Abstract

Remittances remain a vital financial inflow into the economies of Sub-Saharan Africa (SSA). Many studies have outlined its role in indicators such as health, education, poverty reduction, economic growth, financial development, among others. This stimulates the need to harness the benefits associated with this financial inflow. The study proposes an idea to utilize remittances in Sub-Saharan Africa and advances recommendations to augment existing initiatives. A descriptive approach was used. The study recommends the creation of a health account to encourage savings purposely for the healthcare financing of remittance recipients in SSA. It further outlines processes via which such an account could work and the prospective benefits be reaped.

Introduction

Remittances sent to Sub-Saharan Africa (SSA) have remained steady over the period relative to other financial inflows like foreign direct investment (FDI), official development assistance (ODA), and portfolio equity. Between 2016 and 2020, remittance inflows to SSA have exceeded FDI inflows. For low-income countries, a substantial number currently receive more remittances than FDI (World Bank, 2022a). The socio-economic and political characteristics of these low-income countries may make it problematic for them to attract foreign investments compared to their counterparts with higher incomes. Thus, remittances bring some balance in financial inflows to these low-income countries. According to the World Bank (2022b), even during COVID-19, 90% of global remittances were sent by migrants working in countries where three-quarters of the globe’s COVID-19 cases were recorded. Amid the pandemic, migrants were still motivated to send money to friends and families back home. This income as such presents an alternative source to augment existing health financing strategies in SSA. If the region must achieve the universal health coverage target of the sustainable development goals, it is imperative to explore and utilize these kinds of financial inflows.

Literature Review

Ratha et al. (2011) estimated the use of remittances by selected African countries. They identified several items that remittance recipients spend their funds on. Notable among these were food, education, construction of new houses, setting up businesses, and health. It was revealed that the selected African countries consistently spent higher proportions of their funds on food, education, and health. Figures from their estimation showed that countries had spent between 16.1% and 89.4% of the total remittance receipts on these three items (food, education, and health), irrespective of the source of remittance. In Senegal, for example, 66.9%, 82.2%, and 89.4% of remittances received from migrants outside Africa, within Africa, and within the country, respectively, were spent on these three items (ibid). These highlight the relevance of this financial inflow particularly to the health of the people of this region.

Some scholars have extended the conversation and presented empirical evidence of the relevance of remittance to the health of the region and beyond. Amega (2018) concluded that remittances reduce infant and adult mortalities, and extend life expectancy and chances of surviving to age 65 in SSA. Amakom and Iheoma (2014) confirmed that an increase in remittances results in an increase in life expectancy at birth in SSA. In developing countries, remittances were found to improve the health of children (Ahmad et al., 2019). Chauvet et al. (2009) found that remittances improve child and infant mortality rates in developing countries. Additionally, remittances promote access to private healthcare services in developing countries (Drabo & Ebeke, 2011). Zhunio et al. (2012) argued that remittances decrease infant mortality and increase life expectancy in low- and middle-income countries.

From the reviews, much can be harnessed from this financial inflow to shape the development of SSA. Some remittance and insurance experts have suggested the purchase of insurance packages for remittance recipients and/or senders from funds remitted (Thom et al., 2021; Ocansey, 2022). They argue that this will ensure access to healthcare at unprepared times. They have suggested money transfer operators (MTOs) like Western Union partner with insurance companies and sign-up remittance recipients to various insurance packages. MTOs will then deduct insurance premium charges from remittances received to cover the health needs of the recipients (ibid). This approach is acknowledged to be a step further towards improvement in health financing. However, a setback is that, for remittance recipients with “good” health who sign up for this policy, there is a tendency that they will not utilize health services over a period, although their health insurance premium has been paid for. That is, people may subscribe to health insurance packages that they may not eventually utilize. This may reduce the urge for resubscription or new enrolments onto the policy in future. It raises a plausible question: Will remittance senders be committed to the continuous payment for the health of remittance recipients (via insurance premiums) even when the latter (remittance recipients) do not consume? Or will remittance senders be likely to commit resources only when recipients consume health services? For example, if a recipient of a health insurance package has not visited the hospital over a period, will that affect the remittance sender’s decision to continue with the insurance policy or even purchase more for other beneficiaries? These are questions that would require empirical scientific investigations. However, inherent in these is that there may be emergency days when remittance senders may not be capacitated to finance the health needs of remittance recipients in real time. Thus, saving for such days is crucial.

