Abstract

This paper explores the existence of monetary subordination in the Eurozone as an extension of the Core-Periphery approaches developed during the Eurocrisis. The analysis establishes the existence of monetary subordination in the EMU as the foundation for subordination at large. European monetary subordination is found to be supported by three pillars: the hierarchy of euro money-like balances, the nature of the euro as hybrid money and the fragmentation of the monetary jurisdictions coupled with their selective integration. To begin exploring the effects of monetary subordination, the paper introduces the analysis of the Eurozone crisis as a result of subordination coupled with deleveraging, highlighting the asymmetric impact of the latter on subordinate and non-subordinate members.

Introduction

Theorisations of Core and Periphery relations grounded in production and trade for European countries were prominent in the 1980s (Seers et al., 1979; Seers and Vaitsos, 1980). However, this tradition has said little about the role of money in generating hierarchy among European Monetary Union (EMU) member countries. Recent work has revived the traditions of Imperialism, Structuralism, and Dependency Theory to analyse asymmetries in the dollar-based international system, now formalised in the International Financial Subordination (IFS) agenda (Alami et al., 2022; Alves et al., 2022; Bonizzi et al., 2019; Carneiro and Conti, 2022; Koddenbrock et al., 2022; Vielma and Dymski, 2022). 1

IFS describes how the asymmetric power of finance structures global relations and constrains emerging markets (Alami et al., 2022). Money and the monetary system are central to financial subordination because of the working – or failure – of money as an organising principle (Lapavitsas, 2013), and because of the power that specific forms of money acquire when they extend beyond national borders. This focus has been reinforced by financialisation and the rising asymmetries in the global world economy (Kvangraven, 2020; Musthaq, 2021; Reis and De Oliveira, 2021).

Existing connections between money and dependency have mainly concerned developing countries or the CFA Franc (Koddenbrock and Sylla, 2019). These studies emphasise external imperial relations, such as France’s dominance, whilst neglecting the internal hierarchies that can emerge within monetary unions themselves.

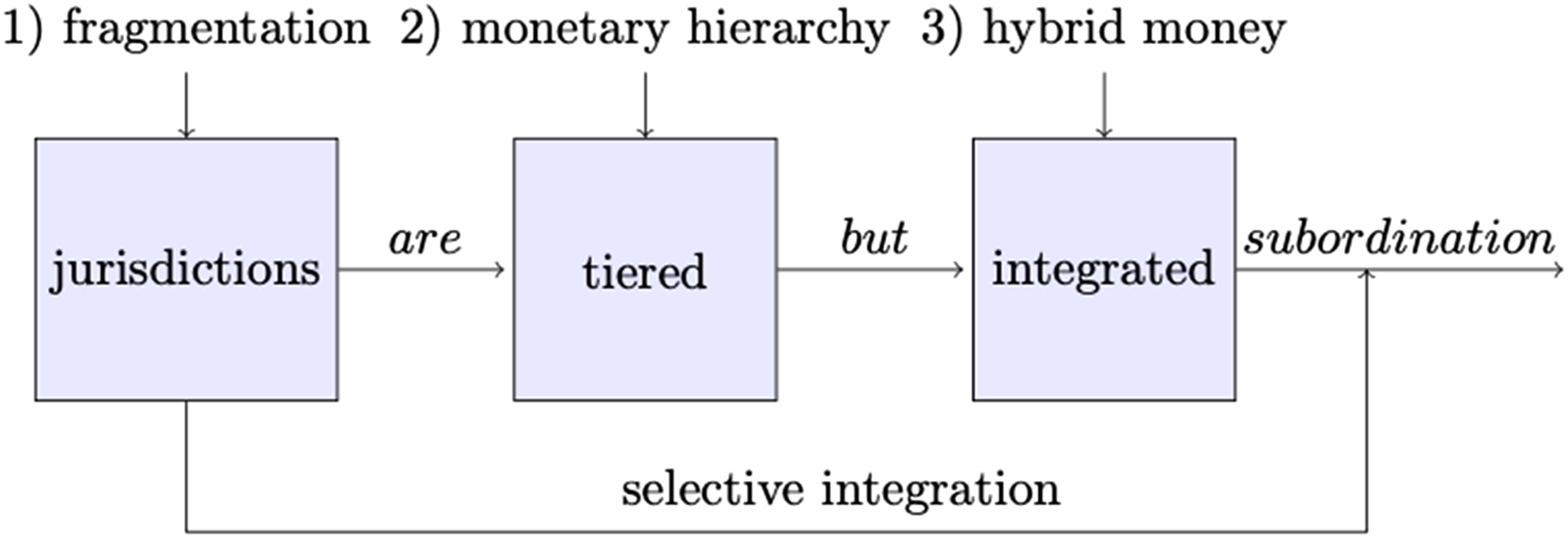

This paper argues that monetary subordination exists within the Eurozone, where a single and common currency integrates jurisdictions that remain structurally distinct. Far from a monetary union, the eurozone remains a process of monetary integration, building bridges across jurisdictions. The euro is an inherently hierarchical currency generating monetary subordination via three euro-specific pillars (fragmentation, monetary hierarchy, and ‘hybrid money’): fragmented monetary jurisdictions are hierarchically tiered but remain integrated via the working of the euro as a peculiar form of – hybrid – money. This hybrid money stems from the setup and working of TARGET2, the payment system for the Eurozone, which is the fundamental linchpin for the survival of the euro.

The paper develops a conceptual framework of monetary subordination in the Eurozone, grounded in observed institutional and financial dynamics. It clarifies how the Euro Area’s monetary architecture embeds hierarchy and how these asymmetries intensify under stress. The study contributes to three lines of the literature: first, extending the monetary dimension of IFS beyond currency hierarchies (De Conti and Prates, 2018; De Paula et al., 2017; Prates, 2020; Prates and Pereira, 2020); second, reframing the Eurozone periphery through the concept of monetary subordination (cf. Becker et al., 2010; Becker et al., 2015; Becker and Jäger, 2012; Gambarotto and Solari, 2015); third, integrating the literature on EMEs (Garcia-Arias, 2015; Kaltenbrunner and Painceira, 2015, 2018; Powell, 2013) with the Macro-Finance (Braun et al., 2018; Gabor, 2020)/Money View lens (Mehrling, 2013, 2020; Murau et al., 2021) and Marxian theories of money and finance (Labridinis, 2014; Lapavitsas, 2013).

