Abstract

This article examines India’s challenges in a rather underexplored dimension—the information and communications technology (ICT) sector. This article deals with a key question: What impedes India’s prospects in the world’s ICT sector? The article identifies China’s strategic footprints in India’s ICT sector as the primary challenge and provides a deeper analysis of it. The article relies on quantitative data concerning the four key sub-sectors—e-commerce, consumer electronics, semiconductors and the telecom sector—to critically examine the strategic footprints of Chinese ICT in India’s ICT sector. The article further examines India’s evolving policy landscape in response to growing challenges. It concerns the recent debates in the tech policy circles and explores the scope of ‘technology decoupling’ from China. The article argues that India should see the concept of decoupling as distinct from US–China decoupling. Rather than decoupling, diversification away from China in a phased manner is found to be critical to secure India’s future in the evolving technological landscape.

This is a moment of choice and opportunity. It could be the best 10 years ahead of us that we have ever had in human history or one of the worst because we have more power than we have ever had before.—Erik Brynjolfsson

Introduction

In the history of humanity, two pivotal factors that contributed to reshaping the global world order are (a) geography and resources such as food, topography, water, energy and minerals) and (b) technology (nuclear, missiles, etc.). In the rapidly growing environment characterised by the fourth industrial revolution, technological advancements are becoming a key to preponderant economic growth, national power (strategic advantages over competitors), and the ability to reshape the world order by attaining technological supremacy.

Experts have noted that today nations stand at the cusp of colossal changes wherein technological advancements are the most decisive factors enabling a nation’s capability to project power. Russian President Vladimir Putin also arguably pointed out that ‘Whoever leads in artificial intelligence in 2030 will rule the world’ (Gill, 2020). Concerning the changing world order and highlighting the next battleground, Bob Murray writes

the race is one of technological adoption—that is, the acceptance, integration, and use of new technology in society. From artificial intelligence to quantum and everything in between, governments are in a race to leverage these technologies at scale and speed—the first adopter advantage for emerging disruptive tech could not be more prevalent in the world of geopolitics and deterrence. (Murray, 2020)

Consequently, the securitisation and weaponisation of emerging technologies such as artificial intelligence (AI), big data, telecom and semiconductors have come from fiction to reality. Intense competition for technological supremacy and influence has encapsulated the domain of conflict between major powers. Let us consider a buzzword in today’s world, AI technologies. Reacting to the defeat of a Go Champion by an AI system, Chinese President Xi Jinping asserted that China has to lead in this technology. With its 2017 Artificial Intelligence Development Plan, China is preparing itself to develop the most sophisticated AI infrastructure in the world by 2030. Scholars also argue that China’s AI development lies central to its military–civil fusion strategy that ultimately aims to drive China’s military modernisation (Kania, 2019). Interestingly, China filed 2.5 times more patents in AI technologies than the United States in 2018. According to estimates, China also produces 10 times more graduates than the US universities specialising in AI research. With the fear of losing this race, the Trump administration rushed to pass an executive order in 2019 that established the American AI initiative. The successive Biden administration played more systematically to hit where China is most vulnerable, that is, the semiconductor supply chain, raising the standards from a great power competition to a potential sign of an evolving rivalry over chokepoint technologies. The ongoing technology war between the United States and China demonstrates that technology lies at the centre of the nation’s security measures, domestic policymaking, as well as alliance politics.

One of the most vital facets of this technology war is technological ‘decoupling’ and ‘technology bifurcation’—a trend that disintegrates the innovation systems of two states. Countries such as India stand at a crucial juncture wherein the ongoing stifle can prove to be a moment of opportunity. In an attempt to diversify the global ICT value chains, countries such as India are seen as a potential alternative to China. India’s recent industrial policies, such as Made in India, Start-up India, Atma Nirbhar Abhiyan (Self-reliance Mission) and Performance-Linked Incentive (PLI) Scheme, are also aimed at deviating the global supply chain towards its manufacturing potential. However, the question that lingers is how prepared is India for a new technological era. Considering an improved policy environment and cheap factors of production, it is understood that India has great avenues to offer, but is India itself subjected to technological dominance?

At the cusp of these debates, this article deals with a key research question: To what extent China impedes India’s prospects in the ICT sector? To critically examine this dimension, the article addresses three objectives: (a) to understand the strategic depth of China’s ICT products and services in India’s ICT market, (b) to understand and assess the changing course of India’s technology policy landscape and (c) to critically understand India’s major challenges and prospects in the ICT sector, by especially analysing the question of decoupling from China. This article limits itself to understanding the presence of China’s ICT in the four key sub-sectors: e-commerce, consumer electronics, semiconductors and the telecom sector. A mixed-method approach has been adopted utilising both quantitative and qualitative approaches to arrive at a systematic understanding. The article relies on quantitative data regarding the ICT exchanges between India and China (also India and other countries) sourced from Indian government websites, news articles, individual web searches and so on.

Understanding the Chinese Footprints in India

China’s presence in India’s ICT is studied under the following four sub-sectors:

