Abstract

This study considers the Opera del Duomo in Pisa, the organisation tasked with building the world-renowned complex located in the Square of Miracles, from its inception to the formation of the Grand Duchy of Tuscany in the sixteenth century. It draws upon Besharov and Smith's understanding of hybridity to document the factors driving the transition from a form of hybridity characterised by a high level of conflict between the logics of the State, the Church and the Commune of Pisa to a form in which the State logic dominated over the others and conflict was overcome. The article unveils how the regulatory power of the State generates changes in the interactions among logics over time, with particular attention to the role of accounting and accountability practices. It shows how historical studies help to untangle situations in which logics coexist in extreme conflict and identify new ways to engage with them.

Introduction

Organisational hybridity is gaining prominence in the accounting literature, which has begun to explore the place of accounting in hybrid organisations, whose defining characteristic is the presence of multiple logics, each reflecting the expectations of the different actors that characterise a particular field (Battilana and Lee, 2014; Lounsbury et al., 2021). This is common to organisations operating in many fields, such as healthcare, social enterprises and cultural industries (Besharov and Smith, 2014; Maran and Lowe, 2022). Logics may coexist peacefully in some organisations whilst being in extreme conflict in others (Besharov and Smith, 2014).

Studies have explored accounting as a managerial tool that organisations can use to manage conflicting organisational principles arising from different logics (Begkos and Antonopoulou, 2022; Gooneratne and Hoque, 2016; Järvinen, 2016; Kaufman and Covaleski, 2019). Research has shed light on the interconnection between accounting and organisational processes, showing how accounting can inform actions aimed at balancing contrasting logic prescriptions over time (Lepori and Montauti, 2020; Miller and Power, 2013). Other work has highlighted the limitations of accounting as an instrument to manage hybridity (Clune et al., 2019; Ferry and Slack, 2022; Morinière and Georgescu, 2022; Rautiainen et al., 2022). Accounting has been mainly framed as a managerial tool that tends to make an economic logic prevail within an organisation over others, such as those related to social objectives.

New perspectives are emerging which seek to provide insights into the role of the regulatory power of the State in influencing the interrelation between multiple logics within organisations and the related function of accounting. Through regulatory interventions at the organisational and field levels, the State can intervene in the ways in which organisations manage the plurality of logics (Convery and Kaufman, 2022; Kurunmäki and Miller, 2011; Munzer, 2019). At the field level, the State can rearrange institutional logics, key actors and resources, thereby reframing the broader institutional field in which the organisation operates (Munzer, 2019). At the organisational level, the State can directly influence logic instantiations within an entity by regulating the organisational structures and control practices, such as management accounting practices, reporting practices and corporate governance, which organisations use to manage logics’ pluralism (Convery and Kaufman, 2022; Hooks and Stewart, 2015). Nevertheless, a holistic view is still lacking of the factors both at field and organisation levels on which the State can intervene to manage organisational hybridity. Much is still to be learnt about how the State can succeed in asserting one logic over others through its regulatory interventions, but in a way that ensures compatibility between existing logics, thereby minimising conflict. Therefore, this study addresses the following research questions: (1) How does the State intervene through regulatory interventions at the field and organisation levels to manage organisational hybridity? (2) In the context of these State interventions, what role do accounting and accountability practices play?

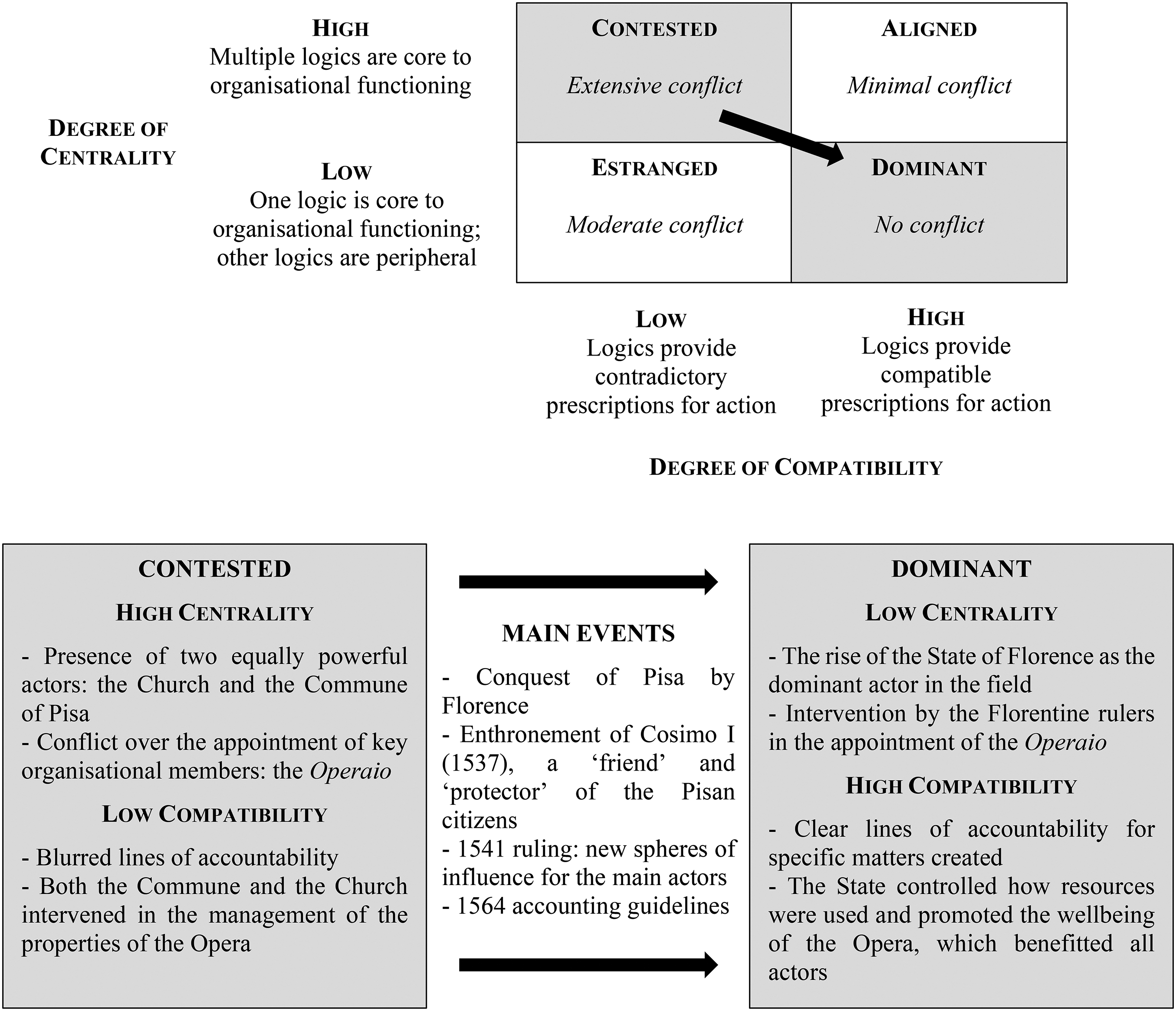

This study considers the forms of hybridity experienced by the Opera del Duomo in Pisa (hereafter the Opera); an independent organisation tasked with building a monumental cathedral complex (Fusco, 1903). This complex still represents the heart of the city of Pisa in the world-famous Square of Miracles, with its ‘leaning tower’. The Opera offers the opportunity to analyse the unravelling of the complex interrelations among different logics existing within the same organisation over an extended period of time. As the richest and most important organisation in Pisa, soon after its establishment in the eleventh century the Opera attracted the attention of the most powerful actors in the city, namely the Commune of Pisa and the Church. Following the conquest of Pisa by Florence, a third actor was added, the Florentine State. Each of these actors brought its own logic as it sought to influence the functioning of the Opera. The study focuses on the Opera from its establishment until the formation of the Grand Duchy of Tuscany at the end of the sixteenth century, when the rulers of the Grand Duchy, the Medici family, managed to shape the hybridity of the Opera in a way that ensured that the organisation could be used as an instrument of public policy to increase the power of their State.

This article draws upon Besharov and Smith's (2014) conceptualisation of hybrid organisations. To Besharov and Smith (2014), the ways in which logics are instantiated within organisations are heterogeneous and depend on several interconnected factors. These factors influence the degree to which logics are compatible with each other and how much they influence key organisational practices, leading organisations to experience different forms of hybridity over time. The study identifies the field and organisation level factors through which the Medicean State intervened, especially accounting and accountability practices. It shows how changes in these factors enabled an evolution from a form of contested hybridity, in which different logics conflicted with each other, to a form of dominant hybridity, in which the logic of the State became dominant, and the logics of the Commune of Pisa and the Church contributed to reinforcing it. In doing so, the article answers Besharov and Smith's (2014) call to carry out longitudinal studies to investigate the changes in hybridity forms over time and their driving forces.

