Abstract

In the emerging triad competition between the US, China and the EU, the control over infrastructures is increasingly contested. This paper asks how this conflict of connectivity influences the EU’s infrastructure policy and what specific factors play a role when translating these global shifts into strategies. We develop a political-economic perspective that highlights the relevance of infrastructures for capitalist production and the pattern of dependencies between actors. Viewing the triad competition in infrastructural terms, we argue that the EU is in the process of becoming a geopolitically and geoeconomically oriented infrastructural policy actor. Two cases in the field of high-tech infrastructure are studied more deeply: the EU’s development of the satellite navigation system Galileo and its strategy on 5G. They show that – despite the EU’s geoeconomic approach – the particular mode of global competition in combination with internal political factors can hinder the translation of geoeconomic ambitions into specific policies.

Introduction

The political economy of globalisation traditionally focuses on the development of cross-border trade in goods and services, of foreign direct investments of transnational corporations, and of the creditor-debtor relationships that are formed by financial flows (for an overview see Dicken, 2011; Held and McGrew, 2003; Michie, 2019). Analyses also focus on how these processes and relationships have been supported and promoted by international treaties, regimes and organisations. It is often presumed that, due to the expansionism of competing economies and the processes of technical innovation, a further progression of globalisation is a law of nature. Yet, these very components of the liberal international order recently face challenges, as exemplified by the protectionist foreign trade policy that has characterised the US approach towards both China and the EU under the Trump administration. This has highlighted that globalisation is by no means an inevitable process but underlies essential preconditions.

In terms of these preconditions, the political-economic discussion has primarily dealt with the social, political and institutional dimensions of globalisation, that is, the balance of social forces (Cox, 1987), international power relations (Van der Pijl, 2006), and forms of governance (Barnett and Duvall, 2005). The material dimension, meaning the infrastructural networks that operationally enable cross-border economic connectivity in the first place, was traditionally taken as given and therefore rarely made the subject of inquiry. This seems to be gradually changing (Flint and Zhu, 2019; Leonard, 2021). The reasons for this are multi-layered. One reason is that the production and use of infrastructures – particularly those related to transport and energy – entail considerable carbon dioxide emissions and thus are subjects of an ecological debate. Furthermore, infrastructures often prove to be rather sensitive, unstable and contested. This has been highlighted by the costly blockade of the Suez Canal in 2021, the shutdown of Chinese harbours as a consequence of Beijing’s zero-COVID strategy, and the international conflict over the gas pipeline Nord Stream 2. Finally, in light of the shifts in global power relations and the emergence of a new triad competition between the US, China and the EU, the control over infrastructures and their geopolitical instrumentalisation are increasingly contested (Abels and Bieling, 2022).

In this paper, we add to an emerging debate on the relevance of infrastructures for global order by making the case for a political-economic perspective on their production and operation. We develop a theoretical understanding of infrastructures that underlines not just their strategic but also productive aspects. On the one hand, control over infrastructures involves forms of territorial and social control. Their specific configuration reproduces or changes the dependencies between actors – state agencies, businesses, and civil society. Infrastructural control is not only, often not even primarily, a concern of governments, but also of private capital, particularly transnational corporations. Thus, our perspective sets itself apart from state-centred approaches such as the ones found in the recent academic discourse on ‘weaponisation’ (Farrell and Newman, 2019; Gertz and Evers, 2020). On the other hand, we underline the importance of infrastructures for the spatio-temporal anchoring and expansion of capitalist production. They embed processes of capitalist development materially and present opportunities to shift investments temporally and across geographical distances.

Empirically, we are focussing on infrastructural strategies of the EU. So far, this subject has been sidelined by analyses of US and Chinese infrastructure policy, in particular Beijing’s Belt and Road Initiative (BRI) (Andornino, 2019; Benabdallah, 2019; Zhou and Esteban, 2018). In the academic debate, the EU usually appears as a ‘reactive’ infrastructure policy actor – with occasional exceptions (Meunier and Nicolaidis, 2019). Yet, this does not pay justice to the evolution of EU infrastructure policy. It has been departing from an internal market perspective focussing on the liberalisation and privatisation of network industries (Clifton et al., 2003) via a phase of ‘securitising’ infrastructures after 2001 (Bossong, 2014) to a recent phase of embracing a geopolitical and geoeconomic logic. European infrastructure policy is increasingly directed outwards and should thus be examined as a specific phenomenon. Under the Von der Leyen presidency, the EU has shifted its agenda further towards an active infrastructure policy and strategic autonomy, with proposals like the EU’s ‘New Industrial Strategy’ and the recent ‘Global Gateway’ initiative at its heart. It is against this background that this paper asks how the EU’s competition with the US and China influences its infrastructure policy and what EU-specific factors play a role when translating geoeconomic ambitions into infrastructural strategies.

Our argument is two-fold. On the one hand, there is indeed a change in EU infrastructural policy induced by the afore-mentioned global shifts that makes the EU adopt a more geoeconomic approach to its overall decisions and strategies. On the other hand, however, while external competition has a mobilizing effect and creates an impulse to act, the particular mode of global competition and internal conditions have mediating effects on the policy outcome. The insufficient organisation of competences and resources as well as strongly diverging national conditions lead to a substantial fragmentation in policy responses that might run counter to a geoeconomic orientation. This fragmentation also serves as a doorway for Chinese and US strategies of interference which, depending on the particular mode of competition in an infrastructural field, have an additional divisive effect on the EU. As a consequence, it is precisely in situations of high global pressure that the EU’s ability to act tends to be impaired. The assumption that the EU will act strategically on infrastructure just because global circumstances require it is thus misguided. Rather, certain constellations of interests and institutional arrangements are prerequisites for this.

The argument is supported by the findings of this study. The first section conceptualises infrastructures of globalisation in political economic terms and unfolds our perspective. Based on this, we argue that the formation of transnational infrastructure policy is best understood as a product of global competition, mediated by its particular mode and the condensation of public and private interests. The second section then discusses the current triad competition in infrastructural terms. The third section empirically outlines the EU's position and the challenges it faces in that context. This reveals a general shift of EU narratives and agenda towards a geoeconomic logic; yet, the fourth section demonstrates that the intensified conflict between the US and China and internal political factors hinder a more strategic and coordinated response to infrastructural challenges. It does so by reconstructing historical processes in two fields of high-tech infrastructure: satellite navigation and telecommunication. The conclusions discuss the theoretical and political implications of our findings.

