Abstract

A widely held view in economics and comparative capitalism states that the crisis in the eurozone was a crisis of labour cost competitiveness. This view maintains that a divergence in unit labour costs engendered a cleavage between the euro area’s core and periphery. Critics have disputed this and drawn attention to export specialisation, along with global competition, rather than intra-European competition. To make progress on this agenda, this article focuses on structures of production as a source of crisis vulnerability. It advances the notion that countries have unique forms of articulation within global capitalism, and that this matters to understanding national crisis trajectories. Focussing on the Portuguese case, the article scrutinises the interactions between export specialisation, global competition and industrial decline. The article shows that Portugal’s current account deficit developed within a context of industrial change and deindustrialisation, which was facilitated competition from China and Eastern Europe. By stressing industrial patterns and global competition, the article provides a more concrete analysis of production than most accounts of the eurozone crisis.

Keywords

Introduction

The Global Financial Crisis (GFC) may have been global in scope, but its manifestations varied according to individual countries’ articulation within the world economy. Major channels of transmission included trade and financial flows (Akyüz and Paolo 2017). Portugal was crisis prone due to large payment imbalances and was first hit when the banks faced difficulties in accessing finance on international wholesales markets from 2008 (Bank of Portugal 2009; Lagoa et al., 2014: 102). The initial phase of crisis management witnessed counter-cyclical policies and generous transfers to finance under the European Union’s (EU) coordination (Costa and Castro Caldas 2014). When the GFC mutated into a ‘sovereign debt crisis’ (McNally, 20111), the Portuguese state was shut out of international financial markets. After a fierce pressure from domestic and international financial institutions, Portugal was the third eurozone country to request a bailout from the ‘Troika’ of the International Monetary Fund (IMF), European Commission (EC) and European Central Bank (ECB) in April 2011 (Stadheim 2021). The structural adjustment programme deepened austerity and opened the door to an unprecedented neoliberal restructuring (Costa and Castro Caldas 2014; Hespanha et al., 2014). After a recovery with almost 2% growth in 2010, Portugal fell back into recession and returned to growth only in 2014 (World Bank 2020a).

It is widely agreed that peripheral eurozone countries’ vulnerability stemmed from their large current account deficits and dependence on capital inflows. As a result, scholars in economics and comparative capitalism (CC) have devoted their attention to explaining how these imbalances developed. A commonly held view states that the imbalances resulted from a divergence in unit labour costs (ULC) between core and peripheral countries (Arestis et al., 2013; Blanchard 2007; ECB 2012; IMF 2011; Lapavitsas 2019; Lapavitsas et al., 2012; Pérez-Caldentey and Vernengo 2012). A different, albeit partly overlapping view maintains that the crisis (and the failure to resolve it) are results of the eurozone’s ‘flawed institutional design’ (Arestis and Sawyer, 2011; Arestis et al., 2013; Botta 2014; De Grauwe 2010). 1 Whilst the political and methodological differences between mainstream and heterodox interpretations should not be understated, analyses from both strands in economics share a logic that revolves around ULC (hereafter referred to as the ULC view’). The ULC view has underpinned painful labour market reforms imposed by the Troika, as well as labour legislation that national governments have introduced in the name of ‘competitiveness’, within a post-bailout context.

There is still scope for a much greater sensitivity to singularity when accounting for crisis vulnerabilities. Much of the literature in economics and CC focuses on what crisis ridden countries had in common. In the search for commonalities, unique historical and economic factors are often ignored. This article shows that detailed empirical case-based research can provide insights that challenge both the dominant and the heterodox crisis diagnoses, along with the policy prescriptions that follow. It is crucial to gain a more refined understanding of the causes of the crisis in the eurozone. The efforts to build back from the GFC and the Covid-19 pandemic need to be informed by a context specific understanding of trade, industrial development and competition.

The article shows that production matters to understanding the eurozone crisis. In international political economy it is widely known that ‘globalisation’ has been constituted by a new division of labour engendered by an expansion of world trade and internationalisation of production driven by global value chains and production networks (Charnock and Starosta 2016; McGrew 2018). Yet, the global economy does not feature as the main context in most analyses of the euro crisis. This article draws attention to the interaction between Portugal’s place within the global division of labour and the country’s pattern of product specialisation. It is inspired by studies that approach European integration and the eurozone crisis from a historical materialist perspective and which situate these within the totality of global capitalism (Bieler et al., 2019; Germann 2023; Poulantzas 1976; Romão 1982; Serfati 2016). The major advantage of this approach is a rejection of unilinear notions of development and an appreciation for historically and geographically specific expressions of capitalism. These studies stress the social relations of production that underpin capital’s drive towards internationalisation and regionalisation. In doing so, they are sensitive to the dynamic character of processes of regionalisation, and to how this is intimately intertwined with the exploitation of working classes across space. Moreover, they are informed by a political commitment to the betterment of working-class lives. While this provides a theoretical starting point, the empirical contribution advanced here builds on Storm and Naastepad (2015a) and Felipe and Kumar (2011). Their analysis holds that ULCs were largely irrelevant in causing the crisis in the eurozone and that the periphery’s main vulnerability was a specialisation in products that faced competition from China. Their empirical analysis is based on aggregate indexes for product specialisation. This is a crucial starting point, but their findings can benefit from being complemented by detailed qualitative analysis of how structures of production and processes of structural change interacted with competitive dynamics in the world economy, based on case study research.

Filling this gap, this article provides a single-case study of the Portuguese case. Some of the questions that guide the analysis are: How is Portugal integrated within global capitalism and how has this form of integration shaped the country’s crisis vulnerability? What does the country produce and export? Which countries compete in these sectors? Did Portugal’s export specialisation and exposure to competition from China and other low-wage economies cause the country’s external deficit? The article draws on trade data from the United Nations Statistical Division (UNSD) Commodity Trade (UN Comtrade) database which is available through World Integrated Trade Solution (WITS) and on production data from Eurostat and OECD. The article concludes that Portugal’s trade deficit must be understood in the context of deindustrialisation and industrial recomposition. Portugal’s traditional low-tech industries were in decline in the 1990s and 2000s, faced with competition from China and Central and Eastern Europe. Initially, their decline was accompanied by a rise of other manufacturing sectors, but the 2000s witnessed a generalised stagnation across manufacturing.

The article is structured as follows. Section two reviews the dominant interpretations of the crisis in the eurozone. Section three presents a series of critiques of the ULC view. Section four presents a case study of Portugal. Section five concludes.

