Abstract

This article examines the role of the Big Three asset management firms – BlackRock, Vanguard and State Street – in corporate environmental governance. Specifically, it investigates the Big Three’s relationships with the publicly listed Carbon Majors: a small group of fossil fuels, cement and mining companies responsible for the bulk of industrial greenhouse gas emissions. Engaging with the corporate governance concepts of ownership and control, and exit and voice, it charts the rise to prominence of the Big Three, including their environmental, social and governance (ESG) funds, in the ownership of the Carbon Majors. Having established their status as key sources of permanent capital that are unlikely to exit from their investment positions in the world’s most polluting publicly listed corporations, the article examines how control may be exercised through voice by analysing the Big Three’s proxy voting record at Carbon Major annual general meetings. It finds that they more frequently oppose rather than support shareholder resolutions aimed at improving environmental governance and that their voting is more likely to lead to the failure than to the success of these resolutions. Remarkably, there is little to distinguish the proxy voting of the Big Three’s ESG funds from their non-ESG funds. Regardless of whether these resolutions succeeded or failed, they also tend to be narrow in scope and piecemeal in nature. Overall, the article raises serious doubts about the Big Three’s credentials as environmental stewards and argues instead that they are little more than stewards of the status quo of shareholder value maximization.

Keywords

Introduction

From a position of relative obscurity two decades ago, the ‘Big Three’ asset management firms – BlackRock, Vanguard and State Street – are now among the most prominent players in global financial markets (Fichtner et al., 2017). Together these three firms currently manage over $20 trillion in assets and control 80 percent of the market for exchange traded funds (ETFs) (Braun, 2021). The Big Three own more than 20 percent of shares in the average S&P 500 company, a number that is predicted to double to over 40 percent in the next two decades (Bebchuk and Hirst, 2019a), and have growing ownership stakes in corporations across the OECD (Fichtner and Heemskerk, 2020).

With their spectacular growth the Big Three have been thrust into the spotlight, and a debate has emerged over whether they can or should leverage their massive ownership stakes to influence the companies in their portfolios (Wigglesworth, 2021). This debate has taken on particular urgency in the context of the climate crisis. In the United States, the giant asset managers have come under fire from both sides of the political spectrum, with Progressive Democrats chiding them for not doing enough to push for a low-carbon energy transition, and Republicans accusing them of using their ‘green’ agenda to manipulate markets and raise energy prices to the detriment of consumers (Braun, forthcoming).

For a time, the Big Three seemed to be embracing a role as stewards of a more environmentally sustainable form of capitalism (Mooney and Temple-West 2020). As part of these efforts, the Big Three pledged to introduce new environmental, social and governance (ESG) funds for investors, integrate more robust ESG criteria into their monitoring of and engagement with companies in their portfolio, and perhaps most importantly, become active in proxy voting at company annual general meetings (AGMs) to back shareholder resolutions aimed at bringing business practices in line with environmental sustainability. In his annual letter to company executives in 2021, BlackRock CEO Larry Fink insisted that on his clients’ list of priorities ‘no issue ranks higher than climate change’. Embracing the apparent climate concerns of BlackRock’s clientele, Fink celebrated the ‘tectonic shift’ toward sustainable assets, called for an accelerated energy transition toward net zero emissions by 2050, one that is equitable for ‘vulnerable communities and developing nations’, and encouraged companies in BlackRock’s portfolio to improve disclosure by adopting the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD) and the Sustainability Accounting Standards Board (SASB). Yet in 2022, Fink’s tone changed dramatically, as he declared that business should not act as the ‘climate police’. Citing gloomy economic circumstances, skyrocketing energy prices and the geopolitical uncertainties caused by Russia’s invasion of Ukraine, the Big Three now appear to be caving in to right wing political pressures, treating a rapid low-carbon energy transition as a pipe dream that is incompatible with their primary goal of maximizing returns for investors (Masters, 2022).

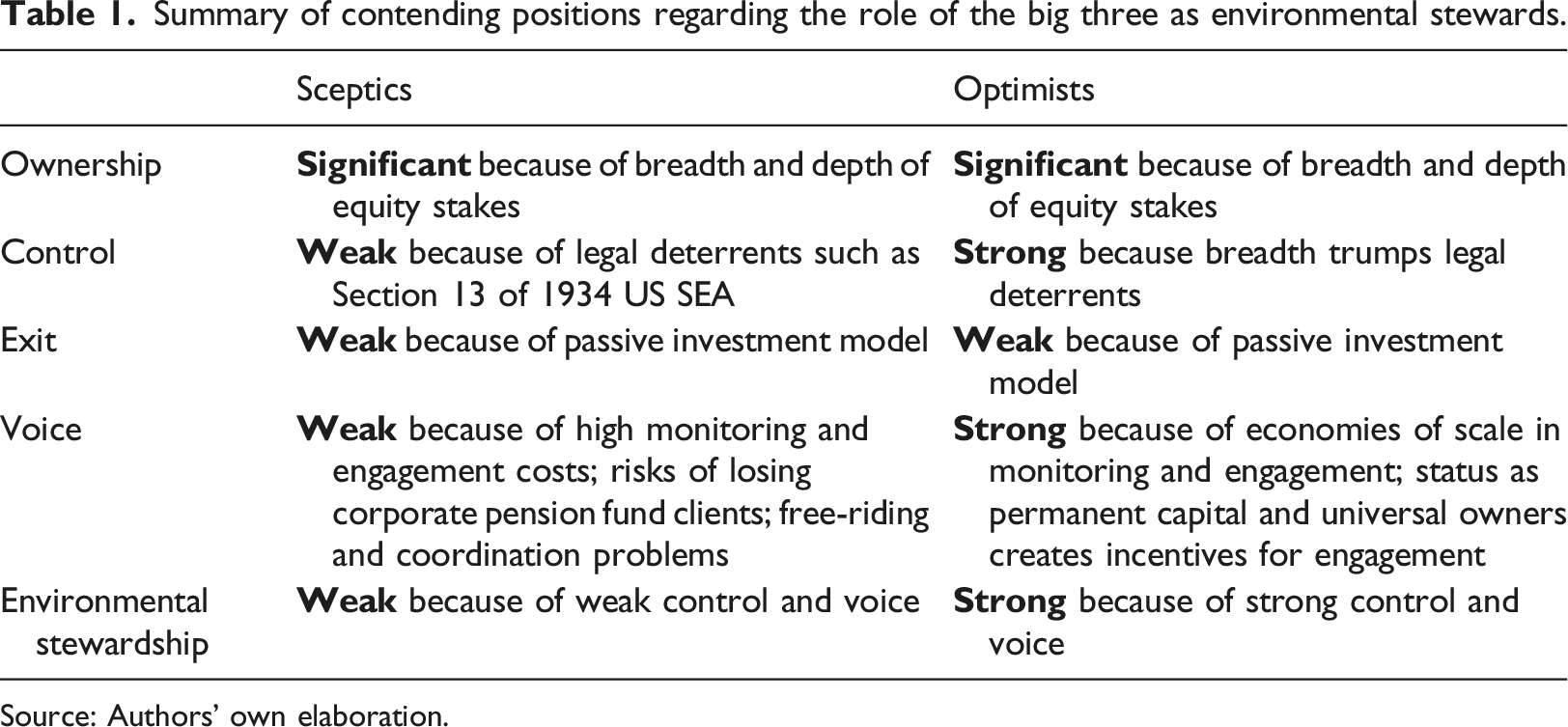

What are we to make of the Big Three’s shifting position on sustainable finance? Is the most recent U-turn a meaningful departure from their putative embrace of climate advocacy in the not-so-distant past? More fundamentally, how much importance should we assign to the actions of dominant shareholders like the Big Three in efforts to avert climate breakdown in the first place? In the growing academic literature on asset management firms, opinion on these types of questions is deeply divided. On the one hand, sceptics claim that the Big Three are unlikely to wield much influence in corporate governance because they act as passive and permanent investors that track broad market indices and employ low-fee business models that are incompatible with high-cost monitoring and engagement. On the other hand, optimists argue that the Big Three’s status as ‘permanent capital’ means they have clear incentives to engage corporate managers and may adopt longer investment time-horizons needed to kickstart a low-carbon energy transition. According to this more sanguine view, the Big Three, as universal owners with a stake in nearly every corporation listed on the stock market, have an interest in the performance of the entire economy, and will therefore internalize the costs of ‘externalities’, including environmental damage.

In this article, we aim to bring much-needed clarity to these debates by providing the most comprehensive study to date of the role of the giant asset management firms within corporate environmental governance. Specifically, we develop what is, as far as we are aware, the first analysis of the Big Three’s relationships with 55 publicly listed companies within the ‘Carbon Majors’: a group of 100 fossil fuels, mining and cement companies responsible for over 70% of industry’s cumulative greenhouse gas emissions since 1988 (Griffin, 2017). In exploring these relationships over long periods of time, we engage with key concepts in the corporate governance literature: ownership and control, as well as exit and voice.

