Abstract

This study uses computerised textual analysis methods to examine 1,769 letters to the editor published in the Journal of Accountancy between 1951 and 2020. Arguing that these letters enunciate an evaluative and expressive stance about issues affecting the profession, we first map the social characters, concepts, and subjects that letter writers talk about. Second, we build on this initial mapping by identifying the discursive communities that are present within the letters and the positioning of ethical words vis-à-vis these communities. Third, we consider the moment(s) in the letter when ethical words are enlisted. The study contributes to our understanding of professional accounting by foregrounding how letter writers articulate their vision of accounting work. The study also demonstrates the usefulness of computerised textual analysis methods for studying historical accounting textual materials.

Keywords

This study examines the viewpoints expressed by CPA (certified public accountant) practitioners in 1,769 letters to the editor that were published in the Journal of Accountancy between 1951 and 2020. Starting from previous research on the public accounting profession (Preston et al., 1997; Roberts, 2010), Bakhtinian-inspired linguistics research on speech communication (Bakhtin, 2013), and ethics-focused research (Preuss and Dawson, 2009), we propose that letters to the editor enunciate an evaluative stance about something important that is happening within the profession. Letters to the editor enlist subject words, social character words and concept words to articulate a viewpoint about accounting work, a viewpoint that is sometimes made denotatively explicit by including specific ethical concept words such as ethics, duty, integrity, and fairness. The provided analysis enlists a series of computerised textual methods to examine the letters to the editor and the ethical stance of the viewpoints expressed within these letters. In turn, the research findings illustrate the topics and social characters that CPA practitioners talk about in their letters to the editor as well as the moments when letters become explicitly about ethics via the invocation of ethical concept words.

The starting premise for the current study is that computerised textual analysis methods allow us to analyse textual materials, such as the letters sent to the editors of the Journal of Accountancy, in ways that are simply not possible with more traditional qualitative methods. As we demonstrate in the analyses that follow, computerised textual analysis not only identifies the topics, social characters and concepts that letter writers were most likely to talk about but also maps the aggregate discursive structure – including the centrality of different social characters and concepts – within the conversation stream. Furthermore, computerised textual analysis facilitates the examination of the micro intra-textual word choice strategies that are used to construct accounting narratives. For example, in the current study, we demonstrate how letter writers are more likely to invoke denotatively explicit ethical concept words when speaking about certain topics and social characters. Similarly, we show the expressive patterns of speaking that are present within the letters; more specifically, that denotatively explicit letters are more likely to include negative sentiment words compared to other normative utterances. These insights complement and extend the findings of previous research on the American accounting profession (Preston et al., 1997; Roberts, 2010).

The study contributes to our understanding of professional accounting associations. More specifically, the study focuses on the ways that letter writers articulate their vision of accounting work and the ethical stances that are invoked in these letters. The AICPA (American Institute of Certified Public Accountants) is one of the largest and most influential public accounting associations in the world, with more than 400,000 members. Previous research has tended to focus on the activities and public communications of the AICPA and how activities such as the publication of ethical codes (Armitage and Moriarity, 2016), education requirements (Mathews, 1994), and disciplinary processes (Jenkins et al., 2018) help to ensure that practitioners provide technically competent and ethical service as well as how public communications, such as those contained in the Journal of Accountancy, provide ethical guidance to the membership (Neu and Saxton, 2022). This prior research is invaluable in that it helps us to understand how professional associations such as the AICPA attempt to produce an ethical practitioner. At the same time, it is individual students-in-training and CPAs who practice public accounting and who must figure out ways to satisfy the demands of clients while simultaneously behaving in an ethically appropriate manner. The letters to the editor published in the Journal of Accountancy provide us with a unique window into the client-oriented, yet ethical, world of these practitioners and the normative and ethical stances that underpin their view of accounting work.

Following this introduction, the next section discusses the activities that the AICPA uses to attempt to produce ethical practitioners, and the following sections draw upon prior research to outline how letters to the editor are an evaluative, albeit curated, response to what is happening within the accounting profession. Subsequent sections describe the data and methods as well as provide our analysis. The discussion section summarises the contribution that the study makes to our understanding of professional accounting association processes.

Producing the ethical practitioner

The AICPA is a national-level organisation that began as the American Association of Public Accountants (AAPA) in 1887. Subsequent iterations of the AAPA emerged via merger, culminating in the creation of the American Institute of Accountants (AIA) in 1936. At that time, the AIA chose to restrict future memberships to CPAs and the AICPA name was later adopted in 1957. Although the AICPA is the national face of the profession, it is state governments that determine CPA license requirements and sanction CPAs for ethical violations through their state boards of accountancy. While there is no requirement to be a member of the AICPA or a state CPA society to hold a CPA license, ‘many certified public accountants choose to belong to the AICPA because of its leading role in the profession’ (Jenkins et al., 2018: 526). Throughout its existence, ‘one of the most important concerns of the Institute has been to maintain its professionalism through the establishment of high ethical standards’ (Edwards, 1987: 2). The AICPA maintains the only Code of Professional Conduct (CPC) ‘that applies to professionals at the national level’ (Jenkins et al., 2018: 527): a code that has been in existence since 1917 and has been updated periodically (Armitage and Moriarity, 2016: 3).

Like other professional associations, the AICPA and state-level associations occupy a delicate position between the members that it ostensibly represents and the governments that grant it a quasi-monopoly over certain types of ‘professional’ work (Puxty et al., 1987; Richardson, 1989). On the one hand, professional accounting associations must produce a technically competent and ethical professional: a practitioner who has a minimum level of technical expertise and ethical standards (Larson, 1977, 2018). On the other hand, it must also represent the interests of its geographically dispersed and somewhat heterogeneous membership (Van Hoy, 1993). This balancing act requires the professional associations to arrange the conduct of their membership (cf. Preston et al., 1997) in ways that do not appear overly heavy-handed and that do not appear to privilege the interests of one group of CPAs over another. When successful, it is assumed that this balancing decreases the probability of financial failures by encouraging members to avoid privileging commercial interests over public interests (Jenkins et al., 2018). In turn, decreased financial failures reduce the perceived need for increased government regulation.

A review of prior research suggests that, over its 136-year history, the AICPA has relied upon education (Alford et al., 1990; Martinov-Bennie and Mladenovic, 2015; Misiewicz, 2007) and communicative activities (Neu, 2001; Neu and Saxton, 2022; Roberts, 2010) to supplement the rules for professional conduct and to encourage the production of technically competent, ethical practitioners. Education standards, for example, provide the AICPA with a way of ensuring a consistent level of technical and ethical expertise, 1 whereas member-directed communication mediums like the Journal of Accountancy provide the AICPA with a softer mechanism to encourage technical competence and ethical behaviour. Roberts (2010), for example, illustrates how editorials in the Journal of Accountancy complement and supplement the rules for professional conduct, while Neu and Saxton (2022) show how Journal of Accountancy editorials allow the AICPA to provide different types of (ethical) guidance to different internal audiences such as partners and students. These different groups of AICPA activities contribute to the production of technically and ethically competent accounting practitioners.

