Abstract

This article considers recent efforts at extending the scope of green finance into insurance schemes to manage the losses associated with the climate crisis in vulnerable countries. Focusing on the case of the African Risk Capacity (ARC), the article argues that these efforts are particularly revealing of the contradictions of what we term the ‘climate-development-finance nexus’ – growing efforts to bridge climate and development activities, with an emphasis on mobilizing green finance in order to do so. In particular, the case of ARC shows how the promotion of insurance should be read as a set of ultimately failed efforts to navigate relations of international financial subordination. Approaching the ARC in this way helps us to understand why the latter has fallen into a shape at odds with the intentions of either member states or the donors who have supported it, the latter illustrated primarily by considering the role of the British Department for International Development. This case, then, is revealing of how green finance more generally is strongly shaped by statecraft within the constraints of existing patterns of financial subordination.

Keywords

Introduction

There is little doubt that the costs of climate crisis are escalating, and disproportionately borne by marginalized people and states. The V20 – a grouping of low-income countries most vulnerable to climate change – estimates that the cost to its members of the climate crisis has already surpassed US$500 billion (V20 2022). How to pay these costs is an increasingly contentious question. Proposals for a global Loss and Damage Fund (LDF) with contributions based on historic emissions were adopted at COP 27 in Sharm-el-Sheikh. However, the conference deferred key decisions about the financing and organization of the fund, and the LDF appears to have been significantly watered down in negotiations about its implementation.

The response to these problems favoured in the metropolitan core has been to extend the frontiers of green finance, especially by promoting the development of insurance against climate damages. Just prior to the agreement on the LDF, Germany launched an insurance-based ‘Global Shield against Climate Risks’, jointly with the V20 and G7 (see G7 and V20 2022). As of late 2023, a significant portion of actual financial commitments related to climate losses were linked to Global Shield. Insurance and the private sector more widely remained favoured sources of finance for core countries in negotiations over the LDF. A UK representative, for instance, insisted early on in LDF negotiations that ‘there is a need to increase volumes and have a broad base of sources beyond public finance’ (qtd. Guerrero 2023). The seemingly final form of the LDF is based on voluntary contributions. To date, these are in the hundreds of millions (rather than the hundreds of billions needed). In late 2023, French President Emmanuel Macron would describe the LDF as a means of ‘mobiliz[ing] new private insurance mechanisms’ (Macron 2024).

This turn to insurance represents a continuation of important trends from the last two decades. Major donors have led efforts to shift the financing of responses to natural disasters in the global south away from ad hoc donor engagements and into the realm of insurance (see Christophers et al., 2020; Dehm, 2020; Grove, 2012; Johnson, 2021; Keucheyan, 2018). Within this wider push for insurance-based mechanisms to deal with climate risks, efforts to develop innovative forms of ‘parametric insurance’ 1 have been particularly important. Rather than insuring a specific property against specific damages, parametric insurance policies pay out when an identified parameter (e.g., rainfall) reaches a pre-defined threshold correlated with damage (for recent critiques of these initiatives, see Aitken 2022; Bernards 2021, 2022; Johnson 2021; Schuster 2021).

In short, whether insurance mechanisms are adequate or just means of addressing losses due to climate hazards looks set to be a major area of contention in global climate politics in coming years. Insurance in this way sits at the heart of what we might call the ‘climate-development-finance’ nexus. Climate and development objectives are increasingly seen as conjoined, and the mobilization of private finance is increasingly seen as central to both (see Bigger and Webber 2021; Gabor 2021; Mawdsley 2018). Through initiatives like Global Shield and its predecessors, policymakers hope to expand the frontiers of ‘green finance’, both into traditional spheres of development aid and towards funding climate adaptation and protection against climate losses. In the bid to build ‘resilience’ against climate change, finance capital has been promoted as both a resource to be tapped and a mechanism of risk transfer away from poor individuals and countries. Parametric insurance, sitting very much at the core of this nexus, offers up a distinct and important lens on the politics of ‘green finance’.

This article traces the contradictions of this emerging climate-development-finance nexus through a case study of the African Risk Capacity (ARC), one of the largest experiments to date with insurance-based responses to climate losses. Launched by the African Union (AU) in 2014, in collaboration with the UK’s Department for International Development (DfID) and other donors, 2 ARC offers parametric insurance against disasters, primarily drought, to participating African governments. ARC in this sense is a key part of the genealogy of the climate-development-finance nexus. ARC has lurched through a series of big and small failures into a form at odds with the intentions of the AU, its members, or key donors. The scheme nearly collapsed in 2018, when precisely one participating country signed on and paid its full premiums. Despite some recovery since, it remains undersubscribed. ARC is heavily reliant on donor funding, despite the hopes both of many participating African governments – who had sought expressly to reduce dependence on donors by accessing private capital markets – and of its main funders, particularly DfID – who aimed to move ‘development’ funding out of government fiscal accounts and shift the costs of climate damages onto African states.

These processes of failure and adaptation deserve close attention in debates about green finance and its relationship to the climate-development-finance nexus. We argue that we helpfully understand ARC as part of an error-prone process by which African and donor states, alongside the African Union – in short, the transnational apparatus of formal development intervention that Gillian Hart (Hart, 2001, 2002, 2009; cf. Mawdsley and Taggart, 2022) helpfully labels ‘Big-D’ Development – have sought to grapple with the dislocations of climate breakdown amidst uneven monetary and fiscal constraints. In Hart’s reading, ‘Big-D’ development is part and parcel of how ‘the conditions for global capital accumulation must be actively created and constantly reworked’ (2001: 650) – a continual process of papering over contradictions of capitalist development necessary in order to enable its continuation. Hart takes as her task to analyse ‘how instabilities and constant redefinitions of official discourses and practices of Development since the 1940s shed light on the current conjuncture’ (2009: 120). ARC is, in this sense, very informative. It is reflective of the growing salience of climate breakdown as a threat to continued capital accumulation, highlighting particularly clearly the financial contradictions faced at the climate-development-finance nexus.

In particular, the truncated development and rollout of ARC has been profoundly shaped by the backdrop of what has been described as ‘international financial subordination’. By the latter, we mean the hierarchical power relations exercised in and through the uneven development of the global financial system, expressed in the form of differential constraints on access to resources, exposure to financial volatility, and ongoing extraction of value disproportionately penalizing actors in peripheral economies (see Alami et al. 2022). A range of recent studies have drawn on this conceptual framework to explore the incorporation of developing and emerging economies into peripheral positions in hierarchical circuits of global finance (see Alami 2020; Alami et al. 2022; Kaltenbrunner and Paincera 2018; Koddenbrock 2020; Kvangraven et al. 2021). Financial subordination in practice means restricted policy space, heightened exposure to financial volatility, and challenges in mobilizing resources, as well as vulnerability to extractive relationships with global financial circuits. These constraints profoundly shape the policy levers by which peripheral states can articulate accumulation strategies and grapple with their attendant contradictions. As Alami et al. (2022: 16) argue, there is considerable analytical value in analysing states’ ‘attempts to negotiate [financial subordination] in ways that are more or less consistent with their accumulation strategies and attempts to engineer particular social contracts between classes’. We think the point holds even if we widen our focus from peripheral states to the wider Development apparatus with which they are often closely enmeshed. Financial subordination, in this sense, is the terrain on which ‘big-D’ Development (per Hart, 2001) must take place.

