Abstract

The relationship between digitalization and the governance and geographies of global value chains has not been explored systematically. This contribution discusses how digitalization affects the variables that determine the localization of manufacturing, i.e. the substitution of work through automation, the deepening of the customer–producer relationship, the rationalization of distribution through digitalized logistics networks, and the increased modularization of supply chains through standardization and ‘platformisation’. The results of the theoretical exploration defy expectations of a straightforward ‘reshoring’ of production through the combined effects of automation and benefits through a co-localization of companies within their target markets. Tendencies that would support a stronger integration of production in advanced economies are instead being undercut by ongoing countertrends towards fragmentation. The contradictory tendencies of a geographical integration of manufacturing and target markets on the one hand and geographical fragmentation through sophisticated supply-chain organization on the other will affect the technologically facilitated processes of value chain restructuring in a sector-specific manner.

Introduction

‘Thank you robot’, a leading German economic magazine proclaimed as it discussed the prospect of bringing back or ‘reshoring’ investment to Germany due to the combined effects of automation and product customization (Menn and Steinkirchner, 2016). These factors, the argument goes, should render investment in high-wage countries profitable, as labour costs will matter less and the proximity of manufacturers to consumer markets will become more relevant in order to respond to instant changes in demand more quickly. A case in point is the so-called Speedfactory, a cooperation of Adidas with a manufacturer in the German city of Ansbach, which was launched as a project supported by the German Ministry of Economy to explore the prospects of reshoring manufacturing back to the country. ‘When I started at Adidas in 1987, the process of closing factories in Germany and moving them to China was just beginning’, the CEO of the company stated. ‘Now, it’s coming back. I find it almost uncanny how things have come full circle’ (quoted in Whipp and Shotter, 2016).

The difficult reality of reshoring, however, was revealed by the announcement Adidas made in November 2019 to discontinue production at the Speedfactory in Ansbach (and at a similar project in Atlanta in the US) and instead use its Speedfactory technologies at two of its suppliers in Asia (Adidas, 2019).This case illustrates that the relationship between the application of new digital manufacturing technologies and location choices of companies does not result in a unilateral trend towards reshoring but is more complicated. The aim of this paper is to analyse how the application of such technologies affects the international division of labour, which is important in order to assess their impact with regard to the creation (or reduction) of employment in terms of the number of jobs and the quality of work.

The analysis proceeds from a global value chain perspective (Gereffi, 2019; Ponte et al., 2019), that is to say, from a perspective on geographically fragmented value chains, examining modifications in the relationships between end user markets, lead firms and supplier networks and whether this makes a redistribution of value in the global economy likely. It thereby contributes to the emerging discussion about the impact of new digital technologies on global value chains (or global production networks) (De Propris and Pegoraro, 2019; Foster and Graham, 2017; Humphrey, 2018; Li et al., 2019; Sturgeon, 2017).

As will be elaborated in the next section, this paper infers a scepticism towards technology-centred accounts, such as the German ‘Industry 4.0’ paradigm, that make it appear as if technology were an agent in its own right shaping social relations. Instead, the question is raised as to how new technologies affect location decisions of firms by expanding the range of possibilities regarding location choices and their respective advantages. In this sense, the application of technology can have contradictory effects with regard to the question of reshoring. It can create incentives for location choices close to end user markets in advanced economies by altering the cost structure of manufacturing and improving the means for a closer interaction with and faster response to consumers in the very region in which manufacturing is located. However, as with previous surges in information and communication technology (ICT), which in a general sense served as the backbone of globalization processes (see Dicken, 2014: 74–113), it can also result in new ways to fragment and globally distribute distinct tasks in global value chains.

This study builds on secondary literature from the disciplines of economics, economic sociology and organizational theory as well as on empirical cases from secondary literature and the author’s own research. 1 The findings of this theoretical investigation not only help to put overstated claims of reshoring into perspective, but they are also a step towards developing a framework of how the scrutinized variables linked to digital technologies affect location choices of companies across sectors and product categories that are not technology-related.

