Abstract

Equity crowdfunding (ECF) has potential benefits that might be attractive to high-quality entrepreneurs, including fast access to a large pool of investors and obtaining feedback from the market. However, there are potential costs associated with ECF due to early public disclosure of entrepreneurial activities, communication costs with large pools of investors, and equity dilution that could discourage future equity investors; these costs suggest that ECF attracts low-quality entrepreneurs. In this paper, we hypothesize that entrepreneurs tied to more risky banks are more likely to be low-quality entrepreneurs and thus are more likely to use ECF. A large sample of ECF campaigns in Germany shows strong evidence that connections to distressed banks push entrepreneurs to use ECF. We find some evidence, albeit less robust, that entrepreneurs who can access other forms of equity are less likely to use ECF. Finally, the data indicate that entrepreneurs who access ECF are more likely to fail.

Keywords

Access to finance is the most important growth constraint for young and innovative ventures (De Prijcker et al., 2019; Manigart & Sapienza, 2017). The rise of new forms of alternative finance elicits the question of whether or not these new forms have differential importance to entrepreneurs (Bruton et al., 2015). The growth of equity crowdfunding (ECF) warrants particular attention. According to industry observers, European providers of early-stage capital invested approximately EUR 11 billion in 2017. With a volume of roughly EUR 630 million across Europe in 2017, ECF already accounts for more than 5% of the market volume and is expected to expand at a fast pace (European Business Angel Network, 2018). Among German startups, crowdfunding is the third most popular source of external capital and only dominated by bank finance and venture capital (German Startups Association, 2017). Recent work has called for a better understanding as to how these different sources of entrepreneurial finance interact (Cumming et al., 2018; Cumming, Deloof, et al., 2019).

Models of entrepreneurial finance traditionally derive adverse selection outcomes whereby high-quality entrepreneurs, who have more information about their projects than potential investors (i.e., there is information asymmetry; Venkataraman, 1997), are less likely to seek equity investments due to the loss of ownership share and the greater opportunity costs of giving up ownership (Meza & Webb, 1987; Stiglitz & Weiss, 1981). In the context of venture capital (Cumming, 2006), this trade-off is commonly observed in ways consistent with theory. It is unclear, however, whether the traditional pecking order theory and signaling theory naturally extends to new forms of entrepreneurial finance brought about by fintech and regulatory change, such as ECF. The traditional pecking order and signaling predictions are potentially offset by new financing technologies that reduce contracting costs and search costs and also offer complimentary benefits of establishing market presence and “traction” (demonstrating interest in a venture’s product). ECF, in particular, offers a fast and relatively 1 standardized way to reach a large number of investors and obtain feedback from the market. It is unclear as to whether the traditional adverse selection costs dominate these potential benefits associated with the new technology, which gives rise to this empirical study. Is ECF, indeed, a viable alternative to previous traditional financing forms of new ventures? Or, does ECF attract entrepreneurs who could not receive funding elsewhere for a very good reason: poor quality? Can a possibly uninformed crowd identify the low-quality from the high-quality entrepreneurs in the project pool of the economy more successfully than outside equity investors and banks? The implications of whether or not ECF attracts the best or worst entrepreneurs are important for academics, practitioners, and policymakers, as we discuss after reviewing the evidence.

In this paper, we contribute to the literature on ECF attracting low-quality or high-quality entrepreneurs by theorizing that the quality of entrepreneurs’ bank connections, as well as the availability of equity investors, will affect their use of ECF. An entrepreneurial project is more likely to be low quality by virtue of its affiliation with a more risky bank. We conjecture that entrepreneurs affiliated with distressed banks—the clearest indication of a risky bank—will be pushed towards ECF. Entrepreneurs associated with less risky banks or with options to access other forms of equity will be less likely to use ECF. Further, we examine whether or not entrepreneurs are more likely to eventually fail if they have used ECF.

We gathered a unique and nearly comprehensive sample of all ECF campaigns in Germany that together account for 90% of the ECF market volume between 2011 and 2015 (Crowdinvest.de, 2018). We examine the German context for three main reasons. First, and most importantly, we have information on whether or not the entrepreneur was affiliated with a distressed bank. Second, German ECF platforms were among the first platforms around the world to start operations in 2011; thus, a large sample exists for statistical analyses. Third, in the German context, there are sufficiently detailed data that enable us to construct a counterfactual sample of ventures without ECF that are similar in terms of observable hard and soft factors and that complement the information on the use of crowdfunding with data about each venture’s bank relationship and whether an outside equity investor was involved. We are unaware of the existence of such detailed data from other countries. Contrary to prior work (e.g., Belleflamme et al., 2014), we can, therefore, estimate the probability of tapping the “wisdom of the crowd,” conditional on all of the venture and managerial traits.

Our analysis gives rise to three main results. First, ventures that are tied to distressed banks are around 9% more likely to use ECF. Those that have already secured equity funding from outside investors are significantly less likely to tap the crowd by a similar order of magnitude. Second, further indicators of bank quality corroborate that the quality of the bank associated with the entrepreneur influences the use of ECF. If connected banks are well-capitalized and liquid, associated entrepreneurs are less likely to tap the crowd for equity. Those banks that have inefficiently managed costs and therefore require high loan-loss provisions are, in turn, more likely to drive entrepreneurs toward ECF. Third, the data reveals that entrepreneurs who are associated with a distressed bank and who do use ECF, in turn, are 10%–12% more likely to fail. Equity funding from outside investors has no significant effect on failure. Notably, the effects of stressed bank relationships and ECF on failure probabilities are not statistically different. This result suggests that an unwise crowd is just as prone as a bad bank to finance the low-quality entrepreneurs in the pool of projects.

Our paper adds to prior literature by evaluating the success of ECF by providing theory and evidence on the importance of the quality of banks as well as the availability of equity investors with whom entrepreneurs are associated with seeking ECF. Our empirical context builds on important recent work in different institutional contexts (Hildebrand et al., 2017; Hornuf et al., 2018; Walthoff-Borm, Schwienbacher, et al., 2018, Walthoff-Borm, Vanacker, et al., 2018) by enabling explicit empirical tests of the use of alternative forms of finance. We examine a dynamic entrepreneurial funding context and show how early usage of different sources of finance affects the use of ECF.

This paper is organized as follows. The next section discusses the theory derived from prior literature and testable hypotheses. Thereafter, we discuss the institutional context in which the data were derived. The empirical tests are provided after introducing the data. The last sections discuss the implications for theory, practice, and policy.

Hypotheses

Pecking Order in Entrepreneurial Finance

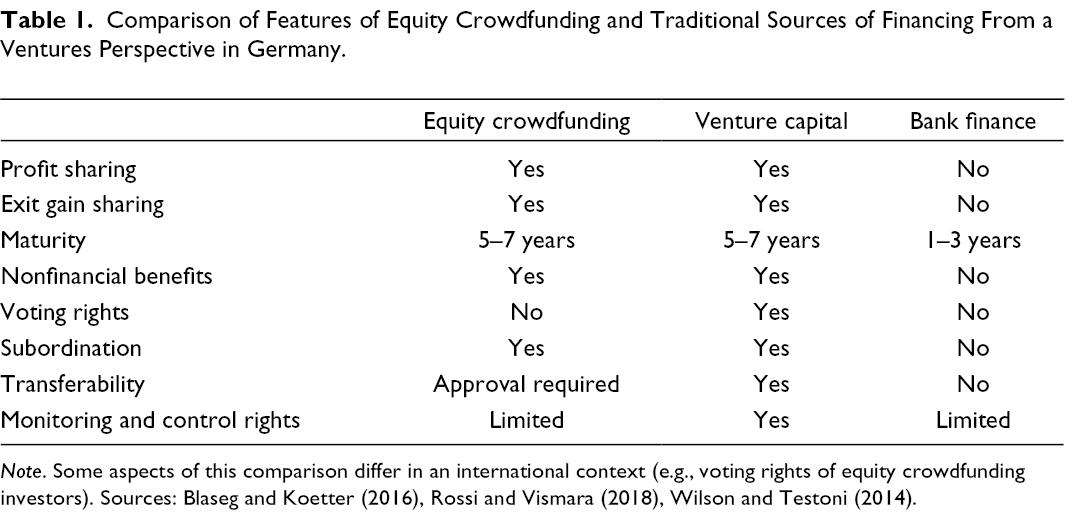

Table 1 provides an overview of the differences and similarities between ECF, venture capitalists (VC), and bank financing from a venture’s perspective and shows how sources of capital differ from one another in Germany. Note that institutional settings differ across countries, which complicates international comparisons of some aspects. ECF in Germany involves the issue of equity-like mezzanine financial instruments, such as silent partnerships and subordinated loans, which combine many features of traditional sources of debt and equity. These financial instruments mimic equity investments that are comparable to venture capital, enabling the crowd to participate in the future cash flows and the proceeds from a potential exit or liquidation. One of the most discussed features of ECF is the possible benefit for ventures from interacting with a heterogeneous crowd of investors, who could provide support similar to VCs (Agrawal et al., 2014; Cholakova & Clarysse, 2015). This potential benefit comes at the risk of expropriation by publishing information to a semi-anonymous crowd in an early stage (Ueda, 2004). These similarities show that ECF could substitute venture capital from a capital structure perspective. Yet, other features require the comparison to debt finance as an alternative source of financing. Similar to bank financing, the crowd investment has a limited maturity of 5–7 years, including no voting and limited monitoring and enforcement rights (Hornuf & Schwienbacher, 2018). The choice between bank finance and venture capital depends on several factors, such as the specific sensitivities of effort and performance and the variations in the ownership structure (de Bettignies & Brander, 2007).