Conceptualising infrastructures of globalisation

The current historical constellation is superficially reminiscent of the one that was prevailing at the end of the 19th and beginning of the 20th century. At that time, too, the hegemonic structures of the world order had begun to falter. Great Britain was struggling to maintain its concept of liberal world order and saw itself exposed to competing capitalist models – first and foremost from the US and Germany. In this ‘age of empire’ (Hobsbawm, 1987), nationalist forces opposed the ongoing processes of globalisation and liberalisation (Dent, 2020). Furthermore, conceptions of geopolitics arose at that time, by which economically and militarily leading states or empires claimed power and control over foreign territory.

In order to grasp the nature and the specific quality of the current constellation of global ‘interregnum’ we should acknowledge the central differences between our time and the turn of the 19th century. These concern the international hegemony and mode of operation of the liberal world order. US hegemony – in comparison to British hegemony – is characterised by more comprehensive and deeper forms of capitalist penetration due to the advanced stage of capitalist development (Arrighi, 1994: 72–73). Transnationally traded services, cross-border value chains, and the underlying infrastructures are of much greater importance. They are flanked by comprehensive legal and institutional frameworks – trade and investment agreements, international organisations, and numerous transnational business networks that support capitalist globalisation. Today’s geopolitical and geoeconomic discourses also differ significantly from earlier conceptions. Developed around the turn of the 19th century by Rudolf Kjellen, Friedrich Ratzel and Karl Haushofer, they discussed politics in terms of natural spatial determinants such as topography or climate and interpreted inter-state relations as a struggle for living space. Later, geopolitical thinking became more military strategic. The desire to maintain control over the Eurasian continent continued to have an effect on geopolitical discussions in the US (Brzeziński, 1997). In this context, energy political considerations, that is, the desire for control over a region with rich oil and gas reserves, played an important role, whereby the focus has broadened to include issues of trade, transport and market development. More recently, we can observe a rising influence of ‘critical geopolitics’ (Albert et al., 2014), no longer understanding space as a natural determinant of politics but, conversely, as a socially and thus also politico-economically constructed factor.

In the context of the ongoing transformation of the global political economy and the emergence of the new triad competition, geopolitical debates centre more and more on geoeconomic considerations. Geoeconomics assumes a rivalry between states that is fought out not with military force but through means of commercial and industrial policy. For Luttwak (1993: 41), geoeconomic strategies differ with regard to ‘the means, from research and development to export finance; the immediate goals of technological and market superiority; and the consequences, internal and external’.

The spatial or territorial component of geoeconomics is by no means exhausted by gaining access to or control over markets through commercial and technological efforts. At least as important, but often overlooked, are state activities to secure access or control over markets through infrastructure policy. Recently, these activities have been subject to greater scrutiny in the context of the critical-liberal ‘weaponisation’ debate. Prominently, Farrell and Newman (2019) argue that globalisation is not a positive-sum game as assumed by concepts of ‘complex interdependence’. Rather, asymmetrical power relations are forming in global networks. The authors identify central nodes (‘hubs’) through which the access and operation of global networks can be monitored and controlled. In this context, ‘weaponisation’ refers to all those processes through which states may seize transnational infrastructures and use them against others. Two of those processes are highlighted: collecting information and monitoring communications to create an advance in knowledge (‘panopticon effect’); and restricting the access to and use of networks for certain actors (‘chokepoint effect’).

For Farrell and Newman, the basis of transnational infrastructural power lies in the asymmetry of global political-economic interdependencies, combined with the institutional and legal control over the central nodes. Adopting a slightly different perspective and addressing more directly questions of geoeconomic competition, Gertz and Evers (2020) also contribute to the weaponisation debate. They argue that China appears to be more capable than the US of exploiting the extraterritorial governance of transnational infrastructures to its own benefit. In contrast to Farrell and Newman, they consider the close relations between states and infrastructure corporations as decisive for the distribution of international control power, which is why they attribute a strategic advantage to Chinese capitalism.

The discussion around weaponisation is instructive as it draws attention to important processes through which infrastructure policy concepts and initiatives are geoeconomically implemented. However, the critical-liberal perspective remains limited for several reasons. First, the state is treated as a unitary actor. The processes of state transformation and fragmentation, and thus also the conflicts fought out within and between state apparatuses, hardly come into view. This seems over-simplistic – particularly in the context of the EU’s ensemble of state apparatuses (Wissel, 2014). Second, relations between state and capital are conceptualised in a one-dimensional manner that focusses on states’ control over national businesses. There is hardly any differentiation between different fractions of capital and their interests. Civil society actors such as trade unions or social movements, which for their part try to influence the arrangements negotiated between state and capital, are also not considered. These two weaknesses ultimately entail that processes of weaponisation are primarily viewed as a product of state action, and not of the condensation of interests between social forces. Finally, while the perspective correctly outlines the strategic importance of infrastructures, their productive function, that is, their role in realising public wealth and private profits, is neglected. Consequently, infrastructures are mostly treated as a means of global power politics and not also as an end of statist and private action.

We propose a political-economic understanding of infrastructures that takes into account both their strategic and productive aspects. With regard to the former, there is a general agreement with weaponisation approaches that patterns of control over infrastructure are highly relevant for questions of global order. Technological and material dominance creates conditions of asymmetric dependency in such networks. These asymmetries are modified by processes of technological and administrative standardisation and norm-setting, for example through international organisations and treaties. This regulatory dimension plays a fundamental role in making these networks viable and specifies who is in control and has access to them. Both material and regulatory asymmetries can be exploited by actors for offensive action. Yet, we stress that it is not just states who are the enactors or recipients of such measures. Private capital, particularly transnational corporations, is in control of vital infrastructure hubs and able to exploit others’ dependency on the infrastructure they are providing – think of the role of commercial energy suppliers or global internet firms. Their interests can by no means be subsumed under those of their country of location. At the same time, private actors can be the target of weaponisation measures, forcing them to adjust their position. These interests are relevant as the supply of cross-border infrastructures turns into a practically lived connectivity only through their use by capitalist firms and numerous consumers. What is more is that in a more complex understanding of state, state apparatuses themselves are competing with each other over resources and influence. For example, on a national level, the interests between different political departments are often conflicting – also with regard to the roll-out and design of specific infrastructures. These complexities should be reflected in a comprehensive understanding of how infrastructures are instrumentalised strategically.

