Abstract

This study investigates the impact of intellectual property (IP) strategy on the governance of technological platform-driven global value chains (GVCs) using a case study of the collaboration between Qualcomm and Chinese smartphone manufacturers. Our findings are twofold. First, even when IP protection is inadequate or technological capabilities of IP users are weak, a well-designed IP strategy can allow a technological platform vendor (Qualcomm) to transfer knowledge to users in developing countries while still protecting their own IPs. Second, by reducing the platform and value chain’s modularity, a good IP strategy can encourage platform vendors to offer more innovation and learning opportunities along GVCs. We show there can be a significant mutual reinforcement mechanism included in an IP strategy that supports the co-evolution of platform vendors and a few selected users (OPPO, VIVO, and Xiaomi) with great potential for learning and innovation in GVCs.

Introduction

One of the central aims of a global value chain (GVC) study is to investigate the roles of lead firms in shaping the international division of labour and its consequences on knowledge diffusion, capability formation, and innovation in the developing world. Existing studies have focused on the role of global buyers or producers in downstream GVCs (Gereffi, 1999; Gereffi et al., 2005; Morrison et al., 2008; Pietrobelli and Rabellotti, 2011). However, along with the rise of an intangible economy, 1 the drivers of GVCs have been fundamentally transformed in high-tech sectors and technological platform-driven GVCs. A growing body of literature suggests that platform vendors (defined below as core technology owners and providers) in upstream GVCs have played an increasingly important role in the development of global high-tech sectors (Gawer and Cusumano, 2002; Gawer, 2009a; Thun and Sturgeon, 2017; Haskel and Westlake, 2017; Humphrey et al., 2018). Platform vendors have adopted GVC governance methods that have been extended from pure transactions and the enforcement of international standards to the management of intellectual property (IP) and licence agreements (Pananond et al., 2020; Lee and Gerrifi, 2021).

As Gawer (2014) highlighted, there are two different definitions of technological platforms. The economics literature defines platforms as multi-sided markets, focussing on the functions of search or social networking through ‘network effects’ that arise between various types of user groups. The research subject of the economics literature usually includes digital platforms, such as Facebook, Amazon, and Google. GVC literature has begun to study digital platforms by adopting the economics approach (Lundquist and Kang, 2021).

On the other hand, the engineering design approach studies the role of a core technology provider in a technological system, such as Intel (central processing unit) and Microsoft (Windows operating system) in the computer industry. This literature views platforms as technological architectures, stressing the role of platforms in shaping the division of innovation labour. Gawer (2009b: 57) defined a platform as ‘building blocks that act as a foundation upon which other firms can develop complementary products, technologies, or services’, and Baldwin and Woodard (2009: 19) defined a platform as ‘a set of stable components that supports variety and evolvability in a system by constraining the linkages among the other components’. Gawer and Henderson (2007: 4) defined a platform ‘owner’ as a firm that owns a core element of the technological system that defines its forward evolution. These definitions indicate that a technological platform could play a crucial role in facilitating learning and innovation in GVCs because it owns core technologies, determines design rules, and provides a solid foundation for innovation.

In this study, we adopt the engineering design literature’s definition of a technological platform and focus on the role of Qualcomm, which is a core technology provider and owner in smartphone GVCs. We contend that intellectual property (IP) is a crucial perspective for understanding technological platform-driven GVCs (hereinafter abbreviated as ‘platform-driven GVCs’). In developed countries, most capital accumulation consists of intangible assets, including IPs. Since the 2008 global financial crisis, intangible investments have surpassed tangible investments in major European countries and the United States, accounting for more than 12% of GDP in 2014 (Haskel and Westlake, 2017: 26, Figure 2). Factoryless manufacturers, who comprise the majority of lead firms in high-tech sectors, organise GVCs based on their own IPs, including patents, brands, trademarks, copyrights, product designs, software, databases, and special business organisational structures (Xing, Gentile and Dollar, 2021: Executive Summary). According to an OECD study that examined key factors affecting GVC participation in advanced and developing economies, IP protection is the single most important factor in GVC participation in the developing world (Xing, Dollar and Meng, 2021: 60, 61; original data was cited from Kowalski et al., 2015).

IPs are particularly important to technological platform vendors. Take the example of mobile phones. Before the first Apple iPhone in 2007, major players in this industry were quite vertically integrated, 2 recouping research and development (R&D) investment primarily by selling final products to customers (Mallinson, 2015). However, with the trend of disintegration and the growing risks of R&D failures, the revenues of product sales alone could not cover the exceedingly large R&D expenditure. A growing number of smartphone companies are turning to specialisation in core technology development and licencing their technologies to final product manufacturers (Mallinson, 2015). Both Qualcomm (the world’s leading integrated circuit (IC) design company) and ARM (the world’s leading technology provider of processor IP) have licencing businesses as their major revenue streams.

In this study, we asked two research questions. First, how does IP strategy lead to learning and innovation in technological platform-driven GVCs? Second, how does IP strategy and changes to GVC governance facilitate the transfer of learning and innovation across firm actors in technological platform-driven GVCs? We focus our analysis on the role of the platform vendors themselves and the relationship between IP strategy and GVC governance. We will discuss further, the inter-firm governance mode determines the method and nature of knowledge transfer in GVC.

To respond to the above research questions, we examine the success story of Qualcomm and its Chinese smartphone customers. This case has two important aspects.

First, the rise of the mobile phone industry in China is a typical example of how technological platforms play a significant role in GVCs. In the 2000s, the dominant adoption of the platform developed by Taiwanese IC design company MediaTek (MTK) resulted in homogenous products, inferior imitations, and intense competition in the low-end feature phone market 3 of China. However, in the 2010s, by closely collaborating with Qualcomm, the leading IC design company 4 in the global smartphone value chain, a small number of Chinese smartphone companies gained a significant share in the world market in terms of shipments and conducted substantial innovation in GVCs.

Second, compared to other industrial goods, IP expenditures account for a higher proportion of the total cost of smartphones, which is of special significance to the development of the smartphone industry (Dedrick and Kraemer, 2017; Xing and He, 2018). Qualcomm, as the world’s largest patent owner of 3G and 4G mobile communication technologies, adopted an aggressive patent licencing model, under which licensees must not only pay expensive royalties known as the ‘Qualcomm tax’, but also accept overbearing reverse patent licencing: to licence their own patents to Qualcomm for free, and should not collect royalties from any of Qualcomm’s customers for these patents. This licencing model of Qualcomm became the subject of numerous anti-trust investigations worldwide. 5 However, it was in this environment that collaborations between Qualcomm and the Chinese firms were conducted.

The contributions of this case study analysis are twofold. First, our study reminds researchers to recognise the important role of IP strategy in facilitating learning and innovation in GVCs. Existing studies about GVCs and IP have focused more on the international IP regime (Durand and Milberg, 2020), IP protection problems (Xing, Dollar and Meng, 2021), and technological capabilities of IP users (Lee, 2019) and have largely neglected the positive role of IP holders themselves in facilitating knowledge diffusion in GVCs.

Second, we have uniquely combined the IP strategy literature (Arora et al., 2001; Chesbrough, 2006; Hanel, 2006) and the GVC governance literature (Gereffi et al., 2005; Yasumoto and Shiu, 2007; Humphrey et al., 2018) to investigate the knowledge transfer mechanism in platform-driven GVCs, that is, how and in what forms knowledge is transferred and how the transfer is affected by the IP strategy.

The remainder of this paper is organised as follows. The literature review section conducts a literature review of the perspectives of IP and value chain governance. The data and methodology section explains the research data sources and methodology. The section of China’s mobile phone industry provides a brief introduction to the rise of China’s smartphone phone industry and highlights the crucial role of the Qualcomm platform in bringing about this change. The next two sections analyse Qualcomm’s IP strategy and its consequences on governance, innovation, and learning in smartphone GVCs. The conclusion section provides a summary of our research findings.

Literature review: IP strategy and GVC governance

There are two lines of literature concerning our research questions. The first line focuses on IP protection and economic development in GVCs.

The international IP regime has become increasingly strict with the expansion of GVC trade (Durand and Milberg, 2020: 412). IP strategy, as an institutional arrangement for intangible asset management, has become increasingly important for value chain governance as well (Lee and Gereffi, 2021:14). Theoretically, the introduction of global IP standards stimulates technology transfer by multinationals from developed countries to developing countries (Hanel, 2006). From an empirical viewpoint, however, very little evidence in the international trade literature supports the positive effect of stricter IPs on innovation, productivity, and FDI inflows (Durand and Milberg, 2020: 413).

Existing literature attributes the reason for limited knowledge transfer under strict IP regimes to poor IP protection and weak technological capabilities in developing countries. According to the Global Value Chain Development Report 2021, as IP protection in developing countries is not as strong as in advanced economies, multinationals with valuable IPs are generally unwilling to transfer intangible assets directly to other companies located in developing countries, but prefer to deploy these assets to their own overseas subsidiaries (Xing, Gentile and Dollar, 2021: Executive Summary; Xing, Dollar and Meng, 2021).

Many case studies about GVC governance indirectly confirmed this point, suggesting that GVC suppliers in developing countries are more likely to realise product and process upgrading but struggle to achieve functional upgrading 6 (Schmitz and Knorringa, 2000; Bazan and Navas-Aleman, 2004; Schmitz, 2006; Morrison et al., 2008). Although the reason is often attributed to lead firm intention to prevent new competitors from entering the segments of their core competence, it can also be explained from the perspective of IPs. When the GVC segments into which suppliers want to enter have rich intangible assets such as design and branding (which can be easily copied and imitated), it would be too risky for a lead firm to transfer knowledge to these segments if the IP protection is inadequate.

