Abstract

Research has shown that Buddhist monasteries’ accounting provides detailed and fulfilling accountability requirements to rulers and the public. However, what influenced such practices is under-researched. In bridging this gap, this study adopts an institutional logic framing and identifies three institutional logics: devotional, public and private that appear to have shaped early accounting thought and practices in Ceylonese Buddhist monasteries. The research comprises the analysis of English translations of 122 inscriptions dating from the first to the sixteenth century. The analysis reveals the co-existence and mutual dependence of the three logics, concluding that these logics influenced accounting at the same time. The accounts are also important tools to maintain the co-existence of these competing institutional logics, highlighting a dynamic two-way relationship between logics and accounting. The study demonstrates the role of accounting as a bridging mechanism, temporarily combining logics to exploit complementarities between them, maintain the hybridity of monasteries and preserve their legitimacy. The ability of accounting to represent all logics enables the stability of monasteries over time.

Introduction

The extant literature on accounting history and practices of ancient kingdoms and civilisations comprises work by Carmona and Ezzamel (2007), Ezzamel (1997), Ezzamel and Hoskin (2002), Jones (2009), Mattessich (1989), Mustafa and Ibrahim (2023), Namazi and Taak (2022), Nissen et al., (1993) and Schmandt-Besserat (1992). However, in the context of Asia and the Indian subcontinent, there are few studies of ancient accounting practices despite the presence of an age-old Indian treatise Arthasāstra (circa 300–184 BC) by Kautilya (Mattessich, 1998) on economic policy, statecraft and military strategy. The focus of this study is on ancient Ceylon, an island nation in South Asia (presently Sri Lanka) and specifically on accounting in its Buddhist monasteries. Previous research in the context of Ceylon includes the work of Kumarasinghe and Samkin (2020) and Liyanarachchi (2009, 2015). Kumarasinghe and Samkin (2020) examined how Ceylonese kings used stone inscriptions as impression management techniques to present a favourable impression to their people. Liyanarachchi (2009, 2015) examined early accounting and auditing practices in ancient Ceylon as a tool for fulfilling accountability requirements in Buddhist monasteries.

The present study is inspired by Kumarasinghe and Samkin (2020) and Liyanarachchi (2009, 2015) due to the use of epigraphic evidence to investigate the historical accounting practices of ancient Ceylon. Yet, this is distinct from prior research in that it offers theory-based insights on what may have influenced accounting thought and practices in Buddhist monasteries. Prior research has shown that accounting in Buddhist monasteries entails keeping records of monastic resources and fulfilling notions of accountability requirements, to support relations with the rulers and people – see Liyanarachchi (2009, 2015). However, while the work of Liyanarachchi (2009, 2015) has provided a rich and valuable contribution to the knowledge of historical accounting practices of ancient Ceylon, it does not explore what may have influenced such practices. Thus, a key objective of this study is to build on existing work and explore what may have influenced early accounting practices in Buddhist monasteries.

The study examines Buddhist monasteries for several reasons. First, in a Ceylonese context, Buddhist monasteries are granted high status in the community for reasons such as royal patronage towards Buddhism, the education of Buddhist monks and their relationship with the kings. Their high status in the community warrants significant donations. These donations engender abundant epigraphical evidence, allowing the examination of monastic accounting practices. Second, religious organisations in general are unique in their characteristics. They are distinct from profit making organisations in terms of their ownership, absence of a profit motive and broader public interest mission. Nevertheless, prior literature has established that religious organisations (both historical and contemporary) engage in secular accounting mainly for control and accountability purposes (see Dobie, 2008a, 2008b; Espejo et al., 2006; Prieto et al., 2006; Quattrone, 2009), resulting in a typical sacred–secular divide (Laughlin, 1988). On the other hand, religious organisations differ from non-profit organisations as they are driven by faith.

The sacred–secular divide (Laughlin, 1988, 1990) recalls the presence of multiple institutional logics in a religious organisation. Thornton et al. (2012) define an institutional logic as the overarching values, assumptions and principles that prescribe how organisational actors interpret organisational reality and determine appropriate behaviour. The challenge of aligning the structures and practices with compatible behavioural templates or ‘logics’ is referred to as institutional complexity (Friedland and Alford, 1991). Institutional complexity can be noticeable in hybrid organisations such as charities, co-operatives and social organisations (due to competing market and community logics) and even more distinct in faith-based organisations, due to the added dimension of spirituality (Roundy and Taylor, 2016). Surprisingly, and apart from a few exceptions (see for instance Creed et al., 2010; Quattrone, 2009, 2015; Tracey, 2016), prior literature on multiple logics has overlooked the phenomenon of faith-based organisations (Lusiani et al., 2019) and non-Western religions (Gümüsay, 2020; Tracey et al., 2014). As Greenwood et al. (2014: 1214) describe, religion is a core societal institution, which ‘has its overarching “logics” or “master rules” that prescribe and proscribe social – including organisational – behaviour’, but the multiple logics that may operate ‘within’ a religious organisation are generally under-researched. In addition, although several scholars have shown the importance of historical analyses for understanding the emergence, consolidation and change of logics (McKenna, 2008; Padgett and Ansell, 1993), there is scarce analysis of institutional logics in hybrid organisations in a historical setting.

Prior literature on multiple institutional logics predominantly adopts a binary focus, in which logics are either reported as contradictory (Dunn and Jones, 2010; Greenwood et al., 2014) or as compatible (Lusiani et al., 2019, 2023; Perkmann et al., 2019) and rarely as mutually dependent (see Smets et al., 2015). Organisations seem to respond to institutional complexities by either decreasing the ‘centrality’ of conflicting logics by structurally compartmentalising their enactments (separating the logics) or by decreasing their ‘incompatibility’ by blending them in new practices or arrangements (integrating the logics) (Gümüsay et al., 2020). In the context of faith-based organisations, conflicting logics can be ‘incompatible’ (resulting in inconsistent organisational actions) and ‘central’ (where multiple logics are treated as equally valid and relevant to organisational functioning) to the organisation (Besharov and Smith, 2014). Thus, to address institutional complexity, pre-defined organisational responses, such as separation or integration, may not suit. Moreover, in a faith-based organisation, the separation or integration of values such as spirituality/devotional, community/public and material/private logics may result in controversy and public resentment (Boone and Özcan, 2016; Gümüsay et al., 2020; Washington et al., 2014). Yet strikingly, faith-based organisations or more precisely, Buddhist monasteries, as in the context of this study, appear to have managed such seemingly irreconcilable demands remarkably well and Buddhism as a faith and associated organisation has remained quite stable over time.

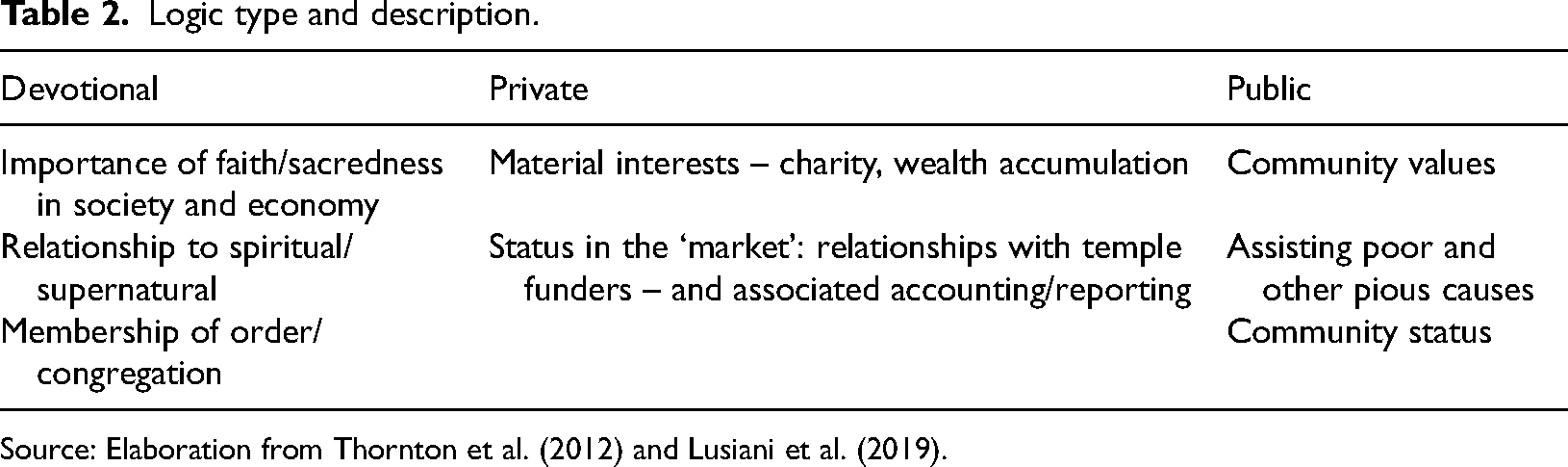

Our study, therefore, addresses the above lacunae and seeks to investigate two issues. First, using a multiple institutional logics lens (see Thornton et al., 2012), we seek to answer the question, ‘What influenced early accounting thought in ancient Ceylon?’, a context that is generally understudied. Second, we explore the role of early accounting thought and practices in Buddhist monasteries operating through multiple logics with seemingly contradictory demands. Following Lusiani et al. (2019), three institutional logics are recognised to be at play in the case study: devotional, public and private logic. Devotional logic has been a key feature of temporal administration (including accounting) of religious organisations till the present day (see Da Silva et al., 2017; Quattrone, 2004, 2009). It reflects the importance of faith/sacredness in society and economy (Thornton et al., 2012). Public logic emphasises community values (Thornton et al., 2012), with reference to the interest of embracing pious causes, whereas private logic focuses on material interests/wealth of monasteries as institutions (Lusiani et al., 2019).

