Abstract

This study analyzes how family control influences firms’ acquisition activity using a socioemotional wealth (SEW) approach and discusses their anticipated SEW gains and losses when making acquisition decisions. Data collected from Spanish public companies from 2010 to 2015 indicates that family firms are more reticent about undertaking acquisitions than nonfamily firms, and their lower propensity is more pronounced when there are no former politicians on the board of directors whose presence could reduce potential SEW losses. Furthermore, the benefits of former politicians on the board of family firms in terms of acquisition activity only occur in low-velocity industries.

In the family business literature, the term socioemotional wealth (SEW) has become a central component of research analyzing a wide array of firm behaviors. At the time of this writing, the term “socioemotional wealth” produced an astounding 69,600 Google search results, which is even more impressive considering that the term first appeared in the literature approximately 15 years ago (Gómez-Mejía et al., 2007). SEW refers to the “non-financial aspects of the firm that meet the family’s affective needs, such as identity, the ability to exercise family influence, and the perpetuation of the family dynasty” (Gómez-Mejía et al., 2007, p. 106). SEW encompasses family control, family members’ identification with the firm, emotional attachment, binding social ties, and dynasty or transgenerational succession (Berrone et al., 2012; Chirico et al., 2020; Jiang et al., 2017; Swab et al., 2020). All these nonfinancial aspects embedded in SEW affect firms’ decision-making, as preserving SEW is of utmost importance for family firms (Gómez-Mejía et al., 2007).

This study analyzes the relationship between family firms and strategic decisions taken regarding the volume of acquisitions from a SEW approach. Most of the previous literature focused on family firms’ acquisitions has embraced the dominant economic perspective (De Cesari et al., 2016; Feldman et al., 2019). This perspective assumes that family firms’ risk aversion dissuades them from acquisitions (given the high probability of failure) because of their highly concentrated ownership and undiversified wealth (Caprio et al., 2011; Feldman et al., 2019), ignoring the presence of nonfinancial goals (Chrisman et al., 2012; Gomez-Mejia et al., 2018). Under the umbrella of prospect theory (Kahneman & Tversky, 1979; Tversky & Kahneman, 1992) and the behavioral agency model (BAM; Gomez-Mejia et al., 2021; Wiseman & Gomez-Mejia, 1998), other researchers have come to a similar conclusion but tend to emphasize nonfinancial arguments. According to these scholars, family firms exhibit a lower propensity toward acquisitions compared with nonfamily firms because of the SEW loss they often entail (Gomez-Mejia et al., 2018; Hussinger & Issah, 2019). From this perspective, acquisitions conducted by family firms should not be viewed as a choice between a clear loss and clear gain (i.e., a pure gamble) because these decisions potentially simultaneously entail losses and gains in both financial and SEW terms (Gomez-Mejia et al., 2014, 2018) known as a mixed-gamble scenario (Bromiley, 2010; Martin et al., 2013; Tversky & Kahneman, 1992).

Although some previous studies have examined the relationship between family firms and acquisitions from a SEW approach (see literature review), the question of how family firms may be able to shelter SEW from losses when acquiring has not been addressed. Using the FIBER model by Berrone et al. (2012), where FIBER refers to a set of five dimensions that capture SEW (Family control and influence, Identification of family members with the firm, Binding social ties, Emotional attachment of family members, and Renewal of family bonds to the firm through dynastic succession), we discuss theoretically why family firms overall may engage in a lower volume of acquisitions, how they may be able to use former politicians on their boards to help them acquire, and industry conditions that make the politicians’ role more salient in these endeavors.

Previous literature has discussed the role played by former politicians on boards (Hillman, 2005; Lester et al., 2008), suggesting that political connections can help firms better comprehend public policies and bureaucratic procedures (Agrawal & Knoeber, 2001; Goldman et al., 2009), achieve preferential treatment by the government and win government contracts, extract concessions, lower tax rates (Faccio, 2006), or gain access to capital from financial institutions (Khwaja & Mian, 2005; Yeh et al., 2013). In this research stream, some studies have analyzed the benefits of political connections in acquisitions and have suggested how they increase the likelihood to acquire targets (Arnoldi & Muratova, 2018; Ding et al., 2014; Ferris et al., 2016; Xu et al., 2015), the inclination toward cross-border acquisitions (Albino-Pimentel, Anand, & Dussage, 2018; Pinto et al., 2017; Tu et al., 2021), and the effects on merger premiums, announcement returns or post-merger financial and operating performance, among others (Bertrand et al., 2016; Bi & Wang, 2018; Brockman et al., 2013; Li et al., 2021; Schweizer et al., 2019; Yang & Zhang, 2015). All in all, the main object of these previous studies has been to provide empirical evidence on the effect that political connections have on acquisition propensity and its financial outcomes. A main contribution of our research is to extend this literature by considering how the presence of former politicians on the boards of family firms may be used as an instrument for them to overcome their reluctance to pursue acquisitions from a SEW perspective.

The analysis of political connections in family firms is especially important in the Spanish context for two reasons. First, the ownership structure in Spain is highly concentrated in the hands of families, and these core shareholders generally play an active role in their boards (Aguiar Díaz & Santana Martín, 2006; Cuervo, 2002; Faccio & Lang, 2002; La Porta et al., 1999; Ruiz-Mallorquí & Santana-Martín, 2011). Second, as a result of the massive privatization waves in Spain over the last few decades, CEOs and directors of many listed companies were appointed by the Spanish government (Bona-Sánchez et al., 2014; Cuevas-Rodríguez et al., 2007). Thus, although state ownership was completely sold off, the government still had a way to intervene and prevent, for example, foreign takeovers of firms by restricting voting rights and/or placing ceilings on ownership shares (golden shares). With such privileges, the Spanish government could preserve its political control over privatized firms, explaining the importance of governmental networks in Spanish board compositions (Farinós Viñas et al., 2016; García-Meca, 2016). More than 45% of Spanish-listed firms have politically connected boards (Bona-Sánchez et al., 2014). This government intervention and the importance of firms’ political connections deserves attention as it has been documented not only in Europe but in non-European countries such as China (Chen et al., 2011; Fan et al., 2007; Gao et al., 2019) and much of Latin America (Gomez-Mejia et al., in press)

Moreover, we go further and analyze the extent to which former politicians’ positive role in influencing family firms’ acquisition decisions is contingent on a third variable, the competitive industry’s velocity, defined by a change in industry population size (number of firms) in a given period (McCarthy et al., 2010). We suggest that high competitive velocity industries reduce the benefits that former politicians bring to the board, which leads to higher potential SEW losses and a lower tendency to acquire. To our knowledge, this important relationship (i.e., how competitive industry velocity affects the relationship among family firms, acquisitions, and former politicians on boards) has never been explored before.

The remainder of this article is organized as follows. The next section reviews related previous research. This leads to the hypotheses, followed by the methodology used for analysis. Results are presented in the next section, followed by the conclusion.

Literature Review and Hypotheses

Family-controlled firms, or businesses owned and managed by families, are prevalent worldwide (Chirico et al., 2020). Literature shows the growing attention that family business research has received more than the last two decades (Worek, 2017). Family firms’ SEW or “affect-related value embedded in the family firm” (Gómez-Mejía et al., 2007) manifests itself in a variety of differently related forms, which Berrone et al. (2012) define in the FIBER model in terms of five dimensions, as previously noted. While the exact number of SEW dimensions is still a subject of debate (Debicki et al., 2016; Hauck et al., 2016), empirically there is both indirect (Gomez-Mejia et al., 2011) and direct (Gomez-Mejia & Herrero, 2022) evidence that socioemotional wealth in its various forms plays a more important role in family-controlled firms.

The analysis of acquisitions in family firms from a SEW perspective has been addressed by different works. Hussinger and Issah (2019) and Gomez-Mejia et al. (2018) analyzed the predictions about the occurrence and relatedness of acquisitions in family firms. They showed that family businesses are hesitant to acquire firms because the hoped-for financial gains are uncertain, whereas the loss in SEW terms is certain. In addition, there is a preference for related targets when an acquisition occurs in family firms. Along the same line, and applying a more classical agency perspective, Miller et al. (2010) examined two characteristics of family firms’ acquisitions (their scale and their scope), arguing that the level of family ownership is associated with a smaller scale of acquisitions but also with the preference toward diversifying acquisitions to reduce business and portfolio risks. Boellis et al. (2016) suggest that risk aversion, SEW, and lack of information are why family firms present a higher propensity toward greenfield initiatives versus acquisitions when entering foreign markets. Patel and King (2016) examined whether the prospect of being acquired motivates family firms to engage in defensive acquisitions to mitigate the threat to their SEW. Comparing small-, medium-, and large-sized family firms, they conclude that mid-sized family firms are more attractive as takeover targets (as they provide a better balance between synergies and costs) and thus are more likely to acquire other firms. Other works have also studied how nonfinancial considerations, such as institutional environment, shape family firms’ SEW-oriented attitude (see King et al., 2022). For instance, some literature argues that family involvement’s negative impact on acquisition propensity (Requejo et al., 2018) or the acquiring shareholder valuation (Feito-Ruiz & Menéndez-Requejo, 2010) seems to be contingent on the legal system of the country (shareholders’ legal protection) where the family firm operates.

Recent research focuses on the heterogeneity of family firms (Chrisman et al., 2018; Chua et al., 2012; Daspit et al., 2021; Stockmans et al., 2010), emphasizing the importance of analyzing differences in their corporate governance. Accordingly, when considering family firms’ acquisitions, some researchers have analyzed the influence of the degree of family ownership (Diéguez-Soto et al., 2021), the level of family involvement in the top management team, or the family cycle stages (Schierstedt et al., 2020; Steen & Welch, 2006). Mariotti et al. (2021) suggest how important the presence of nonfamily board members is, in addition to the generation ruling the firm. Similarly, Chen et al. (2021) suggest that family firms’ international acquisitions should be understood and discussed in the context of different financial block holders. Pazzaglia et al. (2013) provide empirical evidence on how having a nonfamily CEO explains the differences in earning quality between acquired and nonacquired family firms. Other works have documented how not only the founder’s presence on the board (Bauguess & Stegemoller, 2008; Fuad et al., 2021) but also the differences in SEW between founder and descendant board chairs (Haider et al., 2021) impact the relationship between family control and acquisition decisions. All of these studies point to the heterogeneity among family firms when it comes to acquisition behavior.

Despite their contributions, the studies noted earlier have overlooked an essential dimension of family firm governance in many countries: the political profile of directors who sit on their boards. Research on non-market strategies has long argued that, in addition to developing competitive behaviors guided by market principals, firms can also engage with non-market actors, notably governments, to better achieve their objectives (for recent reviews, see Dorobantu et al., 2017 and Sun et al., 2021).

Next, we address the issue of why family firms are likely to engage in a lower volume of acquisitions, leading to our first baseline hypothesis, to be followed by hypotheses concerning the positive role of former politicians in reversing that stance (our second hypotheses) and how high industry velocity mitigates former politicians’ positive role in this regard (our third hypotheses).