The other reason that is given in the literature for the limited knowledge transfer in GVCs is the technological capabilities of local firms. Lee (2019: 11) highlighted that strict IP protection may hurt the diffusion of knowledge in GVCs as latecomer countries are usually not equipped with strong ‘innovation capabilities’. 7 Within this context, Lee (2019) highlighted the importance of capability formation for knowledge transfer and IP protection. It is suggested that firms in developing countries should promote imitative innovation under a loose IP regime in the form of petit patents and trademarks. 8 They should even temporarily move from GVCs to domestic value chains to accumulate capabilities (Lee, 2019: xvii, Section 3.5).

In summary, this first line of literature attributes the failure of knowledge transfer under strict international IP regimes in GVCs to factors in developing countries, such as poor IP protection or weak capabilities; however, these studies do not explain the paradox of Qualcomm which show opportunities for learning and innovation in GVCs even under a strict international IP regime.

The second line of literature is focused on IP strategy, value chain governance, and platforms. Existing literature suggests that a good IP strategy can facilitate knowledge transfer to external firms while still creating value for the IP holder (Arora et al., 2001; Chesbrough, 2006; Hanel, 2006). However, few studies on IP strategy have discussed how and in what forms knowledge is transferred, which, to a large extent, determines the opportunities for learning and innovation in GVCs. Studying and incorporating the perspective of inter-firm value chain governance can fill this gap in the literature. As per the GVC governance theory, value chain governance modes are determined by combining the following three factors: the complexity of transactions, the codifiability of transactions, and supplier capabilities (Gereffi et al., 2005). When the complexity of transactions, codifiability, and supplier capabilities are high, the GVC governance mode becomes modular. If the codifiability of transactions decreases and the other two factors remain unchanged, the governance mode changes to relational. Under modular inter-firm governance, complex knowledge will be codified and lead firms and suppliers (or platform vendors and users) will need not pursue costly communication. Conversely, when adopting relational governance, they must work more closely through joint collaboration and intensively exchange tacit knowledge.

As the basic technological architecture of the platform is modular (Baldwin and Woodard, 2009; Gawer, 2014), platform-driven GVC-related literature has paid particular attention to the impact of the codifiability of transactions, namely, the impact of the platform’s modular technological architecture on value chain governance and knowledge transfer. Based on a case study of the feature phone industry, Yasumoto and Shiu (2007: 66) pointed out that a fully modularised technological platform can enhance the inter-firm modular mode of GVC governance between platform vendors and users, as it enables users to easily develop a final product even if they have insufficient knowledge of the platform. While, on the one hand, this reduced the product development barriers to entry of a feature phone, however, on the other hand, it limited the transfer of knowledge and hindered bilateral mutual learning between them. When a platform is fully modularised, platform vendors and users do not need to exchange in-depth information except prices.

Conversely, Humphrey et al. (2018: 411) indicated that technological changes in the smartphone industry can break down degrees of platform modularity. Accordingly, the GVC governance mode may shift from an arm’s length market to a relational mode, thereby increasing coordination and contact between platform vendors and users. This study further highlighted that such interactions help platform users learn more tacit knowledge from platform vendors and acquire more knowledge (such as technology roadmaps) about the platform, which are critical to the R&D of a final product at the technological frontier. 9 Such relational GVC governance eventually provided platform users with more learning and innovation opportunities (Humphrey et al. 2018).

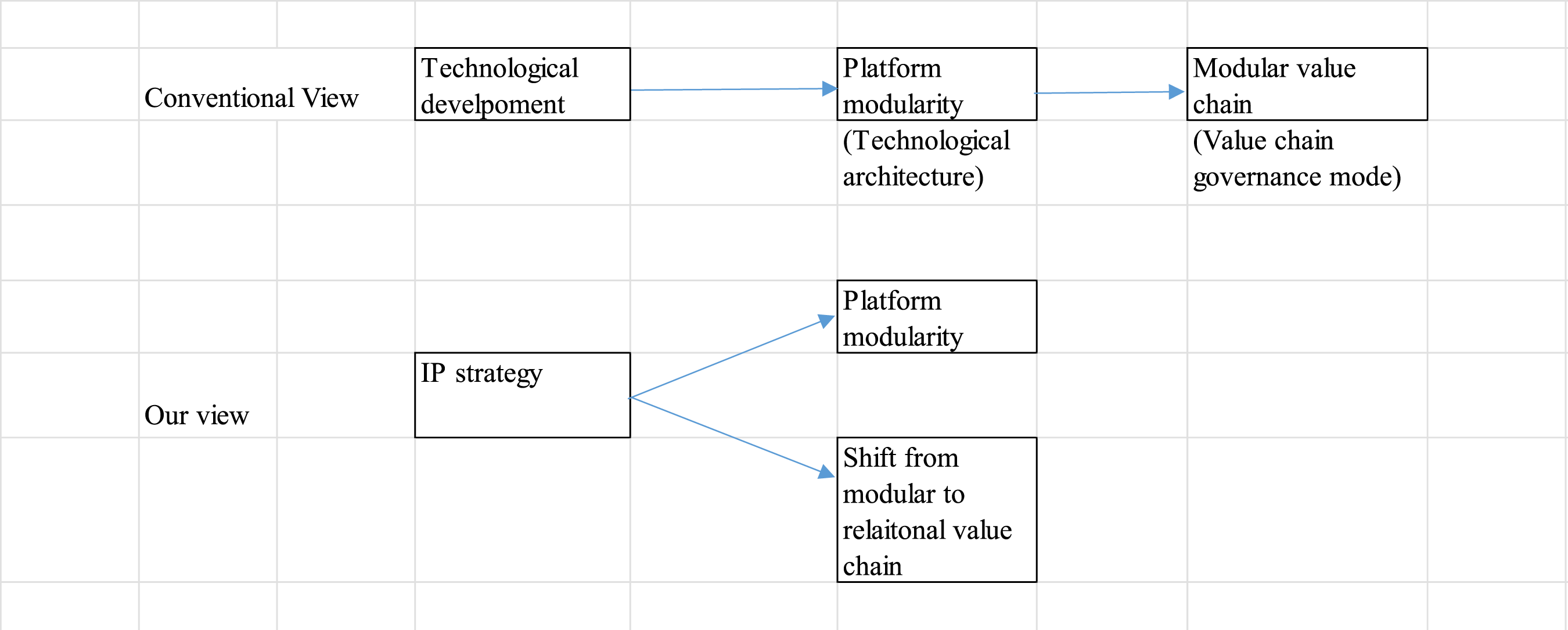

The literature on GVC governance generally considers the modular governance mode being a result of technological development (Ambos et al., 2021: 7). As Figure 1 suggests, conventional studies believe that technological development determines the modularity of a platform, and the modularity of a platform determines the degree of inter-firm modular GVC governance. These studies considered that the platform and value chain modularity are exogenous and not affected by firm strategy. However, without a strategic perspective, as we will show, we cannot explain why Qualcomm, rather than other platform vendors, can gain the largest share in the world’s smartphone chipset market (see the section of China’s mobile phone industry for details). A platform vendor’s strategy, such as its IP strategy, will likely have significant consequences on the degrees of platform modularity and the modular value chain governance (Figure 1). In other words, firm strategy and technological development should have equally important impacts on platform modularity. A study combining IP strategy analysis and GVC governance theory can help us gain a more profound understanding of the leading share of Qualcomm in the world’s smartphone chipset market and the mechanism of knowledge transfer in platform-driven GVCs.

10

Comparing views of GVC governance and platform modularity. Source: The authors.

