Abstract

The European Green Transition requires massive financing efforts, with estimates of EUR 620bn EUR annually, and the headwinds are substantial. Central banks seem overstretched and busy tightening to combat inflation; treasuries are subject to austerity-inducing fiscal rules; and banking systems are afflicted by non-performing loans, fragmentation, and risk aversion. We employ the Monetary Architecture framework to analyze the EU’s monetary and financial system as a constantly evolving hierarchical web of interlocking balance sheets and study its capacity to find “elasticity space” to meet the financing challenge. To this end, we draw on a four-step scheme for Green macro-financial governance along the financial cycle of balance sheet expansion, funding, and final contraction. We find that, first, Europe’s monetary architecture still has ample elasticity space to provide a green initial expansion due to its developed ecosystem of national, subnational, and supranational off-balance-sheet fiscal agencies. Second, as mechanisms to consciously organize the distribution of long-term debt instruments across different segments are absent, its capacity to provide long-term funding is limited. Third, institutional transformation in the last two decades has greatly improved the capacity of the European monetary architecture to counteract financial instability by providing emergency elasticity. Fourth, the capacity of the European monetary architecture to manage a final contraction of balance sheets is limited, which is a general quandary in modern credit money systems. Our analysis points to the need for further investigations into techniques for monetary architectures to manage long-term funding and balance sheet contractions.

Keywords

Introduction

The European Union (EU) has enshrined its commitment to reach net-zero carbon emissions by 2050 in the European Climate Law. This requires massive investments to decarbonize sectors such as industry, transport, energy, housing, and food. With the European Green Deal describing the roadmap for financing the EU’s Green Transition, the European Commission (2023) expects additional investment needs of EUR 620bn annually. That amounts to about 4% of the annual EU GDP, a sum that is not outside of reach but neither is it trivial as multiple crises dampen the EU’s growth prospects—including stubborn inflation, energy price spikes, and wars. Moreover, central banks seem overstretched and occupied with tightening monetary policy rather than improving financing conditions; the European fiscal rules seem contrary to enabling the financing of decarbonization projects; and European banks are afflicted by non-performing loans, cross-border fragmentation, and risk aversion (Valiante, 2015). This begs the question if and how the EU’s monetary and financial system has the capacity at all to provide Green Transition financing at the stated financial volumes.

Traditionally, state-led investments are conceptualized along a monetary-and-fiscal-policy dichotomy, which emerged with Keynesianism after World War II (Hansen, 1949; Keynes, 1936) and the ISLM model (Hicks, 1937). It defined two options for states to stimulate the economy: Expansionary monetary policy would expand central banks’ balance sheets by lowering interest rates or conducting open market purchases. Expansionary fiscal policy would increase government spending, typically financed by sovereign debt issuance. The so-called neoliberal turn, emerging roughly in the 1970s, restricted on normative grounds what the state could do regarding monetary-and-fiscal-policy (Stockhammer, 2016), but perpetuated the monetary-and-fiscal-policy dichotomy. This dichotomy, however, is restrictive as it neglects that the state commands many more balance sheets than only central banks and treasuries, notably various off-balance-sheet fiscal agencies (OBFAs) (Guter-Sandu and Murau, 2022). OBFA is an umbrella term for entities like development banks, investment funds, public companies, or special financing vehicles that act on behalf of the state and are endowed with public backstops but have a different governance structure that makes them subject to different legal, political, and administrative stipulations (Laudage et al., 2024). While OBFAs can also expand and contract their balance sheets and as such interact with and influence the wider monetary and financial system, their activities do not sit well within the traditional monetary-fiscal dichotomy.

In line with the rise of “ecosystem thinking” on Green Finance in International Political Economy (IPE) (Sharma and Babić, 2024), we argue that analyses of Green Transition finance in Europe should move past the monetary-and-fiscal policy dichotomy and look at the EU’s wider “monetary architecture”—an analytical approach that apprehends the EU’s monetary and financial system as a web of public, private, and hybrid balance sheets which interlock via different credit instruments and comprise various types of OBFAs (Murau, 2020). This approach—emerging from the recent scholarship of the Money View (Mehrling, 2017) and critical macro-finance (Dutta et al., 2020; Gabor, 2020)—offers a novel historical-institutionalist way of analyzing the political economy of the European monetary and financial system. Other models of Europe’s monetary and financial system describe it with less institutional detail and historical specificity—for instance, New Keynesian Dynamic Stochastic General Equilibrium (DSGE) models (Smets and Wouters, 2002), Post-Keynesian Stock Flow Consistent (SFC) models (Godley and Lavoie, 2007), or flow of funds (FoF) models (Duc and Le Breton, 2009). These provide simplified representations of real-world institutional configurations and feed them with statistical data to analyze and predict variables such as prices, quantities, or interest rates. The Monetary Architecture approach, by contrast, inductively synthesizes and maps political-economic configurations. It shifts the focus away from changing numerical values of data within static institutional structures and addresses institutional changes upfront which can emerge through policymaking, private decisions, or technocratic bricolage.

With this approach, we seek to address the question of what capacity the European monetary architecture has to deliver on the challenge of Green Transition financing. To do so, we take a deep dive into the empirics of the European monetary architecture, explaining its institutional set-up and outlining its constituent parts, in order to then assess its capacity for shouldering the financial expansion that is expected for transitioning to a carbon-neutral state. Our approach is primarily inductive, extracting insights from the specificities of the European monetary architecture, but is also inspired by the trailblazing theoretical analyses of Post-Keynesian economists like Minsky (1986) and circuitistes like Rochon (1999) and Graziani (2003). We tackle this issue through the prism of a procedural macro-financial governance scheme (Murau et al., 2024) which comprises four steps. We assume that financing the Green Transition requires first a large-scale expansion of various public, private, or hybrid balance sheets to create money and provide financing for decarbonization projects. This “green initial expansion” must be followed, second, by a long-term funding process during which the newly created credit instruments must be distributed across the monetary architecture and find balance sheets that are willing and able to hold them (Mehrling 2020). Third, financing the Green Transition can only succeed if there are suitable firefighting balance sheets in place that can backstop the process in case financial instability arises. And fourth, the financing of the Green Transition is completed once an orderly contraction of balance sheets takes place. This four-step process ensures that the expansion of the monetary architecture is undertaken in a sustainable way and that its debt-carrying capacity is increased and safeguarded across the entire financing cycle of the Green Transition.