Family Control and Volume of Acquisitions

A mixed gamble is a situation with the potential for both gain and loss outcomes as opposed to a pure gamble, which has the potential for either loss outcomes or gain outcomes but not both (Bromiley, 2009, 2010; Levy, 1992; Martin et al., 2013). According to prospect theory, where the mixed-gamble concept is anchored, loss aversion makes decision makers attach greater weight to an asset’s loss than to a financially equivalent gain (Kahneman & Tversky, 1979; Tversky & Kahneman, 1986, 1991). That is, losses are weighed more heavily than gains when individuals consider the consequences of their gamble, an idea that was incorporated in further refinements of the behavioral agency model or BAM originally developed by Gomez-Mejia et al. (2001) and Wiseman and Gomez-Mejia (1998).

More recently, Gomez-Mejia et al. (2014) introduced the notion of mixed gambles into the family business literature to explore how subjective estimations of potential losses and gains in firm risk (in their study measured by R and D investments) are likely to differ for decision makers in family versus non-family firms. This mixed-gamble logic was extended by Gomez-Mejia et al. (2018) in a subsequent article focused on differences in acquisition activities between family and non-family firms. Using a similar mixed-gamble perspective, two recent studies examined differences between family and non-family firms on internationalization (Alessandri et al., 2018) and tax evasion (Eddleston & Mulki, 2021). According to BAM, decision makers frame problems using a reference point to compare anticipated outcomes from available options, and this leads to loss avoidance even if it means accepting a higher risk (Gomez-Mejia et al., 2000; Wiseman & Gomez-Mejia, 1998). Derived from this BAM’s logic, family-owned firms are likely to be loss averse with respect to SEW (their primary reference point) and are risk willing when it comes to tolerating performance hazards (i.e., probability of failure and below-target performance) to preserve that wealth (Gomez-Mejia et al., in press). Hence, when family firms choose between an action that would confer gains (but a subsequent reduction of SEW) and an alternative action that would protect SEW (but with uncertain economic benefits), they would tend to favor the latter.

There is some debate among family business scholars about whether and how the five SEW dimensions of FIBER (conceptually derived by Berrone et al., 2012) are empirically distinct (see Gomez-Mejia & Herrero, 2022). With that caveat in mind, the five-dimension FIBER model still offers an overarching scheme that captures the major elements of SEW as inferred from the broad family business literature. Using FIBER as an analytical tool, we next explore how SEW protection is likely to depress acquisition volume in family-controlled firms (our first hypothesis).

Family Control

Acquisitions often require external financing that weakens family control and independence (first dimension of the FIBER model). Steijvers and Voordeckers (2009) explain financing policies in private family firms considering interest rate and business collateral as well as personal collateral requirements. Boellis et al. (2016) suggest that family businesses are caught between two alternatives (debt or cash financing), both of which can have undesirable consequences when facing the opportunity to acquire a firm. For instance, debt-financed acquisitions can increase financial leverage, financial distress, and the risk of bankruptcy, while cash-financed acquisitions by family firms would imply a high probability of unwelcome future sales of new equity needed to overweight the cash takeover (Furfine & Rosen, 2011; Martynova & Renneboog, 2009; Santos et al., 2014). Finally, Caprio et al. (2011) suggest family firms are particularly reluctant to make acquisitions when the stake held by the family is not large enough to guarantee control after the transaction. These authors point out the importance of analyzing firms’ ownership structure and the use of control-enhancing devices such as dual-class shares and pyramids in acquisition decisions. The latter devices are commonly used across Continental Europe and are well represented in the ownership structures of Spanish family firms (Sacristán-Navarro & Gómez-Ansón, 2007). Pyramidal structures refer to the situation in which a dominant shareholder owns a significant fraction of a firm that owns a significant fraction of another firm and so on. By using pyramids, a large shareholder can exercise control over a firm through a chain of intermediate firms (thanks to their voting rights) and exceeding their cash-flow rights (Faccio & Lang, 2002; La Porta et al., 1999). Thus, pyramidal structures enable founders of family firms to retain a lock on control and dictate corporate policies or install family members as CEOs (Jara et al., 2021), while the remaining shareholders may lack the power or the incentives to oppose the families’ decisions (Bennedsen & Wolfenzon, 2000).

Family Identification

Acquisitions can enhance SEW in family firms by strengthening family identity and family brand, especially in related acquisitions (Gomez-Mejia et al., 2018). Indeed, the identity of a family firm’s owner is inextricably tied to the business that usually carries the family’s name (Berrone et al., 2010), which makes these owners to see the business as an extension of the family itself (Christensen-Salem et al., 2021). With such heightened identification of family owners with the firm, family members are motivated to pursue a favorable reputation because it allows them to feel good about themselves (Deephouse & Jaskiewicz, 2013). Along this line, Maran and Parker (2021) provide empirical evidence that acquisitions in family firms are driven to reinforce brand reputation and that financial and accounting motivations have only marginal importance.

Binding Social Ties

Among the drawbacks that acquisitions could imply for family firms’ SEW endowment is damage to the family’s social network or binding social ties. Family owners are often deeply embedded in their local area, are active participants in community associations, and tend to develop extended relationships with entities that interact with the firm (Astrachan, 1988; Berrone et al., 2010; Lester & Cannella, 2006). Acquisitions may require access to unknown suppliers and clients, as well as dependence on experts and consultants from outside the family core, which could weaken family owners and executives’ established interpersonal grid.

Emotional Attachment

Acquisitions could imply some potential pitfalls, as problems of integration and distinct culture may appear with the acquired firm or duplication of processes that often require reorganization, demotions, and job cuts may be present (Vaara et al., 2012), creating emotional distress for the people involved (King et al., 2022). Because family-controlled firms have an emotional attachment for their core business, technologies, and products (Gomez-Mejia et al., 2010), Kim et al. (2020) suggest that they are more likely to possess a culture of “place-basedness” by transferring family values to the organization. However, it may not be possible to align the family culture with the target’s corporate culture in the acquisition context. Along the same line, analyzing the family firms’ establishment mode choice in foreign markets, Boellis et al. (2016) conclude that although acquisitions constitute the quicker way to grow, the choice of greenfield venture (vs. acquisitions) allows a family firm to replicate the existing organizational structure and reduce costly and risky integration with a foreign company. In short, the disruption of existing routines due to integration processes between the target and the acquirer could imply emotional turmoil and thus SEW losses. However, Hussinger and Issah (2019) recognize the possibility of SEW gains for family firms when making specific acquisitions (related ones). The affect and emotional attachment to the core business shown by family members could be strengthened through related acquisitions as family firms “stick to what is dear to their heart” (Hussinger & Issah, 2019, p. 358). Indeed, related acquisitions can allow family firms to benefit from synergies and complementarities of their own assets, to apply their accumulated experience to the acquired firm, and to preserve their age-old established knowledge (Davila et al., in press; Duran et al., 2016).

Family Dynasty

Acquisitions can help overcome market entry barriers and gain competencies and resources that firms do not hold currently, thus contributing to their long-term survival and competitive advantage (Fuad et al., 2021; Steen & Welch, 2006). In terms of SEW, family owners want their business to survive and be passed onto future generations (Miller & Le Breton-Miller, 2014). So, acquisitions could be a strategy to ensure business continuity (Gu et al., 2019) and transgenerational sustainability, key elements of dynastic motive under the SEW umbrella. However, we also acknowledge evidence that acquisitions are very risky, with most acquisitions ending in failure, particularly unrelated ones (Hitt et al., 2001; Uhlenbruck et al., 2006). Because of the risks involved, investments in acquisitions could be a roadblock to ensuring firm survival, especially in foreign acquisitions (Gu et al., 2019) endangering renewal of family bonds to the firm through dynastic succession (Berrone et al., 2012).

Based on the arguments and empirical research noted earlier, the mixed gamble facing family firms in regard to acquisitions is biased toward the domain of losses. This is because the dimensions of the family’s SEW that are hampered by acquisitions outweigh potential prospective gains that may be derived from this strategic endeavor. Hence, expected losses in firm-embedded SEW elements would make family firms more reticent to acquire than non-family firms. This leads to the baseline premise of our model, namely that there is a direct and negative relationship between family control and volume of acquisitions:

The Moderating Role of Former Politicians on Boards

Previous research has argued that firms with political engagement can benefit when making strategic decisions (Baron & Hall, 2003; Bonardi, 2011; Bonardi et al., 2006; Boubakri et al., 2013; Mellahi et al., 2015) through two types of non-market capabilities (Albino-Pimentel, Dussauge, & Shaver, 2018): (1) firm political competence in terms of accumulation of experience in dealing with political authorities. Political competence allows firms to anticipate nonbeneficial government regulations and prevent them or, at least, minimize the effects on their own interest (Bonardi et al., 2006) and (2) firm political connections deriving from social ties with high-ranking government officials (Berrone et al., in press). With such relationships, firms may gain power and authority, feel more confident, and have government authorities intervene on their behalf. This is consistent with prior research on the benefits obtained by firms with political connections in cross-border acquisitions (Frynas et al., 2006; Schweizer et al., 2019) or being less sensitive to risk in their investments (Boubakri et al., 2013; Chen et al., 2010).

Based on the literature, we suggest that family firms can develop non-market strategies and derive benefits of having former politicians on boards in acquisition decisions. More specifically, we propose that former politicians on boards moderate the relationship between family control and volume of acquisitions. Politicians serve to cushion firm risk and thus allow the family to engage in bigger acquisitions as they are likely to increase (decrease) the weight given to potential SEW gains (SEW losses), particularly those related to family control. That is, the beneficial effects of politicians on boards may be higher for family firms, overcoming the “SEW inertia” that purportedly depresses family firm acquisitions.

Acquisitions generally demand external financing. Former politicians on boards can help firms obtain better deals in bank loans and fiscal support (Herrera-Echeverri et al., 2016; Khwaja & Mian, 2005; Peng, 2003) because they increase both the firm’s legitimacy (Hillman, 2005) and its reputation for strength, reliability, and credibility. Some researchers argue that former politicians on boards help firms obtain preferential interest treatment (Faccio, 2006, 2010) and, in some extreme situations, bailouts (Faccio et al., 2006). Although these benefits equally apply to non-family and family firms, they are especially critical for the latter in acquisition contexts. Croci et al. (2019), Anderson and Reeb (2003), and Ellul (2008) have documented that debt financing is the most favorable choice in family firms who avoid equity financing because of fear of diluting or relinquishing the family’s ownership concentration. Access to better external financing conditions (mediated by former politicians) could guarantee family control and preserve the SEW endowment. Indeed, SEW is feasible only with family control because this is an enabling condition for the family to enjoy other SEW utilities (Gomez-Mejia & Herrero, 2022; Gómez-Mejía et al., 2007).

