Abstract

As climate change mitigation efforts intensify, land-based solutions such as carbon sequestration and biodiversity enhancement are emerging as a key strategy requiring substantial financial investment. This paper examines the current Scottish approach to achieving net zero, highlighting the role of corporate welfare in shaping market development. Using interviews and document analysis in a process tracing design, the study shows how the private sector plays a key role in leading and shaping climate change mitigation efforts such as voluntary carbon codes and public programs to fund them. It introduces the concept of assetization cascades to capture how corporate welfare initiatives support and drive the creation of new natural capital assets by drawing in more actors that engage in assetization. The findings contribute to the literature on corporate welfare, assetization and the evolving role of the state in climate governance.

Introduction

The escalating impacts of the climate and environmental crisis demand urgent action, not only through technical innovation but also through large-scale mobilization of financial resources. Among the emerging strategies experiencing a surge in investment, land-based solutions have gained prominence as pillars of climate mitigation (EEA, 2024). They include land-based carbon sequestrations marketable as carbon credits, regenerating land for use as a natural carbon sink, and improvements in biodiversity. Such innovations for natural capital investment have grown in recent decades as they are often regarded as the solution to mobilizing investment to mitigate the climate and environmental crisis. They are one of the many approaches to green transition policies that are supported by public funds and part of a wider development of current forms of state intervention (Bulfone et al., 2023; Larsen and Jackson, 2025; Lepont and Thiemann, 2024; Wansleben, 2024). In the United Kingdom, and particularly in Scotland due to its geographic features and landownership pattern, land-based approaches to climate mitigation have become central to net zero strategies. Supported by voluntary carbon markets and public funding with few conditions attached for land use changes, these policies have fueled an surge in rural land acquisition by diverse investors. Among them are unlikely buyers, ranging from asset managers and insurance companies to beer breweries and a fast fashion mogul. As diverse as they might seem, and indeed many of their motives are diverse, they all recognize the potential that Scotland’s land offers for making profits through natural capital assets, and not least through the corporate welfare provided by generous and unconditional funding schemes of which the effectiveness is still unclear. But how did these corporate welfare programs form and expand for natural capital assets such as voluntary carbon credits when the market for these assets had not even been established?

This paper examines Scotland’s road to net zero as a case showing how climate mitigation-related public corporate welfare measures were expanded through and with infrastructure-building efforts by financial actors and key intermediaries. These actors used their instrumental influence and brought established landowners on board to shape a voluntary carbon market characterized by low regulation and generous, largely unconditional public funding. The Scottish government readily adopted and supported this approach to meet its climate development goals (net zero by 2045), co-creating a natural capital-based climate agenda with the private sector and maintaining this trajectory with minimal adjustment until today. The initial creation of natural capital assets, specifically, carbon credits from woodland and peatland restoration, attracted further investors, who in turn contributed to building additional infrastructure for new asset classes. As a result, the natural capital sector continues to expand, along with the scope and scale of corporate welfare funding.

Previous literature has discussed how constructing or governing infrastructure can manifest in corporate welfare spending (Cooiman, 2023). I build on this argument by first demonstrating how the private sector plays a critical role in shaping the assetization process, influencing markets and driving corporate welfare programs for newly created assets. This influence arises from the private sector’s participation in infrastructure building as a co-creation process alongside the state. Second, I argue that corporate welfare for assetized land can trigger what I call assetization cascades, in which asset creation accelerates as more actors are drawn to the sector by enhanced profit opportunities supported by corporate welfare. As these actors enter, they further contribute to assetization, infrastructure development and initiatives for additional corporate welfare measures. In this way, corporate welfare initiatives can catalyze self-reinforcing assetization cascades, leading to the continual creation of new assets.

The article proceeds as follows. The second section briefly introduces land-based climate solutions to provide contextual information. The third presents the theoretical framework, discussing corporate welfare and its relation to assetization, and the fourth outlines the methodology and case. The emergence of Scotland’s natural capital strategy is analyzed in the fifth section, with the conclusion discussing the findings and their broader implications for climate governance.

Land-based solutions to climate change

Land plays a critical role in addressing the climate and environmental crisis. Improved land management can support a more balanced ecosystem that is beneficial to overall biodiversity and sustainable food production. Furthermore, land can be a carbon source or sink. Land use, while not responsible for the majority of carbon emissions, accounts for around 11% of global net anthropogenic greenhouse gas emissions (Skea et al., 2022: 7). Importantly, the right land use can also capture carbon, alongside its other ecosystem benefits, and offers the greatest potential for emissions reductions outside of phasing out fossil fuels (Nabuurs et al., 2022: 750).

The path to harnessing the potential of land in climate mitigation is far from straightforward, however. It requires a balancing of societal needs, for example, in terms of food production or housing, with ecological restoration. High uncertainty and constrained state capacity (Findeisen, 2023) fuel fierce debates on the right mitigation and adaptation measures. The need to mobilize financial flows to fund those measures creates windows of opportunity for various actor groups, including state and private sector actors, channeling financial support for specific strategies either through private, public or blended investment.

One approach governments use to evoke financial flows into land use changes is to allow for and even support financially valuing natural capital, that is, the world’s natural assets, and integrate those natural capital assets into institutions and markets. An expression of this is the global and national certification standards that emerged to secure carbon credits or other ecosystem services out of regenerative measures. Examples include voluntary standards for enhancing biodiversity, forest coverage or peat health. Forests are a natural carbon sink and provide additional environmental benefits depending on type and location. Peatlands share this potential: while drained peatland emits carbon, restored peatland absorbs it, contributing to net zero goals.

Carbon or ecosystem benefits can be quantified and made marketable by codes. Credits resulting from such codes can be sold on markets, in the case of carbon credits, to businesses aiming to offset their emissions. This nature-based approach complements technological solutions like direct air capture and Carbon Capture and Storage. Though voluntary markets remain smaller than compliance markets, their role is growing (Climate Change Committee, 2022). Voluntary carbon markets nevertheless face credibility challenges, especially in the Global South (Greenfield, 2023). For credits to be effective, they must be additional, meaning that emission removal or avoidance would not happen without revenue from selling the credits. This is not always easy to guarantee, nor is the permanence of such measures and the corresponding emission reduction or extent to which the buyers’ emissions are not avoidable. As voluntary initiatives are run mostly by non-state actors, their reliability can vary. Such quality concerns make domestic, government-backed standards attractive. Marketed as “homegrown” and restricted to domestic trade, they promise greater accountability.

In the UK, such initiatives have been created in an attempt to finance the land use changes needed to reach net zero: First and foremost, they are the Peatland Code (PC) and the Woodland Carbon Code (WCC), but also similar approaches to draw financial investment into the country’s natural capital. Both codes are equally recognized as part of the UK’s net zero strategy. They count towards the national greenhouse gas emission reduction targets, even if, compared to other emission trading systems, the voluntary carbon schemes are not mandatory or legally binding (UK Woodland Carbon Code, 2023a). These approaches can only be effective, however, if the projects lead to long-term land use changes. As they are often maintained under voluntary codes, it is not entirely clear how these long-term changes can be legally guaranteed and enforced. Furthermore, no Corresponding Adjustment as required by Article six of the Paris Agreement (UNFCCC, 2016) is implemented in regard to how these private voluntary offsets contribute to the UK’s national strategy. This means that they count fully towards the UK’s and its nations’ national goals under the Paris Agreement (Brander et al., 2022), which makes these solutions prone to double counting.

