Abstract

This article’s endeavour is to explore the consequences of remittances on the growth of an economy by employing a panel of 17 selected remittance-receiving Asian nations over the years, stretching from 1993 to 2017. Initially, the study used the panel unit root test to identify whether the variables are stationary or not. Subsequently, by using cointegration test, a long-run association among the variables was seen. Finding a long-run relationship, ‘fully modified ordinary least square’ method has been applied to examine the impact of remittances and other explanatory variables on the output per capita of Asian nations. The coefficient of remittances being positive and statistically significant implies that remittances enhance growth in these countries. Inflows of remittances to the Asian region are abundant and, considering the present trend of migration, it is likely to grow. To maximize the developmental effects of these inflows, developing pro-remittances in formal public and private infrastructure are a crucial policy target for governments in the region. Moreover, in addition to conventional determinants of growth like investment in human and physical capital, trade and foreign direct investment (FDI), Asian countries can increase their growth by mobilizing the remittances.

Introduction

The trend of remittances in the past two decades has led to newer developments in the discourse of remittances. This discourse has been developed due to the remarkable rise in remittance flows into the developing nations. The World Bank (2006) claimed that the developing nations received US$436 billion as remittances, which formed approximately 75% of the entire world’s remittance flows in 2014. Valued at US$256 billion in the year 2016, Asia accounted for approximately 50% of the entire remittance inflows into the developing nations. Simultaneously, the output of the Asian economy has also been rising at a considerably high rate. This implies that rising inflows of remittances may be one of the drivers of rising output in the Asian economy.

During the second half of the century, researchers working on economic development of developing countries have recognized surplus labour (Lewis, 1954), investment in human capital (Barro, 1991; Romer, 1986), technology change (Solow, 1956), physical capital investment, foreign aid (Chenery & Strout, 1966), foreign direct investment (FDI) (Balasubramanyam et al., 1996; Grossman & Helpman, 1991; Romer, 1990) and research and development (Aghion & Peter, 1992) as the main drivers of growth. In addition to this, some other researchers have focused on the role of institution, freedom and social capital as the main drivers of growth and development (Owens, 1987; Sen, 1999; Westlund & Adam, 2010).

Along with these factors, researchers (Giuliano & Ruiz-Arranz, 2009) insist that remittances are also considered as one of the foremost factors, which enhance growth. According to them, remittances can enhance the growth of an economy in countries with weak financial sectors by extending a substitute way to overcome credit constraints. Research by Acosta et al. (2007) and Adams and Page (2005) also validate that these inflows are positively related to growth rates and are negatively associated with poverty-related indicators. These huge inflows lead to a formation of human capital, declining child labour and promote entrepreneurial activities in the recipient countries (Yang, 2008). Yang (2004), in Philippines, found that remittances support the families of the migrants by reducing their credit constraints. In line with Yang, Aggarwal et al. (2011) have shown that remittances help to overcome liquidity constraints and thereby enhance development of the developing countries financially.

The existing studies linking the remittances with the growth of an economy are contradictory in nature. Few researchers like Faini (2007) as well as Ramirez and Sharma (2008) observed that there exists a positive effect of remittances on the growth of an economy, while some others (Barajas et al., 2009; Gupta, 2005; International Monetary Fund [IMF], 2005) find an inverse or absolutely no relationship. Therefore, the evidence on the relationship between remittances and growth is not conclusive in nature.

Thus, to address this issue in the Asian context, this article endeavours to explore the consequences of remittances on the growth of an economy by employing a panel of 17 selected remittance-receiving Asian nations over the years, stretching from 1993 to 2017.

This article is presented in terms of the following sections. Given the introduction in Section I, Section II provides a glimpse into the inflows of remittances in the selected 17 Asian nations. Section III outlines the theoretical framework on the linkage between remittances and growth of an economy. Section IV provides a brief review of literature on the relationship between remittances and economic growth. Section V deals with materials and methods of the study. Section VI consists of the results and analysis of the outcomes obtained after applying the appropriate methodology. Finally, Section VII provides the conclusion, which summarizes the entire study undertaken and proposes few policy recommendations.