This study selects and analyses the English translations of 122 inscriptions (see Appendix 1) dating from the first to the sixteenth century AD. This timeframe covers the reign of approximately 32 kings and seven different administrative capitals/kingdoms in ancient Ceylon. The focus is on ancient Ceylon, where there is availability of rich first-hand information in the form of rock inscriptions. They demonstrate the existence of the art of writing since an early era: that is an important element of accounting practices, as asserted by Ezzamel and Hoskin (2002). Moreover, given Ceylon's strategic position on the maritime Silk Road, it thrived as a trade hub during the sixth century AD (Jayawardana, 1964) and likely adopted calculative practices and modes of reciprocity, which may have been followed in Buddhist monasteries. Epigraphic and historical evidence suggest that the aforesaid three logics may have coexisted and are mutually dependent (Smets et al., 2015). They may have instigated early accounting thought in ancient Buddhist monasteries. Accounting has played a crucial role in responding to institutional pluralism, by addressing the multiple logics individually and by combining the key features of different logics. This generates complementarities between competing logics by showing relevant aspects of one logic into the enactment of another (Smets et al., 2015).

This study contributes to the extant literature in several ways. First, it provides an incremental contribution (Corley and Gioia, 2011) to current research by offering theory-based insights on the impetus of accounting thought and practices in antiquity, in a context that is generally under-represented. It also contributes to the wealth of literature on multiple institutional logics, by examining a non-Western faith-based organisation, subject to intense institutional complexity, in a historical setting, which is again scarcely researched. This study reinforces the view of prior scant literature on the coexistence of competing logics, by asserting that multiple institutional logics with conflicting demands can coexist (see Lusiani et al., 2019, 2023) and mutually reinforce each other (see Smets et al., 2015) as opposed to competing. In so doing, they influence everyday activities, without featuring major institutional change. This study explores how coexisting logics may also have induced accounting practices in antiquity and how accounting aids Buddhist monasteries to manage the logics in everyday practices, over time. It offers an incremental contribution in showing a dynamic two-way relationship within logics in a religious organisation context. More precisely, this study argues that private, public and devotional logics encapsulating wealth, relationships with funders (mostly to kings) and community, and abstinence from worldly desires, respectively, influence the recording of incomes, expenditures and balances. In other words, these logics influence the nature of accounting. These same accounts also allow monks to provide accountability to their devotional logic, ensuring that wealth is not spent by individual monks or on worldly goods, support public logic by safeguarding the relationships of the monasteries with rulers and their public image, and they allow the maintenance of a private logic as an important tool in managing monastic wealth. As a result, the accounting supports multiple institutional logics as argued by Lusiani et al. (2019, 2023). In essence, accounting is an important bridging mechanism, which temporarily combines competing logics to exploit complementarities between them, and skilfully imports relevant aspects of one logic into another, as and when it appears valuable. Accounting helps to maintain the hybridity of Buddhist monasteries and to preserve their legitimacy, with key elements of all logics combined (Smets et al., 2015), enabling monasteries to remain stable over time.

The remainder of the article is structured as follows. The next section provides a review of the literature, followed by a description of the research context (ancient Ceylon) and the methods used. We then present an analysis of the various inscriptions using an institutional logics lens. The final section offers some concluding comments and thoughts for future research.

Literature review

This section reviews the literature from two key perspectives. First, an overview of prior accounting literature on religion/religious orders is given. Second, we give a brief review of the literature on institutional logics, including some relevant accounting history literature.

Accounting and religion

Booth (1993) and Laughlin (1988) note that little research has been developed on accounting in churches and religious organisations till the early 1990s. In a 2006 special issue on ‘Accounting and Religion’, Carmona and Ezzamel (2006) further note a lack of academic interest in accounting in religious institutions. They find this surprising given the prominence of such institutions in most historical and contemporary societies. In the quoted 2006 special issue, several authors provide insights on varying religious institutions. Cordery (2006) describes the accounting of a New Zealand missionary order, suggesting missionaries may have been tempted to avoid secular accounting in their early and challenging missionary work. However, good accounting records are maintained, and accountability to funders based on those same records is enacted. Espejo et al. (2006) recount how Spanish authorities attempt to establish the financial status of brotherhoods in 1769. The enlightened Spanish State attempted to reduce Church influence and, in 1783, the State passed a law to regulate the brotherhoods. However, as Espejo et al. (2006) note, such a law does not ‘prescribe any process of accountability for the brotherhoods’ (2006: 144). Prieto et al. (2006) report on accounting in a Spanish monastery. They note that, although the accounting methods used were common at the time, ‘the specific characteristics of the sophisticated method used by the Benedictine monks served both accountability and decision-making purposes’ (Prieto et al., 2006: 242). Work by Dobie (2008a, 2008b) details accounting in monastic houses and church priories from the late Middle Ages. Dobie (2008a) suggests the need to maintain such houses on a sounder financial footing – given increasing debt and falling donations. That increases the prevalence and relevance of accounting, although accounting varies from house to house. Dobie (2008b) is more specific and examines the accounts of the bursar at Durham Cathedral Priory from 1278 to 1398 to identify the financial position of the Priory and determine what financial controls are in place (examples include supporting schedules, monitoring of credit and narrative explanations). Gatti and Poli (2014) explore the creation of a control and accountability system within the Papal States following a 1592 Papal Bull. They show how accounting as a technology helps in that it ‘allowed the Pope to concentrate and centralize political power’ (p. 492). Finally, Leardini and Rossi (2013) link power and accounting. In their study of Verona's Santa Maria della Scala monastery, they suggest that ‘accounting played a key role in reinforcing both hierarchical and horizontal power relations among friars’ (p. 415) at the monastery.

In the management literature, some contemporary studies link and compare modern-day management practices (such as accounting) to those of ancient religious orders (see De Vaujany, 2010; Hiebl and Feldbauer-Durstmüller, 2014; Rost et al., 2010; Wirtz, 2017). The message from such literature is that something can be learned from organisations that have survived over time. For example, Hiebl and Feldbauer-Durstmüller (2014) study the role of a cellarer in a Benedictine abbey and compare this to a modern-day chief financial officer's role. As another example, Mutch (2016) explores Scottish religious practices and how the accountability embedded in such practices results in the Scottish pre-eminence of accounting textbooks of the 1700s. Some Jesuit-specific studies have also been undertaken, as this religious order is known for good recordkeeping. Quattrone (2004) provides an extensive and rich view of the Jesuits, detailing elements of accounting and accountability practices. He focuses on the influence of non-economic arguments on the development of these practices. Quattrone (2009: 88) further explores an accounting treatise of the Jesuit Lodovico Flori. By examining this one and another early accounting treatise, he offers insights into how accounting can be aided by visual representations as a communication medium.

In relation to the present study, work by Liyanarachchi (2009, 2015) offers insights into accounting in Buddhist monasteries. Liyanarachchi (2009) focused on Ceylon and outlined the accounting and auditing practices of Buddhist monasteries based on epigraphic evidence. Liyanarachchi (2009) illustrates how Buddhist monasteries have kept proper records of ‘income’ and expenses, and annually read their statements aloud to maintain their reputation and to safeguard goodwill towards monks, the king and the people. Liyanarachchi (2015) extends his previous work, exploring the role of the seven antecedents of double-entry bookkeeping (namely writing, numerals and arithmetic, private property, money, capital, commerce and credit, see Littleton, 1927) – in supporting the development of previously identified Buddhist monastery accounting. Based on epigraphic evidence and other corroborating historical records, Liyanarachchi (2015) tests if and how the seven antecedents of double-entry bookkeeping may have underpinned the development of simple recordkeeping at Buddhist monasteries. Despite showing the existence of all seven antecedents, there is no evidence to support the existence of double-entry bookkeeping in ancient Ceylon. Thus, Liyanarachchi (2015) concludes that ‘recordkeeping methods are context-specific, and antecedents may not necessarily lead to the double-entry bookkeeping method’ (p. 100).

In summary, the accounting and management history literature reveals some interesting studies on accounting in religious organisations and some literature on accounting in Buddhist monasteries. However, only a few studies (see for instance Creed et al., 2010; Quattrone, 2009, 2015; Tracey, 2016) consider multiple logics at play in religious organisations, and how these may (or may not) have affected accounting and accountability practices. To this end, this study draws on institutional logics, and the next section provides an overview of this approach from the extant literature.