Corporate welfare and climate finance: Dynamics between state and private sector

The increasingly critical climate challenges require a huge amount of (financial) investment. In Scotland alone, the investment required to reach net zero is estimated to be £5 billion per year until 2030, with most to fund land use (Scottish Parliament Information Centre, 2024). However, who pays for that investment and how it is best spent is far from straightforward. In the context of neoliberal developments, with progressively more public assets privatized (Christophers, 2019) and public functions increasingly delegated to private actors, the state’s room for maneuver to act without taking the private sector into account is considerably restricted. Despite the private sector’s pivotal role, the state’s is far from irrelevant, and arguably experiencing renewed importance. Not only is the state integral to market making in its specific contingencies (Fligstein and Dauter, 2007; Polanyi, 1944), but it also acts as a structuring force for the actors involved, setting necessary institutional frameworks and distributing resources, as Silverwood and Jackson (2025) have shown for renewable energy markets in the UK.

One expression of a structuring activity towards public development goals is corporate welfare, that is, the transfer of (financial) resources from the state to corporate actors in order to reach public development goals with no or only weak conditionalities attached to those transfers (Bulfone et al., 2023). It entails an active state but with reduced steering capacity. The concept of corporate welfare has recently been picked up again in the political economy literature by Bulfone et al. (2023) and can be located among de-risking research and approaches (Dafermos et al., 2021; Gabor, 2021). Applied corporate welfare measures can manifest in a variety of forms, ranging from direct financial transfers to tax exemptions, market making and de-risking interventions. Previous definitions were relatively broad, encompassing most public transfers targeting businesses (instead of individuals) (Farnsworth, 2013: 1). Bulfone et al. (2023) therefore especially highlight the importance of weak conditionality for distinguishing corporate welfare from other forms of state transfers. They argue for the necessity to observe both the nominal terms of agreement for the transfer and its actual impact on corporate behavior (Bulfone et al., 2023: 259). Corporate welfare, in this form, implies a structural power relation between a weak state and the private sector, as no or weak conditionalities reduce the state’s capacity to enforce its development goals in a more consequential way.

Scholars such as Lindblom (1977) have long explored the mutual dependency between business and state in capitalist societies and have herewith refined the theory of structural power, evaluating its variation (Hacker and Pierson, 2002), and the variety of scope conditions that influence especially businesses’ power mechanisms vis-à-vis the state (James and Quaglia, 2019; Kastner, 2018; Trampusch and Fastenrath, 2021; Young and Pagliari, 2017). Businesses can benefit from structural power, threatening “exit” or investment withdrawals (Culpepper, 2015), for example, by employing instrumental power through concrete actions in the form of lobbying practices, donations or knowledge transfers, or without the active engagement of business, depending on how realistic policy-makers perceive the exit threat (Bell and Hindmoor, 2014; Fairfield, 2015).

Such systemic pressures and power struggles make corporate welfare transfers an integral part of capitalist societies (Farnsworth, 2013). Corporate welfare is a manifestation of structural power dynamics that benefit the private sector and stem from the state’s need to attract investment, for example, to finance the green transition, and prevent businesses from exiting. In order for this positionality of state and private actors to be established, however, the corresponding infrastructure must be in place (Cooiman, 2023). While governments are most certainly involved in such market making, they are not necessarily the dominant actor, nor does the impetus always come from them. Corporate welfare programs can also be initiated by the private sector, which can enter as a first mover, building a market infrastructure by defining the conditions, and getting the state on board as a co-creator by convincing it to support the market with corporate welfare with weak conditions (Cooiman, 2023).

Corporate welfare and assetization cascades

Such dynamics can be observed in frontier markets such as land use-based voluntary carbon and natural capital markets. The state can ease financial, judicial or organizational hurdles for actors with corporate welfare programs in order for the corresponding sectors to expand and develop. This concerns the impact of corporate welfare on the establishment of a new market, but also more broadly the establishment and revaluation of innovative instruments for climate mitigation measures through assetization processes. Using corporate welfare to change the value of goods or activities that foster climate protection shifts the boundaries of existing financially viable climate mitigation measures. In this process, new asset classes can be established (e.g., carbon credits). Assets are “the institutionalization and ongoing presence of a property title that affords a claim on value” (Tellmann et al., 2024: 4). As such, assets must be created through assetization processes. Assetization has come into scholarly focus in recent years (Adkins et al., 2020; Birch and Muniesa, 2020; Birch and Ward, 2024; Langley, 2021). It is the process of turning things into a (financial) asset class through socio-technical institutions and involves an element of abstraction. For example, land-based voluntary carbon credits are not found in nature. Rather, socio-technical institutions such as legal tools are needed to help abstract private property claims from the carbon emitted or not emitted from a plot of land. Furthermore, institutions such as (voluntary) codes and auditing institutions, as well as legitimacy for the abstractions to be accepted, are all pivotal in allowing land-based carbon to become an asset class. The infrastructure for new assets to function and be accepted must be built, either by the state or by private actors. While the state’s role in assetization processes would still benefit from further theorization, there is already significant scholarly literature on the topic. Adisson and Halbert (2022) show how the state itself can be a major actor by transforming its public properties into financial assets. However, governments can also assist in and foster assetization, for example, for geopolitical ends (Ward et al., 2023), sometimes retaining some form of political obligation for the private sector actors involved (Rogers, 2023). Furthermore, governments can also be pawned by the private sector as Golka (2023) found how financial intermediaries use deceptive frames to depoliticize the way the assetization process is perceived by third parties, including governments. Another major aspect of the state-assetization nexus is the state’s role in providing and delineating the legal and regulatory context for assetization dynamics (Langley, 2021; Muniesa et al., 2017; Pistor, 2019), acting as the structuring entity. This goes from seemingly banal matters such as securing private property rights to more complex considerations that support private sector confidence, such as public guarantees or auditing functions. Specifically, assets that are very illiquid, such as landed property, are often not attractive per se to a broad range of investors but rather only to a selective group. If it is possible to further assetize them by abstracting a more liquid form of property from the otherwise illiquid asset, for example, by creating sellable carbon credits derived from landed property ownership, they can gain in attractiveness. For that to happen takes state support through legal guarantees, for example of contracts (Bogner, 2024) and, potentially, through corporate welfare measures that de-risk and incentivize private actors. In this way, new asset classes can be created.

