Abstract

Drawing on signaling theory, we explore the signaling effect of family firm status on firm value in the acquisition context as well as important contingencies influencing the signal’s effectiveness. Based on a sample of 486 observations of acquisitions in France, Germany, Italy, and Spain from 2011 to 2019, our empirical results suggest that acquirers purchase family firms at a higher firm value than non-family firms. This relationship is moderated by the target firm’s financial performance (i.e., high vs. low) and listing status (i.e., private vs. public) prior to an acquisition, as well as the type of acquirer (i.e., financial vs. non-financial) and the acquirer’s geographic location (i.e., cross-border vs. domestic). Our study’s findings suggest that family firm value is driven not only by the characteristics of the family firms that become acquired but also by the characteristics of the acquirers as they influence the effectiveness of the family firm signal.

Keywords

Introduction

An acquisition, in which one firm (acquirer) purchases a portion or all shares of another firm (target), is an important activity in the corporate setting to realize financial or strategic gains (Harrison et al., 1991; Seth, 1990). How much an acquirer should pay for a target is a central but complex issue in the acquisition context. Typically, the purchase price depends heavily on how the target is assumed to develop and what added value acquirers expect in the post-acquisition period (e.g., Gompers et al., 2016; Kaplan & Ruback, 1995). However, ex-ante acquisition targets’ prospects can be difficult for acquirers to predict (e.g., Reuer et al., 2012; Sanders & Boivie, 2004), making it challenging to determine a target’s acquisition price, hereafter referred to as firm value. This process is even more complex when the acquisition target is a family firm: that is, when the founder or members of a founder’s family maintain ownership in business and managerial control (Anderson & Reeb, 2003). Family firms are associated with higher levels of opacity compared to non-family firms (e.g., Anderson et al., 2009; Bona-Sánchez et al., 2019) because family firms possess idiosyncratic characteristics and have a much greater “play space” due to family members’ influence on firm decision-making (Gedajlovic et al., 2012; Gómez-Mejia et al., 2007), which can translate to a wide spectrum of potential firm value outcomes. Prior research has started to explore the implications of family firm characteristics and behaviors for firm value from different perspectives. Studies on the sellers’ perspective, for example, have inferred value premiums for family firms due to owner families’ emotional attachment to their firms (e.g., Astrachan & Jaskiewicz, 2008; Zellweger & Astrachan, 2008; Zellweger et al., 2012). Literature from the acquirers’ perspective is more ambiguous (Ahlers et al., 2014). Some studies have found that family firms exhibit higher firm values relative to non-family firms (e.g., Gonenc et al., 2013), while others have proposed value discounts because acquirers might consider family firms to be less efficient than non-family firms (e.g., Granata & Chirico, 2010).

These studies have advanced our initial knowledge, showing that unique family firm characteristics can have various implications for firm value differences between family firms and non-family firms. However, the literature still lacks a deeper understanding of the nature of the links between family firms’ idiosyncratic characteristics as well as other stakeholders’ characteristics and family firm value in the acquisition context (Ahlers et al., 2014; Feldman et al., 2019; Schickinger et al., 2018). Such an omission is surprising given that family firms are the most common organizational form worldwide (e.g., Gedajlovic et al., 2012) and a growing number of owning families are considering selling their businesses to outsiders (Neckebrouck et al., 2017). Because family firm acquisitions occur frequently and their global economic impact is substantial, a better understanding is needed on family firms as targets in acquisitions and of the potential contingencies that affect central sales aspects, such as firm value (e.g., Ahlers et al., 2014; Haider et al., 2021; King et al., 2022).

In light of these considerations, we examine in this study: (1) how does the family firm status affect the firm value of targets in acquisitions? and (2) how is this relationship influenced by important contingencies in the acquisition context? To address these research questions, we draw on the signaling theory (Spence, 1973). This theoretical perspective allows us to elaborate on the effect of family firm status, a signal that only family firms can reliably send (e.g., Schellong et al., 2019), on firm value. We propose this signal is a visible, costly to imitate for non-family firms, and relevant indicator for acquirers to infer the firm’s unique, value-creating potential in the post-acquisition period by shifting the focus from non-economic family goals to economic goals, justifying higher firm values for family firms relative to non-family firms. We further predict that the strength of the family firm status signal depends on the signal fit (i.e., target financial performance prior to the acquisition), signal interpretation (i.e., differences based on acquirer type), and degree of information asymmetry (i.e., induced by the targets’ private or public listing status, as well as the distance between acquirers and acquisition targets in terms of industry and geography). Data for our study are based on a sample of 486 observations of acquisitions in France, Germany, Italy, and Spain from 2011 to 2019.

We contribute to research on family firm valuation (e.g., Ahlers et al., 2014; Anderson & Reeb, 2003; Granata & Chirico, 2010; Villalonga & Amit, 2006) by extending the literature’s focus beyond solely considering family firm characteristics as the underlying reason for valuation discounts and premiums (e.g., Gonenc et al., 2013; Granata & Chirico, 2010). In addition, we contribute to the nascent research stream centered on family firms in the acquisition context (e.g., Feldman et al., 2019; Granata & Chirico, 2010; Zellweger et al., 2012) by shedding light on the mechanisms of how acquirer characteristics, such as acquirer type and geographic location, affect outcomes. Furthermore, we advance the family firm research using signaling theory as a theoretical basis (e.g., Schellong et al., 2019; Stutz et al., 2022)—to date, the family firm status signal has mainly been used to dichotomously distinguish family firms from non-family firms (e.g., Schellong et al., 2019). By introducing important contingency factors (e.g., signal fit, signal interpretation) that influence the strength of the signal, we expand the horizons of current theorizing on the signaling perspective in family business research.

Theoretical Background

Given our research focus on family firm value in the acquisition context, we first synthesize relevant background literature on the topic and then provide a brief introduction to signaling theory before developing our research hypotheses.

Family Firm Value

In general, a key aspect of firm valuation is how a firm is expected to develop in the future, with these expectations usually relating to the firm’s financial performance (e.g., Feldman et al., 2019; Kaplan & Ruback, 1995). In the acquisition context, a target’s development depends on the acquirer’s opportunities to improve the firm: for example, in terms of enhancing a firm’s operational efficiency or expanding a business beyond its current fundamentals (e.g., Kaufman, 1988; Reuer et al., 2012). An approximation of future financial performance is already difficult to gauge and highly uncertain for non-family firms, but this approximation is even more complicated for a family firm. Researchers have extensively studied family firm financial performance (e.g., Anderson & Reeb, 2003; Miller et al., 2007; Villalonga & Amit, 2006) and found evidence for both the underperformance and overperformance of family firms due to the family firm idiosyncrasies (Gedajlovic et al., 2012). Among others, these idiosyncrasies include long-term orientation, risk avoidance, and preferring to pursue non-financial family goals (e.g., Gedajlovic et al., 2012; Gómez-Mejía et al., 2007; Wright et al., 1996).

Although family firms’ financial performance and valuation appear to be thematically close and tightly linked, the topic of family firm value has received scant attention in prior research. Only a few studies have expanded the focus from family firm financial performance to examining family firm value from different angles: Early work on family firm valuation has taken the insider’s point of view (e.g., Astrachan & Jaskiewicz, 2008; Zellweger & Astrachan, 2008; Zellweger et al., 2012), applying an emotional perspective and predicting that due to their socioemotional wealth (SEW) and the related emotional attachment, family firm owners overestimate their firm’s value. Other work has considered the outsider’s perception of family firm value (e.g., Ahlers et al., 2014; Gonenc et al., 2013; Granata & Chirico, 2010) and suggested that, like family firm financial performance, family firm value is influenced by these firms’ idiosyncrasies. Thus, unsurprisingly, these studies have reported mixed results. On the one hand, scholars have argued that outsiders, such as acquirers, perceive the family firm as an unprofessional and inefficient form of organization, which, consequently, hurts family firms’ valuation compared to that of non-family firm acquisition targets (Granata & Chirico, 2010). On the other hand, researchers theorize that acquirers are willing to pay higher prices for family firms relative to non-family firms to convince the family selling the firm and giving up private benefits (Gonenc et al., 2013). Ahlers et al. (2014) put forward a real options perspective on family firm valuation, proposing conceptually that family firms as acquisition targets have both upside and downside value potential: that is, family departure after an acquisition carries opportunities for external value creation (which increase the family firm value) and risks losing family-dependent benefits (which decrease the family firm value).

In sum, the extant studies mainly focused on the relationship between family firms’ characteristics and family firm value. More recent work centered on family firms in the acquisition context, however, suggests that it is important to consider the characteristics of both the acquisition target and the acquirer when analyzing acquisition outcomes (Feldman et al., 2019). Building on the advancements in the literature, we examine the family firm value in the acquisition context, looking at both the characteristics of the family firm targets and those of the acquirers, which can have implications for the interpretation of family firm characteristics.

Signaling Theory

The origins of signaling theory are attributed to the seminal work of Spence (1973) and other closely related research (e.g., Stiglitz, 2002) that has investigated the implications of information asymmetries in various markets. From a signaling theory perspective, asymmetric information environments include an insider that obtains certain information and may send this information consciously or unconsciously in the form of a signal to an outsider who lacks this information but would like to obtain it (Connelly et al., 2011). Outsiders can use the signal (i.e., the information) to infer the quality or intent of insiders (Bergh et al., 2014; Connelly et al., 2011; Riar et al., 2021). Applied to our research context, a target (considered an insider) likely possesses information in areas such as its operations, stakeholder relations, strategies, and capabilities to perform in a specific business environment. An acquirer (considered an outsider) is usually unable to fully capture such information and intangible characteristics from the outside. Hence, there is an information asymmetry between acquirers and targets, making signals particularly relevant (Connelly et al., 2011; Spence, 1973). Indeed, signals that contain some piece of relevant information about a target’s prospects can be useful for an acquirer to mitigate the problem of asymmetric information and to draw conclusions on a target’s quality (e.g., the opportunity to create more value than the current firm fundamentals may suggest)—and, ultimately, its firm value (i.e., acquisition price).