Comparison of Features of Equity Crowdfunding and Traditional Sources of Financing From a Ventures Perspective in Germany.

Note. Some aspects of this comparison differ in an international context (e.g., voting rights of equity crowdfunding investors). Sources: Blaseg and Koetter (2016), Rossi and Vismara (2018), Wilson and Testoni (2014).

The traditional pecking order theory of the capital structure of internal finance, followed by debt and outside equity, is well accepted by a large body of work (Meza & Webb, 1987; Myers & Majluf, 1984; Stiglitz & Weiss, 1981). Bank funding takes the form of debt, whereas VCs typically provide convertible preferred equity, convertible debt, or straight equity (Cumming, 2006). Whereas some authors state that the decision to use one type of capital versus another may be driven by necessity rather than by choice (Coleman et al., 2016), others argue in line with the pecking order theory, adjusted for potential constraints imposed by debt capacity (Cumming, 2006; Vanacker & Manigart, 2010). Debt is usually preferred by entrepreneurs because it is cheaper, does not dilute ownership, and entails less extensive monitoring compared with venture capital finance (de Bettignies & Brander, 2007). A distinct feature of venture capital is the provision of high-value managerial input to the venture, thus making venture capital more attractive, enhancing the chances of success from the perspective of the entrepreneur (Baum & Silverman, 2004). Therefore, whether bank finance or venture capital finance is preferred depends on a variety of factors, including the specific risk profile and current profitability of the venture, as well as the skills and the experience of the entrepreneur (Ueda, 2004; Winton & Yerramilli, 2008).

VC investors are much more active investors who take larger ownership shares and greater control rights into their investee ventures (Cumming, 2008; Cumming et al., 2008) relative to ECF investors (Ahlers et al., 2015; Cumming, Meoli, et al., 2019). VCs typically take between 20% and 40% ownership and have effective control, whereas ECF investors typically collectively take less than 20% ownership and have scant control rights. As such, VC investors are much more active in adding value to their investees than ECF investors. Entrepreneurs who can benefit from the advice and networks of VCs prefer VC finance, and VC-backed ventures are normally expected to be acquired or publicly listed on a stock exchange within 7 years. ECF-backed ventures, by contrast, do not face such systematically high growth expectations or assistance from professional investors. Therefore, ECF is typically lower in the pecking order relative to VC as an alternative source of equity investment for entrepreneurial ventures. Further, once a venture obtains ECF, it is less likely to raise follow-up funding due to the costs and negative signals associated with dispersed ownership of early-stage ventures and the associated efforts and costs of managing a large pool of investors (Signori & Vismara, 2018). In sum, in the absence of funding constraints for entrepreneurial ventures in traditional forms of finance, such as venture capital or bank or angel finance, entrepreneurs would not select into ECF. This is also confirmed by Walthoff-Borm, Schwienbacher, et al. (2018), who find that especially start-ups without internal funds and debt capacity use ECF. We go beyond their important finding that start-ups of higher quality rely first on debt instead of ECF by examining the impact of the (un)availability of competing sources of start-up funding on the likelihood of using ECF.

Entrepreneurs Affiliated with Distressed Banks

Credit is a crucial source of external funding for young ventures around the world (Cosh et al., 2009; Robb & Robinson, 2014). The quality assessment of opaque new ventures is difficult, and information asymmetries are paramount during early-stage financing (Jensen & Meckling, 1976; Meza & Webb, 1987; Stiglitz & Weiss, 1981). Banks try to resolve the information asymmetry between savers and investors by developing screening competencies and acting as delegated monitors (Diamond, 1984), thereby mitigating the information frictions that plague small and new ventures (Petersen & Rajan, 1994, 2002). Credit contractions are particularly painful for small new ventures (Jiménez et al., 2012; Robb & Robinson, 2014). The financial crisis of 2008 gave rise to a large number of distressed banks, which, in turn, exacerbated credit contractions (Puri et al., 2011).

Entrepreneurs who have ties to distressed banks face pronounced problems when seeking external capital for the following five reasons. These pronounced problems are not merely attributable to the fact that an entrepreneur is, of course, much less likely to obtain capital from the distressed bank with which it already has a relationship. Instead, there are five other primary factors that mitigate an entrepreneur’s chances of being able to seek capital elsewhere.

First, external sources of capital, such as banks, are a source of governance for entrepreneurs (Berger & Udell, 1998). Distressed banks, however, are less likely to monitor and add value to an entrepreneur relative to nondistressed banks (Berger et al., 2001). In general, other investors, such as venture capital providers, are much better external monitors for entrepreneurs than even healthy banks (Manigart & Wright, 2013). Distressed banks typically suffer from internal governance problems, less skilled lending officers, and distracted attention by virtue of being in distress and risking bankruptcy themselves. This distorted attention and ability translate into weaker governance for entrepreneurs who are affiliated with distressed banks, which, in turn, results in lower quality entrepreneurs with less value-added external governance provided by their sources of capital.

Second, entrepreneurs are, of course, credit constrained by virtue of being tied to a distressed bank (Berger et al., 2013). Credit-constrained entrepreneurs make relatively inefficient decisions that are more short-term in nature compared with what would be otherwise optimal, as they have to focus on achieving and presenting short-term results to obtain capital from elsewhere (Yung, 2019). This inefficient allocation of attention towards short-termism means that entrepreneurs tied to distressed banks will, on average, be of lower quality than entrepreneurs not tied to distressed banks.

Third, external sources of capital normally benefit their investees by enabling a superior business network through which entrepreneurs can join (Manigart & Wright, 2013). This network includes other companies that could offer strategic advantages to the entrepreneur (e.g., suppliers and/or stakeholders) and other financiers that could partner in syndicated lending or other financing arrangements. However, distressed banks are much less likely to have these quality networks and offer these advantages to their investee ventures (Berger et al., 2013). In fact, a tie to a distressed bank would be a negative signal to other potential strategic partners and other financiers to which an entrepreneur might have sought a networking relation.

Fourth, lending relationships with small entrepreneurial ventures are typically regionally proximate to mitigate information asymmetries that are typical for small ventures (Berger & Udell, 1998). If a bank is distressed, there will be less lending to other ventures in the same region where the bank is based. As such, there will be fewer agglomeration benefits associated with ties to distressed banks. The worsened economic conditions resulting from distressed banks, in turn, make entrepreneurs worse off by being tied to distressed banks.

Fifth, stakeholders of entrepreneurial ventures tied to distressed banks may have concerns about the financial stability of the entrepreneurial venture. If the bank has uncertain survival prospects or an uncertain ability to lend to the entrepreneurial venture, it is less likely that the entrepreneurial venture will be able to provide new products, innovative products, and/or support the existing products that the entrepreneurial venture offers to its stakeholders by virtue of its distressed source of bank capital. This stakeholder concern will subsequently weaken the growth prospects of entrepreneurial ventures tied to distressed banks. Empirical evidence is consistent with a greater rate of venture failure by virtue of ties to distressed banks, even when these ventures otherwise show higher rates of productivity (Anderson et al., 2019).

For these five reasons, a tie to a distressed bank is a negative signal about an entrepreneur’s quality. Which other type of investor is more likely to take note of such a signal? Or, put differently: for an entrepreneur with a tie to a distressed bank, where, pushed to seek capital elsewhere, is it feasible for that entrepreneur to obtain capital?