Addressing the productive dimensions, this paper underlines the importance of infrastructures for the spatio-temporal anchoring and expansion of capitalist production. This refers to David Harvey’s concept of the ‘spatio-temporal fix’, linked to ‘capitalism’s insatiable drive to resolve its inner crisis tendencies by geographical expansion and geographical restructuring’ (Harvey, 2001: 24). It underlines the relevance of the linkage between economic and non-economic elements, that is, of a socio-politically generated, relatively durable ‘structured coherence’ in the process of capitalist accumulation (Jessop, 2006: 162). Infrastructures play a key role in this as they allow for the mobility of capital, goods and services, thus structuring spaces and ensuring the stability of the capitalist process. ‘Fixing’ here has a double meaning. On the one hand, it is a matter of fixing the processes of capitalist development spatially and temporally, that is, of anchoring or embedding them materially. On the other hand, the process of producing and realising added value in capitalist development tends to be unstable and requires constant reparation. Infrastructures create opportunities to shift profitable investments across space – which they bridge, for example, through transport and communication – and time – creating incentives to invest in large-scale infrastructural projects to realise added value in the future.

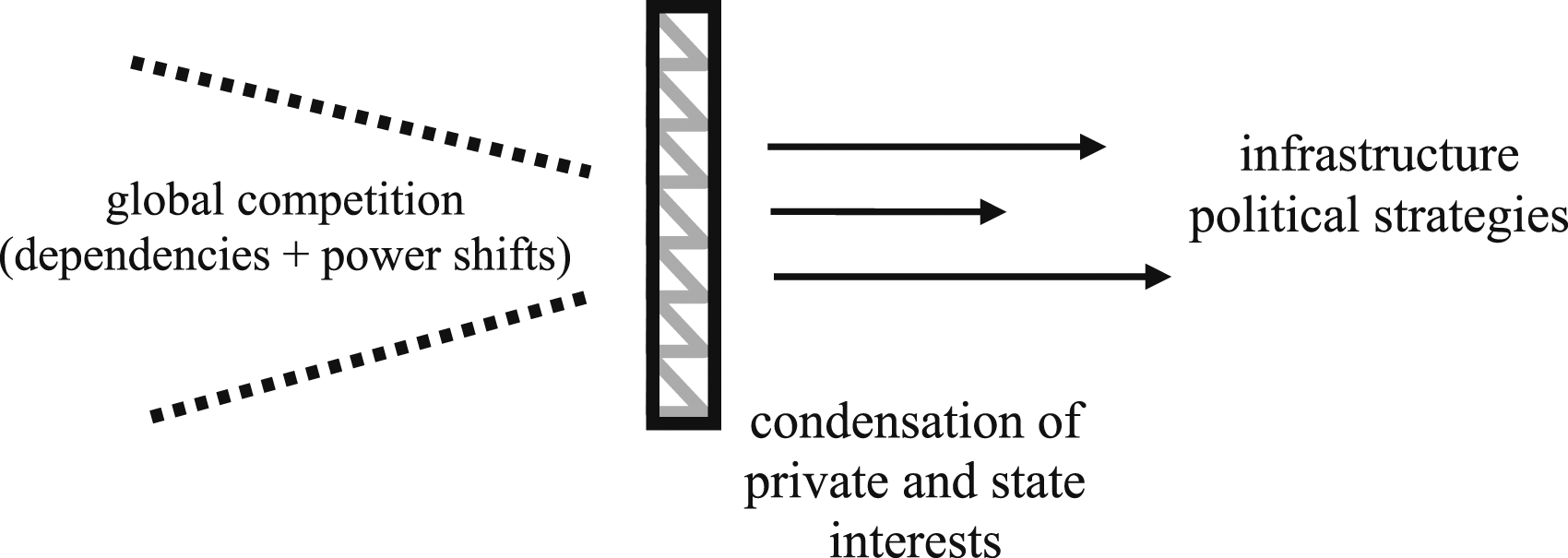

Overall, infrastructures serve as means as well as an end of public and private action. They can be used as strategic instruments because they are also a prerequisite for successful economic action. Thus, there is considerable global pressure – both politically and economically – on political spaces like the EU to assert themselves in global competition by ensuring the control over and the access to globalisation-relevant infrastructures. The degree of competition varies with the infrastructural dependencies in which the actor stands to others, as well as changes in global power relations that make exploitation of these dependencies more or less likely. How competition is then translated into specific infrastructural strategies at certain points is subject to a complex condensation of interests in said political space. Positions of public and private actors are articulated according to their respective interests in and capabilities for infrastructural development and control. The condensation of these interests is in turn determined by the resources and institutional access available to said actors. Compatibilities and incompatibilities of their interests can lead to opportunistic alliances. As a result, the scope of infrastructure policy is narrowed down to a certain selection of measures. Figure 1 captures this mechanism graphically. Mechanism of infrastructure policy formation (own illustration).

The following two sections examine the EU’s position in the triad empirically, outlining the recent global power shifts in infrastructural terms and discussing the difficult position in which the EU finds itself. They also outline how this has resulted in a reorientation of the EU’s infrastructural narratives and agenda.

Conflicting connectivity in the triad competition

Some authors discuss the recent competition over global order in terms of a conflict of connectivity. Mark Leonard (2021: 15) argues that ‘the shape of our global order will be defined by the battle between [the] three empires of connectivity’. Connectivity, in our understanding, consists of four interrelated aspects: the material features of globalisation-relevant infrastructure; its financing, including the actors involved and the criteria applied; its hedging through various trade and investment policy agreements and measures; and finally, its utilisation and provision. In combination, these factors structure the geoeconomic conflict over connectivity between the three centres of the triad.