Recognising that ‘society has always organized itself in complex ways to face societal challenges, and that logics’ multiplicity is an established characteristic for many organizations, also historically’ (Lusiani et al., 2023: 196), the study joins the literature that has started to explore the historical roots of organisational hybridity (Antonelli et al., 2017; Lusiani et al., 2019, 2023). Investigations of early forms of hybrid organisations can help to untangle institutional complexity, that is, situations in which logics coexist in extreme conflict (Greenwood et al., 2011), and identify new ways to engage with it. By adopting this original perspective, the article also contributes to the emerging literature on the ways in which organisational hybridity is influenced by the State's regulatory power (Convery and Kaufman, 2022; Kurunmäki and Miller, 2011; Munzer, 2019). It offers a holistic reading of the field and organisation level mechanisms through which the regulatory power of the State acts and generates changes in the interactions among logics over time. In doing so, the work offers new insights into the potential of accounting and accountability practices as means by which regulatory power can intervene to ensure a peaceful coexistence of logics over time (Begkos and Antonopoulou, 2022; Hooks and Stewart, 2015; Lepori and Montauti, 2020). The article also broadens the compass of previous research that has framed accounting as a tool that mainly contributes to spreading an economic logic in an organisation (Ferry and Slack, 2022; Hooks and Stewart, 2015; Morinière and Georgescu, 2022; Rautiainen et al., 2022). It does so by providing evidence of the role of accounting in supporting logics other than those limited to the efficient use of resources, in particular a logic whose main goal is increasing the influence and splendour of a State (Baños Sánchez-Matamoros and Gutiérrez-Hidalgo, 2012; Bigoni et al., 2018, 2023).

The remainder of the article is organised as follows. The next section presents the theoretical framework informing the study. This is followed by a review of the accounting literature on organisational hybridity and by an explanation of the method used in carrying out this research. After an historical introduction to the Opera as an early form of hybrid organisation, the unfolding of the institutional logics within the Opera from its foundation to the formation of the Grand Duchy of Tuscany is presented. The last section provides a discussion of the findings and concluding remarks.

Theoretical framework

Institutional logics are ‘the socially constructed, historical pattern of material practices, assumptions, values, beliefs and rules by which individuals produce and reproduce their material subsistence, organize time and space and provide meaning to their social reality’ (Thornton and Ocasio, 1999: 804). Institutional logics arise from external socially constructed stimuli and motivate internal mental cognition by bringing the content of societal institutions into individual and organisational actors. They provide insights on how external actors operating in a particular realm of social life attempt to influence organisations by infusing their values and beliefs into organisational action (Friedland and Alford, 1991; Thornton, 2009; Thornton et al., 2012). Institutional logics are historically contingent; they can change over time according to changes affecting the external actors they are related to (Ocasio et al., 2017). External actors not only constrain but also empower internal organisational members. Internal organisational members’ behaviour tends to be consistent with existing institutional logics, but at the same time their practices and ways of being influence rules, relations and distributions of resources, thus reinforcing or weakening institutional logics’ instantiations within an organisation (Thornton et al., 2012).

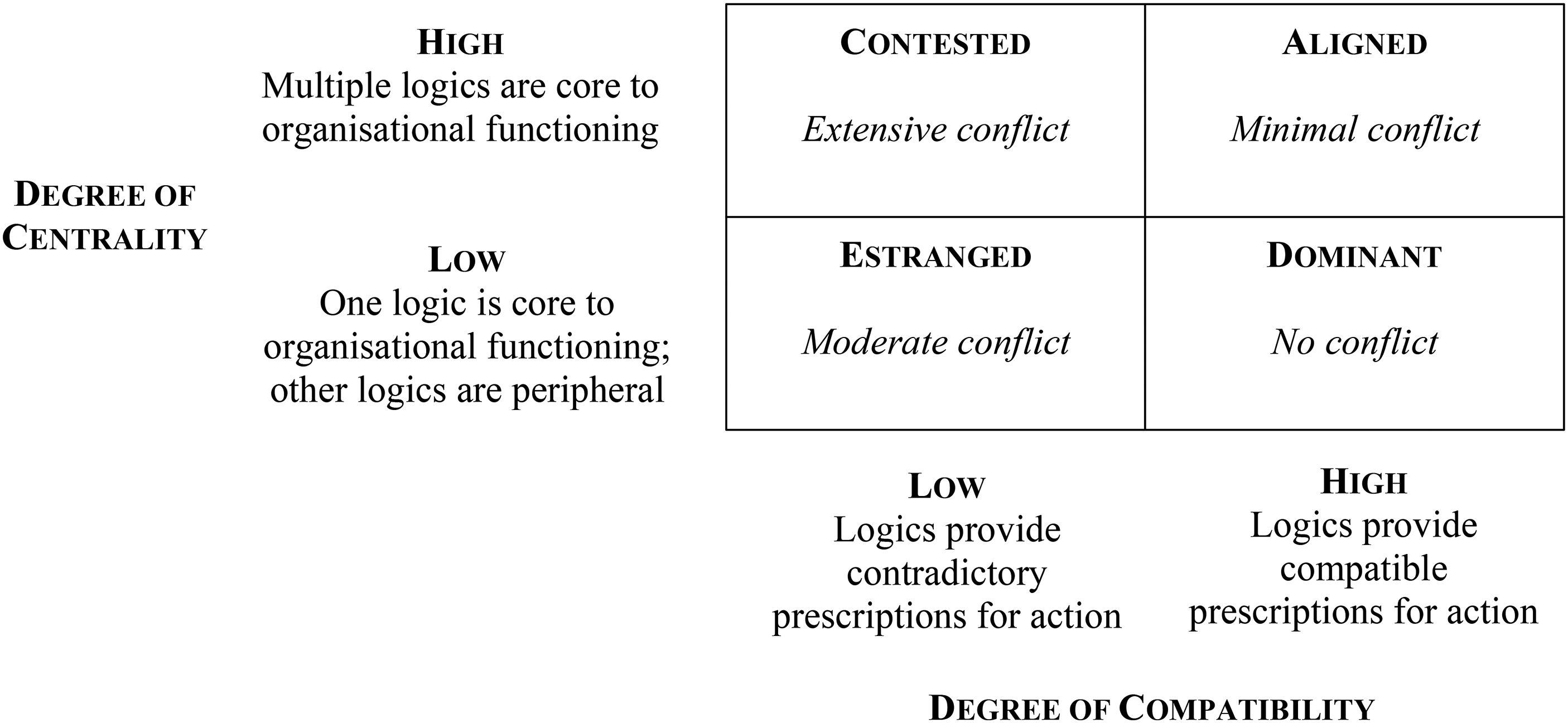

Organisational fields usually witness the coexistence of multiple logics (Besharov and Smith, 2014; Lounsbury et al., 2021). Consistently, many organisations are characterised by hybridity for they combine multiple logics in their structure and practices (Besharov and Smith, 2014; Greenwood et al., 2011). The presence of multiple logics can generate conflict in some organisations (Jakob-Sadeh and Zilber, 2019), whilst in others these logics may blend and coexist (Binder, 2007; McPherson and Sauder, 2013). Besharov and Smith (2014) recognise ideal types of hybrid organisations, each with different levels of internal conflict. They identify two dimensions along which hybridity varies within organisations, centrality and compatibility, and the factors affecting this variation.

Centrality is ‘the degree to which multiple logics are each treated as equally valid and relevant to organizational functioning’ (Besharov and Smith, 2014: 369). High centrality occurs when multiple logics influence key processes whilst with low centrality only a single logic is central to core organisational functioning and the others are limited to peripheral activities. Centrality is determined by factors at the field, organisational and individual levels. At the field level, centrality is affected by the structure of the field and the power of actors operating in such field. Powerful external actors can influence the way in which the organisation functions and the goals it pursues. In fields where different powerful actors exist, the logics associated with those actors end up being infused into core organisational practices, and, as a result, centrality increases (Besharov and Smith, 2014).

At the organisational level, the mission and strategy of an entity expose it to specific institutional logics (Besharov and Smith, 2014). Furthermore, the level of dependence of an organisation on field-level actors determines the extent to which the said organisation absorbs the logics associated with such actors into core organisational practices. When an organisation depends on a specific external actor for resources, it will implement the logic associated with that actor, and its logic becomes more central to organisational functioning than logics associated with other actors operating in the same field. This causes a decrease in centrality. Conversely, in the case of lack of dependency, an organisation may resist prioritising a particular logic and thus it may experience increasing centrality. Additionally, an organisation can seek to implement a strategy to increase centrality. For example, it can alter its core practices to reduce its dependency on a powerful field actor in favour of a less powerful one (Besharov and Smith, 2014).

At the individual level, the extent to which organisational members adhere to logics is crucial. Members with strong ties to a particular actor will tend to be more influenced by the logic associated with that actor, which fuels a low level of centrality. By contrast, when members are tied to multiple field actors, organisations may experience higher centrality. Lastly, the relative power of organisational members influences the degree of centrality. When the members of an organisation have equivalent power, the logics they promote are more likely to be incorporated into core organisational practices. This implies an increasing level of centrality. If just a few individuals hold power, only the logic they carry will influence core organisational practices, which reduces the centrality of logics (Besharov and Smith, 2014).

To Besharov and Smith (2014: 367), compatibility is ‘the extent to which the instantiations of logics imply consistent and reinforcing organisational actions’. A lower degree of compatibility emerges when different external actors promote organisational goals that are inconsistent with each other. At the field level, compatibility is affected by the number of actors operating within an institutional field and the relationship between them. For example, a low level of compatibility may arise when multiple actors are active in a field and each of them claims jurisdictional control over an organisation, whilst a high level of compatibility may emerge if a single actor is active in a field, or if a particular actor dominates others. A high degree of compatibility may also be the result of multiple actors being active in the field, but whose claims do not overlap (Besharov and Smith, 2014).