E-commerce and Internet-based Platform Services

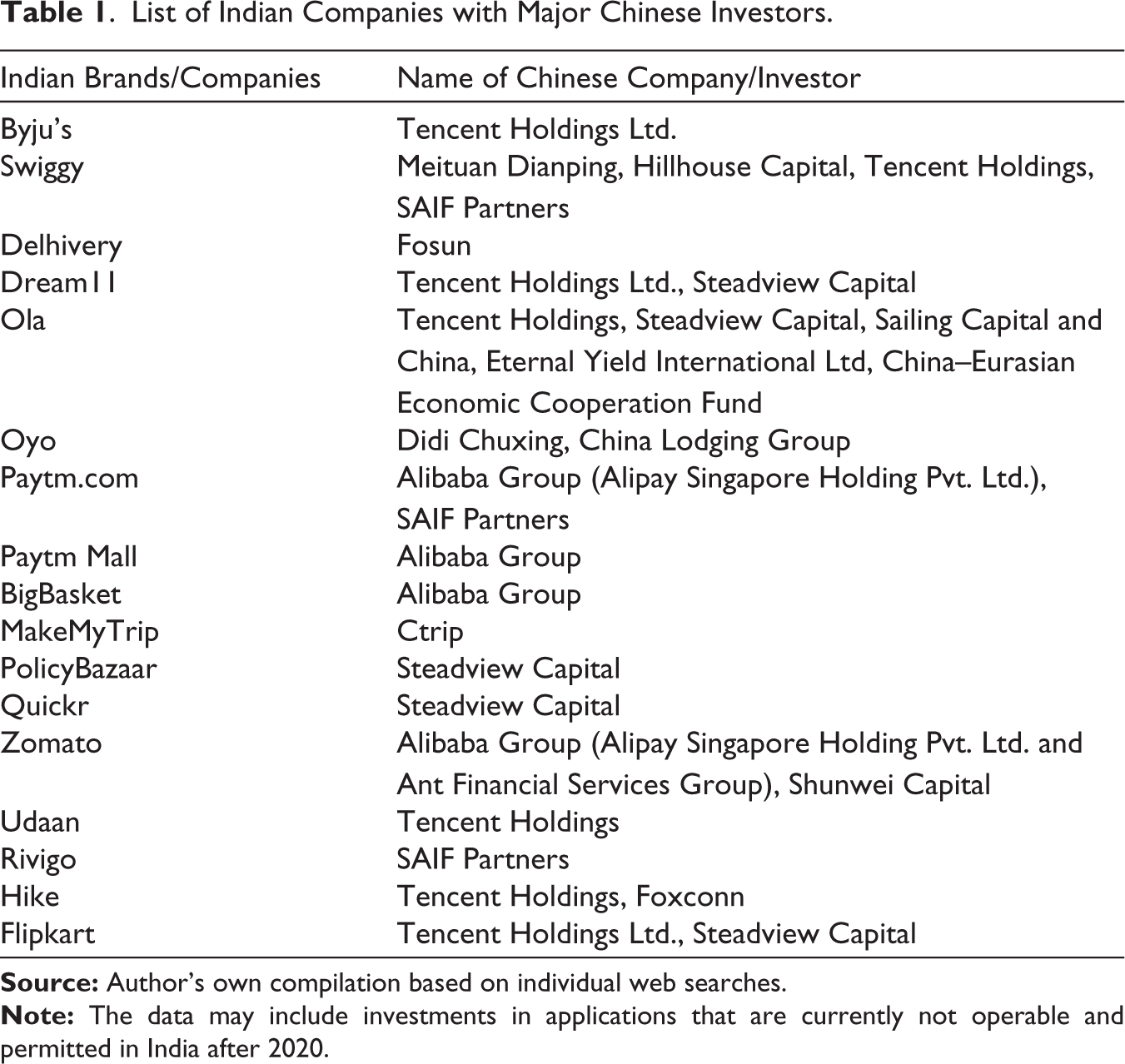

During the last decade, Chinese investors have come to dominate in significant stakes of India’s ICT companies. China’s outward foreign direct investment (FDI) rose from $107.84 billion in 2013 to $146.5 billion in 2022 (Ministry of Commerce of the People’s Republic of China, 2013, 2022). Around two dozen Chinese tech companies have acquired Indian start-ups in recent years (see Table 1). Chinese corporate trio of Baidu, Alibaba and Tencent only have funded 92 unicorn firms including Ola, Oyo, Byju’s, Paytm, etc. In 18 out of India’s top 30 unicorns, Chinese investors have now secured major stakes (Bhandari et al., 2020). China has invested a total sum of around $4 billion in the tech start-up sector in India (Bhandari et al., 2020).

List of Indian Companies with Major Chinese Investors.

Not only limited to products and services owned by Chinese companies, Chinese investors also control the widely used foreign apps in India. China, being unable to lure India towards its Belt and Road Initiative (BRI), seems to have successfully made inroads into Indian markets through its virtual BRI, that is, venture capital investments, and penetrated its cheaper products into Indian markets. Before the 2020 app ban, Alibaba’s UC Browser constituted a 50% share of the browser market share in India. Similarly, TikTok became the most popular short-video-streaming platform in India with the highest number of downloads.

The nature of Chinese investments in India differs significantly from that in other countries. While investments elsewhere primarily focus on physical infrastructure, in India, they predominantly flow through venture capital funds into Indian companies and foreign-owned companies based in India (see Figure 1).