Institutional logics

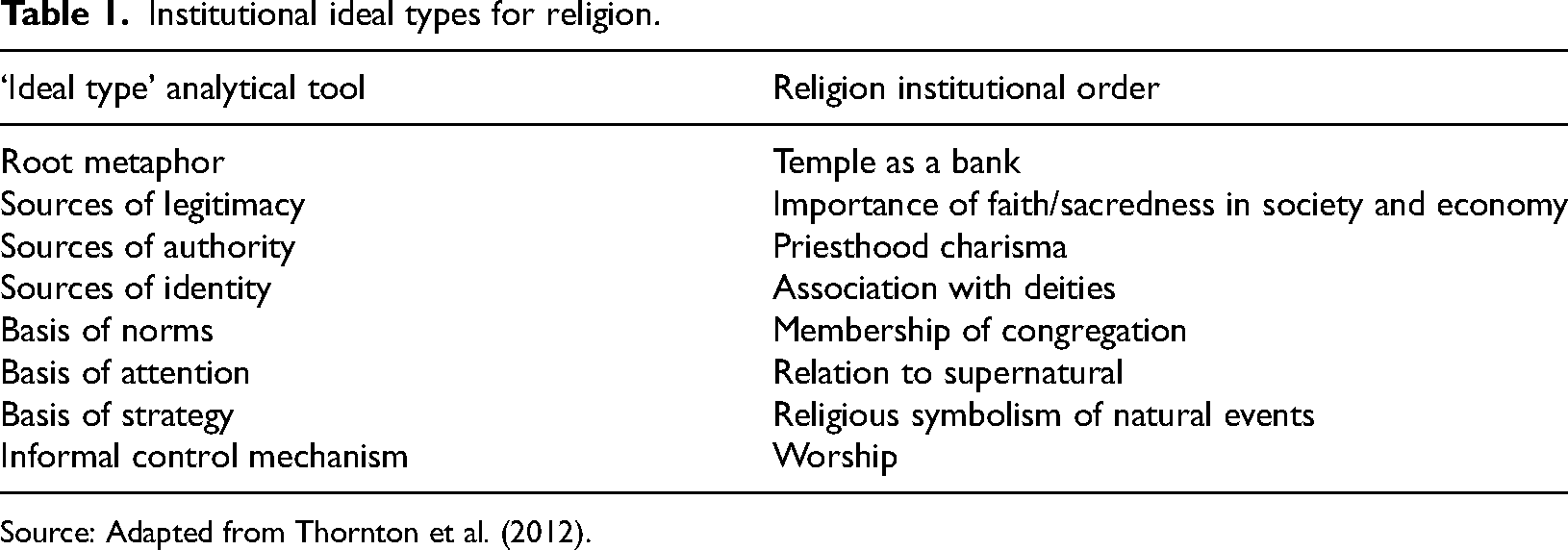

The concept of institutional logics is used as a theoretical lens in this study. To paraphrase Thornton and Ocasio (2008), an institutional logic is a socially constructed pattern of symbols and practices – including assumptions, values and beliefs – by which individuals and organisations provide meaning to their activities. That is, the institutional logic approach recognises societal, organisational and individual components affecting institutional orders. Thornton et al. (2012) identify religion as one of seven forms of institutional orders and provide an ‘ideal type’ – an analytical tool that can be utilised to understand the generalised processes that shape the institutional logic of an order (see Table 1). They also provide an ideal type for the profession: this is relevant to the accounting profession today, but we do not consider it relevant for the timeframe of this study. It is important to note that the institutional logic resulting from an ‘ideal type’ is not prescriptive, and the ‘order’ categories are partially autonomous (Thornton et al., 2012). Other ‘ideal types’ noted by Thornton et al. (2012) include family, community, State, market and corporation. Despite the prominence of ‘belief’ and ‘religion’ in institutional logics theory, a few scholars have studied religion from an institutional perspective. Prior studies on religion and logics have focused on Christian organisations such as churches (see Creed et al., 2010), religious orders (Quattrone, 2004, 2009, 2015) or religious movements (Tracey, 2016). Non-western religions have been largely neglected (Gümüsay, 2020; Tracey et al., 2014).

Institutional ideal types for religion.

Source: Adapted from Thornton et al. (2012).

Earlier studies support the view that an organisation is dominated by a single logic, and they study the processes by which an organisation moves from one dominant logic to another, over time (Greenwood et al., 2011; Lounsbury, 2007). However, more recent studies argued that multiple logics may coexist in an organisation over time. Kraatz and Block (2008) refer to this as institutional pluralism, with Greenwood et al. (2011) terming it ‘institutional complexity’. Such co-existing logics may be either competing (Dunn and Jones, 2010; Greenwood et al., 2014; Pache and Santos, 2010) or compatible (see Lusiani et al., 2019; 2023; Perkmann et al., 2019), but they are rarely interpreted as mutually dependent (Smets et al., 2015). For example, Smets et al. (2015) produced a year-long ethnographic study of re-insurance trading in Lloyd's of London and asserted that their community and market logics were mutually dependent, positively feeding off each other. Prior literature has also documented the management of institutional complexity and suggests various responses, such as decoupling (Meyer and Rowan, 1977), compromise (Oliver, 1991) and combination (Battilana and Dorado, 2010; Busco et al., 2017). However, not all strategies are successful in sustaining multiple logics over a long period of time (see Conrath-Hargreaves and Wüstemann, 2019). Only the combination of practices drawn from different logics is seen as satisfying the competing demands of different stakeholders and it is also referred to as ‘blended hybridization’ (Greenwood et al., 2011: 352). A combination of logics is observed to induce hybrid practices in an organisation (Dai et al., 2017) and it is considered the only response that indicates a ‘real’ hybridisation because elements of competing institutional logics and contradicting demands are combined over time (Battilana and Lee, 2014; Conrath-Hargreaves and Wüstemann, 2019).

A related stream of literature explores the role of accounting, in the realm of multiple institutional logics. Some scholars have considered accounting as a mechanism to manage institutional complexity through decoupling (Siti-Nabiha and Scapens, 2005), compromise (Amans et al., 2015; Ezzamel et al., 2012) or a combination of multiple logics (Busco et al., 2017), whilst some others view (management) accounting as a source of organisational tensions (Malina and Selto, 2001; Rahaman et al., 2010). Moreover, some prior studies have highlighted that institutional complexity leads to different accounting practices (Dai et al., 2017; Ezzamel et al., 2012). For instance, Dai et al. (2017) record the reconfiguration of management accounting practices in a Chinese state-owned-enterprise following an initial public offering, whereas Ezzamel et al. (2012) indicate the introduction of budgeting practices in the field of education, as a result of the emergence of a new business logic. This line of research has been extended by Conrath-Hargreaves and Wüstemann (2019) as they explore how an organisation (whose response is noted as ‘reactive decoupling’) uses accounting to superficially comply with a newly arising logic, in an effort to justify its legitimacy.

In the accounting history literature, many studies draw on institutional theory in a broader sense (see Gervais and Quinn, 2016; Quinn and Jackson, 2014), while a few of them mention or utilise institutional logics. McKinstry et al. (2019) mention the notion of a ‘situated logic’, which is not an institutional logic as described by Thornton et al. (2012) but it captures the notion of differing forms of rationality, that apply in scenarios of accounting change. Quattrone (2015) extends his prior work on Jesuits’ accounting by using institutional logics, and noting that the logics of Jesuit administrative procedures, while centralised, are also flexible to local context. Quattrone (2015: 436) also proposed that the varying logics of the Jesuits over time ‘challenge[ ] key assumptions in … one or more dominant logics that are internally stable and shape practice’. More recently, Quinn et al. (2021) supported Quattrone (2015), noting how Jesuit accounting control rules have maintained a core stability over four centuries, but have been adapted according to internal and external factors. Lusiani et al. (2019) also use institutional logics in a study of a hybrid organisation, a charity, facing competing institutional logics (see also Lusiani et al., 2023 for a similar study on a hospice that operated in the fourteenth to sixteenth century Venice). Lusiani et al. (2019) note three logics, which they term devotional, private and public logics. These three logics embody different interests of the charity they study – spiritual interests, material interests and social interests – as well as depicting specific relationships with different stakeholders (church, charity members, the State/society). Lusiani et al. (2019) also point out that knowledge of how different logics coexist and are interdependent is limited, even in a contemporary setting (see Quattrone, 2015). They also note that accounting practices may be viewed as tools ‘by which the correct and transparent conduct is ensured in the devotional, private and public spheres’ (Lusiani et al., 2019: 457).

Context, sources and method

Ancient Ceylon and Buddhism

Mahavamsa is one of the prominent chronicles of Ceylon. It was written by the monk Mahanama in the Pali language in the fifth or sixth century AD (Codrington, 1924; Geiger, 1912). According to Mahavamsa, Ceylonese history traditionally starts in circa the sixth century BC, upon the arrival of the Indian prince Vijaya and his followers (Geiger, 1912). Prince Vijaya became the first king of the country, and since then the island has been ruled by approximately 186 kings (Paranavitana, 1933). From the sixteenth century, the country experiences varying degrees of rule from several European nations, namely the Portuguese and Dutch empires. Finally, in 1815, Ceylon became part of the British Empire.

With the arrival of Buddhism in Ceylon in the third century BC, Buddhism received royal patronage and since then, government administration, architecture, language and literature, social conventions/customs and individual thinking have been inspired by Buddha's teachings (Liyanarachchi, 2009). Since the teachings of Buddha have been introduced to Ceylon, merit (pin) and demerit/sin (pav) are guiding life principles. Good deeds or good karma will result in merit, good consequences and good re-birth; bad karma will result in negative consequences and bad re-birth (Gombrich, 2012). Gombrich (2012) further explains that karma refers to actions driven by intention; it is a universal self-governing law, and it operates by itself, without any divine force. ‘Like any natural law, it applies in the same way to everyone and does not discriminate based on power, social status or caste’ (Liyanarachchi, 2008: 124).