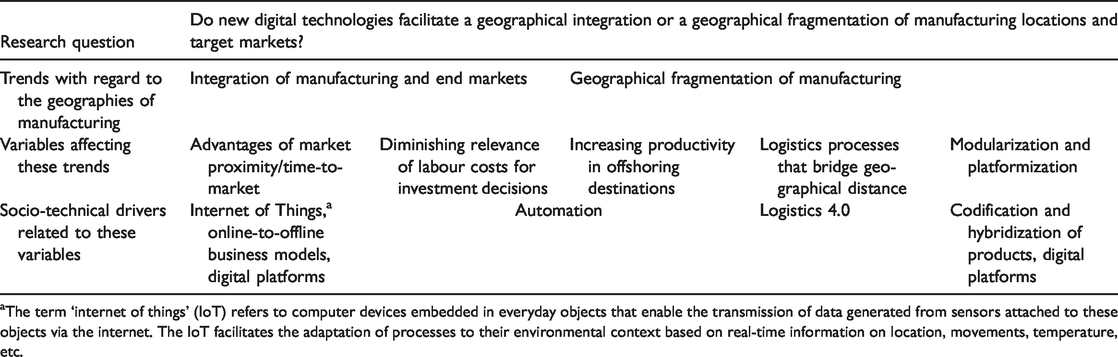

The article is structured as follows (see Table 1). In the following section, I assess the nature of new digital technologies and their relationship to broader socio-technical changes that affect inter-firm relationships. Following this, the third section discusses the impact of digitalization with regard to the question of reshoring by illuminating the key factors at work. I scrutinize to what extent a surge in automation makes labour cost differentials less relevant with the effect that the allocation of manufacturing to high-wage countries could become economically feasible in formerly labour-intensive sectors. In the fourth section, I discuss whether new digital technologies create incentives for companies to localize their manufacturing activities in proximity to end user markets, as new possibilities for the customization of products provide advantages for companies that respond quickly to customers’ preferences. The subsequent section deals with counteracting tendencies by examining how digitally enhanced logistics networks can provide options for lead firms to pursue global sourcing while simultaneously guaranteeing quick market response and a diversification of product supply. In the penultimate section, I discuss whether structural changes related to increased modularization and platformization of product architectures can reinforce such tendencies and thus counteract incentives towards reshoring. In the conclusion, the findings are summarized by stating that the assumption that digital technologies would unilaterally support reshoring is flawed. Trends towards a stronger intra-regional integration of manufacturers and end markets in responsive on-demand production models are counterbalanced by the fragmenting effects of modern logistics networks and enhanced ways to modularize supply chains through the codification and platformization of manufacturing. The digital transformation of the economy will thus lead to new configurations of the local and the global, not a return of manufacturing to advanced industrial economies.

Overview of the analytical steps.

aThe term ‘internet of things’ (IoT) refers to computer devices embedded in everyday objects that enable the transmission of data generated from sensors attached to these objects via the internet. The IoT facilitates the adaptation of processes to their environmental context based on real-time information on location, movements, temperature, etc.

New digital technology, production models and the division of labour

In academic and public debates alike, claims about a disruption of economic relations or a revolution in manufacturing are common and it is hard to distinguish fact from fiction, or sober analysis from media hype. In their much-acclaimed book The Second Machine Age, Brynjolfsson and McAfee single out a set of three characteristics of the digital transformation that would explain an imminent rupture in economic relations: (1) the exponential growth of integrated circuit processor speed and related technological applications, (2) the replicability of digital information at almost zero cost and (3) the ability to endlessly recombine innovations according to the building-block (or the platform/app) principle. Due to these developments, they identify the current historical phase as an ‘inflection point’ (Brynjolfsson and McAfee, 2014: 9) for various game-changing digital technologies through which ‘science fiction keeps becoming reality’ (56).

At a more concrete level, Sturgeon (2017) identifies a bundle of technologies as elements of a new digital economy (NDE) that are characteristic of the present phase of digitalization. 2 He thus relates technological changes to economic forms of organization. Sturgeon lists the following socio-technical developments: advanced manufacturing, robotics and factory automation; new sources of data and the internet of things (IoT); cloud computing; big data analytics; and artificial intelligence (AI). When related to manufacturing, such technologies do not create new social realities in their own right, but manifest themselves in socio-technical solutions for industrial organization. These solutions are ‘social’ insofar as they combine new technologies with modifications of the social organization of production, i.e. by establishing new approaches to the division of labour or by demanding new skills and retraining workers (Hirsch-Kreinsen, 2016a).

New digital technologies are applied by actors in companies in an experimental fashion in order to modify processes, which can result in new paradigms of industrial organization, or ‘production models’, with their own specific product politics, organization of production and labour relations (see Boyer and Freyssenet, 2003: 40–45). In this model, the term ‘product politics’ refers to the strategies of enterprises to address specific market segments like the differentiation of products, quality standards and product cycles. The ‘organisation of production’ characterizes the production processes, the application of certain production technologies, the relationship with suppliers and the governance of innovation processes (Boyer and Freyssenet, 2003: 41).

The German term ‘Industry 4.0’ testifies to the expectation that the application of new technologies will result in a disruptive change in production models, a profound transformation that can be classified as a stage of industrial development (Kagermann et al., 2013). The anticipated outcome is the creation of advanced production models which combine the efficiency of highly automated manufacturing with the flexibility to cater to a highly differentiated customer demand. In terms of product politics, this involves a more direct link between manufacturers and individual customers. Customers can more easily communicate their preferences to firms which can in turn quickly deliver products according to these specifications. In such a model, production efficiency mainly relies on the ability to customize products and guarantee quick time-to-market, rather than just on the capacity for cost-efficient production of large volumes. In terms of the organization of production, this not only requires further steps towards automating manufacturing processes, but also the application of IoT and AI technologies, i.e. methods of data generation and processing through which firms can permanently adjust production processes to shifting market requirements. Industry 4.0 therefore entails the digital integration of the whole value chain in order to guarantee the efficient interlock of processes at all stages of production. Arguably, as the example of the Adidas Speedfactory illustrates, the organization of production would also imply an intra-regional setting in order to combine advantages of a proximity to markets with the ability to tightly integrate supply chains.

