Abstract

In 1992, Naresh Goyal started on a journey to build the best airline in India, Jet Airways. With rising market share and revenues, Jet Airways began climbing up the ladder of success. It gradually became one of the household names in the Indian aviation sector. In 2005, it came up with an initial public offering (IPO) to reach greater heights with large investments from the funding raised. A ‘paradigm shift’ in the Indian airline business came in 2006 with the increased competition and entry of low-cost carriers. The rise in the competition impacted Jet’s turnover, which was ultimately reflected in the diminishing profitability margins. With a series of industry challenges and questionable managerial decisions, Jet became a debt-ridden and loss-making enterprise from being one of the leaders in the aviation sector. Eventually, in April 2019, Jet Airways temporarily ceased its operations because of a lack of funding available to sustain it. The consortium of lenders, led by State Bank of India (SBI), faced a serious dilemma; whether to revive the airline by looking for potential investors or declare Jet bankrupt and begin the bankruptcy proceedings.

Keywords

Discussion Questions

1. I. Based on ‘Table 1: Pre-IPO period financial highlights’ calculate for all the given years

Year-on-year growth rates of total revenues and total expenses assuming 1999–2000 as the base year. Compounded annual growth rate (CAGR) for total revenue and Earnings Before Interest Tax Depreciation and Amortisation (EBIDTA). Earnings Before Interest Tax Depreciation Amortisation and Rent (EBIDTAR) margin, EBITDA margin, Earnings Before Interest and Tax (EBIT) margin, net profit margin and long-term debt to equity ratio.

II. What can you interpret about companies’ pre-initial public offering (pre-IPO) financial performance based on your calculations?

2. If you are undertaking due diligence of an airline as a prospective target for acquisition, which areas would you analyse under the following aspects: financial, operational, marketing and human resource?

