Abstract

This study examines how the Great Kanto Earthquake of 1923 influenced the depreciation disclosure practice adopted by Japanese companies in the years that followed. Prior to World War II, corporate accounting behaviour varied widely in Japan, as there were few substantive rules regulating the contents of financial statements. Assessing how a large-scale extrinsic shock such as a major earthquake affects and shapes corporate accounting practices in an unregulated disclosure environment such as this would seem important to understand the intrinsic impact of exogenous shocks. By statistically analysing the contents of 547 financial statements issued by 51 machinery, electrical and transportation equipment manufacturers during the six years from 1921 to 1926, this study shows that the substantial damage inflicted by the Great Kanto Earthquake discouraged companies from disclosing depreciation expenses by reducing or failing to recognise them at all and rendering them less important in their financial statements.

Introduction

Extraneous factors, such as natural disasters, wars and legislation, have affected the accounting behaviour of companies (Arnold and Matthews, 2002; Cheng et al., 2019; Funnell and Walker, 2020). Throughout history, humankind has faced mortal threats. In the first 20 years of this century alone, the world has had to deal with natural disasters that have included wildfires, earthquakes, major storms, droughts and floods. Social problems such as hunger and poverty persist, and economic crises periodically challenge the world's financial structure. As the COVID-19 pandemic has demonstrated, new viral outbreaks can shake the foundations of global stability. Through their disastrous effects, exogenous shocks, directly and indirectly, can radically affect human thinking and social systems, often resulting in the significant transformation of individual and organisational behaviour. The purpose of this study is to examine how such extraordinary exogenous events can shape the accounting behaviour of private companies. As indicated in Cheng et al.'s (2019: 2) assertion that ‘changes in accounting choices observed subsequent to a natural disaster are less likely to be attributable to endogenous factors such as unobserved heterogeneity or reverse causality’, natural disasters are suitable events in considering changes in corporate accounting behaviour. Above all, the focus of this study is to examine the extraneous factor that is the Great Kanto Earthquake and its subsequent influences on Japanese accounting practices. By so doing, this study clarifies how the nature and role of accounting in companies have developed and changed from a macroscopic perspective across space and time.

Over the centuries, Japan has survived repeated natural disasters, 1 typified by significant earthquakes. In particular, Japan's environmental conditions have kept it vulnerable to natural disasters, including typhoons, heavy rainfall (leading to floods), heavy snowfall, and landslides due to the rugged topography with steep inclinations. Earthquakes in the Pacific Rim seismic zone are prevalent around Japan. Therefore, Japan is a nation that has been experiencing frequent significant natural disasters. While the Great East Japan Earthquake of 2011 is only the most recent example, the Great Kanto Earthquake of 1923 remains among the most devastating of all, having caused enormous damage to a large and densely populated area centred on Kanagawa and Tokyo. As a result of its impact, more than 100,000 people were killed or declared missing. In addition to the intense shaking, ground liquefaction, landslides and tsunami that are common in earthquakes, the Great Kanto Earthquake produced a massive fire in the Kanto region, where wooden houses were still prevalent, resulting in large-scale damage to property and widespread loss of life.

Beyond its tragic impact on the lives of so many, the Great Kanto Earthquake may also have influenced accounting practices – particularly those related to depreciation – given the significant damage to many of the assets held by Japanese companies. We already know that the earthquake affected the solvency of many companies and exacerbated the recession after World War I. Thus, it is possible that the earthquake caused corporate managers who were worried about the deterioration of business performance to purposefully reduce depreciation expenses to secure a certain level of net income. By statistically analysing the contents of the financial statements issued by 51 Japanese machinery, electrical and transportation equipment manufacturers during the six years from 1921 to 1926, this study set out to determine whether the disclosure of depreciation expenses by these companies, triggered by the damage caused by the Great Kanto Earthquake, may have lessened and thus could have caused a type of earnings management.

Prior studies have gradually been accumulating to highlight the negative and positive impacts of the Great Kanto Earthquake, both on the entire Japanese economy and on individual companies in Japan. Specifically, studies focusing on the relationship between earthquakes and accounting have been accumulating for the post-war Japan period (e.g., Kawashima, 2017; Nakata, 2011; Tsumuraya, 2013; Yoshizumi, 1998). In particular, Yoshizumi (1998: 63–69) evidenced accounting policy changes, including changes in the depreciation policy, immediately after the Great Hanshin Earthquake in 1995. However, the impact of disasters in Japan's pre-war period on the corporate accounting behaviour of depreciation is still under-researched. Furthermore, most accounting studies on the impact of natural disasters focused on the functions of accounting during the post-disaster recovery and did not examine how exogenous events impact subsequent accounting behaviour. This study aims to fill this research gap.

The Working Rule for Financial Statements, issued in 1934 by the Ministry of Commerce and Industry, provided a prescribed form for the items to be disclosed, but it resulted in no significant impact on financial reporting practice (Noguchi and Nakajima, 2008), as it did not have any coercive force. Thus, before World War II, there were no truly effective regulations in Japan specifying the contents of financial statements, including depreciation disclosure, which meant that the accounting behaviour of Japanese firms varied widely across companies. Such a condition gives us a valuable opportunity to consider how a major exogenous shock can shape a company's accounting practices in a loosely regulated environment – an environment quite different from the modern setting, with its extensive mandatory regulations (Noguchi et al., 2021: 193, 211).

In the financial statements published in the 1920s, depreciation expenses were often presented separately from other income and expense items because of their non-cash expenditure nature. Depreciation as a special item with discretionary treatment was also recognised in the regulations of the contemporary income tax law and judicial precedents. Given this particular status, depreciation expenses constituted one of the most commonly used items for which the company managers could exercise their discretion in corporate accounting. Thus, by elucidating the depreciation behaviour of pre-war Japanese companies, how corporate managers exercised their discretionary powers could also be identified.

The remainder of this article is organised as follows: In the next section, we discuss the main findings of prior research regarding the relationship between natural disasters and the role of accounting and note the perspective missing from most previous studies. We then provide an overview of the Great Kanto Earthquake, the Japanese economy and depreciation practices in the 1920s, and the proposed research framework. Next, we specify our hypothesis regarding the possible change in depreciation disclosure induced by the exogenous shock of the earthquake in 1923, followed by the data used for the study, a description of the proposed analytical models, the results obtained, and our interpretation thereof. Finally, we summarise our findings and discuss their implications.

A review of prior research: accounting, economy and natural disaster

Studies on the relationship between natural disasters and accounting have been rapidly accumulating. For instance, Sargiacomo et al. (2014) and Sargiacomo (2015) focused on the 2009 Italian earthquake, whereas Lai et al. (2014) analysed the impact of the 2010 Italian flood. Miley and Read (2013), Vosslamber (2015) and Jayasinghe et al. (2020) focused on the 1929 Murchison earthquake, the 1931 Napier/Hawke's Bay earthquake and the 2010–2011 Christchurch earthquake in New Zealand. Baker (2014) and Perkiss and Moerman (2020) examined the impact of Hurricane Katrina, which struck the Gulf Coast of the United States in 2005, while Sciulli (2018) focused on the 2010–2011 floods in Australia.