The remainder of the paper proceeds as follows. The next section delves into the connections between the IFS agenda and the EMU. The following two sections, then, explore the monetary dimension of subordination in the Eurozone by defining its mechanics and looking at its three pillars in the EMU: monetary hierarchy, hybrid money, and selective fragmentation and integration. These mechanisms make subordination a structural characteristic of the Union. Successively, the paper elaborates on the significance of monetary subordination in the Eurozone by offering, as an example, its effects on financial fragility and the Eurozone crisis. The final section draws the conclusive remarks.

Studying the EMU between monetary hierarchies and an EMEs lens

This paper studies the internal asymmetries of the European Monetary Union, using the International Financial Subordination lens (Alami et al., 2022), even though its members are not EMEs. IFS, originally developed to analyse how financial power constrains EMEs in a hierarchical world economy, is here applied to the Eurozone as a framework to understand monetary subordination. Amongst the six analytical axes proposed by Alami et al., this paper focuses on the monetary one, analysing how the structures beneath monetary unification reproduce hierarchy. While finance remains a polarising force in the EMU (Tooze, 2019), this paper argues that subordination in the EMU has a monetary nature and, as such, conceptualises the monetary foundations of asymmetries in the EMU.

Starting with Prebisch (1950), core-periphery relations were already linked to the financial sphere and international monetary order of the post-war American hegemony. These insights, influenced by Keynes’s emphasis on the interdependence of current and capital accounts (Keynes, 1969), highlight that the reliance on controls and monetary arrangements should characterise the mechanism shaping their interactions.

Later Post-Keynesian and Marxist contributions discuss the presence of hierarchies in monetary systems. The former scholars understand the monetary hierarchy as a phenomenon occurring both at the international and at the domestic levels in independent, though related, ways, analysed, respectively, under the broader ideas of the International Currency Hierarchy (Bonizzi et al., 2019; De Conti and Prates, 2018; De Paula et al., 2017; Prates, 2020; Prates and Pereira, 2020) and the Critical Macro-Finance/Money View approach (Braun et al., 2018; Gabor, 2020; Mehrling, 2013, 2020; Murau et al., 2021). Marxist economic theory studies money as an inherently capitalist attribute, which then needs to be analysed at the level of capitalist production that extends from national boundaries to the global world economy, which cannot be clearly separated, especially in the age of fiat money (Lapavitsas, 2013).

The hierarchical nature of balance sheets and of money – understood as the tool to access the specific balance sheet issuing such money – implies two consequences: first, that different monies exist with distinct features and ‘value’, although they may have the same name (Labridinis, 2014), and second, that there exist different prices of the different monies arising in the different monies arising in the different markets such monies are involved in Mehrling (2013). Within the EMU, this hierarchy takes a territorial form: balance sheets located in specific jurisdictions generate an implicit cross-border, inter-jurisdictional exchange rate amongst legacy euros (i.e. the exchange rate between the national legacy currencies that have been replaced by the euro), fixed at par. Maintaining that par requires mechanisms to absorb stress when liquidity dries up at the bottom of the hierarchy, thus requiring elasticity.

The ‘subordination lens’ adopted, thus, examines how monetary integration has reshaped European countries in the last three decades. It belongs to the ‘umbrella concept and associated research Agenda’ of IFS, for it is a local application explaining the ‘processes and relations’ perpetrating asymmetries within the Eurozone (Alami et al., 2022: 4). Rather than looking at the ‘structural power of finance’, this paper delves into the structural power of money and of the monetary architecture, within which the relations of ‘domination, inferiority and subjugation’ (Ibid.) are still found and complemented by the overarching hierarchical tiering of the Eurozone, whose subordinated members are ‘penalized […] disproportionally’ (Ibid.).

Where economic equality is absent, the rationale for monetary unions is the progressive economic convergence of laggards with more advanced members. Such views have been the heart of the Optimal Currency Area debate in its ‘new’ or ‘endogenous’ flavour, which remains the standard metric for evaluating currency (and monetary) unions. Said convergence acts as the remedy to the disparity between the criteria defining a region as an Optimum Currency Area (OCA) and the empirical experience of the EMU, the ‘new’ or ‘endogenous’ OCA tradition argues that the criteria identified 2 rather than being preconditions, are the results endogenous to monetary integration, so to justify the beginning of the establishment of a monetary union even amongst significantly unequal partners (Eichengreen, 1992; Frankel and Rose, 1996; Strauss-Kahn, 2003). Empirical evidence on convergence following the introduction of the euro is mixed (see Diaz del Hoyo et al., 2017; ECB, 2013; Jager and Hafner, 2013; Marelli et al., 2019).

Current understandings of monetary unions neglect the possibility of developing monetary structures to sustain a form of integration that perpetuates the hierarchical tiering of members and their respective jurisdictions. Indeed, the puzzle and paradox of the EMU is the formalised, apparent equality of member states, which is just a legal appearance: beneath the surface, whether one looks at the real economy or financial structures, equality is far from a feature of the Union. In fact, the Monetary Union is tiered and especially tiering, with mechanisms in place that reinforce such asymmetric unification and prevent the rebalancing of the member states, creating an environment akin to the one experienced by EMEs in the international financial and monetary system, but characterised by the unique architecture acting beneath the surface of the single and common currency far from the political discourses and into the realm of de-politicised technocracy and of undemocratic institutions.

Research linking IFS to advanced economies or to the Eurozone remains limited. Most studies of European Dependency neglect the architecture of the euro and focus on more traditional parameters such as deindustrialisation, competitiveness, stagnation, or trade flows (Becker and Jäger, 2012; Botta, 2014; Botta and Tippet, 2022; Celi et al., 2018; Schutz, 2022; Weissenbacher, 2019). Yet, a key feature of subordination is the monopolisation by the core of the interactions between the periphery and the rest of the world (Galtung, 1971; Rombach et al., 2017; Vielma and Dymski, 2022). As is shown in the last section, this relational dimension of subordination can be found in the sequential transmission of the subprime mortgage crisis in the United States to the ‘core’ banking system in the Eurozone, and then to the ‘periphery’ (Murau et al., 2025).

Amongst heterodox perspectives, Gambarotto and Solari (2015) link Core-Periphery in the EMU to European ‘varieties of Capitalism’, but focus narrowly on production and export. 3 O’Connell (2015) interprets the Eurozone crisis as one of ‘deregulated cross-border finance’ but without theorising the EMU’s hierarchical monetary architecture.