At the organisational level, hiring and socialising practices have a key role in determining which actors operate within the organisation, and, hence, which logics they will promote and the related degree of compatibility (Besharov and Smith, 2014). At the individual level, actors selectively draw on and enact institutional logics (McPherson and Sauder, 2013) and through their practices they can reinforce or mitigate the influence of institutional logics over behaviours (Begkos and Antonopoulou, 2022). Extra-organisational relationships affect the degree of agency exercised by organisational actors on institutional logics. This means that in the case of strong links between organisational actors and field-level institutions, organisational actors can strengthen the influence of the logics of these institutions. Weak links between organisational actors and institutions allow actors not to enact fully institutional logics, with positive effects in terms of logics’ compatibility (Greenwood et al., 2011).

Centrality and compatibility have been combined by Besharov and Smith (2014) to identify four ideal types of hybrid organisations, each characterised by a particular level of internal conflict (see Figure 1).

Ideal types of hybrid organisations.

Contested organisations experience low compatibility and high centrality, which result in extensive internal conflict. In this case, multiple institutional logics vie for jurisdictional control within the organisation and provide multiple and divergent prescriptions which are all central to core organisational actions. All these issues generate conflict in relation to the organisation's mission, strategy, structure, power, resources and identity, which determine instability inside the organisation and threatens its survival. Estranged organisations have low compatibility and centrality. Despite the presence of multiple institutional logics, only one is dominant and central to core organisational functioning. These organisations exhibit lower conflict than contested organisations for a dominant logic guides organisational action, and others remain at the peripheral level. Any internal conflicts that may arise because of low compatibility between logics are normally resolved in favour of the dominant logic.

In aligned organisations, both compatibility and centrality are high. These organisations experience minimal internal conflict. High centrality means that multiple logics influence core organisational functioning. The high level of compatibility among these logics in an aligned organisation prevents the development of significant levels of conflict (Besharov and Smith, 2014). Finally, dominant organisations display a high level of compatibility and a low level of centrality. This type of hybridity is characterised by the absence of any internal conflict, as multiple logics coexist within these organisations. Even if organisational actors draw on multiple logics, these logics provide coupling prescriptions and are complementary to those of the dominant logic. As such, a dominant logic guides organisational action, and the other logics at the peripheral level contribute to reinforcing the dominant one. This type of hybridity can lead to a process of assimilation of peripheral logics into the dominant logic (Clune et al., 2019; Thornton et al., 2012).

Literature review

Accounting in hybrid organisations

The origins of hybrid organisations are traditionally traced back to the 1980s, when a conflation of social and market values in organisations arose from the advent of the New Public Management and social pressure for responsible and sustainable behaviour by corporations (Miller et al., 2008). Nevertheless, recent literature has sought to broaden this view by showing how hybridity has characterised organisations even in the distant past, with accounting a particularly important tool to manage institutional complexity.

By investigating the sixteenth-century Scuola Grande di San Rocco, where public, private and religious logics intersected, Lusiani et al. (2019) found that governance arrangements and accounting practices were important in ensuring that these different logics could peacefully coexist in the achievement of the organisation's goals. Further work by Lusiani et al. (2023) focused on the Ca’ di Dio hospice between the fourteenth and the sixteenth centuries. The study questions the oft-assumed tension between different logics that affect organisational functioning and shows how accounting can be an effective tool in the day-to-day management of non-profit entities. Considering the nineteenth-century Royal Silk Factory of San Leucio, Antonelli et al. (2017) identified the ways in which double-entry bookkeeping and labour accounting were used to support the pursuit of both social and economic goals. These pioneering studies challenge the assumption that hybrid organisations are a recent phenomenon and offer insights into organisational functioning that can assist in untangling institutional complexity even in modern organisations.

The much more abundant literature that has investigated contemporary settings has also explored the enabling power of accounting in managing institutional complexity. A wide range of practices have been studied, including management accounting (Begkos and Antonopoulou, 2022; Gooneratne and Hoque, 2016; Järvinen, 2016; Kaufman and Covaleski, 2019; Lepori and Montauti, 2020; Morinière and Georgescu, 2022) and social and financial reporting (Argento et al., 2019; Clune et al., 2019; Ghio and Verona, 2022). Accounting has been depicted as a mechanism that neutralises conflicts between institutional logics by keeping conflicting logics separate (Siti-Nabiha and Scapens, 2005) or by acting as a reconciliation tool that combines elements from different logics (Kaufman and Covaleski, 2019; Miller et al., 2008; Thomson et al., 2014). Recent perspectives have moved beyond a view of accounting as a means for neutralising conflict to an understanding of accounting as a tool for mediating conflict.

This latter perspective emphasises the role of accounting in giving a voice to multiple logics, facilitating the coexistence of diverse logics’ material and symbolic bases (Begkos and Antonopoulou, 2022; Ghio and Verona, 2022). Accounting and its links with different organisational structures and decision-making processes have also attracted the attention of scholars (Ghio and Verona, 2022; Lepori and Montauti, 2020; Miller and Power, 2013). Accounting can have a critical role within organisational processes, which through feedback loops determine actions in response to the need to maintain both internal stability and flexibility following external changes. Lepori and Montauti (2020) showed that accounting in the form of budgeting practices may enable organisations to break down the decision-making process into sub-processes, which creates spaces where actors supporting different logics can engage with each other instead of generating ideological conflicts. Ghio and Verona's (2022) study found that accounting practices in the form of social and financial reports can balance different actors’ interests and concerns, and ease tensions associated with institutional complexity.

Other studies shed light on the limitations of accounting as a mechanism to manage institutional complexity (Clune et al., 2019; Ferry and Slack, 2022; Morinière and Georgescu, 2022; Rautiainen et al., 2022). Whilst the use of accounting technologies may ease conflicts between actors in the short term, in the long term these technologies may be perceived as ineffective in supporting organisations in attaining diverse logic prescriptions (Ferry and Slack, 2022; Morinière and Georgescu, 2022). Within hybrid organisations, accounting may fuel the prevalence of an economic logic over others (Battilana, 2018; Ferry and Slack, 2022). Dissatisfaction with accounting may create frustration among groups that are not represented by an economic logic and intensify conflict (Morinière and Georgescu, 2022; Rautiainen et al., 2022). Moreover, accounting can make previously undisclosed contradictions between logics visible, thereby increasing incompatibility between logics (Clune et al., 2019). Organisations can even use accounting to comply superficially with an emergent logic for legitimacy purposes, which curtails accounting's potential as a tool to ensure compatibility between the emergent and existing logics (Conrath-Hargreaves and Wüstemann, 2019a).

State intervention in hybrid organisations

Recent studies have investigated how the State as an external actor exogenously influences the unfolding of institutional logics within hybrid organisations (Convery and Kaufman, 2022; Gooneratne and Hoque, 2016; Hooks and Stewart, 2015; Järvinen, 2016; Munzer, 2019). With the advent of the New Public Management, hybrid organisations have been used as public policy tools to pursue both the social logic associated with public service delivery and the efficiency-driven economic logic (Opara and Rouse, 2019). Scholars have primarily focused on the role of the State as a provider of funding and on how hybrid organisations act to ensure a steady flow of resources (Conrath-Hargreaves and Wüstemann, 2019b; Järvinen, 2016). The influence exerted by the State on hybrid organisations through its regulatory power is less investigated (Convery and Kaufman, 2022; Kurunmäki and Miller, 2011; Munzer, 2019). Using regulation, the State can rearrange institutional logics, key actors and resources, thereby reframing the broader institutional field (Hooks and Stewart, 2015; Lounsbury, 2008; Zhang et al., 2014). Regulatory power can resolve situations of conflict between logics at the field level and impose a dominant logic with related effects on the organisations operating in that field (Munzer, 2019). Munzer's (2019) study of French post-crisis financial market reforms demonstrates how policymakers enlisted regulatory rule-making processes in defending the dominant logic of the market. Moreover, State power can influence directly the life of a hybrid organisation by supporting a particular logic over others (Convery and Kaufman, 2022; Hooks and Stewart, 2015). This can be achieved through regulatory interventions on the organisational structures and control practices, such as management accounting practices, reporting practices and corporate governance, which organisations use to manage institutional pluralism. Hooks and Stewart's (2015) analysis of State intervention in the organisational life of an electricity provider in New Zealand shows that the State succeeded in imposing an economic logic by co-opting accounting practices, which were used to rationalise a cultural shift from a consumer orientation to a shareholder orientation. Additional insights are provided by Convery and Kaufman (2022), who shed light on the role of the State in influencing the unfolding of institutional logics in a non-profit power marketing organisation during a period of environmental turbulence. The intervention of the State can neutralise the effect that turbulence in the external environment may have on the deployment of logics within an organisation. By imposing a floor level of required spending and administrative procedures related to the budgeting process, the State can control which logic will dominate over the others (Convery and Kaufman, 2022).