Unit labour costs in theory and practice

ULCs can be defined as the ratio of a worker’s total compensation to labour productivity, or as the total labour costs per output. Labour costs include not only wages, but also fringe benefits, severance pay, wages in kind, social security, pension contributions and life insurance. Productivity refers to the number of units produced (e.g. pencils, litres of milk or cars). At firm level, ULCs can be derived by dividing total labour costs by the number of outputs produced. For firms, ULCs are important since labour costs represent a significant part of production costs. Savings made can be channelled into investments or more dividends may be transferred to shareholders. At the national level, many products are produced, and it is impossible to derive ULCs by dividing labour costs on the number of outputs. Therefore, at the aggregate level, output refers to the economy’s value added. ULCs are calculated as the ratio of labour compensation to real GDP. ULC data usually shows the percentage change from the previous year, and it tends to be expressed with reference to a base year. In discussions about international competitiveness, authors often refer to relative ULCs (RULC) where the ULCs of a given country are divided by the ULCs in a base country. In discussions about the eurozone, this base country is often Germany (Felipe and Kumar 2014: 483–491; Frumkin 2006: 251–252; OECD 2007; Powell 2013: 65).

In the beginning of the eurozone crisis, fiscal profligacy and national policy errors were seen as the main cause of turmoil. Mainstream institutions were concerned with problems in the public sector, and the public deficit and debt were heavily scrutinised (European Commission 2010; IMF 2009). The focus on states that had ‘spent beyond their means’ was a powerful narrative throughout the crisis. It provided the theoretical foundation for austerity. As the eurozone crisis spread to countries with fiscal surpluses prior to 2007–8 (i.e. Spain and Ireland), private sector competitiveness figured with increasing prominence in mainstream crisis diagnoses. The Twin-Deficit-Hypothesis focuses on the parallel existence of large budget deficits and current account imbalances (Mavroudeas and Paitaridis 2015). In this diagnosis, ULCs are central. For example, ECB (2012: 5) identifies that ‘[t]he onset of the financial crisis in 2008 has highlighted the problems of diverging external imbalances within … [the EMU] and the role of persistent losses in competitiveness’. The problem was that wages rose faster than productivity, translating into higher ULCs (ECB 2012).

A focus on ULC spans mainstream and heterodox literature in economics and CC. Storm and Naastepad (2015a: 959) point out how ‘[t]he dominant view both on the mainstream right and on the left, holds that the eurozone crisis is a crisis of labour cost competitiveness—with trade imbalances … being driven by divergences in relative unit labor costs [RULC]… between surplus and deficit countries’. In the Portuguese case, this view was advanced before the GFC. Blanchard (2007: 4) argued that from the mid-1990s, a weakening competitiveness (defined as ‘the inverse of unit labour costs relative to those in the euro area’) damaged the current account. A boom in private consumption and investment was accompanied by nominal wage increases which exceeded productivity growth. Consequently, ULCs rose. The boom turned into stagnation in the early 2000s, but RULC continued to increase (Blanchard 2007: 4–6). Blanchard proposed ‘competitive disinflation’ as a solution – a period where high unemployment leads to a decline in RULCs and an improved current account position. He held that ‘a decrease in nominal wages sounds exotic, but it is the same in essence as a successful devaluation’. He warned that the adjustment would be ‘long and painful’ (Blanchard 2007). Domestically, the finance minister who negotiated Portugal’s entry into the ERM in 1992 subscribes to the Twin-Deficit-Hypothesis: The entry level is always difficult … The idea of getting a different [exchange rate] was not realistic. What is correct, however, is that once you enter, you need appropriate policies with respect to wages and budgets. The opposite happened. Wages increased in Portugal far more than in any other country in the eurozone (Interview, Braga De Macedo 2014).

2

The mainstream’s ULC crisis diagnosis had powerful consequences in the world of labour. It provided the theoretical foundation for the strategy of internal devaluation. Within the astonishing scope of social spheres that underwent reforms, the wage-labour relationship was a main variable of adjustment. The structural adjustment programme attacked wages and trade unions’ power. Internal devaluation was presented as a national competitiveness strategy, but it had strong class dynamics. Its logic was to deepen exploitation by extending relative and absolute surplus value (Fine and Saad Filho, 2004; Stadheim 2017).

Post-Keynesians and Marxists dismiss the fiscal profligacy thesis and explain the current account imbalances between the eurozone’s core and the periphery (Arestis et al., 2013; Bibow 2013; Blankenberg et al., 2013; Botta 2014; Cesaratto 2015; Lapavitsas et al., 2012, 2019; Pérez-Caldentey and Vernengo 2012). By scrutinising trade and financial relationships between the core and peripheral eurozone countries, they have overcome the mainstream’s methodological nationalism. Yet, many of them replicate the focus on ULC. Post-Keynesians tend to approach the eurozone crisis through the notion of a ‘mercantilist’ project pursued by the ‘core’ countries. Marxists frame the discussion with reference to world money, imperialism and class. In both accounts the core’s trade surpluses and the periphery’s deficits are two sides of the same story. Regarding Portugal, Reis (2014) states as follows: Portugal was one of the peripheral economies which, since the preparation for the euro, registered a prolonged stagnation, with continuous current account deficits, leading to a high external indebtedness. Peripheral deficits are linked to the surpluses of the core and these fuel the corresponding financial capital’s recycling processes through credit to deficit countries (Reis 2014).

In the heterodox ULC view, the euro was the ‘original sin’ that led to the crisis because it fixed the exchange rate (Arestis et al., 2013: 24; Cesaratto 2015: 152). Peripheral countries entered at a high exchange rate, lost competitiveness (Lapavitsas et al., 2010: 6) and were left with no scope for devaluation except through internal deflation (Arestis et al., 2013: 24). Post-Keynesians hold that the euro was established in the context of an export-led-growth strategy pursued by core countries (Bellofiore et al., 2011; Cesaratto 2015; Pérez-Caldentey and Vernengo 2012; Stockhammer 2016). It was based on a policy of wage moderation where ULCs in the core were kept constant to enhance competitiveness. In the periphery ULCs increased, hence enhancing a real exchange appreciation (Pérez-Caldentey and Vernengo 2012). Bibow (2013: 360) states that the current account imbalances ‘ultimately go back to competitive wage restraint on Germany’s part since the late 1990s’. Similarly, Lapavitsas et al. (2010: 326–337) maintain that the EMU was a race-to-the-bottom with regards to wages and working conditions, and that it was won by Germany.