Consumer Electronics

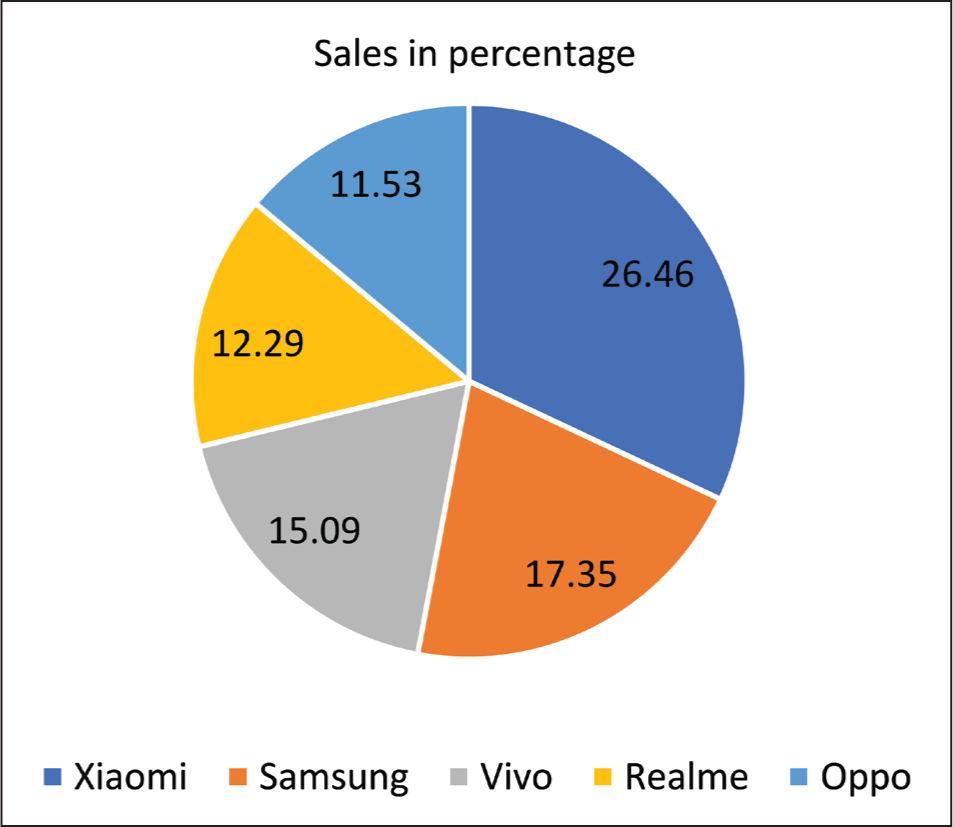

Chinese exports to India have tripled in the last two decades. While India’s exports to China have decreased, India’s imports have surged from 5% in 2000 to 15% in 2020 (Nihalani, 2023). Electronic items rank as the third most-valued category of import items for India. India’s import bill for this category has recorded a compound annual growth rate of 18.3% over the past 15 years, surpassing the import bill of petroleum products and gold (ICICI Securities, 2015). These items include consumer electronic devices such as mobile phones, batteries, modems, mice, keyboards, memory cards, USB flash disks, CPUs, ACs, LCD devices and power banks; hardware components such as switchboards, tube lights, etc., and electronic manufacturing parts such as machine tools, auto components, etc., used in manufacturing processes (Volza, 2023). According to data from the Ministry of Commerce and Industry, the import of electronic goods from China to India was worth US$58.42 billion in the fiscal year 2020–2021, up from US$57.39 billion in the fiscal year 2019–2020 (Ministry of Commerce and Industry, Government of India). The import–export disparity between China and India is particularly pronounced in the electronics segment, with approximately 40% of India’s import of electrical machinery and equipment coming from China (Minhas, 2022). In 2021, out of nearly $5 billion worth of laptops imported by India, $4.35 billion originated from China (Rampal, 2022). Table 2 further exhibits the comparative share of the Chinese and global market in the Indian smartphone market.

The Sale of Chinese and Other Global Brands in the Indian Smartphone Market.

According to Counterpoint Research, a Hong Kong–based research analysis firm, the Chinese smartphone market share has increased 10-fold in the last decade, amidst intense competition from foreign and homegrown brands that were present in India before Chinese brands dominated Indian markets. Currently, four out of the top five smartphone brands in India are of Chinese origin (see Figure 2).