Methods

The analysis of the Opera as a hybrid organisation focused on a period that starts from the Opera's inception in the eleventh century to the formation of the Grand Duchy of Tuscany in the sixteenth century. Besharov and Smith (2014) suggested using longitudinal case studies to delve into the factors influencing the determinants of different configurations of hybridity. Moreover, the analysis of long periods of time enables a clearer understanding of shifts in forms of hybridity, for the more mature a field is, the more the characteristics of institutional logics will impact organisational behaviour (Durand and Thornton, 2018). The study was carried out by means of a qualitative method and has drawn upon rich primary and secondary sources. Primary sources were found at the State Archive of Pisa (henceforth ASPi). The Opera del Duomo (hereafter OD) collection has been important as it includes the main documents relating to the life of the Opera, such as regulations, statutes, legal documents, letters and orders from the officials of the organisation and from local and State authorities, as well as accounting books. Other primary sources, including accounting regulations issued by Grand Duke Cosimo I, were found in other collections of the State Archive of Pisa and at the Opera del Duomo Archive (hereafter AOD).

A qualitative, iterative process of analysis of historical data sources was adopted to identify the key external actors and associated logics affecting the Opera as a hybrid organisation (Hatch and Schultz, 2017). All materials were read separately by each author, after which different sets of discussions took place. Whenever an agreement could not be reached, the authors went back to the sources and then organised a new set of discussions to address any open issues. The authors first discussed which were the main external actors and logics affecting the Opera. Books on the history of the city of Pisa, the State of Florence and the Opera del Duomo, as well as primary sources in the form of legal documents and statutes of the Opera were analysed to identify the main actors whose interests collided as they sought to influence the operations of the Opera. Historical research indicates how, initially, these actors were the Commune of Pisa and the Church. With the conquest of Pisa by the Florentines in 1406, the interests of the State of Florence were added. Primary sources consistently mention the Commune of Pisa, the Church and, later, the State of Florence, thereby confirming how these were the three main actors which sought to influence the activities of the Opera. As a result, three main logics embodied by each of the three external actors were identified, the Commune logic, the Church logic and the State logic. The sources informing the study then enabled an examination of how logics interacted and generated different configurations of hybridity. This was done by considering different factors at the field and organisational levels (Maran and Lowe, 2022). The identification of such factors followed the literature that has identified the ways in which different factors impact the centrality and compatibility of logics in a hybrid organisation (see Battilana et al., 2015; Mair et al., 2015; Maran and Lowe, 2022; Smith, 2014). In doing so, we have also sought to contextualise such factors to the historical case under analysis and its unique institutional context.

In our investigation of centrality, the structure of the institutional field in which the Opera operated has been analysed (see Besharov and Smith, 2014). The power of different actors across time has been documented by means of secondary sources that indicated the influence in society of Communes, the Church and the rising State of Florence (Battistoni, 2013; Bordone, 1985; Ceccarelli Lemut, 2016, 2017; Greco, 2020; Harman and Renwick, 2020). Another important factor in the analysis of centrality has been the relative power of organisational members at the Opera, and how external actors sought to influence their appointment (see Kim et al., 2007). This has involved an analysis of the governance system of the Opera and of the ways in which different actors sought to influence the appointment of key organisational members. To this purpose, two main rulings (ASPi, OD, Diplomatico, 13.04.1208; ASPi, OD, Diplomatico, 25.10.1541) that sought to address conflict around the appointment of the key managerial figure of the organisation, the Operaio, were used, along with the statutory rules detailing the tasks on the Operaio himself, the Breve dell’Operaio (ASPi, OD, 1). Further evidence was provided by orders and letters coming from civil authorities, the ruler and the Archbishop of Pisa (ASPi, OD, 2; ASPi, OD, 3; ASPi, OD, 6; ASPi, OD, 8; AOD, Affari diversi, 1).

When several external forces seek to exert influence over an organisation and demand the latter to account for their choices, accountability may become complex due to potentially conflicting requirements (Vakkuri et al., 2021). Consistent with recent research on hybrid organisations (Battilana et al., 2015; Mair et al., 2015; Maran and Lowe, 2022), the study considers accountability arrangements as a crucial factor in mapping the relations and interactions between an organisation and external actors which, as explained by Besharov and Smith (2014), influence logics’ compatibility. Accountability relationships have been documented by means of original legal documents and nineteenth-century transcriptions that showed how the Commune of Pisa, the Church and the Florentine State engaged with the Opera and sought to intervene in its life (ASPi, OD, 2; ASPi, OD, 3; Bonaini, 1854, 1870), as well as the formal accountability lines dictated by specific rulings (ASPi, OD, Diplomatico, 13.04.1208; ASPi, OD, Diplomatico, 25.10.1541) and ad hoc letters through which external actors demanded explanations for decisions made by the Opera and issued orders (ASPi, OD, 8). Another important factor in the analysis of compatibility has been the degree to which the influence of external actors on the organisation translated into formal controls on how the Opera used its resources. Being the wealthiest organisation in Pisa, the Opera did not formally rely on external entities for funding, but over time was subjected to different requirements as to how its riches were employed in its activities. Formal controls on resource usage by the Opera complemented and integrated the analysis of accountability relationships. Accountability requirements may have regarded specific aspects of the operations of the organisation, whilst control of the use of resources represented a more holistic indication of the influence of a specific logic on the operations of the Opera (Smith, 2014). These controls have been investigated through an analysis of the accounting documents prepared by the Opera in the form of books of revenues and expenses, books of debtors and creditors, journals, lists of properties and books detailing the expenses incurred for the ordinary and extraordinary maintenance of the buildings under the Opera's care (ASPi, OD, 29; ASPi, OD, 141: ASPi, OD, 142; ASPi, OD, 152; ASPi, OD, 154; ASPi, OD, 183; ASPi, OD, 184; ASPi, OD, 187; ASPi, OD, 579; ASPi, OD, 581; ASPi, OD, 617; ASPi, OD, 675). Also analysed were auditing procedures as documented in a specific book prepared by the bureaucrats of the State of Florence (ASPi, OD, 1031) and the accounting rules issued by Cosimo I that the Opera was expected to follow (ASPi, OD, 65).

The Opera del Duomo as a hybrid organisation

The origins of the Opera del Duomo can be traced back to the conquest of Palermo in 1063, when the Pisan fleet raided and plundered the city which at the time was in the hands of the Saracens (Fadda, 2020). The significant spoils of war arising from the defeat of the ‘infidel’ were earmarked for starting the construction of a monumental cathedral complex (Fusco, 1903; Volpe, 1902). The construction of the complex began in 1063, with the building of a new cathedral. Later, the complex was expanded with the construction of a baptistery (1153), a bell tower (1174, the present day ‘leaning tower’) and a cemetery (1278) which together constitute the heart of today's iconic Square of Miracles (Artizzu, 1974).

This spiritual endeavour soon attracted the interest of the citizens of Pisa, who through their generous donations provided significant resources above those coming from the raid of Palermo. Not only did citizens seek salvation in the afterlife by means of their donations, but also to link their names to what had become the most important building site in the city, thereby increasing their social and political prestige. Even though most of the funding needed for the construction of the buildings was coming from the spoils of war and from the citizenry, given the nature of the site it was decided that these resources would be managed by the Pisan clergy (Artizzu, 1974). As the assets donated for the construction of the complex grew, it became necessary to separate these resources from those which constituted the patrimony of the Pisan clergy. As such, the Opera del Duomo was established and entrusted with the duty to administer the income from donations and manage the construction and maintenance of the nascent cathedral complex (Artizzu, 1974). 1 The Opera soon became the richest and most powerful organisation in the city. Its properties constantly grew over time and, by the end of the twelfth century, not only did the organisation own large estates in the Pisan countryside, but also in Sardinia, Corsica and the Middle East (Artizzu, 1974).

Consistent with the way in which the construction of the cathedral complex had started, the Opera del Duomo maintained a strong relationship with the Commune of Pisa and its citizens. Despite being mainly an organisation concerned with building new places of worship, its strong ties with the citizenry meant that it also performed a charitable function by taking in citizens as oblates, thereby offering them protection, food and shelter in exchange for their work or their properties after their death (Greco, 2004). Civil authorities and the citizenry had an interest in the organisation prospering and growing stronger, as this would increase the prestige of the Commune and ensure support for some of its citizens. The Opera was thus influenced by the Commune logic, which was an expression of the interest of the Commune of Pisa in shaping the Opera as an organisation that served the needs of the community. It was understood that all the resources entrusted to the Opera should have been invested in its activity and benefit the Pisan community. In line with the understandings of the Commune logic the Opera's monumental complex, once completed, should have played a central role in the spiritual but also political life of the city (Bonaini, 1854: 47). The magnificent buildings erected in the new city square were to embody the link between the community, which came together and succeeded in a glorious enterprise, and God. This link is recognised in two epigraphs on the cathedral's façade, which celebrate the virtue of the Pisan people, who through their work but also military power made the construction of the building possible.

