Abstract

As a reaction to intensifying global competition, measures related to strategic autonomy are gaining traction on the EU level. Yet they coincide with a general return to fiscal consolidation. With current developments more inconclusive than previously suggested, this article asks how the central actors in EU economic policy, both public and private, position themselves in the autonomy-austerity conflict. It introduces a political-economic approach to the role of (geo)economic ideas and state-business relations in EU policy formation. The article focuses on infrastructure policy as a main field within which the conflict unfolds. A content analysis of official documents systematically maps the positions of relevant actors. While an influential group of southern finance ministries, Directorates-General, center-left parties, and trade unions is promoting strategic autonomy, a shrinking constellation around fiscal austerity contains relevant veto players. The deadlock results in the attempt to reconcile both ideas via “targeted flexibility”: consolidation via the expenditure side and a delegitimization of non-investment spending, coupled with a public de-risking of private investments. The approach is supported by European capital, yet highly inconsistent and runs up against pro-austerity forces. The findings have strong implications for the EU’s future geoeconomic strategy and its ability to compete globally.

Keywords

Introduction

The EU’s economic policy is at a critical juncture, academic observers agree. For an extensive period, it pursued a global strategy that combined fiscal restraint and export-orientation under conditions of open competition. Yet, a stagnating economy and the more widespread use of state-interventionist tools on the part of global competitors, most centrally China and the US, raise questions about the viability of this strategy and allow new ideas to gain traction. Central actors such as the European Commission began to champion “strategic autonomy”—politically repackaged into Open Strategic Autonomy (OSA) to express a persisting commitment to free markets—through which the EU seeks to “protect its strategic assets, infrastructure and technologies” (SWD (2020) 98 final). Some scholars view this reorientation as an altered approach to global order which engages in selective forms of protectionism (Lavery, 2023). For others, it consists of a challenge to neoliberal hegemony based on power shifts among European capital fractions (Schmitz and Seidl, 2023; Schneider, 2022). For others again, it is about a change in the overall function of the EU, turning away from liberal market-making to a state-interventionist market-shaping (Di Carlo and Schmitz, 2023; McNamara, 2024). The formation of industrial alliances, the launch of Important Projects of Common European Interest (IPCEIs), and the establishment of the Recovery and Resilience Facility (RRF) are measures that are usually associated with this alleged shift.

In contrast to the afore-mentioned accounts, this article views these developments not as a fundamental shift but as part of an unresolved conflict of (geo)economic ideas that currently produces rather inconsistent policies. Also in contrast to previous works, it argues that strategic autonomy is set up against fiscal austerity as an idea more than market-liberalism. In parallel to the proliferation of strategic investment instruments, we observe a return of a fiscal restrictive agenda at EU level where, after 4 years, the Commission has reactivated a moderately modified Stability and Growth Pact (SGP), prompting a return to fiscal consolidation. On a practical level, the expected budget cuts are at odds with the requirements of large-scale strategic infrastructure and industrial development as envisioned by proponents of strategic autonomy. Recently, these inconsistencies kept the EU from going beyond minimal agreements in geoeconomic affairs. The so-called Sovereignty Fund, envisioned by the Commission as an RRF successor through which the EU could finance strategic investments of joint importance, was cut down to the Strategic Technologies for Europe Platform (STEP), endowed with a mere €1.5 billion that is taken out of the regular EU budget. Global Gateway, a global infrastructure initiative that should compete with the ones put forward by China and the US, remains heavily reliant on the leveraging and de-risking of private investments through a reallocation rather than sourcing of public funds (Hameiri and Jones, 2023).

Highlighting that the current developments in EU policy are more inconclusive and brittle than previously suggested, the article analyzes the constellation of interests on which this inconsistent state is based. It develops a political-economic approach to the role of economic ideas and state-business relations in the formation of EU policy. It argues that the current political conflict in the EU is mostly one of clashing (geo)economic ideas, centered around the question whether the pursuit of strategic autonomy should entail an abandonment or at least a deferral of fiscal austerity. In particular, the article stresses that business actors, most importantly European and national business associations, have a significant influence on the assertion of certain ideas in EU policy. In line with this, it asks what position central actors in EU economic policy, both public and private, take on the autonomy-austerity conflict.

Empirically, the article focusses its observations on the field of EU infrastructure policy. This is for two reasons. First, in the literature on the strategic turn of European economic policy, attention is largely shared between industrial policy (Lavery, 2023; McNamara, 2024; Schneider, 2022) and trade and investment policy (Meunier and Nicolaidis, 2019; Reurink and Garcia-Bernardo, 2021; Schmitz and Seidl, 2023; Weinhardt et al., 2022). The article adds to the less developed literature on EU infrastructure policy (Abels and Bieling, 2023; Turner, 2021) by focusing on its historical determinants and contemporary political drivers. Second, and more central to the research question itself, it takes infrastructure policy as a key field where the conflict around strategic autonomy and fiscal austerity condenses. Large parts of the strategic autonomy agenda relate to infrastructures, whose development and control the EU sees as vital to its economic and security interests. As the article demonstrates, austerity cuts disproportionately reduce infrastructure investments. Hence, infrastructure policy is where the ideological tensions and practical incompatibilities of ideas come to the fore.

The article undertakes a qualitative content analysis of reports, position papers, and declarations published by relevant actors of EU politics—ministries, Directorates-General, European parties, business and employer associations, as well as trade unions—and systematically maps their positioning within the conflict. The analysis finds that, while an influential group of southern finance ministries, Commission departments, center-left parties, and trade unions is promoting strategic autonomy, the shrinking constellation around fiscal austerity contains relevant veto players: the German finance ministry as well as the conservative and right-wing EU parties. This deadlock results in the attempt to reconcile both ideas, strongly supported by European capital. The large European business associations assemble behind a position of “targeted flexibility” that combines favorable elements from both frameworks: consolidation via the expenditure side and a delegitimization of non-investment spending, coupled with public funds that make private investment in infrastructure more lucrative and de-risk it. While this approach currently dominates EU policy, it is highly inconsistent: from a historical view, strategic investments are most likely to suffer from budget cuts. Furthermore, the approach runs up against the status quo preserving forces of the austerity-prioritizing group. These findings have strong implications for the EU’s future geoeconomic strategy and its ability to compete globally.

The article is structured as follows: the first section analyzes historical and statistical data to demarcate phases of EU infrastructure policy and their underlying ideas and overarching trends. The section fulfills three purposes: it introduces this select field of EU policy; it outlines the historical impact of competing economic ideas on the development of this field; and it highlights their practical incompatibilities. The second section discusses the political-economic approach to EU policy formation based on a conception of economic ideas and a condensation of interests that is substantially affected by state-business relations. The third section discusses methodological considerations for the qualitative content analysis. The fourth section presents the results of this analysis. The concluding section discusses their political and academic implications.

(Geo)economic shifts of EU infrastructure policy

This article takes infrastructure policy as a relevant policy field in which ideological and practical conflicts between strategic autonomy and fiscal austerity become visible. In contrast to other fields, infrastructure policy is less defined by the instruments it uses or the economic sectors it addresses than by the material objects it seeks to establish. It can be broadly defined as all political efforts that seek to maintain, develop, and regulate infrastructures within and beyond a political space. In line with established definitions (Larkin, 2013), this article understands infrastructures as networks. They consist of material or digital facilities, representing the so-called hubs, and the ties that connect these facilities and establish interconnections to other networks—cables, pipelines, rail, and so forth. Infrastructures’ central purpose is to allow for the flow of goods, services, people, energy, and data across space.