Entrepreneurs and their investors face information asymmetry: entrepreneurs know more about their own quality than do the investors. Thus, entrepreneurs use signals to mitigate information asymmetry. Signaling theory has established that signals must be costly to be effective (Akerlof, 1970; Bacharach, 1989; Connelly et al., 2011; Spence, 1973; Vanacker et al., 2019). Otherwise, low-quality entrepreneurs would adopt the same signals as high-quality entrepreneurs. Also, investors must be capable of reading signals to distinguish between entrepreneurs of different qualities.

ECF investors are not as skilled as other types of investors, such as VCs, at distinguishing between high-quality and low-quality entrepreneurs by adequately processing signals. ECF investors comprise many uninformed, unsophisticated, and dispersed ECF investors. The presence of sophisticated equity investors such as VCs reduces the need for entrepreneurs to rely on ECF. Venture capital investors carry out extensive due diligence prior to investment and add value to entrepreneurs after investment (Manigart & Sapienza, 2017; Manigart & Wright, 2013; Sapienza et al., 1996). Moreover, VCs offer strategic, financial, human resource, and marketing and provide their investee firms with an array of valuable contacts, including upstream suppliers and downstream customers. Further, VCs provide connections to top accounting and legal service providers and investment banks at the time of selling the entrepreneurial firm. These same value-added services and coaching advice are much less likely to come from smaller dispersed retail investors through crowdfunding. As such, ECF is a less attractive form of equity finance.

Crowdfunding enables entrepreneurs to exploit uninformed investors with behavioral, gambling, and herding biases (Vismara, 2018). By continuously screening the market to find promising investment opportunities, VCs have developed superior screening and monitoring capabilities to address information asymmetry problems (Colombo & Grilli, 2010; Croce et al., 2013). Banks rely on transaction lending technologies, such as relationship lending, for the selection of opaque ventures (Berger & Udell, 2006). ECF follows a different mechanism for selecting ventures. The platform performs only limited due diligence using its team analysts and a check of formal criteria, such as available documentation and organizational factors to select ventures that can launch a campaign on the platform. The final decision on which ventures receive funding is left to the investors though. The provision point mechanism implies that each ECF campaign manager specifies a minimum threshold based on the capital requirements of the venture as a fundraising goal, which has to be met by the aggregate individual investments. This mechanism should capture the wisdom of the crowd and ensure that only projects with sufficient financial resources are started, thereby limiting the default risk faced by the crowd (Cumming, Leoboeuf, et al., 2019). Empirical evidence suggests, at least in other types of crowdfunding, that the crowd does a good job of evaluating projects and screening the good from the bad (Mollick & Nanda, 2016). Other research highlights the crucial role of information cascades among individual investors for the success of ECF campaigns (Vismara, 2018). Information cascades imply a free-riding problem across the crowd; that is, investors take low-equity stakes and anticipate the “team production dilemma” (Alchian & Demosetz, 1972), but they do not engage in active monitoring.

Just as ECF investors are not effective at processing signals, ECF platforms, likewise, do not act as delegated monitors. Contrary to underwriting banks, they are not liable for the information they provide and take limited responsibility after a successful crowdfunding campaign. Revenue is mostly generated from success fees for offerings that exceed their minimum requested amount. This can induce platforms to act on a short-term focus by maximizing the number of projects and outsourcing the costly due diligence process to the crowd (Adriani et al., 2014), despite reputational risks (Blaseg et al., 2019). An effective selection by the crowd requires individuals who make an informed investment decision after proper due diligence, which is unreasonable to expect for two reasons. First, it is difficult for investors to assess the true ability of the management team or the underlying quality of the venture in the absence of face-to-face interaction. Second, the crowd in ECF consists mostly of uncoordinated amateurs. The crowd is subject to herding behavior and has little incentive to spend much time on extensive due diligence due to small amounts of invested and small returns. As such, it is questionable whether the combination of limited due diligence by the platform and reliance on the collective decision of the crowd is an effective mechanism for selecting good-quality projects (Agrawal et al., 2014).

Overall, we expect that entrepreneurs tied to distressed banks or entrepreneurs who are unable to attract equity investors are more likely to be pushed toward ECF. Our two null hypotheses are, therefore, as follows:

Specification, Sampling, and Data

We construct a sample of ECF and non-ECF ventures that fulfill the criteria of using crowdfunding in Germany from an organizational perspective (e.g., limited liability). In the first step, we constantly monitored the four largest ECF platforms in Germany (Companisto, Fundsters, Innovestment, and Seedmatch) between November 2011 and December 2015. These platforms dominate the market and are comparable in terms of the mechanisms for selecting ventures and the financing instruments used (Crowdinvest.de, 2018). Table OA1 in the online appendix provides descriptive statistics on the ECF platform and offers characteristics. We gathered all provided data about the 163 ventures that used crowdfunding during this observation period.

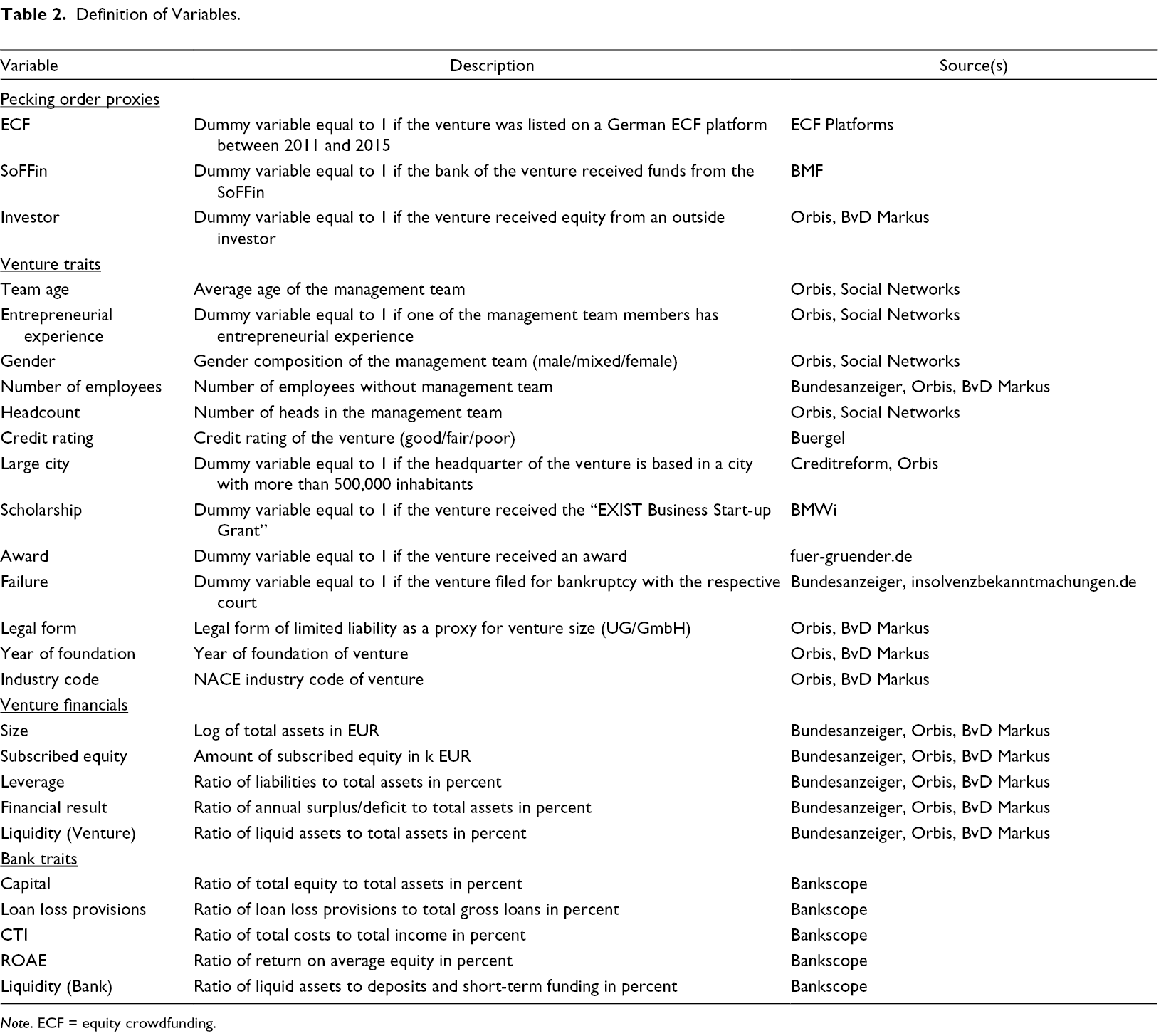

In a second step, we identified 32,005 ventures that did not use ECF, were founded with limited liability between 2008 and 2014, and were not publicly traded using the Orbis and Markus databases. From this sample, we create a counterfactual sample of similar ventures that did not use ECF by applying nearest neighbor propensity score matching without replacement (PSM, see Dehejia & Wahba, 2002) using the NACE industry classification, the year of foundation, and the form of limited liability as a proxy for venture size (Puri & Zarutskie, 2012; Walthoff-Borm, Schwienbacher, et al., 2018). Table OA2 in the online appendix details the procedure that provides us with a counterfactual for each ECF venture. 2 The resulting sample thus includes 163 ventures that used ECF and 163 ventures that did not use ECF but could have. We augment the matched sample with financial reporting data, management and venture traits, and equity investor and bank relationship information (see Table 2 for a full description of all variables). 3

Definition of Variables.