The presence of subordination in the EMU appears evident in general terms, such as persistent yield spreads and low productivity, but elusive in terms of the specific forms of subordination. Whilst Core and Periphery are somewhat recognised, it is mistaken to think of the Core and the Periphery as unitary, cohesive, and homogeneous areas: countries – and their monetary jurisdictions – lie on a spectrum of subordination that revolves around a single centre. There is not a single ‘periphery’ in the Eurozone, but a collective of subordinated countries that experience the ‘peripheral position’ each differently, though mediated by standard mechanisms.

Conceptualising monetary subordination in the EMU

Monetary subordination in EMEs displays two stylised features of ‘the violent forms of expression of the structural power of finance’ (Alami et al., 2022: 19). First, EMEs are distinct jurisdictions (monetary, financial, and fiscal) with delineated borders connected to the rest of the world by specific forms of cross-border flows. Second, their currencies and their liabilities occupy lower tiers of the international hierarchy, bearing lower liquidity premia or higher risk premia. A third stylised feature is instability, as subordinated economies face constraints and fragilities – most prominently Balance of Payment constraints, asset-liability and denomination mismatches, exchange rate risk, and exposure to capital bonanzas and sudden stops.

Monetary subordination in the EMU replicates the first two, though in differentiated forms, whilst the third is mitigated by a mechanism preserving the one-to-one par amongst euro-denominated liabilities across member borders. The historical development of such a latter mechanism is explored in detail in Murau and Giordano (2024).

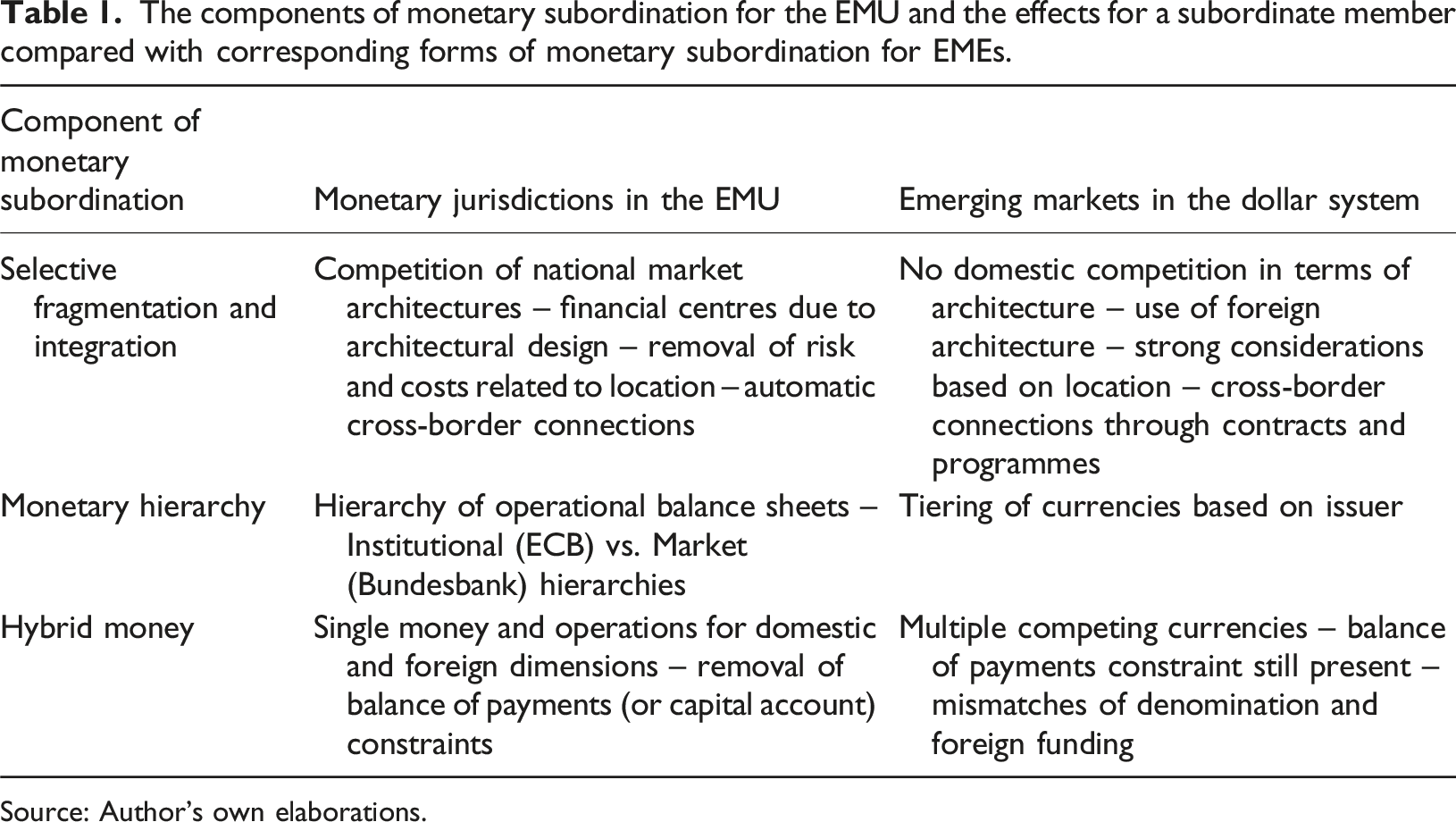

Accordingly, the structural form of monetary subordination in the EMU stems from three features of the monetary plumbing: the fragmentation and integration of the financial infrastructure beneath the euro, the monetary hierarchy of liabilities across jurisdictions, and the hybrid operation of money that bridges domestic and cross-border functions. Across these three, the tension between the fragmentation and the integration of selected markets sets the architecture for polarisation.

Figure 1 shows a conceptualisation of monetary subordination in the Eurozone derived from Table 1. The figure highlights each pillar (numbered items) and the dimension each affects (the shaded squares). In its entirety, Figure 1 can be read as follows: fragmented monetary jurisdictions are hierarchically tiered but remain integrated via the working of the euro as a peculiar form of hybrid money. The shape of monetary subordination in the Eurozone. Note. The numbered items represent the ‘pillars’ of monetary subordination in the EMU. Source: Author’s own elaborations. The components of monetary subordination for the EMU and the effects for a subordinate member compared with corresponding forms of monetary subordination for EMEs. Source: Author’s own elaborations.