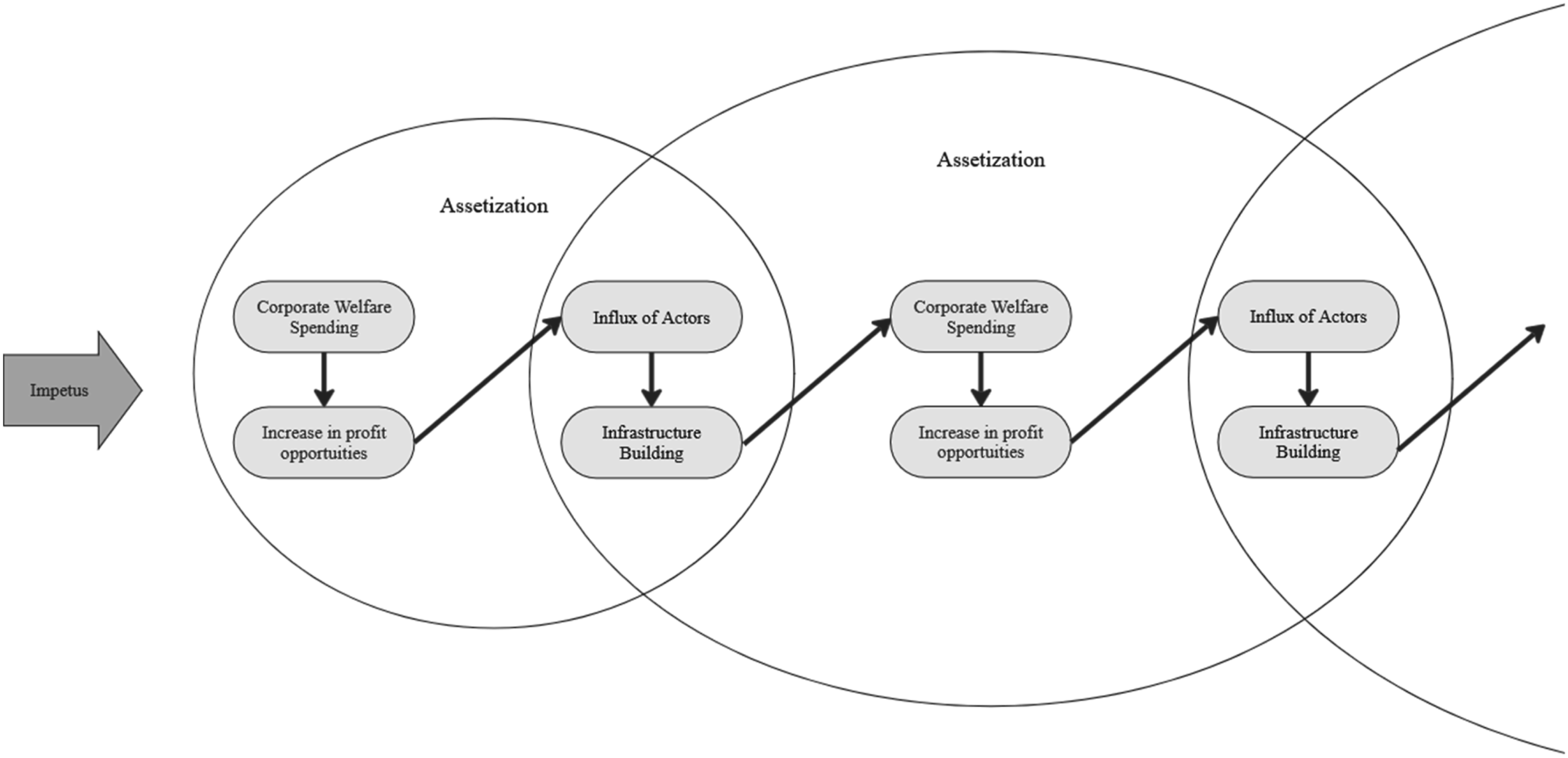

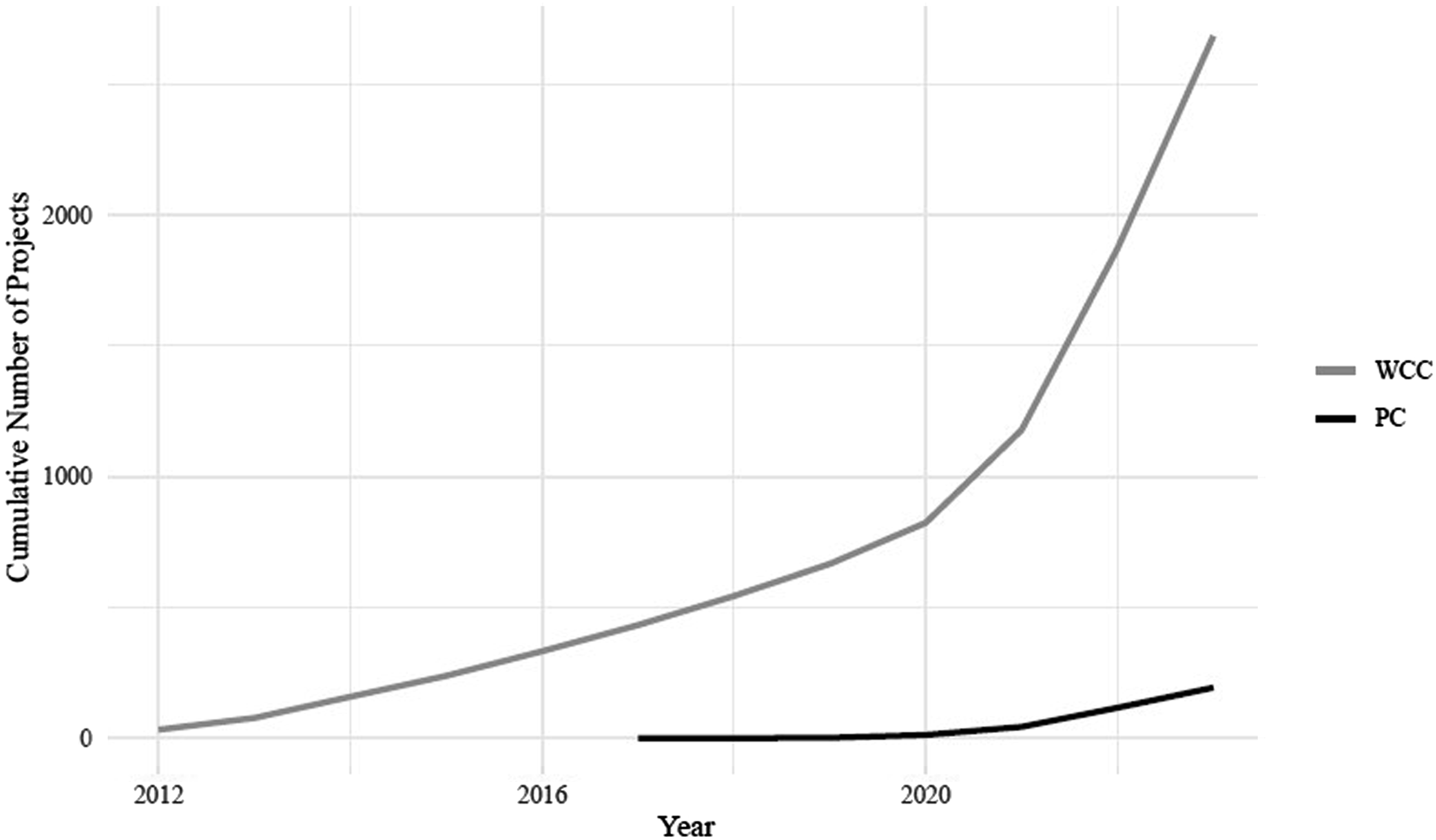

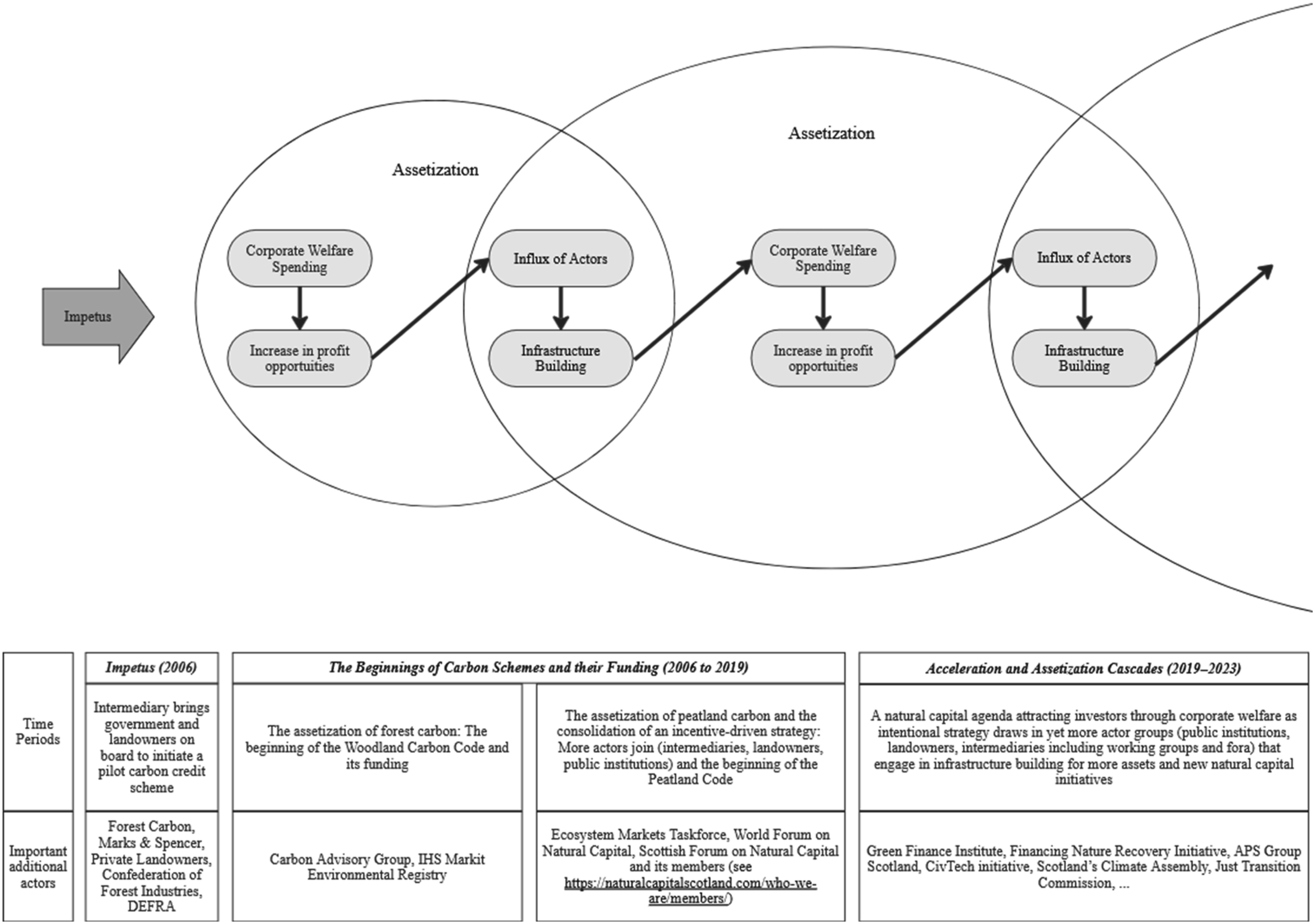

Corporate welfare can thus support the assetization process through two consecutive steps. First, unconditional funding or monetary incentives increase the expected yield from a prospective asset and its infrastructure, making the opportunity attractive to a broader range of actors. Second, the influx of these actors enables further infrastructure building for additional assets, which can itself be supported by additional corporate welfare measures provided as structure around these assets and their markets by the state. The interplay of all of these factors can produce what I call assetization cascades. Assetization cascades rely on attracting a sufficient number of interested actor groups that build asset infrastructures and increase the market, a goal corporate welfare achieves by raising expected profits and reducing risks. Infrastructure building can be done by intermediary groups such as task forces, working groups, consulting firms, law firms and managers and, in co-creation with the state in a structuring role, for upholding legal claims and setting the institutional grounds for such infrastructure. In voluntary carbon markets, for instance, actor groups such as established landowners, financial investors, and intermediary organizations are drawn in by the promise of large returns. These groups may seek to expand their profit opportunities by developing additional assets and advocating for new corporate welfare programs, such as biodiversity credits. In this way, corporate welfare does not simply support individual markets but can catalyze a broader expansion of asset classes. Thus, as displayed in Figure 1 I propose that corporate welfare programs can result in cascade effects as they draw in even more private sector actors that, in turn, build new infrastructure and assets (in co-creation with public institutions) for additional corporate welfare programs. Assetization cascades. Cumulative number of carbon code projects (WCC & PC); Sources: Freedom of Information request to Scottish Forestry and IUCN UK Peatland Code website (IUCN UK Peatland Programme, 2025).

