided not to approach VCs from other regions, such as the United States. For example, different governance structures and a dominant role of banks as LPs in the venture capital funds result in a different institutional environment for VCs in countries such as Germany compared to the United States (Becker & Hellmann, 2005). Return expectations, and hence investment behavior, also differ between countries such as the Netherlands and the United States (Manigart et al., 2002). In addition, venture capital funds in Europe tend to be smaller than in the United States, and the average funding per round remains significantly lower in Europe (Crunchbase, 2022; Gompers et al., 2020). Accordingly, we focus only on VCs in the DACHNL region.

To identify decision-makers, we searched for venture capital firms in the respective countries using, for example, Crunchbase, lists of officially registered venture capital firms, and venture capital associations. We then screened potential respondents directly through company websites and the professional social network LinkedIn and focused on roles that are typically involved in investment decisions such as investment analysts, investment associates, and investment managers (Gompers et al., 2020). Before VCs could participate, we explained the aim and specified the target group for the survey to ensure that the potential participant actively engaged in investment decisions. Of the about 200 VCs contacted, 76 participants completed the entire survey (response rate of around 38%), resulting in 608 decisions.

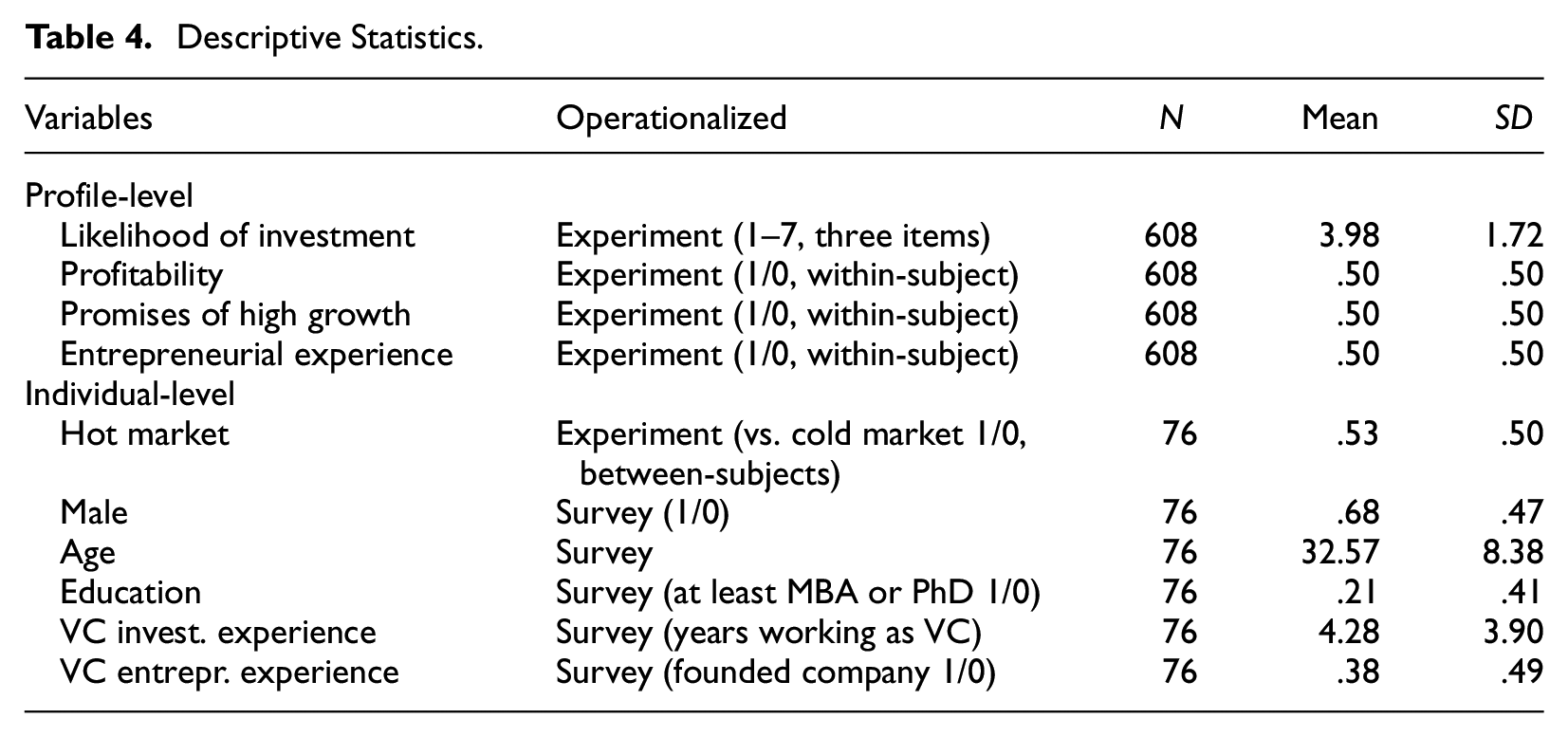

Our sample size is comparable to other conjoint studies in new venture financing settings for example, 54 (corporate) VCs (Ademi et al., 2023), 62 venture investors (Warnick et al., 2018), 53 business angels (Murnieks et al., 2016), 62 crowdfunding investors (Scheaf et al., 2018), 53 and 51 VCs (Drover, Wood, & Zacharakis, 2017), and 84 angel investors/VCs (Svetek, 2023). Our sample size of 76 VCs also exceeds sample requirements for the integrated between-subjects design (Hsu et al., 2017) that we used to test the moderating effect of hot and cold market environments. In line with previous studies (Block et al., 2019), we ran the experiment as an anonymous survey due to the sensitivity of the data collected about investment behavior. On average, VCs in our sample were 32.57 years of age; 68% were men; and 38% had founded a company before.

Variables

Dependent Variable