Semiconductor Sector

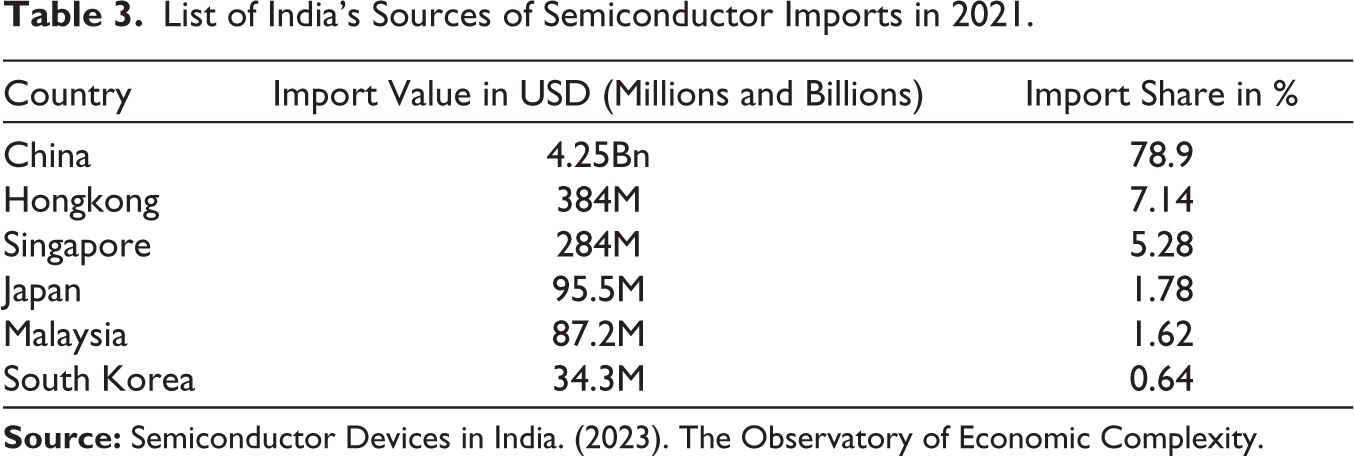

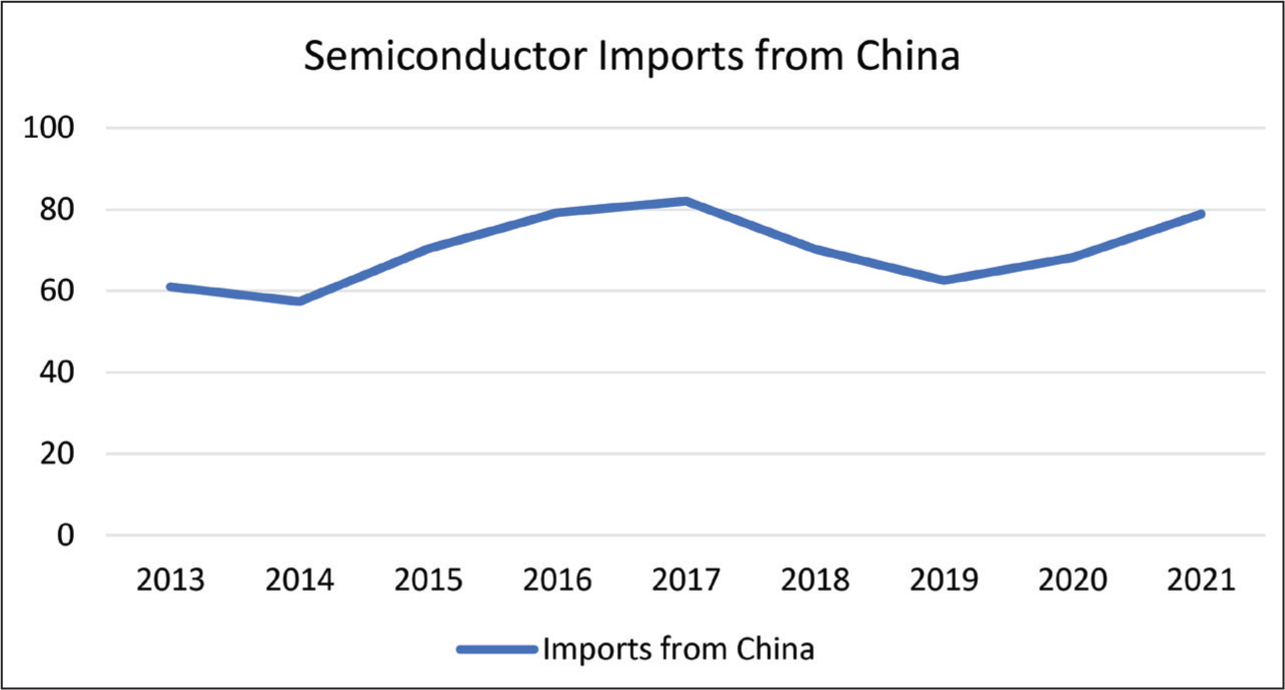

Semiconductor chips, also known as microchips, are essential technical components serving as the backbone for the functionality of various electronic and mechanical devices, ranging from smartphones to cars. The intricacy of the global supply chain is where the semiconductor industry’s beauty lies. Within this chain, semiconductor firms rely on each other for the design, manufacturing, fabrication, assembly, testing and packaging (ATP) of microchips. Key players in the global semiconductor supply chain include the United States, Taiwan, China, South Korea, the Netherlands, Singapore and Malaysia. Currently, India lacks significant capabilities in any segment of this supply chain, thus not being a part of the geopolitically crucial network. Instead, India heavily depends on importing chips from China to meet the manufacturing needs of various electronic items. As the world’s second-largest importer of semiconductor chips, India sources a significant portion from China. In 2021, India imported 78.9% of its semiconductors from China, amounting to US$25.94 billion (Observatory of Economic Complexity, 2023). In terms of several devices, Table 3 shows the sources of India’s semiconductor imports in 2021.

List of India’s Sources of Semiconductor Imports in 2021.

Also, China, a dominant source of India’s semiconductor requirements, has been on the rise in semiconductor imports since 2013 except for a slight dip between 2018 and 2019 (see Figure 3).

Concerns arise for India due to recent disruptions in China’s semiconductor industry, stemming from the US’s October 2022 export control measures (Lis et al., 2022). With China’s chip business facing challenges from other advanced manufacturers such as the Netherlands, South Korea and Taiwan due to US–China tensions, India’s reliance on Chinese chips becomes even more concerning.

Wireless and Telecommunications Services

Wireless and telecommunication services encompass the means of communication through mobile phones, the internet and popular spectrums like 4G and 5G services. India’s telecom landscape involves both state-owned companies such as Bharat Sanchar Nigam Limited (BSNL), Mahanagar Telephone Nigam Limited and private operators such as Bharti Airtel, Idea, Vodafone and recently Jio. Despite the presence of domestically developed enterprises in the telecom sector, India’s telecom infrastructure relies heavily on Chinese telecom vendors, primarily Huawei and ZTE, for the supply of hardware equipment, network gear and switches. Huawei and ZTE commenced operations in India in 2000 and 2003, respectively. Leveraging both technological efficiencies and economies of scale, Chinese vendors have extensively penetrated India’s telecom space, with agreements established with nearly all telecom providers in the country. Chinese vendors command a substantial 44% share of India’s telecom market (IndBiz, 2024). According to Minister of State Sanjay Dhotre’s statement in the Indian Parliament in 2020, 50% of mobile network equipment utilised by BSNL is procured from Chinese vendors Huawei (44%) and ZTE (9%) (The Times of India, 2020, September 17). Similarly, private network operators such as Airtel and Vodafone rely on Huawei and ZTE for 30%–35% of their equipment for their 4G networks.