The 1951–2010 period

Despite the AICPA's best efforts at socialisation and governance, the production of technically competent, ethical practitioners is never completely successful in encouraging appropriate on-the-ground behaviour nor in avoiding financial failures. For example, the 1951–2010 period that we consider saw numerous changes within the CPA profession as well as a series of jurisdictional challenges; challenges that called into question the CPA's jurisdiction and mandate. Although an in-depth analysis of these changes and challenges is beyond the scope of the current study, we draw attention to four changes that occurred during this period as a way of contextualising the study.

First, the emergence of new technologies as well as new sites of accounting-related work changed the nature of the CPA profession. A series of retrospective articles in the Journal of Accountancy to celebrate the centenary of the journal in 2005 asked some of the previous editors to reflect on their time at the helm (Katz, 2005; Shildneck, 2005). Lee Berton (1975–1983) noted that ‘technology was becoming an important issue’ and that Arthur Andersen was already selling other services such as management advisory services (Katz, 2005). A subsequent editor, Colleen Katz (1988–2007), commented that ‘CPAs became more attuned to marketing’ and that this, during her tenure, became a common part of management practice. The selling of management advisory services, the use of technology, and the marketing of professional services were salient aspects of the context during the period that we studied.

Second, new modes of regulation and standardisation also appeared. The emergence of FASB in 1973 was one of these changes, with FASB taking over some of the thought leadership that previously resided with the AICPA's Accounting Principles Board (APB) (Zeff, 2016). 2 During the 1960s, the APB ‘became caught up in problems arising from new kinds of business transactions and new accounting practices’ and was criticised for ‘its inability as a part-time, volunteer body, to act quickly enough to keep up with developments in the marketplace’, with these concerns ultimately leading to the formation of a new independent standard-setting structure of which FASB is the most visible (Tucker, 2002: 1025). In addition to FASB, another editor, Barbara J. Shildneck (1983–1987), recalled that international accounting standards emerged during her tenure; however, there was a tension within the AICPA as well as within its membership between the global push for international standards and the local. She quoted a comment from the previous editor, Lee Berton, that ‘international issues are important at many levels, but here at home, many small firm clients are the corner auto dealers. They don’t rely on complicated financial reports. They need a CPA to act as a business doctor to help them’.

Third, a combination of financial failures and government commissions gave rise to the notion of an expectations gap: that is, the difference between ‘what public and other financial statement users perceive auditors’ responsibilities’ to be and ‘what auditors believe their responsibilities entail’ (McEnroe and Martens, 2001: 345). While the notion of an expectations gap may have first occurred during the 1930s, a series of highly publicised public inquiries involving Senator Lee Metcalf (1970s), Representative John Moss (1970s), Representative John Dingell (1980s and 1990s), and the U.S. General Accounting Office (GAO) (1990s) brought this perceived gap to the fore (McEnroe and Martens, 2001: 346). Indeed, all the editors who were interviewed in the centenary article noted that concerns about the expectations gap had been a long-standing issue dating back to at least the early 1970s and that ‘people are always expecting accountants to uncover what could be so well-hidden it's undiscoverable’.

Finally, the above contextual changes and challenges were accompanied by changing educational requirements, including minimum educational requirements, continuing education, and a state-specific comprehensive CPA exam. Edwards, for example, notes that ‘since the 1950s the AICPA has advocated a postgraduate accounting education as a requirement to become a member of the Institute’ (1987: 6) and, in 1988 after more than 40 years of advocacy, ‘the AICPA proposed an increase in the hours of study from 120 to 150’ (Mathews, 1994: 143). 3 Similarly, all CPA candidates are tested on technical aspects of accounting practice (Williams and Elson, 2010) and most are tested on ethics, sitting both the CPA Exam and, in the majority of jurisdictions, the AICPA Ethics Exam. 4 As Persson et al. (2018: 84) note, many of these educational changes came from the AICPA membership in that these ideas originated from their members and were established after the recommendation of committee work that laid out the rationale for their importance.

These changes and challenges are part of the context for the current study, impacting both AICPA attempts to produce technically competent and ethical practitioners as well as the responses by practitioners to what is happening around them. More specifically, we propose it is this amalgam of AICPA activities and external events that have the potential to trigger a letter to the editor from individual practitioners about what is happening in the profession. The next section considers these letters in more detail.

Letters to the editor

A formal letters to the editor section first appeared in the Journal of Accountancy in 1951. Prior to this time, the journal sporadically published letters within an ad hoc correspondence section or within the appendices. However, in 1951, the journal started to include a letters to the editor section and to index this section in the table of contents. Since 1951, there have been nine different editors, who we assume were responsible for handling and making editorial decisions on the letters section: John L. Carey (1937–54), John L. Lawler (1954–56), Charles E. Noyes (1956–66), William O. Doherty (1966–75), Lee Berton (1975–83), Barbara J. Shildneck (1983–87), Colleen Katz (1988–2007), Joanne Fiore (2007–15), and Kim Nilsen (2016–20).

To help us understand the construction and functioning of letters to the editor, we draw upon previous Bakhtinian-inspired linguistic research on written speech communication and other prior research. This research draws attention to four salient aspects of letters to the editor.

First, as mentioned previously, letters to the editor are a discursive response (Bakhtin, 2013: 69) to something important that is happening within the profession: something that someone has said or done. Letters to the editor are incited in that something interrupted the daily work routines of the letter writer and motivated him/her to write to the editor. The letter could be a response to something that the letter writer read in the Journal of Accountancy. Alternatively, it might be a response to a new AICPA initiative and the ways that the initiative will adversely impact certain membership groups. Or it could be triggered by an external actor such as the IRS, the SEC or Sarbanes-Oxley and the ways that these actors and regulations impact/constrain professional practice. Finally, the letter can be a response to the role of CPAs in specific external events like financial failure or fraud. Regardless of the specific trigger, the key point is that letters to the editor are what Bakhtin refers to as ‘discursive answers’ from a current or potential CPA member that are directed to specific audiences such as the AICPA and to other members who potentially might read the letter (cf. Bakhtin, 2013: 95).

Second, letters enlist relevant subject words, social character words and concept words to craft a response. Subject words signal to the reader what the letter is about (cf. Bakhtin, 2013: 60). Subject words are often somewhat field-specific words that refer to a set of practices (e.g., accounting, auditing, consulting, etc.) and can take the form of either a noun or verb. Social character words are nouns that identify the social actors (e.g., accountants, the SEC, FASB, the government etc.) who participate within the field and within the narrative itself (Jones, 2014: 8). Social character words are presumed to be relevant to both the letter writer and to the audiences to which the letter speaks. Finally, concept words are also nouns but denote things that are both less practice-based and more general. Examples of concept words include ethics, independence, democracy and so on. 5 Concept words provide a conceptual frame that helps the reader to move from the specific to the general and to thus understand how the subject matter and the behaviours of the social actors within this specific setting should be interpreted.