Note. ECF = equity crowdfunding.

Our main question tests whether or not the probability that venture i applies for crowdfunding yi = 1 also depends on its association with a distressed, and thus more risky, bank. We identify distressed banks as those that received equity support from the German Special Fund for Financial Market Stabilization (“SoFFin”). In October 2008, the German Federal government founded the SoFFin in response to the turmoil in the aftermath of the collapse of the Lehman Brothers. The fund was designed to strengthen the capital base of German banks that were hit by taking over problematic positions and providing other guarantees. The fund supported a total of 10 German banks since its inception, with a total volume of outstanding equity and guarantees of 192 billion Euros in 2009. By the end of 2015, the SoFFin remained exposed to three German banks, with shares and hybrid capital equivalent to a total volume of about 16 billion Euros. We matched bank names from the Creditreform database, with public information provided by the SoFFin, which supported banks and estimated the following probit model:

The dependent variable in Equation (1) is an indicator that equals “1” for ECF ventures and “0” for non-ECF ventures. Bank health aside, ventures choose a form of financing based on further observable and unobservable characteristics (Manigart & Wright, 2013). Therefore, we specify control variables xi to gauge venture and management traits that influence the choice between debt (Robb & Robinson, 2014) and equity (Cassar, 2004).

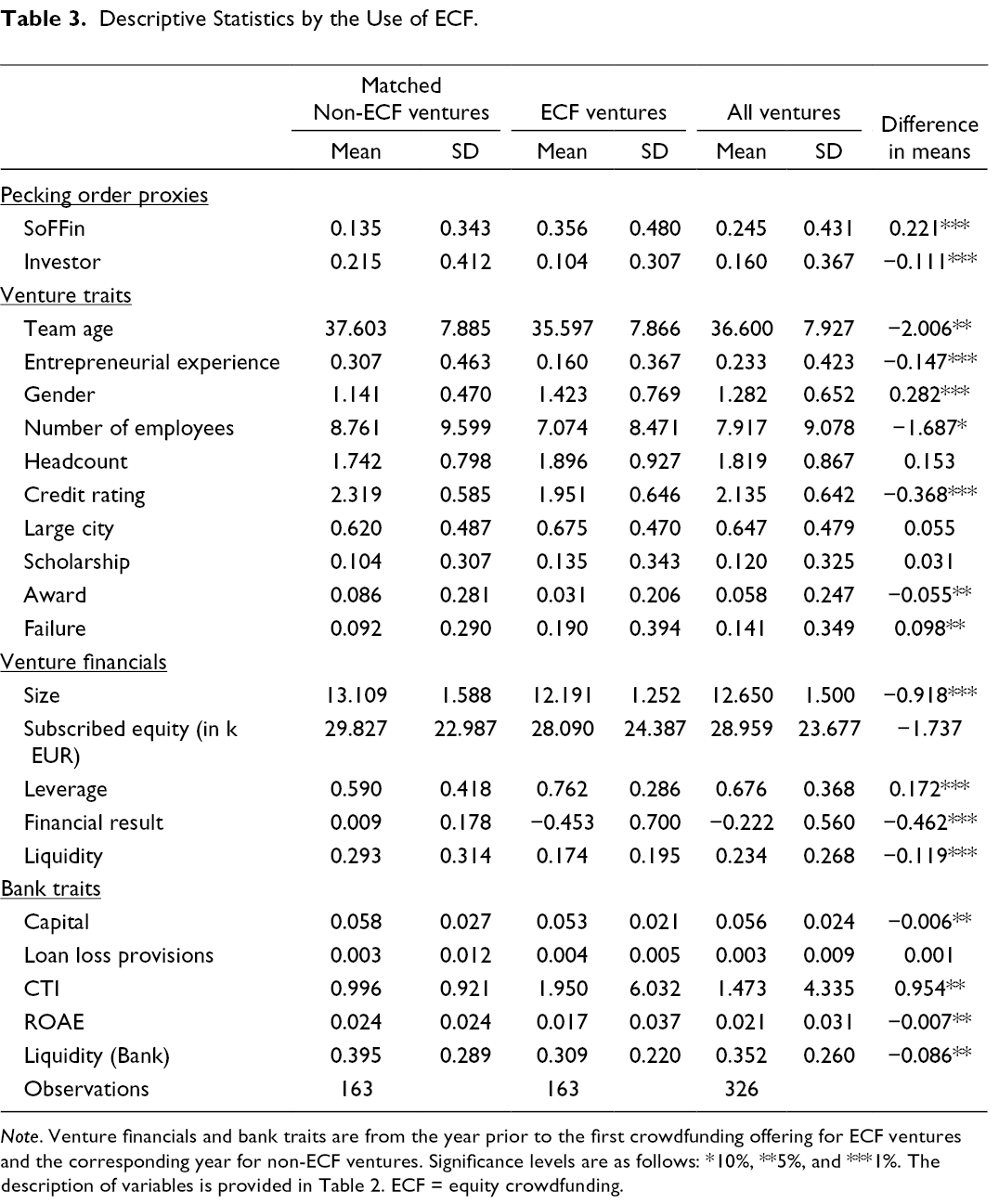

Table 3 shows descriptive statistics for all covariates and tests whether the means differ between the ECF and non-ECF ventures. Consistent with available empirical evidence (e.g., Walthoff-Borm, Schwienbacher, et al., 2018), ECF ventures are smaller, less liquid, perform worse regarding financial results, and have higher leverage. Other venture traits related to the management team, governance, and riskiness of the venture differ significantly. Most notably, ventures that seek ECF have significantly worse ratings and fail more often.

Descriptive Statistics by the Use of ECF.

Note. Venture financials and bank traits are from the year prior to the first crowdfunding offering for ECF ventures and the corresponding year for non-ECF ventures. Significance levels are as follows: *10%, **5%, and ***1%. The description of variables is provided in Table 2. ECF = equity crowdfunding.

Main Result: Determinants of ECF

To assess the role of ECF as a way to mitigate the funding constraints of young ventures, we estimate that the likelihood of new ventures seeking to crowdfund is conditional on whether they are tied to stressed banks and whether they have access to outside equity.

We first consider potential funding constraints that arise, in line with the first hypothesis, from ventures’ relationships to distressed banks, as measured by capital support by the SoFFin. We collect bank relationships for all 326 ventures from the Creditreform and Orbis databases, which we compare with the payment information provided to crowdfunding platforms as well as self-reported information on ventures’ webpages, to control for multiple bank relationships. In total, we identify 83 different banks, of which two were supported by the SoFFin. 4

In addition to these potential bank funding impediment indicators, we specify an empirical test of the second hypothesis, that ECF is less likely used by young ventures if an equity investor is already invested. We collect data on outside equity investors who were already present before the venture started an ECF campaign by gaging changes in the subscribed capital in the years after the foundation and before the use of ECF. Table 3 already revealed that this is significantly more often the case for ventures not engaging in ECF. Whereas 21.5% of non-ECF ventures have an investor on board, only 10.4% of those running an ECF campaign do.