A Glimpse into the Inflows of Remittances in the 17 Selected Asian Countries

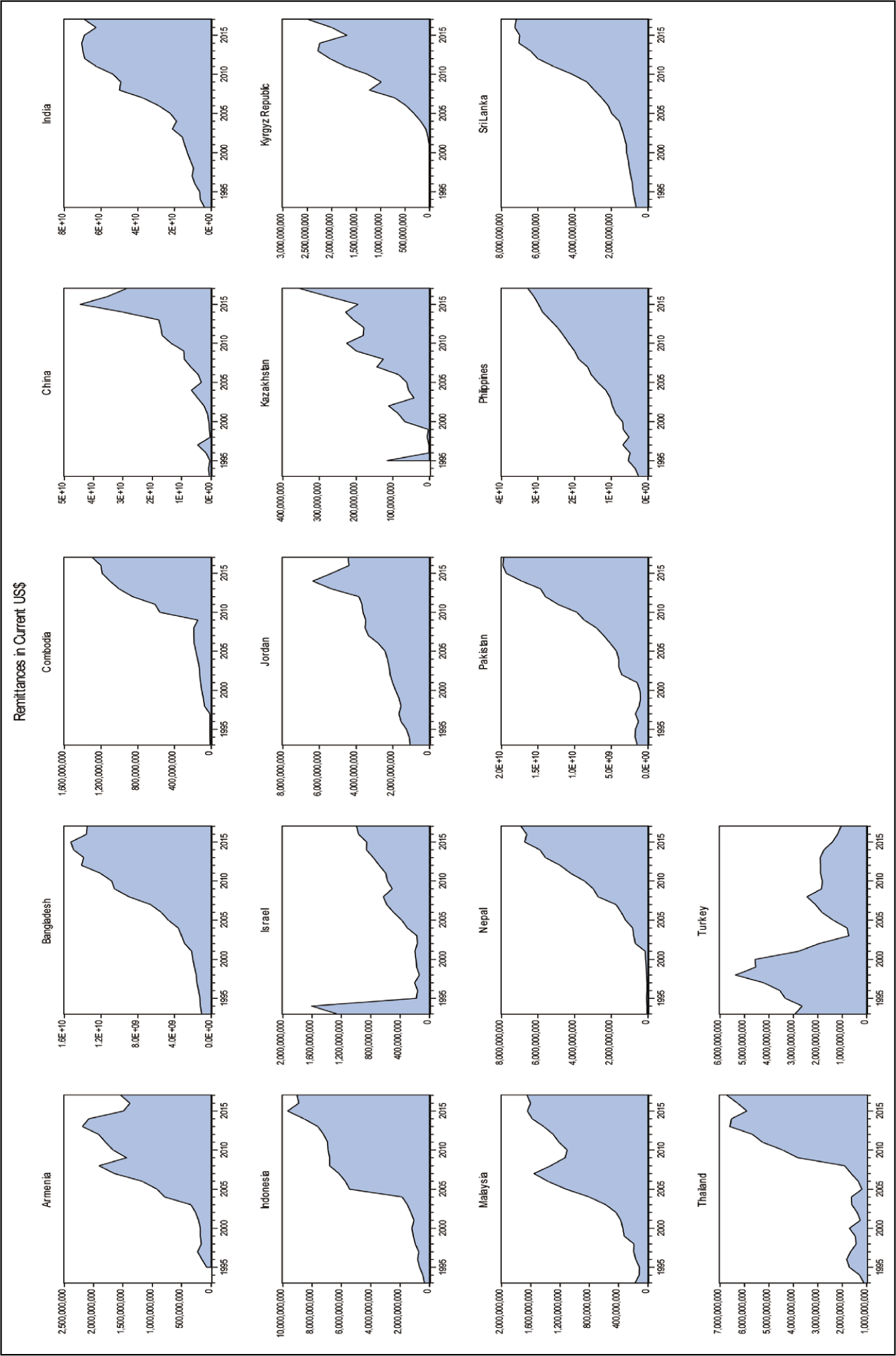

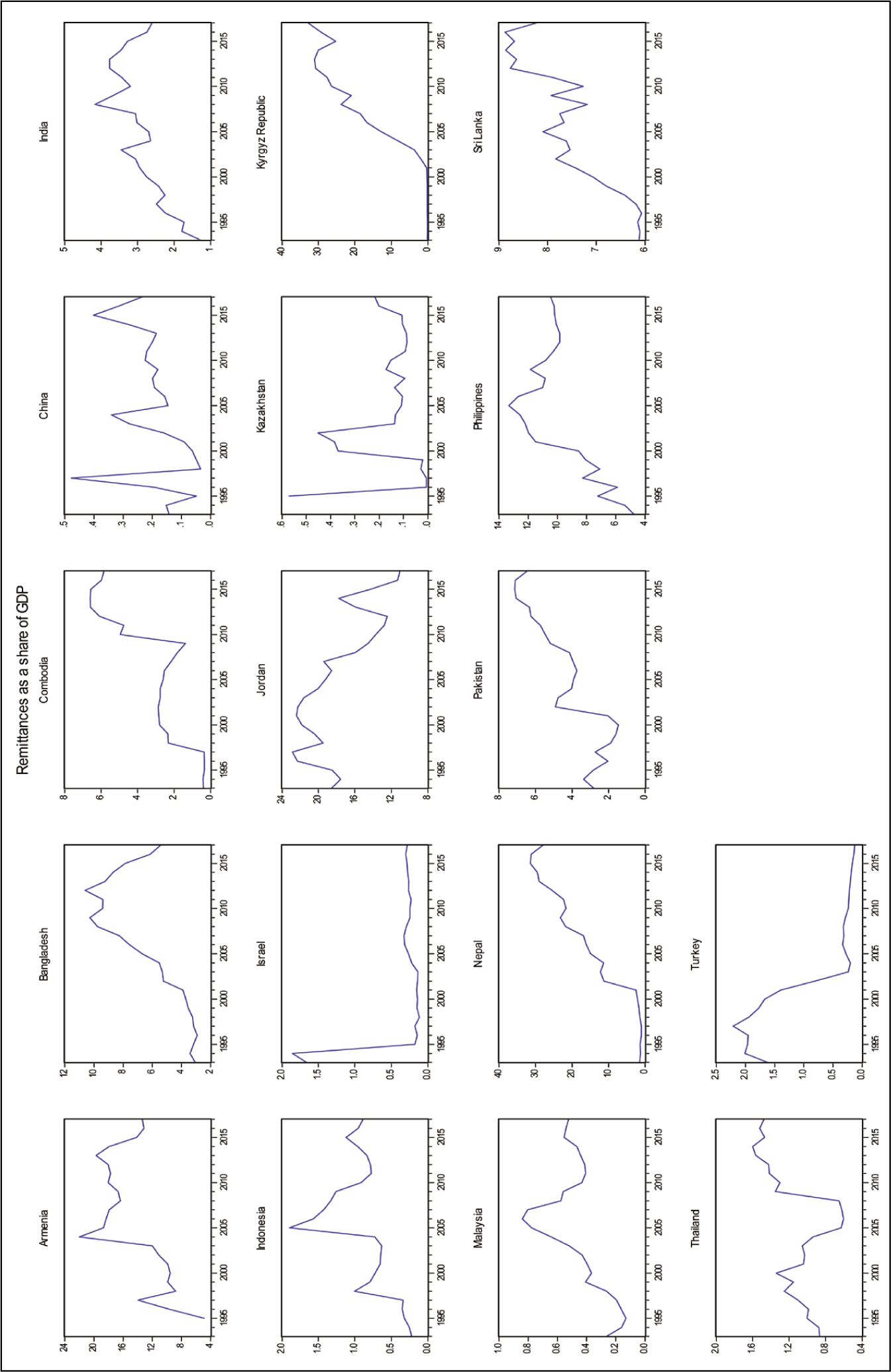

Remittances are generally accepted to be one of the tangible benefits of migration in the developing countries. As stated by the International Fund for Agricultural Development (IFAD, 2017), the Asian region is the ‘the most dynamic region for both remittance flows and migration growth’. With the highest outflow of migrant workers from the region, Asia is the largest beneficiary of remittances. Out of the top 10 remittance-receiving countries, seven hail from Asia. Figure 1 of the article shows the time series data of remittances from 1993 to 2017 for the 17 selected countries. These nations have been picked in terms of availability and uniformity of the data. Among the recipient countries, in 2016, China and India had accounted for half of the total remittances coming into Asia, where India received US$63 billion, while China received US$61 billion. It has been observed from Figure 1 that since the year 2000, India is the major recipient of the inflows of remittances. On the other hand, remittances that China received in 2000 were much lower, but between 2000 and 2017, it has risen significantly. The remittances received by some Asian countries constitute a significant percentage of their GDP (Figure 2). For instance, remittances flowing into Nepal form a considerable portion of their GDP. It has been observed from Figure 2 that remittances accounted for almost 30% of Nepal’s GDP in 2016. Remittances to GDP ratio of Nepal was only 2% in 2000, and it has risen sharply in the past 17 years. Remittances have a positive impact on the government revenue, helping to raise liquidity in the financial institutions of Nepal (Bhattarai & Subedi, 2021). Similarly, in the case of Kyrgyz Republic, remittances amounted to 31% of its GDP in 2016. Looking at the data of the past 10 years, it is observed that the remittances to Bangladesh and Philippines range from 8% to 12% of their country’s GDP. In 1993, remittances were 3% of Bangladesh’s GDP, which jumped to around 6% in the year 2017. With an almost 9% remittances to GDP ratio in 2017, Sri Lanka also has experienced stable inflows of remittances over time (see Figures 1 and 2). Similarly, in the case of Pakistan, in the year 1993, remittances were 2.8% of the GDP, which increased to 6.45% of the GDP in the year 2017.

Out of the 17 selected countries, China and Kazakhstan have the lowest remittances to GDP ratio. The contribution of remittances to GDP was around 0.5% and 0.1%, respectively, in 2016. Though China is the recipient of a very large inflow of remittances, remittances to GDP ratio is very low due to the wide expansion of the economy. Going through the data, it has been observed that, on an average, remittance to GDP ratio is less than 1% in the world, and it is sufficiently lesser than half of that in developed economies.

Over the years, the existing literature focusing on the developmental effect of remittances for the recipient’s countries has offered various viewpoints. As per the neoclassical approach of the 1960s, at the microeconomic level, the process of migration is seen as a process, which optimally allocates the various factors of production for the general benefit. This theory suggests that the process of factor price equalization will ultimately result in the stoppage of migration when the wage levels of the home and the host country are at par. According to this viewpoint, the movement of labour from agricultural and rural regions to the industrialized and urban regions is a necessity for economic growth (Todaro, 1969). However, during the 1980s and the 1990s, the new economics of labour migration (NELM) approach appeared in response to the neoclassical theories. The scholars of this approach argued that migration is instrumental in supplying prospective investment that is specifically vital in the case of imperfect capital and insurance (risk) markets, which mostly exist in the developing nations (Stark, 1991; Taylor & Wyatt, 1996). These kinds of markets are usually underdeveloped and not accessible to the non-elite groups.

