Abstract

Set in the municipal archives of Braga, this article studies the accounting system and practices of the Monastery of Santa Ana, a female monastery located in a small town, Viana do Castelo, in the north of Portugal, during the eighteenth century. This work is a full-scale examination of the interlink between governance and accounting aspects of Benedictine organisations. It sheds light on the extent of management and administration that the female gender was able to exercise pertaining to a monastic order. The use of ‘displacement’ and ‘restraint’ concepts is pivotal to such exploration in the Monastery. The analysis of the accounting practices makes visible that large parts of its governance was embedded in social and internal accounting controls rather than the principal-agent type of relationship between the abbess, her auxiliaries and the monastery. Moreover, accounting practices help to appreciate the level of freedom of nuns that exceeded the actual freedom of a contemporary married woman.

Introduction

Monastic organisations can be credited with remarkable achievements in accounting (Ponzetti, 2014). The historiography of monastic accounting is largely indebted to Pietra (1586) and Flori (1677), a Benedictine and a Jesuit monk, respectively, for their treatises on monastic bookkeeping in 1586 and 1677. Earlier examples of rules of accounting and formularies date to the middle of thirteenth century (see Denholm-Young, 1937: 169–176; Hockey, 1975: 46–51). Despite this wealth of potential primary sources, Booth (1993), Cordery (2015), and Carmona and Ezzamel (2006: 117) note that the study of ‘the relationship between accounting and religion or religious institutions is remarkably sparse’. When referring to monastic establishments, Dobie (2008: 141) calls for ‘more detailed research at the micro-level on individual monastic houses to reconstruct and explain … their accounting and management techniques and processes’. Although Dobie (2015a: 144) indicates that detailed information based on ‘monastic accounting records has been used as the basis for many studies on a range of economic and social issues’, he points out that fewer studies focused their analysis of monastic systems on accounting and financial management. Some notable exceptions include the works of Schwartz (1982) on the incomes and expenses of Benedictine sugar mills of colonial Brazil in the seventeenth century; Prieto et al. (2006) on the sophisticated bookkeeping system used by the Benedictine monks of the Monastery of Silos (Spain) during the eighteenth century; Barnabè and Ruggiero’s (2004) study of the accounting books held in an Italian monastery since the eighteenth century; Bigoni et al. (2021) on the accounting representation of time and space in an Italian Benedictine priory; and of course Dobie himself (2008, 2015a, 2015b) on accounting, management and control of the Benedictine corporation at Durham cathedral priory. Dobie (2015a: 142) outlines that the traditional focus of accounting history research on monastic establishments is on the agency relationships and therefore the disciplinary account (i.e., external auditing) exercised by the general Chapter (or Congregation) and the Church to ensure the viability of the monastic houses and avoid any dilapidation or wasting of resources of the abbeys (or priories) by abbots and their auxiliaries.

The works of Charreaux (1997, 2008), Feldbauer-Durstmüller et al. (2019), Inauen et al. (2010a, 2010b, 2013), McGrath (2005), and Wirtz (2017) revisit the problem of agency and disciplinary accounts and argue that Benedictine governance is dominated by collegiality and participatory co-determination rather than principal-agent relationships.

These works imply the use of the concepts of ‘displacement’ (i.e., separation and autonomy of the monastic institution from other religious and social structures) and ‘restraint’ (e.g., specific rationalisation of internal tasks, practices, roles) to illustrate the functioning principles of Benedictine establishments.

In that sense, Wirtz (2017) adds that the role played by accounting remains largely unexplored. This is reinforced by Prieto et al. (2006: 223) who state, ‘there is still a lack of investigations into how accounting tracked the entire process of economic transactions within monasteries, as well as between monasteries and external parties.’

Prieto et al. (2006) and Landi (1999) also observe that most of the studies concerning monastic orders refer to male orders and their ability to administer with diligence the related patrimonies. The exploration of female convents might have the potential to contribute to a broader understanding of the ability of women to succeed in the same task. In this work, we suggest a re-interpretation of the theoretical concepts of ‘displacement’ and ‘restraint’ through the literature review of both accounting and novels, poetry, essays, and short stories genres (e.g., Camino, 2001a; Dolin, 1993; Hernández-Pecoraro, 1997; Lowe, 1990) to add a gender ‘flavor’ to the analysis of female Benedictine monasteries. In doing this, we expect to contribute to histories of accounting and religion (Abdul-Rahman and Goddard, 1998; Booth, 1993; Carmona and Ezzamel, 2006, 2009; Hernández-Esteve, 2005; Lewis, 2001).

First, this study aims at addressing the calls made by Carmona and Ezzamel (2006, 2009), Dobie (2015a) and Prieto et al. (2006) to explain the relationship between accounting and governance in monastic institutions. It examines the roles, governance mechanisms, accounting practices, and control systems of the female Monastery of Santa Ana of Viana do Castelo (hereafter referred to as ‘Monastery’), located in the north of Portugal, during the eighteenth and nineteenth centuries.

Second, it aims at adding a ‘gendered dimension of accounting in religious institutions’ (Carmona and Ezzamel, 2009: 520): available archival evidence of the Monastery permits the analysis of the representational function of accounting (see Quattrone, 2009) by reflecting or disregarding gender issues related to the governance of the Monastery of Santa Ana. In the eighteenth century the option of entering a convent was not necessarily a free choice for a woman (Bowden, 2011; Kuehn, 1994, 1996; Lowe, 1990): the illustration of nuns’ roles and boundaries of freedom within the Monastery will help to compare these nuns to their male (monks) or contemporary female counterparts (married women in family settings) as represented in secondary sources. Rapetti (2014) and Lavrin (1966) highlight that nuns and nunneries have become relevant to the shaping of the aristocracy since the thirteenth century, in the Roman Catholic Church. Chavarria (2009a, 2009b) outlines how the aristocratic origins of the nuns, the wealth (patrimonies) of their respective families, the monastery location, and the richness of the territory were relevant constituencies of several female monasteries between the sixteenth and eighteenth centuries. The Monastery of Santa Ana had significant properties, as happened with most of the religious institutions (Fernández et al., 2005; Ferreira, 2002; Marques, 1976, 1977; Maté et al., 2004, 2008; Prieto et al., 2006; Villaluenga, 2005). While we are not specifically interested in deepening the relationship between aristocracy and religion, these aristocratic origins of Santa Ana may contribute to a more comprehensive depiction of the gendered dimensions of ‘displacement’ and ‘restraint’.

The selection and analysis of the archival sources available at the Arquivo Distrital de Braga (ADB or Municipal Archives of Braga) is contextualised within the Portuguese socio-political environment in the period examined. Accordingly, this study adopts the view that accounting is a social practice that should be studied in the context in which it operates (Burchell et al., 2001; Gomes, 2008; Miller, 1994; Miller and O’Leary, 1987; Morgan and Willmott, 1993), and ‘as a phenomenon local in both space and time’ (Carnegie and Napier, 1996: 7).

The remainder of the article is structured as follows: the next two sections elucidate the theoretical underpinnings of the study, with reference to the concepts of ‘displacement’ and ‘restraint’. There is then a contextualisation of the Portuguese religious institution of Santa Ana, followed by an overview of the research method. The findings sections comprise the specific aspects of ‘displacement’ and ‘restraint’ as depicted through the governance mechanisms at the Monastery and its accounting and control practices. A thorough discussion of the evidence within the theoretical framework adopted prompts some main conclusions on the contributions of the work and streams of future research.

Benedictine governance system and agency problems: Displacement and restraint

Governance in religious institutions is any set of processes, customs, policies, laws and institutions affecting the way the organisation is directed and controlled (Inauen et al., 2013). Charreaux (1997) links the concept of governance to agency relationships and the way decisions of ‘senior executives’ (agents) of any organisation are influenced by financial controls and incentives identified by the owners or shareholders (principal) of that organisation. Wirtz (2017) refers to governance practices as ‘disciplinary accounts’ and sees them as management tools to mitigate ‘potential conflicts of interests’ (p. 260) either in a business or in a religious organisation.

From an organisational point of view, a Benedictine monastery can be interpreted in various ways (Hopwood and Miller, 1994). It is a religious organisation (Berry, 2005) accountable to the general Chapter and generally to a bishopric of reference. The general Chapter is a general assembly of monks, typically composed of representatives of monasteries of the Benedictine order. Baynes (1878), Chisholm (1911), and Fanning (1908) indicate that the name ‘Chapter’ derives from the habit of convening monks or canons for the reading of a chapter of the Bible or a heading of the order's rule. The expression ‘coming together for the chapter’ (convenire ad capitulum) is rooted on the sixth century St Benedict's Rule that monks begin their daily assemblies with such reading. That meaning was then transferred from the text to be read to the meeting itself and then the body gathering for it.

Displacement

A distinctive characteristic of a monastery with respect to other social, economic and religious institutions is its ‘displacement’. The organisational displacement is interpreted with respect to the corpus of the Church, from which it maintains a degree of independence, which materialises through the accountability relationship towards the general Chapter (Chisholm, 1911) and/or the bishopric: the main external audit bodies. In the study of monastic organisations, an agency framework is often used, for instance Bigoni et al. (2013) and Dobie (2015a) focus on the agency between either the diocese and the bishopric or the priory, the provincial and general Chapter and the bishopric, from a disciplinary perspective.

A comprehensive understanding of ‘displacement’ involves the examination of an agency framework as applied to monastic institutions. The conceptual framework of agency theory, which dominates corporate governance research (Filatotchev and Boyd, 2009) is based on the seminal article by Jensen and Meckling (1976), which defines the agency relationship as a contract under which one or more persons (the principal/s) engage another person (the agent) to perform some service on their behalf.

Corporate finance research has used this framework to study the relationship between a corporation's senior management and its shareholders and works like Hiebl and Feldbauer-Durstmüller (2014) refer to the agency framework to discuss the relationship between a Benedictine abbot and the cellarer by comparison with the roles of the chief executive officer (CEO) and the chief financial officer (CFO) of a corporation. Agency theory assumes that each agent rationally pursues thier own interests even at the detriment of the corporation, in a context of information asymmetry with respect to the principal. Consequently, agency theory suggests that a set of governance mechanisms, such as incentives and oversight practices (controls) are applied by the principal, to reduce information asymmetry and prevent agency conflicts. These mechanisms are alternatively referred to as disciplinary accounts by the literature on Benedictine establishments. While explicit incentives are banned by the Rule - they are a violation of the monastic vow of poverty and referred to as a ‘vice… to be utterly rooted out’ (McCann, 1969: 84–85) - oversight practices of external controllers are considered.