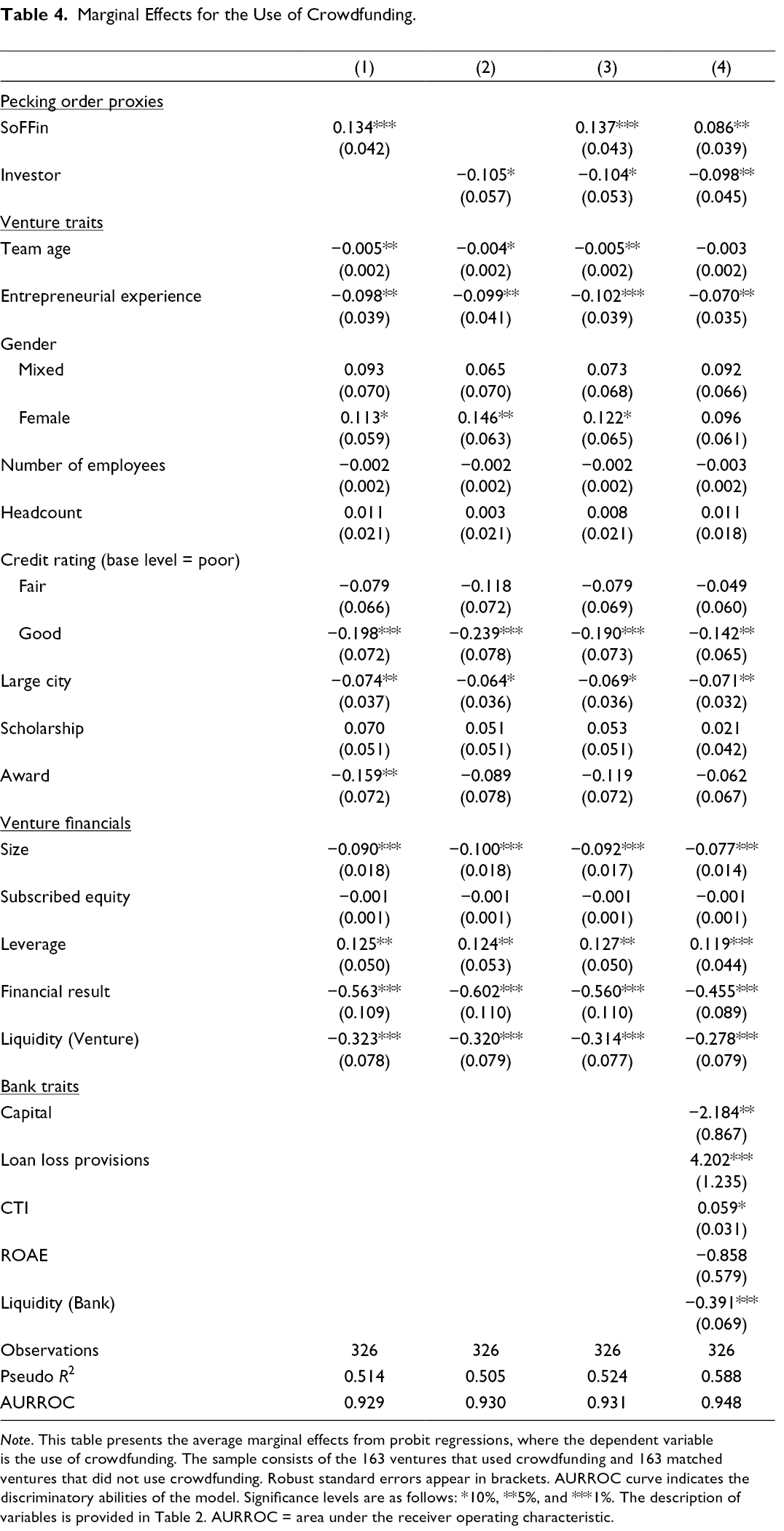

Table 4 provides empirical evidence from regression analyses beyond the descriptive indications in Table 3 to test formally whether we cannot reject Hypotheses 1 and 2. Specifically, we show in Column (1) the marginal effect estimates of the probit model in Equation (1). First, we specify only the potential funding constraints due to an association of the venture with a distressed bank. The parameters of the according SoFFin indicator variable are statistically significant at 1% and positive. This result strongly supports the first hypothesis, that young ventures associated with a distressed bank are more likely to seek ECF funding. The estimated effect is also economically significant. The likelihood of ECF use increases by roughly 13% when a venture’s bank is supported by the SoFFin. Given that we control for important managerial and financial traits of ventures documented in prior literature, this finding is, therefore, consistent with Hypothesis 1. Above and beyond venture characteristics that push entrepreneurs further down in the pecking order of capital structure, the association with a distressed bank further amplifies the tendency to seek equity funding from a presumably uninformed crowd.

Marginal Effects for the Use of Crowdfunding.

Note. This table presents the average marginal effects from probit regressions, where the dependent variable is the use of crowdfunding. The sample consists of the 163 ventures that used crowdfunding and 163 matched ventures that did not use crowdfunding. Robust standard errors appear in brackets. AURROC curve indicates the discriminatory abilities of the model. Significance levels are as follows: *10%, **5%, and ***1%. The description of variables is provided in Table 2. AURROC = area under the receiver operating characteristic.

This inference is further supported by the first test of Hypothesis 2 in Column (2). Here, we specify the second main variable of interest, namely, whether an outside equity investor was already on board before launching an ECF campaign. The statistical result is consistent with the hypothesis that the presence of equity investors renders it less likely that young entrepreneurs seek ECF. The estimated magnitude of a 10% reduction of this probability is also sizeable. But the effect is only statistically significant at the 10% level when ignoring any further information on the health of a ventures’ bank relationship.

Columns (3) and (4), however, provide crucial qualifications regarding this finding. Note first that both hypotheses are also jointly supported when specifying the two indicators of whether an entrepreneur was tied to a distressed bank and when it had an equity investor on board at the same time. The magnitude, direction, and significance of these effects remain largely unaffected. Yet, an important additional concern is that the likelihood of choosing ECF is driven by other bank risk indicators that correlate with the SoFFin indicator and subsequent lending and risk-taking. To avoid this concern, we accept the first hypothesis, based on such a spurious correlation, and include bank-level control variables that gauge the financial health of banks using the CAMEL (capital, asset quality, management quality, and liquidity) supervisory ratings system. We calculate CAMEL variables for the year prior to the first crowdfunding offering for ECF-funded ventures and the same year for all matched non-ECF ventures. 5

Column (4) features two crucial insights. First, both main testing variables remain supportive of the two hypotheses, even after the inclusion of these bank-risk controls. Whereas the association effect with a distressed bank is somewhat smaller with 8.6%, the presence of equity investors is now statistically significant at the 5% level. Second, three of the five specified CAMEL proxies are statistically significant at the 1% and 5% level, respectively. Consistent with the first hypothesis, relationships with banks exhibiting more risky financial profiles render it more likely that entrepreneurs will seek ECF. Less well-capitalized banks are less able to buffer asset price depreciation. Banks with lower-quality assets exhibit higher loan loss provisions relative to total gross loans, which indicates more exposure to credit risk shocks. And finally, lower shares of liquid assets expose banks to random macro and financial shocks. Consistent with Hypothesis 1, we find that higher capital and liquidity ratios at the bank level reduce the likelihood of using crowdfunding, whereas a higher loan loss provisions ratio increases the likelihood. The result corroborates that a relationship with a stable and well-managed bank also reduces the need for young ventures to seek alternative funding from a crowd. The positive SoFFin and the negative outside investor effects remain statistically and economically significant, which implies that these indicators of potential constraints faced by young ventures are unlikely to merely confine unobserved traits as credit supply shocks, again consistent with Hypotheses 1 and 2.

Finally note that goodness-of-fit indicators like the receiver operating characteristic curve (AURROC) corroborate the discriminatory power of the model and show that the probability of using crowdfunding is explained quite well by the model (Hosmer & Lemeshow, 2012). In sum, the results in Table 4 clearly support Hypotheses 1 and 2, indicating that young ventures are more likely to use ECF when more conventional providers of early-stage funding are stressed or absent.

Venture Traits

To assess if our results depend on the degree of information asymmetries and the quality of the venture, we first consider nine well-established venture traits that gauge softer management factors as well as ratings to proxy for the riskiness of the venture.

First, we consider demographics such as age and gender as well as the experience of the management team (MT) (Franke et al., 2008; Hsu, 2007). For each venture, we collect the identity, gender, and birthyear of all MT members from the Bundesanzeiger. We match the identity of each MT member to manually collected information from professional social networks, such as LinkedIn and XING, obtaining the curriculum vitae of each executive. The variable Entrepreneurial Experience equals “1,” if at least one MT member has founded and led a venture before the current undertaking, and “0” otherwise. The effects of Team Age and Entrepreneurial Experience are significantly negative, indicating that younger and less experienced MTs are more likely to use ECF. Both MT traits offer important funding criteria for traditional outside investors, and having ties to a weak bank seems to aggravate these funding hurdles for young entrepreneurs. Gender gauges the composition of the MT. The value “1” indicates male-only, “2” mixed, and “3” female-only MTs. Relative to male-only MTs, the marginal effects for mixed MTs are not statistically significant, but female-only MTs are 10%–14% more likely to tap the crowd. This finding confirms results that female-owned ventures are less likely to obtain external funding (Coleman, 2000).

