Abstract

This study examines the tone of editorials published in the Journal of Accountancy. Drawing upon prior historical accounting and linguistic-anthropological research, the study proposes that editorials in practitioner journals like the Journal of Accountancy communicate an expressive tone to internal audiences. This tone from the top is important because it communicates a professional worldview to a geographically dispersed and somewhat heterogeneous readership. The study utilises computerised methods to identify the tone expressed about key topics in 46,189 sentence-level editorial utterances published in the Journal between 1916 and 1973. The analysis illustrates that topics involving external social actors, institutions and events were more likely to use a negative tone compared to the topics speaking about internal aspects of the profession. The study contributes to our understanding of professional accounting narratives by enumerating the topics that Journal of Accountancy editorials speak about, by illustrating how sentence tone varies depending on the sentence topic and by documenting how the prevalence of certain topics changes over time.

This study examines the tone expressed in 46,189 sentence-level utterances contained within the Journal of Accountancy editorials between 1916 and 1973. Drawing upon prior historical accounting and linguistic-anthropological research, the study proposes that editorials in practitioner journals like the Journal of Accountancy communicate a tone from the top (Gunz and Thorne, 2015; Schwartz et al., 2005) about key topics and stakeholders to internal audiences. This tone from the top is important because it communicates a professional worldview to a geographically dispersed and somewhat heterogeneous readership. More specifically, we propose that the tone expressed in individual sentences is almost as important as the subject of the sentence because the tone communicates how readers should think and feel about certain topics. Furthermore, we suggest that it is the tonality of different sentences that allows the editorialist to construct a nuanced and persuasive narrative about professional accounting work. The provided analysis both identifies the topics that the editorial sentences discuss and illustrates how tone varies across topics. Consistent with our expectations, topics involving external social actors, institutions, and events were more likely to express a negative tone compared to topics speaking about internal aspects of the profession.

The study makes three contributions to the understanding of professional accounting association communications. First, the study foregrounds the topics that Journal of Accountancy editorials speak about. The Journal of Accountancy is published by the American Institute of Certified Public Accountants (AICPA). 1 The AICPA is a federal-level umbrella organization that represents members from the different state-level CPA associations and is one of the largest and most influential public accounting associations in the world. During its formative years, this practitioner journal contained editorials that communicated the AICPA's point of view about what was happening in the profession (Roberts, 2010). The current study enlists topic modelling methods to identify both the specific groupings of words that comprise a topic and the topics that are present within the editorials. Previous research (Ferri et al., 2018, 2021; Neu et al., 2021) documents how topic modelling methods allow researchers to systematically identify and analyse discursive patterns within large-scale corpora of historical textual accounting material. The current study complements this previous research.

Second, the analysis illustrates the importance of examining the tone expressed in sentence-level professional utterances. Previous research on professional narratives (including historical research) tends to emphasise how public accounting associations communicate a cognitive point of view about professional accounting work (Persson et al., 2018; Preston et al., 1995). The current study draws upon prior linguistic-anthropological research and proposes that such communications are simultaneously evaluative and expressive (Bakhtin, 2010: 85) in that professional narratives are comprised of tone-specific subjects. Editorials talk about social characters, institutions, practices and events within individual sentences, but the tone used to talk about these subjects varies. It is this tonal variability that not only allows the editorialist to communicate how the audience should feel about certain events and social characters but also contributes to the construction of a nuanced, and hence unambiguous, aggregate-level narrative. 2 The current study highlights how sentences are used within Journal of Accountancy editorials to express a variable tone from the top. More generally, the study both draws attention to the importance of considering the role of tone within historical accounting narratives and complements recent research on the communication of tone within accounting disclosures (see Gandhi et al. 2019; Huang et al. 2014; Loughran and McDonald, 2011, 2016).

Third, the study demonstrates the utility of computer-assisted research methods when studying large-scale, multiyear historical textual accounting materials. Traditional narrative historiography studies such as Edwards (1955, 1956), Creighton (1984), Hanlon (1994) and Preston et al. (1995) highlight how careful consideration of accounting artifacts vis-à-vis the internal and external dynamics (Klegon, 1978) of the profession helps us to understand the trajectory of professionalization processes. At the same time, such methods are not well suited for analysing microlevel intratextual discursive relationships within large, multiyear document corpora (see DiMaggio et al., 2013). As studies such as Preston et al. (1995) illustrate, it is possible to provide a nuanced reading of large-scale, multiyear document corpora but this invariably involves selecting a subset of the data and/or focusing on a small number of thematic categories. In contrast, computer-assisted historiographic methods provide us with a ‘colder’ but more systematic reading of the entire document corpus.

3

As DiMaggio et al. (2013: 577) state: Topic modeling algorithms are a suite of machine learning methods for discovering hidden thematic structure in large collections of documents… Furthermore, a topic model might uncover topics that a researcher using hand coding methods might not otherwise have seen… With topic models, researchers can discover new patterns in their text data and analyse much larger collections than is possible by hand.

The current study demonstrates how computer-assisted methods foreground systematic patterns within historical accounting materials and suggests that such methods complement, but do not replace, traditional historiographic methods.

Following this introduction, the next section considers the role of tone within professional narratives. We then discuss the data and methods and present the results. The final sections provide a conclusion as well as a discussion of the findings and implications of the study.

The tone from the top

Starting from previous accounting history research and drawing upon prior linguistic-anthropological research, we propose that editorials within the Journal of Accountancy communicate multiple understandings about accounting work and other developments within the profession to different internal readerships. This vantage point suggests that microlevel sentences can be viewed as the base level ‘intratextual unit’ for meaning construction (Silverstein, 2005: 8). Sentences enlist a series of intratextual meaning construction strategies (Briggs and Bauman, 1992), being built around nouns which denote social characters, institutions, events, and aspects of professional work. In turn, sentences are combined into aggregate-level professional narratives. This said, sentence-level communications and aggregate editorial narratives are not neutral descriptions; rather, they articulate a tone-infused point of view (Voloshinov, 1994: 168). The remainder of this section elaborates on these ideas and how this vantage point informs our understanding of AICPA editorial communications.

Prior research on accounting associations highlights that it is impossible to understand the accounting profession without considering the nexus of macrolevel social relationships that impact accounting practice (see Fogarty et al., 2006; Merino and Mayper, 1993, 2001). For example, governments grant accounting associations a quasi-monopoly over certain types of professional work (Puxty et al., 1987; Richardson, 1989); however, these quasi-monopolies are always somewhat open-ended, resulting in jurisdictional battles among different professional groups vying to provide similar professional services (Himick, 2016). Furthermore, while governments provide professional associations with a quasi-monopoly, they also utilise regulatory agencies to govern and constrain the activities of professional associations (Malsch and Gendron, 2011). The Financial Accounting Standards Board (FASB), the Securities and Exchange Commission (SEC) and the Public Company Accounting Oversight Board are some of the regulatory agencies that impinge on how public accounting is practised within the United States; similar regulatory agencies exist to govern the accounting profession in other jurisdictions such as Australia and the United Kingdom.

The macrolevel context with its professional privileges, jurisdictional challenges, and regulatory constraints encourages accounting associations like the AICPA to attempt to produce somewhat standardised accounting professionals and to guide how practitioners practise accounting. Larson (1977, 2018) refers to this as the ‘producing the professional producer.’ Like other accounting associations, the AICPA uses ethical codes (Gaa, 2004; Preston et al., 1995), education requirements (Alford et al., 1990; Martinov-Bennie and Mladenovic, 2015; Misiewicz, 2007), as well as disciplinary mechanisms (Armitage and Moriarity, 2016; Jenkins et al., 2018) and communication activities (Neu and Saxton, 2022; Roberts, 2010) to attempt to produce technically competent professional accountants who meet minimum standards of professional conduct (De George, 1990; Sonnerfeldt and Loft, 2018). Klegon (1978) refers to the macrolevel context as the external dynamics of the profession, whereas the production of accounting practitioners is part of the internal dynamic.

