Abstract

Since the Coronavirus Disease 2019 (COVID-19) outbreak, international relations (IR) literature on the pandemic’s implication on global politics has generally increased, while studies on small businesses and human developmental consequences in the developing world have lagged. In this context, through a micro-level analysis, this article investigates the extent to which the COVID-19 pandemic affects the economically bottom-class citizens and their businesses, focusing on small-scale vendors in Ghana. It utilises content analysis to examine 384 small-scale vendors in four cities/towns (Accra, Tema, Sunyani, Ho) in Ghana between August and October 2021. We show that the pandemic has negatively affected economic life and ordinary living conditions by increasing poverty among economically bottom-class citizens, likely to have dire long-term consequences nationally. Further, we contend that the small-scale vendors and entrepreneurs recognise leveraging the increasing Chinese global economic influence. Thus, China provides an exit point through which the people can navigate themselves out of the COVID-19 predicaments. Our study is novel for its first-level—individual—analysis of the impact of COVID-19 in the Ghanaian market space from an IR perspective. It also provides policy relevance.

Keywords

Introduction

In late December 2019, China informed the world of a new Coronavirus Disease 2019 (COVID-19) outbreak. Thailand confirmed the first case outside China on 13 January 2020, while Europe recorded its first case in France on 17 January 2020. Egypt recorded Africa’s first case on 14 February 2020—the same day France reported Europe’s first death. Nigeria and other countries, including Algeria, Cameroon and Morocco, followed in late February and early March 2020. By March, Europe and the USA had become the pandemic’s epicentre. The World Health Organization (WHO) officially declared a global pandemic on 11 March 2020 (Cucinotta and Vanelli 2020). Although the pandemic has affected the world economically, its impact in some places like Africa is more likely to elucidate the most disastrous consequences. Gauttam, Singh, and Kaur (2020, 320–21) note that ‘low-income countries have been critically vulnerable to the pandemic’ because ‘unlike developed countries, the developing countries have already been facing woeful inadequacy of doctors, paramedics, drugs, medical kits, and health infrastructures’.

Thus, scholars have initiated studies into the likely human security and development consequences of COVID-19 in Africa, albeit dominated by scholars in development studies and economics. Aspects of international relations (IR) is conspicuously missing. Although development studies and economics lead the discussion, they usually focus on country-level, global and macroeconomic impacts, which together are only a tiny aspect of the bigger picture of African COVID-19 analysis and need first-level and IR analysis to complement it. Thus, the purpose of this study is twofold. The first is to do a micro-level analysis focusing on small-scale vendors in Ghana to investigate the extent of the COVID-19 impact and consider how to navigate out of it. The second is to show the intersection between human development and IR regarding the COVID-19 discussion. Several questions underpin this study. To what extent the COVID-19 pandemic has personal-level economic and developmental implications for the low-income class in developing countries like Ghana? How could these low-income citizens and entrepreneurs deal with the COVID-19-related repercussions?

We employ content analysis to examine the responses of 384 small-scale vendors (traders with GH¢500–3,000 capital) in four cities/towns (Accra, Tema, Sunyani, Ho) in Ghana between August and October 2021, compiled through a structured questionnaire and unstructured interviews. The research made two critical findings. First, it found evidence to confirm that the pandemic has indeed negatively affected the economic life, personal living conditions, and development and businesses of the small-scale vendors, thereby increasing poverty levels. Second, the small-scale vendors and entrepreneurs hope to use the Chinese presence in Ghana as a leveraging resource. They bid to leverage favourable outcomes from the Chinese global presence, especially in the Ghanaian market space. Thus, China provides an exit point through which the people can navigate themselves out of the COVID-19 predicaments. This shows how a country’s (China) interplay and presence in another country (Ghana) may help the host’s citizens to deal with COVID-19-related economic repercussions.

Our work is unique because there has been little academic consideration of how IR may mitigate the impending personal and human development crisis of COVID-19, especially in Ghana. Thus, it makes a valuable addition to the body of literature on COVID-19’s impact and solution from an IR perspective. It also has a policy and practical relevance, guiding policymakers and low-income earners in dealing with the COVID-19 economic problem. The rest of the article is structured as follows: the next section reviews the literature on how IR has studied the COVID-19 issue and what we also need to consider. The third section discusses the overview of Ghana’s COVID-19 situation. In the fourth section, we show a historical link between pandemics and economic development, followed by research design and methods. We then present our findings in the sixth section. The final section offers concluding remarks.

How Has IR Studied COVID-19?

Since the pandemic, many IR discussions have fixated on world politics, particularly the interplay of the USA and China and the implication for the old debate of their power struggles for global leadership. Thus, within a short period, the COVID-19 pandemic has significantly increased scholarly articles on the pre-pandemic discussions about China’s rise and the US’ fall and the whole concept of a supposedly ongoing power shift from the USA to China and the future of world order (Allison 2017; Gilli and Gilli 2019; Yan 2018). For example, Campbell and Doshi (2020) believe that the US domestic and international failures regarding the pandemic are likely to change its global leadership position and catapult China to that position. Peckham (2020) tows a similar line, arguing that China’s ascent is possible because its response and management of COVID-19 have shown the country’s strong central authority.

From a Chinese global health diplomacy perspective, Gauttam, Singh and Kaur (2020, 319) claim that COVID-19 ‘likely will change the post-COVID geopolitical world order’ due to the exposure of the inadequacies in healthcare of countries worldwide—developing and developed countries—by COVID-19 and China’s demonstration of intent to help. They explain that although the world blames China for COVID-19 origination, it has exploited the global health emergency with health diplomacy, projecting itself as a benevolent leader and expanding its international influence and hegemonic ambition at the expense of the USA (ibid). Smith and Fallon (2020) agree, arguing that the pandemic presents China with an opportunity through its COVID-19 aid to amass meaningful friendship and build a long-lasting favourable international image.

Nevertheless, Ameyaw-Brobbey (2021a) disagrees with this assertion. He compares the US and China’s international response to the pandemic and considers how the international public is receiving both to project how they will likely shape the leadership competition. He argues that China may win some friends due to its COVID-19 aid. However, they are unlikely to substantially shape positive global public perception of China to beat the USA because of its position in the pandemic narration and the ideational attachment of the US’ diplomatic style. Other scholars argue that the pandemic might have caused more harm than good to China. They claim it has lost a chance to present its development model and credibility to the world because its blame for the origination may validate the global public’s negative opinions of China and its identity and accelerate the already existing negative trend (Ameyaw-Brobbey 2021b; Kavalski 2021).

Thus, swift COVID-19 responses domestically and the spread of aid to other countries alone may be inadequate for China to reconstruct and lead the post-COVID-19 world (Akon and Rahman 2020). Akon and Rahman (2020) believe that it faces too many unsurmountable domestic and international challenges that may become obstacles to its post-COVID-19 world order functional capabilities. Zhao (2021) believes that although the pandemic presented China with an opportunity to assume the global leadership position, it flawed it because its initial narratives were too aggressive, showing its authoritarian style as a successful alternative and democratic states as failures. It is significant to note that although these hard-line realpolitik examinations are essential, they are underpinned by significant assumptions that may or may not be the case. Again, such concentration reduces IR’s first and second levels of analysis.

What Needs to Be Studied?