Whereas previous research reveals that the number of MT members and the number of employees are quality signals to outside investors (Davila et al., 2003), the according marginal effects for the Number of Employees and the MT Headcount are statistically insignificant.

The variable Credit Rating ranges from A (good) to C (poor) and is obtained from the rating agency Buergel. Robb and Robinson (2014) confirm that better external ratings enhance the chances of obtaining a loan, whereas ventures with poor ratings are credit-constrained. Hence, we expect that poor credit scores increase the likelihood of using ECF, as they should amplify already-existing credit supply frictions, which we hypothesize to be characteristic of a relationship with a distressed bank. 6 The estimated marginal effect of a positive credit rating is significantly negative in all models. A good credit rating decreases the probability of using ECF by 14%–24% compared with ventures that have a bad rating.

We also specify a Large City indicator equal to “1,” if the venture is located in a city with more than 500,000 (urban) inhabitants, because most financiers invest only within a close geographic scope in order to reduce distance‐sensitive costs, such as monitoring (De Prijcker et al., 2019). We expect that ECF provides a greater alternative outside the largest cities. The significantly negative marginal effect confirms that ECF is roughly 7% less likely for ventures located in large cities. Put differently, the lack of agglomeration effects due to lackluster loan supply by distressed banks is partly mitigated for ventures residing in urban environments, which offer more funding alternatives.

Finally, we control for the reputation of the venture, which is an important quality signal to reduce information asymmetry when acquiring outside funding (Higgins & Gulati, 2006). Given the short history of new ventures, we focus on awards won in business plan competitions and scholarships, which we both hand-collect and match by venture names to our data. Both credentials symbolize MT capability, establish social standing, and increase the chance of receiving external finance (Howell, 2017), yet either indicator—Scholarship and Award—is insignificant, indicating that winning an award has no statistically significant effect on using ECF.

In sum, our results attribute an important role to more tacit venture traits as well as to credit scores. Less experienced, younger, and female MTs are significantly more likely to tap the crowd. More risky ventures and those residing outside urban areas are more likely to use ECF. The results corroborate our previous findings that ventures of lower quality appear to need funding from a crowd.

Financial Traits

Due to notoriously light public reporting requirements in Germany, we rely on a rudimentary balance sheet and a few indicators of financial performance to control for the impact of five well-established financial variables on the likelihood of the use of ECF. We measure Size as the natural logarithm of total assets to mitigate the influence of outliers. 7 We observe the amount of Subscribed Equity and gauge Leverage as the share of total liabilities to total assets. The Financial Result equals the ratio of annual surplus, or deficit, reported on the balance sheet, relative to the total assets of the venture. Finally, Liquidity is the ratio of cash and accounts receivable to total assets. We compare the data from one year prior to the start of the ECF campaign with the exact same year when the matched venture did not use ECF. 8

The data indicate that financial traits have significant effects on the odds of using ECF for all financial covariates but subscribed equity, as shown in Table 4. Smaller and less profitable ventures, with lower liquidity buffers and more leverage, seek funding from the crowd more often. These results confirm prior evidence (e.g., Walthoff-Borm, Schwienbacher, et al., 2018) and suggest that it is the more risky and potentially more funding-constrained ventures that are attracted by the crowd. Overall, note that the inclusion/exclusion of different control variables does not affect the main results pertinent to our hypotheses.

Competing Failure Hazard

If ventures associated with distressed banks or without external equity are indeed more likely to be pushed into ECF because they are low quality ex ante, we expect that more of these ventures eventually fail ex post, compared with non-ECF entrepreneurs who managed to receive funding elsewhere. To discern the low-quality from the high-quality entrepreneurs along this train of thought, we propose an empirical ad-hoc test that exploits our plentiful manually collected data to reveal successful and unsuccessful ECF ventures. Specifically, we track all ventures, crowdfunded or not, and estimate whether they filed for bankruptcy with their respective courts, conditional on funding sources. 9

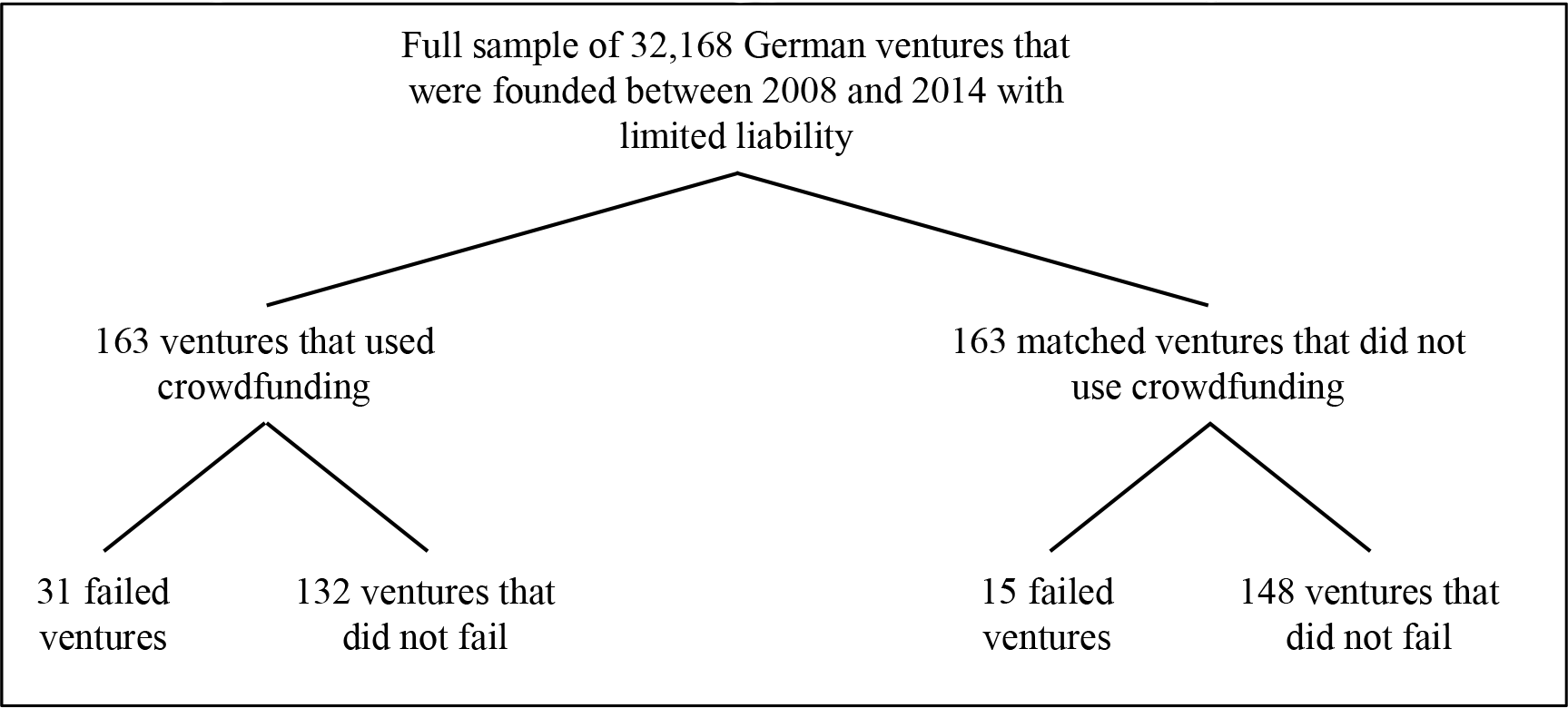

Figure 1 illustrates that out of a total of 326 matched ventures, 46 failed between 2011 and 2016. 10 Note that the unconditional failure rate is significantly higher among crowdfunded ventures compared with noncrowdfunded ones: 19% as opposed to 9%. To operationalize this ad-hoc test on the role played by ECF, distressed bank association, and their interaction to explain the failure of new ventures, we estimate Equation (2) using a probit model as our main workhorse specification.