In Dobie's (2015a, 2015b) analysis, cases of misconducts, frauds, misappropriation and dilapidation of resources by abbots of a priory and their auxiliaries are prevented through oversight controls: these are the peculiar ‘displaced’ relationships that dominate the Benedictine order. This prevention occurred through the monitoring of general and provincial Chapters, the exercise of legislative power over all abbeys of a Congregation and the episcopal visitations. Accounting representations, in these cases, are used to convince the ‘controller’ (general Chapters and bishopric) about the effective and efficient use of resources, that the house is not living beyond its means and getting into debts.

At the individual level, the term ‘displaced’ refers to the vow of monks and nuns to enter ‘an entirely different world of strict religious discipline’ (Bowden, 2011: 484; see also Martin, 2018). By referring to the individual displacement in the female Benedictine order, Lavrin (2014: 95) outlines: when a woman took the black veil as a professed bride of Christ, the irrevocable nature of her vows signified more than a personal commitment. It was a way of life that was acceptable and desirable for those who followed it and for the society that nurtured the values it implied.

Lavrin (2014) considers that in the baroque period (1600–1750) women's convents were emblems of political and religious dominance (see also Berman, 2002) as well as of spirituality and gender values thanks to the meaning attributed to their ‘displacement’: sheltering consecrated women from the perils of a natural and social environment that could be hostile and threatening to the pursuits of a religion that demanded ascetic and contemplative practices and emphasised recogimiento (gathering with the self) and observance of well delineated rules of daily life. (p. 95)

Harz (2011: 1) defines the convent as ‘a physically and psychically safe place, a regenerative haven’. She describes the ‘displacement’ as the retreat into a stable and unified identity by locking out difference and projecting it onto the ‘other’.

Wirtz (2017: 267) adds that the vow of stability (stabilitas loci, Chapter 58 of the Rule, see St Benedict, 1981) means that the monk or the nun ‘never again leaves [exits] the monastery and premises’ without express permission. ‘Displacement’ may be a challenge to agency theory because the unit of analysis of the latter is the contract governing the relationship between the principal and the agent … given assumptions about people (e.g. self-interest, bounded rationality, risk aversion), organisations (e.g. goal conflict among members) and information (e.g. information is a commodity that can be purchased). (Eisenhardt, 1989: 58)

Since in a monastery the exiting option (i.e., terminating the underpinning contract or subscribing a new contract with a different organisation) will not be part of the range of mechanisms available to the monks/nuns once they take the vows (i.e., they are ‘displaced’), the only way they can influence the monastery governance is ‘by actively participating in deliberative bodies’ (Wirtz, 2017: 267). In these terms, ‘displacement’ drives the study of the rationalisation of roles within the monastery participatory governance. Inauen and Frey (2010) and Inauen et al. (2010a, 2010b, 2013), while recognising the presence of disciplinary accounts, explain that the Benedictine governance is mainly supported by collegial mechanisms, which are not typically recognised by agency theory. These mechanisms are embedded in the Rule of St Benedict (Regula Benedicti, see St Benedict, 1981).

The Rule of St Benedict represents, since 534 AD, the founding set of guidelines of the Benedictine orders, such as the female guidelines at the Monastery of Santa Ana. It contains precepts for organising monastic life, which demonstrate a broad knowledge of human nature, especially in terms of socialising practices (Fong and Tosi, 2007) and control over the inputs and processes due to the ‘displaced’ nature of monasteries. At the organisational level, this flexible system allows for strongly diverging monastic establishments with local, situational, and temporal adaptations. This is one of the essential secrets of success of the Benedictine organisations. It is also the reason why it is important to proceed with case studies which explore Benedictine establishment's governance and accounting practices (Eckert, 2000; Inauen et al., 2013; Jaspert, 2012; Power, 2010). On the other hand, the governance system continues to rely on similar basic principles, which apply indifferently to male and female convents, and make the Rule of St Benedict one of the most influential religious constitutions in Western Christendom. Following Rost et al. (2010), the Rule prescribes complementary participation processes in relation to the activity of any auxiliary monk or nun. Part of this governance concept is having a two-tier board structure, that is, there is a management board (the abbot and the officials) and a separate advisory board (internal Chapter), which is also a supervisory board consulting the management team. Its main task is to consult with the management and discuss contentious issues. The advisory board exclusively consists of insiders, that is, elected and nominated members of the monastery (Sacra, 1986). The reliance on these mechanisms of governance stands in sharp contrast to agency theory (Lorsch and MacIver, 1989; Mizruchi, 1983; Zahra and Pearce, 1989), where only outsiders are believed to be independent of the organisation management and thus able to prevent agency problems (Fleischer et al., 1988; Waldo, 1985). In summary, the ‘displacement’ concept refers to the analysis of both an organisational and individual dimension, which affect the monastery governance (i.e., rationalisation of roles and tasks) and its agency towards the general Chapter and archbishopric.

Restraint

The concept of ‘restraint’ also implies an individual as well as an organisational dimension. On the one side, it refers to the constraint or coercion of women within the specific hierarchy of a religious institution (Kooi, 2001; Voogt, 2000). Nonetheless, Sierra (2009) sees monastery as a lesser restraint than marriage, in the historical timeframe considered. By commenting on Cavendish (1668), he anticipates how a cloister of restraint has the potential to preserve a space of indulgence and privileges within a male-free community, in other words, a place of freedom (see Dash, 1996). Exercise of extravagance intended as luxurious living (Knowles, 2004), excess in food and drinks, possession of their own chambers, horses or attendants (Pantin, 1931) are also quoted by Dobie (2015a) as one of the reasons for stricter internal controls in Benedictine establishments since the later Middle Ages. Although these habits are prohibited by the Rule (McCann, 1969), Knowles (2004) and Rost et al. (2010) connect these privileges to the aristocratic lineage of most monks and nuns. On the other side, ‘restraint’ has managerial implications, which are embedded in the Rule and translated into a rationalisation of accounting.

Although Kieser (1987) claims that the economic success of Benedictine establishments could be a source of temptation and expose abbots to significant risk of conflict of interest, Wirtz (2017) reminds us that the Benedictine monasteries’ organisation is characterised by the rationalisation of accounting and management practices. Dobie (2015a) offers a categorisation of four broad areas of ‘restraint’ varying from personal skills, abilities and business knowledge to regulation of a variety of contracts and finally several detailed measures for accounts preparation and financial management. He discusses that, in addition to obedience, the administration of the monastic establishment works based on delegation of areas of operation, which means a precise allocation of assets, streams of income or costs (see also Heale, 2009 on the high level of female managerial involvement in fifteenth century monastic affairs). As a result, auxiliaries need ‘adequate knowledge of finance and accounting…to ensure that the abbey can look forward to a future lifetime that equals the abbey's past lifetime’ (Hiebl and Feldbauer-Durstmüller, 2014: 53). These skills and capabilities are ‘usually both strongly intertwined with the secular system (as the financial manager of the abbey) as well as the sacred system (often by being a monk of the abbey)’ (Hiebl and Feldbauer-Durstmüller, 2014: 52). Bowden (2011: 488) notes that ‘the accounts also contain evidence of significant managerial skills by senior members of some convents who kept the accounts and annotated the arrangements being made’. Makowski (2012: 28), who examines the relationship between nuns and their lawyers in the later Middle Ages, concludes that ‘cloistered women were able to successfully conduct the day-to-day administration of their affairs’.

Detailed bookkeeping preempts internal controls as well as the openness and consent of the monastic house to establish a set of checks and balances (Dobie, 2015a: 149) based on the size of transactions, restrictions to powers upon offices and ability to stipulate contracts with external parties. The prescription of ‘faithful account of their receipts and expenses’ (Dobie, 2015a: 151) implies that accounting attests the stewardship of auxiliaries and allows the identification of those who are generating a surplus or running a deficit.

In summary, the ‘restraint’ concept refers to both organisational and individual dimensions, which affect the way in which personal privileges are accounted for and balanced within a detailed system of internal controls as well as the accounting knowledge and capabilities emerging from it.

In the case of the Monastery of Santa Ana, we address the following research questions: how is the governance of the Monastery connected with its accounting practices? More specifically, how do ‘displacement’ and ‘restraint’ emerge from the governance and accounting practices of the Monastery?

Displacement and restraint of gender

Following the previous section, the concepts of ‘displacement’ and ‘restraint’ are largely explored by non-accounting history frameworks such as English studies and liberal arts. In this section, the relationship between accounting studies and gender, in both secular and monastic lives are explored.

Despite the progresses of the Enlightenment, across the eighteenth and nineteenth century, Hunt (1992) recalls the inferiority and subordination related to the treatment of women, in both scientific studies and private lives. It was a common habit, accepted by law, that ‘daughters, sisters, wives and widows were legally and socially subject to their male relatives, in varying degrees’ (Lowe, 1990: 209; see also Kuehn, 1994, 1996). As a result, Walker (1998) identifies the accounting ‘restraint’ of female consumption in any British household, which also served to contain women in domestic roles. Dolin (1993: 22) highlights that, the home was seen as a passive and not an active realm, and property, when associated with women, though it was … declined in status… the woman was often perceived … to be merely passive medium through which the active line of property had to pass.

Dolin (1993: 25) also outlines that women during the eighteenth century were installed in the domestic idea and in narrative fictions and images ‘to represent property's visible status, its status not as a right but as a thing’.

Camino (2001a), in her linguistic analysis of Azevedo's El muerto disimulado (Portugal, 1621–1644) recalls situations common to contemporary women in the eighteenth century such as being denied to access money or property unless the men of the family were dead or otherwise absent. Writing, travelling, taking revenge or administering properties were among restricted areas for women (see also Camino, 2001b). Even in dramas, houses were considered the domain for the feminine and of the domestic, whereas the streets and the open public spaces were the realm of adventure that is associated with the masculine (Kark, 2012). Hernández-Pecoraro (1997) recalls the recurrence of the same issue in Cervantes's Don Quixote, where the female object is always constructed by a male subject who is unable or unwilling to recognise one cohesive female subjectivity.

There is however an exception of this ‘restraint’ and inability to exercise any agency, which is represented by the physical ‘displacement’ of women in convents (Camino and Krulfeld, 2005; Glenn, 2017; Hernández-Pecoraro, 1997; Howe, 2016; Kark, 2012; Labanyi, 2015; O’Brien, 2008, 2010). Lowe (1990) posits that religious life offered opportunities for the exercise of power by women, such as self-government and patronage from the most important political families, not available to those of the female gender who stayed within the structure of the family and who were, therefore, ‘restrained’ by men at every stage.