The appearance of subordination arises from selective fragmentation across jurisdictions, as evidenced by liquidity flows within the EMU. The complete liberalisation and ‘unification’ (i.e. explicit guarantee of 1–1 par of the euro liabilities issued by the National Central Banks) of cross-border payments with a fragmented monetary infrastructure both in terms of central bank’s jurisdictions and market preference leads to a concentration of liquidity flows from bottom to the apex of the hierarchy in times of market uncertainty due to the loss of private rebalancing flows out of the apex.

Such flows are mediated by the working of money in the EMU, where domestic and cross-border functions are not distinct thanks to the TARGET system and the ‘hybrid’ nature of euro-balances. Structural fragmentation of markets and jurisdictions, coupled with the integration and de facto unification of specific segments (liquidity flows, collateral policies, and liquidity flows for securities settlements), allows and underpins the division between subordinated and non-subordinated member countries. This is most hidden in a monetary union, and depends on the institutional and private setup of the regional monetary architecture.

In the IFS for emerging markets, the monetary dimension is often perceived as a hierarchical tiering of currencies, with the US dollar at the apex and currencies issued by EMEs at the bottom. The same approach cannot be applied to the EMU, as the currency is a single and common one. Yet, the hierarchy persists in the nature and working of the euro as well (Giordano, 2025), substantiating the idea of a monetary subordination within a union of legally equal partners.

Table 1 summarises the three key dimensions of monetary subordination in the Eurozone compared to EMEs. First, the definition of what is national and what is international for EMEs aligns with national borders, thereby necessarily confining the monetary infrastructure to national borders. A complete monetary union – for example, a country issuing its own money – eliminates distinctions by providing a single set of infrastructure that serves all agents. An incomplete one blurs such a distinction: the delineation of jurisdictions (in the European case, coinciding with the national borders) relies on the artificial fragmentation of markets and infrastructures as well as the selective integration of other segments, primarily payments. Hierarchical relations among member states require that their jurisdictions exist as distinct entities.

Second, monetary jurisdictions are hierarchical. Most important is the hierarchy of balance sheets and their liabilities rather than money, given the ‘money confusion’ (Labridinis, 2014) arising from all money liabilities being denominated in euros. Indeed, the Eurozone shows undeniable tiering of central bank balance sheets – and thus of the money liabilities they issue. Such a monetary hierarchy occurs along two axes: an institutional one that sees the ECB as the apex (Murau and Giordano, 2024) and a market-based one with the Bundesbank as the apex. Crucially, if the National Central Banks (NCBs) balance sheets are tiered, private monetary and other financial institutions will be tiered according to what official balance sheet they can promptly access (Giordano, 2025).

This leads to the third pillar of monetary subordination in the EMU: ‘hybrid money’, or the coincidence of monetary policy operations and cross-border funding operations. This pillar is required for two reasons. On the one hand, it maintains the money liabilities of all NCBs at par, thereby allowing the hierarchy to be ‘masked’. On the other hand, it leads to mechanisms that polarise cross-jurisdictional flows. Ultimately, this has a significant side effect: it creates contingent debt relations for the member countries (Giordano and Lapavitsas, 2023).

Substantiating the three pillars of monetary subordination in the EMU

Structural fragmentation and selective integration

The selective integration highlights the key problem created by fragmentation: financial integration in the EMU advances through payments and settlement – an integration of money flows, but not at the level of infrastructures. This appears, for example, in the fragmentation of collateral valuation and use, as well as of the Central Securities Depositories (CSDs) and Central Counterparties (CCPs) along national lines. The concern for this type of fragmentation was present in the Giovannini Report (The Giovannini Group, 1999), which found the infrastructure of financial markets and specifically of repo markets to be highly national-based and poorly connected, and recognised that the simple introduction of the common and single currency could not be sufficient to bridge these gaps and lead to a well-functioning plumbing of the Euro.

Debt markets in the euro area never became fully integrated. Clearing houses, CSDs, and collateral management frameworks remained nationally organised, creating parallel infrastructures rather than a genuinely unified system (Allen and Moessner, 2012). Securities formally denominated in the same currency were subject to different eligibility criteria, settlement procedures, and liquidity conditions across jurisdictions (Gabor and Ban, 2016). During the sovereign debt crisis, these divisions amplified market stress: spreads widened not only because of fiscal fundamentals but also because fragmented infrastructure constrained liquidity and increased counterparty risk (Merler and Pisani-Ferry, 2012).

At the level of clearing, two tendencies have been at play throughout the history of the Euro: the fragmentation of market infrastructure into three main CCPs (located in France, Italy, and Germany) and the centralisation of clearing for transactions with multiple collateral sources through the French LCH RepoClear. At the level of settling, the history of market infrastructure shows that CSDs have strong links to the trading platform they serve.

The technical and operational connections to the securities settlement systems led to a consolidation of CSDs at the national level (many national CSDs merged towards the end of the 1990s to remain larger but domestic CSDs, for example, the Spanish SCL and Espaclear), where the Central Banks were also in charge of their supervision. The hurdles to the unification of securities markets identified by The Giovannini Group (2003) remain almost unaltered, especially in terms of the legal practices for the trading of securities, which remain essentially embedded in national legal systems. 4

This fragmentation has two major consequences. First, it entrenches hierarchy not only through market sentiment but through institutional design – the use of different infrastructure and of different instruments to carry out transactions and funding, especially for the European universal banks. The decentralised structure of European central banking, coupled with national market infrastructures, reproduces a tiered system of liquidity. Fragmentation, per se, is not the source of hierarchy, but the partial integration that connects fragmented markets and allows for money to move from one fragmented jurisdiction/market to another freely. The monetary union hyper-liberalises the European national economies by enforcing a market structure and a backing of ‘foreign’ euro-denominated claims of other Eurozone jurisdictions in a way that resembles the liberalisation of Asian countries in the 1980s/90s and more generally of developing countries exposed to international dollar flows.

Second, the Eurozone is built on the knife edge of integrating passively as much is required for an apparent common monetary policy, whilst at the same time refraining from bringing forward unification at the structural level: such an issue arose with the political hurdles of giving up national sovereignty in the 1990s, but has been reinforced by the selective and technocratic integration pursued by the ECB Governing Council. Passive integration in which infrastructures are not unified but the par between liabilities of different jurisdictions is guaranteed and automatically supported – that is, by having no limits to cross-jurisdictional money flows, cannot foster a unified and even monetary union, but only leads to the perpetration of asymmetries and fragmentation at the level of the financial plumbing (the ‘minimum convergence’ approach shown by the European Monetary Institute and the soon-to-be Eurozone members in the 1990s).