Signaling theory suggests that if communicating information about a certain quality is not costly for insiders that do not possess the desired quality, all insiders would send the signal (Spence, 1973). Hence, signal cost is essential for separating equilibria (Bergh et al., 2014). In addition, signals are stronger when they are sent frequently (Janney & Folta, 2003), consistent among each other (Gao et al., 2008), and less distorted by the signaling environment (Lester et al., 2006). On the signal receiver side, outsiders must be able to observe a signal and pay attention to it in a potentially noisy environment (Gulati & Higgins, 2003). Signals are perceived as reliable when the information that is sent in the form of a signal is congruent with the quality (or intent) expected by outsiders receiving the information (Connelly et al., 2011). Different outsiders may interpret the same signal differently (Rynes et al., 1991).

In fact, signaling theory has previously been applied across a range of contexts in the family business research field to examine questions, among others, on corporate social responsibility, earnings management, employer attractiveness, consumer perception, investor preferences, and succession (e.g., Chandler et al., 2019; Huang et al., 2019; Schell et al., 2020; Schellong et al., 2019; Sekerci et al., 2022; Stutz et al., 2022). Family business researchers have mainly applied signaling theory in three areas: (i) signals individual family members send—for example, how heirs signal their abilities (Schell et al., 2020; Zhang, 2019); (ii) signals family firms send—for example, through charitable donations, compliance with governance standards, and investments in environmental and social projects (e.g., Gavana et al., 2017; Louie et al., 2019; Maung et al., 2020); and (iii) the family firm status as a signal itself—for example, for applicants, consumers, or investors (Duncan & Hasso, 2018; Hauswald et al., 2016; Schellong et al., 2019; Stutz et al., 2022).

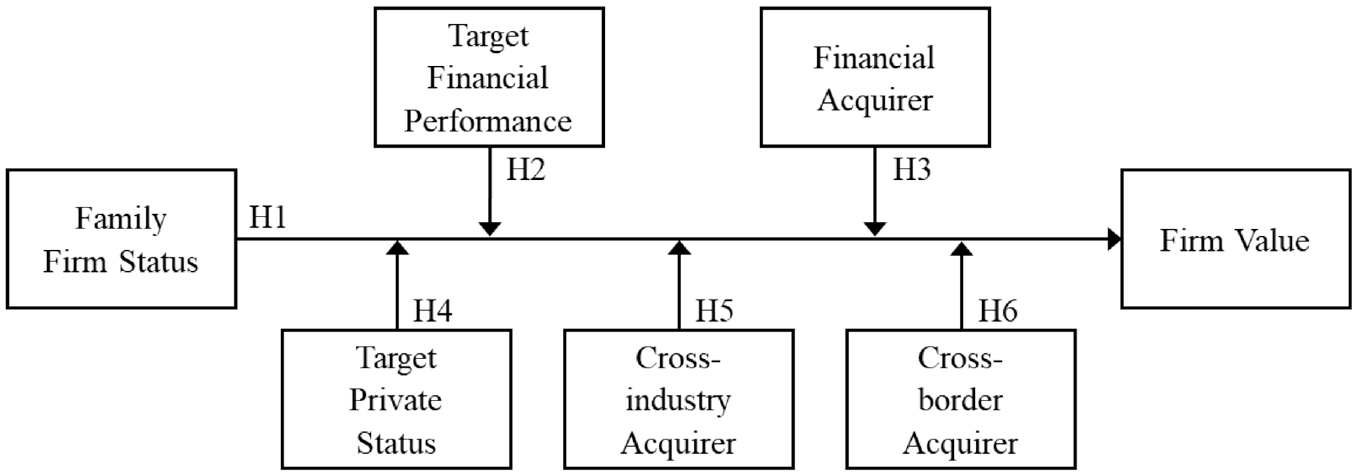

We adopt this third signaling perspective to study the role of the family firm status as a signal in the acquisition context. This perspective is useful because acquisitions are characterized by information asymmetries among acquirers and targets (Louis & White, 2007; Reuer et al., 2012). The family firm status signal allows outsiders—here, acquirers—to distinguish between family firms and non-family firms (e.g., Schellong et al., 2019). This is important because there may be potential value drivers that all types of targets can realize, as well as unique value-enhancing factors that only family firms can offer. Drawing on the insights from signaling theory, we discuss in the following section how the family firm status signal influences firm value in the acquisition context by illustrating the unique family firm-related factors. Subsequently, we outline the roles played by important contingencies for the family firm status signal’s effectiveness (see Figure 1).

Research model.

Family Firm Status as a Signal

Applying signaling theory to the acquisition context suggests that an acquirer can use the family firm status signal to draw conclusions on the firm value of targets (e.g., Reuer et al., 2012), which largely depends on what value gains acquirers expect after an acquisition (e.g., Gompers et al., 2016; Kaplan & Ruback, 1995). The family firm status signal is effective in acquisitions because it is visible to acquirers (e.g., on websites and annual reports), costly to imitate for non-family firms (as they cannot send it), and relevant to acquirers’ assessment as the family firm status signal contains some piece of relevant information from which acquirers can draw conclusions about a target’s characteristics and value-maximizing potential in the post-acquisition period (McGrath et al., 2004; Trigeorgis, 1993). Importantly, the family firm status signal may be effective even if it is not sent consciously (Comment & Jarrell, 1991; Louis & White, 2007).

Overall, we theorize that acquirers purchase family firm targets at higher firm values than non-family firm targets due to the family firm status signal. Family firms as acquisition targets signal distinct opportunities to acquirers, which enables them to create (thus far) unexploited economic value in the post-acquisition period (e.g., Feldman et al., 2016). Indeed, family firms’ behavior is often influenced by non-economic goals whose pursuance creates SEW for the owning family (Gómez-Mejia et al., 2007) and serves as the primary reference point for decision-making (Berrone et al., 2010, 2012; Gómez-Mejia et al., 2011), even when the non-economic goals are at odds with the owning family’s and other shareholders’ financial interests (Kellermanns et al., 2012). Transferring ownership from the owning family to an acquirer as part of an acquisition may change the focus ex-post. Acquirers will likely exploit available economic opportunities because family goals are expected to play no role or a subordinate role for the new owner (Nguyen et al., 2013). Hence, even if their overall firm performance is good, relative to non-family firms, family firms signal unique potential (e.g., to grow or to restructure) that acquirers can realize by shifting the focus from non-economic goal-driven decision-making to economic-driven decision-making in the post-acquisition period (Ahlers et al., 2014).

For example, to safeguard SEW, owning families are often willing to accept the risk of lower financial returns (Berrone et al., 2010; Gómez-Mejia et al., 2007, 2023). They avoid exploring risky but high-return business strategies that might result in a loss of SEW (Gómez-Mejia et al., 2011; Lim et al., 2010; Mishra & McConaughy, 1999), thereby reducing the firm’s ability to grow. Because acquirers typically lack family goal requirements, family firm targets might signal unique, untapped opportunities for growth due to the possibility of exploring new technologies or business models that could expand a target’s business scale (e.g., Grundström et al., 2012). Moreover, because pursuing non-economic goals is important to owning families (Gómez-Mejia et al., 2007, 2011), family firms are often associated with inefficient business operations (e.g., Sharma, 2004; Zellweger, 2007). For example, family firms tend to squander resources by holding onto loss-making assets because of emotional attachment or by refusing to relocate manufacturing sites from the region in which they are embedded to low-cost production countries due to the owning families’ sense of responsibility toward the local community (e.g., Dyer & Whetten, 2006; Sharma & Manikutty, 2005). Thus, acquirers are likely to see more opportunities and greater leverage in family firms relative to non-family firms to restructure the acquired firms through improving processes and revoking decisions free from family-centric considerations. In addition, family firms frequently rely on internal financing and are often associated with a tendency to underinvest due to the strong desire to maintain control (Berrone et al., 2012; Gedajlovic et al., 2012; Mishra & McConaughy, 1999), inhibiting family firms from fully realizing their economic capacities. Acquirers offer targets the necessary means and ease capital restrictions by optimizing financial structures to maximize economic value creation (Erel et al., 2015).

In addition, as acquisition targets, family firms signal to outsiders that they likely possess specific advantages originating from the firms’ resources that might promise acquirers unique value gains in the post-acquisition period. Family firms are frequently equipped with unique resources that provide them with advantages over non-family firms: among others, family social capital, family human capital, and family patient capital (e.g., Arregle et al., 2007; Sirmon & Hitt, 2003). Even if not all of these resources are transferred to an acquirer (e.g., patient capital), some—such as social capital—will likely carry over. For example, a family firm target’s special relationship with key stakeholders, such as customers, suppliers, and community organizations (e.g., Hitt et al., 2001), could be expected to continue. Hence, family firm targets might signal to their acquirers that some of the advantages of family firms will continue to pay off in the future, especially when the acquisition does not necessarily mean the end of the family’s contribution to the business (Steen & Welch, 2006).

Taken together, the family firm status of acquisition targets constitutes a signal that is visible, costly to imitate for non-family firms, and relevant to inferring unique opportunities that benefit the target economically in the post-acquisition period. Acquirers may interpret the signal such that they can exploit previously underutilized opportunities due to family influence, as well as benefit from family firm-specific resources that carry over and could lead to competitive advantages after an acquisition deal is closed. For these reasons, we expect higher firm values for family firms relative to non-family firms in the acquisition context.

Financial Performance as a Contingency for Signal Effectiveness

The strength and, consequently, the effectiveness of a signal increases with signal fit—that is, “the extent to which the signal is correlated with unobservable quality” (Connelly et al., 2011, p. 53). Drawing on this idea of signal fit, we expect that in the acquisition context, the target’s observed financial performance moderates the strength of the family firm status signal. A higher family firm target financial performance may lead acquirers to believe the target is less likely to have forgone economic goals and, hence, that they have fewer levers and opportunities to increase the target’s financial performance (i.e., lower signal fit) in the post-acquisition period.

