Abstract

Departing from the Regulation Approach and the concept of spatio-temporal fixes, this article analyses how different mechanisms of financialization have ameliorated and accelerated crisis-tendencies in the North European forest industry and its implications for labour, suppliers and corporate R&D. Although wood products can potentially ameliorate the climate crisis by substituting plastics, petrochemicals, polyester and various other applications from fossils, firms have been slow to advance into these higher value-added segments. Instead, under an increasingly financialized accumulation regime, innovation has been undermined through R&D downsizing while dividends have been increased to shareholders at labour’s expense. Meanwhile, amid ultra-low interest rates, the industry’s profitability has been supported by appreciating forest assets that are increasingly treated as a new financial asset class by the financial sector. Evidently, while some mechanisms of financialization are detrimental to firms, the financialization of forests has constituted a profitability-enhancing socioecological fix (McCarthy, 2015; Ekers & Prudham, 2017) not only for financial capital (Ekers, 2019) but also for non-financial firms themselves. In the long run, however, it is highly uncertain if forest asset prices can be kept from depreciating amid the problems of profitability, weakened ecological carrying capacity, rising interest rates and strained supplier relations.

Introduction

Researchers have showed that high-value added biorefinery products from wood could provide sustainable substitutes to fossil fuels, chemicals, plastics, cement and cotton (Backlund and Nordström, 2014; Hellsmark et al., 2016; Brunnhofer el al, 2020). For this reason, the OECD (Oborne, 2010) and the European Commission (2012) have put high hopes for the bioeconomy, that includes the forest industry, to mitigate the climate crisis by substituting fossil-based inputs with bio-based materials. Further commercialization of bio-based materials requires visions, long-term strategies, risk-taking and large investments by lead firms in the forest industry. However, the movement towards higher value-added outputs has been slower than expected (Hansen and Coenen, 2017). Instead, firms have trimmed their organizations, closed research labs, decreased R&D spending and been slow to exploit high quality research infrastructure that has been built over several decades (MoRe, 2010; Hellsmark et al., 2016). This seems odd, considering that the industry could capitalize on society’s piecewise decoupling from fossils, the immense political support the North European forest industry enjoys, and that the traditional business model of the European forest industry has reached its maximum potential (Brunnhofer et al., 2020). What explains this apparent failure on behalf of the industry?

This article traces the evolution of corporate strategies and industrial restructuring by foregrounding how capital accumulation has been reproduced during the institutionalization of Northern Europe’s neoliberalized mode of regulation. The article demonstrates how the industry globalized and became increasingly financialized the last four decades following easier forms and increased incentives for financial value-extraction, capital markets’ expectations of quarterly profits and the necessity to defend share prices amid takeover threats on a global market for corporate control. The article shows that the globalization and financialization of North European capitalism, underpinned by neoliberal modes of regulation, have spawned heightened competition, new geographical horizons and increased managerial uncertainty which, coupled with large production chains and a historical scepticism towards R&D, created an inhospitable environment for innovation in the forest industry. Profitability has instead been generated by the squeezing of labour and suppliers, R&D downsizing following a tendency to reduce organizational slack, while the financialization of forests, that is, the nominal appreciation of forest land, has greatly ameliorated crisis tendencies among lead firms by improving their balance sheets, share prices and credit ratings. As is elaborated in the article, the financialization of forests has in this way constituted a socioecological fix, that is, a temporarily stabilizing force for capitalism’s crisis tendencies (Harvey, 2001; Jessop, 2006; French et al., 2011). The socioecological fix is one of six profitability-enhancing fixes that are elaborated throughout the article’s empirical section.

The following research questions are asked: How have changes in the mode of regulation, accumulation regime change and financialized globalization affected profitability, strategies, innovation and labour in the North European forest industry, and why? How is shareholder value maintained in the industry amid long-term profitability decline? How has governance of research and innovation activities evolved during the three latest decades of finance-dominated capitalism, and why?

Before elaborating on the article’s theoretical framework, it is necessary to explicate the two ways by which the industry can contribute to reduced greenhouse gas emissions: through substitution, as renewable forest products replace fossil-based or other environmentally unsound products; and through carbon sequestration, that is, through forest growth and bio-based products. Moderately harvested forests contribute to more sequestration than unharvested forests, as carbon is significantly sequestrated during the growth phase of young trees, as well as in forest products. According to the Swedish Environmental Protection Agency (2022), Swedish forests sequestered 38 million tonnes of CO2 equivalents and wood products sequestered 7 million tonnes of CO2 equivalents in 2020. In comparison, domestic transport emitted around 15 million tonnes the Swedish Environmental Protection Agency (2022). When it comes to substitution, textiles from wood materials, such as viscose, are significantly more environmentally friendly than polyester and cotton, the latter requiring huge quantities of pesticides and irrigation in the Global South (Hassegawa et al., 2022). Prefabricated building components of wood in multi-storey buildings likewise significantly reduce emissions by substituting cement (Lehmann, 2013). Bio-composites can increasingly substitute plastics, and applications from lignin could significantly contribute to industry’s inevitable decoupling from fossils. Lignin constitutes one fourth of a boreal tree and can be used in a wide range of applications, including as inputs for fuels, chemical products and carbon fibres. Carbon fibres are used in various industries, including aerospace, electronics and construction (Backlund and Nordström, 2014; Luo and Abu-Omar, 2017). However, significant investments in basic and applied research are required for further commercialization of these emerging products.

The following section provides an overview of the Regulation Approach and the socioecological fix, which is followed by a section that discusses the article’s methodological considerations. The subsequent section backgrounds how the post-war managerial culture evolved amid the North European forest industry’s structural realities. The penultimate section provides an empirical account of accumulation regime change, industrial restructuring and innovation system governance in the North European forest industry the last four decades. The article finalizes with a concluding discussion on the empirical findings.

The Regulation Approach, the socioecological fix and corporate financialization

The Regulation Approach aims to explain how the improbability of capital accumulation can be reproduced, temporarily stabilized and regularized for relatively long periods of time despite capitalism’s inherent contradictions and crisis-tendencies (e.g. Lipietz, 1988; Aglietta, 2000; Jessop, 2013; Neilson and Stubbs, 2016). Of interest is not only how industry-specific and macro-level extra-economic mechanisms such as norms, habits, laws and networks emerge but also their sources of crisis and change. Specific accumulation regimes, that is, regularized modes of production, investments, consumption and remuneration (Lipietz, 1987:14) are underpinned by ensembles of institutions called modes of regulation. These are politically and socially mediated, or more specifically, formed by social struggles and compromises between different fractions of capital, strata of labour and environmental movements. Regulation scholars typically highlight five interacting, hierarchically positioned institutions that make up a mode of regulation (Lipietz, 1988:14): • The wage relation (wages and social wages, labour processes etc), • Forms of competition or market relations between capitalists and firms (corporate governance and competition rules), • The financial system (banking and credit systems, degree and form of financial regulation, allocation of capital to production, national currencies), • Forms of state intervention, • The insertion into the international regime (trade, cross-border financial flows, currency regulation, transnational economic and political configurations) (Lipietz, 1988; Jessop, 2013).

The evolution, varying hierarchies and specific configurations of these institutional forms may to varying extent improve capital accumulation or accelerate crisis tendencies, or a combination of both, in different sectors.