The analytical focus of this article is on EU infrastructure policy in fields such as transport, energy, and communication. Technical infrastructures serve as material prerequisites of economic production and, if integrated in transnational cross-border networks, of regional and global exchange. Educational institutions and the healthcare system, at times discussed as “social infrastructures,” are also central to societal development. Yet for the purposes of this analysis, they play a subordinate role as they are operated differently and are subject to fundamentally different discourses.

Historically, the cycles of infrastructure policy were subject to changing (geo)economic conditions and ideas. European integration in the 1980s and 1990s envisioned a downright contradictory role for infrastructure policy. On the one hand, infrastructures were viewed as networks indispensable for the completion of the single market. The EU regarded them as “the central nervous system” of the European economy (SEC (2010) 1395 final) and European capital pushed for infrastructural development, with a strong focus on internal connectivity and the completion of the single market (ERT, 1984, 1991). The European Structural and Investment Funds (ESIFs) for regional development and cohesion were part of the EU’s attempt to boost infrastructure investments in its periphery. Substantial investments were also directed towards modernizing infrastructure in countries in Central and Eastern Europe that were preparing for EU accession.

At the same time, forms of “horizontal” industrial and infrastructure policy displaced sectoral support schemes that were formative for the post-war era (Bulfone, 2023). The market-liberal view was that state intervention would sustain nonviable industries and crowd out private investments. Hence, the purpose of policy was reduced to a role of correcting market failures. Article 107 of the TFEU holds that “any aid […] favoring certain undertakings or the production of certain goods shall […] be incompatible with the internal market.” An exception was established for “the execution of an important project of common European interest.” This did not end support schemes, but states had to refer to less direct forms of state-intervention in the form of off-balance sheet financing and favorable regulation (Thatcher, 2014). Sector-specific liberalization directives sought to establish a “level playing field” for European companies via the liberalization and organizational separation of infrastructure and service providers. This concerned network-bound infrastructures such as transport, energy, and postal services. Effectively, a combination of state aid restrictions, European fiscal rules, and liberalization directives led to public consolidation efforts through the selling of public infrastructure assets.

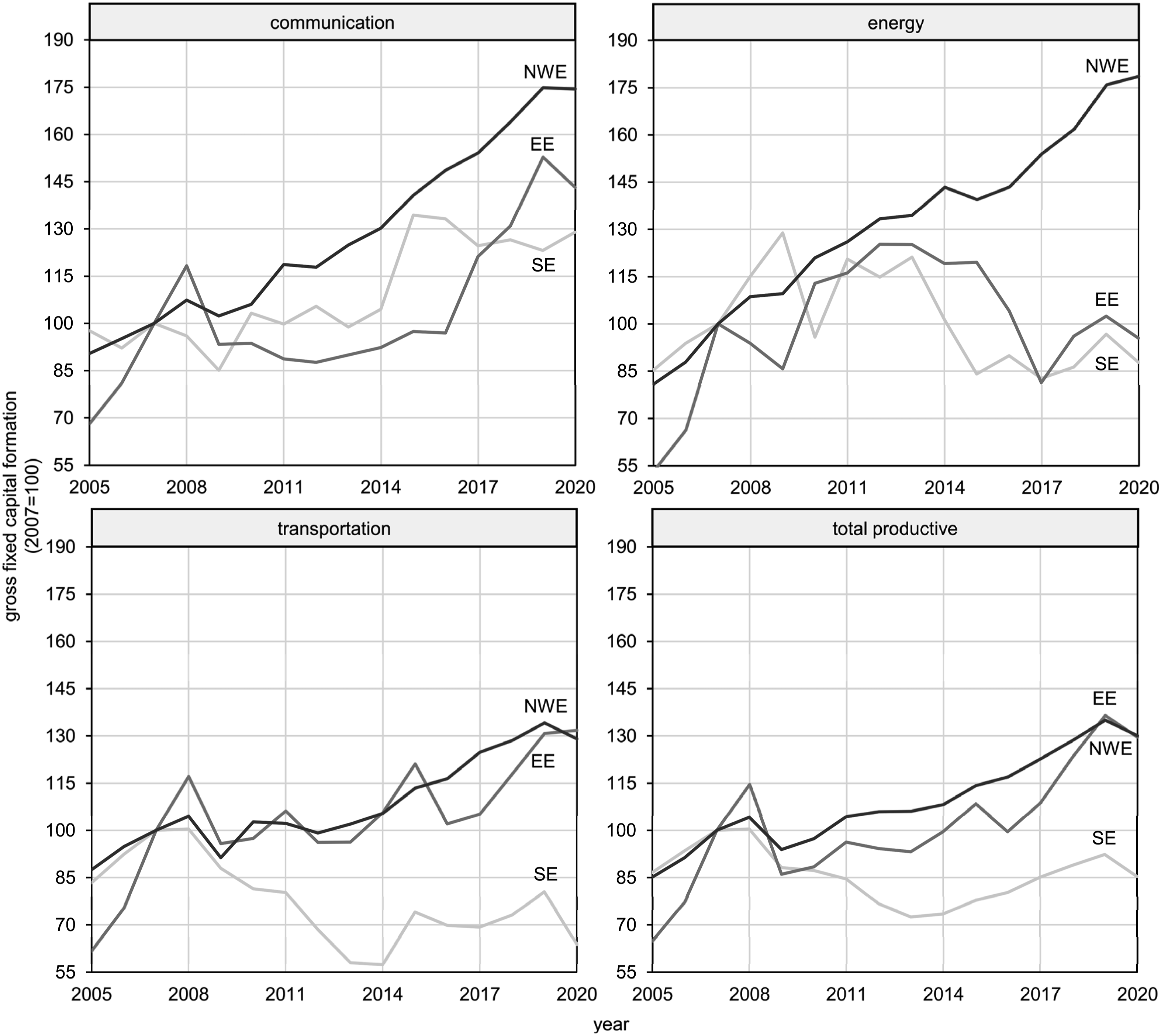

In the euro crisis, the EU turned towards more radical austerity-political ideas, which impacted heavily on the infrastructure policy of its member states. After 2010, infrastructure investments were viewed less in terms of stimulating demand and the economic recovery and more as a field that could be slashed to consolidate households. Figure 1 provides a differentiated perspective on the effects of this agenda, splitting up investment in communication, energy, transportation, and total productive investment into regional categories. Productive investment includes assets that are themselves materially produced, which subtracts land purchases and natural resources, and excludes residential buildings. After the outbreak of the euro crisis, total productive investments in current prices stagnated in Northern and Western Europe (including France, Germany, and the Netherlands) and only lately increased significantly. For Eastern Europe (including Poland, the Czech Republic, and Romania), there has been steady growth after 2009, whereas productive investment in Southern Europe (including Italy, Spain, and Portugal) fell to less than three quarters of its value in the crisis and only slightly recovered since. This demonstrates the asymmetric impact the euro crisis had on national investment levels and how it contributed to a deterioration of infrastructure investment mostly in the South. Productive investment in different sectors for European regions (EE = Eastern Europe; NWE = Northern/Western Europe; SE = Southern Europe), 2005–2020 (source: Eurostat, own calculations).