As proposed above, the family firm status signal is visible, costly to imitate, and relevant for acquirers that intend to improve acquired firms’ financial performance (e.g., Kaplan & Strömberg, 2009). An excessive SEW focus usually harms a firm’s financial performance (Kellermanns et al., 2012), and observing low financial performance in family firms may signal to acquirers that owning families have forfeited their firms’ economic potential to preserve and extend their SEW. Thus, acquirers are more likely to expect they will increase family firm targets’ profitability more significantly: for example, through exploiting growth opportunities, improving operational efficiency through cost reductions, and optimizing capital structures (e.g., Gompers et al., 2016; Kaplan & Strömberg, 2009) previously underutilized due to family influence (e.g., Ahlers et al., 2014) when they observe a lower financial performance. This results in acquirers being more willing to pay a valuation premium.

Conversely, the family firm status signal being incongruent with an acquirer’s expectations weakens the signal’s positive effect on firm value because acquirers are more likely to expect lower potential to increase their target’s financial performance. Specifically, better financial performance might be observed as an indication of a well-performing family firm target that has already leveraged its full economic potential and focused on economic rather than SEW-related goals pre-acquisition. Moreover, acquirers might attribute the higher financial performance to family ownership and management because owner-managers are typically directly in charge (Anderson & Reeb, 2003; Anderson et al., 2009), and hence, the firm’s financial success might be driven by a single individual. While any acquirer faces the risk of losing human capital after acquisitions (Wulf & Singh, 2011), acquirers may face a drastic loss of within-firm human capital with the post-acquisition departure of an owner-manager, who is the central figure uniting decision-making, relationships, and knowledge (Ahlers et al., 2014). Such departure might be especially harmful to well-performing family firms because family members often hold key positions (Chrisman & Patel, 2012; Gómez-Mejia et al., 2018) and may withhold important information from non-family managers (Lee et al., 2003).

In sum, based on family firm targets’ financial performance, acquirers may have different expectations regarding their opportunity to substantially improve the targets’ financial performance in the future. Particularly for well-performing family firms, acquirers run the risk that all the levers of economic value creation have already been pulled. Thus, acquirers are expected to be less willing to pay relatively higher prices for family firm targets with higher financial performance because there is less upward potential to multiply their value through post-acquisition activities. As a result, the family firm status signal’s positive effect on firm value is expected to be weakened for family firm targets with higher financial performance.

Type of Acquirer as a Contingency for Signal Effectiveness

The interpretation of signals can vary across the outsiders receiving the same signal (Connelly et al., 2011; Rynes et al., 1991). Accordingly, different types of acquirers can interpret the family firm status signal differently. We distinguish between financial acquirers (e.g., financial institutions or professional investment firms) and non-financial acquirers (e.g., other family firms or non-family firms) because these types are perceived as viable buyout options for owning families (e.g., Chrisman et al., 2012; Dehlen et al., 2014; Feldman et al., 2019).

We expect the family firm status signal’s positive effect on firm value in acquisitions to be strengthened for financial acquirers compared to non-financial acquirers for several reasons. Due to the heavy pressure to generate above-average returns for their funds’ investors in a relatively short period of time (Gompers et al., 2016), financial acquirers (e.g., private equity firms) are mainly driven by economic factors that pay off quickly. As discussed above in more detail, the family firm status signals a focus on non-economic goals that would preserve or expand a family’s SEW, even at the expense of economic goals (e.g., Berrone et al., 2012; Gómez-Mejia et al., 2007; Kotlar et al., 2018). Financial acquirers typically have extensive plans to restructure, refocus, and operationally improve the acquired firms (Davis et al., 2014; Kaplan & Strömberg, 2009) and are likely to interpret the family firm status signal such that they can expect significant value gains because of unique opportunities previously underutilized due to family influence. Compared to non-financial acquirers, financial acquirers usually take a structured approach to systematically identify opportunities to grow the business, reduce costs, and improve the financing and capital structures of targets during the holding periods (e.g., Gompers et al., 2016; Kaplan, 1989; Kaplan & Strömberg, 2009) after which they typically sell the firm at a higher price (with holding periods for investments in private equity amounting to around five years; Gompers et al., 2016). Hence, financial acquirers expect their post-acquisition activities to heavily influence the financial performance of family firm targets. Non-financial acquirers, in turn, might have similar decision-making patterns as the family firm target and a more long-term focus. For example, non-financial acquirers—such as other family firms, family offices, or corporates—are likely to also consider non-economic objectives in their strategies and decision-making, such as empire-building, securing strategic assets, or reducing risk through diversification (e.g., Feldman et al., 2019; Haider et al., 2021; Trautwein, 1990).

For these reasons, we expect financial acquirers will likely use the family firm status signal more intensively in their assessment and interpret the signal more favorably due to their economically driven business model compared to non-financial acquirers that might also consider non-economic objectives. Thus, we expect the family firm status signal to have a stronger effect on firm value in the acquisition context when the acquirer is a financial acquirer compared to a non-financial one.

Degree of Information Asymmetry

Signals are expected to have less impact in situations characterized by lower levels of information asymmetry and greater impact in situations characterized by higher levels of information asymmetry (Spence, 1973). We put forward that information asymmetry is higher when (1) targets are privately held; (2) acquirers are not from the same industry as the targets; and (3) acquirers are foreign, thereby strengthening the overall relevance of the family firm status signal. We discuss each aspect separately below.

Target Private Status as a Contingency for Signal Effectiveness

We expect the family firm’s signaling effect to be stronger for private acquisition targets than for publicly listed ones due to lower pressure to disclose information and minority shareholder protection in the private firm context relative to the public firm context (e.g., Doshi et al., 2013; Loderer & Waelchli, 2010; Reese & Weisbach, 2002). In general, whereas publicly listed firms must disclose information that may influence stakeholders’ decisions and prepare reports that are publicly available and accessible (e.g., Farraghe et al., 1994), private firms are usually exempt from such requirements. Hence, prospective acquirers have limited access to accurate, timely information on private targets, resulting in greater information asymmetry between acquirers and private targets. Consequently, acquirers are more likely to rely on signals, such as the signal sent by family firms, to draw conclusions on a private target’s potential leverage in value creation. In turn, because acquirers of publicly listed targets have broad access to information about the firms to be acquired (Capron & Shen, 2007), the family firm status signal is expected to be less relevant.

Furthermore, acquirers might expect greater value gains with private family firm targets compared to public family firm targets because private firm managers are less accountable to their stakeholders and have better control over the information they communicate (e.g., Capron & Shen, 2007; Reuer & Ragozzino, 2008); this allows them to deviate from what is considered economically best for the firm. Thus, acquirers likely expect private family firms to have a stronger focus than public family firms on non-economic goals (e.g., expanding SEW) at the expense of economic goals, such as generating financial returns (Carney et al., 2015; Gómez-Mejia et al., 2007; Kotlar et al., 2018) and acquirers predict greater leverage in value creation with private family firm targets versus public ones from the same post-acquisition activities (e.g., shifting the focus from non-economic family goals to economic goals). Overall, we expect the signal effect of the family firm status to be stronger for privately held family firms.

Cross-Industry Acquisition as a Contingency for Signal Effectiveness

We expect family firms’ signaling effect to be stronger for cross-industry acquirers compared to within-industry acquirers because the degree of information asymmetry increases when acquirers and targets are not industry related (e.g., Borochin et al., 2019; Capron & Shen, 2007). Due to less—and potentially lower quality—information, we propose that the uncertainty in assessing value-enhancing potentials of targets is significantly greater for cross-industry acquirers compared to within-industry acquirers (e.g., Capron & Shen, 2007). Therefore, cross-industry acquirers are expected to rely more on the family firm status signal to adapt a target’s firm value. By contrast, acquirers operating in the same or related industry domain as a target are better positioned to evaluate an acquisition opportunity based on more and better-quality information (Ahuja & Katila, 2001; Cordes et al., 2021; Graham et al., 2017). Hence, within-industry acquirers are more likely than cross-industry acquirers to understand what part of business performance can be attributed to the targets themselves (i.e., their characteristics) rather than other factors, such as the market conditions in a particular industry. Thus, within-industry acquirers can better distinguish between targets with “good” and “bad” prospects and identify the potential for optimization much more easily than cross-industry acquirers can do due to lower information asymmetry. Hence, within-industry acquirers are less likely to rely on signals, such as the family firm status signal. For these reasons, we expect the family firm status signal to be stronger for cross-industry acquirers compared to within-industry acquirers.

Cross-Border Acquisition as a Contingency for Signal Effectiveness

We expect family firms’ signaling effect to be stronger for cross-border acquirers compared to domestic acquirers. In general, the degree of information asymmetry is higher when targets are geographically distant (Capron & Shen, 2007; Kang & Kim, 2010; Reddy & Fabian, 2020). Cross-border acquirers are less familiar with the institutional, cultural, and regulatory context relative to domestic acquirers (Adair & Brett, 2005; Capron & Shen, 2007; Westbrock et al., 2019) because acquirers’ expertise is often country-specific (Krishnan & Masulis, 2013). Hence, cross-border acquirers have less information and understanding about, for example, the rule of law and its application in another country. In addition, the physical distance of cross-border acquirers might increase the difficulty of evaluating distant assets (Rosenkopf & Almeida, 2003), and the communication barriers (e.g., due to culture or language) might further hinder overcoming the problem of asymmetric information among managers, buyers, and sellers (Capron & Shen, 2007; Cuypers et al., 2015). Such distance strengthens the relevance of signals. In sum, given the higher degree of information asymmetries for cross-border acquirers compared to domestic acquirers, we expect the family firm status signal to be stronger for cross-border acquirers.

Methods

Sample and Data Collection

Data for our study are based on acquisitions of family firms and non-family firms in France, Germany, Italy, and Spain from 2011 to 2019. We selected these countries because they are among the largest economies in the European Union and have a high proportion of family firms (Faccio & Lang, 2002). Furthermore, these countries have a high proportion of private firms (Franks et al., 2012). This makes the inclusion of private firms, next to publicly listed firms, in the acquisition context especially relevant.

The acquisition deal data were retrieved from Thomson’s SDC Platinum Mergers and Acquisitions database (hereafter referred to as SDC database). Data on the firms from these deals (e.g., on financials, ownership, and management) were obtained from Bureau van Dijk’s Amadeus database (hereafter referred to as Amadeus database); we combined annually archived Amadeus extracts with the online version of Amadeus to identify global ultimate owners. Our starting population included all French, German, Italian, and Spanish acquisitions available in the SDC database from 2011 to 2019. We only considered acquisitions in which the acquirers owned at least 50% of the shares after the deal was completed to ensure they had sufficient control over the acquisition target to implement and enforce post-deal measures. In total, we obtained information on 2,510 acquisitions.