Corporate welfare implies a structural dynamic between the state and the private sector stemming from the state’s systemic need to attract investment, for example, in climate change mitigation efforts. However, I argue in line with Cooiman (2023) that the state-centric focus of the corporate welfare literature should be expanded by bringing the private sector’s role in building infrastructure for corporate welfare to the forefront. It can take an active, co-creating role, and this infrastructure building can consist of or lead to assetization processes, especially regarding frontier markets such as natural capital markets.

An important aspect to consider at this point is that these assetization dynamics are based on profit seeking. This means that the measures are not necessarily the most effective with regard to alleviating climate and environmental pressures and might just be the most profitable options for the moment, not least because they are supported by corporate welfare.

Methodology, data and the Scottish case

This research contributes to the previous literature on corporate welfare and assetization by shedding light on their structural interaction and the actions of private market actors and the state. To investigate market development for natural capital assets, actors’ infrastructure building, and cascade effects, it uses a single-case process tracing of the Scottish road to net zero, embedded into the broader UK context. The UK overall sits at the extreme end of the spectrum of corporate welfare for private sector climate action, especially regarding support for voluntary carbon markets. It is one of the few western countries with a national domestic and government-backed voluntary carbon market as one possibility for natural capital investment. Other countries, such as the USA, Germany, France and Spain, have some projects, but many of them are not on a national scale and often do not entail such an established market and funding (Cevallos et al., 2019). As “concepts are often defined by their extremes” (Gerring, 2007: 101), exploring a case such as the UK aids observation of the processes and causalities that must subsequently be tested in further research. This single, within-case study offers a more inductive exploratory form of process tracing (Mahoney, 2015; Trampusch and Palier, 2016), which not only traces causes-of-effects by reconstructing the sequence of events of the emergence of this climate finance corporate welfare system but also investigates cascade effects and connects them with corporate welfare schemes.