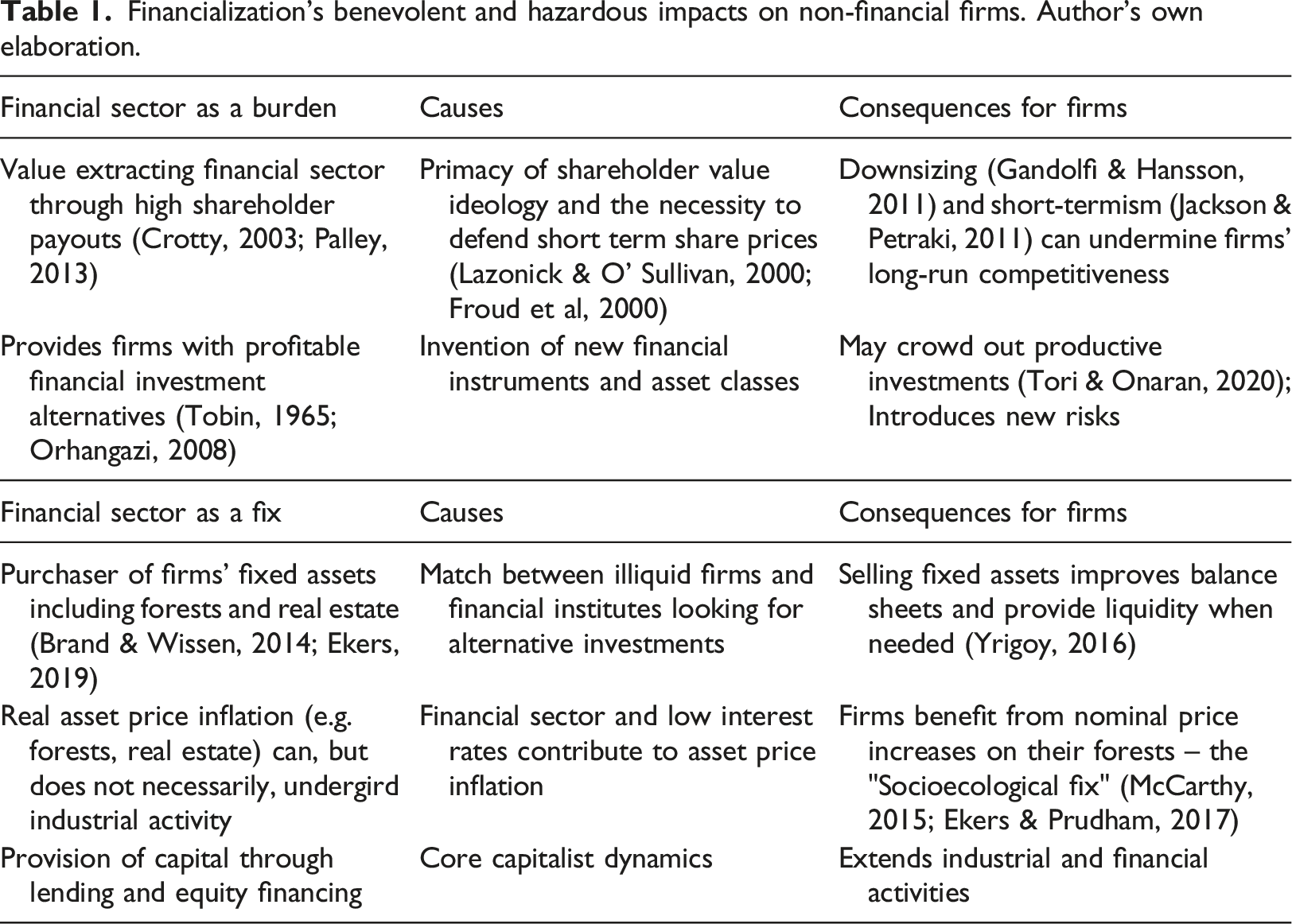

Financialization’s benevolent and hazardous impacts on non-financial firms. Author’s own elaboration.

Historically, global commodity markets did not correlate with financial markets until the early 2000s, when financial actors incorporated commodity assets into financial portfolios and index funds (Moore 2015:99). The rising financial value of forest assets, and the overall financialization of nature (Brand and Wissen, 2014; Moore, 2015:100) is referred to as a ‘socioecological fix’ that provides yield-hungry investors with alternative investments and income sources (McCarthy, 2015; Ekers and Prudham, 2017; Ekers, 2019). In this article, the socioecological fix is broadly defined as a fix that ‘maintain accumulation by enrolling new elements of nonhuman nature into circuits of [financial] capital’ (McCarthy, 2015:2485). More specifically, while North European forests have been commodified for centuries, the financialization of forests in recent decades have provided yields to institutional investors, which have greatly benefited non-financial firms as is shown later in this article. Similar fixes have previously emerged in other industries, including in the North American forest industry. Between 1983 and 2009, institutional investors bought 43 million acres of forests to a value of 39,7 billion dollars in the US (Gunnoe, 2014) and have become large forest owners in Canada since 2003 following judicial amendments (Ekers, 2019). Airlines, retailing, agriculture, tourist and food industries have likewise swapped fixed assets for cash with financial investors since the 1980s and increasingly since the financial crisis of 2008–09 as a way to improve balance sheets, liquidity and profitability (Yrigoy, 2016).

The main expression of corporate financialization is shareholder value ideology, which emphasizes (quarterly) returns to financial actors over other aims (Lazonick and O’Sullivan, 2000), that was consolidated in the Swedish economy by the mid to late 1990s (Brodin et al., 2000). Although post-war scholars saw benefits of organizational slack (Chandler, 1977), Jensen and Meckling (1976) argued that excess capacity leads to inefficiency, unnecessary diversification and excessive budgets (Luan et al., 2013). As such, cost-cutting and downsizing of employees were defended by academic shareholder value proponents and eventually reached the corporate world. Managers, who previously only downsized reactively during recessions, started to downsize proactively to improve profitability. Layoffs became decoupled from business cycles and no longer depended on the operational success or failure of firms (Fligstein and Shin, 2007). The 1990s have been referred to as the ‘downsizing decade,’ as layoffs of both blue- and white-collar workers became a popular management conduct all over the world (Lazonick, 2010), despite ‘the vast majority of evidence suggests that downsizing activities fall short of meeting financial and organizational objectives’ (Gandolfi and Hansson, 2011).

Some scholars have also discussed shareholder value’s impact on innovation (O'Sullivan, 2000; Lazonick and Prencipe, 2005). Innovation is an uncertain, social, collective and cumulative process that requires experience, trust, creative learning environments, acceptance of failure, sustained finance and independence from profit demands until market maturity (Lazonick, 2010). There is an obvious tension between corporate R&D investments, that are potentially unprofitable in the long run, and financial markets’ expectations of short-term profits (Tulum and Lazonick, 2018). One tenet of shareholder value maximization has been the focus on core competencies and divestments of inefficient divisions, that non-the less can have high innovation potential. According to neoclassical theory, capital markets efficiently reallocate capital from declining industries to the innovative enterprises of tomorrow. This does not hold empirically, as much greater amounts of capital are removed from equity markets than is reinvested in innovation (Perez, 2012:12). Lowered corporate R&D spending at the end of the 20th century follows an international pattern of R&D outsourcing, as business scholars at the turn of the Millennium introduced strategic R&D outsourcing as a way to create competitive advantage (Lazonick, 2010).

Methodology

Interviewees.

Given the complexity of the world, interviewee accounts are not seldom stylized interpretations fused with ideologically biased ‘conventional’ wisdom, especially considering broad, nonspecific and unfocused topics. Problematic issues including inaccurate and selective memory, ex-post rationalization, ideological biases and potential agendas (‘manipulative witnesses’) must therefore be considered when analyzing interviewee data (Smith and Elger, 2014:120). The variety of data-collecting techniques allowed for method triangulation as to remedy the limitations of interviewee data and to increase the results’ reliability, validity and completeness (Buch-Hansen and Nielsen, 2020:42–43). Interviews also enabled the author to contrast and double-check interpretations made from other data-collecting methods utilized in the study (Zachariadis et al., 2013:863–864).