The asymmetry is differently pronounced with the various asset types. Budget cuts in the EU’s southern periphery had particularly strong negative effects on public investment in transportation and energy infrastructures. In light of weak economic performance, private investment was insufficient to compensate for this. Infrastructure policy on the EU level was also affected, as the disbursement of ESIF infrastructure investment funds was made conditional on states’ non-violation of macroeconomic and budget rules (Deffaa, 2016). As another consequence of the euro crisis, extant asset stocks in the southern periphery, primarily transport and energy infrastructures, were sold to foreign investors to consolidate households. In Greece, the Hellenic Republic Asset Development Fund (HRADF), a dedicated privatization fund, was supposed to create €50 bn. in revenues, yet generated only a fraction of this sum (HRADF, 2020). The fire sale made southern member states dependent on foreign investment from non-European actors. For example, the Shanghai-based conglomerate COSCO Shipping bought up a total of 67 percent of the shares in the port of Piraeus in Athens, one of the largest ports in Europe.

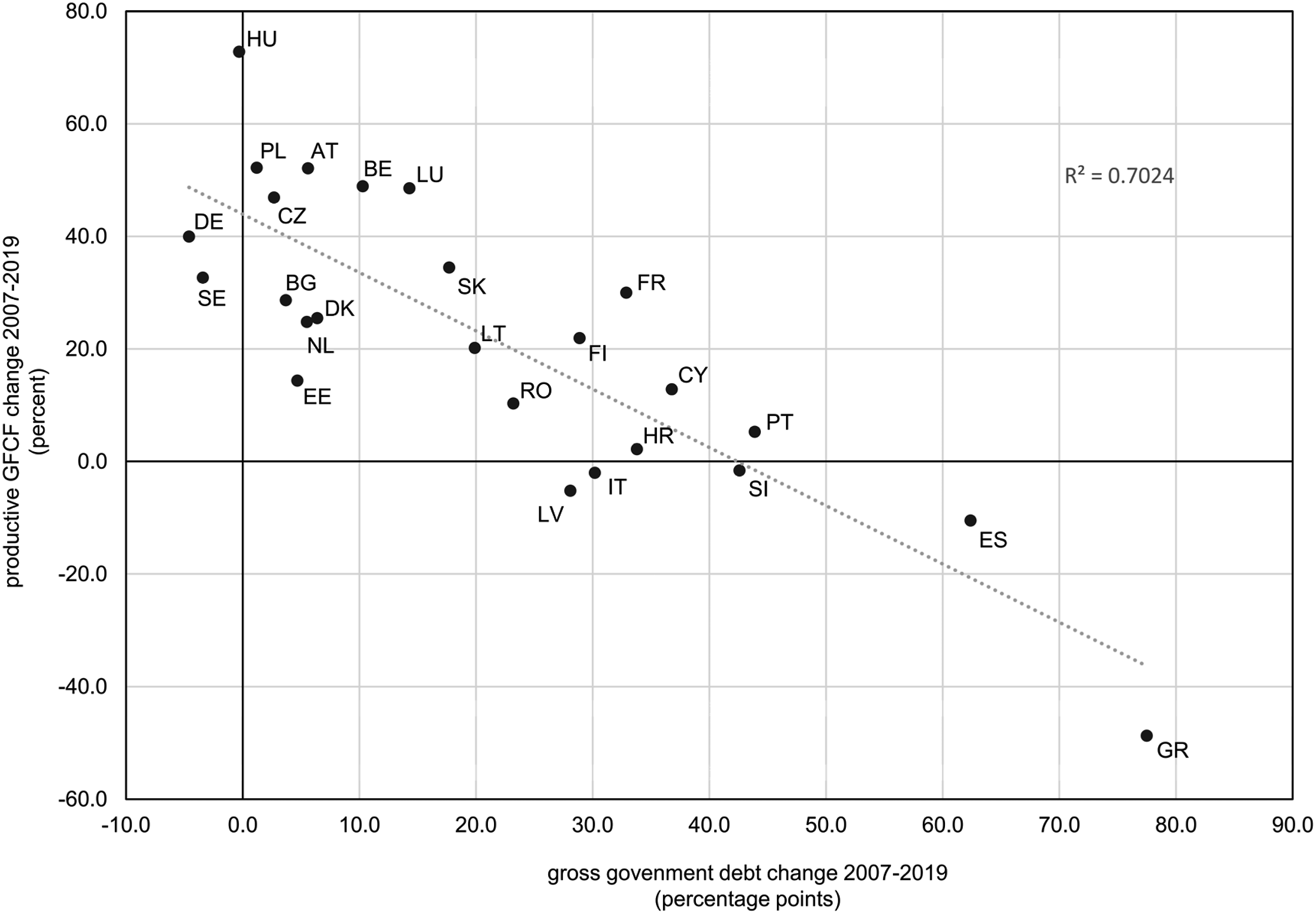

Figure 2 plots the relationship between changes in productive investment and changes in gross debt levels during the euro crisis. It highlights a strong correlation between the two. Generally, one could assume that causality runs both ways. If infrastructures are considered material foundations of economic performance, a drop in investment in such assets will bring down growth levels and increase debt-to-GDP ratios. Yet, in the case of the euro crisis, a debt shock, caused by the bailout of European banks and the recessionary effects of the global financial crisis, came relatively early. Debt levels for Spain, Italy, and Portugal peaked in 2014—around the same time productive investment in Southern Europe reached its lowest point. Hence, the combined data supports the thesis that infrastructure-related investment suffered significantly from a restrictive fiscal agenda. Change in productive investment and in debt levels between 2007 and 2019 for EU member states except Ireland and Malta (source: Eurostat, own calculations, alpha-2 country codes).

Modifications of EU infrastructure policy after 2020 can be attributed to the intensifying global competition as much as the problems of the euro crisis approach in infrastructure policy. The EU has been struggling to produce a coherent response to the Chinese Belt and Road Initiative (BRI), which it fears will cement China’s position as a trade hub and provide it with control over essential global infrastructures. Under President Biden, the US has broken with long-standing constants of economic policy and is implementing large-scale investment programs, like the Inflation Reduction Act (IRA), that strongly subsidize the national development of technology and infrastructures. Against the backdrop of intensifying global competition, the self-proclaimed “geopolitical Commission” von der Leyen engaged in a much more outward-looking infrastructure policy. This reflected in initiatives such as the Important Projects of Common European Interests (IPCEI), which exploit exemptions in the EU’s state aid rules to promote key technological sectors. Both the Commission’s New Industrial Strategy and the European Green Deal build on a strategic agenda that seeks to expand and transform European infrastructure, with a strong focus on digitization and renewable energy. The political context of the pandemic and the breakthrough of negotiations over the RRF, which was allocated resources in the amount of €750 bn., then allowed the EU to also provide some funding for these goals. With the simultaneous deactivation of the SGP, the steps taken during the pandemic represented at least a temporary break with both the fiscal consolidation agenda and its focus on “horizontal” infrastructure measures.