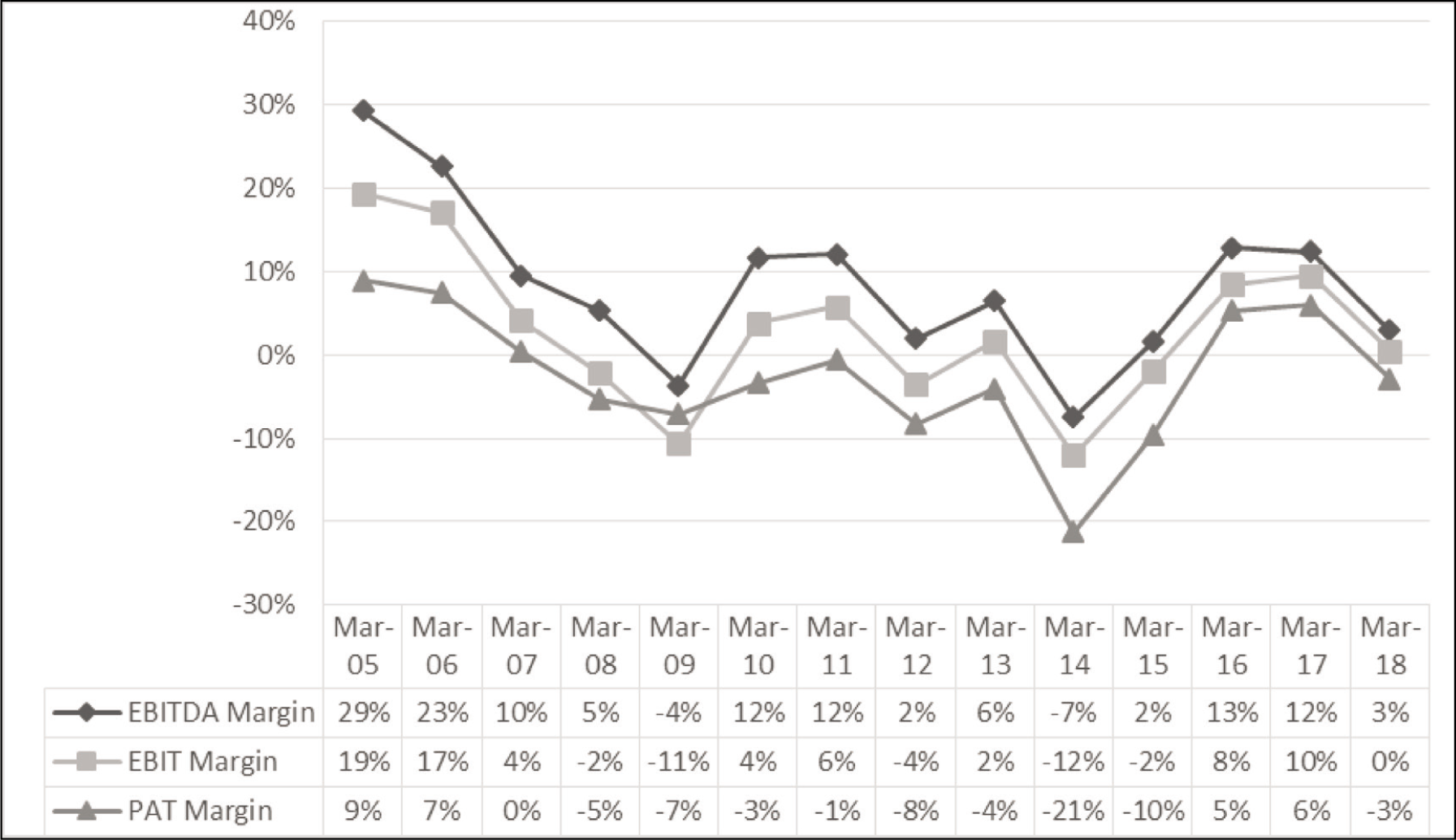

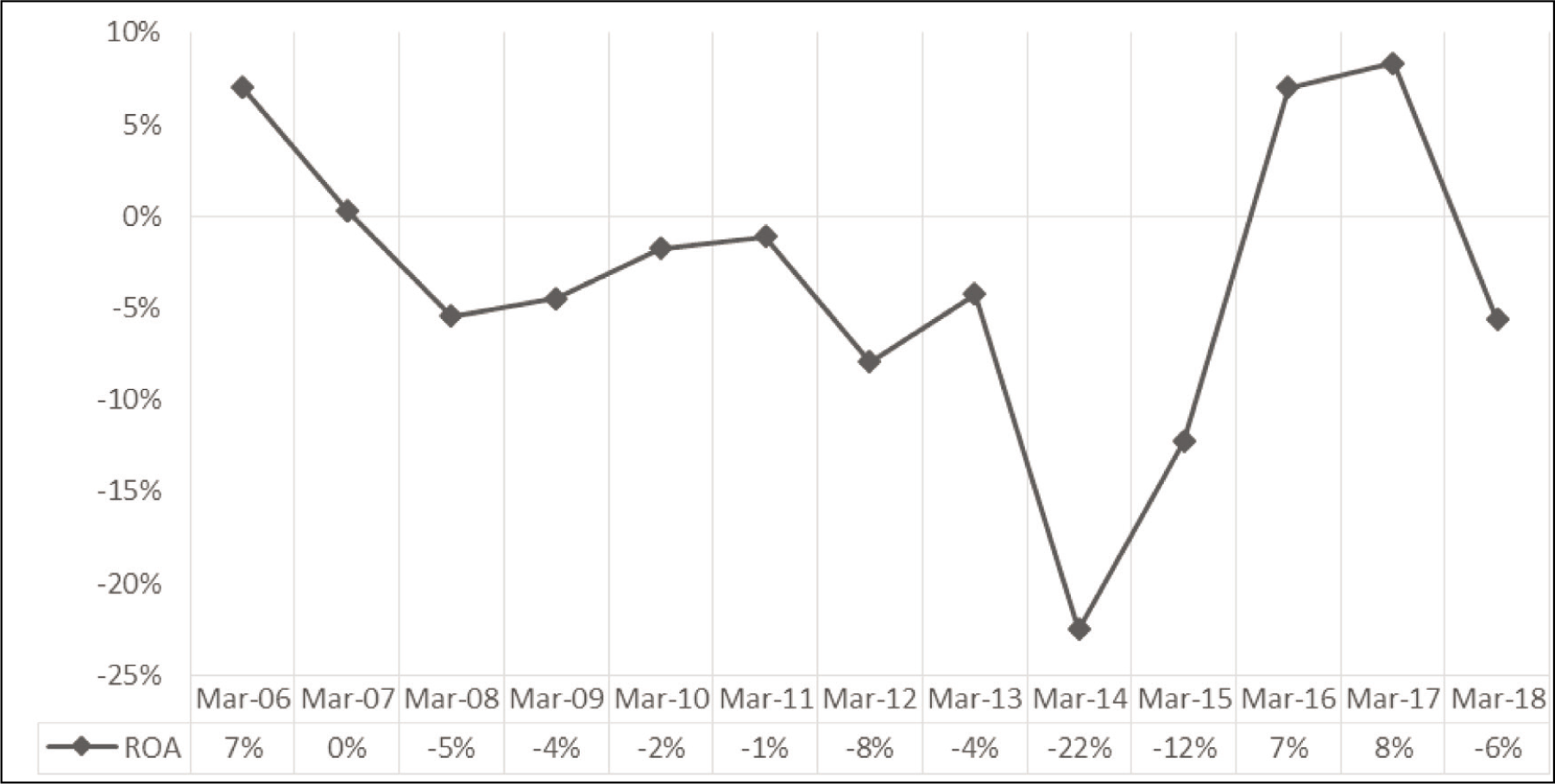

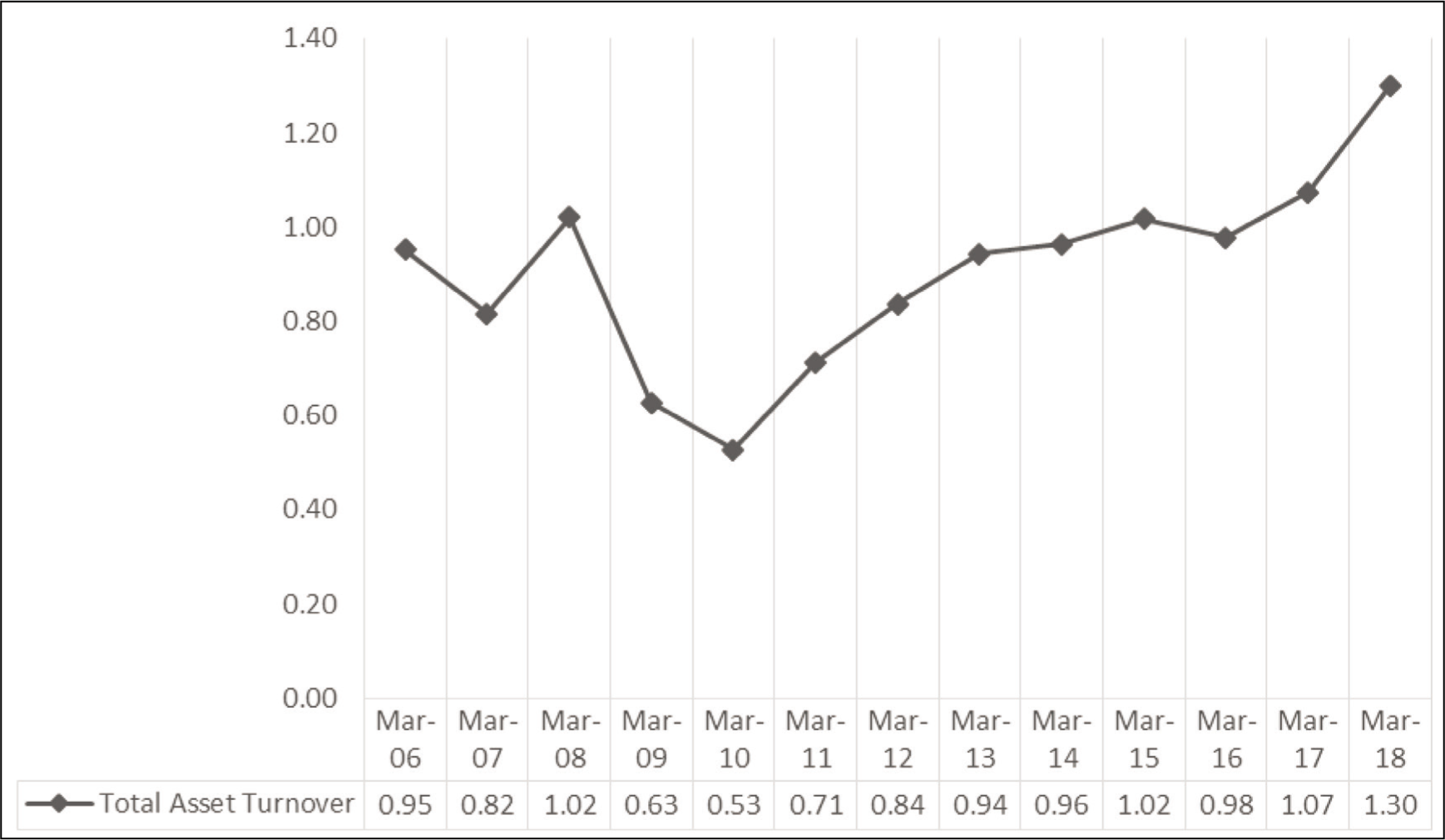

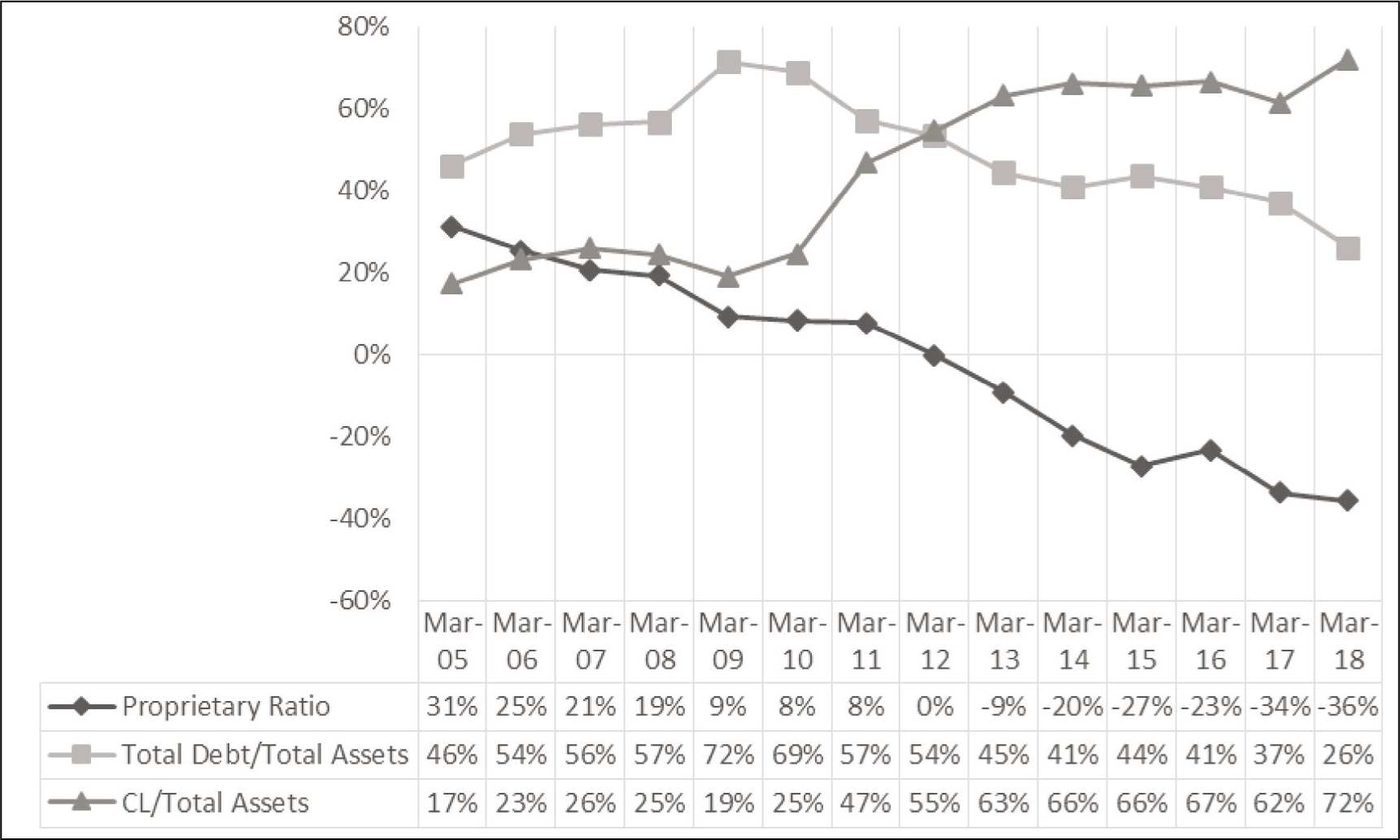

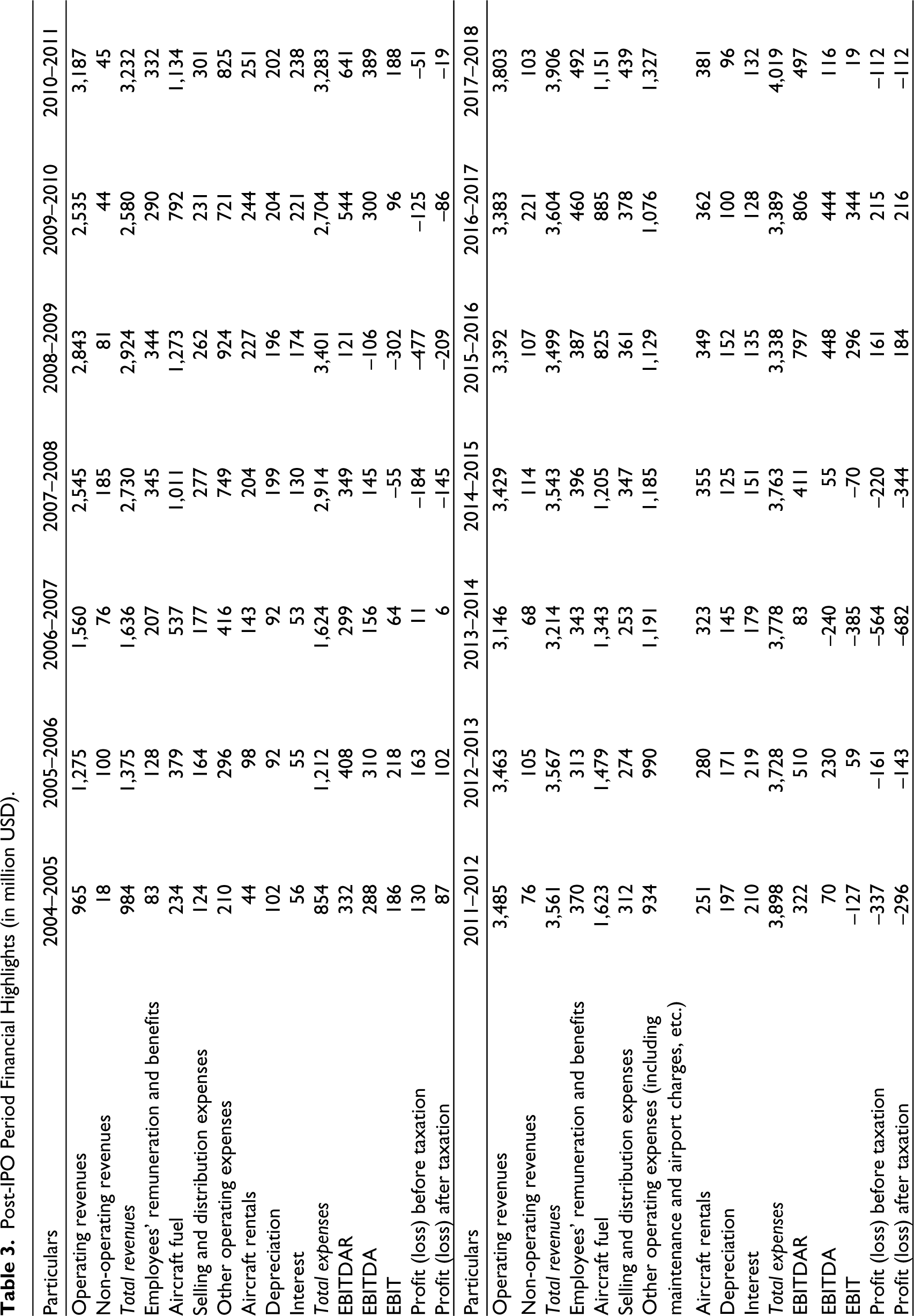

3. What are your key observations about the post-initial public offering (post-IPO) financial performance of Jet Airways based on your interpretation of Figures 2–7 in consideration of Table 3? You are required to make individual comments for each figure.