The ability to influence governance outcomes hinges on share ownership. Ceteris paribus, the higher an owner’s equity stake, the greater its capacity to control outcomes. As a first step, our research explores the Big Three’s ownership of Carbon Major equity as it unfolds from 1998 to 2021. Our findings point to the dramatic rise to prominence of the Big Three as investors in the Carbon Majors. 1 Since the global financial crisis, these equity stakes in the Carbon Majors have soared, with BlackRock and Vanguard in dominant positions and State Street the fourth largest investor. Even the ESG funds of the Big Three, we find, are heavily invested in the Carbon Majors. As a growing source of equity financing for the Carbon Majors, and with the Carbon Majors a shrinking component of their investment portfolios, the Big Three are in a strong position to exercise significant power over the corporate governance of the publicly-listed companies at the heart of climate breakdown.

But does prominence translate into actual influence? To assess whether ownership of shares entails control over governance, we need to examine the means through which control is secured, namely, through exit and voice. As permanent owners tracking broad market indices, the giant asset managers seldom threaten to exit from their investment positions (i.e. sell off shares) as a way of influencing corporate management. Instead, the Big Three rely mostly on voice, directly engaging management to shape corporate decision-making. Thus as a second step, our research explores voice by examining the proxy voting record of the Big Three at Carbon Major AGMs since 2014. Here we focus on shareholder and management resolutions in four key areas: environmental governance, buybacks and dividends, director elections and executive remuneration. Contrary to the claims of some researchers, our analysis shows that the Big Three seldom defy management in supporting shareholder environmental resolutions. Astonishingly, we find that the voting behaviour of the Big Three’s ESG funds on environmental resolutions is almost identical to that of their non-ESG funds. The Big Three invariably support resolutions on dividend and buyback approvals, and they consistently back management when it comes to director elections and executive remuneration. This suggests the Big Three are in general alignment with incumbent managers of the Carbon Majors, and they are firmly orientated toward securing short-term shareholder returns rather than promoting the long-term investments necessary for a low-carbon transition. Engaging in a fine-grained analysis of environmental resolutions as a third step, we show that the combined voting decisions of the Big Three are more likely to lead to their failure than to their success, and that, irrespective of whether they succeed or fail, the bulk of these resolutions tend to be narrow in scope and piecemeal in nature. Not only are the Big Three generally laggards rather than leaders in shareholder climate advocacy, such advocacy itself tends to be very limited in ambition.

Overall, in taking a comprehensive approach, our findings indicate that the Big Three’s most recent attempts to distance themselves from sustainable finance are less a U-turn and more a consolidation of a long-standing position of climate obstructionism. For the Big Three, environmental stewardship has always taken a backseat to shareholder value, and so their recent attempts to distance themselves from the rhetoric of sustainable finance in a context of heightened uncertainty should come as no surprise. Our research thus raises serious doubts about the role of shareholders like the Big Three in climate advocacy. At best, such advocacy efforts should be considered a minor complement to wider, more ambitious state-led strategies to bring about a low-carbon energy transition. Yet, in view of our findings, these efforts more likely represent, in the words of BlackRock’s former chief investment officer for sustainable investing, a ‘deadly distraction’ that delays such state-led efforts (Fancy, 2021).

The remainder of the paper is organised as follows. In the first section, we review the existing literature on the role of the Big Three in corporate governance and lay the foundations of our analysis with a discussion of the key concepts of ownership and control, as well as exit and voice. In the second section, we outline our three-step methodology aimed at gaining a more comprehensive view of the role of the Big Three in corporate environmental governance. In the third section, we map the centrality of the Big Three in the ownership network of the Carbon Majors and trace their rise to prominence over time. In the fourth section, we analyse the proxy voting record of the Big Three at Carbon Major AGMs. In the fifth section, we drill down into the data on proxy voting by examining marginal cases where the voting of the Big Three determined the success or failure of environmental resolutions. Finally, in the conclusion, we summarize our key findings and discuss the limits of shareholder climate advocacy.

Debating the Big Three

A growing body of literature has examined the implications of the Big Three’s rise for corporate governance in general, and for environmental governance in particular. As mentioned in the introduction, this literature is deeply divided on the capacity of giant asset managers to influence outcomes. These disagreements stem from differences relating to key concepts in corporate governance: ownership and control, as well as exit and voice.

Ownership and control

In the corporate governance literature, there is a protracted debate stretching back to Berle and Means (2010), whose landmark study boldly proclaimed that the diffusion of shareholding had separated ownership from the control of companies. One conundrum in this debate is to specify the percentage stake required to assert control. Formally, control requires majority ownership (50.1 percent) of shares with voting rights, but with dispersed shareholding, effective control can be exercised with stakes as low as five percent (Davis, 2008; Mizuno et al., 2020). 2 There is a clear consensus within the existing literature that the ownership shares of the Big Three are significant both in terms of their breadth (diversification) and depth (concentration), and that they will likely grow further in the coming years (Bebchuk and Hirst, 2019a). What is disputed is whether the giant asset managers will use these ownership stakes to exercise meaningful control over corporate governance.

The disagreement centres partly on legal issues. Those sceptical of the Big Three’s capacity to convert their ownership into control point to Section 13 of the United States Securities and Exchange Act of 1934 as a formidable regulatory deterrent (Bebchuk and Hirst, 2019a; Lund, 2018; Morley, 2019). Section 13 subjects shareholders with a five percent or more stake to extensive disclosure requirements if they are found to have acquired their stake with the purpose of exerting control over the company, and sceptics argue that this dissuades asset managers from trying to influence governance outcomes. Optimists, meanwhile, tend to downplay such legal hurdles, claiming that the entities that are subject to such legal requirements, the individual funds of the Big Three, rarely have ownership stakes significant enough to classify them as ‘insiders’ with control over management (Fichtner et al., 2017: 308). Yet, the main source of disagreement in the literature is less about formal laws and more about features that are inherent to the Big Three’s business model. In other words, the debate concerns the precise means through which control is secured, namely, through exit and voice.

Exit and voice

Building on Albert Hirschman’s (1970) classic framework, studies of corporate governance have explored the influence of shareholders through the concepts of ‘exit’ and ‘voice’ (see Aguilera and Jackson, 2003). Exit involves selling shares in a company as a way of registering dissatisfaction, and the threat of exit can be used by shareholders as a way of influencing corporate decision-making. Voice refers to direct shareholder engagements with management through such actions as public campaigns, private meetings and proxy voting at company AGMs.

One of the key characteristics of the Big Three in corporate governance is that they do not tend to exit; as permanent capital they have a reputation for passively following broad market indices and therefore do not divest from the companies held in their portfolio (Bebchuk and Hirst, 2019a: 2034; Jahnke 2019a). Companies may fall out of an index that is tracked by the passive investors, and the threat of falling out of a particular index may compel companies to act in certain ways (Grahl and Lysandrou, 2006; Petry et al., 2021). But this is different from the explicit threats to dump a company’s shares in order to influence outcomes. This is not to say that exit is entirely impossible for index investors. Patrick Jahnke (2019b) notes that passive asset managers can switch indices, they can discontinue funds, they can incentivize their investors to place money in certain funds by reducing fees on those funds, and they can lobby index providers to make amendments to the indices they track. However, such actions are cumbersome and costly relative to simply exiting from investment positions in the way that active shareholders do.

If exit is off the table then how do giant asset managers secure control over corporate governance outcomes? Do they use their voice to compensate for their lack of exit? On these questions the existing literature is sharply divided. Sceptics claim that, as passive investors, the Big Three are as unlikely to wield voice as they are to exit, making them deferential toward corporate managers (Bebchuk and Hirst, 2019b). In addition to the legal barriers of Section 13, the high costs of monitoring and engaging with management go against the Big Three’s low-fee business model. Furthermore, any serious challenges to management could mean a loss of lucrative pension services that asset managers provide to large companies. The use of voice is also deterred by a clear free rider problem as all investors would benefit from monitoring and engagement but only the activist shareholder incurs the cost. Finally, there is a coordination problem: the conflicting interests of the hundreds of funds the Big Three manage, and their tens of thousands of clients, make it difficult to come to a unified position on changes to corporate governance (Lund, 2018; Morley, 2019).

Optimists, however, argue that the prospects for giant asset managers to use voice are considerable (Barzuza et al., 2020; Fichtner et al., 2017). Put simply, the idea is that because the Big Three lack the ability to exit and are stuck with large equity stakes in most listed corporations, they have clear incentives to engage directly with corporate managers, and, due to their large size, they enjoy economies of scale in monitoring. The optimists place much more stock in both the capacity and willingness of the Big Three to use their voice to engage in effective climate advocacy. Two unique characteristics of the Big Three’s business model mean that they have clear incentives to use their amplified voice in ways that promote environmental stewardship (Fichtner and Heemskerk, 2020; Jahnke, 2019b). First, as permanent owners, giant asset managers have the potential to act as patient capital, adopting long-term investment horizons and eschewing a narrow focus on the short-term returns associated with shareholder value maximization (Deeg and Hardie, 2016; Fichtner and Heemskerk, 2020). If major investors are patient, then it follows that corporate managers will be incentivized to engage, among other things, in the long-term investments needed to decarbonize their business activities. Second, the Big Three’s position as universal owners is also conducive to environmental stewardship because it gives them a stake in the entire economy (Azar et al., 2021; Braun, 2016). Since universal ownership involves internalizing so-called externalities, the expectation is that giant asset managers will use their voice as a means of exerting control over companies to reduce the costs of environmental damage across their portfolios.