Historical background – Imaginaries, R&D and innovation in the forest industry during the post-war period

Moore (2015) highlights that capitalism has been dependent on ‘the four cheaps’: natural resources, food, energy and labour-power. Sweden’s capitalist development took off in the 1870s following increasing labour supplies amid growing agricultural productivity and high foreign demand for Swedish forest products and iron ore. Sweden became the world’s largest exporter of pulp before WW1 and natural resources still accounted for 50% of exports in the 1950s (Erixon, 1997). Since then, the industry’s profitability turned increasingly volatile. Reoccurring challenges included overinvestments and overcapacity; natural or man-made disturbances of raw material flows; increasingly stringent environmental regulation; tough foreign competition, including from producers in the Global South enjoying cheaper raw material; and competition from the petrochemical industry that outcompeted many biochemical niche products (Melander, 1997). Profitability levels have generally been lower than in other industries (Erixon, 1997; Melander, 1997:175), a well-known fact that contributed to a reoccurring existential anxiety about the industry’s long-term survival.

These characteristics, coupled with large-scale investments in pulp- and paper-mills and subsequent physical path-dependencies, have resulted in a conservative industry culture with industry leaders oftentimes sceptical about the value of (costly) R&D and innovation activities (SPCI, 1992:7; Melander, 1997; Eriksson, 2010:165), instead emphasising strategies based on economics of scale, cost reductions, intensified labour processes (increasing labour productivity) and industry consolidation. However, the industry has also housed innovation optimists, mostly comprising technical staff but also entrepreneurial-minded and visionary capitalists (Brunninge and Melander, 2016; A1), emphasising the potency (Rennel, 2010:349–350) and necessity (SPCI, 1996:9), of innovating into new higher value-added products (Eriksson, 2010). Observing achievements of cellulose applications in chemicals, fuels and clothing during WW2, Glesinger (1949) argued that biochemicals and biorefineries could become promising segments for the future forest industry. Three decades later, Goldstein (1978) demonstrated at the World Forestry Congress of 1978 that wood materials could replace fossil fuels as inputs for global chemical needs (Nilsson, 2009). Throughout the 20th century, wood materials research has also resulted in commercial gains outside of traditional papermaking, resulting in biochemical divisions at some paper producing firms in the post-war period. Contrasting these victories in product innovation with the industry’s overall cynicism towards R&D, a dominant innovation-sceptical imaginary has co-existed and competed with alternative imaginaries emphasising the potential that R&D-intensive innovation has on the industry. Here, imaginaries imply that actors resort to simplified economic, political and social construals, worldviews, sensemaking making systems and semiotic ensembles, as they cannot grasp the complexity of the world in its entirety (Sum and Jessop, 2013).

The upcoming empirical section documents how changes in the North European mode of regulation have impacted on corporate strategies and imaginaries that eventually reinforced tendencies to reduce corporate R&D. The empirical subchapters also document how profitability has been maintained in turbulent times through the institutionalization of a number of fixes, including labour downsizing and writeups of forest assets amid the financialization of forests. The empirical section is chronologically presented in a historically linear fashion, while the subchapters tie into the Regulation Approach’s five core institutions presented in the article’s theoretical chapter.

Accumulation regime change and industrial restructuring in the North European forest industry

Emerging financialization and intensified forms of competition

Following a deep recession in the late 1970s, two currency devaluations of the Swedish currency in 1981 and 1982 fueled seven consecutive years of expanding exports and profits in the forest industry (Rennel, 2008). The Stockholm stock exchange boomed from 1980 following lowered dividend taxation (Investor’s annual reports 1980–1981), financial deregulation and reforms by a previous right-wing government which aimed to stimulate household savings in equity markets (Jonsson and Lounsbury, 2004). Meanwhile, a domestic consolidation period took place in the forest industry, starting with a power struggle between leading firms to acquire the Iggesund mill, the industry’s ‘Roll’s Royce’. Continuing mergers and acquisitions (M&A) activity prompted Stora to increase its dividends from 1985 as an explicit strategy to increase its share price (Annual report). A culmination of the M&A wave was reached during the height of the export and stock market boom in 1990 when two large European firms were aquired by SCA and Stora for unpresidentedly large price-tags (Rennel, 2014:99–100).

Amid scrapped capital controls in 1989 and Sweden’s movement towards EU membership, the CEO of MoDo largely summarizes the industry management’s imaginaries of the future weight of financial markets in 1989: ‘MoDo will become more stock market-oriented during the 1990s. This means that MoDo more than before will focus on profit development, value growth and solidity ... We can expect fierce competition for resources on the international capital markets in the 1990s. Investors will put higher demands on firms… In order to attract capital in the future, we must be able to present competitive key figures for earnings per share, dividend growth and stable profitability over the business cycles’ (Annual report). Stora’s chairman stated later that ‘The 90s will be the decade of competition…. Globalization, an integrated Europe, the overcapacity of the forest industry and [new] environmental regulation will lead to intensified competition. In addition, there is the struggle with other industries for competent employees and available capital’ (Stora’s annual report 1993).

The boom ended in the early 1990s when a domestic financial crisis (Skyrman et al, 2022) took place during a global recession, resulting in a large drop in export demand. Akin to a price-rigging fix, managers in Europe and North America would in earlier times collectively adjust output according to the business cycle to maintain stable price levels, resulting in newspaper prices of 350–400 SEK per ton in fixed prices between 1973 and 1989. New EU-compatible competition laws made such price-rigging activities illicit, resulting in a 30% drop in European newspaper prices in 1992, followed by intensified price cyclicality and managerial uncertainty (Luthbom, 2018:199, 216–217). Also extra-political factors intensified competition between firms. Having grown rapidly following the domestic M&A period, some firms started to question the utility of participating in industry-wide research collaborations through the joint research institute STFI together with smaller firms. STFI was thus heavily defunded from the early 1990s and employees was halved from 306 in 1989 to 161 in 2001, the lowest number in its history (Eriksson, 2010).