As discussed in the previous section, cultural and structural difficulties can appear in the acquisition process, resulting in the need to reorganize the acquired company, which may provoke emotional upheaval (Vaara et al., 2012). Family firms could be more prone to acquire when they anticipate the potential help that former politicians could provide to solve such integration problems. A related potential spillover effect may be the need to engage in demotions and job cuts if the integration process results in resource redundancies, which would tend to tarnish the family’s image and, thus, SEW. Having former politicians on board may serve to smooth out this integration (for instance, by spreading it over time or securing government assistance to absorb any pain felt by employees).

Finally, acquisitions may require the firm to come in contact with a new unfamiliar external environment and personnel (Cruz et al., 2010; Hitt et al., 2001). Former politicians may provide family firms with better access to these outsiders, thus expanding their social ties into unknown territory (Bona-Sánchez et al., 2019). These social ties can be particularly helpful for some acquisitions, especially international acquisitions, where family firms encounter considerable environmental uncertainty requiring contact with new governments and need information about local regulations (Albino-Pimentel et al., 2018). Former politicians in family firms would reduce information asymmetry between the firm and the new government, improving their engagement in private communication (Ferris et al., 2016; Li et al., 2008; Wang et al., 2016; Xu et al., 2013). Taken as a whole, all of the benefits accrued by having former politicians on the board may reduce firm risk and thus help the firm survive for future generations. Hayward et al. (2022) use the term “family vulnerability” to explain the importance of family firms’ relationships with external resource providers such as suppliers, clients, and other organizations, and former politicians may shelter some of that vulnerability.

Considering all the factors noted above, we propose that the potential benefits and SEW gains derived from acquisitions are amplified in family firms with former politicians on the board:

Competitive Industry Velocity

As argued in the preceding hypothesis, former politicians are especially valuable in acquisition processes for family firms, more so than for non-family firms. However, the benefits for family firms of having former politicians on board are expected to atrophy over time in high-velocity industries where many changes in competitive actors are produced (Eisenhardt, 1989). Indeed, high competitive industry velocity demands both comprehensiveness and speed in making strategic choices (Talaulicar et al., 2005). Comprehensiveness, referred to as the degree to which a choice is based on a thorough problem analysis, is important for selecting the right target in acquisition contexts, the time of acquisition, and to assure strategic fit between the acquirer and target (Angwin & Meadows, 2015). As comprehensiveness implies extensive analysis, it usually takes time and reduces the speed of decision-making. Despite this fact, speed is critical in high-velocity environments where competitiveness (due to the entry of new companies) is also high. That is, strategic decisions should be made in a timely manner (decision speed) because delays under high competitive industry velocity can be detrimental (Eisenhardt, 1989).

In other words, former politicians’ ability to access current politicians and acquire updated knowledge is severely reduced over time, and the information they can provide to family owners will be less accurate, unavailable, or obsolete in high competitive velocity industries. In addition, although politicians would have the documented power accrued to those in central network positions in a community of elites, they could restrict information flow (Pettigrew, 1973). This argument is closely aligned with the idea of power suggested by Freeman (1978). The individual who is between other actors has more control over information flow from one sector of the network to another. That person (politician) becomes a gatekeeper of information flow. Such restrictions are particularly problematic in high competitive velocity environments where strategic decisions, such as acquisitions, must be made quickly and with very limited information (Bourgeois & Eisenhardt, 1988). In such settings, where competition is fierce, a premium is placed on timely and accurate data. However, politicians, by their very nature tend to suffer from ideological rigidity and myopic personal and political goals (Clarke et al., 2005; Gao et al., 2019), limiting their value in securing and accurately interpreting environmental cues (Pettigrew, 1973). We argue that the critical help that politicians can provide family firms to cope with their vulnerability and dependence on external resources decreases in high competitive velocity environments because of the required comprehensiveness and speed in making strategic choices.

Because of their vulnerability, family firms are more dependent on former politicians to protect them from harm. Therefore, it is reasonable to expect that the SEW benefits of political embeddedness in acquisitions for family firms proposed by Hypothesis 2 decrease when the firms operate in high competitive velocity environments. Based on the arguments above, we propose the following hypothesis:

Method

Sample and Data Collection

The data sample consisted of a number of publicly held Spanish companies that were quoted during the period of 2010 to 2015. This particular five-year period allows us to work with data from before the reform of the General Accounting Plan was introduced in 2016, as the plan introduced major changes in government regulations (Royal Decree 602/2016). We acknowledge the limitation that our study only selected the boards of directors of large Spanish companies quoted on the stock exchange given that these firms are only a fraction of the total number of Spanish firms. However, they were chosen due to their obligation to publish data related to corporate governance and performance (Pérez-Calero et al., 2015).

To obtain the sample of firms in our study, we started with a total population of 176 large firms quoted in the Spanish Stock Exchange by capitalization for the period of 2010 to 2015. A data-cleaning process was subsequently carried out to include only those firms that were both listed in at least two consecutive years of the study period and had complete publicly accessible data. As a result, we obtained an unbalanced panel of 150 firms with 831 firm-year observations. The sample is representative of the total population, as the 150 firms represent 85.2% of the total sample.

Dependent Variable

The volume of acquisitions was measured by the log of the value of all acquisitions made by the company in a given year (Chen et al., 2016; Gamache & McNamara, 2019; Gamache et al., 2015; Miller et al., 2010). The deal value of each operation was calculated by multiplying the price paid per target share by the number of shares purchased (Goranova et al., 2017; Haunschild, 1993). Of the total 150 companies, 76 made 280 acquisitions during the period of 2010 to 2015. We excluded acquisitions such as institutional buyouts, mergers, joint ventures, and share buybacks (Gomez-Mejia et al., 2018). To omit trivial transactions, we included only those acquisitions that involved at least 5% of the ownership of a target company (minority stakes), where the deal was valued at 1€ million or more (Miller et al., 2010). Finally, we eliminated those acquisitions that lacked information about the percentage of the acquired stake or deal value. The information was taken from the ORBIS database.

Independent Variables

Following the proposal of the European Family Business Group and the board of the Family Business Network, we considered a firm to be family-controlled when a single person or family held more than 5% (individually) or 25% (family group) of the firm with at least one family member as the director. We assigned values of 1 and 0, respectively, for family and non-family businesses (Anderson & Reeb, 2004; Fuad et al., 2021; Haider et al., 2021; Yang et al., 2020). The 5% cutoff should be interpreted in light of a long stream of research on the control of large publicly traded firms’ reporting requirements that use a 5% ownership threshold as a conventional proxy for a principal’s capacity to exert major influence over the firm’s affairs (Feldman et al., 2016; Gomez-Mejia et al., 1987, 2018; Tosi & Gomez-Mejia, 1989). This measure is better than that used in studies that examine only family ownership (Anderson & Reeb, 2003; Berrone et al., 2010), as it captures both family ownership and family involvement (Chrisman & Patel, 2012; Patel & Chrisman, 2014).

We used the SABI database (a broader version of Amadeus for Spain and Portugal, distributed by Bureau van Dijk, which provides online information on over 850,000 Spanish firms, taken from the annual reports lodged with the Mercantile Registers), which provides information about each of the company’s stakeholders, including the percentage of ownership at the end of each study year. In the first search, we identified those stakeholders that were individuals or families. To this end, SABI classifies stakeholders into the following categories: (A) insurances, (B) banks, (C) industrial companies, (E) mutual and pension funds, (F) financial companies, (I) one or more physical persons or families, (J) foundations/research institutes, and (S) public authorities/states/governments. Therefore, we kept those stakeholders included in the “I” category. Then, the companies were classified into family and non-family firms, based on the ownership structure and family members’ participation on the board. Company classification using SABI or Amadeus has already been used in previous studies in Spain (Rojo-Ramírez et al., 2011) and internationally (Diéguez-Soto et al., 2014; Frank et al., 2011; Pindado & Requejo, 2015).

To identify the members of the same family in the Spanish context, every person has two surnames: The first surname is inherited from the father and the second surname is inherited from the mother. Unlike in other contexts, this greatly facilitates the identification of the members of a single family, including an endless number of generations in the case of men and up to the third generation in the case of women (Gomez-Mejia et al., 2001). Moreover, the existence of two surnames allows finding siblings, cousins, and nephews/nieces with a lower error rate. In addition, the children of female board members are easily identifiable, as their second surname is their mother’s first surname (Sacristán-Navarro et al., 2011).

The term “politicians on board” (Bona-Sánchez et al., 2014; Hillman, 2005) is used to measure the existence of directors with political experience on the board of each acquirer firm, and it is measured as a dummy variable that takes the value of 1 if at least one of the directors has held a political position in the past; otherwise, this variable is assigned a value of 0 (Bona-Sánchez et al., 2014; Lester et al., 2008). Spanish incompatibility norms prohibit active politicians from holding corporate directorships. There is a formal prohibition against public officials holding firms’ directorships while serving in office (Pascual-Fuster & Crespí-Cladera, 2018). A former politician can only join a board of directors after a minimum period of two years without occupying a political position (normative). Therefore, following previous studies in Spanish (Bona-Sánchez et al., 2014; Pascual-Fuster & Crespí-Cladera, 2018) and other contexts (El Nayal et al., 2021; Goldman et al., 2009; Lester et al., 2008), we analyzed political connections in the form of former politicians on firms’ boards of directors.

The companies’ boards were examined for directors with political (elected or appointed) experience at the regional, national, or European levels. We first created a database of former politicians with the names of all politicians for the period of 1975 to 2012. We started in 1975, at the time of Spain’s transition (after the death of Generalissimo Francisco Franco) to democracy. We downloaded the information from different websites: the European parliaments, other foreign parliaments, the Spanish parliament, Senate, central government (prime minister, government ministers, and state secretaries), and regional parliaments in Spain for the abovementioned period of 1975 to 2012. We also contacted the Moncloa (equivalent to the White House in the United States) press department to obtain additional information about the list of Secretaries of State and Ministers. The result was a database of former politicians with names, surnames, political party affiliations, dates of appointment, and dates of end of appointment.

We then identified the names of all board members of the firms included in the sample for the period of 2010 to 2015. To obtain this information, we downloaded every individual Corporate Annual Report for each firm for each year from Comisión Nacional del Mercado de Valores (CNMV). These reports include external data about the firm’s corporate government, including board members and their education, former employment, and interlocks. This second database includes information about each firm’s board members for each year of our sample.

After creating the two individual-level databases (former politicians and members of the board), we performed an automatic matching process with both datasets and compiled a list of board members who had also been elected as political representatives. We completed this information with news articles about relevant political appointments in large Spanish firms, as gathering information about local (city) governments was beyond the scope of our research. The individual information about board experience in politics was added at the board/company level.

Finally, we measured the competitive industry velocity of the target firms using the number of new companies that entered the industry annually. Industry velocity is a source of environmental or competitive uncertainty (Bourgeois & Eisenhardt, 1988; Pfeffer & Salancik, 1978), as some industries are more attractive to acquirers than others. This measure has already been proposed in previous work as a change in industry population size (number of firms) in a given period (McCarthy et al., 2010). To calculate the variable, we first obtained the primary four-digit NACE codes (statistical classification of economic activities) for all the target firms in our sample.Then, we obtained the entire list of companies in each of those industries, using the SABI database (Iberian Balance Analysis System). Finally, we filtered the groups of firms in each industry by their date of constitution to determine which of them had entered each sector and when.