The Church logic embodied by the Pisan clergy was obviously important for the functioning of the Opera. The logic of the Church was an expression of the interests of the Church as a powerful actor whose priorities were not only sacred but also secular. The Pisan clergy, headed by the Archbishop as the main administrator of the considerable wealth of the organisation when it was first set up, saw the Opera as an important means to reinforce their power and prestige. It was also considered as a potential source of income despite the organisation's resources being separate from those of the clergy. The Opera was also seen as pivotal to religious veneration. In the opinion of Archbishop Ubaldo, the main goal of the Opera was promoting the worship of the Virgin Mary, to whom the cathedral was dedicated, which meant that the organisation must have a tight link with the Church (ASPi, OD, Diplomatico, 13.04.1208). As a result, since the establishment of the Opera, the Commune and its citizenry and the Church were the main external actors which vied for power and resources, attempting to affirm their dominance and jurisdictional control over the organisation (Greco, 2004).

With the beginning of the Florentine domination of Pisa in 1406, a third actor arose, the State embodied by Florence and its growing dominions in Tuscany. After a period of prolonged war between Florence and other city-states, including Pisa, under Cosimo I de’ Medici and his sons Francesco I and Ferdinando I Florence extended its area of influence to almost all the territories of today's region of Tuscany (Diaz, 1976; Fusco, 1903), a process which culminated with the creation of the Grand Duchy of Tuscany in 1569. Cosimo I and his successors sought to end the struggle between Pisa and Florence which had characterised the first decades following the conquest of the city by the Florentines and involved local potentates and institutions in the government of the State. As part of this strategy to strengthen the State without resorting to the use of violence, control of powerful institutions at the local level became paramount (Diaz, 1976; Greco, 2020). As a result, a third logic, that of the Florentine State, emerged, one which saw in the Opera an important means to increase the wealth of the State and a conduit to promote its power and might at the local level. The Opera's assets should have been managed with the ultimate goal of increasing the grandeur of the entire Florentine State. For example, Cosimo I and his heirs sought to turn the Opera into a commercial enterprise capable of generating wealth and prosperity for the entire State (Battistoni, 2013). Furthermore, the Grand Dukes saw the Opera and its assets as instrumental for the celebration of the Grand Ducal dynasty through artistic embellishments (Garzella et al., 2014). As a result, the Commune, Church and State competed for hegemony over the Opera so that they could manage its assets according to their own interests. The Opera had to manage competing organisational principles stemming from diverse institutional logics related to each external actor. Over time, it embodied different kinds of hybridity.

Contested hybridity: the Church and the Commune of Pisa

Centrality: the institutional field and key organisational members

Since its establishment, the Opera del Duomo operated in a field which included two very powerful actors, the Church and the Commune of Pisa. Between the twelfth and fifteenth centuries, the Church was a major source of power, so much so that not only did the Pope rule over parts of today's central and southern Italy (the so-called Papal States), but often had a significant impact on international politics and even challenged imperial power (Harman and Renwick, 2020). The influence of the Church was not limited to the political sphere but extended to how individuals conducted their lives. It exercised hegemony in the scanning of time in local communities, with churches’ bell towers representing the main means to measure the passage of time (Le Goff, 1980). The life of citizens was closely linked to the properties of the Church, especially sacred buildings and lands, and within its legal and normative grids. Baptism as the act of acquiring minimal civil rights in a Christian society, the recourse to the ecclesiastical forum for a wide range of matters and the presence of several charitable institutions and orders depending on the Church are examples of the influence exercised by the Church on local communities (Baños Sánchez-Matamoros and Carrasco Fenech, 2019; Greco, 2020). At the local level, the Church's authority was embodied by the Bishop or Archbishop. The bishop enjoyed a significant degree of autonomy from the Roman Curia and was responsible for leading the local clergy and Catholic community, with its authority often extending to secular matters (Battistoni, 2013).

Since the eleventh century, the communities of northern and central Italy started to organise themselves as new political and economic entities, a process which led to the birth of the so-called Communes (Bordone, 1985; Ceccarelli Lemut, 2016). The birth of the Commune of Pisa is inextricably linked to that of the Opera. The first step towards the self-determination of the Pisan community as a political entity was the 1063 sack of Palermo, which brought together the community and provided impetus for the formation of new civil authorities, especially the consuls, an assembly of citizens and a senate of 40 members (Ceccarelli Lemut, 2016). The Commune soon started extensive public works to improve and defend the city, but also issued new laws and created a new judicial and administrative system. Further impetus to the development of Pisa as a political unit came from Emperor Frederick I's diploma in 1162, which granted the Commune of Pisa full autonomy and reinforced the power of its civil authorities (Ronzani, 1996). Later, citizens who were not part of the Pisan aristocracy demanded to be involved in the management of the city, and in 1254 they appointed the Capitano del Popolo as the new head of the Commune. Furthermore, they established the Magistracy of Elders, which became the most important deliberative body of the Commune (Ceccarelli Lemut, 2009). Civil authorities represented a new source of power that vied for influence over the main institutions of the city, especially its most renowned, the Opera.

As noted by Besharov and Smith (2014), the relative power of organisational members impacts centrality, and the more influential an organisational member is within the organisation, the more impactful their action will be. As a result, external actors will try to influence the appointment of powerful organisational members, for those who hold power within an organisation and are deeply involved in key decision-making processes are more likely to succeed in ensuring that the logic they carry will influence how the organisation itself operates. Both the Church and the Commune sought to take a role in the regulation of the tasks and appointment of the top managerial figure of the Opera, the Operaio, who was responsible for the day-to-day management of the organisation. The Church and the Commune clashed several times over the right to appoint this important figure, on which all the other organisational members of the Opera depended, both lay and ordained. The Opera's top managerial figure had been appointed by the Archbishop since the establishment of the organisation (Fusco, 1903). Especially in the first century of the life of the Opera, the Archbishop had a dominant influence on the Opera, to the point of being able to directly sell some of the properties of the organisation, even if this should have been a prerogative of the latter's management (ASPi, OD, Diplomatico, 1.09.1128). The relationship between the Church and the organisation was so tight that the boundaries between the two were blurred. This is shown by how contemporaries perceived the role of the Opera and the Operaio. Martino del fu Oddo and his wife offered themselves to the Opera as oblates, provided that, after their death, all their properties went to the Opera to be used ‘for the power and love of God’, thereby recognising the organisation's function in the spiritual domain (ASPi, OD, Diplomatico, 30.04.1142). At the same time, on swearing an oath of loyalty to the Operaio, they emphasised that he was ‘responsible for secular matters’ as they clearly believed that the management of the assets of the organisation was a secular issue (ASPi, OD, Diplomatico, 30.04.1142).

Despite this situation, at the beginning of the thirteenth century, the Commune chose and appointed a new Operaio, thereby starting a five-year dispute between the Church and the Commune over the legitimacy of this appointment. The Archbishop stressed that the buildings in the Square of Miracles served religious purposes, were built on church-owned land, and that most of those working for the Opera were clerics. As such, he claimed that the management of the Opera was the responsibility of the Church (ASPi, OD, Diplomatico, 13.04.1208). The Commune contended that, despite ancient customs, the Operaio had always worked in tight connection with municipal authorities. Moreover, many of the belongings of the Opera had been donated by the citizenry or the Commune (ASPi, OD, Diplomatico, 13.04.1208). The dispute ended in 1207 with an arbitration by eminent legal experts which confirmed the legitimacy of the appointment and the right of the Commune to choose the Operaio. The arbitration also freed the Operaio from the jurisdiction of the ecclesiastical forum (Ronzani, 1996).

Building on the favourable outcome of the arbitration, the Commune sought to further reinforce the primacy of its own logic over the Opera by issuing written regulations about the figure of the Operaio. Specific provisions about the administrative functions of the Operaio and his staff were issued to reinforce the link between the Opera and the community, which gave prominence to the Opera's charitable function. In 1332 these regulations, the so-called Breve dell'Operaio (ASPi, Inventory; ASPi, OD, 1), placed the appointment of the Operaio in the hands of civil authorities. The Operaio was appointed for life and was expected to attend to the management of the Opera and the administration and maintenance of its properties. The Operaio was required to devote his life to managing the Opera, to the point of having to entrust his personal affairs to an attorney and being forbidden from having children. He was to serve the organisation with the highest diligence, and his ultimate goal was to maintain and improve the Opera's cathedral complex and other properties (ASPi, OD, 1). The Opera was then provided with several bureaucrats, including a notary and two lawyers, who were accountable to the Operaio (ASPi, OD, 1).

Even though the 1207 ruling tipped the balance of power in favour of the civil sphere, struggles between the Church and the Commune over the Opera continued (Battistoni, 2013; Fusco, 1903). Five years after the arbitration, the Archbishop still claimed that ‘whether the city is ruled by a sovereign or not, the Operaio needs to be judged by the Pisan Archbishop and be accountable to him’ (ASPi, OD, Diplomatico, 16.08.1212). The Operaio responded to such claims by refusing to appear before the Archbishop's religious tribunal, thereby showing his intention to follow the guidance from civil authorities for the discharge of his daily duties, which led to his excommunication. The situation was so serious that Pisan civil authorities had to petition the Pope to have the excommunication removed (Volpe, 1902). The arbitration and the Breve dell'Operaio clearly placed the Opera under the care of civil authorities. Nevertheless, the significant power enjoyed by the Church in this period, the obvious link between the activity of the organisation and the management of religious buildings, and continuous interference from the Archbishop in its affairs meant that the organisation experienced high centrality, with both the Church and the Commune logics at the core of the Opera's functioning.