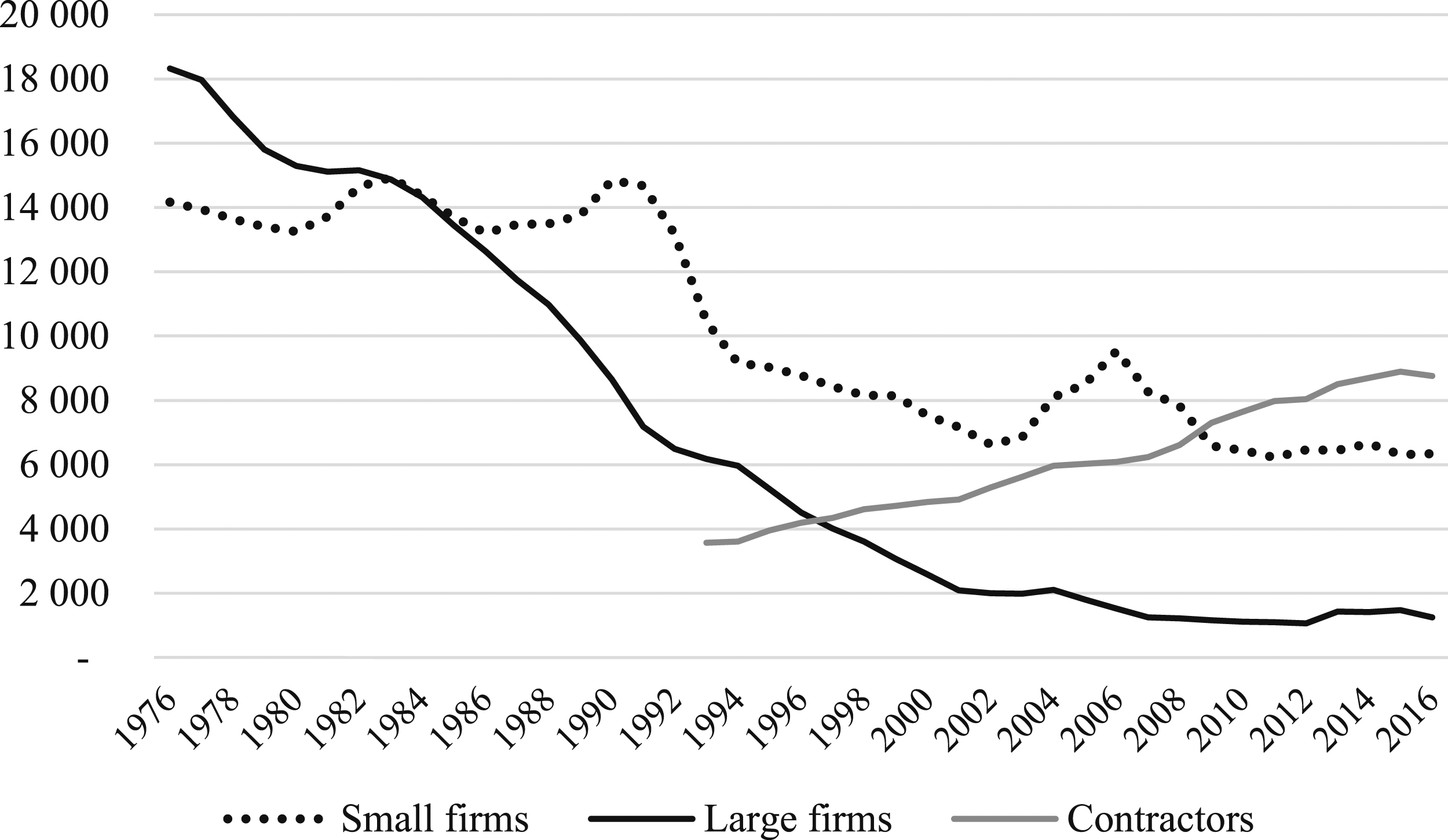

Organizational fixes – increasing exploitation, downsizing and outsourcing during the downsizing decade

Swedish employees and production in the Pulp and Paper industry, 1980-2019.

Source: Stranne et al (2006), Arbetet (2019)

Large firms also externalized wage and vehicle costs by outsourcing logging activities (Figure 1), forcing loggers to seek employment at smaller firms or become timber suppliers themselves, requiring large debt-funded investments in machinery equivalent to several yearly salaries (SIA, 1991). Layoffs and self-employment resulted in longer working hours (Ager, 2012:65) and a rapid decrease in union membership (Kjellberg, 2019), which in turn affected workers’ bargaining power and remuneration (GS-facket, 2011). Kept in a permanent state of competition (Skogen, 2017), many suppliers have recorded low profitability the last three decades (Furness-Lindén, 2008; Skogforsk, 2017) to the benefit of lead firms enjoying cheap supplier contracts. When outsourcing logging activities, lead firms also lowered their ambitions in bringing about technology-enhanced logging productivity: ‘… outsourcing of loggers, downsizing of technical competence at the large firms and R&D cuts at Skogforsk and SLU [two major research institutes] resulted in the end of a successful’ innovation system between machine manufacturers, forest firms and researchers that ‘had worked with success in more than 50 years’ (Ager, 2012:78). At the turn of the millennium, the century long trend of increasing harvest productivity began to decline (Erlandsson, 2016). Logging and silviculture employees in different types of firms. Source: The Swedish Forest Agency.

Insertion into the Post-Fordist international regime and the failure to institute a global spatial fix

Harvey (2001, 2011) elaborates geographical expansion as a key capitalist fix. Spatial fixes were likewise instituted in the forest industry throughout the post-war period, with periods of local industry consolidation taking place up to the 1960s, regional consolidation in the 1970s and nationwide consolidation in the 1980s (Rennel, 2008). As this chapter shows; however, the attempt to create global forest industry champions as a global spatial fix largely failed.

International M&As became increasingly common when capital controls were abolished and firms entered the global arena for corporate control in the early 1990s (Van Apeldoorn and Horn, 2007). A common theme of cross-continental M&As was that corporate labs ‘were shut down or disappeared in conjunction with mergers’ in both Europe and North America (SPCI 2004:2) which undermined the industry’s innovation capacity. Although relatively few takeovers took place in the first half of the decade, a global M&A wave swept throughout Europe by the mid-1990s and it was soon perceived that the forest industry lagged behind other industries in this trend. Managers were not used to the new turbulent business cycle fluctuations, as the boom year of 1995 was followed by a slump in 1996, and global consolidation became an established imaginary to create shareholder value (Moore, 1996). M&As and divestments became more plentiful as leading firms attempted to create global champions in the 2000s (Rennel, 2008). Complementary to M&A activities, many firms also embraced the managerial trend of focussing on core competencies, despite the fact that the industry had historically defended against cyclicality through product diversification (Melander, 1997:347). Hailed by shareholder value proponents, while acting in strategic opposition to conventional industry practices (Ottosson and Galis, 2011:467–468), the newly merged Finnish–Swedish firm Stora Enso went from a traditionally vertically integrated company to focus on three core business areas: fine papers, publication papers and packaging boards (ibid., 465–466). Aiming to become a price leader through global market shares, the company bought paper mills on all continents, which, at the end of a global cross-industry M&A frenzy, included the infamous and inflated acquisition of Consolidated Papers in 2000. A poorly performed due diligence, optimism following the peak of an economic cycle, an overestimated value of the US forest product markets and managerial overconfidence resulted in an inflated price-tag for Consolidated Papers. Stora Enso divested its North America operations a couple of years later, incurring losses of between 2 to 3,5 billion euroes between 1998 to 2008 depending on accounting method (Rennel, 2010:138). According to Ottosson and Galis (2011:469), ‘a total of some EUR 7-8 billion in losses accrued through the [company’s] strategy of global expansion through acquisitions and divestments’.

Stora Enso was not unique in this remark. Norske skog transformed itself from a diversified forest company in the 1990s that divested everything except its printing paper segment, went on an international buying spree in order to become a global paper champion, only to file for bankruptcy in 2017. After failed M&A activities in Russia, incurring losses of 575 million SEK (Sjöstrand, 2016:133), the Swedish government decided to divest its paper mills in the listed state-owned firm AssiDomän on explicit shareholder value arguments. Between 2000 and 2001, employees shrank from 18,000 to 2000, while the share price rose by 150%. An R&D chief of staff openly protested the divestiture in national business press, and the corporate lab at the Piteå mill was shut down shortly after the divestment (Dagens Industri, 2001; SPCI 2004:2). When adjusting to the weighted average cost of capital, SCA’s acquisitions of packaging mills amounted to losses of up to 20 billion SEK according to Rennel (2014:187). According to one sceptical investor, ‘SCA… has bought factories for 80 billion SEK over the past ten years and today has a market capitalization of 50 billion SEK’ (SPCI 2008:10). By comparison, the most profitable North European firm has by far been the non-listed cooperatively owned Södra. Not having to defend a share price, while being geographically tied to its homogeneous cooperative owners, company management contemplated to expand internationally in the 1990s but chose instead to focus on its three pulp mills in Southern Sweden.

Downsizing of corporate R&D and new forms of state intervention

As a consequence of the costly 1980s merger period, firms divested their biochemical departments in order to improve their balance sheets. Despite ‘very good profitability of lignin products’ (annual report, 1988), having the largest production in Europe, MoDo divested its lignin products facilities in 1989 while Stora divested its biochemical facilities in 1990. As a way to cut costs further following the early 1990s crisis, downsizing of R&D took place in the sector that traditionally had invested comparatively little in research (SPCI, 1992:7). R&D as a share of revenue varied between 0.5 and 1.9% at individual firms in the post-war period and averaged 0.9% in 1990 (SPCI, 1996:3, 1992:7). The number decreased in the 1990s and further in the 2000s, as the top R&D spender (SCA) allocated 0.55% of revenues on R&D in 2006, compared to 1.2% in 1989. In today’s currency, Holmen more than halved its R&D budget between 1990 and 2020, from 225 million to approxmitaely 100 million SEK. Six corporate labs were shut down between 2000 and 2010 (MoRe, 2010).