Before we scrutinize this expectation systematically, it is important to put the claim of a Fourth Industrial Revolution into perspective. Industry 4.0, first of all, constitutes a narrative about potential developments. Furthermore, it has a techno-centric connotation, as it assumes definite social outcomes related to the development of certain base technologies (see Hirsch-Kreinsen, 2016b; Pfeiffer, 2017). Rather than taking the narrative of a distinct stage of production (regardless of the industry or product involved) for granted, the question ought to be how new technologies are integrated into existing socio-technical settings and whether the results amount to a paradigmatic change in production models. Viewed from this perspective, research has underlined the incremental and path-dependent character of changes as firms selectively invest in a very specific set of applications selected from a bundle of technologies that match their requirements (Butollo et al., 2019; Hirsch-Kreinsen, 2019). In particular, there is a continuity between Industry 4.0 and Lean Production methods which, ever since the 1990s, have aimed to reconcile production efficiency with a growing diversification of products and enhanced flexibility of processes (Womack et al., 1990).

These insights are important for correctly assessing the impact of new digital technologies on the geographies of production. Rather than proceeding from the notion that new digital technologies create their own realities in terms of the international division of labour, the question which demands an answer is that about the degree to which the existing product politics and the organization of production are actually modified through the application of such technologies. Companies’ location decisions depend on a variety of factors that do not only include production costs and time-to-market, but also the costs for transportation, the availability of an adequately skilled workforce, infrastructure, state support and trade policies, to name just a few. The aim of the discussion that follows is not to provide a comprehensive theory of how these factors relate to one another, but to discuss to what extent the application of new digital technologies can affect location decisions in favour of reshoring – or cause the opposite, namely a growing geographical fragmentation of production.

Reshoring and offshoring effects of automation

In the public discourse, automation is treated as a key factor facilitating the new allocation of manufacturing to high-wage countries, since labour costs matter less when production is highly automated. A more localized production is envisioned, one in which fully automated companies cater flexibly to the needs of a regional customer base, thus offsetting the potential disadvantages of higher costs with the advantages of time-to-market and low transport costs (Andersson et al., 2018). While reports of a trend towards a regional integration of end markets and manufacturing are not unfounded (see discussion in the next section), hopes for a trend towards reshoring through automation are. There are various reasons for contending as much.

First, emphatic statements about the feasibility of reshoring usually treat exaggerated claims about full automation as facts. Advances in processor speed and AI have shifted – and will continue shifting – the frontier of what tasks can be automated. The jobs subjected to automation increasingly include not only low-skilled routine tasks, but even highly skilled professional work. In their study of the future of professions, Susskind and Susskind (2015) provide examples of automated or semi-automated functions that affect the work of tax advisors, journalists, lawyers and architects, among others. It is undisputable that new automation technologies will change a great number of professions in a profound way, implying new occupational roles and new ways in which human labour and automated systems interact. However, calculations such as the ones presented by Frey and Osborne (2017), which state that up to 47% of jobs in the US are under high risk of substitution in the future, are not reliable as an approximation to actual labour market developments because there is a gap between the theoretically feasible substitution effects and the actual implementation of automation equipment (cf. Moody, 2018; Pfeiffer and Suphan, 2018). These calculations assume a faultless implementation of automation equipment which contradicts the history of automation. The adaptation of technological solutions to a broad range of uses has always had to struggle with frictions and complex processes of adjustment to the specific materiality of production processes. More importantly, they focus on the sheer theoretical feasibility of automation without scrutinizing the return on investment, a factor which is of paramount importance in order to understand whether automation pays off economically. Besides material costs for technological devices, the efforts required to re-engineer processes and the additional costs related to adjusting work organization and retraining workers are not considered. 3 However, such requirements may well increase as a result of more complex and flexible production systems. In general, the assumption of a comprehensive wave of automation is not consistent with the non-linear and asynchronous implementation of automation technology that is characteristic for the history of automation (Wajcman, 2017).

Second, it is a mistake to assume that the effects of automation will affect industries in high-wage countries the most, especially since key sectors in these regions, such as the automotive industry, are already highly automated. 4 At a global level, China has become the main buyer of automation equipment since 2013, with a share of 30% of sales in 2016 (International Federation for Robotics (IFR) 2017: 16). The bulk of this investment is in ‘catch-up innovation’, that is to say, the installation of robot equipment that has long been established in advanced economies but was too expensive in other places because of relatively high investment costs and the availability of a large supply of cheap labour. Both of these factors have changed in China in recent times, as robot equipment has become cheaper due to progress in microprocessor technologies and labour has become more expensive due to labour shortages and increasing worker aspirations (Butollo and Lüthje, 2017). In this context, there is a large scope for catch-up automation, with the associated effects on productivity and hence on the competitiveness of companies in China and other emerging economies. Taking the present geography of automation as a reference, it seems counter-intuitive to suggest that a surge of automation would support tendencies towards reshoring given that catch-up automation in emerging economies could also have the effect of lowering unit labour costs of producers if productivity-enhancing automation equipment is deployed.