By March 2020—a month after Africa recorded its first COVID-19 case—the pandemic had spread continent-wide. As of 7 January 2022, Africa’s total cases were over 7 million, with over 157,000 deaths (WHO 2022). Although Africa has the least cases and fatalities, COVID-19’s repercussions are grave there due to the continent’s pre-COVID-19 ‘disproportionate burden of poverty and disease’ (Ataguba 2020, 325; see also Anyanwu and Salami 2021). Thus, IR scholars’ concentration on hard-line realpolitik on COVID-19-related matters may neglect the human developmental needs. Like all regions, governments in Africa responded to COVID-19 with fiscal, expansionary monetary, macrofinancial policies and adjustments, and vaccine acquisitions, while financial institutions supported governments’ and African Union’s efforts to reduce personal hardships. The African Development Bank (AfDB), for example, mobilised a response package of US$230 billion between 2020 and 2021, created a COVID-19 Rapid Response Facility (CRF) of US$10 billion, and approved a US$27.33 million grant to the Africa Centres for Disease Control and Prevention (Africa CDC) (ibid, S1).

Nevertheless, the control measures, including lockdowns, quarantines, border closures and government fiscal policies, have exacted significant personal and national financial costs. COVID-19 shrank Africa’s economic growth by 2.1% in 2020 (African Development Bank [AfDB] 2021), and Southern Africa alone fell by 7.0%, Central Africa fell by −2.7%) and West Africa fell by −1.5% (Anyanwu and Salami 2021, S5–6). The fall in economic growth in 2020, increased debt, inflation (10.4%) and high food prices affected households in countries such as Ghana, Nigeria, Ethiopia and Senegal. The continent’s exchange rates also remained 5% weaker than in the pre-COVID-19 period, while the gross domestic product (GDP) per capita contracted by 10% in 2020 (AfDB 2021). The fall in economic activities and governments’ revenue increased governments’ indebtedness. The debts of governments in sub-Saharan Africa increased to 70% of GDP, and fiscal deficits doubled in 2020 (Anyanwu and Salami 2021, S7). Consequently, these have exacerbated the continent’s already worrying poverty levels and deteriorating people’s ordinary living standards. Lakner et al. (2021) estimate that sub-Saharan poverty is likely to vastly increase due to COVID-19 as about 27 million to 40 million new poor would be added. In 2020 alone, about 30 million Africans became extremely poor, while about 39 million more are expected to be pushed into extreme poverty in 2021 (AfDB 2021).

Ataguba (2020) notes that the microeconomic cost of COVID-19 in Africa is related to individuals and households because even when government and insurance schemes cover diagnosis and treatments, individuals and families may still incur other indirect costs, including transportation. COVID-19 may bring other health issues that individuals and families may cater for through out of pocket, especially in Africa, where out-of-pocket health expenditure remains exceptionally high (Ataguba 2020). Moreover, the informal sector accounts for about 89% of all employment in sub-Saharan Africa, and people’s inability to work due to COVID-19 restrictions would cause families to suffer. This would be exacerbated by the absence of appropriate contracts and worker protections (Ataguba 2020). It would be difficult to cite examples from all the countries that make up Africa or even sub-Saharan Africa in a single article. Thus, various scholars may use country-specific cases. For example, focusing on Nigeria, Ozili (2021) shows that COVID-19 affected oil demand and use, leading to a decline in its prices that caused a crisis in the Nigerian economy. COVID-19 stopped economic agents in Nigeria from economic activities due to lockdowns, social distancing policies and people’s fear and anxiety of contracting the disease. This further militated against the government’s fiscal policies and financial assistance to respond to the economic crisis. Thus, the pandemic affected borrowers’ capacity to service bank loans, weakening banks’ capacity and willingness to lend more. The decline in oil prices and economic activities also affected the national budget (Ozili 2021). Consequently, the pandemic affected the larger Nigerian population because most fall into the low-income bracket.

Although this example is from Nigeria, this scenario of how COVID-19 affected the Nigerian population is not different from others. We need to note that because scholars of development studies and economics have done most work on COVID-19’s impact in Africa, they have professed solutions from that perspective. Surprisingly, despite COVID-19’s dangers to the developing world like Africa, McKibbin and Fernando’s (2020) attempt to guide global policymakers on the macroeconomic outcomes and benefits of a globally coordinated response advised against spending and investing in public health. They ‘demonstrate the scale of costs that might be avoided by greater investment in public health systems in all economies but particularly in less developed economies where health care systems are less developed and popultion [population] density is high’ (ibid, 1). Pelizzo et al. (2021) investigated the extent COVID-19 affected Africa’s economic development and found that the pandemic has slowed down African economies, although to different degrees across the continent. Nevertheless, the continent may help itself out of the crisis by developing and focusing on agricultural food products and abundant natural resources. While it is important to utilise abundant agricultural food products and natural resources, it is necessary to stress on good governance that prioritises economic reforms, improved infrastructural base and sound social welfare programmes to mitigate future shocks.

These suggested solutions might not be wrong. However, we believe that the value of one’s living standard lies in living itself. Thus, the best judges of living conditions are the people who live the life and not what a government says they are. Therefore, we need to find solutions from the people’s perspective. In this context, small-scale vendors in Ghana evoked solutions to their COVID-19-related economic problems from an IR perspective. They professed that China’s interplay and presence might help them deal with the COVID-19-related economic impacts.

Economic Consequences of Pandemics

The link between epidemics or pandemics and economic decline is historical as scholars have recorded the negative consequences of the Justinianic plague, Black Death and, more recently, severe acute respiratory syndrome (SARS) and Ebola. Nevertheless, these studies have focused on country-level examination, and individual-level assessment is still lacking. Boroda (2008) revealed that although epidemics like smallpox and measles attacked territories in Europe such as Italy, the Roman Empire and the Mediterranean region in AD 165–180, AD 251–260, and AD 541–760, Europe, generally, did not experience any significant epidemic after the year 760 until the thirteenth century. Consequently, this, among other things, allowed Europe to experience unprecedented economic development after 760 due to prolonged periods of interrupted demographic growth and higher population density for agriculture.

Earlier, the Justinianic plague, for example, had affected the able population—the backbone of wealth creation—in England with grave economic implications (Hatcher 1977). The outbreak of the Black Death plague had catastrophic consequences on Europe because the tremendous reduction of the population, including children, affected the chances of quick demographic restoration and recovery, agriculture and the whole European economy (Boroda 2008, 51–52). In Egypt and throughout the Nile Delta, the plague’s depopulation, especially in the rural areas, left ‘no one…to gather the crops’ (Borsch 2014, 125). Thus, the Black Death affected and wholly collapsed the Egyptian economic infrastructure—anchored on an effective irrigation system (ibid). In China, Hai et al. (2004) explored the service sectors to investigate the economic impact of the SARS outbreak. They revealed significant adverse effects, estimating a decrease of 50–60% and 10% in revenue from foreign and domestic tourists, respectively, by 2003 end. Through a multiplier effect, the scholars estimated that the impact on the tourism industry would indirectly affect other service sectors. Thus, SARS was likely to course China to lose US$25.3 billion in 2003—about 2% of the country’s 2002 GDP—and likely to slow the country’s growth rate (ibid).

The Ebola outbreak in some West African countries in 2014–2016 also produced significant economic losses to the affected countries. The outbreak affected agricultural production, mining, service industry, and trade and commerce. In Guinea, Sierra Leone and Liberia, the Ebola outbreak exacerbated poverty as, in all countries, estimated poverty rates increased 2.65–22.5% between 2014 and 2016 (United Nations Development Group [UNDG] 2015, 57–58). Ebola stigmatisation, quarantine and international border restrictions reduced foreign trade and investments that affected jobs and livelihoods in neighbouring countries (ibid, 58–61). Adverse effects on agriculture and the economy directly increased food insecurity and undernourishment in the affected and neighbouring countries (ibid 2015, 61–67). This reference to different pandemic periods and specific examples gives evidence that the economic consequences of pandemics are historically rooted. Thus, the link between epidemics or pandemics and economic decline is historically recorded.