4. From a potential investor’s perspective, perform SWOT (Strengths, Weaknesses, Opportunities and Threats) analysis for Jet Airways.

5. I. Summarize the pros and cons of each of the four alternatives suggested for bailing out Jet Airways after it temporarily ceased its operations.

II. As a consultant to the lenders, considering all the relevant aspects, which alternative would you suggest to be the best? Justify your opinion.

Introduction

It was the morning of 17 June 2019, probably one of the most critical days in the history of Jet Airways had arrived. The time had come for the generation of people, who saw Jet rise to the pinnacle of India’s airline industry, to face the ground reality of Jet’s decaying financial situation. All the bankers of Jet Airways had gathered for a consortium meeting led by the State Bank of India (SBI) 1 . The fate of 20,000 plus employees and a lot of stakeholders were to be decided that day.

The airline had already temporarily ceased its operations in April 2019 on account of the lack of funding available to sustain it. Since March 2018, the share price of Jet Airways declined by more than 85%. The lenders had to collectively choose whether to find a way to revive Jet Airways operations or declare the airline ‘bankrupt’.

Period-wise Analysis of Jet Airways

Jet Airways witnessed a slow and painful descent from being India’s largest airline in 2010 (based on market share) to cease its operations in 2019. As per the Directorate General of Civil Aviation (DGCA) 2 report in 2018, Jet Airways was still the second largest airline in India with around 15% share in the domestic market (Directorate General of Civil Aviation, 2018). The company posted net losses for seven years out of the last nine financial years in the annual report. When the consortium lenders and many other industry experts decided to look back at Jet’s journey, some questions naturally popped up in everyone’s mind, like ‘What went so terribly wrong over the years? Did it happen due to financial mismanagement? Was it a corporate governance issue? Or was it the competition in the Indian airline industry that Jet could not handle?’ A simple answer would be a combined effect of all those things and many others (Arora & Ravi, 2019). However, for the consortium, the simple answer was not going to be sufficient. They needed to conduct a more detailed study to analyse major problem areas and understand what could make Jet fly again.

Privatization of Airlines in India [Before 1993–1994]

In 1953, eight domestic airlines from India were merged and nationalized under the Air Corporation Act, 1953 and since then, for almost four decades, the airline industry of India was dominated by a single player, ‘Indian Airlines’. In 1992, the ‘Open Skies Policy’ was announced as a part of liberalization reforms that challenged the dominance of the public sector. This allowed private airlines to begin their airline services in India. The privatization was to boost economic efficiency, promote the enterprise culture and enhance the tourism sector in India by offering foreign tourists more choices to travel to India.

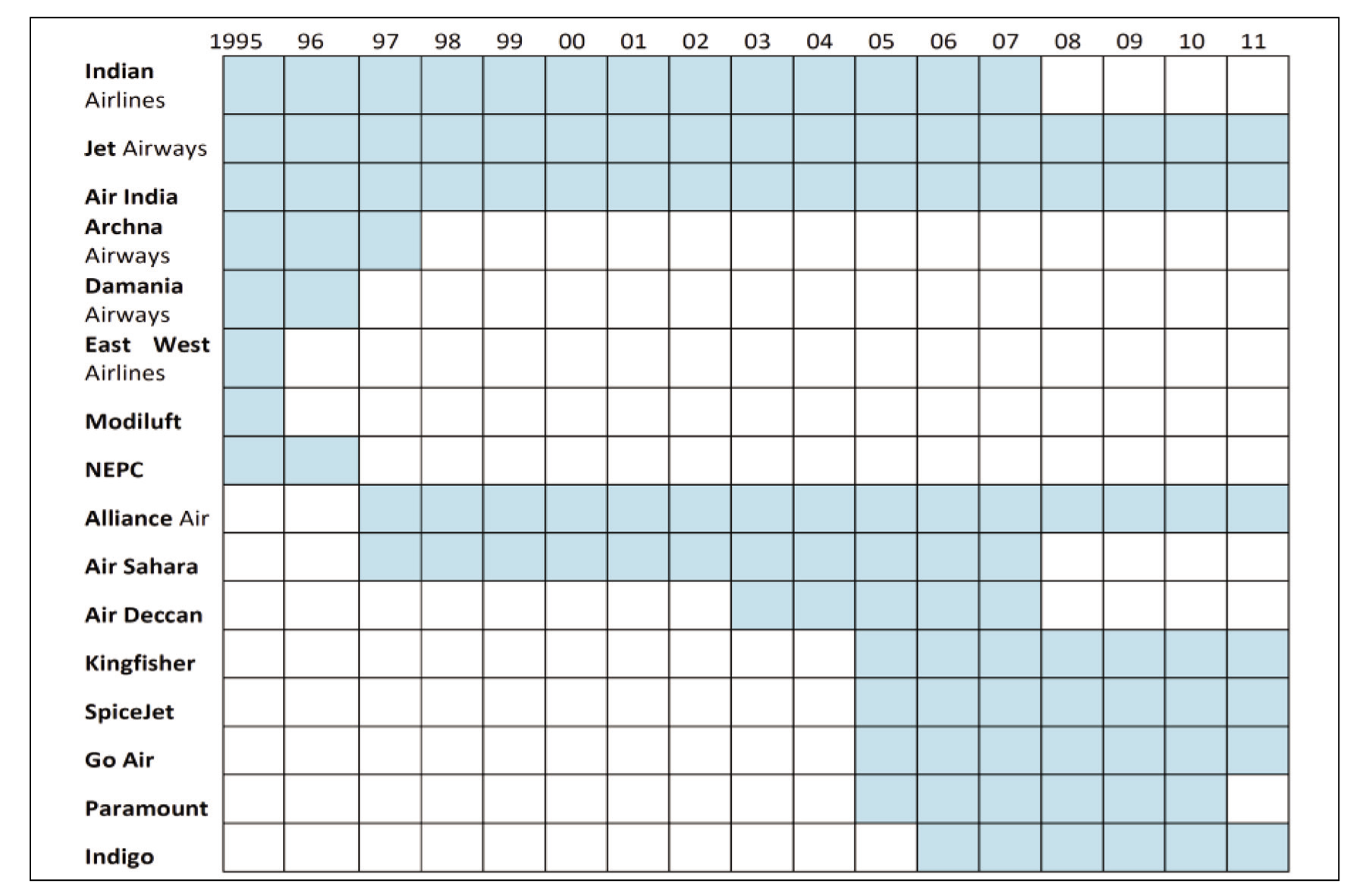

Such economic reforms enabled private players like Damania Airways, ModiLuft, East-West Airlines, Archana Airways, Natural Energy Processing Company Limited (NEPC) Airlines, Air Sahara and Jet Airways to enter the Indian airline industry. As a part of the ‘Open Skies Policy’, these private players had the freedom to decide their own schedules, services and fares. On account of this, the airline sector in India experienced significant growth in the number of air passengers from 13.8 million in 1990–1991 to 21.6 million in 1995–1996 (Ministry of Civil Aviation, 2012) 3 . However, due to challenges of high operating costs and fierce competition from the domestic as well as foreign carriers, Indian Airlines, which earned profits worth USD 25.5 million in 1990–1991, had to suffer losses worth USD 82.57 million in 1993–1994 (Mazumdar, 2009). Furthermore, the industry compressed soon (see Figure 1), as private players like East-West Airlines, ModiLuft, Archana Airways, Damania Airways and NEPC Airlines had to shut their operations within the next few years (Verma, 2019). This effectively indicated that financing to the airline industry had always been a high-risk proposition from the point of view of lenders.

The Take-off (1993–1994 to 1998–1999)

‘Naresh, if you cannot make Jet Airways better than the best, then send these two aircrafts back today’, these were the words of JRD Tata, the ‘Father of Indian Aviation’ while passing on the baton to Naresh Goyal. Jet’s first two aircrafts arrived on 18 April 1993, which JRD received at Goyal’s request (Saran & Mehra, 2012). In the years since those words of wisdom were spoken, Goyal and Jet Airways had lived up to the exceptionally high standards set by JRD Tata. Jet Airways started off aggressively by ordering 10 aircraft in 1996, and by the end of the financial year 1996–1997, Jet had a market share of 20%, which was only second to the government-owned Indian Airlines. By June 1999, Jet Airways was handling approximately 195 flights daily at around 37 destinations in India; hence, Jet decided to expand its fleet size 4 by adding 10 Boeing 5 737–800 aircrafts 6 (Cummins, 2019).