Overview of Insurance in Sub-Saharan Africa

An overview of the insurance culture and insurance market in SSA has been one that has portrayed slow exploitation of the sector, notwithstanding the prospects. The insurance market in SSA and Africa generally has been relatively restricted, with the microinsurance coverage ratio in Africa, for example, pegging at only 5.4% (Statista, 2023). The insurance penetration rate which measures “the ratio between the value of premiums written in a particular year in a particular country to the GDP of the respective country,” remains at low levels in SSA. The rate was 16.99% in 2017 for South Africa (the country with the highest penetration rate in SSA). It was followed by Namibia, Lesotho, Mauritius, and Zimbabwe, with rates between 4% and 7%. About half of the countries in the region had a penetration rate of less than 1% (Rudden, 2022, cited in Statista, 2023). Recent analyses of the penetration rate revealed that South Africa remained the only African country ranked among the top 20 countries with the highest rates. Even that, the figure had fallen from the almost 17% in 2017 to 12.2% in 2021 (Statista, 2023). Rudden (2022) argues that the “low penetration is because the African insurance industry is still in its infancy, premiums are financially out of reach of many people, and financial literacy is relatively low” (cited in Statista, 2023).

Policy Proposal

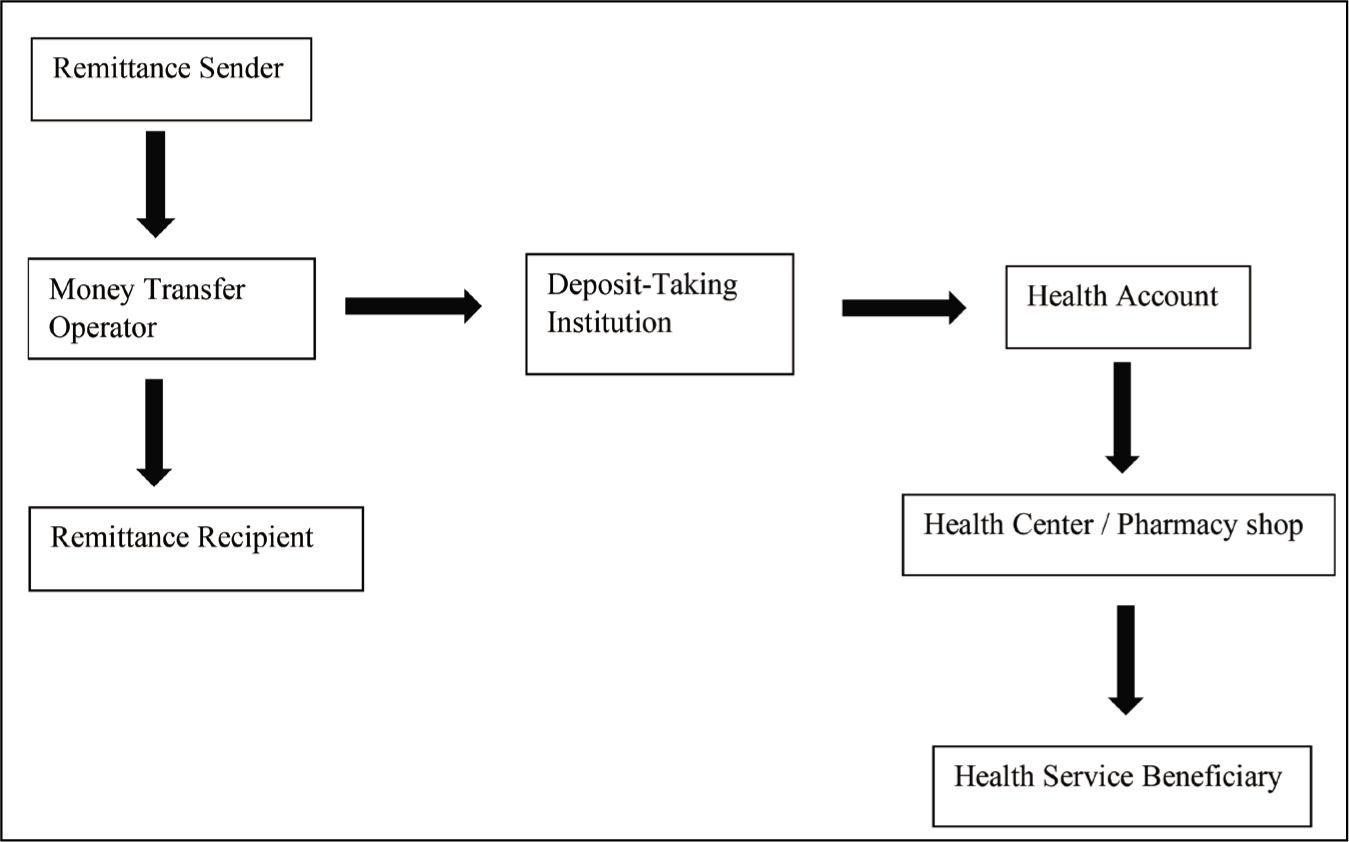

This article hence proposes the introduction of a health account which will allow remittance senders to save a fraction of remittances into such an account and will be accessed by identified beneficiaries back home when they need health services. The process starts with a sender remitting money via an MTO. With the status quo, a beneficiary of the money sent would walk up to the MTO to withdraw all their funds. But with this intervention, the MTO will have to collaborate with a deposit-taking institution (DTI) like a bank and keep a fraction of the remitted funds in a health account for interested clients. The DTI will hold the funds of depositors in this account until it is needed. The MTO in extensive consultations with remittance senders, beneficiaries, and any other identified stakeholders will further identify and collaborate with specific health centers where beneficiaries can sign up for health services. These health centers must have the capacity or be capacitated with systems that will enable them to accept the mode of payment associated with this intervention. Training and workshops should also be provided to staff to abreast them with the development.

The remittance sender gets the priority to select people to be registered on the health account as beneficiaries. A premium per beneficiary per period (say monthly or quarterly) will be paid into the single health account created for the beneficiary(ies), preferably when the sender makes general remits. Beneficiaries will then be offered vouchers or cards which will allow them to seek health services at their registered health centers and bills deducted from the health account. Specific pharmacy shops can also be brought on board to enable beneficiaries to purchase medicines with their voucher or card. Funds in the health account that remain unused at the end of the financial year (say one year) will be rolled over for the following year. Depending on the financial standings of clients (senders and beneficiaries), and their attitudes toward saving in the health account over a period, among other factors, beneficiaries may be allowed “overdraft” spending from the health account and pay back later, subject to the approval of the MTOs, DTIs, and remittances senders.