Coronavirus Disease 2019 in Ghana

Ghana recorded its first two cases on 12 March 2020—imported from Norway and Turkey (Ministry of Health 2020). Then, the country experienced a steady growth in imported cases and local transmissions. As of 9 January 2022, the country had over 148,000 cases with 1,313 deaths (WHO 2022). The government instituted measures to control the spread of the disease. Thus, on 16 March, it banned and closed all public gatherings, including churches, mosques and schools, indefinitely. It also instituted travel restrictions for all travellers arriving from countries with 200 or more COVID-19 cases within the past 14 days (Kenu, Frimpong, and Koram 2020). It tightened the border restrictions with a complete closure on 21 March 2020 (KPMG 2020a) and instituted a 14-day mandatory quarantine. Nevertheless, it lifted the air travel restriction on 1 September 2020.

As part of the detect, contain and prevent measures, the government imposed a partial lockdown on certain parts of the country—Greater Accra Metropolitan and Greater Kumasi Metropolitan Areas—starting 30 March 2020 (Ansah 2020). The lockdown was a strategic plan to effectively implement its tracing, testing and treating (3T) strategy. Thus, by mid-May 2020, Ghana had tested an estimated 161,000 people, the second highest in Africa behind South Africa (Taylor and Berger 2020). This 3T approach earned the country global admiration. The WHO, for example, took lessons from Ghana’s ‘pool testing’ technique which saves time, opening the argument that small powers may have certain qualities that global powers may need to learn (ibid). The country’s effective implementation of the 3T strategy enabled it to halt lockdown in the two major regions of Ghana after 3 weeks of its imposition (CGTN 2020).

Nevertheless, in the post-lockdown period, the government ensured social distancing, mask wearing and a ban on social gatherings. Some scholars note that the lifting of the lockdown led to a relaxation of the testing regimes the government instituted (Antwi-Boasiako et al. 2020). The government worked hard to control the spread of the virus. However, some measures have had devastating effects, especially on the informal sector, low-income earners and small enterprises. For example, ordinary Ghanaians lost their sources of livelihood, exacerbating poverty and standard of living. The government attempted to mitigate the microeconomic impact of the pandemic by introducing some relief packages. For example, it introduced a 3-month tax holiday and instituted funding programmes for businesses (Mensah and Boakye 2021, 9).

Additionally, it absorbed the water bills for all Ghanaians, offered a 50% subsidy on electricity bills for residential and commercial consumers, and complete absorption for the poorest consumers from April to 2020 ending (Nkrumah et al. 2021, 2). It introduced the Coronavirus Alleviation Plan (CAP) to cushion households and livelihoods and support micro, small and medium enterprises (MSMEs) with soft loans to reduce job losses. It also initiated a free meal distribution programme to head porters (Kayayei) (Antwi-Boasiako et al. 2020; KPMG 2020b). Despite COVID-19 hardships, the government imposed a 1% COVID-19 health recovery levy on all goods and services supplied within the country from 1 May 2021 (Ghana Revenue Authority 2021). The present nationwide conditions make it difficult to argue that the government’s relief packages were sufficient to alleviate the COVID-19-related plight of the low-income earners and small-scale enterprises in the country.

Methods

We utilised field data to investigate how the COVID-19 pandemic affects low-capital and -income entrepreneurs in Ghana and consider remedial measures from their perspectives. To do this, we surveyed four cities—Accra, Tema, Sunyani and Ho—with a structured questionnaire and unstructured interviews between August and October 2021. We selected the cities to give a broader scope of Ghanaian society. We used a mixed research technique—qualitative and limited Statistical Package for the Social Sciences (SPSS) descriptive statistics—as the grand research method. While the range of qualitative techniques helps us understand human behaviour and reaction, its combination with others ‘give us different, complementary pictures of the things we observe’ (Lune and Berg 2017, 2). We read aloud nineteen-point questions and options to randomly sampled vendors for their responses. The interaction assumed an unstructured interview with intermittent follow-up questions, and each process took approximately 15 min. We collected a total of 384 responses (127 males and 257 females). All the respondents owned businesses, and their capital ranged between GH¢500 (US$90) and GH¢3,000 (US$486).

We divided respondents’ age into intervals. The interval 41–50 recorded the highest frequency (117), and below 20 years old recorded the least (17). Vendors also recorded high dependents. About 114 vendors recorded 5–6 dependents, while 103 vendors recorded 7–8 dependents. Overall, if we consider the least number of dependents for each range and multiply by the frequencies, we talked with vendors with over 2,000 dependents. We used content analysis to examine the responses, finding patterns and themes. Content analysis is a ‘careful, detailed, systematic examination and interpretation of a particular body of material in an effort to identify patterns, themes, assumptions, and meanings’ (ibid, 182). Thus, we grouped similar opinions and titled them. Similarly, we grouped vendors’ items on sale into nine, namely clothing, footwear, home appliances, agricultural produce, etc. Miscellaneous means that the vendor sold a bit of many things together. We put the responses on SPSS version 23 for descriptive analysis. We also observed ethics by explaining the nature of the study to the respondents to assure non-responsibility and anonymity.

Small-Scale Entrepreneurs’ Predicaments Amid Coronavirus Disease 2019

Some countries in sub-Saharan Africa experienced sustained economic growth and national development that helped them achieve some poverty reduction successes (AfDB 2021; Anyanwu and Salami 2021; Arrighi 2002) before the outbreak of COVID-19. Some scholars have argued that the sustained growth and associated poverty reduction resulted from the interactions of various mutually inclusive domestic and international factors. Thus, the disappearance of any of the elements could adversely affect the poverty reduction successes (Pelizzo, Kinyondo, and Nwokora 2018). Therefore, at the onset of the COVID-19 pandemic, many predicted that Africa, especially the sub-Saharan Africa, would be the worst hit economically (Lakner et al. 2021; Mahler et al., 2020; Sumner, Hoy, and Ortiz-Juarez 2020). Indeed, in Ghana, small-scale vendors are among those low-income earners who have been adversely affected by COVID-19.