Within these attempts to produce accounting practitioners, written communication such as editorials in practitioner journals like the Journal of Accountancy allows the AICPA to provide timely guidance to internal audiences (Roberts, 2010: 115). Professional accountants are stratified and divided by the part of the country where they live, whether they work in public or private practice, and their level of seniority (Roberts, 2010: 98; Van Hoy, 1993). In contrast to ethical codes and educational requirements, which are relatively static because of the lead times involved in making changes, editorials are timelier and address topical public interest issues that have significant implications for the accounting profession. Furthermore, editorials allow the AICPA to craft a narrative that captures ‘just the right tone’ when talking about certain subjects.

Previous linguistic anthropological research is useful in thinking about how editorials attempt to capture the ‘right’ tone. First, this stream of research emphasises the importance of examining sentence-level enunciations and the intra-textual ways that meaning is constructed (El Ayadi and Smith, 2008: 338; Silverstein 2005). These enunciations use nouns to signal to the reader what the utterance is about (Bakhtin, 2010: 60). ‘Subject words’ such as accounting, auditing, and consulting help to indicate the topic, whereas ‘social character words’ are used to refer to both people such as accountants and institutions such as the SEC, FASB and the government. 4 As Jones (2014: 8) notes, social character words are the building blocks around which narratives are constructed. It is the placement/juxtaposition of these different types of nouns as well as other words within sentence-level enunciations that facilitate meaning construction (Briggs and Bauman, 1992: 147; El Ayadi and Smith, 2008: 336).

Second, this perspective stresses that sentence-level enunciations are not only infused with a tone but also that tonal variability is used strategically to construct aggregate-level narratives. For Bakhtin (2010: 84), sentence-level enunciations are always expressive in that they express ‘the speaker's subjective emotional evaluation of the referentially semantic content.’ On the one hand, sentences are expressive because sentence-level enunciations enlist prevalue-infused social characters (Silverstein, 2005) that readers of a magazine like the Journal of Accountancy will recognise because they are part of the authoritative discourse of the profession. As Voloshinov (1994: 168) states, these ‘articulated words are impregnated with assumed and unarticulated qualities.’ 5 On the other hand, the sentences themselves accentuate these sentiments by using helper words to accomplish the ‘speech will’ of the editorialist (Bakhtin, 2010: 77). As Voloshinov (1994: 165) notes, it is these value judgments that ‘determine the very selection of the verbal material and the form of the verbal whole.’ Voloshinov (1994: 165) continues by stating that it is through intonation—or what can be referred to as sentiment or tone—that the expression of value judgments ‘finds its purest expression.’ 6 Although the tone is easier to detect within verbal communication (via meta-communicative cues), similar cues exist within written communication (El Ayadi and Smith, 2008: 340). Following previous linguistic and anthropological research (Briggs and Bauman, 1992: 149; Voloshinov, 1994: 167) as well as from recent research on accounting disclosures (Gandhi et al. 2019; Loughran and McDonald, 2011, 2016), we assume that the careful selection of specific verbs, adverbs and adjectives helps to construct a communicative tone.

Third, this vantage point draws attention to the importance of tonal variety within aggregate-level narratives. Whereas the incorporation of words that express tone into sentence-level enunciations reduces ambiguity by complementing the preimbued value judgments about specific social characters, the articulation of different sentiments about different social characters and other subjects in different sentences helps to build more nuanced yet unambiguous aggregate-level narratives. Editorials, for example, can speak about a mixture of protagonists and people/things that stand in their way (Roberts, 2010: 97). Within such narratives, the variability between a well-meaning accounting association and/or individual practitioners versus governments and regulators who are always trying to constrain and impede professional activity helps to construct a professional narrative. Alternatively, editorials might speak about ‘good’ accountants versus accountants who don’t follow the rules of professional conduct. In both examples, it is the presence of tonal variability that helps to ensure that editorials have an unambiguous ‘moral to the story’ (Farias et al., 2021; Statler and Oliver, 2016). Stated differently, it is the combination of ‘differently toned’ characters and subjects that allows the editorial to construct a nuanced yet unambiguous professional narrative.

Implicit within this prior research are two premises that are central to the current study. First, this perspective emphasises that the tone of editorial utterances is almost as important as the subject matter. Social characters, whether they are accountants or the government or regulators, are what linguists refer to as a token: words that point to a more abstract type (Nakassis, 2013; Silverstein, 2005: 9). Abstract types such as the auditor or the government are preimbued with expressive characteristics within professional speech genres, meaning that readers of an editorial in the Journal of Accountancy already have an opinion about these social characters. At the same time, the intratextual positioning of adjectives, verbs, and adverbs alongside the social character allows the editorialist to burnish and accentuate these character-specific sentiments (Briggs and Bauman, 1992). It is for these reasons that we propose that the intratextual construction of tone is almost as important as the subject of the sentence. Stated differently, utterances about social characters are always expressive but this expressiveness is accentuated through the intratextual enlistment of helper words within the sentence.

Second, this vantage point suggests that tone must be examined at the sentence level rather than at the aggregate editorial level. For the reasons explained above, the aggregate tone of an editorial will always consist of a series of sentence-level, mostly social character–specific, tones. For example, consider the following three sentences from our data:

‘CPA students receive good training.’ ‘The AICPA ensures that all members have excellent ethical standards.’ ‘Despite this, government is unwilling to stay out of internal matters.’

In this simple example, the editorial refers to four social characters (students, AICPA, members, and government) and contains two positive-toned sentences and one negative-toned sentence (‘unwilling’ was the negative-tone word). On an aggregate level, the editorial seems to be positive because there are two positive sentences and only one negative sentence. Furthermore, on an aggregate level, we cannot determine whether the editorial is talking positively about all four social characters or whether there is tonal variability across the characters. It is for these reasons that it is important to move down to the level of individual sentences since it is there that the tonal variability across social characters tends to be more visible.

The preceding discussion has three implications for the current study. First, it foregrounds the importance of focusing on sentence-level editorial content since sentences are the base-level narrative building blocks. Second, it proposes that sentences involving different social characters, practices and events will express different tones. Finally, it implies that aspects of the external dynamic (especially social characters such as governments, regulators and other institutional actors who can constrain and censure the profession) will be associated with a negative tone, whereas aspects that relate to the internal dynamic will be more favorable. The next section outlines the data and methods that we use in the study.

Data and method

The study uses sentence-level editorial data published in the Journal of Accountancy between 1916 and 1973 as our data source. The Journal Accountancy started to publish editorials in 1916 and stopped publishing editorials in 1973. Our approach was sequential, starting with a thorough review of all physical/digital copies of the journal from 1916 forward to identify the editorials. The identified editorials were scanned, processed with OCR software, and checked for accuracy. We then used the open-source statistical software R to prepare a corpus of editorials and to partition the editorials into sentences. The final data set consists of 46,189 sentences taken from 552 editorials published between 1916 and 1973. 7

Like previous topic modelling-based historical accounting research, we use Latent Dirichlet Allocation (LDA) methods to identify the latent thematic speech topics that are present in the corpus (Ferri et al., 2018, 2021; Neu et al., 2021). Topic modelling approaches are becoming increasingly popular within the social sciences because topic modelling provides a mostly objective method to identify thematic topics within corpora that are too large for noncomputerised, researcher-directed intensive readings (DiMaggio et al., 2013; Huang et al. 2018). 8 Additionally, topic modelling approaches facilitate the comparison of narrative topics across different institutional settings—comparisons that allow researchers to both partially validate their results and to better understand how narratives vary across institutional contexts. We return to this point in subsequent sections.

LDA topic modelling methods have been referred to as a ‘bag of words’ approach since it uses Bayesian probabilities to identify co-occurrences of different words with the corpus. In essence, LDA algorithms attempt to identify words within the different sentences that discriminate among thematic topics (DiMaggio et al., 2013: 578). Given that LDA topic modelling methods are a mathematical approach to identifying thematic categories given a unit of text (i.e. sentences or editorials) and a group of unit-level observations (such as the corpus of sentences or editorials), the only real requirement is that the unit of text is consistent across the entire corpus (see Huang et al., 2014). 9 Furthermore, our decision to focus on sentences is consistent with our theoretical framing and with Huang et al. (2014). As Huang et al. (2014: 1492, footnote 5) state, it is appropriate to focus on sentences because ‘the sentence is a natural unit in language for expressing opinions.’ In terms of a specific LDA method, the current study utilises the structured topic modelling (STM) algorithms of Roberts and colleagues that are available in R (Roberts et al., 2014). These algorithms have been used in a variety of academic studies (Chen et al., 2020; Farrell, 2016; Roberts et al., 2019; Schmiedel et al., 2019).

