Abstract

The euro has been at the heart of the debate about the crisis in the Eurozone. For some, it represents a fixed exchange rate regime, which hampered peripheral countries’ competitiveness, and for others, the European Monetary Union has a ‘flawed institutional design’ and an insufficient degree of integration that engendered the crisis. The present article analyses monetary integration from a materialist perspective. It draws attention to political agency, power and crisis management. The article focuses on the case of Portugal and poses the question of how the country's authorities were compelled to request a rescue package from the International Monetary Fund, the European Central Bank and the European Commission in 2011. It shows that this decision was triggered by the political agency of a series of players within the world of finance, most notably Portugal’s domestic banks, the independent Bank of Portugal and the European Central Bank. Reflecting their material interconnection through the European monetary system, their agency was highly coordinated. The strategies for crisis management that came to deepen the recession were not the result of insufficient European integration – they rather reflected Portugal’s form of integration within the European Monetary Union at the specific moment of crisis.

Keywords

Introduction

Two decades after the launch of the euro and one decade into the inception of the crisis in the Eurozone, the European project is subject to profound challenges, itself partly a symptom of the social tensions that were generated by that crisis (Hall, 2018). A large body of literature has sought to tackle the causes of the crisis in the Eurozone, but no consensus has emerged. Answers to the question of what type of crisis this was vary from a crisis of sovereign debt and fiscal profligacy, to a twin-deficit-crisis, a balance of payment crisis, a crisis of the euro, a crisis of financialization, a crisis related to different ‘varieties’ of capitalism, and a crisis of capitalism itself. Most interpretations in economics – orthodox and heterodox alike – share a focus on macroeconomic imbalances – either in the public or the private sector or both (European Central Bank, 2012; European Commission, 2010; Cesaratto, 2014; Frenkel, 2012; Pérez-Caldentey and Vernengo, 2012; Storm and Naastepad, 2015). Reflecting this focus, the literature in economics suffers from an under appreciation of the role of politics in shaping the evolution of the crisis (Copelovitch et al., 2016). Notwithstanding the crucial differences between mainstream and heterodox interpretations, most of them neglect or attribute only a secondary importance to political agency as a constitutive factor in the crisis.

Addressing this gap, this article draws attention to political agency, power and crisis management. It focuses on the manifestations of the eurozone crisis in the still understudied case of Portugal. While Portugal’s economic articulation within the Eurozone (and the world economy overall) informed the way in which the country was initially hit by the crisis, the strategies for crisis management also shaped the trajectory and anatomy of the crisis. The global financial crisis reached Portugal in 2008, when Portuguese banks faced increasing difficulty in accessing finance on international wholesales markets (Bank of Portugal, 2009a; Lagoa et al., 2014: 102; Jurek and Marszalek, 2014: 21). A first phase of crisis management witnessed the implementation of anti-cyclical policies and a series of measures vis-à-vis the banking system (Ministério das Finanças e Administração Pública, 2009; Torres, 2009: 60–61). These were always in line with guidelines at the European level, including those from the Council of the European Union, the European Commission (EC), ECOFIN and the Eurogroup meetings (Council of the European Union, 2008: 2; European Commission, 2008, 2014; Ministério das Finanças e Administração Pública, 2009: 21). In March 2010, when the EC started insisting on ‘improved fiscal discipline,’ Portugal switched to fiscal consolidation and internal devaluation (Costa and Castro-Caldas, 2014: 94). Portuguese authorities passed three austerity programmes that are referred to as the Stability and Growth Programs (SGP1-3) and were thereafter compelled to request a bailout from the Troika of the International Monetary Fund (IMF), EC and European Central Bank (ECB) in 2011. The structural adjustment programme that it was conditional on deepened austerity and internal devaluation and opened the door for an unprecedented neoliberal restructuring (Costa and Castro-Caldas, 2014; Hespanha et al., 2014). After a recovery with almost 2% growth in 2010, Portugal fell back into recession in 2011 (World Bank, 2018), thus lending support to the widespread argument that austerity aggravated the recession (Constâncio, quoted in Jones, 2018).

Contrary to the widespread idea that the rescue packages in the European periphery were imposed from the outside, the literature on Portugal acknowledges that series of domestic players actively promoted the bailout. These included political parties, the banking system and domestic scholars (Lains, 2013; Louçã and Mortágua, 2012; Moury and Standring, 2017; Rodrigues and Reis, 2012). Indeed, the bailout was announced amid a political crisis, after a strong pressure from the country’s domestic banks, without any discussion in parliament and without the consent of the prime minister. The Socialist Party was effectively squeezed out of government when the opposition parties voted down a fourth fiscal consolidation package, SGP-4. After the snap elections in June 2011, ‘going beyond the Troika’ was a mantra throughout the right-wing coalition government composed by the Social Democratic Party (PSD) and the Social and Democratic Centre – People’s Party (CDS-PP) in charge of implementing the structural adjustment programme between 2011 and 2014 (Lima, 2015: 10).

The contribution of this article is to document and analyse the agency of a series of institutions within the world of finance, both within and beyond Portugal, in the run-up to the bailout. It does so with reference to the debates about the relationship between structure and agency and forms of power (Hay, 2002; Miliband, 1969; Poulantzas, 1969). While the literature on Portugal has already pointed out that the domestic banking system exercised an enormous political pressure on the government prior to the bailout (Lains, 2013; Louçã and Mortágua, 2012; Pena, 2014), so far there is no complete interrogation of their agency. This article assembles a detailed chronology of events based on reports in the Portuguese media and the international financial press. The analysis is also informed by interviews with a former president and a former senior advisor of the Portuguese Debt Management Office, Instituto de Gestão de Tesouraria e do Crédito Público (IGCP) and with two academics. 1 Reports and press releases published by the ECB, the Bank of Portugal and IGCP provided corroborating evidence.

The article shows that there was a strong degree of concerted action between the Portuguese banks, the Bank of Portugal and the ECB. While a range of social forces activity pushed for the Portuguese government to request a bailout, these institutions had the power to trigger it. In accounting for this, the article provides fresh empirical details into the authoritarian character of governance in the Eurozone (Schneider and Sandbeck, 2019). It simultaneously analyses the interaction between internal and external drivers of neoliberal adjustment, which so far is left out of political economy studies of the crisis in Portugal. In analysing the agency of these institutions, the article interrogates their interconnection through the Eurosystem. While the euro is already at the heart of the debates about the causes of the Eurozone crisis, it is often treated as a fixed exchange rate regime, which has hampered competitiveness in the Eurozone’s periphery. In other approaches, the EMU has a ‘flawed institutional design,’ which engendered the crisis. In the latter view, the insufficient degree of integration is the root of the crisis. Contrasting with the institutional design view, this article provides a materialist analysis of Portugal’s integration with the EMU. Informed by a Marxist approach to economic integration it develops the notion of the EMU as ‘financial architecture’ that is historically specific. This architecture incorporates various national and international institutions, including central banks, private banks, credit rating agencies and the state. The architecture formed a structure that shaped the agency of a series of players within finance. The article argues that Portugal’s specific form of integration translated into forms of political agency that led to a bailout and that opened the door to a neoliberal resolution of the crisis. Furthermore, it emphasizes that Portugal’s financial architecture is not static, but dynamic and contingent on the ECB’s monetary policies. In the context of the crisis, this conditioned the relationship between the Portuguese state, the domestic banks and the ECB, which again informed the agency of each one of these.