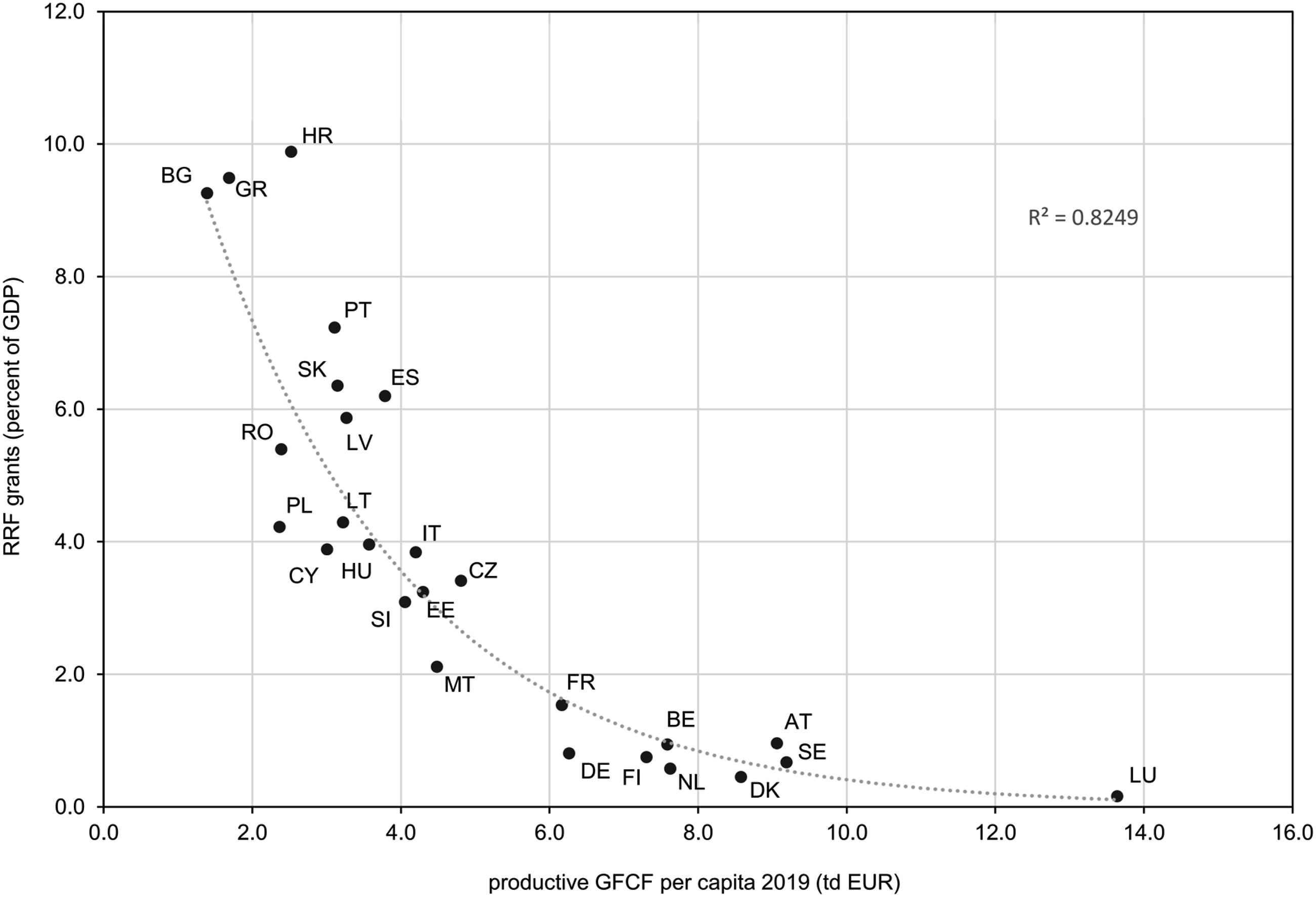

They also reflected an estrangement from the infrastructure political principles of previous phases of European integration. The infrastructure gap in the EU underlines the failure of financial capital to allocate available resources towards infrastructures in an effective manner (Ougaard, 2018). This gap does not just concern the EU’s deficit vis-à-vis global competitors but also the disparity between member states. Figure 3 highlights an exponential, negative correlation between the per capita investment in 2019 and the grants provided to the individual member states by the RRF. It shows that the fund has the potential to remedy, at least to some extent, the asymmetries between member states’ financial ability to develop infrastructures. It also constitutes a break with the pro-cyclical logic of the euro crisis where those countries most strongly affected by the crisis had to cut back on infrastructure investment the most. Productive investment per capita 2019 and total RRF grants for EU member states except Ireland (source: Bruegel RRP dataset, Eurostat, own calculations, alpha-2 country codes).

Yet, member states were able to agree only on one-off instruments rather than permanent institutional reconfigurations. Germany and like-minded northern states resist a fundamental renegotiation of the EU’s fiscal rules as well as the setup of successor instruments to the RRF (Abels, 2023a). This contributes to a contradictory situation where calls for strategic investment and decisive action in infrastructure policy are clashing with a practical reduction of funds that could finance such measures.

Economic ideas and state-business relations in EU policy

The political-economic framework underlying this article highlights the relevance of economic ideas for the formation of EU policy and the role that businesses play in the competition of said ideas. The approach ties in with works by political economists that view the formation of economic policy as well as the political-institutional responses to crises as closely linked to changes in the prevalent economic ideas (Baker and Underhill, 2015; Blyth, 2011). Hall (1993: 279) argues that policy-makers operate on the basis of overarching frameworks of ideas which determine “not only the goals of policy and the kind of instruments that can be used to attain them, but also the very nature of the problems they are meant to be addressing.” Ideas form the interpretive lens through which actors identify problems and narrow down appropriate policy responses. Economic ideas form elements of larger policy paradigms, persistent “cognitive model [s] shared by a particular community of actors” (Carson et al., 2009: 11). Scholars have argued that competing economic ideas and paradigms are shaping international relations and constellations of geoeconomic competition (Beeson and Li, 2015).

A fundamental question within the academic debate concerns under which conditions economic ideas are contested or even replaced. Heuristically, we should not take a shift in policy as a definitive indicator of a shift in the underlying belief system. We might observe policy innovations that seem at odds with hegemonic ideas but turn out to be pragmatic, short-lived fixes rather than long-lasting reorientations. Hence, identifying the replacement or decline of economic ideas presupposes the observation of adjustments in perceptions and attitudes, not merely in policy outcomes (Daigneault, 2014: 463). Crises and economic upheavals represent potential turning points where competing ideas are articulated and rival over dominance in the political discourses surrounding these crises. Fundamental ideological shifts are most likely to take place in times of pronounced crisis, where inconsistencies and inadequacies within the dominant sets of ideas are revealed. Such moments may contribute to an updating of the underlying cognitive frameworks based on the experiences made with associated policy instruments.

Ideological change might take a more incremental or more conflictual form. From a perspective of “policy learning,” the updating of ideas follows a process where new information is internalized and the interpretative framework is transformed accordingly (Moyson et al., 2017). However, if we view European politics—and other political levels—as spaces where competing beliefs and interests condense (Brand et al., 2011), the contestation and replacement of economic ideas is better thought of as the result of actors seizing moments of disruption and crisis to propagate their own vision. This perspective does not rule out the possibility that the interpretive frameworks guiding the action of governments, businesses, social movements, or other social forces are changing over time. Still, it assumes that these changes will largely remain tied to political factions, “their positional advantages within a broader institutional framework [and] the ancillary resources they command” (Hall, 1993: 281).

Analyses of EU policy formation should thus focus on social relations, the positions of influential actors, and potential coalitions. Policy is largely made in intergovernmental rounds where governments negotiate over policy proposals. It evolves around the positions taken by structurally powerful member states as well as the interpretive frameworks they promote. Businesses and their associations play a decisive role in this process. Coen (2009) speaks of a specific “European business-government model” in which EU institutions invite business representatives’ input on legislation processes, while corporations set up representations and associations tasked with pulling decision-making close to their preferred outcomes. EU-specific business associations like the European Round Table for Industry (ERT), BusinessEurope, and SGI Europe as well as national associations such as the Federation of German Industries (BDI) and the Movement of the Enterprises of France (MEDEF) are influential in these contexts. These associations not only represent the interests of powerful national sectors but also an overarching transnational capital interest. As is demonstrated in the analysis conducted in this article, national outlier positions do exist, but European capital is without a doubt capable of developing and representing shared positions. In EU infrastructure in particular, businesses have a privileged position as member states, operating under highly constrained public budgets, count on their ability to steer large sums of private capital into desirable projects. Labor is also represented through its national umbrella organizations of trade unions and the European Trade Union Confederation (ETUC), although a constellation of “austerity corporatism” that emerged after 2010 has side-lined labor representatives and trade unions in the European context (Meardi and Tassinari, 2022).