Hence, what is the capacity of Europe’s monetary architecture in each of the four steps of the financing process? We find that the European monetary architecture—despite various headwinds—has ample elasticity space to provide an initial green expansion due to its advanced ecosystem of OBFAs on a national, subnational, and increasingly supranational level. However, its capacity to provide long-term funding is limited as there are hardly any mechanisms in place to consciously organize the distribution of long-term IOUs across different segments, particularly among NBFIs. While the monetary architecture’s capacity to provide emergency elasticity from firefighter balance sheets to combat financial instability has increased since 1999 and seems in comparatively good shape, the capacity to manage and orchestrate the financing cycle’s final contraction is underdeveloped and appears more like an abstract idea rather than a practical possibility.

Our contribution is threefold: First, our four-step macro-financial governance scheme adds to the debates about debt sustainability (Eichacker, 2023; Kentikelenis et al., 2016; Lavoie 2013; Nersisyan and Wray, 2010; Prates, 2020; Reinhart and Rogoff, 2015) by conceptualizing debt sustainability not statically, as a hard limit or threshold that once breached produces irreversible damage on the economic systems in question, but as a matter of the long-term governance of the financing cycle. This foregrounds the long-term funding of debt instruments, the importance of putting into place mechanisms for stabilization, and the necessity of considering the issue of the final contraction of debt instruments. This procedural approach goes beyond the debates connected to Modern Monetary Theory (MMT), which are mostly concerned with the expansion of balance sheets and not with issues of funding and contraction. Second, we add to the European hidden investment state literature (Bezemer et al., 2023; Kedward et al., 2022; Marois, 2021; Mertens and Thiemann, 2018; Mertens et al., 2021). By looking beyond the monetary-fiscal dichotomy, we highlight that financing large-scale transformations is a process that requires macro-financial governance of different segments in the monetary architecture. Third, we map the European monetary architecture with its idiosyncrasies and put it into conversation with the wider Green Finance literature (Baines and Hager, 2023; Campiglio, 2016; Dafermos et al., 2021; Fichtner et al., 2024; Schütze and Stede, 2024). We show how the balance sheets of the Eurosystem, commercial banks, NBFIs, and the fiscal ecosystem interlock in an idiosyncratic and historically specific way and highlight the role of OBFAs in this network.

The remainder of this article is organized as follows. The second section provides a conceptualization of today’s European monetary architecture as a web of balance sheets that interlocks through various credit instruments. The third section discusses the capacity of the European monetary architecture to finance the Green Transition, drawing on our four-step scheme for Green macro-financial governance. The last section concludes by pointing to the need for further investigations into techniques for monetary architectures to manage long-term funding and balance sheet contractions.

Conceptualizing the Eurozone monetary architecture

The Monetary Architecture framework perceives financing as a process that involves specific forms of balance sheet operations which require different counterparties in a web of interlocking balance sheets (Borio and Disyatat, 2015; Murau et al., 2024). Hence, financing the Green Transition in Europe boils down to identifying suitable counterparties in the European monetary architecture that have the capacity to partake in the financing process.