A variety of data sources are used in this research to investigate the emergence of natural capital markets and corporate welfare schemes. Primary documents from parliamentary sessions and government agencies and data on voluntary carbon markets, the Scottish net zero and natural capital strategy are reviewed. Data on the funding and number of carbon code projects were obtained through Freedom of Information requests to NatureScot and through statistics provided by Scottish Forestry. Additionally, news sources and interest group statements were examined. Semi-structured interviews conducted in 2023 with 19 politicians, experts, owner group representatives, intermediaries and other relevant actors were used to triangulate the other data and to obtain additional insights (details in the Appendix 1). Interviewees were chosen purposively in order to gain specific information and to mitigate non-response bias (Lynch, 2013); interviews lasted between 30 min and two hours.

Scotland as a crucial case in the UK’s land-based natural capital strategy

Scotland is a crucial case among the UK nations and especially relevant with regard to land-based natural capital solutions due to its geographical features. According to the Climate Change Committee, Scotland is home to around half of the UK’s trees and 70% of its peatlands, thus accounting for an estimated 30% share of the UK-wide costs associated with land use (change) (Scottish Fiscal Commission, 2024). Since the most mature parts of the UK natural capital market relate to woodland (through the WCC) and peatland creation (through the PC) as of now, Scotland’s geographical and geological features, with its vast peatlands and land suitable for forestry, make it the most attractive location for those wanting to participate in this market in the UK. Additionally, the high Scottish land concentration plays a major role for this attractiveness, as projects are more likely to be introduced at scale due to profitability. So far, Scotland has been defined by an extremely high ownership concentration and some dominant (partly aristocratic) large-scale landowners. These established landowners have a long time horizon for their landed assets. They therefore tend to be risk averse and mostly welcome new businesses and investors due to their willingness to invest (e.g., for aging farmers without willing successors or landowners looking for joint venture opportunities) and to test new ventures such as carbon credits. In recent years, interest in the Scottish land market has increased among a range of such non-traditional or new entrant investors, due to the lucrative opportunities for natural capital investment. Of major interest to them is establishing areas that can be used for offsetting or insetting carbon or creating other profitable environmental benefits. Here, especially land in the worst ecological condition has the biggest margin for improvement and can generate the most carbon credits.

All landowner groups interested in carbon markets and/or land use change for climate mitigation purposes rely heavily on intermediaries: Those facilitating acquisitions, such as Savills, but especially working groups which work on coding natural capital and developers or land management companies that know carbon codes, their requirements and the markets. The number of such organizations and companies has grown in recent years, and some are actively involved in creating investment opportunities and markets for their clients in addition to land management alone. Some were formed by existing landowners, some by corporations that use the carbon codes and some specifically to fill the demand for developers (Mann and Matijevic, 2022). Many intermediaries operate mostly in Scotland, but others also have UK-wide business or membership. As discussed later, intermediaries have successfully kicked off the voluntary carbon codes project in Westminster. Those codes, the PC and WCC, are the most prominent features of the Scottish land-based natural capital strategy, even though a variety of potential assets has emerged over time. While the two certification schemes are related, they are administered separately by different bodies. The WCC has consistently remained under public sector oversight, whereas the PC has been managed by the IUCN UK National Committee, part of an international nature conservation organization, via an appointed executive board. Scotland has more and larger (by land area) projects under the WCC and PC than the rest of the UK (UK Woodland Carbon Code, 2023b).

Supported by corporate welfare measures, this focus on Scotland also shows in the public spending distribution in the UK, with a total of 151.3 million pounds in grants and partnership funding between 2019 and 2022 in Scotland (England: 22 million pounds; Wales: 3.3 million pounds) in forestry alone (Forest Research, 2022). Thus, Scotland has far-reaching public financial support for land use change under the two codes. For the WCC, the public financial support is distributed through the Forestry Grant Scheme, which replaced the Scottish Rural Development Programme in 2015 and is now administered by Scottish Forestry. Through the Forestry Grant Scheme, up to 85% of the costs of land use change can be covered by a public grant (mostly it is around 50%), and a maintenance payment rate can be won (Interviewee 6). For the PC, the Peatland ACTION Fund was established in 2012 as part of the Scottish strategy for peatland restoration. To administer the funding and codes, it partners with NatureScot (rebranded in 2020), the agency responsible for delivering nature conservation and heritage targets. The Peatland ACTION funding covers as much as 100% of the costs. There is no comprehensive insight on how much of the cost of restoration schemes comes from private sources apart from the purchase price of the land, if it is not already owned. A study by Okumah et al. (2019) on the cost of peatland restoration in the UK found that public support schemes fund the majority of restoration costs, although the sample is very small and it is only an approximation.

The funding schemes are not entirely free of conditions, and in some cases funds could be withdrawn for non-delivery, for example, if woodland work is not completed (Swindon, 2022). Also, withdrawal from carbon credits is possible in principle. In the case of Peatland ACTION funding, however, such conditionalities only exist for 10 years, while even the PC requires a project to run for at least 30 years; and, of course, there is little gain environmentally in upholding the land use change for only 10 years (Brander and Broekhoff, 2023). There is no consideration of what would happen if the land use changes again after this period. This and the absence of ongoing monitoring of grant use qualify these measures as a form of near unconditional corporate welfare. Regarding land use changes, the necessity for restorative changes to be long-term is another problematic aspect with respect to conditionalities. Even if conditionalities are introduced during the project period, private property rights and the freedom to sell the land (as the codes are not legally binding), for example, after project completion, severely restrict control over the long-term funding impact.

My analysis of what factored into Scottish climate mitigation strategy in its current form, with special regard to land-based solutions and related corporate welfare, starts with the beginnings of the first UK carbon schemes in 2006. I distinguish two periods: The moderate developments of 2006 to 2019, and 2019 to 2023, when public and private policies and actions on climate change intensified.

Scotland and its journey to net zero

The beginnings of carbon schemes and their funding (2006 to 2019)

The assetization of forest carbon

The natural capital strategy in the form of the domestic voluntary carbon schemes initially derived mainly from the instrumental influence of intermediaries at a time when environmental change and destruction were discussed but not seen as the most pressing issue. The initial idea came in 2006 from the founders of Forest Carbon, a land management company and intermediary. With a couple of partners (Marks & Spencer and some private landowners), they started planning and lobbying the Forestry Commission under the Department for Environment, Food & Rural Affairs (DEFRA) (Forest Carbon, 2023). DEFRA set up a Carbon Advisory Group of UK forest industry and carbon market experts in 2008 and launched the WCC in 2011 after a pilot phase. In the following year, the WCC market evolved, not least through infrastructure development around it, such as the IHS Markit Environmental Registry, which displays carbon credit data and makes them marketable. This system, in which the first UK land-based carbon assets would function, and its legitimacy were thus built, enabling the first assetization of land-based carbon. From the beginning, it was possible to use public grant aid to grow forest eligible under the WCC. While not “advertised” explicitly by the government at this early stage as an integral part of the voluntary carbon code, it was nevertheless mentioned as a possibility in guidance on the WCC (UK Woodland Carbon Code, 2012).