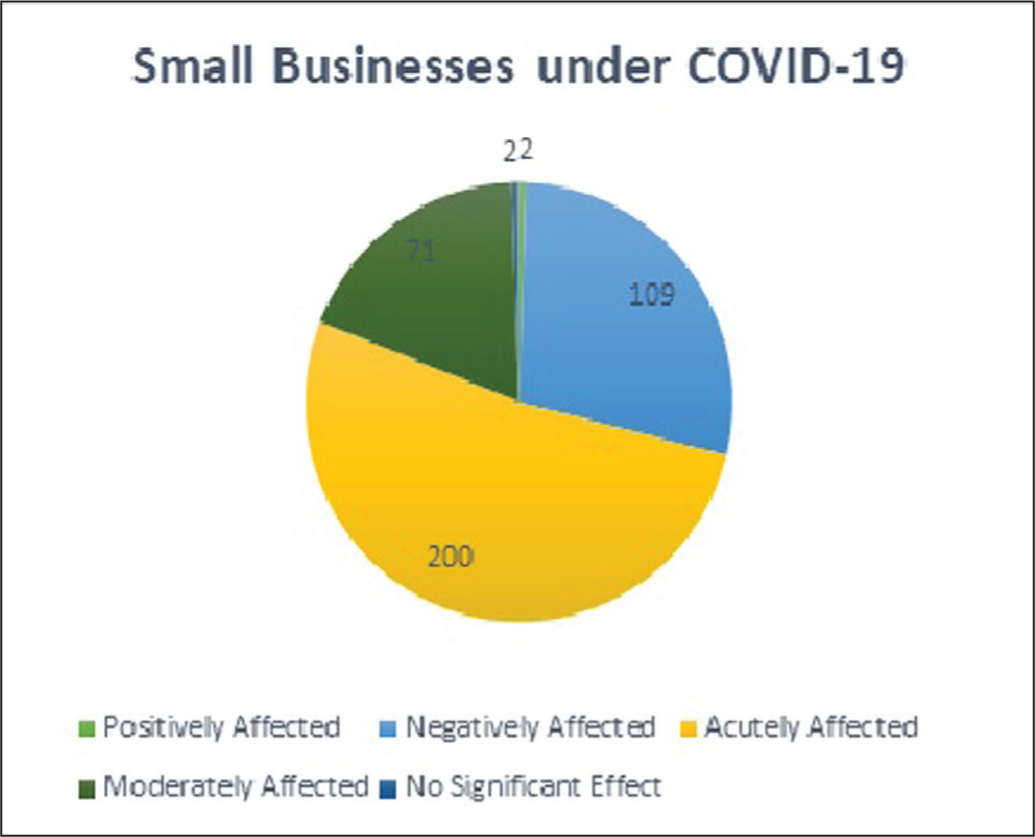

Ghana’s 2021 population census indicates that 50.3% of the total 58.1% of the labour force (15 years and older) is employed (Ghana Statistical Service [GSS] 2021, 27). Generally, economic activity among males (63.5%) is significantly higher than among females (53.0%) (ibid, 28). However, there are slightly more self-employed females (91%) than males (88.5%). The gap widens in the private informal sector ([female, 81.1% and male, 73.7%]; ibid, 130). Nationally, the private sector employs 89.7% of the labour force ([private formal is 12.6%, and private informal is 77.1%]; ibid, 130). Our survey randomly collected more female small-scale vendors (257 [66.9%]) than males (127 [33.1%]). The GSS (2021) findings that females in the private informal sector in Ghana are more than males perhaps validate the vast difference. Our results indicate that COVID-19 has indeed negatively affected Ghanaian small-scale vendors, as shown in Figure 1.

The virus’ initial secrecy, uncertainty and anxiety paved the way for many conspiracy theories and associated panic. This panic was exacerbated by the astronomical rate of death recorded in some parts of the world, especially in China, and viral videos—many of them fake—of the Chinese government’s treatment of infected persons. This anxiety, panic and government control measures like lockdowns and social distancing prevented the different economic agents (individuals, households, firms, government institutions, etc.) from engaging in economic activities. While economic agents stayed out of economic activities based on legality, some, especially individuals, feared contracting the disease by engaging in economic activities like buying items because many of the country’s foreign items come from China. The result is that the small-scale entrepreneurs, many of whom utilised the streets, were adversely affected. Indeed, the COVID-19 pandemic negatively affected different categories of economic agents, and those at the bottom of the economic ladder were mostly affected. Nevertheless, we need to state that some traders took advantage of the opportunities the pandemic brought.

Understandably, despite the enormous difficulties, two vendors through the interactions indicated a positive effect—self-discipline—because they could change aspects of their lives during the restriction period. One respondent noted that she

quickly shifted to selling masks and hand sanitisers. It was short-lived but very brisk business from the onset. Some of us who started mask and sanitiser business early, right from the time we heard of the virus outbreak in China had become big sellers at the time everyone else decided to sell them.

However, we cannot overestimate the positives of selling masks and other COVID-19-related items because it was not a sustainable business. Since the demand for such items has drastically dwindled in Ghanaian society due to the pandemic’s control, the traders have reverted to the sales of their original trade items. At the time of concluding data collection in late 2021, a few traders only supplemented their wares with a few masks and other COVID-19 prevention and control items. For example, three pieces of mask were sold for GH¢ 1 (US$0.15).