We stated earlier in this section that topic modelling approaches provide a mostly objective method for identifying thematic categories: the reason being that the algorithms calculate the best division of words given a specified number of researcher-selected topics (what is referred to as k values). This said, STM algorithms also contain a group of diagnostic tests that allow the researcher to identify a small range of optimum k values (Roberts et al., 2014). For the current corpus, the optimal number of topics falls somewhere around 20. 10 To assess the sensitivity of our findings to the selected k value, we ran the analyses using k = 18 and k = 22. The overall results did not change. 11

Similar to Huang et al. (2014: 2152), a central premise of the current study is that it is necessary to measure the tone associated with different sentences. To do this, we use Loughran and McDonald's (2011) financial negativity measure. Loughran and McDonald's (2011) article demonstrated that a finance/accounting-specific dictionary approach to measuring tone not only was superior to more general dictionary approaches but also helped predict stock market returns and stock market volatility. Methodologically, the article by Loughran and McDonald (2011) is extremely important because it proposed a series of different measures for tone and it also worked through the advantages and disadvantages of the different measures. Initially, the authors suggested six finance/accounting-specific measures of tone: negativity, positivity, uncertainty, litigiousness, strong modality and weak modality (Loughran and McDonald, 2011: 44). Althhough all measures had some predictive ability, Loughran and McDonald (2011) suggest that the negativity measure is the best general-purpose measure. A subsequent review article by these same authors notes that research articles building on their work have typically used the negativity measure ‘to gauge the tone of business communications’ (Loughran and McDonald, 2016: 18). The R sentiment module that we subsequently use to measure tone includes two of Loughran and McDonald's (2016) tone measures: the negativity measure and positivity measure. This said, Loughran and McDonald (2016: 32) advise against using the positivity measure since there is ‘little incremental information in positive word lists.’ 12

Before continuing, it is useful to return to our previous simple editorial example above to illustrate how Loughran and McDonald's (LM) negativity measure is calculated. The simple editorial example contained three sentences: ‘CPA students receive good training’ (1), ‘The AICPA ensures that all members have excellent ethical standards’ (2), and, ‘Despite this, government is unwilling to stay out of internal matters’ (3). The LM approach for negativity ‘counts the number of words associated with a (negative) sentiment scaled by the total number of words in the document’ (Loughran and McDonald, 2016: 11). The first and second sentences each have one positive word (‘good,’ ‘excellent’), whereas the third sentence has one negative word (‘unwilling’). Dividing these counts would result in the following negativity scores for the three sentences: first sentence (0), second sentence (0), and third sentence (.09). 13

The current study starts from this scaled LM negativity score contained within the R sentiment package and then converts this score into a binary 1/0 indicator variable that was coded 1 if the sentiment/tone score was negative and 0 if the sentiment/tone score was nonnegative. Our negativity measure contains less information than the initial scaled negativity score but, at the same time, it introduces an additional control for the length of the different sentences. For example, we can imagine two sentences expressing exactly the same tone but the second sentence containing several additional words (for instance, ‘the government keeps trying to meddle in internal matters’ vs. ‘despite what we have been doing, the government keeps trying to meddle in internal matters’). The use of a 1/0 indicator variable for negativity assigns both sentences a value of 1 regardless of the number of words in the sentence. 14

Additionally, to ensure that sentiment/tone words are not double counted in both the topic model results and the tone score, we removed the words contained in Loughran and McDonald's (2016) word list from the corpus prior to running the topic model. Given that Loughran and McDonald's (2016) word list contains mostly adjectives and adverbs with some verbs, the removal of these words did not impact the identified topics since the identified topics contain mostly nouns and verbs. As mentioned previously, the use of Loughran and McDonald's (2011, 2016) dictionary approach to measuring sentiment or tone is the dominant approach within financial settings (Kearney and Liu, 2014: 175), having been used in multiple previous studies (Gandhi et al., 2019; Johnman et al., 2018).

The LM negativity measure is highly useful because it allows us to examine the granular detail of editorials: an endeavor that is simply not possible with qualitative research methods. Furthermore, the combination of a topic modelling approach and LM's negativity measure makes it possible to identify patterned relationships among social characters and negative helper words, again something that would be almost impossible to do with qualitative research methods. At the same time, the LM negativity measure will always be somewhat noisy. For example, the LM approach measures the adjectives, verbs, and adverbs that convey tone and that co-occur in the same sentence as a social character. Looking at our data, such sentences can be a declarative sentence such as ‘governments are always meddling’, but it is also possible that the sentence is not expressing a direct negative tone about the government (e.g. ‘in the absence of government intervention, there will be negative consequences for CPA firms’). Furthermore, it is possible that individual sentences will talk about more than one social character in a single sentence, such as when sentences two and three from our simple example are combined (‘The AICPA ensures that all members have excellent ethical standards’ (2) yet, ‘despite this, government is unwilling to stay out of internal matters’ (3)). Both of the above examples point to the noisy nature of computer-assisted approaches. This said, computer-assisted approaches allow us to identify aggregate patterned relationships within the corpus.