Toward a more comprehensive approach

Summary of contending positions regarding the role of the big three as environmental stewards.

Source: Authors’ own elaboration.

Universal ownership implies that the Big Three have significant equity stakes across all sectors, including those most responsible for climate change. There seems to be a consensus among sceptics and optimists that the Big Three are significant owners in the carbon economy. Yet, there have been surprisingly few attempts to explore this in a systematic way, with the handful of studies that do exist focusing on snapshots of ownership over short periods of time (e.g. Influence Map, 2018). We offer the first attempt to map the Big Three’s ownership of the 55 publicly listed companies within the ‘Carbon Majors’: a group of 100 fossil fuels, mining and cement companies responsible for over 70% of industry’s cumulative GHG emissions since 1988 (Griffin, 2017). Our approach is the most comprehensive to date in that it examines the Big Three’s ownership of the world’s most polluting publicly listed companies across several different dimensions over an extended period of time.

There is a burgeoning literature exploring the voice of the Big Three in proxy voting at company AGMs (Briere et al., 2019; Fichtner and Heemskerk, 2020; Griffin, 2020; Majority Action, 2020). These studies also tend to focus on short periods of time, and what is more, they examine the Big Three’s voting on shareholder ESG resolutions separately from manager resolutions on short-term objectives like stock buybacks. Our approach offers greater breadth and depth in extending the temporal scope of the analysis and in examining the proxy voting of the Big Three across a wider range of resolutions directly and indirectly related to environmental governance. It is only by considering the asset managers’ use of voice in a more holistic and dynamic sense that we can adequately assess whether they do indeed, as the optimists suggest, swim against the tide, shunning short-term shareholder value maximization and embracing patient environmental stewardship.

Data and Methods

With a more comprehensive approach, we aim to bring clarity to the debates about the role of the Big Three asset managers in the environmental governance of the publicly listed Carbon Majors. It should be acknowledged that state-owned Carbon Majors account for 90 percent of proved oil reserves (Heede and Oreskes, 2016: 15), and that together with privately held Carbon Majors are responsible for roughly two-thirds of the Carbon Majors’ cumulative emissions since 1988 (Griffin, 2017: 8). However, we maintain that analysing the publicly listed Carbon Majors is still of the utmost importance because it allows us to study forms of shareholder activism which are simply not possible for their state-owned and privately held counterparts. If we want to assess the potential for sustainable finance, then our attention should be focused on the publicly listed Carbon Majors that are responsible for the lion’s share of emissions by publicly listed companies. Moreover, even though many of the publicly listed Carbon Majors are dwarfed by their state-owned and privately held counterparts in terms of legacy emissions and existing hydrocarbon assets, the major climate risk of the publicly listed Carbon Majors derives neither from their cumulative emissions nor their proved reserves, but from their ability and willingness to explore and develop new sites of extraction. According to Heede and Oreskes (2016: 18), if these companies follow through with plans to invest in further fossil fuel exploration and production, then they will exceed the carbon budget and push global warming past the 2 degree celsius limit set by the 2015 Paris Agreement. The investment decisions made by the publicly listed Carbon Majors are thus absolutely central to our planetary future.

Methodologically, we follow a three-step process (see also Baines and Hager, 2022). The first step is to map out the prominence of the Big Three in ownership of the Carbon Majors with the purpose of gaging their potential influence or control over those companies most responsible for environmental damage. Utilizing the Bloomberg Professional database, we examine ownership prominence across various dimensions. One dimension is static and involves measurement of the centrality of the Big Three in the Carbon Major’s ownership network in 2021. Another dimension is dynamic and charts the Big Three’s equity stakes in the Carbon Majors from 1998 to 2021. Specifically, we measure the position of the Big Three in the rankings of top owners of Carbon Major equity, the overall value of Carbon Major assets in the Big Three’s portfolios, the Big Three’s ownership of the Carbon Majors as a percentage of the latter’s total market value, and the Carbon Majors’ assets as a percentage of the Big Three’s total assets under management (AUM). Tracing ownership across these dimensions gives us a comprehensive view of the potential power relations between the Big Three and the Carbon Majors. More specifically, this method gives us a sense of both the degree to which the Carbon Majors rely on the Big Three for equity financing, as well as the relative importance of the Carbon Majors in the Big Three’s investment portfolios. As part of our mapping of prominence, we also compare the ownership stakes of the Big Three’s non-ESG and ESG funds in the Carbon Majors.

The second step in our analysis is to explore voice by examining the proxy voting record of the Big Three at Carbon Major AGMs from 2014 to 2021. We use the Proxy Insight database to map out the Big Three’s voting on shareholder and management resolutions across four key domains: environmental governance, buybacks and dividends, director elections and executive compensation. As part of our examination of voice, we compare the proxy voting record of the Big Three’s non-ESG funds to their ESG funds. When it comes to shareholder resolutions regarding ESG, it is important to note that even shareholder resolutions regarding ESG that obtain majority approval are normally ‘precatory’. In other words, they are intended to advise management on the shareholders’ preferred direction of company policy and strategy, but they are not legally binding (Neville et al., 2019: 111). Though they are not sanctioned by law, we argue there are several reasons for examining the Big Three’s proxy voting record on resolutions as a facet of voice.

One reason is practical. BlackRock itself admits that behind-closed-door meetings may be more effective in steering corporate policy than votes against management (Fichtner et al., 2017: 318; see also Azar et al., 2021). But the problem with trying to systematically analyse this facet of voice is that it is often hidden from view. An advantage of examining proxy voting is that the data are publicly available and more amenable to precise numerical mapping. Another reason for focusing on proxy voting at AGMs is more substantive. While lacking legal status, shareholder resolutions can play a vital role in raising awareness and shifting discourses and expectations on corporate governance (Neville et al., 2019). At the same time, if shareholder resolutions are indeed meaningless, it should be costless to vote in support of them. We can therefore regard proxy voting as a minimum baseline for exercising voice. If the Big Three do not throw their weight behind non-legally binding ESG resolutions then we have little reason to think that they will support more robust forms of engagement.

We examine manager resolutions on buybacks and dividends because in the literature on financialization, share repurchases and dividend payouts are considered a proxy for short-termism (Lazonick, 2014). By diverting resources to dividends and buybacks, companies prioritise short-term share returns, which may militate against the long-term investments required to decarbonize their business models. For example, money that flows to shareholders in the form of dividends and stock buybacks could instead be spent on investments in renewable energy (Kenner and Heede, 2021: 6; see also Choquet, 2019). We also examine Big Three voting on resolutions on board appointments because, much like dividends and stock buybacks, the balance of Big Three’s votes for and against on these resolutions gives us a general sense of the degree to which they are willing to rebel against management. Part of the reason why giant asset managers are deemed passive is precisely because they tend to vote with management on crucial issues such as the appointment of directors (Fichtner et al., 2017). Furthermore, although not all proxy battles over company directorships at the Carbon Majors are tied to environmental issues, some of the most high-profile ones are. For example, in May 2021 the Big Three made headlines at ExxonMobil’s AGM for going against management and voting in support of the ‘climate friendly’ candidates for the board put forward by a small hedge fund named Engine No. 1 (The Economist, 2021: 61–62). Examining the voting record of the Big Three on shareholder and management resolutions of this type allows us to place episodes like the Engine No. 1 revolt at the ExxonMobil AGM in a broader context, to gage whether it is a ‘one-off’ or part of a wider pattern.

Additionally, in step two, we examine resolutions on executive compensation because while executive compensation need not be directly related to environmental concerns, where such compensation is tied to performance-related financial metrics, Carbon Major executives may have incentives to prioritise short-term objectives that conflict with the long-term decarbonisation of their business models (Plender, 2021). And where their compensation is tied to production metrics such as oil and gas reserve replacement ratios, Carbon Major executives have a direct set of incentives that stand against efforts to reduce emissions (Kenner and Heede, 2021). More generally, the Big Three could side with shareholders and against management on remuneration for the simple reason that they consider it excessive. In this way, the proxy voting record of the Big Three on executive remuneration provides another indicator of their willingness to go against management. The main purpose of step two of our analysis is thus to assess whether the Big Three are using their voice to champion environmental stewardship or to uphold the status quo of shareholder value maximization as overseen by incumbent managers.

The third and final step is to drill down into proxy voting, examining marginal cases where the combined voting shares of the Big Three determined the success or failure of environmental resolutions at the Carbon Majors. Looking at marginal cases is a way of assessing whether voice translates into control, and whether that control is being employed to facilitate or obstruct ESG. An advantage of the Proxy Insight database is that, in many cases, it includes information from the shareholder on reasons for voting in a particular way. Beyond tallying votes for and against, we can leverage these data to develop a richer understanding of the Big Three’s motivations. In addition to information on voting rationale, Proxy Insight also offers a brief description of each resolution, allowing us to evaluate their scope and nature. Here, we can get a sense of whether the environmental resolutions on which the Big Three vote are narrow and piecemeal (i.e. focusing on disclosure) or wide-ranging and ambitious (i.e. focusing on achieving steep reductions in emissions or even phasing out exploration and production activities altogether).