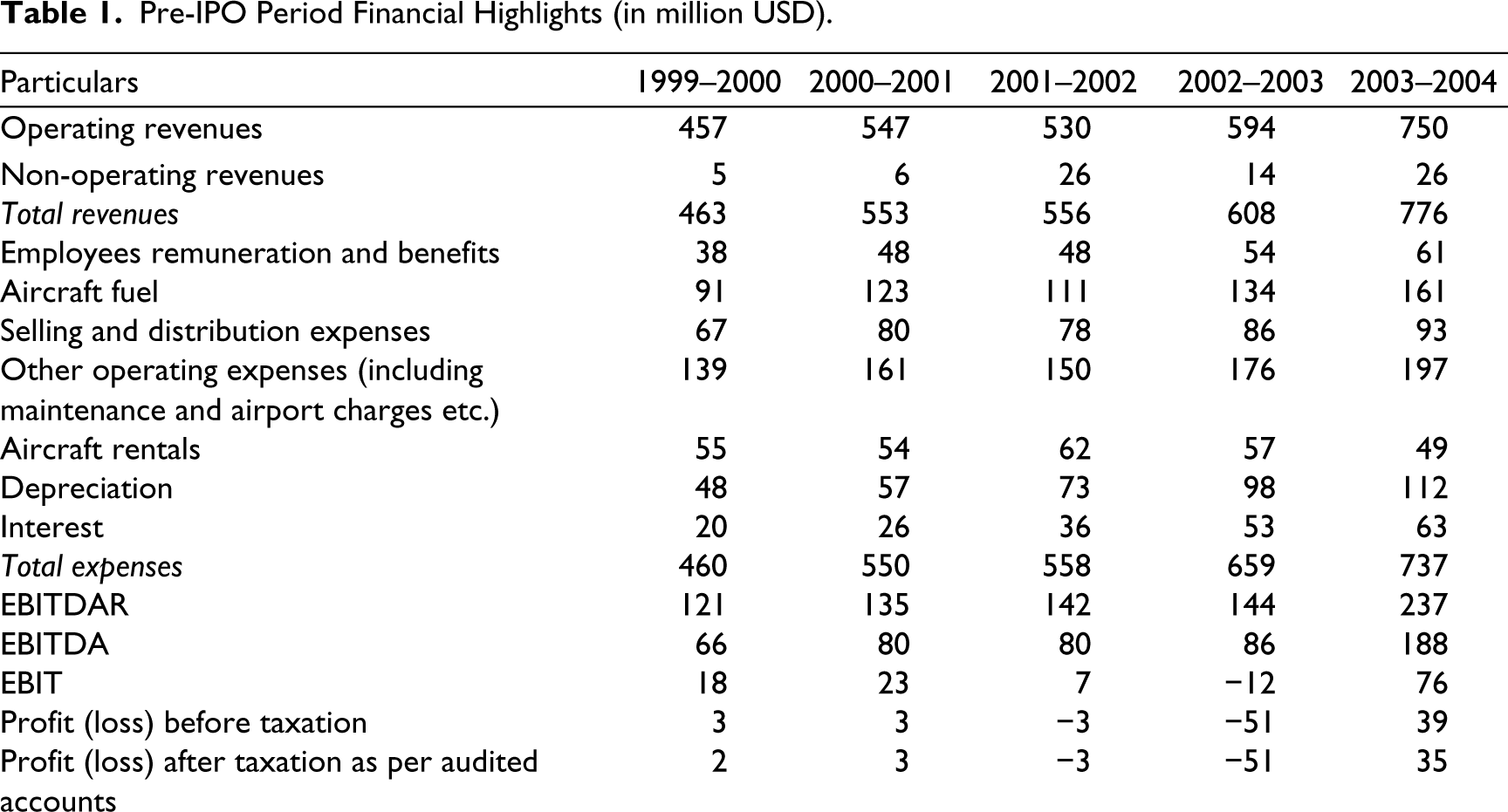

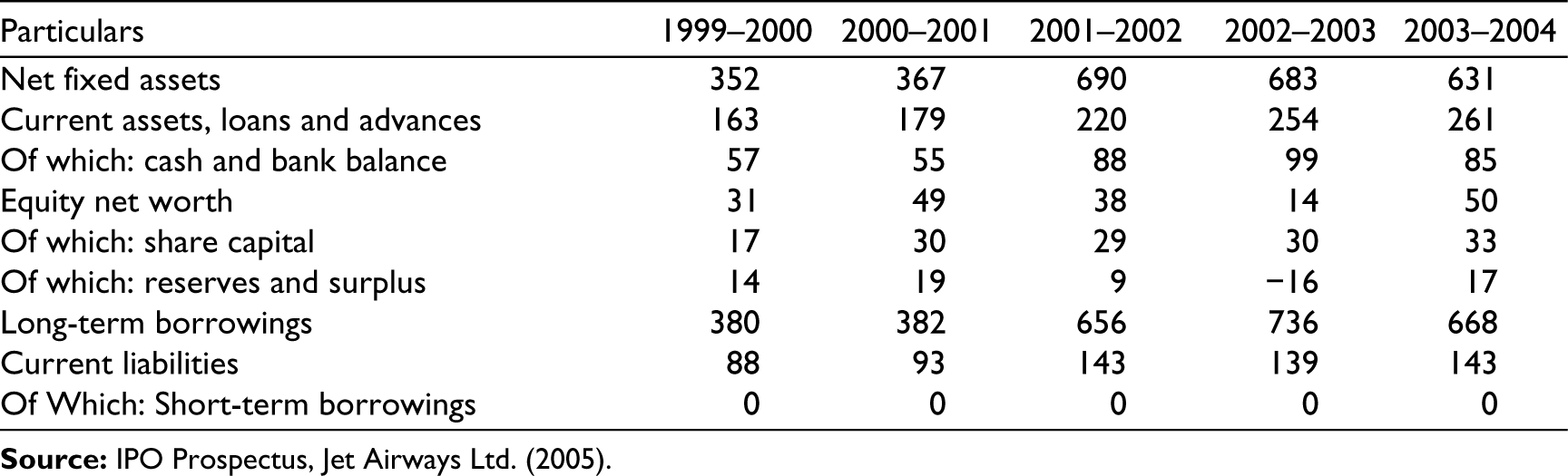

Pre-Initial Public Offering Period: Growing the Top Line (1999–2000 to 2003–2004)

As experienced in the 1990s, Jet Airways’ scale of operations and revenues continued to expand extensively. However, the profitability margins were starting to become a slight concern. Before Jet announced its IPO, it had highly fluctuating net profit margins (see Table 1). Such fluctuations were not uncommon in the initial stage of the business cycle, especially for an airline. However, in the years ahead, the Indian airline industry saw a paradigm shift with the entry of low-cost carriers (LCCs) 7 .

Pre-IPO Period Financial Highlights (in million USD).

Post-Initial Public Offering Period: The Turbulence Ahead (2004–2005 to 2006–2007)

The genuine progress of domestic players, especially private airlines, was witnessed during this period; LCCs were a game-changer. First among the list was Air Deccan, followed by SpiceJet 8 , Go Air and IndiGo 9 . However, Jet’s management considered them as ‘Fringe’ players and underestimated the competition (Verma, 2019).

During the same period, ‘Kingfisher Airlines’ (KFA) took a different approach and launched luxury carrier services, including costly wine, quality meals and the finest entertainment facilities even for domestic, short-distance flights. KFA started operations in 2005 and became a direct competitor of Jet in the full-service business. SpiceJet and Indigo, the LCCs, who commenced their operations in 2005 and 2006, respectively, also started to pick up some market shares due to their productive efficiency (Jain & Natarajan, 2015). The LCCs were able to offer cheaper services on account of fewer facilities offered to their customers. Additionally, low marketing expenses, savings on distribution costs and reduced training expenses enabled them to operate competitively (Goel & Shukla, 2004). Gradually, it became difficult for Jet to protect its market shares, and Jet’s management had no choice but to take the competition seriously.

Acquisition of Air Sahara and Its Impacts (2007–2008 to 2010–2011)

In 2004, all LCCs together had a combined market share of 5%, and by 2009, that figure was close to a substantial 63.3% (Ministry of Civil Aviation, 2012). With the rising competition from LCCs, Jet Airways needed to do something quickly before things got out of hand.

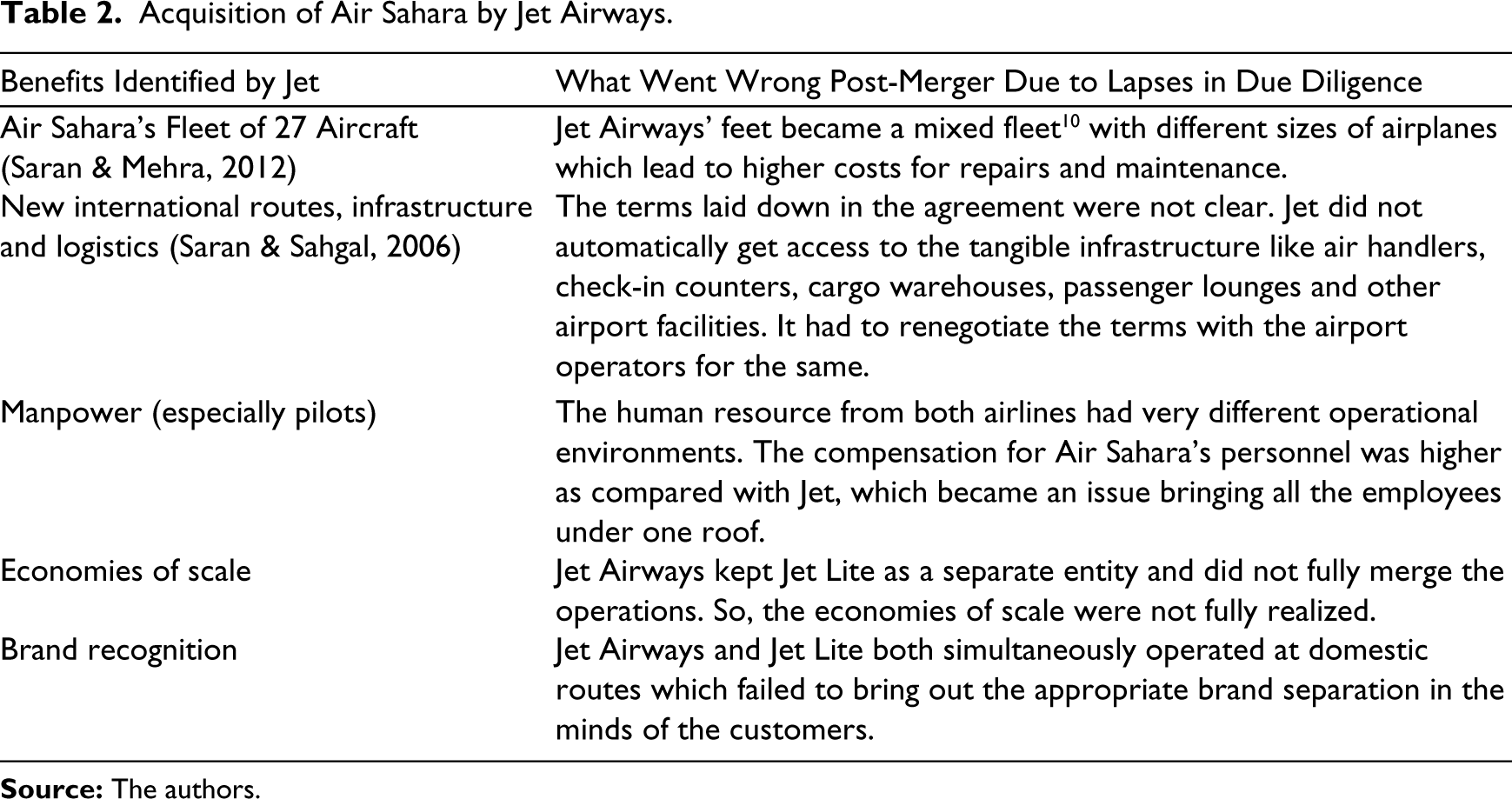

The top management of Jet decided to enter the low-cost airline market by acquiring Air Sahara. The deal, though made with the correct intentions, failed to bring out the appropriate outcome. The post-acquisition market share of Jet Airways was estimated to be 42%. Jet Airways acquired Air Sahara on 12 April 2007, for a total valuation of approximately USD 332.61 million (Ghosh, 2018). Air Sahara was renamed ‘Jet Lite’ and kept operating as a wholly owned subsidiary of Jet Airways.