To map the acquisition deal information retrieved from the SDC database with the firm data, we identified acquisitions’ corresponding firms in the Amadeus database by matching full firm names, including legal entity types and at least one location identifier, such as city, zip code, or street name and number. We excluded observations (1,036) from our overall sample when matches would have been speculative, which resulted in a sample of 1,474 observations. We further eliminated observations (809) with missing data on our study’s dependent, independent, moderator, and control variables, as well as observations (179) where the targets had negative earnings before interest, taxes, depreciation, and amortization (EBITDA), 1 leaving us with a final sample of 486 observations.

Measures

Dependent Variable

Firm Value

In line with previous research on family firm valuation in the acquisition context (e.g., Granata & Chirico, 2010), our dependent variable was measured as the ratio of enterprise value (EV) over EBITDA (i.e., EV/EBITDA multiple). The EV/EBITDA multiple is one of the most applied valuation approaches among investment professionals and has a high valuation accuracy (Asquith et al., 2005; Chullen et al., 2015; Eaton et al., 2021; Gompers et al., 2016; Kaplan & Ruback, 1995; Liu et al., 2002). 2 The EV represents an economic measure reflecting the value of a target. From the SDC database, we obtained the acquisition targets’ EV at deal effective date, which is calculated “by multiplying the number of actual target shares outstanding from its most recent balance sheet by the offer price and then by adding the cost to acquire convertible securities, plus short-term debt, straight debt, and preferred equity minus cash and marketable securities” (Thomson Reuters, 2017, p. 80). The EBITDA is measured using operating income before interest, taxes, depreciation, and amortization. We retrieved the EBITDA values for the 12 months prior to the deal effective date from the Amadeus database. To alleviate concerns about outliers, we winsorized the EV/EBITDA multiples at the 2.5th and 97.5th percentiles (e.g., Aktas et al., 2019; Siqueira et al., 2018).

Independent Variable

Family Firm

In line with previous research on the differences between family firms and non-family firms (e.g., Chrisman & Patel, 2012; Gómez-Mejia et al., 2023), we used a binary measure for family firms. Our binary measure—family firm dummy (FFD)—was coded as 1 when the firm was a family firm and coded as 0 otherwise. We distinguished family firms from non-family firms based on ownership and managerial involvement (Anderson & Reeb, 2003). Regarding ownership, a family had to be the firm’s largest shareholder (Xu et al., 2020) and possess at least 25% of the outstanding cash flow rights. The 25% threshold was chosen to ensure sufficient family control for family characteristics to influence the firm and outcomes, such as firm performance and, ultimately, firm value (Andres, 2008; Franks et al., 2012; Lins et al., 2013).

We obtained ownership information from the Amadeus database. In cases of missing ownership data for a given acquisition year, we used ownership data for up to 3 years prior to the required year as an approximation because ownership is usually held over years or even generations (Jaskiewicz et al., 2015). Regarding family management, at least one family member had to be in the management prior to the acquisition. Moreover, following the work of Miller et al. (2007), we required that at least two family members be involved as owners or managers. We identified family members involved in a family firm’s management using two strategies: First, we searched for managers with the same last name as the owner family (e.g., Gentry et al., 2016; Mani & Durand, 2018; Rutherford et al., 2008), and second, we conducted a web-based search to identify family relationships for managers who did not share the same last name as the owner family. The first author conducted coding, and another trained researcher independently checked a subsample; the author team discussed discrepancies to reach an agreement.

Moderators

The first moderator, target financial performance, was measured as a target’s asset turnover in the year prior to acquisition completion as an indicator of how efficiently assets were used (Hunton et al., 2003). The second moderator, financial acquirer, was a dummy variable coded as 1 when the acquirer was a financial institution, an investment holding company, or an investment fund—acquirers with a Standard Industrial Classification (SIC) code starting with 6 in the SDC database—and 0 otherwise (Carow et al., 2004). The third moderator, target private status, was a dummy variable coded as 1 when the target was a privately held firm and 0 otherwise. The fourth moderator, cross-industry acquirer, was a dummy variable coded as 1 when the target’s four-digit SIC code did not match the acquirer’s and coded as 0 otherwise (Linn & Switzer, 2001; McGahan & Porter, 1997). The last moderator, cross-border acquirer, was a dummy variable coded as 1 when the acquirer was located outside the European Union and 0 otherwise.

Control Variables

We included firm-level, deal-level, and context-level variables as controls in our regressions. To control for firm-specific conditions and company life cycles, we controlled for target firm size, measured as the natural logarithm of total assets, and target firm age, measured as the natural logarithm of the acquired firm’s age (Anderson & Reeb, 2003; Isakov & Weisskopf, 2014). We used a binary measure—family CEO—to control for whether the CEO was a family member or not; this was coded as 1 when the CEO was a family member and 0 otherwise. In addition, we controlled for return on assets based on EBITDA, one of the most used variables for measuring firm performance (Anderson & Reeb, 2003). Specifically, we used target EBITDA margin in the 12 months prior to the deal effective date to control for historic profitability and target asset turnover. To control for capital structure, we used target financial leverage in the 12 months prior to the deal effective date, measured as total liabilities divided by total shareholders’ equity (Isakov & Weisskopf, 2014). In addition, we controlled for the stake acquired in the specific acquisition, measured as the ownership share acquired by the acquirer to control for deal-specific conditions, control premiums, and minority discounts (Damodaran, 2012). To control for influencing factors of the environment, we used year dummies based on the deal completion years, target country dummies, and target industry dummies based on one-digit SIC codes to control for year, country, and industry fixed effects.

Results

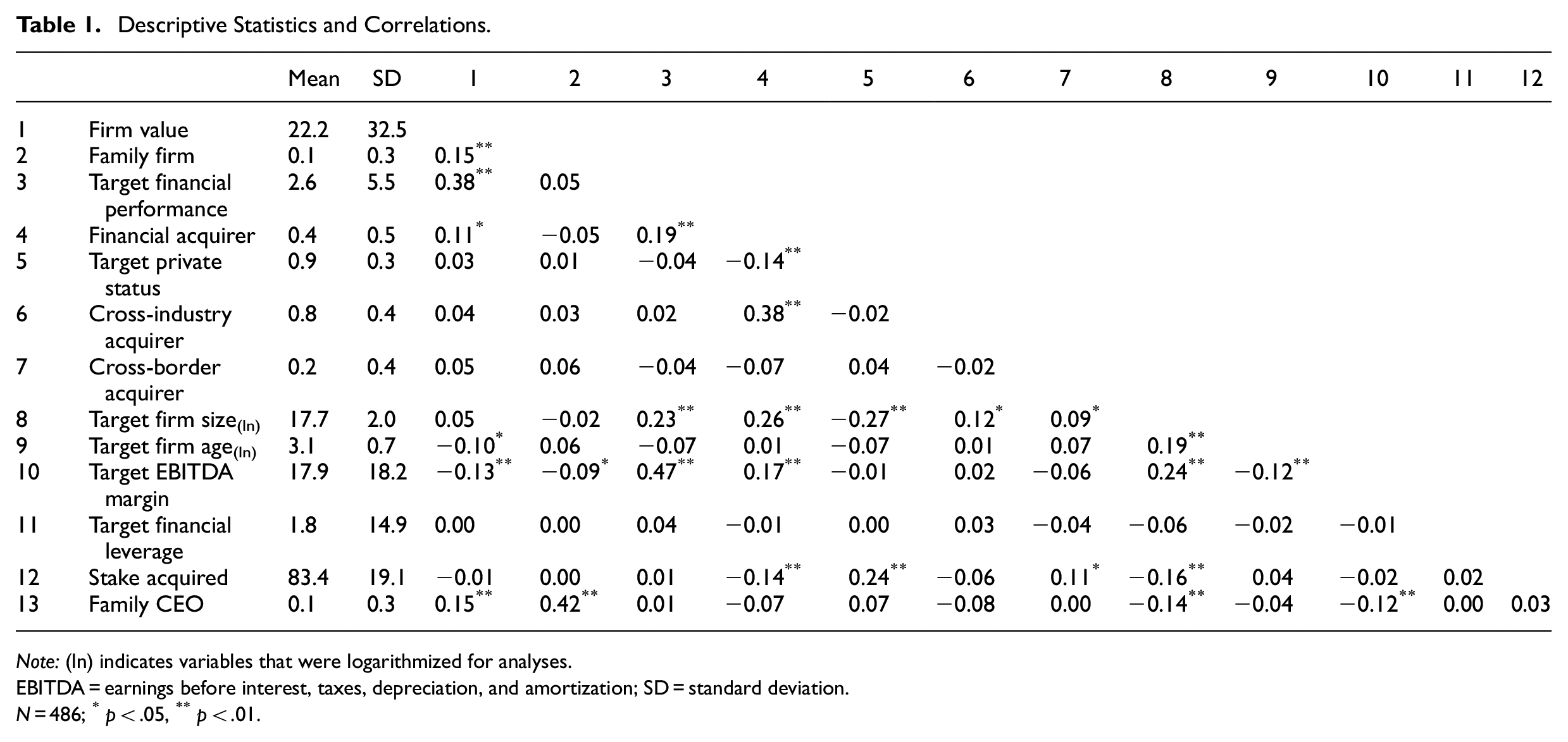

Table 1 displays the means, standard deviations, and Pearson correlation coefficients. The correlations between the variables in our research model are moderate, indicating they are empirically distinct. Variance inflation factors are all below 2. This is below the rule of thumb of 10, indicating no risk of multicollinearity (Hair et al., 2010).

Descriptive Statistics and Correlations.

Note: (ln) indicates variables that were logarithmized for analyses.

EBITDA = earnings before interest, taxes, depreciation, and amortization; SD = standard deviation.

N = 486; *p < .05, **p < .01.