The studies cited above focused mainly on the role of governmental accounting and issues of accountability in government and non-profit organisations in the post-disaster recovery process for relatively recent twenty-first-century natural disasters (Sargiacomo et al., 2021: 198).

Other studies examined the connection between natural disasters and the role of business accounting. For example, Christensen (2002) considered the impact of catastrophes such as hurricanes and earthquakes on the informativeness of earnings in the property and casualty insurance industry in the US between 1989 and 1992 (Christensen, 2002: 224, 232–233). Michels (2017) examined the impact on the market of the disclosure and recognition practices of US companies faced with natural disasters during the period from 1994 to 2012 (Michels, 2017: 3, 12). Cheng et al. (2019) analysed the effect of natural disasters on the accounting behaviour of firms in the US during the period from 1989 to 2018 (Cheng et al., 2019: 18–19). Cheng et al. (2019: 28–29) suggested that managers may view natural disasters as an opportunity to implement so-called big bath procedures as part of earnings management. Specifically, Cheng et al. (2019: 14, 21, 23) indicated that companies facing natural disasters tend to report ‘large negative non-recurring charges’ (in special items), as well as improved performance (ROA) in the three years immediately after the natural disaster. Furthermore, higher stock returns and increased CEO compensation can be found afterwards in companies that suffered natural disasters (Cheng et al., 2019: 25, 27).

The studies noted above examined the relationship between capital markets and accounting information and addressed the opportunistic behaviour of corporate managers that can be triggered by natural disasters, with a focus on present-day accounting practices governed by tightly regulated accounting rules. In particular, earnings management is recognised as ‘“disclosure management” in the sense of a purposeful intervention in the external financial reporting process, with the intent of obtaining some private gain (as opposed to, say, merely facilitating the neutral operation of the process)’ (Schipper, 1989: 92). The motives for earnings management include the interventions in capital markets (investors, shareholders), contracts (contracts on lending and manager compensation) and regulations (industry regulations) (Healy and Wahlen, 1999: 370–371, 376–378). The relevant accounting behaviour may also be recognised in the companies that faced natural disasters under the loose regulations in pre-war Japan covered by this study.

To the best of our knowledge, the representative previous research in the field of accounting history featuring the Great Kanto Earthquake is the study by Shimizu and Fujimura (2010). In their research, the authors examined how Kanematsu, a large Japanese trading company, used its specific accounting practice to deal with the disaster, though the analysis is only limited to the case of an individual company.

On the other hand, research on the impact of the Great Kanto Earthquake has progressed more rapidly in the field of economic history. For example, Hunter (2014) and Hunter and Ogasawara (2019) discussed the impact of the Great Kanto Earthquake on the market economy and the government's response after the disaster. In particular, Hunter and Ogasawara (2019: 1357) pointed out that the exogenous shock of the earthquake caused price fluctuations that spread to provincial cities not directly affected by the earthquake.

Also, Okazaki et al. (2019: 2, 28) pointed out that the Great Kanto Earthquake forced inefficient companies to exit and provided significant opportunities to improve technology and production techniques, but the benefit was mostly limited to large companies that had more access to finance and were already technologically developed. Okazaki et al. (2023) focused mainly on small- and medium-sized companies and banks in Yokohama City that were damaged by the earthquake. Significantly, they pointed out that the Bank of Japan's provision of liquidity had both positive and negative impacts, in that the ‘policy was effective in preventing the credit crunch from amplifying the damage by the earthquake’, but the growth rate of some of the surviving companies was noticeably slowed (Okazaki et al., 2023: 33–34). Okazaki et al. (2023: 5, 33–34) also indicated that access to bank credit was important for the survival of the companies after the earthquake.

In another study, Imaizumi et al. (2016) examined how the Great Kanto Earthquake influenced the spatial distribution of industries in Tokyo. Yoneyama (2009) also analysed the impact of the earthquake on the insurance industry, while Ogasawara (2022) examined the long-term effects of the Great Kanto Earthquake on children's health.

Related to this topic, Okazaki et al. (2023: 5) pointed out that ‘much of the existing literature on the economic impact of natural disasters has focused on impacts at the macro-economic, regional, household, or individual level. In contrast, only a limited number of articles conduct firm-level analysis’. Responding to this suggestion, the aim of the present study is to fill this gap by focusing on accounting behaviour undertaken by specific parts of companies regarding depreciation as an important internal financing source, belonging to the three industries of machinery, electrical and transportation equipment producers.

Research on depreciation practices adopted by pre-war Japanese companies has accumulated as represented by the following studies: Takatera (1974), Miyajima (2004), Aochi (2014), Ono (2008) and Kitaura (2014; 2022). They identified income levels, shareholding structures, existence of creditors, industrial structures and the tax system as the factors that affected depreciation behaviour (Aochi, 2014: 195; Kitaura, 2014: 135, 174–176; 2022: 82; Miyajima, 2004: 257–258; Ono, 2008: 152; Takatera, 1974: 17). However, the relationship with exogenous shocks such as earthquakes is still under-researched.

Based on the awareness of the issues above, the aim of the present study was specifically to examine how a devastating natural disaster that occurred in Japan nearly one hundred years ago shaped a particular accounting practice of Japanese companies operating at the time. Our study differed from all previous studies in that it focused on the impact of the exogenous shock, the Great Kanto Earthquake, on the accounting practice of depreciation discretionarily exercised by companies under the loose regulations in pre-war Japan.

The Great Kanto Earthquake and the Japanese economy in the 1920s

In the 1910s, Japan found itself in a booming economy. World War I brought about Japanese prosperity, which in turn promoted the rapid development of heavy industry (Nakamura, 1971: 128, 133). At that time, Japan faced price increases in heavy industrial goods due to the difficulty of importing these goods from Europe and the US (Hashimoto, 1984: 37, 39). Moreover, as military transportation and worldwide trade expanded, the demand for shipping increased dramatically (Hashimoto, 1984: 31). As a result, investment in the shipbuilding industry and the related steel industry intensified (Hashimoto, 1984: 31–34). Although the shipbuilding industry later faced a recession, it continued to be a core industry (Hashimoto, 2000: 49, 51). Furthermore, the expansion soon spread to other industries, including machine tools, mining equipment, electrical machinery and prime movers (Hashimoto, 1984: 37).

However, after World War I, the Japanese economy entered a period of chronic recession, marked by prolonged low growth throughout the 1920s (Okazaki, 1997: 84). Moreover, on 1 September 1923, Japan was struck by a magnitude 7.9 earthquake, with an epicentre in Sagami Bay, approximately 40 km southwest of Tokyo. The Great Kanto Earthquake caused massive damage to a wide swath of Japan's Kanto region, including Tokyo and Kanagawa (Moroi and Takemura, 2004: 34; Okazaki et al., 2019: 5; Tokyoshi, 1925: 9, 160–163). More than 100,000 people died or went missing in the devastation, and more than 450,000 homes were destroyed by the ensuing fires (Imaizumi et al., 2016: 53; Shimizu and Fujimura, 2010: 308). Damage from the earthquake has been estimated at nearly 5.5 billion yen, roughly equivalent to 35 per cent of Japan's GNP at that time (Imaizumi et al., 2016: 54; Okazaki et al., 2019: 4).