Third, the combination of subject, character and concept words communicate an evaluative normative stance, a stance that is made ‘denotatively explicit’ (Briggs and Bauman, 1992: 156) via the inclusion of ethical concept words such as ethics, integrity, duty and fairness. An utterance, according to Bakhtin, is always evaluative (2013: 85) in that it typically conveys – either implicitly or explicitly – a positive or negative appraisal. The inclusion of ethical concept words, however, also explicitly signals that there is an ethical dimension to the subject or social character being discussed: that these words are ‘signs that speakers treat as stance-like’ because they denote that the topic is about the ‘good’ or ‘bad’ (Kockelman, 2012: E107). This ethical dimension often pre-exists within the conversation stream in that certain social characters are assumed to be imbued with ethical characteristics (cf. Winkler, 2011). For example, the previous section noted how AICPA activities and communications often emphasise the importance of ethics, implying that professional practice must be both technically competent and ethical. Similarly, certain topics such as advertising are pre-associated with ethics in that these topics are assumed sometimes to pose ethical dilemmas that must be navigated. The pre-existence of ethical connections to certain social characters and subjects makes it more likely that writers will invoke specific ethical concept words within their letters when talking about these characters and subjects: including when talking about a ‘new’ event such as a financial failure (cf. Neu, 2001; Soltani, 2014). In this regard, letters simultaneously index the social position from which the letter writer speaks (Agha, 2005) and express strong positive or negative sentiments about the social characters that are invoked within the letter (cf. Bakhtin, 2013: 97). In line with research in other contexts (e.g., El Ayadi and Smith, 2008; Schumacher et al., 2012), we believe letter writers in our context particularly like to write about topics that trigger their attention, and these triggers are more likely to elicit a negative response than a neutral or positive response.

Fourth, letters to the editor are simultaneously a discursive response and, as we alluded to above, part of a curated conversation stream within the Journal of Accountancy. Previous research illustrates that magazine and newspaper editors act as gatekeepers who exercise discretion over what gets published within letters to the editor sections (Da Silva, 2012; Wahl-Jorgensen, 2001). Editors follow a series of often informal rules when deciding which letters to publish (Da Silva, 2012: 252). These rules value both controversy and balance as well as originality and conciseness (2012: 259). This prior research also suggests that the decision to publish is sometimes a confirmatory process where editors publish letters that are consistent with the newspaper's viewpoint as well as the editor's personal viewpoint (Gregory and Hutchins, 2004: 194). In this regard, letters do provide insights into how CPAs view what is happening in the profession, but the aggregate letter stream is, itself, mediated by the norms that guide letter selection. As Wahl-Jorgensen (2007: 97) notes, letters are not a perfect representation of public (or membership) opinion, but the individual letters are factually accurate, and the conversation stream itself tends to be balanced in the sense that it represents the different views that are expressed by people submitting letters. 6

Research questions

In the analysis that follows, we use the provided theoretical framing materials to motivate our examination of three aspects of the letter publication process. Research question 1 (RQ1) focuses on the aggregate stream of letters to the editor that have been published since 1951 and examines not only what subject words, social character words and concept words have been central to the conversation but also the discursive communities to which these focal words belong. This first analysis piece shows us both what was incited, and how letter writers make sense of professional work. Research question 2 (RQ2) moves down to the level of the utterance and analyses which subject, character and concept words tend to be accompanied by the word ‘ethics’. The final research question, RQ3, explicitly considers the expressive aspects of letters and examines whether ethical words are more likely to be used within negative sentiment letters. This final research question both shows the amalgam of topics and social characters that letter writers feel strongly about as well as the ways that the enlistment of denotatively explicit ethical concept words contribute to expressive and evaluative utterances. The next section discusses the data and methods that will be used to consider the three research questions.

Data and method

As noted earlier, the corpus of letters to the editor that we analysed was published in the Journal of Accountancy between 1951 and 2020. We selected this time period because it was in 1951 that the journal started to systematically publish letters to the editor and to index the letters in the table of contents. We reviewed the table of contents and then went to the specified pages to download the letters. 7 The final data set consists of 1,769 letters distributed across seven decades. More than 80 per cent of these letters were written by a current CPA or by a student who was working towards their CPA. The letters section sometimes contained a response by the editor or an AICPA or FASB to previously published letters. We did not include these responses in our data since we are interested in letters from current and prospective CPAs designation. Additionally, most letter writers published but a single letter; there were 1641 authors who published one letter. 8

Our theoretical framing suggested that subject words, character words, and concept words are integral to the construction of narratives. To identify the relevant words, we used the text processing module in R to generate a document-term matrix that consists of all the unstemmed words in the corpus. We then generated a frequency listing of all the words, from which we identified words of interest, including phrases such as ‘management advisory services’ that the context section suggested might be important. In this process of identification, we combined singular and plural word forms (e.g., our term clients captures instances of both ‘client’ and ‘clients’) as well as words with the same root (e.g., our term independence captures instances of both ‘independent’ and ‘independence’). 9 We also aggregated a small number of words that we thought had the same meaning into an aggregate ethics term consisting of ethics, ethical, unethical, moral, morality, integrity, objective, objectivity, fair and fairness. While we think that this inclusive measure of denotatively explicit ethics is appropriate, we also ran the regression reported later using a narrow measure of denotatively explicit ‘ethics’ and the results were similar. In short, our theoretically guided process led us to identify an aggregate term for ethics and focal subject words, character words, and concept words. Our analyses use indicator variables for the dependent variable and independent variables, with the exception of the negativity measure. 10