The article is structured as follows. The first section reviews the competing interpretations of the crisis in the Eurozone. The second section discusses the relationship between structure and agency and forms of power with reference to finance. The fourth section shows how Portugal’s financial architecture was transformed in the context of monetary integration. The fifth section analyses how this architecture acquired new dynamics following the 2007–2008 crisis, in response to the ECB’s monetary policies and establishes the concept of a ‘triangular circuit of finance,’ which spanned the Portuguese state, the domestic banks, and the ECB. The sixth section accounts for the agency of the Portuguese banks, Bank of Portugal and the ECB in the run-up to the bailout. It shows that their agency was conditioned by the financial architecture associated with the EMU and the triangular circuit of finance. The last section concludes the article.

The crisis in the Eurozone

The most repeated explanation of the crisis in the Eurozone focuses on fiscal profligacy and national policy errors. Greece’s first Memorandum of Understanding highlighted that fiscal targets had consistently been missed despite a ‘benign economic environment’ and maintained that this was owed to ‘systematic overspending, endemic tax evasion and persistently overoptimistic tax projections’ (European Commission, 2010). In the Portuguese case, the IMF acknowledged ‘impressive’ progress and ‘significant overperformance’ in 2007 (IMF, 2008: 16–18; IMF, 2010), but concluded that ‘Portugal’s fiscal situation remains weak’ and that consolidation had to continue (IMF, 2008: 18; IMF, 2010: 27). It is this crisis diagnosis that provided the theoretical rationale for austerity and for a deepening of European fiscal integration through various post crisis treaties, which have tightened the European Union’s (EU) grip on member states’ fiscal policy. However, as the crisis evolved and spread to Eurozone countries with fiscal surpluses up until 2007 (Spain and Ireland), the private sector figured with increasing prominence in mainstream accounts (Mavroudeas, 2015). In Ireland, Spain and Portugal, the current account deficits had grown exponentially from the 1990s or early 2000s, but it was not driven by the public sector. This begged for an explanation for why private sector competitiveness had declined. Key to this was the development of unit labour costs (ULCs), i.e. the relationship between labour costs and productivity. The argument was that crisis ridden countries had lost competitiveness due to wages rising faster than productivity, and this translated into higher ULCs (European Central Bank, 2012: 6). In policy terms, this diagnosis served as a justification for the strategy of internal devaluation, which, in the absence of national currencies, sought to boost exports by squeezing nominal wages.

The heterodoxy rejects the idea that fiscal profligacy is the root cause of the crisis in the Eurozone and instead look to growing current account imbalances in the context of the euro (Arestis and Sawyer, 2011; Cesaratto, 2014; Frenkel, 2012; Lapavitsas et al., 2012). 2 Contrasting with methodologically nationalist interpretations, the heterodoxy emphasizes the economic relations between the Eurozone’s core and its periphery, through trade and finance. The imbalances resulted from the creation of the euro which led to the ‘ultimate fixing in the nominal exchange rate between countries’ (Arestis et al., 2013: 24). Core countries pursued an export-led growth strategy based on squeezing wages and keeping inflation low in pursuit of competitiveness whilst the opposite happened in the periphery. There, ULCs increased, and the net result was a real exchange appreciation which undermined competitiveness (Bellofiore et al., 2011; Cesaratto, 2014; Pérez-Caldentey and Vernengo, 2012). In both post-Keynesian and Marxist approaches, the trade surpluses of the core were channelled into the periphery though financial recycling, and this led to high levels of private indebtedness.

More pertinent to the question of crisis management are those approaches in economics that see the crisis in the Eurozone as a result of the EMU’s ‘imperfect institutional design’ (hereafter referred to as the ‘institutional design view’). The balance of payment view versus the institutional design view is a distinct debate within post-Keynesian economics, but there are nevertheless overlaps between the two positions (see, for example, Arestis and Sawyer, 2011; Arestis et al., 2013). The post-Keynesian institutional design view scrutinizes many of the EMU’s features that contributed to generating the Eurozone crisis and to the failure to resolve it. Implicit is that European integration is inherently desirable, that insufficient integration helped to generate the crisis, and that the solution is to integrate deeper and better. In a typical statement, Botta holds that (2012: 3–4) ‘The current eurozone crisis seems to have been decisively aided by the original institutional setup of the eurozone and its incomplete nature with respect to a fully developed federal union.’

The institutional design view stresses the tension between unified monetary policies and the lack of mechanism for fiscal transfers in the EMU, which makes it different from the USA. The EMU does not possess mechanisms for fiscal transfers between surplus and deficit countries and is therefore not a fully integrated monetary area. De Grauwe (2010: 3) highlights that the EMU is not ‘embedded in a political union’ and that there is an ‘imbalance between full centralization of monetary policy and the maintenance of almost all economic policy instruments … at the national level.’ Cesaratto (2014: 17) recommends that the EMU ‘move in the American direction – by obliging members to have balanced budgets, federalize existing debt, and creating a federal budget.’ In the context of the Eurozone crisis, it is held that Greece should have received (bilateral) fiscal transfers from other member countries, which could have reduced financial markets’ fear of sovereign default (De Grauwe, 2010).

The ECB is of central importance to the institutional design view. Arestis and Sawyer (2011: 23–24, 27–28) criticize the EMU’s one-size-fits-all monetary policy, which contributed directly to the current account imbalances. Furthermore, the ECB is based on the principle of central bank independence (CBI) where central banks cannot monetize governments and where there is a complete separation between monetary policy and fiscal policy. Its reliance on Northern American credit rating agencies, short of its own credit ratings, is another problem. De Grauwe’s (2010: 1–3) holds that the Eurozone crisis started when credit rating agencies went on a ‘frantic search’ for potential sovereign debt crises, and ‘sized upon Greece.’ Therefore, the ECB should stop relying on the outsourcing of risk evaluation and instead do this internally. The main critique of the ECB, however, is that it cannot, or does not take on the role of a lender of last resort (LOLR) vis-à-vis governments (Arestis et al., 2013: 25; Lavoie, 2015). Its construction is based on the efficient-market-hypothesis, which assumes that member states would not run into financial problems. When this turned out to be untrue, the lack of a LOLR contributed to aggravating the financial turmoil (Lavoie, 2015: 12, 16–17).

The institutional design view successfully identifies problems that fed directly into the Eurozone crisis and into the failure to resolve it. Despite this, it does not go far enough in capturing the EMU as a holistic entity that spans the national and the European level, that integrates various institutions within the world of finance, and that is historically specific to the internationalization of money under the euro. It analyses many separate problems with the EMU, and it seeks to find technical fixes, but in doing so, it overestimates the degree of solidarity between Eurozone member states (Cohen, 2012), and fails to capture the class dimensions of the European project, and of the monetary union in particular. It bypasses the question of whether the EMU’s design in fact concentrates power and serves the purpose of neoliberal restructuring rather than being a result of policy errors. An analysis that captures the historical distinctiveness of the EMU should address how monetary and financial integration transformed the social relations of production within member states. Contrasting with the post-Keynesian design view, the present article offers a Marxist analysis of monetary integration. It develops the notion of a ‘financial architecture’ rather than an ‘institutional design.’ The argument developed here is that European monetary integration transformed Portugal’s financial system through changes in property relations, modes of regulation, and the direction of financial flows, and that this amounted to a reconfiguration of the country’s financial architecture. There were strong class elements to this process, and this came to condition the political agency of institutions connected to finance capital both within and beyond Portugal in the context of the crisis in the Eurozone.