Model for Proposal

The model shown in Figure 1 simplifies the proposal outlined above. A sender who has opted for a health account would have their money split into two: a greater fraction to be received in cash by the remittance recipient and a smaller fraction kept with the MTO, and by extension a DTI. The reserved funds will only be released when beneficiaries consume health services and must finance that. Beneficiaries will then get the flexibility to spend the remittances received on other goods and services, while they further get to access health services.

A Model for the Proposal.

Benefits of Proposal

With this approach, remittance senders only pay for the health of beneficiaries when they consume health services. Unused funds in the health account at the end of a period will be rolled over for the next period. The advantage of this over subscribing to an insurance package is that people may not be demotivated to discourage financial contributions to the scheme even when they do not utilize health services presently. There is some assurance to the beneficiaries that they can contribute now and enjoy health services in the future.

This intervention will also offer remittance senders some control assurance on the intended and actual utilization of the funds sent. Remittance senders will have the option to decide who becomes a beneficiary of the health account. This will ensure that the targeted beneficiaries are the ones who actually benefit. Remittance senders will also have an assurance that a fraction of funds remitted meant for healthcare is spent as such. The possible advantage will be the motivation for senders to remit more in future.

Moreover, this intervention can offer some flexibility for beneficiaries to consume healthcare with insufficient health account balance and payback in future. This approach should however be subjected to intensive scrutiny to appraise its feasibility. A thorough assessment should be conducted on beneficiaries and remittance senders before they are granted such an offer.

MTOs will continue to benefit from the low exchange rate conversions resulting from their partnerships with banks and/or the commission or brokerage fees they charge for such transactions; just like they do for general remittances. They may also benefit from market-share expansion as they introduce this innovative service.

DTIs will benefit from charges on services rendered to beneficiaries including payment of health bills to health centers on behalf of beneficiaries. It will also be an opportunity for DTIs to market their service offers to these prospective clients to expand their customer base.

Health centers will likewise benefit from additions to their customer base and associated spillovers like personal recommendations from beneficiaries.

Finally, beneficiaries of a health account will benefit from access to healthcare and reductions in out-of-pocket health expenditures.

Recommendation

It is highly recommended that further scientific inquiries be conducted into the design, implementation, monitoring, and evaluation of such a scheme (health account). For instance, further studies should be conducted on the characteristics of migrants, their attitudes towards insurance, and feasibility in the implementation of a health account system in SSA.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.