Abstract

How to finance the Green Transition toward net-zero carbon emissions remains an open question. The literature either operates within a market-failure paradigm that calls for carbon taxes or cap-and-trade to help markets correct themselves, or via war finance analogies that offer a “triad” of state intervention possibilities: taxation, treasury borrowing, and central bank money creation. These frameworks often lack a thorough conceptualization of endogenous credit money creation and disregard the systemic and procedural dimensions of financing the Green Transition. We propose “Monetary Architecture” as a more comprehensive framework that perceives the monetary and financial system as a constantly evolving and historically specific hierarchical web of interlocking balance sheets. Using the United States as a case study, we stress the importance of a systemic financing dimension that uses all available elasticity space in the monetary architecture while considering a division of labor between firefighting balance sheets such as central banks or treasuries and workhorse balance sheets such as off-balance-sheet fiscal agencies or shadow banks. Procedurally, public workhorses should provide an initial balance sheet expansion and crowd in the rest of the monetary architecture, notably shadow banks, for long-term funding. Firefighters should prevent systemic instability and manage a possible final contraction.

Keywords

Introduction

The Green Transition—an economic and industrial restructuring to net-zero carbon emissions—dominates discussions in the public sphere. Governments throughout the world are increasingly run by politicians with mandates to rebuild pandemic-stricken economies in a climate-conscious fashion and to construct policies compatible with the Paris Agreement to which most have signed up. The challenge is immense, and the costs are proportionate to it. The price tag for a global transition to net-zero may amount to as much as $73 trillion (Jacobson et al., 2019), although costs of $30–$60 trillion have been suggested for the US only (Energy Transitions Commission, 2020). Either way, a large part of the capital stock will have to be renewed within a generation—for instance in the fields of housing, transportation, infrastructure, agriculture, industry, and energy. This will entail mobilizing vast amounts of finance, previously seen only during periods of massive societal transformations. The latest IPCC report states that “financial flows are a factor of three to six times lower than levels needed by 2030 to limit warming to below 2°C” (IPCC, 2022).

For a long time, the dominant framework has been to see carbon emissions as an externality—a form of market failure—that is not adequately priced in an otherwise efficient economic system (Pearce, 1989; Stavins, 1988). The policy prescriptions stemming from this framework focus on market-correcting (e.g. carbon taxes) or market-creating (e.g. cap-and-trade) strategies that would “internalize” this externality (Liu et al., 2019). The first is the world of Pigou where a penalty on carbon emissions incentivizes firms and individuals to switch to lower carbon alternatives, while the second is the world of Coase where total allowable emissions are set in advance and permits to pollute are either allocated or auctioned to firms. This way, carbon emissions are supposed to acquire a price and be internalized in markets. There is broad agreement that some level of carbon pricing would be useful for accelerating the move to a low carbon economy (Stiglitz et al., 2017). However, warnings have also been issued that carbon pricing will not trigger sufficient private sector investments to bring about the Green Transition (Lilliestam et al., 2021), and that the political road to achieving a meaningful level at global scale is arduous (Le Billon and Kristoffersen, 2020), not least due to detrimental distributional effects, with carbon pricing initiatives so far stuck at covering only about a fifth of global greenhouse gas emissions (World Bank, 2021).

Beyond the market failure paradigm, another strand of literature addresses what the role of states may be in financing the Green Transition and often draws on war finance analogies (Malm, 2020; Nersisyan and Wray, 2019) to sketch out a “triad” of ways to achieve it: taxation, treasury borrowing, and central bank money creation. Taxation, in this case, rather than being market-correcting, involves the ramping up of any form of taxes to increase fiscal capacity (Galbraith, 2019; Knuth, 2021). Next to paying for green state expenditure via general borrowing, the idea has been floated to issue green sovereign bonds earmarked for projects with environmental benefits (Heine et al., 2019; Semmler et al., 2021). Central bank money creation has similarly been proposed, for example, by advocates of Modern Monetary Theory (MMT) (Nersisyan and Wray, 2019), Green Quantitative Easing (De Grauwe, 2019; Langley and Morris, 2020), Green central bank collateral (McConnell et al., 2022), or Green Targeted Long-Term Refinancing Operations (van’t Klooster and van Tilburg, 2020). Dikau and Volz (2021) argue that most central banks would have a respective mandate for conducting green policy (see also Boneva et al., 2022).

Compared to the market-failure paradigm, the “triad” model has the advantage of acknowledging that financing the Green Transition might not happen simply by fixing market failures or creating carbon markets and that political impetus may well be crucial (Ouma et al., 2018). However, from a macro-financial perspective (Gabor, 2020), the triad framework has three shortcomings. First, taxation and treasury borrowing typically describe how a government can increase its cash flow which can then be used for investment through government expenditure. But outside of “heterodox” economists’ circles, this often follows the problematic conceptualization of the loanable funds theory, which assumes that there is a defined quantity of ex ante financial resources that must be reallocated. While there is some merit to this view in commodity money systems, the opposite is true in a credit money system: New credit money is created ex nihilo when a financial institution gives a loan or purchases a bond from a counterparty. This implies that the monetary system has an inherent potential for expansion which can be leveraged for financing a large-scale transformation. While some reallocation of existing money, although insufficient, can be beneficial, the bulk of money required for financing the Green Transition can be endogenously created, it does not have to be redistributed (Murau and Pforr, 2020).

Second, the triad approach often lacks a systemic understanding. The volume of credit money needed for a large-scale transformation is so substantial that it cannot be borne solely by public institutions such as the central bank or the treasury; to assume that this can be done without far-reaching reverberations in the non-public sector is dubious. Rather, the entire or for the least a great part of the monetary and financial system must be harnessed systematically. Credit money creation can be carried out both by public and private balance sheets such as commercial banks and shadow banks and in different parts of the system. Some recent scholarship hints at this (Chenet et al., 2021; Dafermos et al., 2021; Dunz et al., 2021; Fontana and Sawyer, 2016) but as yet there is no fully developed framework, especially one accounting for the role of off-balance-sheet fiscal agencies (OBFAs) and the shadow banking sector.

Third, the triad approach ignores the procedural dimension (cf. Rochon, 1999). Financing a large-scale transformation is a long-term process that requires diligent macro-financial management and coordination of different parts of the credit money system. Not only does the system have to deliver on a “green initial expansion” to create credit money today, but it also has to fund it over a long period of time, avoid an implosion of the credit network, and eventually manage repayments and contraction later. Accounts that rightly emphasize the system’s unlimited capacity to create credit money ex nihilo but disregard its subsequent progression through and impact on the system miss the complex procedural dynamics at play. This is important because there is nothing inherently less risky about an expansion in green assets (Aramonte and Zabai, 2021; Daumas, 2023; D’Orazio and Popoyan, 2019)—these have to be processed and managed over the long term in a similar way to conventional assets.