Structure and agency, forms of power

Portugal’s financial architecture can be understood as a ‘structure’ that shaped the political ‘agency’ of financial actors at the peak of the Eurozone crisis. Structure may be broadly defined as the ‘context … within which social, political and economic events occur and acquire meaning,’ whereas agency can be taken to mean ‘the ability or capacity of an actor to act consciously, and in so doing, to attempt to realize his or her intentions’ (Hay, 2002: 94). The relative emphasis on structure versus agency has important implications in terms of how power is understood. If structures determine agency, actors may, by implication be rendered powerless. As stated by Connor (2011), ‘if social structures are to provide the starting point for analysis and practice, there may be little justification for recognizing the agency of individuals.’ The either-or position, where either structure or agency shapes outcomes may have gone out of fashion. Indeed, Connor (2011) speaks of a ‘false dichotomy’ between structure and agency whilst Vadrot (2017) holds that the two are dialectically co-constituted. An attempt to transcend this dualism is made by Jessop in the strategic-relational approach, which sees the structure and agency as abstractions can be distinguished from one another at a theoretical level, but which are ‘interwoven’ in concrete contexts (Hay, 2002). Las Heras (2018) nevertheless holds that in this approach ‘power is meaningless because agency can always be “redefined” so that it is explained through structural determinations.’ Breaking with determinism, he insists that power relations are historically specific and connected to class, and he proposes to speak of ‘contingent action’ rather than structural necessities. In the field of entrepreneurial research, Ng (2018) holds that ‘rules … constrain as much as they enable the entrepreneur to create, reproduce and modify the rules of their embedded structure.’ Importantly, structures might be enablers and not just constraints. In the context of the present argument, the ‘structure’ at hand is the EMU as a ‘financial architecture’ and the flows of money that derive from the ECB’s monetary policy. The actors discussed are the financial institutions that pressured the Portuguese government to request a bailout (i.e. the domestic banks, the Bank of Portugal and the ECB). The purpose is not to conclude whether either structure or agency caused the bailout, but rather to interrogate the interconnection between the Eurosystem and the agency that unfolded at these various levels of finance, including the extent to which the former represented constraints or offered opportunities.

Closely related to the structure-agency debate is that on forms of power, particularly structural and instrumental power. This goes back to the Miliband-Poulantzas debate, which sought to advance hitherto underdeveloped Marxist theories of the state (Miliband, 1969; Poulantzas, 1969). In The State in Capitalist Society, Miliband analyses the concentration of power in the hands of giant corporations in advanced capitalist societies. His analysis of the state observes a close relationship between the holders of state power and the agents of private economic power, which he refers to as the ‘ruling class’ (Miliband, 1969: 55). He stresses the joint class background of businessmen and those who serve the state apparatus, the actual participation by members of the capitalist class in government and in the state apparatus and the ‘personal ties’ between the two (Miliband, 1969: 59; Poulantzas, 1969: 72). 3 This gives capital ‘instrumental’ power. Poulantzas (1969) criticizes him for a failure to conceptualize capital and the state as abstract categories. Instead, he understands capitalist classes and the state as objective structures and the social relations between them as an objective system of regular connections in which agents or people are, ‘in the words of Marx, “bearers”’ of such structures (Poulantzas, 1969: 70, italics in original). If there are overlaps of personnel between capital and the state, this is not what matters the most – since, the state has its own ‘specific internal unity,’ or logic, which unites its members. The state has ‘relative autonomy’ vis-à-vis the various fractions of capital, and according to Poulantzas (1969: 72–74) this better equips it to serve the interests of this class as a whole. These ideas lie at the origins of the notion of structural power.

In the recent literature, including on the power of finance, instrumental power refers to lobbying, campaign donations, the activities of organizations that represent businesses, and business’ privileged access to policy makers. Structural power reflects the fact that firms are ‘the agents of economic activity in capitalist democracies’ and to the ‘financial sector’s central position in the economy’ (Braun, 2018; Culpepper and Reinke, 2014). These are fairly general ideas. More pertinent to the present argument, Braun (2018) has developed the notion of infrastructural power, as a sub-type of structural power, to advance the analysis of the contemporary politics of finance in the Eurozone. He argues that finance possesses infrastructural power, which ‘stems from entanglements between specific financial markets and public-sector actors, such as treasuries and central banks, that govern by transacting in those markets’ (Braun, 2018). The concept is applied to analyse power in the realm of monetary policy, which is exercised by public monetary authorities (i.e. central banks) but relies on private financial markets for its implementation. The central argument is that state actors generate ‘infrastructural entanglements’ when they transact in financial markets and that this gives rise to a certain type of financial sector power. The two markets under consideration are repo and securitization markets, key sectors of market-based banking through which the ECB implements monetary policy. The notion of entanglements is central here, since it seeks to capture the nexus between the public and the private sphere, and in doing so, breaks with the widespread notion of a dichotomy between the state and the market and/or finance. Instead, the hybridity view states that ‘state and market actors form a hybrid public–private partnership’, or a ‘franchise system.’ The approach recognizes that state agency ‘is often market based’ in the sense that state actors are ‘not just regulators but also participants in financial markets’ (Braun, 2018).

The present analysis has similarities with Braun’s notions of finance’s infrastructural power and entanglements. A merit of the analysis is the way in which it captures the interconnectedness between state actors and financial markets. Not only banks, but states too are embedded in international financial markets. 4 In capturing this, it overcomes Weberian notions that see the state as emancipated from society. It also avoids assuming that state actors are uniform (indeed much like Miliband, 1969). The present article looks at how different actors in finance, including state actors, were materially entangled at the peak of the sovereign debt crisis. There are also some differences from Braun’s argument, which partly reflects the object of enquiry and research question at hand. While Braun (2018) applies the concepts of infrastructure and infrastructural power to the repo and the securitization markets, this article approaches the notion of a ‘financial architecture’ from the vantage point of an EMU member country. It nevertheless seeks to go beyond the nation state as a unit of analysis and to advance a class analysis. The notion of an architecture incorporates a whole series of public and private financial actors: the ECB, the Bank of Portugal, the IGCP, credit rating agencies, private banks and wholesale financial markets. Given Portugal’s asymmetrical integration into the EMU, it must necessarily place a great emphasis on the hierarchical nature of the Eurosystem. Finally, there is a difference with regards to the type of agency that is sought explained. Braun (2018: 2–3) writes that ‘state agency is often market based’ and that the ‘entanglement makes central bankers, who seek to maximize their economic steering capacity, dependent on bankers, giving the latter infrastructural power.’ This suggests a focus on agency in the general conduct of monetary policy. In contrast, the present article investigates agency in the form of a deliberate attempt to shape political outcomes, in the context of a ‘critical juncture’ (Braun, 2015).

Portugal’s financial architecture and the EMU

To advance a materialist analysis of Portugal’s historically specific financial architecture, which constitutes the ‘structure’ at hand in the present analysis, it is useful to borrow from Romão’s (1982) and Poulantzas’ analyses of economic integration. Romão’s (1982) distinguishes between ‘formal’ and ‘real’ integration. Formal integration refers to the legal-political forms of integration and includes memberships in economic organizations (Romão, 1982: 1089). This may include the European Economic Community (EEC), EU or EMU. Real integration, on the other hand, refers to the process of transnationalization of capital. It concerns the forms of capital reproduction and accumulation across national territories, which correspond to the needs of capital in a specific phase of capitalism. It includes the sphere of production and the sphere of circulation – i.e. it may concern processes such as the reorganization of production through foreign direct investments (FDI) or global value chains just as much as the internationalization of money and finance. The latter is arguably a defining feature of the present phase of capitalism. Real integration concerns the material dimension of economic integration and it is constituted by a re-articulation of social relations of production across national boundaries. Along these lines, Portugal’s integration with Europe can be analysed in terms of the ‘the internal articulations of the Portuguese economic structure and its insertion in the framework of international economic relations’ (Romão, 1982: 1087). This approach emphasizes class relations and seeks to transcend the nation state as a unit of analysis.