Therefore, migration is viewed as an approach of livelihood to overcome market restrictions and encourage the families to undertake investment and industrious activities, which will enhance their incomes. In accordance with the livelihood and NELM approach, latest studies centred on microeconomic approach, like that of Quinn (2006), have supported the viewpoint that movement of labour is more akin to being an income tactic undertaken by people in response to scarcity rather than a response to impoverishment (Hampshire, 2002). The hypothesis of relative deprivation postulates that the households endeavour to enhance their economic status through migration in the home country. The households that suffer from deprivation are more probable to strategize and undertake migration as a medium of strengthening their financial base.

The focus of the microeconomic approach emphasizes on the causes as well as the usage of remittances, while the other trajectory sheds light on the impact that remittances have and employs a macroeconomic model to examine the effect of remittance inflows on the home countries. Barajas et al. (2009) identified three channels through which these monetary inflows can impact economic growth.

First, the inflows of remittances may affect the economic growth by directly influencing the rate of capital accumulation. In the case of financial constraints faced by households for investment purposes in the home country, remittances help to enhance the financial capacity of the households, thereby contributing to the economic growth. This can be linked with the self-interest motive of the remitters as the migrants would invest in their home country so as to generate an added source of income for the households.

The second channel is the growth of labour force in the economy. The beneficiary of remittances may regard the amounts received as an alternative to labour income, and this may result in increased leisure activities. Among others, the resultant effects are a decline in labour workforce participation, reduction in the labour efforts and disinterest in job searches or investment in high-risk projects. By using a two-sector dynamic stochastic general equilibrium (DSGE) model, Acosta et al. (2007) have shown that with a rise in remittance, there is a decline in labour supply, accompanied with higher consumption levels that are more inclined towards non-tradable items. Based on this model, Shapiro and Mandelman (2016) have found that, on the one hand, countercyclical nature of remittances restricts the contraction in consumption and investment in the face of any downturn and, at the same time, leads to a decline in supply of salaried labour. This process counteracts the upward pressure on wages during the time of recession, and in turn, unfavourably affects the process of recovery of an economy. In line with this, Annen et al. (2016) have used a DSGE-RBC (real business cycle)model and found that, on the one hand, the income effect caused by a permanent rise in monetary transfers can result in a reduced output in the long term, while, on the other hand, the temporary shocks in transfers of wealth seem to have a positive impact on output as well as investment.