To address these shortcomings, we propose to reframe the thinking around financing the Green Transition and mobilize the concept of “Monetary Architecture” (Murau, 2020) as a constantly evolving and hierarchical web of interlocking balance sheets that allows us to take endogenous credit money creation seriously and think about the systemic and procedural financing dimensions. Choosing the US as a case study, we argue that meeting the systemic financing challenge of the Green Transition requires mobilizing and coordinating the entire monetary architecture. While a reallocation of carbon-intensive capital will be unavoidable (Hockett, 2020), it will be insufficient on sheer numbers to bring about a net-zero transformation (IEA, 2022). Therefore, we assume that the Green Transition requires a substantial expansion of balance sheets to kickstart a new financing cycle. Procedurally, we not only need a strategy for how the monetary architecture can enable this expansion but also how it can be funded over a long-term horizon without leading to a disorderly contraction and endangering the financial stability of the monetary architecture.

Our analysis indicates the importance of maintaining a division of labor between two categories of balance sheets that depends on their respective hierarchical position in the monetary architecture. Hierarchically lower balance sheets are the “workhorses” most suited to provide the elasticity for the initial expansion and take over the bulk of the long-term funding. The hierarchically highest balance sheets are the “firefighters” best positioned to prevent a disorderly breakdown of the funding process and facilitate an orderly contraction. Workhorses comprise some OBFAs such as public investment banks or government-sponsored enterprises, ultimately controlled by public authorities, or private institutions such as commercial banks and shadow banks. The main firefighting institutions are the Federal Reserve and the Treasury, which are complemented by firefighting OBFAs such as the Federal Deposit Insurance Corporation (FDIC). Keeping the functions separate can facilitate these two types of balance sheets fulfilling their roles suitably while ensuring that the potential financial system related downsides of a large-scale green restructuring of the economy can be forestalled or mitigated. To steer the green financing process, the state thus plays an integral role in each phase but via different balance sheets.

We make a twofold contribution: first, we add to the incipient literature that looks at how private financing should be steered toward decarbonizing our economies (e.g. Chenet et al., 2021; Kedward et al., 2022; Krebel and van Lerven, 2022). The novelty in our approach lies in providing a conceptual framework that allows us to simultaneously reflect on the systemic and procedural aspects of Green Transition financing. Second, we add to the literature on the role of public finance and OBFAs in this process (e.g. Dafermos and Nikolaidi, 2019; Deleidi et al., 2020; Mertens and Thiemann, 2018; Orian Peer, 2020). Going beyond the triad model, we provide a blueprint for a division of labor between various public balance sheets for steering the monetary architecture through different phases of the financing process toward the goal of net-zero, including the crowding in of shadow banking balance sheets.

The remainder of this article develops our argument. The first section explains the Monetary Architecture framework envisaged to address issues on financing the Green Transition. The second section highlights the systemic financing dimension and considers the division of labor between different parts of the architecture. The third section argues via a three-phase scheme of the financial cycle that the procedural financing dimension entails currently neglected questions on funding and contraction. The last section wraps up our arguments in light of the Monetary Architecture framework.

Monetary Architecture as a conceptual framework

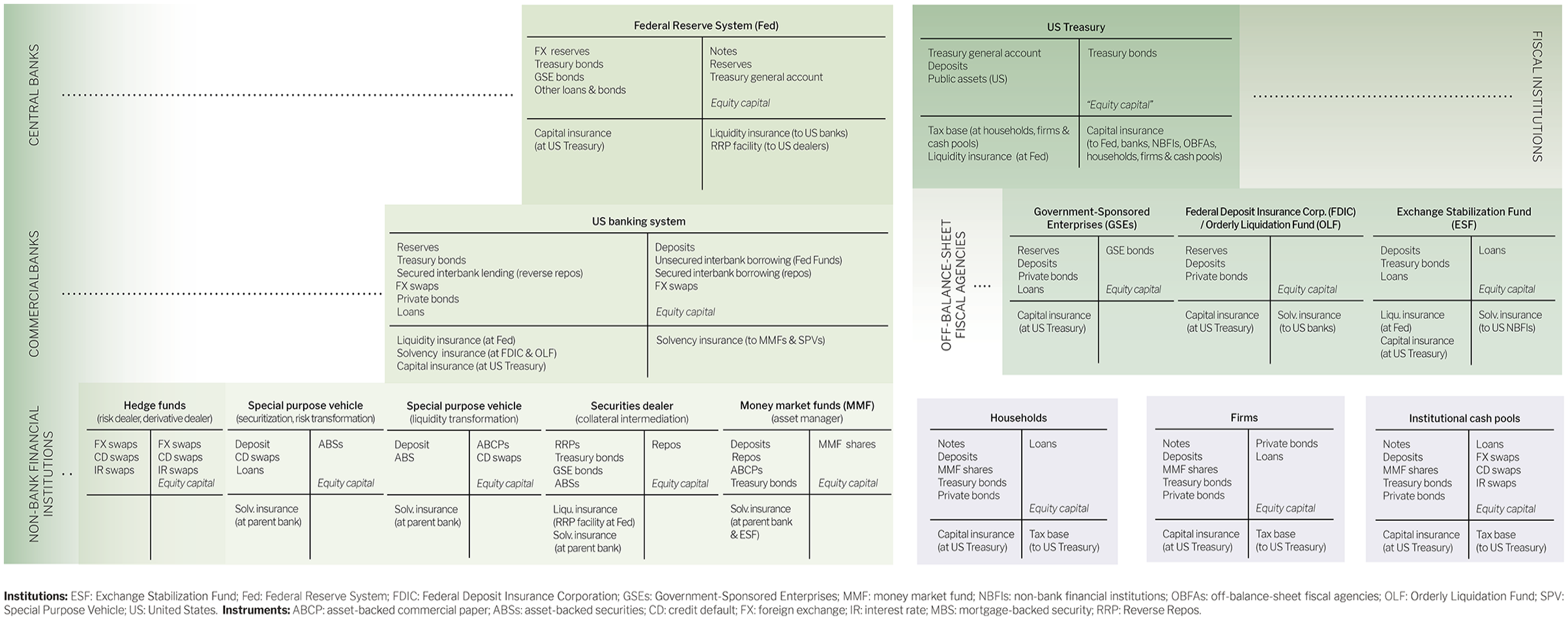

Our first argument is that the Monetary Architecture framework (Murau, 2020) offers a useful conceptual lens to appropriately grasp the macro-financial challenges connected to financing the Green Transition. Monetary architecture is a shorthand to describe an institutionalist model of historically specific formations of the monetary and financial system as a web of interlocking balance sheets (Mehrling, 2011) that is subject to continuous institutional evolution. Figure 1 presents an idealized model of the current US monetary architecture, which we use as an example and reference point to illustrate potential pathways for financing of the Green Transition.

The US monetary architecture as a web of interlocking balance sheets.