This, in turn, translates into uneven development of financial markets at large, with the national markets that play prominent roles in the Union (French and German) being deep and liquid enough to allow the expansion of capital markets and the concentration of investment in core financial assets.

The fragmentation shapes the ECB’s monetary policy and, in turn, tries to remove the appearance of fragmentation. Fragmentation persists in government bond spreads, prompting the ECB to act swiftly (Mody and Nedeljkovic, 2018; Pisani-Ferry, 2012). Without the perception of fragmentation, despite the presence of its infrastructural form, the political request for unification is removed. The condition is that payments for the marginal agent (bank, firm, or consumer) clear and settle, which is provided as a guarantee of the TARGET system and the Eurosystem’s infinite elasticity of liquidity provision. In turn, passive integration is pursued technocratically to foster the appearance of an integrated Union.

Monetary hierarchy

Having shown that separate jurisdictions exist in the EMU, subordination in the EMU hinges on the hierarchy of jurisdictions, especially of the liabilities issued in each one. Private monetary and other financial institutions consider the balance sheets of the NCBs as single entities rather than as faces of the unified Eurosystem. Such considerations arise primarily from two reasons: first, NCBs have different risk profiles in the event of a breakup of the Eurozone; and second, NCB balance sheets support the Monetary and Financial Institutions within their monetary jurisdiction. Consequently, higher deposits of non-Euro Area residents in specific NCBs entail lower perceived risk as well as lower transaction costs due to the presence of counterparts in the jurisdiction. In other words, the liabilities of such NCBs are valued more than the liabilities of other NCBs, similar to the hierarchical tiering of currencies in the International Financial Subordination literature – especially its Post-Keynesian flavour (see De Paula et al., 2017; Prates, 2020; Prates and Pereira, 2020).

The tiering of official balance sheets is empirically shown in Giordano (2025) for both the European Currency Unit (the precursor of the Euro), and for Euro-balances. The paper shows that there is not only an official tiering of balance sheets with the ECB as the apex but also a hierarchy of the NCBs’ balance sheets based on market preference, as encapsulated by the demand for liabilities of different NCBs. This applies to both non-Euro Area residents and domestic actors, thus suggesting an established tiering of balance sheets in the eyes of holders of money and money-like assets denominated in euro.

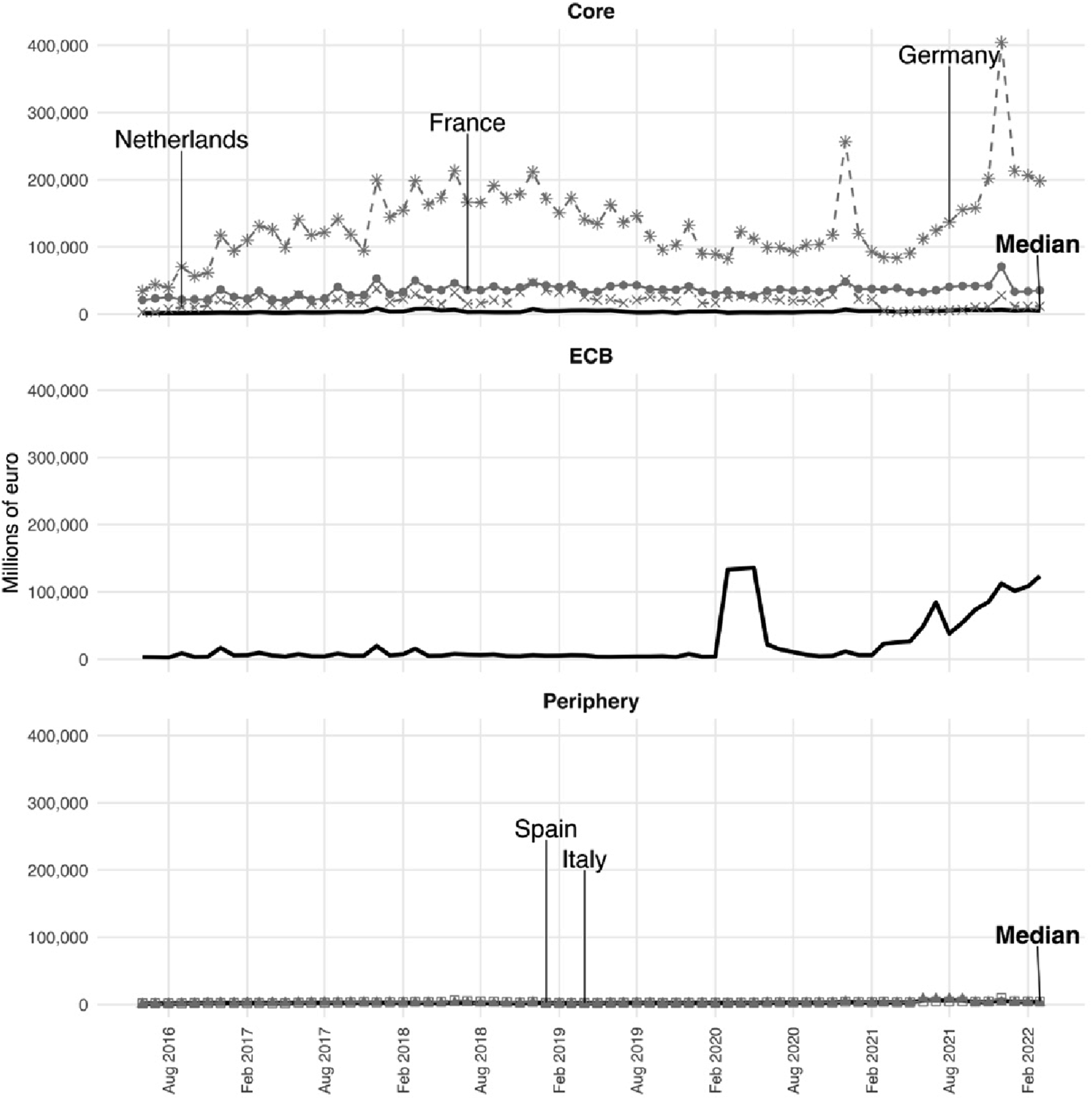

Since 2016, there has been a considerable increase in the liabilities of the Bundesbank to non-Euro Area residents, as depicted in Figure 2, whilst most of the Eurozone NCBs’ liabilities have remained negligible except for Banque de France and the De Nederlandsche Bank. In addition, a cyclical component, driven by banks’ end-of-year window dressing, shows non-EA residents accumulating reserves at the Bundesbank in December, followed by de-accumulation the following January. These point to the structural polarisation putting the Bundesbank at the apex of the market-based monetary hierarchy defined by private agents’ preference for the Bundesbank’s and the German banking sector’s liabilities.