The triad competition has its roots in the rapid growth of the Chinese economy and the crisis of the transatlantic partnership that coincided with it. The country overtook its regional competitor Japan to become the world’s second largest economy. With newfound confidence, it also championed alternative conceptions of world order on the international stage. These shifts were fuelled by internal problems of capitalist accumulation in the OECD world, most notably reflected in the global financial crisis that began in 2007. It was evident that the motor of liberal globalisation was stuttering, while statist development models gained ground. Governments and regional development banks such as the New Development Bank (NDB), the Japan-led Asian Development Bank (ADB), and the Asian Infrastructure Investment Bank (AIIB) dominated by China, assumed functions that were previously carried out by the IMF and the World Bank. China in particular provided bilateral financing and investments to strategic partners at terms that those considered preferable over the conditionality of the global financial institutions.

China has outlined its approach to globalisation in the ‘Made in China 2025’ strategy. The country seeks to transform its economy from a labour-intensive production centre for low-tech goods to a frontrunner in technological development and the production of complex manufacturing goods. At the same time, China seeks to achieve autonomy by increasing the share of domestically produced goods in the overall production chain. The strategy highlights the central role of international champions such as Alibaba, Baidu, Huawei and Sinopharm that are often either state-owned or indirectly controlled by Chinese Communist Party staff. Also, it points towards the multidimensionality of China’s conception of connectivity, that is, the intertwining of infrastructures of communication, energy, transportation and technology.

The BRI is the mainstay of Chinese connectivity. As a global infrastructure programme, it seeks to connect China to other economic centres in Asia and Europe via overland and sea routes. It combines physical infrastructure such as roads, railroads and ports with non-physical infrastructure through communication, trade agreements, and commercial standards. Economies along the trade routes receive large-scale investments to consolidate the role they play in the overall plan and to safeguard their political stability. For Beijing, the economic prospects are manifold as the BRI could expand the markets for Chinese products and bind countries that are rich in raw materials to its economy. The BRI will make China the world’s trade hub and ‘cement China’s place at the centre of a network of regional production networks’ (Beeson and Watson, 2019: 405). Along the maritime ‘road’, China seeks to loosen the grip of the US, investing heavily in countries that control trade chokepoints (Goodman and Perlez, 2018).

The US has reacted to the Chinese advances by trying to consolidate its leadership role. Due to the centrality of its financial sector in the global accumulation process and its function as a hub for digital infrastructure, the US is in a strong position to do so. Yet, its information technology leadership is threatened by China’s move towards a high-tech production centre and its strategies of appropriating knowledge and technology. Against this backdrop, US president Barack Obama pursued a containment strategy to limit Chinese expansionism. His ‘Pivot to East Asia’ strategy envisaged an increased diplomatic and economic role for the US in the region. It built on work relationships and increased trade and investment activities with ASEAN countries, accompanied by a strong military presence. Economically, the strategy was to be supported by the Trans-Pacific Partnership (TPP), a trade and investment agreement with major players in the region that would exclude China. The agreement was meant to set standards in the Chinese neighbourhood in terms of dispute settlement, the protection of intellectual property rights, and data and financial flows.

However, Obama’s foreign policy towards East Asia was of limited success. A change of strategy was implemented under Donald Trump. The US administration moved from containment to confrontation, increasing the pressure on China in terms of trade and investments. Starting 2018, it engaged in a costly trade war, imposing high tariffs on Chinese goods. Trade sanctions aimed at industrial sectors that formed integral parts of the ‘Made in China 2025’ strategy, seeking to limit China’s ability to expand in those areas. In 2019, Trump signed an executive order that allowed the US to restrict, prohibit and even reverse transactions in the area of information and communication technology that could pose ‘an undue risk of catastrophic effects on the security or resiliency of United States critical infrastructure or the digital economy of the United States’ (Executive Order 13873). The US furthermore imposed sanctions on Huawei and other Chinese high-tech companies and limited their access to US markets.

Given the stability and continued dynamism of the Chinese development model, the Biden administration is now cautiously re-adjusting its approach. The hard stance on China remains. At the same time, the prospect of a complete decoupling is no longer on the agenda and the unilateral approach is being abandoned in favour of cooperation with allied governments in Europe and Asia. Inter alia, this found its expression in the G7’s decision of June 2021 to implement the Build Back Better World (B3W) initiative, which the US had proposed as a counter-project to Chinese connectivity.

A European infrastructure policy in the making?

European integration has always been a product of both, internal dynamics and global power relations (Lavery and Schmid, 2021). The recent global shifts put pressure on the member states to sort out their affairs and find a way to preserve their economic sovereignty. This is a new constellation insofar as in previous phases the geopolitical and geoeconomic capacities and fiscal resources for an active connectivity strategy were rather limited. A first phase, beginning in the 1980s, was focussed on the development of the Single Market via liberalisation and privatisation (Clifton et al., 2003), flanked by regional policy instruments. Pressured by transnational capital, first and foremost the European Round Table of Industrialists that had published two seminal reports on ‘Missing Links’ and ‘Missing Networks’ (ERT, 1984, 1991), the development of the Trans-European Transport Network (TEN-T) moved up on the agenda. The objective was to build cross-border transport routes, networks of energy supply and telecommunication to increase the competitiveness of European businesses. Although the strategy reached out geographically, it remained limited to its direct vicinity: the Western Balkans and the European Neighbourhood Policy areas.

In a second phase, which began in the 2000s and was strongly influenced by the discourse on international terrorism, cybercrime and related threats, the afore-mentioned internal focus persisted. At the same time, national and European policies became increasingly ‘securitised’ (Bossong, 2014). This concerned mostly so-called ‘critical infrastructures’ in the fields of energy, transport and communication (European Council, 2008).

The recent phase is marked by a geopolitical and geoeconomic rethinking of both, the inward focus of EU infrastructure policy and its market-liberal globalisation strategy. In view of the BRI and the ‘Made in China 2025’ strategy, European behaviour is becoming more ambivalent towards Beijing. China is the EU’s second largest export market after the US – and vice versa. Yet, the economic interaction between the two economies has been unequal as China was unwilling to open its market to European companies to the same degree the EU had opened its own. China gained competitive advantages by using state financing to cut out European competitors or, in some cases, buy them up and absorb their technologies and know-how.