In 1996, one professor and industry observer argued that new shareholders’ demand for faster and increased returns resulted in ‘disorientation, apathy and lack of visions … In this situation, management has followed the American concept of cutting costs as much as possible and major downsizing of employees...’ Further downsizing cannot be made without ‘dire consequences for the core business… [The industry] can almost be described as hostile towards R&D… If one strives for short-term goals and lack visions, one sees a limited value of research’. (SPCI, 1996:9)

Another researcher noted that, from the mid-1990s, managers ‘transferred their R&D costs from their own firms (through downsized research) to the state (through expanded university research)’ (SPCI, 2005:6; see also SPCI, 2011:3) as increased public R&D spending ‘illustrates a mirror image of the downsized corporate R&D’ (Novotny and Laestadius, 2014). Meanwhile, the growing number of PhD graduates, following increased government research, could not find work at the downsized corporate R&D departments (SPCI, 2005:6). One senior corporate researcher said that to ‘…propagate for state (R&D) investments is important, but it must be a difficult task to convince politicians to invest if we [in the private sector] have divested [our R&D] and also don’t hire researchers that have been educated in industry-wide projects’ (SPCI, 2005:3).

A long-term chairman at the Finnish company Ahlström testified that ‘the short-sightedness in the industry is obvious. R&D won’t be executed if it is not certain that it will deliver immediate results… R&D expenditures are shamelessly low… State and private institutions that finance basic and applied research are doing their shares. The reluctance is found in the business sector’ (SPCI, 2005:8). Deteriorating status, autonomy and freedom of corporate researchers was likewise recounted in the industry (SPCI, 2004:2, 2005:8; B1). Most crucially, outsourcing of corporate R&D decreased firms’ technical know-how and absorptive capacity, that is, firms' ability to integrate new technology into existing production processes (A1, B1, C1, D1, E1). The CEO at Holmen complained that ‘University research results have to be more clear and researchers must communicate how the research can be used’ by firms, while a researcher maintained that ‘… there is much research that is not used by the industry… The knowledge exists but is not applied’ (SPCI, 2006:2). The loss of absorptive capacity has in turn decreased the industry’s ability to move into new business segments, such as biorefinery applications (Hellsmark et al., 2016).

All in all, thwarted innovation followed from the R&D downsizing, as according to a former strategic controller: ‘By defining the “selection funnel” in R&D so narrowly, the creation of long-term valuable product platforms is made impossible. Only R&D that can contribute to further optimization of existing [products and processes] is requested. Uncertain development investments are avoided. The consequences for innovative power and entrepreneurship are devastating’ (SPCI, 2008:1). This phenomenon was largely global, as 90% of corporate leaders thought that the industry should spend significantly more on R&D according to one international survey (Processnet, 2007).

However, increased talks about product innovation occurred in the industry following the failed M&A period of the 2000s. This materialized in new R&D strategies from 2008 in SCA and Stora Enso whose R&D expenditures doubled within a couple of years, which included the construction of new R&D centres in and outside of Northern Europe as well as the formation of new cross-industry and academia collaborations. Especially, Stora Enso has been in the forefront as the industry’s most research-intensive firm, not least due to its two long-term strategic shareholders, the Finnish state and the Wallenberg family. The latter initiated the Wallenberg Wood Science Center in 2009 in collaboration with Swedish universities and has paid out over 500 million SEK in research grants stemming from the family’s research foundations. Stora Enso also deserted its failed core competency strategy and have widened its product portfolio to include advanced wood building materials, textiles made from dissolving pulp, while pilot plants have been built for biochemical applications and lignin-based carbon materials. However, while retaining support from policymakers, the industry still devotes considerably less resources to R&D than other industries and R&D expenditures at SCA and Holmen are currently at all-time lows. The Swedish Forest Industries Federation itself wants to see ‘at least’ a 50% increase in R&D spending (SPCI, 2017:1), while a report from The Royal Swedish Academy of Engineering Sciences (IVA, 2018) says that ‘… the industry needs to undergo a transformation’ where the industry ‘sees itself as an obvious part of the knowledge economy and becoming significantly more research-intensive than today’.

Increasing financial extraction through dividends and buybacks

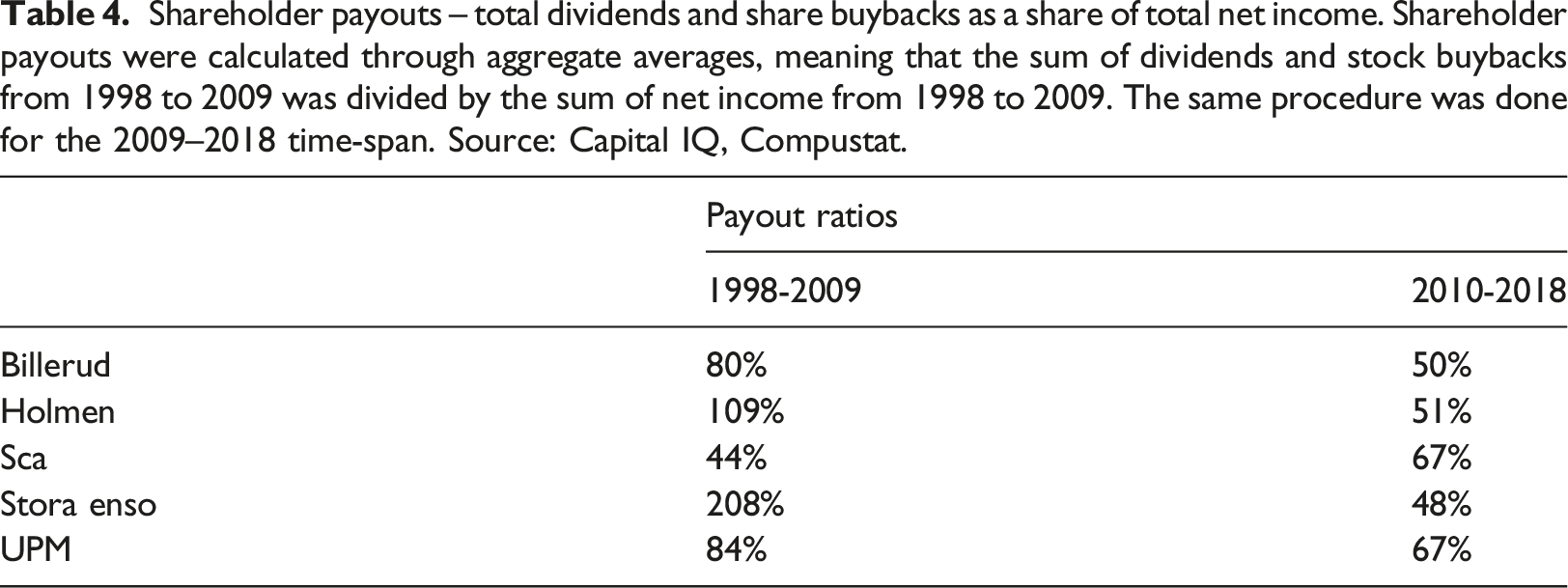

However, while downsizing labour and R&D, increasing value extraction through dividends and buybacks occurred as shareholder value became norm in the Swedish economy (Brodin et al., 2000). As the share of foreign portfolio ownership increased on the Stockholm stock exchange, from in 7% in 1990 to 30% in 1995 to 40% in 2000 following scrapped capital controls in 1989, so too did the influence of foreign institutional investors. In 1996, Goldman Sachs proposed in an open letter to forest industry CEOs that a predetermined dividend yield should be paid regardless if the forest companies made profits or not. According to the investment bank, such measures would reduce managers' freedom of action, but in the meantime increase their credibility in creating shareholder value (Dagens Industri, 1996) In addition, ‘As part of the downsizings, strategy and business development departments have been sharply cut and the dependence on external (and expensive) investment and financial advisers has increased correspondingly’ (SPCI, 1999:8).