O’Brien (2008) analyses the appeal of Zaya's Spanish novellas in the sixteenth century, pointing out that the heroines’ only route to physical safety and fulfilment is via the convent. By recalling the work of Russ (2015), Howe (2016) establishes a further aspect of women's ‘restraint’ in the lack of access to education. This derives from a Renaissance notion that women's speech, whether oral or written, places them in the public sphere where men's gaze upon them threatens their sexual purity. Nevertheless, this denial has not stopped notable nuns and female saints such as Sister Teresa de Cartagena, whose education was the primary means of elevating themselves from the canon of centuries. The works of Bowden (2011), Martin (2018) and Dolin (1993) outline that although enclosed life might theoretically cut the nuns off from the outside world, it actually supports a positive ‘restraint’: to sustain the convents’ foundations in the long term, senior nuns had to take an active role in the management of the properties. Bowden (2011: 488) argues that ‘in many cases they relied on the advice and the contacts of their confessors or external agents, but the accounts also contain evidence of significant managerial skills’. Bowden (2011) also suggests that despite the guarded and limited access points between the religious and the secular worlds, any negotiation across them and the actual shape of these two worlds’ relationship received fundamental inputs by the nuns. Since texts were essential to the secular and religious life for their effective performance, it was expected that nuns would have a working knowledge of Latin and accounting practices.

The role of women in Benedictine monasteries was also functional to the dynamics of the Rule (see Galbraith and Galbraith, 2004; Gervais and Watson, 2014), making no difference between male or female organisations. Clark (2003) adds that Benedictine nuns were also nourished by the rich liturgical experience of monastic life and were exposed to educational opportunities not available to most lay women.

This was one of the reasons for which the choice of ‘displacement’ for an enclosed order (i.e., the Benedictine one) represents a strategic means to be part of a recognised hierarchical body, with a formally recognised authority, the abbess, who took over normally male activities, such as fund raising. Strasser (2004) outlines that religious women, and even cloistered nuns, far from being extraneous or obstructionist, contributed to the modernising processes of communities and states and she documents their political importance and constitutive role.

Our study of accounting and governance in the Monastery of Santa Ana, will consider if and how gender played a role in the governance (see also McMillin, 1992), and how ‘restraint’ and ‘displacement’ were represented in the accounting control system.

Background: The Monastery of Santa Ana de Viana do Castelo

In Portugal, nobles and wealthy people founded many feminine monasteries, starting in the sixteenth century, to prevent dispersion of the family wealth, once the principle of primogeniture 1 was applied. Single daughters who could not access the family patrimony (Dias, 2007: 396), or who were denied unprofitable marriages, were forced to take on the monastic vows (Marques, 1976, 1977; Rocha, 1996, 1999; Serrão, 1980). In Portugal, in the sixteenth century, the majority of the abbesses came from the nobility (Marques, 1977). The Monastery of Santa Ana was built in the beginning of the sixteenth century (Araújo and Silva, 1985) by the municipality and the nobility of Viana da Foz do Lima, today Viana do Castelo (Guerra, 1895) to house the unmarried maidens of the distinguished families of the county (Fernandes, 1979; Marques, 1976; see Figure 1). The religious women always kept the name of their family of origin and were addressed to as Madre (Mother) or Dona (Lady), which is related to their degree in the lineage (see Andrade, 1996). Accordingly, the nuns brought to the Monastery the status and stratification they had outside, which was reflected in the hierarchical position and role they assumed in the administration of the Monastery and in the privileges and interests they enjoyed.

Monastery of Santa Ana: location and design. Source: Arquivo Municipal de Ponte de Lima (Municipal Archive of Ponte de Lima) – ‘Os mosteiros beneditinos femininos de Viana do Castelo: arquitectura dos séculos XVI ao XIX’.

Until the beginning of the seventeenth century, the Monastery had five perpetual abbesses, the daughters of the founders of the Monastery, who possessed a high status in the society and supported financially the Monastery with dowries, properties and money (Guerra, 1895; see also ADB, Maço de pergaminhos, Cota 265).

Throughout its existence, the Monastery always had a large community, reaching a maximum of 300 women in the eighteenth century, despite the high level of wealth required to join it, and the restrictions imposed regarding the lineage of the nuns. Both these requirements added to the good reputation that it had in safeguarding the good customs of the time (see Guerra, 1895; Rocha, 1999).

At the end of the seventeenth century and during the first half of the eighteenth century, a time when the Monastery had more religious members (Fernandes, 1979), it underwent expansion works in the dormitories and restoration and enlargement work in the church (see ADB, Despesa da Obra dos Dormitórios e do Mirante, Cota 140; Fernandes, 1979, 1999; Rocha, 1999). The restorations performed on the Church evidenced the good taste and the lineage of the religious women in the Monastery (see Rocha, 1999).

However, the second half of the eighteenth century was marked by a governmental attack on the religious orders, which culminated in the nineteenth century with the interdiction of admittance of new male and female elements to the religious orders, followed by the extinction of masculine orders in 1834 (Afonso, 1972; Serrão, 1996). The extinction of this Monastery occurred in 1895, the year when its last religious element died. The building and part of the fence (cultivated land properties) were handed over to the Congregação de Nossa Senhora da Caridade (Congregation of Our Lady of Charity; Fernandes, 1999), to which they still belong today. The remaining properties were placed in a public auction in 1896 (see ADB, Fazenda Nacional - Venda dos Bens Compreendidos nas Disposições das Leis de Desamortização, Cota B, FN 289).

Research method

The analysis of the Monastery of Santa Ana de Viana do Castelo is conducted on the archival materials stored in the municipal archives of Braga, with specific attention to the organisational and accounting documents of the Monastery. These sources were complemented with secondary sources (mainly in Portuguese) on the monastic life in Portugal. The period considered is the eighteenth century, corresponding to the maximum expansion of the monastic community, when they still benefited from the protection of the King and, after, of the Queen of Portugal.

The analysis of ‘displacement’ seeks to identify both the individual conditions of women who became nuns at Santa Ana and to provide a reconstruction of roles that characterised the collegial governance of the Monastery. In the first instance, some of the archival documents considered are dated from the sixteenth and seventeenth century: they relate to the amount and disposal of the assets accumulated throughout the years and the disciplinary rules of its first settlement. As the Monastery was a Benedictine one, the governance and religious set of regulations was represented by the Rule of St Benedict (480–550 AD), as locally applied.

Our effort is to visually reenact the organisational chart of the Monastery in the eighteenth century, the positions and roles of the nuns and their reciprocal relationships over specific accounting or religious matters, thus highlighting the governance mechanisms of the Monastery (see Rowlinson et al., 2014) and discuss them in relation to agency theory assumptions. With respect to the works of Dobie (2015a) and Bigoni et al. (2013), less emphasis is dedicated to the accountability relationship between the Monastery and the bishopric (external auditing body): we should emphasise that some books are missing, such as the constitutional documents and the Livro das Visitações (book of visitations). It was possible to collect information from the recordings made in other books, such as the book Assentos Vários da Madre Escrivã; Defuntas e Profissões, Treslado da Provisão do Arcebispo de Braga para o Regímen da Fazenda (ADB, Cota 255). As suggested by the title, this book translated the book of visitations and the regime of the finances into practical guidelines for the correct bookkeeping.

The analysis of ‘restraint’ at Santa Ana focuses on accounting practices, the internal control system, and the type of skills and abilities implied by the detailed financial and management operations. In what concerns the administration and accounting system of the Monastery, this was determined by the Regímen da Fazenda (regime of the finances), emanated by the archbishop of Braga, in 1621.

The access to the primary sources allowed a systematic scrutiny of the most relevant accounting and non-accounting books and how they were related together in a precise system of recording. Our representation of the accounting processes considers both the financial and material (exchange of goods) aspects of the transactions. These accounting processes shed light on peculiar aspects of the Monastery governance (i.e., ‘restraint’ as rationalisation of practices, tasks and roles) and its internal controls (see also Dobie, 2015b; Prieto et al., 2006). Details regarding the diet of the nuns, and the personal expenses in occasion of relevant celebrations also emerge from the analysis. They help to identify those privileges emerging from the accounting records that fulfil the individual dimension of ‘restraint’.

Displacement at Santa Ana: Dominance, governance and external audit

In this section, fundamental aspects of ‘displacement’ (gender, individual and managerial) are articulated as they functioned at Santa Ana.

Dominance: The status of displaced women and their proprietas

The accounting and administrative books show that the Monastery had several properties obtained by private 2 and familiar donations, such as the relatives of the five perpetual abbesses, as well as land inherited by the religious women and money (ADB, Livro de Arrendamento, Cota 261, fls 63; ADB, Livro da Madre Escrivã, Cota 135; ADB, Livro do Tombo, Cotas 2–6).

These possessions and money were directly and indirectly exploited by the Monastery (ADB, Livro de Arrendamento, Cotas 260–262), but under the supervision of the religious women. The administrative and accounting books of the Monastery confirm that religious ‘displacement’ meant religious women having direct or indirect access to and control over money or properties (Connor, 2004; Kirkham and Loft, 2001; Laurence et al., 2008; Virtanen, 2009; Walker, 2006).

This was the case of the three first perpetual abbesses. Their status and influence in the life of the Monastery can be ascertained by their role in obtaining authorisation to annex other monasteries, such as the Monastery of Valboa and Loivo. For this, Abbess D. Margarida and her sister D. Isabel went to Lisbon to speak with the King who complied with their request (ADB, Maço de pergaminhos, séculos XII-XVII, Cota 265). As a result, the archbishop of Braga consented to the annexation of the monasteries but imposed as a condition that the Rule of St Benedict should be followed and the Monastery should be under his jurisdiction, and not the municipality (Guerra, 1895; Costa, 2007).

One of the brothers of the three first perpetual abbesses donated a farm with a rent of over 200 bushels of wheat when he placed a daughter in the Monastery (Guerra, 1895: 138). Another brother, who was Mayor of Bragança, donated all his assets to them upon his death, after having paid for the construction of the dormitory and the execution of the altarpiece of the main altar, and established a chapel with an allowance of 16,750 réis per year. From the archival sources, it is also possible to verify that the founder of the Monastery and father of the last two perpetual abbesses donated his assets to the Monastery, including a significant portion of land (ADB, Maço de pergaminhos, séc. XII-XVII, Cota 265). Also, the third perpetual abbess contributed a dowry, composed of money and lands, to two orphaned daughters of an old servant to be accepted in the Monastery (ADB, Maço de Partes de Livros Desmembrados, Mapa e Lembranças dos Cadernos de Visitação, Cota 263).

The dowries were of consistent amount, and they increased over time (see, e.g., ADB, Livros de Receita e Despesa, Cota 59, fls 32), in order to select the new admissions of religious women (Afonso, 1972; Andrade, 1996; Dias, 2007). At the beginning of the eighteenth century, the values ranged from 800.000 to 1.000.000 réis, but in some cases the values reached 1.200.000 réis and in one case 1.600.000 réis (ADB, Livros de Receita e Despesa, Cota 47, fls 47, Cota 55, p. 76, Cota 59, fls 32, Cota 62, fls 58). Attesting the good reputation of the Monastery was the fact that in the eighteenth century, King John V became protector of the Monastery, having financed some of the works carried out in it (Rocha, 1999). This King had a great deal of influence over the Monastery, as shown by his recommendation, in 1730, of welcoming secular women to the Monastery, accompanied by their maids (ADB, Índex do Cabido, 6.° Vol., fls 107 e 108).