5

National central bank liabilities to non-euro area residents denominated in Euro, 06/2016–03/2022 (mn euros). Median (black) with key countries (grey) highlighted with different point shapes. Source: Author’s own elaborations on SDW and National Central Banks Data. Note. Data available only since 2016. Core countries: Germany, France, the Netherlands, Belgium, Austria, Finland, and Luxembourg. Periphery countries: Italy, Spain, Greece, and Portugal. For clarity, in the ‘Periphery’ panel, Italy is the filled triangle, and Spain is the empty square. The two are indistinguishable as neither reaches €10,000 mn at any point throughout the period, which highlights the contrast with the Core countries.

The result is a coexistence of different euros (issued by the single NCBs) that bring forward the legacy monies of the pre-euro countries and allows for the existence of ‘quasi-foreign exchange reserves’ in the form of TARGET balances. A hierarchy of euro-denominated liabilities was revealed clearly by the Eurozone crisis. Sovereign bond spreads reached unprecedented levels – with Greek 10-year yields peaking above 30% while German bunds fell below 2%, despite their common denomination (De Grauwe, 2013; Murau et al., 2025). At the same time, the ECB’s collateral framework imposed differentiated haircuts, with securities from stressed jurisdictions subject to larger discounts, thereby institutionalising asymmetries in access to central bank liquidity. These practices entrenched the perception that not all euros were equal, reinforcing a monetary hierarchy within the union.

Hybrid money

The concept of hybrid money stems from the replacement of both a private and public form of funding with a ‘hybrid’ one instead, namely, the use of the TARGET(2) mechanism. In cross-border and cross-currency systems, payments are carried out mainly through a correspondent banking system in which non-resident banks open an account with a resident bank to channel payments in foreign currency. The correspondent banking system is effective in netting gross flows and carrying short-term imbalances.

With more permanent net imbalances, however, a funding system is required to fund the foreign currency liabilities. Such a funding system arises first in private markets with interbank loans through which the deficit banks seek to fund their net flows. This comes with the respective interbank rate, which adjusts in response to the availability of interbank funds. Net payment imbalances are financed through private loans at interest rates at which lenders are willing to finance the imbalance. The interest rate, in turn, would rise as deficits worsened until no one was willing to fund such imbalances. The net payment imbalances would be reflected in interest rate differentials at first.

However, suppose the imbalances persist and funding becomes less available. In that case, an official funding mechanism backstops the deficit banks: central banks can provide the funds required by entering into Foreign Exchange Swap agreements with the counterpart central bank, channelling the foreign currency to the domestic banking sector. The failure of the interbank market is replaced by public funding, usually characterised by two features: it is collateralised, and the two central banks entering the Foreign Exchange Swap pay different interest rates, so that the ‘deficit’ country pays a premium for the liquidity obtained.

In international markets, there is a hierarchy of funding – private, backed by public – that is allocated through its prices, and that keeps a clear distinction between the two. On the contrary, the advent of tensions in the Eurozone interbank and money markets showed that the TARGET mechanism is a hybrid form of funding in which standard monetary policy operations serve to finance cross-border liquidity flows. Furthermore, the interest rate that NCBs have to pay on TARGET balances was set equal to the one on Main Refinancing Operations (ECB, 2016a, 2016b), though the effective interest rate after NCBs pool their interest income is less clear to determine.

If we look at the pre-euro example of Italy, it can be seen that repo operations and FX swaps were the key tools for refinancing operations at the Banca d’Italia between 1992 and 1996 (Buttiglione et al., 1997). The two, however, played different roles: the former was used as a monetary policy tool to regulate liquidity in circulation, whilst the latter remained stable and did not signal monetary policy changes. Therefore, they were distinct tools with distinct operations.

This changed with the introduction of the euro and the decentralised NCBs, given that refinancing repo operations carried the guarantee of being valid for cross-border intra-Eurozone transactions, thus effectively acting as currency swaps between the different ‘legacy euros’. The hybrid system introduced by TARGET2 allows distortions to arise in which the ex ante elasticity of payments and the ex post ‘funding discipline’ (Mehrling, 2020) are mediated by the central bank’s liquidity-supplying operations. It is a feature specific to the Eurozone’s architecture that commercial banks use one set of collateral and essentially only one facility to carry out both refinancing operations and funding of cross-border payments. This, in turn, explains where the tension lies. On the one hand, the ECB’s refinancing operations become akin to a ‘floor system’ with full allotment rather than a corridor system with flexible standard allotment, thereby allowing banks to draw as much liquidity as ‘necessary’. On the other hand, the fact that the 1–1 par across NCBs’ liabilities is guaranteed by the conversion of liquidity in TARGET balances makes the full allotment of the refinancing operations also a full allotment of ‘foreign’ 6 currencies to carry out cross-border payments, both financial and non-financial.

This was the case, for example, with the first Long-Term Refinancing Operations, which saw Italian and Spanish banks drawing funding of around €300bn by January 2012, as compared to the €50bn drawn by Germany and Luxembourg and the €150bn by France and Belgium, but that also coincided with an easing of funding conditions for German banks, due to the flow of Long-Term Refinancing Operations funds drawn by Italy and Spain into German accounts. Such flows were mediated by the TARGET guarantee attached to the Long-Term Refinancing Operations.

Monetary subordination and subordinate deleveraging: A lens for the financial fragility in the Eurozone

Finding subordination in the monetary architecture of the EMU shows the structural nature of the hierarchical relations amongst its member states. Within such a structure, then, agents’ behaviours can be analysed to assess how monetary subordination affects subordination at large. Whilst there are several – real and financial – consequences of monetary subordination in the EMU, one overarching result, consistent with the IFS literature, is subordinate financial development, linking monetary and financial subordination.