In the first half of the 1990s, many firms paid low or cancelled dividends during unprofitable years. Amid suffering profitability, firms increased their dividend yields a way to please shareholders from the mid-1990s. In the words of Stora Enso’s CEO, ‘The shareholders have no reason to complain. We have changed our dividend policy during the business cycle - in principle half of the profits compared to a third earlier - and we have an ongoing repurchase program’ (Affärsvärlden, 2003). One industry observer later referred to Stora Enso as a ‘capital destroying dividend machine’ (Donner-Amnell, 2013), while a journalist referred to Holmen as a ‘printing press’ (Affärsvärlden, 2003), as the firm, with a yearly revenue of around 16 billion SEK, paid out close to 8 billion SEK in ‘special dividends’ in 1999 and 2001 following divestitures.

Amid the acquisition of some forest industry firms by Private Equity funds (Rennel, 2010, 2014), firms likewise became diligent share repurchasers when share buybacks were legalized in Finland in 1997 and in Sweden in 2000 after being prohibited since 1895 (Gårdö, 2003). Stora Enso bought shares worth 1523 billion euros between 2000 and 2005. Its Finnish competitor UPM (SPCI, 1998:6) bought back shares to a value of 1127 billion euros between 1998 and 2001 and in 2005. Major buybacks were also conducted by Holmen (2000 million SEK in 2000) and Billerud (1160 million SEK between 2002 and 2004). An industry analyst argued that ‘financial means are paid out as dividends or used for share buybacks rather than being used for greenfield investments… The message to external actors is simple: “we have no coherent strategies, so we distribute our money [to shareholders]”’ (SPCI, 2001:2). The analyst argued that the industry’s low share prices are a result of ‘… owners and management that have embraced the focus on share price developments and shareholder value’ (ibid).

Shareholder payouts – total dividends and share buybacks as a share of total net income. Shareholder payouts were calculated through aggregate averages, meaning that the sum of dividends and stock buybacks from 1998 to 2009 was divided by the sum of net income from 1998 to 2009. The same procedure was done for the 2009–2018 time-span. Source: Capital IQ, Compustat.

The financialization of forests as a socioecological fix

Following massive destruction of capital, the imaginary of creating shareholder value through M&A was abandoned by the mid-2000s and managers’ spatial horizons moved from global to regional (F1). All in all, the first 10 years of the 21th century was a lost decade for the forest industry (SPCI, 2009:10; Rennel, 2010). Erik Ottosson, Strategic Controller at SCA 1994–1998, wrote that ‘The balance sheets are generally not particularly strong. For a series of years, great values have been returned to shareholders. Arguments have been made that investments [in new products/business models] aren’t needed and that the cash flow generation will be stable and positive for many years to come. Boards and management have tried to create shareholder value through high dividend payments... Conclusion: The Nordic forest industry is in a dangerously weak position for the future’ (SPCI, 2008:1).

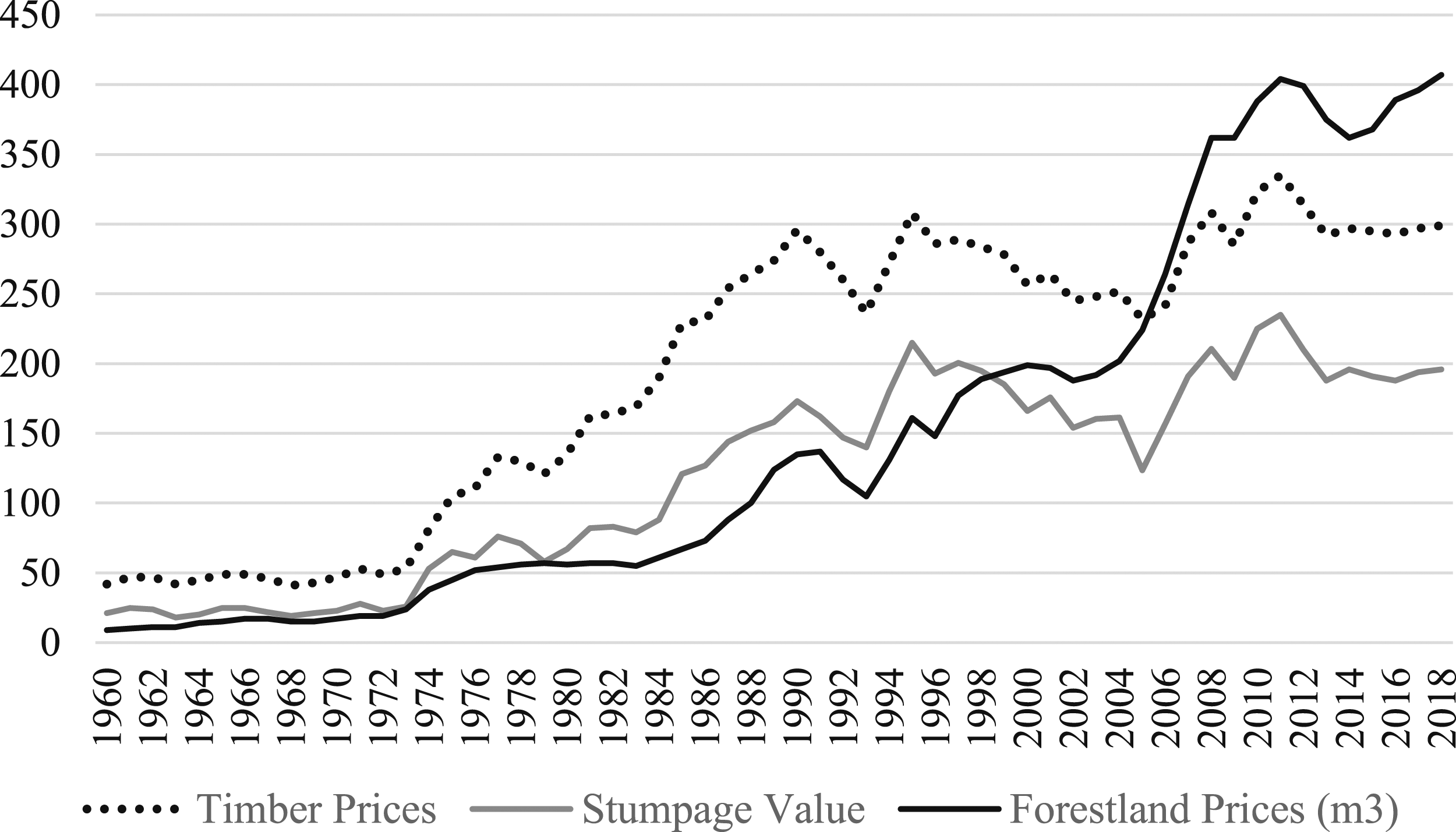

However, financialization has lately had another significant impact on the forest industry. Following low interest rates and institutional investors’ interest in forests as a new financial asset class, forest land prices have appreciated significantly the last decades, and the source of profits have thus increasingly come from financial avenues among lead firms. Forest land prices developed in line with the profitability of forestry (logging activities) until the mid-1990s, whereafter prices rose despite stagnating forestry profitability (Figure 2). This decoupling of forest land prices with forestry profitability coincided with similar upswings on real estate markets, stock markets and the credit cycles starting in the mid-1990s (Andersson and Jonung, 2015). Stumpage Value (the difference between timber revenue and felling costs) and Timber Prices as commonly used proxy measures for forestry profitability, in SEK (real values), and Forestland prices, in SEK (nominal values). Sources: The Land Survey and The Swedish Forest Agency (2022).