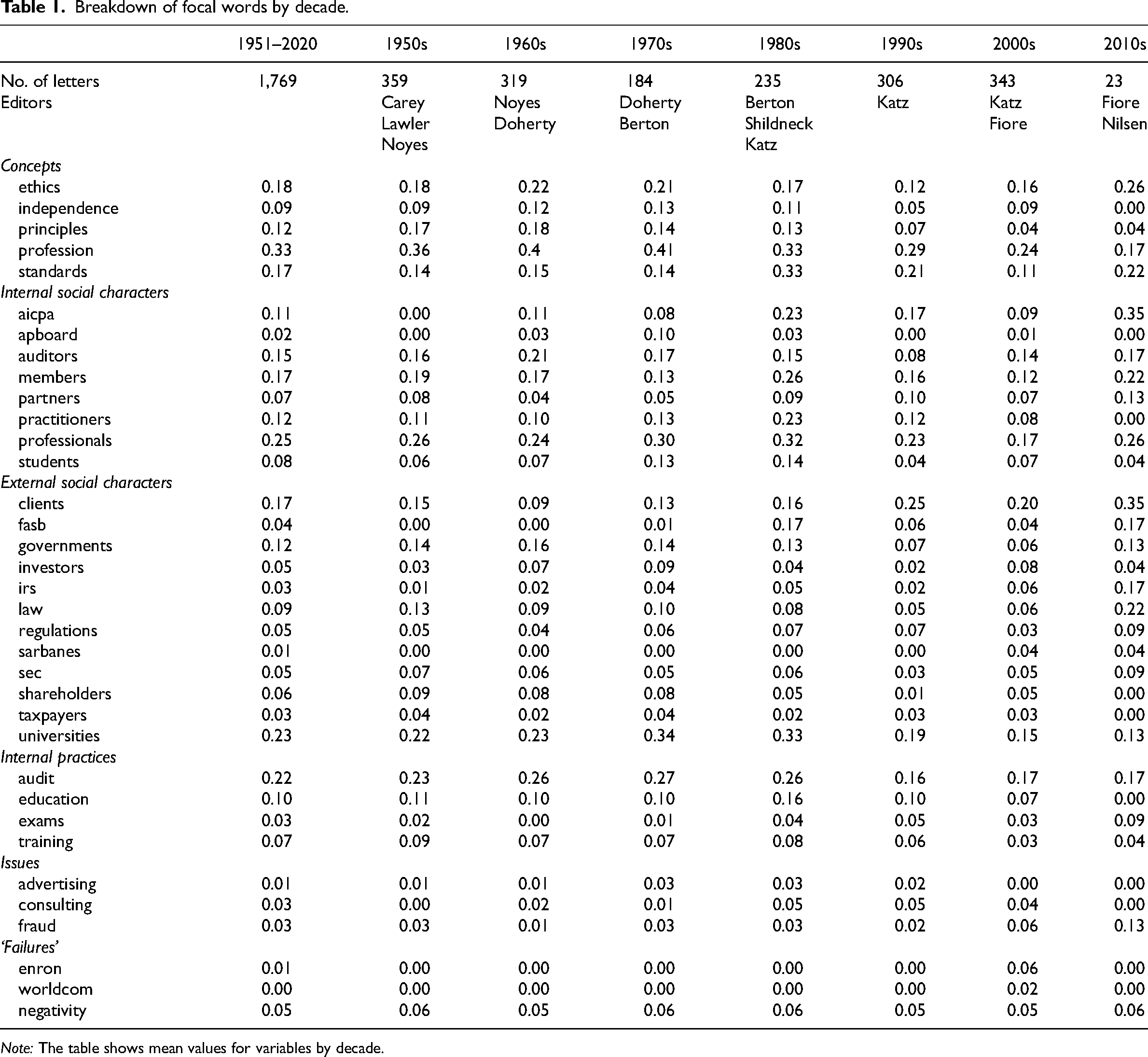

Table 1 provides summary information on the focal key words. Included in the list of focal words are Enron and WorldCom since these two words appeared multiple times. 11 Table 1 reports the percentage of letters that included the keywords by decade as well as the aggregate percentages for the entire 1951–2020 period. Table 1 also summarises the number of letters per decade and the different editors that were responsible for the letters section during the different decades. Finally, Table 1 organises the focal keywords into different groupings: concepts, internal social characters, external social characters, internal practices, issues and ‘failures’. These categories follow from our previous suggestion that the letters will contain concept, character and subject words; more specifically, the final three groupings (internal practices, issues and ‘failures’) represent a finer partitioning of the subject category.

Breakdown of focal words by decade.

Note: The table shows mean values for variables by decade.

The descriptive information reported in Table 1 highlights what the letters addressed and illustrates how the letter topics and the number of letters published by decade varied over time. These variations are not surprising given the changes and challenges that were happening to the CPA profession at different moments in time. This is particularly evident in terms of the focal words enron, sarbanes, and worldcom, since these events did not occur until the 2001–2002 period.

To examine RQ1, we use the social network analysis modules that are available in R. Social network analysis methods consider the connections among the different nodes, the centrality of individual nodes, and the discursive communities to which the different nodes belong. A key feature of social network analysis is that the connections and centrality of individual nodes can be reported visually analyses and to allow for a more parsimonious presentation. The results did not change when we used continuous independent variable measures instead of the indicator variable measures (i.e., via a visual graph of the connections and centrality) as well as via the use of numerical indices (Borgatti, 2005; Borgatti et al., 2009; Borgatti and Everett, 2006). The current study adopts the page rank measure that has been used in previous social network research to measure centrality and which was developed by Google (Rosa et al., 2018; Schoch, 2018a, 2018b). 12 Additionally, we use the community detection algorithms developed by Traag et al. (2019) to identify the discursive community to which ethical concept words belong. Social network analysis methods have been used in a variety of prior accounting studies (Chapman, 1998; Neu et al., 2021, 2022; Neu and Saxton, 2022; Richardson, 2009, 2017).

To examine RQ2 and RQ3, we use logistic regression techniques to consider which of the key words predict the inclusion of an ethical concept word (ethics) and whether the inclusion of denotatively explicit ethical words is associated with the expression of negative sentiments. Our measure of sentiment borrows from prior textual analysis studies within the accounting/finance area (cf. Kearney and Liu, 2014: 175); more specifically, the financial dictionary approach of Loughran and McDonald (2011, 2016). The use of Loughran and McDonald's dictionary approach to measure sentiment is the dominant approach within financial settings area (cf. Kearney and Liu, 2014: 175) and has been used in many recent textual analysis studies (cf. Gandhi et al., 2019; Johnman et al., 2018; Loughran and McDonald, 2020). 13 The Sentiment Analysis module within R allows us to generate a negativity measure that starts from Loughran and McDonald's word list and ‘counts the number of words associated with a (negative) sentiment scaled by the total number of words in the document’ (Loughran and McDonald, 2016: 11). 14 This form of sentiment analysis provides a measure of the expressive aspects of the letters. The logistic regression results that are subsequently reported include a series of indicator variables to control for changes in the relationship between our dependent and independent variables over time. We also ran, but did not report, a logistic regression that includes a series of indicator variables for the different journal editors. In the unreported regression, the results for our focal words did not change and all editor control variables were insignificant.

Before presenting the analysis, it is useful to summarise component parts of our textual analysis method and to indicate how this method complements and extends previous accounting-focused historical research. We start by gathering the letters to the editor and using R algorithms to generate a frequency listing of the words in the corpus. This listing, in conjunction with our preconceptions regarding conceptually significant social characters and concepts, is then used to select a group of keywords. Next, social network algorithms within R were used to re-arrange the data and to generate visual discursive maps and summary quantitative measures for the centrality of the included words. Finally, we remove the focal words from the corpus and then use sentiment analysis algorithms to calculate whether the words that are packaged around the focal words express a negative sentiment. As we demonstrate in the analysis that follows, this combination of computerised methods foregrounds both the aggregate discursive structure of the letters and the micro intra-textual ways that the letters are constructed.