Data and methodology

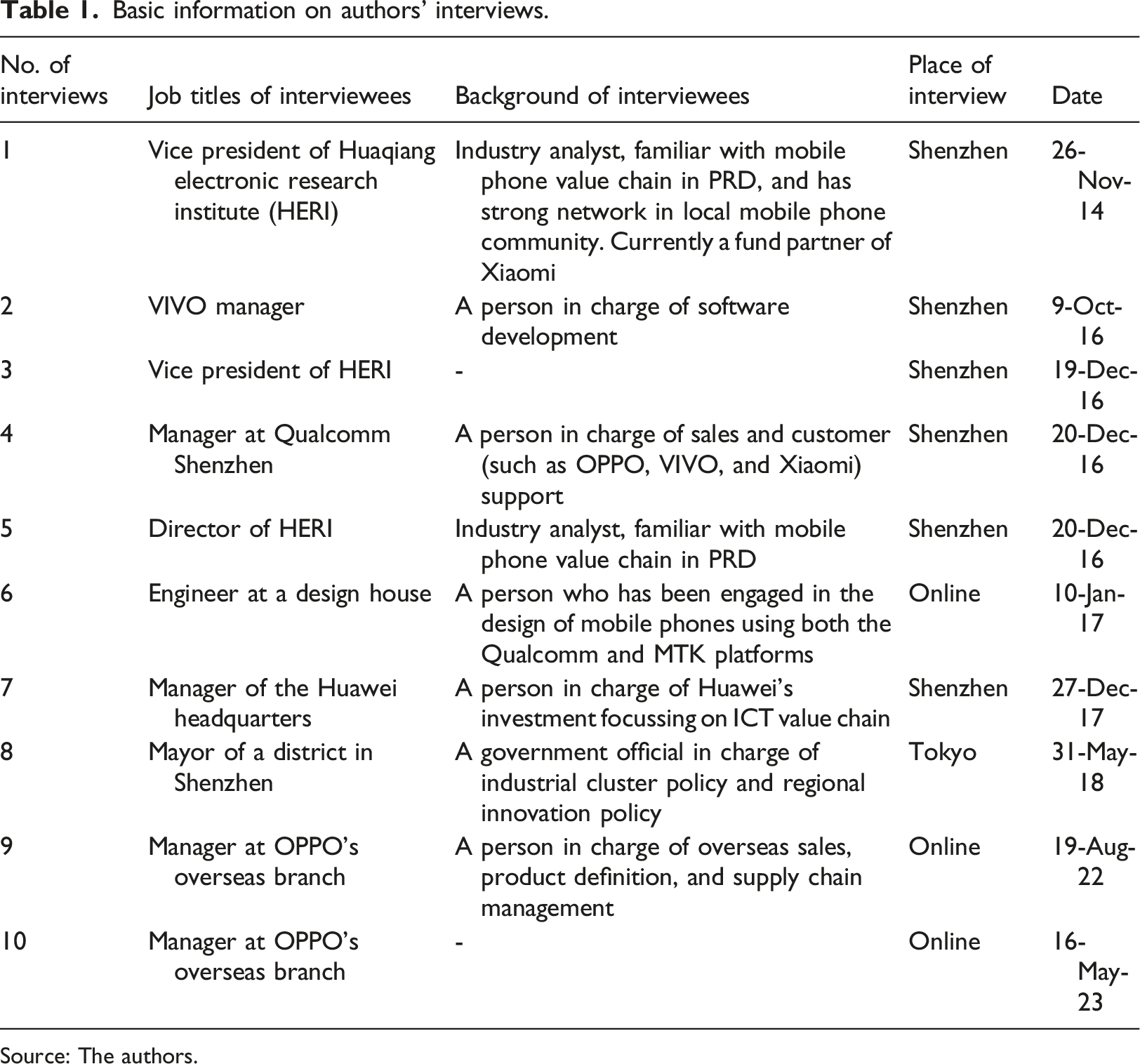

Pearl River Delta (PRD), with Shenzhen as its central city, is the largest mobile phone industrial cluster in the world. Among the top 10 global smartphone companies in 2020, five of them (Huawei, VIVO, OPPO, Realme, and Techno) are located in PRD. Between 2009 and 2019 (except 2018), we made annual visits to the PRD to conduct interviews with various types of companies in the mobile phone value chain, including system integrators, design houses, vertically integrated mobile phone firms, parts suppliers, and technological platform vendors (for details of system integrators, design houses, and vertically integrated mobile phone firms. See next section, particularly Figure 2), as well as local government officials, industry analysts, venture capital managers, and journalists in this region. Our focus was on knowledge diffusion and innovation mechanisms along the mobile phone value chain.

Basic information on authors’ interviews.

Source: The authors.

In addition to interviews, we collected company information from Form 10-K (hereinafter 10-K) of Qualcomm, which are documents that the United States Securities and Exchange Commission requires all public companies to file every year and usually contain more detailed information than company annual reports. However, since major Chinese mobile phone companies are either not listed (OPPO and VIVO) or listed very late (Xiaomi in July 2018), we were unable to obtain similarly detailed and systematic data from their public information. This is a limitation of this research. For this reason, we collected secondary data as far as possible from the websites of market research companies and industry news to describe the whole picture of the smartphone industry.

Rise of the Chinese smartphone industry and changes in platform leadership

This section briefly introduces the significant structural change in China’s mobile phone industry between the 2000s and the 2010s and highlights the crucial role of the Qualcomm platform in facilitating this change.

Structural change of China’s mobile phone industry

The mobile phone industry in China has experienced significant structural changes since the 2010s. In the 2000s, about two-thirds of the mobile phones made in China came from the formal sector, in which the major players were foreign brands such as Nokia and Samsung, and only a few local companies (such as Huawei and ZTE) were in this sector. The remaining one-third of the mobile phones, most feature phones, were manufactured by numerous small and medium-sized enterprises in the informal, unregulated, and illegal ‘shanzhai’ 12 sector (Brandt and Thun, 2011; Ding and Pan, 2014; Gao, 2011).

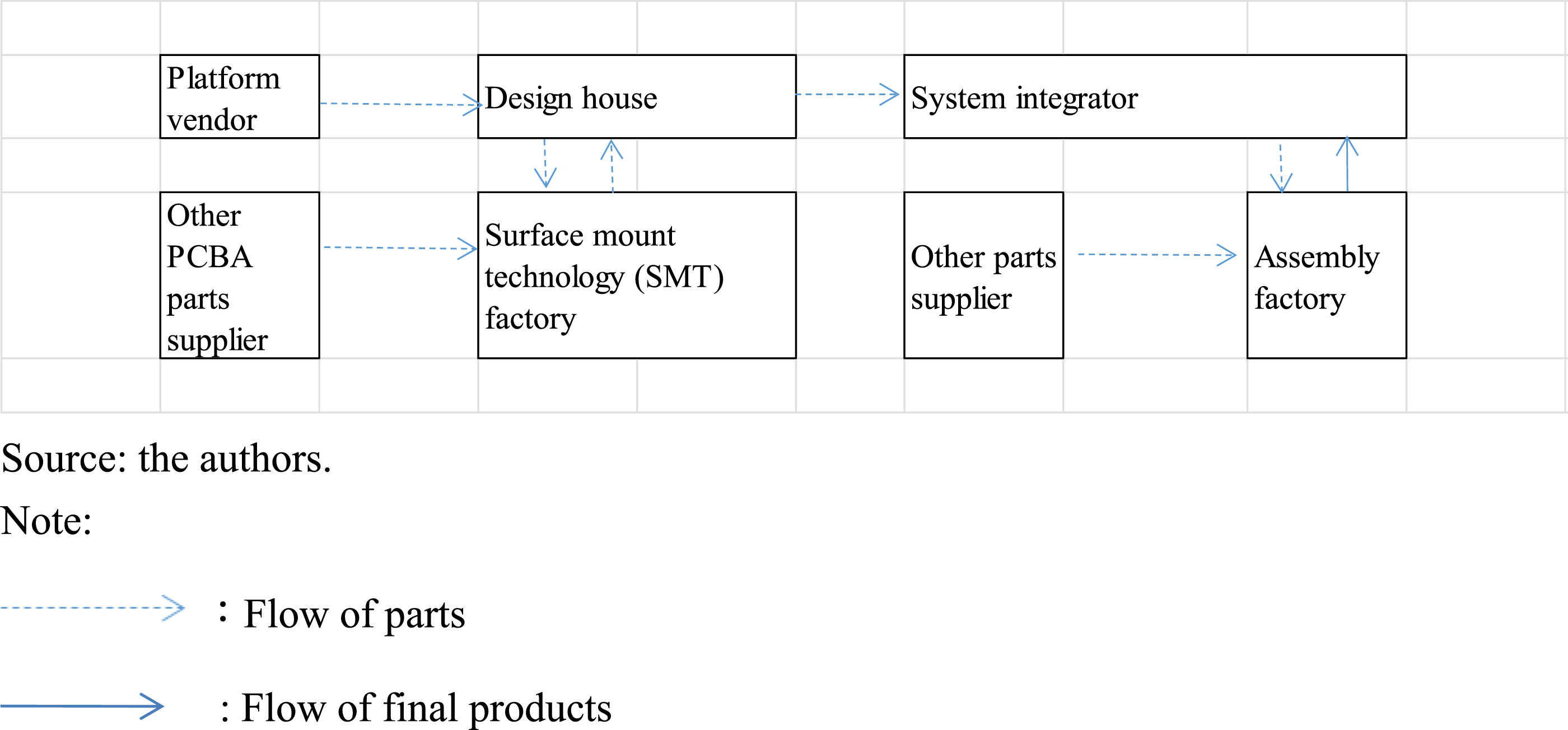

As shown in Figure 2, the value chain for shanzhai mobile phones was highly disintegrated, having independent manufacturers in each segment. The product development of a mobile phone primarily involves two processes: system integration and design. Large mobile phone companies such as Apple, Samsung, or Huawei usually integrate these processes into their internal organisations. In the shanzhai sector, however, independent companies existed in both processes: the system integrator and the design house. It was estimated that by 2010 there were 2000 system integrators and 500 design houses in China (Ding and Pan, 2014: Table 4). The shanzhai mobile phone value chain. Source: the authors.

System integrators often have dozens to hundreds of employees, do not have an R&D department, and partially take charge of product definition, supply chain management, project management, and sales. Design houses, who are also as small as system integrators and usually regarded as their outsourced R&D department, specialised in PCBA (printed circuit board + assembly) hardware design, some software designs, and PCBA production. The governance modes of the shanzhai mobile phone value chain, including the relationships between platform vendor and design house, or design house and system integrator, are typically an arm’s-length market. This has the disadvantages of producing highly homogenous products and poor imitations of branded mobile phones (Imai and Shiu, 2007; Ding and Pan, 2014).