In fact, the single and common currency creates a channel for financial fragility in peripheral members stemming from their subordinate position. This fragility emerges in two dimensions: acutely during crises, when hierarchical tiering becomes visible, and latently in tranquil periods, through the growing polarisation of intra-EMU balances such as TARGET2 (Murau and Giordano, 2024). As in EMEs, fragility reflects subordination, though in the EMU, it is mediated by the institutional setup of the monetary union.

In this sense, the Eurozone crisis can be understood as a crisis of subordination: it is a local outburst stemming from the Global Financial Crisis (GFC), in which the local ‘core’ mediated and propagated financial instability onto the local subordinated members. Following Galtung’s (1971) insight into the monopolisation by the core of the relations between the periphery and the rest of the world, the subordinate nature of the crisis can be appreciated as stemming not from the markets affected but from the transmission mechanism that triggered the turmoil: the core banks and their behaviour.

Some of the features of financial subordination affecting developing countries – primarily the forced access to finance denominated in foreign currency – have been argued to be the leading cause of the division between Core and Periphery instead of the division of labour in the real economy (see Tavares, 1985; Vernengo, 2006). However, whilst these authors highlight the constraints on the Balance of Payments resulting from the use of external finance as the cause of divergence (Alami et al., 2022), the Eurozone has the opposite problem: polarisation is driven by the removal of the necessity for Balance of Payments adjustment mechanisms via the unlimited balancing offered TARGET2 system (Cesaratto, 2013).

The Eurozone crisis was not a standard Balance of Payments crisis or a crisis of capital flows and recycled surpluses (Copelovitch et al., 2016; Hall, 2014), but a crisis arising from the debris of the GFC combined with a precise monetary architecture of the EMU, which has been argued to be the result of a flawed monetary design (see Lavoie, 2015 for an explanation of the Eurozone crisis based on the ECB’s reluctance to buy bonds and the lack of a common fiscal authority, both key features of the monetary architecture of the EMU playing a role in the crisis but not the underlying cause, namely, the contagion from the Global Financial Crisis – see Murau et al., 2025). Similarly, finding the roots in fiscal (unsustainable government debts) or monetary (credit expansion in the periphery due to the single interest rate) inconsistencies fails to explain the sequentiality of the crisis: the Eurozone crisis is one of subordination for it was sparked by the core’s position as intermediary between the ‘periphery’ and the outside (as shown also by the heavy carry trade taking place) and it was catalysed by the financial plumbing of coexisting fragmentation and integration. At its very heart, it was a crisis of funding for financial institutions in the core, causing funding pressures for subordinated members, which eventually spilt over into the sovereign debt markets of weaker countries.

As of 2009, German and French banks – heavily exposed to the speculations and bubbles of the US markets – were already undergoing structural deleveraging (Brunnermeier et al., 2016; Koo, 2011; Roxburgh et al., 2010), 7 whilst the banking sectors of peripheral European countries were not faced with the necessary shift to debt-minimisation. The Global Financial Crisis led to contractions in core banks’ balance sheets primarily for three reasons. First, they held the largest holdings of USD-denominated instruments in the Eurozone – primarily Asset-Backed Securities (McCauley, 2018). Second, the decreasing supply of USD financing liquidity by US-Prime MMFs affected them the most (Feyen et al., 2012), which had a large impact, considering that European banks held around $30tn of foreign assets at the beginning of 2008 (Baba et al., 2009). Third, they could not secure USD financing through Foreign Exchange swaps because they were considered increasingly risky and thus with higher premia by their counterparts – US banks and other financial institutions.

Following the path of deleveraging, Eurozone core banks shifted to a ‘home bias’ (Milesi-Ferretti and Tille, 2014) in their interbank lending. It reduced their cross-border exposure to banks in ‘peripheral’ countries – Greece, Italy, Ireland, Portugal, and Spain – leading to the fragmentation of interbank markets along the national borders. These culminated in price differentials for the different instruments in 2008 and solidified during 2009, remaining a key feature of the post-crisis Eurozone.

Whilst the first markets to be affected were the unsecured interbank markets, the reliance on short-term debt markets triggered a cascade effect for which peripheral banks shifted to secured interbank markets and to the issuance of short-term papers, both of which still experienced contractionary forces (Lane, 2012). For example, the first interbank market to be strongly affected was the Greek one, where once interbank lending froze and domestic money markets dried up as counterparty risks skyrocketed, costs for interbank lending increased by 500 b.p. (IMF, 2009).

The freezing of funding markets for Greek banks culminated in the inability to sell bonds as of October–November 2009, the shrinking of the use of European commercial paper due to a lack of buyers, and the ultimate drying up of repo markets. Under those circumstances, coupled with the shift in the credit cycle shown by the increase in the direct loans (i.e. liquidity assistance) by the Eurosystem (via the Bank of Greece) from €6.3bn in March 2009 to €48.1bn 1 year later, the contraction spilled over to the Greek treasury which now also found it increasingly difficult to refinance itself. Indeed, the credit cycle shifted in Greece in the first months of 2009 and quickly spilt over from banks to firms as reported in the Flash Eurobarometer survey on access to finance for small and medium-sized enterprises.

Only successively, with the first downgrades of the Greek government bond rating by the main rating agencies between October and December 2009, did the Eurozone crisis hit the sovereign debt market. Greek banks’ financing was just the peculiar transmission mechanism arising from the architecture of the EMU, whilst the crisis hitting sovereign securities was ultimately due to the shift from leveraging to deleveraging of the lenders in the cross-border interbank market, combined with the recourse to repo markets where the government bonds are used as collateral.

The prolonged effects on sovereign debts and the sequentiality of the countries affected were compounded by the role of repo markets in smoothing the contraction of interbank unsecured lending (Murau et al., 2025). Crucially, the downgrade of sovereign bonds entailed the revaluation of the collateral posted to provide liquidity. These created a spiralling dynamic that led to increasing bond spreads primarily due to the role of the Eurozone infrastructure, which increased the haircuts applied to the sovereign bonds already under stress. Given the high concentration of government bonds in the balance sheets of MFIs within the national borders, the lower value of collateral (or the higher relative price of liquidity) entailed that financial institutions in the subordinate countries suffered further difficulties in securing funding, thus having to reduce their activities, curtailing further the credit cycle.