The discursive network (RQ1)

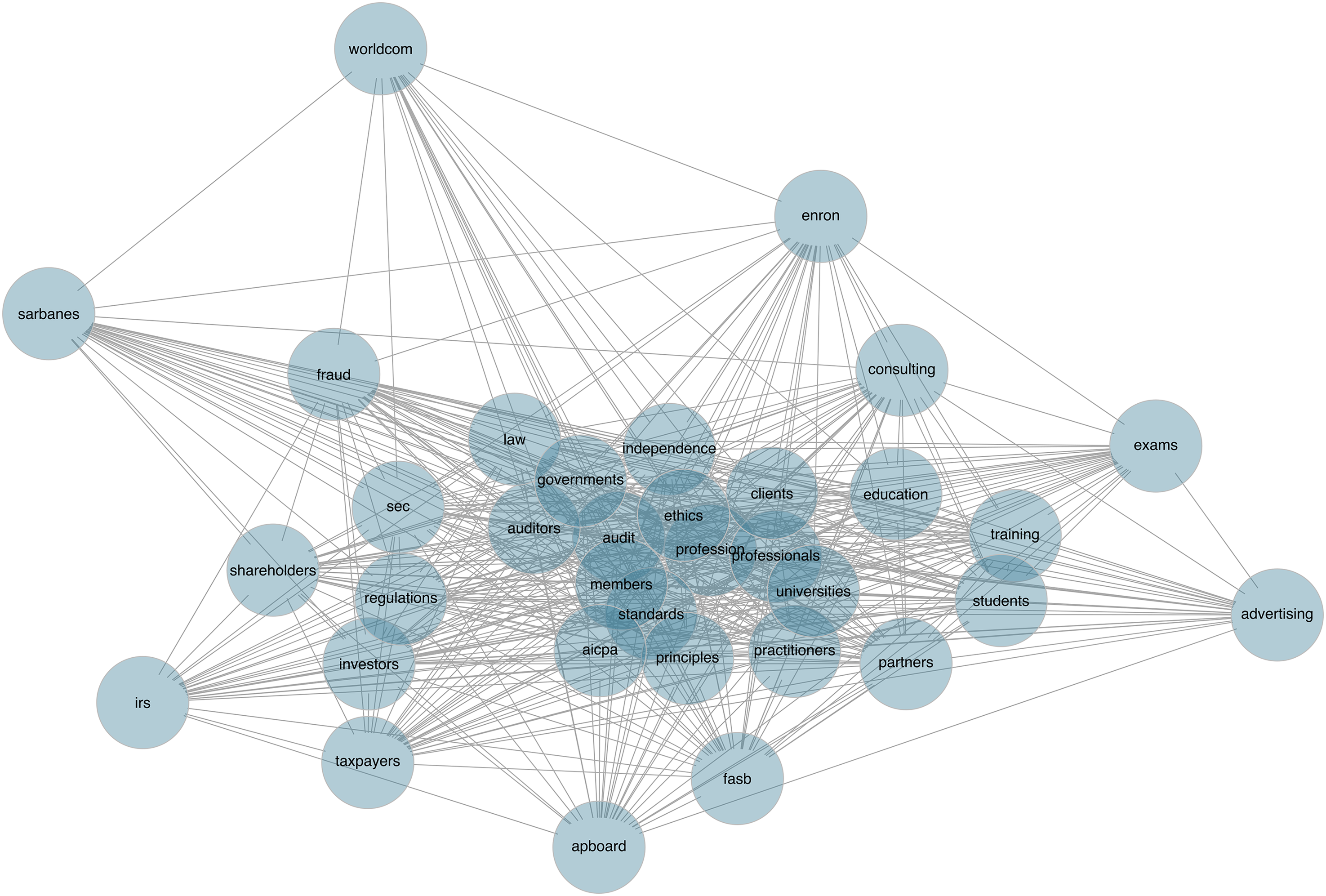

Figure 1 illustrates the discursive network of the letters to the editor, whereas Table 2 provides page rank centrality measures, ranked from the most to least influential nodes (words).

Sociogram of the discursive network of the letters to the editor.

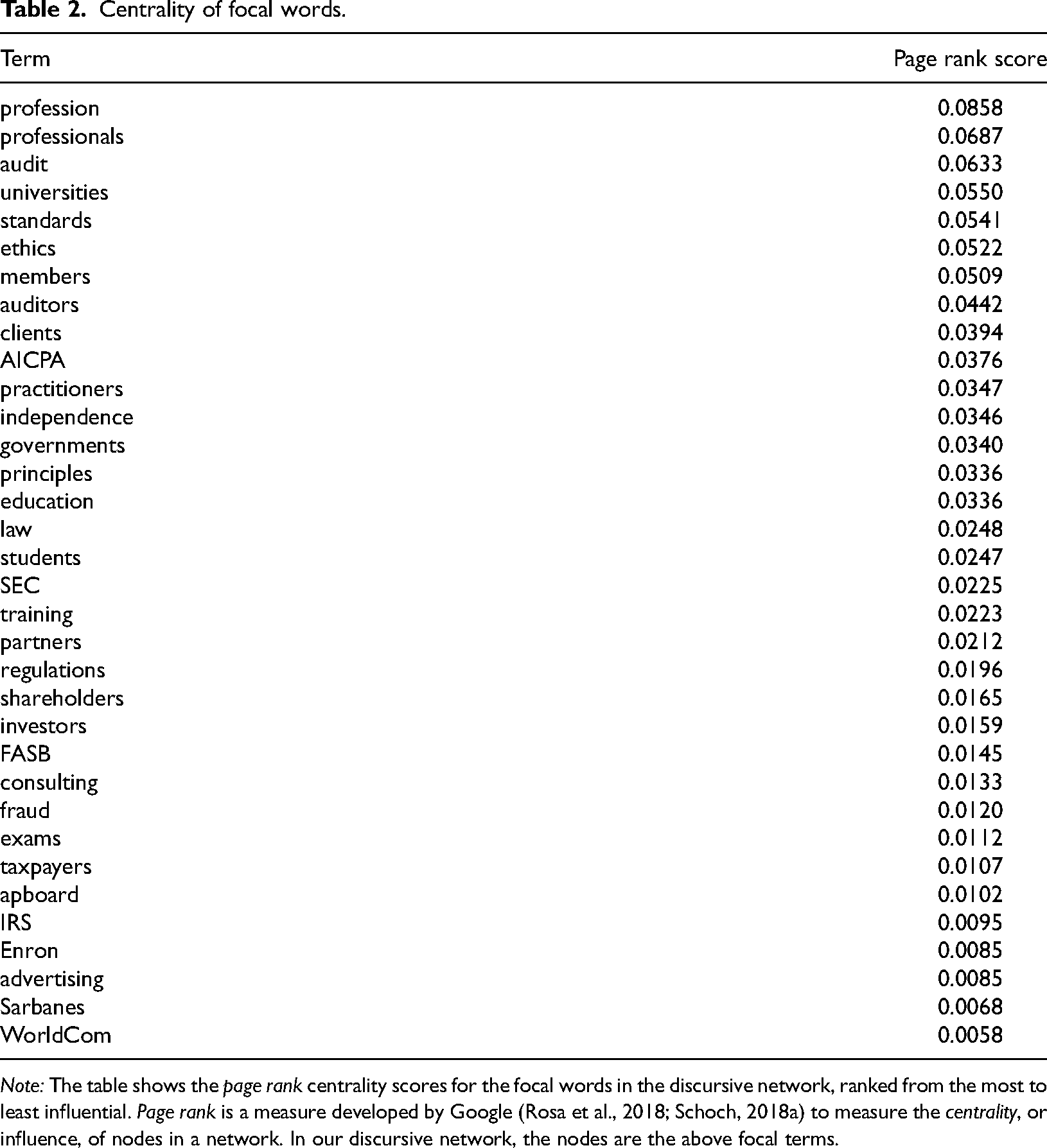

Centrality of focal words.