The assetization of peatland carbon and the consolidation of an incentive-driven strategy

While the WCC progressed, a DEFRA publication led to the establishment of the Ecosystem Markets Taskforce, a group of business and finance representatives. They recommended the development of a UK-wide Peatland Code (Ecosystem Markets Task Force, 2013; Reed et al., 2013), laying the groundwork for the PC infrastructure. They specifically required a Peatland Code to be oriented on the WCC and to join and contribute to growing the voluntary market and related infrastructure such as “technical and market support services” (Ecosystem Markets Task Force, 2013: 20–21). The UK government responded in 2014 that it would follow the Task Force’s recommendation, mobilizing financial and other resources to support a pilot UK Peatland Carbon Code (DEFRA, 2013: 19-20) and investigating what was needed to “unlock” private investment, again acting in a structuring way by opening up development of an institutional framework for intermediaries such as the Task Force to operate within. At the time, the topic of peatland restoration was discussed independently on the political level, for example, in the Scottish Parliament, but no clear path forward had yet emerged. Up for debate were more monetary incentives as well as motivational strategies to raise awareness of the importance of peatland and the possibility of cooperation between local corporations and landowners to showcase their eco-philanthropy (Scottish Parliament, 2012). In 2013, the pilot phase of the Peatland Code started under the leadership of a professor formerly at Birmingham University and DEFRA. The code was subsequently launched at the World Forum on Natural Capital in Edinburgh in 2015. In this way, the initial land-based carbon asset under the WCC was the catalyst for further assetization, leading to the second land-based carbon asset under the PC also initiated by private sector actors. New actor groups joined the scene and, together with the government, built the infrastructure to assetize peatland carbon and secure corporate welfare. From the beginning, the PC was supported by novel corporate welfare funding in the form of Peatland ACTION. The codes and the initial funding around them, for the WCC a continuation of previous forestry grants and for the PC newly established Peatland ACTION funding subject to few conditions, were supported by a willing government and organizations such as the Scottish Forum on Natural Capital (Interviewee 9) which has a plethora of intermediary and private sector groups as members, such as consulting and advisory firms, financial actors including green finance actors and landowners and managers 1 . Established by a variety of non-governmental organizations in 2013 as part of the inaugural World Forum on Natural Capital (attended mostly by the private sector but supported by the former First Minister, showing how the Scottish government acted as a structuring force to legitimate the work of various intermediary organizations), the Forum was influential in putting “natural capital” as a concept on the government’s agenda and stimulating the carbon codes debate (Interviewee 9). However, pressure on governments from a variety of actor groups, mainly from the green finance sector, to achieve their development goals, and the idea that this was only possible with extensive support to the private sector to invest accordingly, was present even earlier, from the codes’ beginnings (Interviewee 11). Initially, carbon credit generation was not the focus, and public financial support for land use-related carbon reduction was discussed as an independent matter. Later, however, carbon credit schemes, which provide a more lucrative source of profit for owners than land use change alone and were set up by a mix of green finance actors and government agencies, gained importance. More and more woodland and peatland creation grants were submitted and approved (Scottish Forestry, 2018: 5) and more explicitly related to carbon credits. While the codes and their funding were set up to attract new private funds (Kinver, 2015), established landowners were not considered as major actors in funding climate mitigation measures on their land. Considering the extremely long-term perspective of very large established landowners, there was no initial rush among them to engage in the carbon markets (Interviewee 2; Interviewee 10). While there was certainly some interest in the carbon codes, there was also much hesitation around joining a risky frontier market. Furthermore, it was just not the major topic on the agenda of landowners (Scottish Parliament, 2015). The government, while not focusing enormously on regulating those established landowners (seldom discussed in parliament), mostly used incentive structures to bring them on board. There were occasional calls to increase demands on the different owners, but these were not followed up (e.g., Scottish Parliament, 2017). While climate change was already a pressing issue before 2019, it had not yet attracted the Scottish government’s full attention and focus. As established landowners were also laggard, financial actors and intermediaries had room to shape actions and measures significantly by building infrastructure for the codes and securing their position. The grant schemes that were previously mostly independent of the carbon codes were used increasingly by private business and investors. Established landowners, not yet willing to engage in a risky frontier issue, solidified their position as a vital stakeholder that needs to be convinced rather than obliged to get on board. Both of these strategies resulted in path dependencies revolving around a strategy based on natural capital assets at the time when the road to net zero accelerated from a side issue to the main focus.

Acceleration (2019–2023)

A natural capital agenda: Attracting investors with corporate welfare as intentional strategy

After a previously relatively sluggish uptake, in 2019, climate change became the center of attention, and the voluntary carbon market kicked off with an influx in demand and attention to the issue (see Figure 2).

In that year, the government amended its net zero targets through the Climate Change (Emissions Reduction Targets) (Scotland) Act 2019. While the target in the whole of the UK is net zero by 2050, Scotland had set itself the more ambitious legally binding target of 2045. Reaching the UK-wide net zero target by 2050 depends on Scotland achieving net zero by 2045, as Scotland has a greater capacity than the rest of the UK to implement changes (Net Zero, Energy and Transport Committee, 2021). In this context, Scotland also established a Just Transition Commission and Scotland’s Climate Assembly as advisory groups. Building back “green” after the COVID-19 pandemic, and changes accompanying the end of Common Agricultural Policy (CAP) subsidies, led the Scottish government to consider drawing more on private sector resources and contributions in the redesign (Scottish Government, 2020). While these resources are, for example, supposed to be channeled into energy projects through Scotland’s Green Investment Portfolio, land use-related measures formed a main point in the updated strategy and were granted significantly more funding (Macfarlane and Brett, 2022; Scottish Government, 2020). Despite the Just Transition Commission’s recommendation to attach conditions to funding now that it was used more, this seemed to have been no pressing topic for the designers of the updated strategy.

A major acceleration resulted from both the publication of the “Finance Gap for UK Nature Report” (eftec and Rayment Consulting, 2021) commissioned by the Green Finance Institute (a private organization aligned with the City of London) and from COP26 in the fall of 2021. During COP26, former First Minister of Scotland Nicola Sturgeon highlighted governments’ fundamental role in channeling private investment, underscoring the role of public funds (Greater London Authority, 2021) and committing to a “values-led and high-integrity market for natural capital” (Scottish Government, 2022b). Shortly after the summit, NatureScot and the government first mentioned a finance gap in nature funding of 20 billion pounds in connection with grant programs and other corporate welfare measures, which has since been dominant in the discourses around Scottish net zero. The finance gap is portrayed as a constant threat to reaching targets and has justified various measures to attract private capital (Scottish Government, 2022c; NatureScot, 2023). The figure has not been independently researched by a public body as of now and is currently under growing criticism, as it does not seem to hold up to scrutiny (Macfarlane, 2024). However, it is repeatedly used by public agencies and government representatives to justify unconditional or nearly unconditional funding in natural capital markets that by now is directly tied to and advertised for the assetized land uses (e.g., NatureScot, 2023a). The Scottish government is under pressure to deliver under public scrutiny and with ambitions to trump Westminster. NatureScot has since heavily promoted the corporate welfare approach to assetized land use on the government’s behalf. The Peatland program manager framed it as follows: “We need to make this market attractive to private finance, and we’re not waiting. We’re talking to various companies, we’re going to financial advisers. The government has committed 250 million pounds – about $327 million – and we’d like landowners to take advantage of that resource.” (Segal, 2022).