ARC is plainly articulated around some of the most violent contradictions of global capitalism – namely, the impacts of climate breakdown, particularly insofar as they manifest as famine for rural populations rendered disproportionately vulnerable to increasingly unstable patterns of rainfall through the historic development of colonial capitalism (see Bernards 2021; Watts, 2013). Finance capital in and of itself has played a predominantly indirect role in the development of ARC, but nonetheless the uneven distribution of power over money and finance has exerted a kind of gravity on the development and operation of the project. But both in its initial design and its development in practice, ARC is also profoundly shaped by relations of financial subordination. This is manifested in the fiscal and monetary constraints facing peripheral countries, and with which both donor countries and African governments have persistently grappled, and in the paradoxical character of the actual engagements of finance capital with ARC. Efforts to tap capital markets for investment in climate adaptation have foundered. ARC has had more success in transferring some climate risks to global financial markets, particularly through reinsurance, but these relationships have wound up being articulated on extractive terms. ARC thus offers us a useful lens on how the responses of the ‘Big-D’ Development apparatus to climate breakdown are refracted through dynamics of financial subordination. The emphasis here on the relational and failure-prone ways that states and other authorities grapple with climate breakdown amidst the contradictory relations of financial subordination helps us to grasp why ARC has wound up looking very different from what either the AU or donor governments had intended.

We develop these arguments in three main steps. The first section below traces the development of ARC, showing how its genesis reflected important conjunctural factors in the early 2010s, both within the AU and its member states and major donors. With respect to the latter, we concentrate primarily on the role of DfID, which was the largest initial funder of the ARC programme as a whole (as distinct from later providers of subsidies to country premiums), and while certainly not the only donor involved, has arguably played a central role for the longest. We move on in the following section to outline how ARC’s operations have played out in practice, showing how ARC as a specialized agency and major donors have grappled with the embedded obstacles posed by relations of financial subordination. The third section outlines the insertion of ARC into global financial circuits.

The pre-history of the ARC (2010–2014)

Recent proposals for insurance-based responses to climate damages build on a considerable history of preceding experiments, of which ARC is a particularly important example. The AU, alongside donors and international organizations (especially DfID and the World Food Programme (WFP)) negotiated the establishment of ARC between 2010 and 2014. In March and April 2010, the Joint Annual Meeting of AU Ministers of Finance (AU, 2010a) and a Ministerial Conference on Disaster Risk Reduction developed proposals for ‘the creation of an African-owned Pan-African disaster risk pool’ (AU, 2010b). In November 2012, ARC Agency was established as a specialized agency of the AU (AU, 2012a). ARC founded an affiliated financial entity to provide risk pooling and risk transfer services (ARC, 2013). ARC Insurance Ltd – domiciled in Bermuda – was launched in early 2014. The ARC Secretariat provides support to participating government administrators in customizing the Africa RiskView (ARV) software package which is used to predict famine based on satellite rainfall data and to trigger payouts, and in preparing disaster response plans (see, for example, Republic of Senegal, 2013). If a payout is triggered then the receiving government must further submit a Final Implementation Plan for approval, providing additional detail on how resources are to be expended in light of the specific severity of the drought, its geographical distribution, and associated population vulnerability (ARC, 2012: 5).

This section traces the process that led to the establishment of ARC. The AU sought expressly to carve out greater policy space for member states. The turn to engagements with private finance in order to do so makes sense given the rush of speculative capital seeking investment outlets in ‘frontier’ and ‘emerging’ markets in the aftermath of the Global Financial Crisis (Alami, 2022; Bassett, 2018; Nellor, 2008). In practice, donor funding still proved necessary, and the UK’s emergence as a key donor was very much shaped by the austerity agenda pursued by the Conservative-led coalition government from 2010–2015. In short, ARC emerged out of parallel modes of financial statecraft in the context of deeply embedded relations of financial subordination.

African ownership and the ‘triple crisis’

In 2011, African Finance Ministers acknowledged that ‘the current system of ad hoc unpredictable funding for disaster response causes the depletion of critical assets and the reallocation of government resources from planned investment in times of crisis, slowing economic growth and creating significant setbacks to development’ (AU, 2011a: 22). In place of this ex-post system, ARC promised to contribute towards proactive ex-ante disaster responses. The aim was that a parametric insurance scheme would ‘speed the early flow of funds to a country following a disaster, based on objective triggers, enabling government response actions that reduce the dislocation caused by such events’ (AU, 2011b: 3). It was thought that African governments could save money by pooling their drought risks. Commercial insurance for individual African governments was deemed too costly given their ‘risk profiles’ (DfID, 2014a: 26), based on calculations that capital requirements for separate national contingency funds would be double the cost annual premium payments relative to a collective insurance scheme (AU, 2011a: 43). ‘Approaching the market as a group’ was seen as a means of limiting premium costs (ARC, 2016: 9; Nyirenda and Goodman, 2013: 2).

ARC clearly spoke to a broader set of political-economic concerns within the AU. ARC was explicitly a response to the intensifying contradictions of capital accumulation, and shaped strongly by conjunctural circumstances in the aftermath of the 2008 Global Financial Crisis. This is visible in the multitude of references to what was increasingly termed a ‘Triple Crisis’ of (1) The Global Financial Crisis; (2) climate breakdown; and (3) the Global Food Crisis of 2008 in the preparatory discussions surrounding ARC’s establishment (AU, 2010c: 3). ARC was part of a more general political impetus towards making Africa ‘food secure’ amidst climate breakdown (AU, 2010a). Rising food prices, and concerns among African elites about the potential for popular unrest as a consequence (Branch and Mampilly 2015), spurred a range of initiatives to enhance food security. Climate hazards were also increasingly seen as a threat to national development strategies – indeed, AU member states pushed for ARC’s remit to be expanded from drought to a wider range of climate risks (e.g., floods and cyclones) (AU 2012b).