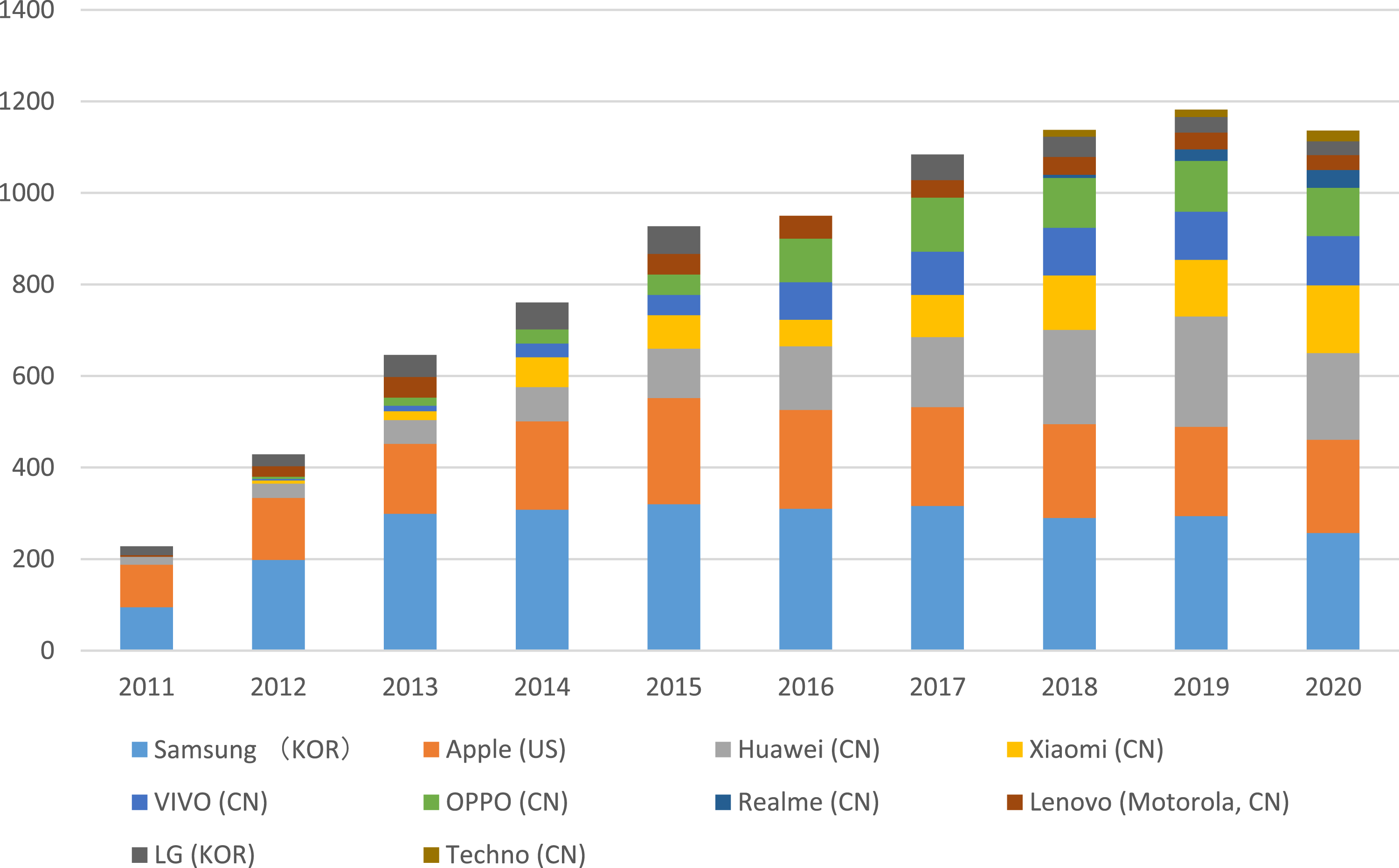

Since 2011, China’s mobile phone industry has achieved rapid growth and has been significantly upgraded in terms of industrial organisation and value creation (Interview 1, Huaqiang Electronic Research Institute (HERI), 2014; for details, see Table 1, the same below). As shown in Figure 3, except for Samsung, Apple, and LG, all the top 10 brands in the world are from Chinese companies. An increasing number of vertically integrated Chinese firms that had both the design house and the system integrator functions emerged and kept growing. In the 2000s, the number of vertically integrated mobile phone companies was no more than 10, but it increased to 30 in 2016 (Interview 3, HERI, 2016). In 2020, the seven Chinese companies ranked in the world’s top 10 smartphone brands (Figure 3) are all vertically integrated. Shipments of major smartphone brands in the global market (million units). Source: Data of 2011–2017: IHS iSuppli; Data of 2018, 2019, 2020: Informa Tech. IHS iSuppli was merged by Informa Tech in 2019. Note. KOR: Korea; CN: China.

The rise of Chinese brands has led to certain increase in profits. According to estimations by Counterpoint (2017, 2018), during the period between 2016 and 2018 (the data are all for the second quarter), the data of the global handset profit share for major smartphone brands are Apple (62.8%→62%), Samsung (28.8%→17%), Huawei (2%→8%), OPPO (3%→5%), VIVO (1.9%→4%), and Xiaomi (3% in 2018). In view that the global smartphone shipments rapidly increased during this period (see Figure 3), the profits captured by Chinese companies were thus substantial.

The success story of China’s smartphone industry resulted from the interaction between GVC participation and the support from the innovation system (Humphrey et al., 2018; Lema et al., 2018). The smartphone GVC in the 4G era created ample learning and innovation opportunities for Chinese manufacturers. China’s innovation system, at both the national and regional levels, enabled them to invest heavily in capability development to better benefit from GVC participation (Interview 8, a district in Shenzhen, 2018). In this study, our analysis emphasises the former, that is, the collaboration with the technological platform vendors in smartphone GVCs.

From MTK to Qualcomm

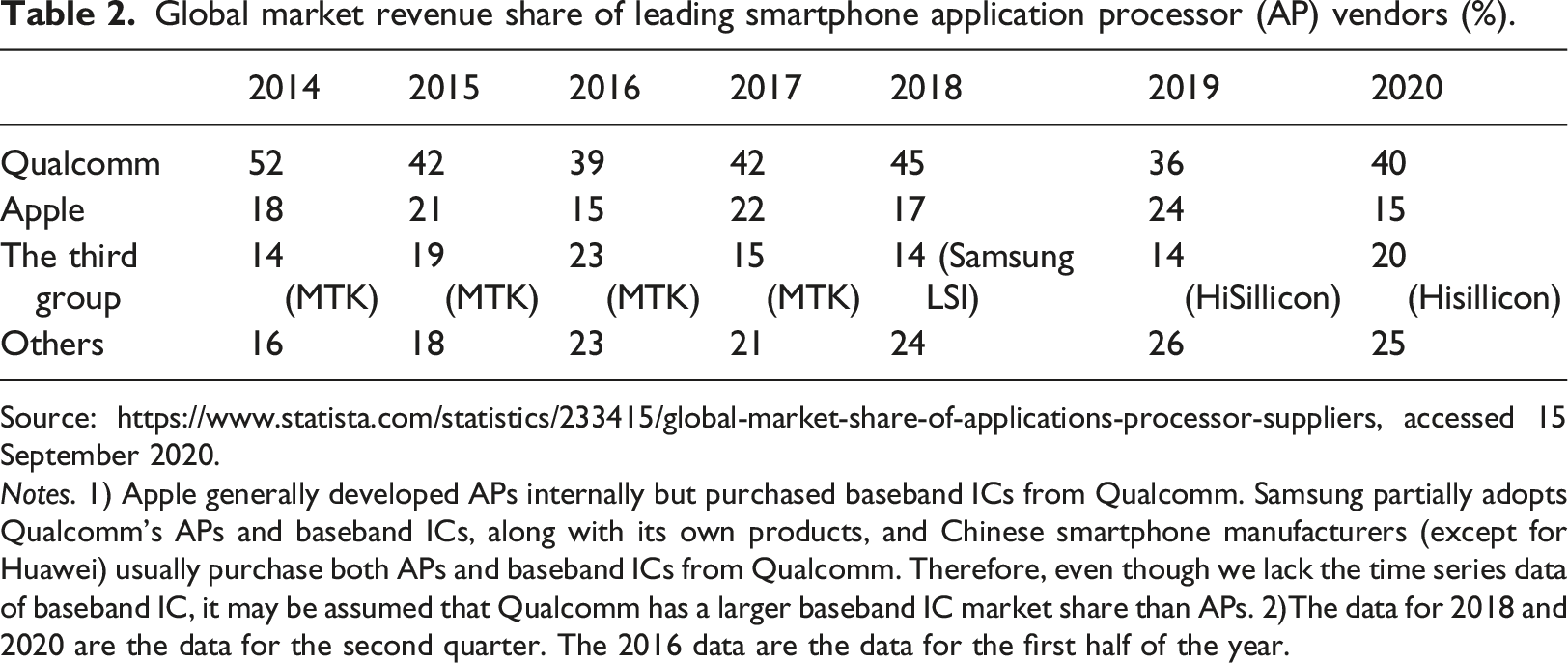

During the 2G era (1993–2008) and 3G era (2009–2013), MTK served China’s huge middle- and low-end markets through the adoption of a turnkey solution strategy that completely modularised its platform. At that time, technological platform vendors primarily served large mobile phone companies (such as Ericsson and Nokia) with strong technological capabilities. It was difficult for Chinese companies with weak capabilities to develop mobile phones based on existing platforms. In view of this situation, MTK integrated the baseband IC and the multimedia application processor into a single chipset platform, packaging the operating system, various software applications (e.g. MP3 players and phone camera drivers), and sometimes the user interface into its chipset. This platform greatly reduced the workload of hardware and software designers. MTK further provided a reference design that made mobile phone development easier by codifying design information (Imai and Shiu, 2007). MTK’s turnkey solution strategy significantly reduced the technological barriers for entry into China’s mobile phone sector. It has specifically met the requirements of many of China’s underserved small firms. According to an estimation by iSuppli, at its peak in 2009, MTK’s share reached 80.5% of the market for GSM-based 13 baseband IC chipsets in China.

Global market revenue share of leading smartphone application processor (AP) vendors (%).

Source: https://www.statista.com/statistics/233415/global-market-share-of-applications-processor-suppliers, accessed 15 September 2020.