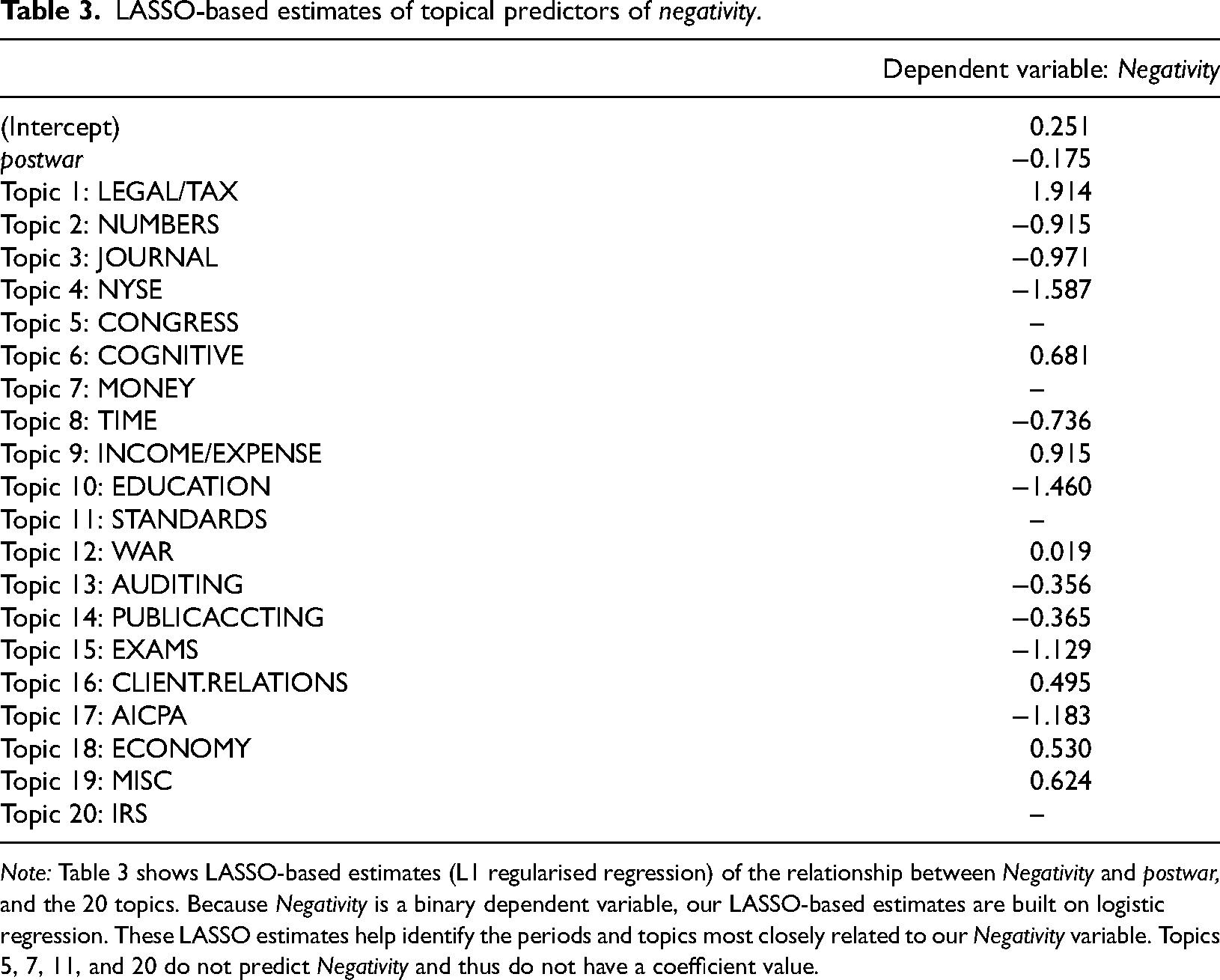

To assess the relationship between the LM negativity score and the identified topics, we use the topic-LASSO algorithms available in R. 15 The topic-LASSO model was developed to assess whether the topics identified by the STM topic modelling algorithm help to predict an arbitrary indicator variable, in this case, Negativity. The topic-LASSO algorithm is a wrapper for the GLMNET R module (Hastie et al., 2021) that adopts the more general algorithm for use with the STM outputs. LASSO regression algorithms apply a penalty function to variable coefficients as a way of correcting for potential multicollinearity in the topics as well as potential overfitting of the data. 16 As the results reported in Table 3 highlight, one of the unique features of LASSO regressions is that regression results only include coefficients for variables that are significantly related to the dependent variable since the penalty function sets nonsignificant coefficients to zero (Hastie et al., 2021: 6). Although the LASSO algorithms are the most appropriate statistical method for assessing the relationship between Negativity and the identified topics, we also utilised a more familiar logistic regression approach to provide a check on the LASSO results. We also used the nonindicator version of LM's negativity measure as the dependent variable. These two groups of results, which we do not report, are consistent with the reported LASSO results.

In addition to the aforementioned variables, we also include a time variable to control for changes over time. The postwar variable is coded 1 if the sentence was included in an editorial after 1945 and 0 otherwise. We use this variable in the subsequent analysis to assess whether negativity increases or decreases in the postwar period as well as to assess whether the prevalence of the different topics changes over time. 17