The valuation of Air Sahara was considered as ‘significant overvaluation’ by many experts from the industry (Dalal, 2006; Livemint, 2019a). At the time of the acquisition, Air Sahara already had accumulated losses of around USD 160.57 million (Mahalakshmi, 2013). Besides, the amount was payable in cash, financed from additional borrowings, increasing Jet’s high leverage. Furthermore, there were a lot of possible lapses in the due diligence carried out by the Jet’s management which cost them dearly in the years to come (see Table 2).

Acquisition of Air Sahara by Jet Airways.

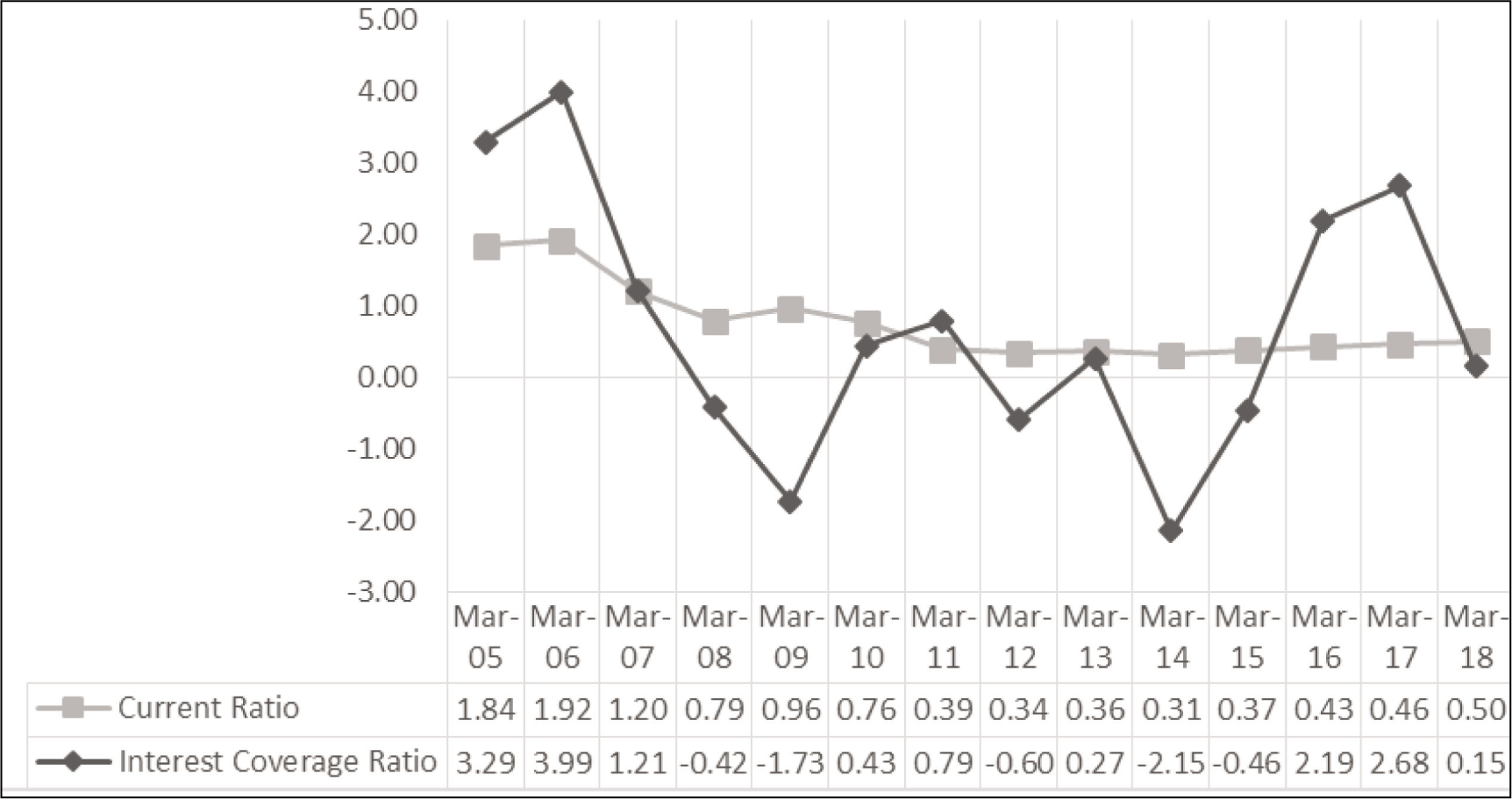

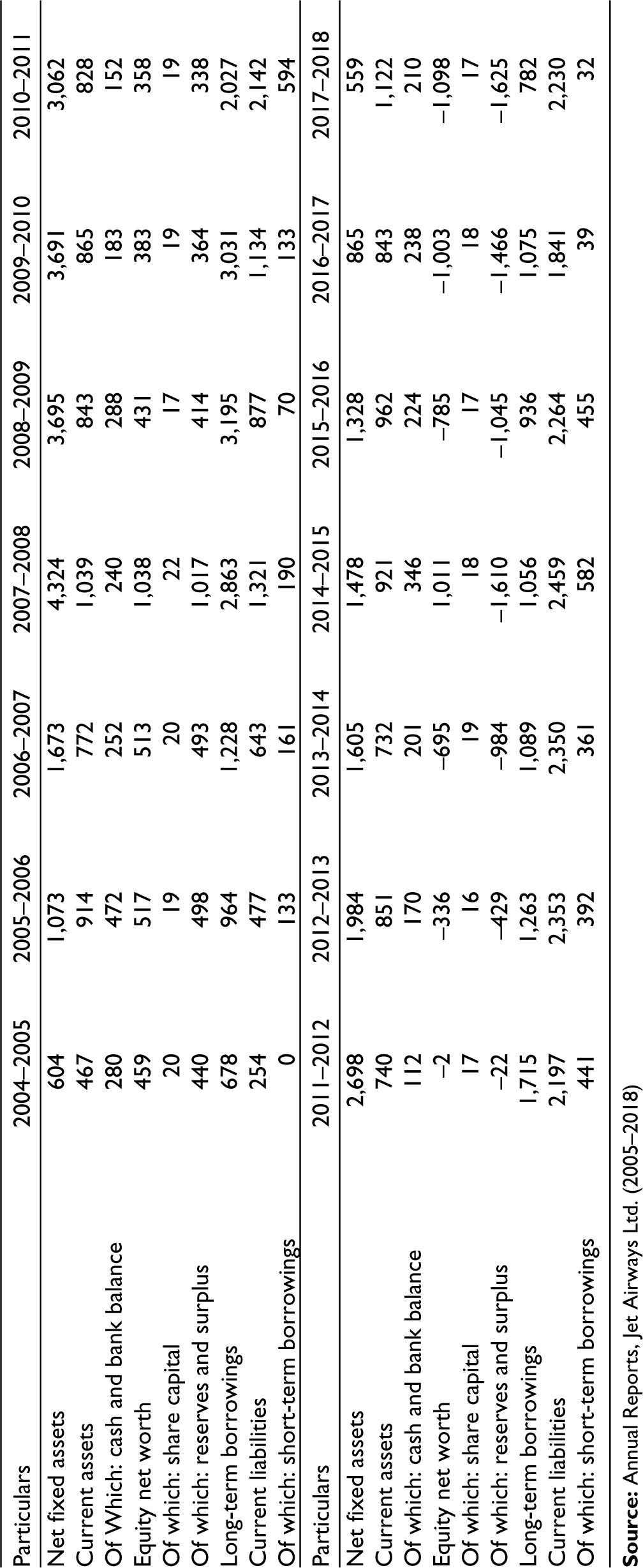

Jet’s financial solvency was adversely affected during this period (see Figures 2–6 and Table 3), and the bankruptcy risk was starting to appear (Shirur, 2013). This was because of the failed acquisition of Air Sahara and other operational issues in the competitive industry (Jet Airways Ltd., 2005–2018). When the lenders decided to look back over this period, they realized that the true concern for Jet was not the revenues, but the core problem resided in very low and fluctuating profit margins.

The Continued Operational Woes (2011–2012 to 2014–2015)