Beyond the immeasurable personal suffering inflicted by this event, the earthquake damaged or destroyed the properties of countless private companies. Specifically, in Tokyo, which was severely damaged by the Great Kanto Earthquake, the machine-related industry, including machinery manufacturing, and ship and vehicle manufacturing industries, was a ‘representative of urban industry’ (Imaizumi, 2008: 346), which is why we focus on these industries. Notably, at that time, it was extremely difficult to restore these assets since few insurance policies covered earthquakes (Hashimoto, 2000: 12). 2 As a result, many of the affected companies lost a significant portion of their assets and found themselves insolvent. As a consequence, multiple Japanese banks and companies faced the crisis of bankruptcy (Hashimoto, 2000: 12). The Japanese government promptly declared a payment moratorium, extending the settlement of bills and the repayment of loans for one month. On 27 September 1923, the government promulgated the Loss Compensation Due to Earthquake Bill, based on which the Bank of Japan was to rediscount all earthquake-related debt (Hashimoto, 2000: 12; Shimizu and Fujimura, 2010: 308). To ease the crisis, the government provided up to 100 million yen as compensation to Japanese banks for any losses they might incur (Hashimoto, 2000: 12; Shimizu and Fujimura, 2010: 308). This ensured liquidity and erased the immediate cash flow concerns of most of those affected (Okazaki et al., 2023: 2). On the other hand, despite the investment in reconstruction projected immediately after the earthquake, that part of the programme did not proceed as planned, due to the political turmoil of frequent changes in the Cabinet, with the result that demand for reconstruction declined and general purchasing power waned (Nihon Ginko Hyakunenshi Hensan Iinkai, 1983: 104). Therefore, ‘the economic recovery was temporary and did not result in significant growth’ (Nihon Ginko Hyakunenshi Hensan Iinkai, 1983: 103), and still, the recession that followed could not be avoided.

In fact, the policy of loss compensation created a new problem. By March 1924, the Bank of Japan had rediscounted 430 million yen of earthquake bills, of which approximately 200 million yen remained uncollected (Hashimoto, 2000: 12; Kishida, 2017: 178; Nihon Ginko Hyakunenshi Hensan Iinkai, 1983: 97). This was largely due to the fact that the bills underwritten by the Bank of Japan included many bad debts that had nothing to do with the earthquake, including bad bills caused by the post-war depression following World War I (Hashimoto, 2000: 12; Kishida, 2017: 178; Shimizu and Fujimura, 2010: 308). 3 Not surprisingly, this became an essential trigger for the Showa financial depression in 1927 (Shimizu and Fujimura, 2010: 308). 4 Thus, the most important macro event with a major impact in Japan which occurred before the Showa financial crisis of 1927 was the Great Kanto Earthquake of 1923.

The 1920 post-war crisis, the earthquake crisis of 1923, the related Showa Financial Depression of 1927 and the Great Depression of 1929 were among the cyclical events that harmed the Japanese economy in general, and the shipbuilding industry in particular (Hashimoto, 2000: 1, 11–13, 27, 35, 49; Okazaki, 1997: 116). Nonetheless, in Japan, heavy industry was developed and technological innovation in electrification was achieved as part of Japan's urbanisation during the 1920s (Nakamura, 1971: 138, 154–155; Okazaki, 1997: 116, 118). Construction projects were promoted, and industries such as civil engineering, construction, electric railways and electric power became the main economic drivers (Hashimoto, 2000: 46–47; Nakamura, 1971: 142; Okazaki, 1997: 116).

Depreciation practice in the 1920s

By the 1920s, Japan had established a capitalistic market economy system that was not significantly different from those of Western countries such as the US (Okazaki and Okuno, 1993: 2). Most companies’ funds were raised through the issuance of shares and corporate bonds (Okazaki and Okuno, 1993: 2). Extensive powers, including the decision-making for dividend payments, were recognised as belonging to shareholders (Kitazawa, 1966: 66–67; Miyajima, 2004: 169). In addition, a small number of major shareholders often served as officers (Morikawa, 1995: 33, 35). As a result, a structure was established in which such owner-managers dominated company management.

The practice of depreciation appears to have begun in Japan in the 1870s and 1880s (the early Meiji era), in line with the introduction of Western technology. However, Japanese businesses did not adopt such a practice voluntarily, though the Meiji government actively promoted the policy. As a consequence, in the early Meiji era, the companies that regularly implemented depreciation were companies that were regulated by the government, which included banks and companies that received subsidies from the government, as represented by the shipping companies (Takatera, 1975: 15).

In contrast, the practice of recording depreciation was minimal among companies unregulated or unprotected by the government. Depreciation expense is at present regularly or systematically recognised on an income statement as an item representing the consumption of tangible assets. Such conceptualisation was not necessarily shared in corporate accounting in the 1920s. Depreciation was not necessarily recognised as an expense. A popular practice permitted by the regulative framework was to treat depreciation as an item of profit appropriation for future replacement funds. 5

The provision of the Commercial Code and the treatment of depreciation in the tax system during the Taisho era (1912–1926) made it possible for corporate managers, at their discretion, to recognise depreciation in their financial statements. There was no provision in the Commercial Code stipulating the calculation of net income. The only effective regulation prescribed under the Commercial Code was on asset valuation: specifically, assets were to be valued below market price (Kitaura, 2016: 37; Noguchi et al., 2021: 194; Paragraph 2 of the 1911 Revised Commercial Code). 6 However, the below-market valuation basis was mostly applied to assets having market value; as the depreciable basis, most of the fixed assets were, in practice, valued at cost (Takatera, 1974: 340).

In addition, the tax authorities in 1918 had allowed depreciation to produce tax savings if the depreciation directly resulted in the devaluation of fixed assets. This allowance seems to have offered corporate managers an incentive to recognise depreciation expenses for tax-saving purposes. However, the low corporate tax rate and small tax savings were insufficient to have depreciation expenses recognised on any significant scale (Kitaura, 2014: 117).

Rather, the recognition of depreciation expenses was largely affected by the companies’ dividend policies. Shareholders at that time specifically demanded that companies pay dividends regularly and at a high level, if at all possible. Consequently, companies recorded depreciation only if they could realise more income than the dividends expected by their shareholders. Indeed, it was possible to calculate net income without recognising depreciation expenses and distribute the profits so calculated as dividend payments because depreciation expenses were long-term costs associated with the consumption of fixed assets. By using the time difference between the time of consumption and that of reinvestment of reserve funds, the companies could temporarily maintain the dividend rates.

Indeed, depreciation was only recorded on an ad-hoc basis throughout the 1920s, and it has already been clarified that the depreciation rate after World War I was lower than the level of the wartime period from 1914 to 1919 (Miyajima, 2004: 162, 209, 254). In addition, management tended to maintain high dividends to meet the demand from the minority shareholders in the 1920s (Miyajima, 2004: 162, 209, 257–258). 7 Moreover, as described above, Japan experienced consecutive recessions in the 1920s. Thus, managers adjusted depreciation expenses to secure the net income needed to maintain a certain level of dividends under the loose regulations and chronic recessions of the time.