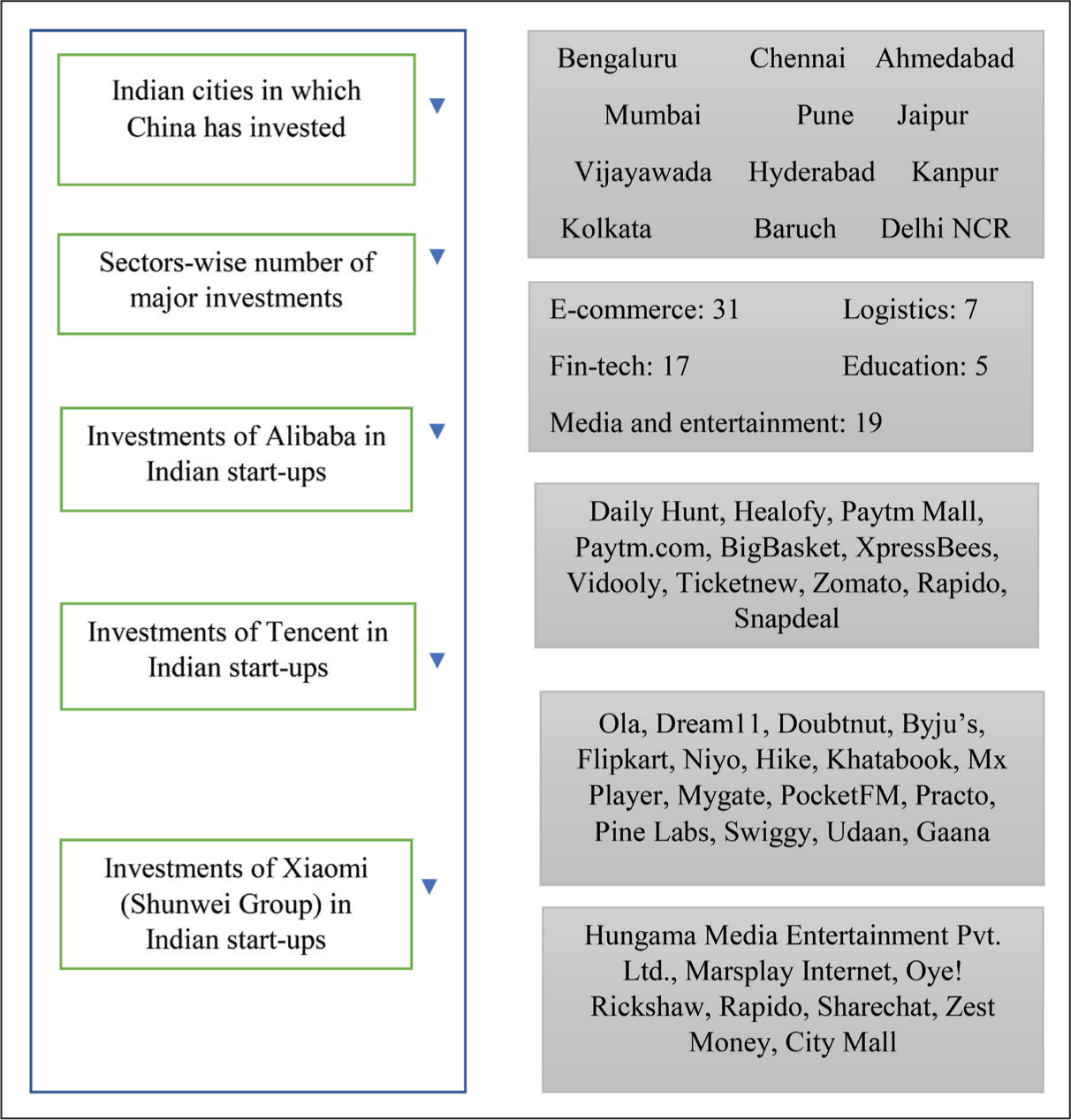

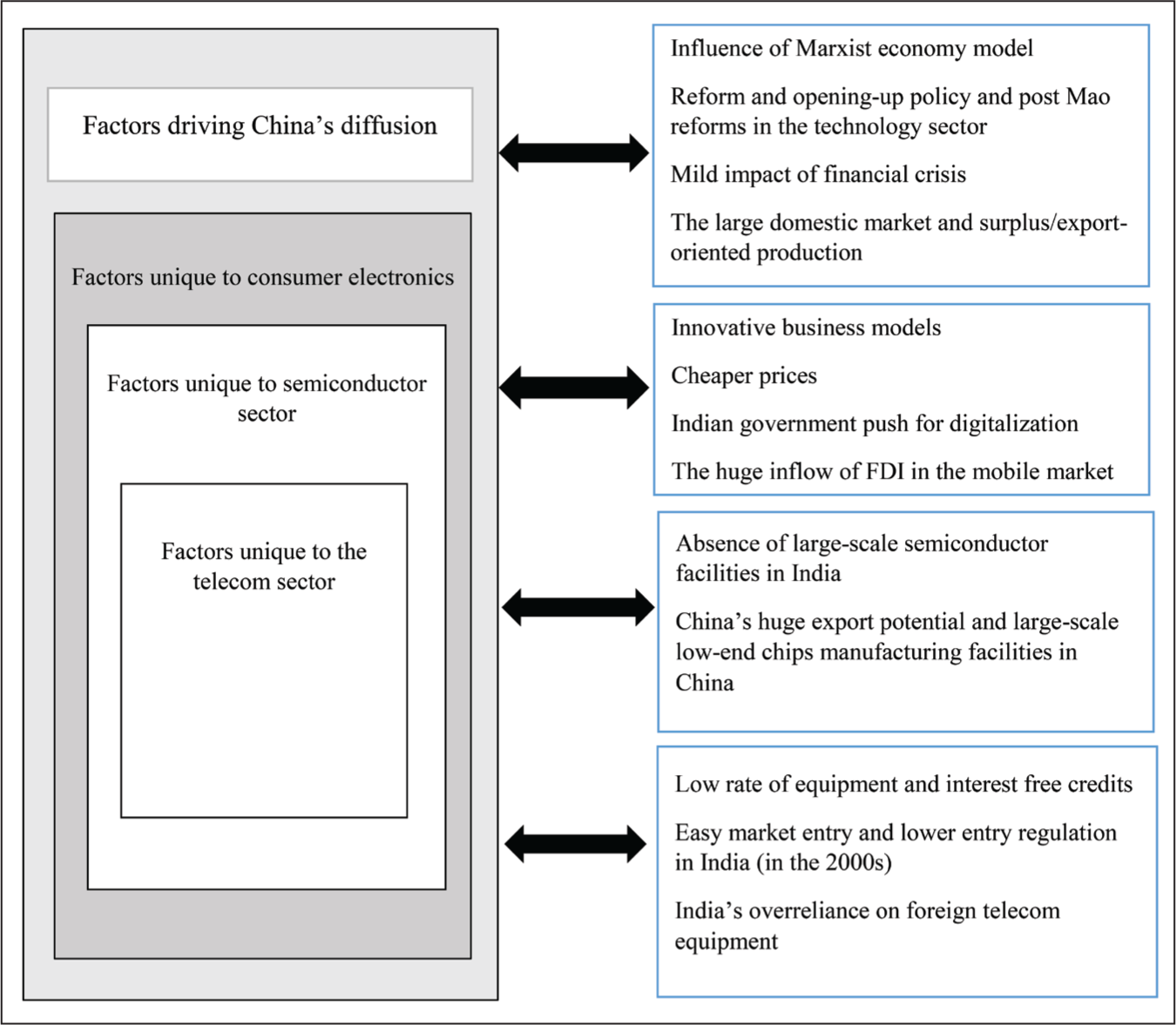

China’s significant presence and influence in India’s ICT sector stem from various push and pull factors associated with Chinese policies and investment strategies. The diffusion of China’s ICT in India, particularly in the telecom and mobile phone sectors, is a relatively recent phenomenon. China’s extensive reforms, coupled with the rising purchasing power and larger disposable income of its populace for offshore investments in technology companies, have facilitated China’s ICT diffusion in countries like India. However, similar push factors present in many advanced nations have not resulted in comparable outcomes. Chinese companies have adeptly exploited key limitations in India’s technology landscape. Unlike neighbouring countries, Chinese investments in India exhibit two distinct dimensions. First, they are largely driven by the private sector, posing less immediate concern for Indian national security interests. Second, they target internet-based industries, including the platform economy, which eagerly seek foreign-invested funds. Unlike visible assets such as ports, roads and railways, Chinese presence in India’s start-up and tech sector aims to secure strategic control of India’s economy and foster dependence on China. Figure 4 illustrates sector-wise key factors enabling China to capitalise on the Indian tech market.

Regarding Chinese investments, three key reasons explain why Chinese investors have had a profound impact on India’s tech ecosystem. First, the lack of major venture capital investors in India to fund Indian start-ups has created an opening for Chinese investors, who possess substantial funds for offshore investments and enjoy state support. This has allowed them to exploit vulnerabilities in the Indian start-up ecosystem, as India has yet to establish a reliable venture capital funding mechanism of its own. Chinese investors have capitalised on this gap early on. Additionally, Indian start-ups benefit from the superior market coping practices, technology and professional experiences of Chinese companies. For instance, after Alibaba acquired a 40% stake in Paytm, the latter emerged as a dominant player in the digital payments market, benefiting from the demonetisation drive and the Indian government’s push for a digital economy.

Second, the risk-taking behaviour of Chinese investors, unlike others, is appealing to the Indian start-up sector, especially for loss-making start-ups on the verge of collapse. Instead of shutting down, funds-starved Indian start-ups often opt to trade market share. India’s telecom sector serves as a notable example. Chinese telecom companies illustrate how overseas firms can outcompete domestic and foreign competitors by offering more favourable business terms. Due to a scarcity of technological resources and necessary hardware to meet network requirements, Indian firms rely on foreign vendors. Before Chinese vendors dominated the market, European companies such as Ericsson and Nokia were major suppliers to Indian network operators. However, Chinese vendors such as Huawei and ZTE entered the Indian market in the 2000s, offering significantly cheaper prices for network gear, which were more attractive to Indian telecom players compared to European dealers. Chinese vendors introduced easy payment terms, including interest-free loans and soon came to dominate the Indian telecom space as major suppliers of telecom equipment.