Sources and method

An archival approach is used to collect data. This study predominantly employs primary sources. These sources are pre-historic slab, pillar and rock inscriptions, which have been discovered, recorded and translated by researchers at the Department of Archaeology of Sri Lanka, namely Müller (1883), Wickremasinghe (1928), Paranavitana (1933) and Codrington (1924). Inscriptions are a means of mass communication for inhabitants of ancient Ceylon. The most common form is carving on rock surfaces. These inscriptions are in many parts of the island, mainly near age-old temples and monasteries, water tanks, ports and other prime locations of the time.

The epigraphic material used in this study dates from the first century AD during the reign of King Kutakanna – the 30th king in the royal lineage of Ceylon (Paranavitana, 1933). The sample consists of 122 inscriptions (see Appendix 1) for the period from the first century to the sixteenth century AD, during the reigns of approximately 32 kings and over seven administrative capitals or kingdoms. In addition to these inscriptions, several other historical records, including Mahavamsa, the great chronicle written by Mahanama and translated by Geiger (1912), Purathana Lankawa (Ancient Lanka) From 304-560 AD by Jayawardana (1964) and History of Buddhism in Ceylon by Rahula (1956) have been used. These texts are used to check the accuracy of details and translations provided in inscriptions and to gather independent corroborating evidence on the prevailing socio-political and economic environment. Although the inscriptions themselves provide valuable economic, social and political information about early civilisation in Ceylon, only a handful of attempts have been made so far to analyse them from an accounting perspective.

A meaning-oriented manual content analysis approach is used to analyse the ancient inscriptions. Initially a list of predefined classifying rules, ‘to assist in categorising, coding and recording data’ has been developed, based on the prior work of Kumarasinghe and Samkin (2020: 10). These rules consist of identifying the purpose, time and location of each inscription and the reigning king. Inscriptions with no time-related information are excluded. For example, one inscription from the North Central Province, written on an oblong copper plaque, has been excluded as its translators cannot assign it to the reign of any king in particular or estimate its palaeographical age. The content of the inscriptions is then classified according to themes that represent forms of logic, which may affect Buddhist monastic accounting. The themes used (devotional, public and private) are drawn from institutional logics and prior work by Lusiani et al. (2019). For the period of analysis here, devotional logic refers to how Buddhist monks follow Buddha's teachings, adopt a frugal lifestyle and abstain from sensual pleasures to pursue spiritual goals. Therefore ideally, Buddhist monks should not pursue worldly desires or engage in endeavours with a profit motive. Public logic refers to the social interests of monks, who are bestowed with the responsibility of preserving and disseminating Buddha's teachings. Over the years, monasteries receive abundant donations, mainly by kings that make them more established, developed and wealthy, therefore managing monastic wealth becomes crucial. This gives rise to the private logic.

To process the analysis of the inscriptions according to the three themes mentioned above, we draw from the ideal types presented by Thornton et al. (2012) and the work of Lusiani et al. (2019). Table 2 shows how we interpret whether relevant inscriptions are representative of devotional, private or public logic. Each column of Table 2 represents a feature of each logic, and when more features of a logic emerge from an inscription, such inscriptions (or part of them) are classified accordingly.

Logic type and description.

Source: Elaboration from Thornton et al. (2012) and Lusiani et al. (2019).

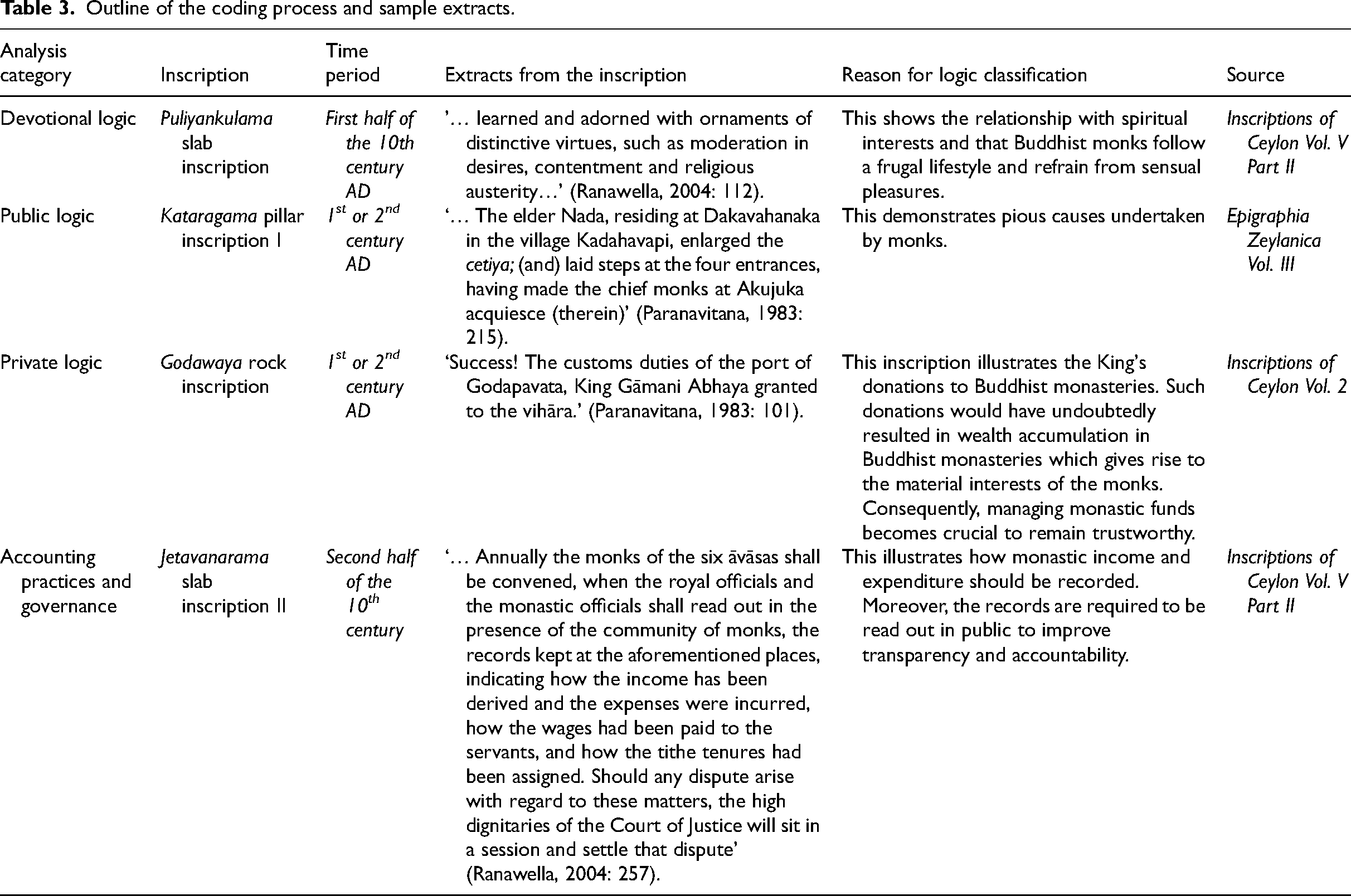

Coding is carried out by one of the authors in the first instance and checked by the other author. An outline of the coding process is provided in Table 3.

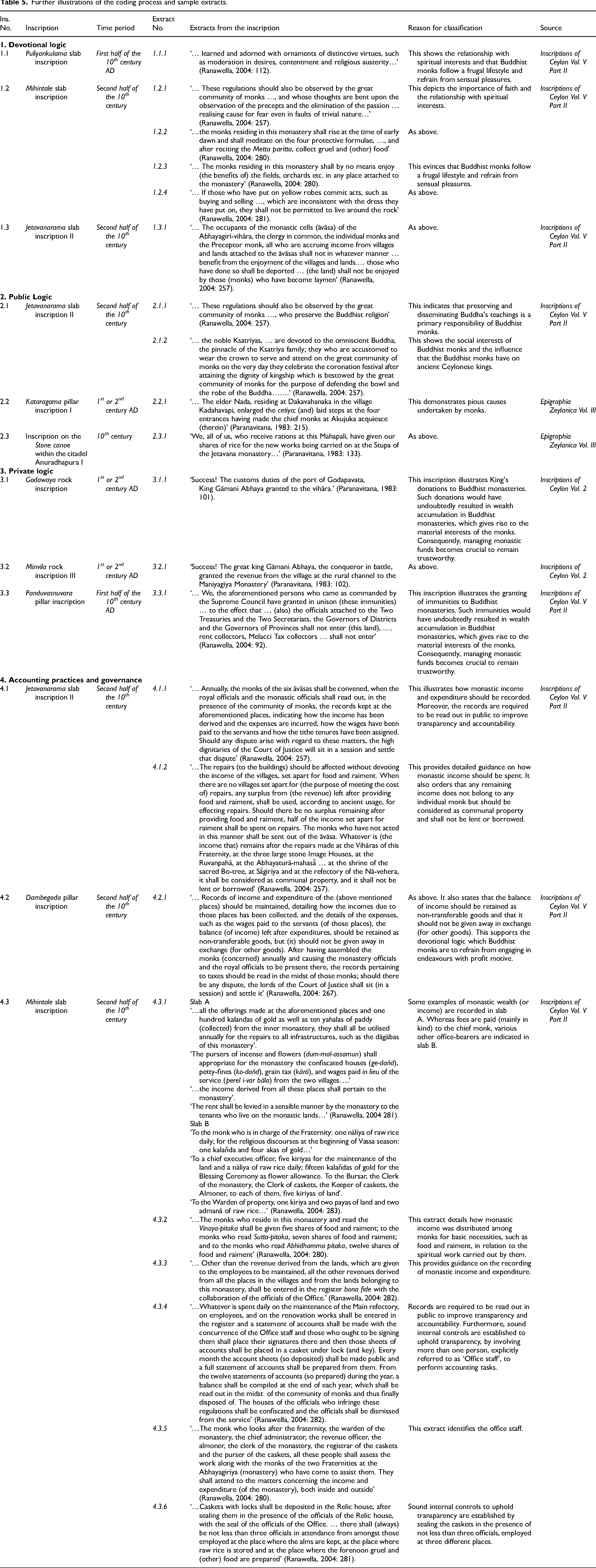

Outline of the coding process and sample extracts.