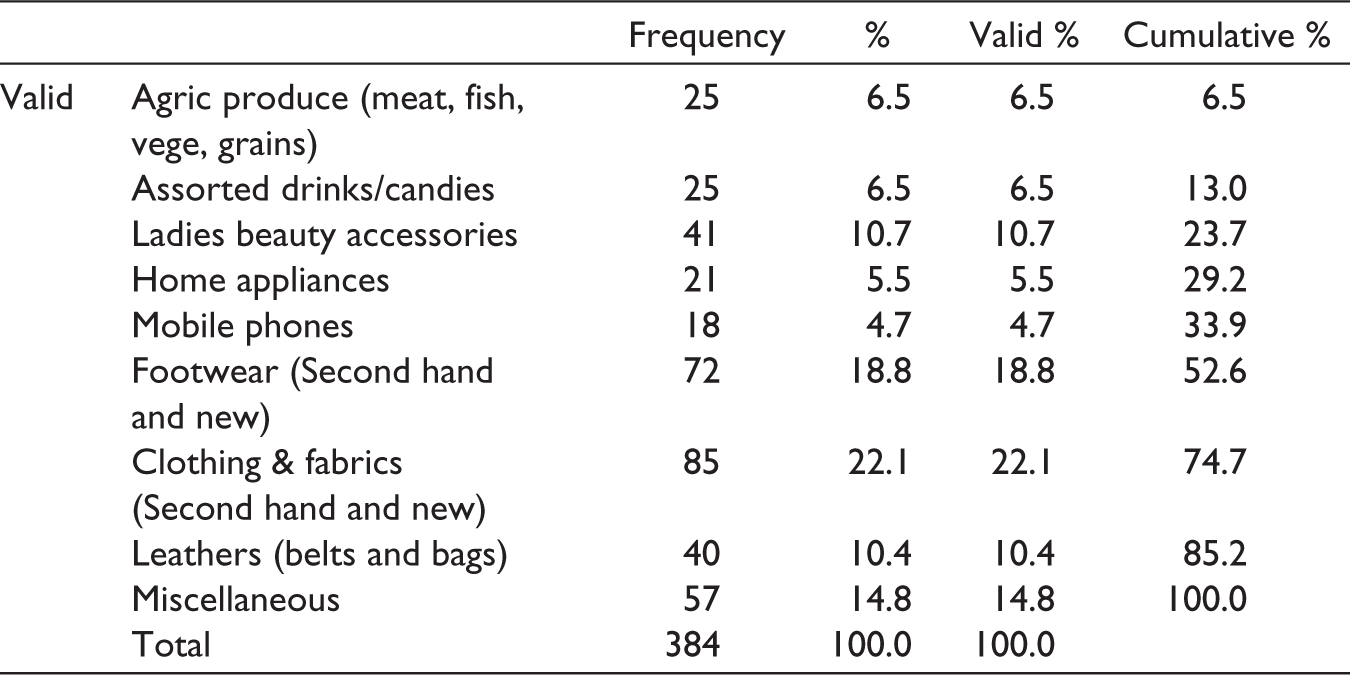

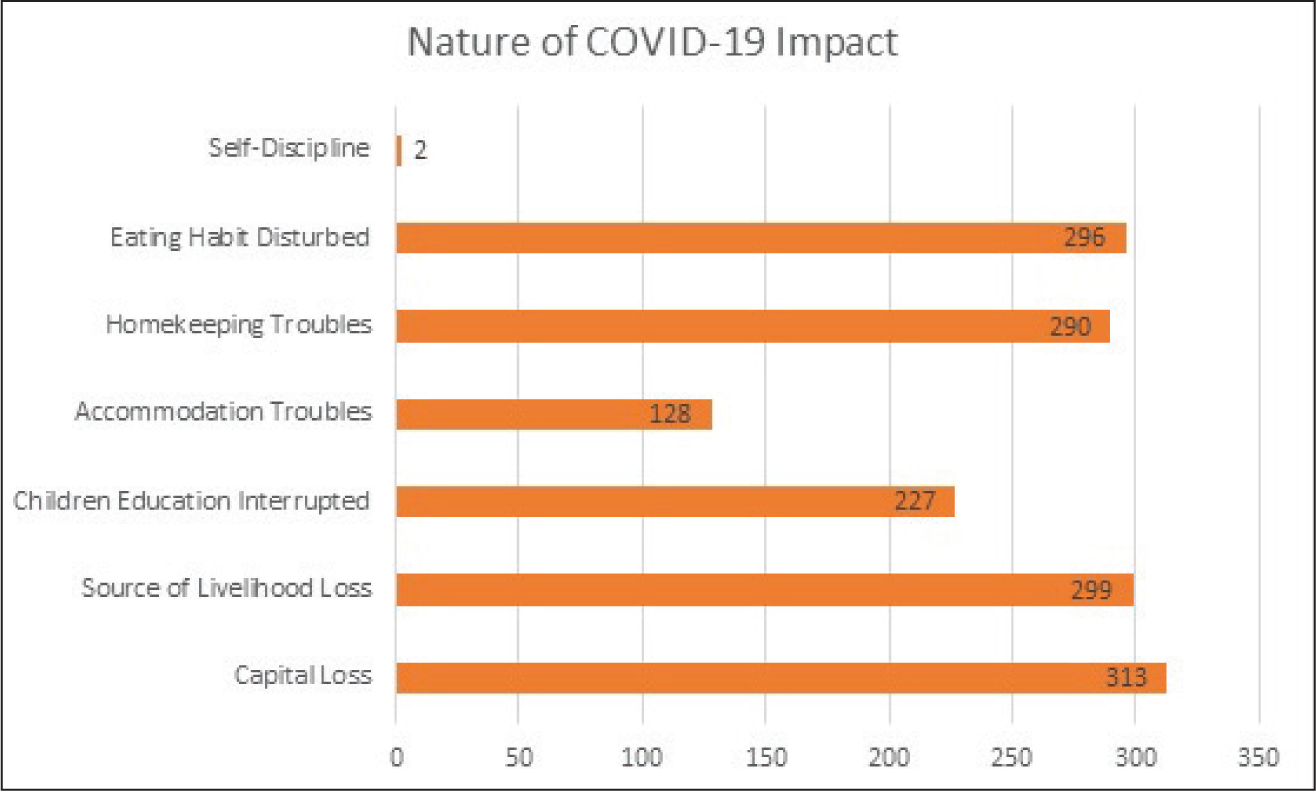

We grouped nine types of items through the content analysis, as shown in Table 1. Footwear and clothing and fabrics in second hand and brand new recorded the highest frequencies. Several vendors did not sell one particular item. Thus, we named it miscellaneous, recording the third-highest frequency. The mode of business or sales of second-hand clothing and footwear, and to some extent, the new ones—street hawking—means that such vendors were largely acutely affected during the pandemic. Generally, we observed seven predicaments that COVID-19 has brought on the small-scale vendors through our interactions and content analysis. As shown in Figure 2, they include loss of business capital, loss of livelihood, interruption in children’s education, troubles in paying accommodation rents, problems in keeping the home, distorted eating habits and self-discipline. These impacts show that COVID-19 has affected small businesses and increased owners’ poverty, thus, affecting personal living standards. The small-scale vendors are not high earners. Therefore, they are not high savers. Their money is always in circulation, retail buying and selling.

Distribution of Vendors’ Goods and Items

The daily profits are the sources of livelihood for themselves and their dependents. Thus, a short break of 2 or 3 weeks without buying and selling can elucidate negative consequences on themselves and their families. Therefore, the general theme was that business capital became household spending money. One vendor (selling agricultural produce) noted:

I had taken delivery of new stock of food items, including plantain and many other perishable food crops. Just two days after, the government announced the lockdown. Although some people made some panic buying before the lockdown, we had to eat the bulk of the rest at home because they could not be saved for long. By the time I came back here [selling location], I had spent all my money, and I needed the savings and loans agency to restart (communication with vendor, Ho, 12 October 2021).

Another seller averred a similar scenario. Her ‘location means the students are [her] main customers. When they stay at home, [she] also stays home. When they stay too long when it is not a regular vacation that [she] had planned for, [her] business gets affected’ (communication with a vendor, Tema, 29 August 2021).

The pandemic’s direct effect on small businesses has extended beyond the lockdown periods. It has increased individual poverty and worsened living standards. The loss of families’ daily income prompted some vendors to readjust families’ daily food consumption and general housekeeping standards. This even affected family cohesion and happiness in some situations. Although they are low-income earners, we found that our respondents have larger dependent sizes through a cross-tabulation of age and vendors’ dependents. About 114 vendors had 5–6 dependents, while 103 had 7–8 dependents. It reflects the GSS (2021) findings of Ghana’s higher average household size (four). Consequently, the negative effect of COVID-19 on the 384 vendors goes further to affect an estimated 2,000 other people. A second-hand clothing vendor noted the negative impact on his son’s education even after an ease in restrictions:

We planned towards his [pointing to his son] level 100 [university entrance], and the virus unexpectedly came. He is heartbroken, and his demeanour has changed since we resumed work because we could not save enough, and we [family] have also used the little we kept. So, he thinks he might not be able to go to school when the next academic year begins. In fact, where the virus came from and whoever brought it has inflicted the most incredible pain (communication with a clothing seller, Accra, 17 August 2021).