Sample of new ventures that applied for crowdfunding and failed. Notes. This figure shows the sample of ventures that applied to one of the four largest equity crowdfunding platforms in Germany for funds between 2011 and 2015. To account for the small number of ventures that used ECF in 2015, we extended the observation period for failures by one year. Some ventures applied multiple times for funding. The data on nonapplicants were obtained from the Orbis database. The data about crowdfunding applicants were collected from observing applicant data directly in the online platforms maintained by Companisto, Fundsters, Innovestment, and Seedmatch.

The dependent variable is an indicator Fi equal to “1,” if the venture declared insolvency, and “0” otherwise. Failure indicates whether the projects were ultimately successful or turned out to be low quality, with unpaid bills and, for the most part, a total failure for investors. The variables SoFFin and ECF are indicators equal to “1,” if the venture is associated with a distressed bank and used ECF, respectively. The interaction between both financing forms is then captured by γ, whereas the vector x features the same control variables as before.

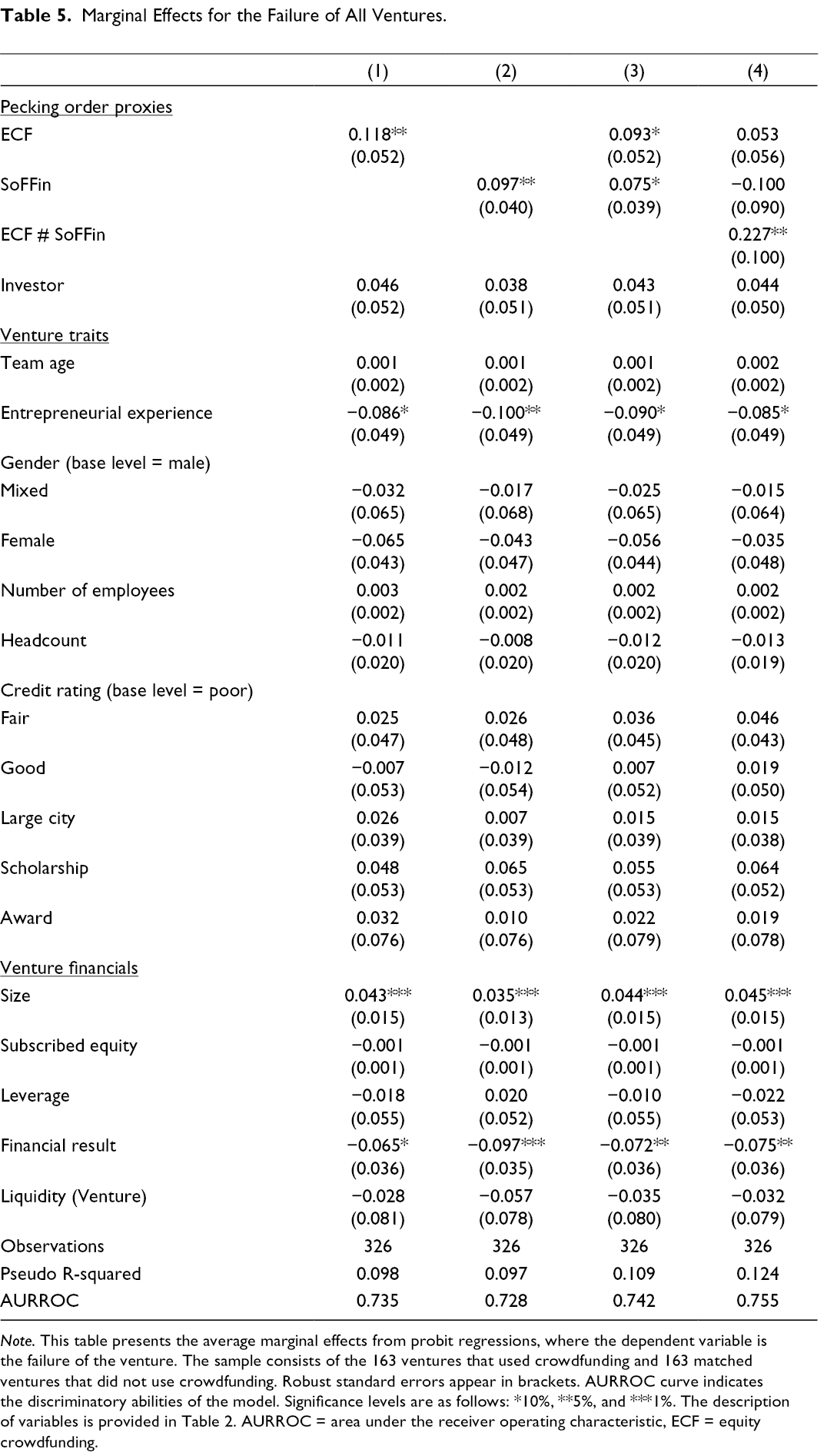

Table 5 shows the results from a reduced form competing for hazard specification using a probit model for the entire sample. We explain failures for the full sample of all 326 ventures, conditional on the presence of the alternative financing forms. Furthermore, we specify all of the tacit venture traits, as well as financial indicators as discussed above, as control variables.

Marginal Effects for the Failure of All Ventures.

Note. This table presents the average marginal effects from probit regressions, where the dependent variable is the failure of the venture. The sample consists of the 163 ventures that used crowdfunding and 163 matched ventures that did not use crowdfunding. Robust standard errors appear in brackets. AURROC curve indicates the discriminatory abilities of the model. Significance levels are as follows: *10%, **5%, and ***1%. The description of variables is provided in Table 2. AURROC = area under the receiver operating characteristic, ECF = equity crowdfunding.

The effect of using ECF on the likelihood of eventual failure is estimated in Column (1), whereas Column (2) shows the marginal effect if the venture is connected to a SoFFin-supported bank. Consistent with Hypothesis 1, failure is significantly more likely for both indicators (ECF and SoFFin) of a venture that is of lower quality and therefore pushed further down in the pecking order of capital. The estimated marginal effects indicate an increase of around 12% and 10%, respectively. These magnitudes are substantial given an unconditional failure probability of 14% (=46/326). These results show ECF is associated with lower-quality entrepreneurs. The presence of an outside equity investor, in turn, has no significant effect on the occurrence of insolvencies. This result might indicate that, compared to stressed banks and an uninformed crowd, early-stage financiers with skin in the game are more successful in avoiding the low-quality entrepreneurs in the applicant pool.

As a simple first-pass inspection regarding whether it is the relationship to a distressed bank in itself or, rather, the resulting push of young entrepreneurs into ECF that renders subsequent failure more likely, we specify both proxies for low-quality ventures in Column (3). The respective marginal effects remain intact regarding magnitude, sign, and significance compared to Columns (1) and (2). That the discriminatory power of the model improves slightly suggests that either aspect of being a venture of inferior quality has an individual influence on failure likelihood.

Column (4) tests more explicitly whether ventures that maintain both ties to bad banks and funding from the crowd are particularly endangered by failure. To gauge any such undesirable interaction when both sources of funding occur at the same time, we specify an according parameter, which is significantly positive and large in Column (4). At the same time, both individual indicators are no longer statistically different from zero. This result thus underpins that the hike in failure probabilities is driven by the subgroup of new ventures that face credit constraints from bad banks and receive, at the same time, funding from uninformed crowd investors. Potentially, stressed and inattentive bankers continue lending without monitoring well, which an uninformed crowd is misreading as a signal of quality. This interpretation is further supported since we do account for a range of well-established drivers of failure among young entrepreneurs in the form of venture traits and financials. This approach mitigates concerns that we merely gauge omitted factors with our proxies for the quality of financiers that drive ventures down the pecking order of finance. Specifically, we find that more experienced and financially successful ventures are significantly less likely to fail, while, within this group of generally small young entrepreneurs, only the relatively large ones file for insolvency with the courts when they go out of business.

The ad-hoc nature of this empirical test is clearly subject to a number of limitations. At the same time, we provide in the online appendix some important indications that these findings are not driven by the choice of estimation method. Table OA4 demonstrates that the results for the main test variables, SoFFin and ECF, remain qualitatively unaffected when using, instead of a probit model as in Equation (2), a Cox proportional hazard rate model, a logit model, or a linear probability model, respectively. Related, we rule out the very reasonable concern that the failure probability result is subject to selection bias by some ventures into ECF. The results from the second stage of an accordingly specified Heckman selection model in Table OA5 also confirm the qualitative results reported here.