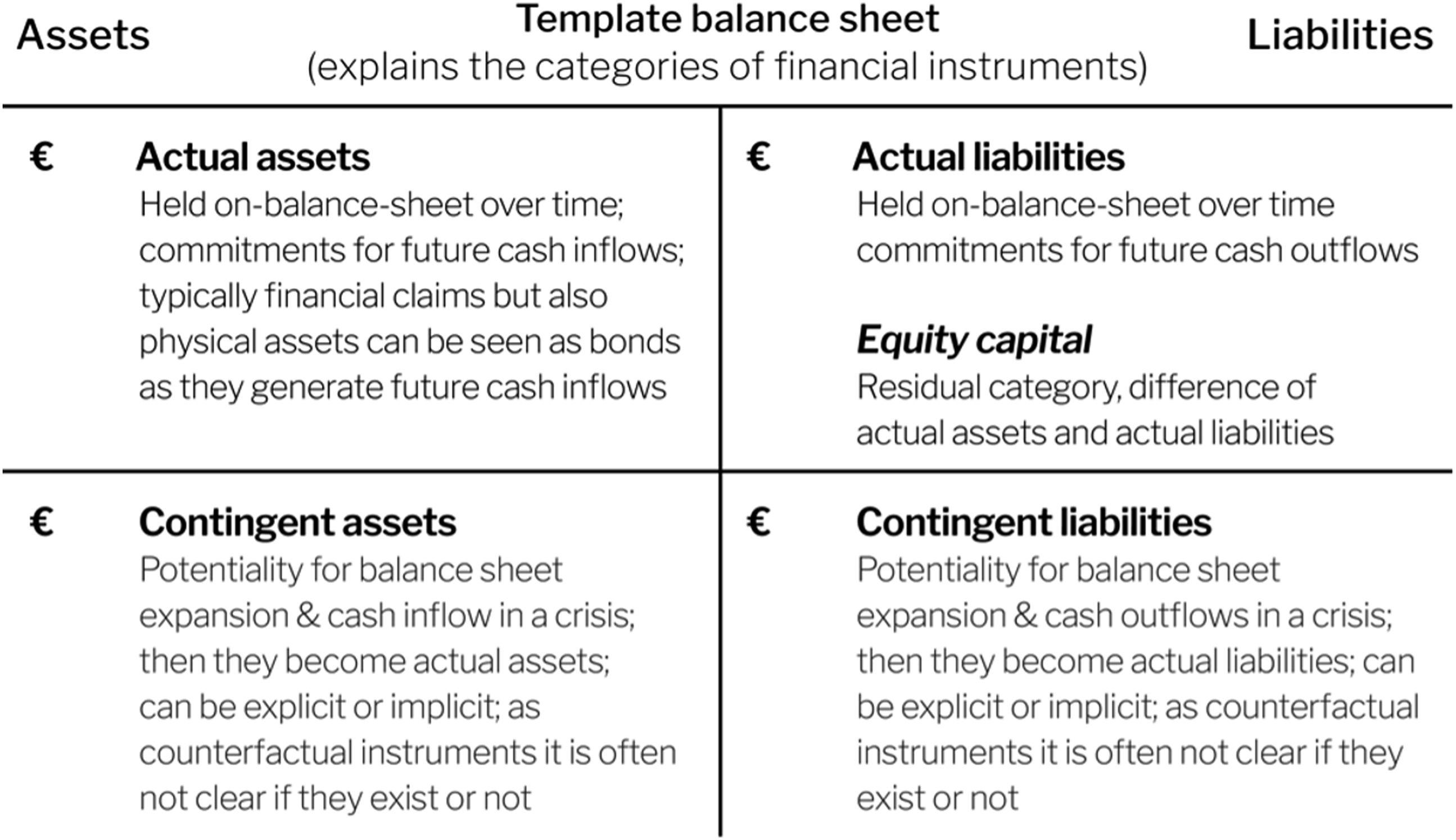

To model the real-world monetary and financial system in a historical-institutionalist way, the Monetary Architecture framework represents all financial institutions as well as households, companies, and various state-related entities as balance sheets. These balance sheets have a hierarchical relationship with each other and interlock through the instruments they hold as assets and liabilities (Mehrling, 2017). Figure 1 presents a “template balance sheet” that, in different variations, can be used to portray all the institutions that are part of the monetary architecture via the different instruments they hold (cf. Murau, 2020). On the left-hand side, it portrays assets which are thought of as commitments for future cash inflows. On the right-hand side, it portrays liabilities which are commitments for future cash outflows. The upper part of each balance sheet depicts actual instruments, which are directly observable on balance sheet; the residual between actual assets and actual liabilities forms the institution’s equity capital. The lower part of each balance sheet shows contingent instruments. These are counterfactual instruments which imply the potential to become actual assets or liabilities in the moment of a crisis (Haldane and Alessandri, 2009). Contingent liabilities typically are guarantees that one balance sheet gives to another one, whereas contingent assets are guarantees that a balance sheet receives from another one. Template balance sheet for the monetary architecture framework.

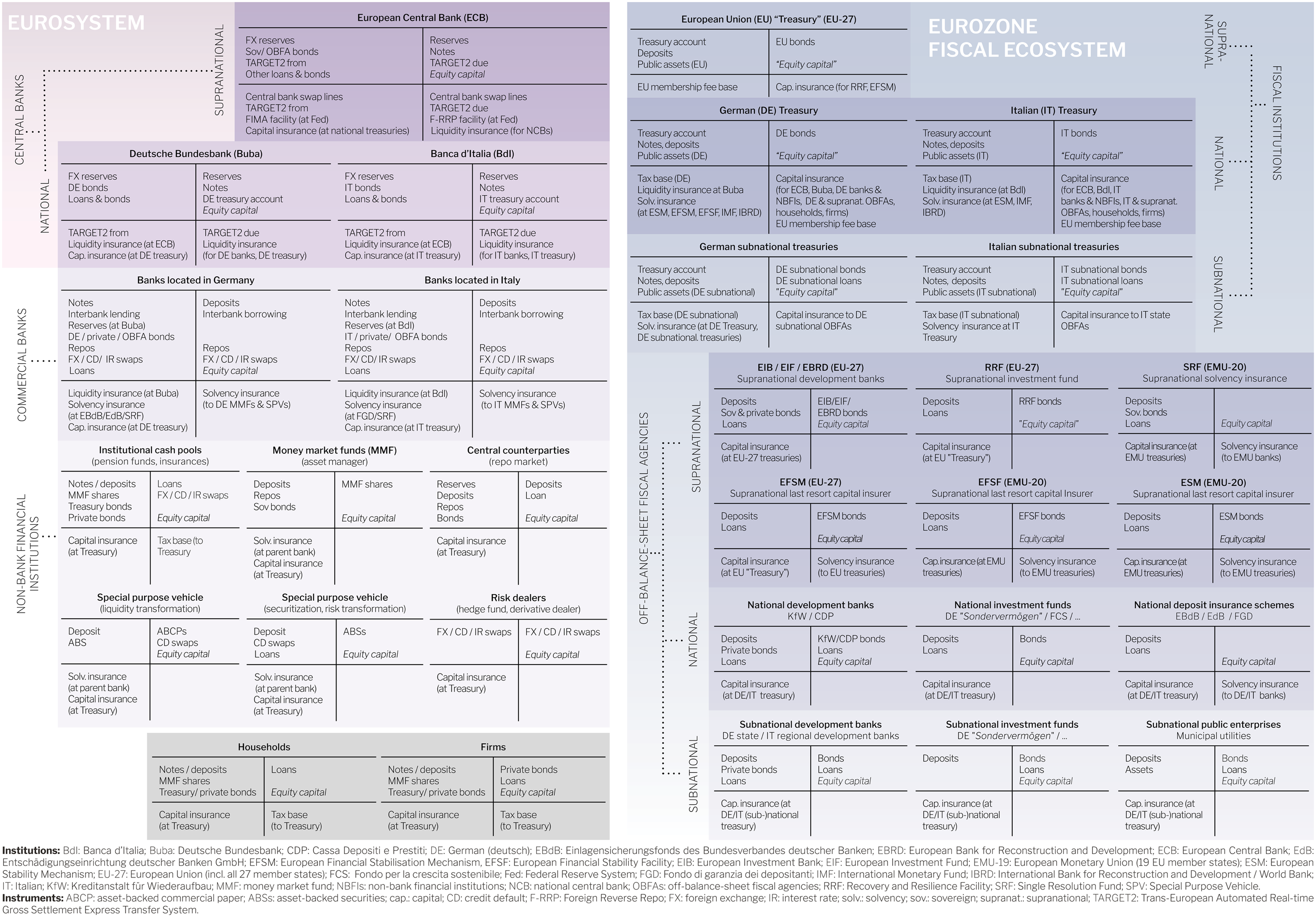

Drawing on the template balance sheet, Figure 2 visualizes the status quo of the European monetary architecture. It looks at the four “segments” of the monetary architecture: central banking, commercial banking, NBFIs, and the fiscal ecosystem which comprises treasuries and OBFAs. It distinguishes a national and a supranational layer for the central banking segment and an additional subnational layer for the fiscal ecosystem. We only include two member states, Germany and Italy, which represent surplus and deficit countries, but the model could easily be expanded to all 20 members of the European Monetary Union (“EMU-20”) or all 27 EU member states (“EU-27”) by adding those member states which have not (yet) introduced the single currency (“Non-EMU-7”). Our analysis necessarily navigates both the EMU-20 and the EU-27. The Eurozone monetary architecture as a complex web of interlocking balance sheets.

Central banking

The central banking segment comprises the European Central Bank (ECB) and the national central banks (NCBs). The figure merely visualizes the balance sheets of the Bundesbank and the Banca d’Italia. Together with the other EMU-20 NCBs and the ECB, they form the Eurosystem.

The ECB and the NCBs issue three types of central bank money as their liabilities: reserves, which function as money for banks; the national treasury accounts, which offer deposit services to fiscal entities; and notes, which function as money for everyone in the monetary architecture. Central bank money is the hierarchically highest form of money in the monetary architecture. It is simultaneously a debt and a non-debt because it is created with the same balance sheet mechanics as any other form of credit money and is constructed as a promise to pay, but it promises to pay nothing else but itself (Murau and Pforr, 2020). On the asset side, central banks hold foreign exchange (FX) reserves, various securities such as national treasury bonds and OBFA bonds, and loans. While NCBs hold primarily instruments of institutions from “their” national jurisdiction, the sovereign bonds issued by the German treasury (Bundeswertpapiere, “bunds”) function as EUR-denominated safe assets (Brunnermeier et al., 2016).