Results: Sentence topics

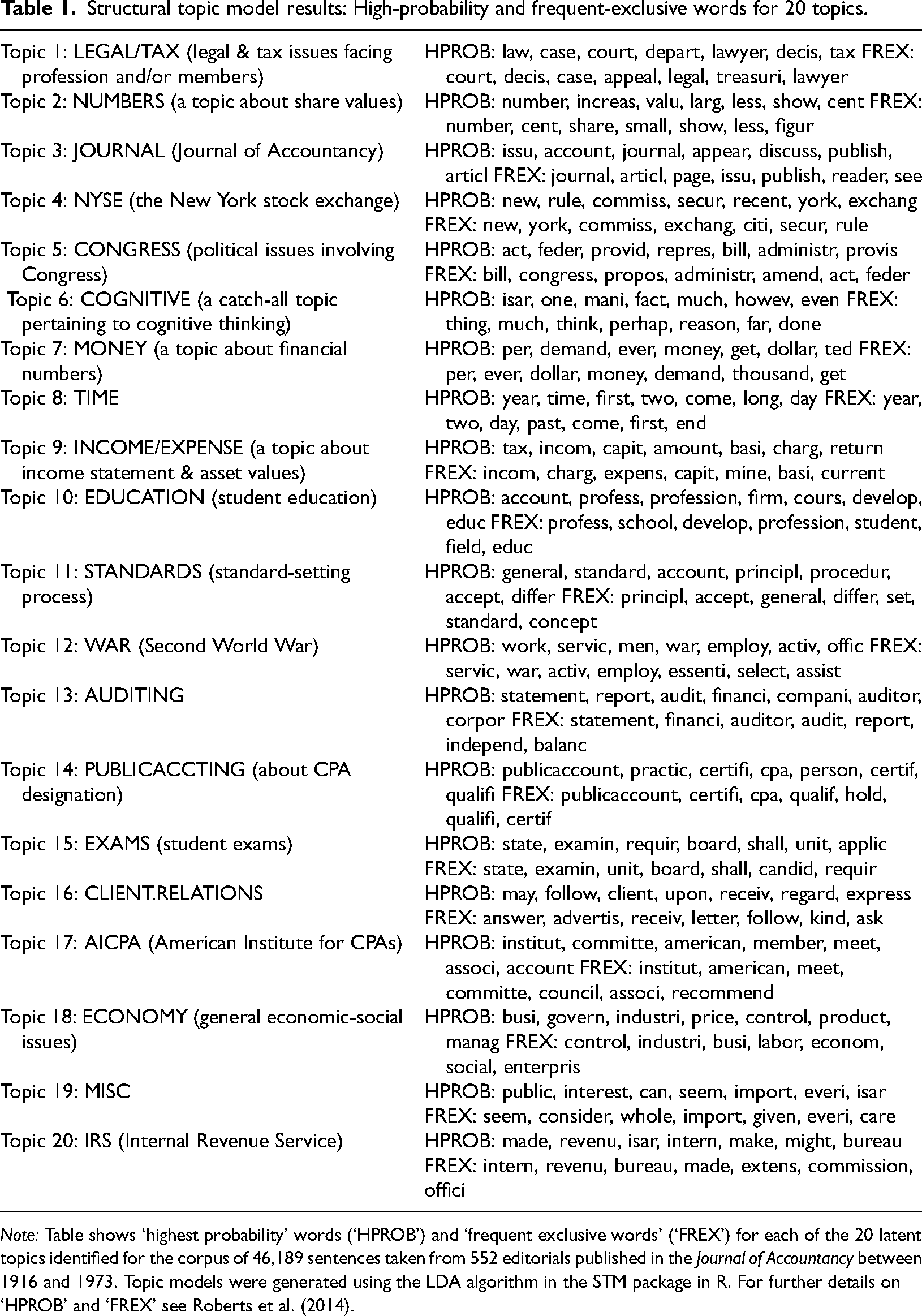

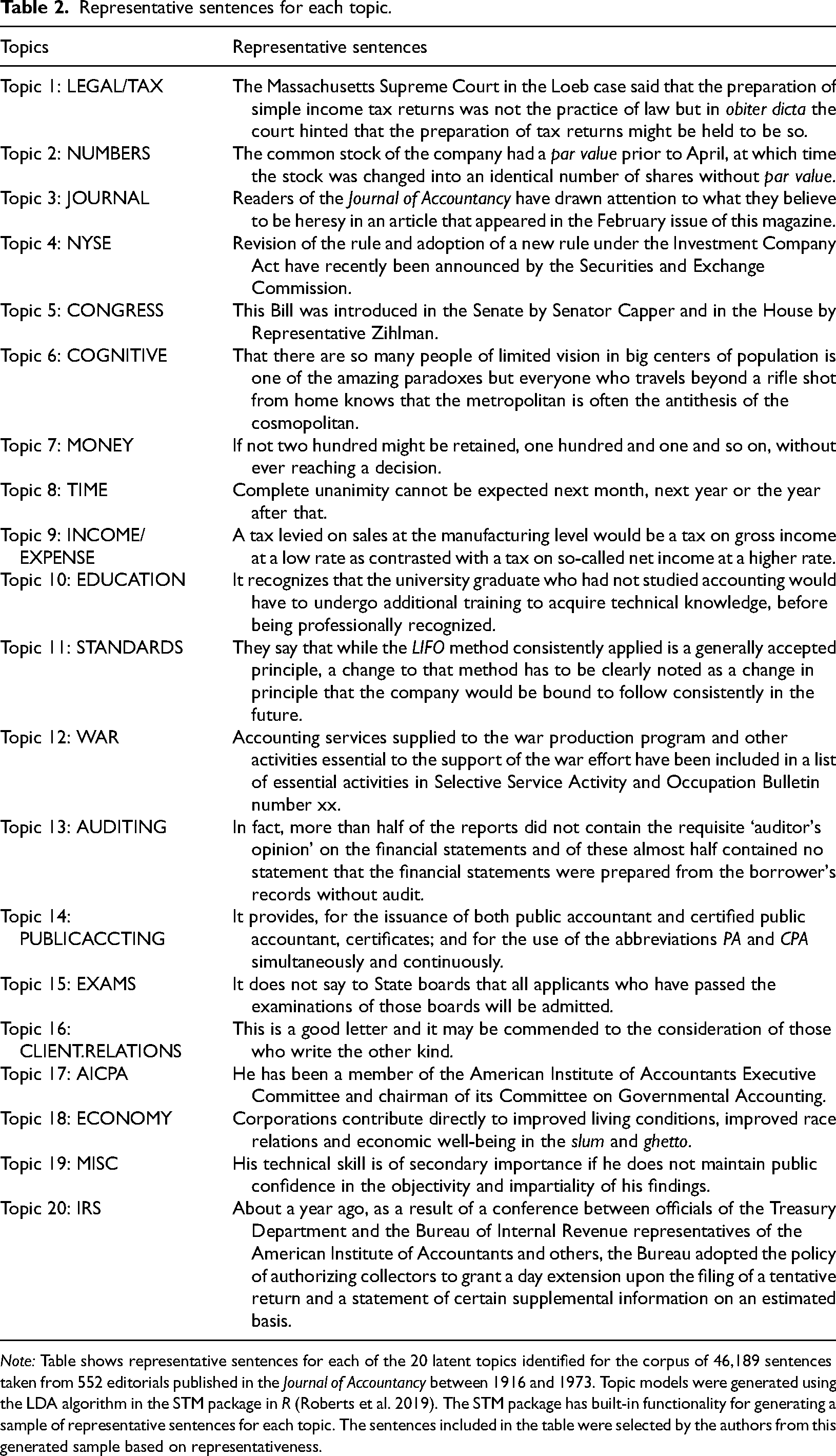

Table 1 reports a combined listing of the ‘frequent and exclusive’ (‘FREX’) and ‘high probability’ (‘HPROB’) words for the 20 topics identified by the topic modelling algorithms, whereas Table 2 provides an illustrative sentence for each topic to help the reader better visualise the microdata. The ‘FREX’ words are those that are frequent and exclusive to specific topics, whereas the ‘HPROB’ words are those that have a high probability of being associated with a topic but that may overlap across different topics (Roberts et al., 2019: 13). A review of the ‘FREX’ and ‘HPROB’ words illustrates how most of the topics were built around the types of subject words and social characters that we discussed in the previous tone from the top section. To help with the interpretation, we label the topics that have an easily identified theme with a single-word descriptor and we also add a short phrase descriptor to give our interpretation as to what the topic is about. This said, it is important to remember that these labels and phrases help with interpretation but they do not fully capture the complexity of the topics contained in the tables.

Structural topic model results: High-probability and frequent-exclusive words for 20 topics.

Note: Table shows ‘highest probability’ words (‘HPROB’) and ‘frequent exclusive words’ (‘FREX’) for each of the 20 latent topics identified for the corpus of 46,189 sentences taken from 552 editorials published in the Journal of Accountancy between 1916 and 1973. Topic models were generated using the LDA algorithm in the STM package in R. For further details on ‘HPROB’ and ‘FREX’ see Roberts et al. (2014).

Representative sentences for each topic.

Note: Table shows representative sentences for each of the 20 latent topics identified for the corpus of 46,189 sentences taken from 552 editorials published in the Journal of Accountancy between 1916 and 1973. Topic models were generated using the LDA algorithm in the STM package in R (Roberts et al. 2019). The STM package has built-in functionality for generating a sample of representative sentences for each topic. The sentences included in the table were selected by the authors from this generated sample based on representativeness.

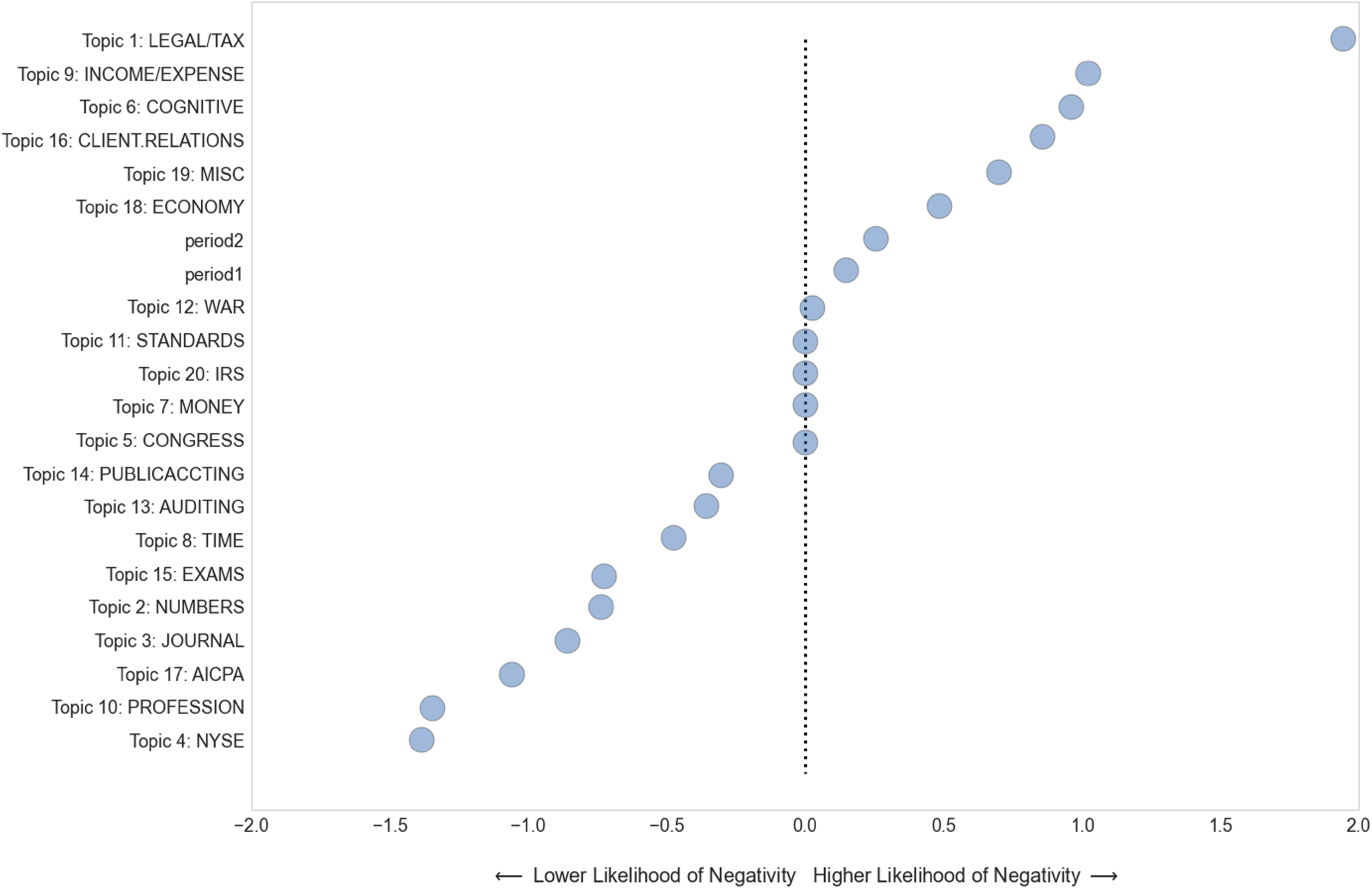

LASSO-based estimates of topical predictors of negativity.

Note: Table 3 shows LASSO-based estimates (L1 regularised regression) of the relationship between Negativity and postwar, and the 20 topics. Because Negativity is a binary dependent variable, our LASSO-based estimates are built on logistic regression. These LASSO estimates help identify the periods and topics most closely related to our Negativity variable. Topics 5, 7, 11, and 20 do not predict Negativity and thus do not have a coefficient value.

The identified topics are somewhat consistent with prior qualitative research (see Abbott, 1983; Preston et al., 1995; Roberts, 2010). For example, there is a group of topics that talk about external social characters/institutions and the relationship of these social actors to the profession. This grouping includes the topics ‘LEGAL/TAX,’ ‘NSYE,’ ‘CONGRESS,’ ‘IRS,’ and ‘CLIENT.RELATIONS.’ There is another grouping that speaks about more technical accounting topics such as ‘INCOME/EXPENSE,’ ‘STANDARDS,’ and ‘AUDITING.’ Finally, there is a grouping that is focused on internal aspects of the profession such as ‘EDUCATION,’ ‘EXAMS,’ ‘PUBLICACCTING,’ and the ‘AICPA.’ As the sentences included in Table 2 illustrate, each of these topics talks about slightly different aspects of professional accounting work.