The final channel is the total factor productivity through influences of remittances on the real effective exchange rate (REER) (Chami et al., 2005). The remittance inflow puts upward pressure on REER and, in turn, reduces the competitiveness of the tradable sector in the economy. In view of the inflows of remittances, another mechanism that seems to affect REER was discussed by Acosta et al. in 2007. They have observed that with a steady rise in the income of any given household, there is a decrease in labour supply, as the recipients of the remittances tend to choose leisure over work. A fall in the supply of labour causes an increase in the wages of the labourers. Eventually, this process will lead to an increase in the production cost, thereby creating shrinkage of the tradable sector. The effects discussed here, that is, resource allocation effects and labour effects, can lead to an increase of the REER, which will reduce the competitiveness of the tradable sectors of these economies internationally.

Studying these three distinct channels, we can deduce that there is a dual impact of remittances. As there is no theoretical unanimity among the economists and scholars regarding the possible impact of inward remittances on the economic growth, one approach to resolve this debate is to examine this issue empirically. The older empirical studies examining the connection of economic growth with remittances show mixed results (see Section IV). This variation in the different empirical research can be attributed to the usage of different methodologies to examine the results, variance across countries, model specifications and time horizons. Keeping this in view, the study utilizes panel data analysis to probe into the relationship between inflows of remittances and economic growth in the selected 17 Asian nations.

Literature Review

Remittances can affect economic growth of an economy through different channels. One of the micro-evidences on impact of remittances shows that it can promote entrepreneurial activities by reducing the credit constraints (Yang, 2004). Lack of access to credit due to less efficient credit and financial market is one of the prime concerns for the households in developing countries. By reducing credit constraints, remittance inflows can help these households to indulge into entrepreneurial activities. In line with this, Giuliano and Ruiz-Arranz (2009) have also concluded that remittances enhance financial development by reducing the problem of liquidity constraints. Using panel data estimations over the years (1975–2003), Aggarwal et al. (2011) find a direct relation of remittances and financial development. In addition to the financial development channel, remittances also help in the formation of human capital, which is recognized as one of the most prominent drivers of growth. Yang (2008) finds a direct relationship between remittances and schooling of children in Philippines. Calero et al. (2009) in their study in Ecuador find similar results. In line with this, Acosta et al. (2007) conducted their study in 11 countries of Latin America and show that remittances are associated with education and health of the children of those countries.

Apart from this, remittance inflows can considerably affect the credit worthiness of the country and hence increase its reach to the international capital market. The World Bank (2006) has claimed that a country’s credit rating is calculated on the basis of the magnitude of remittance receipts of the country. A country can reach a high credit rating if the magnitude of its remittance inflows remains high and stable. Credit from international credit market can help a nation boost its human capital and physical investments, thereby boosting the economic growth of the nation. In addition to this, some countries can make use of the opportunity of stable flows of remittances and accept remittances in the form of international capital market securities as collateral and forward the transaction to the recipient at lower rates. One of the major examples of such securitizations was in Mexico in 1994, where the workers’ remittances were readily accepted in long-dated international capital market securities (Ketkar & Ratha, 2001). According to Nyamongo and Misati (2011), Turkey is the largest issuer of remittance-backed securities at 35% followed by Brazil (31%) and Mexico (24%). This can help a country to convert the remittance flow from consumption expenditure into investment expenditure and help in boosting the economy towards higher growth.

The study on the remittances and growth is found to be debatable in nature, with claims and counterclaims. Out of the studies which have directly linked remittances and growth of an economy, Fayissa and Nsiah’s (2010) comprehensive study is worth mentioning. They used data related to 36 African nations and observed that the remittances impacted positively on the growth of an economy. Employing a similar method, Ramirez and Sharma (2008) confirm similar findings in the case of Latin American and Caribbean countries.

Apart from these positive strands of literature, contradictory findings have also been well documented in the literature. For instance, Lim and Simmons (2015), in their study, find that remittances do not increase economic growth. According to them, people mainly use it for consumption, and it has a nominal effect on productive investment. Similar to Lim and Simmons, Gupta (2005) and IMF (2005) find no association between remittance inflows and growth. Chami et al. (2005) have claimed that remittances slow down the growth of an economy by reducing the recipient’s motivation to work and increasing financial dependency. In addition to this, researchers like Amuedo-Dorantes and Pozo (2004) state that the inflows of remittances might harm a country’s competitiveness by appreciating the real exchange rate.

Materials and Methods

Specification of the Model

The model adopted for analysis relies on the following neoclassical production function.

where Yit is the output, Ai0 is the technological advancement of the country and Vit denotes the main variable of interest, that is, remittances and other control variables used in the study. The parameter, θit encompasses the effects of growth of the variables in Vit. Kit represents the physical capital in country i in period t, Hit is the status of human capital in country i in period t, Lit is the labour force in country i in period t and eit is the random error term. In addition to these, the growth effects of omitted variables are captured by the parameter ϑ. Equation (1) is divided by L, and it resulted in the following form:

where, yit is the per capita output, k denotes the per capita physical capital and h represents per capita human capital. Converting Equation (2) in a natural logarithm form gives the following expression:

Integrating the components of Vit in Equation (3) gives us the following equation:

where, rem is the migrant remittance, open is the openness of the economy, FS is the financial status and Govt. Exo represents government expenditure. The coefficients θi, (i = 1, …, 5) corresponds to the responsiveness of output per capita with respect to remittances, trade openness, financial status, government expenditure, physical capital and human capital, respectively.