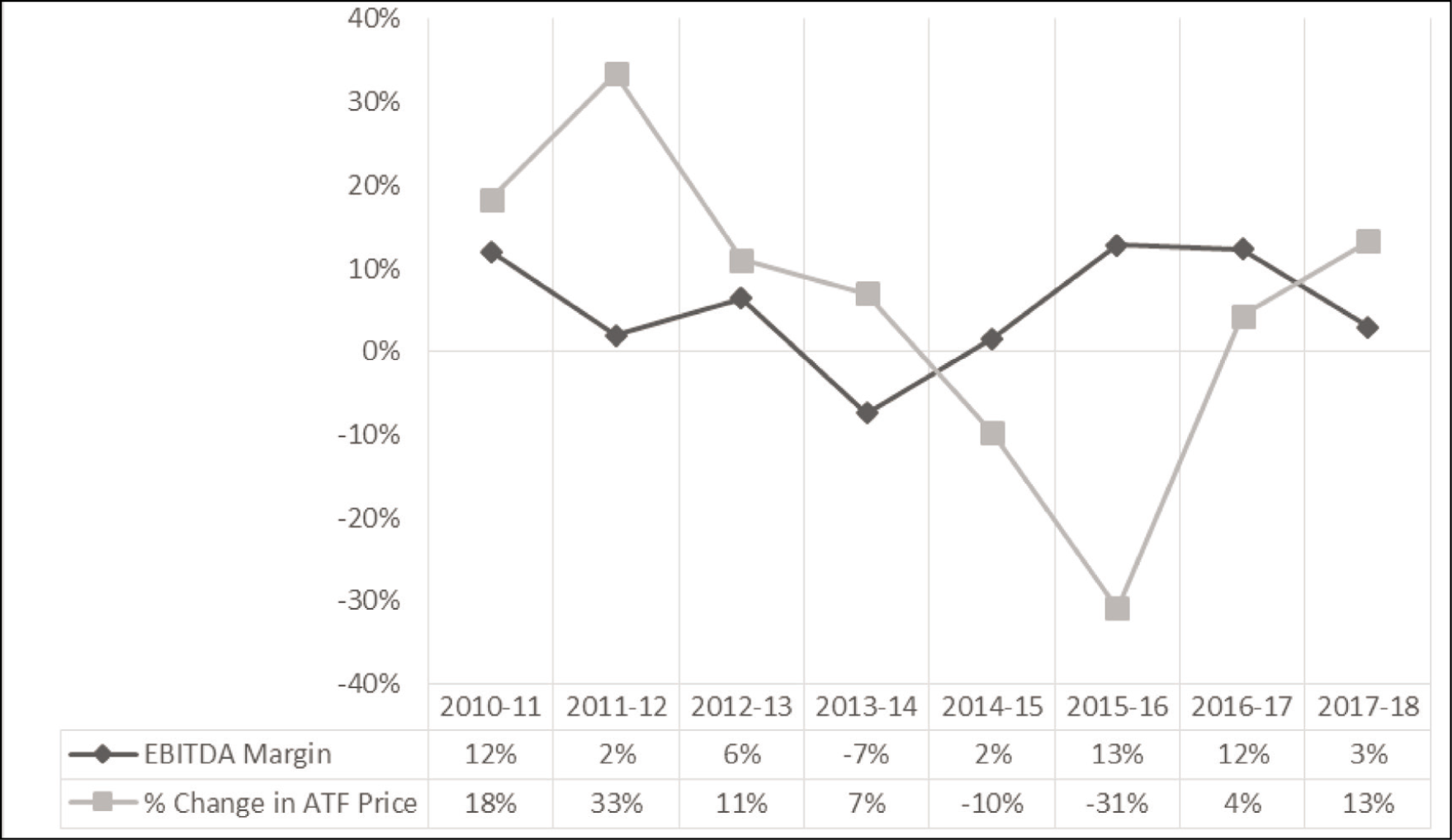

The uncertainty of the aviation turbine fuel (ATF) 11 prices created a lot of volatility in the cost structure of the airlines (Shunmugam, 2017), and Jet was no exception to this. On average, ATF cost as a percentage of total revenues ranged from 30% to 40%. Ideally, hedging was one of the methods to mitigate the risk of volatility. However, Jet never had the policy to hedge ATF price risk (Jet Airways Ltd., 2019); hence, any adverse movement in the ATF prices significantly impacted Jet’s margins (see Figure 7). Jet’s major issue during this period was that the high investments made in the earlier periods failed to generate the necessary revenue growth.

In 2013, Etihad Airways 12 picked up a 24% stake in Jet Airways for USD 379 million from promoters (Phadnis, 2018). Jet lowered its long-term borrowings during this period by selling fixed assets and used the proceeds to lower the debt. Shareholders welcomed this effort to increase the proportion of equity in the capital structure. However, the constant cash losses in operations limited the company’s effort of reducing the debt. The company started funding through short-term liabilities to reduce the long-term debt (see Figure 5 and Table 3).

Post-IPO Period Financial Highlights (in million USD).

The Losing Fight for Existence (2015–2016 Onwards)

A significant reduction in ATF prices finally halted Jet Airways’ loss-making streak of eight years during the FY 2015–2016 and FY 2016–2017 (see Figure 7). However, Jet’s positive performance based on this favourable external factor did not last long. The long-lasting problems in the operational model and cash flow issues started to appear again when the ATF prices rose in FY 2017–2018.

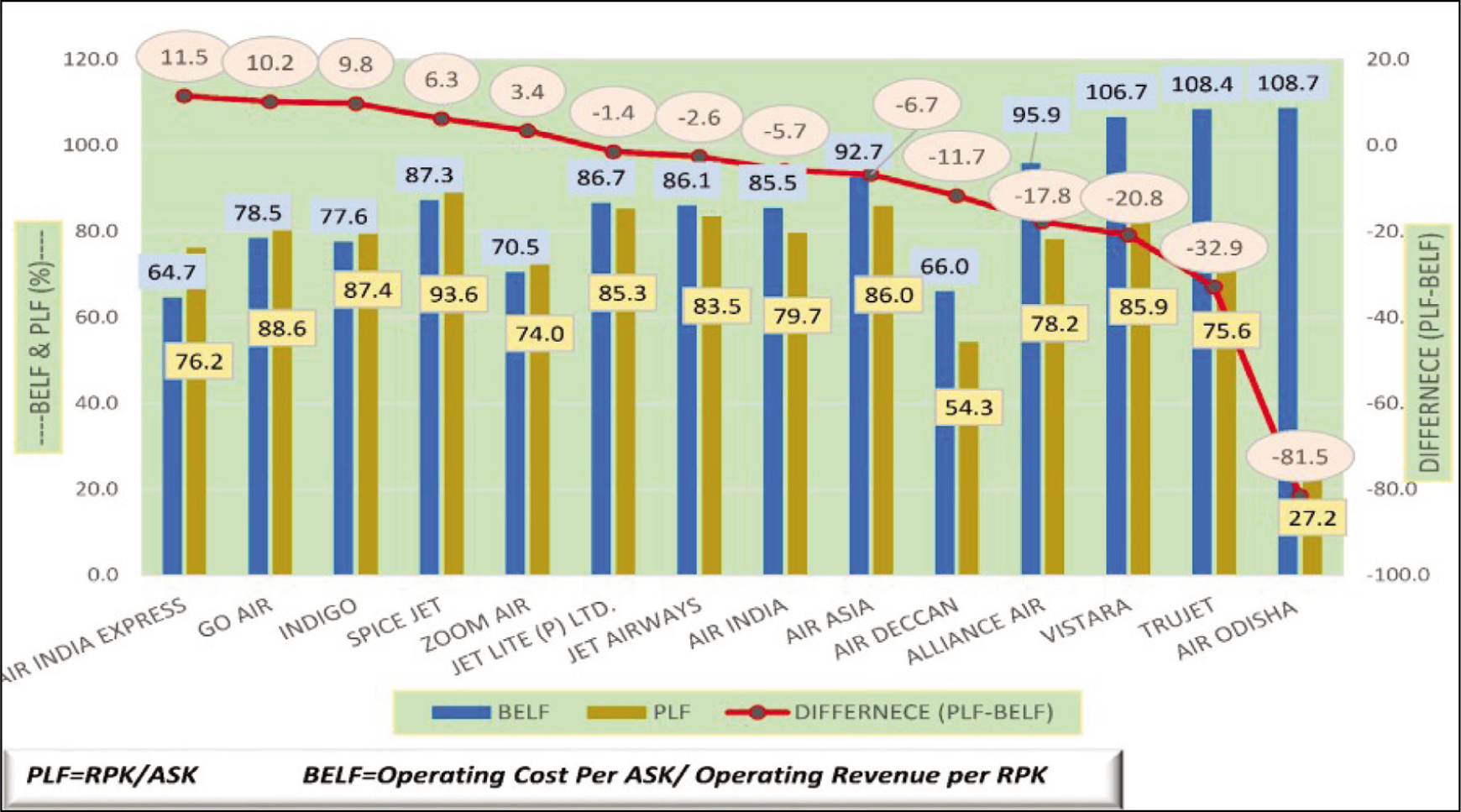

The company effectively failed to raise any further short- or long-term funding, and it became eminent that the questions would be raised about the company’s solvency. Jet Airways had a breakeven load factor (BELF) 13 of 86.1%, and its passenger load factor (PLF) 14 was only 83.5%. Hence, there was a negative gap of 2.6% (see Figure 8). A lower PLF as compared with BLFF meant that the company would have operational losses. By November 2018, the company’s outlook started to look negative, with the company defaulting on its loan instalments.

On account of all these issues, Jet was indeed struggling for its survival. Initially, Jet defaulted on its loan repayment to the domestic lenders in December 2018; then, in March 2019, it missed a bond interest payment and repayment of external commercial borrowing (ECB). The situation aggravated with Jet not being able to pay its operating creditors and salaries of its own employees (Ghosh & Chowdhury, 2019). By this time, Jet was flying only a few of its 112 aircrafts, and the rest were grounded temporarily.

Corporate Governance Issues in Jet Airways

Behind Jet’s financial failure, possibly, a few corporate governance issues remained in the shadows. It was important for the consortium lenders to find the issues, if present, and sort them out on a priority basis before even thinking about ways to bail out Jet. Over the years, Jet’s Board of Directors panel seemed like a promoter-led board, with Naresh Goyal making most of the decisions. Some of the issues which came into the limelight through the public domain were as follows:

While acquiring Air Sahara, Naresh Goyal ignored the advice of professional associates who told him that Jet was paying a lot more than what Air Sahara was worth. Industry experts also raised questions when Goyal decided to have a single management team lead by himself for both Jet Airways (a full-service business) and Air Sahara (a low-cost business). Experts believed that two separate teams should have managed the two separate types of businesses. Jet was very successful with a narrow-bodied fleet

16

; however, it gradually created a mixed fleet by adding wide-bodied aircraft

17

(Financial Express, 2019). Having a mixed fleet meant that the maintenance costs would be relatively high. Additionally, Goyal decided to configure wide- bodied planes incorporating only 308 seats, whereas the global standard was 400 seats. Effectively, Jet was losing one-fourth of potential revenue. When this was happening, Jet’s Commerce Chief Sudheer Raghavan and Chief Executive Officer (CEO) Nikos Kardassis tried to advise Goyal, but he was adamant (Chowdhury & Mishra, 2019a). In August 2018, Jet deferred its announcement of April–June quarter results on account of the audit committee not recommending the financial results to the Board of Directors pending closure of certain matters. The Bombay Stock Exchange (BSE)

18

sought clarification as the information provided by the Jet to the exchange lacked some details (Economic Times, 2018). In November 2018, two independent directors of Jet, Vikram Mehta and Ranjan Mathai, resigned from the board. Both cited the reason that there was an increase in workload from their other commitments and the inability to devote time to Jet (Chowdhury, 2018; The Hindu Business Line, 2018). This was around the time when Jet was facing liquidity issues and was negotiating a possible equity infusion by Tata Sons (Chatterjee, 2018). Jet was struggling to raise any short- or long-term funding towards the end of 2018; hence, Jet offered discounted forward bookings intending to fill its planes. CEO Vinay Dube, at that time, opposed this idea, saying that such a move was not financially viable for a full-service carrier already burdened by losses. However, Naresh and Anita Goyal disregarded his objection (Chowdhury & Mishra, 2019a).

Similarities with Failure of Kingfisher Airlines

For the consortium lenders, especially for SBI, the temporary shutdown of Jet was like a ‘deja-vu’. Not so long ago, the bank had seen the fall of one of its most infamous borrowers, Kingfisher Airlines (owed around USD 241 million to SBI out of USD 1,370 million payable to 17 banks). Broadly, KFA suffered various structural, operational and strategic problems like faulty aircraft leasing systems, rising operational costs and lack of clear business strategy (Sulphey, 2020). Looking back at the journey of both airlines, a lot of similarities could be drawn between the reasons for the failure of Jet and KFA.