Owning emissions: Who holds carbon major equity?

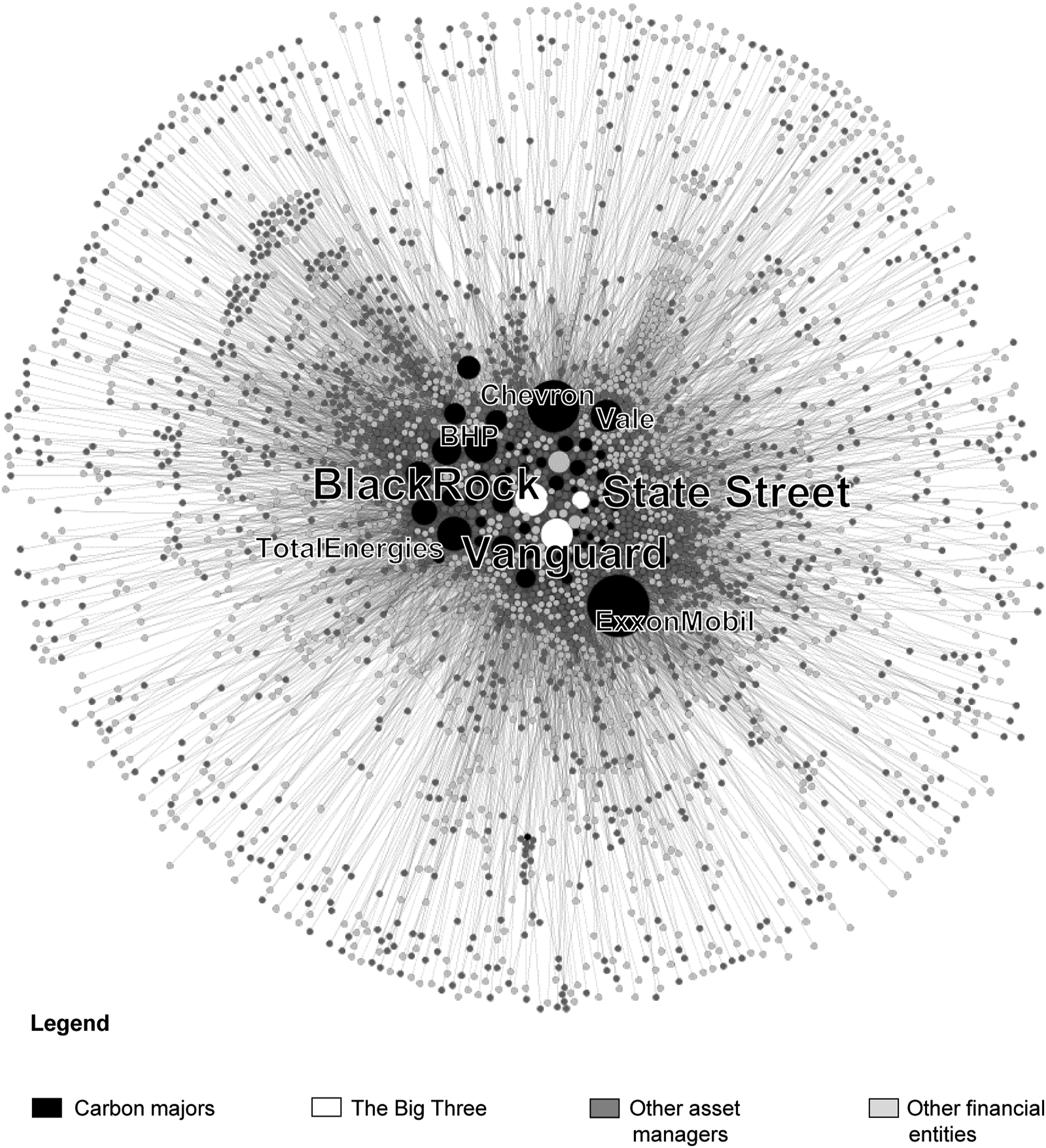

Our analysis begins with an examination of the prominence of the Big Three asset managers in ownership of the Carbon Majors. In Figure 1, we begin with a static view of the centrality of the Big Three in the Carbon Major ownership network in 2021. The figure maps the network of owners of the 51 publicly listed Carbon Majors for which comprehensive equity ownership data are available. This mapping is limited to ownership ties in excess of 0.01 percent of common shares outstanding. The size of each node for the Carbon Majors reflects its market capitalization, and the five largest Carbon Majors by market capitalization are labelled in the figure. The size of every other node reflects the total market value of equity positions taken by owners of these firms, with the ownership position of the Big Three represented by the black nodes. As we see, BlackRock and Vanguard occupy a central position in the ownership network of the Carbon Majors. Their position is much larger than any other investor. State Street, for its part, is less prominent than BlackRock and Vanguard, but is still the fourth largest investor in the network, behind Capital Group. The network of equity ownership in the publicly listed Carbon Majors, 2021. Source: Bloomberg Professional (2021)

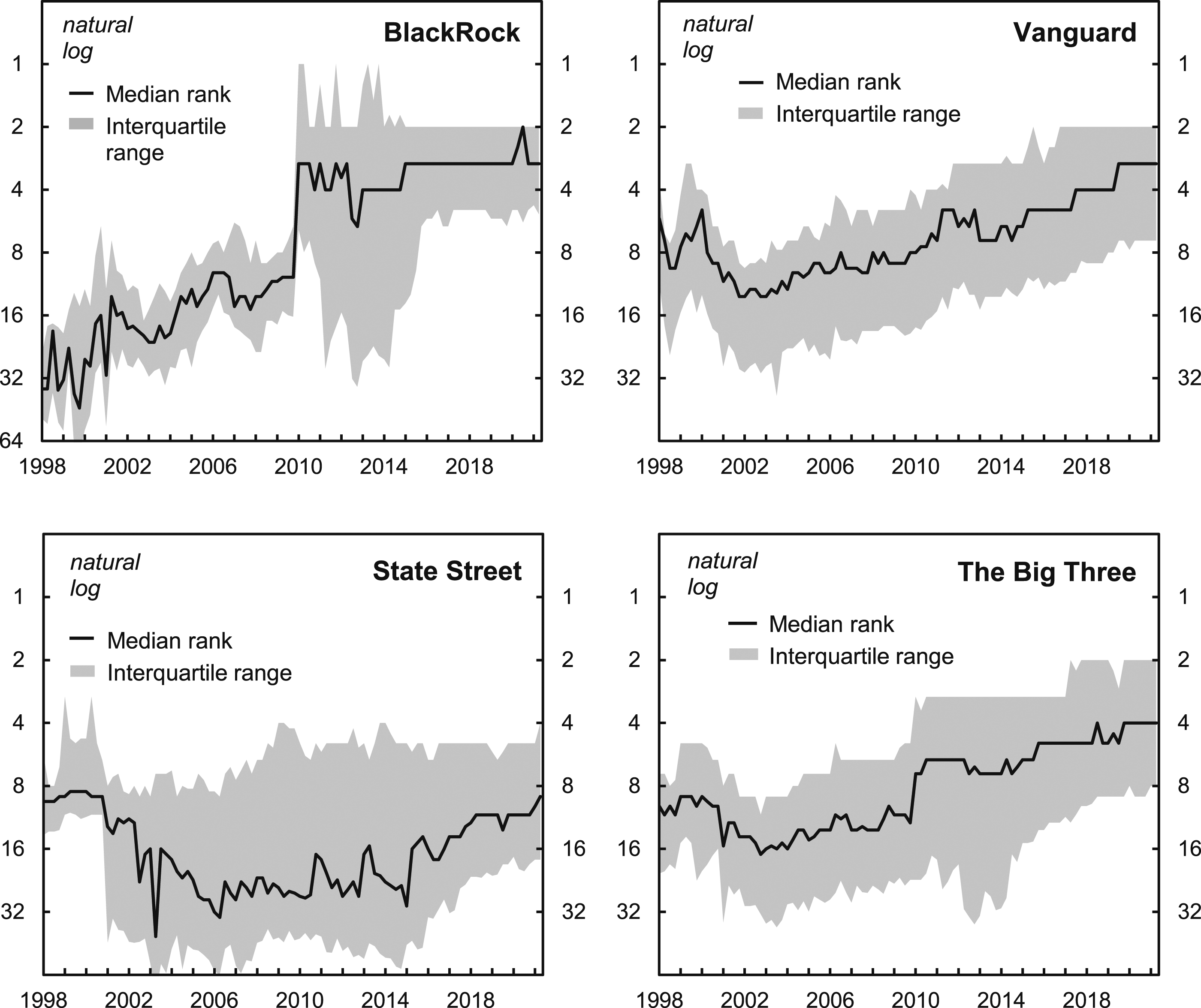

In the remainder of this section, we move to dynamic measures to assess how the prominence of the Big Three unfolds over time. Figure 2 offers data on BlackRock, Vanguard and State Street’s position among owners of the publicly listed Carbon Majors as ranked by size of equity holdings. The data are presented on a natural log scale to facilitate comparison and to draw attention to rates of change. Blackrock’s median ranking increased steadily from the late 1990s to 2009. After its acquisition of Barclays Global Investors in 2009, BlackRock ascended to the uppermost echelons of the Carbon Major equity network with a median ranking of third largest owner. As we see, Vanguard’s median position among the equity holders of the Carbon Majors has risen steadily over the last two decades and it now shares with BlackRock a median ranking of third largest owner. BlackRock’s ownership positions are, however, more concentrated among the uppermost rankings of equity holders in the Carbon Majors as indicated in its narrower interquartile range. The ownership position of State Street fell from the late 1990s to around 2006 but has since rebounded to give it a median ranking of ninth largest owner of the Carbon Majors. The Big Three’s rankings among equity holders of the publicly listed Carbon Majors. Source: Bloomberg Professional (2021)