Ordinary least square regressions with remittances and financial status as independent variables do not address issues regarding endogeneity. It fails to account the problem of endogeneity (Kumari & Bharti, 2021). However, based on the literature, it is plausible that the magnitude of both remittances and financial status increases with higher growth rates. Thus, it would lead to an overstatement of the effects of both the variables. In the existing literature, it is generally seen that variables are not subject to reverse causality like creditors’ right, and a country’s legal system is most commonly used as an instrument for the variable financial status (La Porta et al., 1997). However, these variables do not vary over time, and so they cannot be used in panel framework. Thus, the problem of endogeneity has been addressed by employing the fully modified ordinary least square (FMOLS) method. This method has advantages over ordinary least square method as the estimator since the problem of endogeneity and serial correlation can be taken into consideration.

Data and Variable Description

To attain the objective of this article, annual data of 17 chosen countries have been taken into account over the period of 1993–2017.The study has chosen 17 countries in terms of availability and uniformity of the data. The selected 17 countries are Bangladesh, China, Armenia, Cambodia, India, Israel, Jordan, Indonesia, Philippines, Kazakhstan, Kyrgyz Republic, Malaysia, Nepal, Sri Lanka, Pakistan, Thailand and Turkey.

Output per capita is the dependent variable of the study. There has been a general perception that has been agreed upon by various researchers like Mankiw et al. (1992) and Barro (1991) on the positive role of human capital on output per capita. The study used human capital index as a proxy variable for the human capital, and data for human capital index are obtained from the Penn World Table (Feenstra et al., 2017). The data on physical capital have also been obtained from the Penn World Table (Feenstra et al., 2017). The study anticipated that physical and human capital will have a positive effect on output per capita in selected Asian countries. Regarding remittances, the study hypothesizes that the inflow of remittances drives economic growth by directly influencing the rate of capital accumulation. In the case of financial constraints faced by households for investment purposes in the home country, remittances help to enhance the financial capacity of the households, thereby contributing to the economic growth. This can be linked with the self-interest motive of the remitters as the migrants would usually invest in their home country so as to generate an added source of income for the households.

The study employed the ratio of remittances to GDP to measure remittances. We have collected the data on remittances from World Bank Development Indicators (World Bank). Inopenness i,t is the openness of the economy, which is measured by the ratio of export to GDP. Like remittances, data on openness have been collected from World Bank Development Indicators. Openness is expected to positively affect the growth of the economy. Berg and Krueger (2003) claimed that it allows the countries to promote innovation and entrepreneurial activities via increasing the competitiveness and access to large markets. Furthermore, existing literature (King & Levine, 1993) on growth also emphasized the significance of financial development of a country on economic growth. The study incorporated the financial status of the countries as one of the regressors in the empirical model, and it is expected to have a positive effect on output per capita. The ratio of domestic credit to the private sector is expressed as a percentage of GDP as a proxy for financial status. This is recognized as one of the standard measures of financial depth in the existing literature (King & Levine, 1993; Levine et al., 2000). The data on financial status have been taken from World Development Indicator (World Bank). Moreover, the model of the study used government expenditure, which is not only used to capture the effect of fiscal policy (Barro, 1991) of a country, but it is also regarded as an important contributor towards economic growth of a nation. In developing countries, it has a significant influence on the distribution and allocation of resources. Like financial status, data on government expenditure has also been taken from World Development Bank Indicator (World Bank).

Methodology

Stationary Test

At the initial stage, it is essential to see whether the given data are stationary or not. For this purpose, the study has conducted two tests recommended by Levin et al. (2002) and Im et al. (2003). These two tests are generalization of augmented Dickey–Fuller (ADF) test for time series approach and overcome the problems of complicated limiting distribution in individual time series techniques. The test recommended by Levin et al. (2002) is popularly known as Levin–Lin–Chu (LLC) test, and it assumes the presence of unit root in null hypothesis, while the opposite is the case in the alternative hypothesis. Furthermore, it assumes common unit root process through the all-panel members. In contrast, the Im–Pesaran–Shin (IPS) test assumes individual unit root process through all the panel members. Accordingly, the null hypothesis for IPS test is that H0: ρi = 0 for all is against the alternative hypothesis of H1: ρi < 0 for some is or for at least one i.

Structure of the LLC and IPS tests can be shown in the form of the following ADF regression equation:

Where , Pi= number of flags, and

Cointegration Analysis

Following the stationary test, the subsequent step is to analyse the cointegrating association among the variables. For analysing the cointegrating relationship, the study has used Pedroni (1999) as well as Kao (1999) residual cointegration test methods. Pedroni recommended two types of cointegration tests, namely panel test and group test. The panel tests are also commonly known as ‘within dimension’, which contains four test statistics, namely ‘Panel-v’, ‘Panel-rho’, ‘Panel PP-statistic’ and ‘Panel ADF-statistic’. In contrast, group tests are also known as ‘between dimension’, and that encompasses three test statistics, namely ‘Group-rho’, ‘Group PP-statistics’ and ‘Group ADF-statistics’. These seven test statistics are based on estimated residuals from the following regression specification:

where ai = fixed effects specific to countries, and δ i indicates deterministic time trend. The term ε i,t denotes estimated residuals, and the following regression equation is performed on it to assess the null hypothesis of no cointegration.