Full-service business model: Both Jet and KFA were full-service airlines providing premium services to customers. However, a lack of control on the operating expenses coupled with price-sensitive Indian customers made it difficult for the airlines to have stable profit margins. Unlike Jet, KFA could not generate profit even for a single financial year (Kaul, 2012). On the other hand, the LCC model adopted by many airlines was based on controlling operational costs. As a part of this model, LCCs used to implement strategies like higher utilization rate of its aircraft, converting some of its fixed costs to variable costs and rent or subcontract some of the business activities (Ahmad, 2010).

High leverage: The businesses of both airlines were highly levered, but the investments they made out of those borrowed funds could not generate the expected returns. Eventually, the cash flow pressure of debt repayments started backfiring (Sharma, 2019).

Failed acquisitions: In 2007, KFA acquired ‘Air Deccan’, which was a loss-making LCC. However, KFA failed to conduct proper due diligence and ended up with the burden of additional losses. Later, KFA tried to rebrand ‘Air Deccan’ as ‘Kingfisher Red’, but could not get it to run as planned and eventually closed its operations in 2011. The failed acquisition case was very similar to Jet’s unsuccessful acquisition of Air Sahara (Das & Kalesh, 2011).

Possible corporate governance issues: Throughout their entire journey, the management of both airlines made questionable strategic decisions (Panigrahi et al., 2019), highlighting the possibility of corporate governance issues (Vikraman, 2017).

External Industry Challenges

With Jet on the path to become another KFA, it was time for the consortium lenders to start looking at the bigger picture, the Indian airline industry. In addition to the internal problems faced by Jet, the external business environment in India at that time was not at all conducive. Not just Jet, almost all the other airlines barring a few, were struggling to make profits. Air India, one of the oldest and largest players in the Indian airline industry, had been struggling to operate profitably for many years. It also faced intense competition, fluctuating profit margins, high debt and other operational issues. Considering these challenges, the government authorities attempted divestment in Air India in 2018; however, it did not receive any bids from potential investors (Agarwal & Reddy, 2020).

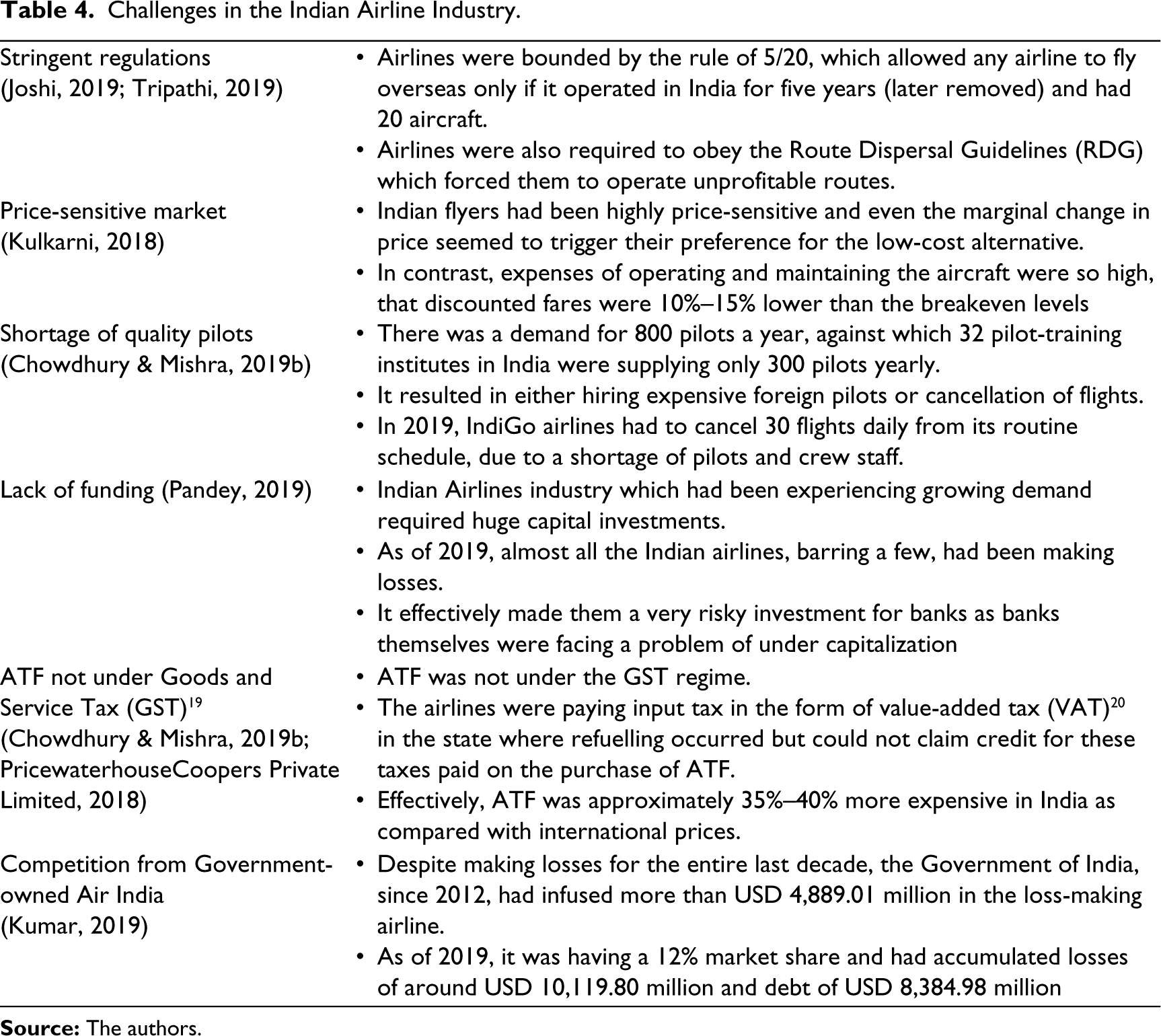

In 2019, the CEO of Interglobe Aviation (IndiGo) Ronojoy Dutta, in one of his interviews, said that: ‘The airline is a very unforgiving industry and there are many paths to failure, only a few paths to success’ (Financial Express, 2019). Indeed, there had been a lot of problems in the highly competitive Indian airline industry, which had indirectly made the revival of Jet Airways a lot more complicated (see Table 4). The consortium lenders had to consider these industry challenges in any discussion revolving around a turnaround possibility and bailout.

Challenges in the Indian Airline Industry.

Plan for a Bailout

Based on a consultation with the consortium of lenders, an Extraordinary General Meeting (EGM) of Jet Airways was held in February 2019, in which a bailout plan was identified. A total funding gap of USD 1,228.83 million was supposed to be raised through a combination of debt restructuring, equity infusion, and sale and leaseback mechanisms (Kundu, 2019a). By the mid of March 2019, Jet was flying only five planes and was desperately seeking emergency funding of USD 57.83 million from the consortium (Economic Times, 2019b).

Debt Restructuring

When Jet’s management was seeking emergency funding from lenders, SBI Chairman at that time, Rajnish Kumar, made the following statement in March 2019, ‘SBI’s desire is that the airline keeps on running. The bank-led effort is to see that the resolution plan happens … it should not take a month … in the next one week, you should have something’ (Rebello, 2019). The talks of finding a restructuring plan had already started, and as part of it, both Naresh and Anita Goyal stepped down from their respective positions on the board of Jet (Economic Times, 2019a).

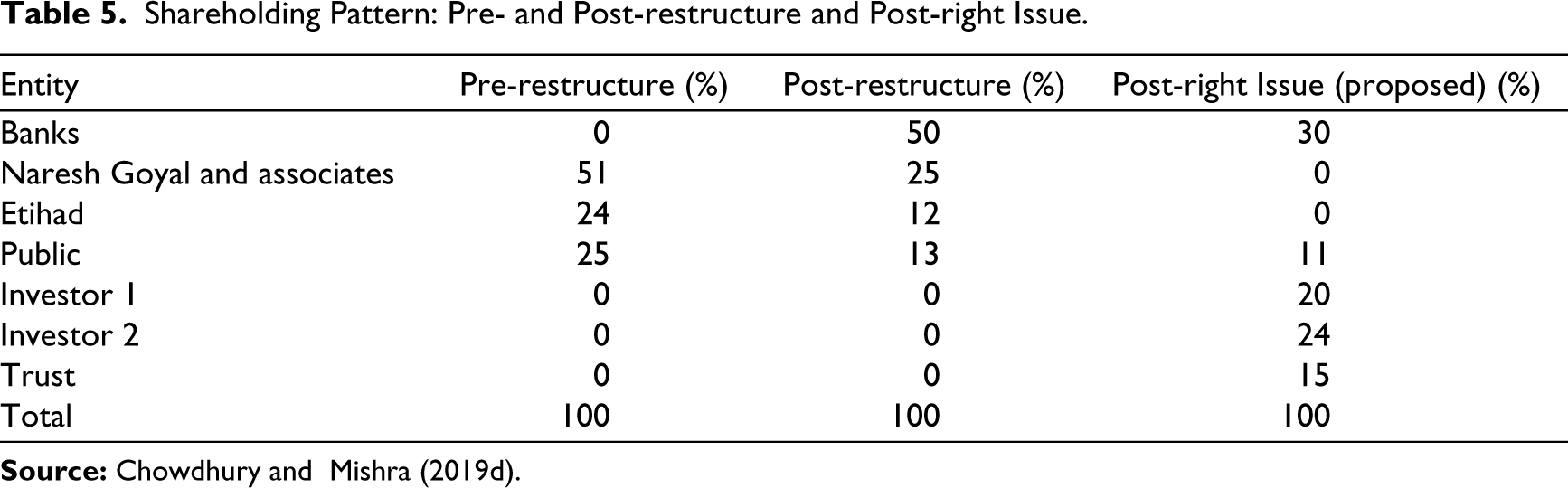

Jet owed a total debt of USD 1,156.55 million to all the consortium banks led by SBI. The plan was to convert some of the debt from lenders to equity shares in such a way that the consortium would effectively have a controlling interest in Jet Airways. Subsequently, the same could be offered to interested strategic investors (see Table 5).

Shareholding Pattern: Pre- and Post-restructure and Post-right Issue.

The debt restructuring plan was to convert a part of the debt into 114 million equity shares by paying a token of USD 0.01 based on Reserve Bank of India’s (RBI) 21 circular (dated 12 February 2019) ‘Prudential Framework for Resolution of Stressed Assets’ 22 (Reserve Bank of India, 2019).