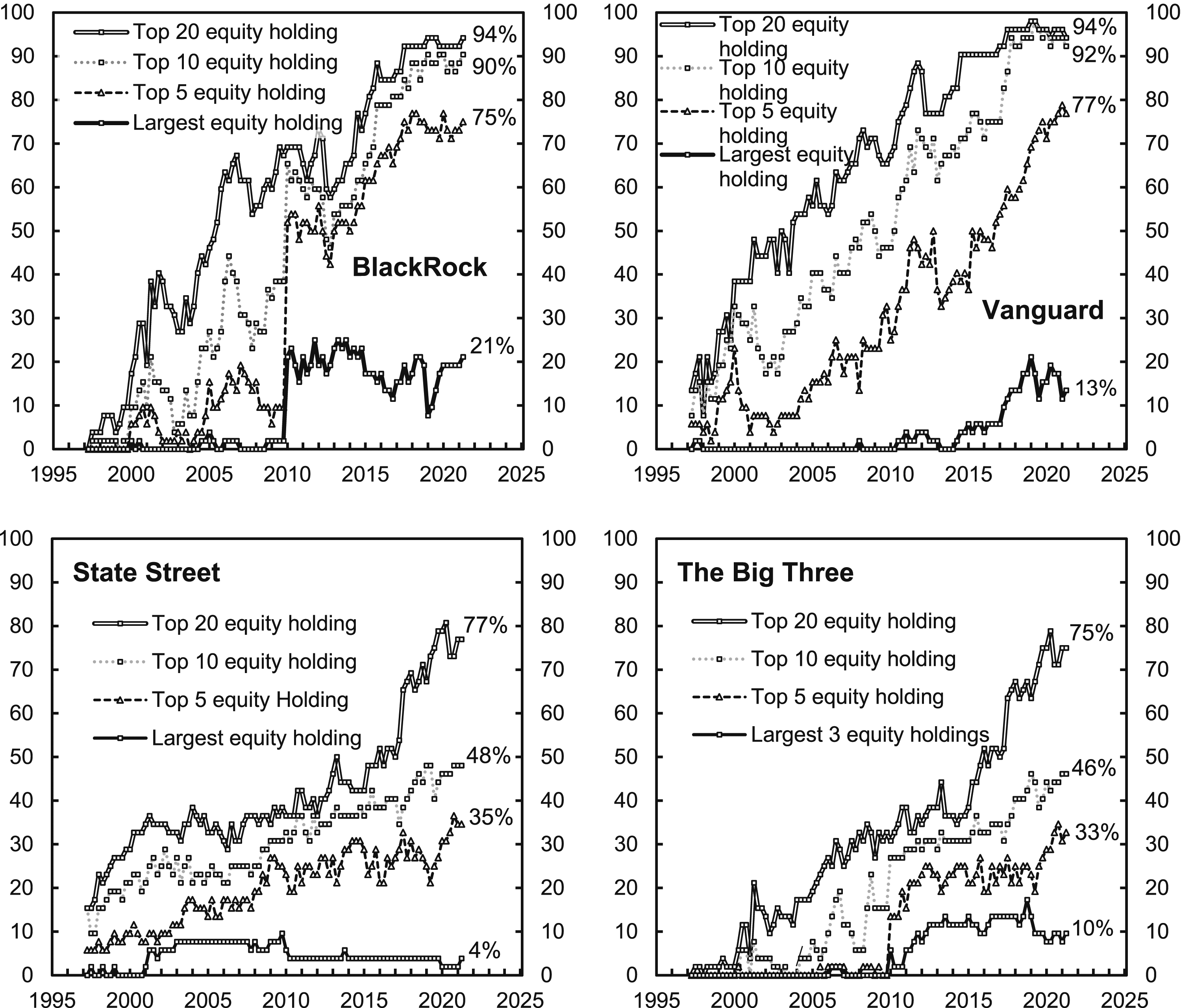

Although Figure 2 offers a vivid depiction of the historical ascent of the Big Three’s prominence in ownership of the Carbon Majors, there are other ways of presenting the data on their equity rankings. Figure 3 shows the percentage share of top 20, top 10, top 5 and largest equity holdings for each of the Big Three. Starting with BlackRock in the top left panel, we can see that it had relatively few equity positions in the publicly listed Carbon Majors in the late 1990s, and that its equity positions expanded significantly in the subsequent two decades. As of 2021, BlackRock is among the top 5 equity owners in 75 percent of the publicly listed Carbon Majors, and it is the largest equity holder of 21 percent of them. As in the previous chart, we can see a significant rise in BlackRock’s equity position after the acquisition of Barclays Global Investors in 2009. The top right panel in the figure shows that Vanguard’s ascent has been similarly dramatic. In the late 1990s Vanguard only had equity holdings in a few of the publicly listed Carbon Majors. But by 2021, it was a top 5 owner in 77 percent of the Carbon Majors and the largest owner of 13 percent of them. State Street has also seen its equity stakes in the Carbon Majors increase over this period, though its share of top 20, top 10, top 5 and largest equity holdings is considerably lower than for BlackRock and Vanguard. The bottom right panel indicates that in 2021 the Big Three were all found in the top 5 equity holdings of 33 percent of the publicly listed Carbon Majors and were the largest three equity holders of 10 percent of them. Decomposition of the Big Three’s rankings among equity holders of the publicly listed Carbon Majors. Source: Bloomberg Professional (2021)