‘Within-dimension’ approach assumed null hypothesis, that is, H0: ρi = 1 for all i against the alternative hypothesis, that is, H1: ρi < 1 for all i. However, ‘between-dimension’ Approach assumed null hypothesis, that is, H0: ρi = 1 for all i against the alternative hypothesis, that is, H1: ρi < 1 for at least one i.

Kao (1999) cointegration test is basically an extension of the Dickey–Fuller and ADF test of univariate time series modelling in the context of panel data. This test is grounded on the Engle–Granger two-step procedure, and it assumes homogeneity across all panel members.

The Fully Modified Ordinary Least Square

To estimate the long-run relationship, the study has performed FMOLS, for which the following regression equation has been considered:

where, ai = country-specific fixed effects, yi,t represents output per capita, β denotes vector of slopes (k, 1) dimension and ui,t is the stationary random terms. xi,t denotes (k, 1) vector of independent variables. It is presumed that the explanatory variables are integrated processes of order one (I(1)) for all i, where

We obtain FMOLS estimators by making endogeneity and serial correlation to the OLS estimator. The resulting FMOLS method can be expressed in the given equation:

where,

Outcomes of the Stationary Test

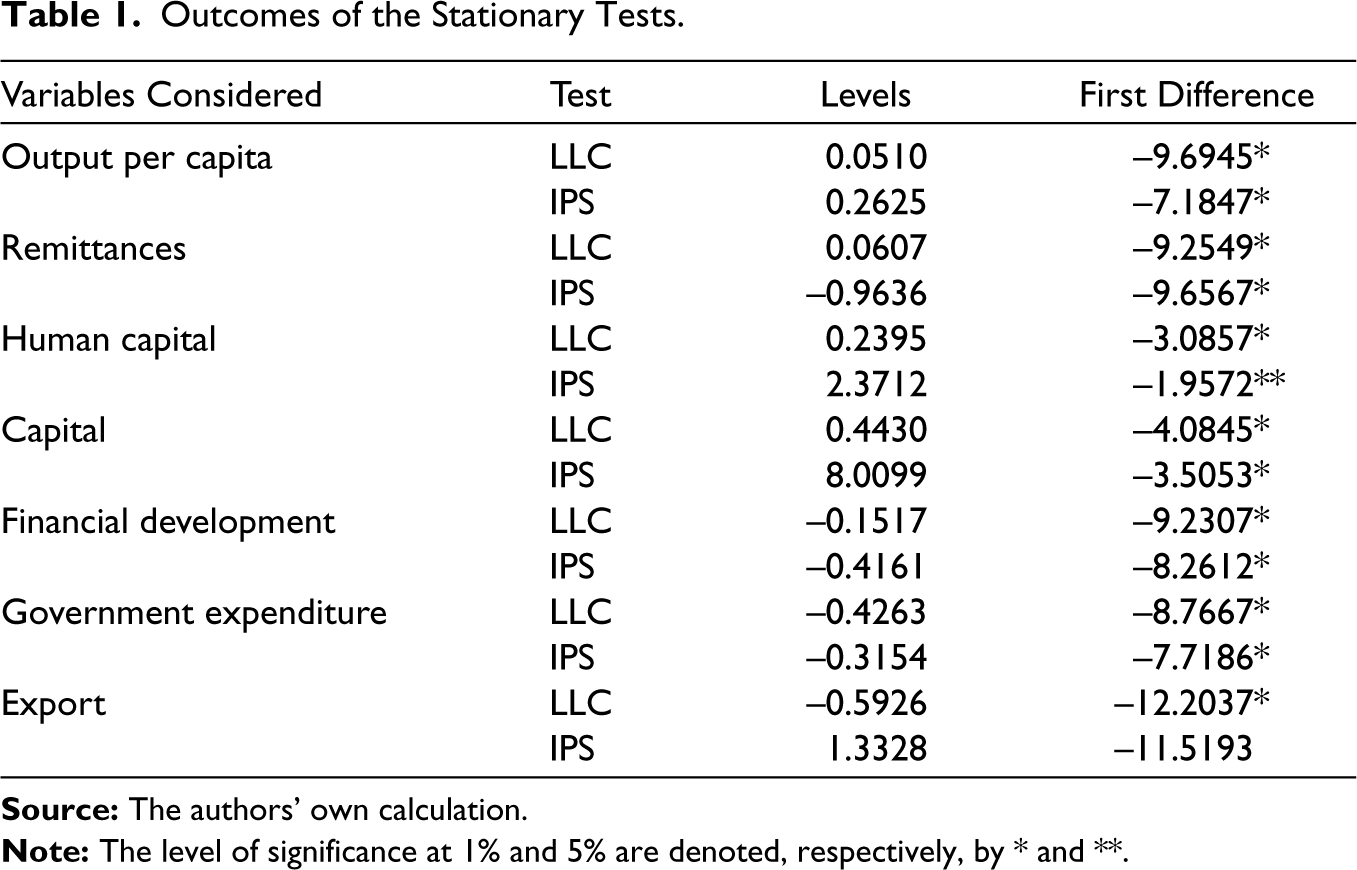

To determine the appropriate method of estimation, it is mandatory to test the stationarity characteristics of the variables used in the study. As mentioned in section ‘Methodology’, the study applied two tests, namely LLC and IPS tests to detect the stationarity characteristics of the variables. Table 1 displays the outcomes of these tests. The study applied both these tests to all concerned variables in their levels and first differences. It has been concluded from the results that the variables have been found to be non-stationary at their levels and turn out to be stationary in first difference.