Notes. 1) Apple generally developed APs internally but purchased baseband ICs from Qualcomm. Samsung partially adopts Qualcomm’s APs and baseband ICs, along with its own products, and Chinese smartphone manufacturers (except for Huawei) usually purchase both APs and baseband ICs from Qualcomm. Therefore, even though we lack the time series data of baseband IC, it may be assumed that Qualcomm has a larger baseband IC market share than APs. 2)The data for 2018 and 2020 are the data for the second quarter. The 2016 data are the data for the first half of the year.

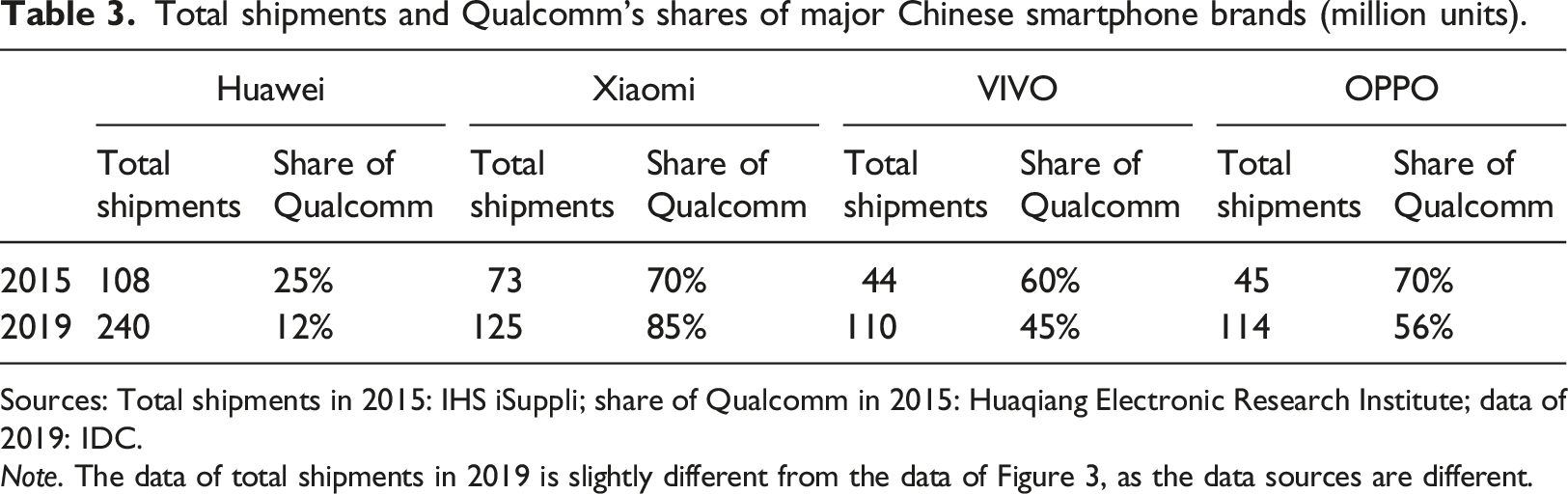

Total shipments and Qualcomm’s shares of major Chinese smartphone brands (million units).

Sources: Total shipments in 2015: IHS iSuppli; share of Qualcomm in 2015: Huaqiang Electronic Research Institute; data of 2019: IDC.

Note. The data of total shipments in 2019 is slightly different from the data of Figure 3, as the data sources are different.

Qualcomm’s IP strategy

Qualcomm’s business model

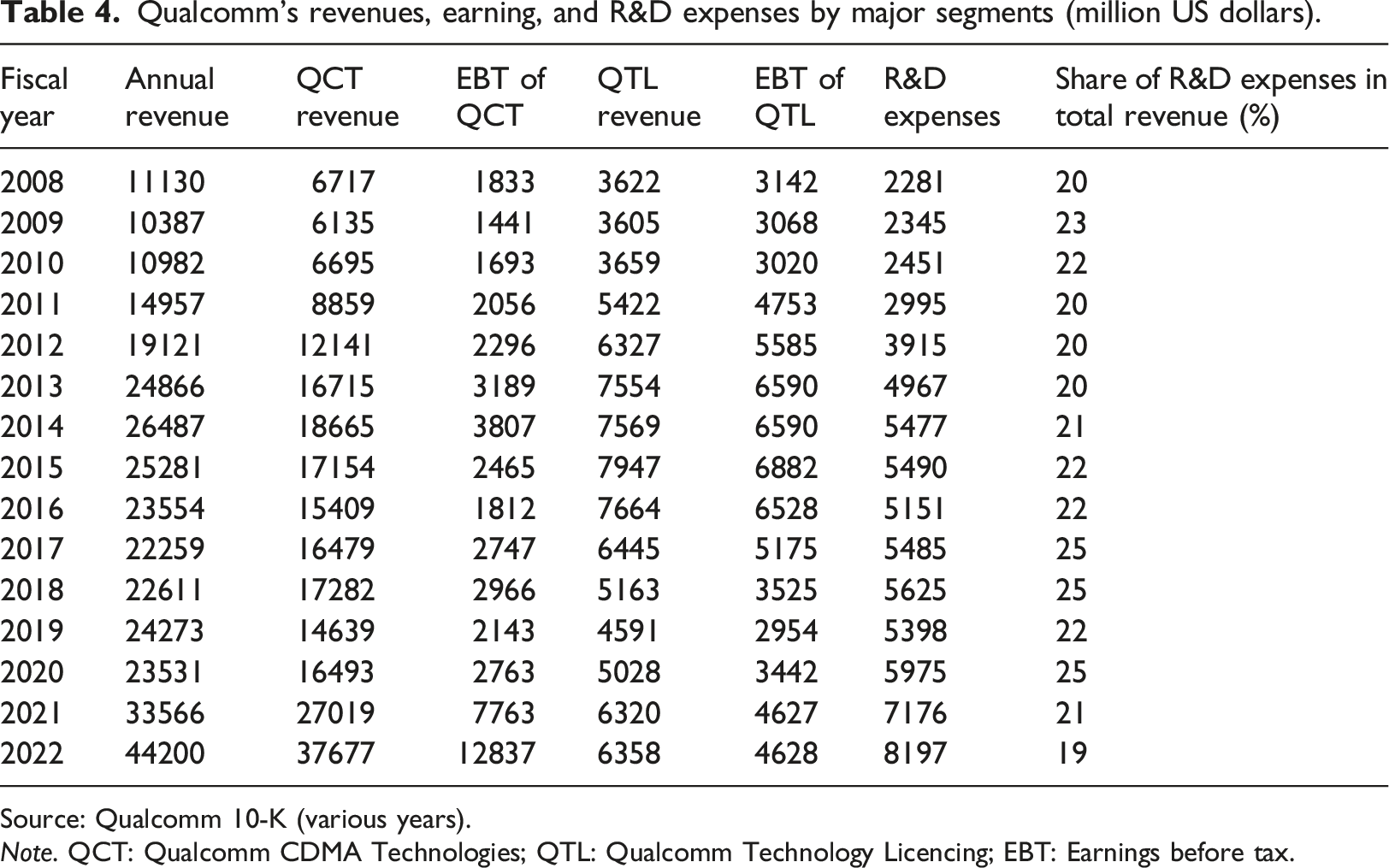

Qualcomm’s revenues, earning, and R&D expenses by major segments (million US dollars).

Source: Qualcomm 10-K (various years).

Note. QCT: Qualcomm CDMA Technologies; QTL: Qualcomm Technology Licencing; EBT: Earnings before tax.

Qualcomm concentrates on the R&D of core technologies and supports customers in downstream value chains to develop final products on the basis of its technological platform. The chairman of Qualcomm China, Pu Meng, stated, ‘Through the long-term R&D in the field of fundamental mobile technologies, we have become the R&D engine in the mobile industry. Then, through sharing and collaboration, we facilitated our partners to achieve more innovation’ (QbiAI, 2020).

In the 1990s, the telecommunication markets in Europe and Asia were dominated by a few national monopoly telecom carriers. They formed solid relations with incumbent telecommunication multinationals, which made new entry into these markets very difficult. As a latecomer, to break this situation and capture value from technology licencing, Qualcomm built a unique patent licencing model, known as the ‘no licence, no chips’ policy. 14 Under this model, customers have to pay licence fees and royalties to Qualcomm whenever they purchase chipsets from the company. In Qualcomm, the IC chipset business is known as QCT (Qualcomm CDMA Technologies). The patent licencing business is known as QTL (Qualcomm Technology Licencing). 15 In recent years, although QCT created the largest revenue in Qualcomm’s total business, QTL has produced the largest profit stream, which to a large extent supported the huge R&D expenses of the company (see EBT 16 of QCT and EBT of QTL in Table 4).

A smartphone not only has communication functionality but also includes mobile internet, camera, and audio functionality. The prices of Qualcomm’s chipsets generally account for no more than 20% of the total smartphone manufacturing costs. 17 However, in the QTL business, in addition to fixed licence fees, Qualcomm collects royalties on the basis of a certain ratio (5% for 3G CDMA or WCDMA devices (including multimode 3G/4G devices) and 3.5% for 4G devices that do not implement CDMA or WCDMA (including 3-mode LTE-TDD devices)) 18 of the wholesale selling price of an end-product smartphone rather than on its own chipset price (Qualcomm 10-K, 2015). In 2015, the basis for Qualcomm’s royalty collection was reduced from 100% to 65% of the wholesale selling price of a smartphone in China. For example, in 2017, the wholesale selling price of Xiaomi MIX2 was $336, which adopted the Qualcomm chipset Snapdragon 835 priced at $62.56. According to the above royalty ratio in China, Qualcomm collected a royalty of $10.92 (336×65%×5%) from this smartphone model (Xing and He, 2018: Table 1).