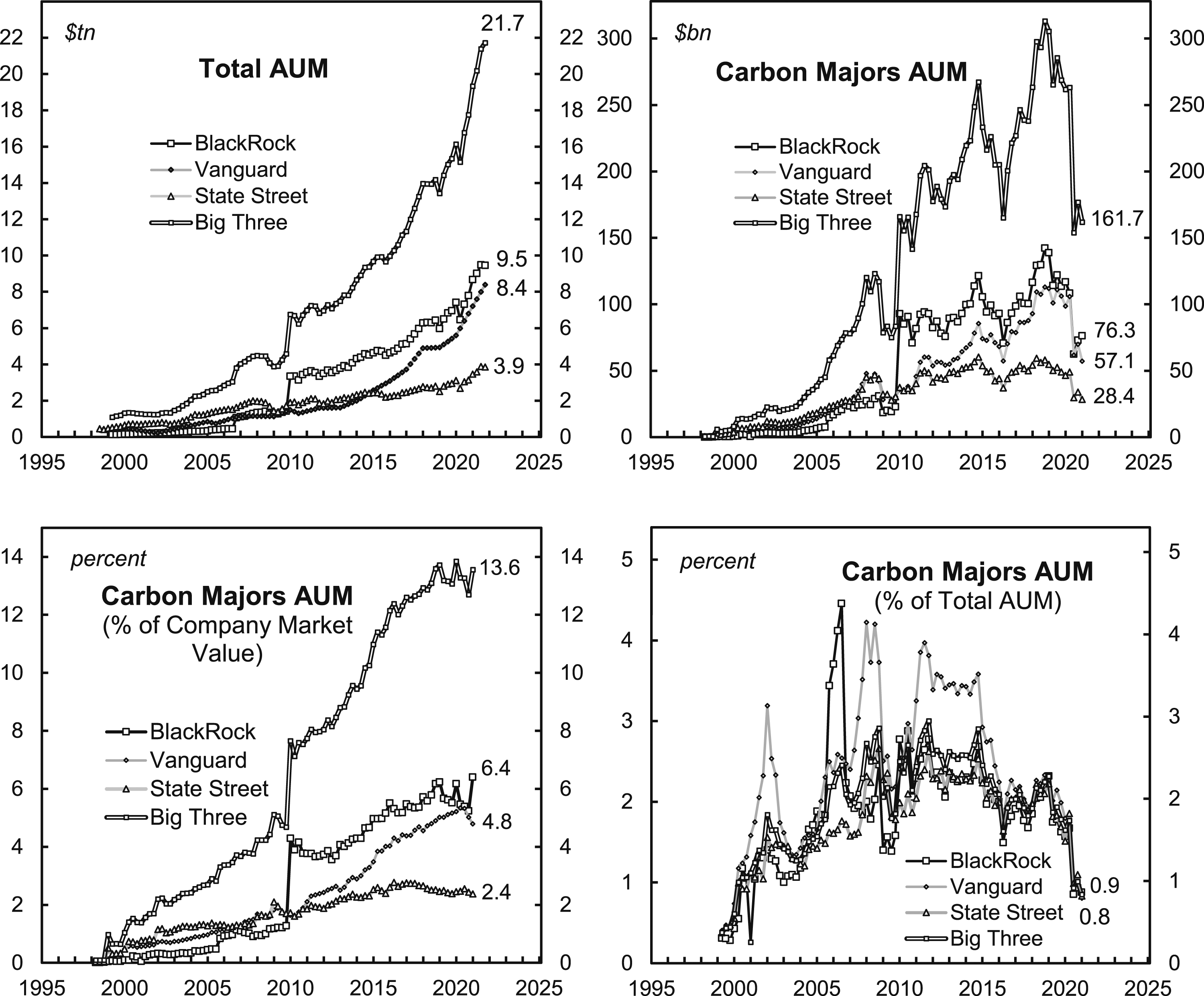

Figure 4 focuses on the Carbon Majors’ share of AUM and market capitalization. The top left panel tracks the total AUM of the Big Three and showcases their dramatic growth. From a marginal position in the early 2000s, the AUM of BlackRock, Vanguard and State Street combined have grown to nearly $22 trillion. The top right panel tracks the market value of the equity holdings that the Big Three have in the publicly listed Carbon Majors. Again, we see a general increase in the size of holdings, but this appears to be heavily modulated by commodity price shifts and concomitant changes in the market value of the Carbon Majors. The bottom left panel shows that as a percentage of the Carbon Majors’ market value, the Big Three’s holdings have increased dramatically over the last two decades, and that together they hold nearly 14 percent of the Carbon Majors’ equity. The role of commodity price shifts and changes in relative capitalization appear to be further underlined in the bottom right panel which presents the value of the Big Three’s holdings in the Carbon Majors as a percentage of their total AUM. Here, we see that the total percentage of the Big Three’s AUM represented by the Carbon Majors has fallen significantly in recent years from a peak between 2006 and 2014 when commodity prices, and in particular oil prices, were at elevated levels. The size of the Big Three’s holdings in the publicly listed Carbon Majors. Source: Bloomberg Professional (2021). Vanguard total AUM data from Wyatt (1998), Fender (2003), Forbes (2005), Investment Management Association (2006), Wyatt (2006), Asia Asset Management (2009), Barr (2010), Bogle (2011), Investments & Pensions Europe (2014, 2015, 2016, 2017), Housel (2017), Kozlowski (2018), Delventhal (2019), Zacks Equity Research (2020), Square Well Partners (2021), ADV Ratings (2022). Note: 22 observations were recorded for Vanguard’s total AUM in the period 1998 to 2021, where Vanguard’s total AUM data is missing it is interpolated.

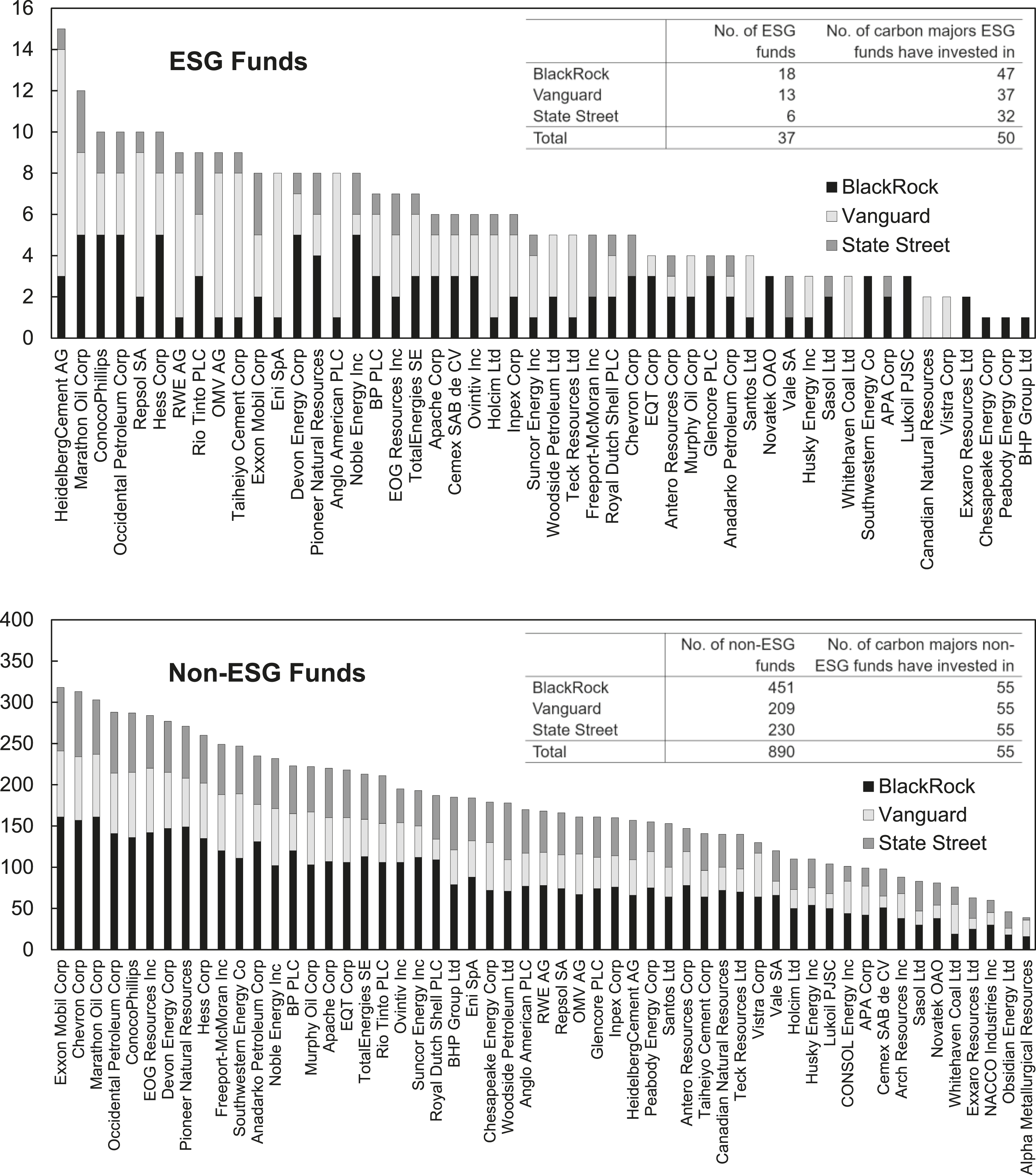

What role do the Big Three’s ESG funds play in relation to the Carbon Majors? There are two different approaches that ESG funds might take: they may either look to avoid ‘sin stocks’ like fossil fuels, or they might seek to retain them with the aim of engaging management to stem environmentally destructive activities (Buller, 2021: 3). In Figure 5, we present data on the Big Three’s ESG and non-ESG funds holdings of Carbon Major equities. As we can see, the ESG funds of the Big Three clearly have a strategy of retention rather than avoidance. There is very little to distinguish the ownership profiles of ESG and non-ESG funds. Of the 55 publicly listed Carbon Majors analysed in the study, no fewer than 50 have been invested in by the Big Three’s ESG funds from 2014 to 2021. The five which have not comprise four coal companies: CONSOL Energy Inc, Arch Resources Inc, NACCO Industries Inc, Alpha Metallurgical Resources Inc; and one Albertan Tar Sands operator: Obsidian Energy. Publicly Listed Carbon Majors in which the Big Three’s ESG and non-ESG funds have invested, 2014–21. Source: Proxy Insight (2021)

The Big Three’s potential influence

To briefly summarize, our network analysis reveals the centrality of the Big Three in the ownership of the Carbon Majors in 2021. Further, we show that the equity stakes of all three giant asset managers have climbed steadily over the past two decades. The global financial crisis marked a key turning point, as the Big Three’s total AUM and their equity stakes in the Carbon Majors soared from 2009 onwards. Even the Big Three’s ESG funds are heavily invested in the Carbon Majors. Our research thus reveals the unparalleled structural prominence of the Big Three in the Carbon Majors’ financial networks.

What we also show is that, as a percentage of their total AUM, the Carbon Majors represent a shrinking component of the Big Three’s overall investment portfolios. In short, what this means is that the Big Three are becoming more important to the Carbon Majors as a source of equity financing, while the Carbon Majors are becoming less important to the Big Three as a source of their overall returns. This puts the Big Three in a position to exercise significant influence over the Carbon Majors, as they can pressure the Carbon Majors to change their behaviour without major ramifications for their funds’ own performance.

The Big Three’s voice: shareholder value or environmental stewardship?

The previous section documented the prominence of the Big Three in ownership of the Carbon Majors. But to what extent does this prominence translate into actual influence over corporate governance? Are they using their position as universal and permanent owners of the Carbon Majors to champion environmental stewardship through long-term, patient capital? In this section, we assess the Big Three’s use of voice by examining their proxy voting record on resolutions at the AGMs of the Carbon Majors.