By definition, a monetary architecture consists of four segments: central banks, commercial banks, non-bank financial institutions (NBFIs), and a fiscal ecosystem, which is made up of treasuries and OBFAs (Guter-Sandu and Murau, 2022). In addition, we add firms, households, and institutional cash pools such as pension funds to the picture (Pozsar, 2015). The institutions in these segments are represented as balance sheets. These can be either individual balance sheets as in the case of the Fed or the Treasury, or aggregate balance sheets for households, firms, banks, etc. These institutions are either public (such as the Treasury), private (such as banks and NBFIs), or a hybrid of both (such as the Federal Reserve and many OBFAs).

All these institutions interlock through the instruments they hold as assets (denoted on the left-hand side of each balance sheet) and liabilities (on the right-hand side). Each institution holds different credit instruments such as deposits, loans, or bonds as assets or liabilities on-balance-sheet. Each asset of an institution must be another institution’s liability. Some of the institutions have a hierarchical relationship with each other. For instance, central banks are hierarchically higher than commercial banks, which in turn are hierarchically higher than NBFIs. The hierarchical structure is due to the nature of payment systems which need central nodes through which payment flows are organized (Aglietta, 2018). This is true for banking systems, which typically have a central bank at the apex, and commercial banks and NBFIs that occupy layers below. We can expand this idea of hierarchy also to other balance sheets, integrating treasuries and OBFAs.

For each institution, we distinguish between actual and contingent assets and liabilities. The upper part of each balance sheet denotes the actual instruments, the lower part the contingent ones. Actual instruments are what you typically expect to find on a balance sheet. They can be measured and reported at a given moment in time. Assets are instruments that promise a future cash inflow, liabilities are commitments for a future cash outflow. Assets can be purely financial or physical, but we follow here the Minskyan idea that a house is also just a form of bond that leads to future cash inflows and consequently treat it also as a financial asset (Minsky, 1986). The residual between actual assets and actual liabilities is the institution’s equity capital.

Contingent assets and liabilities are “counter-factual” instruments. From the perspective of the treasury, for instance, its ability to tax households, firms, and cash pools can be conceptualized as a contingent asset. In a crisis—defined as the endogenous contraction of the credit money system—contingent instruments may transform into actual ones in order to compensate for the loss of assets on a given balance sheet. According to Haldane and Alessandri (2009), contingent instruments can take the shape of—implicit or explicit—liquidity, solvency, or capital “insurance” (they may also be called “guarantees” or “backstops”) from higher-ranking to lower-ranking balance sheets. We depict them as contingent liabilities of the insuring institution and contingent assets of the insured institutions. The inherent structure of granting and receiving backstops predetermines the role of a balance sheet as a workhorse or a firefighter. The balance sheets receiving backstops from the hierarchically higher balance sheets assume the role of workhorses; the ones that do not have a hierarchically higher correspondents but may grant or receive mutual horizontal backstops (i.e. the Fed and the Treasury) assume the role of firefighters.

The system is organized around the transfer of public, private, and hybrid credit instruments (“IOUs”) that are issued as liabilities of higher-ranking institutions to function as monetary assets for lower-ranking institutions. First, money forms of the central bank involve notes issued for everyone, reserves for banks, and the treasury general account for the treasury. Second, commercial bank money is defined as deposits that are formally constructed as promises to pay central bank money, but no such central bank money is needed to create them. Deposits can be used by households, firms, and cash pools, treasuries and OBFAs, as well as different NBFIs. Third, NBFIs issue instruments which in some respects function as substitutes for deposits and may be called “shadow money.” In our example, those are money market fund (MMF) shares, repurchase agreements (repos), and asset-backed commercial papers (ABCPs). They can be held by households, firms, cash pools, or other NBFIs (Murau, 2017). The defining feature of the different types of money is that they have a stable price vis-à-vis each other—that is, they trade at “par,” a one-to-one exchange rate.

The creation of credit money follows the logic of a “swap of IOUs” between a hierarchically higher and a hierarchically lower institution. Since the model describes a fully self-referential system in which no “outside” money such as gold exists, money creation is fully endogenous to this system (Murau and Pforr, 2020). Central bank money can be construed as “public inside money” which has also a credit character and which is created in a structurally parallel way as private bank money (Mehrling, 2020).

Finally, each institution has a specific elasticity space. Any balance sheet can be extended to some degree by creating new credit instruments, which requires the simultaneous expansion of both assets and liabilities while interacting with another balance sheet as counterparty. The elasticity space describes the extent to which such an expansion on an individual balance sheet is possible and hence the capacity to contribute to credit money creation and the provision of new financing (cf. Gurley and Shaw, 1960). We define a balance sheet’s elasticity space as determined by three factors. The first factor is the willingness and ability of other institutions in the architecture to act as counterparty for balance sheet expansion and maintaining that level of expansion. This factor varies with the financial cycle, but may also be determined by capital allocation decisions related to questions of power, agency, or other ideational factors (Krippner, 2012; Quinn, 2017). The second factor is the access that a balance sheet has to contingent instruments, that is, mainly the extent to which hierarchically higher institutions—notably the central bank and the treasury—stand ready to supply them with emergency funds in a crisis. The third factor are the “stipulations” for the allowed on-balance-sheet activities and how these stipulations are enforced. Stipulations is a broad term deliberately chosen to describe such restrictions because they manifest themselves differently in each of the four segments. For instance, commercial banks are subject to banking regulations which comprise rules such as reserve ratios or capital buffers and are enforced via supervision, whilst NBFIs face much milder forms of regulation and supervision. Central banks’ on-balance-sheet activities are, if at all, “regulated” through stipulations connected to their mandate, their level of institutional independence, and the collateral framework which determines the assets they are allowed to purchase. The US Treasury is constrained by the checks and balances of Congress’s budget authority and the debt ceiling established with the Public Debt Acts of 1939 and 1941.

The US monetary architecture as depicted in this model is the result of an ongoing historical process of institutional evolution and adaptation (Schwartz, 2013; Mehrling, 2022). It emerged through the interaction of private innovation and public intervention, often spurred by the imperative to finance large-scale transformations brought about by wars and reconstruction. For instance, the creation of a federal Treasury in the US—with the autonomous power to issue securities and the ability to function as general capital backstop due to its power of taxation—was highly controversial and happened only in the aftermath of the US War of Independence. It goes back to the “Assumption” plan initiated by Alexander Hamilton, whereby the Treasury would assume states’ outstanding war debts (Frieden, 2016). The Treasury’s counterpart, the Fed, was only founded in 1913. For most of the 19th century, the US had a banking system without a central bank that would act as lender of last resort. There were some note-issuing public banks, the First and Second Bank of the US, just as the Treasury issued notes—so-called Greenbacks—in the Civil War era. The reliance of the banking system on Treasury bonds as assets is a relic of the two World Wars. Due to the US’s traditional reliance on long-term, rather than short-term debt, dealer banks have come to play a crucial role. The 1933 Glass-Steagall Act—a response to the Great Depression—separated commercial banks from investment banks (here found under the label NBFIs, split up according to their main functions) and shaped the structure of the US monetary system, even though it was repealed in the 1990s (Mehrling, 2011).