CC literature has much in common with heterodox economics. Many CC scholars have a similar view of competitiveness in the context of monetary integration to that of heterodox economics and see the euro area crisis as one of external price – and indeed labour cost competitiveness (Hall 2012, 2018; Stockhammer 2016). In the traditional VoC view, coordinated market economies such as Germany compete on quality and skills rather than price (Hall and Soskice 2001: 42). Its more recent formulations, however, attribute importance to price and labour costs when accounting for export success and failure. The coordinated wage bargaining system stands out as a guarantor of wage repression and hence falling or stagnant ULCs in the North. Meanwhile the South lost the capacity to devalue, and its ‘fractious’ union movement precluded wage discipline. Due to their respective institutional arrangements, the EMU suited Northern economies’ export-led model but not the Southern demand-led growth model (Hall 2012). The Keynes and Kalecki inspired Growth Model perspective sees financialisation as a major factor behind the imbalances, but also highlights ULCs when accounting for the relationship between demand-led and export-led growth models (Stockhammer 2016). Baccaro and Benassi (2017) hold that German exports are price sensitive, and some sectors increasingly so, but that overall export prices are more important than RULC. Baccaro and Tober (2022) have argued that wages determined export performance in the German case, but not in other countries.

In sum, while the heterodoxy does not concur with savage wage cut, but have instead proposed deeper EMU integration and reform, wage increases in core countries, or that crisis ridden countries should break out of the EMU, a core element of their analysis tends to replicate mainstream accounts. ULCs or export prices stand out as a root cause of uneven competitiveness, and wage repression the sole cause of Germany’s competitiveness (Storm and Naastepad 2015a). While mainstream economics sees Germany as a role model, the heterodoxy sees it as the source of the periphery’s problems.

Bringing in the role of product specialisation

There are longstanding critiques of ULC as a measure of competitiveness. The critiques include methodological, historical and logical inconsistencies. Firstly, some have pointed to the problems with calculating ULCs at the aggregate level rather than firm level. Since the national economy produces many goods and services, aggregate ULCs are effectively a ‘unitless magnitude’ (Felipe and Kumar 2014). Second, the ULC argument does not focus on actual labour costs and production levels, but rather the rate of change of the ratio between the two. Usually, the period analysed goes back to the mid-1990s, thus the historical trajectory of the current account and its relationship to ULC remain unexplained. Third, historical evidence shows that following World War Two, countries with the strongest reduction in price competitiveness were those whose market share increased the most (Felipe and Kumar 2014: 498). This puts into question the use of ULC as a proxy for competitiveness.

Fourth, the ULC argument assumes that labour costs are the only costs that determine export competitiveness. Storm and Naastepad (2015a: 966) note that ‘[w]hat matters in international competition is the “gross output price” of a product or service—the full (national accounts) price, which includes the costs of intermediate inputs and labor [and] a profit margin’. Felipe and Kumar (2011: 27) maintain that profits can also harm competitiveness. Therefore, ULC should be complemented by ‘unit capital costs’ (UCC). In 12 eurozone countries, Portugal included, UCC increased faster than ULC. For Storm and Naastepad (2015a: 966) Southern European economies’ exports are not sensitive to RULC, which ‘did not affect trade balances of Greece and Portugal in a statistically significant manner’ (cf. Storm and Naastepad 2015b; Storm and Naastepad 2015c). RULC account for 0.7% of the Spanish trade deficit and 7.9% of the Italian. The authors conclude that ‘[t]he bottom line is that RULCs are basically irrelevant’ (Storm and Naastepad 2015a: 966).

Fifth, the ULC argument rests on the assumption that peripheral eurozone countries are in direct competition with Germany. As Smith (2016: 88) says, the imperative that they must resort to savage wage cuts rests on the false premise that Germany is Greece’s, and other peripheral countries’ ‘principal rival’. In the heterodox scholarship, this assumption stems from the affirmation that the core’s surpluses and the periphery’s deficits have similar size. This appears convincing at the level of the eurozone as a whole, but it bypasses individual countries’ specific trading patterns. In the Portuguese case, this poses a problem since the most important trading partner is Spain, another ‘peripheral’ country. Following the ULC logic, it would be more appropriate to conclude that Spain is Portugal’s main competitor.

Sixth, in assuming that peripheral countries are in direct competition with Germany, the ULC argument tends to ignore the question of product specialisation. Mainstream and heterodox economics tend to disregard the fact that different countries provide different products to the global market and therefore compete on different markets. A notable exception includes contributions to the VoC and Growth Models perspectives, which are not oblivious to export specialisation. Felipe and Kumar (2011) maintain that Portugal and Greece do not compete with Germany, but with China, because their specialisation profiles are similar to those of the latter country. They compare peripheral eurozone countries’ export baskets with the German one and conclude that German exports are the second most complex and diverse in the world. Among the world’s 10 most complex products Germany controls a significant share. In contrast, Portugal ranks as 53rd, Greece 52nd, and China 51st (Abdon et al., 2010; Felipe and Kumar 2011). They suggest that product specialisation is the source of trouble: We believe that this is where the real problem of the peripheral countries lies. Their lack of competitiveness vis-à-vis Germany is not due to the fact that they are expensive (their wage rates are substantially lower), or that labor productivity has not increased. The problem is that they are stuck at middle levels of technology and they are caught in a trap. Reducing wages would not solve the problem (Felipe and Kumar 2011: 11).

This view is supported by Storm and Naastepad (2015a; 2015c) who hold that technological or non-price competitiveness is most important, not price competitiveness. They argue that export performance is determined by the composition of commodities for exportation and export destinations. While Germany’s export market share grew 0.45% on average between 1996 and 2007, this reflected an export orientation towards countries with high growth and an increasing specialisation in medium-tech products with a fast-growing market. Upper-market products with high to medium technology represent over half of exports and these are sold at high prices. In contrast, Portugal produces low-tech, and the destinations of Portuguese products are ‘saturated’. Of the hundred most complex products on the world market, Germany has a share of 18%, whereas Portugal controls 0.04% (Felipe and Kumar 2011: 29; Storm and Naastepad 2015a: 969). Portugal, Greece and Italy lost global market shares between 1996 and 2007, and this reflects an export specialisation which corresponds with that of China. Portugal’s export specialisation has a 52% overlap with the Chinese, whilst Germany has 22% (Storm and Naastepad 2015a: 968–969). If China were the comparator, and the policy of internal devaluation were to be pursued with this in mind, it would mean even deeper wage cuts than what was implemented through the Troika adjustment programmes (Smith 2016: 90). However, this would have been meaningless if, as argued by Felipe and Kumar (2011) a 20–30% reduction in nominal wages would not be enough to compete with Chinese wages.

These arguments find support in the literature on Portuguese industrial policy (see Godinho and Mamede 2016; Mamede 2014; Mamede et al., 2014). This literature maintains that Portugal’s external accounts eroded over the last two decades and that this stems in part from a specialisation profile which overlapped with that of China and Eastern European countries (Godinho and Mamede 2016: 334; Mamede et al., 2014: 251). Out of a group of 27 European economies, as of 2004, Portugal had the second highest correlation of revealed comparative advantage with Asian economies (Mamede 2014: 3–4). With the internationalisation of production and the adjustments to enter the EMU, Portugal’s traditional sectors faced competitive pressures (Mamede et al., 2014: 253, 269). Godinho and Mamede (2016: 334) speak of three competitive shocks: China’s entry into the WTO, the EU’s expansion to the East and the euro’s appreciation vis-à-vis the dollar between 2001 and 2008. Consequently, value added in manufacturing stagnated between 2000 and 2008 whilst almost one in every five jobs were lost. Textiles and clothing were both in decline.