Following Murnieks et al. (2011) and Warnick et al. (2018), we used VCs’ likelihood of investment as our dependent variable, measured with three items on scales from 1 (low) to 7 (high). After reading each profile, respondents answered the following three questions: (1) “What is the probability that you would invest in this startup?” (2) “If you were to invest in this startup, what is the likely amount you would invest?” and (3) “Whether you invest or not, how successful do you think this opportunity will be?” The three-item scale showed strong internal consistency (Cronbach’s alpha = .95). We thus use the mean as our dependent variable.

Independent Variables

In line with our conjoint experiment, we denoted the dummy variables profitability as 1 if the new venture is profitable and 0 otherwise. To ensure that VCs perceive profitability as a signal in line with our theory, participants were provided with the definition of the attribute: “Current profitability of the company.” This frames the information as an objective state of the company.

We defined the dummy variable promises of high growth as 1 if new ventures project highly ambitious growth rates and 0 if they project moderately ambitious growth rates. To ensure that VCs perceive this as cheap talk, participants were provided with the definition of the attribute: “How the founders communicate their growth ambitions in terms of projected revenue growth over the next 5 years.” The use of terms like “communicate,” “projected,” and “over the next 5 years” ensures that these are understood as mere claims.

Using the between-subjects conditions, we defined the dummy variable hot market as 1 if VCs evaluated new ventures in the hot market condition and 0 if VCs evaluated new ventures in the cold market condition.

Control Variables

We included several relevant control variables in our analysis. As a relevant benchmarking variable based on our conjoint experiment, we created a dummy variable for entrepreneurial experience, denoted as 1 if entrepreneurs had a high level of founding experience and 0 otherwise. Consistent with prior research (Drover, Wood, & Zacharakis, 2017; Murnieks et al., 2011) and based on the post-experimental survey, we included several control variables regarding the VCs’ characteristics: the respondent’s gender, with male as 1 and female as 0; age of the respondent in years; education as 1 if VCs hold a PhD or an MBA; VC investment experience in years; and VC entrepreneurial experience (1 = previously founded a company, 0 = had not previously founded a company). Table 4 presents operationalizations and descriptive statistics for all our variables.