For example, the Puliyankulama slab inscription (see Table 3) records that Buddhist monks are ‘learned and adorned with ornaments of distinctive virtues, such as moderation in desires, contentment and religious austerity’ (Ranawella, 2004:112), implying that they follow a frugal lifestyle and refrain themselve from sensual pleasures. This shows their relationship with spiritual interests (as per Lusiani et al., 2019; Thornton et al., 2012). Thus, this inscription has been classified under the devotional logic. Moreover, the Kataragama pillar inscription notes that a senior monk residing in a certain village ‘enlarged the cetiya (pagoda/stupa); (and) laid steps at the four entrances having made the chief monks at Akujuka acquiesce (therein)’ (Paranavitana, 1983: 215). This, as per Lusiani et al. (2019) demonstrates pious causes undertaken by the monks and it has been classified under the public logic. Godawaya rock inscription denotes that ‘the customs duties of the port of Godapavata, King Gāmani Abhaya granted to the vihāra’ (Paranavitana, 1983: 101), illustrating kings' donations to Buddhist monasteries. As noted, such donations would result in wealth accumulation (as per Lusiani et al., 2019) and engender material interests of the monks. Hence, this is classified under the private logic. Finally, the second Jetavanarama slab inscription indicates that ‘annually the monks of the six āvāsas shall be convened, when the royal officials and the monastic officials shall read out, in the presence of the community of monks, the records kept at the aforementioned places, indicating how the income has been derived and the expenses were incurred’ (Ranawella, 2004: 257), which outlines how monastic income and expenditure should be recorded and accountability discharged. Moreover, the records are required to be read out in public and, thus, they have been categorised as accounting practices and governance.

Some words of caution on the sources and methods should be spent. First, while there is no intention to be a-historical, occasional use of modern terminology is inevitable. Second, as Jones (2009) underlines, the accounting practices discussed here may not form part of a fully-fledged system, but they arise from many diverse elements. Thus, following Miller and Napier (1993), this study intends to contribute to knowledge in a piecemeal fashion. Some other concerns will be discussed later as limitations of the study.

Findings: logics identified

Overview of inscriptions

This study draws on 122 translated inscriptions (see Appendix 1); all but three are lithic in nature. Of these inscriptions, 76 record an immunity grant, a donation, or both to Buddhist monasteries. Immunity grants are royal edicts by the king, over certain lands gifted to Buddhist monasteries or directed to crown officials for their faithful service. Revenue officers or other officials representing the royal household cannot enter those lands to collect taxes, rents or fines, because it is prohibited by the king. Such immunity provisions even forbid the arrest of a person who enters the immune land after committing a murder. The murderer can only be arrested outside the boundaries of the immune land (Rahula, 1956; Ranawella, 2004). Donations of money and in kind, together with immunities, result in an accumulation of wealth, which warrants systematic recordkeeping practices. Thus, these 76 inscriptions appear to be representative of a private logic.

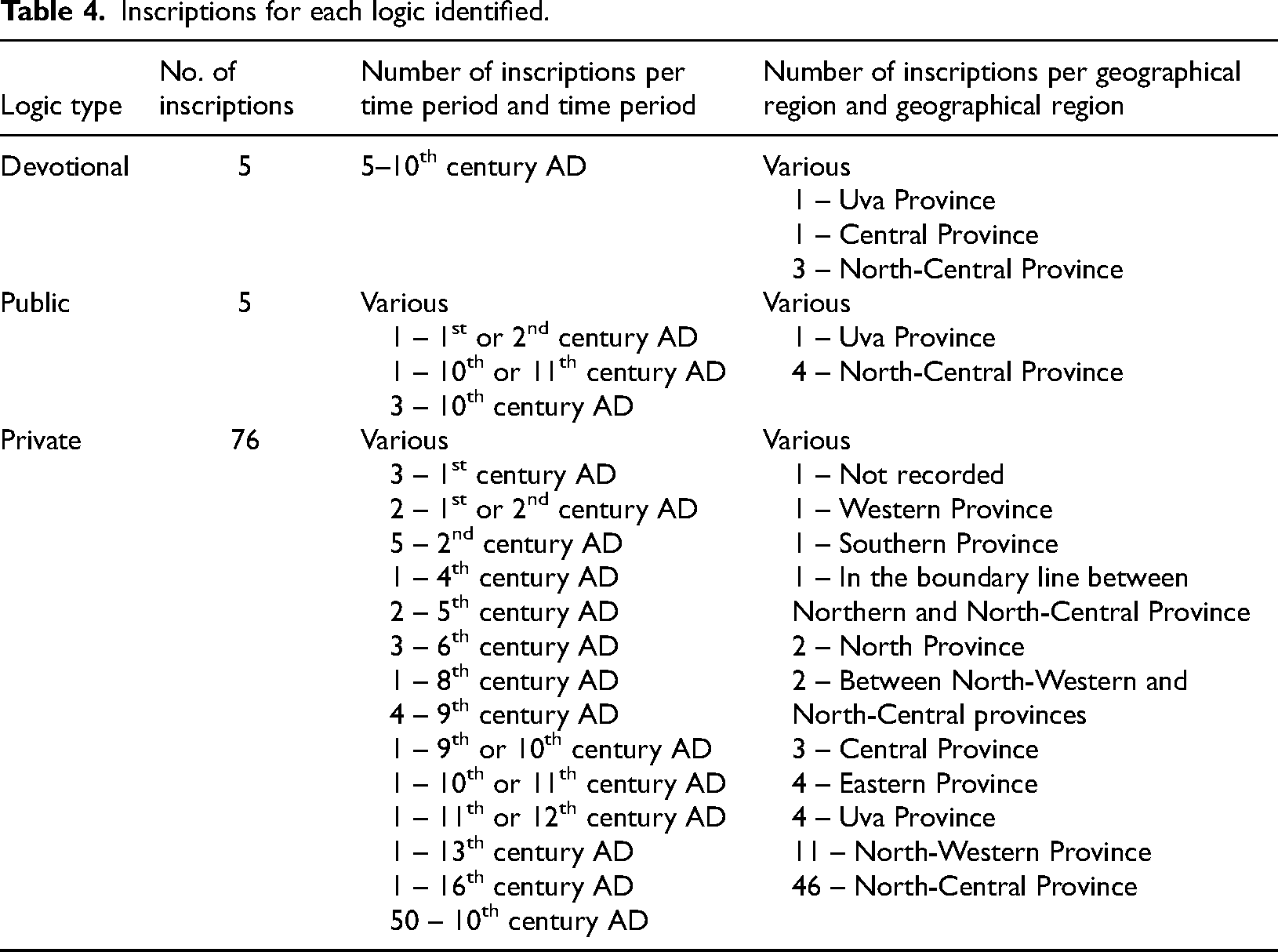

In addition, five inscriptions have been categorised under devotional logic and five under public logic. The number of inscriptions for each logic category, time and geographical region is depicted in Table 4.

Inscriptions for each logic identified.

Further analysis of inscriptions reveals they originate from all over Ceylon, but most of them (71 of 122) are referred to its North-Central Province. This province includes the first administrative capital of ancient Ceylon – Anuradhapura – which is ruled by over 100 kings for approximately 1,300 years (Geiger, 1912). This is the longest period held by any administrative capital in ancient Ceylon. Furthermore, this province is currently not densely populated, thus the preservation of the rock inscriptions in their original historical sites has been relatively less complicated. These reasons justify the placement of most inscriptions in the North-Central Province. Furthermore, the highest number of inscriptions represent the reign of King Dappula IV (924–935 AD), with 34 records.

A closer examination of the inscriptions reveals that they relate to nine common topics, namely: king's charitable acts, charitable acts by others, immunity grants by the king, king's grants to royal ministers/individuals, prototype banks, sets of ecclesiastical regulations agreed by common consent, village administration, administration of justice and other. The greatest number of inscriptions in the sample are royal edicts by the king to grant immunities over certain land. Most inscriptions are representative of a period from the ninth to the eleventh century. Most of the inscriptions from this period record immunity grants, whereas inscriptions during the first to third centuries mostly record charitable acts. The remainder of this section examines examples of the three logic types. Table 5 includes the examples referred to in this section and offers detailed illustration of the coding process and the analysis.

Further illustrations of the coding process and sample extracts.

Devotional logic

Buddhist teachings suggest that an individual's volitional actions result in accumulating karma, either good or bad, and result in one's endless wandering of life, known as the samsāra, the cycle of death and rebirth. Therefore, the Buddhist monasteries are occupied by monks, who left their homes and families to follow a frugal lifestyle and abstain from sensual pleasures, with the aim of putting an end to the suffering and the cycle of death and rebirth, ultimately in the pursuit of nirvāna.