Hypothesis development

The Great Kanto Earthquake caused an immense loss of assets owned by Japanese companies in the Kanto region. The financial statements of the sampled companies confirm that the damage recorded was on an unprecedented scale. A survey of 31 observations (31 financial statements) that clearly recognised related losses immediately after the earthquake struck found that the average loss amounted to 10.72 per cent of the total assets owned at the end of the previous period, with a maximum loss of 58.34 per cent. 8

Even in this situation, companies continued to pay dividends. In fact, the financial statements of the sampled companies (547 financial statements of 51 companies) confirm that 72 per cent (146/201) of the companies paid dividends before the earthquake, while 57 per cent (198/346) of the companies paid dividends even after the earthquake. Then, six out of 39 companies that continued to pay dividends in the post-earthquake period specifically implemented accounting measures to reduce capital immediately after the earthquake to eliminate the deficits recorded and resume dividend payments. The above points indicate that even in the period following the Great Kanto Earthquake in 1923, managers of Japanese companies had an incentive to commit to carrying out some accounting measures to meet shareholder expectations of dividend payments. Recording depreciation, which did not involve cash expenditures, was one of the most suitable methods for such measures in the sense that discretionary adjustments were possible.

Specifically, as the recession after World War I lengthened due to the earthquake, and corporate performance continued to lag, it could be reasonably expected that depreciation expenses would continue to be reduced in view of the relationship between corporate performance, dividends and depreciation expenses described in the previous section. It was also possible to recognise no depreciation at all. Thus, the level of disclosure of depreciation expenses could also be expected to decline given the reduced importance of the expenses in the company's financial statements.

In fact, the separation of company ownership and company management had not been sufficiently established in the 1920s, and the corporate managers, who were also major shareholders, had no special incentive to actively disclose corporate information in order to raise external funds. 9 On the other hand, minority shareholders, who had no control over corporate management, tended to intensify their demand for higher dividends in order to recover their investments early. Thus, in a prolonged economic recession, boosting net income by reducing depreciation expenses or disregarding them completely would be a reasonable solution that satisfies the demands of both the owner-managers and minority shareholders under the unregulated accounting disclosure settings of the time.

Based on the reasoning above, we formulated the following hypothesis:

The disclosure level of depreciation expenses in the financial statements of Japanese companies in the heavy industries of the Kanto region decreased subsequent to the 1923 Great Kanto Earthquake.

The hypothesis only applies to the unique corporate governance structure of Japanese companies in the 1920s, as described above. In this sense, it is not necessarily a self-evident proposition, but one to be empirically examined.