The case of Portugal

Reference to global capitalism and the internationalisation of production is required to advance the present analysis of Portugal’s crisis trajectory. With this purpose in mind, it is relevant to reflect on the concept of integration. This is because different forms of integration into global capitalism engender different crisis vulnerabilities and mechanisms of crisis transmission. Drawing on Romão (1982) one can distinguish between ‘formal’ and ‘real’ integration. Formal integration refers to the legal-political forms that integration takes and include the membership of a given country in an economic organisation such as the EEC/EU. Real integration refers to the process of transnationalisation of capital. It concerns the forms of capital reproduction and accumulation, and how this takes place across national territories, according to the needs of capital in a particular phase of capitalism. Hence, Portugal’s integration into the world economy can be analysed in terms of the ‘the internal articulations of the Portuguese economic structure and its insertion into the framework of international economic relations’ (Romão 1982: 1087). Real integration includes the sphere of production and the sphere of circulation. This means that Portugal’s integration through trade flows and international production networks matters to the present analysis.

Bieler et al. (2019: 806–809) maintain that unevenness, which reflects the expansionary essence of capitalist accumulation and competition between capitals, has always been part of the geopolitical dynamics of European integration. They hold that the causes of the eurozone crisis date back to peripheral countries’ entry into the EEC/EU or before since free trade policies from the 1960s developed asymmetries between countries. Serfati (2016: 262) holds that what facilitated the collapse of Southern economies was their dependence on low-tech, low-skill and low-wage exports, and a financial subordination to foreign capital. In Portugal’s case, an economic approximation with Europe from the end of the 1960s occurred alongside the continuation of colonialism (Romão 1982). Poulantzas (1976: 24–25) insightfully captured Portugal’s contradictory integration into the world economy. He argued that the Portuguese regime ‘systematically promoted the investment of foreign imperialist capital’ – notably American capital – which invested ‘to directly exploit the popular masses’ in Portugal and to use the country as a ‘staging-post in the exploitation of other countries’, that is, the African colonies.

It can be expected that Portugal’s current account deficit prior to the GFC reflected a product specialisation which overlapped with that of China and Eastern European economies. Felipe and Kumar (2011) and Storm and Naastepad’s (2015a) findings call for a focus on patterns of product specialisation and global rather than intra-European competition. The 2000s were not only marked by the finalisation of the euro project, but also by China’s entry into the WTO in 2001 and the EUs expansion to Central and Easter Europe in 2004 and 2007. These events are usually not discussed in literature on the eurozone crisis. The evidence presented below corroborates the argument developed by Felipe and Kumar (2011) and Storm and Naastepad (2015a) but shows that the Portuguese story is somewhat more complex. Portugal’s traditional low-tech export industries such as textiles and clothing were in decline in the 2000s, but their demise dates further back. Initially, the effect on the trade balance was mediated by the rise of medium-tech sectors. The novelty of the 2000s was not the erosion of the traditional sectors, but rather that virtually all sectors were in stagnation or freefall.

Before analysing Portugal’s exports, some stylised facts concerning the payment imbalances are needed. First, the large current account deficit developed in the context of a transition from strong economic growth in the second half of the 1990s to stagnation in the 2000s. Between 1995 and 2000, the average growth rate was 4.1%, but this dropped below 0.9% between 2001 and 2005 (World Bank 2020a). The strong growth rates in the 1990s were driven by a boom in construction, and the subsequent stagnation by its hollowing out. Monetary integration was intertwined with financial liberalisation, and the resulting financial inflows were directed towards housing and construction, as the heterodox literature has discussed extensively (Lapavitsas et al., 2012; Previdelli and Souza 2012; Rodrigues and Reis 2012; Rodrigues et al. 2016). Hence, Portugal differed from Greece, Spain and Ireland, which did not enter a slump at the turn of the millennium.

Second, Portugal’s trade deficit preceded the current account deficit. Portugal witnessed a growing current account deficit from the mid-1990s – before other crisis ridden eurozone countries. The trade deficit dates much further back. In fact, the external balance of goods and services was negative the entire period from 1970 to the GFC. This is highly relevant since heterodox analyses see the euro as the main cause of the periphery’s competitiveness problem. From the mid-1980s, Portugal’s trade deficit was accompanied by a growth of secondary income, largely consisting of personal transfers, which helped keep the current account in balance (IMF 2016). Large outwards migration flows from Portugal had ensued from the outbreak of the colonial wars in the 1960s (Romão 1982). Remittances accounted for almost 9% of GDP in the early 1980s but became negligible by the turn of the millennium (World Bank 2020b). Hence, Portuguese emigrants’ income is part of the balance of payment trajectory – an insight that is usually left out of discussions about the eurozone crisis.

Third, Portugal’s negative trade balance derives from an import growth which exceeded export growth (World Bank 2020c). In the 1990s, this was mainly due to imports of consumer goods, which increased as a share of total imports. The share of capital goods also increased (WITS 2022a). The decade before Portugal’s EEC membership was marked by rapid trade orientation, but in the early 1990s exports declined and stagnated thereafter (World Bank 2020c), thus contrasting with the global trend towards trade expansion. One cannot speak of an erosion of export capacity – due to ULCs or any other factor – but it is relevant to pose the question of why exports failed to keep up with imports.

To assess the relationship between Portugal’s export specialisation and the trade deficit, it is necessary to decompose the general index of complexity. Felipe and Kumar (2011) and Storm and Naastepad’s (2015a) argument is based on aggregate indicators for technological complexity. Their findings can benefit from being complemented by a detailed analysis of structures of production and external imbalances. Therefore, this paper uses UN Comtrade, the largest repository of international trade data, and WITS, which comprises several databases including UN Comtrade and the WTOs Integrated Trade Data Base.