The concrete form of state and multilateral responses to these tightening contradictions was profoundly shaped by relations of financial subordination. ARC was part of a wider push by a number of African governments to negotiate wider development policy space amidst persistent constraints on resources (AU 2010a; AU 2011a). Many African states in the 2010s sought to loosen the structural constraints of financial subordination and the political constraints associated with aid and debt financing in the preceding decades (Kragelund, 2012). This was facilitated by debt write-offs in the previous decade, and high rates of economic growth driven by the global commodity price boom. At the same time, record low interest rates in the core following the GFC and Eurozone Crisis spurred a ‘search for yield’ among asset managers looking for higher returns in peripheral markets. African territories collectively were increasingly viewed as ‘frontier markets’ ostensibly ripe for investment (Alami 2022; Nellor, 2008). Against the prospect of lower aid levels and seeking policy autonomy, many African governments sought to access global financial markets, exemplified by the rise of African listings on sovereign bond markets (Bassett, 2017).

The establishment of ARC reflected this conjuncture. The AU explicitly framed ARC in terms of the ‘desire of African governments to have greater ownership of disaster response and the continued constraints on aid budgets’ (AU, 2011b: 1). Whilst it was acknowledged that donor funds would be crucial for initial capitalization, emphasis was placed on ‘projecting a clear path to self-sustainability beyond donor and international organization support over several years’ through building member premium contributions, and (critically) mobilizing ‘other’ funding sources, especially international financial markets (AU, 2011b: 5).

ARC was intended to do this in two ways. First, it was envisaged that ARC would pursue ‘risk layering’ through a ‘coordinated use of risk retention, risk transfer, and contingent financing from international financing entities’ (AU, 2011b: 5). The ARC Project Team saw international financial markets as the primary mechanism for more effective management and responses to climate disasters: ‘[ARC] aims to create a new way of managing weather risk by transferring the burden away from African governments, and their vulnerable populations who depend on government assistance, to international financial markets that can handle the risk much better’ (ARC, 2012: 2). ARC was understood as being ‘strategically positioned to match ARC member states’ need for cost-efficient risk transfer to the growing demand from the international risk markets for scale and diversity in their portfolios’ (ARC, 2016: 12). This was controversial – an independent Cost-Benefit Analysis commissioned by ARC concluded that there were likely limited gains to be had from transferring risks to financial markets (Clarke and Vargas Hill, 2013: 1). 3 ARC’s position was that, although not satisfying a vision of ‘pure economic efficiency’, engagement with reinsurers in particular would facilitate ‘flexibility in risk management and premium setting’, building the client and capital base so that the insurance scheme could ‘survive and grow without continual donor support’ (ARC, 2012: 7-8). Second, ARC was empowered to ‘devise innovative ways of resource mobilisation’ (AU, 2012a: 15). While further continued engagement with traditional humanitarian aid was foreseen, it was hoped that this would ‘crowd-in further financing from public and private sectors’ (ARC, 2016: 10). Very early on, ARC began to elaborate plans to establish an Extreme Climate Facility (XCF) which aimed to ‘secure up to US$500 million of initial climate adaptation capital from the private markets for ARC member states in 2017’ (ARC, 2016: 16). ARC was seen from the start, then, in part as a vehicle for expanding the frontiers of ‘green finance’ into climate adaptation activities in AU member states.

We return in Placing ARC in global finance to a discussion of the concrete form of the links between ARC and global finance. For now, it’s worth noting that in this sense, the development of ARC mirrors and anticipates wider patterns. Development practice increasingly seeks to pose climate adaptation and other projects as investable ‘frontiers’ for overaccumulated finance capital (see Gabor, 2021; Mawdsley, 2018). But, as Bigger and Webber put it, ‘not all frontiers are equally investable, nor do they all promise lucrative returns’ (2021: 47-48). Investment in development projects has been highly uneven, with the poorest countries generally largely skipped over (see Bernards, 2023). It’s perhaps not a surprise, then, that the investment-mobilizing functions attached to ARC have generally failed to materialize. On the other hand, ARC has ultimately managed, to a limited degree, to shift climate risks to capital markets, primarily through reinsurance. What’s critically different about this latter mode of engagement with finance capital is precisely that it doesn’t involve risky or speculative investments in peripheral territories by finance capital, but rather, ultimately, the creation of steady streams of premium income. The latter have come, far more than initially intended, from donors. Most parametric insurance schemes are heavily dependent on subsidies – from donors and, in micro-level schemes, from recipient governments. Johnson (2022: (2) usefully argues that ‘If index insurance is a “cash cow,” it is only by virtue of the perpetual subsidies directed toward it’. In this sense, Johnson rightly argues that the framing of parametric insurance as a mechanism for speculative investment is misplaced. Insofar as parametric insurance produces financial returns, Johnson notes that ‘weather insurance is more accurately understood as an infrastructure for channeling surplus from donors, development banks, host governments, and humanitarian agencies’ (2022: 6-7). Johnson’s characterization of parametric insurance projects generally as an ‘infrastructure for generating rents’ is apt with respect to ARC, but this remains something of a puzzle, given that this was distinctly not the intention of any of the main stakeholders involved. The key task taken up in what follows is to unpick the political terms on which this ‘infrastructure’ has taken shape with respect to ARC.

ARC reflected in no small part an initiative by African states and policy elites, collectively through the AU, to draw on global financial markets in the early 2010s to carve out Development strategies with greater autonomy from donor power, against a backdrop defined by the intensifying ‘triple crisis’ on one hand and the global ‘search for yield’ on the other. The concept of financial subordination is helpful in capturing the limits to the strategies pursued by the AU here. ARC depended very heavily on external market circumstances over which AU members had very little control, and towards which ARC was still positioned in a fundamentally subordinate way. Far from securing autonomy from donors, moves to attract private finance ironically wound up, if anything, increasing reliance on donor money, for reasons that will become clear in the next section. For now, though, the next subsection outlines briefly how ARC also dovetailed, superficially but in important ways, with the austerity-era reconfiguration of UK aid.

DFID, austerity, and development assistance

ARC appealed to some donors as a way around obstacles to the expansion of insurance coverage. Experiments with individual-level coverage through parametric microinsurance schemes date to the late 1990s and early 2000s. They had, by this point, largely failed (see Bernards, 2022; Johnson, 2021). As Johnson (2021) notes, part of the response to this trend was to encourage experiments with ‘macro’ level coverage. The World Food Programme and USAID launched the first ‘humanitarian weather derivative’ in Ethiopia in 2006, and the World Bank set up a similar programme in Malawi in 2008 (see Johnson, 2021: 264). The ARC clearly built on these precedents. The turn to indirect coverage through sovereign insurance schemes was explicitly seen as a more sustainable alternative to individual- or household-level schemes (Clarke and Dercon, 2016).

ARC was initiated by the AU, but DfID was involved by December 2010 (DfID, 2014a: 2-3). The justification for DfID support was rooted in concerns about the efficiency of existing humanitarian aid, closely echoing the AU’s assessments. In DfID’s ‘Business Case’ for ARC, it was asserted that ARC would enable African countries to ‘rely less on humanitarian responses that are still too slow’ (DfID, 2014a: 16-17). But DfID’s concrete approach to supporting ARC also reflected (1) the Conservative-led Coalition Government’s (2010–2015) austerity agenda, and (2) what, to borrow Perry’s (2021: 364) useful phrase, might be described as ‘a racial grammar that is often concealed’, but remains constitutive of Development practice, in which ostensibly weak African institutions and corrupt or incompetent rulers need ‘capacity building’ interventions in order to be made ‘deserving’ of investment.