So far, the government is opting to continue incentivizing new investors rather than regulating established landowners. As Lord Deben (Member of the House of Lords and Chair of the Climate Change Committee) put it at a meeting of the Net Zero, Energy, and Transport Committee, investment needs to come to the UK and the government needs to set the context in which that investment comes (Net Zero, Energy and Transport Committee, 2021). As the interest from investors is there, it only needs to be encouraged with the right steps (Hurley et al., 2023). Large established landowners often also position themselves along these lines and seek cooperation with financial actors in the form of joint ventures that allow for a customized contract (compared to tenancies) (Interviewee 4). Financial actors such as the Financing Nature Recovery UK initiative align with the interests of private landholders by expressing that this group should receive “fair payments for using land to provide these services” (Financing Nature Recovery UK, 2022: 12).

With the infrastructure in place and the conviction that the ground must be set for private finance to invest in Scottish natural capital, new actors are coming in that work on assetization of land-based natural capital.

Assetization cascades: More corporate welfare, more actors, and more assets

More corporate welfare opportunities for net zero measures are planned or already established and continue to carry weak conditionalities. They include a price floor guarantee, “a mechanism that guarantees a minimum price floor for peatland projects aiming to sell carbon credits, de-risking private investment and project delivery” (APS Group Scotland, 2023: 14), likely making the assetization of land use in as many ways as possible even more attractive. The Scottish government has been criticized for not routinely assessing the impact of policies and spending on emissions (Auditor General, 2023: 16) to ensure that grants and funding contribute significantly to the net zero target. With some exceptions, however, this has so far not led to much public demand for more scrutiny. Such profit opportunities have the potential to attract even more actors that will work on constructing asset and corporate welfare infrastructure.

Apart from funding for projects that can generate carbon credits, the Nature Restoration Fund also supports projects “that restore wildlife and habitats on land and sea” (NatureScot, 2023c). A grant scheme through the Facility for Investment Ready Nature in Scotland (FIRNS) has been set up by the Scottish government, NatureScot, and the National Lottery Heritage Fund. Justified by statements made by the Green Finance Institute in 2021, the scheme can help projects succeed on natural capital markets and attract private investment.

Not only has the Scottish government increased opportunities for grant funding, but it is also facilitating creation of new assets: Currently, its CivTech initiative is working on integrating biodiversity credits into Scotland’s net zero strategy. Supported by a variety of public and private groups, such as the Scottish Nature Finance Pioneers, NatureScot and the Scottish government’s Private Investment in Natural Capital program, the initiative is supposed to be modeled after the WCC and PC and to “help address the £20 Billion finance gap for nature in Scotland” (CivTech, 2022). At the time the research was conducted, no dedicated funding was yet in place for biodiversity credits specifically. However, there were already some blended finance initiatives in place that support the formation of a biodiversity credits market (Nature Finance Pioneers, 2022) and explore how public funds can support private investment models in biodiversity (e.g., Glencripesdale temperate rainforest restoration project) (NatureScot, 2022). These initiatives contribute to assetizing the biodiversity of land, making it open for investment.

Many other types of nature credits (water quality credits, soil codes, etc.) and corresponding blended finance initiatives are planned or being considered (Scottish Government, 2024) and explored by variously composed working groups. In these considerations, the Scottish government has prioritized the position of the private sector and sidelined the possibility of increased regulation (partly to be addressed by a potential new land reform). This not only increases the corporate welfare and actor density in the existing codes and thus creates feedback loops but also further drives the cascading spread of infrastructure-building and assetizing dynamics.