Third, for Chinese investors, diversifying into targeted markets and recognising their strategic importance are crucial, especially given the concerted effort from the Chinese state to expand internationally. The Indian market holds both strategic and retail value in this context. Companies such as Alibaba and Tencent have expanded their investment horizons in India accordingly. China also tailors its investments to align with the needs of India’s growing digital and consumer market. Following India’s demonetisation drive, Chinese investments in India’s fintech sector (e.g., Paytm) and e-commerce sector (e.g., BigBasket) have increased. Considering India’s position as the world’s fifth-largest auto market, China is now urging its companies to enter the Indian market for electric vehicles. Leveraging existing Chinese brands such as Volvo and MG, China is facilitating the entry of companies like BYD into India’s electric vehicle market besides ICT.

India’s Evolving Technology Policy Space

Concerns regarding the potential infiltration of Chinese-origin vulnerabilities in critical systems have heightened, prompting a reassessment of reliance on Chinese-made telecom and power equipment. Notably, Chinese digital products, both tangible and intangible, including preloaded applications on Chinese mobile phones and data mining practices, have come under increased scrutiny. For instance, in 2010, the Indian government received a hint that the Chinese employing spyware in their telecommunications technology. However, the debt-ridden Indian telecom players and price-sensitive Indian consumers were lured by extremely lucrative deals from Chinese vendors. Back then, such reports were sidelined as ousting Chinese vendors could have directly affected India’s 3G adoption drive (Rao, 2014). Thus, the lack of cheaper alternatives and the absence of local sources forced the government to allow the penetration of Chinese technology wherein economic interests overrode security interests.

However, the Indian government’s approach towards China’s technological presence started to shift in recent years due to two prominent developments. First, China’s aggressive geopolitical moves against India in the Himalayan bordering region culminated in the 2020 Galwan border crisis between the two neighbours. Second, the US–China technology war has created a window for India to reduce its reliance on China and revamp its position as a manufacturing powerhouse.

India’s approach to navigating the complex geopolitical landscape, particularly in the aftermath of the Galwan crisis in May 2020, can be classified into four distinct categories: (a) intimidation, boycott and protectionism; (b) localisation and liberalisation; (c) industrial policies and (d) technology diplomacy.

The threat from Chinese technology was also eminent before the Galwan crisis, but the response of the Indian government was not bluntly aggressive. In 2016, the Indian government banned the import of specific electronic items from China that included mobile phone brands citing violations of security codes by Chinese manufacturers (The Economic Times, 2023). A year later, India’s Ministry of Electronics and IT asked 21 smartphone manufacturers to furnish details of the frameworks and practices (Saha, 2017). According to the reports, the Indian government also planned to direct all foreign smartphone makers to set up their servers in India to ensure the data protection of Indian users (Aulakh, 2017).

Responding to China’s aggressive military action in the Galwan area at the Sino-Indian border, Indian leadership acted promptly to boycott Chinese goods and services, particularly in the ICT domain. Highlighting what is called the Indian tech crackdown on Chinese companies, the Indian government in June 2020 banned over 150 Chinese apps including popular apps such as TikTok, UC Browser and ShareIt (Garg, 2022). In a second major blow to the Chinese tech entrepreneurs, the Indian regulatory agency, Enforcement Directorate, froze more than $58 billion in the bank accounts of Vivo India and Oppo Mobile, accusing them of tax evasion practices (Mehta, 2022). India also updated its FDI policy. Without naming China, the updated rules mandated the investor who is a foreign national from the bordering country to ensure approval from the government route, and not through a direct FDI window (Siddhartha, 2020). To control the reliance on Chinese vendors in the telecom sector, the Indian government disallowed the use of Chinese equipment by any Indian telecom player, which delayed the 4G upgrade process. BSNL was banned from using equipment from Chinese vendors like Huawei and ZTE as a retaliative move after border clashes (Mankotia, 2020).

The anti-China policies in the business and tech sector have not been limited to the regulatory actions of the central governments as the governments at the state level have also undergone a policy reconsideration. While the government of the Indian state of Maharashtra temporarily paused the progress on three Chinese projects running in the state, the Haryana government halted the power station contracts with two Chinese companies (Chauhan, 2020; Lewis, 2020). Indian Railway also terminated a contract for installing a signalling and telecom system worth 471 crores with a Chinese firm CRSC Group after the border clashes (Chaturvedi, 2020). In 2021, without putting an outright ban on Huawei, the Indian government disallowed deals with the company for the 5G rollout plan (BBC, 2021, May 5). This reflects how India’s approach towards China’s involvement in its critical infrastructure has shifted towards boycott and protectionism.

In the wake of the geopolitical crisis, the anti-China sentiments among the Indian public also gained popularity and created an opportunity for the policy of localisation and liberalisation. This approach emphasises the need for India to strengthen its domestic capabilities while simultaneously liberalising policies to encourage economic growth. Leveraging an opportunity offered by combined factors—the COVID-19 disruptions and tense state of relations with China, the Indian government launched its ambitious Atma Nirbhar Bharat (or self-reliance) programme and the campaign ‘vocal for local’ aimed at making India self-reliant. Technology is one of the five major pillars of the Atma Nirbhar programme. Indian policymakers have emphasised diversifying its import basket and enhancing its domestic capabilities in the ICT sector. Indian Cabinet Minister Nitin Gadkari in an interview said that India will try to curb Chinese investments in many sectors, especially the MSME, and will instead welcome other foreign ventures in the Indian market (The Times of India, 2020, July 1).

To boost India’s ambitious Atmanirbhar Bharat programme, the Indian government procurement portal, Government E-Marketplace (GeM) also mandated its seller to specify the ‘country of origin’ (The Times of India, 2020, June 23). GeM has also enabled the provision for the seller to specify the percentage of content that is locally sourced to promote Make in India. The portal, thus, introduces a Make in India filter for all products listed on the platform. The Department of Telecommunications also announced deploying end-to-end indigenously developed telecom technology products (PIB, 2022).

Amid a wave of policy transformation, the Indian government’s approach towards technology policy advocacy also showcases a more liberal approach. On the question of software and architectural designs, India advocates the development and promotion of open-source platforms that make the use and transfer of ICT technologies more affordable, transparent, flexible and inclusive for all. India’s domestic initiatives like digital public infrastructure, centred around open architectures for payments, showcase India’s commitment to open and inclusive technological frameworks. India’s new Data Protection Bill, 2023, seeks to resolve the concerns regarding data localisation by moving from strict data localisation to a more rational approach allowing data sharing practices. To resolve supply chain hurdles in telecom and semiconductors, India supports the promotion of an open RAN and RISC-V Foundation, an open-source alternative to ARM instruction set architecture.