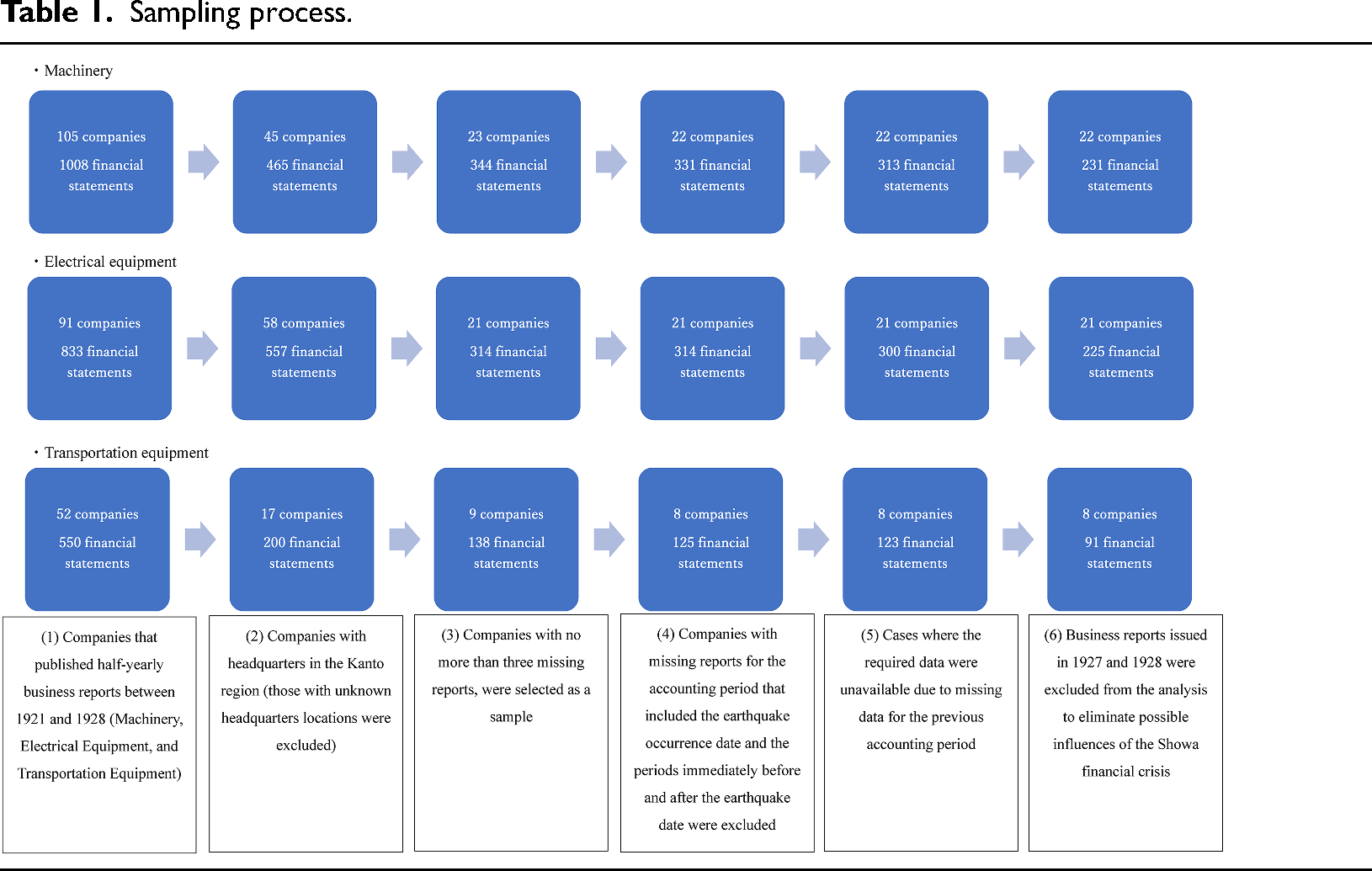

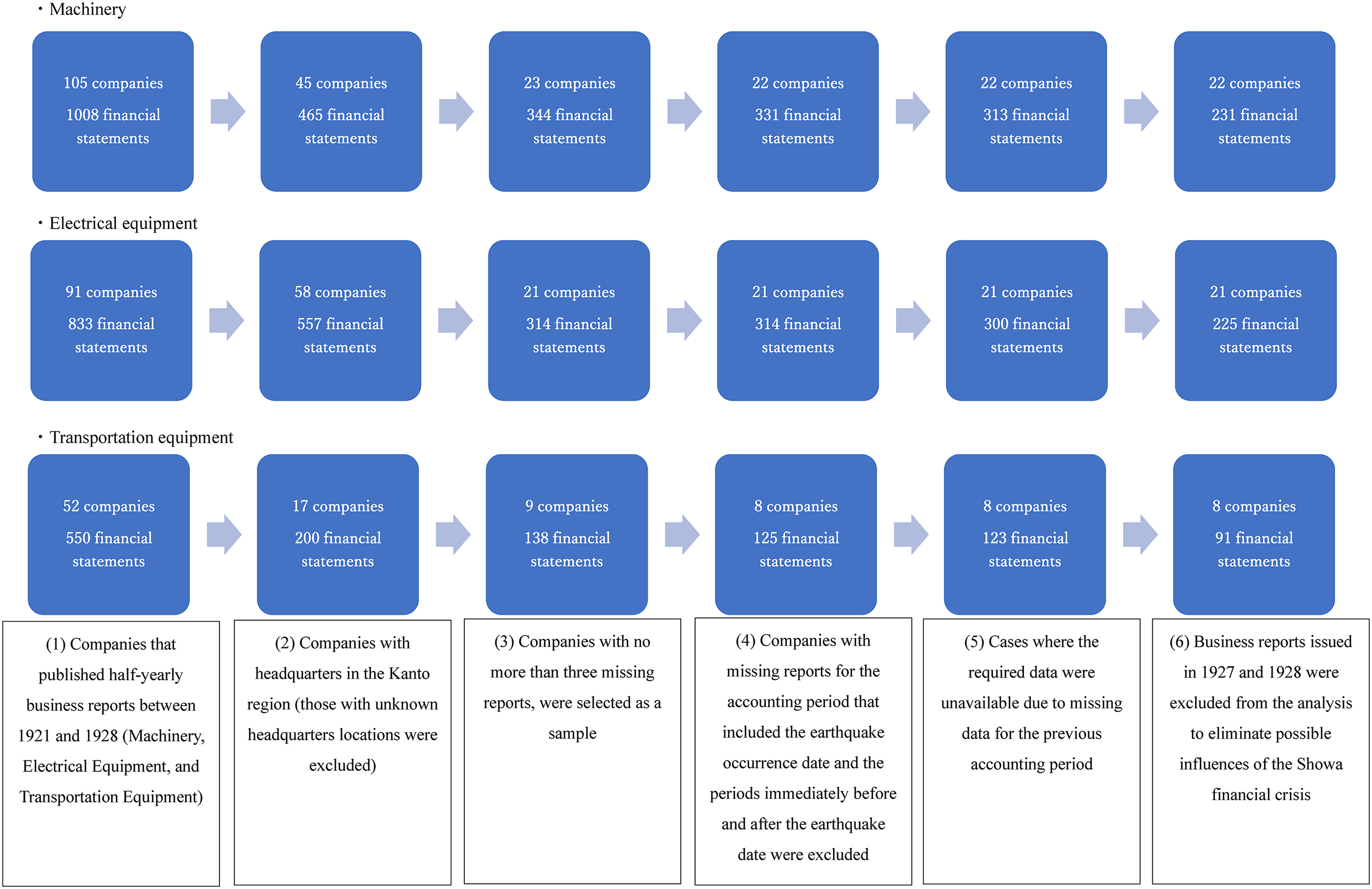

Data

Among the companies that published half-yearly business reports between 1921 and 1928 (available from the Japan Digital Archives Center, J-DAC), those that (1) were classified in the Machinery, Electrical Equipment, and Transportation Equipment categories of the database, (2) had headquarters in the Kanto region (and those having unknown headquarters locations were excluded), and (3) had no more than three missing reports were selected as a sample. On the other hand, (4) companies with missing reports for the accounting period that included the earthquake occurrence and the periods immediately before and after the earthquake were excluded from the sample. 10 Also, (5) the cases where the required data were unavailable due to missing data for the previous accounting period and (6) business reports issued in 1927 and 1928 were excluded from the analysis in order to eliminate possible influences of the Showa financial crisis. As a result, 51 (22 machinery, 21 electrical equipment, and 8 transportation equipment) companies, with a total of 547 financial statements, were retained for analysis (see Table 1). The three industries selected were included in the category of heavy industries, which require significant amounts of capital investment, so each of these three industries had a substantial proportion of fixed asset components compared with other industries and was thus assumed to have had a stronger incentive to recognise depreciation expenses. We use this dataset to test the hypothesis about the depreciation disclosure practices of Japanese companies in the 1920s.

Sampling process.

This study analysed both scenarios (1) where the financial statements issued in the period in which the earthquake occurred (the 6th period) and those in the subsequent period (the 7th period) are included in the sample, and (2) where these financial statements are excluded, since these two periods might have directly reflected the earthquake's damage that should be clearly distinguished from ordinary depreciation. For this purpose, depreciation expenses and losses related to the earthquake damage were separately identified from the financial statements disclosed by the selected companies.

Additionally, to capture the changes in depreciation rates before and after the earthquake by limiting the analysis to companies that clearly disclosed depreciation expenses in their financial statements, the above full sample was divided into the following two categories: (a) those that recognised depreciation expenses explicitly (234 financial statements), and (b) those that did not (313 financial statements).

Analysis

Studies focusing on the content and quality of corporate financial reporting in the early twentieth century include Barton and Waymire (2004) and Van Overfelt et al. (2010). Barton and Waymire (2004) examined the quality of the financial reporting of 540 companies listed on the New York Stock Exchange before and after 1929, and Van Overfelt et al. (2010) examined the quality of the financial reporting adopted by 131 companies during the period from 1905 to 1910 (Noguchi et al., 2021: 197–198). Both studies identified the following factors as those affecting the financial reporting practice.

company age and company size representing the costs of asymmetric information and political costs, ROA or ROE indicating company performance, and bond issuance and financial leverage as a surrogate for agency costs (Barton and Waymire, 2004: 86–88; Van Overfelt et al., 2010: 10–13, 20–21).

The explanatory variables used in these previous studies were considered to be effective in the present study to examine the disclosure of depreciation expenses because these variables were utilised to determine whether or not depreciation was disclosed in the financial statements as the basis for determining the transparency of information disclosure. To test the validity of the hypothesis proposed regarding the depreciation disclosure practices of Japanese companies, we estimated the cumulative distribution function

Specifically,

Following the previous studies mentioned at the beginning of this section, we selected control variables that we believe will affect the disclosure of depreciation expenses.