An Exit Route: China as a Leveraging Resource

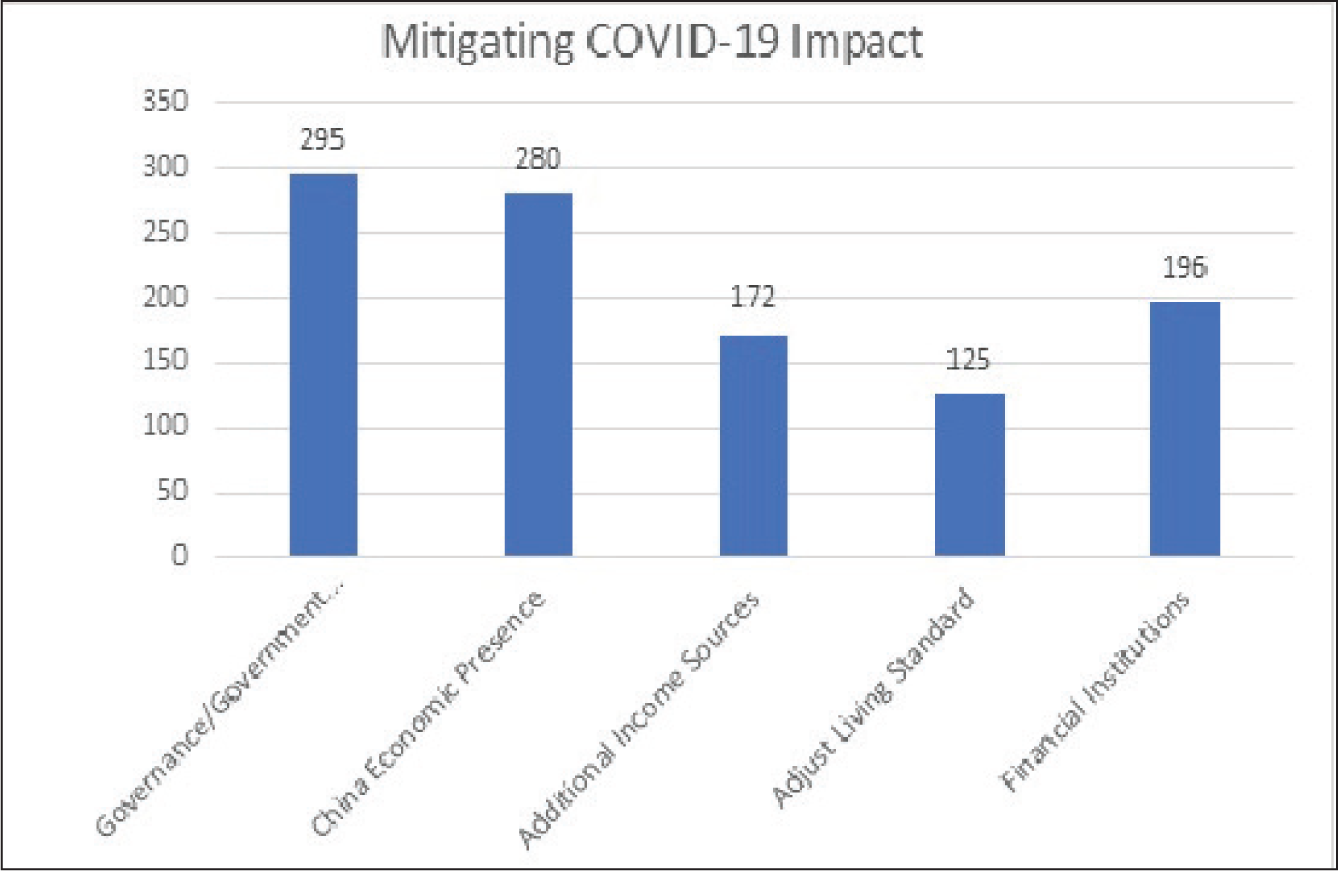

All governments—including authoritarians—present economic situational reports with regime security in mind, either thinking about the next election or the public reaction. Thus, some of their reports and solutions may not reflect the reality of living in some cases. Since the value of people’s living standards lies in their living, they are the best judges and best placed to suggest some solutions to their predicaments. Through our survey, we identified five mitigating factors—effective government and governance, China’s economic presence, finding sources of additional income, adjusting living standards in the short term and seeking help from financial institutions like savings and loan agencies and banks. Each vendor opined at least one. We present this in Figure 3. In most countries—developed and developing—it is not uncommon for the public to place their fate in the government as the focal source of alleviating hardship. Thus, it is not an aberration for the public to stage demands on the government. Therefore, it is not surprising that in our survey, we counted more vendors who believe that sound government policies devoid of corruption would help them back in business. One vendor (ladies’ beauty accessories) believes that ‘the government knows what they can do, but it is not in their interest to do because that reduces the amount of money that goes into their private accounts’ (communication with vendor, Accra, 8 October 2021).

However surprising is the number of vendors who noted China’s role in the local economy in different ways. We concentrate on the China factor in this work as we believe it has more research significance than the obvious public reliance on the government. As many as 280 vendors hope to use the Chinese presence in Ghana as a leveraging resource because China provides available and affordable goods that one can start up and build on with little capital. During our interaction, a mobile phone vendor in Tema (20 October 2021) noted that ‘there is no money nowadays due to the sudden outbreak of the disease. But we can restart, thanks to China. We have phones for every pocket [income status], and buyers have been coming. If the virus does not increase again, we shall overcome’.

There is no doubt that China has become a central figure in Ghana’s and, by extension, Africa’s economic developments (Brautigam et al. 2017; Marfaing and Thiel 2013). This economic engagement was the product of Jiang Zemin’s ‘going out’ initiative encouraged in the 1990s and became an official government policy in the early 2000s. In simple terms, the Chinese government encouraged Chinese firms and entrepreneurs to invest in international markets and establish their presence internationally to acquire international skills and experience (Shambaugh 2013). Shambaugh (2013, 138–39) writes that the Chinese government motivated its local companies and businesses to ‘form large internationally competitive companies and enterprise groups through market forces and policy guidance’ to ‘take advantage of both markets’ and ‘increase export of goods and labor services and bring about a number of strong multinational enterprises and brand names’. Today, the going out policy has become successful mainly due to China’s economic success propelled by its economic model, the ‘Beijing Consensus’ (Ramo 2004). Under the model, China used market liberalisation to strengthen local firms, actively pursued foreign direct investment (FDI) that granted foreign companies a significant role in its economic growth and, finally, mobilised capital through the stock market (Cho and Jeong 2008, 464).

Due to the Chinese government’s desire for firms to go international, it has significantly relaxed and streamlined administrative controls and approval processes. Although China motivates its firms to go abroad, Chinese outward FDI is regarded as state-owned because the government takes a significant role in firms’ investment processes (Buckley et al. 2007, 500). Most importantly, the government controls important companies that dominate their industries like Sinopec (energy) and the Export–Import Bank of China (Exim Bank) (economic and finance sector). In this regard, it appoints the directors of these critical companies who become members of the Communist Party. This allows the government to direct companies to priority areas and influence them to help achieve foreign objectives through direct instructions regarding investment and lending (Kurlantzick 2013). The link between the government and Chinese firms operating abroad also helps the government to support Chinese firms to win international competitive tenders.

However, this does not mean that the Chinese government controls every private Chinese-owned firm or business operating internationally. Several individuals venture into the international market to do their small-scale businesses without the knowledge of the Chinese government or who may not even be in the books of the Chinese embassy in the host country until some issues or problems emerge. Nevertheless, all the Chinese firms and businesses—small-scale firms without Chinese government’s knowledge or big-scale firms with Chinese government control—contribute significantly to improving the living standards of people in their host countries. Since the early 2000s, China has attempted to improve its public diplomacy in Africa through economic payments and manufactured products, scholarship schemes and media interactions (Jiang et al. 2016).

Traditionally, public diplomacy has focused on state-directed strategies governments use to communicate with the public outside their geographical boundaries to attract them to their values and policies. However, in this work, we see the concept from its new perspective (see Seib 2009), where government and non-state actors such as private individuals, groups, private and multinational corporations, and firms aid their home country to communicate with the host public. Academic debates exist as to whether China has achieved any success in this regard (e.g., see Benabdallah 2017; Liang 2012). According to Ramo (2004), China’s development model has given hope to political elites and the general public of developing countries who have particularly suffered from poverty and economic backwardness under the Washington Consensus. The latter has over the years applied Western neoliberal economic principles heavily characterised by structural adjustment programmes without considering the requirements and developing countries’ specific characteristics. Thus, Ghanaian small-scale vendors’ recognition of China as a leveraging resource goes a long way to credit China’s international image-building effort as well as corroborates Ramo’s assertion.