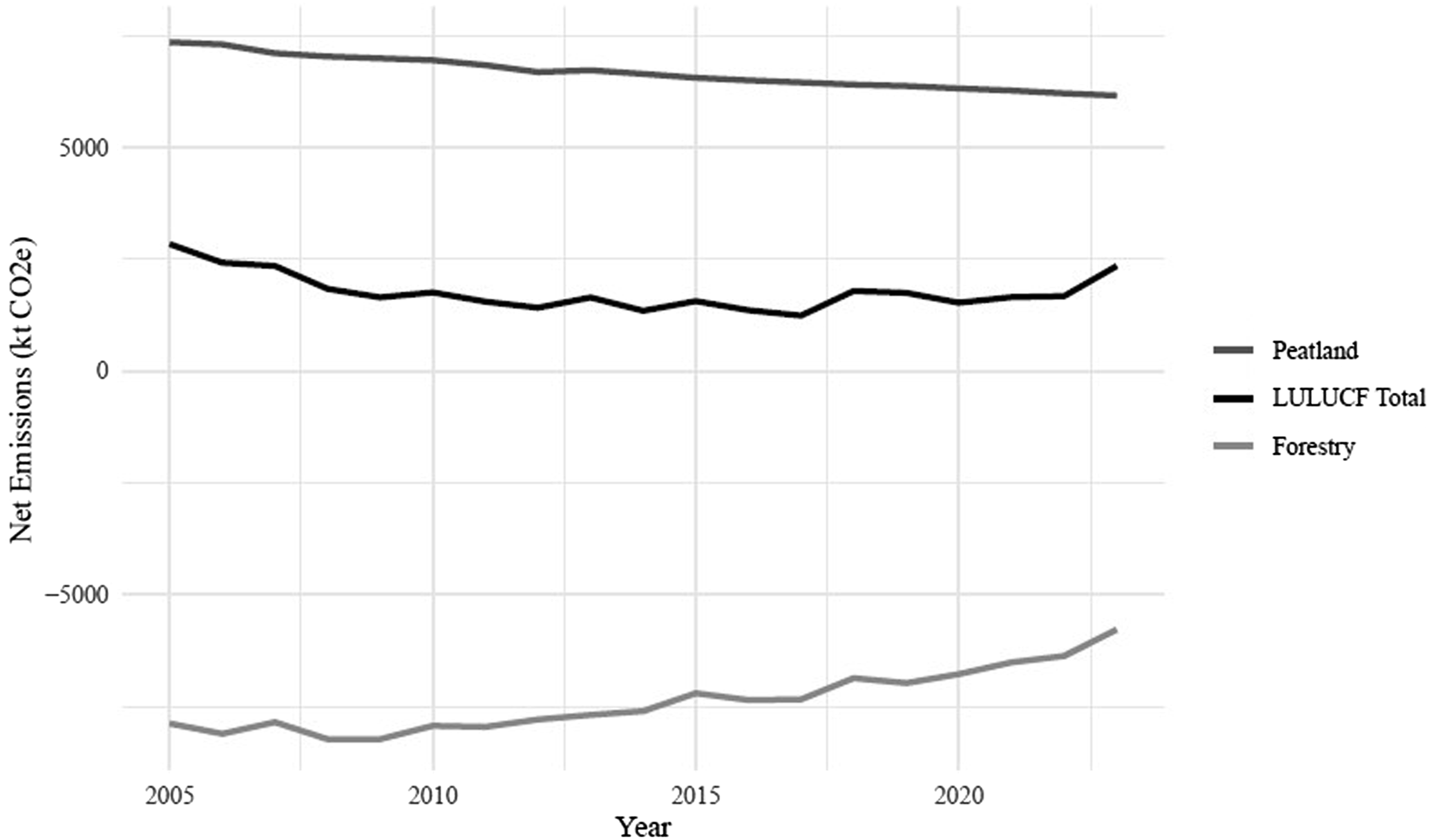

Despite all these initiatives, a clear overall improvement in environmental and emission outcomes cannot be made out. As Figure 3 shows, there has not been an unambiguous reduction of estimated emissions in the Land-Use, Land-Use Change, and Forestry sector (LULUCF). While net emissions from peatland are slowly sinking, there has even been an increase in the forestry sector. Of course, these developments can have many causes though and are not necessarily attributable to the effectiveness of the voluntary carbon markets alone. Estimated net CO2 emissions in Scotland for Peatland, Forestry and total Land Use, Land Use Change and Forestry (LULUCF) 2005–2023. Source: UK local authority and regional greenhouse gas emissions statistics: 2005-2023.

Despite these ambiguous results, the path started by the private sector and the Scottish government is unlikely to end anytime soon. A dense green finance ecosystem has developed in Scotland and the UK more generally, with more and more corporations as well as networks, working groups, task forces and initiatives focused on administration of the current carbon codes but also involved in initiatives for new codes intended to set the standards and already in line to support their infrastructure (Herko, 2023; NatureScot, 2022). Figure 4 displays those developments in relation to the argument presented in this paper. Assetization cascades and periodization of the Scottish case.

In general, and despite the market slowdown since 2023, particularly among risk-averse established large landowners, the market will only mature in the future when more owners have carbon credits to sell and are more confident about the risk level of such investment. There is an expectation that funding will eventually dry up (Interviewee 13) and there may yet be some regulatory intervention with regard to land use and protection (Vevers, 2023), for example, by possibly making some agricultural subsidies conditional on biodiversity improvements (Scottish Government, 2022a). A new land reform was planned for the end of 2023, then postponed to 2024 and is currently going through parliament. Proposed reforms include the introduction of a public interest test to increase the responsibility and scrutiny of those who sell or acquire landed rural property in Scotland, an approach involving more regulation. However, it does not necessarily demand anything from the owners of rural land with a low turnover rate, nor does it stop or intend to stop the cascade of new natural capital assets. As a high-ranking civil servant remarked, this is the strategy that is considered to work well at the moment (Interviewee 12). As private owners and investors are expected to lead the way in nature market making (DEFRA, 2023) and all UK governments willingly provide secure legal structures as well as a lot of funding that is mostly subject to only weak conditions, thus assuming the role of structuring agent that provides the necessary institutional background as well as funding, new markets for new corporate welfare opportunities are being developed in co-creation with those manifold intermediary groups. These dynamics result in a cascade of the assetization of nature.

Conclusion

Scotland’s and the UK’s path to net zero is still evolving, and at a rapid pace. The respective governments are in the company of all governments facing the increasingly urgent question of how to deal with climate change and environmental degradation. The variety of approaches taken by different countries shows that there is no single way to deal with these issues.

In Scotland in particular, a market-based approach has been taken in which the government facilitates marketization of natural capital assets through corporate welfare spending. Infrastructure building as a co-creation process between the private and the public sector has encouraged and continues to encourage corporate welfare spending on land use change projects. The government readily adopted the proposed strategies to meet its climate-related development goals, and once this path was taken, there was little discussion of alternative options and more regulatory policies. The influence of intermediaries and the business sector in creating the first carbon code and the finance gap, researched and promoted by the financial sector, played a key role. Corporate welfare to incentivize land use change provided a path of least resistance to encouraging woodland creation, peatland restoration and other environmental improvements. While established owners have been, and still are, relatively cautious about frontier markets, especially if they have a very long-term focus, initial skepticism has given way to action. Many are now looking to take advantage of the available grants and work with investors to share the risk. The availability of corporate welfare has also added to the momentum of assetization in Scotland, with initiatives for various codes and projects on the horizon, promoted by a variety of private sector actors in collaboration with their public counterparts. The influx of investors, the increased attention, the emergence of more specialized intermediaries in the field and the formation of various forums and groups concerned with natural capital development have catalyzed a mix of initiatives that in turn promote different forms of corporate welfare based on newly defined assets such as biodiversity credits. Taking the empirical findings presented in this article, I first argue that a market-based approach to climate mitigation can evolve if the private sector can significantly shape this path by initiating innovative strategies and being active infrastructure builders in developing new asset classes in sectors where there are high prospective profits. These may, for example, be sectors that are already subject to a public grant scheme. In expanding a sector and its investible assets, private sector actors can co-create corporate welfare programs with public entities that are looking to reach their climate development targets. The focus on the state’s role in the corporate welfare literature should, therefore, be refined by paying more attention to the actions of the private sector and its role in building the infrastructure for assets that benefit from corporate welfare.

Second, I propose that this path can further evolve because corporate welfare can form a symbiosis with assetization dynamics. The increase in funding with few conditions attached attracts more actors, who in turn engage in a similar pattern of building further infrastructure for more assets to be supported by corporate welfare measures, thus creating cascading effects. The literature on market-based climate governance should therefore carefully consider the dynamics resulting from assetization processes.

At a theoretical level, this research points to the entanglements between infrastructure building, corporate welfare, and assetization. It adds to the literature on market-based climate governance and the dynamics of state-market interaction. Further research should test the proposed arguments in different contexts, examine the conditions under which these entanglements occur and identify potential scope conditions. Factors such as the fiscal context or the salience and urgency are likely to have an impact. On a more practical level, the results of this research show how many current climate change mitigation strategies have the potential to be a slippery slope for publicly funded private windfall profits with unclear societal benefits. As the conditions attached to corporate welfare are weak, requirements for positive results regarding an investment’s effectiveness could likely not be enforced. As mentioned earlier, natural capital assets such as carbon credits are only effective if they lead to long-term changes and are additional to other measures. Relying on voluntary, non-enforceable codes cannot guarantee that, as assetizing nature spreads, the public money spent does in fact improve the climate and the environment. Furthermore, while assetized land-based solutions to climate change attract investment and force action, they are influenced by the profit imperative underlying such investment. This narrows climate action down to the most profitable measure and omits alternative, potentially more suitable, solutions.

Supplemental Material

Supplemental Material - The Scottish road to net zero: Corporate welfare and assetization cascades

Supplemental Material for The Scottish road to net zero: Corporate welfare and assetization cascades by Hanna Doose in Competition & Change.

Footnotes

Acknowledgments

I want to thank Charlotte Rommerskirchen and the IPE Research Group for hosting me at the University of Edinburgh and providing valuable feedback on this work. I would also like to thank Christine Trampusch, Brett Christophers, Benjamin Braun, and Michael Kemmerling for their helpful and constructive comments. Finally, I want to express my sincere appreciation to my interviewees, without whom this work would not have been possible.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Note

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.