Overall, the ad-hoc tests on this rich manually collected sample reveal rather robustly that ventures tied to distressed banks that use ECF are also significantly more likely to eventually fail, compared to non-ECF-funded ventures that are not connected to bad banks. As such, this evidence points towards the conclusion that the low-quality entrepreneurs especially seek funding from the crowd.

Discussion, Policy Implications, and Future Research

In this paper, we hypothesize that entrepreneurs who are tied to more risky banks are more likely to be low quality. A large sample of ECF campaigns in Germany shows strong evidence that connections to distressed banks push entrepreneurs to use ECF. We find some evidence, albeit less robust, that entrepreneurs who can access other forms of equity are less likely to use ECF. Finally, the data indicate entrepreneurs who access ECF are more likely to fail.

There are potentially two types of ventures that are in our matched samples: those that did not apply for crowdfunding and those that did apply for crowdfunding but were not listed by the platform. Most likely, the matched sample comprises the former and not the latter, given the breadth of the potential matched sample comprised of over 32,000 start-ups; the ECF ventures in our sample comprise 163 start-ups. Therefore, our evidence implies that, on average, the quality of entrepreneurial ventures that seek ECF in Germany is lower than the quality of ventures that do not seek ECF after matching. The evidence does, therefore, not imply that crowd investors are bad at screening projects; rather, the evidence implies that the average quality of ventures is lower in ECF, and investors are willing to take the risk and make crowdfunding investments with a preference for skewness in terms of hoping for outlier positive returns from some investments.

Our evidence does not directly enable an assessment of whether or not ECF investors are worse at screening and due diligence. That type of wisdom of the crowd argument could only be tested with data unavailable to us. Essentially, what would be needed would be to take into consideration that the crowd selects projects among the deal-flow preselected and suggested by the ECF platform. So, the backers do not select among all start-ups or all fundraising start-ups, but select those among the start-ups applying to ECF platforms, and those selected by the investment’s platforms. It would be interesting to compare start-ups: (1) applying to the ECF platforms but who were not selected by the teams, (2) the selected start-ups not financed by the crowd, and then (3) the ECF’s financed start-ups. With a such comparison, future scholars could comment on the capacity of crowdfunders to evaluate and screen ECF projects. Our data do not allow for this type of analysis, but we hope future scholars will be able to obtain such data.

Our evidence nevertheless does contribute to our understanding of adverse selection and how pronounced it can be in ECF. The most direct policy implications for our research focus on information sharing for investors. Investors should be made fully aware of the risks associated with ECF through information disclosed on the platform webpages and through online material made available alongside crowdfunding regulations disclosed from securities authorities. Moreover, our findings imply that regulations that limit the amounts of investment per year from retail investors, as well as regulations that limit the amount of ECF capital that can be raised by entrepreneurs per year can mitigate the potential losses associated with crowdfunding relative to what might be achievable, on average, from investing elsewhere. At the same time, ECF enables entrepreneurs’ access to capital and investors access to the possibility of superior returns with potential outlier projects.

It is important to highlight the fact that the estimates here are based on the average venture in the sample and not the outliers. There are two types of outliers: (1) very bad and, in some cases, even fraudulent ventures and (2) extremely successful ventures. Markets like crowdfunding, with very low listing standards, are often viewed like lotteries, as the payoffs are very skewed and can be enormous for a small number of very successful ventures. For example, some ECF ventures have turned out to be extremely successful, such as Rewalk Robotics Ltd, which achieved an IPO in 2014 on NASDAQ. 11 As such, understanding the motives of ECF investors is somewhat akin to understanding the economics of lottery markets and junior stock exchanges with very low listing standards (Carpentier et al., 2012). Conversely, there is some work on the context of rewards-based crowdfunding that shows that rates of fraud are substantially lower than that which is observed on public stock exchanges (Cumming et al., 2016). In addition to the due diligence implications of this study for policymakers and practitioners, there are related implications for the overall design of support programs in entrepreneurial finance. Our evidence appears to be consistent with the view that crowdfunding fills an even more risky spectrum of the early-stage financing market than do traditional equity investors. But, future work is needed to better understand the intersection between the different forms of finance; the optimal mix of VC, debt, and crowdfunding in different economic and institutional environments; and the efficient role for legislation and government programs, so that each of these segments might best complement another.

Our findings are certainly consistent with the presence of extreme information asymmetry between entrepreneurs and investors in ECF campaigns. Likewise, as researchers, we do not observe all of the characteristics of the entrepreneurs. We are not fully able to assess whether the results are driven by unobserved characteristics of the management team, project, technology, or industry. Future research with more fine-tuned data and/or different institutional settings might shed additional light on these issues. This type of work would inform not only academics about pronounced sources of information asymmetry but also continue to inform practitioners in their due diligence checks and policymakers with optimal design of regulatory structures.

Conclusion

External finance is crucial to entrepreneurial activities. However, continental Europe is plagued by scarce early-stage capital. Moreover, poor bank profitability, paired with tighter regulations to combat risk-taking after the financial and sovereign debt crises, imply that young ventures’ access to bank credit is hampered.

In this paper, we test whether the emergence of ECF as an innovative form of external funding is both attractive and successful for such ventures. Thereby, we shed light on the broader question of whether ECF is conducive to match small denomination savers efficiently with innovative projects or if an uninformed investor crowd is more likely lured by proverbial low-quality entrepreneurs from the project pool. Also, in response to recent calls to better understand how different sources of funding interact (e.g., Cumming et al., 2018, Cumming, Deloof, et al., 2019), we examined the intersection of bank finance and ECF.

To this end, we manually collect a sample of 326 German ventures, of which 163 ran an ECF campaign, between 2008 and 2015. To gauge potential funding constraints faced by these ventures, we collect their bank relationship(s) to approximate potential credit frictions. These ventures do business with 83 banks, underscoring the importance of bank credit in the German financial system, even as an early-stage financier. Also, we identify whether or not an equity investor was invested in the venture, which should reduce funding constraints. This information is combined with hand-collected and web-crawled data on financials, ratings, management teams, and campaign-specific traits to specify a regression model that explains two main questions. First, can we identify the determinants of young ventures’ choices to tap the crowd for funding? And, second, how likely are crowdfunded ventures to fail? Failure would ultimately unveil these ventures as low-quality rather than high-quality projects not efficiently selected by the mechanisms in ECF.

An important first result is that young ventures are significantly more likely to use ECF if they are connected to banks that were bailed out by the German government after the financial crisis. Likewise, the presence of an outside equity investor reduces these odds substantially. Thus, it seems that tighter funding constraints induce ventures to take to the crowd for funding.

Moreover, we find that ventures do not choose ECF randomly. Our evidence clearly points to a lower likelihood for ventures that are larger, more liquid, less unprofitable, and rated well to use ECF. Besides financial profiles and credit ratings, we also provide evidence that more tacit indicators, in particular, management team traits, matter in the choice of ECF. Specifically, younger and less experienced management teams with female participation tend to use ECF more often. Together, these results suggest that ventures of lower-quality consider the less conventional method of ECF to raise external finance.

We also assess whether projects that use ECF are more likely or not to be successful for the investors. Specifically, we conduct an analysis based on manually collected insolvency data for each of the 326 ventures between 2011 and 2016. The results imply that ventures tied to distressed banks and that use ECF are also significantly more likely to eventually fail, compared to non-ECF-funded ventures that are not connected to bad banks. As such, this evidence points again toward the conclusion that especially the low-quality entrepreneurs seek funding from the crowd.

Supplemental Material

Supplementary Material 1 - Supplemental material for Equity Crowdfunding: High-Quality or Low-Quality Entrepreneurs?

Supplemental material, Supplementary Material 1, for Equity Crowdfunding: High-Quality or Low-Quality Entrepreneurs? by Daniel Blaseg, Douglas Cumming and Michael Koetter in Entrepreneurship Theory and Practice

Footnotes

Acknowledgments

This article is based on the doctoral dissertation of the first author at Goethe University Frankfurt. We are grateful to Editor Sophie Manigart and the entire anonymous review team for their excellent comments and guidance. We are grateful for feedback received from participants at the SFA conference, EntFin Lyon conference, and the P2P Financial Systems Bundesbank/SAFE/UCL conference as well as seminars at Goethe University Frankfurt. We owe thanks to many colleagues whose suggestions helped in the development of this manuscript and specifically want to thank Lars Hornuf, Christoph Siemroth, Armin Schwienbacher, Bernd Skiera, and Adalbert Winkler for their detailed feedback.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

Supplemental Material

Supplemental material for this article is available online.

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.