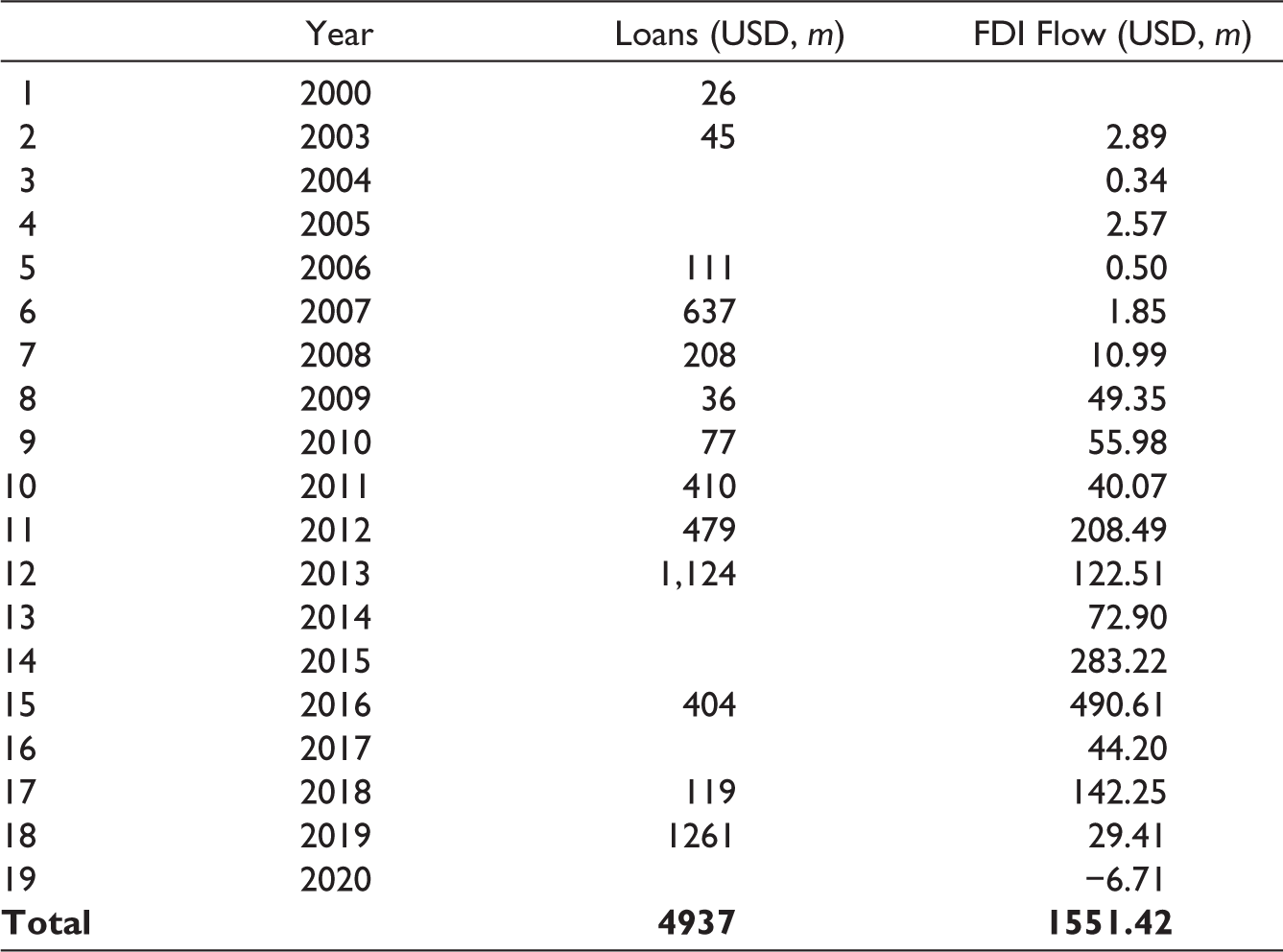

Chinese economic engagement in the Ghanaian economy, like most of Africa, is highly noticeable from both observational positions and official information and statistics. From observation, it is not difficult to find Chinese-made products ranging from clothing and shoes, simple machines, household items, food, office accessories to electronics and electrical appliances in almost every shop in the market space. Although our efforts to access the number of Chinese firms and businesses registered in the Ghanaian economy and the sectors under which they do business from the Ghana Investment and Promotion Centre (GIPC) proved futile, we were able to utilise available official data from the China–Africa Research Initiative (CARI) and Boston University Global Development Policy Center (BUGDPC) on Chinese loans to Ghana and Chinese outward FDI flow into the Ghanaian economy between 2000 and 2020 to measure the prevalence of Chinese engagement in the Ghanaian economy. We present this in Table 2.

Chinese Engagement in the Ghanaian Economy

The CARI and BUGDPC’s data sources included government documents such as the China statistical yearbooks, Statistical Bulletin of China’s outward foreign direct investment published by China’s MOFCOM, contractor websites, fieldworks, interviews, and media sources (CARI and BUGDPC 2021). We estimated about US$4.9 billion Chinese loan commitments to Ghana and about US$1.6 billion FDI flow into the country between 2000 and 2020. Although loans are significantly higher than Chinese investments, we cannot deny that governments acquire loans to improve various sectors of the local economy such as energy and power, health, defence, agriculture, transportation, water and sanitation, among others. When these loans are properly supervised and utilised, the improvement of these sectors improves the country, aids private businesses and promotes economic opportunities, as well as the general living standards of the public.

In the Ghanaian case, these loans went into projects, including the Lake Volta settlement and township electrification, the Bui hydropower project, coasting fishing landing site, building and rehabilitation of Accra–Kumasi road and the Ofankor–Nsawam section, upgrading polytechnics, vocational and technical training centres, Upper West and Northern region rural electrification, purchase of Yaxing buses, Cape Coast Kotokuraba market rehabilitation and Kpong Water Supply project, among others (ibid). By saying this, we do not imply that the Ghanaian government properly utilises Chinese loans, devoid of corruption and embezzlement that characterise African governments, especially when Chinese loans are criticised to be too flexible, unsupervised, with no strings attached, breeding corruption and empowering political leaders against the people. Indeed, Chinese loans are part of its high-politics diplomacy and may not directly affect Ghanaians’ lives. Undoubtedly, however, one does well when their countries do well. Thus, an improved economy and infrastructure would likely aid small-scale businesses.

Chinese FDI flows to Ghana have continuously increased since 2003. However, it declined in 2020 obviously due to the COVID-19 pandemic. We need to note that although official sources are necessary to elaborate on the prevalence of Chinese engagement in the Ghanaian economy, in some cases, they do not tell us much if we cannot reconcile the data from official Chinese documents with the actual investment projects in the host country. Importantly, there are usually large gaps between planned—intended and discussed or even initial agreements that are released to the media—and realised—actual projects that are implemented on the ground—investments (Brautigam et al. 2017). This situation, on the one hand, creates a condition to overestimate Chinese actual investments in most of Africa, including Ghana. That is, although Chinese investments significantly contribute to growth and development through job creation and sources of livelihood, they are less extensive than we often assume. Even when investments are approved investments, not all approved investments often come to fruition. Thus, we need to be careful when drawing conclusions about Chinese investments in Africa.

On the other hand, the numbers may also be understated because they do not capture Chinese money parked in offshore financial centres as well as privately owned smaller investors whose existence the Chinese embassy in the host country may not even be aware of. For example, comparing data on several actual Chinese FDI projects in six African countries with the Chinese Ministry of Commerce data, Shen (2015) found that projects in the host countries were at least 2.5 times more than the number recorded by the Chinese government. Statistically, Chinese investment plummeted in 2020, but it does nothing to the reliance of small-scale vendors and the general Ghanaian population on Chinese products and had no effect on Chinese engagement in the Ghanaian economy in the post-pandemic era. Although we do not have investment data for 2021–2022 at the time of manuscript preparation, the pre-COVID-19 era investments in Table 2, traders’ observations and experiences in the market space give enough reason for the small-scale vendors’ optimism about using the Chinese presence in Ghana as a leveraging resource.