The results reported in Table 1 and Table 2 appear unsurprising. For example, previous research on the professions has proposed that professional work involves balancing both internal social relationships among members (Van Hoy, 1993) and external social relationships with relevant publics (Puxty et al., 1987): what we, following from Klegon (1978), referred to as the internal and external dynamics of the profession. Similarly, prior historical research on different accounting associations has foregrounded the salience of specific social relationships and provided a qualitative analysis of the dynamics of these relationships (Hanlon, 1994; Preston et al., 1995).

A key premise of the current study is that the identification of sentence-level discursive topics and the prevalence of the different topics contribute to our understanding. The qualitative studies noted above provide us with a ‘warm’ narrative about professional accounting associations. These studies intertwine theoretically informed analysis and the selection of quotes to illustrate analytical points with the objective of helping us to understand both the topics of professional discourse and the dynamics of accounting associations. This said, these interpretations cannot capture and represent the aggregate discursive structure of accounting association utterances since, in the absence of computer-assisted methods such as topic modelling techniques, it is almost impossible to identify both the discursive topics contained within over 46,000 sentences and the prevalence of these topics. For these reasons, we propose that a ‘warm’ qualitative analysis is not a substitute for a ‘cold’ computer-assisted analysis.

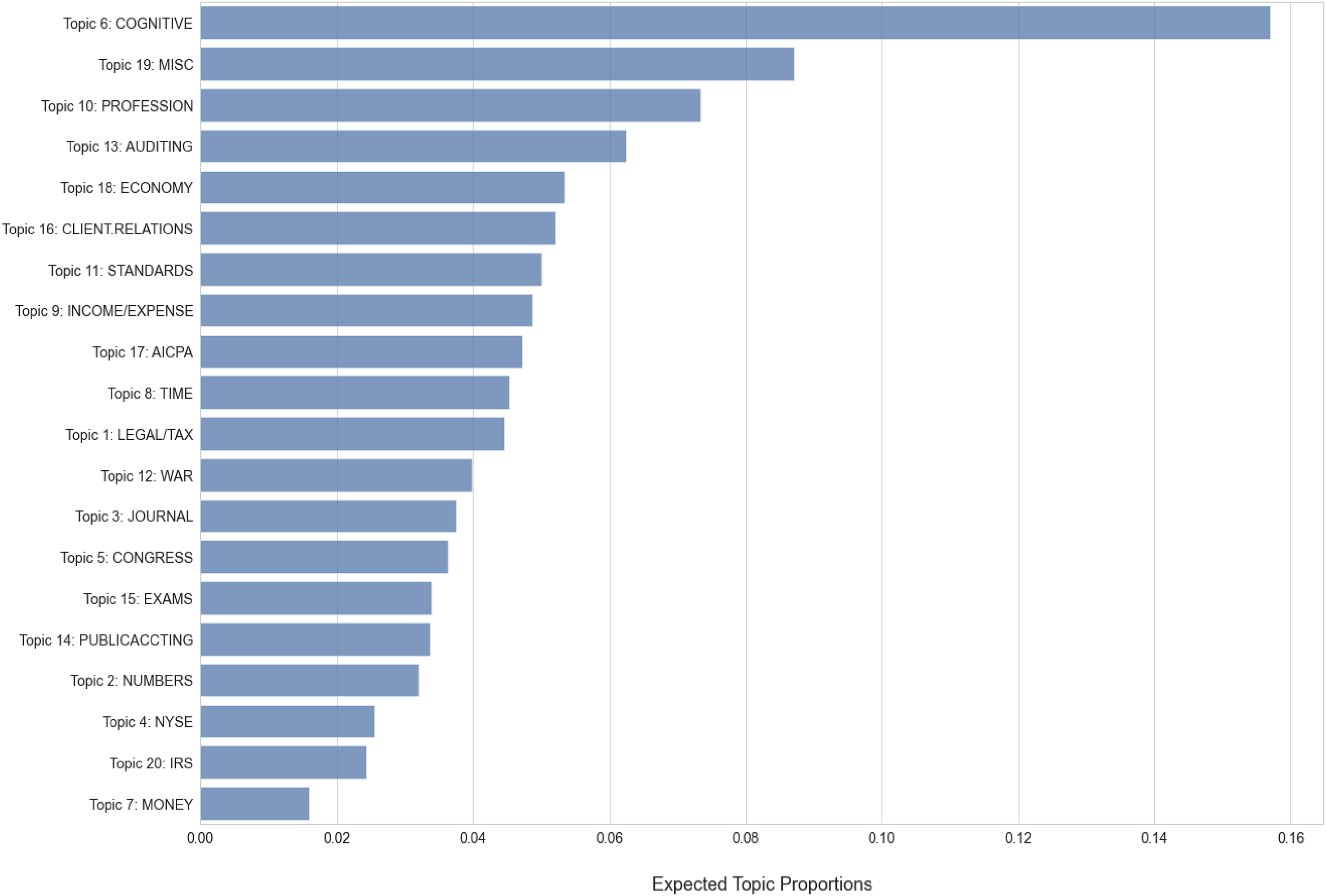

Figure 1 illustrates the rank-ordered prevalence of the topics identified via topic modelling. These prevalence numbers indicate which topics were more pervasive—such as ‘EDUCATION,’ ‘AUDITING,’ ‘ECONOMY,’ and ‘CLIENT.RELATIONS’—and those which were less pervasive such as ‘NYSE,’ ‘MONEY’ and ‘IRS.’ In doing so, Figure 1 provides us with an aggregate-level listing of what the AICPA editorials talked about.

Topic frequency in Journal of Accountancy editorials.

Although we think that the results contribute to our understanding, this cold reading can be complemented with a slightly warmer reading. For example, the prevalence numbers—when juxtaposed with the ‘FREX’ topic words reported in Table 1 and the illustrative sentences reported in Table 2—provide some tentative insights into the thematic content of AICPA discourse. For example, the two most prevalent topics (‘MISC’ and ‘COGNITIVE’) are rhetorical rather than subject-specific topics in that they include words that are used to articulate a point of view and develop an argument (i.e. seem, consider, think, perhaps). The next most frequent topics include ‘EDUCATION,’ ‘AUDITING,’ ‘ECONOMY,’ and ‘CLIENT.RELATIONS.’ The ‘AUDITING’ and ‘CLIENT.RELATIONS’ topics appear to be about the quotidian day-to-day activities and interactions that CPA members deal with regularly. In contrast, the pervasiveness of ‘EDUCATION’ utterances seems to be less about day-to-day accounting practice and more about the AICPA trying to work out the role of education within the profession. Finally, the ‘ECONOMY’ topic appears to be more outward looking and more focused on general philosophical questions about business and society. In sum, the combining of the prevalence numbers with the illustrative sentences provides us with an aggregate-level, yet somewhat specific understanding of the sentence-level utterances contained in the editorials.

As mentioned previously, a topic modelling approach also allows us to compare results across institutional contexts. For example, the identified topics overlap with but are also different from the topics identified by Neu et al. (2021) in their study of the communication activities of the Canadian Institute of Chartered Accountants (CICA) over the 1912–2010 period. The two sets of results overlapped in terms of some of the identified topics: specifically, topics about the legal and tax systems, the economy, financial statement items such as assets, revenue and expenses, exams, and the professional journal itself. At the same time, there were differences in some of the topics as well as the prevalence of the different topics. A comparison of the results highlights that the AICPA and CICA communicated similar yet different messages to their audiences. This said, we are unsure whether these differences reflect differences in the external and internal dynamics of these two professional groups or whether the differences simply reflect idiosyncrasies within the modes of communication. Furthermore, we are unsure why the AICPA decided to stop publishing editorials in 1973 whereas the CICA continued, after 1973, to publish editorials.