The Coalition government nominally reaffirmed commitments to spend 0.7% of GDP on development aid, while shifting the form of aid expenditures in ways that allowed the government to move them out of government fiscal accounts (Heppell and Lightfoot, 2012; Mawdsley, 2017). A key instrument for such purposes was aid provision in the form of ‘development capital’ – development spending delivered in the form of investment in public or private enterprises (DfID, 2014b: 25-26; cf. DfID, 2015a; ICAI, 2015; Mawdsley et al., 2018). ARC was one of the earliest examples of such investment. In September 2014, DfID announced its intention to provide ARC with £90 million of development capital over 20 years (matched by Germany’s KfW), including initial start-up capital of £30 million (with subsequent disbursements subject to performance triggers), and an additional £10 million in grants for technical assistance (DfID, 2014a: 2-3). The accounting status of development capital is important here. The £90 million of Development Capital for ARC was classified as ‘Non-Fiscal’ expenditure (DfID, 2014a: 74). Because DfID expects the amount to be repaid in full after 20 years, it is treated as a recoverable asset rather than an expenditure on DfID’s balance sheet (ICAI, 2015: 42). Simultaneously, DfID claimed the investment could be classified as positive ODA because it matched criteria of both being for the purpose of developing countries’ economic development and concessional at an interest rate of 0% (DfID, 2014a: 77). The funding mechanism for the capitalization of ARC was thus rooted in the UK government’s attempt to reconcile aid commitments with nominal fiscal deficit reduction.

Yet the use of recoverable funding mechanisms implied an effective shift of the fiscal burden for development spending onto developing countries themselves. The UK government’s aid strategy was explicit about this, stating that the overall ‘vision’ was to help ‘achieve a secure, self-financed, timely exit from poverty’ (DfID, 2014b: 3; emphasis added). The durable structural obstacles to that ‘self-financing’ are normalized here through the deployment of racialized paternalism. DfID’s underpinning ‘Theory of Change’ for ARC notably emphasized ‘changing incentives for risk management’, expecting that ‘in valuing their extreme weather risks for insurance, African governments [will] become aware of the costs they face with each drought and are motivated to reduce these risks as far as they can and transfer the residual risk to a reasonably priced insurance policy’ (DfID 2014a: 57). It is hopefully clear from the previous sub-section that the implication here that African governments were not aware of the costs associated with climate change is absurd, but reflective of the racialized paternalism underlying much of DfID's engagement with ARC. Likewise, DfID specifically aimed to maintain leverage over AU members through ARC. DfID dismissed the option of directly supporting commercial insurance to selected countries, reasoning that this ‘would not incentivise contingency planning or require reporting on delivery of benefits to poor people’ (DfID, 2014a: 26). DfID similarly wanted a large equity stake in ARC, rather than funding premium payments, as the latter ‘would not give DfID leverage with the ARC Governing Board, the Board of ARC Ltd, or the Peer Review Mechanism which decides which contingency plans are “good enough”’ (DfID, 2014a: 61). The option to provide capital as a grant, which DfID estimated would have saved at least US$60 million more over a 20 year period for African countries due to the ‘investment’ not needing repayment (DfID, 2014a: 63-64), was ruled out in the belief that higher premiums were needed to ‘motivate disaster risk reduction in country’ that is, to discipline African governments into reducing their financial exposure to climate change (DfID, 2014a: 71-72). DfID asserted that it was crucial that access to insurance coverage was conditional upon engagement with institutional reform and capacity building procedures: ‘ARC will require countries to identify the right risks to transfer and to have strong contingency plans in place before they can join’, and be subject to an ‘effective monitoring process’ (DfID, 2014a: 57). Whilst the Cost-Benefit Analysis asserted that the success of such contingency planning would depend on the pre-existence of a ‘large-scale, well-targeted social safety net…that can be scaled up in times of hardship’ (Clarke and Vargas, Hill 2013: 3), DfID’s own emphasis was on the capacity of state managers to quantify climate risks and diligently spend the state’s resources, seeking to ‘encourage significant behaviour changes’ in the administration of government that would see the costs of climate change integrated into the domestic budgets of African states (DfID, 2014a: 45). DfID’s vision of its role in ARC, in short, was profoundly shaped around a racialized paternalism which sought to externalize the costs of running the scheme while maximizing the disciplinary power DfID could exert over participants.

The establishment of ARC in the early 2010s thus reflected a superficial conjunctural compatibility of objectives between African policymakers (especially within the AU) and donors (especially DfID). The former sought to embrace financial innovation as a way of mitigating the climate crisis whilst loosening the constraints posed by relations of financial subordination. The latter sought to reconfigure aid and climate finance – as ‘development capital’ – in a manner that minimized their own fiscal obligations while maintaining policy leverage. Our emphasis on practices of Development mediated through relations of financial subordination is helpful in understanding these dynamics. The surface objective of moving from post-hoc to pre-financed catastrophe assistance masked underlying tensions over policy autonomy for African states and over who should pay, as well as fundamental contradictions around the fiscal space available for peripheral governments. Crucially, though, structures of financial subordination inhibited the realization of DfID’s vision for the scheme as much as they did the AU’s. This became apparent in the truncated progress of ARC in practice, to which we turn in the next section.

ARC in practice (2014–present)