Furthermore, economic integration can be an asymmetrical process whereby social formations are unevenly integrated, and this manifests itself through power relations across and within such social formations. Poulantzas’ (1978) work provides insights into this and can add to the above insights on structural and infrastructural power. Analysing the relations of international domination that emerged in the aftermath of World War Two, he takes interest in the relations of domination within the metropolis itself, in the context of North American investments in Europe. He defines a dominated social formation as one where ‘the articulation of [the] specific economic, political and ideological structure expresses constitutive and asymmetrical relationships with one or more other social formations which enjoy a position of state power over it’ (Poulantzas, 1978: 43–44). He counters the view that domination and dependence play out as a conflict between ‘autonomous’ and ‘independent’ states and their national bourgeoisies. Instead, it inserts itself within the dominated countries: The [capitalist mode of production] no longer just dominates these formations from ‘outside’, by reproducing the relation of dependence, but rather establishes its dominance directly within them; the metropolitan mode of production reproduces itself, in a specific form, within the dominated and dependent formations themselves. (Poulantzas, 1978: 46)

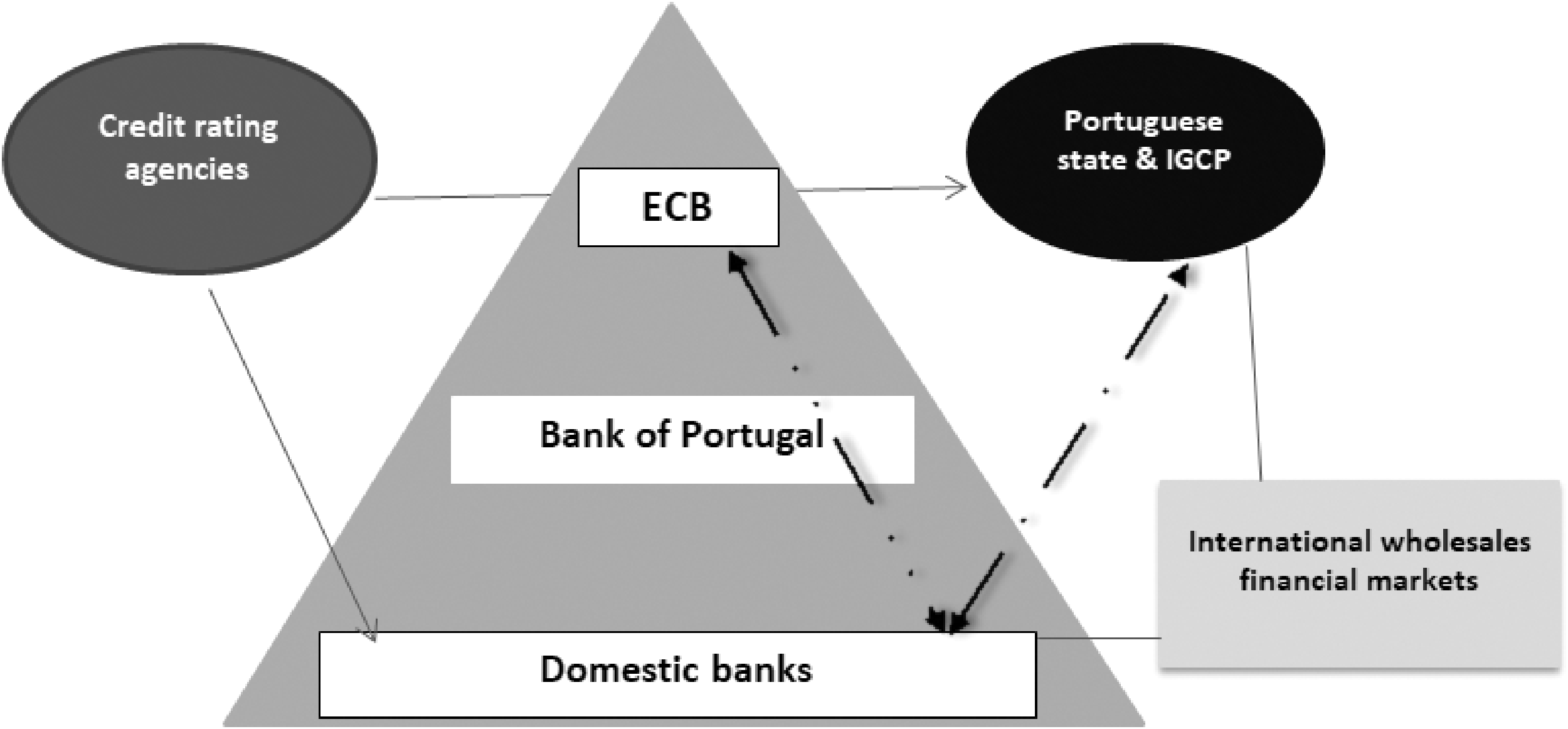

Under European monetary integration, Portugal’s financial system is inserted into a hierarchical international system – the Eurosystem. This architecture forms an entity that is historically specific and constituted by material relationships and forms of governance and regulation. Portugal’s ‘financial architecture’ incorporates various institutions within the world of finance, and it spans the Portuguese and the European level, as illustrated in Figure 1. It comprises entities that are domestic (the Bank of Portugal, IGCP and Portuguese banks), institutions from the EMU level (the ECB), and international entities that are not strictly speaking European (international credit rating agencies and international wholesales financial markets). This architecture is different from Portugal’s former financial architecture. When Portugal entered the EEC in 1986, the financial architecture inherited from the Carnation Revolution was largely intact (Pinho, 1997: 3). That architecture was characterized by state ownership of the banking system, central bank coordination of credit allocation and a series of mechanisms that channelled financial flows towards the needs of the state, at a low cost (Noronha, 2013; Rodrigues et al., 2016: 8). 5 From the mid-1980s, it was profoundly transformed – indeed, it was dismantled within a decade.

Portugal’s architecture of finance under the EMU.

With the creation of the EMU, the Bank of Portugal became part of the European System of Central Banks (Figure 1). There was a hierarchical element to it since it was made subordinate to the ECB and monetary autonomy was lost. Capital movements were liberalized from 1986 onwards (Antão et al., 2009) and this opened the possibility for a deeper ‘real’ integration through the sphere of finance. Lei Bancaria of 1992 introduced many of the elements of the Single Market Programme Directives (Pinho, 1997: 15). Portugal deregulated interest rates and adopted the First and Second European Banking Directive in 1992 (Pérez-Caldentey and Vernengo, 2012: 11). There was a shift in ownership, since privatization was ‘important in showing the neoliberal commitment of the Portuguese political elites to both a market-driven European integration,’ and since the income generated was used to comply with the Maastricht criteria (Rodrigues and Reis, 2012: 196). Three constitutional revisions opened for a privatization of banking (Rosa, 2014). The first private banks were set up in 1984 and 1985 and they ‘prospered’ (Antão et al., 2009: 428). With the implementation of the Second Banking Directive, barriers to entry for new banks were lifted once and for all (Pinho, 1997: 4–5).