Control Variables

Referring to previous studies on corporate governance, we included the following control variables that might affect the proposed relations. To control for firm-level tendencies to acquire, we used the variables firm size, firm performance, and previous acquisition activity. Firm size was measured using the log of the number of employees in each acquirer firm for a given year (Revilla et al., 2016; Strike et al., 2015; Vandekerkhof et al., 2015), which could represent a firm’s ability to undertake acquisitions (Gamache et al., 2015). Firm performance was measured using Tobin’s q of the acquirer firms (Shim & Okamuro, 2011). Finally, as learning effects may affect acquisitions (Gomez-Mejia et al., 2018; Haunschild & Beckman, 1998), we controlled for the likelihood of acquisition in the previous year, which was coded as 1 if there was one or more acquisitions in the previous year and 0 otherwise.

We also included CEO and board-level characteristics of the acquirer firms that can influence the acquisition volume, such as the percentage of non-executive directors (Cai & Sevilir, 2012), calculated as the sum of non-executive directors on each board divided by the total number of board members, and CEO tenure, measured as the number of years the CEO has been at the helm of the organization (Salancik & Pfeffer, 1980). Existing evidence indicates that board independence increases directors’ capacities to influence firms’ strategic decisions, including acquisition decisions (Datta et al., 2009; McDonald et al., 2008). A greater proportion of outside directors on a board expands the base of expertise in the formulation of critical strategic decisions (Zahra, 1996), suggesting that firms with high percentages of outside directors are likely to be more confident in undertaking more acquisitions (Datta et al., 2009). CEO tenure has also been argued to influence acquisition decisions (Graffin et al., 2016; Jung & Shin, 2019; Pavićević & Keil, 2021; Walters et al., 2007). Long-tenure CEOs, who have more firm-specific human capital than newly hired CEOs (Gounopoulos et al., 2021), increase the likelihood of making well-informed acquisition judgments that positively affect firms’ acquisition propensity.

Given that several theories on acquisitions have proposed that industry conditions affect acquisition activity (Haunschild & Beckman, 1998), we controlled for two industry variables. First, to control for synergies between the acquirer and the target firms, we used the diversifying level variable, measured as the sum of the squares of the percentage of sales in each four-digit Standard Industrial Classification segment (Hitt et al., 1997). When the business activities of the acquiring and target firms are similar, the acquirer will be prone to acquiring new firms. Second, as different sectors vary considerably in terms of operational and strategic goals (Gomez-Mejia et al., 2018), we controlled for industry effect using industry dummy variables according to the codes of the Spanish Classification of Economic Activities (CNAE).

We also identified outside blockholders, measured as the sum of shareholdings by individuals or institutions that control more than 5% of the total shares (Shim & Okamuro, 2011). We controlled for the capital intensity ratio, measured as the natural logarithm of total assets divided by total sales (Iyer & Miller, 2008). Third, to control for the year effect, we included a dummy variable for the year in which the acquisition took place (Haunschild, 1994; Haunschild & Beckman, 1998). Finally, different sources were used to gather these variables, including corporate governance annual reports as well as SABI and Thomson Reuters Eikon databases.

Analytic Technique

The dependent variable, volume of acquisitions, is a continuous variable with a large proportion of 0, in such a way that its distribution is clearly right-skewed. For that reason, despite using the log-transformed variable (Gamache & McNamara, 2019; Gamache et al., 2015), the literature suggests a two-part model. Such models comprise a mixture of two parts (Boulton & Williford, 2018). The first step in implementing a two-part model is to create two new variables from the outcome variable: (a) a binary variable indicating whether an observation has a zero or a non-zero value (i.e., whether the firm makes acquisitions or not), and (b) a continuous variable containing only the non-zero values. Values of zero on the original outcome are considered missing on this new variable (log of the total value for firms that made acquisitions). In determining the specification of the model, we considered the panel structure of our dataset so that we estimated a two-part model using a random-effects probit regression for the binary variable and random-effects Generalized Last Squares (GLS) regression for the continuous variable. The results obtained for both the fixed and random effect models were consistent and the Hausman test showed that the estimators for the random effects were not only consistent but also more efficient.

The first part of our model thus predicts the probability of a firm engaging in acquisition(s):

Then,

where X is a matrix of explanatory variables, θ is a vector of variable coefficients and G(·) is the probit function. The model is estimated on the full sample. Now, for firms making acquisitions, the following equation determines the volume of the acquisitions:

where X is a matrix of explanatory variables and β is a vector of variable coefficients. This second part is conditional on Y > 0; as a consequence, it is estimated on the sample of non-zero observations using a random-effects GLS regression. This model explains how the explanatory variables affect the volume of acquisition.

While we use this methodology to test our first and second hypothesis, to test third hypothesis we use only a model using random-effects GLS regression. That is because the competitive industry velocity of target firms (moderator variable) is only a characteristic of firms that make acquisitions, not those who do not, and therefore should only be studied in that subsample.

Endogeneity Issue

Family business research might be particularly vulnerable to endogeneity problems (Zhang et al., 2022). In this study, the potential for endogeneity could be due to the effect of simultaneous causality or the omission of important possible variables (Hermalin & Weisbach, 1998, 2003). Some firms may engage in acquisitions, not because of higher family control but because of unobserved variables influencing both family control and acquisitions. Thus, and although endogeneity could be a problem, there is no evidence for it in this case. The correlations between the family control variable and the residuals of the regression are not significant (Bascle, 2008; corr = –.06). This implies that endogeneity is not a concern in our study.

Nevertheless, to confirm or reject the theoretical predictions that there is an endogeneity issue with the family control acquisitions, we used a Hausman test (Greene, 2000), performing a two-stage analytical procedure. First (Model 0), we regressed family control on two instrumental variables theoretically associated with family control: (a) the number of family firms in the firm’s location and (b) the number of family firms in the firm’s industry (Chirico et al., 2018). For the first variable, information was obtained about the autonomous community where the company was registered. Then, we gathered information about the number of family firms in each Spanish autonomous community using a report published by the Spanish Institute of Family Companies (2015). Similarly, for the second variable, we obtained each firm’s classification according to the CNMV, we used the same report to obtain the number of family companies in each activity sector.

We verified that neither of the instrumental variables was correlated with acquisition volume, although they were correlated with family control (–.10** and .11** for the number of family firms in the firm’s location and the number of family firms in the firm’s industry, respectively). The residual (λ) obtained from the equation (Model 0) was included as additional explanatory variables in the subsequent models (1–7). The residuals of Model 0 were not significant for any of the models, suggesting that our results are not affected by problems of endogeneity in these cases. Moreover, we conducted a Durbin-Wu-Hausman test, which failed to find a systematic difference across coefficients when endogeneity controls were included, further limiting the likelihood that endogeneity biased our reported results (p value of .18).

Finally, to test for endogeneity we also estimated a regression model via two-stage least squares (2SLS) using the predicted variable of family control as our instrumental variables. We verified the relevance and exogeneity of the instrumental variables (Bascle, 2008; Semadeni et al., 2014). The instrument relevance requires a strong fit between the endogenous regressor and the instruments (Bascle, 2008). We analyzed the relevance of the two instruments using the Stock–Yogo test, whose results reduced concerns about the weakness of the instruments (the F statistic was equal to 10.126; thus, we feel comfortable rejecting the null hypothesis of weak instruments). The condition of exogeneity implies that instruments are not correlated with the error term of the structural equation. We analyzed the exogeneity of the instruments using Hansen’s (1982) J statistic, whose results indicated that the instruments could be considered exogenous (p value of .63). Again, the results of the Davidson-MacKinnon test (F statistics of 1.494 and p value of .16) (Davidson & McKinnon, 1993) and Hausman test 1 (χ2 of 3.04 and p value of .9316) indicate that endogeneity is not a concern in our study and that our GLS results were robust.

Results

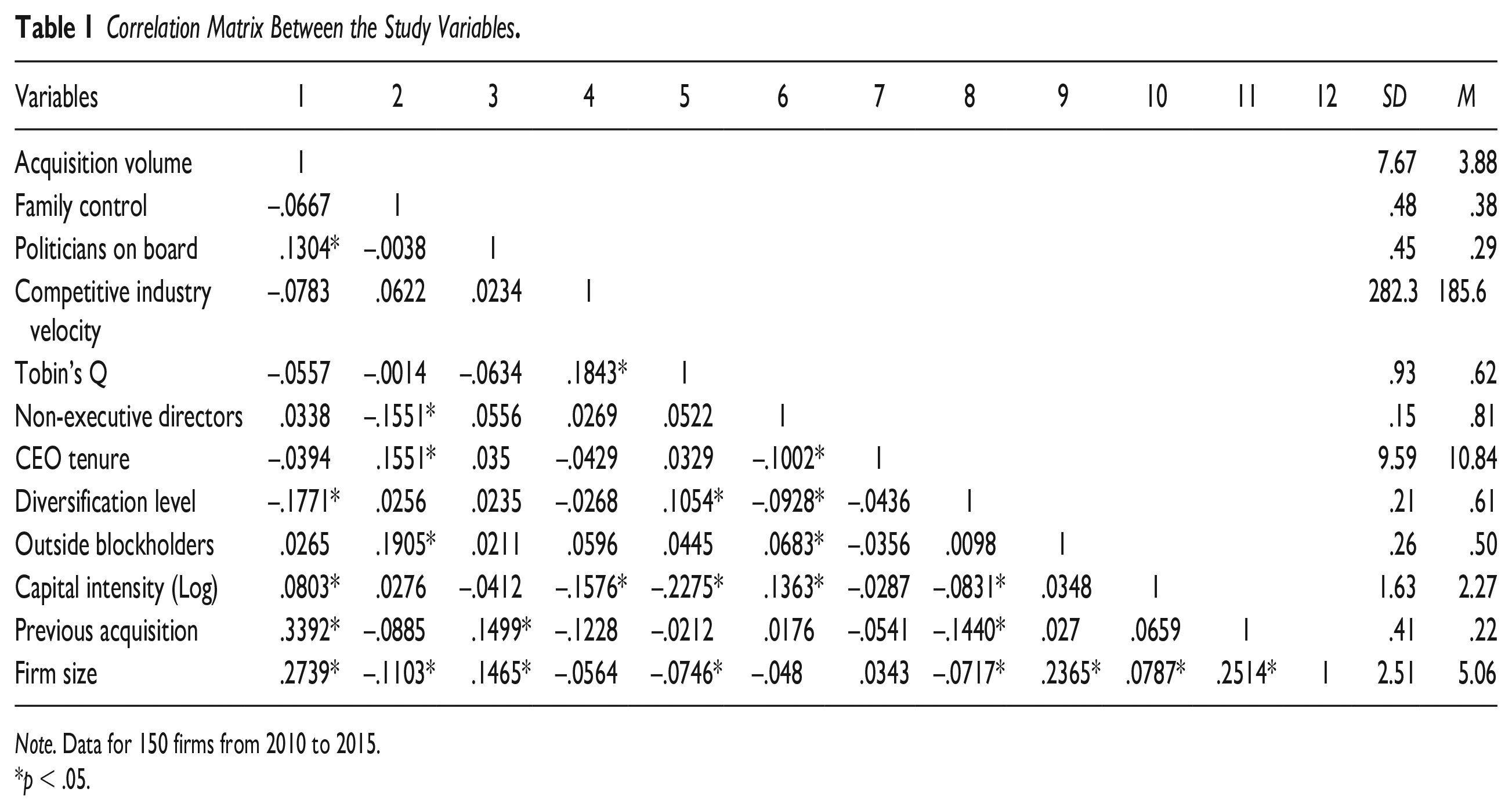

Table 1 summarizes the descriptive statistics of the study variables and the correlation matrix between the variables. All variance inflation factors (VIFs) are substantially lower than 2 (average VIF of 1.49), suggesting that multicollinearity does not pose any problems.