The examples provided outline elements of individual ‘displacement’, related to proprietas and dowries, which are a controversial matter in Benedictine establishments (Dobie, 2015a; McCann, 1969). In the case of Santa Ana they explain the link between aristocracy and monastic order. With respect to Harz (2011), this link justifies a multiplicity of identities (Benedictine nuns and representatives of the aristocracy) which are conveyed through the choice of the monastery. Proprietas and dowries are also an expression of an acquired freedom of its members which is acceptable and desirable as emblem of dominance (Lavrin, 2014).

Despite the enclosed nature of the Monastery, the nuns had attorneys, who acted on their behalf regarding the properties and businesses they had outside the Monastery (ADB, Livro de Arrendamentos, Cota 261; ADB, Livro da Despesa, Cotas 95, 103 and 112).

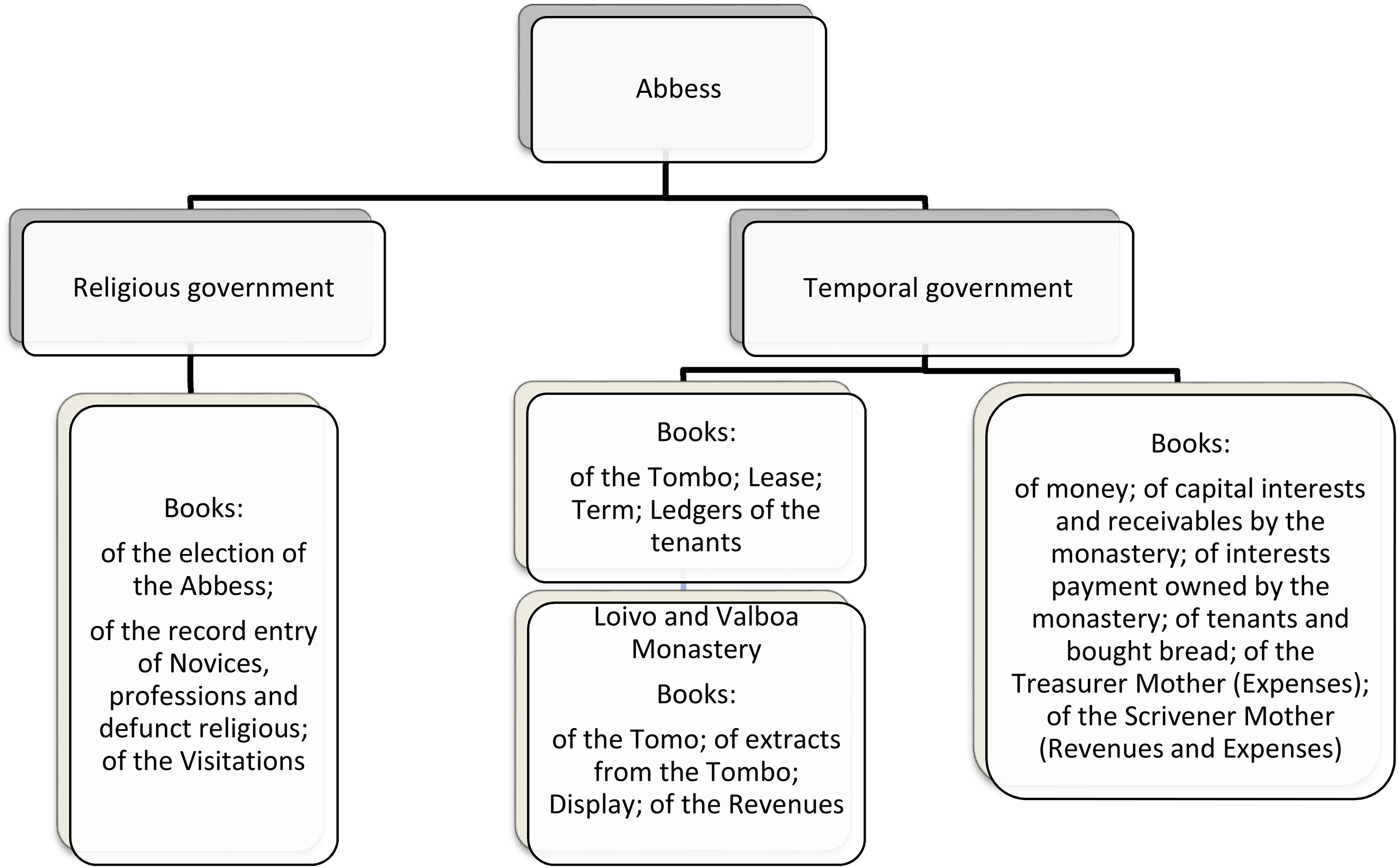

Collegial and participatory governance at Santa Ana

The administrative organisation of the Monastery (see Figure 2) followed the Rule of St Benedict 3 and is recalled in the regime of the finances (see ADB, Maço de Partes de Livros Desmembrados, Mapa e Lembranças dos Cadernos de Visitação, Cota 263): it is a vertical administration, which is quite common in Benedictine monasteries (male and female), where the maximum authority was concentrated in its main figure, the abbess, but with several levels of participation rights by the nuns (Costa, 2007). The abbess ruled the Monastery, both religiously and temporally, with the assistance of several official mothers (auxiliaries). Figure 2 is a reconstruction of governance roles and functions from the primary sources analysed.

Administrative organisation of the Monastery.

The abbess oversaw imposing discipline, assuming and signing all economical actions and contracts on behalf of the Monastery. Her role, within the ‘displaced’ environment of the Monastery, does not seem to differ from that of the abbot in Spain (Prieto et al., 2006), England (Dobie, 2015a, 2015b), Italy (Bigoni et al., 2021), Brazil (Schwartz, 1982). The primary sources evidence that in the first half of the eighteenth century, the revenues did not cover all the expenses, nonetheless the Monastery underwent major works (ADB, Livro da Receita e da Despesa, Cota 51, pp. 79 and 109, see Figure 3). These transactions needed to be signed by the abbess, demonstrating how the managerial power of the abbess was indifferent to the female gender. In addition, they show how becoming member of a monastery as abbess removed restrictions for women (Camino, 2001b) such as writing and administering properties, in contrast with domestic life (Dolin, 1993; Walker, 1998).

Book of Revenues and Expenses 1795–1801 (ADB, Livro da Receita e Despesa, Cota 67, fls. 2).

The names of the religious women were written in the first page of the main book of the accounting system. For the period 1795–1801, the name of the abbess, the Escrivã (scrivener mother) and the Tesoureira (treasurer mother) (see Figure 3) appear together, indicating their level of relevance in the administration and control of the Monastery. These were not household transactions (see sub-section on accounting practices e.gs of household transactions), but relevant asset investments and loan policy decisions exercised at a collective level and without any form of male monitoring, thereby supporting Lowe’s (1990) argument on the self-government allowances to nuns in a society where the idea of women who make their own decisions was irksome, worrying and simply unacceptable. It is also self-evident that despite the fact that the Monastery made every religious person invisible to outsiders and separated from the secular world, there were points of contact and negotiations between the religious and the secular worlds that involved the abbess.

From the seventeenth century, the abbesses began being triennially elected (Araújo and Silva, 1985), according to what was established by the Council of Trento (Dias, 2007); some of them being re-elected several times (Guerra, 1895; see also ADB, Eleições das Abadessas, Cota 252).

The election was made in the presence of the representative of the archbishop of Braga. A priest-scribe was appointed and all ‘professed nuns who, according to the Rule, have a vote, and normally voted in similar elections’ were called (ADB, Eleição das Abadessas, Cota 252, fls 1). On election day, mass was said, and after all the outside personnel had left, the church was closed, and the archbishop's representative declared to the nuns the reason for his presence. He also recommended that they elect as abbess, that nun who in their consciences judged most worthy for the office, without dying of passion, affection or hatred for anyone, and that they only pay attention to what is best and most convenient for the good of the convent (ADB, Eleição das Abadessas, Cota 252, fls 1).

With respect to agency theory, this finding confirms the collegial nature of the top administration of Santa Ana (see also Inauen and Frey, 2010; Rost et al., 2010), which was not only voted, but also chosen based on merit and business acumen for the future of the Monastery. Like in male Benedictine monasteries (see Prieto et al., 2006), the abbess could count on the advice of Capítulo (internal Chapter), which was a consultation organ or advisory board. The internal Chapter comprised the mothers of the order and the religious deputy, to whom the abbess resorted for the resolution of matters of high responsibility for the Monastery, such as the election of new abbesses, the acceptance of novices, the periodical visitations and on the religious matters (ADB, Maço de Partes de Livros Desmembrados, Livro das Visitações, Cota 263; ADB, Livro da Receita e Despesa, Cota 48; see also Costa, 2007). On the economic matters the internal Chapter was consulted for the assignment of attorneys, the buying and selling of lands and properties, and the monitoring of the main revenues and expenses of the Monastery (ADB, Maço de pergaminhos, séc. XII-XVII, Cota 265).

The abbess had as auxiliaries of the religious and temporal government several nuns, each playing a different role in the hierarchical administration of the Monastery (see Figure 2). The prioress mother helped her with the ruling of the Monastery and replaced her in case of sickness or any other impediment and the sub-prioress mother, who assisted both (ADB, Livro da Madre Escrivã, Cota 136, fls 1). There was also the Madre das Confissões (confession mother), the Madre Sacristã (sacristan mother), the Madres Gradeiras (eavesdropping mothers) and the singing mothers, who took care of everything necessary to the spiritual and liturgical activities of the Monastery (ADB, Livro da Despesa, Cota 112; ADB, Livros de Receita e Despesa, Cota 48, fls 17). As auxiliaries of the temporal government the abbess could count on the scrivener mother, in charge of the records of all the actions of the monastery and several accounting books, the fiduciary mother, who managed the money which came in and out of the Arca do Depósito (ark of the deposit), and the treasurer mother, who was in charge of the expenses of the Monastery. There were also two Madres Celeireiras (garner mothers), who were responsible for the goods that came in and out of the barn (wheat, rye, corn and flour), two Madres Provisoras (provisory mothers), who took care of the food for the community, the Madre Enfermeira (nurse mother), who looked after religious patients, the Madre Rodeira (attending mother), who took care of all the matters of the entrance of the Monastery, and the Madre Campeira (field mother), who oriented the works of cultivation of the various products of the fence (cultivated land properties). 4

This partition of roles within the female monastic community of Santa Ana is very similar to the one depicted by Inauen and Frey (2010) and aligned with the Benedictine pillars of collegial governance and participation (co-determination). As the abbess was elected as well as the deputies’ mothers in the internal Chapter, the whole monastic community was held responsible for decision making in important business affairs (ADB, Eleição das Abadessas, Cota 252, fls 1). At the same time, there was a two-tier board structure, specialised at its core: the internal Chapter, conceived as an advisory board (consultation role), and the auxiliary board where both religious and temporal matters were delegated to specialised managerial figures (nuns).