An important aspect of the monetary union is the TARGET system which connects the balance sheets of the ECB and all EU NCBs. TARGET stands for “Trans-European Automated Real-time Gross Settlement Express Transfer System” and was upgraded to the TARGET2 system in 2007-8 (Schelkle, 2017). It enables NCBs to carry out cross-border inter-central bank payments. If any surpluses or deficits remain at the end of each business day after clearing, the NCBs shift their claims and liabilities to the ECB balance sheet in a process called “novation.” This provides an unlimited funding mechanism for cross-border imbalances which is integral to maintaining monetary union (Bindseil and König, 2012) and makes the ECB the hierarchically highest balance sheet in the Eurosystem, thus functioning as a central counterparty (CCP) to all other NCB balance sheets (Murau and Giordano, 2024).

As NCBs continue to interact with “their” national banking systems, German banks hold their reserves at the Bundesbank, Italian banks at the Banca d’Italia, etc. Hence, NCBs are also the lender-of-last-resort to “their” national banks and offer liquidity insurance. Monetary policy is centrally decided by the ECB Executive Board but implemented by the NCBs (ECB, 2000).

Commercial banking

The commercial banking segment comprises banks located in the different EU member states, here again depicted via Germany and Italy as examples.

Banks create deposits as liabilities which function as money for most other institutions with access to bank accounts. Deposits are created when banks hand out a loan or purchase a bond with a counterparty in a balance sheet operation that may be called a “swap of IOUs” (Mehrling, 2017). On the asset side, banks hold various types of loans and securities, predominantly from counterparties in their national jurisdiction. While the balance sheets of different EMU-20 member states appear similar at a higher level of abstraction, there are significant national idiosyncrasies. For instance, as opposed to their Italian counterparts, German banks rely to a large extent on covered bonds (Pfandbriefe). Similarly, within each jurisdiction, banks differ significantly in their asset structure, although we abstract from such a level of granularity here. For risk management purposes, banks use various derivatives such as foreign exchange swaps, interest rate swaps, and credit default swaps. To protect their balance sheets and ultimately the integrity of their customers’ deposits, they have extensive contingent assets in the form of liquidity backstops from central banks, solvency backstops from deposit insurance OBFAs, and capital insurance backstops from national treasuries.

Banks are typically seen as the key entities to provide financing. In the contemporary system, banks are the hierarchically lower institutions that interact with companies and households to grant loans, whereas central banks are the hierarchically higher safety valves whose balance sheets should stay lean in normal times and only expand when the system is under stress. In this logic, banks are the workhorses and central banks are firefighters (Murau et al., 2024).

Monetary unification raised hopes that Eurozone banking systems would grow together as one, but the Eurocrisis reversed that trend and induced fragmentation. It exacerbated banks’ “home bias,” maintained their idiosyncratic “legacy” structures, and allowed cross-border lending to a very limited extent (Bénassy-Quéré et al., 2018). The reduction of intra-European cross-border activities is a reason for the Eurosystem’s increasing TARGET2 balances. The Banking Union project launched in 2012 sought to foster banking system integration. Although it harmonized regulations and centralized supervision, it failed to overcome fragmentation (Rostagno et al., 2019).

Non-bank financial institutions

NBFIs in the European monetary architecture display fewer national legacy structures and are integrated into the wider international shadow banking system (Endrejat and Thiemann, 2020). In our depiction, the European shadow banking “daisy chain” (Pozsar et al., 2012) comprises institutional cash pools such as pension funds and insurance companies, money market funds (MMFs) that issue MMF shares, central counterparties (CCPs) that pool the issuance of repos and other instruments, and special purpose vehicles (SPVs) used for securitization and liquidity transformation that create asset-backed securities (ABSs) and asset-backed commercial papers (ABCPs), as well as risk dealers such as hedge funds that hold various types of derivative products (Nabilou and Prüm, 2019).

Due to the European universal banking model, more types of financial activities can be carried out on European bank balance sheets than on US ones (Bayoumi, 2017). Hence, the Eurozone’s NBFI sector comprises around two-fifths of Eurozone financial assets, roughly on par with the banking sector (ESRB, 2023), whilst US NBFIs constitute close to two-thirds of the total value of financial assets, thus dwarfing its banking sector, which constitutes around one-fifth (FSB, 2022). The European NBFI sector is less diverse than in the US as some institutions are missing or are insignificant (e.g., venture capital funds). With regard to institutional cash pools, the image is more diverse. While European pension funds are significantly smaller than their US counterparts (€3 trillion vs US$23 trillion) and more than half of the assets are in the Netherlands alone, European insurance corporations are bigger than their US counterparts (EUR 9.2tn vs USD 8tn). 1

Attempts to foster EU financial integration comprised targeted institutional evolution of the NBFI segment—for instance, by placing emphasis on a Europeanized repo market (Gabor, 2016; Gabor and Vestergaard, 2018) or by promoting securitization via Capital Market Union (Braun and Hübner, 2018; Engelen and Glasmacher, 2018) with mixed results (Lehmann, 2020).

Fiscal ecosystem

The fiscal ecosystem comprises treasury balance sheets, which represent the main balance sheets of states and are subject to the checks and balances of the executive and legislative branches of government, as well as OBFAs, which also perform parts of states’ fiscal functions but are often designed as public-private hybrids and not controlled and regulated in the same way as treasuries, while receiving explicit or implicit treasury guarantees. National treasuries function as capital insurers of last resort for the rest of the architecture—that is, they stand ready for bailouts and recapitalization in major financial crises—while receiving liquidity insurance from central banks.

In the figure, treasuries and OBFAs are located on a national, supranational, as well as subnational level which plays out differently across EU member states.

The Eurozone is a monetary union without a fiscal union as it maintains national sovereignty over their treasury balance sheets (Mody, 2018). No autonomous European treasury was created that would raise taxes, issue sovereign debt, and have budget authority over the monetary union. Instead, the strategy adopted comprised the creation of ex ante criteria about treasuries’ legitimate budget deficits and debt-to-GDP ratios written down in the Stability and Growth Pact (Mariotto, 2022) and coordinated via the European Semester (Verdun and Zeitlin, 2018). While a supranational EU-27 “Treasury” balance sheet exists, it does not have its own “tax base” but depends on membership fees paid by the member states. 2 While it issues bonds to a marginal extent, it is barred from using the proceeds to finance the EU’s core budget, although it does lend them on to certain non-EU countries (EC, 2020).