In summary, the findings contribute to our understanding of AICPA communication activities in three ways. First, they complement the results of previous narrative-style qualitative research by providing a complete enumeration of the sentence-level thematic utterances contained in the Journal of Accountancy editorials. Second, the combining of prevalence statistics with illustrative sentences foregrounds the types of topics that the editorials talked about. Finally, the findings suggest that these editorial utterances are similar yet slightly different from the results reported by Neu et al. (2021) within the Canadian context.

Results: The tone of sentences

Table 3 and Figure 2 provide the topic-LASSO results for the association between Negativity (our measure of tone) and the individual topics. Consistent with our theoretical framing, the tone expressed in sentence-level data is patterned. More specifically, 17 of 20 topics were associated with a distinct tone, with eight of the topics more likely to express a negative tone and nine topics more likely to express a nonnegative tone. These findings draw attention to how it is possible, via the combination of different sentence-level enunciations, to construct an editorial-level narrative that is both tonally variable yet unambiguous in its story line.

LASSO-based estimates of topical predictors of negativity.

The aggregate level results reported in Table 3 and Figure 2 provide the cold numbers in terms of the tonal variations but do not, by themselves, provide us with an interpretational starting point for understanding the variations in tone. To help us visualise the micro data, we selected a series of illustrative sentences for the topics that had the strongest negative tone (‘LEGAL/TAX,’ ‘INCOME/EXPENSE,’ and ‘CLIENT.RELATIONS’) as well as for several of the topics that had the strongest nonnegative tone (‘EDUCATION’ and ‘NYSE’). We selected these sentences by rank ordering the sentences by their nonindicator variable negativity score and then reviewing the rank-ordered results. 18

The illustrative sentences for ‘LEGAL/TAX,’ ‘INCOME/EXPENSE’ and ‘CLIENT.RELATIONS’ are quite consistent with our preconceptions regarding the expression of an editorial opinion. For example, the ‘LEGAL/TAX’ sentences include: ‘always there will be a portion of our tax burden imposed because of incompetence or willful wrong-doing’ and ‘unfair laws and restrictions and excessive taxes will defeat their own purpose.’ Similarly, the ‘INCOME/EXPENSE’ sentences opine that ‘this would impose on business as a whole a burden of expense both intolerable and unnecessary’ and ‘numerous alleged deficiencies were cited such as the absence of income statements and failure to reveal sales and cost of goods sold.’ Sentences about ‘CLIENT.RELATIONS’ were also negative. For example, one sentence notes that ‘the procedures will eventually embarrass both his client and himself,’ whereas another comments that ‘it is doubtful if a client who would wish to amend a report for publication would be hindered by such a threat.’ Interestingly, most of these illustrative sentences were forward looking in that they used the verbs ‘would be’ and ‘will’ to opine about what will happen in the future if a certain course of action is taken.

In contrast, the nonnegative sentences for the ‘NYSE’ and ‘EDUCATION’ are also evaluative but these sentences do not express a negative tone. The ‘NYSE’ sentence states that the ‘sale of securities is the thing for which the exchange exists,’ whereas the ‘EDUCATION’ sentence notes that ‘he did more to raise the standards of accounting education and to stimulate the highest professional ethics.’ These two sentences are also different from the previous negative-toned sentences in that they use verbs that are backward/present-looking rather than forward-looking verbs such as ‘will’ and ‘would.’

The results contribute to our understanding of AICPA communication activities in two ways. First, they illustrate the aggregate-level patterns in tone: more specifically how the tone expressed in individual sentences is associated with the topic of the sentence. Second, the findings highlight that topics about the internal aspects of the profession tend to be associated with a nonnegative tone, whereas sentences pertaining to the external professional dynamic tend to express a negative tone. This result is most pronounced for topics pertaining to the profession itself compared to external social characters/institutions and external events. For example, the topics ‘EDUCATION,’ ‘AUDITING,’ ‘AICPA,’ ‘JOURNAL,’ and ‘EXAMS’ were associated with the expression of a non-negative tone. In contrast, the topics ‘LEGAL/TAX,’ ‘CLIENTS,’ ‘ECONOMY,’ ‘WAR,’ and ‘CONGRESS’ were associated with a negative tone. This said, not all topics—see ‘NYSE’ and ‘INCOME/EXPENSE’—fall neatly into this categorization.

Temporal dimensions

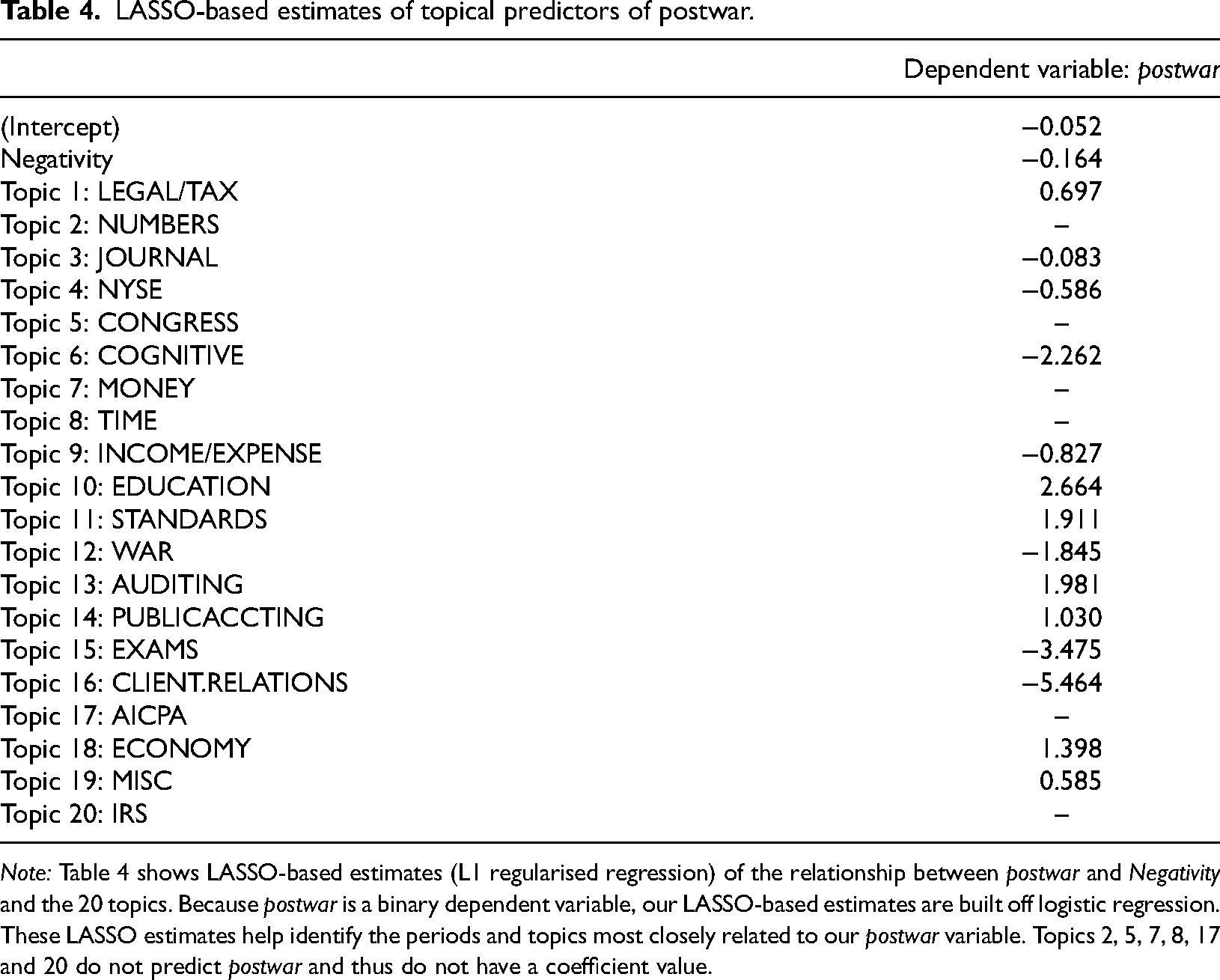

To help us to understand the temporal dimensions of sentence-level utterances, Table 4 reorders the sentence-level data and uses the temporal variable postwar as the dependent variable and the negativity variable and the topic variables as independent variables. This reordering foregrounds the temporal aspects of sentence construction.