Compatibility: accounting tools and accountability relationships

Accountability relationships can contribute to strengthening the influence of a logic on an organisation by ensuring that organisational members answer to certain external actors and not others (Maran and Lowe, 2022). In the first period of analysis the Opera's accountability relations were blurred and unclear, with both the Church and the Commune seeking to ensure that the organisation was accountable to them and that they were involved in decision-making. Until the twelfth century, the Opera was mainly considered a religious entity and the Operaio was expected to keep the Archbishop constantly informed on how the organisations’ patrimony was used and on the appointment of lay or ordained people who would work for the Opera, which the Archbishop could reject (Battistoni, 2013). Nevertheless, the Operaio engaged also with the Commune, especially around the management of the lands and other properties of the organisation, which fell within the jurisdiction of civil authorities. It was also customary for the Operaio to present an account of his activity that included his usage of the Opera's money to the Commune (ASPi, OD, Diplomatico, 13.04.1208). Following the arbitration of 1207 and the issuing of the Breve dell'Operaio, accountability relationships became clearer, although the Operaio was still expected to answer for this activity both to the Church and the Commune.

The Breve dell'Operaio stated that the Operaio had to swear an oath of loyalty to the civil authorities, which was meant to clarify that in carrying out his activity he was expected to have the city's best interest at heart. Furthermore, the Operaio had to reside in a house provided by the Opera and was not allowed to receive anyone except ambassadors and officials of the Commune to avoid undue influence on his work (ASPi, OD, 1). The Breve dell'Operaio required that the Operaio use specific accounting tools for ensuring the diligent and transparent management of the Opera. Within one month of his appointment, the Operaio was required to make an inventory of all the Opera's properties. Although the Operaio could sell non-essential movable assets, he had to seek approval from the Commune if he wished to sell or rent out immovable assets, which further shows how the institution was influenced by the Commune's logic (ASPi, OD, 1). With the help of the Opera's notary, the Operaio was expected to account for the financial results of his decisions (ASPi, OD, 1). The inventory book, the Libro de’ debitori e creditori and the Libro delle entrate e delle uscite were the main books kept to account for the various transactions affecting the organisation. The first book offered a snapshot of all the Opera's properties, while the other two summarised the organisation's payables and receivables and the cash movements arising from various operations respectively. The links between these books are not clarified in any regulations.

As shown by the accounting books, the main revenues of the Opera consisted of rent of properties, sales of products and duties from privileges granted by the Commune, which added to donations of lands by wealthy citizens (ASPi, Inventory). It was therefore clear how most of the organisation's income came from engagements with the citizenry and civil authorities, which reinforced the position of the Commune vis-à-vis the Church, for resource dependency is an important enabling factor for ensuring that a specific logic influences organisational activity (see Besharov and Smith, 2014). Any revenues received by the Opera should have been reinvested in the organisation's activity, especially the maintenance of properties, the construction or acquisition of new buildings, the remuneration and care of people involved in organisational activities, and charity (ASPi, OD, 1). Crucially, the Breve dell'Operaio clarified that the Operaio was expected to ‘spend every year, as much as he can, all the money in his hands for the activity of the Opera’ (ASPi, OD, 1). It was therefore understood that the organisation's goal was not wealth accumulation but contributing to the splendour and renown of the city and helping citizens in need. This goal was reinforced by the prohibition to lend any of its money, which was a means more to ensure that resources were not diverted from the organisation's main activity than to avoid the unholy practice of earning interest on loans 2 (ASPi, OD, 1).

Clear evidence of the need for the Operaio to account to the civil authorities is provided by the description of auditing practices in the Breve dell'Operaio, which turned into law the ancient custom of presenting the Opera's accounts to civil authorities and established a clear procedure for doing so (ASPi, OD, Diplomatico, 13.04.1208). The accounting books drawn up by the Operaio were to be audited every year in May by officers appointed by the Commune. The auditors had to check that all the income was reinvested by the Operaio in pursuing the Opera's goals and identify any fraudulent activity. The auditors had to prepare a report within one month of their appointment, which was made public. The seriousness of the procedure was such that the auditors were expected to provide an evaluation of the work of the Operaio in the form of a ‘verdict’. He could have been ‘acquitted’ if the auditors believed that his actions had been consistent with the interests of the Opera, or ‘convicted’ in case of overspending or fraud, which would have caused the issuing of fines and even the removal of the Operaio in the most serious cases (ASPi, OD, 1).

Although weakened by the issuing of a written statute establishing clear lines of accountability that privileged the Commune, the Archbishop was still able to demand that the organisation, and the Operaio in particular, answered to him for some aspects of their operations. In fact, the 1207 arbitration established the authority of the Archbishop over religious matters, including overseeing the appointment of any salaried official who was expected to perform sacred duties and investing the Operaio with new paraliturgical responsibilities, such as swearing-in the head of the Commune and taking a role in ceremonies held during religious festivals (ASPi, OD, Diplomatico, 27.12.1234).

The way in which the Opera could manage its assets was also affected by different requirements dictated by conflicting logics. The reinforcement of the Commune in the thirteenth century meant that civil authorities sought to turn the magnificent cathedral and its surroundings into the heart of public life, despite the obvious religious function of the building. Therefore, in 1214 it was decided to clear the area around the cathedral of all buildings, including the chapter house, to create a large space to be used for public gatherings (Ronzani, 1988). This decision was met with resistance by the Church, with the members of the Chapter still refusing in 1247 to move to the new premises allocated by the Operaio although ‘the Pisans had very quickly torn down [their] cloister’ (Bonaini, 1870: 993). Eventually the Chapter moved to the Opera's existing headquarters, with new premises built for the latter on land donated by the Chapter, provided that a new hospital for pilgrims was built by the Opera itself, which was to be managed directly by the clergy (Bonaini, 1854). The new, large space in front and around the cathedral which still characterises today's Square of Miracles was then used for meetings between civil authorities, heads of households and the representatives of professions, thereby becoming instrumental to the political life of the city. Moreover, even processions culminating in the Operaio, not a member of the Church hierarchy, donating candles to the Virgin Mary, were organised in this new space (Bonaini, 1854). Such events showed the attempt by the city to create a direct, unmediated relationship with the divinity and testified to how the Opera had started to operate at the boundary between the sacred and the secular, which clashed with the Church's claim to being the only intermediary between the faithful and God. Further controversy arose when the new cemetery was built in 1278. The land targeted by the Operaio for development was donated by the Archbishop following two years of negotiations and after the Commune threatened to ‘employ every possible way and means to get those lands and orchards as established by the Operaio’ (Bonaini, 1854: 51–52). The construction of the cemetery was funded by the Opera, and even if it was formally part of its patrimony the proceeds from requiem masses celebrated by the clergy were retained fully by the Church (Ronzani, 1988).

As a result, in the first period of analysis, the Operaio was at the centre of a network of different accountability demands by powerful actors, leading to controversy and compromise in the management of the properties of the Opera. These actors sought to pursue their own goals through the organisation, this resulting in low compatibility.

Dominant hybridity: enter the State of Florence

Centrality: the institutional field and key organisational members

The beginning of Florentine domination in 1406 meant the entry of the State 3 into the struggle between the Church and the Commune for jurisdictional control over the Opera. Conquest by the Florentines weakened Pisan civil authorities as they had to bend to a new master's will. In the first decades of Florentine domination, the relationship between the two cities was one of pure exploitation, with the State of Florence often seeking to steal the riches of Pisa. After the conquest, Pisa remained an intractable part of the State of Florence and successfully rebelled in 1494, only to be retaken after a long siege in 1509, which caused the death or escape of two-thirds of its population (Bigoni et al., 2023). A turning point in the relationship between Florence and Pisa was the enthronement of Cosimo I de’ Medici, who sought to turn his State into a strong, dynastic dukedom and rule by means of consent more than force. Cosimo's political strategy was based on integration rather than exploitation through institutional reforms aiming to centralise power but without completely removing the autonomy of local elites. He created new bureaucratic bodies to mediate between the centre and local communities. Among these bodies, the Nove conservatori della giurisdizione del dominio fiorentino (henceforth the Nove) were particularly important as they watched over the administration and financial management of local communities (Diaz, 1976; Greco, 2020). Local communities retained both their ancient statutes and their traditional political bodies, which were expected to engage with the bureaucratic apparatus created by the ruler (Greco, 2020). The creation of a professional administrative apparatus made up of career bureaucrats, chosen for their ability rather than their belonging to the upper class (Diaz, 1976), was a distinctive feature of the Florentine State under Cosimo I and his heirs, one which enabled the Grand Duke to form a thorough understanding of what was happening in each part of his dominion (Bigoni et al., 2018).

The fifteenth century witnessed a decline in the authority of the Church, with power struggles leading to the Western Schism at the end of the fourteenth century and the election of two Popes, who then became three following a Council of Cardinals held in Pisa in 1409. It was not until the Council of Constance (1414–1419) that the Church was finally reunited under one leader. Widespread corruption and moral decay had estranged many believers, and the diffusion of humanist values clashed with the dogmatic tradition of the Church (Bigoni et al., 2013). This period of decay reached its climax with the Protestant Reformation which further weakened the authority of the (Roman Catholic) Church and ended its claim to absolute power over Western Christendom.