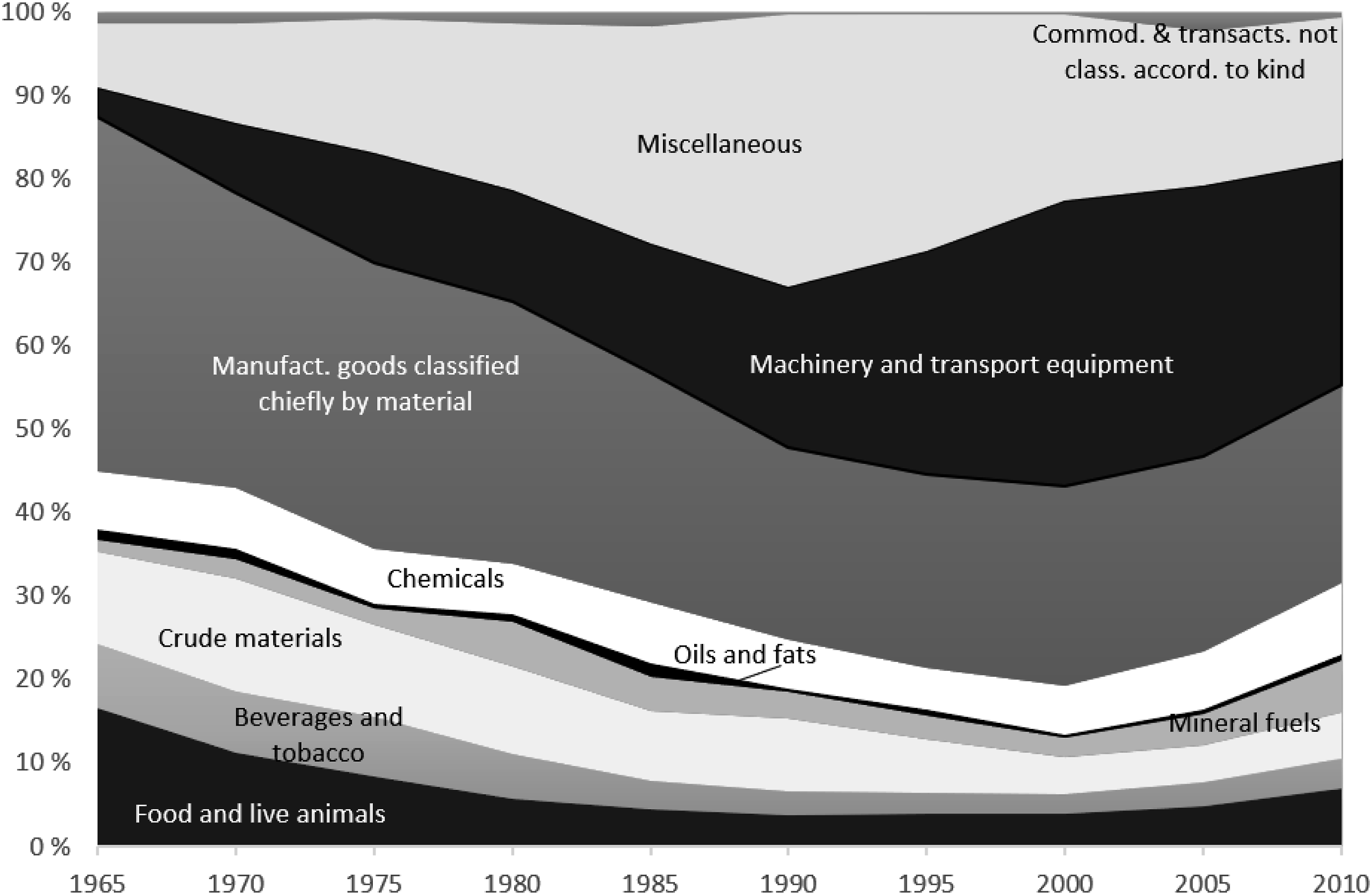

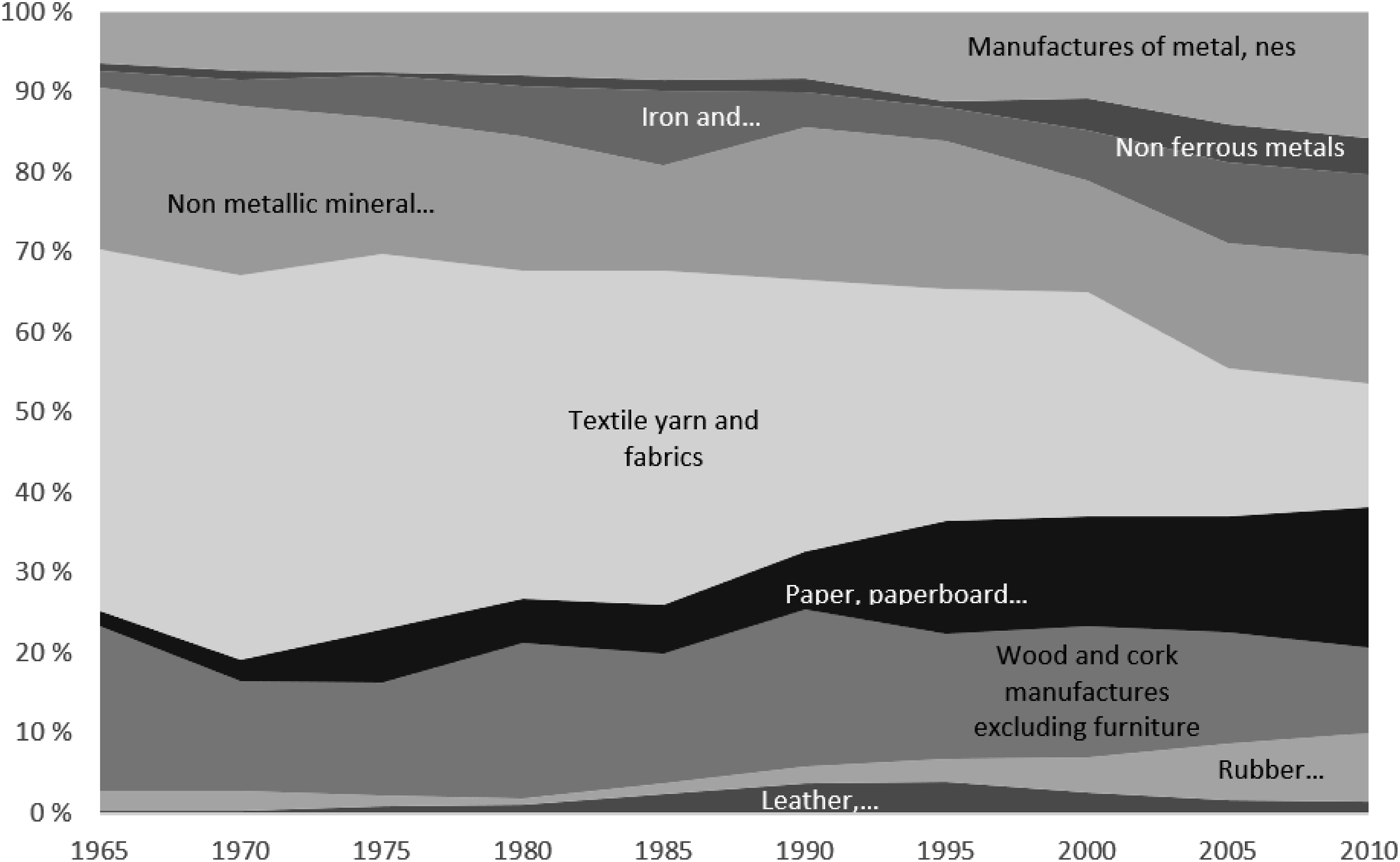

Among Portuguese exports to the world, the most important category from the 1960s was ‘manufacture goods classified chiefly by material’ (Comtrade 2019). This accounted for 42% of exports of goods in 1965 (Figure 1). The category includes traditional exports such as textiles, clothing and wood. Within this category the most important subsectors were ‘textile yarn, fabrics, made up articles’ and ‘wood and cork manufactures’ (Figure 2). By 1990, Portuguese exports were still heavily concentrated in the traditional sectors. ‘Textiles and clothing’ represented 29% of export revenue whilst ‘footwear’ represented 8% and ‘wood’ 12% (WITS 2022b). Beyond the traditional exports, ‘machinery and electrical equipment’ accounted for 13% of export revenue (WITS 2022b). Portuguese exports of goods to the world, by classification (1965–2010). Notes: Full series names from the top are (1) Commodities and transactions not classified according to kind; (2) Miscellaneous manufactured articles; (3) Machinery and transport equipment; (4) Manufact goods classified chiefly by material; (5) Chemicals; (6) Animal and vegetable oils and fats; (7) Mineral fuels, lubricants and related materials; (8) Crude materials, inedible, except fuels; (9) Beverages and tobacco; (10) Food and live animals. The figure is based on trade values in US$. Source: UN Comtrade. Classification SITC, Rev 1. Commodity codes 0–9. Portuguese exports of manufactured goods classified chiefly by material (1965–2010). Notes: Full series names from the top are: Manufactures of metals, n.e.s.; (2) Non-ferrous metals; (3) Iron and steel; (4) Non-metallic mineral manufactures, n.e.s.; (5) Textile yarn, fabrics, made up articles, etc.; (6) Paper, paperboard and manufactures thereof; (7) Wood and cork manufactures excluding furniture; (8) rubber manufactures, n.e.s., The figure is based on trade values in US$. Source: UN Comtrade. Classification SITC, Rev 1. Commodity codes 61–69.

As expected, Portugal’s export structure did represent a vulnerability, exposing the country to competition from China and Central and Eastern Europe. In 1992 ‘textiles and clothing’ were responsible for 29% of Chinas export revenue, ‘machinery and electrical equipment’ for 14% and ‘footwear’ for 6% (WITS 2022c). The rates were almost identical to those in Portugal. Textiles and clothing had thrived after Portugal joined EFTA in 1960 (Truett and Truett 2019) but Anderson (1962) insightfully warned that the industry was uncompetitive and dependent on colonial exploitation: ‘The basis of much of this industry is artificial, as it is heavily dependent on forcibly depressed cotton prices in the colonies, and drastically protected markets in the same territories’. In 1960, the colonies were the source of 82.7% of raw cotton imports, and the destination of 35.8% of cotton manufacturing exports (Anderson 1962). 3