Financial liberalization also involved a qualitative shift in the public debt regime which also forms part of Portugal’s financial architecture (Figure 1). The dismantling of the post-Revolutionary financial system went hand in hand with a state-led effort to create a market for public debt (Rodrigues et al., 2016). This came to reshape the interconnection, or the ‘entanglement’ between state actors and financial markets. From a mainstream perspective, the Portuguese financial system was repressed. The reserve requirements and cheap financing of public debt represented a ‘distortion’ and an ‘implicit taxation’ on the banking system (Antão et al., 2009: 419). A Treasury bill market was set up in 1985, and this was ‘the starting point for a public debt market’ (Antão et al., 2009: 422). Its prominence grew quickly, with the outstanding value increasing from 3.5% to 13% of GDP between 1985 and 1987 (Antão et al., 2009: 422). As part of CBI, which was enshrined in the convergence criteria (Arestis and Sawyer, 2011: 27), government monetary financing by the Bank of Portugal was banned (Antão et al., 2009: 26). The rates of compulsory reserves were reduced from 17% to 2% of total deposits between 1989 and 1994 (Pinho, 1997: 13; Rodrigues et al., 2016: 488) and with their subsequent release by the Bank of Portugal, an equivalent of 12% of GDP were transferred to the banks in the form of public debt titles (Antão et al., 2009: 427; Rodrigues et al., 2016: 9), thus benefiting the emerging finance capital. The liberalization of interest rates opened the door for public debt to become a potentially profitable asset. In the context of the EMU, the sovereign debt market was opened to foreign investors, paving the way for an internationalization of the creditors to the state. By 2008, 80% of Portugal’s public debt was held by foreign creditors, thus it was heavily reliant on foreign funding (Rodrigues et al., 2016: 494; Santos et al., 2018: 477). Finally, the creation of the euro was accompanied by the attempt to create a single financial space and a vision of a pan-European repo market was an important part of this. Sovereign debt played a central role. The ECB used its collateral framework to ensure that all sovereign debt within the Eurozone would face the same terms when used as collateral – facilitating the free movement of cash and collateral across borders. The ‘Europeanization of sovereign collateral’ implied the creation of a large amount of liquid collateral out of assets that had previously been illiquid (Gabor and Ban, 2016). The ECB gave private credit rating agencies the task of evaluating the collateral eligibility of sovereign debt in 2005 (Braun, 2018: 4), and thereby incorporated them into the financial architecture. Portuguese sovereign debt is structurally connected to wholesales financial markets through the repo markets, since government bonds are used as collateral in most transactions (Gabor, 2016; Gabor and Ban, 2016). That is, the Portuguese state is embedded in international financial markets (Figure 1). By the same token, it is also inserted into a financial architecture that is historically specific to the internationalization of money and finance. This forms part of the broader social relations which constitute Portugal’s articulation within the European project.

A triangular circuit of finance: The ECB, the banks and the Portuguese state

In addition to these historical particularities, the turbulence on international financial markets in 2008 and the ECB’s monetary policies brought about temporary dynamics to Portugal’s financial architecture. These temporary dynamics formed part of the structure that framed the agency of financial players in the run-up to the bailout. As banks in Portugal and elsewhere in the Eurozone faced trouble accessing wholesales financial markets, the ECB implemented a series of measures to channel liquidity into the banking system (Rodríguez and Carrasco, 2014: 9; Wolff, 2014). This acquired political importance in a second stage of the crisis, when the Portuguese state was excluded from international financial markets. Several credit rating agencies downgraded Portuguese sovereign debt the summer of 2010 (Freire and Santana-Pereira, 2012: 180) and after the rejection of SGP-4 (Fitch Ratings, 2011; Oakley et al., 2011). Bond yields rose and foreign investors increasingly withdrew (Bank of Portugal, 2011: 11). In this context, the ECB’s monetary policies came to condition the relationship between domestic banks, the Portuguese state and the ECB itself. By the announcement of the rescue package, a ‘triangular circuit of finance’ had emerged. This circuit involved the Portuguese banks, the state and the ECB. The ECB channelled liquidity into Portuguese banks; the banks channelled liquidity into the state through sovereign bond purchases; the state was dependent on the domestic banks for the issuance of public debt; and sovereign debt was deposited as collateral at the ECB in exchange for more liquidity. Thus, there was an alteration in the modality of articulation and in the form of entanglement between various financial players, including the public and private, at the peak of the crisis. This aspect of a financial architecture is not accounted for by the institutional design view. By the spring of 2011, both the Portuguese state and the banks were dependent on the ECB’s liquidity operations, and this informed the political agency that unfolded.

The triangular circuit of finance was not simply a product of spontaneous market mechanisms. Instead it reflected the ECB’s crisis policies. As banks in the Eurozone faced problems accessing international wholesales markets, the ECB came to play an important role in ensuring bank liquidity (Bank of Portugal, 2011; Wolff, 2014). The ECB initially refused to intervene directly in government debt markets and assistance took the form of refinancing operations (Gabor, 2014). With the ‘acute banking crisis,’ trillions of euros were pumped into banks when the ECB extended its lending through the main refinancing operation (MRO) and the launch of several programmes under the umbrella of long-term refinancing operations (LTRO) from November 2008 onwards (Rodríguez and Carrasco, 2014: 9; Wolff, 2014). An increasingly significant share went to peripheral Eurozone countries, including Portuguese banks (Wolff, 2014: 6–7).

The ECB’s monetary policies strongly incentivized banks’ purchase of sovereign debt. Reflecting this was a ‘carry trade’ whereby Portuguese banks recycled ECB liquidity into sovereign debt and deposited the latter as collateral at the ECB in exchange for more liquidity (Bank of Portugal, 2011: 11). An essential part of the ECB’s monetary policy in the context of the crisis was its collateral policy (Wolff, 2014). The main components of collateral policy are the definition of which assets are eligible as collateral, which credit rating is required for the assets to be used as collateral, and the size of the haircuts in relation to the market value of the assets. The ECB allows a broad range of assets to be applied as collateral (Gabor and Ban, 2016: 626; Pinho, 2015; Wolff, 2014: 4). This includes several types of debt instruments (issued by central governments, central banks, other public institutions, supranational institutions, credit institutions and corporations and asset backed securities). For the evaluation of the creditworthiness of such assets, the ECB relies on the risk evaluations of four credit rating agencies: S&P, Moody’s, Fitch and DBRS (European Central Bank, 2016).

To facilitate a transfer of liquidity into European banks, the ECB made changes with regards to the assets that qualified as collateral (Bank of Portugal, 2009b: 327; Wolff, 2014: 4). In October 2008, the minimum rating required for assets to be eligible collateral (except ABS) was reduced from A- to BBB- (Bank of Portugal, 2009b: 333; De Grauwe, 2010: 2; Wolff, 2014: 5). This included sovereign debt. When rating agencies progressively downgraded peripheral sovereign debt, banks could nevertheless continue to use this as collateral to access ECB liquidity. Given that the Eurosystem has a single framework for eligible collateral (the ‘Single List’ as of 2007), the changes applied to MRO as well as LTRO (Wolff, 2014), and Portuguese banks would have benefited regardless of which of the refinancing programmes they made use of.