Note: The table shows the page rank centrality scores for the focal words in the discursive network, ranked from the most to least influential. Page rank is a measure developed by Google (Rosa et al., 2018; Schoch, 2018a) to measure the centrality, or influence, of nodes in a network. In our discursive network, the nodes are the above focal terms.

The network mapping provided in Figure 1, confirmed by the page rank scores in Table 2, indicates that the discursive network has a fairly dense discursive core with the six most central nodes being profession, professionals, audit, universities, standards and ethics. The inclusion of these nodes within the discursive core is mostly consistent with our expectations in that the letters are about the profession. The centrality of universities and ethics within the discursive core is, perhaps, somewhat more surprising. While we expected the letters to articulate an ethical viewpoint, we didn’t expect ethics to be so central. 15 With respect to universities, the frequency results reported in Table 1 illustrate that this focal word was quite prevalent in the early decades of our data but declined in frequency after 1990.

The network map and page rank results also illustrate a peripheral ring of less central nodes. Included in this ring are the words apboard, irs, enron, advertising, sarbanes and worldcom. The inclusion of enron, sarbanes and worldcom at the periphery isn’t surprising since these are temporally specific events that occurred late in our data period 16 and, similarly, apboard was mostly relevant prior to the formation of FASB.

Network analysis methods also allow us to tentatively identify discursive communities within the letters by highlighting the density of connections among the different nodes and by using this information to partition the aggregate network map. More precisely, ‘community structure describes the organization of a network into subgraphs that contain a prevalence of edges within each subgraph and relatively few edges across boundaries between subgraphs’ (Shai et al., 2017: 1). The identification of discursive communities is subjective because it depends on not only the structure of the underlying network but also on the community detection method used, the mathematical thresholds selected to calculate density, and the number of sub-community partitions (Traag et al., 2019). This said, it is possible to vary the threshold values within the cluster-Leiden community detection method to learn about both the existence of relatively stable discursive blocks and communities that exist within the network (Traag et al., 2019).

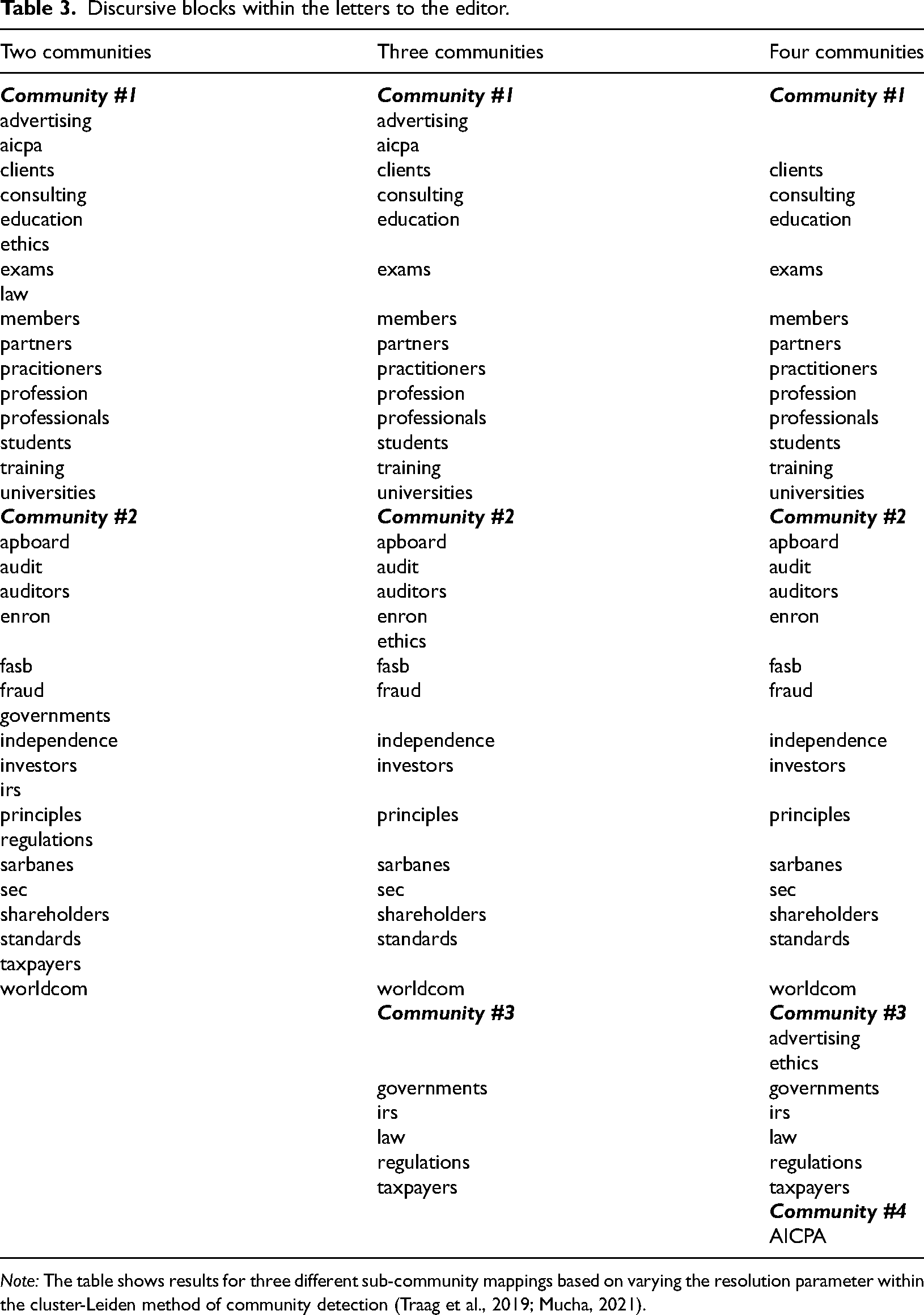

Table 3 provides three different sub-community mappings based on varying the resolution parameter within the cluster-Leiden method of community detection (Mucha, 2021; Traag et al., 2019). 17 The progression from two relatively large communities to four slightly smaller communities illustrates not only the relatively fixed nature of the communities but also the discursive blocks from which communities are built. 18

Discursive blocks within the letters to the editor.