By the eve of the colonial liberation, Portuguese textile and clothing produce was protected by the 1974 Multi Fibre Agreement (MFA) which imposed quotas on developing countries’ exports to EEC countries (Fernandes and Tang 2020). Trade with Europe was progressively liberalised through EFTA, the EEC and the Single Market (Amador and Opromolla 2009). In 1994, the WTO Agreement on Textile and Clothing substituted the MFA. The quotas were phased out and the sectors were fully integrated into the GATT/WTO system by 2005. This liberalisation exposed Portuguese producers to competition from China and other low-wage countries (Fernandes and Tang 2020; Lains 2018; Schütz and Palan 2016; Truett and Truett 2019). The EU’s expansion to Eastern and Central Europe added to the low-wage competition.

Competition particularly came from Bulgaria and Romania where textiles and clothing were important sources of export revenue (Amador and Opromolla 2009). There, textiles and clothing represented 14% and 13% of export revenue, respectively in 2007 (WITS 2022d, 2022e). Portuguese wages in the sector were low compared to the EU average (45% in 2001) but in Bulgaria and Romania they were much lower (6% and 9%) (Truett and Truett 2019). Alongside the EUs eastwards expansion, textiles and clothing lost importance as a source of export revenue in Portugal. In 2003, these sectors accounted for 16% of export revenue, but by 2008, it had dropped to 10% (WITS 2022b). Thus, Storm and Naastepad (2015a) and Felipe and Kumar (2011) correctly identify export specialisation as a source of the imbalances. While labour costs appear to have played a role, it was intra-industry wage differentials across different geographies that mattered to the textile and clothing industry’s trajectory. This is different from the rate of change of aggregate ULC, which is the ULC view’s major focus.

Deindustrialisation in Portugal’s traditional sectors nevertheless dates further back than the 2000s. The contribution of textiles and clothing to total export revenue was in freefall already in the early 1990s. From having represented over 30% of export revenue in 1988, it had dropped to just over 23% by 1995. Portuguese footwear was in decline from the mid-1990s and its contribution to total export revenue dropped from 10% in 1994 to 4% in 2007 (WITS 2022b). According to the Association for Portuguese Textiles and Clothing, the industry ‘faced several competitive shocks’ and a continuous turmoil’ composed by several ‘succeeding crises’. These crises included the liberalisation of world trade, China’s entry into the WTO and the EU’s Eastern enlargement (ATP 2018). The latter two events represented continuity rather than rupture.

It is essential to stress the dynamic aspect of Portuguese exports. In the 1990s, the traditional low-tech sectors were substituted by medium-tech. Despite the erosion of textiles and clothing, the share of manufacturing goods of total exports increased from 78% in 1988 to 83% in 1993 and remained stable until 2003 (WITS 2022f). Low wages had been a driver of industrial relocation towards Portugal in the 1960s and 1970s, but by the early 1990s, the Iberian Peninsula was ‘superseded by Central Eastern Europe in its function of low-wage periphery’. Many transnationals shut their plants in Spain and Portugal and moved their operations elsewhere (Serfati 2016: 266–277).