A further change to the collateral policies concerned the haircuts. This alteration made sovereign debt a particularly attractive asset from the perspective of the banks. The ECB’s acceptance of assets with a lower credit rating represented a higher degree of risk, and to compensate for this, it applied larger haircuts. Consequently, less liquidity was allocated for a given amount of assets. For example, uncovered bank bonds with a low credit rating saw the haircuts increase from approximately 15% to almost 40% in 2010, whereas highly rated ABS saw an increase from approximately 5% to 16%. The haircuts applied to government bonds, on the other hand, were only modified marginally. Until 2013, the haircut for highly rated government debt with five to seven years maturity was 3%. For lower-rated government bonds with the same maturity it was 5% until January 2011 and 8% thereafter, until July 2013 (Gabor and Ban, 2016: 629; Wolff, 2014: 4–5). 6 This meant that banks could access more ECB liquidity if they deposited public debt as collateral than if they used other assets. In fact, it was a strong incentive. Sovereign debt gave the banks access to more ECB liquidity than other assets gave. Consequently, a carry trade developed whereby banks profited enormously from the spread between the low rate charged by the ECB and the high bond yields on public debt (Pinho, 2015).

Portuguese banks became increasingly dependent on financing from the ECB from 2008 onwards. The recourse to Eurosystem refinancing operations by Portuguese institutions multiplied by almost six times between 2007 and 2008, when the average daily balance of refinancing reached €3,888 million. It reached an historical high on 31 December when the balance of resident institutions stood at €10,210 million. MROs were widely used, as the ECB set a fixed interest rate on an unlimited amount of liquidity, but Portuguese banks took use of LTRO too. Participation in MRO intensified significantly from October 2008, and the average balance in this scheme increased to €1,005 million, up from €189 million in 2007. For LTRO operations with three months’ maturity, the daily average balance of resident institutions increased from €525 million in 2007 to €2,257 million in 2008 (Bank of Portugal, 2009b: 331–332). From the first half of 2010, there was again a sharp increase in the ECB financing of Portuguese banks. The Portuguese banking system continued to be in expansion between December 2009 and December 2010, and a main driver behind this was the profitable enterprise whereby banks invested in public debt and recycled this at the ECB (Bank of Portugal, 2011: 44). By 2011, after successive downgrades of the sovereign and bank debt, and with the banks’ exclusion from wholesale financial markets, Portuguese banks continued to rely on the ECB for liquidity (Bank of Portugal, 2011: 45, 63; Pinho, 2015).

The carry trade that developed became a phenomenon in various Eurozone countries, including Spain, Italy, Germany, Belgium, Luxemburg, Malta and Portugal (European Systemic Risk Board, 2015: 73). The institutional design view has not taken on board the extent to which this carry trade represented a shift in the Eurozone’s design. The phenomenon has mainly been analysed by mainstream economics, which speak of a ‘doom loop,’ ‘feedback loop,’ ‘deadly embrace’ or a ‘diabolic loop’ between banks and the state (Erce, 2015; Farhi and Tirole, 2018). While these concepts capture the economic intimacy between the state and finance, many studies neglect the ECB’s role. It is essential to note that the relationship was in fact triangular, involving the ECB, and went beyond a ‘mutual embrace.’ It involved a shift in the modality of articulation of the Portuguese state and banks within the EMU. It temporarily deepened Portugal’s real integration within the EMU, but more importantly, it changed the form of integration and of entanglements. It represented an alteration of the social structures and state structures within the Portuguese social formation – thus it constituted an example of how domination plays out through an insertion within the dominated formations (Poulantzas, 1978). At the peak of the Eurozone crisis there was a temporary alteration in the financial architecture. The ECB was in the position to force the Portuguese state into default, and this had strong implications for the political agency of finance in the critical juncture of the spring 2011.

The political agency of the ECB, Banco de Portugal and the domestic banks

The role of finance in triggering the rescue package can best be understood with reference to Portugal’s financial architecture and the triangular circuit of finance. These constituted a structure that framed the agency of a series of financial players. At stake prior to the bailout was the Portuguese state’s ability to issue public debt (Castro-Caldas, 2014). While the banks were the first to be excluded from international financial markets, the state was next in line. To roll over existing debt, it was dependent on selling Portuguese government bonds (PGPs) and Treasury bills (T-bills). Facing repayments of over €9.5 billion between April and June 2011 (Instituto de Gestão de Tesouraria e do Crédito Público, 2011: 2), the inability to access open markets could in the worst case provoke a sovereign default. Reflecting the articulation of the Portuguese financial system within the EMU, the political agency among financial institutions spanned the Portuguese and the European level, and it included Portugal’s domestic banks – as creditors to the state, the Bank of Portugal and the ECB. There was a strong degree of coordination between these three levels, reflecting their material interconnection in the context of the triangular circuit of finance.

On 1 April, the Portuguese Debt Management Office IGCP held a first debt auction since the collapse of the government (Oakley and Wise, 2011). It was an ‘extraordinary’ auction, which had not been pre-scheduled by the IGCP and the Ministry of Finance (Oakley and Wise, 2011; Pinho, 2015; TVi, 2011). Portugal raised €1,645 billion through the sale of PGBs with 15 months’ maturity at an average interest rate of 5.79% (Instituto de Gestão de Tesouraria e do Crédito Público 2011a: 1; Oakley and Wise, 2011). Demand for the bonds was 1.4 times higher than the amount on offer and it was described as a ‘success’ (Oakley and Wise, 2011). The Ministry of Finance evaluated it positively considering the ‘politically and economically difficult situation’ and said they would continue to issue public debt (TVi, 2011). The day before this, on 31 March, the PSD sent a letter to the prime minister and the president to argue in favour of a bailout. On 1 April, the Bank of Portugal sent a letter to the same recipients, with the same message, and it was signed by the governor (Moury and Standring, 2017: 668). This conscious action had a clear intention (Hay, 2002: 94) that was inherently political, and this stands out as a contradiction with the principle of CBI.

On 4 April, the Bank of Portugal held a meeting with the most important domestic banks in the country. The central bank governor, Carlos Costa, advised the CEOs of the banks that ‘[y]ou cannot continue to finance [the emissions of Portuguese public debt]’ since ‘[t]he risk is that the banks will go under, that is, the healthy part, whilst it is the Republic that created the problems’ (Pena, 2014: 15). This statement alluded to the dominant narrative at the time, that it was the fiscally profligate state that had caused the crisis, and that the banks should be cautious, since a default by the state could lead to the failure of the banks. His message was echoed by the Bank of Portugal’s Financial Stability Report of May 2011 which stated that ‘the banking system’s exposure [to sovereign debt] is not immune to potential losses deriving from the negative assessments of financial markets players and rating agencies and should be gradually reduced under the deleveraging process in the financial system’ (Bank of Portugal, 2011: 11). Both recommended that domestic banks reduce their exposure to Portuguese public debt, but while the report promoted a gradual adjustment, the head of the central bank encouraged a more abrupt change in investment behaviour. Without access to the markets, the state could default or be compelled to request a bailout to avoid defaulting.