A key conceptual question is the relationship between the Fed and the Treasury. Although sometimes consolidated into a single government balance sheet (Kelton, 2020), we treat them as independent institutions that are, however, mutually supportive. Upon its foundation, the Fed was intended to be an autonomous entity, designed following the Bank of England’s model, that was supposed to be discounting firms’ short-term commercial debt, but due to two world wars and massively extended sovereign debt issuance ended up supporting the Treasury bond market. The Treasury-Federal Reserve Accord of 1951 reestablished the Fed’s policy autonomy (Conti-Brown, 2016) and introduced what we see as reciprocal liquidity and solvency guarantees of Fed and Treasury. The degree of fiscal-monetary cooperation changes over time and arguably with the financial cycle. It has intensified after the 2007–9 Global Financial Crisis (GFC), for instance via the QE programs, in which the Fed purchases Treasury securities and the interventions in the Treasury market of March 2020 when the Covid-19 pandemic led to financial turmoil.

At the same time, the Treasury is not a unitary actor but has several sub-balance sheets in the form of OBFAs to which it has relegated various functions while providing capital insurance (Guter-Sandu and Murau, 2022). The US OBFAs are largely the result of the 1930s and New Deal Reforms. The FDIC was introduced in 1933 to provide solvency insurance to the commercial banking system (Federal Deposit Insurance Corporation, 1984). The Dodd-Frank-Act extended this system with the Orderly Liquidation Fund (OLF). The Exchange Stabilization Fund (ESF) was introduced in 1934 to stabilize the international monetary system (Schwartz, 1997) but has since then been used as a multipurpose vehicle, for instance to backstop the crumbling MMF industry in the GFC (Murau, 2017). The oldest among the Government-sponsored Enterprises (GSEs), Fannie Mae, was founded in 1938 to expand the secondary mortgage market (Quinn, 2019).

From the 1970s onwards, the New Deal regulations led to a proliferation of new types of NBFIs and the emergence of what today is called the shadow banking or market-based credit system. NBFIs form a “daisy chain” of balance sheets that jointly carry out a similar form of maturity, liquidity, and risk transformation as traditional commercial banks do on their own balance sheet (Pozsar et al., 2012). During this, they create shadow money. MMFs competed with commercial banks by offering deposit-like accounts with higher interest rates, which was possible because they are not regulated as banks. ABPCs were issued on the balance sheets of Special Purpose Vehicles (SPVs), which commercial banks sponsored and endowed with solvency guarantees without having to expand their balance sheet and keeping more equity. The emergence of the tri-party repo market led to a new form of wholesale money market, competing with the Fed Funds market, which used short-term loans collateralized with US Treasury bonds and, prior to the GFC, with securitized private debt, first and foremost MBS issued by the GSEs (Murau, 2017). While the shadow banking structures have been transforming over time, the Dodd-Frank-Act has barely touched them and they continue to be a prolific feature of the US monetary architecture.

In sum, the Monetary Architecture framework provides a systematic overview on the monetary and financial institutions and instruments of our time, and how they interconnect. It shows how today’s setup of interlocking balance sheets is the result of past crises and political decisions, many connected to large-scale transformations such as wars and reconstruction. Any plan to finance the Green Transition must start with the current setup of the monetary architecture and will unavoidably have an impact on its future shape.

Financing the Green Transition as a systemic challenge

Our second argument is that—if any of the cited numbers of $30–$60 trillion are to go by—financing the Green Transition as a politically desired large-scale transformation of capital stock requires a balance sheet expansion that is so vast that it can only be achieved if as much elasticity space of the real-world monetary architecture as possible is mobilized. It is neither realistic to expect that “the market” in the form of private banks and firms will make the right and sufficiently large investment decisions that lead to such a sum if only carbon taxes are in place. Nor is it likely that individual public balance sheets such as the treasury and the central bank alone can create and allocate the volume of capital required for the Green Transition—in particular given the preferences of US citizens and policymakers who have little appetite for a government-only solution.

To finance the Green Transition, some types of balance sheets in the monetary architecture must act as counterparties and expand, thereby issuing a short-term IOU that can be used as money to make investment into new capital stock as well as a longer-term IOU such as a loan or bond which promises payment of money in the future and can be held or traded on within the monetary architecture. The big question for financing the Green Transition is which institutions—or rather which combination of institutions—should do this “heavy lifting”? Whose elasticity space should be tapped into, and which instruments should be used? While this question is rarely asked explicitly, we believe that three dominant answers can be found in the literature.

First, the expectation from an endogenous money perspective would be that the heavy lifting is done by banks and firms which act as counterparties (Minsky, 1986; Moore, 1988). Banks create credit money in the form of deposits and provide it to firms which in turn issue loans or bonds as their liabilities that banks can hold as assets. This is typically considered the main mechanism of money creation and financing investments in real capital stock in modern market economies. This financing technique, however, assumes that banks expect the investment to be both profitable and at an acceptable risk. However, investments that qualify for the Green Transition may often not have such a “positive investment case” (cf. e.g. McKinsey & Company, 2020) as they require internalizing external effects, which by definition reduces their profitability. Therefore, we find that this technique is only rarely explicitly mentioned in the literature on financing the Green Transition, for instance by Campiglio (2016), although he also does not believe that the entire heavy lifting for the Green Transition could be done this way.

A second strategy is based on the loanable funds theory—a framework within which the question about the heavy lifting has little merit because balance sheets are not assumed to expand endogenously to provide financing. Rather, it is assumed that there is a limited, exogenously given volume of money—the “loanable funds”—that must be distributed among different balance sheets in the monetary architecture to be spent on capital stock and hence finance real investments. From this angle, the Green Transition is imagined to be paid for by re-allocation of existing money stock, not creation of new credit money, and public balance sheets run the danger of crowding out private investment (Lamperti et al., 2019). Some of the market-failure paradigm literature uses the loanable funds theory explicitly (Carattini et al., 2021), others refer to it more implicitly when focusing on state investment banks or multilateral development banks, which—despite their name—are no banks proper as they cannot create money (Skovgaard, 2017). Likewise, some of the triad literature thinks about the Green Transition within the loanable funds framework. For instance, taxation implies that the treasury draws on the tax base as its contingent asset and extracts deposits from households and firms to then invest it, or treasury borrowing may be taken to imply that the treasury collects pre-existing money from households or firms with a promise to repay it later in the future.

A third answer is that the “heavy lifting” should be done by the treasury, the central bank, or both. A relevant part of the triad literature does assume that new money is being created when public balance sheets seek to raise money to finance the Green Transition. Treasury borrowing entails the issuance of treasury bonds (Robins and Muller, 2021), facilitated by primary dealers who distribute them on to different secondary market participants. These could be banks financing the purchase of bonds by expanding their balance sheet and creating deposits or the Fed accepting the bonds as assets and creating new money on the Treasury General Account. Other ways are imagined for how the central bank could provide the financing for green investments into capital stock. For instance, some Green QE proposals envision a direct interaction between the central bank and households or firms, which would receive central bank money in order to invest in capital stock (Pettifor, 2019). Such operations are conceivable but are not presently common in the US monetary architecture (Omarova, 2021).