Despite this offshoring, Portuguese exports did not deindustrialise overall. What took place was a recomposition of manufacturing exports, which reflected a spatial reorganisation of certain value chains. The share of consumer goods in total exports declined from 64% to 54% between 1993 and 2003 whilst the share of capital goods increased from 13% to 22%. ‘Machinery and transport equipment’ overtook ‘textile and clothing’ as Portugal’s most significant export sector. From 1993 to 2003 this sector’s contribution to export revenue increased from 21% to 34% (WITS 2022f). ‘Transportation’ and ‘machinery and electrical equipment’ also rose. The export capacity in machinery and transport equipment was largely driven by FDI in the automobile sector (Amador and Cabral 2008; Cabral 2004). In 1995 Ford and Volkswagen opened the automotive assembly plant AutoEuropa in Setúbal outside Lisbon. This occurred within a context of a spatial reorganisation by German automobile suppliers, as producers relocated production to low-wage economies (Krzywdzinski 2014). AutoEuropa was responsible for 12% of exports and 2.1% of GDP just 1 year after its inauguration. With the most capital-intensive components being imported from countries such as Germany, the UK and France, and with product strategy, marketing and investment decisions carried out in Germany and the USA, Portugal’s insertion into this value chain appears to have been a subordinate one (Bieler et al., 2019: 812; Wise, 2017). Nonetheless, machinery and transport equipment made up for lost export revenue resulting from deindustrialisation in textiles and clothing. This substitution of one manufacturing branch by another is not accounted for by the critiques of the ULC argument (Felipe and Kumar 2011; Storm and Naastepad 2015a), who do not analyse peripheral countries’ dynamic industrial trajectories.

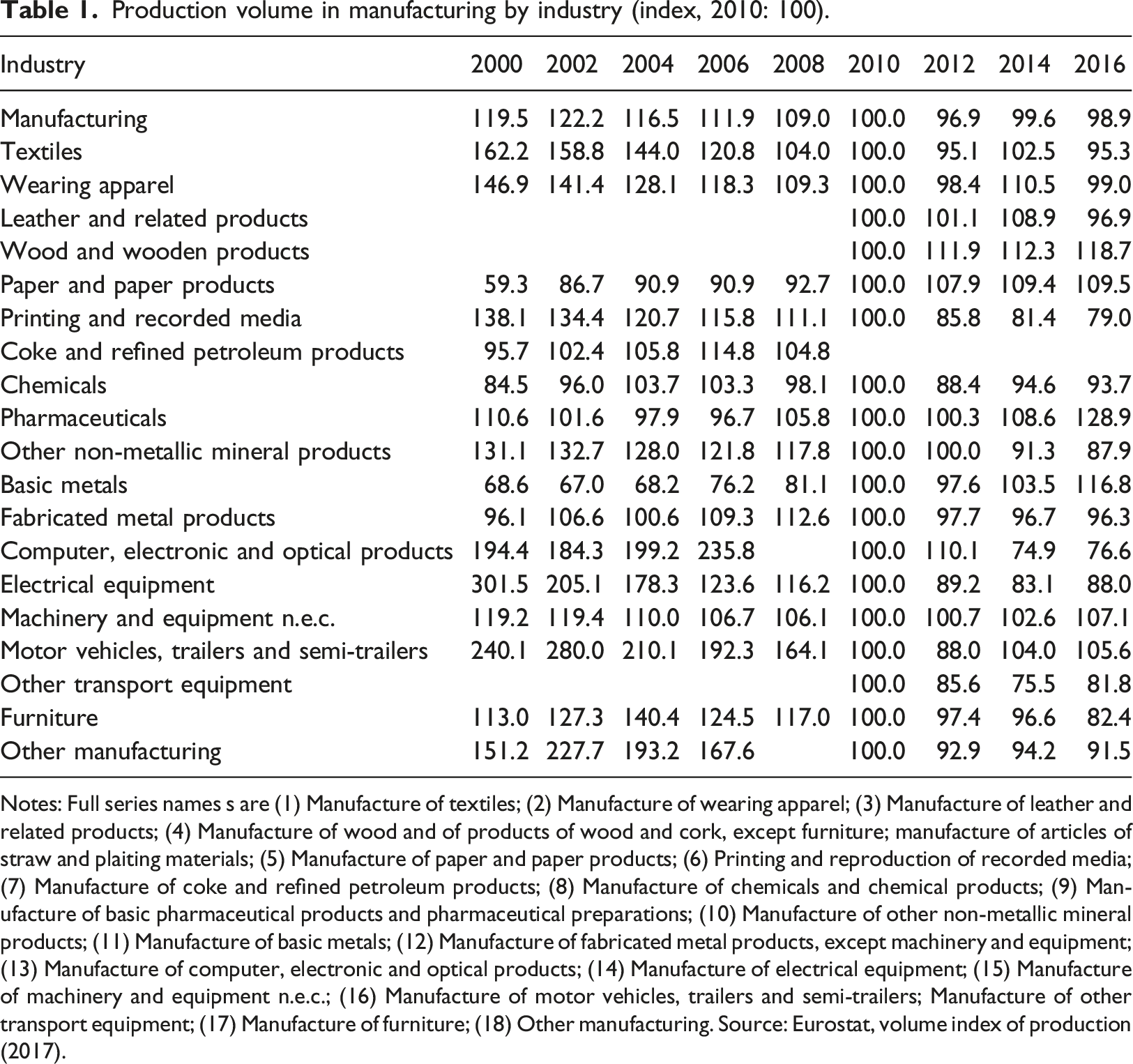

Portugal’s crisis trajectory did not end with a mere substitution of one manufacturing branch by another. Instead, the turn of the millennium initiated a period of stagnation and generalised deindustrialisation. This shift occurred within a transition from an investment surge in the second half of the 1990s to a slump in the 2000s, as Mamede (2014) points out. Gross fixed capital formation reached 28% of GDP in 2000 but dropped to 23% of GDP in 2008. From having been well above the euro area average, it dropped to average and thereafter far below (Eurostat 2017a). Reflecting this, the production volume in construction and manufacturing decreased significantly before the GFC. OECD’s records of the volume of production in manufacturing, which starts in 1955, show that the volume produced was almost consistently rising until 2002. Thereafter, it was in sharp decline. Using 2015 as a base year, the peak volume in 2002 was 42% higher than in 2015 (OECD 2020). The volume produced in construction peaked in the early 2000s and then plummeted (OECD 2019). Although textiles and clothing deindustrialised prior to 2003, there had not been an overall decline in Portugal’s total manufacturing production. But from 2003 Portugal deindustrialised at the aggregate level. The decline was sharp between 2002 and 2009. Thus, in aggregate terms, deindustrialisation occurred from the early 2000s until the GFC.

Production volume in manufacturing by industry (index, 2010: 100).