Correlation Matrix Between the Study Variables.

Note. Data for 150 firms from 2010 to 2015.

p < .05.

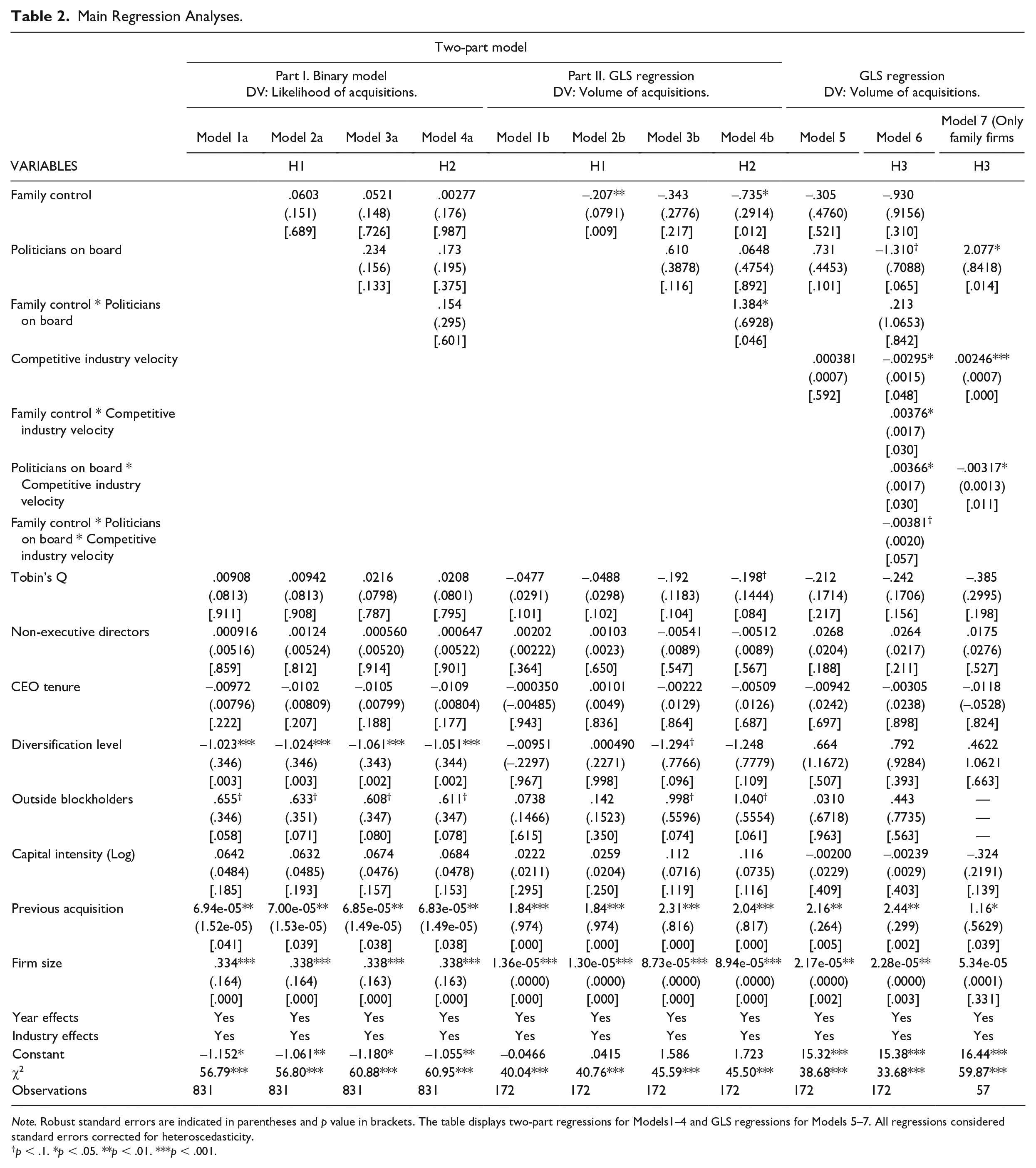

In Table 2, we present the results of the two-part model (Models 1–4) and GLS regression (Models 5–7). As previously mentioned, we use two-part model to test the first and second hypotheses and GLS regression to test the third hypothesis.

Main Regression Analyses.

Note. Robust standard errors are indicated in parentheses and p value in brackets. The table displays two-part regressions for Models1–4 and GLS regressions for Models 5–7. All regressions considered standard errors corrected for heteroscedasticity.

In Models 1a to 4a we show the result of the probit regressions that represent the first part of the two-part model. Meanwhile, in Models 1b to 4b, we show the results of the GLS random-effects regressions that represent the second part of the two-part model. Being aware that there may be different behaviors between companies that make acquisitions and those which do not, the first stage of the model shows that there are no differences between the families that make acquisitions and those that do not. Therefore, we discuss the second part of our model (columns b) as it tests the hypothesized effects that are focused on in this study (Grossman et al., 2012).

There was an increase in significance across models, and the joint significance test of the explanatory variables showed the variables that were significantly different from 0 in all models.

Baseline Hypothesis 1 predicted a negative relationship between family control and volume of acquisitions. Model 2b shows that the coefficient is highly significant and negative (B = –.21, p < .01). Therefore, Hypothesis 1 is supported.