The first control variable is the size of the company. Here, the natural logarithm of the total amount of assets at time t,

The company age may have also affected the depreciation disclosure practice. The business life cycle and the related business risks of a company are expected to change in accordance with the company's age. As business risks change, the information disclosed by management to minority shareholders may change in relation to the cost of asymmetric information. Therefore, adding a variable representing the time over which the company had operated, from its establishment to the specific accounting period, is necessary to control this factor. For this purpose, the natural logarithm of the company's time of operation as of time t,

As described earlier, the prior literature in Japanese accounting history has shown that dividends and net income were tied closely together. This means that a company was assumed to have first attempted to secure the necessary level of net income from its pre-depreciation income to finance the dividend payout expected by its shareholders. Depreciation expenses were recognised only when the surplus could afford them. Consequently, depreciation is considered to have been recognised as an adjustment to secure the necessary level of net income required to pay dividends, especially when there are no effective rules for income calculation, as was the case in the 1920s.

In this study,

A company's total liabilities are also likely to affect its depreciation disclosure practice. Reliance on debt finances could be expected to have diminished the incentive for managers to disclose depreciation information to shareholders. The debt-equity ratio for period t,

As mentioned above, significant parts of corporate funds were covered by the issue of shares (Okazaki and Okuno, 1993: 2). When a company has unpaid shares,

13

the manager may have an incentive to positively adjust the amount of net income for dividend payments to encourage shareholders to make additional investment payments, possibly adjusting depreciation expenses downward for this purpose and thus reducing their importance in the financial statements. To account for this possibility, a dummy variable to identify companies with unpaid shares,

Results

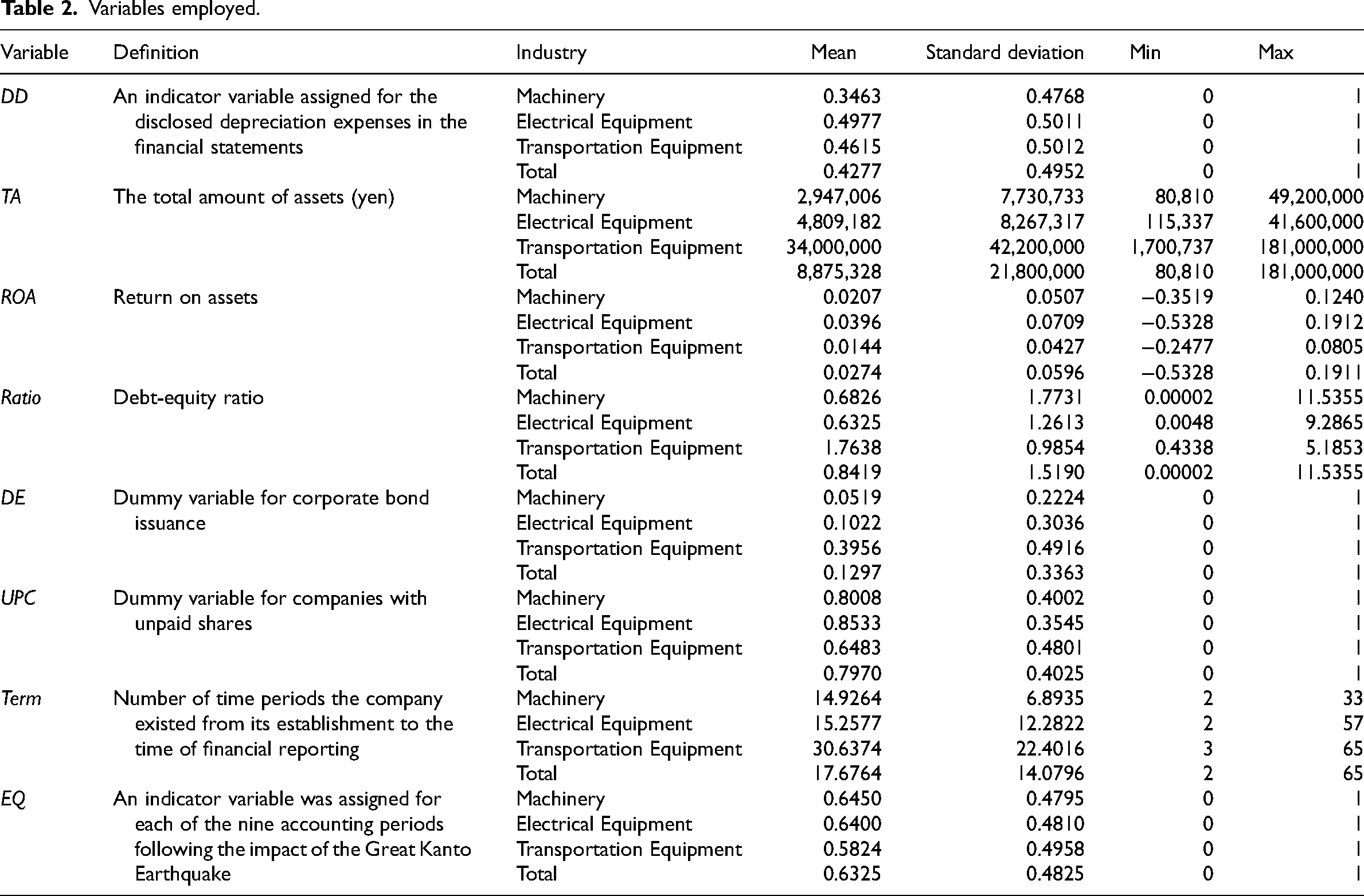

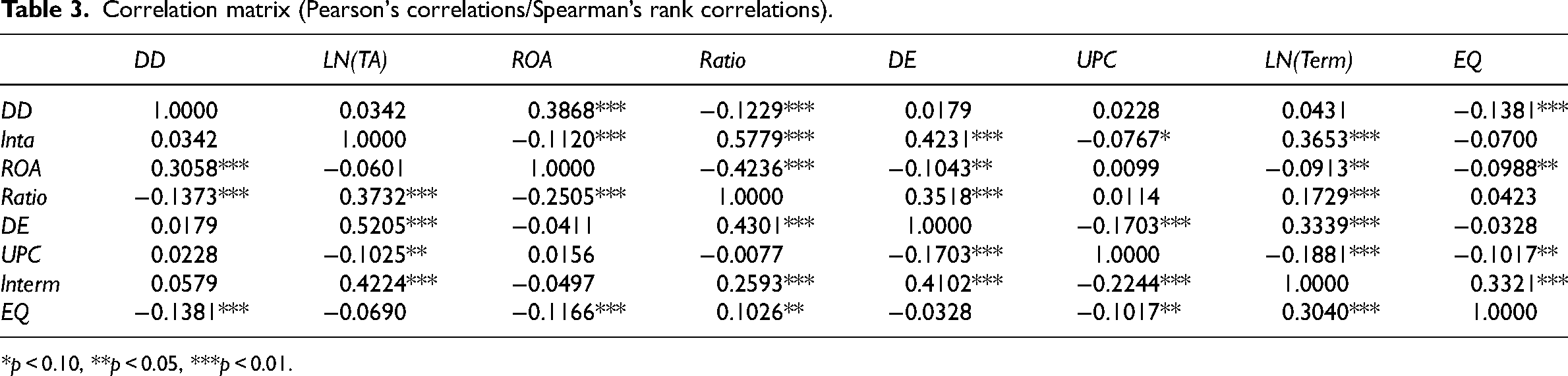

Table 2 shows descriptive statistics for the variables in the model. Table 3 provides also the correlation matrix of the variables. A certain level of correlation between them exists, but in no case was a correlation identified as reflecting extreme issues that would make one of the variables specified unsuitable for the analysis.