Since the Eurocrisis, the European monetary architecture has witnessed a proliferation of supranational OBFAs, which have transformed the fiscal ecosystem and have led to a more significant degree of fiscal integration than exists on paper—paradoxically in tandem with the tightening of fiscal rules (Guter-Sandu and Murau, 2022). Supranational “workhorse” OBFAs comprise investment vehicles such as the European Investment Bank (EIB), the European Investment Fund (EIF), the European Bank for Reconstruction and Development (EBRD), and the Recovery and Resilience Facility (RRF), introduced as the EU’s response to the COVID-19 pandemic with the right to autonomously issue securities and use the proceeds to support EU member states (Bekker, 2021). Supranational “firefighting” OBFAs are the Single Resolution Fund (SRF) and the European Stability Mechanism (ESM), as well as its predecessors, the European Financial Stabilization Mechanism (EFSM) and the European Financial Stability Facility (EFSF).

On the national level, the dominant types of OBFAs are development banks. Mertens et al. (2021) compile a list of 26 national development banks in the EU. The largest ones are the German Kreditanstalt für Wiederaufbau (KfW) and the Italian Cassa Depositi e Prestiti (CDP), next to the French Caisse des dépôts et consignations (CDC) and the Dutch Bank Nederlandse Gemeenten (BNG). Their assets in relation to national GDP are 14.4% (KfW), 24.4% (CDP), 15.6% (CDC), and 19% (BNG); most other NDBs have figures below 5%. 3 Similar structures exist on the subnational level. In Germany, the 16 federal states have their own development banks which range in size from 22 % to 1.3% of state GDP. 4 Italy has a network of public banks that comprises several Mediocredito institutes. Some of them are publicly owned (e.g., MedioCredito Centrale), and others are private (e.g., Banca Mediocredito del Friuli Venezia Giulia) or in public-private ownership (e.g., Mediocredito Trentino Alto Adige).

Central banks, commercial banks, NBFIs, and the fiscal ecosystem comprising the European “Treasury” and a range of OBFAs together constitute the four main segments of the European monetary architecture. Understanding this institutional layout, with its idiosyncrasies and dissimilarity with other monetary architectures like the US one, enables a better grasp of what is at stake in the question of the capacity of the European monetary architecture to sustain an expansion over a long time horizon and to do so in an orderly fashion, without risking debt sustainability becoming a systemic issue that might jeopardize the wider project of financing the Green Transition. The next section analyses this financing process, tailored to the European monetary architecture, and foregrounds strengths and challenges that can be identified throughout.

Financing the Green Transition in the Eurozone monetary architecture

The web of interlocking balance sheets depicted in Figure 2 is the real-world construct that must finance the Green Transition. The EU assumes that most of the EUR 620bn per year would come from the private sector, coupled with an expansion of public sector balance sheets that can plug the gap left by less appealing investment propositions (EC, 2023). However, this overview covers parts of the picture; adopting the monetary architecture as conceptual lens brings more nuance.

Financing the Green Transition is a long-term process that requires macro-financial governance and a division of labor between different balance sheets of the monetary architecture, while maintaining the debt-carrying capacity of the system. We suggest therefore that macro-financial governance involves a scheme that comprises four steps: first, an initial balance sheet expansion; second, long-term funding, that is, a strategy for which balance sheets should hold the long-term IOUs originally created; third, mechanisms to ensure financial stability, that is, to prevent the funding process from imploding in a financial crisis; and fourth, facilitating an orderly balance sheet contraction at the end of the financing cycle.

Drawing on this scheme, we discuss the capacity of the European monetary architecture in its present form to carry out the four steps and to provide macro-financial governance for Green Transition finance. We contrast different options for how each of the steps can theoretically be implemented and apply the approach on the real-world institutional setting, taking into account the various financial, political, and legal constraints the EU is subject to as an ongoing idiosyncratic integration project.

Step 1—green initial expansion

As the opening step of the macro-financial governance scheme, financing the Green Transition requires a “green initial expansion” of balance sheets. Two institutions must act as counterparties and simultaneously expand their balance sheets as a swap of IOUs. One of the credit instruments thus created functions as money, for instance, a deposit, and should be used to pay for investment activities. The other credit instrument, typically a loan or bond, is the reverse balance sheet entry. It is a promise to pay an even greater sum of money in the future (Minsky 1986; Murau and Pforr 2020). A green initial expansion requires “elasticity space” on both balance sheets involved, that is, capacity to expand further, which depends on several factors: the willingness and ability of other institutions to act as counterparties for balance sheet expansion; the various “stipulations” in place for allowed on-balance-sheet activities and how they are enforced; and the available contingent guarantees that are explicitly or implicitly in place from hierarchically higher balance sheets (Murau, 2020). Which balance sheets in the European monetary architecture have the elasticity space to carry out such a green initial expansion?

The first option is traditional bank financing. Commercial banks create deposits as short-term IOUs. Their counterparties could be households which create loans or mortgages as longer-term IOUs on the liability side of their balance sheet, or firms which could also create a loan or issue securities such as bonds or commercial papers (Tobin, 1963).

This approach constitutes the primary mechanism for a green initial expansion as it is the default for how the contemporary credit money system is supposed to work. Moreover, the Eurozone architecture is more bank-centered compared to the ones in Anglo-Saxon countries (Demertzis et al., 2021). However, given the financial volumes expected for the Green Transition, the capacity of European banking systems to provide additional elasticity space for financing new green investments seems limited. Since the Global Financial Crisis (GFC), European banks have exhibited risk aversion for new lending while often being saddled with non-performing loans (Di et al., 2023; Quaglia, 2019). While EU economies are in a recession due to the overlapping pressures of the post-COVID lopsided recovery and the energy shock after the Russian war on Ukraine, the financial cycle is in a downswing and the elasticity space on banks’ balance sheets is reduced. At the same time, the post-GFC regulatory environment seeks to contain financial instability, which effectively disciplines bank balance sheets (Thiemann, 2023) and makes them increasingly dependent on government derisking (Gabor, 2020).

A second option for a green initial expansion would follow the monetary-and-fiscal-policy dichotomy and involve using elasticity space on public balance sheets, notably central banks and treasuries. This entails the issuance of new liabilities on treasury balance sheets via sovereign bonds, or the issuance of new liabilities on central bank balance sheets via the creation of new currency or reserves (Wray and Nersisyan, 2019).