Subsequently, the presidents of Portugal’s four most important banks appeared in the national press and pledged for a bailout. A well-known reporter, Judite de Sousa, held a series of TV interviews between 4 April 2011 and 7 April 2011 (Lains, 2013: 2). This included the CEO of Millennium BCP, Carlos Santos Ferreira, BES’s CEO Ricardo Salgado, Fernando Ulrich of BPI and Santander Totta’s CEO Nuno Amado. The bankers agreed that Portugal had to request assistance (Castro-Caldas, 2014). The CEOs warned that the banks could no longer continue to finance public debt and announced that there was no alternative to a bailout (Ferreira, 2011a; Pena, 2014: 15). Carlos Santos Ferreira was the first to proclaim it to be ‘indispensable that the country seeks a short-term loan’ (Tavares and Bugge, 2011). He recommended that Portugal should urgently request assistance from the European Stabilization Fund and the IMF, maintaining that a bridging loan of minimum €10 billion was necessary. He held that ‘[w]ith the worsening of the economic situation, with the interest rates reaching historical records, and with rating agencies successively lowering the rating of the banks, it is imperative to listen to the key players of the Portuguese banking sector’ (Ferreira, 2011a). Ricardo Salgado, the chairman of BES, defended the same position (Ferreira, 2011b; TSF Rádio Notícias, 2011) and said that ‘the banks are losing out’ because they are lending to the state, and that ‘they cannot concede any more credit under the current circumstances’ (TSF Rádio Notícias, 2011). The chairman said that the banks had ‘always been at the market, helping the state-owned-firms and the state, but that due to the worsening of the ratings, the banks have to reconsider their situation’ (TSF Rádio Notícias, 2011). Salgado insisted that Portugal should request interim assistance from Brussels and repeated that this was ‘imperative’ in order to ‘neutralize’ the effects of the rapid increase in interest rates and to ‘calm down’ the markets as well as the Portuguese (Inácio, 2011; TSF Rádio Notícias, 2011). The President of the Portuguese Banking Association (APB), Antonio de Sousa, echoed this message. He made it clear that it was ‘urgent’ to ask for assistance from Europe, because the banks did ‘not have any more credit to give’ (Agência Lusa, 2011). Portuguese finance capital was united in the message that the country should seek a bailout.

The bailout was announced on 6 April following the second debt auction after the collapse of the government. This was two days after the meeting between the domestic banks and the Bank of Portugal and immediately after the banks’ CEOs appeared on TV. Unlike the auction on 1 April, this was an auction of T-bills. Whilst bond auctions have a maturity of above 18 months and tend to be dominated by foreign investors, T-bills have shorter maturities and tend to be dominated by domestic players (Moreira Rato, 2015). It was a ‘double auction’ of T-bills worth €1,005 million, €455 million of which had a twelve months maturity and €550 of which had a six months maturity (Agência Lusa, 2011). The bills had an interest rate of 5.9% and 5.1% respectively (Agência Lusa, 2011; Instituto de Gestão de Tesouraria e do Crédito Público, 2011: 1). Only €100 million were purchased by foreign creditors, and public entities and domestic banks bought the rest (Jorge, 2014: 22). Despite the bankers’ pledge to stop buying Portuguese public debt, they stepped in and bought it after all. The debt auction was nevertheless portrayed as a sign that Portugal was ‘outside of the markets’ (Jorge, 2014: 22). Hours after the auction, the minister of finance, Fernando Teixeira dos Santos, announced the bailout in an email to the business newspaper Journal de Negócios. He did so without the prime minister's consent: The country was irresponsibly pushed into a very difficult situation on the financial markets. Faced with this difficult situation, which could have been avoided, I understand it to be necessary to resort to the financing mechanisms that are available in the European framework. (Agência Lusa, 2011; Garrido, 2011; Jorge, 2014: 22; Mundy, 2011)

While the above chronology of events points to financial institutions within Portugal – notably the central bank and the domestic banks, as players that pushed for the bailout, the political agency spanned all the way to the European level, reflecting Portugal’s financial architecture. It is well known that the ECB pressured Ireland into a bailout in 2010 (Castro-Caldas 2014). The Irish bailout came only months before the Portuguese, when the ECB threatened to stop the liquidity going into Irish banks. Beyond media reports about various forms of pressures vis-à-vis Irish ministers (Bardon, 2015; Telegraph, 2015), in 2014 it became publicly known that the ECB sent a letter explicitly threatening to cut off the provision of Emergency Liquidity Assistance to the Irish banks if the government did not immediately apply for a bailout and commit to ‘undertake decisive actions in the areas of fiscal consolidation, structural reforms and financial sector restructuring’ (European Central Bank, 2014; The Economist, 2015; Taylor, 2014). Notwithstanding the ECB’s commitment to the principle of CBI (Draghi, 2018), the institution dictated the undertaking of neoliberal policy reform in Ireland. The ECB has subsequently published the correspondence between Jean-Claude Trichet and the Irish finance minister, and its role in provoking the Irish bailout is an undisputed fact (European Central Bank, 2014).

A number of statements by key players indicate that the ECB was a protagonist also in the Portuguese case (Castro-Caldas, 2014), but in a more obscure way. Soon after the bailout announcement, it emerged that the ECB, together with the Bank of Portugal, played a role in coordinating the Portuguese banks. APB president António de Sousa clarified the position taken by the bankers when they declared that they would not continue to purchase public debt. As a representative of Portuguese finance capital, he pointed his finger at the ECB: ‘When it became clear that state financing needs implied more funding by banks, banks said this could not be done because they had clear instructions from the Bank of Portugal and ECB to do the opposite, to diminish their exposure and not increase it’ (Castro-Caldas, 2014; Khalip, 2011; Público, 2011). The cycle of financing between the banks, the ECB and the Portuguese state could not continue any further, and according to De Sousa, it was the ECB and the Bank of Portugal that had made this decision: ‘Banks did not want to create an additional problem for the state, but they have been warning that the model could not keep working … In order to lend to the state, banks had to ask for money from the ECB, and that triangulation mechanism has reached its limits according to the ECB and the Bank of Portugal’ (Khalip, 2011).

When de Sousa was quoted in the Financial Times the following day, he explicitly placed the responsibility for the bailout on the ECB rather than on Portuguese banks. According to Financial Times, De Sousa said that the ECB pressed the country’s lenders to stop increasing their use of its liquidity, ‘setting in train events that led Lisbon to ask for a bail-out’ (Wise et al., 2011). His view of the causal mechanisms at work could not be clearer. The statement can plausibly be interpreted as an acknowledgement that it was in fact the threats by the bankers to stop financing the state that triggered the bailout. Furthermore, De Sousa said that the ‘message from the ECB and Portugal’s central bank not to expand their exposure to ECB funding came a month ago,’ and that the ‘main reason for the banks’ heightened exposure was linked to their financing of public sector and government debt.’ De Sousa explained that ‘the instruction led them to conclude [that] they could not increase their exposure to state debt.’ He noted that they ‘didn’t say that we couldn’t do x or y, but they were very clear about the message’ (Wise et al., 2011).

The president of the ECB, Jean-Claude Trichet, fiercely denied De Sousa’s narrative, and held that ‘We didn’t force the banks to do anything. We didn’t force the government or the authorities in general … to do anything’ (Wise et al., 2011). Trichet’s denial may have reflected the ECB’s fears of criticism after a political backlash after having forced Dublin to accept a bailout the year before. After Trichet had spoken, the head of APB withdrew his initial statements. De Sousa’s new position was that ‘there were no guidelines whatsoever from the Bank of Portugal, nor from the ECB of course, in the sense that the Portuguese banks should not continue acquiring national public debt’ (Castro-Caldas, 2014; Jornal de Negócios, 2011a). This reflected a 180-degree turnaround with regards to his narrative about the role of ECB and the Bank of Portugal in triggering the Portuguese bailout.

It is not clear exactly how urgent the Portuguese bailout was, or indeed if it was necessary (Lains, 2015). There was always an alternative in the sense that the government could have defaulted, which has been common across countries and throughout history (Reinhart and Rogoff, 2008). Disregarding this option, there was a consensus in the international financial press that the Portuguese state was able to honour its debt obligations in April, although there was less certainty around debt maturing in June (Mundy, 2011). The Financial Times (FT) immediate reaction to the bailout announcement was to publish an editorial piece titled ‘Banks 1 – Portugal 0’. It argued that ‘Another Eurozone country has been humbled by its banks’ (Financial Times, 2011) and suggested that Portugal should have delayed the bailout until after the elections in June. It held that ‘[u]ntil now, the government had appeared to be holding its ground’ and that ‘Lisbon should have stuck to its position’ (Financial Times, 2011). The FT highlighted that Portugal could still afford to postpone a bailout and that the interest rates were not unaffordable (Financial Times, 2011; cf. Lains, 2015).