Variables employed.

Correlation matrix (Pearson's correlations/Spearman’s rank correlations).

*p < 0.10, **p < 0.05, ***p < 0.01.

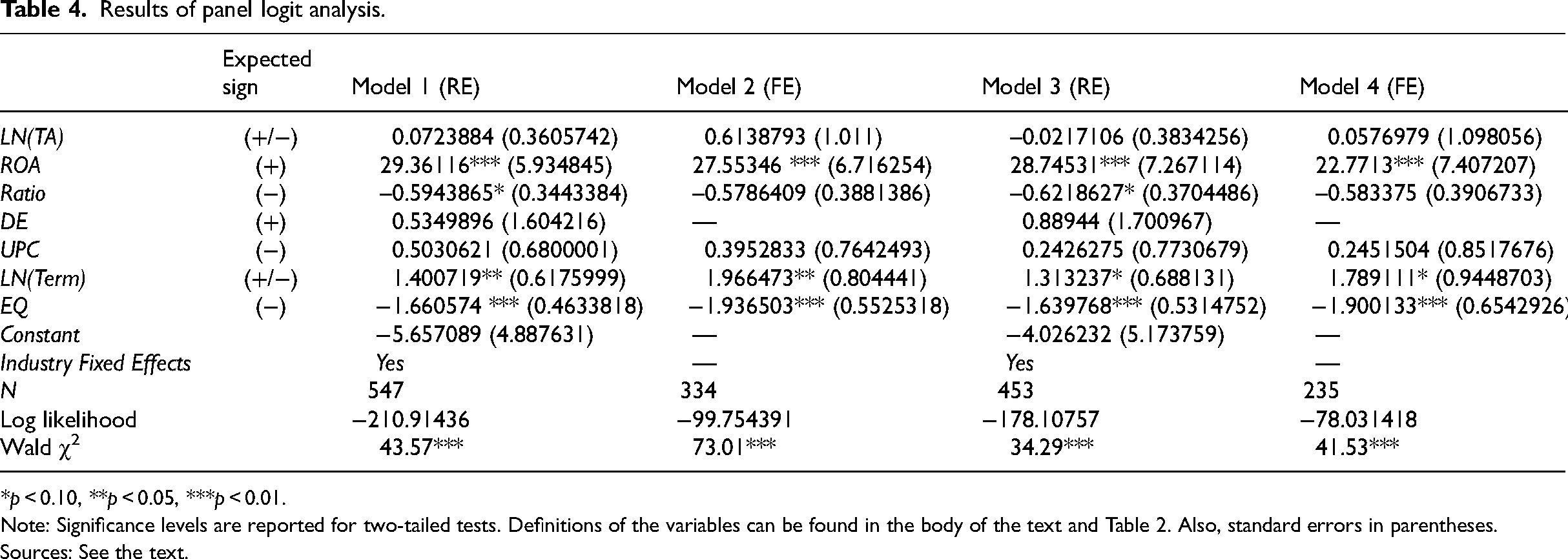

Table 4 shows highly consistent results for the random and fixed effects models for the entire sample covering the full period from 1921 to 1926 (Models 1 and 2) and the sub-sample excluding the 6th and 7th periods immediately after the disaster (Models 3 and 4). 14 For Models 2 and 4 applying the fixed effects model, 213 observations from 20 groups in Model 2 and 218 observations from 25 groups in Model 4 were excluded from the analysis because the outcomes, the disclosure of depreciation expenses in the financial statements, were time-invariant within the same company. 15

Results of panel logit analysis.

*p < 0.10, **p < 0.05, ***p < 0.01.

Note: Significance levels are reported for two-tailed tests. Definitions of the variables can be found in the body of the text and Table 2. Also, standard errors in parentheses.

Sources: See the text.

Except for

As for the critical variable of interest – the indicator variable for the accounting periods following the Great Kanto Earthquake,

The decline in the disclosure of depreciation expenses might have been due to the value of depreciable assets declining from the recognition of impairment losses stemming from the earthquake, and thus the importance of the disclosure decreased accordingly. However, the available data indicate that, while the earthquake-related impairments may have resulted in temporary reductions in total assets, these reductions were not sustained. 16 In fact, for the 466 observations where the individual holdings of real estate (as represented by buildings, which were said to have been heavily damaged by fires caused by the earthquake) can be ascertained from the financial statements, we calculated the ratios of the real estate holdings to total assets and compared the periods before and after the earthquake. No statistically significant difference was found between the two, based on Welch's t-test (12.6% for the period before (0.113 s.d.) and 13.9% after the earthquake (0.107 s.d.)).