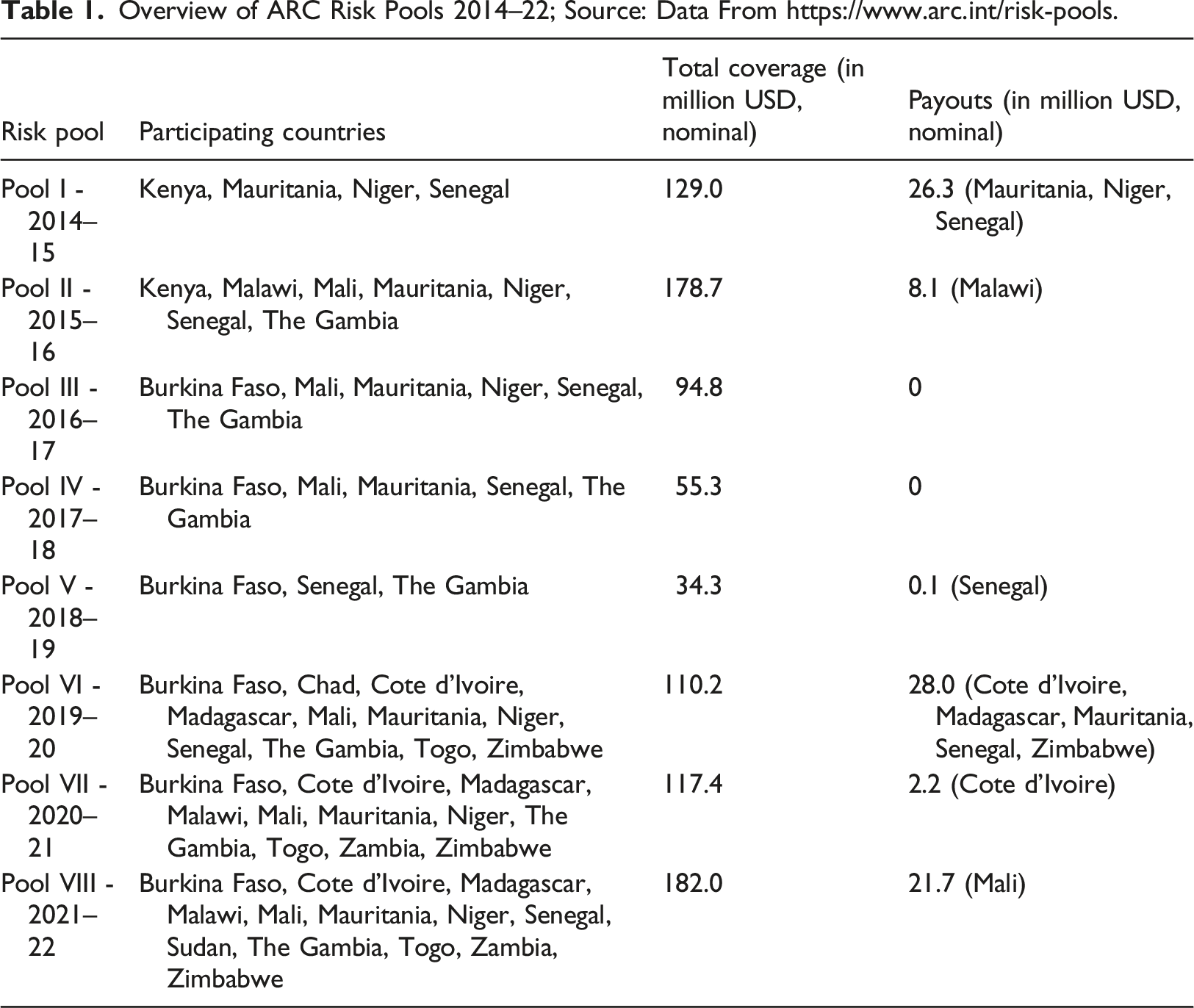

Overview of ARC Risk Pools 2014–22; Source: Data From https://www.arc.int/risk-pools.

‘Skin in the game’

ARC’s first risk pool in 2014/15 comprised four countries (Kenya, Mauritania, Niger, and Senegal). Outside of this, Mozambique was deemed eligible but chose not to purchase insurance, whilst Malawi, Burkina Faso, Zimbabwe, Mali, and The Gambia expressed interest in participating in later pools and were receiving technical assistance on submissions to the ARC Board (DfID, 2015b). ARC made three payouts from Risk Pool I (to Mauritania, Niger, and Senegal) totalling US$26.3 million (a total which, notably, has only been surpassed once in the years since). The inaugural risk pool was generally seen as having ‘proven [the] utility of ARC’ (ARC, 2015: 9).

Malawi, Mali, and The Gambia ultimately joined the four original participants in Risk Pool II in 2015/16. DfID’s (2015b) appraisal again highlighted ‘excellent progress’. DfID was especially pleased with the extent of country ‘ownership’, assessed in terms of the proportion of premiums paid from national fiscal revenues, which stood at 100% across the first two pools. Indeed, not surprisingly in light of the DfID priorities discussed in the preceding section, DfID’s emphasis in early evaluations was almost entirely with whether countries were promptly paying premiums independently out of national budgets. DfID’s (2016: 19-20) position was justified in paternalistic terms of ensuring African countries maintained ‘skin in the game’ in relation to the management of their own climate risks. Already, this portended disagreement with ARC Agency over how ARC should continue to expand. ARC Agency saw donor premium support as necessary to increase participation due to embedded fiscal constraints across countries, illustrated by Zimbabwe’s inability to pay premiums and join Risk Pool II (ARC, 2015: 20).

As these issues came to a head, a lethal drought in Malawi failed to trigger payouts, revealing significant tensions around the ARC’s reliance on parametric insurance mechanisms. In April 2016, President Peter Mutharika declared a state of emergency due to a drought which had devastated crop production (Reuters, 2016). In May, the FAO and WFP estimated that 6.5 million people (roughly 1/3 of the country) in 24 out of 28 districts were food insecure. ARC’s estimate, based on ARV modelling, had been that only 20,594 people would be affected, so no payout was triggered (see ActionAid, 2017). Pressed by civil society groups, the Malawian government launched an appeal. An investigation led by the Lilongwe University of Agriculture and Natural Resources (LUNAR) revealed that the discrepancy in estimates was partially due to errors in ARV customization, which had seen the wrong type of maize inputted as the reference crop (ARC, 2017: 19). Adjusted ARV modelling suggested 2 million people were affected; ARC eventually made a payout of US$8.1 million. For the Malawian government, this was nonetheless too little (the model still underestimated drought impacts and response costs) and by definition too late to facilitate an ‘early response’.

Critics claimed that the Malawian case highlighted engrained issues with parametric insurance. ActionAid (2017: 12) asserted that ARC modelling was ‘complex and opaque and not conducive to a participatory, transparent, and accountable decision-making process’. Moreover, they argued the ARV model omitted key variables (soil conditions, compounding drought effects, evapotranspiration, food price inflation) which increased the probability of basis risk events (ActionAid 2017: 13). 5 Malawian government officials argued that in light of the basis risk problem, parametric insurance did not represent value for money over possible alternative: donor grants for social safety nets, adaptation plans, and national contingency funds (ActionAid 2017: 16-19). Malawi withdrew from subsequent risk pools, and were hardly alone in doing so, especially after a similar failure in Mauritania the following year (see Johnson 2021: 266). There was a precipitous drop off in the number of participating countries and total coverage following Risk Pool II (see Table 1).

The failures in Malawi and Mauritania highlighted a disconnect between ARC’s technocratic pursuit of ‘objective’ triggers for climate finance (AU, 2012a: 4), and the landscape of political contradictions within which it operated. ARC remained keen to assert that problems with the scheme were more a product of capacity issues on the part of member states rather than parametric insurance itself (ARC 2017: 12). Yet, ARC also took note of the impact of ‘political sensitivities’, electoral concerns, and ‘regime change’ was having on ARC membership, requiring further efforts to ‘deepen linkages between ARC and existing national systems to ensure sustainability and continuity in view of political change’ (ARC 2017: 14-15). Amid declining participation, DfID also increasingly pushed ARC to make reforms (DfID, 2018: 6).