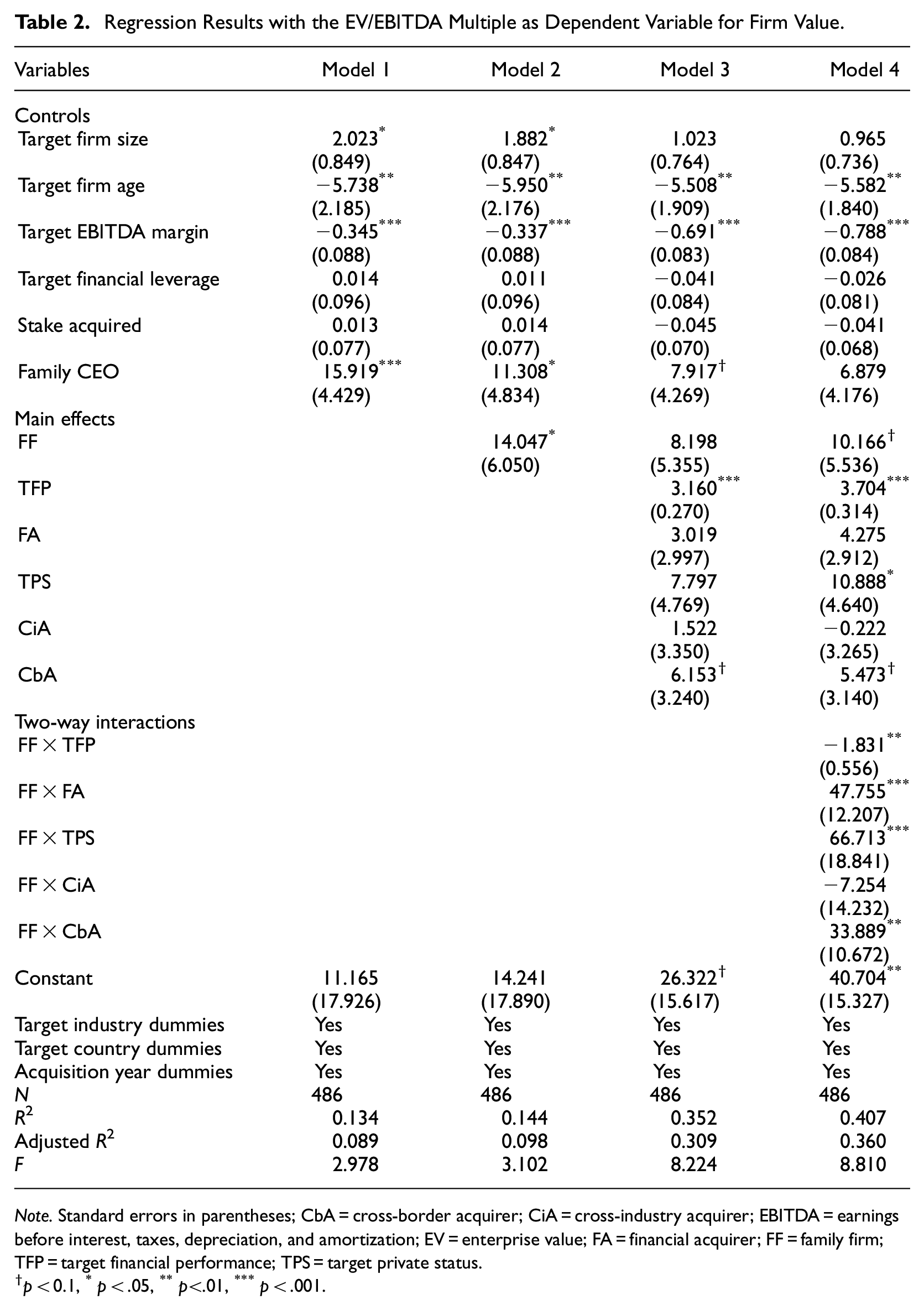

We used ordinary least squares regressions to test our hypotheses. Table 2 presents the regression results using the EV/EBITDA multiple as the dependent variable for firm value. We first added only the control variables, as seen in Model 1. Then, we included the main effect in Model 2, after which we entered the moderator variables and two-way interaction terms in Models 3 and 4. Model 4 presents the full specified model, which explains 36% of the variance in firm value. When computing the interaction terms, we mean-centered our variables. To better interpret the moderating effects, we plotted the significant interactions based on the regression coefficients in our analyses (see Figures 2–5).

Regression Results with the EV/EBITDA Multiple as Dependent Variable for Firm Value.

Note. Standard errors in parentheses; CbA = cross-border acquirer; CiA = cross-industry acquirer; EBITDA = earnings before interest, taxes, depreciation, and amortization; EV = enterprise value; FA = financial acquirer; FF = family firm; TFP = target financial performance; TPS = target private status.

p < 0.1, *p < .05, **p<.01, ***p < .001.

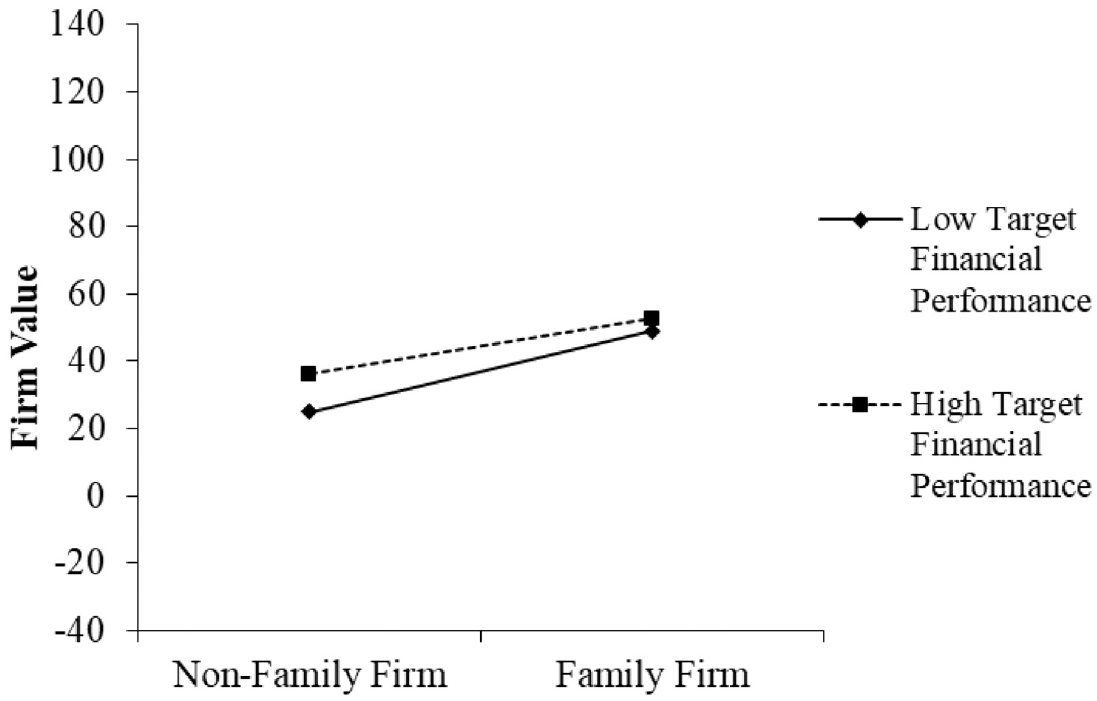

The interactive effect of family firm status and target financial performance on firm value.

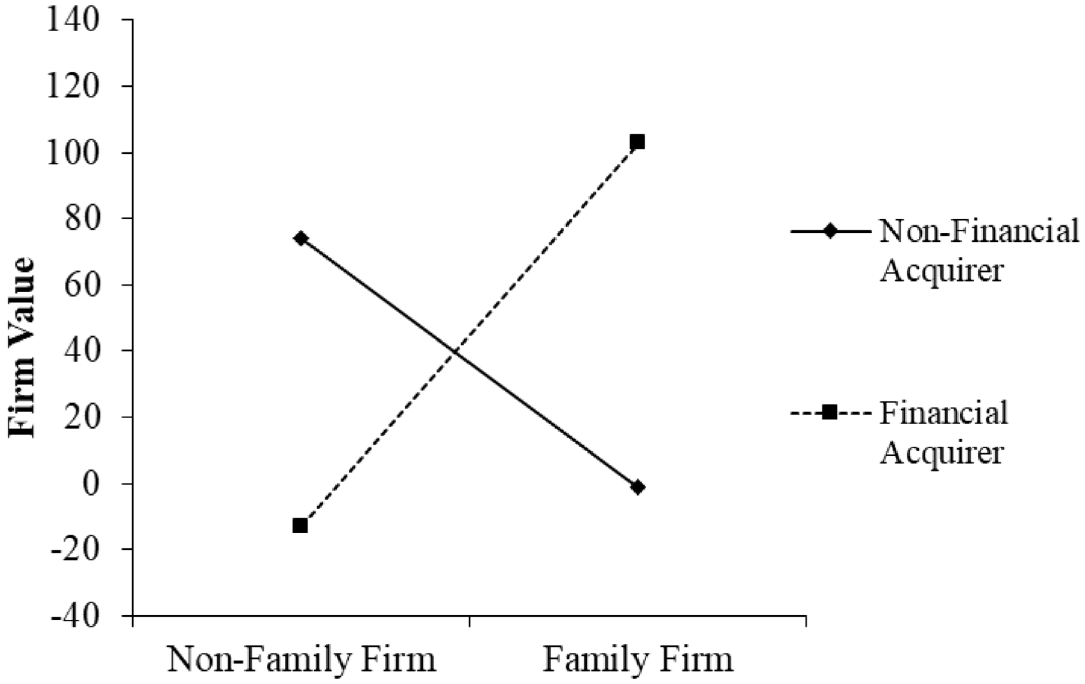

The interactive effect of family firm status and financial acquirer on firm value.