For Europe, the acquisition of the German robotics company KUKA by the Chinese Midea Group in 2017 was a turning point. After that, the EU began to take precautions to keep critical technology and advanced production chains within its member states. It implemented a stricter framework to control FDIs to protect assets critical to its ‘essential security interests’ and ‘public order’ (Regulation 2019/452). Yet, the EU’s political fragmentation prevents a more comprehensive response. Neither does the regulation enable the EU to protect critical technology and assets, nor does it compel states to carry out thorough screening at the national level. Until recently, only half of the member states have implemented their own national mechanisms on FDIs (Meunier and Nicolaidis, 2019). Chinese investments in the EU itself and in countries bordering it have also mitigated the EU’s ability to set standards and gain influence on globalisation-relevant infrastructures in its neighbourhood. In reaction, the EU now portrays China as a ‘cooperation partner with whom the EU has closely aligned objectives’, but at the same time as an ‘economic competitor in pursuit of technological leadership, and a systemic rival’ (JOIN(2019) 5 final).

Relations between the EU and the US have also been strained (Bieling, 2018). Under Donald Trump, the EU itself has been the target of several aggressive trade measures and the rise of nationalist populism has drawn into question the transatlantic alliance. Although interests are realigning under the Biden administration, the EU has begun a process of emancipation in terms of infrastructural control and standard-setting. The ‘Connecting Europe and Asia’ strategy of 2018 widened the EU’s connectivity approach ‘from the neighbourhood to the Pacific’, channelling investments and seeking to connect the TEN-T to Asian networks (JOIN(2018) 31 final). Under president Ursula von der Leyen, the Commission adheres to the geoeconomic agenda and develops it further. This continuity is evident in the ‘New Industrial Strategy’ (COM(2020) 102 final), in which it calls for a European ‘strategic autonomy’ that reduces its ‘dependence on others for things we need the most: critical materials and technologies, food, infrastructure, security and other strategic areas’. It justifies this agenda with reference to the ‘new and ever-changing geopolitical realities’, indirectly referencing China (‘new powers and competitors are emerging’) and the US (‘established partners are choosing new paths’). In general, the communiqué puts a lot of emphasis on aspects of digital sovereignty. This has found its expression also in another document of that year, the EU’s strategy ‘Shaping Europe’s Digital Future’ (COM(2020) 67 final). There, the Commission clearly outlines the competitive character of its agenda, underlining the necessity for the EU to ‘develop and deploy its own key capacities, thereby reducing our dependency on other parts of the globe’ and retain its ‘ability to define its own rules and values in the digital age’.

The EU has also undertaken specific steps to allow for an implementation of its infrastructural agenda. Under the label Important Project of Common European Interest (IPCEI) the EU has softened its competition rules and allowed industrial policy intervention for key industries such as hydrogen plants, semiconductor development, and cloud infrastructure. In late 2021 the European Commission also announced that it would make its infrastructure policy more outward-looking. The ‘Global Gateway’ initiative reflects an EU approach to connectivity that seeks to further geoeconomic interests in Africa and Asia. It promises to mobilise up to €300 billion in investments dedicated to these regions and conditional on the adherence to European standards (JOIN(2021) 30 final). This shows the EU’s ambition to expand its global relevance through means of infrastructure policy and foreign investments.

Crisis measures following the onset of the pandemic have underlined the EU's ability to mobilise the financial resources required for such a strategic transformation. The Commission has triggered the Stability and Growth Pact’s (SGP) ‘general escape clause’, temporarily deactivating the EU’s fiscal framework. Against the initial resistance of some northern countries, the EU has also set up a recovery fund totalling €750 billion and financed by joint European bonds, from which member states can draw for national investment programmes. With a focus on green and digital investment, infrastructures in the fields of energy and communication receive specific attention in those programmes. The NGEU is a temporary setup, operating until 2023. It is closely linked to the Multiannual Financial Framework (MFF), the EU’s budget of more than €1 trillion for the period from 2021 to 2027. Taken together, they constitute a substantial investment package that heralds a state-interventionist turn. Yet, the instruments for now remain temporary. Also, it is far from certain if an extension of such measures to a grander infrastructural agenda is viable.

Contrasting European strategies on GNSS and telecommunication

The previous sections have outlined a broader strategic shift of the EU’s agenda towards a more geoeconomic orientation of its infrastructure policy. However, as we discussed earlier, global competition is translated into concrete measures only through a condensation of interests. The following two case studies reveal that this condensation is predetermined by two central factors: the mode of external competition and the EU’s internal political conditions. We select cases from the fields of satellite navigation and telecommunication: the EU’s decision to develop its own Global Navigation Satellite System (GNSS) Galileo and its agenda on 5G. They are mainly chosen for reasons of comparability. Both are high-tech infrastructures, both of high strategic relevance. In both cases, the US and China constitute the main competitors. Yet, the time periods of their respective conception differ – being almost two decades apart – which produces some interesting results. Although we would generally expect the 5G case to result in a more strategic and coordinated response of the EU due to the intensified triad competition and its geoeconomic orientation in recent years, the opposite is the case. Remarkably, while global pressure exists in both cases, they differ in terms of the mode of external competition and some specific internal conditions. The case of GNSS illustrates the overcoming of internal fragmentation though policy coordination, while the 5G case reveals the EU’s persistent difficulties to develop a comprehensive approach under conditions of intense external pressure and internal divisions.

There are four general strategies with which actors can react to uncertainty about their future access to globalisation-relevant infrastructures: build parallel infrastructures to compete with pre-existing ones via own standards; build parallel infrastructures but make them compatible with pre-existing ones; secure access to pre-existing infrastructures in exchange for opening up own systems, that is, create interdependencies; or gain access to pre-existing or upgraded infrastructures via contracting. In the case of satellite navigation, the EU’s strategy reflects largely the second of the afore-mentioned options, building compatible infrastructures. Yet, the European course of action was not the product of consistent planning but of several decision-making instances that eventually prevented failure and paved the way for Europe’s own GNSS. In the case of 5G, the constellation and strategy of the EU is somewhat different. So far, its implementation rather reflects the fourth option of gaining access to infrastructures via piecemeal contracting, lacking a coherent position.