A commonality among these ways of reflecting on how the heavy lifting could be carried out is that they only consider some selected institutions and their instruments and elasticity space in the monetary architecture. There is no “systemic” view that would consider all different types of balance sheets that presently exist. Yet, to reach the quoted numbers for financing the Green Transition, the goal must be to mobilize as much elasticity space as possible. This may involve some re-distribution of funds and the usage of traditional ways for money creation but should also entail crowding in other institutions to use their instruments and elasticity space, or potentially setting up new ones. Against this backdrop, the Monetary Architecture framework with its inherent notions of hierarchy and hybridity offers an entrypoint for conceptualizing a financing strategy that is truly systemic and respects the inherent division of labor between firefighting and workhorse balance sheets. Accordingly, we wish to make three arguments.

Our first point is that the hierarchically highest public balance sheets may not be the ideal candidates in the monetary architecture to be put to the forefront for using their elasticity space to shoulder the heavy lifting. The triad literature typically calls for a greater involvement of the central bank and the treasury for a green initial expansion, pointing to the massive transformations that the balance sheet of the Fed has undergone ever since the GFC and the Covid-19 pandemic. With some central banks shifting into climate issues (Dombret and Kenadjian, 2021), the Fed faces calls to integrate climate change considerations in its operation as well. Qualitative approaches call for changing the composition of central banks’ balance sheets, quantitative ones for enlarging the balance sheet by adding green assets. However, while both the GFC and Covid-19 interventions were conducted ex post, calls for a similar intervention in the case of the Green Transition are made on an ex ante basis. Although the Fed has recently joined the Network for Greening the Financial System (NGFS) and created two internal committees aimed at exploring this issue (Brainard, 2021), it still shows resistance to both options (Riksbank, 2023).

Reservations about the excessive use of central bank but also treasury balance sheets are often shrugged off as monetary and fiscal conservatism. However, there are other reasons to caution against the excessive use of elasticity space at the apex of the hierarchy to finance the Green Transition. Firefighting balance sheets can become politically contentious and constrained, and thus serve their objectives with less effectiveness. For instance, the Treasury might be beholden to government imperatives that deny the necessity to publicly finance a Green Transition; the Fed, on the other hand, is an independent institution that in times of crisis will prioritize financial stability over other policy objectives. Similarly, in inflationary times, both these balance sheets face pressure to engage in anti-inflationary policies which might not be compatible with a green expansion.

In case of a crisis, as these balance sheets are situated at the apex of a hierarchical system, they are the ones that expand to accommodate distressed assets from hierarchically lower balance sheets. Hence, the balance sheets should ideally be kept lean in “normal” times in order to maintain their capacity to forestall the next crisis, not least because these balance sheets do no benefit from hierarchically higher backstops. Although they mutually backstop each other, there are limits to the extent to which they can bail each other out without undermining confidence in the system. For instance, monetary financing—understood as central banks purchasing treasury debt on the primary market—is a politically contested operation and comes with a considerable risk for negative side effects on the monetary architecture and the real economy. On the other hand, large-scale treasury bailouts of central banks are historically unprecedented events with consequences that are hard to predict.

Our second point is that large-scale transformations of capital stock—as past periods of war and reconstruction have shown—can be well financed with OBFAs doing the heavy lifting of the financial expansion. OBFAs can interact with multiple parts of the monetary architecture and seek to incentivize balance sheet expansion. At the same time, they are workhorse balance sheets not at the top of the hierarchy, so they do not need to be involved in safeguarding the system. As they are subject to less stipulations limiting their elasticity space and enjoy more policy autonomy, they can mobilize their own balance sheet to provide additional elasticity space for the monetary architecture, for instance, by issuing bonds earmarked for green projects, or they can steer the monetary architecture in the direction of financing the Green Transition by crowding in other balance sheets.

There are several examples in US economic history when OBFAs assumed a critical role in financing large-scale transformation. During WWI, the War Finance Corporations (WFC) purchased Liberty Bonds and Victory Notes issued by the US Treasury. Its annual purchases amounted to about 0.9% of GNP (Butkiewicz and Solcan, 2016). The WFC inspired the creation of the Reconstruction Finance Corporation (RFC) in 1932, which was used to expand the monetary architecture first to combat the slump of the Great Depression, then to provide financing for WWII. The RFC both lent to state and local governments as well as to banks, railroad companies, and mortgage associations. During the war, the RFC granted business loans of close to 40 bn USD. To put this into perspective, the volume of bank loans rose from 21 bn USD in 1938 to 40 bn USD in 1945 (Olson, 1988). Around the same time, the US government started creating the network of GSEs aimed at the mortgage market. Federal Home Loan Banks made direct loans to homeowners. Fannie Mae was tasked with fostering a secondary market in mortgages by engaging in the securitization of mortgage assets (Quinn, 2019). In 2010, together with the Government National Mortgage Association (Ginnie Mae), GSE portfolio holdings and securitization covered 56% of the outstanding whole home mortgages (Jaffee and Quigley, 2012). Later, similar GSEs expanded in other sectors, for example, the Student Loan Marketing Association (Sallie Mae), which is a GSE established in 1972 and involved in nurturing the student loan market.

Some of these OBFAs persist in a similar form to their original one, others have disappeared or assumed other functions. Recent calls for establishing new OBFAs aimed at the Green Transition build on these models and envision, for instance, the provision of equity capital in blended finance initiatives to de-risk investments or the funding of existing green bonds by bulk-buying and securitizing them. An existing proposal on these lines for a US OBFA solution to finance the Green Transition is to set up a Federal Investment Agency (Hockett and Omarova, 2018), which could help solve political constraints in the US Congress regarding the use of the US Treasury’s elasticity space. An alternative would be a green GSE which would engage in green securitization and could issue green agency bonds that, if it receives Fed backing, could also act as a novel safe asset.

Our third point is that, while commercial banks may be seen as the go-to institutions for financing investment in capital stock, an even higher elasticity space is to be found in the shadow banking system. The question is whether it could be beneficial to harness the elasticity space on the various NBFI balance sheets for financing the Green Transition and, if so, how and to which extent. The idea to mobilize shadow banking balance sheets for financing the Green Transition is contested, and maybe for a good reason. Not only were shadow banking structures the main culprits of the GFC, they also circumvented the New Deal era safety features for the banking system and have played a major role in enhancing wealth inequality (Caverzasi et al., 2019). Moreover, shadow banks are argued to be responsible for reproducing the current lock-in into the carbon-based production system, for instance via the collateral chain (Dafermos et al., 2021). The argument often heard prior to 2007 that shadow banking structures are efficiency-enhancing has largely disappeared. Still, rather than treating financing the Green Transition as one superproject geared at financial expansion and regulating the shadow banking system as a competing superproject seeking to achieve financial contraction, it may be beneficial to change the perspective and ask how these institutional structures can be productively integrated in the financing challenge of the Green Transition. Not only can the shadow banking sector potentially be decarbonized, for instance by calibrating the greenness of assets providing the collateral in repo agreements and securities lending (Dafermos et al., 2021), but it may also be that some shadow banking balance sheets may be used in a different way. The inherent challenge, of course, is how it could be possible to gear shadow banks’ balance sheets toward supporting the financing aspect of the Green Transition that goes beyond mere greenwashing. To come to terms with this question, we will have to think about the procedural aspect of financing a large scale transformation.