Note: The table shows results for three different sub-community mappings based on varying the resolution parameter within the cluster-Leiden method of community detection (Traag et al., 2019; Mucha, 2021).

The community detection results reported in Table 3 highlight three stable discursive blocks that stay the same across the three mappings. The first discursive block (what is called community #1 in Table 3) includes internal social characters (i.e., members, partners students, etc.), educational practices (i.e., education, exams, training), universities, clients and the focal word profession. This first discursive block is arguably an important part of the letters to the editor discursive network in that it contains most of the highly central nodes (see Table 2). Interestingly, discursive community #1 connects together the internal social characters that comprise the CPA profession, the educational practices that produce CPAs,and the clients who purchase CPA services.

In contrast to community #1, discursive community #2 focuses on the practice of auditing, including who performs audits (i.e., auditors), the concepts (i.e., independence, principles, standards) and external social characters (i.e., fasb, sec) that guide audit practices, the external parties that use audited financial statements (investors, shareholders), and the problematic events that sometimes occur (fraud, enron, worldcom). This discursive block is anchored by, and built around, three central nodes: audit, standards and auditors. The third stable discursive community consists of the focal words governments, irs, regulations and taxpayers; however, this community does not contain any central focal words.

The discursive community results reported in Table 3 are important for two reasons. First, the results illustrate how letter writers think about and connect the different aspects of professional work. These cognitive maps suggest that letter writers distinguish between the system of professional practice on an abstract level – including the educational practices that produce the accounting producer and the clients that purchase CPA services – and the system of concepts and institutional actors that sustain audit activities. In this regard, the results complement and extend previous system of professions research (Abbott, 1983, 2014) by showing that letter writers distinguish between the system that produces accounting professionals and the system that attempts to ensure that audit outputs are credible.

Second, the results suggest that ethical words are a central node within the discursive network, but that ethics does not belong to a single discursive community. This finding is not surprising since ethics can be viewed as: part of the process of producing the professional CPA practitioner (community #1), something that guides concrete auditing practices (community #2), and a discursive touchstone that is enlisted in a variety of other situations. In part, it is the multi-purpose attributes of ethical words that contribute to the centrality of ethics within the discursive network.

Denotatively explicit ethics (RQ2 and RQ3)

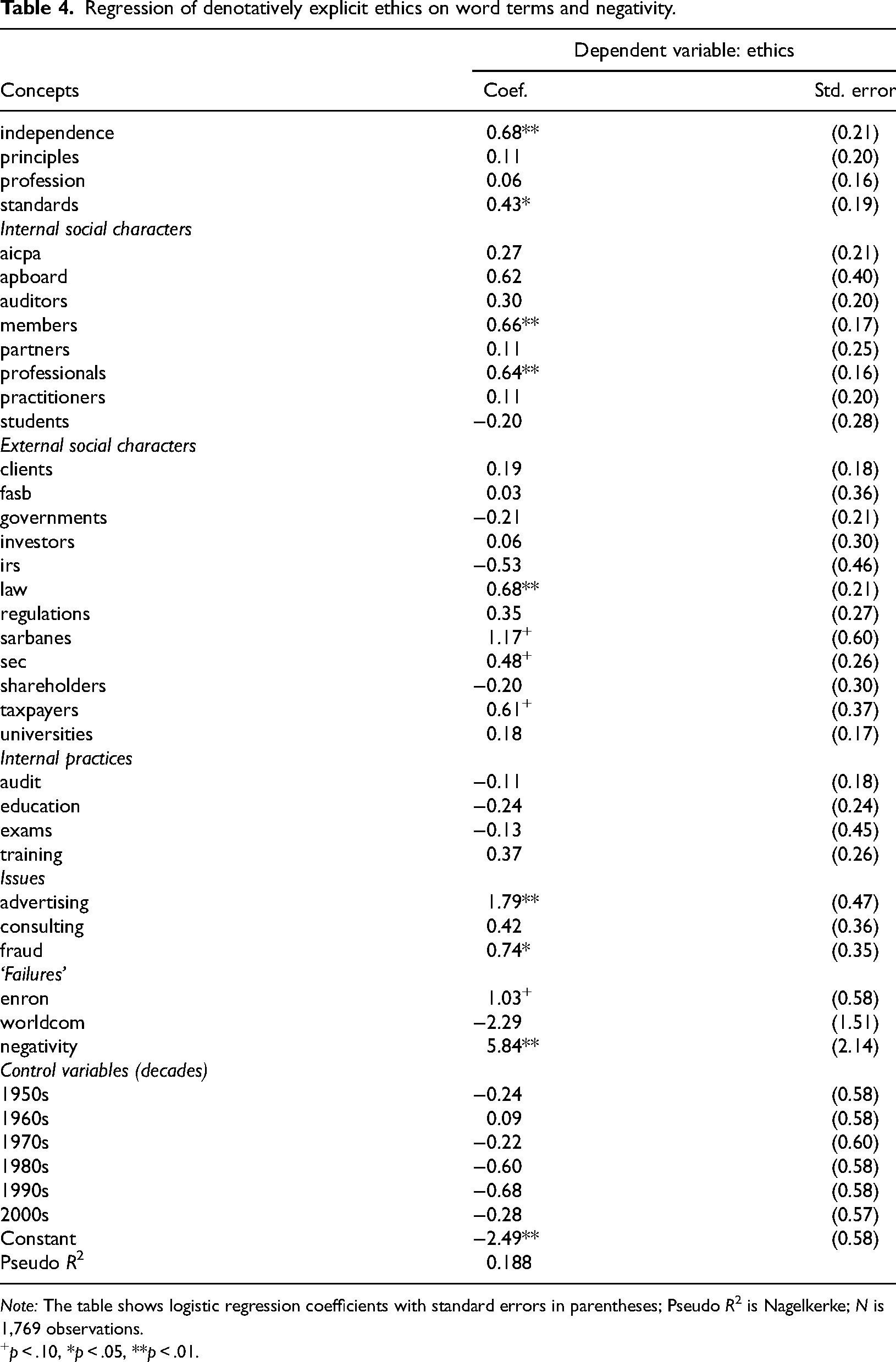

The theoretical framing sections proposed that the inclusion of denotatively explicit ethical concept words convert a point of view into an ethical point of view which, we propose, is more likely to occur around certain subject, character and concept words. More specifically, we suggested that some social characters, subjects and concepts are pre-imbued with ethics whereas some events call into question assumptions about the ethics of the profession. For these reasons, we proposed that subject words such as principles and standards, character words such as professionals and members, and subject words like sarbanes, enron and worldcom would be positively associated with the inclusion of denotatively explicit ethical words. We also suggested that the invocation of denotatively explicit ethical words is more likely to be associated with the expression of negative sentiments. Table 4 shows the results from our tests of the above predictions. 19

Regression of denotatively explicit ethics on word terms and negativity.