The critical step in the plan was for Naresh Goyal to relinquish his control over Jet and pledge his equity shares with the lenders. It was also decided that the lender will further infuse USD 216.85 million into the company via debt instruments against Goyal pledging his shares. In accordance with this, in April 2019, over 57.9 million held by him were released and kept under ‘non-disposal undertaking’ as security against borrowings. The debt restructuring was completed, and subsequently, the lenders had the following alternatives.

Alternatives with the Lenders

Alternative 1: Right Issue

The lenders were considering the ‘Right Issue’ as an alternative. Under this proposal, Jet would raise USD 216.85 million through equity infusion by two new investors. National Investment and Infrastructure Fund (NIIF) 23 was likely to be one of them. Existing shareholders (post-restructure) would renounce a portion of their rights to the new investors, and the balance shareholding of Etihad and Goyal would be transferred to a trust managed by the lenders with a call option on the trusts’ shares (see Table 5). The call option was exercisable at a strike price of USD 2.17 per share plus 8% per annum carry. Any revenue generated from the sale of shares or exercising the call option would be passed on to Goyal and Etihad. As part of the plan, the domestic lender had to take a haircut of USD 375.88 million, and foreign lenders had to take a haircut of USD 169.15 million.

Alternative 2: Approaching Strategic Investors

SBI released an ‘Expression of Interest (EOI) 24 ’ on behalf of Jet Airways to invite bids from various strategic and financial investors. The EOI offered between 31.2 and 75% stake of Jet Airways for investment purposes. By the mid of April 2019, five entities had submitted EOI and the offer seemed to have generated some interest among investors.

Though the plan was set, there were a few hurdles in the way. The first hurdle came from ‘The Supreme Court of India’ (SC) 25 scrapping ‘Resolution of Stressed Assets’, a circular by RBI published on 12 February 2019. The debt restructuring, which was completed earlier, was based on the guideline from this circular. However, the SC called it ‘Against Constitution’. Though the already executed bailout plan of Jet Airways was not to be impacted much due to SC’s decision (Adhikari, 2019), the news did create some confusion and delay in the sale process (Majumdar, 2019).

On 17 April 2019, Jet Airways decided to temporarily cease its operations as lenders’ consortium, led by SBI, rejected the plea for emergency funds. Jet’s flight slots at various airports (a total of 440 slots) were temporarily allocated to the other carriers in the industry (Sinha, 2019). The temporary shutdown made the situation worse for potential investors as Jet was no longer generating cash flows from operations, and the share price was steadily falling (The Hindu Business Line, 2019). However, the aviation ministry had clearly stated that Jet could resume its operations, the slots would be reallocated to Jet (Kundu, 2019b). The potential investors had started asking lenders for taking almost 80% on their total dues, which seemed a bit too much for the lenders to agree to (Chowdhury & Mishra, 2019c).

Alternative 3: Etihad Airways Increasing its Stake

While the debt restructuring plan was being chalked up at the start of 2019, Etihad Airways was supposed to provide funds once the debt of the consortium lenders was converted to equity. It was supposed to infuse USD 231.31–274.68 million. The issue was that Etihad had valued Jet’s share at a fair valuation of USD 2.02–2.17, which was well below the prevailing market price at that time. It was also asked to offer an emergency funding of ₹108.43 million to Jet Airways, which the lenders would match. Etihad had refused to comply with this condition (Economic Times, 2019a) and had further stated that there was no intention to increase the investment in Jet while the right issue plan was being designed. It was ready to renounce the rights and was not keen to invest as long as Goyal controlled Jet Airways (Chowdhury & Mishra, 2019a).

Things took a turn when Naresh Goyal stepped down from Jet Airways. Towards the end of April 2019, lenders had resumed negotiations with Etihad, and it was one of the five entities to submit the EOI (Choudhury, 2019). However, any negotiations with Etihad were attached with one condition to waive-off the open offer requirement as per norms laid down by the Security Exchange Board of India (SEBI) 26 . As per SEBI’s takeover code 27 , if a company was to acquire more than 25% of shares in another listed company, it had to make an open offer to the minority shareholders of the target firm for another 20% stake (Upadhyay & Kundu, 2019). Etihad was against the open offer as Etihad believed that it would be considered an exit strategy for minority shareholders rather than a tool to fetch funds for Jet (Chowdhury & Mishra, 2019c). SEBI had previously never given an exemption to any company regarding the open offer. According to the SEBI guidelines, the exemption was allowed only to banks, financial institutions or lenders that would acquire more than 25% of shares (Upadhyay, 2019).

Alternative 4: Declaring Bankruptcy

The last alternative, of course, was to declare Jet Airways as ‘Bankrupt’ under the Indian Bankruptcy Code (IBC) 28 and start the liquidation process by handing Jet over to the National Company Law Tribunal (NCLT) 29 . Once corporate insolvency resolution process (CIRP) 30 would be initiated, NCLT would appoint an interim resolution professional (IRP) 31 , a third party, which would control assets and would try to find a suitable investor within 180 days from the commencement of CIRP which could be extended by another 90 days, if required. If a resolution plan was approved and sanctioned by NCLT, it would be mandatory for Jet to accept it (The Ministry of Corporate Affairs, 2016) 32 . Since the inception of IBC in 2016, the NCLT resolution process had managed a recovery rate of 43% till March 2019 (Livemint, 2019b).

Jet would have to be liquidated by selling all its assets if a resolution plan was not approved within that period. Liquidation would typically result in a much lower recovery rate; historically, it had achieved only 20% recovery from assets (Gandhi, 2019).

Previous Successful Turnarounds

Considering the alternatives available with the lenders, the critical questions were ‘whether there was any turnaround possibility or not? If yes, how feasible did it look?’ The airline industry, all over the world, had seen a lot of business failures, but the industry had also seen some successful turnarounds.

In the Indian context, if the lenders wanted to have a look, there had been a successful turnaround of SpiceJet. In December 2014, SpiceJet Airlines was on the verge of closure due to a liquidity crisis. They had accumulated losses of USD 221.13 million, a debt of USD 206.32 million and short-term liabilities of over USD 332.78 million (Shukla, 2017). Its share price was close to USD 0.20 per share in December 2014. Ajay Singh took over a 58% stake in the company in January 2015 and started to sort out its problems from scratch (Ahmad, 2019). He brought in an open-door policy allowing senior officials to discuss and make decisions quickly (Mishra, 2016). Subsequently, the airline took a series of critical decisions to improve the company’s operational performance significantly.

Regaining customers’ trust: Singh focussed on improving o-time performance (OTP) and ensured that all the interfaces like websites and counters at airports were working again. It improved its OTP from 49.6 to 75% during the turnaround period.

Discontinuing unprofitable routes: SpiceJet closed five domestic and three international destinations as part of the turnaround process (Shukla, 2017).

Increasing ancillary revenues: Apart from primary operations, SpiceJet also improved its ancillary revenues. The share of ancillary revenues out of total revenues saw an increase from 7% to 17%.

Emphasis on revenues over market share: Singh stopped offering discounts on premium seats during holidays. The earlier management tried to increase the market share with this practice, but Singh realized that the adverse impact on revenues was much more worrisome.

Improved cost control: SpiceJet also increased the number of fuel-efficient planes in its fleet; it started to focus more on Boeing Max aircraft, which was expected to cut down its cost by 5%–10%. Singh also cut down on some of the human resources.

SpiceJet was one such odd example of a turnaround in the Indian airline industry. However, it was not a full-service airline. For a turnaround of a full-service airline, the lenders could look at the famous turnaround of Malaysia Airlines. Malaysia Airlines was going through the worst times in its history of five decades, as it had incurred losses worth USD 449.74 million in 2005 and was left with limited cash that could run the operations merely for three and half months. In such a complex scenario, a new CEO, Idris Jala, was appointed with the turnaround task at hand.

For Malaysia Airlines, Jala’s primary action was to improve the airline’s profit and loss (P&L) statement on a priority basis. Further, he identified that the airline was struggling with three major problems: network inefficiency, insufficient revenues and ineffective cost control. Considering these issues, the following major steps and initiatives were executed by Idris Jala:

Ensuring survival: Jala’s first bold step was selling the airline headquarters in an expensive area of downtown Kuala Lumpur, which helped the airlines raise USD 34.39 million. These funds provided the airline with an additional time of 20 more days to manage its operations. ‘Laboratories’ for improving network efficiency and enhancing revenues: Jala created teams of 10–15 people from diverse backgrounds and functions and named them ‘Laboratories’. These laboratories were made accountable for evaluating and managing the routes’ profitability and other major business functions. Within six months, various unprofitable routes were closed down. At the same time, several other routes were converted into positive contributors to the P&L. Furthermore; there were a total of 160,000 P&L, which consisted of individual P&L for every single route by day, by month and by flight number. Additionally, these laboratories also emphasized reducing costs without affecting passengers’ travel experience. Improving productivity: Jala also stressed upon ‘discipline of action’, that is, to persistently assess the outcomes and ensure it was done within the specified timeline. Additionally, around 15% of the manpower (over 3,000 employees) was separated using a mutual separation scheme, retirement scheme or contract expiry (Tiwari & Kainth, 2014). Significant cost reduction: Through a decrease in spending on fuel consumption, inflight maintenance, corporate sponsorships and manpower, a substantial cost reduction worth USD 116.67 million was achieved.

Malaysia Airlines successfully implemented its business turnaround in two years with this kind of action and outcome-oriented strategy. Initially, they had kept the target of achieving profits worth USD 151.52 million in 2008, which they overachieved in 2007, with an actual profit of USD 258.11 million (Dichter et al., 2008).

Conclusion

Throughout the journey of Jet Airways, which spanned over almost three decades, a lot of factors adversely affected their business. It can be said that improper decision-making, financial mismanagement, failed merger with Air Sahara, competition from LCCs combined with never-ending industry challenges ultimately led to the downfall of Jet Airways.

Though some strategic investors like Hinduja Group 33 (based in London) and Etihad Airways (based in Abu Dhabi) had shown some interest in taking over Jet (Ghosh, 2019), the operational creditors of Jet Airways, on the other hand, were filing cases and putting legal pressure on the consortium lenders to opt for the bankruptcy option. The pressure was slowly starting to pile up on the lenders, and it was time for them to make a choice. The decision was to be based purely on the opinion of consortium lenders on a turnaround possibility. The key question was whether any investment made in Jet Airways as part of the bailout would be financially viable or just delay the inevitable happening. It was also critical to think about how it would affect both the operational creditors and lenders.

All the stakeholders of Jet had their eyes glued to the decision that the consortium lenders were going to take that deal. The airline had already ceased its operations on account of lack of funding available to sustain, but an adverse outcome of this meeting was going to look like the last nail in the coffin for Jet Airways.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.