This is reflective of devotional logic, where Buddhist monks pursue spiritual goals. The devotional logic shows features such as the importance of faith and the relationship with spirituality (Lusiani et al., 2019; Thornton et al., 2012; see Table 2). In total, five of the 122 inscriptions are categorised as containing evidence of devotional logic. This logic is illustrated in, for example, extracts 1.1.1 and 1.2.1 as per Table 5. These extracts describe Buddhist monks as ‘learned and adorned with ornaments of distinctive virtues, such as moderation in desires, contentment, and religious austerity’ (extract 1.1.1; Ranawella, 2004: 112) and as ‘the great community of monks … whose thoughts are bent upon the observation of the precepts and the elimination of the passion, … realising cause for fear even in faults of trivial nature’ (extract 1.2.1; Ranawella, 2004: 257). Buddhist monks also follow a strict daily routine, where they awake very early and spend most of their time meditating and praying in the pursuit of spiritual goals – extract 1.2.2, for example, notes monks ‘shall rise at the time of early dawn and shall meditate’. Also, ideally, Buddhist monks should not pursue worldly desires. At the time of these inscriptions, such desires would reflect matters such as enjoying benefits or income from villages and lands. Extract 1.2.3, for example, notes ‘monks residing in this monastery shall by no means enjoy (the benefits of) the fields, orchards and etc. in any place attached to the inner monastery’ (Ranawella, 2004: 280); extract 1.3.1 notes ‘individual monks and the Preceptor monk, all who are accruing income from villages and lands attached to the āvāsas shall not in whatever manner [benefit from] the enjoyment of [the wealth produced by] villages and lands; those who have done so shall be deported’ (Ranawella, 2004: 257). The monks should also not engage in commercial activities. For example, extract 1.2.4 notes ‘if those who have put on yellow robes commit acts, such as buying and selling … which are inconsistent with the dress they have put on, they shall not be permitted to live around the rock’ (Ranawella, 2004: 281).

Such devotional guidelines are overseen at the monasteries by a resident chief monk, ‘who is responsible for its discipline and order’ (Rahula, 1956: 135). However, devotional logic tends to emphasise notions of morality and identity of Buddhist monks, urging them to render an account to the self and the monastery. The concepts of merit (pin), demerit or sin (pav) and karma, which constitute devotional logic, restrained the monks from violating monastic regulations and acted as tools of self-regulation. This moral guidance appears to be similar to that identified by Carmona and Ezzamel (2007) in Mesopotamia and ancient Egypt and to the Jesuits morale as suggested by Da Silva et al. (2017).

Public logic

In total, five of the 122 inscriptions are categorised as containing evidence of public logic, which, in this study, refers to the social interests of Buddhist monks (see Table 2). The relevant inscriptions mainly show evidence of the monks being entrusted with the responsibility of preserving and disseminating Buddha's teachings (or dharma). This is evident in extract 2.1.1, for example, which states that ‘regulations should also be observed by the great community of monks, who preserve the Buddhist religion’ (Ranawella, 2004: 257).

As mentioned by Lusiani et al. (2019), assisting the poor is another important feature of this logic (see Table 2). However, this is not supported by the inscriptions examined here. As explained under the devotional logic, monks live a simple life, refraining from worldly pleasures. They are not allowed to enjoy or use wealth, and in ancient times, they beg for food to symbolise self-denial and moderation of desire. This suggests that the Buddhist monks are mostly dependent on laymen. This may be the reason for the non-existence of epigraphic evidence to support that the monks assisted the poor. However, in the later centuries, monasteries have grown in size and wealth – which is discussed further in the private logic sub-section. Although monasteries become the owners of property and/or money, such property is regarded as the benefit of the members who belong to that monastery and not as individual monks’ possessions – who cannot own properties (Liyanarachchi, 2009). As evidenced in extracts 2.2.1 and 2.3.1, monks use any surplus to further develop their own monasteries, building pagodas/stupas (cetiya) or other Buddhist monuments to be worshipped by the public. Although it is quite possible that the monks help the needy, with money or in-kind, this may have occurred at a personal level and is not recorded in inscriptions.

With the introduction of Buddhism to Ceylon in the third century BC, the monks become an important group in society, owing to their knowledge and reputation to the learning of Buddhist doctrines. They are lifelong learners, and they diversify their intellectual interests into other areas such as language, grammar and literature (Rahula, 1956). A Buddhist education system emerges (Kumarasinghe and Samkin, 2020) and the monks start engaging in disseminating knowledge beyond the spiritual domain, to recruit followers of Buddhism in the royal family members, other elites and lay people. Extract 2.1.2 shows the influence that the monks have on ancient Ceylonese kings (see also Bigoni et al., 2013; Espejo et al., 2006; Gatti and Poli, 2014, for influence of the church on the state), as it clearly indicates that the kingship is bestowed by the great community of monks: ‘…the dignity of kingship, which is bestowed by the great community of monks for the purpose of defending the bowl and the robe of the Buddha…’ (Ranawella, 2004: 257).

The above implies that the blessing of the Sangha (the order of the monks without any specific location or establishment) is crucial for an individual to be crowned as king. The king had a close relationship with the chief monk in a monastery and the Great Chronicle, Mahavamsa, provides abundant evidence that at times monks provide advice to the king regarding ruling the state.

Thus, in ancient Ceylon, Buddhist monasteries are not only considered as religious organisations but flourished as prominent socio-political institutes. They have direct links to the teachings of Buddha and the order of monks that is established to preserve and to continue such teachings (Liyanarachchi, 2009). Through education and their relationship with kings, the public logic of Buddhist monasteries is fostered, granting them status in the community (Thornton et al., 2012).

Private logic

In total, 76 of the 122 inscriptions are categorised as containing evidence of private logic, which refers to wealth accumulation and material interests of the monasteries, in the context of this study (see Table 2). As noted earlier, private logic emerges as monasteries become more established, developed and wealthy. Managing monastic funds is crucial to safeguard the reputation of monks, to remain trustworthy and to maintain a good relationship, especially with kings. As it may be envisaged, this private logic has more interactions with accounting, which is detailed in the next section.

According to the epigraphic evidence examined, kings donate substantial wealth to monasteries – such as land and other forms of contributions –as a sign of their devotion and respect towards Buddhism and Sangha. For example, extracts 3.1.1 and 3.2.1 indicate that kings have granted ongoing revenue sources, such as ‘customs duties of the port of Godapavata’ or ‘the revenue from the village at the rural channel’ to the nearby monasteries. The Great Chronicle, Mahavamsa from the fifth century, provides further evidence of ancient kings constructing and donating monasteries or money to the monks. According to Liyanarachchi (2009), kings donate land to the Sangha (Buddhist monks in general) and build living quarters, swimming pools and monastic infrastructures; they provide parks and forestland for the use of Buddhist monks. Epigraphic evidence reveals that donations to Sangha are also made by private individuals (Rahula, 1956). In addition to land and money, monasteries also receive immunities. Epigraphic evidence shows that monasteries are often exempt from land taxes, irrigation taxes, rent and similar contributions to the kingship. For example, extract 3.3.1 notes ‘the officials attached to the Two Treasuries and the Two Secretariats, the Governors of Districts and the Governors of Provinces shall not enter (this land); rent collectors, Melacci tax collectors shall not enter’. As a result of wealth accumulation over time, wealth management activities in monasteries become more important.

Discussion of the findings on the relationships among the identified logics

The findings are now discussed according to the coexistence and mutual dependence of logics, the institutional complexity of Buddhist monasteries and the use of accounting. Finally, the combination of multiple logics via accounting is analysed. Additional references to the epigraphic evidence are introduced to support the discussion.

Coexistence and mutual dependence between logics

Accumulation of wealth in monasteries and the proficiency in reading and writing derived from learning Buddhist doctrines (see public logic) granted Buddhist monks significant control over lay people in ancient Ceylon (Liyanarachchi, 2009). As a result, the kings are cautious to win a positive relationship with the Buddhist monks for the sake of a peaceful and successful ruling (Rahula, 1956). These factors lead Buddhist monasteries to become a prominent organisation in the ancient Ceylonese society.