Third, the effects of catch-up innovation also affect low-wage countries close to the US and Western Europe, where productivity gains through automation add to the advantages of geographical proximity to major end user markets. Disinvestment in classic low-wage destinations like China due to rising costs could therefore reinforce trends towards ‘nearshoring’, i.e. a redirection of investment or sourcing from the global to the regional level. This, in essence, is the conclusion of a market research study by McKinsey & Company entitled ‘Is apparel manufacturing coming home?’ (Andersson et al., 2018), which highlights how the adoption of advanced automation equipment could affect the costs of manufacturing. Assuming optimistic scenarios, according to which automation would lead to a reduction of labour time by 40–70% for a pair of jeans until 2025, redirecting sourcing from China or Bangladesh to Mexico or Turkey would indeed become cost-competitive. Reshoring from China to the US, however, would only become cost-competitive if automation led to a reduction of labour time by 70%, whereas such conditions would still be insufficient for manufacturing in Germany to pay off in terms of production costs (Andersson et al., 2018: 19–20). Therefore, even given a frictionless deployment of automation equipment (and neglecting the associated investment costs), projections point towards the feasibility of nearshoring rather than reshoring. 5

If nearshoring prevails, the implications for workers in advanced industrial economies are very different than in the positive scenario envisaged in the reshoring narrative. The pressure for cross-border offshoring would increase rather than decrease as companies in close geographic vicinity to major end markets are able to produce at a cheaper cost without major losses in productivity. This can be illustrated by the case of the European automotive industry, a highly automated sector with the predominance of intra-regional production networks. This industry has been subjected by a surge in automation in Central and Eastern Europe (CEE) as German lead firms require suppliers (mainly for quality reasons) to use the most advanced automation equipment. As some highly automated producers in CEE are now able to offer cheaper unit labour costs, manufacturers in Germany are less able to compete at the level of manufacturing excellency alone and are forced to redefine their roles as innovation-heavy manufacturing hubs in a multi-tiered global production network (Krzywdzinski, 2017; Schwarz-Kocher et al., 2018).

In general, the arguments suggesting a general trend towards the regionalization of manufacturing locations should be qualified, seeing as lead firms pursue multi-tiered sourcing strategies for different product categories and quality levels. Prospects for re- or nearshoring through automation are more relevant for certain niche-product categories in which sales prices matter less (return on investment thus becoming feasible) and for which a quick reaction to market demand is paramount. In fact, the Adidas Speedfactory fits exactly this description as it aimed at the production of limited editions of high-quality shoes with a very high sales price. By no means did Adidas actually pursue the plan to substitute its mass-production facilities in China, Vietnam and Indonesia with factories in Germany. 6 Completely contrary to its representation in public media, the Speedfactory was not a case indicating that Adidas would redirect its sourcing strategies from Asia to Germany, but rather an effort to complement the Asia-centred production system with an additional facility for exclusive products. In a general sense, reshoring therefore ought to be regarded as an option for manufacturers that can be explored for certain product categories rather than a general trend that affects essentially all manufacturing activities regardless of product types and price category.

Intra-regional production in the on-demand economy

If automation does not render a comprehensive reshoring of manufacturing probable, the increasing demand for instant delivery of customized products might. Models of customized mass-manufacturing of the Industry 4.0 type project an economy in which customers order their personalized item which is then produced in a nearby production facility to ensure instant delivery. The vision is one of de-globalization (De Propris and Pegoraro, 2019), of a decentralized production network close to end user markets, an idea that appears in more radical forms as a 3D-printing utopia in which customers send their design to local print shops specializing in their product category and materials. 7

This digitalized version of a manufacturing system that is responsive to rapidly changing and highly diverse market demand is in line with trends towards flexible manufacturing in recent decades. Geographically integrated clusters of SMEs in some sectors proved more responsive to market fluctuations, as they were able to quickly adapt their production volumes, combine manufacturing with strong innovative capabilities and cooperate with their peers for mutual benefit (Herrigel and Zeitlin, 2010; Piore and Sabel, 1984). Production relied on strong feedback loops between innovation and manufacturing, which made the geographical separation of design and manufacturing that had been the hallmark of the early globalization of labour-intensive industries (Fröbel et al., 1981) difficult. A growing differentiation of consumer demand and the prevalence of lean retailing models that rely on a large variety of product supply and a quick turnover of new styles have heightened the importance of a close interaction between innovation and target markets on the one hand and a quick link between innovation and manufacturing on the other (Abernathy et al., 2006; Herrigel, 2015).

Technologies based on the IoT can push the boundaries defining the ability of companies to react quickly to the diversified demand from customers. To be sure, new digital technologies are not the root cause of investment decisions close to target markets, since these represent a long-term trend of tighter market–producer interactions in an increasingly multipolar global economy (Herrigel et al., 2013). However, such technologies can increase the possibilities of transmitting specific customer requests to more flexible and versatile production processes that provide additional advantages for this sort of regional integration compared to global sourcing. As De Propris and Pegoraro (2019) argue, ‘technological change is, therefore, creating a new competitive environment in some markets where value creation hinges on a technology-innovation-production-market continuum’ (230), resulting in benefits for producers who re-bundle innovation and manufacturing processes and co-locate them within the same region.