The heated competition between the United States and China over emerging technologies has strengthened the role of geopolitical considerations in domestic policymaking. For instance, the global supply chain of semiconductor chips is under reconstruction due to American export control measures. In the pursuit of diversifying production away from China, businesses as well as governments are exploring alternatives without completely severing ties with China. This strategy is termed by the United States as the ‘China Plus One’ strategy. India, alongside nations such as Vietnam, Thailand and Malaysia, emerges as a favourable alternative. In this evolving geopolitical scenario, India’s time remains crucial in navigating between closer economic ties and dependency on its Asian neighbour, and leveraging an opportunity to reinvent its role in the global economy as a manufacturing power. The allure of easier market access, a substantial pool of engineers and the potential for wider economies of scale have prompted companies to contemplate and initiate partial relocation of their value chain to India.

This significantly turned the policy focus of the Indian government towards the ICT domain. To lure foreign investment in India’s ICT sector, the Indian government has rolled out an attractive package of government financial support of $10 billion in the form of the PLI scheme. Through the PLI scheme, the government sought to receive applications from foreign investors to invest in India’s manufacturing sector including the ATP sites for semiconductor chips, electronic items such as laptops, mobile phones, etc. Through this scheme, the Indian government sought to manoeuvre the opportunity to shift the focus from China to India as the manufacturing hub amid the growing uncertainties of business in China and the US–China tech war.

Lastly, India’s enhanced focus on technology diplomacy can also be seen as part of India’s efforts to participate in changing the contours of global supply chains. India acknowledges the necessity of global partnerships in navigating the complex technology landscape due to specialisation in different parts of the supply chain. The joint statements from the American National Security Advisors’ meeting and the Modi–Biden summit underscore the increasing importance of technology collaboration between India and the United States (The White House, 2023). The recent culmination of the initiative of critical and emerging technologies (iCET) in 2022 highlighted the need to build trusted telecommunications and resilient supply chains, which indirectly points out building a collaborative approach to counter China’s dominance in ICT supply chains (The White House, 2023). India’s multilateral approach towards building a resilient supply chain is reflected in its Resilient Supply Chain Initiative in collaboration with Japan and Australia which is also directed to move supply chains away from China (PIB, 2021).

Clearly, in recent years, India’s approach has evolved to locate around external challenges. The heightened military tensions brought about a realisation that dependence on a strategic adversary poses inherent risks, prompting a re-evaluation of technological engagements. Before the Galwan phase, economic necessities seem to have overridden security concerns. This lens suggests that India emphasised more on the mutual economic benefit derived from trade. In recent years, a noticeable shift can be seen towards prioritising security. In short, from an economy-first approach, India’s technology policies have adopted a security-first approach. This shift has been evident in various technology spheres, including telecom infrastructure, mobile applications and semiconductor manufacturing.

Is Decoupling a Feasible Option for India?

It is evident that China holds significant strategic depth in India’s ICT sector, and India’s approach towards China is experiencing a notable shift. While countries such as the United States, Japan and India are rhetorically promoting ‘decoupling’ and taking relevant actions, a central debate in India’s technology policy and its foreign policy towards China is: Is decoupling feasible for India? It is pertinent to assess whether the move towards greater self-reliance is a prudent, proactive decision amidst rising protectionist sentiments worldwide, or if it is a short-sighted manoeuvre based on an outdated import substitution strategy. The following are key factors that lie central to India’s key challenges.

The Import Factor

In 2020, as part of a populist policy measure, the Indian government implemented aggressive policies aimed at reducing the presence of Chinese vendors in India’s ICT sector and promoting the ‘Made in India’ tag in the manufacturing sector. A visible impact is evident in the share of electronic goods in India’s import basket, with total merchandise imports declining to 10.82% in 2022–2023 from 12.02% in 2021–2022 (Outlook India, 2023, April 13). However, in the electronics category, China’s share in India’s imports has risen from 39.6% to 48.4% over the last four years (2018–2022) (Mazumdar, 2023). These figures indicate that while the geopolitical crisis at the border prompted a shift in policy direction, it failed to stimulate production capabilities that could decrease India’s imports from China. Despite an initial decline in import figures, which could also be attributed to the timeline of the COVID-19 pandemic, India’s import basket in the electronics category remains dominated by China.

It also poses a challenge for India to sustain a downward trend in its imports from China. Many products in India’s export basket are manufactured using raw materials and intermediate goods sourced from China. According to a study, India’s imports from China play a significant role in boosting its exports across various categories. Since India depends on China for raw materials and processed goods, imports also contribute to India’s production output in numerous sectors (Raju & Saradhi, 2019). This implies that imports from China are essential to India’s current manufacturing capabilities and are intricately linked to India’s export capacity.

The ‘Made in China’ Tag in India’s ICT Sector

Despite aspirations to enhance domestic production, India’s manufacturing technologies remain underdeveloped. Renowned Indian economist Raghuram Rajan has pointed out the prevalent use of government incentives in assembly rather than original manufacturing, indicating a lack of focus in key sectors (Singh, 2023). Make in India, touted as a flagship policy to promote domestic manufacturing, lacks emphasis on critical sectors, highlighting its inability to drive significant change. The policy’s shortcomings are evident in India’s ongoing dependence on China, especially in high-tech industries where India lacks independent production capabilities. Skill shortages, regulatory uncertainties and inadequate access to finance further impede progress, necessitating deeper domestic policy reforms. Additionally, the lack of capital flow in the private sector stands as the primary contributing factor to China’s dominance in India’s tech start-up ecosystem. India’s private sector grapples with insufficient R&D funding, particularly in hardware and technology domains, hindering its competitiveness in the global market.

The low-risk tolerance of Indian private sector entities is identified as a factor contributing to challenges in private sector investment. The risk-averse nature of the private sector may hinder investments, especially in areas requiring substantial risk-taking, such as basic science and research. However, a noticeable shift is occurring within the private sector as they recognise the evolving national sentiment, influenced by both the government and the public. However, in parallel to the private sector in the United States, their Indian counterparts seem to be trailing behind government initiatives rather than leading the charge in seeking to decouple from China.