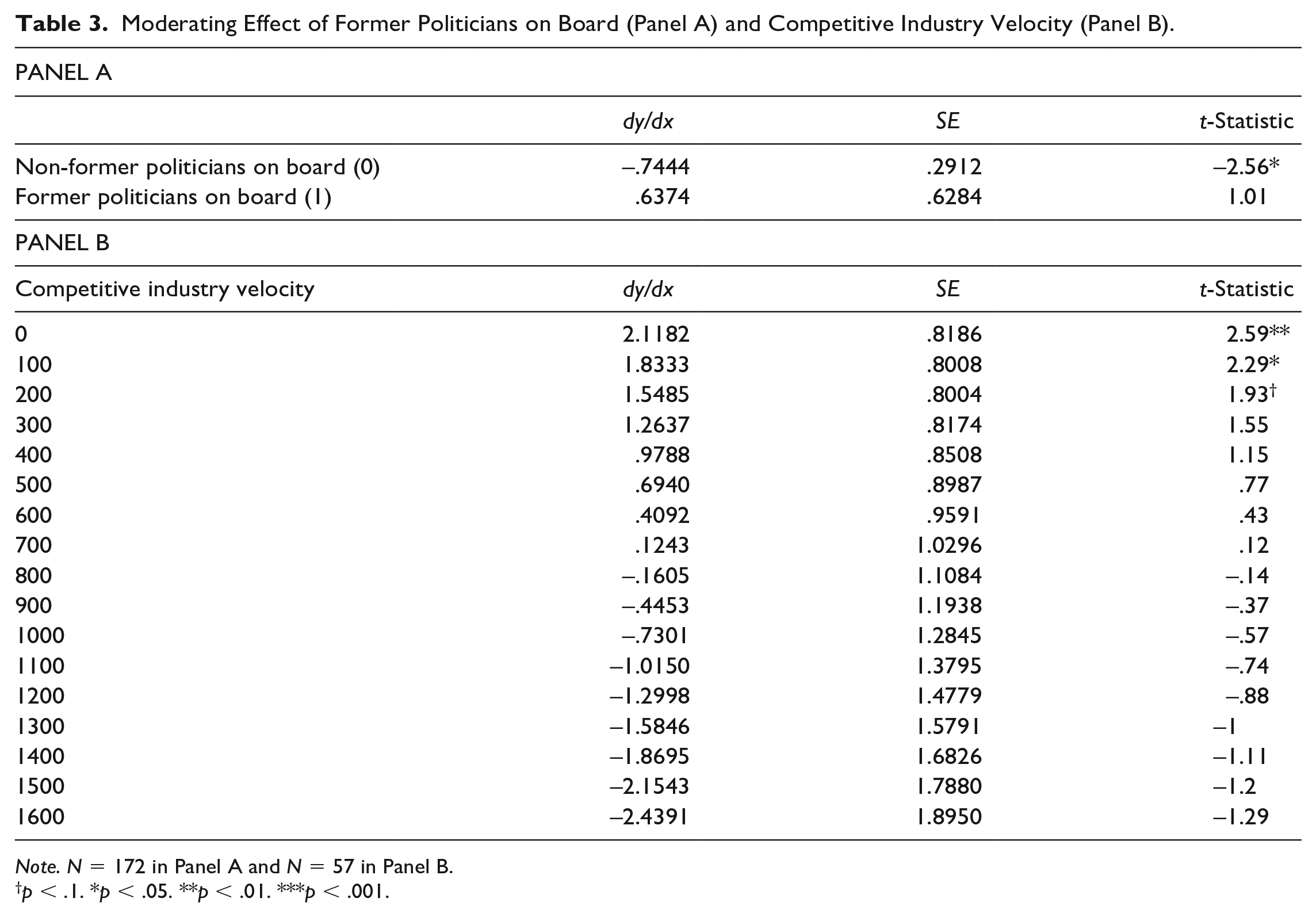

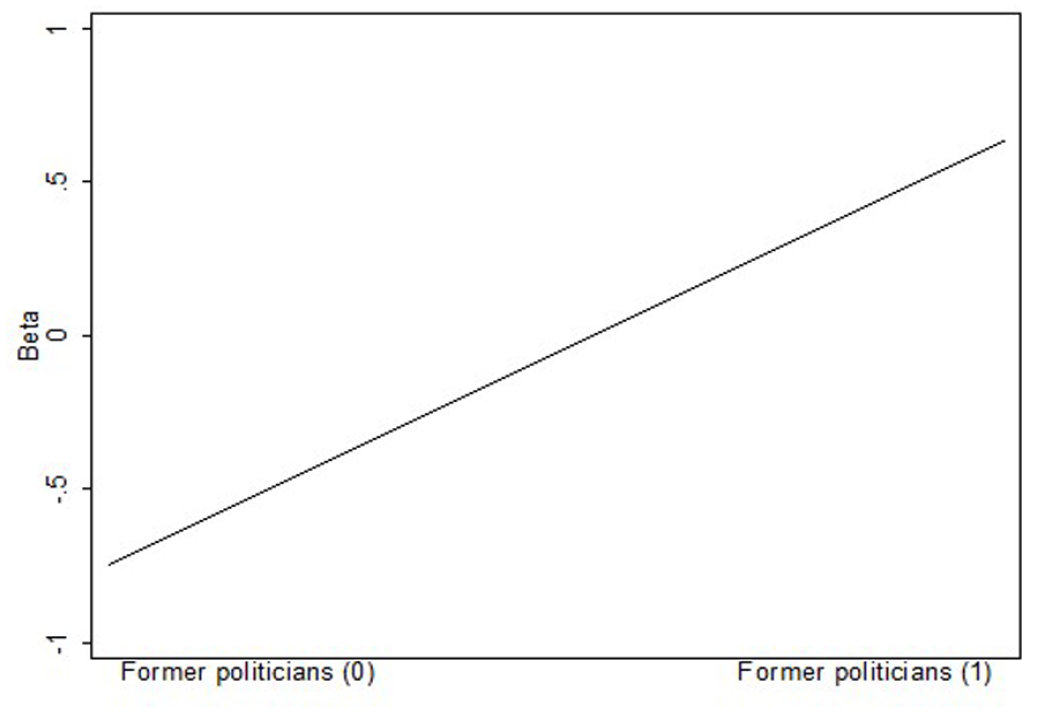

According to Hypothesis 2, the presence of politicians on the board has a moderating effect on the relationship between family control and the volume of acquisitions. The results obtained in Model 4b could confirm this expected moderating effect (B = 1.38, p < .05). However, since these types of models are very different from linear-additive regression models, we interpreted the interaction coefficient by looking at the marginal effects and recalculating the standard error (Brambor et al., 2006; Michiels et al., 2013). We displayed this information in Table 3 and Panel A and graphically represented it in Figure 1. It shows that the coefficient for not having former politicians on board is negative and significant. Therefore, in agreement with Hypothesis 2, these results reveal that family firms are more reluctant to engage in acquisitions when there are no former politicians on board.

Moderating Effect of Former Politicians on Board (Panel A) and Competitive Industry Velocity (Panel B).

Note. N = 172 in Panel A and N = 57 in Panel B.

p < .1. *p < .05. **p < .01. ***p < .001.

Marginal Effect of Family Control on Acquisition Volume Depending of the Presence of Former Politicians on Board.

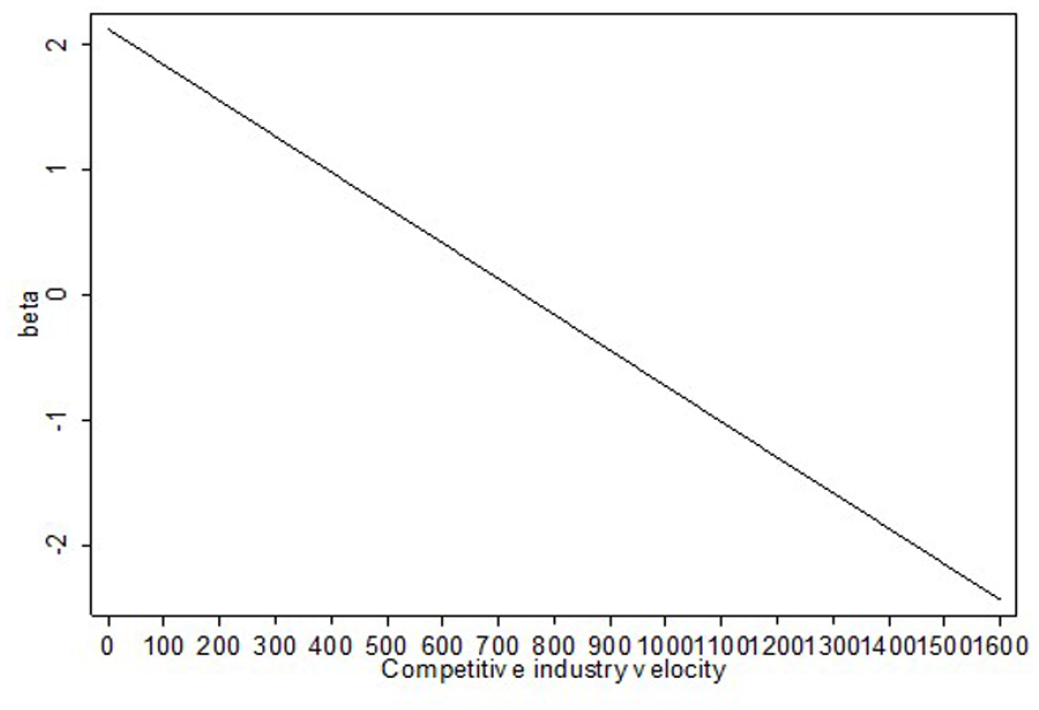

Model 6 tests Hypothesis 3, which states that the volume of acquisitions is affected by a three-way interaction between competitive industry velocity, family control, and former politicians on board. The coefficient for the three-way interaction was negative and marginally significant (B = –.00, p < .1), indicating that the degree of competitive velocity in the industry tends to decrease the interaction effect between the family control and former politicians variables presented in Hypothesis 2. Model 7 also tests this hypothesis using the family firm subsample. This shows that competitive industry velocity weakens former politicians’ positive effects on the acquisition activity of family firms. The coefficient of the interaction term between former politicians and competitive industry velocity was negative and significant (B = –.00, p < .05), providing additional evidence for Hypothesis 3. Similar to the method used for interpreting Hypothesis 2, we interpreted the interaction coefficient by looking at the marginal effects and standard errors. To this end, we calculated the derivate for several relevant ranges of the target industry’s competitive velocity values (Brambor et al., 2006; Huybrechts et al., 2013). We display this information in Table 3 Panel B and graphically represent it in Figure 2. It shows that former politicians’ effect on acquisition volume in family firms is only significant if the competitive industry velocity varies from 0 to 200 firms entering the target firm’s sector annually (which encompasses 74% of the total sample). Thus, Hypothesis 3 is supported, indicating that low levels of competitive industry velocity lead to a stronger relationship between former politicians and the volume of acquisitions for family firms.

Marginal Effect of Former Politicians on Acquisition Volume as Competitive Industry Velocity Changes (for Family Firms).

Robustness Checks

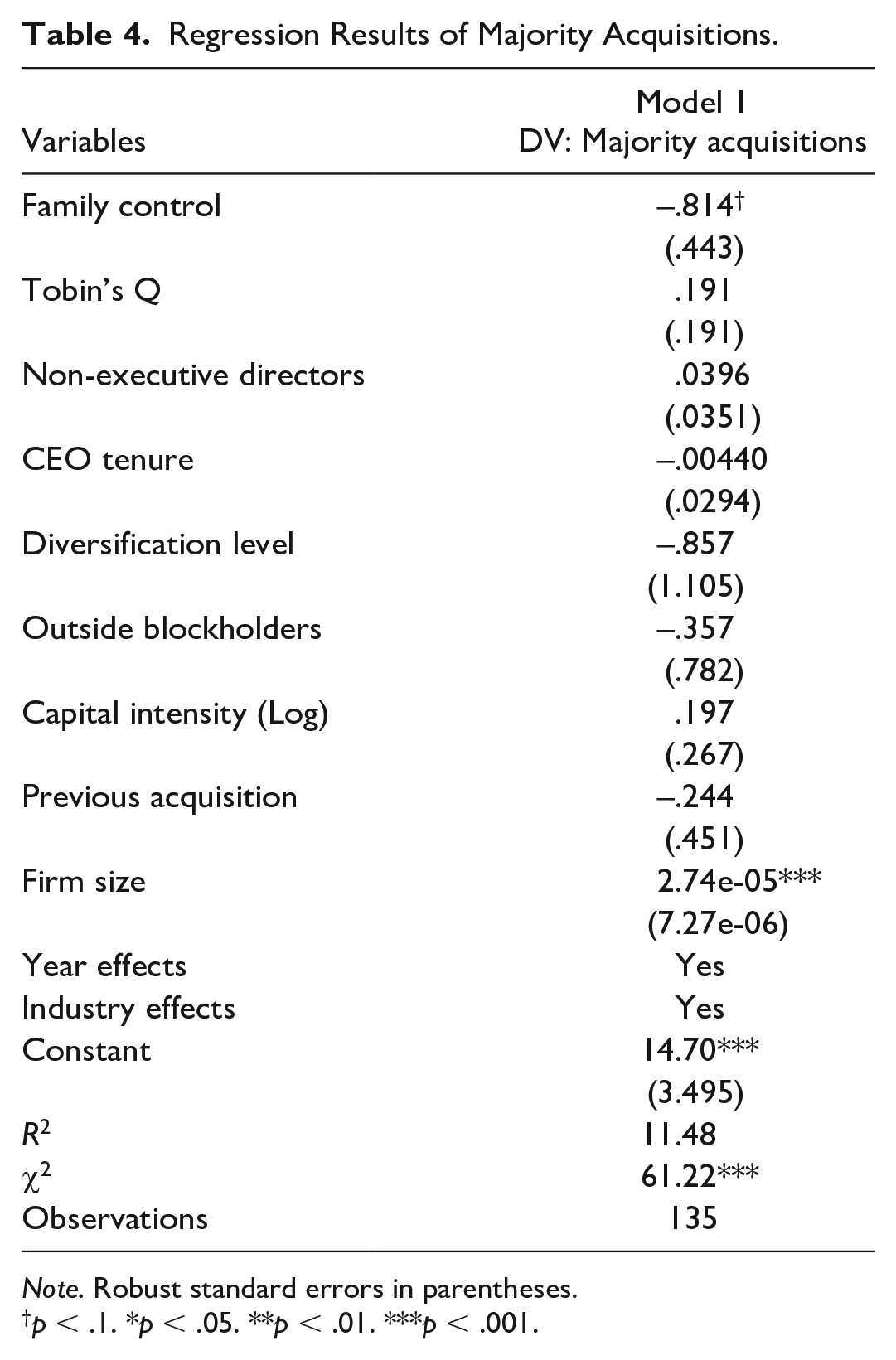

We conducted additional analyses to verify the robustness of our results across different model specifications. We made changes in the size of the sample for including those firms that made majority acquisitions, that is, acquisitions in which a majority stake is taken in the target firm (i.e., those that pose more than 50% of the shares of the acquired companies). We replicated the analyses and considered only those operations that pose the acquisition of more than 50% of the shares of the target. In the database provided by ORBIS, these acquisitions fall in the category of “majority stake.” The results, shown in Table 4 (Model 1), are not different from those previously published, supporting the robustness of our analyses.

Regression Results of Majority Acquisitions.

Note. Robust standard errors in parentheses.

†p < .1. *p < .05. **p < .01. ***p < .001.