The other important part of the QTL business is the reverse patent licencing model (also known as the ‘grant-back model’). Qualcomm asks its licensees to licence their own patents to Qualcomm for free. Qualcomm also requests these licensees to not collect royalties from any other Qualcomm customers for these patents. Reverse patent licencing has two implications for Chinese smartphone manufacturing customers: On the one hand, it allowed start-up companies with few of their own patents (such as OPPO, VIVO, and Xiaomi) to cut costs on patent expenses. On the other hand, it forced incumbent companies (such as Huawei), which have several of their own patents, to develop their own chipsets to lessen their reliance on Qualcomm (Interview 7, Huawei, 2017).

Qualcomm’s IP strategy in China

In spite of its huge economic scale, China’s IP protection is insufficient. China’s position on the Intellectual Property Ranking of International Property Rights Index only rose from 59 to 47 between 2011 and 2020. Qualcomm has also suffered from IP protection problems in China until 2017. On the other hand, there was still a huge gap between Qualcomm’s Chinese customers (OPPO, VIVO, and Xiaomi) and its other major customers such as Apple and Samsung in terms of technological capabilities. Despite the circumstances, however, Qualcomm has paradoxically deepened cooperation with its Chinese customers, providing them with rich opportunities for innovation and learning (see next section). Why could Qualcomm do so despite the customers’ comparatively weak technological capabilities and the inadequate IP protection, which are usually regarded as the two major factors that hinder knowledge transfer in GVC? We argue that Qualcomm’s unique IP strategy has enabled it to overcome these problems.

High-tech companies use different strategies to disclose their technologies as patents or maintain them as trade secrets. Qualcomm patented most of its technologies and licenced them to other companies. Therefore, protecting Qualcomm’s IP means maximising QTL revenues.

Qualcomm’s licencing model enabled the company to secure QTL revenues from its own chipset users even under poor IP protection in China. This is because Qualcomm can accurately determine the volume of licensee sales by checking the sales of chipsets. Additionally, it is easy for Qualcomm to obtain the wholesale selling price of each model of a smartphone as it is publicly available information. Using this information, Qualcomm can potentially stop the supply of chipsets if a customer does not pay sufficient royalties. This ability to monitor its chipset users helps Qualcomm avoid damage to its QTL revenues.

Most non-Qualcomm chipset users must also use Qualcomm’s patents and pay licencing fees and royalties to the company because Qualcomm is one of the world’s largest wireless communication SEP holders. However, given the comparatively weak IP regime in China, it is very difficult for Qualcomm to effectively collect licence fees and royalties from these companies.

There are two types of cases in which this can occur (Interview 9, OPPO, 2022). First, large companies can and do often obtain patent licences from Qualcomm but not fully report shipments to avoid paying enough royalties because Qualcomm would not have accurate information on their shipments. Second, small companies do not obtain licences from Qualcomm and, therefore, not pay licence fees and royalties. Hence, the most efficient way for Qualcomm to protect its IP is by simply assisting its own chipset users to beat these competitors and gain a larger market share. 19

The limited technological capabilities of licensees are regarded as the other constraint for knowledge transfer in GVCs (Lee, 2019). However, Qualcomm’s licencing model can and has increased learning and innovation to overcome this problem faced by Chinese smartphone manufacturers. This is because its licencing model is essentially a contractual arrangement that stimulates knowledge sharing and capability formation. Qualcomm’s method for collecting royalties can be regarded as a typical sharing contract. Intuitively, a sharing licencing contract is not as efficient as a fixed licencing contract. Under the former contract, a licensee has to share a certain percentage of gains with the licensor. The more revenue that is created, the more is shared by the licensor, which greatly reduces a licensee’s motivation in its innovation efforts. However, if we shift our focus from licensees (smartphone companies) to the licensor’s motivation (Qualcomm), we reach a different conclusion. 20

Under its sharing licencing contract, Qualcomm must care about both the IC chipset shipments and the wholesale selling price of each smartphone model. Qualcomm must not only facilitate the total sales of its Chinese smartphone manufacturing customers but also help them sell products at higher wholesale selling prices, namely, by doing whatever it can to generate added value. For this purpose, Qualcomm shared knowledge substantially with its customers. This knowledge includes not only fundamental mobile communication technologies but also patents, source codes, and technology roadmaps that enable the development of a final smartphone as well as tacit knowledge generated during the process of product development (Interview 2, VIVO, 2016; interview 3, HERI, 2016; interview 4, Qualcomm, 2016). This is the main justification behind Qualcomm’s insistence on collecting royalties based on the final smartphones. For Chinese smartphone manufacturers, which face major technological and knowledge gaps in comparison to Qualcomm, the sharing of this codified and tacit knowledge creates significant learning opportunities. As discussed in the next section, a selected few companies with great potential for innovation and learning that would maximise the QCT and QTL revenues for Qualcomm, eventually benefited from these opportunities and grew into top smartphone brand companies worldwide.

The impact of Qualcomm’s IP strategy

The impact on platform modularity

To maximise the QCT and QTL revenues through its licencing model, Qualcomm intentionally lowered the degree of platform modularity. This resulted in the knowledge transferred to customers becoming less codified, the degree of product differentiation to become deeper, and the room for innovation expanding. Existing literature (Gereffi et al., 2005; Yasumoto and Shiu, 2007; Humphrey et al., 2018) views product modularity as an outcome of technological development; however, the Qualcomm case suggests that a firm’s IP strategy also has significant impacts on modularity.

Two methods were applied by Qualcomm to lower the modularity of the platform and support deep product differentiation (Interview 5, HERI, 2016). The first method was substantially opening the hardware driver source code, which enabled the ability to add various new hardware functions into a smartphone. Qualcomm opened approximately 80% of its hardware driver source codes to smartphone companies (in comparison to MTK, which opened only 20% of its source code) (Interview 6, a design house, 2017). This meant that Qualcomm users had a better opportunity to differentiate their products compared to MTK users. Two patterns defined the use of these hardware driver source codes. First, Qualcomm itself developed many special hardware functionalities, such as the soft light dual camera function, and the Sense ID ultrasonic fingerprint function, and allowed only one company, as the world’s first user, to differentiate its product by using these functions. For example, Xiaomi 5S was the first user to adopt the Sense ID ultrasonic fingerprint function, which was provided and supported by Qualcomm. During this process, Xiaomi made simultaneous use of the patents and source codes on this function. After a period (usually 3 months), other customers were allowed to adopt a similar feature and use related source codes (Interview 3, HERI, 2016). The second pattern was when smartphone manufacturers independently developed their own new functionality for their smartphone on the basis of Qualcomm’s hardware driver source codes. For example, OPPO Find 7 contained the Voltage Open Loop Multi-Step Constant-Current Charging (VOOC) flash charging function, which was developed by OPPO and was also the world’s first. Although Qualcomm developed its own flash charging technology, the company still supported the development of OPPO Find 7.

The second method used to lower platform modularity was to allow users to modify certain design parameters of a new platform before it was launched by Qualcomm. A good example is VIVO. Qualcomm usually shares the most original evaluation report on the new platform with VIVO, including important information on features, power consumption, launch dates, and costs. Based on this information, VIVO can request Qualcomm’s product definition department to adjust certain features and performance parameters, which go beyond the scope of a standardised Qualcomm platform, to meet the latest demand trends (Interview 2, VIVO, 2016).

In summary, to obtain more QCT and QTL revenues, Qualcomm has lowered the degree of platform modularity through the above two methods to provide customers with more opportunities for innovation. This, combined with the efforts to lower the degree of inter-firm modular governance, enabled Qualcomm and customers to achieve co-evolution.

The impact on value chain governance

Under its licencing model, Qualcomm has two options to maintain customer relations – to sell chipsets to a large number of customers as much as possible or to strengthen the relationships with a small number of leading customers. As its managerial resources are limited and most customers may not be equipped with strong technological capabilities to develop high-end products (under the first option), Qualcomm has formulated a strategy to support a few selected customers by shifting from modular to relational value chain governance. In Qualcomm’s monthly global support meetings, customers are categorised into five ranks in terms of shipments and product technology. 21 Leading customers ranked in the top position are given the highest priority for receiving new technological information, product customisation, and resolving problems jointly. Before releasing a new platform, Qualcomm closely communicates with leading customers to reflect the best possible requirements for it. After a platform has been adopted, Qualcomm often sends a team to its leading customers for joint product development (Interview 3, HERI, 2016). The company also allows leading customers’ research teams to visit its headquarters and jointly develop new products. Besides a technology assistant team and an after-service department, leading customers’ engineers can engage in face-to-face communication with Qualcomm’s core engineers and learn extensively from them (Interview 4, Qualcomm, 2016). This interaction is important for expanding tacit knowledge and the formation of technological capabilities (Ernst and Kim, 2002: 1425).

Among Qualcomm’s more than 300 licensees, very few companies are leading customers that receive such support. According to the data available from its 10-K filing for 2016, 2017, and 2018, the QCT and QTL revenues from Qualcomm’s top five customers – Apple, Samsung, Xiaomi, OPPO, and VIVO – were 54%, 58%, and 52% of its total consolidated revenues, respectively. 22 These five companies maintain a typical relational tie with Qualcomm, receiving direct support from the Qualcomm headquarters in San Diego. The lower the rank of a licenced customer, the weaker the support it receives and the more modular the relationship with Qualcomm is. For some unlicensed users, the governance mode was arm’s length market (Interview 9, OPPO, 2022).