Systemic financing of the Green Transition as a procedural challenge

Our third argument is that financing the Green Transition is a long-term process that requires diligent macro-financial governance and coordination of different parts of the monetary architecture. Not only do the balance sheets in the monetary architecture have to create credit money today, they also have to put it to productive use over a long period of time, avoid an implosion of the credit network, and find a solution for the inherent need to repay the debts later. The distinction between workhorses and firefighters helps to develop a strategy for tackling the associated governance challenges.

To substantiate our argument, we present a simple scheme in Figure 2 which suggests that systemically financing a large-scale transformation such as the Green Transition must comprise three ideal-typical phases of a financial cycle: initial expansion (green), long-term funding (yellow), and final contraction (red). This scheme takes on board ideas on the financial cycle of the Money View (Mehrling, 2020) as well as monetary circuitistes (Rochon, 1999) and Post Keynesians (Bonizzi and Kaltenbrunner, 2020). These approaches emphasize that credit is inherently unstable and that sustaining financial stability requires provisions for managing both regular defaults of credit contracts as well as potential cataclysmic credit defaults that can endanger the whole system.

Three phases of financing large-scale transformations.

The scheme starts with an initial expansion of balance sheets within the monetary architecture during which financing is provided via a swap of IOUs between different types of balance sheets. Subsequently, the monetary architecture must “fund” the investment over a long-term horizon. This means that the initial balance sheet expansion must be maintained in the system ceteris paribus while the actual instruments created are moved across balance sheets. The short-term IOUs (credit money) have to be used for investments in greening the capital stock while the long-term IOUs must be distributed to balance sheets that are willing and able to hold them over a long time horizon (Mehrling, 2020). As different balance sheets are in charge of an initial expansion and long-term funding, the transition between both steps is a major challenge in the financing of a large-scale transformation. This involves making sure not only that the credit money created is used for the appropriate investment purposes but also that the long-term IOUs are not paid back too soon or have to be liquidated in a credit crunch. At the end of the financial cycle, when the funding phase is over and repayment is due, the final contraction should occur—ideally in an orderly fashion as outstanding loans and bonds are repaid, and the monetary architecture reverts to the initial level of expansion. Rochon (1999) refers to it as “monetary reflux” that coincides with a “destruction of money” as the monetary circuit comes to an end.

As the three phases are ideal types, they cannot be perfectly distinguished in practice. Nevertheless, the scheme gives us a useful way of thinking about the procedural challenges of financing the Green Transition. The literature focuses almost exclusively on the phase of a green initial expansion—and sometimes correctly notices that there is no objective limit to it (Kelton, 2020; Nersisyan and Wray, 2019)—while affording a much lesser importance to the funding and contraction phases. However, if the history of financing cycles and financial innovation is any indication, questions of funding and contraction are essential for determining if financing the Green Transition can succeed, while overlooking them may lead to deleterious consequences down the line. Drawing on the distinction between workhorse and firefighter balance sheets in a monetary architecture, we make four propositions for what diligent macro-financial governance of the procedural dimension might entail.

First, as the Green Transition is a politically-desired large-scale transformation, we believe that the pivotal role for manufacturing a green initial expansion in phase (i) must be taken over by balance sheets that are under the control of the state. Relying merely on the private sector to be a first mover for expanding its balance sheets and making the desired investments in housing, transportation, infrastructure, agriculture, industry, and energy will likely not deliver a successful or timely transition. The necessity of mobilizing public balance sheets to close the financing gap is indeed widely recognized and increasingly accepted (IPCC, 2023). The obvious question then is which balance sheets through which the state appears in the monetary architecture are most suitable for the task.

We argue that public or hybrid workhorse balance sheets that are located further down in the monetary hierarchy, notably OBFAs, are most suited for this purpose. Historical examples of past large-scale transformations point in this direction. For instance, the WFC, the RFC, and the GSEs provided vast sums of ex ante financing to a scale that the Fed and the Treasury would not have been able to achieve, be it due to political constraints, ideological reasons, or prohibitive stipulations such as debt ceilings and central bank price stability mandates.

The idea to resort to public OBFAs for financing the Green Transition is not unheard of and currently being pursued, for instance via the much-publicized adoption of the Inflation Reduction Act (IRA), the flagship Green policy package of the Biden Administration. One feature of the IRA is the ringfencing of $20 bn to create a National Green Bank (NGB), although details about its exact operations are currently scarce (CGC, 2022). That said, the largest share of the IRA is in the form of tax credits, with about a fifth in the form of grants and a tenth loans (White House, 2022). As the IRA is to be financed mainly by levying taxes on corporations, closing tax loopholes, and reducing healthcare spending (Rao, 2022), it focuses mainly on a redistribution within the monetary architecture rather than an initial green expansion of balance sheets. Overall, the IRA is still a watered-down version of the Green New Deal (GND) initially proposed by the Democrats, and is estimated to fall short of reaching the US climate target by 22%–45% (Climate Action Tracker, 2022). It is a case in point for the problems we identify in ex ante provision of financing via the Treasury as it relies by necessity on political compromise and struggles over direction of resource allocation from the Treasury balance sheet, as opposed to OBFAs which tend to have a specific mandate and thus better mitigate political constraints.

Second, to ensure that an initial green expansion can be funded in phase (ii), it is necessary to distribute the long-term IOUs to balance sheets that are willing and able to hold them over a sufficient time horizon. As public balance sheets can only fund a portion of the required sum, the other part must be taken over by private balance sheets. While banks, households, and firms should certainly play a considerable role, the most sizable elasticity space available for this purpose in the US monetary architecture is that of the shadow banking sector, which accounts for more than half of total US financial assets (FSB, 2022). The shadow banking sector has been rightfully criticized for the role it played in the build-up to the GFC, when it contributed to proliferating toxic assets that would lead to the collapse of the global economy. Notwithstanding a small post-GFC dip, the shadow banking sector has since only soared, against the backdrop of various regulatory initiatives (Woyames Dreher, 2020). The issue then becomes that of how to put the shadow banking sector to productive use and harness its available elasticity space to help fund the Green Transition.