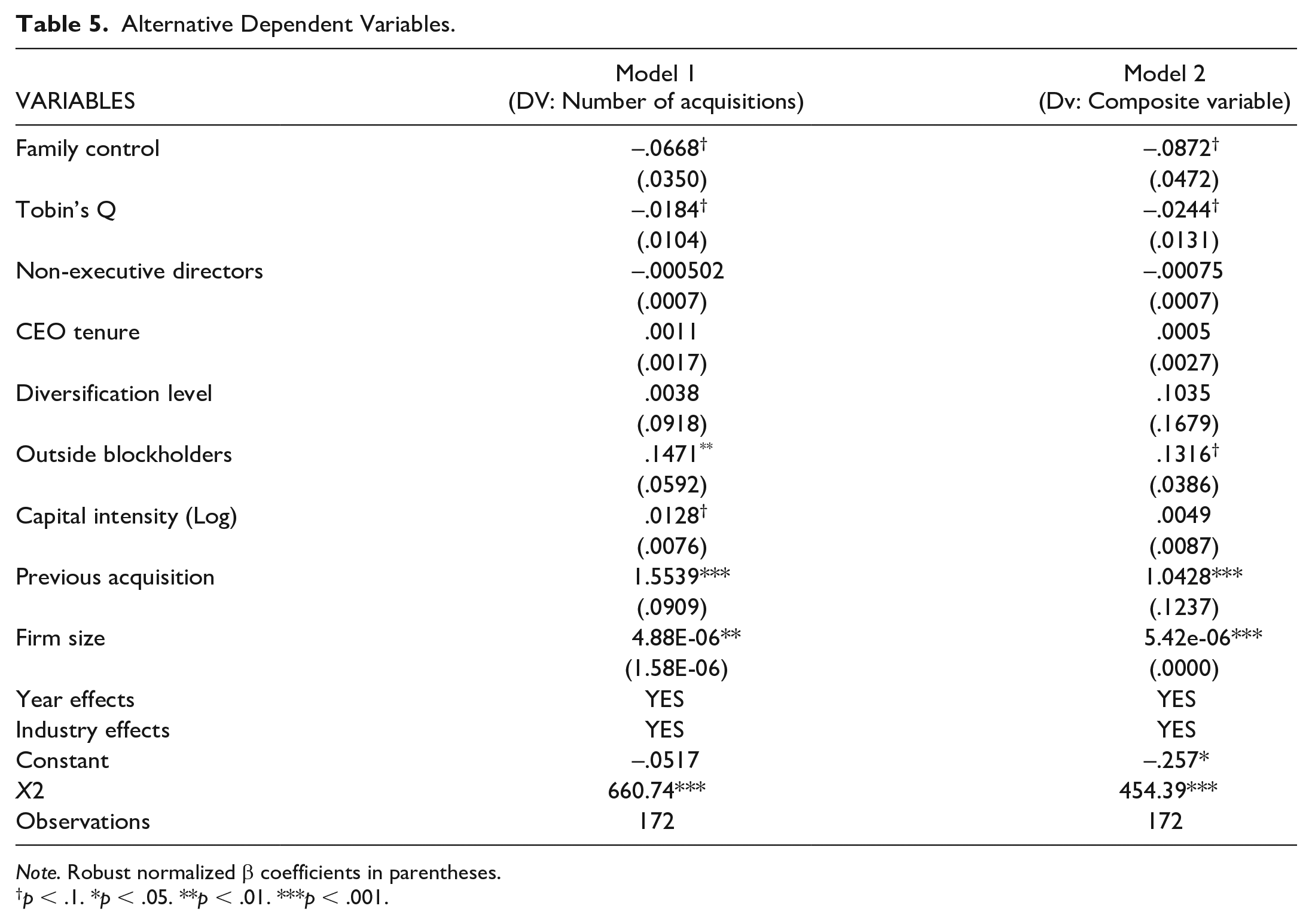

Second, we assessed whether the baseline hypothesis is also supported when the number of acquisitions is used as a predictor instead of their value (Gamache & McNamara, 2019). To measure the number of acquisitions, we counted the number of complete acquisitions made by a given firm in a given year (Chen et al., 2020; Haunschild & Beckman, 1998; Miller et al., 2007). This variable ranged from 0 to 7. In addition, and given the fact that the correlation between this variable (number of acquisitions) and the one used in the main model (log of total value) is high (.58***, p < .001; Krause et al., 2015), we calculated a composite variable as the average of their standardized values. The obtained results did not differ from those shown in the main model. These results are presented in Models 1 and 2 in Table 5.

Alternative Dependent Variables.

Note. Robust normalized β coefficients in parentheses.

p < .1. *p < .05. **p < .01. ***p < .001.

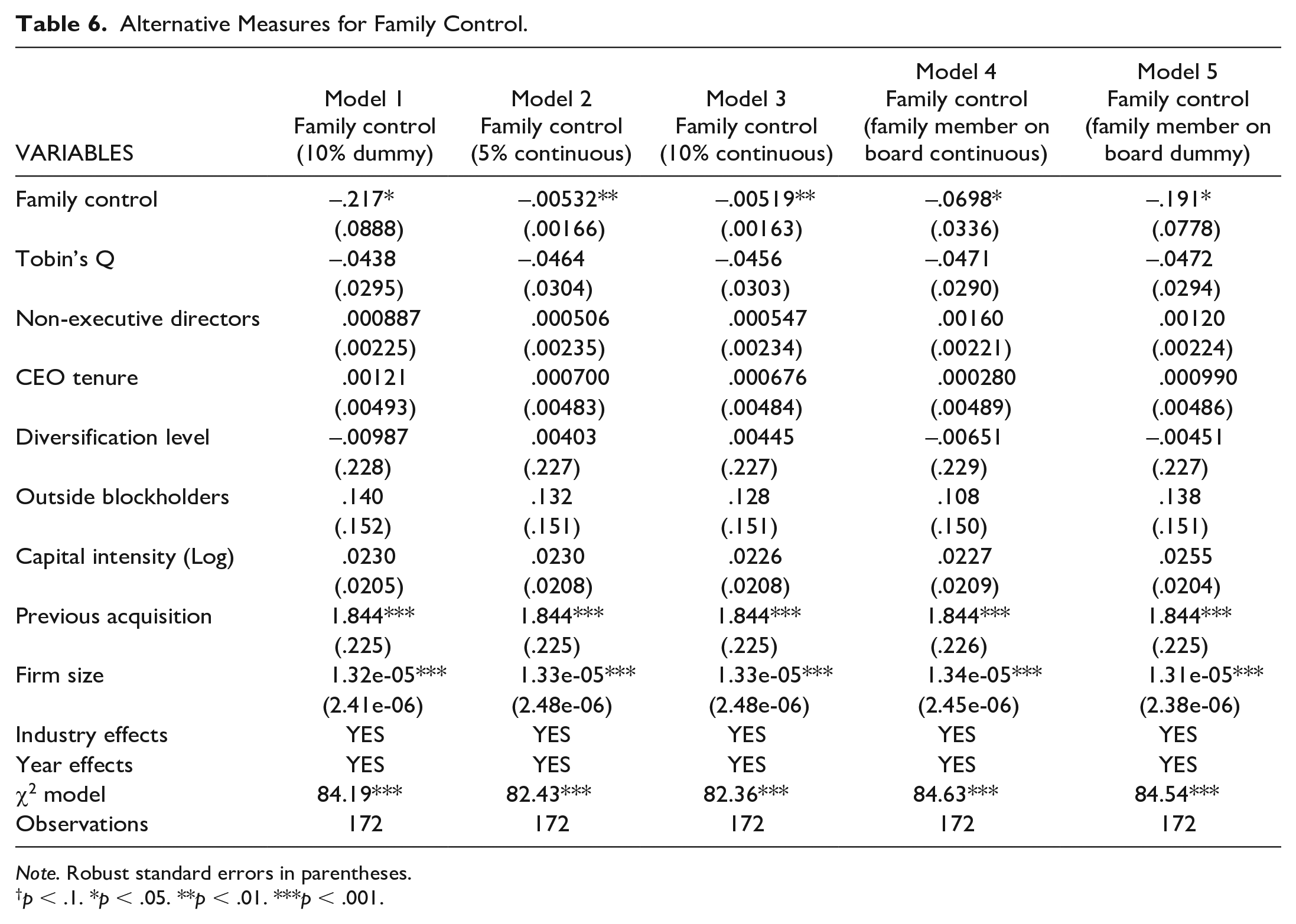

Third, following previous studies (Gomez-Mejia et al., 2019), alternative family-control dummy variables were used as a robustness test. That is, we employed different ownership cutoffs for categorizing family firm ownership, considering 10% of a firm’s shares owned by a single person or family (individually; Sacristán-Navarro et al., 2011) and using this categorization instead of our initial approach (more than 5% for a single person). Moreover, we measured family control (Chirico et al., 2018) considering the ownership of a minimum of 5% and 10% of a firm’s shares in a continuous variable. That is, if ownership was greater than 5% and 10% and at least one family member was involved in the board, then the percentage of family equity was coded as a continuous variable (Patel & Chrisman, 2014). Finally, we also considered family involvement separately, considering both the presence and number of family members on the board (Casillas et al., 2019). All results were confirmed, suggesting that our results are robust to different measures and operationalization of family control. These results are presented in the Models in Table 6.

Alternative Measures for Family Control.

Note. Robust standard errors in parentheses.

†p < .1. *p < .05. **p < .01. ***p < .001.