These tensions were amplified by the basic embedded contradictions of financial subordination – particularly in the form of fiscal constraints faced by subordinated states. Risk Pool V for 2018–19 had only 3 participants with total coverage of just US$34.3 million, of which only the Gambia actually paid agreed premiums (see Johnson 2021: 266-267). In combination with the Malawian controversy, both ARC and donors identified fiscal constraints on the part of participating and prospective members as the key reason for reductions in pool size. Even prior to Risk Pool III, DfID (2017: 17) stated that despite a number of countries being ‘technically ready to join ARC’, they were not able to ‘mainly because of fiscal constraints’. In 2018 and 2019 reviews, DfID likewise attributed falling participation to fiscal constraints (DfID 2018, 2019). Similarly, ARC (2019: 37) noted that ‘fiscal limitations have been the main hindrance for countries to adopt risk financing options which often require advance expenditure in anticipation of disasters’.

This was not a new issue. Consultations with prospective members during the establishment of ARC anticipated that most countries would ‘need donor support to meet their initial annual insurance premium payments’, and envisaged that this would be realized through bilateral arrangements with existing development partners in individual countries (ARC, 2013: 20). Both ARC and DfID sought to frame fiscal constraints as a question of resource management rather than resource availability. In early assessments, DfID continued to express concerns that premium support would distort the incentive structure that ARC was attempting to introduce, whereby African countries – in paying premiums in full – would come to recognize their financial exposure to climate risks, and make cost-effective investments to reduce them (DfID 2014a, 2016, 2017). ARC (2017: 36) argued that one of the primary issues regarding premium financing was the lack of priority it was given in national budgeting, which was compounded by ‘payment fatigue’ if multiple years went by without a payout. However, despite the reluctance on the part of both the ARC secretariat and DfID, in light of continued declining participation, especially the ‘risk pool of one’ in 2018 (see Johnson 2021), ARC and sceptical donors ultimately had to accept that subsidies were essential for the continuation of ARC.

ARC Replica and the reluctant return of subsidies

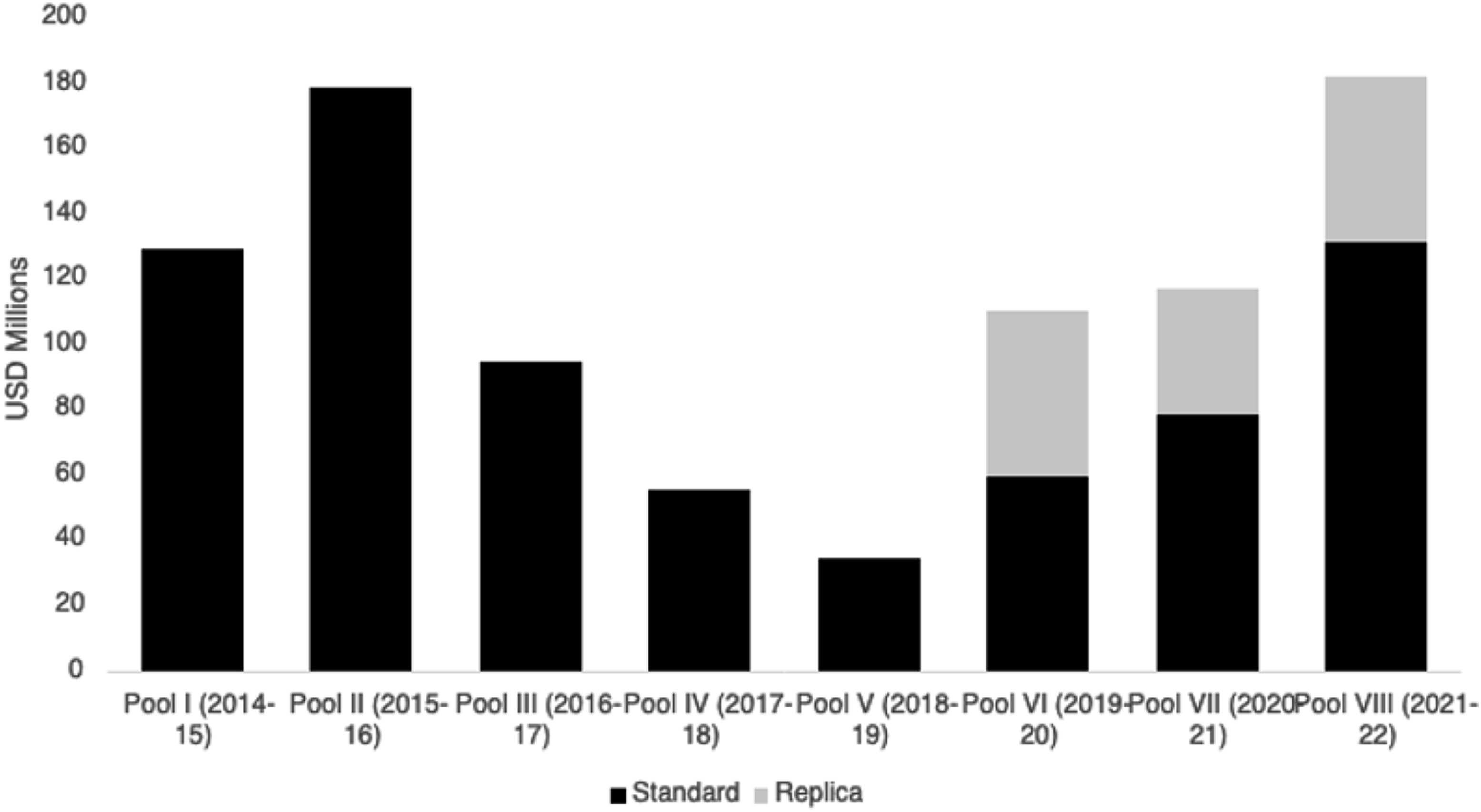

By 2019, DfID (2019: 3) had conceded that ‘[i]t is now clear that ARC will not become sustainable in the short term without premium support being made available for countries’. From 2016 ARC Agency had already committed to developing ‘Replica Coverage’, whereby UN agencies, donors, and NGOs would be able to purchase insurance policies from ARC which matched the existing coverage of individual countries. ‘ARC Replica’ – as the product was named when it was launched – was piloted in 2018, though initially hampered by Senegal and Mauritania’s refusal to pay their premiums. The 2019–20 Risk Pool saw the WFP and StartNetwork purchase insurance coverage for Burkina Faso, Mali, Mauritania, Senegal, the Gambia, and Zimbabwe with funding from the German and Danish governments (WFP, 2019). As shown in Figure 1, the provision of Replica coverage played a major part in the restoration of participation in subsequent years. Total coverage reached a new high of US$182 million in the 2021–22 Risk Pool, of which just over 50 million was financed through ARC Replica (ARC, 2022). Premium support through ARC Replica was justified on the basis that it would not just supply additional funding, but facilitate the accrual of experience and expertise in risk management within member countries. ARC Replica donors were to have greater involvement in ARV customization, training, and consultancy in the development of contingency plans. The WFP (2019) asserted that the objective was to expand coverage in countries with ‘limited technical and financial capacity’. Total coverage under ARC Standard and ARC Replica, 2014–2022, in USD millions; Source: data from https://www.arc.int/risk-pools.