The EU’s current macro-financial regime makes these policies hard to implement. The Stability and Growth Pact, albeit often criticized for not being “biting” enough, limits the capacity of treasury balance sheets to expand to finance investment. The ECB’s statutes prevent the Eurosystem from primarily considering factors such as employment and output, and the central banking segment is not supposed to engage in credit allocation (van ’t Klooster and De Boer, 2023). The overall vision for the Eurozone as stipulated in the Maastricht Treaty is to keep public balance sheets lean. It is true that European treasuries expanded their balance sheets (manifested in increased sovereign debt levels) in the GFC and the Eurocrisis as they bailed out failing banks and backstopped the real economy in the COVID-19 crisis (Tooze, 2021), all the while central bank balance sheets expanded massively via TARGET2 imbalances, asset purchase programs, and tweaks in the collateral framework (Murau and Giordano, 2024; van ’t Klooster, 2023). Yet, treasury and central bank balance sheets are biased toward “reactively” expanding ex post while it is politically, legally, and administratively difficult to make them “pro-actively” expand ex ante as it would be required for a green initial expansion. This bias has been cemented by various post-crisis regulations such as the supranational Fiscal Compact or national fiscal austerity measures such as Germany’s constitutional debt brake (Laffan and Schlosser, 2016).

This points to a third option for manufacturing a green initial expansion: OBFAs (Guter-Sandu and Murau, 2022). OBFAs have the potential to offer substantial elasticity space that can be harnessed for a green initial expansion. This refers both to existing OBFAs and OBFAs that can be newly created. Due to their typically hybrid ownership and governance structure, OBFAs are not primarily bound by the logic of short-term profit maximization and can make investment decisions based on other rationales such as decarbonization effects. As they have explicit or implicit guarantees by treasuries, OBFAs are attractive as counterparties and have advantageous financing conditions but are subject to different stipulations restricting their elasticity space. Development banks, for instance, can provide financing for decarbonization projects at a volume that is proportionate to the task (Kedward et al., 2022). Taking the case of Germany, its two federal and 16 state development banks have assets that amount to up to 30.1% of state GDP. 5 The EU-level RRF has been used to provide funding for Green projects in the energy sector (Bekker 2021) while investment in public transport can be carried out by railway OBFAs (Finger et al., 2019). And investment funds such as the German Klima-und Transformationsfonds, a federal Sondervermögen, can support investments in housing insulation and residential heating systems, with disbursements running via subnational OBFAs (Golka et al., 2024).

Overall, as none of the options sketched are mutually exclusive, all three contribute to the capacity of the European monetary architecture to provide for a green initial expansion. That said, while traditional profit-oriented bank financing and the conventional monetary-and-fiscal-policy tools receive still the most attention, the usage of OBFA financing seems to offer the greatest potential for harnessing elasticity space.

Step 2—long-term funding

A green initial expansion of balance sheets results not only in the creation of short-term IOUs that have to be spent on green projects but also of long-term IOUs that require funding—that is, they have to be placed with other balance sheets that are willing and able to hold them over a long time horizon (Mehrling, 2020). Funding the green initial expansion may thus involve the distribution of instruments across balance sheets, segments, and jurisdictions. The success of this process depends on the capacity of the monetary architecture to organize the distribution and maintain the funding (Cesaretto, 2017; Graziani, 2003). This ensures that the debt instruments created as part of the initial expansion are carried forward sustainably throughout the lifetime of the financing cycle. If this fails, the transition might be impacted by rising inflation or end up in a financial crash (Borio, 2014; Minsky, 1986). While ensuring that the credit money created is used for productive green investments is a challenge on its own, the concern of the macro-financial governing scheme is with the financial side of the operation and the capacity of the monetary architecture to absorb the additional volume of debt. How can this be achieved in Europe?

As a first possibility, the long-term IOUs could simply remain on the balance sheets of the institutions that were part of the initial expansion. In this case, a bank could give a company a loan and keep that loan as an asset in its books until it matures. This funding strategy is still very prevalent in Europe (Hardie, 2016) but poses specific challenges for the Green Transition. For instance, by keeping long-term IOUs on their balance sheets, banks are less able to free up elasticity space for new lending. Furthermore, the fragmentation of the European monetary architecture with heterogenous national banking systems—that is, different regulatory frameworks, legal systems, and banking practices—creates barriers to cross-border investment and long-term funding (Matthijs and Blyth, 2015). This may lead to uneven national progress in meeting the challenge of the Green Transition.

A second possibility would be to sell the long-term IOUs to other balance sheets willing to hold them. This could achieve a wider distribution of instruments within the monetary architecture and allow a diversification between the balance sheets involved in the initial expansion and the long-term funding (Mehrling, 2020). Yet, it opens questions about the management of demand and supply of the involved instruments, distribution mechanisms, and desired outcomes.

In principle, the European monetary architecture has numerous balance sheets that can support long-term funding of an initial green expansion. Next to households, firms, and banks, this applies to different NBFIs. Notwithstanding the incipient nature of NBFI investment in decarbonization and the challenge of preventing greenwashing (Baines and Hager, 2023), NBFIs can be incentivized to hold green assets by introducing inducements such as tax credits or deductions for investments in green projects, or subsidies and grants to support green initiatives and reduce financial risk for investors. Similarly, regulatory measures can be conceived like mandates or quotas requiring institutional investors to allocate a certain share of their portfolios to green investments or disclosure requirements that expose investors (as well as the wider public) to informed decision-making (Fichtner et al., 2024). Funding can also operate by accepting green assets as collateral in repo transactions between different private institutions. A key role here would come to CCPs, which contribute to setting standards for eligible repo collateral (Dafermos et al., 2021). The Green Taxonomy currently developed by the EU could serve as an important tool to help privilege instruments created in a green initial expansion in the funding process (Schütze and Stede, 2024).

Central banks as the hierarchically highest balance sheets have considerable power in making these assets attractive by purchasing them via open market operations or making them eligible assets in their repo operations (Murau et al., 2024). Still, this proposal entails a degree of conscious management of the financial system which is not found in practice to date. The European monetary architecture largely relies on market forces and self-organization to coordinate the distribution of instruments in the process of long-term funding as there are no specific institutions in place that could aid in matchmaking. That said, an already-existing or newly created OBFA could take this on and coordinate the placing of green bonds (Kedward et al., 2022). It could, for instance, buy and sell individual green loans or portfolios of green loans to specific institutional investors.

A third possibility to facilitate long-term funding would involve the restructuring of the long-term instruments created in a green initial expansion via securitization in order to tailor them specifically to the risk, liquidity, and maturity preferences of other balance sheets (EBA, 2022). Prima facie, this can enhance the long-term funding capacity of the Eurozone architecture as it promises to crowd in more balance sheets for whom the existing green assets are not suitable or attractive enough (Acharya et al., 2013).