The ‘smart factory’, as proposed by the Industry 4.0 concept, envisages the possibility of ‘lot-size one’ production, the manufacturing of individualized products without a significant loss in productivity compared to standardized mass-manufacturing (Kagermann et al., 2013). Such factories are projected to manufacture products according to customers’ needs by quickly adapting manufacturing through flexible automation and comprehensive digital monitoring and connection of processes based on IoT technologies. Data transfer between raw products, machines and workers can be monitored and processes can be adjusted in real time according to instant market demand. In essence, this model relies on the intensification of lean techniques of supply chain management, which ensure just-in-time and just-in-sequence delivery of components while avoiding productivity losses due to large inventories (Rüttimann and Stöckli, 2016; Schlick et al., 2014). As mentioned before, so far the Industry 4.0 concept is rather a narrative than a reality. However, the successful implementation of such models could create advantages for companies to react instantly to customer demand, whereas the relatively longer production cycles that are required when manufacturing is set up globally would turn out to be disadvantageous. Technological progress could thus potentially provide further incentives to reshore (or nearshore) manufacturing.

The Industry 4.0 approach, however, represents only one approach towards production systems that more quickly respond to consumer demand. Another path leads via the application of digitalized supply chain coordination techniques that were pioneered in e-commerce. In this vein, the Chinese e-commerce giant Alibaba pursues strategies towards an on-demand production system, originating both from its Business-to-Customer (B2C – retail) and its Business-to-Business (B2B – wholesale) operations. On its main B2C platform Taobao, small brands, often backed or run by web celebrities, have gained considerable popularity and market influence. Ming Zeng, a senior strategist of the company, recounts the example of such a web celebrity, who offered a selection of just 1000 self-created items on the platform, which were sold out within one minute after going online. All sales after that moment were recorded as pre-orders, which were then produced on demand by suppliers: Zhang has almost turned her apparel retailing business into an on-demand business—but at mass-production price points. An order placed on Taobao […] sets the entire value chain in motion. Buyers know that they are reserving clothing that will be made to order and that they will have to wait seven to nine days for manufacturing and shipping. LIN’s partner factories have already begun working on the first batch of preorders. (Zeng, 2018: 12–13)

The result of this distribution-driven approach is remarkably similar to the paradigm of customized mass-manufacturing associated with Industry 4.0 (Zeng calls this ‘C2B’– customer-to-business, see Zeng, 2018: 89–112). Unlike with Industry 4.0, however, the technological capabilities to guarantee a quick reaction to consumer demand do not stem from flexible automation capabilities: entrepreneurs like Zhang use China’s vast and diversified landscape of low-tech suppliers to fulfil the orders. Strikingly, the proliferation of e-commerce-based retail has led to a surge in orders for small-scale producers, often even family-run backyard workshops. In the so-called Taobao-villages, networks of such workshops, specialized in certain product categories, cater to the specific demands of online shoppers (Fan, 2019). As a result of this peculiar mode of ‘flexible specialisation’ (Piore and Sabel, 1984), China’s traditional patterns of local clustering of small-scale producers are brought online – rather than being replaced by highly automated mass producers that are envisaged in the Industry 4.0 paradigm. A similar approach is pursued in Alibaba’s B2B business segment with the so-called Tao factory platform, where buyers gain quick access to a diversified localized production network while local suppliers receive support and upgrading of their marketing functions as they are connected to the online community (see Lüthje, 2019; Schneidemesser, 2019).

In the ‘smart factory’ model of Industry 4.0 and in the ‘smart network’ model of Alibaba, geographic proximity between customers and production networks is paramount in order to reap economic benefits associated with the quick response to diversified demand. If such variants of customized manufacturing were to proliferate, they would reinforce tendencies towards regionally integrated production systems. This also could involve the reshoring of certain manufacturing activities of firms catering to customers in advanced industrial countries. However, there are also new options emerging for an increasing geographical fragmentation of manufacturing, which will be explored in the following section.

Logistics 4.0: Offsetting the advantages of geographical proximity?

As public attention is mainly drawn to visionary models like that of the ‘smart factory’, the relevance of digitalized logistic networks as enablers of flexible manufacturing is largely neglected. And yet it is highly relevant for the evolution of the global division of labour. Indeed, the globalization of production was accompanied by a ‘logistics revolution’ which not only facilitated the transport of goods within and across regions but also became a precondition for lean supply chain organization, which ensures lower storage costs and faster responsiveness to market requirements (Vahrenkamp, 2011). Such tendencies are now driven further towards what has been termed as ‘Logistics 4.0’ (Bousonville, 2017).This term describes the interlinking of processes, objects and supply chain actors through IoT technologies that provide real-time information regarding the location and the condition of objects that can be used to streamline delivery processes (ibid: 5). The generated data can also be used to run AI algorithms in order to detect patterns, which can in turn improve the predictability and hence efficiency of logistics processes. Furthermore, the logistics sector is particularly suited for implementing cutting-edge technologies such as advanced automation (autonomous vehicles, warehouse automation), the IoT (digital tracking systems), big data and AI (predictive analytics) (Coe, 2014). In a way, logistics networks can be interpreted as the material counterpart to the data traffic that is ubiquitous in the modern economy.