LASSO-based estimates of topical predictors of postwar.

Note: Table 4 shows LASSO-based estimates (L1 regularised regression) of the relationship between postwar and Negativity and the 20 topics. Because postwar is a binary dependent variable, our LASSO-based estimates are built off logistic regression. These LASSO estimates help identify the periods and topics most closely related to our postwar variable. Topics 2, 5, 7, 8, 17 and 20 do not predict postwar and thus do not have a coefficient value.

The results reported in Table 4 illustrate two aspects of sentence-level utterances. First, the tone of the sentences changes over time, with sentences becoming less negative. Second, it appears that sentences about the accounting profession as we currently know it are become more prevalent. For example, sentences about ‘EDUCATION,’ ‘STANDARDS,’ ‘AUDITING,’ and ‘PUBLICACCTING’ are more pervasive while sentences about the ‘JOURNAL’ and specific, concrete topics such as ‘INCOME/EXPENSE’ and ‘EXAMS’ are less pervasive. At the same time, topics about the external dynamic of the profession (‘LEGAL/TAX’ and ‘ECONOMY’) also become more prevalent in the postwar period. Although the above interpretation is mostly speculative about why these changes occurred, we can conclude from the temporal data that the prevalence of sentences about specific topics did change in the postwar period as did the amount of negativity being expressed in the sentences. We return to these findings and to the need for additional research regarding these changes in the discussion section that follows.

Discussion and conclusions

The current study has focused on sentence-level editorial AICPA communication within the Journal of Accountancy. We proposed that sentence-level enunciations are the base-level building blocks for constructing more aggregate-level professional narratives. Sentences allow the editorialist to express different sentiments or tones about specific social characters, institutions, practices and events which, in turn, aggregate into a tonally variable and nuanced yet unambiguous editorial. The provided topic modelling and LASSO regression results for the 46,189 sentences contained in the editorials for the 1916–1973 period are consistent with this perspective.

More specifically, the study provides three groups of findings. First, the study shows that a significant portion of editorializing focused on the topics of ‘EDUCATION,’ ‘AUDITING,’ ‘ECONOMY,’ and ‘CLIENT.RELATIONS,’ whereas the ‘NYSE,’ ‘MONEY,’ and ‘IRS’ were the least prevalent topics. Second, editorial sentences were more likely to use a negative tone when speaking about ‘LEGAL/TAX,’ ‘INCOME/EXPENSE,’ and ‘CLIENT.RELATIONS’ compared to ‘EDUCATION’ and the ‘NYSE.’ As the illustrative sentences suggest, negative-toned sentences appear to be more likely to speak about future consequences of some action and to use forward-looking verbs such as ‘will’ and ‘would be’ compared to non-negative-toned sentences. Finally, both the overall tone and the prevalence of certain topics within the editorial sentences change over time, with sentences becoming less negative and with sentences about ‘EDUCATION,’ ‘STANDARDS,’ ‘AUDITING,’ ‘PUBLICACCTING,’ ‘LEGAL/TAX,’ and ‘ECONOMY’ becoming more pervasive.

The aforementioned findings make two primary contributions to our understanding of professional accounting associations. First, the study complements and extends prior qualitative research on the AICPA and accounting associations more generally by using a topic modelling approach to enumerate a listing of the sentence-level topics that the AICPA discussed. Prior research on American accounting firms and the AICPA itself (Preston et al., 1995; Roberts, 2010) foregrounds the importance of examining professional accounting association communications and highlights some of the key topics that professional accounting associations talk about. The current study complements and extends this research by examining a specific communication medium (editorials published in the Journal of Accountancy) and by providing a more complete listing of the topics discussed. As mentioned previously, topic modelling approaches not only identify the topics contained within the corpus but also indicate the prevalence of these topics.

Second, the study highlights the importance of considering the tone from the top: more specifically, how editorial sentences used different tones when talking about different social characters, institutions, practices, and events. We proposed that the use of tonally infused sentences allows the editorialist to construct aggregate-level editorials that are tonally variable yet unambiguous narratives about professional work. More specifically, the results illustrate that subjects of professional accounting association discourse are both infused with tone and tonally variable. This finding extends prior qualitative research on the AICPA and other accounting associations.

Clearly, these contributions are inseparable from our use of computerised textual analysis methods. Like prior research on accounting disclosures (see Gandhi et al., 2019; Huang et al., 2014; Loughran and McDonald, 2011, 2016), our use of computerised textual analysis methods allowed us to examine a large-scale corpus of textual accounting materials in ways that are simply not possible with more qualitative methods. These methods allowed us to partition the 552 editorials into over 46,000 sentences. We did not have to reduce the amount and complexity of the data by selecting two data end points (Preston et al., 1995) nor were we faced with what DiMaggio et al. (2013) refer to as a ‘heroic’ interpretational task involving the iterative interpretation and reinterpretation of large amounts of textual data. Furthermore, the computer-assisted textual analysis methods made it possible to increase the complexity of the data by partitioning the editorials into sentence-level components. This partitioning, in turn, showed how sentences used different tones depending on the sentence topic. In these ways, our use of computerised textual analysis methods made possible types of aggregate-level and microlevel analyses that would have been almost logistically impossible otherwise. These analyses, in turn, contributed to our understanding of professional accounting associations by, first, identifying the topics that professional accounting associations talk about, and second, illustrating the tonal variability across topics.

We have emphasised throughout the study that computerised textual analysis methods complement and extend, but do not replace, traditional forms of qualitative-based historical research involving the use of archival and oral history methods. Computer-assisted textual analysis methods both provide a cold reading of the aggregate data and facilitate a slightly warmer interpretative understanding of the aggregate discursive structure of the textual materials. At the same time, this approach does not have the warmth of qualitative, interpretive analyses. Furthermore, the current study does not stand by itself but rather starts from the prior qualitative research of Preston et al. (1995), Fogarty et al. (2006), Merino and Mayper (1993, 2001) and Roberts (2010) on the American accounting profession. The extension, in this case, primarily relates to enumerating a list of narrative topics and analysis of how individual sentences express different sentiments about different topics. Our mode of analysis, like previous research on the tone of accounting communication, assumes that word list approaches to measuring tone provide an imprecise yet useful way of identifying sentiment: an approach that harnesses the power of ‘big data’ to overcome the noisy-ness of the measures (Loughran and McDonald, 2016: 6). The current study does exactly this, showing how Loughran and McDonald's (2016) financial negativity measure varies depending on the sentence topic. At the same time, the topic modelling approach that we use as well as the noisy-ness of the negativity measure and the aggregate nature of the topic-LASSO analysis results in a situation where our data/method combination highlights relationships and flags potential anomalies but does not allow us to adequately explain why we observe the patterns that we do. For this reason, there is still much that we do not understand about AICPA editorial communications – aspects of AICPA communication that deserve further research attention.

One of the issues that merit additional research is the changes over time in the prevalence of different topics within editorial communications. For example, the temporal results presented in Table 4 draw attention to how the prevalence of different topics changed in the postwar period. We suggested that these changes could be a movement toward a view of the American public accounting profession that is more consistent with our current-day vision of professional accounting work. This said, our aggregate-level approach to the patterns within the aggregate-level data can be, at best, speculative because it is almost impossible for us to provide a deep reading of these patterns. For these reasons, we think that additional qualitative research similar to Preston et al. (1995) and Roberts (2010) would help us to better understand the shifting understandings of the accounting profession and professional work that are implicit within AICPA editorial communications.

The above suggestion regarding issues that merit further research draws attention to the ways that computer-assisted historical research can work together with traditional historical methods to increase our understanding. More specifically, we believe that iterative qualitative–quantitative–qualitative sequences of investigation—investigations that move across levels and methods of analysis—will extend and challenge our understanding of accounting. This vantage point does not assume that qualitative research, nor quantitative research, are junior partners in this endeavor. Rather, it is the complexity of historical accounting data combined with the importance of a better understanding of accounting processes that makes it necessary for us to use all of the research methods that we have at our disposal.

Footnotes

Author's note

Abu Rahaman is also affiliated at Schulich School of Business, York University, Canada.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was funded by University of Calgary Haskayne: Research grant number RT758558. University of Calgary Haskayne Research Grant, (grant number RT758558).