Galileo

GNSSs provide geo-spatial positioning with high accuracy – the exact level of which depends on the respective system – for purposes of localisation, navigation and tracking of an entity equipped with a receiver. Control over their components and data allow for a strategic disabling or distortion of services for select locations and periods of time. Satellite navigation thus lends itself to both aspects of weaponisation: surveillance and restricting access. Matters of control and availability are all the more important as GNSSs play a key role in globalisation processes. This concerns, inter alia, the navigation of automobiles, aircraft and shipping, logistics such as traffic monitoring and tolling, agricultural planning, services such as mapping and delivery tracking, but also commercial activities such as customer profiling. Satellite navigation is also part of modern warfare as it allows for real-time surveillance, weapons targeting, drone navigation and so forth.

Galileo is a priority project of the EU’s TEN-T programme that is financed and carried out in cooperation with the European Space Agency (ESA), with which the EU has a large overlap in membership. Introduced in 1999, the project sought to establish a European satellite network that provided an independent global positioning system under civilian control. In 2011, the first active satellite was put in orbit. Galileo became fully operational in 2019. In 2021, 26 satellites have been launched, of which 22 are operational. The deployment of a second generation of satellites is in planning, with an order of 12 additional satellites for €1.47 billion already placed. This contract was obtained by Airbus and Thales Alenia Space, which reflects the industrial policy character of the project. National governments stay involved not only in the overall planning of the project but also its implementation. At Airbus, France, Germany and Spain together have a blocking minority of 26 percent of shares. The company has also received considerable public funding in the past. Thales Alenia Space is owned by Leonardo S.p.A. and the Thales Group, in which the Italian and the French government respectively are the largest shareholders.

The reasons for member states to get involved in a costly and risky endeavour such as establishing a European GNSS were manifold. First, they sought to rival the US for technological development and market shares in satellite navigation as they expected the market to expand in the following years (COM(1998) 29 final). Second, Europe’s GNSS would increase its independence from military systems such as GPS or the Russian GLONASS, both of which could deny access to European countries in case of conflict. Finally, ‘nurturing homegrown technical expertise in space technology’ and ‘open[ing] the possibility that Europe could set a new global standard for navigation’ (Beidleman, 2005: 119–120) would allow the member states to pursue their own approach to connectivity in satellite navigation.

Europe’s decision to set up Galileo was not a direct response to triad competition as around the turn of the century, the current global constellation was just emerging. China’s economic output was a fraction of what it is today; its character was still that of a labour-intensive production centre rather than a technological competitor. The global leadership of the US was a lot more consolidated. Nevertheless, in the field of GNSS the two powers and their national corporations were the relevant challengers. Thus, the EU based its strategies on this state of triadic competition that was beginning to emerge. On the one hand, the EU’s initiative reflected the transatlantic crisis following the War in Iraq, which had cast doubts of the strategic alignment of core EU countries like Germany and France with US foreign policy objectives. This division also triggered debates about Europe’s future access to key infrastructures. On the other hand, China’s early involvement and later abandonment of the Galileo project highlighted the strategic competition between Europe and Beijing. In 2004, China had committed itself to participate in the Galileo project with an investment of around €200 million, making it the most substantial non-European partner in the project. The US was particularly wary of this development as it feared that China would get a say in Galileo’s security structures (Beidleman, 2005: 140).

Although European companies hoped for a facilitation of market access in China, Beijing sought to benefit in terms of technology transfers as it had begun the development of its own GNSS. The Chinese government wanted to accelerate the construction process by participating in Galileo and acquiring technological expertise. When it transpired that the European states did not plan on sharing technical information with China, it left the project. In 2020, the satellite system Beidou was completed, ensuring Chinese independence from global competitors and promoting Chinese standards domestically and abroad (Halappanavar, 2020). Most domestic smartphones rely on the system and countries that cooperate with China on the BRI are incentivised to accept Chinese connectivity.

Initially, the main rivalry was between the EU and the US. The US objected to Galileo, fearing it would threaten US leadership in the area of satellite technology and make third parties less dependent on GPS. This would also decrease the pull of its connectivity approach. Military strategic reasons played a substantial role. In a combat situation, US forces use to jam the public GPS signal while tuning into an encrypted signal. Galileo intended to use a frequency in the range of the military signal of GPS for reasons of signal robustness, which would prevent the US from blocking Galileo signals. With a highly precise Galileo system and the US unable to jam it, Washington feared that enemy groups could use Galileo to conduct attacks. Consequently, it took a confrontational stance on the matter. Several EU member states still found it no longer acceptable that their access to GNSS would remain contingent on the foreign policy decision-making in Washington. In addition, the development and operation of military equipment like missiles that was dependent on GPS technology effectively had to be signed off on by the US military. The EU’s arms industry was hence also pushing for a European counter-project (Dworschak, 2007).

When the US realised that Galileo would go ahead, it started to engage in negotiations. In June 2004, the EU and the US came to an agreement. In exchange for its general approval of the system, the Bush administration achieved a shift of Galileo’s public signal to a frequency standard that would not interfere with the military signal of GPS. Instead, both systems would provide their public signal at a shared frequency. This would allow for future jamming in case of conflict, leaving each other’s military communication intact. Finally, both parties agreed on the interoperability of their systems by harmonising standards and licensing requirements. Therefore, while Galileo was a milestone as it gave proof of the EU recognising the importance of infrastructural independence, the EU generally went for a compatibility-oriented approach in the area of GNSS.

Already in 1999, the European Commission had proposed to promote Galileo as a private-public partnership (PPP). It was of the view that this ‘would confirm private sector commitment to the project’, while the private sector’s pressure ‘to generate income and reach profitability’ would ensure that ‘user’s needs are given central importance’ (COM(1999) 54 final: vi). This approach illustrates that the European countries were still viewing infrastructure in terms of business profitability more than geopolitics. The inspiration for conceiving Galileo as a PPP came from a study by PricewaterhouseCoopers, proposing a concession model as it projected high gains from the project (Feyerer, 2015).