Descriptive Statistics.

Results

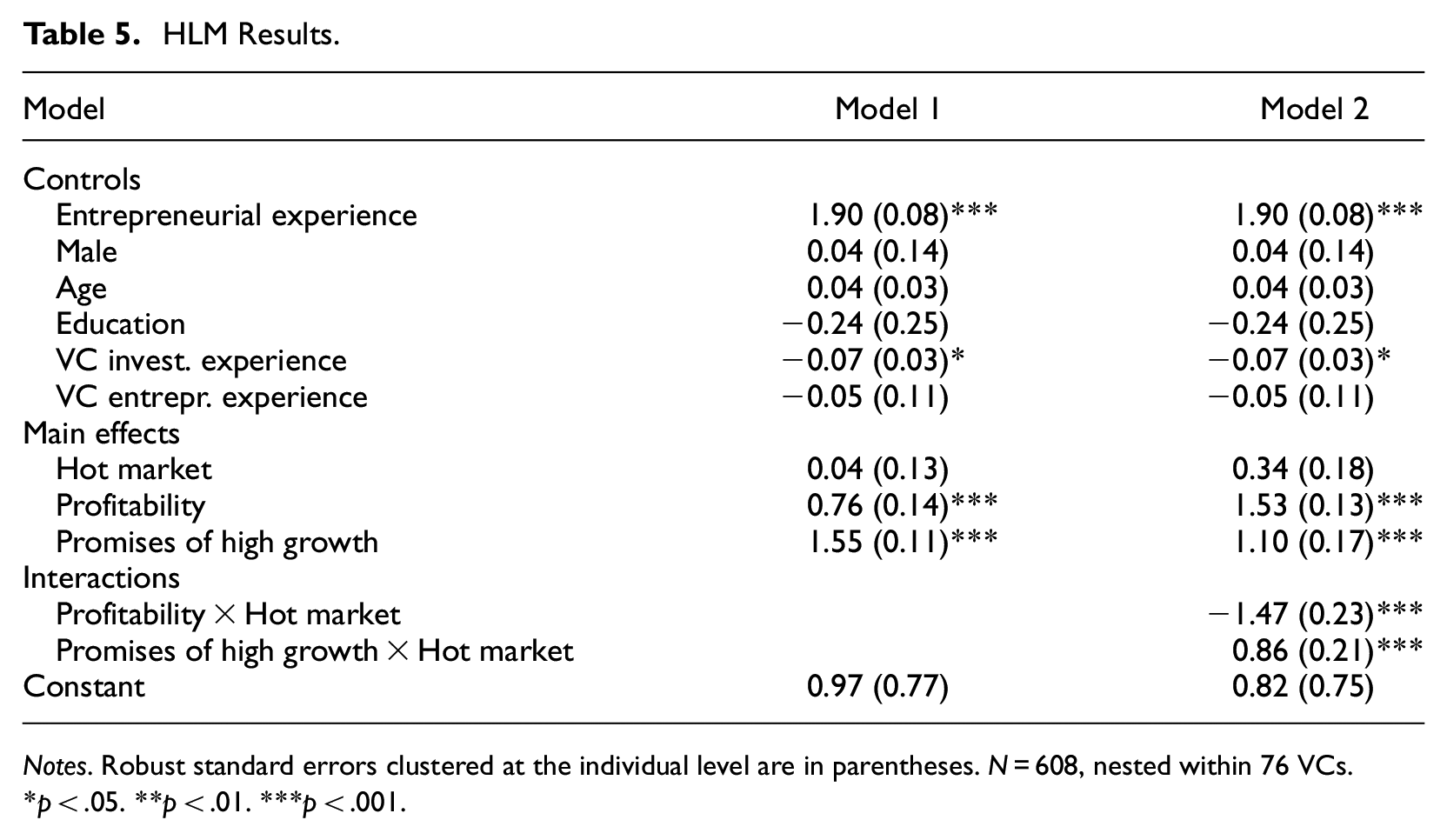

Because 76 VCs made 608 decisions, the data from our conjoint experiment are multilevel. We used hierarchical linear modeling (HLM) to account for possible autocorrelation between decisions of individual VCs (Lohrke et al., 2010). Because of their effectiveness with nested data, HLM analyses have become a standard approach in conjoint studies (Ademi et al., 2023; Kleinert et al., 2022; Murnieks et al., 2016). The orthogonal design means no correlations between attributes are present, and correlations are only possible between variables at the individual level. All the variance inflation factors were below 3.0, so individual-level multicollinearity is not a concern for our analysis.

We report our HLM results in Table 5, in which Model 1 presents the main effects and Model 2 adds the moderating effect of hot markets. Before we test our hypotheses, we consider the main effects of the independent and control variables. We find that profitability has a positive and significant effect (β = .76, p = .000) and promises of high growth too (β = 1.55, p = .000). Using the results in Model 1 to calculate the average marginal effects, we find that profitability increases the likelihood of investment from 3.60 to 4.36 (by 21.11%), whereas promises of high growth increases it from 3.21 to 4.76 (by 48.29%). Although both are relevant to VCs, the effect of promises of high growth is considerably stronger than the effect of profitability. However, the results in Model 1 also suggest that entrepreneurial experience has a stronger effect (β = 1.9, p = .000) than both profitability and promises of high growth—an unsurprising result, considering that the team is often regarded as the most important success criterion by VCs (Gompers et al., 2020).

HLM Results.

Notes. Robust standard errors clustered at the individual level are in parentheses. N = 608, nested within 76 VCs.

*p < .05. **p < .01. ***p < .001.