Logistics 4.0 is particularly useful for overcoming geographical distance, i.e. for the ‘annihilation of space through time’, as Marx (1973: 23) famously remarked in his early outline of Capital. Particularly relevant factors for the present discussion are the merger between logistics and manufacturing in large suppliers and the e-commerce/logistics nexus. The first of these developments relates to shifts in supply-chain governance in which lead firms transfer significant value-chain activities to large suppliers that typically combine logistics, supply chain management and manufacturing functions. The vertical integration of manufacturing has significantly decreased in recent decades, as lead firms have focused on their core business in design and marketing and the more lucrative parts of product assembly. Such tendencies are not universal and are playing out differently across industries depending on the respective product architectures. In the automotive industry, brand-name companies are often only responsible for 20–25% of value creation, while a significant share of production volumes are provided by first-tier suppliers (sometimes referred to as Logistiker in German) (Schwarz-Kocher et al., 2018). In the garment industry, large sales intermediaries or larger and more capable suppliers have emerged, although supply chain concentration is regularly being undercut by renewed waves of subcontracting (Butollo, 2015; Frederick and Staritz, 2012; Zhu and Pickles, 2015).

In the electronics industry, brand-name companies rely on huge contract manufacturers that supply the entire hardware, often including co-design activities (Chen, 2002; Lüthje et al., 2013; Raj-Reichert, 2019).The common ground between all these approaches is the coordinating role that large suppliers assume by taking on supply chain management and logistics responsibilities in modularized supply chains. As early as the late 1990s, the computer manufacturer Compaq pioneered a hyper-flexible way of organizing the supply chain in cooperation with its contract manufacturer Mitac, which resulted in enhanced capabilities to combine global sourcing with quick market responsiveness. The backbone of this system was the rule that 98% of suppliers would deliver components within three days. Mitac then combined its Korean production facilities with a network of distributed material hubs and the practice of decentralized configuration of products in locations close to the international end markets in order to combine the efficiency of high-volume production with the ability to customize products and time-to-market advantages. Advanced information systems constituted the key technology for the coordination of the supply of modularized components (Chen, 2002). Other electronics manufacturers followed suit, creating the backbone of a flexible manufacturing environment which came to dominate this industry by mastering the pressures related to quick innovation cycles and frequent modifications of products (desktop computers, laptops, various generations of mobile phones, etc.). Their production facilities did not need to be located close to end markets since the combination of digital data transfer, downstream product customization and sophisticated logistics could ensure the fast delivery of products that were adapted to the requirements of target markets although the bulk of hardware production was located overseas.

The second development, a new responsiveness of supply chains through the e-commerce/logistics nexus, rests on Logistics 4.0 implemented by retailers that can quickly respond to a specified market demand even across large geographic distances. These approaches are particularly well developed at e-commerce companies, which excel in the rationalization of the customer–seller relationship (see Staab, 2016). Amazon’s ‘next-day delivery’, for instance, does not operate according to ‘pull logics’, in which customers order first and companies produce and deliver later, because this would require too much time. The company instead runs a network of material hubs close to end markets that operate on the basis of predictive analytics. By monitoring consumer behaviour based on actual sales and shopping-behaviour data, Amazon is able to forecast approximate customer demand to the extent that the company can predictively stock its warehouses with the correct product selection. 8 The forecasts are then only marginally modified in line with actual sales figures. 9 Additionally, Amazon and its competitors are striving to develop more efficient systems for last mile delivery, i.e. the final delivery step to private households, often as fully corporate-owned divisions. As a result, e-commerce companies can deliver a huge selection of goods to consumers, while they do not need to source those products in the regions where they are sold. Unlike the ‘smart factory’ or ‘smart network’ models referred to in the previous section, they do not offer authentically customized products in the sense that these are actually made according to customers’ specifications, but they provide an effective response to a growing differentiation of customers’ tastes through the sheer diversity of products on offer.

Logistics 4.0, be it as part of contract manufacturing services or in the context of e-commerce, thus allows for bridging greater geographic distance while still meeting the requirement of fast market response. On-demand production systems therefore do not necessarily require a regional integration of producers and target markets, as the example of the Adidas Speedfactory may suggest. Logistics 4.0 is in this sense a countervailing factor to reshoring, given that it allows for reconciling the requirements of fast time-to-market with global sourcing.