Private businesses and their organizations, trade unions, and other actors from civil society seek to promote economic ideas that seem compatible with their own interests—and to reinterpret those that are not. It is two economic ideas that this article considers central to contemporary EU economic policy in general and EU infrastructure policy in particular: fiscal austerity and strategic autonomy. Austerity-related economic ideas have long been institutionalized within the legal and procedural elements of the EU architecture. They also guided the bloc’s response to the euro crisis (Helgadóttir, 2016)—although austerity has mostly been referred to as “budget discipline” or “fiscal consolidation” in public discourses due to the negative connotations of the term. Proponents view EU member states in a state of mutual competition that, if not distorted by state interventionism, will safeguard the global competitiveness of the European economy. Infrastructure development in particular is largely subject to market mechanisms, while publicly owned infrastructure becomes the target of privatization efforts. As for its global dimension, fiscal austerity views competitiveness mainly in terms of cost-competitiveness: internal devaluation via the reduction of wages and austerity’s deflationary tendencies are expected to increase the exporting activity of domestic industries (Abels, 2023b).

Strategic autonomy, on the other hand, tends to view the EU as a unitary bloc that stands in competition with global powers such as the US and China. It seeks to maintain the EU’s political-economic significance via a coordination of economic policies and the promotion of overarching European initiatives. As a concept that originally focused primarily on defense and security, it has been stretched—in response to impulses from EU institutions, think tanks, and governments—to include industrial, trade, and infrastructure affairs (Leonard et al., 2019). In the context of infrastructure policy, it provides for an intervening function of the state, which limits infrastructural dependencies against the outside and realizes strategic projects (Abels and Bieling, 2023).

Strategic autonomy has its roots in French discourses centered around a greater European independence from US foreign policy and a directive role of the state (Bora and Schramm, 2023). An increased unilateralism of US foreign policy and competition-distorting economic policies by the Chinese government allowed ideas related to strategic autonomy to gain traction in European politics. The process started in defense and security policy but gradually also affected discussions about the EU’s external economic relations and the development of energy and digital infrastructures (Juncos and Vanhoonacker, 2024).

For the purposes of this article, strategic autonomy is defined as a (geo)economic idea that aims to secure the EU’s capacity to act independently from outside interference via the sourcing of joint funds and the coordinated investment in strategically relevant industries, technologies, and infrastructures. OSA was discussed earlier as a political concept that has made some measures related to strategic autonomy capable of consensus on the EU level. Yet, OSA represents a political invention rather than a relatively coherent economic idea in itself. It functions as a “coalition magnet” (Schmitz and Seidl, 2023) that allows for a variety of interpretations and justifies pursuing at least some degree of state-interventionist policies. Hence, the analysis treats OSA as an outcome of political contest more than an idea, while strategic autonomy is operationalized in line with the afore-provided definition.

Actors seek to balance out or reconcile competing ideas in cases where they expect to benefit from elements of both or for the purpose of alliance-building. As regards fiscal austerity and strategic autonomy, there are two limiting factors to such a strategy, one ideological and one practical. First, while both essentially address different levels of policy-making—strategic autonomy the outcomes, fiscal austerity the budgeting—they entail conflicting perceptions of the state. Strategic autonomy requires a significant amount of state direction to ensure that resources are flowing in strategically desirable initiatives. Fiscal austerity foresees a limited role for state action as well as a general move towards privatization. Second, a historical look at the effects of fiscal discipline on public investment reveals practical incompatibilities. Mühlenweg and Gerling (2023) analyze the statistical relationship between the stringency of fiscal rules and levels of public investment, showing that stricter fiscal rules lead to a stronger decline in public investment than public expenditure. This “disinvestment bias” indicates that, if forced to cut budgets, politicians will disproportionately do so by reallocating resources away from public investments in infrastructures and other assets. This idea of a disinvestment bias is largely supported by data presented in the previous section (Figure 2). The essential consequence is that the attempt to reconcile strategic autonomy and fiscal austerity in a supposedly pragmatic way should be met with considerable skepticism.

Material and methods

What political-economic constellation is underlying the EU’s attempt to still achieve such a reconciliation? The following analysis maps the positions of relevant European actors in infrastructure policy in line with the outlined (geo)economic ideas. It selects actors with respect to the intergovernmental negotiation of member state interests, the pooling of party-political preferences on EU level, and the influence of European capital. The analysis covers the finance ministries of the five largest EU economies—Germany, France, Spain, Italy, and the Netherlands—three relevant directorates of the Commission—the Directorate-General for Economic and Financial Affairs (DG ECFIN), for Competition (DG COMP) and for Internal Market and Industry (DG GROW)—the five largest EU parties—European People’s Party (EPP), Group of the Progressive Alliance of Socialists & Democrats (S&D), Renew Europe (Renew), the Greens/EFA, and Identity and Democracy (ID)—National and European business associations—the Confederation of German Employers’ Associations (BDA), MEDEF, BDI, and ERT—as well as the EU’s cross-industry social partners—SGI Europe, SMEunited, BusinessEurope, and the ETUC.

Views within national governments are not necessarily heterogenous. Particularly between the finance and the economic departments, disagreements occur because the former focus on budgeting while the latter tend to put more emphasis on industrial competitiveness. In countries like France and Italy, both departments are located within the same ministry. For those countries where this is not the case, the decision to code the position of finance ministries is based on their privileged role in central EU bodies such as the Economic and Financial Affairs Council (ECOFIN) and the Eurogroup.

The article undertakes a qualitative content analysis of reports, position papers, and declarations published by these actors as well as media interviews. A total of 150 documents have been selected which explicitly address one or more of the issues of infrastructure policy, SGP reform, fiscal consolidation, and strategic autonomy. Relevant paragraphs have been coded. Actors were mapped, on the basis of all selected paragraphs, along a scale from 1 (highly prioritizing fiscal austerity) to 6 (highly prioritizing strategic autonomy). The selected indicators were deduced from different potential combinations of positions on fiscal consolidation, the sourcing of common EU funds, and public investment in infrastructures. While 1 represents a preference for rigorous fiscal consolidation, a rejection of EU funds, and the subordination of public investments, 6 represents a subordination of fiscal consolidation, a further expansion of EU funds, and a prioritization of public infrastructure investments. Points 1 and 2 are characterized as some facets of fiscal austerity, 5 and 6 as belonging to strategic autonomy, while 3 and 4 describe a middle ground of “targeted flexibility.” The identified positions are momentary assessments based on documents published after 2020. The analysis represents a stocktaking of the current debate in EU policy. Changes between the euro crisis period and the status quo are hard to show systematically as the discourse surrounding strategic autonomy has not been a relevant factor back in 2010 and the years that followed (Juncos and Vanhoonacker, 2024). Changes in positions are outlined and discussed for select actors where their commitment to fiscal austerity in 2010 has been explicitly expressed. This particularly concerns the large business associations such as BusinessEurope and ERT.

When it comes to the public communication of political positions, analysts should be wary of the fact that what is expressed as a position does not necessarily reflect the inherent beliefs of actors. It is not suggested here that all actors associated with a position of strategic autonomy are firmly believing in that vision but that they promote policies aligned with this idea and prioritize it over fiscal consolidation, even if this may be, above all, for self-serving reasons. The position papers, reports, and statements covered by the analysis serve as communication vis-à-vis other parties involved in EU policy formation and as a basis for negotiations. Hence, while there is a certain degree of strategic communication involved, actors still have incentives to accurately represent their political demands.