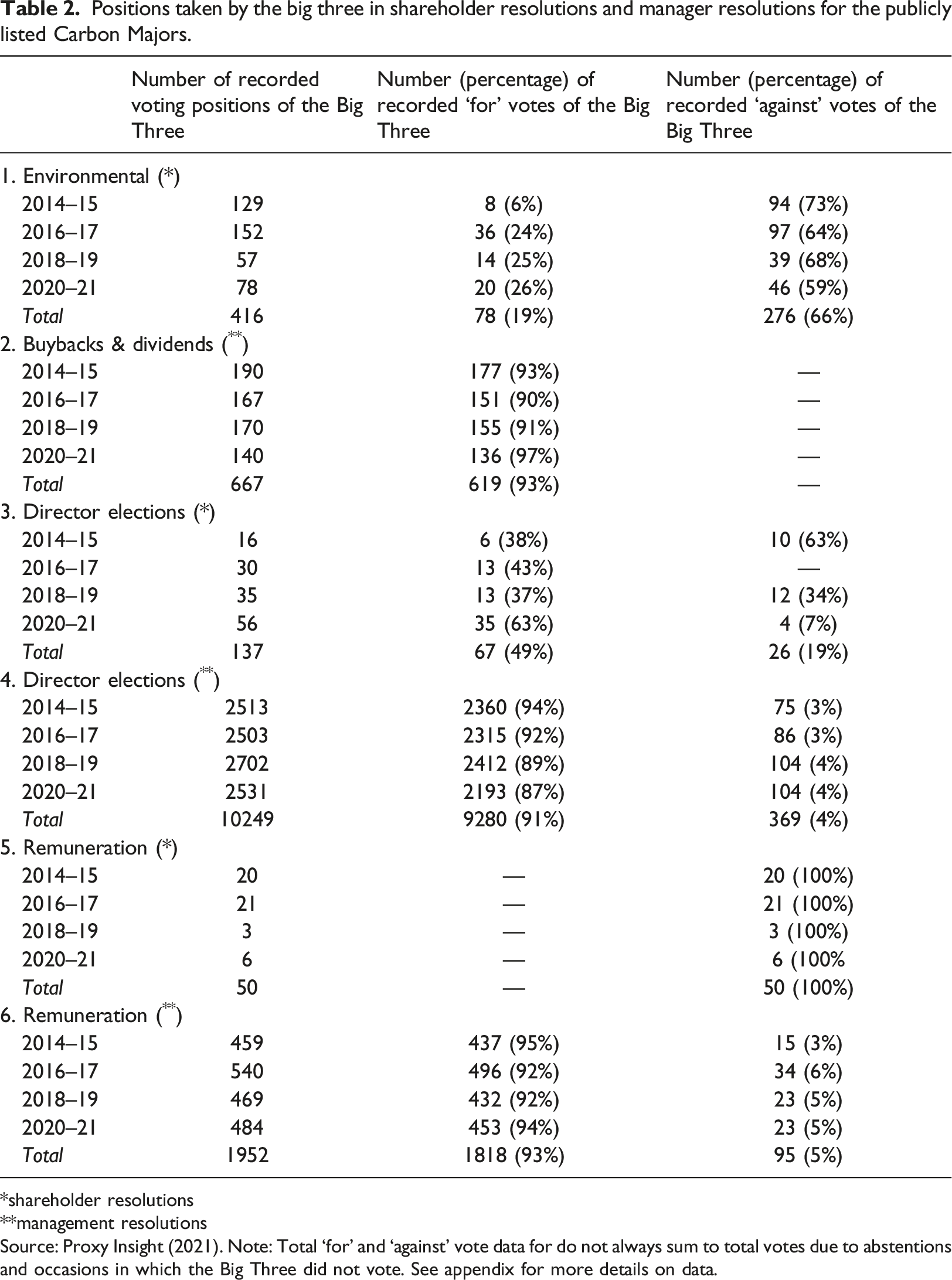

Positions taken by the big three in shareholder resolutions and manager resolutions for the publicly listed Carbon Majors.

shareholder resolutions

management resolutions

Source: Proxy Insight (2021). Note: Total ‘for’ and ‘against’ vote data for do not always sum to total votes due to abstentions and occasions in which the Big Three did not vote. See appendix for more details on data.

The second part of Table 2 shows the Big Three’s proxy voting record on management resolutions concerning dividend payments and stock buybacks at the Carbon Majors. As we see, the track record of BlackRock, Vanguard and State Street is clear from 2014 to 2021, and the Big Three never opposed a management resolution seeking approval for dividend payments and stock buybacks. The few instances where the giant asset managers did not support management resolutions were due to the fact that they did not vote at all.

In part three of Table 2, we see that the Big Three have indeed become more supportive of shareholder resolutions on directors and less opposed over time. But to get a more accurate sense of the degree to which the Big Three are rebelling against the management of the Carbon Majors in the appointment of directors, we need to also consider their far more frequent proxy voting record on management resolutions presented in part four of the table. We see that the Big Three are much more likely to vote in favour of directors put forward by management than those put forward by shareholders. There has been a slight decline in support for directors put forward by management, but the Big Three still overwhelmingly back these management resolutions. Over the entire period, the Big Three vote in support of management resolutions on director elections 91 percent of the time and only opposed them four percent of the time. Therefore, the proxy voting record on the appointment of directors reveals that the Big Three are still very much on the side of the Carbon Majors’ management.

In parts five and six of Table 2, we find the proxy voting record of the Big Three on shareholder and management resolutions concerning executive remuneration at the Carbon Majors. There were very few shareholder resolutions on remuneration voted on by the Big Three. And the message in the table is clear: the giant asset managers have always voted against resolutions on remuneration put forward by their fellow shareholders. In contrast, the number of management resolutions on executive remuneration is considerably larger, and the Big Three almost always vote in favour of them.

Taken together, our analysis of the proxy voting record of the Big Three shows little evidence that they champion environmental stewardship, directly or indirectly, nor does it suggest that they are willing to consistently use their voice against management. But what about the proxy voting record of the Big Three’s ESG funds? Recall from Figure 5 in the previous section that the Big Three’s ESG funds are invested in many Carbon Majors, which may reflect a strategy of retaining their stocks in the hopes of engaging them on environmental issues. According to our research, not only do the Big Three’s ESG funds invest in many of the same Carbon Majors as their non-ESG funds, they tend to vote the same way at Carbon Major AGMs. Based on calculations from Proxy Insight data, we find that, from 2014 to 2021 there were only three occasions in which any Big Three ESG fund voted against the majority of non-ESG funds to support an environmental resolution. This suggests that the retention of Carbon Major stocks by the ESG funds of the Big Three has little to do with engagement and environmental stewardship, even though ESG funds have been found to charge fees that are 40 percent higher than non-ESG funds (Pucker and King, 2022). Overall, then, our findings show that the Big Three generally do not use their voice to defy management and act as environmental stewards. Instead, they appear to be little more than stewards of the status quo of shareholder value maximization.

At the margins: does voice matter?

A remaining issue that cannot be resolved with the data in Table 2 is whether the success or failure of these environmental resolutions at Carbon Major AGMs hinges on the support or opposition of the giant asset managers. In other words, did the proxy voting of the Big Three make any difference to the outcomes? And in those cases where the combined votes of the Big Three did make a difference, was it because of their support or opposition? In this section, we tackle these questions by examining marginal cases where the proxy voting shares of the giant asset managers determined the success or failure of environmental resolutions. We saw in the previous section that the Big Three rarely defy Carbon Major management, bringing into question whether they are willing to use their ownership stakes to exercise meaningful control in corporate governance. By examining marginal cases, we gain a deeper understanding of whether voice is being wielded by the Big Three as a means of control.