In Pisa, despite the challenging situation the Church was facing, the Archbishop believed that the advent of the State of Florence and the consequent weakening of the Commune of Pisa was an opportunity to reiterate its claims on the Opera. Nevertheless, the Florentines, through ad hoc decrees issued in 1408, 1412 and 1483, confirmed that that the Opera was to be governed by the Commune of Pisa, which had no other superiors but the Commune of Florence, although they did not clarify the consequences of this ‘superiority’ (ASPi, OD, Diplomatico, 25.10.1541). The Commune of Pisa sought to strengthen its control of the Opera by updating the Breve dell’Operaio in 1516 and 1522. The revised version stated that the Operaio ‘could not do anything without the permission of [Pisan] civil authorities’, especially purchasing or selling properties (ASPi, OD, 6, page not numbered). During the fifteenth century, when the political and military struggle between Florence and Pisa reached its climax, the Florentines sought to exploit the Opera by funnelling resources to Florence, with many properties taken away from the organisation. Further damage was done by the occupation of several buildings of the Opera by soldiers whilst many of its lands were ravaged and left uncultivated. This caused a progressive reduction in the Opera's revenues (ASPi, OD, 141, 142, 154).

The Operaio, by then a representative of the Pisan citizens’ interests, consistent with the Commune logic, sought to protect the Opera's patrimony and privileges, sometimes with positive results (ASPi, OD, 2, c.20r-v; ASPi, OD, 2, c.36r-c.37r). In particular, the Operaio sold unproductive properties and acquired more lucrative ones. He also purchased shops and hospices in the city, whilst in the countryside he focused on properties in areas which could be easily rented to the Florentine dominators (ASPi, OD, 2, c. 38r-39r; ASPi, OD, 152, c. 84r). In parallel with these activities, the Opera continued to manifest a spirit of solidarity towards the Pisan community. It contravened its own statute and granted the Commune of Pisa financial aid through the concession of loans to fund the struggle against Florence and the reconstruction of the city following its conquest (ASPi, OD, Diplomatico, 8.07.1488). This was a clear strategic attempt by the organisation to change their main practices to favour the logic of the less powerful Commune of Pisa (see Besharov and Smith, 2014). The first period of Florentine domination saw the rise of a new logic, that of the State of Florence, which sought to use the Opera as a means to increase its wealth. This new logic was clearly central to the organisation, given the power of the new actor which had subdued the city by virtue of its superior military might. However, the logics of the Commune and the Church remained crucial, with the organisation now supporting the Commune in its struggles and the Church seeking to reinstate its authority over the Opera.

With the advent of Cosimo I de’ Medici in 1537, the conflict between the Church, the Commune of Pisa and the State around the Opera began to ease whilst the logic of the State started to become dominant. As in the first period of Florentine domination, the State considered the Opera as an important means to increase its wealth and prestige. However, Cosimo I did so by integrating Pisa into his State and promoting the development of the city and its institutions, a policy which was furthered by his sons Francesco I and Ferdinando I (Diaz, 1976). Respecting the most prestigious institution in the city of Pisa, the Opera, would have meant presenting himself as a ‘friend’ and ‘protector’ of the interests of Pisan citizens after years of harsh conflict, thereby making control of the unruly dominion easier. Cosimo I supported the Opera after difficult times, and instead of plundering its riches, he contributed to its growth (Battistoni, 2013). He also intervened in the long-standing conflict between the Church and the Commune over jurisdictional control of the Opera. The Church, despite several unfavourable rulings, never ceased to interfere with the affairs of the Opera.

Another lawsuit between the Archbishop, the Operaio and the Commune of Pisa became an opportunity for Cosimo I to issue a ruling in 1541 that permanently identified the boundaries of the actors’ spheres of influence. Cosimo I confirmed that the Opera was subject to civil authorities. The administration of the Opera's properties was entrusted to the Commune of Pisa through the Operaio, although it was clarified that the Opera was also subject to the Commune of Florence. In a much clearer fashion than the arbitration in 1207, the ruling stated that the Archbishop ‘should not and cannot interfere with the administration [of the Opera], nor give orders to the Operaio’ (ASPi, OD, Diplomatico, 25.10.1541). Nevertheless, the Archbishop had the right to oversee the Operaio's work over spiritual matters and the way in which he engaged with the clergy. The Archbishop had to be consulted regarding the use of sacred buildings, with only the exception of essential maintenance works (ASPi, OD, Diplomatico, 25.10.1541). Although his intervention clearly reinforced the Commune's key role in the management of the Opera, the ruler also sought to enable the Church's logic to influence peripheral activities not directly to oppose this major source of power. Exchanges of letters between the Operaio and the ruler reveal numerous interventions aimed at ensuring that the Church's sphere of influence would not exceed sacred affairs. For example, in 1577 the Operaio wrote to the Grand Duke complaining that the clerics had interfered in the choice concerning positions funded directly by the Operaio, such as music masters, schoolteachers, organists and sacristans. The ruler promptly intervened by reaffirming the authority of the Operaio in the choice of such staff (ASPi, OD, 6). However, later the Grand Duke reiterated, at the Archbishop's request, that these officers obey the Archbishop with regard to their sacred functions (ASPi, OD, 8).

Despite having apparently reinforced the position of the Commune of Pisa, intervention by the ruler meant that the State of Florence took a direct role in the management of the Opera, thereby fleshing out the ‘superiority’ of Florence reiterated in Cosimo I's ruling. To increase the prestige and wealth of its State, Cosimo I and his heirs sought to turn the Opera into a commercial enterprise by boosting the policy of acquiring high-value buildings and lands initiated at the end of the fifteenth century. Hence, the Opera started the construction of a new ‘wheat square’ in 1544, which was to become the city's commercial hotspot. The work on the square involved the purchase and renovation of new buildings and the construction of warehouses and shops. The commercial exploitation of these establishments quickly became the main activity of the Opera under the rule of the Medici family, despite its statutes stating that the Opera's main function was charitable and spiritual and not commercial (Battistoni, 2013). To ensure that this activity could proceed as expected by the Medici, the Nove were given the power to approve or reject the Operaio's decisions around the sale, purchase or rent of properties, although, as per the Breve dell’Operaio, this should have been a prerogative of Pisan civil authorities (ASPi, OD, 6). The ruler gave the Opera the right to claim duties on wheat sold in the new square (ASPi, OD, 3). He allowed the Opera to continue the financing of the Commune of Pisa, a practice which had been previously forbidden (ASPi, OD, 579, cc.116r-117v). On the one hand, this would have allowed the State to push the Opera to strengthen the spirit of solidarity with the community of Pisa and thus meet the requirements of the Commune logic. On the other hand, promoting the role of the Opera as the financing body of the community of Pisa was a way for the State to increase further the wealth of the Opera through interest-bearing loans.

Despite formally respecting the rights of the Church and the Commune, the State of Florence took a decisive role in the life of the organisation, even if this meant imposing its authority over the other actors. In a clear breach of the prerogatives of the Operaio, Cosimo I started to concern himself with the artistic embellishment of the cathedral, to the point of ordering new works; he put significant pressure on the Operaio to complete them in time to show the magnificence of the building to important guests or on special occasions such as his wedding in 1539 (Garzella et al., 2014). In 1559, he even commissioned the creation of two statues to be placed in the cathedral, which was clearly within the remit of the Operaio (ASPi, OD, 579, c.161). Moreover, a limit of 200 scudi was imposed for the maintenance of the buildings in the Square of Miracles, above which Ducal approval was essential (AOD, Affari diversi, 1). The increased influence of the State was clearly perceived by the Operaio himself, who often petitioned the ruler and his bureaucrats for advice or confirming decisions that he was supposed to be able to make independently. This was the case, for example, of increases in the salaries of some officials (ASPi, OD, 6), including a small raise of half a ducat for the cathedral's bell ringer (ASPi, OD, 8), and the request to formally appoint officials suggested by the Operaio himself, so that they would be ‘more obedient’ (ASPi, OD, 6). Ducal interference reached its climax when Francesco I in 1580 opposed the choice of the Operaio made by the Commune of Pisa and appointed another person (ASPi, OD, 6). A few years later, Ferdinando I, too, decided to appoint directly the Operaio despite the Commune having chosen a different individual (Pecchiai, 1906). Interventions by the ruler thereby gave a presence to all the logics revolving around the Opera, but ensured that one logic, that of the Florentine State, became central to the functioning of the organisation, whilst the other two remained peripheral.

Compatibility: accounting tools and accountability relationships

Accountability relationships between the Opera and external actors in the first years of Florentine domination remained mainly those that had characterised the previous period. The Opera was still accountable to the Commune of Pisa, which continued to oversee the activity of the Operaio and audit his accounts. Cosimo I's 1541 ruling crystallised accountability relationships by clearly setting boundaries between spiritual and secular lines of accountability. The Archbishop had the power to hold the Operaio accountable for the results of his actions in the spiritual domain, but could not interfere in any way in the management of the organisation. The Commune of Pisa was confirmed, at least formally, to be the actor to which the Opera owed full accountability. Nevertheless, another intervention by Cosimo I changed this scenario. Although the Commune of Pisa remained the main authority to be consulted in the day-to-day running of the organisation, the creation of new accounting and auditing procedures meant that control of resources was placed firmly in the hands of the ruler and his bureaucrats.