Notwithstanding this, there can be little doubt that finance capital played an essential role in triggering the Portuguese bailout and that their agency was intrinsically interconnected to Portugal’s modality of articulation within the EMU and its form of entanglements. The sovereign debt crisis itself reflected this architecture, since the issuance of public debt on open financial markets acquired a new centrality in the historical context of monetary integration. It was aggravated by the fact that the ECB could not or would not act as LOLR vis-à-vis governments. Concerning the agency behind the bailout, it appeared like the Portuguese banks had the power to force the government to request a rescue package, but this was a mere surface phenomenon. They did indeed exercise an unusual degree of ‘instrumental power,’ but the reason why this immediately shaped Portugal’s policy direction was because of finance’s ‘structural power’ given the configuration of social relations that had emerged at the peak of the crisis. To conclude that the power rested in the bankers’ hands would be to ignore the structures in which they were operating. The ECB, the Bank of Portugal and the domestic banks were all drivers of the bailout, and consequently of the neoliberal adjustment. There was an intrinsic interconnection between their agency, and this was a political expression of their material and regulatory interconnection through the financial architecture and the triangular circuit. The latter constituted the ‘structure’ in which they acted, a structure which equipped them with a peculiar form of structural power. This power did not reflect the centrality of finance in the economy in general terms, but something much more specific – namely the modality of their interconnection at this moment in time. This should not lead to a determinist conclusion whereby the structure provided by the Eurosystem determined their agency and the subsequent political outcome. However, the monetary policies implemented in the ‘explosive’ phase of the crisis (Braun, 2015) did generate a logic that favoured a coherent set of behaviours by multiple actors whose agency provoked the bailout.

Drawing upon Romão’s (1982) notion of ‘real’ integration, the triangular circuit represented a temporary alteration in the internal articulation of the Portuguese social structure and its insertion within the EMU. This alteration was constituted by a shift in social relations within Portugal, but the relations extended beyond national boundaries. The ECB helped to bring about the doom loop, tightening the economic relationship of interdependence between the Portuguese state and the banks, as creditors to the state. The two were financially interlocked within the EMU, and the ECB was in a position to cut off bank liquidity and to force the state into default. The agency of the banks, i.e. the pressure they put on the government to request a bailout, reflected their material articulation within the EMU, through the triangular circuit. The ECB had incentivized the banks’ investments in public debt, but as the rating agencies downgraded Portuguese sovereign debt, the ECB implemented larger and larger haircuts, reducing the liquidity to the banks (Pinho, 2015). Only assistance could solve the problem of bank liquidity (Bank of Portugal, 2011: 63; Moutinho, 2011). This was well captured in the Bank of Portugal’s Financial Stability Report from May 2011: In March the situation in Portugal registered a significant and rapid deterioration, in a context of political instability. … The rating agencies successively downgraded their ratings on the Portuguese state, as well as on the banks and several non-financial corporations. These developments heightened the pressures on the capacity to issue sovereign debt, as well as on Portuguese banks’ access to financing from the international wholesale debt markets, given that these downgrades had a negative effect on the valuation of assets eligible as collateral for credit operations with the Eurosystem. (Bank of Portugal, 2011: 20) The Governing Council of the European Central Bank (ECB) has decided to suspend the application of the minimum credit rating threshold in the collateral eligibility requirements for the purposes of the Eurosystem’s credit operations in the case of marketable debt instruments issued or guaranteed by the Portuguese government. This suspension will be maintained until further notice. … The suspension applies to all outstanding and new marketable debt instruments issued or guaranteed by the Portuguese government. (European Central Bank, 2011) The Portuguese government has approved an economic and financial adjustment programme, which has been negotiated with the European Commission, in liaison with the ECB, and the International Monetary Fund. The Governing Council has assessed the programme and considers it to be appropriate. This positive assessment and the strong commitment of the Portuguese government to fully implement the programme are the basis, also from a risk management perspective, for the suspension announced herewith. (European Central Bank, 2011)

Conclusion

This article has advanced a materialist analysis of monetary integration and its manifestations at the peak of the sovereign debt crisis in Portugal. It has stressed the political agency of finance and crisis management as factors that were constitutive of that crisis. The euro is already at the heart of the debates about the crisis in the Eurozone. The present article has added to the literature on the Eurozone’s imbalances and critically engaged with the literature on the monetary union’s flawed institutional design. The institutional design view has identified problems with the EMU that fed into various failures to address the crisis once it erupted. Yet, in the hope of finding institutional fixes to the Eurozone’s woes, it fails to analyse how the EMU constitutes an entity which spans the national and European level, and which informs political agency. Drawing on Marxist political economy, this article proposed an alternative framework. It stressed that monetary integration was constituted by a material reconfiguration of finance. In doing so, it constructed a historically specific analysis of Portugal’s financial architecture. This architecture incorporates institutions within and beyond Portugal, including the ECB, the Bank of Portugal, the Portuguese debt management office, credit rating agencies and domestic banks. Furthermore, the article argued that the financial architecture under the euro is not static. On the contrary, it acquired dynamics that were specific to the moment of the crisis. As the ECB pumped liquidity into the Eurozone’s banks, it simultaneously generated a triangular circuit of finance and an intimate relationship of interdependence between the Portuguese state and the banks.

Against this theoretical and historical backdrop, the article provided an empirical answer to the question of how Portuguese authorities were compelled to request a bailout from the IMF, ECB and the EC in 2011. Based on reports in the Portuguese media and in the international financial press, the article assembled a detailed chronology of events and an overview of the political agency of a series of players within finance. The analysis was also informed by material published by the ECB, the Bank of Portugal and the IGCP, and by a selection of interviews. The article showed that the Portuguese banks pushed fiercely for the bailout. In fact, they triggered it. Importantly however, the ECB and the Bank of Portugal played a coordinating role. The synchronization between these three levels reflected the triangular circuit of finance which resulted from the ECB’s monetary policies. The ECB was in a position to cut off liquidity from both the banks and the state and to force the latter into default, and this had important implications for the power dynamics at work. The Portuguese rescue package created winners and losers, and amongst domestic elites and capitalist classes, a series of actors wished to see an accelerated neoliberal restructuring. For these actors, the crisis represented an opportunity for change.

In sum, European monetary integration entailed a set of material relations in which the various levels of finance - the European and the national - were materially interlocked in ways that allowed them to trigger a bailout, and consequently a neoliberal adjustment programme. These insights should be taken into consideration in ongoing attempts to rethink monetary policy in the Eurozone’s periphery. While the Portuguese case provides an intricate story of how internal and European financial players interacted, similar dynamics were at work in Ireland and in Greece. These cases illustrate the far from subtle ways in which the ECB’ monetary policy can place constraints on national policy space. The ECB’s ultra-easy monetary policies after the most explosive phase of the crisis have again altered the dynamics of EMU member countries’ financial architecture. The pressure on sovereign debt was generally alleviated and Eurozone banks’ overall exposure to public debt decreased (Allen, 2019). This article has not even begun to address this. Yet, given public debt management agencies’ continued embeddedness in wholesales financial markets, and given the ECB’s reliance on the outsourcing of risk assessment to credit rating agencies, it seems likely that similar dynamics could re-emerge in the future, short of these unprecedentedly loose monetary policies.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.