The way this would work, for instance, is by increasing the availability of green ABSs via the creation of a green securitization OBFA or the endowment of existing OBFAs that already engage in this area (e.g., EIB) with green securitization powers. This can be modelled on US Government-Sponsored Enterprises (GSEs) such as Fannie Mae, which has recently become one of the world’s largest issuers of green bonds, particularly Green MBS (Fannie Mae, 2023). So far, though, the green securitization market in the EU is rather rudimentary. Standing at EUR 10bn at the end of 2021, it compares poorly with the US, which is a market that is roughly 10 times bigger, and even with China, which is in turn over 50% bigger compared to the EU (EBA, 2022). The market has been held back by the aborted Capital Markets Union project (Braun and Hübner, 2018) and by the lack of a robust regulatory framework. Whereas China has developed a rather extensive framework outlining the definition, eligibility criteria, verification, and disclosure for green ABS (EBA, 2022), no such framework exists for the EU. While this is also lacking in the US, the weight of US GSEs in the market, which have developed their own issuance programs, has resulted in a de facto regulatory framework greasing the wheels of green securitization. Despite the bad reputation that securitization has rightfully acquired in the aftermath of the GFC, but given the higher regulatory standards now expected of the underlying assets, it has become a permanent feature of the green finance field, although one that is as yet lacking in the European monetary architecture.

In general, the European monetary architecture does not seem presently well suited to fund a green initial expansion over a long time horizon as there are no clear strategies in place to support the funding process. This has implications for the debt-carrying capacity of the European architecture, given that a large initial expansion of debt instruments might not be able to be sustainably upheld in the funding phase without negative consequences and demands upon firefighting institutions to intervene. Even though the building blocks are there, the scale and speed called for by the imperative of financing the Green Transition would require the development of suitable strategies for macro-financial governance. This would require a step away from the notion that the funding structures required can simply be sorted out by private actors themselves.

Step 3—stabilize against disorderly contraction

The third step in the macro-financial governance scheme pertains to stabilizing against disorderly contractions. Ideally, the green initial expansion of balance sheets would be sustained throughout the period of long-term funding until a final contraction sets in when the majority of green projects are completed, and debts are orderly repaid. In this case, debt sustainability is not an issue as the monetary architecture is able to fund the instruments created throughout their lifecycle. Yet, a balance sheet contraction may occur early and disorderly as credit is inherently unstable (Minsky, 1986)—in this regard, green IOUs are no different than other IOUs. They may lead to green bubbles, “greenflation,” or a breakdown in valuation mechanisms due to rampant greenwashing. For mitigation, firefighting balance sheets can provide liquidity, solvency, or capital insurance to tame the contraction dynamics (cf. Haldane and Alessandri, 2009). What is the capacity of the European monetary architecture to cushion against such disorderly contraction?

First, there is liquidity insurance, which typically refers to the lender-of-last-resort function that central banks exercise for commercial banks or treasuries, but may also entail commercial banks backstopping NBFIs further down in the hierarchy. In the original 1999 Eurozone set-up, central bank balance sheets were meant to remain inelastic by design. While the degree of liquidity insurance for banks remained ambiguous, the liquidity insurance for Treasuries was purposefully restricted when the Eurosystem substituted its unconditional acceptance of Eurozone member states’ sovereign debt in the original two-tiered system with a market-based system that drew on the assessment of private rating agencies (van ’t Klooster, 2023). This created a situation in which Eurozone treasuries lacked liquidity backstops as if they were indebted in a foreign currency (De Grauwe, 2012). But this changed when the Eurocrisis hit. The ECBs and NCBs significantly expanded their elasticity space by introducing emergency purchase programs for various public and private bonds, repeatedly lowering collateral standards. The big game changer was Mario Draghi's ‘whatever it takes' speech, which usered in the Eurozone 2.0 (De Grauwe and Ji, 2015). This was complemented by the automatic widening of TARGET2 balances to substitute private cross-border funding. After the Eurocrisis, the ECB balance sheet was operationalized for active firefighting purposes as its elasticity space was increasingly harnessed for the purpose of asset purchases. The latest example is the Pandemic Emergency Purchase Programme, which was the Eurosystem’s core response to the COVID-19 crisis (Murau and Giordano, 2024). Therefore, the European monetary architecture has developed ample elasticity space to support liquidity insurance. Banks, treasuries, and OBFAs that fund green assets get liquidity insurance from the Eurosystem whereas NBFIs can get liquidity insurance from “parent banks,” if there are any.

Second, there is solvency or deposit insurance, which refers to backstops to pay off banks’ depositors in case of bankruptcy. This is supposed to avoid, for instance, self-fulfilling prophecies that would lead to a run on banks. The different deposit insurance schemes of Eurozone member states were originally kept national but were harmonized during the Eurocrisis (Guter-Sandu and Murau, 2022). The Banking Union project consolidated regulation and supervision on a supranational level, even though it did not implement the planned European Deposit Insurance Scheme through which national deposit insurance schemes would mutually backstop each other (Quaglia, 2019). By consequence, the capacity to provide solvency insurance in a green funding cycle still differs between Eurozone member states.

Finally, there is capital insurance, which refers to the power of treasuries to bail out and eventually recapitalize any other balance sheet in the monetary architecture. Arguably, due to its tax base as a contingent asset, treasuries can discount future tax revenues and thus have a special capacity to provide anticyclical backstops to institutions with negative equity capital. According to the Maastricht Treaty, treasuries should not have to provide bailouts to other institutions. Rather, private institutions are supposed to “discipline” treasuries and induce “prudent” sovereign debt levels. Moreover, the no-bailout clause in the European treaties ruled out that different Eurozone treasuries would provide capital insurance to each other if they should struggle to repay their debt. This logic, however, was put upside down during the GFC and the ensuing Eurocrisis. Various European treasuries provided capital insurance of last resort by bailing out and recapitalizing banks, either directly or by setting up national emergency OBFAs such as the German Finanzmarktstabilisierungsfonds (SoFFin) (Woll, 2014). Moreover, when the contraction dynamics spilled over to sovereigns, various European treasuries provided emergency loans to Greece while pulling in the IMF before setting up the EFSF and EFSM as improvised emergency firefighting OBFAs. Later, the EFSF and EFSM were replaced by the ESM as a permanent OBFA that stands ready to provide capital insurance to EMU-20 treasuries (Matthijs and Blyth, 2015). Even though the Fiscal Compact doubled down on the original logic, there are clear precedents that European treasuries deliver on their capital insurance function in financial crises that threaten systemic stability. This also affects the IOUs created in a green initial expansion.

In sum, the European monetary architecture today has substantially more institutions, instruments, and elasticity space to stabilize against disorderly contractions. This puts it in a relatively good position to carry out the third step in the macro-financial governance scheme. By extension, having these mechanisms in place also increases the debt-carrying capacity of the European monetary architecture.