The Breve dell’Operaio was revised in 1552, with the introduction of a new figure, that of the accountant (the Scrivano). This separated the accounting function from the management of resources, thereby reducing the opportunities for the Operaio to engage in fraudulent activities. Moreover, in 1564 Cosimo I issued accounting guidelines which introduced strict standards to be followed in the keeping of accounts by the Opera (ASPi, OD, 6; ASPi, Comune di Pisa Divisione D, 65). The guidelines detailed how the Opera's transactions were to be accounted for, along with the accounting books to be kept, the way and the order in which they were to be drawn up and the responsibilities of the Opera's officials in keeping them. If the Libro de’ debitori e creditori and the Libro delle entrate e delle uscite were the main books that were traditionally used to account for the operations of the organisation, the guidelines added another four: the Quaderno di spese, the Quaderno di muraglie, the Catasto and the Giornale. The new system centred on the Quaderno di spese, the Quaderno di muraglie, the Giornale and the Libro delle entrate e delle uscite, which were under the direct responsibility of the Operaio. As a first entry, the Operaio had to update the Quaderno di spese and Quaderno di muraglie, which included solely expenses. The Quaderno di spese was updated daily with expenses arising from the day-to-day management of the organisation and minor repair and embellishment works to the buildings under the Opera's care. The expenses relating to major masonry and repair work to the Opera's properties were recorded in the Quaderno di muraglie. Furthermore, the Operaio had to record all other transactions in the Giornale, which became the detailed chronological record of all activities carried out by the Opera and included both revenues and expenses, in cash and in kind. The totals for the main categories of revenues and expenses were recapped by the Operaio into the Libro delle entrate e delle uscite. This offered a holistic view of all the transactions which had an impact on the organisation, whilst detail was still provided in the daybooks (ASPi, Comune di Pisa Divisione D, 65, c.118r). Then, considering these records the Scrivano had to update the Catasto and the Libro de’ debitori e creditori (ASPi, Comune di Pisa Divisione D, 65, c.117v-c.118r).

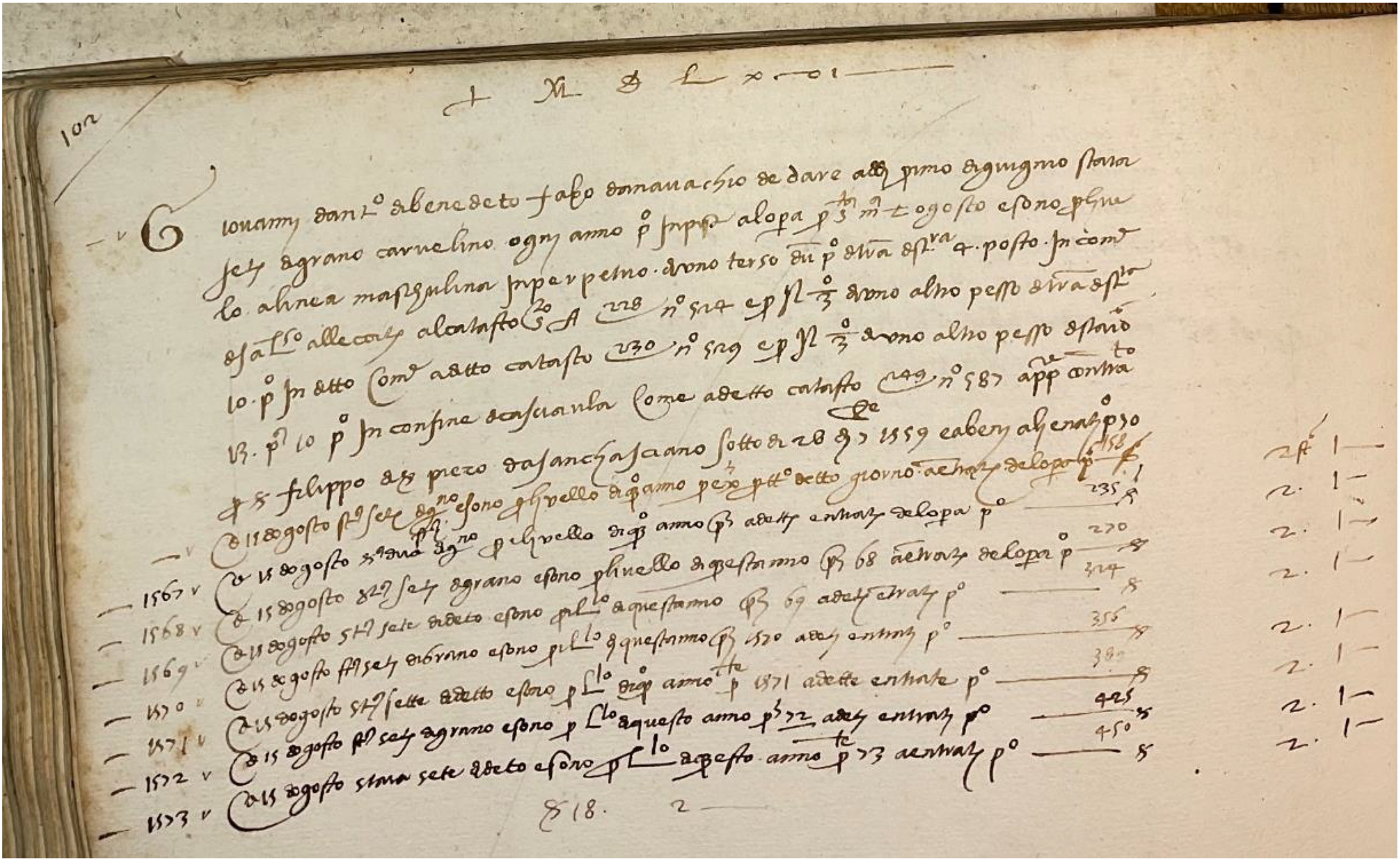

The Catasto represented the inventory of all the Opera's properties. Given the significant increase in these properties, the Catasto was deemed an essential tool to provide an updated snapshot of the wealth of the organisation. Whilst in the old inventory the properties were only briefly described (ASPi, OD, 617, c.1r), the Catasto presented a detailed description of each property with an indication of its boundaries, size, form of tenure, names of current and past tenants, and even the relevant will in case the property had been donated to the Opera (ASPi, Comune di Pisa Divisione D, 65, c.117r). On the left-hand side of the Catasto all properties currently owned and those targeted for acquisition were presented, whilst on the right-hand side those properties that had been sold, rented out or given in exchange for others were identified (ASPi, Comune di Pisa Divisione D, 65, cc.117r-v). This provided a clear understanding of the wealth of the Opera and the way in which it was used. The Libro de’ debitori e creditori summarised the amounts owed by the Opera's debtors and those due to the creditors of the organisation, along with payments received and made in respect of these. In order to achieve complete transparency, the accounting guidelines stipulated that the books should be cross-referenced so that it would have been possible to have a thorough understanding of each transaction. Consistently, the Giornale references led back to the Libro de’ debitori e creditori and from the latter to the Catasto and the Libro delle entrate e delle uscite (ASPi, Comune di Pisa Divisione D, 65, c.117v-c.118r; ASPi, OD, 183, cc.1r-v; ASPi, OD, 184, c.1r; ASPi, OD, 187, c.1r). The working of the new system is exemplified by the following entries referring to the lease of a property, which started with a record in the Giornale that reported the sums owed by the tenant to the Operaio: Wednesday, 4 July [1567] 167/102 | Giovanni d’Antonio blacksmith … must pay seven bushels of wheat and leave it in the shop of Francesco da Capannuli for a total of eight bushels, of which one that was still owing from last year and seven for this year's rent. (ASPi, OD, 675, c.1r, see Figure 2)

Extract from the Giornale (ASPi, OD, 675, c.1r).

The first number in the entry was a reference to the Libro de’ debitori e creditori, namely to page 167 which presented a description of the amounts due and schedule of payments: Sir Raffaello del Setaiolo our operaio and holder of our grains account must receive: From 15 August to 4 July seven bushels of wheat from Giovanni d’Antonio blacksmith, as per this [book on page] 102. (ASPi, OD, 581, c.167v)

The second number in the Giornale entry, 102, was referred to in the Libro de’ debitori e creditori too. On the left-hand side of page 102, a detailed description of the reason why the above payments were due was provided. The name of the debtor and a description of the boundaries of the property were indicated, along with references to the Catasto where the said property had been recorded. When the payments fell due, they were added below this entry: Giovanni d’Antonio di Benedeto blacksmith … must pay seven bushels of wheat to the Opera of Santa Maria in Pisa every year in mid-August, which are due to a perpetual lease of a piece of land of 4 staia

4

in the commune of S. Lorenzo alle Corti as indicated in the catasto A on page 228 n. 524, along with one third of another piece of land of 10 staia in the said commune, as indicated in the catasto on page 230 n. 529, and for one third of another piece of land of 13 staia bordering Casciavola, as indicated in the Catasto on page 249 n. 587. This contract has been drawn up by Filippo di ser Piero da Sanchasciano [a notary] on 28 September 1559 [the schedule of annual payments due followed]. (ASPi, OD, 581, c.102v, see Figure 3)