As another qualification, actors’ discursive reference to the same economic idea may conceal diverging interpretations about its specific elements and implications. Fiscal austerity can be undertaken from the expenditure side—cutting public spending—as well as from the income side—increasing taxes or introducing new forms for taxes. While for fiscal austerity the focus in European politics has almost exclusively been on the former, strategic autonomy has been a more ambiguous idea, at least concerning its policy implications. Juncos and Vanhoonacker (2024) show that the European debate on strategic autonomy was characterized by a divergence in views about what such ideas would mean for the future degree of sovereignty from US policy. The operationalization outlined above treats both fiscal austerity and strategic autonomy as ideal-typical concepts that are used to structure a relatively complex political debate. The selected indicators are meant to translate these concepts into measurable data that cover their basic denominators.

As a final remark, the European Commission plays an ambivalent role in the process of EU policy making. On the one hand, it functions as an agenda-setter and initiator. Decisions and reforms surrounding the strategic autonomy discourse can be retraced to Commission initiatives. At the same time, it functions to a substantial degree as a “broker” of EU policy, staying in close contact with member states governments to identify potential landing zones. The analytical decision was made to code statements of the relevant Directorates-General within the European Commission to outline their positioning in the overall constellation, reflecting their substantial role in pre-determining policy outcomes.

Actor constellations in the austerity-autonomy conflict

Strategic autonomy

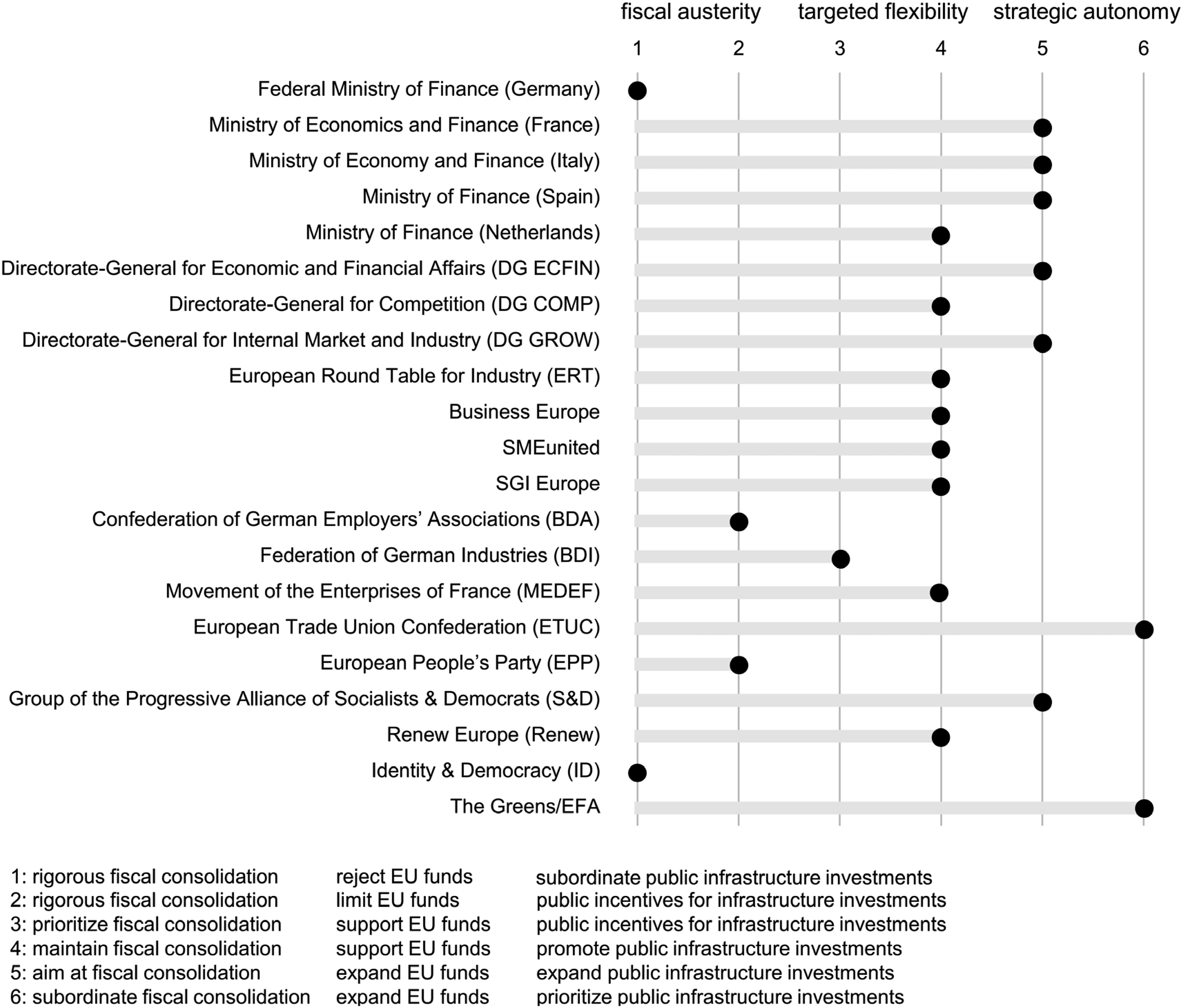

Figure 4 presents the results of the content analysis. A more detailed list of positions and sources is included in the Online Appendix. As a first central finding of the analysis, a substantial group of actors has rallied around the strategic autonomy idea. This concerns the finance ministries of the southern member states, important Directorates-General, the social-democrats and greens in the EP, as well as the trade unions. The French ministry has been outspoken about its support for a reform of the SGP, whose automated features it considers having “led to recession, economic hardship, [and] a loss of production and growth in Europe” (Liboreiro, 2023a). At the same time, it is one of the strongest proponents of an agenda to “strengthen the Union’s strategic autonomy and lay the groundwork for its future economic sovereignty” (Le Maire, 2020). In line with this, it published a joint declaration with the Ministry of Economy and Finance of Italy, in which they express their shared support for further strategic EU resources in the form of a European sovereignty fund (Urso and Le Maire, 2023). The Spanish finance ministry takes a similar position. The southern finance ministries have been long-standing advocates of an SGP reform, but the economic shocks following the pandemic and the emerging discourses surrounding strategic autonomy have allowed them to pursue this agenda more confidently. Positions of relevant actors on competing ideas in infrastructure policy (own depiction).

DG ECFIN under Commissioner Paolo Gentiloni has been at the center of Commission initiatives to reform the SGP under the economic governance review and to establish the RRF. Gentiloni was outspoken about his goal to reform fiscal rules in such a manner that they would allow “for reform and investment and reducing high public debt ratios in a realistic, gradual and sustainable manner” (Liboreiro, 2023b). He has also positioned himself as an early supporter of the RRF and a strong proponent of a permanent sovereignty fund that “safeguards the single market, enhances our strategic autonomy and supports the climate transition” (European Commission, 2024). DG GROW, led by Thierry Breton, has approached these questions from a more industrial angle but came to similar positions where it supported the reform of the SGP to accommodate climate-related and strategic investments as well as the setup of a sovereignty fund to “diversify and reduce our economic and industrial dependencies” (Borrell and Breton, 2020).