There were only two roles played by men in the Monastery of Santa Ana: the manager father, who took care of the shopping for the Monastery, the administration and lease of the lands, the collection of rents, the payment of services, on the behalf of the Monastery because of its enclosed nature (see ADB, Livro de Arrendamentos, Cota 261; ADB, Tombo 1715–18, Vol. I, Cota 2, p. 8), and the chaplain father, who was responsible for the liturgical activities (ADB, Livro de Arrendamentos, Cota 261, fls 1). The Monastery also had several secular attorneys to handle its affairs in places far from it: one in Braga and another in Lisbon (see ADB, Livro da Madre Tesoureira, Cota 40, fl. 20). While a principal-agent relationship was possible between the Monastery and its secular attorneys as depicted by Hiebl and Feldbauer-Durstmüller (2014), our findings confirm that most of the governance mechanisms at Santa Ana, although hierarchically defined, were based on a reciprocal trust, joint-participation/sharing of the main managerial and administrative activities, and internal social control before oversight practices of external controllers (Bigoni et al., 2013; Dobie, 2015a). The limited role of men in the Monastery business confirms the unparalleled access to power and money by females (Lowe, 1990) once ‘displaced’ to the Monastery. The gender-neutral principles of democracy inspired by the Rule of St Benedict awarded the abbess similar (if not higher) influence and power than the one depicted by Dobie (2015b) for the abbot of a priory.

External auditing

As for the external control, based on principal-agent relationship (visitations, see also Dobie, 2015a), it was performed by the archbishopric (see ADB, Livro de Receita e Despesa, Cotas 46–90) every three years. After the accounts were verified and signed by the abbess, the scrivener and the treasurer mothers, the book of revenues and expenses was sent to the archbishop, who analysed the records or had them analysed. Compliance of the records towards the regime of the finances (ADB, Assentos vários…, Treslado da provisão…para o regimento da fazenda, fls 4, Cap. 11, Cota 255) was awarded with final approval, which discharged the accountability of the Monastery. Any remarks, such as mistakes, which needed to be corrected, or requests of details on specific records (ADB, Livro de Receita e Despesa, Cotas 65, 68 and 81; ADB, Maços Desmembrados, 17th to 19th centuries, Cota 264) were to be made through the book of revenues and expenses. For the triennium 1710–1713, corrections were demanded to the accounts, which were approved in 1715 when the archbishop visited the Monastery, as follows: Viewed and approved in the form of an account made by Father Frutuoso da Costa and with the statements mentioned therein, the necessary ordinances were sent to make the accounts for the past three years in the form that we have ordered. Viana Feb. 26, 1715 (ADB, Maços Desmembrados, 17th to 19th centuries, Cota 264).

But there were also compliments on the good management at Santa Ana sent by the archbishop. For instance, in the three-year period of 1750–1753, the archbishop praised the abbess for her governance of the Monastery: We approve the accounts and praise the care and zeal with which the Abbess sought to fulfill her obligation, applying a large part of the income and alms for the performance of the Community leaving this good example to its successors. Braga May 18, 1754. (ADB, Livro de Receita e Despesa, Cota 55, fl. 83).

The visitations by the archbishop are at the centre of principal-agent studies within monastic establishments (Dobie, 2015a, 2015b; Wirtz, 2017). The visitations challenged the conduct and capability of the abbess and her auxiliaries, in the same way as for male monasteries. Again, the satisfactory financial records and internal controls would have been a major element in a successful rebuttal of charges of mismanagement, misuse of resources or misappropriation (Bigoni et al., 2013; Dobie, 2008).

Restraint at Santa Ana: Detailed accounting practices and internal control systems

The ‘restraint’ concept has several implications at Santa Ana: at the individual level, ‘restraint’ implied that nuns were only allowed once every two weeks to have contact, on the grid, with outside representatives or relatives when accompanied by Madres Gradeiras (eavesdropping mothers) (ADB, Maço de partes de livros desmembrados, Mapas de Lembranças…, Cota 263). Nevertheless, they were able to benefit from some privileges within the Monastery. In this section, ‘restraint’ also refers to the specific boundaries within which the transactions were approved and recorded, and internal controls were developed.

Restraint in the detailed accounting practices

As anticipated in the former sections, accounting rules of the Monastery in the eighteenth century were contained in the Regímen da Fazenda (regime of the finances), issued by the archbishop of Braga, in 1621. The regime of the finances comprised instructions for the accounting of revenues and expenses of the Monastery, the processing of the related incomes and payments, the specific books to be used according to the type of transactions, who oversaw the individual record bookkeeping in the various books and who would sign them.

Some specific guidelines for the Monastery derived from the Livro das Visitações (book of visitations) 5 and the book of revenues and expenses at the time of approval of the accounts. 6

Any transactions of the Monastery were registered in books (Figures 4 and 5) and most of them were dealt with through public deed. Detailed bookkeeping spanned from the dowry of the novices to lease contracts, admittance of new servants, loans, and interests on loans among others. Nothing was left unmentioned, to protect the Monastery proprietas, so the Monastery would have been able to retrieve its assets at any time (see ADB, Tombo, Cotas 2–6; ADB, Assentos vários da Madre Escrivã…, Cota 255).

Books of the administrative organisation of the Monastery. Note: Loivo and Valboa Monastery were under the jurisdiction of this Monastery.

Economic management of the Monastery.