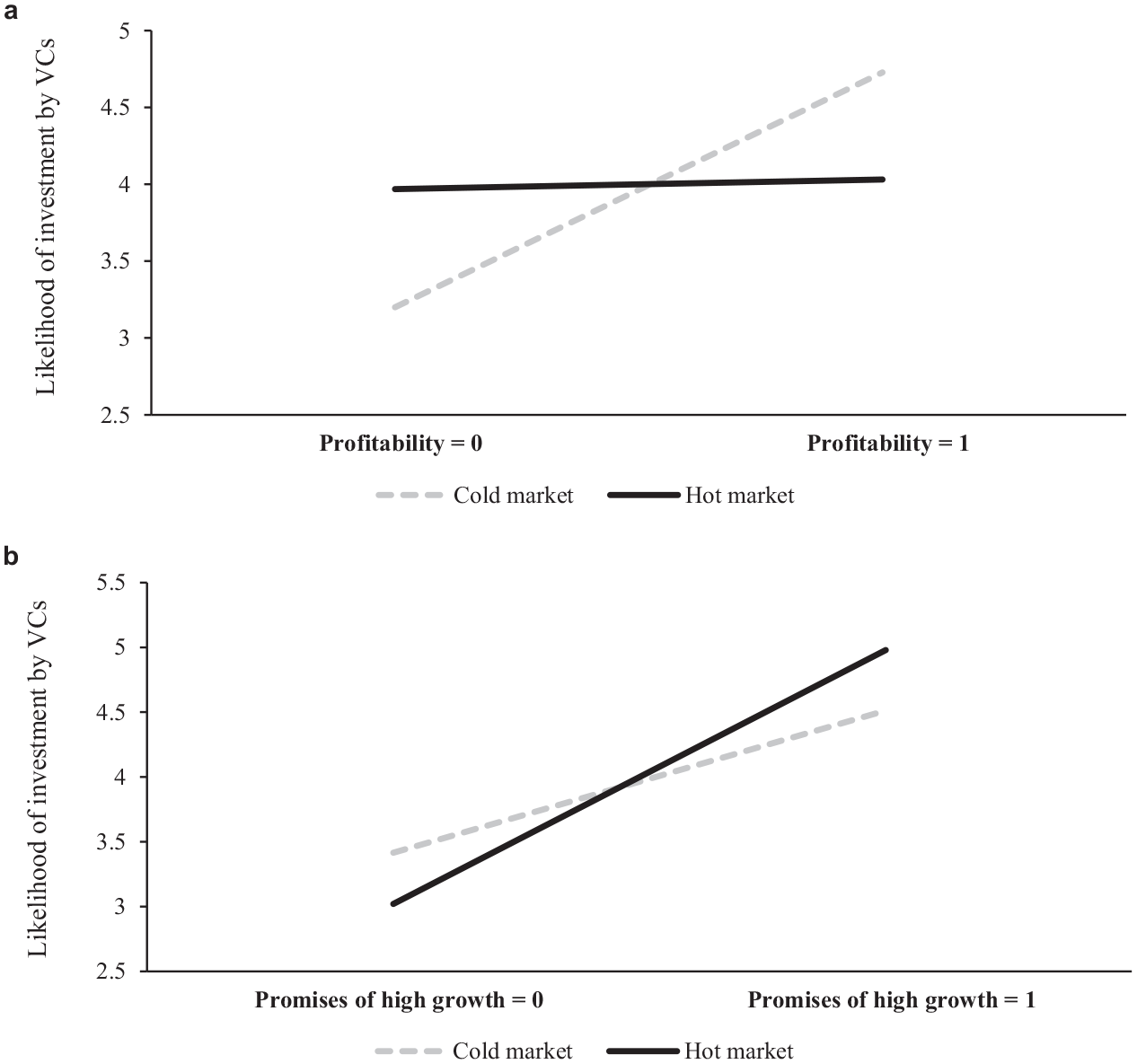

We turn to our hypotheses on the moderating effects of hot markets versus cold markets for signals and cheap talk, as indicated by Model 2. To gauge the effect sizes, we calculated the average marginal effects based on the estimates in Model 2 (for visualizations of the interactions, see Figure 3a and b). In Hypothesis 1, we argue that the effect of profitability is weaker in hot than in cold market environments. The significant and negative coefficient between profitability and hot market provides support for this hypothesis (β = −1.47, p = .000), and Figure 3a demonstrates the magnitude of the effect. Profitability is powerful in cold markets, in which it increases VCs’ likelihood of investment by 47.75%; however, in hot markets, the effect diminishes to only 1.58%.

(a) Marginal effects for interaction between profitability × hot market and (b) marginal effects for interaction between promises of high growth × hot market.

In Hypothesis 2, we argue that promises of high growth has a stronger effect in hot versus cold markets, and our results provide support (β = .86, p = .000). Figure 3b illustrates the magnitude of the effect. In hot markets, promises of high growth increases VCs’ likelihood of investment by 64.84%, whereas it increases the likelihood by only 32.13% in cold markets.

Discussion