S&D is supporting the Commission’s plan to make the SGP more flexible, reduce its pro-cyclicality, and add a permanent financing capacity that would complement the EU’s regular budget (S&D, 2023). Greens/EFA and ETUC are located at the outer end of the spectrum due to their more transformative demands on the SGP review as well as their support for a more interventionist role in the development of strategic infrastructures. Greens/EFA explicitly aligns itself with strategic autonomy and proposes to further expand EU funds, especially to finance the green transition. As regards the SGP, it calls for a comprehensive reform which includes a rule that exempts green investments from budget limits (Greens/EFA, 2023a). Furthermore, it wants fiscal consolidation to be shifted to the income-side rather than be expenditure-based. Hence, the party demands a European wealth and financial transaction tax (Greens/EFA, 2023b).

The ETUC has also been advocating for a substantial revision of the SGP, including steps towards the prioritization of public investment and a modification of the budget deficit limits. It envisages financing of public investments and expenditure via a wealth tax and a windfall tax (ETUC, 2022). The ETUC strongly supports the strategic autonomy agenda but demands it “not be used as a vehicle for austerity measures or deregulation” but instead as a tool to directly finance “quality public infrastructures” (ETUC, 2023). Generally, the ETUC prioritizes investment over expenditure-side consolidation and seeks to direct new sources of funding towards publicly owned infrastructures.

Fiscal austerity

At the other end of the spectrum the analysis locates the Federal Ministry of Finance of Germany, supported by its national employers’ association BDA, as well as the EPP and the right-wing ID faction. As a second key finding, the constellation around fiscal austerity has been losing the support of European capital over the last decade. Yet, Germany as EU’s largest economy remains deeply committed to fiscal discipline. Germany’s finance ministry, after a brief period of state-interventionist measures during the pandemic, has returned to its rigid stance. In a joint declaration with the ministries of several medium-sized and smaller EU economies, the German finance ministry insists on maintaining the SGP’s targets and not exempting public investments from its calculations because “as far as the capital markets are concerned, debt is debt” (BMF, 2023b). Germany has been outspoken about the fact that it considers the RRF and related instruments as one-off measures specifically tailored to the emergency situation of the pandemic. In line with this, it also rejects the establishment of further RRF-style fiscal capacities (BMF, 2023a).

The German finance ministry has received support from the German BDA which, as Figure 4 reveals, constitutes an outlier among European and national business and employer associations for its rigorous insistence on fiscal austerity. The BDA is lobbying to maintain the SGP in its current form, arguing that member states should “respect the unchanged basic principles of the Stability and Growth Pact” and that fiscal consolidation should “not be a matter of negotiation [but] requires binding rules” (BDA, 2023). It was also the only association to withhold its approval from BusinessEurope’s coordinated call for fiscal stimuli and EU financing during the pandemic (BusinessEurope, 2020).

On the party-political side, fiscal austerity has been at the center of the agenda of the conservative EPP, the largest European party before and after the 2024 European elections, and of the right-wing ID. The EPP has called for a further tightening of the SGP “with clear rules and fewer exceptions” (EPP, 2021). Early in the pandemic, it warned that “the current frenzy of Corona spending [could] lead us directly into the next debt crisis” and called for the SGP’s escape clause to run out (EPP, 2020). ID takes a similar position, although in a more drastic and in parts contradictory form. ID is against any EU funds financed by common debt which it views as “a clear violation of the European Treaties” (ID, 2023). The party calls the RRF an “illegal debt-funded […] EU programme” (ID, 2021b). ID demands to “reactivate and reinforce the Stability and Growth Pact to rapidly reduce debt levels across member states.” In line with its populist roots, the ID has at the same time been highlighting the “inadequacy of European instruments,” including the SGP, and has ominously stated that “the EU must not return to austerity” (ID, 2021a).

The fact that the German finance ministry is the only one strongly committed to fiscal austerity among the five mapped ministries should not be equated with it being isolated in that position. In fact, its demands have been shared by the finance ministries of other countries such as the Czech Republic, Denmark, and Austria (BMF, 2023b). However, it is true that the actor constellation around fiscal austerity as an interpretive framework has been losing the support of private capital. First and foremost, this has to do with a move of business actors towards a more mediating position. Central to this development are shifts in the position of the ERT and of BusinessEurope. In 2010, at the onset of the euro crisis, both associations clearly propagated fiscal austerity as an economic idea. The ERT (2010), for example, had been a major advocate of “cutting public expenditure on policies that are not sustainable” in all austerity-related sectors such as pensions, social security, and health.

Targeted flexibility

The positioning of business associations has changed significantly between 2010 and 2020, with both the ERT and BusinessEurope now clearly located within the constellation of targeted flexibility. A third key finding of the content analysis is the overwhelming support that targeted flexibility receives from business actors across Europe which seek the best out of both worlds: a consolidation via the expenditure side, which spares them from higher taxes and levies, coupled with public investments that make private investment more lucrative and de-risks them “by tinkering with risk/returns on private investments” (Gabor, 2023: 1). To that extent, the (non)paradigmatic position reflects a preference for shifting budget cuts away from investments that are considered strategically relevant for profit and competitiveness and towards austerity-conform reductions elsewhere. As Lepont (2024: 2) argues, this position is congruent with a redefinition in state financing where “investment is considered to be good and wise public spending, and even worth borrowing for,” whereas all expenditure “not deemed an investment is delegitimized.” The de-risking of private investment also does not necessarily foresee a greater role for the state but has, without clear conditionality, the potential to reduce state intervention to insuring business action and making it financially lucrative (Bulfone et al., 2023).

The ERT now ties into the strategic autonomy idea by stating that “dependencies can potentially create strategic vulnerabilities that must be managed in the public interest” (ERT, 2021). Beyond that, it has welcomed the RRF and a potential European sovereignty fund. For the public aid of business activities, the ERT proposed tax incentives—similar to the US-American IRA—that could replace “cumbersome and lengthy procedures for upfront applications” for subsidies (ERT, 2020). BusinessEurope—with the exemption of its member BDA—has been supportive of state-interventionist and strategic measures on the EU level, including the ICPEIs and the RRF. It has called for “a significant boost to trans-European infrastructure” through “significantly higher investment” and more counter-cyclical EU funding (BusinessEurope, 2020). Back in the euro crisis, BusinessEurope had been highly suspicious of joint EU debt in the form of Eurobonds as this would have eased the financial pressure on national governments to implement structural reforms (BusinessEurope, 2010). However, the association still holds the position that strategic investment should be coupled with fiscal consolidation to reduce interest rates via lower refinancing costs. In line with this, BusinessEurope, while being open to more generous fiscal adjustment paths, has argued that the current SGP targets need to be maintained and that fiscal rules “must not provide excessive flexibility in their interpretation” (BusinessEurope, 2023). Hence, while global competitiveness and strategic autonomy serve as common denominators for the European social partners—which even led to common declarations of the ETUC and the European business associations (BusinessEurope, 2017)—positions on the EU fiscal framework differ fundamentally.

We see a similar positioning with national member associations of BusinessEurope. The BDI’s communication reflects many discursive elements related to strategic autonomy. It has also been among the first to demand a policy shift towards public stimuli (BDI, 2019). The BDI has been expressing its preference for tax credits as an investment tool. Just like the ERT, it refers to the US as an example: “With the IRA, the USA has shown how it can be done” (BDI, 2023a). However, in line with targeted flexibility as an interpretive framework, the BDI has at the same time been welcoming Germany’s return “towards consolidating fiscal policy” which should be coupled with a “consistent prioritization of spending” (BDI, 2023b).