The Cost Factor

Additionally, India’s dependency on China is exacerbated by a combination of factors, including the absence of cheaper alternative import sources, price-sensitive Indian consumers, lack of significant financial incentives from the state and insufficient venture capitalist funding. For instance, in the telecom switch market, relying on non-Chinese foreign suppliers would lead to higher production costs for Indian telecom operators. Unlike Chinese vendors, these costs are not offset by government policies, thus increasing production costs passed on to consumers, particularly those from lower-income groups. Consequently, cutting off supplies from Chinese vendors remain challenging in the short run. Despite efforts to protest against the ‘Made in China’ tag in tangible goods, China’s entrenched presence in India’s e-commerce sector, business platforms and start-ups through venture capitalist funding persists even after the Galwan incident. As of 2022, four Chinese smartphone brands still dominate India’s smartphone market (Figure 2). Huawei’s network gears have also been supplied widely among Indian operators despite restrictions.

The External Factor

While India aims to enhance technology accessibility and affordability through its multilateral and collaborative approach, its absence and lack of voice at certain platforms hinder its ability to reshape the global technology ecosystem. India’s isolation from key global initiatives and agreements, such as the WTO’s Information Technology Agreement and the Regional Comprehensive Economic Partnership, limits its integration into critical technology ecosystems and supply chains. Non-participation in initiatives such as ITA2, ITA3 and RCEP highlights missed opportunities for India to diversify its trade relations and reduce dependency on China. India’s pursuit of Free Trade Agreements with individual countries as an alternative to multilateral agreements poses challenges. Lengthy negotiation processes and the potential delay in realising benefits may impede India’s efforts to diversify its trade partnerships and reduce reliance on China. Moreover, divergences in interests, such as India’s proposal of its own 5Gi standards in the 5G space, may strain relations within frameworks like the Quad, albeit offering opportunities for India to showcase its technological innovations on a global stage.

Even as India strives to bolster its manufacturing sector, with aspirations to increase its share from the current 17% to 18% of GDP to 25% in the coming decade, it is poised to maintain a significant reliance on China for a substantial portion of imports. Therefore, an immediate call for decoupling and cutting off supply chains from China could detrimentally affect India’s manufacturing interests and significantly impact its production costs. As India’s opportunities and challenges are intricately intertwined in navigating the global technology landscape, a more nuanced approach should prioritise resilience and diversification.

Conclusion and Way Forward

This article contributes to the literature on India’s China challenge in a rather underexplored dimension—the ICT sector. It studies the influence and patterns of Chinese ICT investments in India in four key sub-sectors. It highlights that India’s increasing complexity in its relationship with China is not limited to banning mere applications, rather the nexus between technological capabilities and geopolitics extends comprehensively to encompass data, telecom networks, critical and emerging technologies, semiconductors and the broader landscape of electronic components and supply chains.

The article acknowledges two key factors that give rise to India’s transformed approaches to responding to these challenges: the geopolitical tensions at the Himalayan border, and the ongoing geopolitical backlash against China characterised by heightened scrutiny of Chinese technologies. The article highlights two key reasons behind India’s enhanced emphasis on revising its technology policies: first, its increasing interest in participating in the global supply chains, and second, reducing its reliance on Chinese technology, thereby reducing the associated national security threats.

The article provides an assessment of India’s technology policy in recent years and categorised it into four key areas: (a) intimidation, boycott and protectionism, (b) localisation and liberalisation, (c) industrial policies and (d) technology policies. India’s proactive efforts in policymaking, which are increasingly more aligned with its geopolitical interests, reveal India’s strategic mindset that reflects the growing acknowledgement of the inextricable link between technology and geopolitics. Thus, a realisation that technology is not merely a neutral tool but a driver of competitive geopolitics is now central to India’s strategic calculus.

This article highlighted that India’s journey towards decoupling from China is fraught with challenges, including manufacturing limitations, policy inadequacies and global trade dynamics. It is argued that India’s aspirations of emerging as a manufacturing powerhouse do not align with a narrow interpretation of the term ‘decoupling’. Following the Galwan crisis, India’s approach to handling Chinese investments has shifted to a ‘security-first’ approach from an ‘economy-first’ approach. This parallels the US’s approach to China, where emerging policy dimensions increasingly prioritise American national security considerations. However, the meaning of decoupling over technology must be distinct for India compared to the United States. While the United States as an upstream supplier in the value chain lies in an empowered position, India’s dependence on China is pervasive across various facets of the fragmented supply chain. Acknowledging China’s prominence in the global economic landscape, the imperative of trade with China is unequivocal, and a refusal to engage would be impractical. Thus, India needs to adopt a pragmatic approach that calls for diversification away from China, and careful stocktaking. A shift towards resilience, diversification and a phased approach that combines global integration with local capacity building is proposed.

India’s approach should emphasise strategic dimensions of engagement with China. An emphasis on derisking and diversification should acknowledge that not all tech is strategic. Also, not every aspect of technology collaboration needs to be strategic. There is a need for a comprehensive assessment of vulnerabilities. It is essential to distinguish between individual consumer choices and strategic acquisitions by governments. While personal purchases may be indifferent to the country of origin, strategic procurement necessitates a judicious consideration of geopolitical implications. In fact, other areas of cooperation involving non-strategic technologies can enhance economies of scale for Indian manufacturers. This perspective emphasises the pragmatic approach of taking advantage of collaboration with Chinese companies in areas where it benefits India’s national interest.

Moreover, India needs to build strong and resilient alternatives. Achieving technological self-sufficiency, developing technological know-how, securing venture capital investments and developing sophisticated management practices are vital to realising India’s ambitions. If India tends to do away with Chinese imports, it either needs to find an alternative import destination or ensure domestic manufacturing of these products. To ensure this, India needs to propel growth in manufacturing high-technology products and the raw materials required in their production. Additionally, there is a need to carry out massive reforms in the domestic skilling and labour sector. The focus should first be on incentivising the manufacturing process of raw materials and equipment.

This article contributes to the literature in two significant directions: It updates the literature on India’s China challenge and provides a critical assessment of India’s technology policy options. The article also evaluates the efficacy of India’s current approaches adopted in the aftermath of the Galwan crisis. Overall, the article stimulates the debate on India’s enhanced participation in the global technology landscape.

India’s technology policies are set to evolve in a rapidly transforming world characterised by the intertwined nature of national security, geopolitics and technological development. It remains to be seen whether India’s technological rise emerges as a response to its growing China challenge, as a spillover impact of great power competition over technology, or as part of its aspiration to become a great power. Thus, there remains further scope to decode India’s evolving technology policies and its participation in global supply chains.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received funding from Manipal Academy of Higher Education, India.