Outcomes of the Stationary Tests

Outcomes of the Stationary Tests

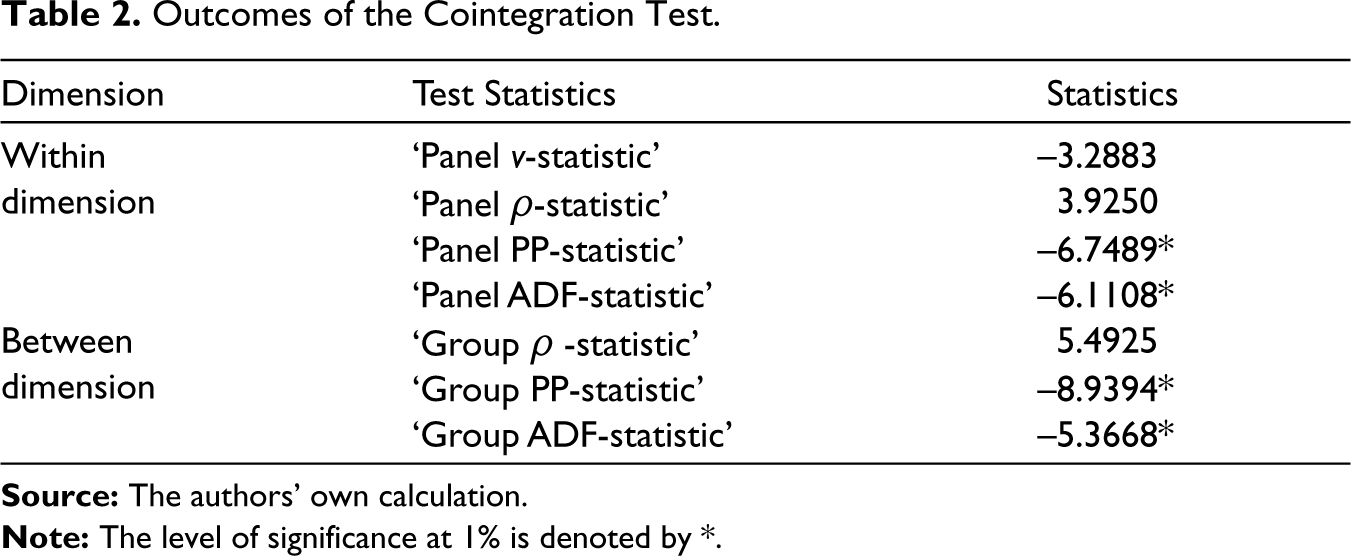

Outcomes of the Cointegration Test

Table 2 presents the outcomes of the Pedroni’s cointegration test. It has been observed from the results that two test statistics under ‘within-dimension approach’ have discarded the null hypothesis of no cointegrating relationship at the 1% level of significance. Likewise, in ‘Between-dimension approach’, two test statistics discard the null hypothesis of no cointegrating relationship at the 1% significance level. On the whole, the results show that four out of seven test statistics have discarded the null of no cointegration among the selected variables at the 1% significance level.

Outcomes of the Cointegration Test

To support the outcomes of the Pedroni cointegration test, the study also applied Kao residual cointegration test. Table 3 presents the outcomes of this test. It has been observed that this test also endorses the presence of long-run relationship amid the variables. Thus, the study supports the presence of long-run association amid the selected variables.