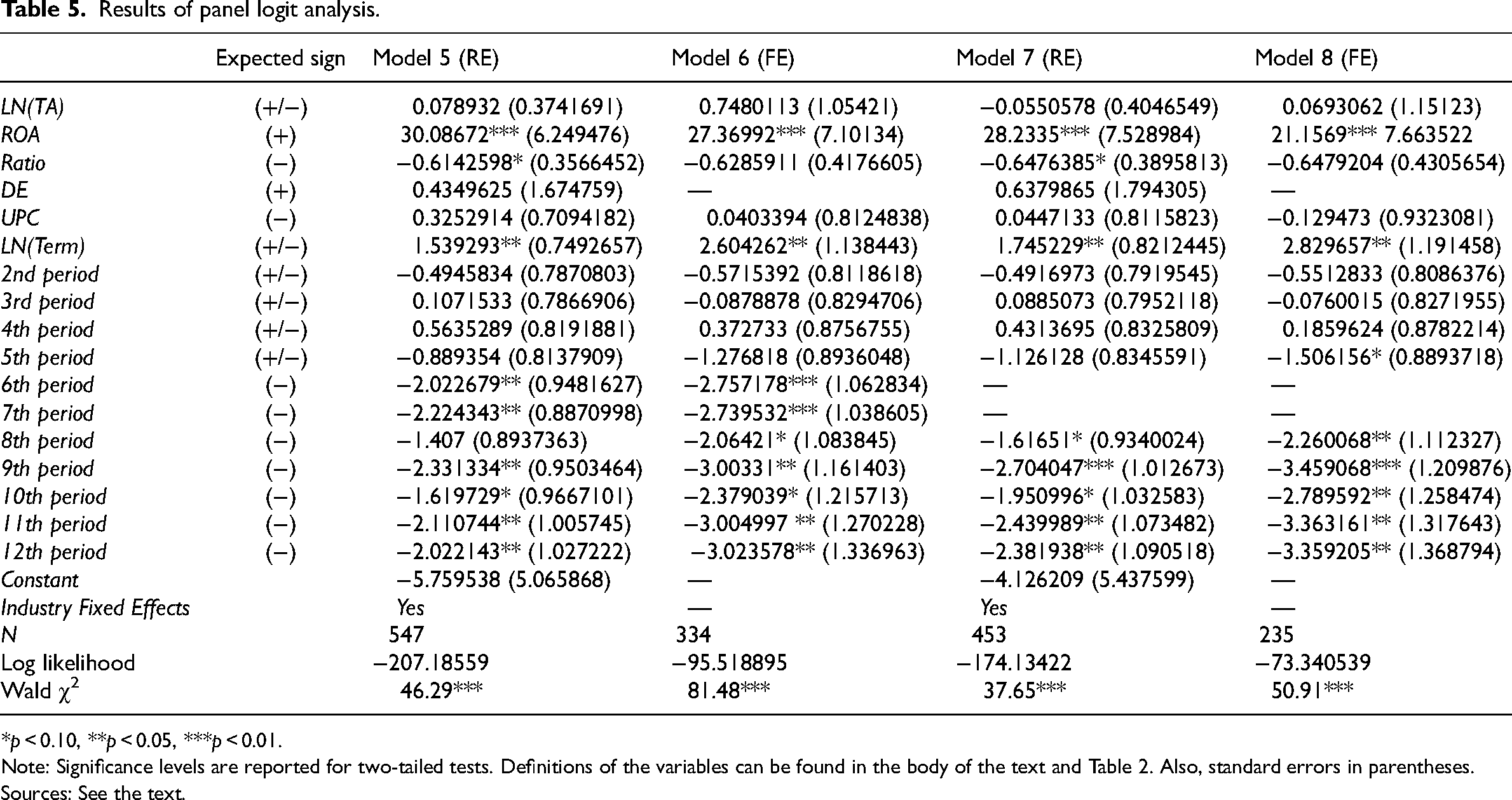

To examine whether the impact of the earthquake was transient and only affected conditions immediately after the occurrence, or whether it had an effect that lasted for an extended period of time, Models 5 through 8 in Table 5 were constructed to show the results of incorporating a time-fixed effect for each accounting period rather than using a single indicator variable that separates the entire period before and after the earthquake. The results reported in Table 5 show a statistically significant negative impact on depreciation expense disclosures that persisted throughout the post-earthquake accounting periods. That the effect lasted through 1926 is consistent with the fact that, after the earthquake, the recession was prolonged, though the economy temporarily recovered when investments for reconstruction were made. Our results thus indicate that the Great Kanto Earthquake triggered a sustained decline in depreciation disclosure that lasted up until 1926.

Results of panel logit analysis.

*p < 0.10, **p < 0.05, ***p < 0.01.

Note: Significance levels are reported for two-tailed tests. Definitions of the variables can be found in the body of the text and Table 2. Also, standard errors in parentheses.

Sources: See the text.

The multiple pieces of evidence available did not support the idea that the decline in the base values of depreciable assets due to earthquake-related impairments caused a temporary decline in depreciation disclosure. Rather, the continued decline in the disclosure of depreciation expenses is consistent with the idea of reducing depreciation expenses for the purpose of recording net income necessary to secure a certain level of dividends during the prolonged recession, as assumed in this study.

Finally, to examine whether the decrease in depreciation disclosure after the Great Kanto Earthquake occurred along with the decrease in the depreciation rate (the ratio of depreciation expenses to average total assets for a specific accounting period), we analysed the financial statements issued by the companies in category

The available data collectively suggest that the reduced depreciation rates or the elimination of depreciation expenses altogether made these expenses less important in the calculation of net income, resulting in an increase in the non-disclosure of this item in the financial statements of the sampled companies. This reasoning suggests that the Great Kanto Earthquake of 1923 discouraged companies from disclosing depreciation expenses in their financial statements for a subsequent period up until 1926, and, in that sense, impeded the spread of the depreciation practice among Japanese businesses in the 1920s.

Concluding remarks

By statistically analysing the contents of 547 financial statements issued by 51 machinery, electrical and transportation equipment manufacturers during the six years from 1921 to 1926, we showed that the Great Kanto Earthquake of 1923 discouraged companies from disclosing depreciation expenses by reducing them monetarily or not recognising them at all, and thus making them less important or irrelevant in their financial statements. In Japan, nationwide accounting regulations were subsequently strengthened in the 1930s, as demonstrated by the publication of the Working Rules for Financial Statements in 1934. The muddled disclosure practices of companies after the earthquake in 1923 are thus considered to be one of the factors that led to the subsequent tightening of regulations.

The reduced level of disclosure of depreciation expenses in financial statements identified in this study differs from the practice recognised in the prior literature of temporarily reporting ‘large negative non-recurring charges’ (Cheng et al., 2019: 14) by the companies having suffered natural disasters. The accounting behaviour was motivated by company managers’ earnings management to meet shareholder expectations of dividend payments. Under loose disclosure rules, companies facing external shocks such as the Great Kanto Earthquake might have intensified their earnings management through discretionary accounting items over the subsequent period following the event. This suggests the need to reconstruct a more suitable analytical framework for corporate accounting responses to exogenous shocks possibly taken in different regulatory settings.

In this way, this study clarifies a point that had not been identified in previous studies, namely the external factor of a huge earthquake impacting depreciation practices at the ‘firm-level’ (Okazaki et al., 2023: 5) (several firms) in the Japanese context, controlling for firm-related factors.

Exogenous shocks such as natural disasters have significant potential to cause extreme damage to human thought processes and behavioural patterns, and can fundamentally change corporate and social systems. Given the widespread use of natural experiments, accounting historians need to find ways to anticipate the changes brought about by these exogenous events through the application of such methods to similar past events.

The results of this study may possibly be biased by the industries selected for analysis. The relationship between the earthquake disaster and the disclosure practice of depreciation expenses may have been more intensified specifically in the three industries selected than in other industries since they occupied a vulnerable position with respect to damage caused by earthquakes in the sense that they were typically urban industries. It is therefore necessary to re-examine the relationship between the exogenous shock of earthquakes and corporate depreciation behaviour across a wider range of industries. In addition, this study analysed companies headquartered in the Kanto region, which was affected by the Great Kanto Earthquake, and specifically compared their disclosure practices before and after the exogenous event. However, a more rigorous examination would have been possible by making a comparison between disaster-affected and non-disaster-affected companies over the same time frame and analysing the differences in their depreciation disclosures. To better understand the impact of the Great Kanto Earthquake on the accounting behaviour of depreciation, it will be necessary to re-examine this point in future research. It would also be appropriate to consider a more extended relationship between exogenous factors, including natural disasters, and corporate behaviour before 1920 and from 1927 onwards, which are not covered in this study.

Footnotes

Acknowledgements

We would like to express sincere gratitude to the anonymous referees for their suggestions and constructive comments. Also, we would like to express sincere gratitude to Professor Massimo Sargiacomo, Guest Editor of Accounting History, and Professor Carolyn Cordery, Professor Carolyn Fowler, and Professor Laura Maran, Joint Editors of Accounting History, for their encouragement, constructive advice, and suggestions to make the paper publishable. We could not have published this study without their dedicated support.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Grants-in-Aid for Scientific Research (grant number 19K13874, 23H00869).