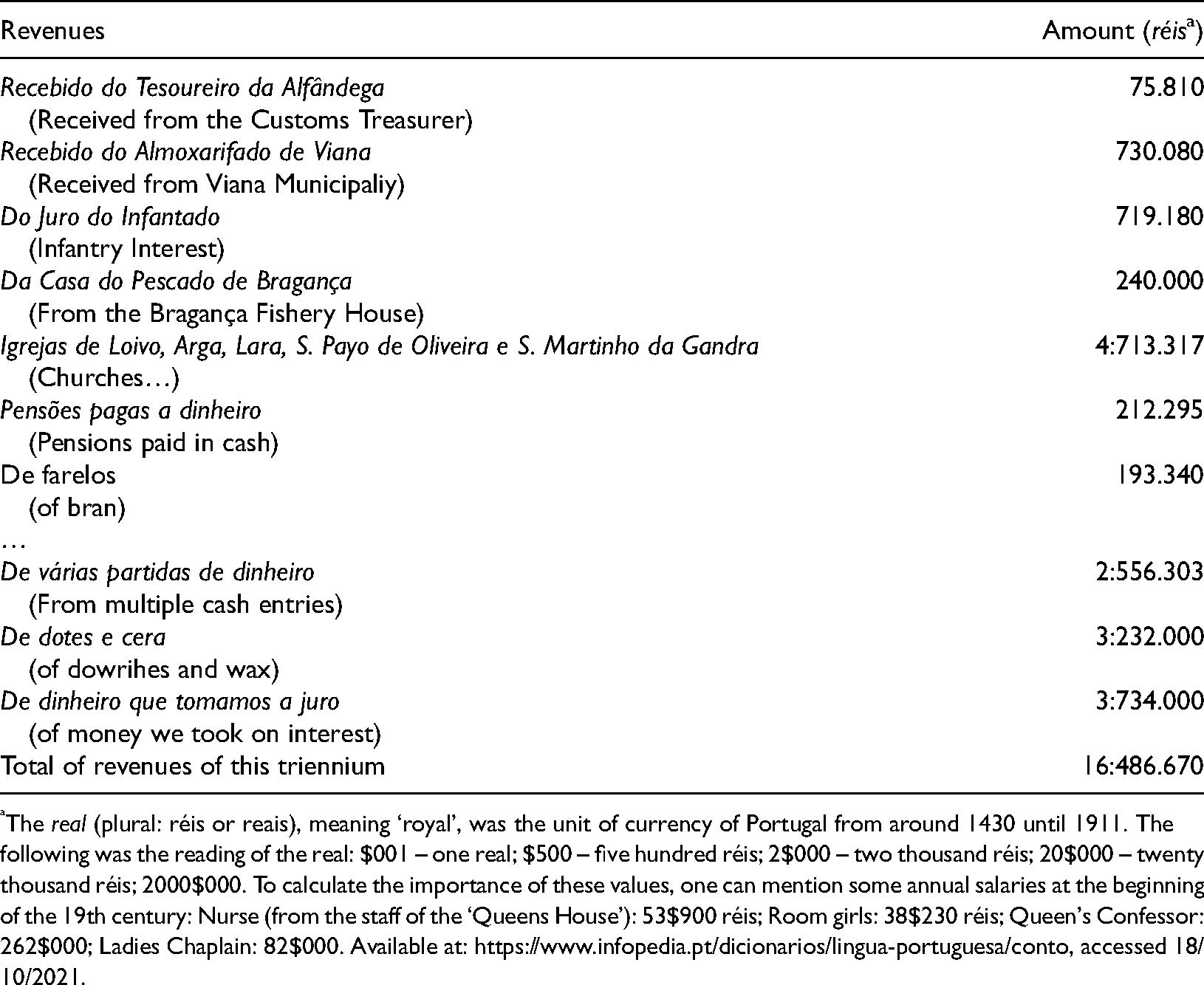

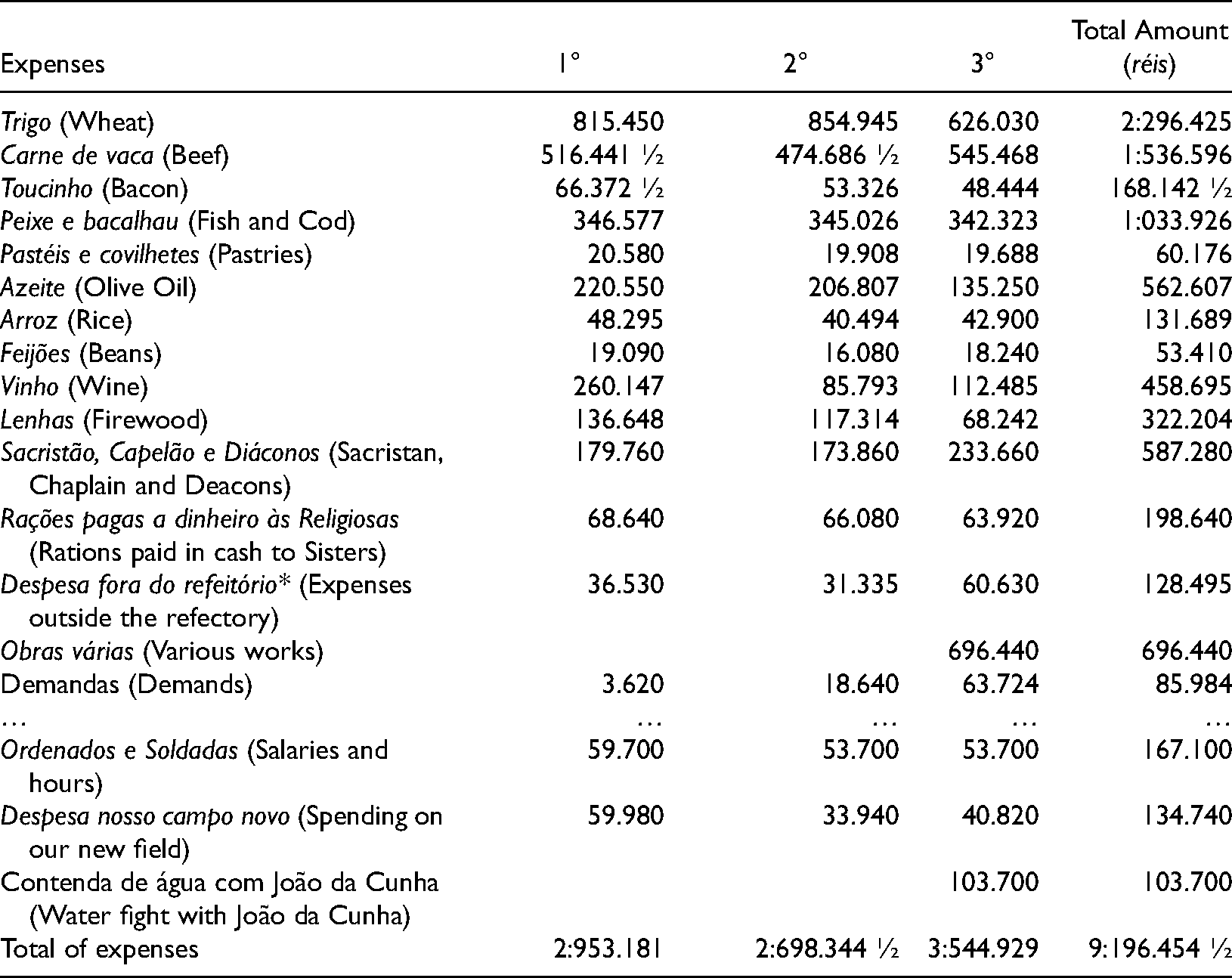

From the triennial auditing of the period 1747–1750, it is possible to have a clearer idea of the revenues and expenses of the Monastery (see Tables 1 and 2), and of the most relevant items in the total of revenues, such as the interest income, church income and dowries (see also ADB, Livros de Receita e Despesa, Cota 48, fls 41 and 79, Cota 68; ADB, Livro da Madre Escrivã, Cota 136, fls 60). The transactions were recorded by the nuns. According to the type of transaction involved, specific responsibilities of the mothers in charge emerged. All the expenses were registered, even the small ones, such as stamps (see ADB, Livro de Receita e Despesa, Cotas 48, 57 and 90). The recording of expenses was the responsibility of the treasurer mother, to whom the money was delivered for the purchases, either by the abbess, the scrivener mother or by the fiduciary mother, while the manager father made most of the purchases. When the money was given to the treasurer mother, two entries were made, one for the delivery of the money and the other for the acknowledgment of receipt of it, as in the example: Demos a bolceira pª gastos a dezoito de Julho quarẽta mil rs. [We gave the treasurer for expenses on the eighteenth of July forty thousand réis].

Summary of the revenues for the period 1747–1750 (ADB, Livro de Receita e Despesa, Cota 54).

The real (plural: réis or reais), meaning ‘royal’, was the unit of currency of Portugal from around 1430 until 1911. The following was the reading of the real: $001 – one real; $500 – five hundred réis; 2$000 – two thousand réis; 20$000 – twenty thousand réis; 2000$000. To calculate the importance of these values, one can mention some annual salaries at the beginning of the 19th century: Nurse (from the staff of the ‘Queens House’): 53$900 réis; Room girls: 38$230 réis; Queen's Confessor: 262$000; Ladies Chaplain: 82$000. Available at: https://www.infopedia.pt/dicionarios/lingua-portuguesa/conto, accessed 18/10/2021.

Summary of the expenses for the period 1747–1750 (ADB, Livro de Receita e Despesa, Cota 54).

Recebi dia asima quarẽta mil rs [I received the day above forty thousand réis] (ADB, Livros de Receita e Despesa, Cota 46A, fls 2–7).

Payments to the Monastery's creditors, as long as they were over a thousand réis, were to be made from the Ark of the Deposit, with a document made by the manager father and signed by the abbess, scrivener and fiduciary mothers (ADB, Assentos vários…, Treslado da provisão…para o regimento da fazenda, fls 4, Cap. 14, Cota 255).