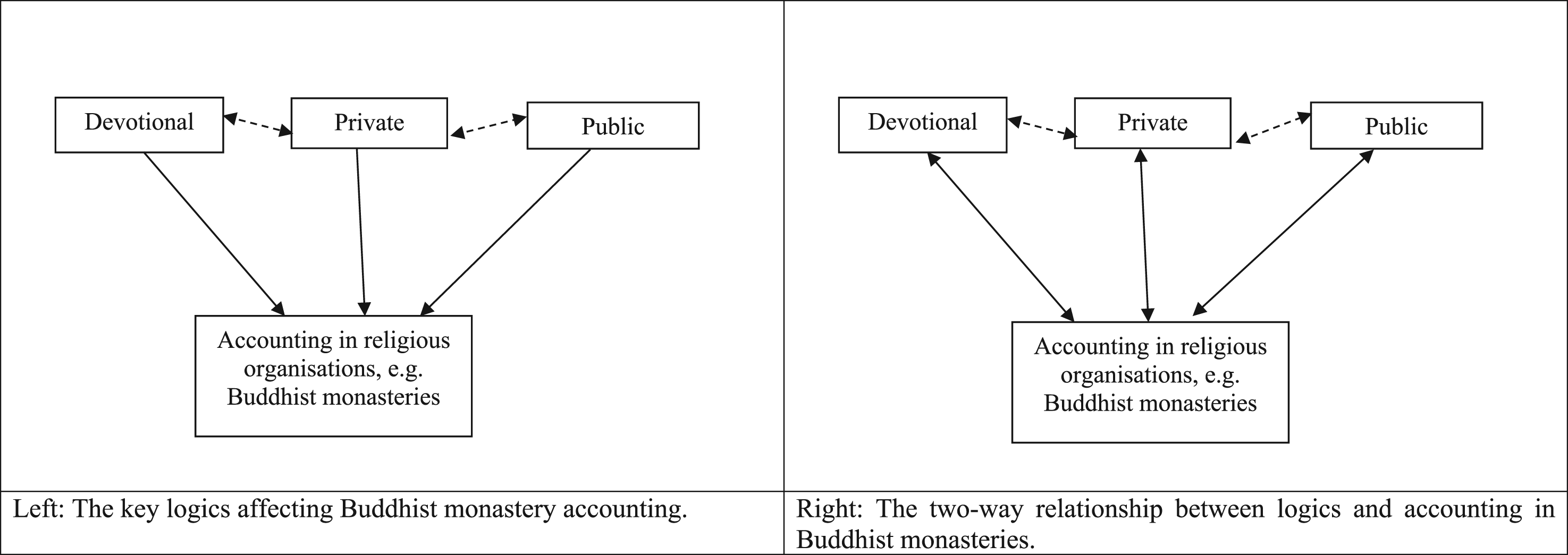

The accumulation of wealth in Buddhist monasteries also results in several issues including wealth misappropriation, the potential decline in discipline among monks and the potential inability of the monasteries themselves to address satisfactorily these issues (Liyanarachchi, 2009). Therefore, kings, as the official protector of Buddhism in the island (Ranawella, 2004), have the authority to intervene to prevent these issues, and as per Liyanarachchi (2009) the interventions include keeping proper records and having an annual public reading of the bookkeeping. Buddhist monks are reliant on kings for donations (Liyanarachchi, 2009) and thus do not want to hurt their relationship through lack of compliance (public logic). The public logic emphasises monks’ responsibility to maintain trustworthy relationships, mainly with kings and people. Unfortunately, Buddhist teachings provide no grounds for business/profit or worldly possessions, as detailed in the devotional logic. Additionally, devotional logic urges Buddhist monks to give up on all their material desires and to refrain from enjoying worldly pleasures. Therefore, misappropriation of monastic wealth by monks would not only jeopardise their spiritual goals but also cause suspicion and mistrust among kings and Buddhist followers. Therefore, wealth management activities in monasteries become crucial. Thus, it can be understood that the devotional and public logics in Buddhist monasteries feed into the private logic in this context and promoted systematic recordkeeping practices to manage monastic wealth. This is illustrated in Figure 1, within the left panel.

Logics and accounting in Buddhist religious organisations. Left: The key logics affecting Buddhist monastery accounting. Right: The two-way relationship between logics and accounting in Buddhist monasteries.

The private logic seems to prevail over the other two logics in ensuring correct wealth management. While the devotional and public logics appear to have dominated and co-existed at first, the accumulation of wealth by Buddhist monasteries (see Liyanarachchi, 2009) pushes the private logic to come into play. This extends Ponte and Pesci's (2022) work by suggesting that, in addition to the context (such as the interplay of location and time), the existing demands on an organisation may also play a key role in shaping organisational changes. Managing material interests (private logic) seems also crucial to promote transparency or to show that wealth is not spent by individual monks or on worldly goods, thereby upholding the devotional logic. Private logic fosters the legitimate impression that Buddhist monasteries remain trustworthy and can maintain a good relationship with kings to foster the public logic. Smets et al. (2015) contend that multiple logics can be contradictory, yet mutually dependent at the same time. In this case, private logic and devotional/public logics are mutually dependent, despite their apparent inconsistencies. In other words, devotional and public logics feed into the seemingly contradictory private logic, and vice versa. This leads to the assessment that the three logics may coexist within ancient Buddhist monasteries. Thus, the double-headed dotted arrows in Figure 1 (left) between devotional/public logics and private logic reflect this mutual dependence. Finally, the private logic implies a need for systematic recordkeeping or accounting practices to be adopted in Buddhist monasteries.

Institutional complexity and the use of accounting

As hinted at in the previous section, accounting is adopted as a tool to respond to multiple institutional logics. Accounting, in the context of this study, refers to both systematic recordkeeping practices about inflows and outflows of resources to and from Buddhist monasteries, and accountability habits such as reading records out loud in assemblies of monks and other similar controls in place. For example, extract 4.3.1 (slab A) provides some examples of monastic wealth and income (such as gold and paddy) and some income sources (such as petty fines, grain taxes and ground rent). The epigraphic evidence also provides some guidance on how they should be spent. For example, extract 4.1.2 illustrates a pecking order of needs, where priority is given to food and raiment. Any remaining income can be spent on maintenance and repairs of monastic infrastructures. Extract 4.3.2 indicates that monastic wealth is distributed among monks in terms of food and raiment, according to the type of spiritual work carried out. Moreover, slab B of extract 4.3.1 indicates some fees paid to the chief monk and other office-bearers.

Some inscriptions refer to royal edicts on the recording of monastic income and expenditure. For example, extract 4.1.1 notes: monastic officials shall read out in the presence of the community of monks the records kept at the aforementioned places, indicating how the income has been derived and the expenses are incurred, how the wages had been paid to the servants. (Ranawella, 2004: 257)

This is a clear example of the use of accounting to address the private logic. Similarly, extracts 4.2.1 and 4.3.3 are reflective of how accounting can be deployed to manage the private logic: records of income and expenditure of the (above mentioned places) should be maintained, detailing how the incomes due to those places had been collected, and the details of the expenses, such as the wages paid to the servants (attached to those places). (Ranawella, 2004: 267) …revenue derived from all the places in the villages and from the lands belonging to this monastery, shall be entered in the register bona fide with the concurrence of the officials of the Office. (Ranawella, 2004: 282)

Extracts 4.1.1, 4.2.1 and 4.3.4 also outline that those records are to be read out in front of the community of monks, monastery officials and royal officials, thereby assigning a form of accountability to them. Whilst this can be directly related to a private logic, it also facilitates a devotional logic that the monks are to be trusted in their spiritual endeavours. The trustworthiness of monks would further uphold their public image and support sound relations with the king, in particular, ensuring public accountability.

Additionally, extracts 4.3.3, 4.3.4 and 4.3.5 refer to various roles within the monastery accounting, all reflective of private logics. Extract 4.3.3 (see above) refers to the ‘concurrence of the officials of the Office’, suggesting that any records were inspected or verified by other people than the records’ keeper. Extract 4.3.4 again mentions concurrency: ‘The register and a statement of accounts shall be made with the concurrence of the Office Staff, and those who ought to be signed them shall place their signatures there, and then those sheets of accounts shall be placed in a casket under lock (and key)’ (Ranawella, 2004: 282).

This extract also notes a year-end summary of accounts to be made ‘from the twelve statements of accounts (so prepared) during the year, a balance shall be compiled at the end of each year…’.

Extract 4.3.5 mentioned several roles: the monk who looks after the fraternity, the warden of the monastery, the chief administrator, the revenue officer, the almoner, the clerk of the monastery, the registrar of the caskets and the purser of the caskets; all these persons shall assess the work, along with the monks of the two Fraternities at the Abhayagiriya (monastery) who have come to assist them and attend to the matters concerning the income and expenditure etc. (of the monastery), both inside and outside. (Ranawella, 2004: 280)

Extract 4.3.6 depicts how caskets should be sealed in the presence of no less than three officials, who are employed at three different places (possibly to increase transparency and to avoid collusion): …Caskets with lockers shall be deposited in the Relic house, after having sealed them in the presence of the officials of the Relic house, with the seal of the officials of the Office. … there shall (always) be not less than three persons in attendance from amongst those employed at the place where the alms is kept, the place where raw rice is issued and at the place where the forenoon gruel and (other) food are prepared. (Ranawella, 2004: 281)

The above extract illustrates that more than one person was involved, explicitly referred to as ‘office staff’, to perform accounting tasks and internal controls. This can be directly attributable to a private logic, not only to curtail fraud and other inappropriate actions by monks, but also to endorse monks’ trustworthiness in their spiritual endeavours, as indicated by the devotional logic. This trustworthiness would further strengthen the public image of the monks, supporting a public logic.

The inscriptions suggest that notions of systematic recordkeeping existed in ancient Ceylonese Buddhist monasteries. To uphold transparency – crucial in handling monastic funds and upholding devotional and public logics – a form of accounting system is put in place to record incomes and expenditures. A sound internal system of controls, such as engaging more than one person in accounting tasks, is also in place. Additionally, the requirement to read out records (or summaries) to the community plays a role in facilitating accountability practices. These practices seem also to encapsulate a devotional logic in that it provides evidence that the monks are devout and do not gain personal benefits from worldly goods, such as land or other forms of wealth, which are donated to the monastery. The trustworthiness of monks would further strengthen their public image and support sound relations with the king, in particular, ensuring a public logic. In essence, it can be argued that the adoption of accounting practices aids Buddhist monasteries in managing and responding to competing logics and organisational demands and supports their legitimacy as a prominent religious and socio-political organisation in ancient Ceylon.