Notes: Full series names s are (1) Manufacture of textiles; (2) Manufacture of wearing apparel; (3) Manufacture of leather and related products; (4) Manufacture of wood and of products of wood and cork, except furniture; manufacture of articles of straw and plaiting materials; (5) Manufacture of paper and paper products; (6) Printing and reproduction of recorded media; (7) Manufacture of coke and refined petroleum products; (8) Manufacture of chemicals and chemical products; (9) Manufacture of basic pharmaceutical products and pharmaceutical preparations; (10) Manufacture of other non-metallic mineral products; (11) Manufacture of basic metals; (12) Manufacture of fabricated metal products, except machinery and equipment; (13) Manufacture of computer, electronic and optical products; (14) Manufacture of electrical equipment; (15) Manufacture of machinery and equipment n.e.c.; (16) Manufacture of motor vehicles, trailers and semi-trailers; Manufacture of other transport equipment; (17) Manufacture of furniture; (18) Other manufacturing. Source: Eurostat, volume index of production (2017).

The empirical findings presented here pose theoretical challenges to the most widespread interpretations of the crisis in the eurozone and of core periphery relations. These challenges have powerful ramifications in the realm of policy making. The simplest point that can be drawn out is that production matters to understanding the Portuguese crisis. Alongside the development of a large current account deficit unfolded a process of industrial decline. Thus, something else than a mere divergence of ULC vis-à-vis core EMU economies occurred. The UCL view looks at the ratio between labour costs and output, but it does not consider the quantities produced and exported. Most analyses have ignored or heavily underappreciated country specific patterns of production. From the onset of the eurozone crisis, the ‘competitiveness problem’ emerged as a major policy focus and a hegemonic discourse. Underpinning it was a narrow, cost centred notion of competitiveness (Miró 2021). With such a general problem, no detailed examination of national industries was needed. The ULC story offered a simple problem and a simple solution. It was the perfect diagnosis for a one-size-fits-all approach to competitiveness which underpinned the structural adjustment programmes in the eurozone’s periphery. An alternative approach to competitiveness would have focused on concrete sectors of production, industrial upgrading and an active industrial policy. This was absent in all the memorandums of understanding that were imposed on the Eurozone’s periphery. In fact, central proponents of internal devaluation expressly rejected active industrial policies (Blanchard 2007).

In dissecting Portugal’s pattern of export specialisation, the present analysis has offered an alternative account of trade imbalances. In doing so, it has added to the heterodox literature on the eurozone crisis. In taking a bird’s eye perspective on intra EU/EMU imbalances, this literature has too often missed out on country specific particularities. While some of the recent CC literature has paid more attention to export specialisation than the heterodox economics literature, some country specific details necessarily get lost in the focus on typologies. This article has shown that Portugal did face competition, but this competition came from China and low-wage economies in Eastern Europe. It was specific to the type of products Portugal exports. The demise of the traditional sectors – notably textiles and clothing – reflected a gradual exposure to competition through liberalisation. This included China’s entry into the WTO, but it started before. The EU’s eastward expansion added to the competitive pressure. Portugal no longer served as a low-wage periphery, and Eastern European economies outcompeted Portuguese wages in textile and clothing. Labour costs played a role in Portugal’s industrial trajectory, but international intra-industry wage differentials appear to have been more important than aggregate ULCs. In scrutinising these dynamics, this paper has challenged the heterodox notion that peripheral eurozone countries were in direct competition with Germany. If production and industrial collapse matter to understanding the Portuguese crisis, such processes of structural change might have generated crisis vulnerabilities elsewhere. Since singularity and context matter to understanding concrete crisis trajectories, this requires detailed, empirical, case-based investigation.

Conclusion

This article has advanced the notion that specific counties have unique forms of articulation within global capitalism, and that this matters to understanding crisis trajectories. It posed the question of what caused the crisis in Portugal. To provide an answer, it critically interrogated the view that diverging ULC trajectories were the main cause of the eurozone’s imbalances. Across strands in economics and CC a range of ULC centred crisis diagnoses have dominated the discussions. This paper showed that the ULC view studies these imbalances at an excessively aggregate level and relies on a single indicator as a proxy for competitiveness. It assumes that Greece and Portugal are in direct competition with Germany. This literature usually bypasses fundamental questions about what is produced and exported, or indeed whether production has collapsed altogether. It avoids approaching the eurozone’s imbalances from a global perspective and circumvents crucial questions around single countries’ roles in the global division of labour. The ULC view does not investigate individual countries’ patterns of export specialisation. Consequently, it has a flawed interpretation of competition within the world economy. Given the ULC view’s policy influence over competitiveness strategies and labour markets (but also radical left-wing proposals such as leaving the EMU) it remains crucial to gain a more refined understanding of single countries’ trade trajectories.

In providing a single-case study of Portugal, the article made several methodological points. First, it insisted that singularity matters. A lack of sensitivity to context underpinned the strategy of internal devaluation, which followed a race-to-the-bottom logic. Heterodox economics has offered an alternative to the mainstream’s methodological nationalism, yet, in focussing on trade and financial flows, it often takes an intra-regional perspective. Single-case studies are well placed to shed light on the merits and limitations to crisis interpretations that take a bird’s eye perspective. Second, history matters to understanding the crisis. The literature on the euro area crisis usually looks at the development of external imbalances from the mid-1990s or 2000. This study showed that several factors that shaped Portugal’s current account trajectory date much further back. This included Portugal’s former colonies in Africa, FDI that sought to exploit cheap labour in Portugal, and remittances sent by Portuguese emigrants. A third methodological point concerns geography and space. The article approached the crisis in Portugal by looking at changing patterns of regional integration, global competition and the geographical reorganisation of specific value chains.

This article stressed Portugal’s productive structure, the pattern of export specialisation and exposure to global competition as drivers of crisis vulnerability. It showed that behind the large current account deficit hides a trajectory of deindustrialisation and industrial recomposition, and subsequently, a generalised industrial decline. At a time when world trade expanded exponentially, Portuguese exports stagnated. The trajectory in textiles and clothing was critical. Textiles and clothing accounted for over 30% of exports in the late 1980s but embarked on a path of sustained decline. The sector faced competition from Eastern European economies and China (and not Germany). In the 1990s this decline occurred alongside the rise of medium-tech exports. Portugal benefitted from the spatial reorganisation of automobile production, although the country’s place within this value chain appears to have been a subordinate one. Also in this sector, a subsequent reorientation towards Eastern Europe seems to have added to the pressure on trade. This, together with the longstanding erosion of textiles and clothing and a hollowing out of industrial production more generally negatively affected export revenue. The 2000s were marked by stagnation or contraction in almost all manufacturing sectors. In sum, production matters to understanding the crisis.

Footnotes

Acknowledgements

The author is grateful to Alfredo Saad Filho, Engelbert Stockhammer, Eugénia Pires, George Labrinidis, Ricardo Paes Mamede and Emiliano Perra for comments on previous drafts and helpful discussions. She also thanks two anonymous reviewers for their generous feedback which helped to improve the manuscript.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Ethics approval

The research conducted for this manuscript received the ethics approval from SOAS University of London.

Data availability

The data that support the findings of this study are publicly available. All sources of data can be found in the list of references.