At the same time, ARC co-launched the Africa Disaster Risk Financing (ADRiFi) Programme in collaboration with the World Bank and African Development Bank (AfDB), in which the latter provided direct premium subsidies of up to 50% over a 5-year period to countries purchasing ARC coverage (e.g., AfDB, 2019). In order to access such funds, participating countries had to commit to purchasing coverage each year of the agreement whilst funding the non-subsidized portion with their own resources. From ARC’s perspective, the ADRiFi framework aimed at ‘embedding disaster risk management and financing in government systems…supporting the ARC insurance premium payments in each participating government for a determined period while policies are being built and integrated’ (ARC, 2019: 22). The objective is for subsidies to be phased out over the 5-year period with countries paying 100% of the total in the final year of the agreement (Martinez-Diaz et al., 2019: 27). The subsidy is thus seen as a temporary measure whilst resource costs for premium payments and risk management techniques are mainstreamed into budgetary cycles and government administration.

Part of the recovery in coverage has also been a consequence of ARC Agency seeking to refine ARV in light of member criticisms of basis risk, as well as moves towards offering new forms of insurance coverage. ARC introduced new sensitivity and robustness analyses of event models, incorporating evapotranspiration data and alternative drought index options into modelling, and improving in-country training in risk management and ARV customization (DfID, 2020: 10-11; ARC, 2019: 15-17). Additionally, after years of delays, in 2020 ARC started offering insurance coverage for tropical cyclones, with Madagascar taking out a policy for 2021–22.

In the main, though, premium support is the primary factor spurring renewed interest in pool participation. This has seen DfID amend its ‘Theory of Change’ (DfID, 2021: 6). Previously it assumed that African governments would be motivated to reduce climate risks through having to purchase insurance coverage, and distrusted premium support as a disincentive for embracing risk ‘ownership’ (DfID, 2016, 2017). DfID now accepts that budgetary constraints and political pressures on scarce resources in member states have thwarted the development of the envisaged ‘market’. By 2021 DfID (2021: 6) was arguing that: ‘Premium subsidies have been identified as a key component in the successful growth of the development insurance ecosystem and the mainstreaming of insurance behaviour…By bringing more countries onboard, achieving regular policy renewal, and effectively marketing the value of insurance by using case studies and story-telling, ARC can shift behaviour whereby effective disaster risk management, including, where relevant, disaster risk insurance, can become the normal practice for African Union Member States’.

In this way, premium support is envisaged as a temporary, transitional mechanism towards the fuller realization of both (1) a functioning market for disaster insurance and (2) African states acclimatized to a set of governance practices necessary for the reproduction of such a market and the norms of individual country risk ownership intrinsic within it. There are clear echoes here of what Christophers (2019) has described in a different context as a politics of the ‘allusive market’ – in which perpetual subsidies are justified as transitional means of laying the groundwork for a self-sustaining market (which will likely never arrive).

The critical point is that we can see here the continued articulation of Development responses to climate breakdown, profoundly limited by relations of financial subordination. DfID sought explicitly to shift the fiscal burden of climate adaptation onto AU member states themselves, but patently failed to do so completely, as concerns about basis risk and fiscal constraints prevented most African governments from participating and drove a number of governments who had participating in Risk Pools I and II to withdraw from further pools. The reluctant adoption of heavy subsidies, most of all through ARC Replica, and the turn towards a politics of the ‘allusive market’, was probably necessary to rescue ARC as a Development project.

Placing ARC in global finance

It is also worth underlining that rather than mobilizing new resources for climate adaptation, ARC has, in effect, created a new extractive stream of surplus from African states and people to global financial markets. This was, again, not intentional, nor reflective of much direct influence on the part of finance capital, per se. Expectations of mobilizing private investment for climate adaptation remain unfulfilled. The XCF remains to be launched (ARC 2020). ADRiFI’s work includes promises to explore means of shifting more risk to private markets in the longer-term: ‘In the future, the ADRiFi team will explore a private sector-led financing instrument that promotes bridging the private sector to support capital risk. This could complement grant funds and donor subsidies which are drying up’ (ARC Ltd 2021). But again, this remains a provisional and uncertain development. Ironically, in a context marked by relations of financial subordination, donor support remains critical to the ‘investibility’ of any of ARC’s programmes. ARC Ltd Retains an investment grade credit rating from Fitch, for instance, despite its ‘weak financial performance’, specifically because of the presence of capital investment in ARC from the now-Foreign, Commonwealth and Development Office (FCDO) (Fitch Ratings 2022). Donor support, in short, is vital for maintaining the financial viability of ARC.

For a number of authors, the turn to insurance mechanisms as means of managing climate breakdown is an aspect of a wider process of ‘financialization’, creating new spaces for the deployment of speculative capital (Grove, 2012; Isakson, 2015; Keucheyan, 2018). As one of us has argued previously of the promotion of markets for microinsurance, though, the fact that Development interventions privilege the interests of finance capital doesn’t necessarily imply that they are driven directly by financial interests – ARC’s efforts to mobilize private finance share an ‘anticipatory’ character with the efforts to promote the extension of microinsurance (Bernards 2022). As noted above, ARC has wound up operating as an ‘infrastructure for generating rents’ in Johnson’s (2022) terms – heavily reliant on subsidies, which are mostly ultimately funnelled to reinsurers.

The significance of this point in the context of wider relations of financial subordination is clearer if we consider the specific channels through which ARC is connected to metropolitan financial markets. As the investment-mobilizing functions attached to ADRiFi and XCF have yet to have any significant impact, at present, these are mainly through reinsurance contracts and through reinvestment of the insurance pool.