Fragmentation through modularization and platformization

The ability to fragment the value chain and – potentially – locate its activities in geographically remote areas depends on the ability to create modular product architectures according to a building-block principle of components with standard interfaces. Once standards are set, suppliers can deliver components according to these specifications which do not need to be negotiated and adapted anew for every product modification (Sturgeon, 2002). This reduces the need for the exchange of tacit knowledge when adjusting products and processes, which would require time and a higher degree of interpersonal exchanges and would therefore benefit from the geographical proximity of involved firms. In addition to that, it is a precondition for the smooth operation of supply chains that bridge large geographical distances because just-in-time delivery of standardized components can be better negotiated and planned in advance. The electronics industry has taken the modularization of product architectures to a new level, which (along with low transport costs) was a precondition for setting it up as a truly global industry comprising several hubs for key inputs such as software, chip design, chip foundries, hard disk drives, hardware components (cables, monitors, keyboards) and hardware assembly. The tension between reaping cost advantages in developing countries while at the same time adjusting products to specific preferences in large target markets can be reconciled through the geographical fragmentation of functions combined with advanced logistics under the condition that such a modular product architecture exists in the first place.

Yet there are limits to the fragmentation of supply chains into neatly separated modules. Herrigel and Zeitlin (2010) have pointed out that strongly modularized supply chains only prevail in certain industries – in particular in the highly globalized electronics and garment industries. In other industries, the modularization options are far more limited and firms need to engage in frequent adjustments which in turn can be more easily achieved based on exchanges of tacit knowledge in a regionally integrated setting (Hildrum et al., 2010). A case in point is the automotive industry that relies heavily on the geographical co-localization of (first-tier) suppliers, not only in order to guarantee that just-in-time delivery targets are met, but also because of the need to adapt components to new requirements linked to market-specific modifications of the final product. The need for a closer interaction between markets, lead firms and supplier networks that creates benefits through mutual learning would support a tendency of intra-regional integration of supply chains (Herrigel, 2015), a tendency that prevails in many industries that are far less globalized than the paradigmatic electronics and garment industries (Herrigel and Zeitlin, 2010).

To what extent, then, do new digital technologies shift the balance between manufacturing approaches that rely on the global sourcing of modularized products or components and those which rely on mutual learning of firms and are therefore predominantly regional? Sturgeon (2017) argues that the capabilities of lead firms to fragment the value chain are enhanced by new technologies, resulting in a ‘further loosening of spatial ties between many business functions, including innovation (and within innovation), production, logistics, marketing, distribution and after-sales service’ (24). He identifies two related reasons for this. First, the ability to codify and transfer information is generally enhanced by computerization as such, as the ability to record data and transfer these data (specifications, benchmarks, real-time process data, among others) increases (see also Ponte and Sturgeon, 2014). This would drive standardization and modularization, which facilitates the offshoring and outsourcing of tasks.

Second, the organizational model of the platform 10 further facilitates a modularization of functions. The platform model has proliferated in recent years because of its superior ability to manage a growing complexity of production systems and the growing role of immaterial, ‘intangible’ assets for the creation of products. This complexity can be handled if systems can rely on third parties for complementary products, draw on outside sources of knowledge and technology and can be partitioned into manageable, interoperable segments (Humphrey, 2018: 8). The organizational form of the platform can help achieve such tasks. As a form of economic organization, platforms constitute a technological core around which inputs by complementors are integrated, which provide add-ons, applications, components, etc. around the technological core of a platform that raise the overall value of the platform and the versatility of its use. The platform model thus offers an opportunity to source inputs by a diverse set of actors, diversifying and enhancing its functions without placing the burden of innovation exclusively on the platform leader. The governance challenges for platform leaders consist of maintaining the platform as a technological core and defining its boundaries while managing the relationship with the complementors. The latter often can be executed without engaging in explicit coordination, as platform leaders – ideally – can govern through a set of explicit or de-facto standards (Humphrey, 2018: 15).

The platform model has altered the architectures of certain products that can consist of several layers of platform ecosystems which in turn allow for a high level of complexity and the possibility to adapt and customize products. Customization is increasingly achieved through a hybridization of these products, i.e. the attachment of software and data content to the physical product, a trend that applies not only to consumer electronics but is also becoming more relevant in household appliances (smart home), the automotive sector (smart vehicles) and other industries. In such cases the physical product, beyond its immediate functionality, becomes a carrier for informational content that might even be more relevant to the value of the final product than the properties of the physical object itself (Haskel and Westlake, 2018). If the customer-specific configuration of a product depends primarily on intangible inputs and less on the properties of the hardware, proximity to end markets does not provide any advantages to manufacturers – contrary to the reshoring-hypothesis. In products that consist of a layered platform structure, the bulk of market-specific customization is shifted to the ecosystem consisting of software elements, often selected by the customers themselves on-line according to their preferences.

The paradigmatic case of a product architecture consisting of a layer of platforms is the smartphone (Thun and Sturgeon, 2019). Its modular product architecture is organized as various layers of platforms: general interconnection standards, regionally specific interconnection standards, chipsets, handsets, operating systems and social networking platforms. Each of these layers can be improved, adapted and modified without affecting the overall architecture of the product, which in turn offers a level of complexity and a range of possibilities that would otherwise be difficult to achieve. The complementors that enhance the functionality of each platform layer focus on highly specific product segments linked to the specifications of the respective platform layers. Sturgeon (2017) therefore interprets the organizational form of the platform as ‘generally modular’ (15) and its effect as one of enhancing the potential for the modularity of supply chains.