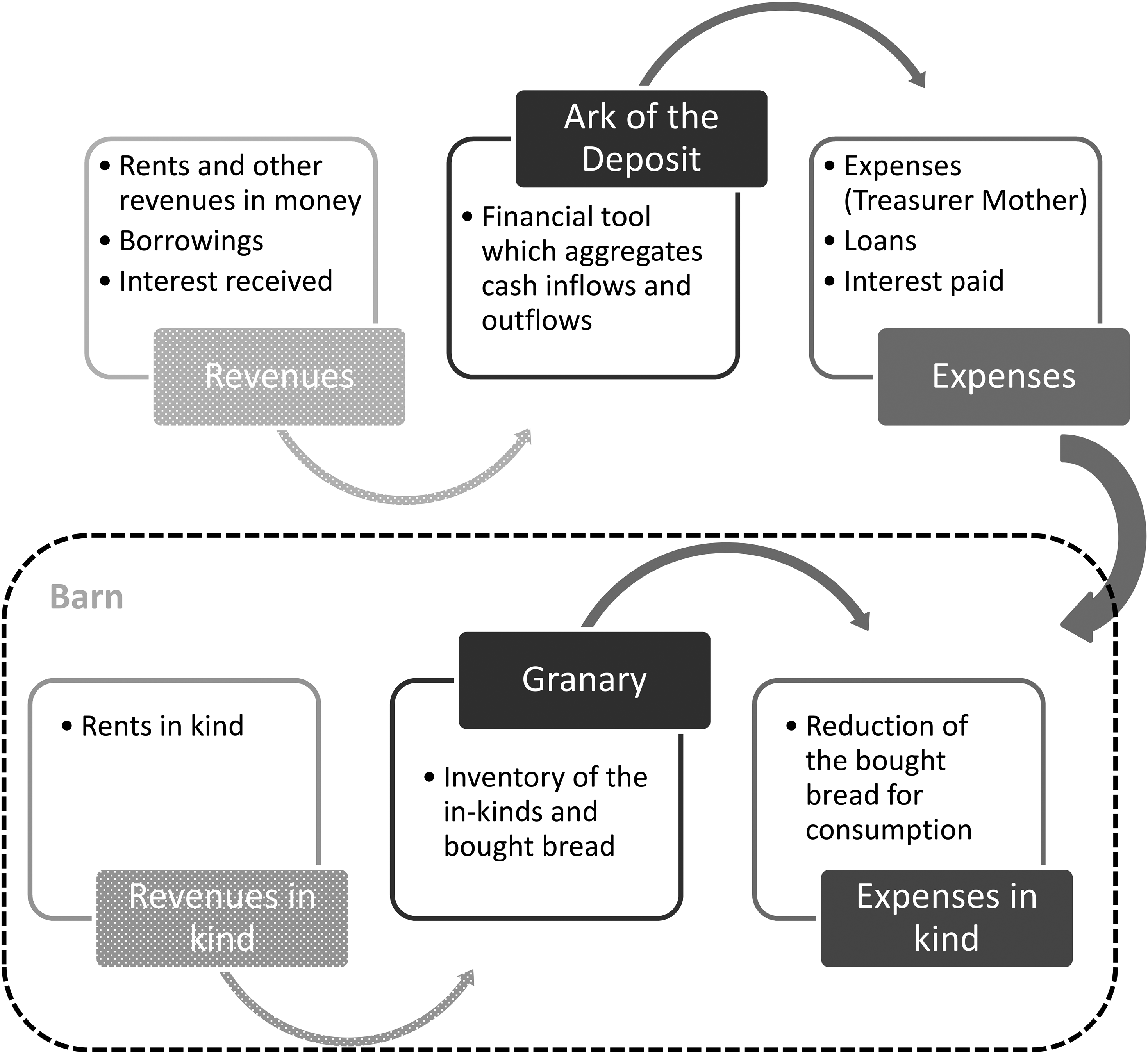

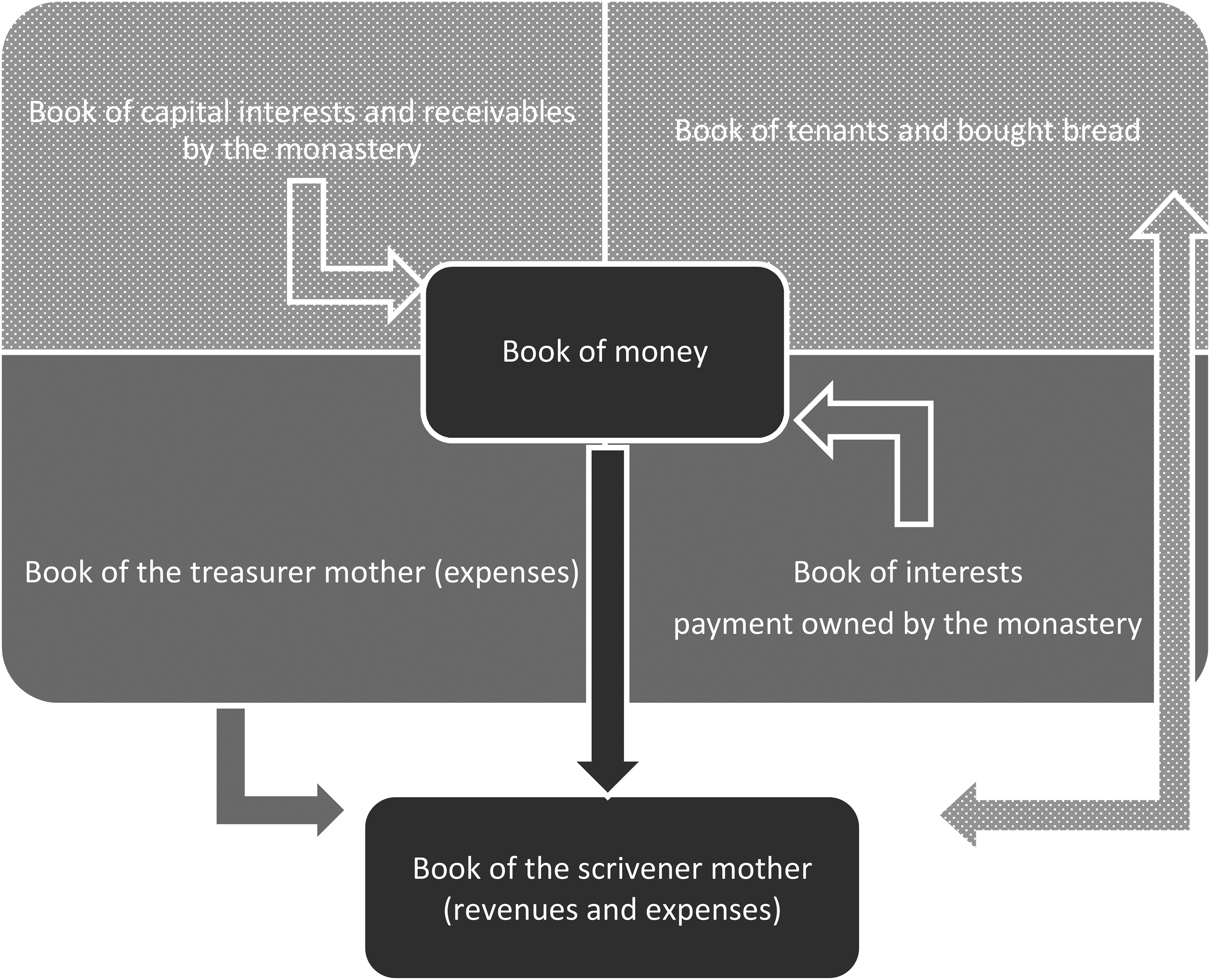

The accounting at the Monastery relied on two tools, as prescribed in the regime of the finances, and similarly to what is illustrated by Prieto et al. (2006): a financial one, called the Ark of the Deposit, served the purposes of aggregating the cash inflows and outflows (see Figure 5), and a storage one, the Celeiro (barn), served the purposes of aggregating the inputs and outputs of goods.

7

Money transactions should have been referred to the Ark of the Deposit, even if the money was used right away. The ark was also a physical space, like a safe, whose three keys were distributed to the abbess, treasurer and scrivener mothers to outline their co-responsibility in the management of money (ADB, Assentos vários…, Treslado da provisão…para o regimento da fazenda, fls 3, Cap. I, Cota 255. It was determined that: there should be two books, one for cash and one for goods, and both books should always be placed in that ark. The entries in these two books should be made by separate titles, by type of revenues and/or expenses and small items should be placed in a single title (ADB, Assentos vários…, Treslado da provisão…para o regimento da fazenda, fls 3, Cap. 3, 4, 5, Cota 255).

The Monastery had overall five types of accounting books (see Figure 6). The inflows and outflows of money from the ark of the deposit were recorded in the book of money by the fiduciary mother. Those records pertain to income and expense of interests and were accounted for by the scrivener mother (ADB, Livro do Dinheiro, Cotas 141–155) in the books of capital interests and receivables by the Monastery and interests payment owned by the Monastery (ADB, Livro das Pagas de Juros que Deve o Convento, Cota 253; ADB, Livro do Capital de Juros a Receber pelo Convento, Cota 253A). The book of money had to be signed by the abbess and the fiduciary 8 and scrivener mothers, as prescribed in the regime of the finances (ADB, Assentos vários…, Treslado da provisão…para o regimento da fazenda, fls 3, Cap. 3e 4, Cota 255).

Accounting processes of the Monastery.

The book of the treasurer mother, later known as book of expenses registered only the expenses of the Monastery which were under the responsibility of the treasurer mother 9 .

The input and output of goods from the barn were recorded by the garner mothers in the book of tenants and bread bought (ADB, Livros dos Caseiros e Pão Comprado, Cotas 156–247). This book had to be signed by the abbess and the garner mothers (ADB, Assentos vários…, Treslado da provisão…para o regimento da fazenda, fls 3, Cap. 3e 4, Cota 255). The garner mothers were responsible for registering the bread bought that they received from the scrivener mother and the bread received from the housekeepers, but they were also the ones controlling the wheat that was sent to the mill, to obtain the flour used to make bread for the community 10 .

Therefore, the concept of ‘restraint’ in terms of disciplined ordering, contents, and relations among the accounting books is significant not only for the internal roles of the nuns but also for the Monastery accounting practices. In that sense, our findings add to Wirtz (2017) and Dobie (2015a) by offering an illustration of a female Benedictine establishment.

Besides these income and expenses books, the Monastery summarised revenues and expenses in a main book, the book of revenue and expense, both in money and goods, where the person responsible for keeping the book was the scrivener mother (ADB, Livro de Receita e Despesa, Cotas 46–90). The system described was the common monastery bookkeeping method in the eighteenth century, both in Portugal and in Spain (see Jones, 2008; Maté et al., 2004, 2008; Oliveira, 2005; Prieto et al., 2006; Silva, 1982).

With respect to the above-mentioned studies, the Monastery of Santa Ana displayed the same attention for detailed accounts, their regularity, arithmetical accuracy, precision and need for supporting documentation (enclosures) of a male priory cathedral (Dobie, 2015a, 2015b). Moreover, the segregation of duties implied by the specialised responsibilities over the bookkeeping (e.g., book of treasurer mother, book of scrivener mother) denotes not only a powerful internal managerial control but also a substantive indifference of the bookkeeping system to gender issues. This specialisation (‘restraint’) of tasks is relevant within the Rule of St Benedict and for the economic success of the Monastery.

The Monastery aimed at maintaining the well-being of its nuns, as also stressed by Hansmann (1980) with reference to not-for profit enterprises: borrowing money to face the expenses could only be made with the approval of the archbishopric and that did not always happen (see ADB, Livro de Receita e Despesa, Cota 51). Therefore, when the revenues were higher than the expenses, the Monastery took the opportunity to redeem loans or place money to earn interest, always keeping an operating fund for priority expenses (see ADB, Livro de Receita e Despesa, Cotas 54 and 59). Through the information rendered, the accounting practices played a major role in the creation of a broader business visibility within the Monastery (Hopwood, 1990; Miller, 1994; Miller and O’Leary, 1987).

Restraint and internal controls

The ‘restraint’ concept at Santa Ana not only implies the definition of precise boundaries and hierarchy of responsibilities in the management of the assets and day-to-day transactions, but it is also the subject of various levels of internal auditing. Compliance with the rules of the regime of the finances was verified periodically: monthly, annually, every three years (see ADB, Livro de Receita e Despesa, Cotas, 46 and 65), for the bishopric, and at the time of providing accounts to the Congregation, through the books of revenues and expenses (see ADB, Livro de Receita e Despesa, Cotas 46–90).

The monthly internal auditing was performed only on the expenses made by the treasurer mother and the garner mothers, in the first day of each month, and it was performed by the abbess, the scrivener and fiduciary mothers, two auxiliary mothers and the manager father, who analysed the expenses of the previous month. Then, the accounts were read to the internal Chapter and if there were any doubts or errors the members of the internal Chapter put them back to the abbess, who would provide clarifications (ADB, Assentos vários…, Treslado da provisão…para o regimento da fazenda, Cota 255, Cap. 13, fls 4).

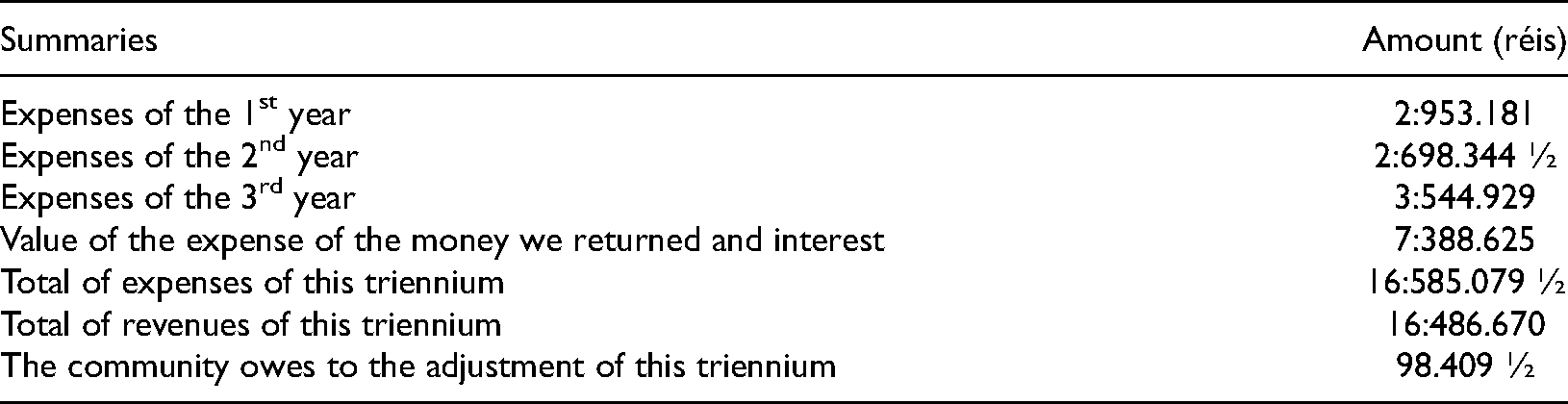

Following the determinations of the regime of the finances, at the end of each year, there was another strict control of all expenses, in money and in goods: the amounts credited, debited and the existing inventory in the Ark of the Deposit and in the barn were double-checked by comparing the amounts given to the treasurer mother and the amounts paid by scrivener mother. Once the accounts were verified and settled, the abbess and the scrivener and treasurer mothers signed them off (see ADB, Livro de Despesa, Cotas 46, 51 and 112; ADB, Livro da Madre Tesoureira, Cota 42). Every three years, in addition to expenses, the abbess, the treasurer and scrivener mothers, and the chaplain father also verified all revenues (see Tables 1–3 11 ). Once the accounts were verified and settled, the abbess, and the scrivener and treasurer mothers signed them off.

Summary of the revenues and expenses for the period 1747–1750 (ADB, Livro de Receita e Despesa, Cota 54).