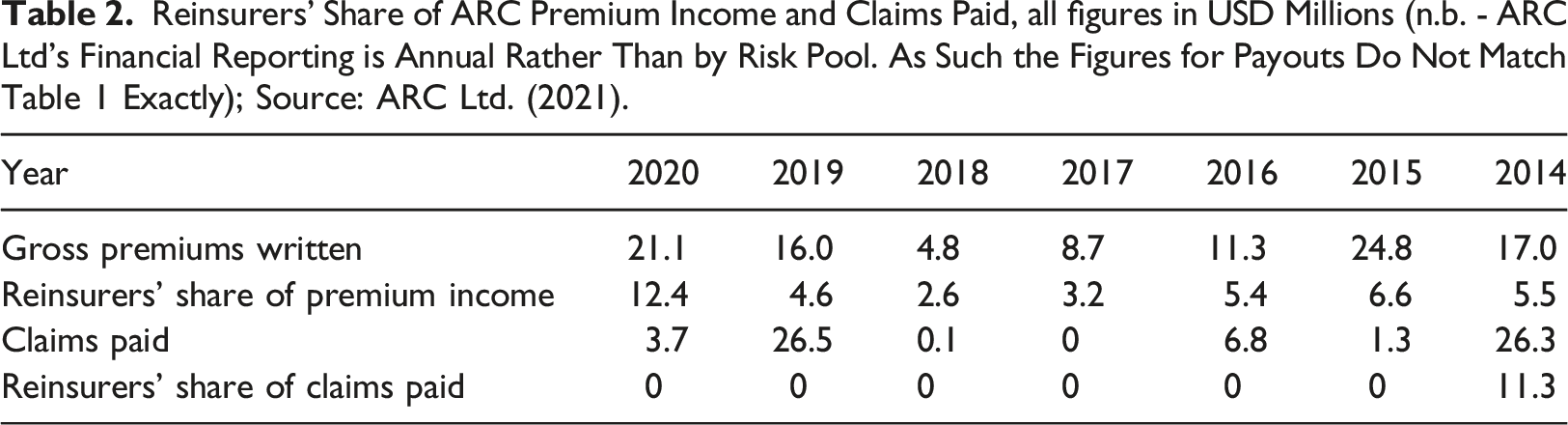

Reinsurers’ Share of ARC Premium Income and Claims Paid, all figures in USD Millions (n.b. - ARC Ltd’s Financial Reporting is Annual Rather Than by Risk Pool. As Such the Figures for Payouts Do Not Match Table 1 Exactly); Source: ARC Ltd. (2021).

A second channel linking ARC to global financial markets is through the reinvestment of the insurance pool. At the end of 2020 (the most recent available figures at the time of writing), ARC Ltd held USD67.6 million worth of marketable investments, of these, 40.9 million were made up of corporate bonds, 11.8 million of investments in mutual funds, and 5.0 million in commercial mortgage bonds, along with 3.0 million worth of US government bonds (ARC Ltd 2021). Or, in other words, government and donor premiums were predominantly reinvested in metropolitan financial assets. On one hand, this makes sense – as an insurer, ARC Ltd needs a pool of relatively stable assets which can be liquidated quickly. Precisely because of the hierarchical organization of the global financial system, however, this means buying up assets from core markets.

The end result of flows of surplus through both channels is one where foregone investments in social infrastructures or climate adaption on the part of African governments, and money spent by donors on premium support in lieu of meaningful transfers for loss and damage related to climate change, wind up recirculated in ways that play a part (albeit a small one) in reinforcing the depth of metropolitan financial markets. What’s critical here is that this dynamic has taken shape despite very little direct involvement of finance capital in shaping ARC’s design. The streams of income involved are not globally systemically important by any stretch, but they do reflect the gravity exerted by relations of financial subordination. The presence of deep liquid pools of capital, concentrated in metropolitan financial markets (both in the form of reinsurers and equity and bond markets on major stock exchanges) necessitates the recirculation of insurance premiums from African people and states to the core.

Conclusion

In the preceding sections, we’ve traced out the development of ARC, a leading example of a wider turn to insurance as a mechanism for the management of climate risks. ARC is best interpreted in terms of the efforts of the apparatus of Development to navigate the contradictions engendered by global capital accumulation (most visible in the ‘triple crisis’ described in ARC in practice (2014 -present)) within the constraints posed by international financial subordination. The history of ARC in practice looks like a series of quiet frustrations of the underlying objectives of both participating AU members and of the UK and other donors. For DfID in particular, who had imagined leveraging ‘Development Capital’ to shift ODA out of the UK government’s fiscal account, the reluctant acknowledgement of the need for indefinite premium subsidies represents a failure (even if couched in allusive references to the eventual payment of premiums by beneficiary countries). Likewise, the hopes of AU member states in the early 2010s of loosening the constraints of donor conditionality through the enrolment of globally circulating financial capital have quietly gone by the wayside. ARC has, in the manner of parametric insurance more generally, been built into an ‘infrastructure for generating rents’ – to use Johnson’s (2022) phrase. Critically, the existing form of ARC was not the express intention of anyone involved, but rather the end-product of a set of failures and adjustments – both on the part of DfID and AU members – seeking to navigate the contradictions of financial subordination.

This case has implications for how we understand relations of financial subordination and the place of finance capital in Development. It’s notable in this case that the social power of finance operates largely indirectly. Rather than finance capital prospecting the earth for new asset streams, here we see a flow of premium income to reinsurers being assembled out of a series of responses aiming to resolve the ‘triple crisis’ of food, climate, and aid budgets. If the end result of ARC has been an extractive system privileging the interests of global finance capital, this is not a result that was directly the design of any of the state actors involved. Equally, relations of financial subordination pose limits on donor agendas as well as those of peripheral countries. The UK and other donors have been unable to pass the costs of climate insurance onto African states as far as they have hoped, because ARC has had to operate through existing fiscal and monetary constraints. Indeed, as noted in the final section above, the UK’s ‘development capital’ in ARC Ltd (and as such, implicit guarantee of its solvency) is a precondition for the insurer’s ability to access capital. All of this reinforces the claim, discussed in the introduction, that there is considerable scope for research on the dynamics of statecraft in the context of financial subordination (see Alami et al., 2022: 16). But this case perhaps further suggests that this research might also usefully be pursued from a relational perspective, stressing in particular the dynamic interactions of political actors seeking to implement different strategic aims and accumulation strategies from different points on global financial hierarchies. The contradictions of financial subordination can frustrate the political aims even of actors relatively favourably placed in relation to global financial circuits.

This case also has important consequences from the perspective of just or equitable green finance. In important senses, ARC in its present form looks like precisely the inverse of most visions of climate reparations or climate justice (see, for example, Sealey-Huggins, 2017; Táíwò and Bigger, 2022; Perry 2021). It represents a net transfer of aid and fiscal resources to finance capital – in the form of premium income transferred to reinsurers and re-investment in government bonds and corporate securities – in return for uncertain protection against climate hazards which African societies have played a disproportionately small role in creating. This flow of rents is underpinned more than intended by donor money, but again rather than meaningfully paying the climate debts of the imperial core, it represents a transfer of resources back to finance capital. Absent more concerted action to directly confront relations of financial subordination, there appear to be significant limits to the extent that the frontiers of green finance can meaningfully be extended in directions that align with climate justice.

Footnotes

Acknowledgements

We wish to thank Sarah Sharma, Milan Babic, and participants at the ‘IPE of Green Finance’ workshop, as well as the anonymous reviewers at Competition and Change for comments on previous versions of this article.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.