Following the burst of the IT-bubble, investors’ interest for fixed, real assets such as real estate and natural resources increased (Lewis, 2005), which put an upward pressure on nominal forest land prices in several economies (Ekers, 2019). Swedish institutional investors became major forest owners in 2004 when Korsnäs and Stora Enso, in order to improve their balance sheets, put their forest assets (valued 17,7 billion SEK) in the newly created a holding company Bergvik Skog AB, of which half was owned and traded by institutional investors. An investor who acquired shares in Bergvik in 2004 would receive a yearly return of 28%, or 1274% over the 15 years (Danske Bank, 2019a). In 2019, Bergvik dissolved into smaller holding companies, some of which were fully owned by institutional investors. In June of that year, Billerud Korsnäs bought back its forests to a value of 6 billion. A couple of weeks later, the pension fund AMF (with a 10% ownership stake in Billerud Korsnäs), bought Billerud Korsnäs’s newly acquired forests for 12,2 billion SEK.

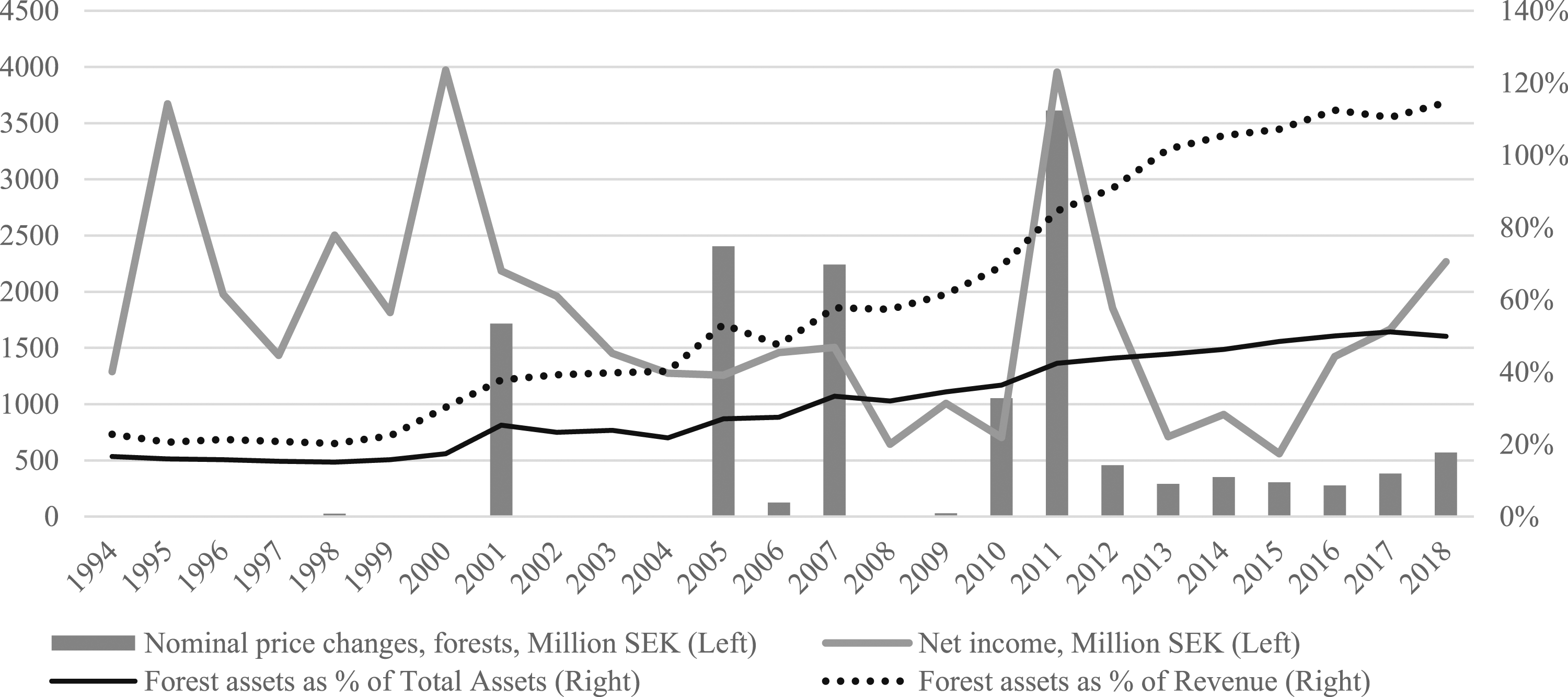

Parallel to ultra-low interest rates and institutional investors’ purchases of forest, firms with major forest holdings accelerated write-ups of their forest assets, despite weakened forestry profitability and the deteriorating ecological health of forests. In 2005, Holmen started to report ‘Change in value of biological assets’ in its income statement. As Figure 3 shows, Holmen’s forest asset write-ups amounted to a total of 7,3 billion SEK between 2010 and 2018, a yearly average of 810 million, and no less than 290 million SEK (in 2013), which significantly improved the company’s balance sheet. SCA’s forest write-ups totalled 15,6 billion SEK between 2005 and 2018 and were often conducted in timely fashion. In 2007, SCA shut down production capacity in its packaging, tissue and sawmill divisions equal to 4900 MSEK, while forest assets were revalued by 5200 MSEK. UPM, the largest Finnish forest owner, has also benefited from nominal value changes in forest assets, totalling 1,45 billion euros between 2004 and 2019. In late 2019, SCA and Holmen more than doubled the value of its forest holdings, from 34 billion SEK to 69 billion SEK, and from 18,7 to 41 billion SEK, respectively, when the firms changed accounting method for their forests, pointing to recent forest purchases conducted by institutional investors. To put those numbers in perspective, the revenue of SCA and Holmen amounted to 20 and 17 billion SEK, respectively. Forest asset price increases in Holmen’s balance sheet. Source: Yearly Reports; Capital IQ.

Concluding discussion

This article has scrutinized industrial restructuring and innovation system governance change in the North European forest industry by examining spatio-temporal fixes and the evolution of the five core institutions that constitute a mode of regulation (Lipietz, 1988:14). The post-war mode of regulation supported capital accumulation in the forest industry by allowing for price-colluding activities that limited uncertainty and price fluctuations, while financial extraction from firms was limited through taxation, resulting in reinvested profits. This generated potential for, but by no means guaranteed, corporate sector induced innovation. However, ‘financialization is an ever-present tendency in corporate capitalism and, once neoliberalism released the constraints against it, it developed rapidly’ (Kotz, 2011). Changes in the mode of regulation have both accelerated crisis-tendences and ameliorated the industry’s profitability crises. Tax reform making dividends cheaper and financial deregulation that incepted and exposed the industry on international markets for corporate control accelerated financialization tendencies in the industry. Increased uncertainty and shortened time horizons following new cyclicality-enhancing competition and expectations of quarterly profits from international capital markets paved way to increased financial extraction from firms.