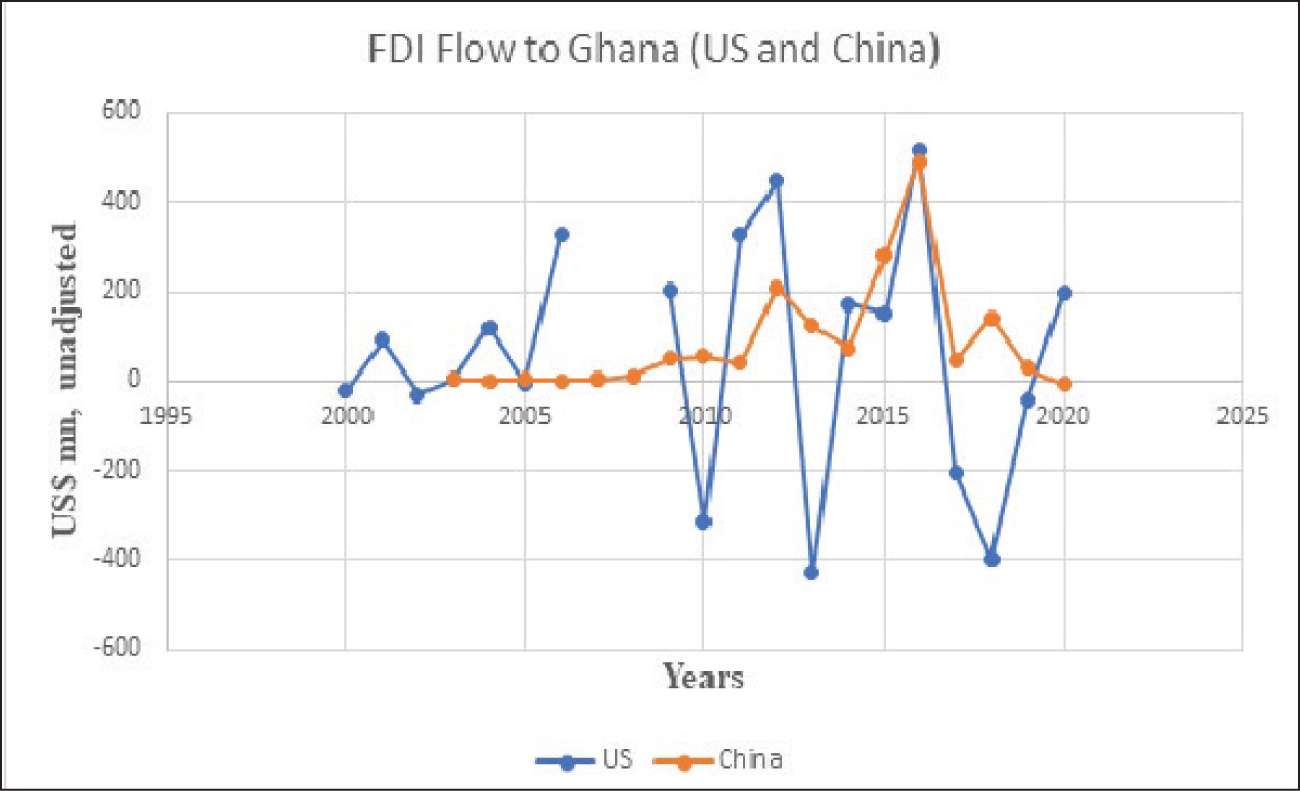

An analysis of China’s role in mitigating the consequences of the COVID-19 pandemic might engender an assumption that China is either the sole investor or the largest source of FDI flow into Ghana in terms of value. It is not. Quarterly reports of several different years of the GIPC indicate that several countries, including the UK, Netherlands, the USA, India, Switzerland and France on different occasions surpassed China’s investment in FDI value. Nevertheless, China has consistently maintained the top position in terms of the number of projects. Due to the US–China international political, economic and leadership competition, we compare the USA and China’s investment trends in Ghana, as presented in Figure 4. As we show in Figure 4, Chinese FDI flows to Ghana have exceeded those from the USA since 2013 except in 2020. Thus, apart from the visible nature of Chinese products in the Ghanaian market by mere observation, statistical data also show China surpassing major investor giants such as the USA, reinforcing why Ghanaian small-scale vendors hope to use China as a leveraging resource.

Chinese presence in Ghana has influenced people’s taste because a significant number rely on China for access to consumer and non-consumer products, including food, clothing and textiles, technological and electrical devices. Chinese manufactured products in Ghana are spearheaded by high-capital Ghanaian businessmen who travel to China or import with online platforms and Chinese traders who set up large wholesale stores. Some of these traders came into the country purposely for business. Others came as part of a state-sponsored or multibillion private or joint construction firm and took to trading instead of going back home after the expiration of their contracts (Marfaing and Thiel 2013). In some cases, Ghanaian students and others seeking greener pastures in China could take advantage of their presence in China to import a few Chinese products into Ghana, albeit their contribution is small. All these groups make sure that even if official Chinese FDI flow to Ghana decreased, its impact in terms of Chinese products in the Ghanaian market space is hardly felt. Although Chinese products are usually accused of their cheap and substandard nature, small-scale Ghanaian vendors highly believe that such products hold the key to freeing them from the predicaments the pandemic brought. In this regard, their inclination to Chinese products in the pre-pandemic era is not different from the post-pandemic period. A footwear vendor even equated the Chinese presence to divinity:

By the grace of the Chinese, we (traders with low capital) can equally do business and at least get what we also deserve. Sometimes I come here with an empty pocket in the morning, but I will get what my children and I will eat by the close of the day. We would have been miserable without the Chinese products, especially after the virus, because we cannot buy and sell American and European items. Those are expensive, and only rich people can buy them (communication with vendor, Accra, 20 August 2021).

The vendor’s assertion perhaps confirms Obeng’s (2018) argument that Chinese traders and products enjoy support within the Ghanaian market. Thus, Ghanaian traders do not necessarily want their removal from the market, albeit some may be dissatisfied with some Chinese traders’ practices. The Chinese economic presence enables the small-scale vendors to bypass the restricted economic networks that hitherto excluded them from accessing the market space (Marfaing and Thiel 2013; Obeng 2018). Nevertheless, we need to clarify that the perception that expensive products have quality and usually from the USA or Europe is not entirely the case. However, the Chinese products present varying quality and pricing levels that allow all buyers to access their needs and small-scale traders with low capital access stock for sale. It is important to note that there are significant numbers of expensive shops with so-called quality products, whose origins are in China. To attract affluent buyers, owners of such shops may claim that their wares are from the USA or Europe. Thus, many Ghanaians may prefer affordable Chinese products due to unemployment, low-income levels and poverty, making the small-scale vendors stay in business.

Conclusion

This article has shown that COVID-19 has harmed small-scale businesses and owners in Ghana. However, the business owners see an exit route in the Chinese economic presence in the Ghanaian market space. We do not generalise our findings that may be peculiar to Ghana. However, we suggest that due to the significant Chinese presence in most African countries and the political and economic similarities of most African countries, our findings may shed light on the more extensive African cases, enabling projections and further research on the topic. Our work may serve as a starting point to discuss COVID-19 economic impact in Ghana and, to an extent, Africa from a perspective outside development studies and economics.

From an IR perspective, this contribution adds to China–Africa public diplomacy. Specifically, we see that China’s public diplomacy through economic interactions yields some successes, at least in Ghana. However, another debate is whether the likeness for the Chinese products is establishing ideational attachment to last in the longer term or surpass US or Europe’s attractiveness. However, we admit that more comprehensive data that include at least half of the country’s geographical regions could have given a much clearer picture. A gap that further studies may fill.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Data Accessibility Statement

The data are readily available upon request from the corresponding author.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.