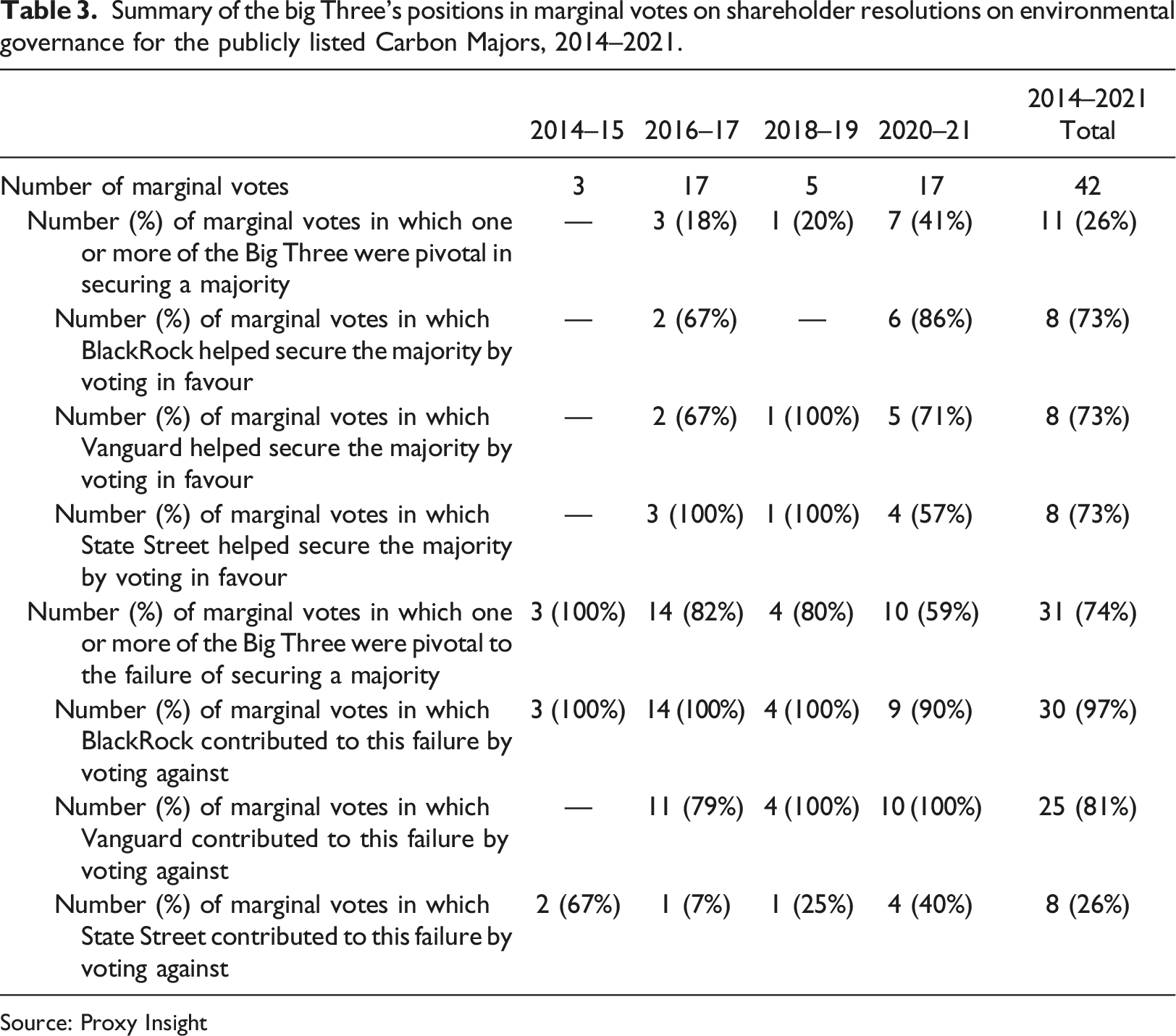

Summary of the big Three’s positions in marginal votes on shareholder resolutions on environmental governance for the publicly listed Carbon Majors, 2014–2021.

Source: Proxy Insight

When examined across time, we see that the obstructionist tendencies of the Big Three have waned slightly, with the declining share of marginal votes to which the giant asset managers were pivotal in voting down. However, the fact that even for the latest period, the Big Three were decisive to the failure of more environmental governance resolutions in gaining a majority vote than they were to the success of such resolutions, suggests that they are still lagging rather than leading general shareholder efforts to improve sustainability performance among the world’s most polluting publicly listed companies. Moreover, when comparing the Big Three, it is notable that BlackRock has been pivotal to the failure of more marginal votes (30 overall) than either Vanguard (25) and State Street (8) despite being the most prominent among the giant asset managers in trumpeting its putative credentials as an environmental steward.

Looking closely at the descriptions of the marginal resolutions in the appendix, we see that the vast majority are focused on the production of reports regarding certain types of emissions (e.g. methane), the impacts of climate-related financial risks, or lobbying activities. Pressuring the Carbon Majors to disclose this type of information is certainly important. But in our view such initiatives tend to be narrow in scope and piecemeal in nature. Take, for instance, resolutions calling for disclosure on climate-related financial risks. Such resolutions are focused more on forecasting the impacts of climate change on investment portfolios, rather than engaging in the immediate action necessary to avert extreme climate change in the first place (Armstrong, 2021). Similarly, resolutions focusing on the need to align political lobbying with publicly declared goals are laudable, but they do nothing to redress the wider systemic issue of corporate capture of government institutions, which is what enables the Carbon Majors to engage in obstructive lobbying practices. Beyond calling for reports, only two of the eleven resolutions that the Big Three swung to successful outcomes involved commitments to reduce emissions (at Chevron and ConocoPhillips in 2021). And none of the environmental resolutions listed in the appendix deal with the most pressing concern of all: namely, the necessity of stopping the publicly listed Carbon Majors from exploring and developing new reserves. Even though the publicly listed Carbon Majors hold only 10 percent of the proved recoverable reserves of fossil fuels, any further investment in fossil fuel exploration and production means that on their own they would exceed the global carbon budget and push warming past the 2°C limit set by the 2015 Paris Agreement (Heede and Oreskes, 2016). Thus, shareholders could have a role to play in dissuading publicly listed Carbon Majors from investing in further development and exploration of fossil fuels, but the marginal cases we examined indicate that it is not on their radar screen.

Earlier we touched on how shareholder resolutions, while lacking legal status, can still play a crucial symbolic role in raising awareness, as well as in shifting discourses and expectations, about the behaviour of corporations. But to be effective in this role, symbols need to reflect the urgency of a given situation. Whether the Big Three determine their success or failure, the rather temperate signals sent out by these environmental resolutions are simply not in line with the drastic action needed to avert climate breakdown.

Conclusion: A ‘deadly distraction’

In this study, we analysed the relationships between the Big Three asset managers and the Carbon Majors. Following a three-step methodology and engaging with key concepts in the study of corporate governance, our aim was to scrutinize the climate advocacy of giant asset management firms by developing the most comprehensive study of their role in environmental governance to date.

First, we looked at the potential influence of the Big Three in environmental governance by charting their prominence in ownership of the Carbon Majors over time. Here we documented the unparalleled rise to prominence of the Big Three, including their ESG funds, in the ownership of the Carbon Majors since the global financial crisis of 2007–2008. As a growing source of equity financing for the Carbon Majors, and with the Carbon Majors a shrinking component of their investment portfolios, we argued that the Big Three have the potential to exercise significant influence in corporate governance. However, as sources of permanent capital, actual influence would not be wielded through the threat of exit, but rather the use of voice. Accordingly, in step two we examined Big Three voice through an analysis of their proxy voting record at Carbon Major AGMs. Contrary to the expectations of some researchers, our analysis showed that the Big Three, including their ESG funds, much more often oppose than support shareholder resolutions aimed at improving environmental governance. Third, we assessed whether voice translates into control through an analysis of marginal cases where the combined proxy voting share of the Big Three determined the outcome of environmental resolutions. Our fine-grained analysis shows that the combined voting decisions of the Big Three are more likely to lead to the failure than to the success of environmental resolutions tabled at Carbon Major AGMs, and regardless of whether they succeeded or failed, the bulk of these resolutions are narrow in scope and piecemeal in nature.

Our comprehensive approach allows us to look beyond the sound and fury of the news cycle and examine the longer term dynamics of corporate environmental governance. Returning to the questions posed in the introduction, our findings indicate that the Big Three’s most recent attempts to distance themselves from sustainable finance are less a U-turn and more a consolidation of a long-standing position of climate obstructionism. For the Big Three, environmental stewardship has always taken a backseat to shareholder value, and so their sudden abandonment of the rhetoric of sustainable finance when market conditions deteriorate should come as no surprise. In other words, the Big Three have generally been laggards rather than leaders in shareholder engagement regarding the climate crisis, and developments in the past year only confirm this.

Overall, then, it is tempting to dismiss the hype surrounding the very limited steps the Big Three made in climate advocacy as greenwashing. Yet judging from our findings, the term greenwashing seems too benign to capture what is at stake. Instead, we side with the view that apparent climate advocacy among the Big Three is best understood as a ‘deadly distraction’, one that diverts attention from the system-level transformations that are urgently needed and that only governments have the power and resources to deliver (Fancy 2021). At best, the climate advocacy of shareholders like the Big Three should be a very minor complement to a wider, more ambitious state-led strategy to bring about a low-carbon energy transition. As a minor component, shareholder advocacy should be focused not on the production of reports, but on demands that the Carbon Majors reduce emissions and cease exploring and developing new fossil fuels reserves. Rather than wait and hope that the giant asset managers will apply the needed pressure to force the Carbon Majors to decarbonize, taxes and subsidies must be completely overhauled to encourage the swift dismantling of carbon-intensive energy systems and the rapid expansion of renewable energy infrastructures. As climate breakdown accelerates, we simply cannot afford any more distractions.

Supplemental Material

Supplemental Material - From passive owners to planet savers? Asset managers, carbon majors and the limits of sustainable finance

Supplemental Material for From passive owners to planet savers? Asset managers, carbon majors and the limits of sustainable finance by Joseph Baines, Sandy Brian Hager in Competition & Change

Footnotes

Acknowledgements

Earlier versions of this article were presented at the Department of International Politics Research Seminar, City, University of London (17 November 2021), the Profiting While the Planet Burns workshop, City, University of London (6 May 2022), and the EuroMemorandum Group Conference, King’s College London (3 September 2022). We would like to thank the participants at these events for their helpful feedback, especially Joel Rabinovich. Thanks also to Joseph Roberts and Ulfa Ali for providing research assistance in the early stages of this project and to Xuying Jiang for assistance in the processing and compilation of the data. Finally, we wish to acknowledge the generous support of the Independent Social Research Foundation, which helped to facilitate this research.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Independent Social Research Foundation; Sixth Flexible Grants for Small Groups Competition

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.