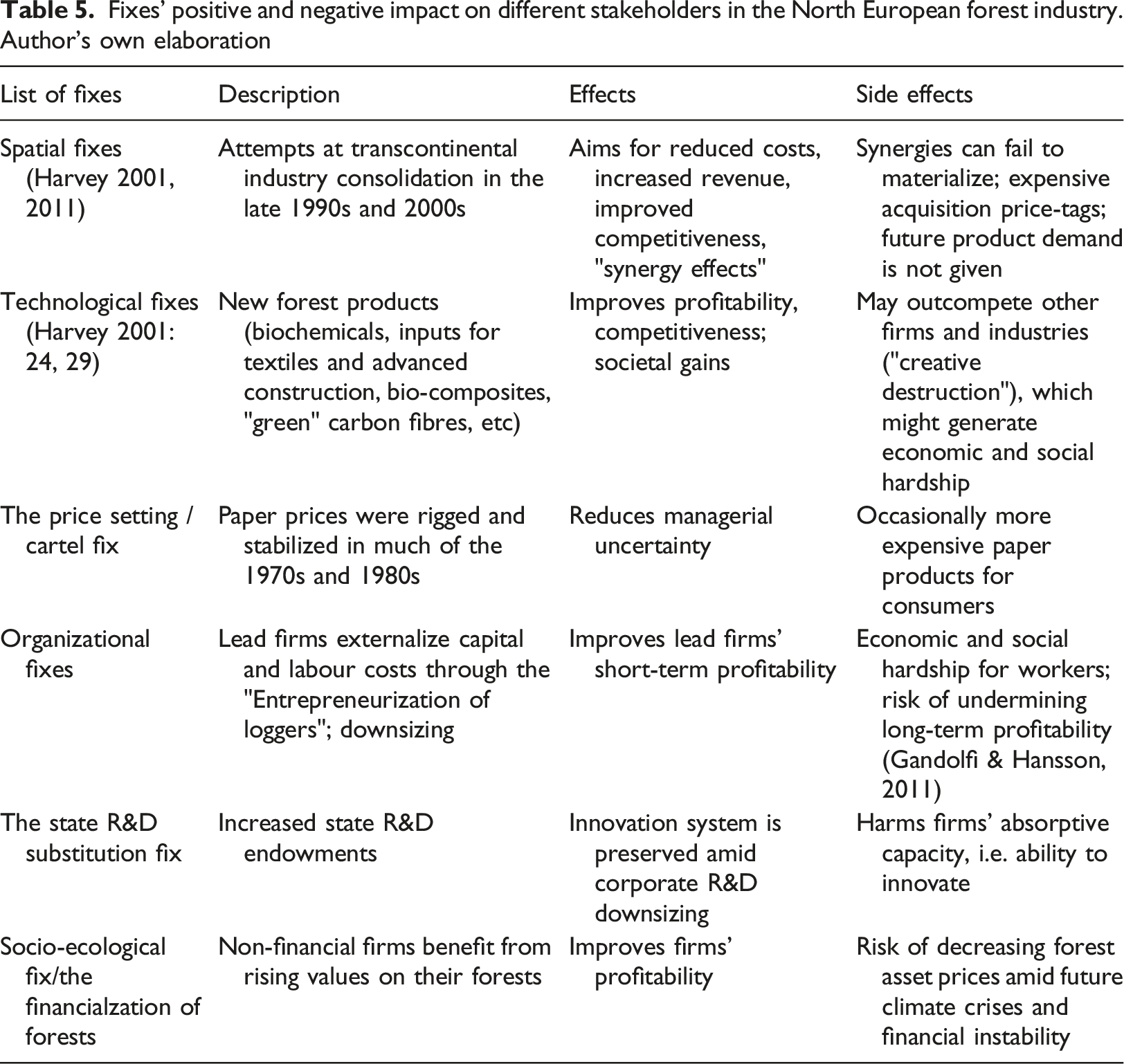

Despite suffering profitability, lead firms have been kept afloat by a number of fixes. As many things can be conceptualized as a fix, one should emphasize that fixes matter differently for particular regions, industries, classes and class fractions. As is highlighted in Table 5, fixes are differently economically efficient in different time and space, differentially benevolent or malevolent to different strata of the (global) population, more or less socially inclusive or regressive, and differently stable, prone to crisis, or externally crisis-generating. From a normative standpoint, some fixes are more economically, politically or socially desirable than others. Organizational fixes (Jessop, 2020:97; Vandaele, 2021:206–207) like downsizing and outsourcing increased short-term profitability for lead firms but was harmful for incumbent workers. The substitution of R&D activities from firms to the state preserved the industry’s innovation system but evidently decreased firms’ absorptive capacity. The technological fix can on the one hand enhance profitability and increase living standards, but on the other hand outcompete firms and industries elsewhere and contribute to redundancies. In the post-war period, Sweden and Finland became world-leaders in forest product R&D (SPCI 2004:2; A1; C1; E2), but as the article has surveyed, this position was lost in the 1990s and 2000s amid corporate R&D downsizing. Moreover, intentions to implement fixes can not only fail but also result in extensive capital destruction. The financialized accumulation regime seems to have reinforced pressures on managers to consolidate globally and institute a global spatial fix, which instead came to intensify the industry’s profitability crisis. More specifically: • On a global market for corporate control, management faced significant risk of being acquired by competitors if they refused to grow through M&As. • M&As became a legitimate and justified conduct from a shareholder value perspective in the industry (Donner-Amnell, 2004:188), and international consolidation was perceived as a viable strategy to deliver shareholder value. • The non-listed cooperative Södra faced considerably less pressures to consolidate globally and kept operations in southern Sweden, which contributed to its relatively high profitability. Fixes’ positive and negative impact on different stakeholders in the North European forest industry. Author’s own elaboration

All in all, financialization has had multifaceted effects on the industry (Table 1). Shareholder value principles such as core competencies, generous shareholder payouts, M&A activities and impulses to reduce organizational (R&D) slack arguably undermined industrial rejuvenation, that is, a stepwise movement from the old papermaking paradigm into higher value-added segments. Meanwhile, firms can exploit the financialization of forests to hedge against asset devaluation by divesting or writing up forest assets in line with rising nominal market values. The financialization of forests constitutes a socioecological fix that temporally stabilizes the current papermaking regime, as forest write-ups undergird industrial activity by improving balance sheets, share prices and credit ratings. By 2022, forest assets equalled 41, 72 and 80% of total assets in Stora Enso, SCA and Holmen, respectively, compared to 15, 12 and 22% in 1990. It was not inevitable that such write-ups would benefit non-financial firms, as shareholder activists from the 1990s and onward have called for firms to divest their forests and put them in listed forest land investment trusts. Dominant blockholders, which characterize Nordic corporate governance, have successfully defended against such schemes. A comparison can be made with the US accumulation regime, where finance-capital rather than industrial capital have benefited from forest asset appreciation (Gunnoe, 2014). A combination of less generous public support, stronger shareholder value norms, larger rates of financial value-extraction, but also a faster decline in paper demand, are seemingly important reasons for a faster forest industry decline in North America compared to Northern Europe. Compared to the US and Canadian forest industries (Ekers, 2019), the socioecological fix has not only benefited financial capital but also North European non-financial firms.

However, it remains highly uncertain if the industry can tackle the problems of profitability, weakened ecological carrying capacity and strained supplier relations, and to what extent the industry manages to commercialize bioeconomy products that can substitute applications from fossil inputs (Nilsson, 2020). As with other fixes, forest write-ups only displace rather than solve the industry’s crisis tendencies. Write-ups have thereto been questioned by some industry observers due to suffering forestry profitability (Figure 2; Nilsson, 2018; SvD, 2019; E2) and ecological exhaustion. Because of climate change, including rising temperatures, less rain and decreased resilience of forest ecosystems due to man-made biological monocultures, wildfires has increased by 231%, storms by 139% and insect pest outbreaks by 600% in Europe since the early 1980s (Hlásny, 2019). Insect pests damaged around 10 million cubic meters of timber in 2018 and 2019 in Sweden (Skogsstyrelsen 2020), prompting a financial analyst to warn against the increased risk of owning forests in the pending climate crisis (Danske Bank, 2019b). As a consequence of the financialization of forests, the industry has not only been exposed to climate risk but also a new type of financial risk. A sudden depreciation of forest asset prices could indeed be devastating.

Footnotes

Acknowledgments

The author wants to thank the editors, including Professor Hulya Dagdeviren, two anonymous reviewers, as well as Laura Horn, Hans-Jürgen Bieling, Lennart Erixon, Claes Belfrage and Markus Kallifatides.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The research was financed by two research foundations – Matts Carlgrens Stiftelse för vetenskaplig forskning och utbildning and Ann-Margret och Bengt Fabian Svartz Stiftelse.