Outcomes of the Fully Modified Ordinary Least Square

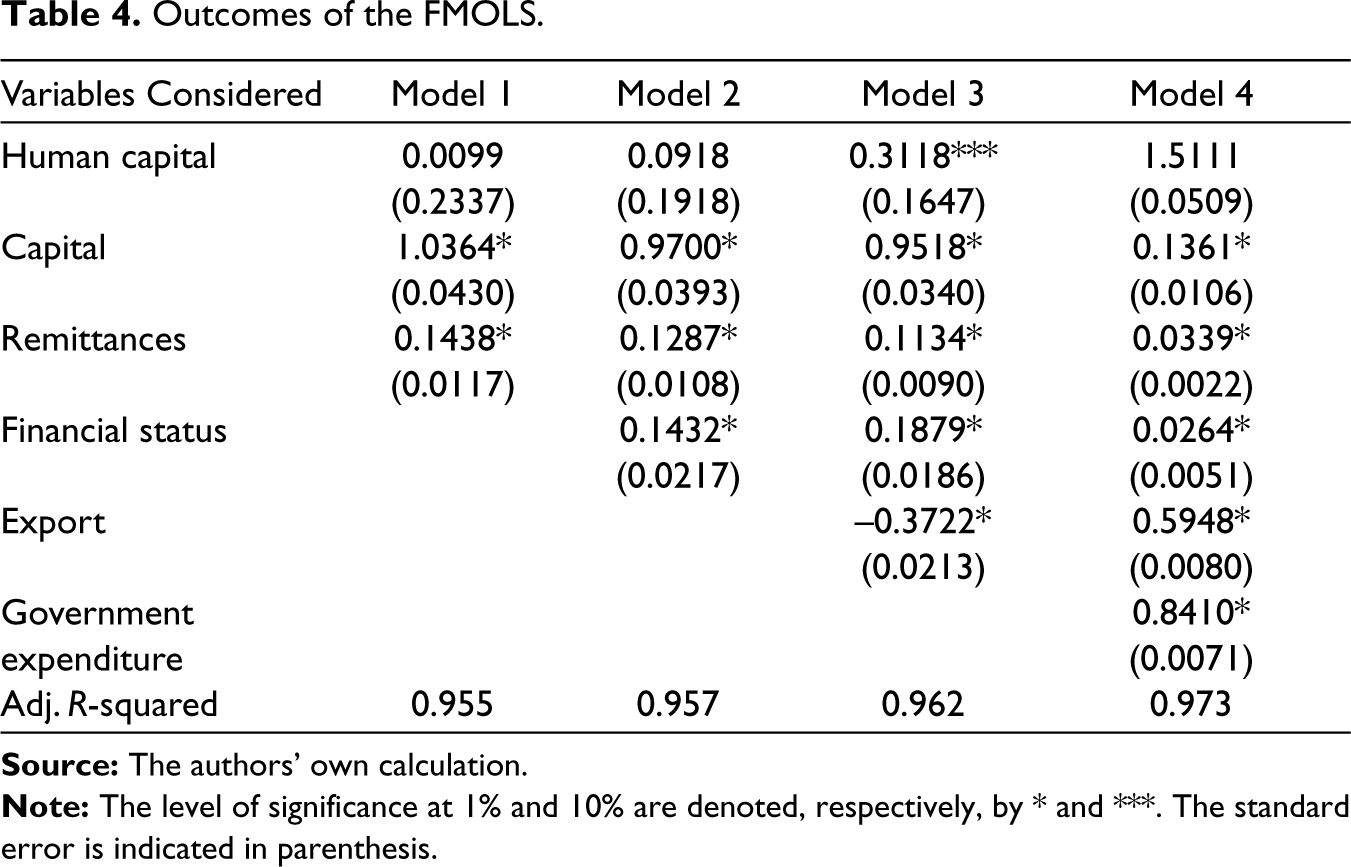

Having found a cointegrating association amid the variables, the study opted for FMOLS panel estimator with output per capita as dependent variable to measure the long-run coefficients of the explanatory variables of the models. The study reported the results of FMOLS in Table 4. Model 1 of Table 4 presents the results of the model with human capital, physical capital and remittances as independent variables. Model 2 incorporates the financial status of the selected countries into the model. Further, the study adds openness variable and is measured as the ratio of exports to GDP into the model, and is represented in Model 3. Finally, Model 4 extends the model by including the policy variable into the model. It has been observed from the results that the focus variable of the study, that is, remittances have a positive and statistically significant effect on the dependent variables in all models.

Outcomes of the Kao Cointegration Test

Outcomes of the FMOLS.

For instances, in model 1, it has been observed that a 1% rise in remittances leads to a 0.14% rise in GDP per capita. Similarly, Model 2 suggests that a 1% rise in remittances leads to a 0.12% rise in GDP per capita. The outcomes of this study supported the previous studies such as Ramirez and Sharma (2008), Faini (2007) and Fayissa and Nsiah (2010). These researchers found the existence of a direct relationship between remittances and growth. In contrast to this, the result of this study is in contradiction to the study of Chami et al. (2005). They found a negative effect of remittances on the economic growth.

In addition to remittances, the coefficients of physical capital and financial status are positive and statistically significant. A 1% point increase in physical capital increases per capita GDP by 1.03% point in model 1. Similarly, model 2 suggests that a 1% rise in physical capital leads to an increase in GDP per capita by 0.97%. Similar results have been observed in models 3 and 4. These outcomes are consistent with the study of Solow (1956) and Barro (1991). They claim that investment in physical capital has a positive and statistically significant effect on GDP per capita.

Coefficient of the human capital is significant at the 10% significance level only in model 3. Though the coefficient is positive in model 3, the coefficients of human capital in other columns are not statistically significant. According to Rogers (2008), certain specific characteristics of a nation, such as black market premium, brain drain and corruption render human capital unproductive. It is due to the fact that resources are diverted towards wasteful activities due to corruption, and human resource is diverted towards activities like rent-seeking. Due to these factors, human capital has a positive effect only in one specification of the model and that too it is at the 10% significance level.

Following remittances, the coefficient of financial status is also positive and statistically significant at the 1% significance level across all models adopted in the study. The outcomes of the study support the previous studies of Levine et al. (2000) and Beck et al. (2000).

In the case of coefficients of the openness variable, the study finds mixed results. In model 3, the coefficient of the openness variable is negative and statistically significant, whereas it has positively affected output per capita in model 4. In the main model, that is, in model 4, the coefficient of trade openness is found to be positive and statistically significant. This result is in line with the endogenous growth theory and neoclassical approach. The literature on endogenous growth theory affirms that trade openness positively affects growth due to technological dissemination between countries and economies of scale, while, according to neoclassical approach, the comparative advantage between the nations explained the positive effect of trade on growth.

The study undertaken is an effort to examine the relationship of remittances and growth, taking into account 17 selected countries from Asia. The study considered the time period spanning from 1993 to 2017. Accordingly, advanced panel data framework has been utilized to address the research problem of the study. At the initial stage, panel unit root test was used to identify whether the variables are stationary or not. Subsequently, by using cointegration test suggested by Pedroni and Kao, a marked long-run association among the variables was seen. Due to the presence of a long-run relationship found in this study, the FMOLS method has been applied to see to what extent the output per capita of Asian nations is affected by remittances and other selected explanatory variables. The results of the FMOLS estimator in all models used in the study show the importance of remittances on output per capita of Asian nations. It implies that remittance inflows in these countries are growth enhancing. The results of the study underlie the importance of remittances for these countries as one of the principal drivers of growth. Policies of the Asian countries should encourage the inflow of remittances by lowering the cost of transferring money. Driving down the cost of sending money is critical to stimulate the inflow of remittances and spurring growth.

Inflows of remittances to the Asian region are abundant and, considering the present trend of migration, it is likely to grow. To maximize the developmental effects of these inflows, developing pro-remittances in formal public and private infrastructure are a crucial policy target for governments in the region. Moreover, in addition to conventional determinants of growth such as investment in human and physical capital, trade and FDI, Asian countries can increase their growth by mobilizing the remittances. Looking at the huge amount of inflows of remittances, the governments of the receiving countries must formulate policies, which will encourage financial literacy, lead to the establishment of banks in areas that lack proper banking facilities, extend incentives to migrants to increase their savings and provide them with the infrastructure to use formal channels while remitting money, which will collectively have a major influence on economic growth.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.