Step 4—facilitate orderly contraction

The last step in the macro-financial governance scheme refers to the final contraction of the balance sheets associated with a particular financing cycle. This entails the repayment of money created during the green initial expansion, which extinguishes the long-term debt instrument but also ceteris paribus the credit money. This would reverse the original swap of IOUs and comprise a symmetrical contraction of balance sheets. While this is the ideal way how the “monetary circuit” would operate (Graziani, 2003), a final orderly contraction of balance sheets at a systemic level rarely seems to happen. Certainly, individual long-term IOUs are being repaid and extinguished; but in the aggregate, total nominal debt levels in all segments of the monetary architecture tend to increase. If regular repayment fails to materialize, a substantial shrinking of balance sheets in the aggregate tends to only occur in a disorderly fashion, through large financial crises. These often have severe economic and social repercussions (Van Dijk, 2013). What is the European monetary architecture’s capacity to facilitate an orderly contraction of balance sheets?

One strategy to deal with facilitating an orderly final contraction is to establish mechanisms that allow the shrinking or even defaulting of balance sheets while shielding the rest of the monetary architecture from its implications and finding ways to maintain the critical functions provided by the contracting balance sheets. This strategy is behind the concept of “resolution,” which became popular after the GFC as a silver bullet to deal with the too-big-to-fail problem (Philippon and Salord, 2017). Large financial institutions were branded as “systemically important” because a shrinking of their balance sheet would lead to spill-over effects in the monetary architecture that would be too substantial to tolerate. The resolution framework seeks to remedy this problem while keeping struggling institutions in private ownership (Laeven and Valencia, 2010).

The EU has developed resolution regimes for systemically relevant banks (Philippon and Salord, 2017) as well as NBFIs such as financial market infrastructures (CPMI-IOSCO, 2014). These include managed take-overs or mergers with other financial institutions and bail-ins, as well as the use of the Single Resolution Fund (SRF) as an OBFA that pools capital to be used in a crisis to pay out defaulting banks. Post-GFC reforms also aimed to reduce opacity in the shadow banking system, through, for instance, shifting bilateral (over-the-counter) instruments such as repos to CCPs to simplify supervision. Plans for a CCP Recovery and Resolution regime have been discussed (Priem, 2018), and while resolution regimes are key to facilitating orderly balance sheet contractions, they are still untested and, as critics point out, hardly enough to defend against substantial financial instability (Asimakopoulos and Howarth, 2022).

This brings us to an alternative strategy to facilitate an orderly final contraction: Rather than keeping defaulting institutions and instruments under private ownership, public firefighting institutions could use their in principle unlimited elasticity space to pull the instruments of defaulting institutions onto their balance sheets and conduct organized write-offs or redistributions of instruments. Public firefighters could thus close down some institutions and recapitalize others before eventually reprivatizing them with a lean balance sheet.

At present, the capacity of the European monetary architecture to carry out such government-centric measures for shrinking balance sheets seems very limited. A quintessential example for this strategy, coming from a different region and a different era, is how the US administration of Franklin D. Roosevelt ended the Great Depression shortly after assuming office. After a system-wide bank run in 1933, the Roosevelt administration declared a nationwide bank holiday and, backed by the 1933 Emergency Banking Act, endowed the Reconstruction Finance Corporation (RFC)—an important OBFA at the time—with restructuring the US banking system, in coordination with the US Treasury and the Federal Reserve (FDIC, 1984; Wicker, 1996). A similar set-up or comparable policies are not currently prevalent in Europe. Even the interventions during the GFC have led more to a backstopping rather than an organized contraction of bank balance sheets.

By consequence, a managed final contraction of the European monetary architecture is doubtful. In fact, it seems to be a more general feature of most, if not all, modern monetary architectures to struggle to facilitate orderly contractions at the end of financing cycles. Instead, they seek to prevent them from using their tools for liquidity, solvency, and capital insurance provision and keep the financing process de facto in an ongoing funding stage by continuously pushing the aggregate repayment further into the future.

Conclusion

This article has investigated the capacity of the European monetary architecture to provide Green Transition financing. Following our conceptual framework, we assume that Green finance must be mobilized by using elasticity space in different parts of the monetary architecture while employing a four-step financing process connected to the dynamics of the financial cycle, namely, balance sheet expansion, funding, stabilization, and final contraction.

We find that the European monetary architecture—despite the stagnation and fragmentation of its banking segment and the disciplining stipulations for treasuries—has ample elasticity space for an initial green expansion because of its developed ecosystem of OBFAs on a national, subnational, and increasingly supranational level. However, its capacity to provide long-term funding is limited as there are hardly any mechanisms in place to consciously organize the distribution of long-term IOUs across different segments, notably within NBFIs. This has implications for the debt-carrying capacity of the European monetary architecture, in as much as a large-scale transformation requires a systemic expansion in debt instruments which the monetary architecture must be able to sustain. While the architecture’s capacity to provide emergency elasticity from firefighter balance sheets to counteract financial instability has greatly increased throughout the last two decades and seems in comparatively good shape and able to deal with potential issues of debt sustainability, the capacity to manage and orchestrate the final contraction of a financing cycle seems underdeveloped and appears more like an abstract idea rather than an actual possibility.

These findings indicate two avenues for future research. First, our analysis calls for more political economy research on systemic funding of large-scale transformations. The funding dimension is largely neglected in the Green Finance literature but is decisive for the net-zero transformation to succeed. It would be desirable to develop a more fine-grained and institutionally specific toolbox on funding techniques and entry points for strategic management of funding, including OBFA schemes for crowding in different parts of the architecture. Second, in the macro-financial governance of large-scale transformations, the final contraction is an open flank—both from a theoretical and a policy perspective. The present institutional set-up has a bias towards expansion but only limited solutions to support organized contractions. Arguably, the volume of both public and private debt in the monetary architecture, which has reached historically unprecedented levels, contributes to manifold political-economic problems. For instance, “dirty assets” from previous financing processes create a carbon lock-in which constitutes one of the biggest headwinds to financing the Green Transition. This points to developing a macro-financial toolbox for contraction management that comprises concepts such as resolution but also looks for other historical best practices.

Footnotes

Acknowledgements

We have presented earlier versions of this article at the “Off-Balance-Sheet Fiscal Agencies and the Role of the State in Financing the Green Transition” workshop in Berlin in July 2023 and at the 35th Annual Conference of the European Association for Evolutionary Political Economy (EAEPE) at the University of Leeds. We wish to thank organisers and participants for constructive feedback. Special thanks go to Milan Babić and Sarah Sharma for editing the special issue, as well as to Elsa Clara Massoc, Dirk Bezemer, Vanessa Endrejat and other colleagues who have provided us with invaluable comments. We'd like to also thank the three anonymous reviewers who have helped us improve our manuscript. All remaining errors are our own.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Deutsche Forschungsgemeinschaft; (499921148).