Note: The table shows logistic regression coefficients with standard errors in parentheses; Pseudo R2 is Nagelkerke; N is 1,769 observations.

p < .10, *p < .05, **p < .01.

The results reported in Table 4 are mostly consistent with our expectations. First, ethical words were positively associated with internal social characters (members, professionals) and with important concepts (independence, standards). We assume that these character and concept words were pre-imbued with ethics and thus were part of the AICPA's and members’ vision of the profession.

Second, events that interrupted inter-textual understandings regarding the ethics of the profession were associated with the use of denotatively explicit ethical words. For example, the inclusion of sarbanes and enron was positively associated with the use of explicit ethical words. Previously, we suggested that the introduction of Sarbanes-Oxley was an event that was not pre-associated with an ethical mode of speaking but that did have potential ethical consequences and thus required explicit inter-textual linking. We also proposed that the financial failures of enron and worldcom might be viewed by letter writers as events that merited explicit ethical commentary. This was the case with enron but not with worldcom. While we cannot be certain, this could be because Arthur Andersen's office in Houston was ‘captured’ by the non-audit fees of Enron and thus potentially complicit whereas the auditors of WorldCom were not viewed in this way. Similarly, as we mentioned in footnote 11, other financial failures received minimal mention in the letters, suggesting that the Enron failure was the only failure event that merited denotatively explicit ethical commentary.

Third, the inclusion of denotatively explicit ethical words was associated with the expression of negative sentiments. This finding is provocative in that it suggests that denotatively explicit ethical words perform both evaluative and expressive roles within the letters: that denotatively explicit ethical words literally help shift the narrative and therefore are a type of indexical (Agha, 2005). While sentiment measures are noisy and imprecise (Loughran and McDonald, 2016: 6), the results draw attention to the expressive aspects of the letters and the ways that the inclusion of specific ethical words is associated with different sentiments. 20

Taken together, the results illustrate that a viewpoint is more likely to be converted into a denotatively explicit ethical stance when the utterance reiterates the pre-existing speech genre and talks about members as ethical professionals or about concepts such as independence and standards, which are partially dependent on ethics. Ethical words are also more likely to be invoked when something new happens that potentially impacts on how individual members will practice ethical decision-making (e.g., Sarbanes Oxley) or that calls into question the ethics of individual practitioners (e.g., Enron). Note that the triggers for invoking ethics are different in these two cases: the first involves a reiteration of a pre-existing inter-textual association between ethics and the subjects, characters and concepts that are integral to professional discourse, whereas the second is a response to new events that potentially modify the position of ethics within professional discourse. Finally, the results suggest that events that incite the use of denotatively explicit ethical words also tend to incite the expression of negative sentiments. In this regard, explicitly ethical utterances appear to be primarily defensive in that such letters are responses to events that have the potential to undermine the presumed ethical nature of CPA practitioners.

Discussion

This study examines the 1,769 letters to the editor that were published in the Journal of Accountancy between 1951 and 2020. The provided analysis highlights how the letters articulate an evaluative stance about subjects, social characters and concepts that are of concern to the membership of the AICPA. The analysis also illustrates not only the centrality of different focal words within the letters but also how these words are organised into discursive communities: discursive communities that underpin how letter writers understand professional work. Finally, the results illustrate that ethical words tend to be invoked when talking about topics that are either pre-imbued with ethical attributes or when events call into question the ethics of the profession. Taken together, the results foreground how current and prospective CPAs enunciate their understandings of professional practice, including the centrality of ethics within these understandings.

The provided analysis contributes to our understanding of professional accounting work. The accounting association that we study – the AICPA – is one of the largest and most influential public accounting associations in the world, with more than 400,000 members. Previous research recognises both the importance of professional associations within the economic sphere and the ways that professional associations attempt to produce technically competent ethical practitioners. The current study complements and extends this research by explicitly focusing on the letters to the editor published in the Journal of Accountancy during the 1951–2020 period. We view these letters as archival, albeit curated, traces that help us to understand how current and prospective CPAs think about and articulate their views of what it means to be a professional accountant.

More specifically, the analyses foreground the discursive maps that underpin the sense-making activities of the letter writers, including which focal words are central as well as the ways that the focal words are organised into discursive communities. For example, the results illustrate two primary discursive communities within the letters, with the first discursive community linking together the internal social characters that comprise the CPA profession, the educational practices that produce CPAs and the clients who purchase CPA services. In contrast, discursive community #2 focuses on the practice of auditing, including who performs audits, the concepts that guide audit work, the involved external social characters, the users of audited financial statements and the problematic events that sometimes occur.

The identification of these two primary discursive communities is an important contribution. Of equal importance, the results suggest that ethics was a central node within the discursive network, but that ethics does not belong to a single discursive community. Rather, ethics is connected to both of the primary communities and thus appears to function as a type of discursive ‘glue’. Upon reflection, this finding is not surprising since ethics can be viewed as all of the following: part of the process of producing the professional CPA practitioner (community #1), something that guides concrete auditing practices (community #2) and a discursive touchstone that is enlisted in a variety of other situations. In part, it is the multi-purpose attributes of ethical words that contribute to the centrality of ethics within the discursive network.

The current study presumed and sought to demonstrate the usefulness of computerised textual analysis methods when studying historical accounting materials. The increasing digitisation of accounting materials and the increasing sophistication of computerised textual analysis methods create a space and an opportunity to study aspects of accounting history that were simply not possible previously. We believe that the study's findings both complement prior historical research such as Preston et al. (1997) and add a degree of precision regarding discursive structure that is very difficult to achieve without computerised textual methods.

At the same time, it is important to acknowledge the assumptions implicit within our methods and the limitations of these methods. Computerised textual analysis and social network analysis methods are designed to move beyond micro-level contextual detail and to summarise upward in order to discern aggregate-level patterns. This process of summarising the letters using focal words and then constructing discursive maps of these words is simultaneously powerful and limiting. It is powerful because it helps us to identify central words and discursive communities. Yet it is potentially limiting because it always erases a portion of the context. The current study has attempted to address this limitation not only by providing adjacent contextual detail (e.g., Table 1) but also by explicitly incorporating contextual variables into the analyses (e.g., the use of control variables for the different decades/editors and by footnoting additional supplementary analyses). These modes of considering context cannot replace an in-depth reading of the documents but it can help contextualise the provided aggregate-level findings.

In sum, the current study documents how letters published in the Journal of Accountancy between 1951 and 2020 articulate a view of what it means to be an (ethical) accounting practitioner. While professional accountancy underwent many changes and confronted many challenges during this time period, the centrality of ethics within the published letters did not change. In this regard, it appears that accounting practitioners continue to view themselves and the profession as ethical.

Footnotes

Data availability

Data are available from the public sources cited in the text.

Declaration of conflicting interests

The authors declare that they have no conflict of interest.

Ethical approval

This article does not contain any studies with human participants or animals performed by any of the authors.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was funded by the University of Calgary Haskayne Research (grant number RT758558).