The European aerospace industry was highly supportive of the project. Given a crisis in the satellite business, Galileo was an opportunity for the market leaders to expand their production and increase profitability. Rainer Hertrich, President of the German Aerospace Industries Association (BDLI) and CEO of European Aeronautic Defence and Space (EADS), the parent company of Airbus, described Galileo as ‘one of the most important infrastructure projects in Europe’ (Welt, 2002). Yet, there was competition among national industries over which parts of Galileo’s development and operation were to be carried out in their respective countries. Eventually, encouraged by the member states the major European stakeholders, including the EADS, Thales and Leonardo, agreed to set up the joint venture ‘Galileo Industries’. This consortium would act as the prime contractor for Galileo in the PPP and exclude competing bids.

The decision to pursue a PPP turned out to be disastrous. The Court of Auditors (2009) noted failures of project management as well as a lack of incentives for private actors to participate in the actual development. The fact that the open Galileo signal would be available for free was casting doubts about the profitability of the project, which is why the companies and the Commission got carried away with debates over liabilities (Dworschak, 2007). The Court of Auditors also criticised that the setting up of Galileo Industries had created a monopolistic situation that had further decreased incentives for private contributions. It took the EU until 2007 to realise that the plan had failed and that it had to nationalise the project. At that time, Galileo was delayed by five years and costs had almost doubled. The Commission itself had warned back in 1999 that such a delay would ‘mean that US dominance will be further consolidated, so Europe will find it considerably more difficult, and probably impossible, to enter the market, and will essentially have to accept the standards set by the US’ (COM(1999) 54 final: 5). Indeed, the years of venturing into the world of concession models had cost Europe a fair amount of market share and technological path-dependency had further established GPS as the global standard.

In the following, the member states could not agree on a new funding structure and Galileo seemed to have reached the end of the road. It was salvaged by a Council decision in 2008 that secured public funding of Galileo by diverting parts of the EU’s agriculture and research budgets. Today, Galileo is a mainstay of EU space policy with more than half of its budget in that area going to the project. The system achieves almost the geospatial coverage of GPS while trumping it in terms of precision. Yet, GPS standards are deeply embedded in consumer markets and national operations and Beidou constitutes a strong rival that promotes its own connectivity approach. The history of Galileo points out the inconsistencies and ad hoc character of the EU’s approach and reveals the fragmentation of member states’ national industries and interests which have greatly delayed the development of Galileo and almost contributed to its failure. However, in the end it also represents a successful attempt to secure European autonomy in GNSS infrastructure as the divides between member states have been bridged rather than deepened by global competition.

5G

High expectations are associated with the new communication standard 5G. Data transmission is to be a hundred times faster than with the Long Term Evolution (LTE) standard. Nationwide 5G data connections are essential for coping with globally increasing data traffic. They make it possible, for example, to organise existing supply chains more effectively through driverless transport systems and mobile robots, whose steering and control requires fast and complex navigation decisions. The digitalisation of everyday life should also advance through cloud systems, smart homes, health services, and entertainment.

The EU recognised the technological and economic potential of 5G rather early and since 2013 has taken various initiatives to promote and implement the new network infrastructure. The initial focus was on stimulating PPPs to modernise mobile technology in the context of ongoing funding programmes such as Horizon 2020. European businesses were generally supportive and several high-tech companies actively took part in these initiatives. In recent years, the process has been further intensified at the national level through the public tendering and awarding of 5G licences and the associated requirements for the private operators. It is often pointed out that the EU is proceeding with digitalisation from a position of relative backwardness in information technology (Burwell and Propp, 2020: 5–6). In terms of software, US corporations like Google, Facebook, Microsoft and Amazon are most advanced, although they are increasingly challenged by Chinese counterparts such as Baidu, WeChat, Tencent or Alibaba. In the field of the physical infrastructure or hardware, the situation is almost the reverse. Here, Chinese companies, particularly Huawei and ZTE, are already considered technological leaders. They are shaping the process of implementing 5G networks, albeit in competition with American (Qualcomm and Intel), European (Nokia and Ericsson) and South Korean (Samsung and LG) corporations.

In this competitive context, the US has chosen a confrontational strategy towards China. This includes not only the Trump administration’s ‘trade war’ but also the harsh FDI screening and banning of Chinese IT companies from the US market. What is more, the US government prohibits other supplier companies from providing essential semiconductors and software elements to ZTE and Huawei. The US motive is threefold (Rodrik, 2020): Commercially, it seeks to defend its information technology leadership against China. In terms of security, the access of China and other authoritarian states to information technology and industrial networks is to be warded off – and with it the possibility of cyber espionage. In terms of data protection policy, the concern is that citizens could be spied on and, if expedient, put under pressure and made compliant.

In principle, these concerns also apply to the EU and its member states. However, until some time ago, the EU dealt with its reservations in a much more restrained manner, for example, through its General Data Protection Regulation (GDPR), which also rejects some US practices. In recent years, however, the EU’s stance – in line with the 2019 China Strategy update – has hardened, particularly as the US has exerted some pressure to push Chinese vendors out of the European market as well (Tekir, 2020). The US has increased diplomatic and security pressure on national governments by threatening to withdraw US troops or cut off access to shared information systems like the Five Eye network. Most Eastern European countries have willingly given in to this demand and joined the anti-Huawei alliance (Noyan, 2021). The former EU member Great Britain and more recently Sweden and Denmark have begun to follow this line. By contrast, countries like Hungary and Greece see little reason to break off cooperation with China as they are partners of the BRI and cooperate also on digital aspects. And still other states – France, Germany, the Netherlands, Belgium, Austria, Portugal and Spain – have already concluded contracts with Huawei or do not want to exclude this in principle but make cooperation dependent on a review procedure.