In this study, we investigate the effectiveness of signals and cheap talk on VCs’ investment decisions, depending on the heat of the market. Our results show that promises of high growth are effective in influencing VCs and that such cheap talk can even be more effective than profitability as a signal. This result is novel and surprising; it suggests that cheap talk can be stronger than signals, even independent of the market condition. One possible explanation is that growth potential represents an extremely important quality dimension for VCs, whose returns ultimately depend on the growth of new ventures (Jain et al., 2008). Yet the strong effect also suggests that VCs are less concerned about the dishonesty of cheap talk. On the flip side, VCs might perceive profitability, despite its credibility, as more ambiguous than promises of high growth. That is, VCs want to understand how new ventures can increase their value in the future, not just how they performed in the past.

Our results highlight the crucial moderating effect of market conditions. The effects of both—signal and cheap talk—are strongly contingent on whether the market is hot or cold, such that the effect of promises of high growth is much stronger in hot than in cold markets. Notably, promises of high growth still remain relevant in cold markets, so even in the absence of heated market sentiments, VCs find these less costly cues important. Profitability, in contrast, is only effective in cold markets, and its effect disappears almost entirely in hot markets. In turn, our results have important implications for signaling research and cognitive perspectives in the context of venture capital and early-stage financing, as well as practical implications for entrepreneurs and VCs.