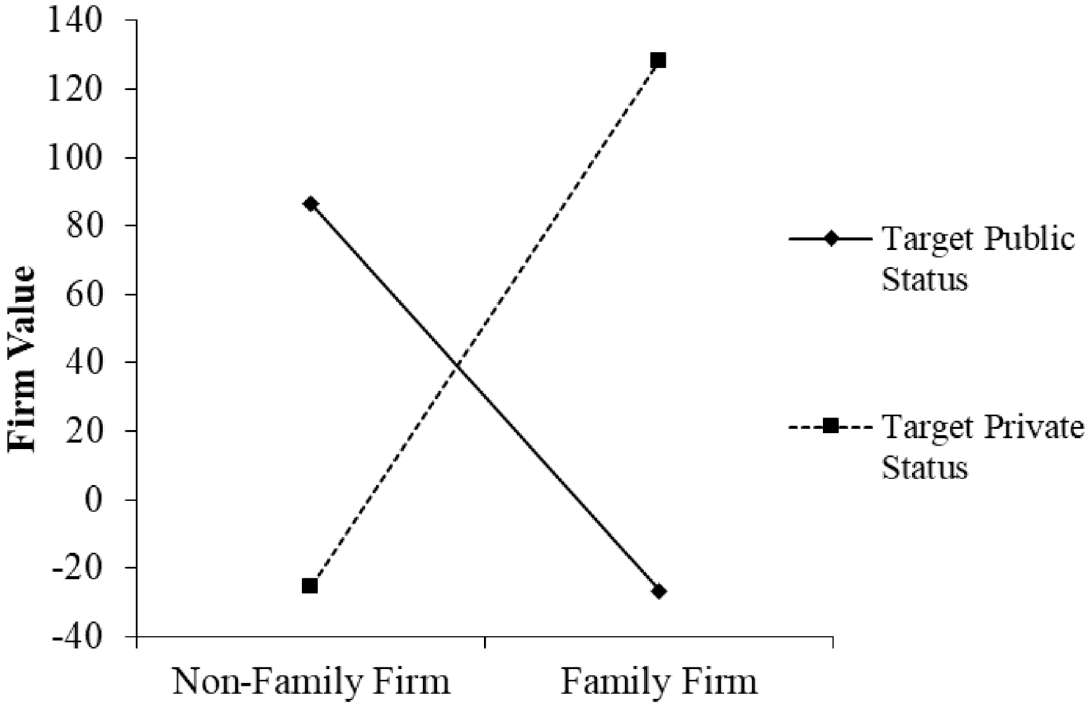

The interactive effect of family firm status and target private status on firm value.

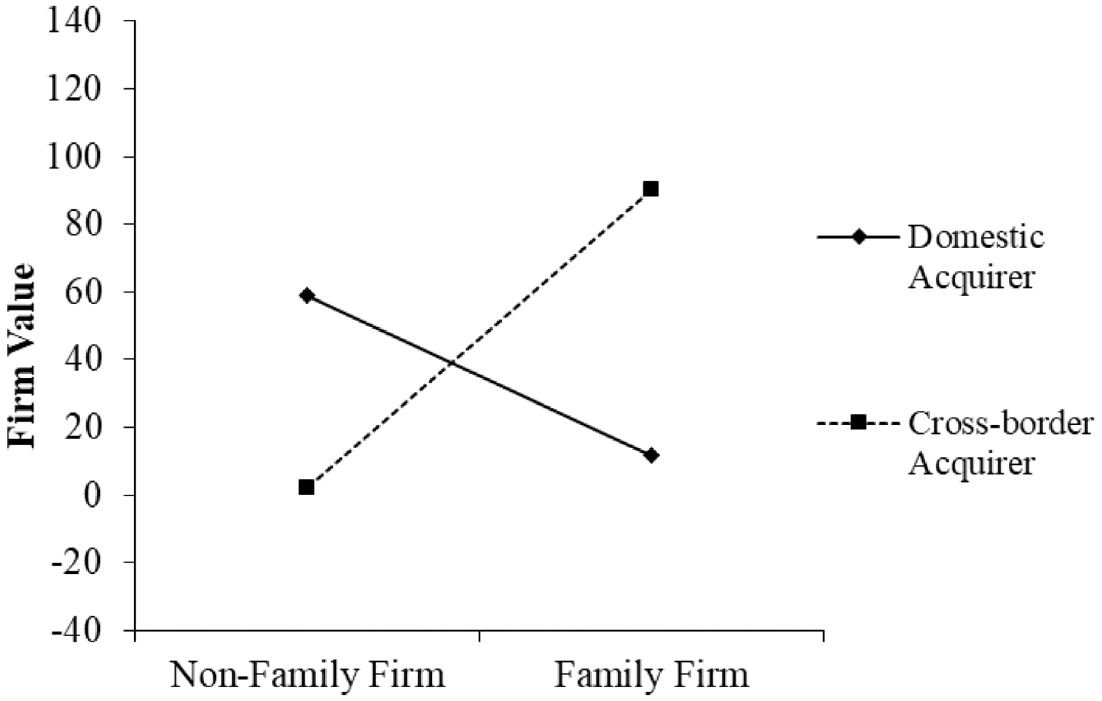

The interactive effect of family firm status and cross-border acquirer on firm value.

H1 suggests that acquirers purchase family firm targets at higher firm values than non-family firm targets in acquisitions. Model 2 provides empirical support for H1, with family firms’ main effect on firm value being positive and statistically significant (β = 14.047, p < .05). H2 predicts the family firm status’ positive effect on firm value in acquisitions will be weaker for targets with higher financial performance compared to those with lower financial performance. Model 4 and Figure 2 demonstrate empirical support for H2, with family firms and higher target financial performance having a negative and statistically significant interaction effect on firm value (β = −1.831, p < .01). H3 posits the family firm status’ positive effect on firm value in acquisitions will be stronger for financial acquirers compared to non-financial acquirers. In line with H3, family firms and financial acquirers have a positive and statistically significant interaction effect on firm value in Model 4 (β = 47.755, p < .001). However, as Figure 3 shows, family firms and non-financial acquirers do not have a weaker, positive interaction effect on firm value (as expected in H3); in fact, they have a negative interaction effect. H4 suggests the family firm status’ positive effect on firm value in acquisitions will be stronger for privately held family firm targets compared to publicly listed ones. In line with H4, family firms and target private status have a positive and statistically significant interaction effect on firm value in Model 4 (β = 66.713, p < .001). However, as Figure 4 shows, family firms and target public status have a negative interaction effect on firm value and not a weaker, positive one (as expected in H4). H5 predicts the family firm status’ positive effect on firm value in acquisitions will be stronger for cross-industry acquirers compared to within-industry acquirers. Model 4 does not demonstrate empirical support for H5, with family firms and cross-industry acquirers having a statistically insignificant interaction effect on firm value. H6 posits family firm status’ positive effect on firm value in acquisitions will be stronger for cross-border acquirers compared to domestic acquirers. In line with H6, family firms and cross-border acquirers have a positive and statistically significant interaction effect on firm value in Model 4 (β = 33.889, p < .01). However, as Figure 5 shows, family firms and domestic acquirers do not have a weaker, positive interaction effect on firm value (as expected in H6) but instead have a negative interaction effect.

Supplementary Analyses

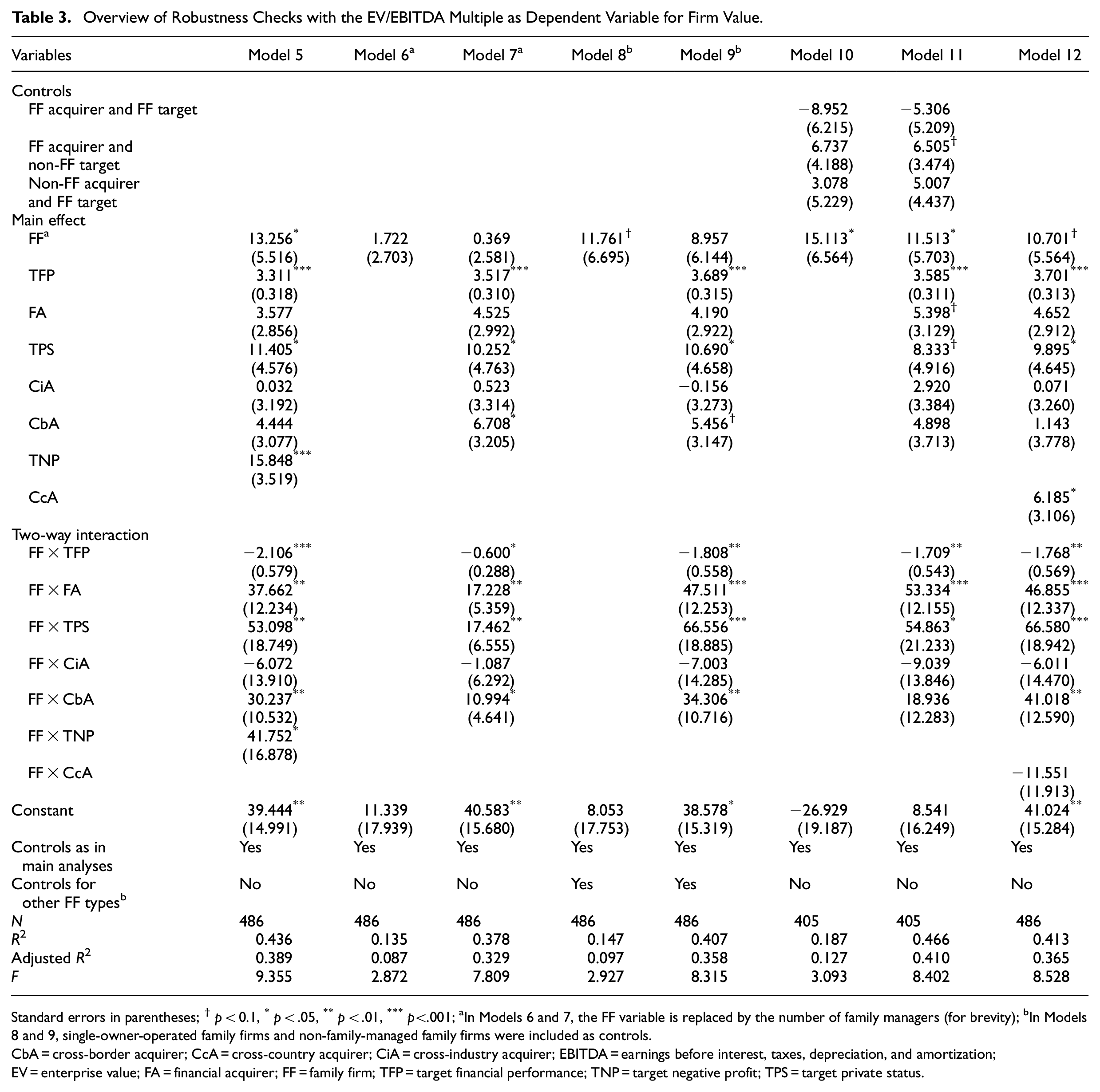

To assess our findings’ robustness regarding alternative specifications and explanations, we conducted additional supplementary analyses (see Table 3).