Such spiral eventually led to the contagion of repo markets and other subordinate countries (the main CCPs, such as LCH.clearnet and Euronext, increased the individual haircuts of the various GIIPS countries throughout the early 2010s), eventually touching Italy (with the ECB announcing the purchases of Spanish and Italian bonds in August 2011 via the SMP), and hitting back to ‘core’ MFIs like Dexia Bank. The Eurosystem’s collateral management facilitated the contagion through the General Collateral Framework, which has been market-based since 2005 and thus amplified the contractions in potentially available funding due to the lower valuation of (sovereign) collateral (Marcussen, 2009; Orphanides, 2017; van ’t Klooster, 2022; Murau et al., 2025).

Leaving the Eurosystem’s reaction on the side, the Eurocrisis should be understood as a crisis of subordination because the financial instability that subordinate countries experienced was a direct consequence of the combination of the banking dynamics of the ‘core’ and the architecture underpinning the hierarchical tiering of Eurozone jurisdictions, working as a transmission mechanism. The crisis shows the tendency of subordinated countries’ financial systems to draw on cross-border interbank markets, rather than core investors forcing a condition of dependency on the periphery. This, in turn, is what defines it as a crisis of subordination, for the victims and forms of the Eurozone crisis are specific to an asymmetric system in which the core has a ‘first-mover’ advantage and thus could undergo deleveraging before the periphery.

In this sense, the process of deleveraging took a more violent form in the periphery, even though the subordinate countries were less exposed to the original source of the crisis – the US financial system. Germany and France began economy-wide deleveraging in 2011–12, with the banking sectors starting even earlier (Buttiglione et al., 2014). Notably, the violence that deleveraging unleashed in the periphery was underpinned by the policy response that ‘core’ countries could put in place, given that they were hit before other members of the EMU. Germany offered significant rescue packages to its ailing banks and recapitalised its domestic banking system with direct equity injections of taxpayers’ money, spending roughly €250bn between 2007 and 2014. Not only is this the highest government support offered in the Eurozone, but Italy – the largest peripheral member – spent only around €4bn to help its banks (Brunnermeier et al., 2016; MEF, 2016), which at the time did not require the same levels of support.

Inevitably, the policies implemented by the Eurosystem and national authorities to support initial deleveraging in ‘core’ countries not only created asymmetric consequences but also shaped the recovery for Southern members. The Long-Term Refinancing Operations (LTROs), for example, coupled with other Eurosystem’s early liquidity provisions, had three asymmetric consequences for Eurozone members. First, it kept ‘zombie’ banks alive in the southern European countries like Italy, where the bank issues began roughly after the deadline of the LTROs. Second, it allowed northern MFIs to offload to the Eurosystem assets that had become risky (i.e. Southern European debt), thereby incentivising the early repair of their balance sheets. Third, although ‘core’ (i.e. German and French) banks refrained from bidding for a significant portion of the LTROs, a part of the funds received by southern banks found their way back to these banks, effectively increasing their deposit and worsening the TARGET balances (Hall, 2012; Vause et al., 2012). Indirectly, the failure to start deleveraging in Italy was enhanced by these asymmetric consequences just as much as the early and swift deleveraging of the German financial sector relied on indirect funding through ECB policies to a greater extent than domestic policies.

Ultimately, it is the combination of deleveraging and subordination (i.e. subordinate deleveraging) that lies at the heart of the post-Eurocrisis faltering recovery shown by an exemplary member of the Southern Periphery like Italy. Subordinate deleveraging, domestically coupled with the possibility of carrying out ‘de-risked’ cross-border investments via TARGET2 and the NCBs’ balance sheet, explains the divergence in economic growth and the sustained net liquidity outflows displayed by Italy in the 2010s. Subordination proved self-reinforcing: crisis begot dependent recovery and renewed fragility.

Persistent TARGET imbalances now function both as evidence and as instruments of subordination. They sustain integration while embedding contingent debt relations that could destabilise deficit members in any exit scenario by requiring a recapitalisation of its banking sector (both private commercial banks and the Central Bank) in case it were a TARGET deficit member. Indeed, the changes that occurred in the wake of the Global Financial Crisis and of the Eurozone crisis, from the monetary to the fiscal and financial ones, have served the purpose of maintaining the Eurozone alive and the euro afloat, rather than improving the working of the monetary infrastructure and of the member states (Giordano and Lapavitsas, 2023).

Conclusion

This paper contributed to the study of the Eurozone and of monetary subordination. It was argued that the Eurozone is characterised by monetary subordination as a structural feature underpinned by a simple dynamic: fragmented monetary jurisdictions become hierarchically tiered, but the monetary system remains in place thanks to the hybrid working and plumbing of the single and common currency. Successively, it employed this subordination lens to examine the example of the Eurozone crisis, which was analysed as a crisis of subordination and of asymmetric – ‘subordinate’ – deleveraging, and, more generally, to show that (financial) fragility is enhanced by subordination working via money and finance. The Eurozone crisis was a crisis of subordination, and so was the prolonged failure to recover during the 2010s.

Following the subordination lens, it is important to stress a similarity between the subordinated countries in the EMU and the ‘periphery’ in the international financial system: the outcomes of monetary and financial subordination are remarkably similar, whilst the mechanisms of subordination necessarily become more subtle and elaborated – though also more formalised and documented – in the context of a single and common currency. Indeed, the case of the Eurozone even shows how monetary systems create persistent asymmetries as structural features of the monetary architecture, requiring apices and conferring significant power on the jurisdiction that takes over this role. Monetary subordination, in other words, does not have to – but can – be a consequence of hegemonic power, but it is a feature of monetary relations amongst economically unequal partners in the context of equal monetary exchange, and thus shapes the power relations of the agents involved.

In addition to the analytical contributions, this paper sought to prompt further research into multiple areas by providing a sound methodological and conceptual elaboration of monetary subordination.

First, other mechanisms of the single and common money should be conceptualised. This paper outlined three pillars that support the existence of monetary and financial subordination in the EMU following the necessary conditions gathered from EMEs, but it does not rule out the possibility of other mechanisms existing or reinforcing it.

Second, the financialisation of euro area members could be approached in a ‘subordinate’ fashion to complement the earlier ‘dependent’ form synthesised in the early 2010s by the Regulation Scholars. The ‘subordinate’ form that has been developed for EMEs can now be applied also to the Eurozone, with formal foundations previously absent.

Third, other monetary unions should be analysed following the same approach. For example, this paper suggests looking at the internal dynamics of the CFA Franc, rather than just being dependent on the French Treasury, to understand the structures and relations amongst its members. This, in turn, contributes to the theoretical and empirical understanding of the role of money for the International Financial Subordination also outside of monetary unions.

Footnotes

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.