To organize the long-term funding on a systemic level, OBFAs can again play a crucial role and crowd in other parts of the monetary architecture, foremost the shadow banking system. The activity of Fannie Mae is instructive in this regard. It would initially buy loans from mortgage lenders, thereby freeing them to originate more mortgages, and eventually securitize them on its balance sheet into mortgage-backed securities (MBS) to place these with investors, including hedge funds, investment funds, pension funds, insurance companies, and other NBFIs. These balance sheets can then use their vast elasticity space to hold the assets and thus provide the long-term funding necessary for enabling a sustainable green expansion. This way OBFAs like Fannie Mae can essentially crowd in the shadow banking sector, steering it toward politically-desired objectives. Recently, for instance, Fannie Mae has expanded also in the green and social bond sectors (Guter-Sandu, 2021). Since 2012 the OBFA has issued over $112 bn in Green MBS, which consist of mortgage loans attached to newly-constructed residential homes that meet specific energy- and water-savings standards (Fannie Mae, 2023a). In 2020, Fannie Mae became the largest issuer of green bonds in the world (CBI, 2021), placing them with a variety of NBFIs, including socially responsible mutual funds, pension funds, sovereign wealth funds, or endowments. In the Monetary Architecture framework, the role of Fannie Mae is therefore that of an OBFA that crowds in the shadow banking sector by drawing on its monetary resources for the purpose of long-term funding of a green expansion.

Third, a particular challenge emerges if phase (iii) kicks in early, that is, if a green initial expansion cannot be sustainably funded and ends in an unexpected disorderly contraction. By definition, this would be a financial crisis—it would likely get ex post branded as the bursting of a green financial bubble—that threatens financial stability. In a credit money system, such a crisis is always possible as credit is inherently unstable. To be able to react to such an uncontrolled contraction, it is important to have hierarchically higher balance sheets in place that can expand in an emergency to ensure system stability and goal integrity—this is by definition the role of public firefighting balance sheets. Depending on the nature of the crisis, the firefighting intervention may involve the Fed managing liquidity conditions, the FDIC providing deposit insurance, or the Treasury bailing out institutions the failure of which would jeopardize the Green Transition. The ability to backstop and manage the funding process in case of a financial crisis is precisely the reason why we believe that the initial green expansion should not be carried out by balance sheets at the apex of the monetary hierarchy—they will not have any backstops any more once the financing process goes wrong.

The disorderly contraction of credit in the funding phase may stem from two types of risk: idiosyncratic or systemic. Idiosyncratic risks present themselves in the form of some green investments failing with necessity during the long-term funding phase. In this case, green investments can fail on their returns or on their greenness, that is, they may in fact turn out to be greenwashed and their value might plummet if there are green valuation mechanisms in place. One factor for preventing the latter is the development of robust green standards and disclosure requirements for companies undertaking green projects. In the case of an OBFA like Fannie Mae, the “greenness” of its bonds is confirmed by annual reviews of the underlying assets’ green certifications, which are awarded by a dozen of approved organizations ranging from for-profits to NGOs and US governmental departments (Fannie Mae, 2023b). This might have the advantage that being a workhorse OBFA, Fannie Mae’s validation of certain green certifiers could lead to a race-to-the-top in terms of green standards, contributing to creating a fertile environment supporting green long-term funding. This can complement or even improve risk hedging practices already present in the monetary architecture, developed by balance sheets such as banks, NBFIs, or some cash pools that are specialized on hedging in risk, including green risk, and diversifying it in their investment portfolios. When idiosyncratic risks cannot be absorbed by private balance sheets, they may become contagious and systemic, and will then require firefighter intervention.

Other systemic risks linked to the Green Transition might arise in the form of physical “Green Swan” events that create financial turmoil as an exogenous shock (Bolton et al., 2020), or as transition risks that emerge because the Green Transition creates stranded carbon-intensive assets which suddenly lose their market value and hence reduce the equity capital of those balance sheets in the monetary architecture who hold them (Chenet et al., 2021; D’Orazio and Popoyan, 2019). However, the bursting of a possible “green financial bubble” created by a green initial expansion is not a well-established position in the green finance literature—this topic has only recently started to get some attention (Brav and Heaton, 2021; Heger and Åkerman, 2021). Moreover, there is disagreement as to whether a green initial expansion would lead to distortions of the price level that would undermine the feasibility of managing its long-term funding. This could happen either through the more limited “greenflation” of the matter required for decarbonization, making thus the Green Transition expensive in the short- to medium-term (Schnabel, 2022), or through the wider inflationary bias of making carbon generally more expensive (Boneva et al., 2022).

Fourth, once the financing process reaches phase (iii), it may be necessary to manage the contraction of the balance sheets. A prevalent strategy for macro-financial governance is to prevent the reversal of the initial expansion and instead to keep the monetary architecture permanently in the funding phase. This can be achieved by continuously rolling over existing debts without clear intentions to repay them—a common practice in sovereign debt markets to-date (Eichengreen et al., 2021). In general, there are no impediments to rolling over green sovereign bonds indefinitely as long as the counterparties in the monetary architecture agree on it and provided there are no stipulations for the balance sheets involved that would prevent it. Moreover, if the central bank either buys green assets outright or accepts them as eligible collateral, it can contribute substantially to entrenching them in the funding phase for the long term.

In case the final contraction does set in, whether planned or unintentionally, firefighting balance sheets can play a role to manage the implosion dynamics and ensure that it does not lead to a systemic meltdown. History offers examples for managed contractions that were carried out by various firefighting balance sheets. For instance, in the first phase of the GFC, the Fed facilitated the orderly contraction of the ABCP market (Murau, 2017). At the peak of the Great Depression in 1933, the US Treasury stopped the cascading bank runs by deciding in the course of a weekend which troubled banks were to be shut down and which were allowed to live on while receiving a US government backstop (Wicker, 1996). Once the funding cycle for WWI ended and the US found itself with a slew of war finance instruments like Liberty or Victory Bonds whose value started depreciating and causing distress to the bondholders (Kang and Rockoff, 2015), it repurposed the WFC into a firefighting OBFA. The WFC ended up buying over 7% of the total market for these bonds, in turn selling them to the Treasury which funded this operation by issuing short-term certificates of indebtedness (Butkiewicz and Solcan, 2016). This episode of managed contraction of war finance notwithstanding, the US as a victor in both world wars arguably never ceased funding the initial balance sheet expansion of war finance. What happened instead was that the US in fact outgrew the problem through rolling it over, that is, replacing old war debt with new debt (Kremers, 1989). In contrast, vanquished Germany saw a hyperinflation, several sovereign bankruptcies, and two resets of its currency, all with deleterious socio-economic consequences (Holtfrerich, 2013).

Conclusion

This article contributes to the literature on the Green Transition by using the Monetary Architecture framework to think about the associated financing challenge. The framework underlines how the monetary and financial system is a constantly evolving and hierarchical web of interlocking balance sheets. Taking the US as a case study, we have stressed the importance of a systemic financing dimension that crowds in the available elasticity space in the monetary architecture while taking into account a division of labor between firefighting and workhorse balance sheets. This allows firefighters to focus on system stability, while OBFAs may be used to take initiative in steering the monetary architecture toward green public policy objectives and various other institutions including shadow banks may be tapped into for their vast potential for balance sheet elasticity.