As a model of industrial organization, the platform model therefore opens up new possibilities to create complex products that consist of a combination of intangible software layers and tangible hardware components. As such it provides options for geographically segmented value chains that rest on the inputs provided by enterprises from various regions. However, if we follow Humphrey (2018: 13–14) in assuming that relationships between platforms and complementors will continue to rely on explicit coordination to a certain extent that require some degree, geographical proximity will continue to matter. Production networks would then continue to rely on geographically embedded hubs and clusters. In new configurations between the local and the global, the layered platform structure provides new possibilities to connect geographically integrated hubs at a global scale.

Discussion and conclusion: Digitalized manufacturing and reshoring

The analysis of the relationship between digitalization and the geographies of production has revealed contradictory tendencies. Rather than assuming a universal trend towards reshoring or its opposite, namely enhanced fragmentation and offshoring, the analysis has highlighted how the introduction of new digital technologies can provide incentives to move in one or the other direction by making both a close interaction in a regionally integrated and highly automated ‘technology-innovation-production-market continuum’ (De Propris and Pegoraro, 2019) or the linkage of dispersed modularized production hubs connected through advanced logistics systems advantageous. Technology thus does not have a one-directional effect on the geographies of production. This is a less tangible theoretical result than the identification of a trend towards reshoring, but it is an assessment that matches the variety of spatial arrangements existing in the world economy today. As new digital technologies do not create new value chain arrangements per se, but are integrated into existing structures that depend on a great variety of factors, future research needs to discern empirically how the application of technologies affects location decisions. The implications at the product or sector level can be as radical as the geographical dispersion of manufacturing in the ICT industry have been in recent decades, but it is unlikely that they will affect all industries in a similar manner.

At a more concrete level, the theoretical discussion presented in the paper about the variables linked to the application of new digital technologies can be summarized as follows:

Automation: It is unlikely that the effects of automation will trigger a general trend towards reshoring. Such claims mostly rest on over-simplified calculations that compare abstract technological possibilities to present day labour markets and thus underestimate the costs and the contradictions inherent in any attempts to automate. More importantly, automation does not only occur in high-wage countries as potential sites for reshoring, but also in emerging economies where its diffusion and growth has been the most dynamic in the recent past. It thus raises the productivity in classic offshoring destinations that maintain advantages of cheaper production costs and combine them with increasingly sophisticated automation equipment. If potential benefits of manufacturers’ proximity to end markets are taken into account, ‘nearshoring’ seems to be a more realistic option than reshoring. On-demand production and logistics: The geographical shift in end markets and the emergence of an on-demand economy, in which companies instantly cater to individual customers’ needs, are intensifying pressures towards investments that are located within or nearby the target markets and could make reshoring attractive. However, the e-commerce/logistics nexus constitutes a countervailing factor to the logic of a regional integration of producers and target markets. This is because requirements for diversity and time-to-market can be met by making a large selection of diverse or customized products instantly available. Such opportunities are amplified through the sophistication of information systems including AI-based predictive analytics that push the boundaries of ‘annihilating space through time’. Thus, global sourcing continues to be feasible, especially in industries where transport costs are low and the modularization of product architectures is easily achieved. Modularization and fragmentation: Enhanced means for the codification of production-related information and the ability to digitally transmit such information expand the scope for a modularization of product architectures and modes of supply chain governance that can tolerate geographical distance. The platform mode of industrial organization is a specific form of a modular architecture that rests on the ability of platform leaders to engage with complementors relying on standards rather than on explicit coordination. Particularly the hybridization of products, i.e. new ways of combining tangible, physical products with intangible information content, provides new possibilities of a geographical disintegration of value chains as the customization of products to regionally specific market demand is increasingly linked to the software layer.

While these findings may inform future empirical investigations into changes in the geographies of specific industry sectors, it is important to keep in mind that the complexity of such issues is heightened by the emergence of a multipolar world market, as emerging economies have been the main centres of consumption growth during the last decade. The reshoring hypothesis is limited, for it adopts only the perspective of advanced industrial economies in order to address the question of whether manufacturing is ‘coming back’. Yet it is more appropriate to ask whether manufacturers from advanced industrial economies would continue to move production capacities abroad in order to benefit from advantages of proximity to large expanding markets in emerging economies. Such approaches to ‘produce where you sell’ (Herrigel et al., 2013) have been a strong motivation for FDI for many years. Indeed, this trend may be reinforced given the productivity-enhancing effects of catch-up automation and new advantages of market proximity through new production models that explore the benefits of a heightened responsiveness to consumer demands by taking advantage of digital technologies.

Footnotes

Acknowledgements

The author would like to thank the editors of this special issue and two anonymous reviewers who provided valuable comments that helped to improve this contribution.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.