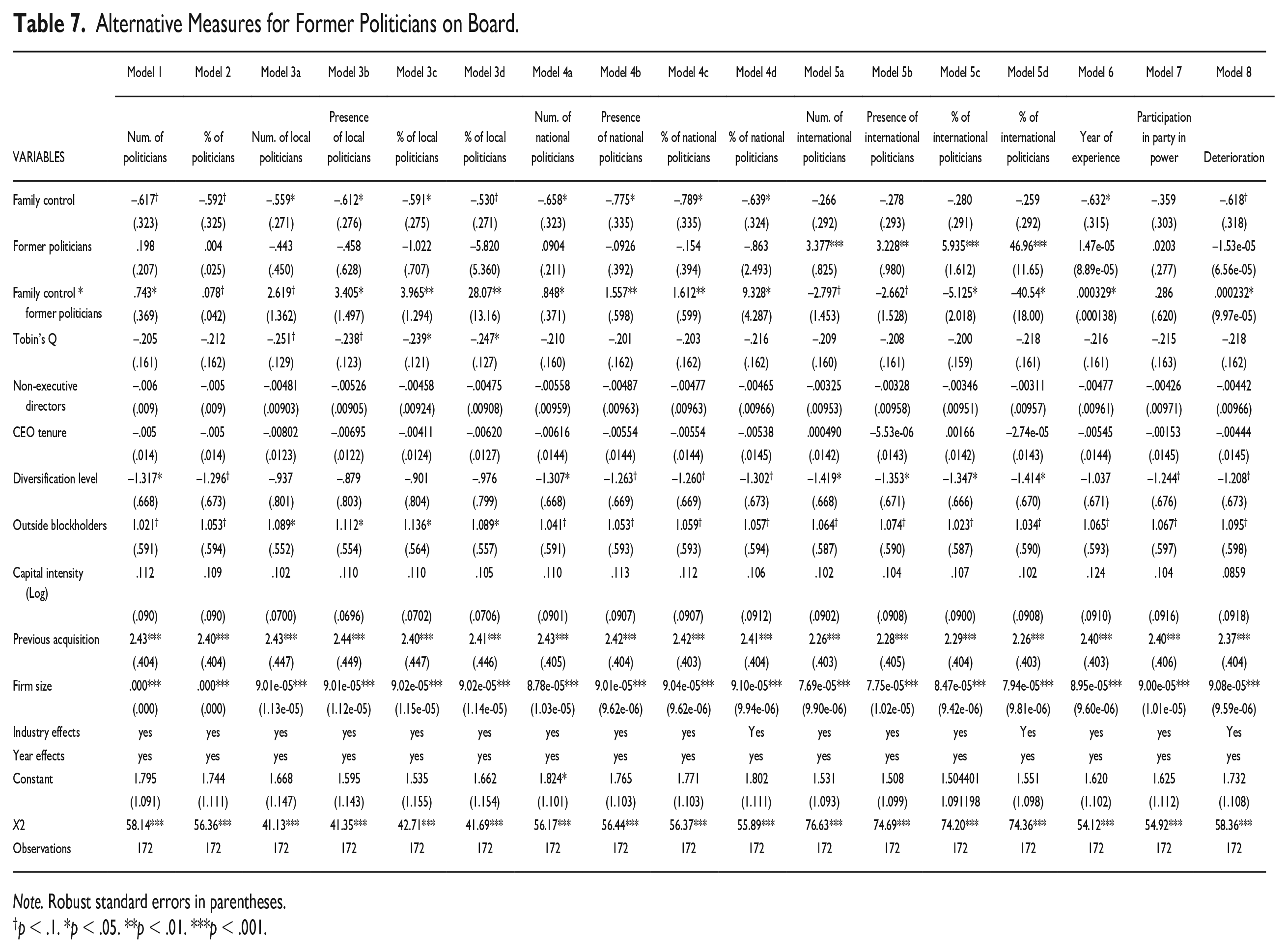

Finally, to verify whether our results were sensitive to the dummy variable “former politicians,” we created two new continuous variables: number of former politicians on board (Hillman, 2005) and the percentage of former politicians with respect to the total number of directors on board (Bona-Sánchez et al., 2014; El Nayal et al., 2021). As the effects of former politicians vary depending on the positions they used to occupy (El Nayal et al., 2021; Lester et al., 2008), we accounted for director-level heterogeneity and considered positions at the regional, national, and European levels separately. Specifically, we included the following variables: number (and presence) of politicians with experience on board who held office in a local, Spanish (senate, congress, secretaries of state, ministers, government presidents), or European government; percentage of politicians in each of these categories divided by the total number of politicians on board; and percentage of politicians in each of these categories divided by the total number of board members. Finally, we included three characteristics that could affect former politicians’ human and social capital (El Nayal et al., 2021; Lester et al., 2008): (1) the director’s years of experience in politics (service tenure) measured by the average number of days that the former politicians were in government service, including the regional, national, and international levels; (2) total number of former politicians who were in the same political party as the one in control in each year of the period of 2010 to 2015; 2 and (3) the duration since the end of office, measured in days elapsed between the last political role served and the day of appointment to the firm. The results shown in the models included in Table 7 remained consistent with our main findings.

Alternative Measures for Former Politicians on Board.

Note. Robust standard errors in parentheses.

p < .1. *p < .05. **p < .01. ***p < .001.

Discussion and Conclusion

This study analyzes the relationship between family firms and the volume of acquisitions from a SEW perspective. We examine how the presence of former politicians on firms’ boards and competitive industry velocity affect this relationship. The study sample consists of publicly held Spanish companies that were quoted during the period of 2010 to 2015. Contrary to the argument based on agency theory that lack of diversified ownership leads family firms to be risk averse to acquisitions, we adopt SEW theory (based on prospect theory and BAM), which proposes that family firms are both risk willing and risk averse as long as they preserve their SEW (Gomez-Mejia et al., 2018, in press). We discuss SEW gains and losses anticipated by family firms when making acquisition decisions. In particular, acquisitions can generate a range of positive outcomes that enhance SEW in terms of gaining firm competencies and resources that make the family firm stronger and more competitive, for example, by strengthening its growth and continuity. However, acquisitions often require external financing and are dependent on external agents that could lead to losses in familial control and weaken family firms’ social ties. We argue that since potential SEW loss is a relevant concern for family firms, which often neutralizes the SEW gains in the acquisition context, there would be a negative association between family firms and acquisitions. Our results show that family firms are less favorable to acquisition decisions (Hypothesis 1), which could be explained as a way to preserve their socioemotional endowment.

The findings also suggest that certain contingent factors, such as the presence of former politicians on the board, could moderate family firms’ risk preference regarding lower volumes of acquisitions. We argue that former politicians bring several benefits to the board, and family firms can anticipate and leverage their help to reduce potential SEW losses (Dreux, 2016; Zellweger et al., 2012). Thus, we propose that the presence of former politicians on the board positively moderates the relationship between family control and the volume of acquisitions. Our results fully support this hypothesis (Hypothesis 2) and confirm this expected moderating effect. In this sense, this study helps to understand the specific resources that a certain profile of directors (former politicians) could bring to family firms’ boards. These resources seem to be critical to family firms’ tendency to acquire. Furthermore, this study presents an additional factor that could interact with the relationship between former politicians and family firms’ acquisitions: competitive industry velocity. We propose that there is a three-way interaction between industry velocity, family control, and the presence of former politicians on boards affecting acquisitions. Our results confirm that the existence of family control and former politicians on boards is negatively associated with the volume of acquisitions as industry velocity increases (Hypothesis 3). These results lead to specific strategic decisions for both family and non-family firms, confirming that the governance of family firms differs from mainstream corporate governance. More specifically, competitive industry velocity is a variable to consider, along with former politicians. Previous studies have either focused on the benefits that former politicians bring to the firm or on the effects of industry variables on acquisitions. Our results show that there is a need to analyze these variables together. High-velocity industries reduce the benefits that former politicians bring to the board, which leads to higher potential SEW losses and a lower tendency to acquire. While our study was conducted in Spain, its results may also be relevant to other contexts (such as in China and some Latin American countries) where politicians often sit on boards.

This study makes several contributions to the literature. First, we enhance our understanding of the strategic decision-making process in family firms. We have replicated in Spain earlier findings in the United States, namely, that family firms are less likely to engage in acquisitions (our baseline hypothesis). Second, we extend prior research on family control’s influence on acquisition activity from a SEW perspective. Family firm research and business restructuring research have evolved into two separate streams (King et al., 2022). Beyond the dominant economic perspective, we believe our empirical research contributes to the understanding of the SEW paradigm as complementary to the economic perspective in explaining strategy development in family firms. Finally, our research sheds light on the governance conditions under which family firms should consider making acquisitions. Specifically, our research indicates that former politicians on the boards of family firms reduce family owners’ vulnerability, which we argue, on balance, helps protect SEW when acquiring other firms. Our analysis also shows that the positive relationship between former politicians on boards and family firms’ tendency to acquire is contingent on competitive industry velocity. To the best of our knowledge, this is the first study that uses SEW theory to analyze the influence of governance issues and industry factors in tandem in the family firm acquisitions literature.

The findings of this study have several managerial implications. Board composition, particularly the presence of former politicians, is a major factor that affects acquisitions. Since family firms with former politicians on their boards engage in acquisitions more than their counterparts that do not have former politicians on their boards, family firms may reconsider their board structure when interested in increasing acquisitions in the future. In other words, former politicians may be perceived as an asset for family firms in planning acquisitions. Furthermore, family firms should study their industries, particularly industry velocity, along with board composition before embarking on acquisition strategies. Overall, there is no clear solution to which variables will impact future strategies or the board composition that will fit all situations.

This study also has several limitations. We conducted our investigation under the umbrella of the SEW framework. However, according to previous research, the stronger the role of the founding family, the more likely the firm is to strive to protect its SEW (Gomez-Mejia et al., 2011). Thus, one would expect to find differences between firms that are owned and managed by the founding family and those family firms that transition into subsequent generations and are professionally managed. Although this issue is beyond the scope of this research, it opens a future research line analyzing differences by family stages.

In addition, there is research that indicates how family firms’ acquisition propensity depends on the legal system in which such firms operate (Requejo et al., 2018). Extending this research to the analysis of the institutional environment would be interesting to further understand family firms’ acquisitions. Equally, it is important for future research to analyze the influence of firm’s financial structure in acquisitions more deeply. Certain financial structures, such as dual-class structures, could allow family firms to retain control (of great value for them) while also raising public equity when coping with acquisitions. We also limited our analysis to publicly held Spanish companies that were quoted from 2010 to 2015, which implies a bias for large firms. Moreover, these firms had to comply with the rules of the CNMV, which is the institution that watches over the stock exchange and collects and publishes the data provided by firms. This includes corporate government reports as well as financial statements (e.g., profit and loss statements, balance sheets, and mergers and acquisitions). To enrich this analysis, future studies should include not only quoted firms but also non-quoted and smaller firms. Firm size is a pertinent variable, and previous studies have shown that it affects acquisition behavior. Furthermore, other countries where former politicians sit on boards should be included in future studies analyzing additional information such as their political affiliation, and the results should be compared across diverse institutional environments. For instance, it would be interesting to see how the results reported here vary between countries with strong versus weak property rights institutions (Acemoglu & Johnson, 2005; Bell et al., 2014). In addition, the results related to the variable of “deterioration of former politicians,” which show that the more time elapsed, the lower the negative effect of family control on the number of acquisitions (Table 7), could be an important launching pad for future studies. It would be interesting to consider factors such as the different government levels in which former politicians participated previously, their political affiliation, and the number of board interlocks they had joined. Finally, in conjunction with board composition and governance mechanism, future studies may consider other dimensions of “industry velocity,” in addition to “competitive industry velocity.”

Research Question

This study analyzes:

1. Why are family firms more reluctant to undertake acquisitions than non-family firms based on a socioemotional wealth (SEW) approach?

2. What is the role played by former politicians on the boards of family firms in acquisitions decisions?

3. How does competitive industry velocity affect the relationship among family firms, acquisitions, and former politicians on boards?

Implications for Practice

1. Former politicians on the boards of family firms reduce family owners’ vulnerability, and they may be perceived as an asset for family firms in planning acquisitions.

2. High competitive velocity industries reduce the benefits that former politicians bring to the board

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors acknowledge the financial support by the R&D Project FEDER Andalucía 2014-2020 (Ref. UPO-1262853), the research project funded by the Spanish Minister of Science & Innovation (Ref. PID2021-128420OB-I00), and the research project funded by Consejería de Universidad, Investigación e Innovación (Junta de Andalucia, PAIDI 2021) Ref. “ProyExcel_00934.”