This inconsistent, nationally fragmented stance of the EU is not unusual, but it points towards the difficulties in developing a coherent strategic position on 5G infrastructure. The difficulties are due to several factors: first, as indicated, the national states have rather different geopolitical and geoeconomic incentives, for example, in terms of transatlantic cooperation (UK), the stimulation of Chinese investments (Italy), technological support of national corporations (Sweden) or the adherence to a market-liberal approach (Germany). Second, the EU does not possess powers and means to bring about an efficient harmonisation of national procurement practices. In general, the rules of the Single Market apply, including those of competition law, despite the 5G mobile infrastructure being also a geoeconomics, industry, security and data protection issue. The Commission is therefore stepping up its efforts to coordinate national positions and practices. To this end, it has suggested excluding high-risk vendors from critical or sensitive elements of 5G technology (C(2019) 2335 final). Finally, external influences also ensure that intergovernmental fragmentation is reproduced. In accordance with a strategy of ‘divide and rule’, the US has put considerable pressure on individual EU member states – sometimes using weaponisation practices – to position themselves against Huawei and China. In return, Huawei has rejected accusations of promoting industrial espionage and passing on sensitive data to the Chinese state and has held out the prospect of releasing 5G codes, patents, licences and technological knowledge. At the same time, however, state actors have threatened retaliatory measures, for example, against the European automobile industry (Tekir, 2020: 129). This fuels fears that a strong involvement of Chinese companies bears the potential for a weaponisation of infrastructures (Gertz and Evers, 2020).

It is rather unlikely that the EU will be able to organise a self-determined modernisation of its mobile communication infrastructure by way of public procurement and contract arrangements. The technological dependence on Chinese companies as vendors of 5G equipment is already considerable – and so is the pressure from the US to oppose this. This strategic dilemma has led to significant delays in deployment. European business associations are highly concerned about these delays as they are detrimental to the competitiveness of European enterprises that ‘depend on connectivity for their business survival’ (ERT, 2020a: 3; see also BusinessEurope, 2019a). At the same time, however, they are also worried about the dangers of cyber-crime and cyber-espionage. Consequently, the associations urge the EU to accelerate the roll-out of 5G by providing further public and private funds, while more closely coordinating the activities of member states within a common regulatory framework based on a ‘fact and risk-based’ approach to cybersecurity and ‘a level playing field in the telecom equipment market’ (ERT, 2020b: 5; see also BusinessEurope, 2019b).

The EU, above all the European Commission, has shown itself to be receptive to such suggestions from the business side. It seeks to speed up digitalisation and the implementation of 5G and has taken several initiatives to this end. Firstly, based on the promotion of the ‘Digital Single Market’, the EU increasingly refers to the slogan of ‘digital sovereignty’ (Burwell and Propp, 2020). This is regarded as a prompt to strengthen the European vendors – Nokia and Ericsson – through industrial policy measures. Accordingly, 20 percent of resources from the newly established Recovery Fund, totalling €750 billion, are dedicated to digitalisation. Secondly, in the sense of a ‘geopolitics light’, the strategy seeks to involve Huawei in 5G for technological and financial reasons but to keep it out of critical or sensitive fields of activity – a process that is not easy to control. Finally, a diversification of 5G networks is promoted as it builds certain excess capacities that maintain a minimum supply in case the network is interrupted.

As the relationship between the US and the EU seems to recover under the Biden administration, it is likely that the EU will to some degree realign with the strategic position of the US. Irrespective of this, it seems certain that in the coming years the European 5G – and prospectively 6G – infrastructure will remain a battleground of conflicting external weaponisation processes. In the absence of sufficient legal competences and financial resources, the capabilities of the EU are largely limited to supporting national governments in the digital modernisation process and coordinating contractual conditionalities. However, the EU has recently launched some initiatives to mitigate at least partially the external depencies – economic, information technological, and security political. Overall, the diverging national economic preconditions and development models in the EU pose obstacles to the development of a common approach in the field of telecommunication and 5G. As the Commission is unable to organise a European approach to connectivity, up to now the EU’s access to 5G networks is secured through piecemeal measures of contracting.

Conclusions

Against the background of an increased articulation of geopolitical and geoeconomic objectives, the EU is undergoing a shift towards a more strategic infrastructure and investment agenda. So far, its individual efforts in specific infrastructural fields are falling behind more far-reaching ambitions. In comparison, our two case studies illustrate that the mode of global competition, that is the divisive strategies of the US and China, differs across infrastructural projects and might keep the EU from realising its potential in the field of infrastructure policy. There are internal political factors that reinforce this effect. EU-specific factors of political organisation play a role. The diffusion of authority on EU level and the lack of joint financial resources render the planning and implementation of large-scale strategies difficult. In addition, the member states – despite monetary and economic integration – still find themselves in a position of mutual competition over investments, jobs, and industrial sites. Therefore, they face incentives to engage in haggling that is inefficient on a larger scale and to block initiatives that do work in favour of a common EU strategy but not their individual economic gain.

Furthermore, a particular economic mindset produces disadvantages in the triad competition. There is a long-standing scepticism regarding measures of industrial policy and public investment that accompanies the EMU’s generally restrictive fiscal setup (Abels and Bieling, 2022). The EU’s globalisation strategy has for a long time relied on the competitive advantages of its export-oriented core and a market-liberal and rule-based approach to international trade. As the first sections of this paper outlined, it only recently started developing a more state interventionist component that particularly concerns the field of infrastructures, but it does so from a relatively backward position.

Overall, our findings reveal that, while there is an undeniable and comprehensive reorientation of EU infrastructural policy towards a geoeconomic logic, there are additional conditions underlying its practical implication. Global competition and the external pressure to avoid infrastructural dependencies and vulnerabilities have a mobilising effect on infrastructural policy. However, these pressures are insufficient to induce policy changes in cases where the divisive mode of US and Chinese influence is particularly pronounced and where internal conditions are set up detrimentally. In the case of 5G, despite a context of increased geoeconomic competition, the internal fragmentation of the EU in terms of interests and views led to a less autonomous response than in the case of Galileo, more than a decade earlier.

If the EU wants to avoid falling behind in the triad competition and being reduced to a battleground of US-Chinese geoeconomic conflicts, it needs to tackle its institutional, political and financial shortcomings. This would include the further pooling of financial resources, as exemplified by the recovery fund and the MFF, and making such instruments permanent. These resources can be used for jointly coordinated investments in strategic infrastructure fields. Institutionally, a reorientation of European investment policy also requires a reform of the EU’s fiscal rules, for example, by implementing exemptions for such expenditure. Politically, further competences of (geo)strategic planning would have to be transferred to the EU. If this is viable – or in the first place, desirable – is a question that the member states and their societies need to answer soon.

Footnotes

Acknowledgments

We wish to thank the two reviewers and the editors for their valuable feedback on earlier versions of this manuscript. All remaining errors remain our own.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.