Qualcomm also adjusts the degree of modular value chain governance at the smartphone model-level. When it jointly develops a series of smartphones with its customers, Qualcomm often concentrates on coordinating the development of the most sophisticated smartphone and then gradually reduces various performances of the product to lower-end products without further coordination. During this process, value chain governance becomes more modular (Interview 9, OPPO, 2022).

Qualcomm’s IP strategy was adopted before the emergence of 4G technology. However, the relational inter-firm governance, as a result of the IP strategy, has brought about greater advantages to Qualcomm’s leading customers, allowing them to better adapt to the technological change of 4G. First, technological changes in 4G made product modularisation more difficult, as radio frequency technology has become very difficult to standardise and integrate into the baseband IC. Under relational inter-firm governance, these customers could continually coordinate with the platform vendor, amplifier, and antenna suppliers to stabilise the telecommunication function (Humphrey et al., 2018).

Second, for 4G smartphones, the life cycle of a mobile phone model was shortened considerably, whereas the R&D cycle grew increasingly longer. The R&D of a smartphone application processor takes 2 years, and the product development of a finished smartphone takes 6–12 months. Under these circumstances, relational inter-firm governance enables platform vendors and users to exchange information on technology roadmaps and begin marketing as early as possible to develop a smartphone that precisely meets the needs of rapidly changing markets (Interview 3, HERI, 2016).

We now examine the impact of Qualcomm’s IP strategy on value chain governance towards Chinese customers in detail. All the top four Chinese brands (Huawei, Xiaomi, OPPO, and VIVO) started to use Qualcomm’s chipsets from their first smartphone model (Huawei in 2009 and others in 2011). Initially, except for Huawei, the technological capabilities of these companies were very limited. The numbers of engineers of the three companies were in the dozens on average. They relied heavily on outside design houses for R&D and received little support from Qualcomm. By increasing investments in technological and marketing capabilities, Xiaomi, OPPO, and VIVO gradually demonstrated greater potential for innovation and learning compared to other Chinese brands. Accordingly, they strengthened their relationship with Qualcomm. Xiaomi, for example, was allowed to send six engineers to San Diego for the joint product development of its second smartphone model Xiaomi 2 in 2012. Since OPPO collaborated with Qualcomm to develop the first 4G smartphone in 2014, and VIVO followed suit, the two companies received substantial support from Qualcomm (Zhihu, 2014; Elecfans, 2019). Thereafter, these three companies gradually entered into a virtuous cycle of cooperation and value co-creation with Qualcomm and eventually became the top tier customers (Interview 2, VIVO, 2016; interview 9, OPPO, 2022).

The case of VIVO, the third-largest smartphone manufacturer in China (2020), represents the aforementioned dynamic evolution of business relationships with Qualcomm (Interview 2, VIVO, 2016). Initially, as a small business, VIVO, which outsourced its R&D department to a design house, was unable to get any support from Qualcomm. Between 2011 and 2015, VIVO gradually internalised its R&D division, increasing the number of software development engineers from 37 to 700. VIVO also established 250,000 sales outlets in China during this time. All of these efforts significantly strengthened VIVO’s relationship with Qualcomm. During the time of our interview in 2016, VIVO interacted frequently with Qualcomm on various levels. At the engineer level, more than 10 individuals communicated with Qualcomm almost every day. At the middle management level, the person in charge of the R&D department communicated intensively with Qualcomm’s vice president at the Chinese branch every month. At the top management level, the CEOs, CFOs, and CTOs of the two companies met each other several times a year to discuss company affairs. Moreover, Qualcomm mobilised its global resources, including 30–40 engineers from Santiago, US, and Hyderabad, India, to support VIVO in the event of an emergent problem. These deep interactions at various levels and the resulting relational GVC governance chains enabled VIVO to develop better products with higher value added. This also brought more QCT and QTL revenues to Qualcomm, encouraging Qualcomm to strengthen its relationship with VIVO further.

Compared to Xiaomi, OPPO, and VIVO, Huawei’s case is more similar to that of Apple and Samsung (Interview 7, Huawei, 2017). Huawei had significant technological capabilities when it began using Qualcomm’s chipsets in 2009, and thus, the two companies have formed a relational tie. However, Qualcomm’s licencing model has limited Huawei’s further development in two ways, which ultimately encouraged Huawei to develop its own chipsets. 23 First, under the licencing model, the more value that is created by chipset users, the more royalties has to be paid. Downstream users thus always have an incentive to develop chipsets in-house to reduce their dependence on Qualcomm. For Huawei, because its technological and knowledge gaps vis-a-vis Qualcomm are not as large as those of other Chinese firms, the desire for in-house R&D of chipsets was thus particularly strong. Second, Qualcomm’s reverse patent licencing compelled Huawei to allow Qualcomm’s other customers to access Huawei’s huge patent portfolio free of charge. In order to protect its own IPs, Huawei similarly had to develop the chipsets in-house.

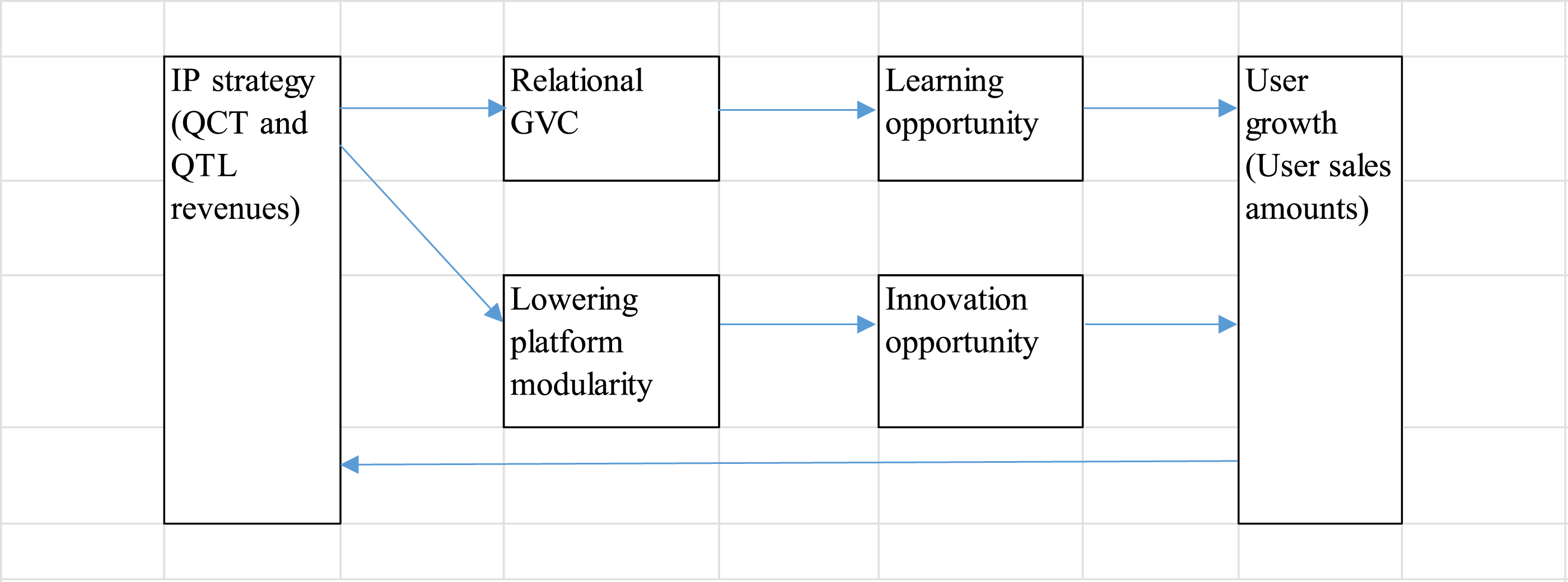

The mutual reinforcement mechanism included in the IP strategy

From the above discussion, it is evident that there is a clear mutual reinforcement mechanism included in Qualcomm’s IP strategy (Figure 4). The growth of customers, that is, the increase in customer sales amount (including sales volume and the wholesale selling price) and market share, will bring more QCT and QTL revenues to Qualcomm and better protects for IPs.

24

This will further motivate the company to invest more on R&D and provide increased innovation and learning opportunities to its leading customers by maintaining low degrees of platform modularity and shifting from modular to relational GVC relationships. Mutual reinforcement mechanism included in Qualcomm’s IP strategy. Source: The authors.