Theoretical Contributions

Our study makes several theoretical contributions. First, by relaxing the previously established boundary condition regarding investor sophistication, it contributes to the growing body of research on cheap talk and rhetorical cues in new venture financing (Anglin et al., 2018; O. Colombo, 2021; Di Pietro et al., 2023; Kleinert, 2024; Steigenberger & Wilhelm, 2018). The cheap talk perspective (Crawford & Sobel, 1982)—originally developed as an alternative—is increasingly used as a complementary lens to Spence’s (1973) signaling theory in new venture financing, recognizing that entrepreneurs frequently use rhetoric and less costly communication as key means in the persuasion process of resource providers (O. Colombo, 2021). Prior research particularly highlights its role in strengthening the effect of signals in a portfolio (Steigenberger & Wilhelm, 2018), whereas other research even points to direct effects (Anglin et al., 2018). Although the cheap talk perspective (Farrell & Rabin, 1996) suggests that it should be effective when senders have no incentive to lie, this explanation appears less conceivable in the entrepreneurship context and at odds with agency theory, which assumes entrepreneurs have incentives to misrepresent or overstate their potential (Eisenhardt, 1989). Previous research therefore argues cheap talk plays a role in the persuasion process because less sophisticated investors are unable to judge the credibility of signals as accurately as experienced investors (O. Colombo, 2021). However, our study illustrates that even VCs, as prototypically sophisticated early-stage investors (Amit et al., 1998), find cheap talk useful, and we empirically show that it may be even more effective than costly signals.

Integrating our findings into prior discussions (e.g., Anglin et al., 2018; O. Colombo, 2021), we highlight three explanations for the effectiveness of cheap talk for sophisticated investors. First, cheap talk may be effective when signals (e.g., about new ventures’ future growth) are not available and especially when it provides information about quality dimensions that are of critical relevance for investors. For example, the growth of new ventures appears to be one of the central quality dimensions for VCs’ assessments (Block et al., 2019). As such, in our context, the promises of high growth might reduce activity-related information asymmetries as a logos appeal when conventional signals for this purpose are less readily available (Steigenberger & Wilhelm, 2018). Second, sophisticated investors may be aware of the risk that such cues simply reflect cheap talk, but they have the power to punish dishonesty, such as through the reputational damage they can inflict on new ventures if they fail to deliver (Shafi et al., 2020). Accordingly, sophisticated investors appear less likely to discount information because it is cheap. Consistent with Kirmani and Rao (2000), rhetorical cues such as promises of high growth might thus turn into a default-contingent signal where VCs can penalize dishonest entrepreneurs. Third, irrational exuberance in the market environment and accelerated due diligence processes may render sophisticated investors particularly susceptible to cheap talk, such that they focus on the salience instead of the credibility of information—a common behavior when decision-makers rely on heuristics (Chaiken, 1980). Taken together, our findings suggest relaxing the boundary condition that receivers must be unsophisticated for determining the effectiveness of cheap talk, with implications for research. We call attention to the possible relevance of cheap talk for more sophisticated audiences, and researchers should continue to advance understanding of how and when cheap talk works. For example, it could be beneficial to further explore different types of cheap talk. As suggested in Table 1, cheap talk could range from highly vague statements to more specific and seemingly grounded claims, such as highlighting the source of customer growth. Insights from language expectancy theory (e.g., Parhankangas & Renko, 2017) could complement cheap talk research. Additionally, further research should disentangle the possible underlying explanations we proposed to understand the effectiveness of cheap talk more clearly and beyond unsophisticated audiences. For example, the question remains as to what extent cheap talk might also contain elements of costly signals due to potential future penalty costs for dishonesty (e.g., Bafera & Kleinert, 2023). To delineate these constructs more precisely, a thorough investigation of this possibility is necessary.