Interestingly, the French MEDEF has taken a similar position to its German counterpart. Together with the Italian association Confindustria, it has been calling for European competitiveness and “strategic autonomy and independence in key sectors,” approving of the Commission’s major strategic initiatives (MEDEF, 2023). Still, it aligns with the position of other business associations rather than the French finance ministry when it comes to fiscal consolidation. MEDEF suggests a more limited reform of the SGP, at the core of which remains a return to the current budget targets (MEDEF, 2023) as MEDEF considers a reduction of member states’ sovereign debt “the prerequisite for their ability to act” (MEDEF, 2017).

The Dutch Ministry of Finance and the European Renew party are two more actors the analysis positions within the targeted flexibility group. This finding is highly relevant. Having been among the austerity hardliners during the euro crisis, the Dutch position has changed with Sigrid Kaag of the social-liberal Democrats 66 assuming office as finance minister in 2022. The Dutch finance ministry signed a joint communiqué with the Spanish ministry on the reform of the SGP, calling European and national investment “indispensable to crowd-in private investments in strategic areas” (Government of the Netherlands, 2022). On future joint-debt funds that go beyond the RRF, however, Kaag commented that “this is not something the Netherlands supports” (van Gaal, 2022). The Dutch positioning in the analysis is the result of a stock-taking of the previous years and will be subject to changes in government after the 2024 elections. However, it clearly demonstrates how policies related to strategic autonomy could gain such traction recently, even among the formerly unified pro-austerity bloc.

DG COMP under Commissioner Margrethe Vestager is also assigned to this group. As its competences are elsewhere, the directorate has shied away from positioning itself too strongly on fiscal rules reform. Vestager expressed her support for OSA and the continuation of the RRF via a sovereignty fund. Yet, in her vision, this fund would not support public investments per se. Rather, it would have de-risking attributes and act more like a venture capital fund. She argues that the “differentiation between us and the US, is that we do not have sufficient risk-willing capital for the scale up period of time” (Mathews, 2023).

Renew is a liberal EU party of which both German finance minister Lindner’s party and French president Macron’s party are members. This makes positioning for Renew rather delicate when it comes to questions of public investment and fiscal consolidation and results in at times ambiguous statements. In large parts, Renew aligns itself with the French preferences. It supports a review of the SGP that would give the Commission more flexibility in setting debt targets for individual member states, arguing that “one size fits all austerity policies are not the adequate answer” (Renew, 2023). It furthermore lent its support to OSA and even a potential European sovereignty fund “to advance the EU’s so-called open strategic autonomy in key areas such as energy infrastructures, cybersecurity, industrial competitiveness or food security” (Renew, 2022). Still, there have been concessions to the more fiscal-disciplinary fractions, which have resulted in Renew stating that it does not suggest the SGP’s “complete overhaul” but “ambitious debt reduction plans” (Renew, 2023).

Conclusions

The EU finds itself at a critical juncture where, in reaction to economic shocks caused by global power competition, strategic autonomy is gaining traction as a (geo)economic idea. In contrast to previous works, this article argues that strategic autonomy is set up against the idea of fiscal austerity more than market-liberalism. Fiscal austerity has been dominant throughout the euro crisis as it united a powerful coalition of state and business actors behind it. Restoring Europe’s global competitiveness in line with strategic autonomy would require a subordination or at least a deferral of fiscal consolidation. Hence, the two ideas display practical incompatibilities.

Infrastructure investments play a key role in reaching political objectives related to strategic autonomy: a reduction of external dependencies and a strengthening of the economic base of EU member states. An analysis of the history of EU infrastructure policy has underlined that, under conditions of fiscal austerity, infrastructure investments are declining disproportionately. During the pandemic, this trend has been reversed to some extent due to alternative policy ideas finding their way into crisis management. Yet, a return to fiscal consolidation in line with the Maastricht targets is imminent and the RRF and other instruments are increasingly likely to run out without a follow-up in place. Against this backdrop, it was argued that the formation of EU economic policy is, in its current state, less consistent and more brittle than previously suggested.

To uncover the constellations of interests and ideological positions underlying this state, a qualitative content analysis was carried out that highlighted three central findings. First, there is a considerable actor constellation that prioritizes strategic spending over fiscal consolidation. Actors that promote strategic autonomy include the finance ministries of the large southern economies, DG ECFIN and DG GROW, the European social-democrats, as well as the Greens/EFA and trade unions—while the latter two lean even more heavily on the idea to strictly subordinate expenditure-side consolidation.

Second, the actor constellation around fiscal austerity is losing the support of European capital. Major lobbyist groups have moved towards an intermediate position. This leaves German finance ministry, the German employers, and the European conservatives as well as the right-wing populist ID. Still, the constellation contains major spoilers and enablers of European action. This concerns Germany first and foremost which, after clearing the way for the RRF in the pandemic, has returned to its rigid austere position, but also the EPP as the largest EU party. The result is a deadlock between the two groups as regards the political weight behind them.

Third, this has coincided with the emergence of a middle-ground constellation that is characterized by the attempt to combine certain elements of the two ideas. It consists of the major European and national business associations, plus the liberal Renew party, DG COMP, and the Dutch finance ministry. Their position picks up the problem descriptions and political recipes of strategic autonomy, mostly a reduction of Europe’s external dependencies via investments in infrastructure and a de-risking of business activity, but combines them with the maintenance of an overall fiscal-disciplinary course. Capital interests across Europe are gathering behind this stance.

Conceptions of what the pursuit of strategic autonomy would actually imply have been diverging between actors, which hinders closing ranks or a co-optation between camps. Both the ETUC and the large European business associations are by and large in favor of state-interventionist measures on strategic infrastructure. Yet the former’s view that public money should mainly flow into publicly owned infrastructures is incompatible with the latter’s preference for the de-risking of private infrastructure development.

A first main implication of these findings is that EU economic policy is currently in an intermediate state where neither proponents of strategic autonomy nor of fiscal austerity are able to fully assert themselves. For now, EU policy in general reflects this ideological deadlock: extant resources like the RRF and the policy spaces created by the SGP’s temporary deactivation are used to finance strategic measures. Yet, we currently see a rollback of these forms of public financing that find their expression in indecisive reforms like the STEP component of the EU budget. The effect of the recent European elections and new appointments to the European Commission is still to be determined, yet the upsurge in right-wing vote shares and the weakening of green-ecological parties are likely to inhibit political initiatives built on strategic autonomy discourses.

A second main implication is that the “targeted flexibility” position taken by European capital might dominate EU policy-making in the medium term. Under the assumption that no agreement on a follow-up fund to the RRF is found, the pressure of strategic investments will be on member states’ national finances. Yet the expectation that they will rebalance their budgets towards supporting geoeconomically relevant business activities is unlikely to be fulfilled. A historical look at EU infrastructure policy highlights that, under conditions of austerity, public investment in infrastructure-relevant sectors has declined disproportionately. Hence, infrastructure policy, but also related areas such as industrial, digital, and energy policy, could turn out the victim of the EU’s latest return to fiscal consolidation. A more fundamental shift in economic ideas towards strategic autonomy might then become a necessary condition for a coherent geoeconomic agenda that restores the EU’s global competitiveness and its ability to react to crises. Yet it would certainly face considerable opposition from the remaining austerity bloc and potentially also from European capital.

Supplemental Material

Supplemental Material - Making “strategic autonomy” rhyme with “fiscal austerity?” Unresolved conflicts of (geo)economic ideas in EU infrastructure policy

Supplemental Material for Making “strategic autonomy” rhyme with “fiscal austerity?” Unresolved conflicts of (geo)economic ideas in EU infrastructure policy by Joscha Abels in Journal of Competition & Change.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

This work is supported by the Excellence Strategy of the German Federal Government and the states under grant EF-BIELIN-2022-01 as well as the German Research Foundation (DFG) within the EUInfra project, project number 526359979.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.