The religious women were responsible for all the accounting records and preparation of the accounting books. It was when the books were audited at different moments in time that the manager father, the chaplain father and ultimately the bishopric would intervene, but just to control what had been done and make the Monastery accountable for its activities and accounts (see also Dobie, 2015b; Bigoni et al., 2013; Wirtz, 2017). In that sense, ‘restraint’ as rationalisation of tasks and accounting practices shields a space of freedom (Cavendish, 1668; Dash, 1996) and unprecedented exercise of agency in an otherwise masculine and patriarchal world (Hunt, 1992; Lowe, 1990). Our findings offer, from an accounting perspective, a reverse narrative of women: from passive objects of masculine property (Dolin, 1993; Hernández-Pecoraro 1997; Walker, 1998) to active administrative and management subjects (see also inversion of gender roles in Camino, 2001a).

Note on personal qualities and abilities

The tasks and bookkeeping considered in the former sub-sections link the specific administrative load to the assumed mastery of a set of individual capabilities and knowledge, explicitly related to merit and expertise. While considerations of personal skills were recalled by the regime of the finances for the election of the abbess, the hierarchical and accounting rationalisation suggests a considerable level of education in religious, management and accounting matters across the board (Bowden, 2011). In addition, the attention to detail was a fundamental component of the mechanisms of governance and control. In a period when the accounting profession was yet to be established in Portugal (Rodrigues et al., 2003, 2004, 2007), the recording of the economic transactions of the Monastery demonstrates the cleverness of the nuns and their access to unique educational opportunities, including bookkeeping education (Edwards, 2011; Roberts, 2013). From the analysis of the primary sources, it seems that religious women were also aware of the cost/opportunity of certain properties: whenever the Monastery had lands which were not leased for many years, it was a common choice to sell them, placing the money and earning interests (see ADB, Livro dos Caseiros e Pão Comprado, Cota 248; ADB, Livro de Receita e Despesa, Cota 69). These findings support a further reverse narrative on ‘restraint’, which contradicts the argument of Russ (2015) and Howe (2016) on women's access to education.

Restraint and exercise of privileges

As indicated by Inauen and Frey (2010), in monasteries there are no possibilities of distributing wealth (Hansmann, 1980), but there is a strong incentive to make life as luxurious and enjoyable as possible. The Monastery of Santa Ana did not escape these desires.

Although food was the major expense, other main expenses regarded salaries, services, charges with the drugstore, the sacristy and the infirmary, and expenditures related to construction works and maintenance. Small luxuries were the extra food rations paid in cash to the religious women and servants (pats), among others (see ADB, Livro de Despesa, Cotas 91–92, 94–95, 97, 103, 110 and 112). From these accounts, the expenses outside the refectory stood out: they included all the non-titrated expenses, often related to festivities, such as the folar (Easter bread), the sugar for the coating of the Christmas and Holy Saturday beans (traditional kind of sugared almonds) or the mulled wine on Christmas, the alms given to individuals and other religious communities, the Easter bouquets offered to notable people, and similar items (see ADB, Livro de Despesa, Cotas 91–92, 94–95, 97, 103, 110 and 112).

The analysis reveals that some expenses were not realated to the monastic community, but made by individual nuns, not only regarding festivities performed in the church of the Monastery, but also in relation to the sacristy (see ADB, Livros de Receita e Despesa, Cota 55). For example, there was an entry in the book of revenues and expenses, for the triennium 1750–1753, describing the value spent on wax: ‘there were no religious women who wanted to cover this expense on her own account… 100,000 réis’ (ADB, Livros de Receita e Despesa, Cota 55, p.1). This record indicates that in past years the nuns were paying these expenses. There were also records referring to the sale of wheat and loans made to the Monastery by specific religious women 12 . This seems to provide a measure of the exercise of privileges that were made visible by accounting for internal control purposes. The wealth of the Monastery was definitely related to the social status of its members: the bookkeeping reveals that the assets left by departed religious women comprised personal money, jewelry, diamonds, extra cells, and similar secular privileges (see ADB, Livro de Receita e Despesa, Cotas 59, 62, 63 and 74). Moreover, from the books, it is possible to understand that there were gratifications, both in cash and in goods, related to specific managerial positions within the Monastery, such as the membership in the internal Chapter (Capítulo, see ADB, Livro de Despesa, Cota 103; ADB, Livro de Receita e Despesa, Cotas 48, 89 and 90). Some religious women also pursued their own businesses within the Monastery (see ADB, Mapa e Lembranças dos Cadernos de Visitação, Maço de Partes de Livros Desmembrados, Cota 263), while the majority dedicated themselves to craftworks, as prescribed by the Rule. The records on various books 13 clearly demonstrate that the religious women did not give up their worldly goods when they entered the Monastery (Costa, 2007), supplementing the monastic rules with further internal arrangements. The detailed bookkeeping seems to complement, instead of hiding, these arrangements, by redirecting them under the internal public eye and scrutiny of the monastic community. While Dobie (2015a) and Knowles (2004) worry about the exercise of individual extravagance and McCann (1969) condemns them, the recognition of privileges at Santa Ana seems to suggest two positive outcomes. The first is the reinforcement of the original link with the aristocracy, which also served as sources of legitimacy of the Monastery (see Rost et al., 2010), and the second is the ability to keep this exercise under the public eye of the internal control system.

Discussion and concluding remarks

This article aimed to flesh out the concepts of ‘displacement’ and ‘restraint’ of the female gender condition through the analysis of governance and accounting practices in the case of the Monastery of Santa Ana de Viana do Castelo.

While those concepts are heavily researched in literature genres such as novels, poetry, short stories (Camino, 2001a; Camino and Krulfeld, 2005; Cavendish, 1668; Knowles, 2004; Lowe, 1990) in connection to gender, there are much less references in accounting history works, except for Walker (1998) and a few others.

Nevertheless, Benedictine establishments have attracted some scattered attention in managerial, business administration and accounting studies, where works like Dobie (2015a, 2015b), Inauen et al. (2010a), Rost et al. (2010), and Wirtz (2017) help to associate the concepts of ‘displacement’ and ‘restraint’ to their specific governance structures, rationalisation of tasks, accounts, and controls.

The Monastery of Santa Ana was created to link the economic interests of the local aristocracy with the physical enactment of St Benedict's Rule for the young daughters of illustrious families of Viana do Castelo. Therefore, it offers the possibility to respond to the call of Carmona and Ezzamel (2006, 2009), Cordery (2015), Dobie (2015a, 2015b), Prieto et al. (2006) and Wirtz (2017) regarding the need for in-depth investigation of accounting and governance practices in monastic establishments. In doing that, we explored how the gender element became relevant (or not relevant) in the management of such a religious institution.

Despite or maybe thanks to the ‘displacement’ offered by Santa Ana, our analysis showed that the nuns benefited from an unparalleled formal condition of power and self-management, with respect to any secular woman at the time, who would have left the tutelage of parents to come under the tutelage of her husband (Hunt, 1992; Sierra, 2009). That level of emancipation, even if not explicitly considered or regarded by the Benedictine Rule, would not have been allowed in secular life, traditionally dominated by men (Connor, 2004; Lowe, 1990; Virtanen, 2009) or supported by any bookkeeping education (Edwards, 2011; Roberts, 2013). After professing, these young women had an active voice in the governance and management of the Monastery. This study has demonstrated that accounting played a significant role in the administration, and internal controls of (and over) the monastic community of Santa Ana. Specific works on the governance and management of Benedictine monasteries (Inauen and Frey, 2010; Prieto et al., 2006) have highlighted how the assumptions of agency theory (which may dominate the disciplinary use of external controls, such as visitations) are challenged by the St Benedict's Rule principle of co-determination (collegial participation to the Monastery governance). Along with Inauen et al. (2010a, 2010b, 2013), Rost et al. (2010) and Wirtz (2017), our work confirmed that in this displaced environment, governance was based on a participatory internal oversight of the inputs and processes. In this context, oversight was assisted by precise bookkeeping of any (personal and organisational) transaction, which was offered to the public scrutiny of the Monastery management bodies.

The analysis of the roles of the abbess and her auxiliaries gave evidence of a rigorous ‘restraint’ of boundaries of responsibility and functions that, in turn, was reflected in a precise partition and contents’ definition of the related accounting books. By comparing the organisational, administrative and accounting practices at the Monastery of Santa Ana with those at other male Benedictine monasteries (for instance, Dobie, 2015a, 2015b), as reported in secondary sources, we noticed a gender indifference of the Rule in relation to management practices.

Significantly, our findings also provided information on the social dimension of the nuns’ life, and the privileges, assets and luxuries that they retained through their link to the aristocracy. We should note that this aspect was in open contrast with the condemnation of the Rule towards any form of personal proprietas (McCann, 1969) and extravagance and it is seen as a management problem by Dobie (2015a) and Knowles (2004). Nevertheless, its persistence at Santa Ana suggested that future areas of research should cover the intertwines between aristocracy and religion and the forms of legitimacy and female emancipation emerging from those.

Santa Ana was an example of effective control and decision-making over the resources of the Monastery. While discharging the Monastery accountability before the bishopric, this outcome implied business acumen of the abbess and her female auxiliaries. They may have been educated, or they may have been chosen in relation to their capabilities and knowledge (Bowden, 2011). As a matter of fact, this has been another relevant element of emancipation through ‘restraint’ in a historical period where generally women were forbidden a proper education (Hunt, 1992).

Our archival evidence has contributed to reconsiderations of ‘displacement’ and ‘restraint’ in religious institutions. The analysis of their organisational and accounting features at Santa Ana has shown how they were elements of emancipation of nuns. A stark difference was found between the nuns’ status, their ability to mobilise wealth and properties (exercise of active management) and the life that the nuns would have been conducting outside the Monastery as spouses (Camino, 2001a; Howe, 2016; Lowe, 1990; O’Brien, 2008).

Our evidence confirmed that empowerment of women was still possible, paradoxically when they were displaced and restrained in monasteries (Lavrin, 2014; Lowe, 1990). The convents’ boundaries seemed to offer a protection from the scrutiny of the social norms at a point that enclosure became a space of freedom, and exercise of an unparalleled authority and influence.

The history and historical archives of Portugal are very rich and, as far as religious orders are concerned, this work is still far from its real potential. It would be relevant to extend this study on the intersection between governance and accounting to other female Benedictine monasteries, to confirm commonalities or differences in the exercise of internal and external disciplinary mechanisms (Gervais and Watson, 2014). Moreover, further comparative possibilities on the intertwined issues of religion, gender, and aristocracy can be raised between monastic orders, beyond the Benedictine one.

Footnotes

Declaration of conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

Delfina Gomes conducted the study at the Research Center in Political Science (UIDB/CPO/00758/2020), University of Minho/University of Évora and was supported by the Portuguese Foundation for Science and Technology and the Portuguese Ministry of Education and Science through national funds.