Second, we contribute to a cognitive perspective of signaling theory (e.g., Drover et al., 2018; Steigenberger & Wilhelm, 2018; Vanacker et al., 2020) by emphasizing that decision-makers, such as VCs, switch between different modes of information processing in response to the market environment, which in turn affects reliance on signals or cheap talk. Growing research that integrates a cognitive view with signaling theory emphasizes that cognitive processes are a relevant determinant of resource-providers’ attention to and interpretation of signals (e.g., Edelman et al., 2021; Mahmood et al., 2019; Tumasjan et al., 2021). However, this research stream tends to assume that cognitive constraints are inherent to certain investors (Butticè et al., 2022) or static in certain contexts that require high cognitive demands (e.g., Kackovic & Wijnberg, 2022; Steigenberger & Wilhelm, 2018). Thus, prior research remains ambiguous as to whether early-stage investors rely on cognitive shortcuts and low-effort processing (Huang & Pearce, 2015) or comprehensive analysis and high cognitive effort processing, which is implicitly assumed in extensive signaling research (e.g., Ahlers et al., 2015; M. G. Colombo et al., 2019; Kleinert et al., 2022). Our study clarifies some of this ambiguity (Fisher & Aguinis, 2017) by explaining that decision-makers such as VCs adapt their cognitive processes to the environment. In this regard, the oscillation between hot and cold market emerges as a central contingency. As we clarify (Table 2), it affects the market sentiment, the institutional logic of VCs and the nature of information asymmetries, which shift from concerns about low-quality investments to fears of missing out. These factors lead to reduced due diligence, so that heuristic-based decisions appear to be enhanced in hot markets, leading VCs to pay more attention to the salience rather than credibility of information. In turn, cheap talk might become more relevant than signals in hot markets. For example, our study shows that in a hot market, VCs almost entirely neglect signals, such as the profitability of new ventures. We believe our contribution can stimulate important further research. Although our study focused on the main effects of signal and cheap talk in the different market environments, it may be useful to study the interactions among signals in a portfolio (e.g., Bafera & Kleinert, 2023). For example, entrepreneurs can boost the attention of their signals (Steigenberger & Wilhelm, 2018), which could also be a viable strategy in hot markets. Furthermore, it might be helpful to understand other contingencies for when decision-makers adjust their cognitive processes and rely on heuristics versus comprehensive analysis.

Relatedly, our dynamic perspective on hot and cold market phases also adds to research on VCs’ decision-making (Ademi et al., 2023; Drover, Wood, & Zacharakis, 2017). A plethora of research has examined criteria for VCs’ decision-making and produced long lists of relevant aspects (Ciuchta et al., 2018; Gompers et al., 2020; Kirsch et al., 2009; MacMillan et al., 1985; Petty & Gruber, 2011; Tyebjee & Bruno, 1984); however, it assumes a financial landscape in which VCs operate independent of market and competitive influences. Accordingly, these studies assume that VCs’ selection criteria are generally applicable, even though VC markets are significantly influenced in reality by fluctuations in hot and cold market phases (Lo et al., 2024; Zhelyazkov & Tatarynowicz, 2021). Our research extends venture capital research by demonstrating the profound impact of market dynamics on the importance of different decision criteria. Accordingly, a dynamic perspective is essential to understand how VCs adjust their criteria and preferences in response to changing market phases. Further research could use our results as a starting point to re-examine criteria that previous studies have identified as generally relevant, depending on market conditions.

Practical Implications

Our results offer important implications for entrepreneurs who seek venture capital funding: not only costly signals but also less costly communication can be effective to attract VCs. Because VCs care about growth prospects, entrepreneurs should highlight these prospects prominently when approaching investors. Entrepreneurs also must understand the potential contingencies created by prevailing market sentiments, so that they can tailor their signals to communicate their ventures’ quality to potential investors. During hot markets, for example, entrepreneurs can maximize their appeal to investors by demonstrating strong growth ambitions (e.g., by strategically putting their venture on a more aggressive growth path before searching for financing). In such hot markets, VCs might more readily overlook other credible information but prioritize salient information that aligns with the current market sentiment. In contrast, in cold markets, entrepreneurs should be aware that investors are likely to assign more importance to profitable business models or conservative financial data to address their risk aversion.