Overview of Robustness Checks with the EV/EBITDA Multiple as Dependent Variable for Firm Value.

Standard errors in parentheses; †p < 0.1, *p < .05, **p < .01, ***p<.001; aIn Models 6 and 7, the FF variable is replaced by the number of family managers (for brevity); bIn Models 8 and 9, single-owner-operated family firms and non-family-managed family firms were included as controls.

CbA = cross-border acquirer; CcA = cross-country acquirer; CiA = cross-industry acquirer; EBITDA = earnings before interest, taxes, depreciation, and amortization; EV = enterprise value; FA = financial acquirer; FF = family firm; TFP = target financial performance; TNP = target negative profit; TPS = target private status.

First, we tested the robustness of the interaction between family firms and target financial performance by shifting the focus from high target financial performance (i.e., high asset efficiency, measured as an acquisition target’s asset turnover) to low target financial performance (i.e., negative profit). When acquirers observe that their targets are generating negative profits, they may expect the family firm to focus even more on non-economic goals that create SEW at the expense of economic goals (e.g., financial performance). We used target negative profit as a dummy variable coded as 1 when the target earned a negative net profit in the year prior to acquisition completion and 0 otherwise. In line with H2, we found the coefficient of the interaction effect between family firms and target negative profit to be positive and significant; see Model 5 (β = 41.752, p < .05).

Second, we used family management as a continuous measure as an alternative to test our hypotheses. For this measure, we counted the number of family members in the family firm’s management in the year prior to the acquisition deal. Non-family firms were coded as 0. Using this definition assumes the signal effectiveness increases linearly with the number of family managers. Finding an insignificant relationship between the family management measure and firm value (see Model 6) indicates that family firms are likely homogenous in nature for this specific relationship and our acquisition context (i.e., our first research question). Regarding the interactions (see Model 7), we found the family management measure and target financial performance to have a negative and significant interaction effect on firm value (β = −0.600, p < .05), the family management measure and financial acquirers to have a positive and significant interaction effect on firm value (β = 17.228, p < .01), the family management measure and privately held family firm targets to have a positive and significant interaction effect on firm value (β = 17.462, p < .01), and the family management measure and cross-border acquirers to have a positive and significant interaction effect on firm value (β = 10.994, p < .05). The significant interaction results for the moderators target financial performance and financial acquirer suggest that acquirers (i.e., outsiders) in general and financial acquirers, in particular, may expect a higher focus on non-economic goals that create SEW (vs. focus on economic goals) with a greater number of family managers involved in a family firm; this allows acquirers to pull greater levers of economic value creation in the post-acquisition period. Furthermore, the significant interaction results of the moderators target private status and cross-border acquirers suggest the number of family members involved in the management of family firms gains relevance as a signal with greater information asymmetry.

Third, we controlled for other types of family firms to examine if our results would change when we imposed different qualifications for what a “family firm” is. To do so, we used further operational family firm definitions to check the robustness of our main results (1) by controlling for different family firm types in our regressions (i.e., adding single-owner-operated family firms and non-family-managed family firms as control variables to our regression models) and (2) by analyzing whether our hypotheses would work when replacing the original family firm definition with other operational family firm definitions (i.e., using single-owner-operated family firms and also non-family-managed family firms as an independent variable for the main relationship and for the interactions). The dummy variable single-owner-operated family firm was coded as 1 when (i) family members were the largest shareholders and owned at least 25% of the outstanding cash flow rights and (ii) only the single owner was involved in management in the year prior to acquisition completion; the variable was coded as 0 otherwise. The dummy variable non-family-managed family firm was coded as 1 when (i) family members were the largest shareholders and owned at least 25% of the outstanding cash flow rights and (ii) no family member was involved in management in the year prior to acquisition completion; the variable was coded as 0 otherwise. Regarding the latter analyses (i.e., when replacing the original family firm definition), the untabulated regression results (for brevity) of the direct effect and interaction effects showed almost no significant results for the two alternate family firm variables, except for the interaction effect of single-owner-operated family firm and target asset turnover (β = 5.378, p < .001). 3 The direct effect and interaction effects for the original FFD variable, however, remained stable when these two additional firm types were included as controls; see Model 8 for the direct effect and Model 9 for the interaction effects. These results support the robustness of our main analyses. The results also confirm that family firm status may only be effective as a signal when the conditions of a family’s managerial control and a family’s ownership in the business apply together.

Fourth, we controlled for the four possible configurations of family firm status and non-family firm status of acquirers and targets to challenge the robustness of the results in our main analyses, as well as to test the alternative hypothesis that our results were not driven by signaling but by varying degrees of agency costs (Feldman et al., 2019). Hence, we added three control variables, with non-family firm acquirer and non-family firm target as the baseline: (i) family firm acquirer and family firm target; (ii) family firm acquirer and non-family firm target; and (iii) non-family firm acquirer and family firm target. The regression result for our main effect is essentially the same as in our main analyses, with family firms having a positive and significant direct effect on firm value (β = 15.113, p < .05; see Model 10). The regression results for our moderators are the same as in our main analyses, except for the interaction effect of cross-border acquirers, which is statistically insignificant (see Model 11). Overall, these findings support the signaling explanation for our main effect, as well as for most of our interaction effects. Interestingly, while the configurations “family firm acquirer and family firm target” and “non-family firm acquirer and family firm target” are statistically insignificant, we find the “family firm acquirer and non-family firm target” configuration to have a positive and statistically significant direct effect on firm value (β = 6.505, p < 0.1).

Finally, we tested our findings’ sensitivity using another definition of cross-border acquirers: that is, based on countries instead of the European Union as an economic market. While the regression result for cross-border acquirers aligns with those in our main analyses with family firms and cross-border acquirers having a positive and statistically significant interaction effect on firm value (β = 41.018, p < .01), the regression result for cross-country acquirers is not significant (see Model 12). This finding indicates that a certain threshold of “foreignness” is required for the family firm status signal to be effective.

Discussion

This research adds to the understanding of family firm valuation by drawing on signaling theory (Spence, 1973). It investigates how family firm status impacts the firm value of acquisition targets and how the strength of the family firm status signal effect is influenced by important contingencies in the acquisition context.

Our study’s findings show that the family firm status signal can have major implications for firm value because acquirers may interpret this signal as meaning they can exploit previously underutilized opportunities due to family influence and also benefit from family firm-specific resources that carry over to the post-acquisition period. Accordingly, we expected and found that the family firm status signal, in general, has a positive effect on firm value (H1).

The family firm status signal’s strength might depend on the signal fit (i.e., target financial performance), signal interpretation (i.e., differences based on acquirer type), and degree of information asymmetry (i.e., induced by the targets’ private or public listing status, as well as the distance between acquirers and acquisition targets in terms of industry and geography). Regarding the first moderator—target financial performance—better financial performance by family firms may lead acquirers to assume the target is less likely to have forgone economic goals to preserve its SEW and, hence, to have less upward potential in the future. Thus, in H2, we expected family firm status’ positive effect on firm value in acquisitions to be weaker for targets with higher financial performance compared to targets with lower financial performance. We found empirical support for H2.

Concerning the second moderator—type of acquirer—we distinguish between financial and non-financial acquirers, and we assume financial acquirers interpret the family firm status signal more favorably due to their economically driven business model compared to non-financial acquirers that might instead consider non-economic objectives (e.g., securing long-term strategic assets). Thus, we expected in H3 that the family firm status signal would have a stronger effect on firm value for a financial acquirer compared to a non-financial one. However, our empirical results show the significant effect for non-financial acquirers is not a weaker, positive effect; in fact, the effect is negative. In contrast to financial acquirers, non-financial acquirers do not make acquisitions their core business. Hence, they might worry about being unable to exploit a target’s full potential because they lack the knowledge and experience to implement and execute post-deal measures effectively; therefore, non-financial acquirers might tend to pay lower prices. Moreover, in post-acquisition periods, problems often occur in terms of integrating the target into the acquirer’s institutional environment (e.g., clashing organizational cultures), resulting in additional downside effects for the firm value of family firm targets—especially for non-financial acquirers, for whom acquisitions are not “daily business.”

For the third moderator—listing status—research suggests that publicly listed firms must disclose information that may influence stakeholders’ decisions and that these firms also are subject to shareholder voice (e.g., Doshi et al., 2013). Private firms, in turn, are usually exempt from such requirements. Thus, acquirers might expect a private family firm to have a stronger focus on non-economic goals than a public one and might predict comparatively greater leverage in value creation with a private family firm target. Therefore, we expected in H4 that family firm status’ positive effect on firm value in acquisitions would be stronger for privately held targets compared to publicly listed ones. Interestingly, our empirical results show that the significant, positive interaction effect for family firms and public status was not weaker, as expected, but instead negative. This may be because post-deal measures in public family firms, which sometimes harm a target’s employees or a region (e.g., job losses because of relocating production to low-cost countries), may face stronger headwinds from minority or remaining family shareholders, as well as from politicians and the media. This makes turnaround and restructuring processes in publicly listed (former) family firms more difficult to implement.

Regarding the fourth moderator—industry relatedness—we distinguish between cross-industry acquirers and within-industry acquirers, and we argue that cross-industry acquirers are less capable of distinguishing between targets with “good” and “bad” prospects and that cross-industry acquirers face much greater uncertainty in assessing value-enhancing potential relative to within-industry acquirers. Therefore, we expected in H5 that family firm status’ positive effect on firm value in acquisitions would be stronger for cross-industry acquirers than for within-industry acquirers. However, our empirical results show that industry relatedness did not exert a statistically significant influence on the relationship between family firm status and firm value. This implies that industry relatedness might be less important than other factors, such as acquirers specializing in certain size classes of targets (Ahler et al., 2016).