Moreover, we have pointed to the procedural financing dimension that considers not only the green initial expansion but also questions of long-term funding and contraction. For the Green Transition to be successful, we need mechanisms that enable continuous funding of green assets as well as a strategy for orderly contraction and the prevention of financial instability originating from a potential green bubble. As the monetary architecture is never static but subject to continuous change, we should expect that the Green Transition will have a considerable impact on its setup—just as the New Deal as well as WW1 and WW2 financing have profoundly shaped how the US monetary architecture looks today.

Our analysis seeks to unveil financing options beyond those discussed in the market-failure or the triad paradigms and cautions against the use of firefighters for tasks that would be better carried out by workhorses. Currently, there is a striking absence of analytical tools suitable for thinking of financing the Green Transition as a systemic and procedural challenge. By introducing the Monetary Architecture framework and exploring its systemic and procedural implications, we attempt to provide the groundwork for meeting this challenge. We have used the current US monetary architecture as an example to illustrate pathways for financing the Green Transition. Located at the apex of the international monetary architecture, the US has “exorbitant privilege,” whereas other states further down the hierarchy have less financial room for maneuver. This is partially balanced by more political leeway concerning issues that are deadlocked within the US.

Our analysis of the Green Transition through the prism of the Monetary Architecture framework can be the starting point for future research. We wish to highlight three different directions.

First, it would be possible to further explore in more concrete terms the four steps of the macro-financial governance scheme that we develop on the back of the Monetary Architecture framework. This could entail studying in greater detail how public workhorse balance sheets can manufacture an initial expansion and which techniques are most suited for crowding in other balance sheets in the monetary architecture. Moreover, the question of how public firefighting balance sheets can support an orderly final contraction without repercussions on systemic stability deserves major attention.

Second, our proposed procedural dimension can also be applied to the question of how to phase out the funding of carbon-intensive assets. Arguably, today’s monetary architecture is still in the funding phase of past initial expansions that created such carbon-intensive assets. For instance, the shadow banking sector, while constantly evolving, is still deeply invested in the fossil fuel sector. Finding suitable macro-financial techniques for phasing these assets out in an orderly way would naturally complement the research perspective in this article which is concerned with organizing and funding a new balance sheet expansion. In the shadow banking sector, known for its agility when it comes to regulatory arbitrage, a particularly fertile avenue for research is identifying the right balance between regulatory control and incentive structure that may steer this sector toward the long-term funding of a green expansion.

Finally, our proposed framework may be used to analyze how other states or regions than the US can harness both their domestic and the international monetary architecture for financing the Green Transition. In this regard, it would be interesting to take into account different institutional settings that are characterized by a less extensive shadow banking sector and to study the various cross-border effects that financing the Green Transition will likely entail.

Footnotes

Acknowledgements

This article showcases the conceptual framework of the OBFA-TRANSFORM project, an Emmy Noether research group financed by Deutsche Forschungsgemeinschaft on the topic “The Political Economy of Financing Large-Scale Transformations. Off-Balance-Sheet Fiscal Agencies in Wars, Reconstruction, and the Green Transition” (![]() ). We have presented earlier versions of the manuscript at the 2021 annual conference of the European Association for Evolutionary Political Economy (EAEPE); the 2022 convention of the International Studies Association (ISA); the 2022 Toronto Conference on Earth System Governance; the 2023 Money as a Democratic Medium 2.0 conference at Harvard Law School, the Hamburg Institute for Social Research, and THE NEW INSTITUTE; as well as at research seminars of City, University of London, the University of Bath, Ludwig-Maximilians-Universität München, Freie Universität Berlin, Hochschule für Wirtschaft und Recht, Berlin, and the Global Climate Forum, Berlin. We wish to thank all participants for the valuable input we have received. For feedback on the project at various stages, we are particular grateful to Milan Babić, Will Bateman, Andrea Binder, Benjamin Braun, Yakov Feygin, Barbara Fritz, Daniela Gabor, Kevin Gallagher, Maria Garcia, Matteo Giordano, Alexandru-Stefan Goghie, Lukas Hakelberg, Sophia Hatzisavvidou, Eckhard Hein, Carlo Jaeger, Sebastian Kohl, Max Krahé, Gregor Laudage, Elsa Clara Massoc, Perry Mehrling, Lara Merling, Daniel Mertens, Olga Mikheeva, Anastasia Nesvetailova, Christopher Olk, Nadav Orian Peer, Stefano Pagliari, Fabian Pape, Matthew Paterson, Tobias Pforr, Jay Pocklington, Joel Rabinovich, Thomas Rixen, Lukas Rudolph, Laura Seelkopf, Janek Steitz, Jonas Teitge, Jan-Erik Thie, and Jens van ’t Klooster. Finally, we are deeply indebted to three anonymous reviewers who have greatly helped us improve our arguments. All remaining errors are naturally our own.

). We have presented earlier versions of the manuscript at the 2021 annual conference of the European Association for Evolutionary Political Economy (EAEPE); the 2022 convention of the International Studies Association (ISA); the 2022 Toronto Conference on Earth System Governance; the 2023 Money as a Democratic Medium 2.0 conference at Harvard Law School, the Hamburg Institute for Social Research, and THE NEW INSTITUTE; as well as at research seminars of City, University of London, the University of Bath, Ludwig-Maximilians-Universität München, Freie Universität Berlin, Hochschule für Wirtschaft und Recht, Berlin, and the Global Climate Forum, Berlin. We wish to thank all participants for the valuable input we have received. For feedback on the project at various stages, we are particular grateful to Milan Babić, Will Bateman, Andrea Binder, Benjamin Braun, Yakov Feygin, Barbara Fritz, Daniela Gabor, Kevin Gallagher, Maria Garcia, Matteo Giordano, Alexandru-Stefan Goghie, Lukas Hakelberg, Sophia Hatzisavvidou, Eckhard Hein, Carlo Jaeger, Sebastian Kohl, Max Krahé, Gregor Laudage, Elsa Clara Massoc, Perry Mehrling, Lara Merling, Daniel Mertens, Olga Mikheeva, Anastasia Nesvetailova, Christopher Olk, Nadav Orian Peer, Stefano Pagliari, Fabian Pape, Matthew Paterson, Tobias Pforr, Jay Pocklington, Joel Rabinovich, Thomas Rixen, Lukas Rudolph, Laura Seelkopf, Janek Steitz, Jonas Teitge, Jan-Erik Thie, and Jens van ’t Klooster. Finally, we are deeply indebted to three anonymous reviewers who have greatly helped us improve our arguments. All remaining errors are naturally our own.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Steffen Murau acknowledges funding by Deutsche Forschungsgemeinschaft (project numbers 415922179 and 499921148).