Our results are also practically relevant for VCs, who might use our insights to reflect on their own decision-making processes. We might assume that VCs make investment decisions based on comprehensive analyses and rational considerations, but in reality, they seem to rely more on heuristic-based decisions in hot markets and fear missing out on opportunities. Using such less reliable metrics may be, to some extent, justified, but being more aware of external influences also may help investors make more informed decisions.

Limitations and Further Research

Our study is not without limitations, and they provide avenues for continued research. First, conjoint experiments are based on hypothetical decision scenarios, so one shortcoming is their potentially limited applicability to real-world decisions (Wood et al., 2014). In reality, VCs may rely on many more influences on their decisions than the attributes we tested in the conjoint experiment. We attempted to increase external validity through interviews, best practices from previous conjoint studies, and theory-driven derivation of the scenarios and attributes in various ways (Hsu et al., 2017; Lohrke et al., 2010). Nevertheless, complementing our study with other methods (e.g., longitudinal designs) would be useful.

Second, our conceptualization and measure of profitability leave room for future research. As a conceptualization, we define profitability as a signal because it is difficult to imitate by low-quality ventures. However, in certain situations, it may not only be the attribute that informs about the unobservable quality of a new venture, but rather the quality proxy itself (e.g., Shepherd et al., 2000). The rather weak main effect of profitability on VCs’ assessments does not point in this direction in our context—maybe because VCs require exits that depend more on future growth than profits. We expect that such an explanation for profitability could be highly relevant for other investor types such as angel investors, who are less dependent on time-sensitive returns from exit events via IPOs or M&As (Gompers et al., 2020). Consistent with many previous conjoint studies (e.g., Warnick et al., 2018; Wood et al., 2014), we focused on two-level attributes in our experiment, that is, new ventures were either displayed as being profitable or not. We acknowledge that two levels limit the nuance of our profitability variable, and we cannot test how VCs respond to the various levels of profitability. However, it is important to stress that respondents in our conjoint analysis view profitability as part of the general descriptions of new ventures, that is, technology firms that are in the early growth stage and have multiple paying customers (see Figure 1). Accordingly, being profitable in our study clearly reflects a significant achievement for new ventures. Nevertheless, a new venture may have recently reached break-even, or it may have been highly profitable for years (Block et al., 2019), and these differences clearly play a role in the signaling effect of profitability and could also explain the weaker effect sizes for profitability in our study. Therefore, it would be valuable for future research to construct more levels to test the effect of profitability on VCs’ evaluations.

Third, our study is limited to one group of sophisticated investors, namely, VCs. We focused on this particular group because they still represent the prototypical early-stage investor and account for a large share of early-stage investments (Drover, Busenitz, et al., 2017). Similarly, their processes are often perceived as particularly structured because, unlike other sophisticated investors such as business angels, they assess new ventures on behalf of their LPs rather than for themselves (Payne et al., 2009). Extending our findings to other sophisticated investors would be worthwhile though. For example, angel investors might rely heavily on their gut feelings even in cold markets (Huang & Pearce, 2015) and use cheap talk differently than VCs.

Conclusion

This study provides insights into the effects of signals and cheap talk on venture capital funding. Their effects critically depend on whether the venture capital market is hot or cold. As we highlight, the optimistic market sentiments and fears of missing out in hot markets can significantly shift VCs’ attention towards cheap talk, such as promises of high growth. Such conditions may even prompt VCs to neglect costly signals such as the profitability of new ventures. Our study has practical implications for entrepreneurs, who must be aware of the importance of adapting their persuasion strategies to market conditions.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.