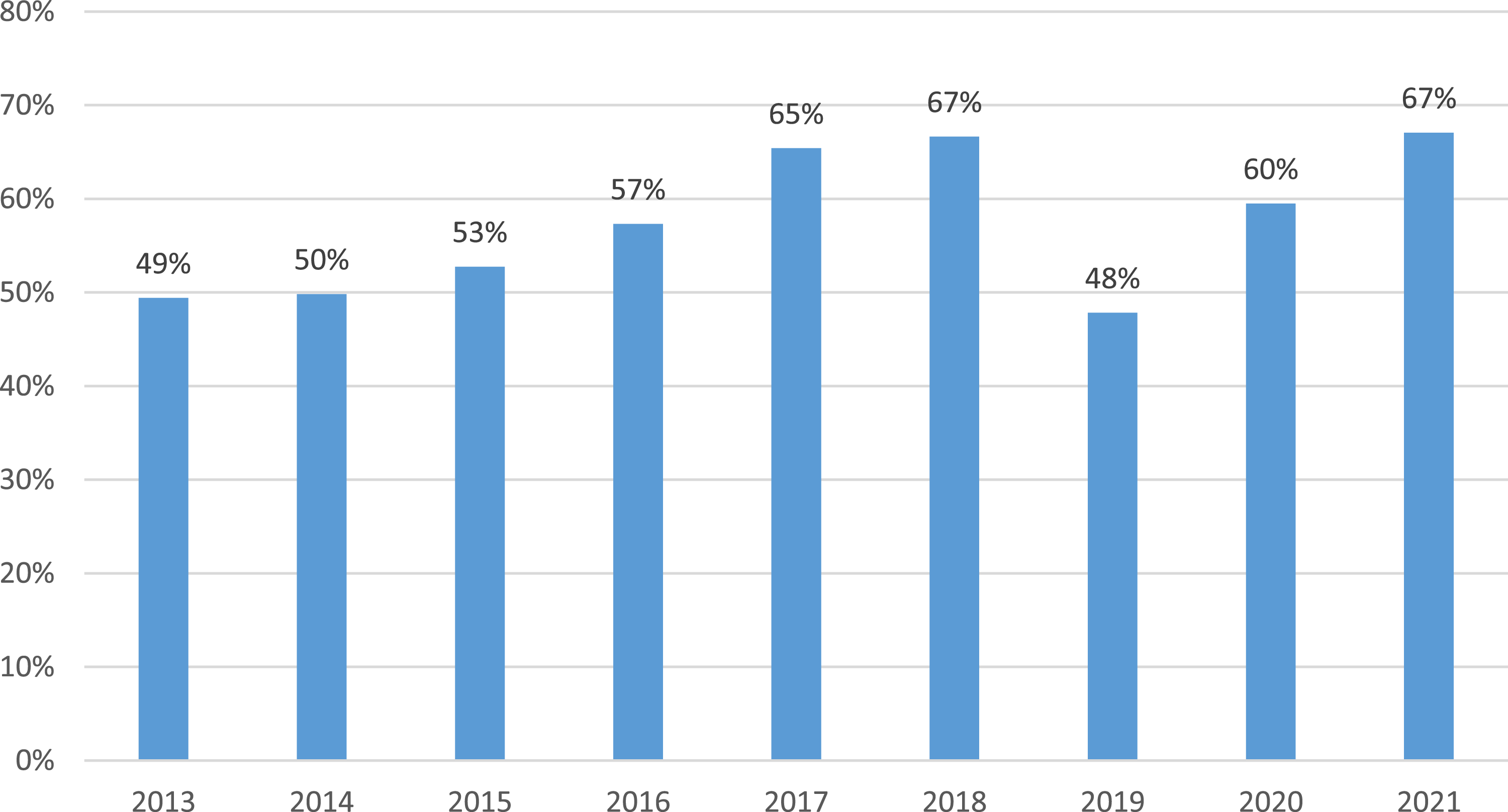

This mechanism is more significant in the Chinese market. As Figure 5 depicts, Qualcomm, which relies heavily on IP revenues, and the Chinese smartphone manufacturers, which have a large domestic market, have become increasingly interdependent.

25

The share of the Chinese market in the overall sales of Qualcomm continued to rise until 2018. After the sudden decline in 2019 (caused by a decline in sales to Apple, which is made in China by Foxconn, see Qualcomm 10-K, 2019), China’s share was soon restored to the previous level after. Shares of Chinese market (including Hong Kong) in the total sales of Qualcomm. Source: Authors calculated based on Qualcomm 10-K, 2015, 2018, 2021.

The Chinese market is important for generating the mutual reinforcement mechanism in three aspects. First, after the 2010s, this market’s demand continued to grow. 26 The middle-class population in China reached 400 million in 2017 (NDRC, 2021), this provided ample room for conducting deep product differentiation by smartphone manufacturers and enabled them to heavily invest in R&D. For feature phones, sales volumes for new models were at most two million units, whereas sales volumes for a single model of smartphone were more than 10 million units. For example, sales volumes of the most popular flagship OPPO and VIVO models – the R9 and X9 – amounted to 20 million units in 2016 (Interview 3, HERI, 2016). The significant increase in sales of a single model means that Chinese smartphone manufacturers can enjoy the benefits of the following virtuous cycle: gaining great revenues from a single model, investing heavily in R&D, strengthening relationships with Qualcomm, sharing more core knowledge and receiving increased support, and eventually developing better model smartphones.

Second, mobile internet in China rapidly developed during the 4G period. Between 2014 and 2019, the number of mobile internet users in China increased from 597 million to 897 million, or 43.6% to 64.1% of the total population (Guan, 2021). Given its large number of mobile internet users, China has fostered various world-class platforms and APPs such as WeChat, Taobao, and Didi. The social networking and transaction requirements generated by these platforms and APPs have forced Chinese companies to develop smartphones with faster data transmission speeds, more stable systems, and clearer camera functions.

Finally, the huge and growing market strengthened the bargaining power of the Chinese government and indirectly strengthened the above mutual reinforcement mechanism. Qualcomm’s licencing model is criticised as abusing market dominance to obtain excessive profits (Hsieh, 2019; Rato and Petit, 2013; Williams, 2018). Therefore, the company has been investigated by global anti-trust authorities. In China, during anti-trust investigations in 2015, in addition to a huge fine of 6.1 billion RMB, the basis for Qualcomm’s royalty collection was reduced from 100% to 65% of the wholesale selling price, and the reverse patent licencing model was abolished in 2015 (Qualcomm 10-K, 2015). 27 Conversely, during the anti-trust investigation of Qualcomm in Korea and Taiwan, which do not have a huge domestic market, the company was only asked to pay fines but the ratio of royalties was not reduced (Qualcomm 10-K, 2017, 2018, 2019). The comparatively lower ratio of royalty collection has motivated Chinese smartphone companies to invest more in innovation, which has led to strengthening their relationship with Qualcomm and enhancing the above-mentioned mutual reinforcement mechanism.

Conclusion

There is a billboard installed by Qualcomm at Shenzhen Airport, China, that includes a striking message: ‘Qualcomm, by sharing inventions, helped seven Chinese handset brands to rank among the top 10 in the world’. This message does not seem to exaggerate. By formulating a well-designed IP strategy, Qualcomm succeeded in helping a few Chinese smartphone companies learn, upgrade, and innovate.

Qualcomm’s case helped us to better understand the two research questions in this study: How does IP strategy lead to learning and innovation in technological platform-driven GVCs? How does IP strategy and changes to GVC governance facilitate this learning and innovation transfer across firm actors in technological platform-driven GVCs? As for the first research question, this case shows that a platform vendor’s IP strategy can have positive impacts on knowledge transfer in GVCs. Existing studies attribute limited knowledge transfer to poor IP protection or weak technological capabilities in developing countries but largely ignores the role of IP holders themselves. Qualcomm’s case reveals that with a well-designed IP licencing model, a platform vendor will be strongly motivated to share knowledge with platform users in developing countries while protecting its own IPs by collecting licencing fees and royalties simultaneously.

Qualcomm’s licencing model on the one hand enabled the company to collect exact and sufficient licence fees and royalties from its chipset users. This motivated Qualcomm to support chipset users to beat non-Qualcomm competitors and increase their market shares. On the other hand, Qualcomm’s licencing model is essentially a sharing contract under which platform users’ expansion of sales volume, the increase in value added, and the accumulation of technological capabilities directly increased Qualcomm’s QCT (Qualcomm CDMA Technologies) and QTL (Qualcomm Technology Licencing) revenues. Qualcomm is thus strongly encouraged to share various knowledge with its users, including on fundamental mobile communication technologies, patents, source codes, and technology roadmaps that enable the development of a final smartphone as well as tacit knowledge generated during the process of product development.

Regarding the second research question, the Qualcomm case indicates that IP strategy can affect the modular governance inter-firm relationships of platform-driven GVCs. Under the unique licencing model, Qualcomm was encouraged to support a small number of selected customers with great potential for learning and innovation and help them create value. Thus, on the one hand, Qualcomm lowered the degree of platform modularity by substantially opening the hardware sources code and allowing the adjustment of platform design parameters, which significantly increased the opportunities of innovation and deep product differentiation. On the other hand, Qualcomm intentionally shifted to a relational governance mode with a few selected Chinese smartphone manufacturers, whereby the company intensively interacts and exchanges knowledge, which provided ample learning opportunities to the latter. Consequently, a mutual reinforcement mechanism was established between Qualcomm and the Chinese smartphone customers, under which they have achieved co-evolution in terms of value creation, capability formation, and IP protection.

Qualcomm’s case appeared to be unique as its business model relied heavily on technology licencing and achieved significant success in the collaboration with customers in developing countries. However, in the long run, the Qualcomm model may become more general. With increasingly intensified competition and larger R&D investments in high-tech sectors, an increasing number of companies, especially technological platform vendors, may adopt similar IP strategies, concentrating on the development of core technologies and relying more on IP revenues.

Future studies will need to focus more on the dynamically shifting relationships between platform vendors and users in GVCs. Indeed, following Huawei, Xiaomi, OPPO, and VIVO, have all began to develop chipset in-house in recent times. Will these companies use their own chipsets more frequently, and break down the co-evolution with Qualcomm? What impact will this have on GVC governance through IP strategy?

Future studies should also identify more success stories of IP strategies formulated by other types of lead firms, such as global buyers, and the IP strategies of other types of intangibles, such as brands, trademarks, and software. It is only after the accumulation of more qualitative and quantitative studies that we can generalise and theorise the significance of IP strategy on GVCs.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Japan Society for the Promotion of Science (24330072) and Institute of Developing Economies, Japan External Trade Organization (IDE-JETRO); (2016_2_20_001).