In terms of the last moderator—geographic location—we distinguish between cross-border acquirers and domestic acquirers. Cross-border acquirers are usually less familiar with the institutional, cultural, and regulatory context relative to domestic acquirers (e.g., Westbrock et al., 2019). The physical distance that cross-border acquirers face might further increase the difficulty of overcoming information asymmetries (e.g., Capron & Shen, 2007). Thus, we expected in H6 that family firm status’ positive effect on firm value in acquisitions would be stronger for cross-border acquirers compared to domestic acquirers. Our empirical results show, however, that the significant effect for domestic acquirers is not positive but weaker; it is actually negative. This might be because domestic acquirers generally know more about their targets (e.g., their weaknesses, liquidity situation, and threats in the domestic market); hence, they have greater negotiating power to squeeze the acquisition price (i.e., firm value), especially when family firms need to sell because of a lack of successors. Furthermore, the effect could also be because families prefer selling to domestic acquirers to remain in contact with the firm they have sold. As a trade-off, the family might be willing to make sacrifices in terms of valuation.

Theoretical Contributions and Implications

We contribute to research on family firm valuation (e.g., Ahlers et al., 2014; Anderson & Reeb, 2003; Granata & Chirico, 2010; Villalonga & Amit, 2006) by showing that family firm value in acquisitions is driven not only by the characteristics of family firm targets (as proposed by prior studies), but also by the characteristics of outsiders such as acquirers, which have implications for the interpretation of the family firm value. Indeed, extant studies explain differences in family firm valuation mainly by focusing on family firm characteristics—particularly, how idiosyncratic family firm characteristics influence agency costs and, hence, family firm valuations (Anderson & Reeb, 2003; Eugster & Isakov, 2019; Isakov & Weisskopf, 2014; Villalonga & Amit, 2006). We extend the literature’s focus beyond solely considering family firm characteristics as the underlying reason for valuation discounts and premiums (e.g., Granata & Chirico, 2010; Villalonga & Amit, 2006) by including the role of acquirer characteristics that may alter how the family firm status signal is interpreted. We provide a new theoretical explanation of why different types of acquirers likely have different preferences depending on their business models and objectives (e.g., financial vs. non-financial acquirers). These preferences, in turn, alter the interpretation of family firm status. We further propose that the interpretation of the family firm status signal differs among acquirers according to their information asymmetry (i.e., cross-border vs. domestic acquirer). Extending our focus to acquirers’ characteristics as a factor affecting family firms’ value may help reconcile seemingly contradictory evidence in the existing research on family firm valuation, which has reported mixed results (thus far): For example, some studies have found that family firms are acquired at a discount (e.g., Granata & Chirico, 2010), and others have suggested that family firms are acquired at a premium (e.g., Gonenc et al., 2013). Our extended focus may further help to better understand the implications of “external” characteristics beyond the family firm and non-family firm status as characteristics of outsiders (e.g., Feldman et al., 2019; Haider et al., 2021), such as acquirer type and geographic location, for family firm valuation.

In addition, we contribute to the nascent research stream centered on family firms in the acquisition context (e.g., Feldman et al., 2019; Granata & Chirico, 2010; Haider et al., 2021; Zellweger et al., 2012) by providing a novel theoretical perspective—signaling theory—on the phenomenon. Despite its maturity (Spence, 1973) and fit for the acquisition context (Reuer et al., 2012), signaling theory had not been applied to the family firm acquisition context prior to this study. Previous studies have mostly relied on theoretical traditions—such as agency theory, the resource-based view, the stewardship versus stagnation perspective, and prospect theory—to study family firms in the acquisition context (e.g., Feldman et al., 2019; Granata & Chirico, 2010; Zellweger et al., 2012). By integrating the signaling theory perspective (Spence, 1973), we shed light on the mechanisms behind how acquirers evaluate family firm specifics. This perspective not only allows us to predict the family firm status signal’s general effect on firm value, but also to theorize how acquirers differently evaluate family firms with varying levels of performance or a different listing status (i.e., private vs. public).

We also advance the family firm research using the signaling theory as a theoretical basis (e.g., Schell et al., 2020; Schellong et al., 2019; Stutz et al., 2022) by introducing important contingency factors that influence the strength of the family firm status signal. To date, the family firm status signal has mainly been used to merely distinguish family firms from non-family firms (e.g., Botero, 2014; Schellong et al., 2019) or family firms with a family CEO from those without a family CEO (Sekerci et al., 2022). We have introduced important contingencies that offer a new foundation on which future theorizing can build by showing that the effectiveness of the family firm status signal may be influenced by signal fit (i.e., the financial performance of family firm acquisition targets), signal interpretation (i.e., different interpretations by different types of acquirers—financial vs. non-financial ones), and the degree of information asymmetry (i.e., privately held family firm targets vs. public family firm targets and cross-border acquirers vs. domestic acquirers). Hence, we expand the horizons of current theorizing on the signaling perspective in family firm research.

Practical Implications

Our study has practical implications both for family firm acquirers and for the owner-managers of family firm targets. Regarding the latter, owner families may consider the role of acquirer type when selling their businesses because the family firm status interpretations of different types of acquirers may affect the family firm’s value in a sale. Specifically, financial acquirers may be willing to pay higher prices for the family firm than non-financial acquirers (e.g., other established businesses) because they likely recognize the greater levers for economic value creation in the post-acquisition period due to their specific business model and objectives. However, compared to non-financial acquirers, financial acquirers may be more likely to jeopardize part or all of the SEW that owning families have built until the acquisition: for example, by revoking decisions that a family made based on their unique values. Selling owner families should, therefore, carefully consider what is important to them in a sale, including in terms of the future of the firm. Acquirers, in turn, might pay attention to how consistent their interpretation of the family firm status is with other signals (e.g., financial performance), as well as look closely at which factors caused the family firm’s (financially) “good” or “bad” situation. For example, it is important to assess what role the family plays in the business and what resources of the family firm would continue to add value in a post-family area. In some cases, it may seem right to involve the family in the post-acquisition period, such as on the firm’s advisory board. Thus, our study can help acquirers classify signals and categorically assess family firms as acquisition targets.

Limitations and Future Research

As with all research, our study has some limitations that offer interesting avenues for further research. For example, signal interpretation might depend on the cultural context (Botero, 2014). While our study is based on data from economically important European countries, our results might not be generalizable internationally. Hence, scholars might consider analyzing whether our theorizing and results vary across cultural or geographical contexts (e.g., Bruton et al., 2022).

In addition, family firm value in the acquisition context (i.e., the price acquirers pay for targets) may not be the sole result of acquirers’ expectations for a firm’s development; they may also be influenced by other factors, such as the negotiation skills of selling owner families and acquirers (Ahlers et al., 2016; Michel et al., 2020). Hence, we encourage future research to explore how differences in negotiation capabilities of family firm targets and different types of acquirers influence the prices paid for firms in acquisitions (e.g., by controlling for deal experience or putting the research focus on the negotiators). However, one might expect that financial acquirers are characterized by particularly salient negotiation skills; the fact that financial acquirers strengthen rather than weaken the effect of the family firm signal on firm value is a strong indication for the validity of our argumentation. Relatedly, despite controlling for several alternative explanations, we cannot fully rule out whether acquisition targets in the deal flow funnels of financial acquirers and non-financial acquirers differ because of potentially diverging deal sourcing strategies. Thus, future research could build on our work by analyzing this phenomenon in more detail using experiments or qualitative methods, such as case studies or interventionist research (Lukka & Wouters, 2022), to gain knowledge about the process of family firm value determination in the acquisition context.

Moreover, although the EV/EBITDA multiple is a well-accepted measure of firm value in research and practice (e.g., Asquith et al., 2005; Eaton et al., 2021; Gompers et al., 2016; Kaplan & Ruback, 1995; Liu et al., 2002), there are various alternative measures. To expand on our work, researchers could investigate how family firms and family-specific resources are viewed and evaluated by outsiders willing to take over and restructure the family firm resources in the event of insolvency or financial distress (Gómez-Mejia et al., 2023; King et al., 2022). In such situations, earnings are often negative, making the use of EV/EBITDA multiple inappropriate and requiring Tobin’s q because negative multiples would be meaningless to determine a firm’s value. In general, it would be interesting to learn whether other measures of firm value yield similar or different results in different contexts. Hence, we invite scholars to use additional firm valuation methodologies in their studies (e.g., discounted cash flow or Tobin’s q).

In addition, even though we included typical firm-level, deal-level, and context-level controls, we could not account for all potential control variables due to the limited data availability. Future research with broader data access might consider testing the robustness of our findings: for example, by capturing further negotiation-related controls (as we have briefly discussed) or by including governance-related variables, such as generation in charge or whether the family takes an active role in the firm after acquisition. With broader data access, it would also be interesting to study how acquirers’ activities after deal closure impact the acquisition targets’ firm performance and value over time (e.g., in holding periods of financial or non-financial acquirers). For instance, scholars might consider examining the value implications of private equity firms for family firms’ relative to non-family firms’ innovation or financial performance (e.g., Guderian et al., 2021; O’Boyle et al., 2012) in the post-acquisition period as well as exploring which family firm characteristics survive the sale of the owning family and under what conditions.

Finally, we suggest conducting research on how family firms can use family firm-specific signals such as family ownership and management in other settings outside of the acquisition context to not only help acquirers, but also other stakeholders to overcome information asymmetries. For example, our analyses focused on established family firms that have lasted for decades on average. It would be interesting to see whether the family firm signal spills over or holds true for family ventures started or financed by business families (e.g., Riar et al., 2022).

Conclusion

The evidence from prior research on family firm value in the acquisition context is both scarce and mixed. This is most likely because in prior research, often, only family firms’ characteristics have been scrutinized as an influencing factor for family firms’ value. Building on signaling theory, we have contributed to the debate on family firm value by considering the characteristics of both family firm targets and acquirers of family firms. It appears that we may be entering a new stage of development in research on family firm valuation that looks at factors beyond the family firm. This expanded view will allow for manifold interesting research endeavors.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.