This evidence and discussion have demonstrated how the three logics influence the nature of accounting and, at the same time, how accounting allows monks to discharge their accountability and show their devotional logic (wealth is not spent for the benefit of individual monks or on worldly goods). Accounting further supports public logic (by safeguarding the monastery’s social interest of being connected with the kings and the community, and its public image) and it is an expression of private logic (as an important tool to manage monastic wealth and the potential risks fraud and misappropriation included). Thus, it is not that accounting only ensures of the co-existence of devotional, public or private logics, but these logics also influence accounting, by suggesting a dynamic two-way relationship which is depicted in Figure 1, right panel. The work of Quinn et al. (2021) hints at such two-way relationship, in the setting of the Jesuit monastic order. That work identifies the emphasis on spiritual guidance in the rules of the Jesuits, which we read as institutional notions of logics.

Lusiani et al. (2019) also explore how institutional complexity – which they define as the existence of multiple logics – can be embedded within an organisation without conflict. They argue that institutional complexity is normally operating in established organisational contexts. Smets et al. (2015) suggests that institutional complexity itself can be institutionalised. This analysis is supportive of both conclusions above, although one logic seems to be more frequently featured (private logic) in the inscriptions analysed - through an accounting perspective. Buddhism as a faith and Buddhist monasteries have remained quite stable over time. While private logic emerges in our analysis, the evidence suggests that devotional logic firmly underpins this private logic. This co-existence of several underlying logics, apparently not in conflict, in an ancient historical setting, supports the findings of Lusiani et al. (2019; 2023) and it may be comparable to more modern realities/organisations such as co-operative banks, which operate based on competing logics (van der Steen et al., 2021).

Combination of multiple logics via accounting

This section discusses how practices and characteristics of different and seemingly competing logics have been combined via the use of accounting in our evidence. For example, the opening few sentences of extract 4.2.1 detail how monastic income and expenditure should be recorded, but then they state that: ‘the balance (of income) left after expenditures, should be retained as non-transferable goods, but (it) should not be given away in exchange (for other goods)’ (Ranawella, 2004: 267).

Recording income and expenditure and calculating the surplus or deficit indicate features of private logic. The above-mentioned extract clearly informs that the balance should neither be consumed nor used as a mode of exchange by the monks, as monks should only pursue spiritual goals and refrain from worldly desires, in pursuing their devotional logic. Therefore, this suggests the reliance on accounting by Buddhist monks that is predominantly shaped by devotional logic.

Extract 1.3.1, in conjunction with extract 4.1.1, outlines the presence of guidelines on how monastic income and expenditures should be recorded. Extract 1.3.1 states: The occupants of the monastic cells (āvāsa) of the Abhayagiri-vihāra, the clergy, the individual monks and the Preceptor monk, all of who are accruing income from villages and lands attached to the āvāsas shall not in whatever manner (benefit from) … the enjoyment of (the wealth produced by) villages and lands… Those who have done so shall be deported … (the land) shall not be enjoyed by those (monks) who have become laymen. (Ranawella, 2004: 257)

Extract 4.1.2 indicates that any surplus should be kept as communal property and shall not be lent or borrowed: …whatever (is the income that) remains after the repairs have been affected at the Vihāras attached to this Fraternity, at the three large stone Image Houses, at the Ruvanpahā, at the Abhayaturā-mahasǟ … at the shrine of the sacred Bo-tree, at Sǟgiriya and at the refectory of the Nā-vehera, shall be kept as communal property, and it shall not be borrowed or loaned. (Ranawella, 2004: 257)

This extract provides further examples of how features of private logic (such as wealth management activities) and devotional logic (i.e., the pursuit of spiritual goals) have been combined in accounting practices. In essence, the quoted extract elucidates how accounting has been deployed to combine features of different and competing logics. Combining the characteristics of multiple logics, also known as ‘bridging’ (Conrath-Hargreaves and Wüstemann, 2019; Smets et al., 2015) or selective coupling (Pache and Santos, 2010), helps to build complementarities between contradictory logics. As per Smets et al. (2015), bridging skilfully imports aspects of one logic (e.g., devotional) into the enactment of another logic (e.g., private), at a time and through a form that appear consistent with the legitimacy needs of a prominent social organisation, such as the Buddhist monastery.

Concluding comments

This study appears significant in several ways, including the provision of an in-depth understanding of the impetus for early accounting and managing institutional complexity in a rather peculiar ancient setting.

Our findings provide an empirical contribution to the literature on accounting history by focusing on a context (ancient Ceylon) and a historical timeframe (first to sixteenth century AD) that is under-represented – despite the richness of primary sources in this region, such as an age-old Indian treatise of Arthasāstra (circa 300–184 BC) by Kautilya (Mattessich, 1998) on economic policy, statecraft and military strategy. This study further offers theory-based insights, enquiring what influenced early accounting thought and practices in Buddhist monasteries in ancient Ceylon. Prior research in this context is scarce and this study contributes to Liyanarachchi's (2009) examination of early accounting and auditing practices in ancient Ceylon, for accountability purposes of Buddhist monasteries and to the Liyanarachchi (2015) study of the role of Littleton's (1927) seven antecedents of double-entry bookkeeping in developing accounting in ancient Ceylon's Buddhist monasteries. Similarly to Kumarasinghe and Samkin's (2020) work, we have used lithic inscriptions as primary sources. Kumarasinghe and Samkin (2020) investigate how Ceylonese kings use stone inscriptions for impression management, by presenting a favourable depiction of government. While offering valuable insights, we believe these studies have not sufficiently delved into the motivations that inspire these practices, whereas this study does so through an institutional logics lens.

This study also incrementally contributes to the literature on multiple institutional logics by examining a non-Western faith-based organisation in a historical setting. Faith-based organisations are generally subjected to institutional complexity due to the interplay between several institutional logics (such as devotional, public and private logics). Despite a few exceptions (see for instance, Creed et al., 2010; Quattrone, 2009, 2015; Tracey, 2016), prior literature on multiple logics seems to have overlooked faith-based organisations (Lusiani et al., 2019) and non-Western religions in particular (Gümüsay, 2020; Tracey et al., 2014). While three forms of logics – devotional, public and private – have been identified here as previously done by Lusiani et al. (2019), we refer to a monastic organisational form, a non-Western system and an earlier historical timeframe than the study of Lusiani et al. (2019). This research exhibits how multiple institutional logics with conflicting demands may not only coexist (see Lusiani et al., 2019, 2023) but also mutually reinforce each other (see Smets et al., 2015), as opposed to competing. In turn, this influences everyday activities (and it is not regarded as a feature of major institutional change). The findings show the role of accounting in managing institutional pluralism, blending features of different logics to build complementarities between them. For instance, prohibiting monks to enjoy any surplus of income, when recording monastic income and expenditure, is an example of importing features of the devotional logic into the private logic.

Conceptually, this study highlights how coexisting logics inspired accounting practices in antiquity and how, over time, accounting aids Buddhist monasteries in managing their logics in everyday practices – a dynamic two-way relationship between accounting and logics as described. More precisely, this study argues that private, public and devotional logics, encapsulating wealth/relationships to funders (mostly kings), relationships to the community and abstinence from worldly desires, respectively influence the recording of incomes, expenditures and balances, and thereby the nature of accounting in Buddhist monasteries. The same accounts also allow for monks to provide accountability of their devotional logic to the community – that wealth is not spent by individual monks or on worldly goods. This safeguards their relationships with rulers and the public image of the Buddhist monastery. Meanwhile, private logic shapes important accounting tools to manage monastic wealth. The accounting appears to respond flexibly to multiple institutional logics, as argued by Lusiani et al. (2019, 2023). Furthermore, the study adds to the work of Lusiani et al. (2019) by emphasising a two-way relationship between accounting and logics (see Figure 1, right panel). The relationship between accounting and institutional logics is opposed to the unidirectional relationship highlighted by Lusiani et al. (2019). The findings highlight how early accounting thought is influenced by institutional logics and they demonstrate the role of accounting in managing such institutional complexity by becoming a bridging mechanism. Accounting in Buddhist monasteries temporarily combines logics to exploit complementarities between competing logics, enabling monasteries to maintain their hybridity. In so doing, accounting has helped to preserve legitimacy of Buddhist monasteries and it has assisted in their survival through generations.

The analysis conducted does carry some limitations. First, our conclusions should be considered as preliminary based on the specific evidence provided. Second the inscriptions analysed lack detail about the actual accounting practices or accounting records. We can only infer from the inscriptions what accounting records may have contained. Unfortunately, the ancient timeframe covered by the analysis typically implies a lack of physical records, as also remarked by prior literature (Liyanarachchi, 2009, 2015). Another limitation is that the inscriptions, by their nature, are summaries of key pronouncements. Thus, they do not provide extensive detail although we believe there is sufficient evidence to support the argument presented here. Finally, the analysis is based on transcriptions and translations of ancient languages. While these translations are done by eminent scholars and palaeographical experts, thus they are as accurate and reliable as possible, the process involves a translation of meanings across cultural, language and time aspects which is not possible to perform without inaccuracies. The translations are taken as they are, to limit issues of a-historicism in the interpretation of words in a contemporary sense.

In terms of future research, while there is a substantial body of accounting history on religious organisations, the field of institutional logics seems a useful but underused framing for such research. Religious organisations are hybrid by nature, for instance, they face a typical sacred–secular divide (see Laughlin, 1988). A sacred–secular divide by definition implies conflicting logics, which may suggest a change. Yet, religious organisations are remarkably stable over time. Thus, more research on religious organisations (or similar organisations) is to be encouraged.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Appendix 1.

List of inscriptions referenced (in chronological order).