Abstract

Keywords

Late afternoon was slowly turning into dusk as Rajeev Singhal, Managing Director of Tata Steel BSL Limited (TSBSL) looked out of his window at the chaotic crowds jostling outside his Shakespeare Sarani, Park Street, Kolkata office. Valued at INR 1 352 billion during acquisition on 18 May 2018 2 , Bhushan Steel Limited (BSL) was renamed Tata Steel BSL Limited after Tata Steel acquired it in one the largest deals of the Indian steel making pioneer since acquiring Britain’s Corus Group Plc. in 2007. Singhal was on deputation from Tata Steel and led the team that was tasked with the goal of successfully turning around and transforming the acquired Bhushan Steel. Letting his thoughts drift, he imagined with pride how this takeover has given the parent company access to high-quality assets, a complementary product portfolio, and a presence in western India, especially in higher-margin downstream product markets. It also provided Tata Steel with an opportunity to increase the market share. All of this, a part of the long-term strategy of the group. Stepping up downstream sales was part of Tata Steel’s deft strategy to counter the vagaries of a cyclical steel business. This is the face of the steel industry, he thought to himself as he marvelled at his company’s acquisition. At the same time, Singhal knew that the acquisition of Bhushan Steel had not been entirely smooth. As per the Ministry of Corporate Affairs (MCA) notification in 2018 3 , promoters of Bhushan Steel exploited myriad complex and fraudulent manoeuvres to siphon off funds through a byzantine web of companies amounting to thousands of billions raised from public sector banks. Eventually, Bhushan Steel was among 12 non-performing assets (NPA), many of whom were from the steel sector, referred for insolvency resolution by the Reserve Bank of India in 2017. Tata Steel’s resolution plan for debt-ridden Bhushan Steel was viewed by all, including public policy planners, bankers, financial and operational creditors, as the operation test case for the newly enacted Insolvency and Bankruptcy Code (IBC). Looking forward, Singhal knew that the Tata Steel BSL team would face several challenges while moving the business and integrating it into the Tata Steel family. As he got ready for the next meeting, random questions quickly went through his mind: was the partnership love at first sight? How will the acquisition impact Tata Steel’s competitive posturing, its rapport with the widened set of stakeholders, and its financial position? Will the acquisition result in a stronger company? Will this acquisition survive the incompatibility of two cultures?

THE TATA GROUP 4

In 1868, Jamshedji Nusserwanji Tata founded the Tata Group. From its early entry into steel and automobiles, the group has evolved into a truly global conglomerate with a presence in over 100 countries across diverse industries such as technology, retail, agrochemicals, chemicals, construction, finance, consumer goods, and hospitality. Prominent public-listed companies of the group included Tata Steel, Tata Motors, Tata Consultancy Services, Tata Power, Tata Chemicals, Tata Global Beverages, Tata Teleservices, Titan, Tata Communications and Indian Hotels. Given its strong brand equity, several Tata Group companies acquired leadership positions, and its products soon became household names. Besides, through its philanthropic trusts, the group contributed significantly towards building some of the finest national institutions for science and technology, medical research, social studies and performing arts.

As of 31 March 2020, the group had a combined employee strength of over 660,800, a market capitalization of around INR 9.3 trillion, and revenue of INR 7.5 trillion.

ABOUT TATA STEEL 5

Tata Steel was established in Jamshedpur, India, in 1907. As the earliest manifestation of the vision of its founder, J. N. Tata, Tata Steel continued to carry the 150-year-old legacy and grew to become the 10th largest steel manufacturer in the world. Beyond steel making, Tata Steel also exhibited exemplary corporate citizenship and business ethics.

With operations and commercial presence in multiple countries, Tata Steel had a consolidated steel production (Tata Steel India + Tata Steel Europe + Tata Steel South-East Asia + Rest of the World) capacity of 28.54 million tonnes per annum (MTPA), as per company’s Integrated Report and Annual Accounts 2020–21. In India, Tata Steel’s manufacturing units were located at Jamshedpur, Jharkhand, with a production capacity of 11 MTPA, and at Kalinga Nagar, Odisha, with a production capacity of 3 MTPA, which was in a capacity expansion mode to 8 MTPA. Tata Steel’s business model was based on vertically integrated operations across the steel value-chain that extended from mining, iron and steel making, and rolling products. Its hot metal production capacity mostly used the capital-intensive basic oxygen furnace (BOF) route, reducing its dependence on scrap imports. It also allowed greater quality control over final products.

THE INDIAN STEEL INDUSTRY – AN OVERVIEW

The steel sector’s direct contribution to India’s overall GDP was nearly 2% 6 , and because of the high dependency of other sectors, the indirect contribution was estimated to be much larger. In terms of output effect and employment multiplier on the Indian economy, the steel industry created approximately 1.4x and 6.8x multiplier effects, respectively, making it a keenly observed industry from public policy perspectives 7 .

The history 8 of modern steel making in India started with the aspiration of the legendary Jamshedji Nusserwanji Tata in the 1880s to take India into modern manufacturing that finally fructified into the formation of the Tata Iron and Steel Company in 1907 9 . It took a good twenty years of the intervening period for Tata to convince the then Secretary of State for India in the British Government and the Viceroy to amend the restrictive mining and prospecting laws of those times. Sakchi village, near Jamshedpur in the eastern state of Jharkhand, was chosen as the manufacturing location given its proximity to the rich iron-ore belt (Gorumahisani), coal (Jharia coal fields), and a developed port for exporting the steel and import of the machinery (Calcutta). The company made its first pig iron in 1911 and rolled out the first ingot of steel the very next year. In the subsequent years, the Indian Iron and Steel Company Ltd (1918) and Mysore Iron and Steel Works were founded. The formative years of the industry also witnessed the start of a number of smaller steel-producing units using machinery and technologies of lower capital intensity.

Iron ore was considered a crucial raw material for the steel industry, and India was considered to be well-endowed, both in quantity and quality. The iron ore reserves were estimated to be about 8 billion tonnes, much higher than most Asian countries. The Indian steel sector sources almost the entire requirement of iron ore and non-coking coal domestically. Likewise, the availability of manganese and refractory clays were considered to be abundant. However, the steel companies always found the reserves of coking coal with low ash content (8%–12%), limestone, chrome, and a few other raw materials to be wanting and inadequate. Hence, more than 85% of the coking coal used by integrated steel producers in blast furnaces is imported. Similarly, since not enough scrap was generated in the country, about 30% of melting scrap used in the electric arc furnaces & induction furnaces was imported as well.

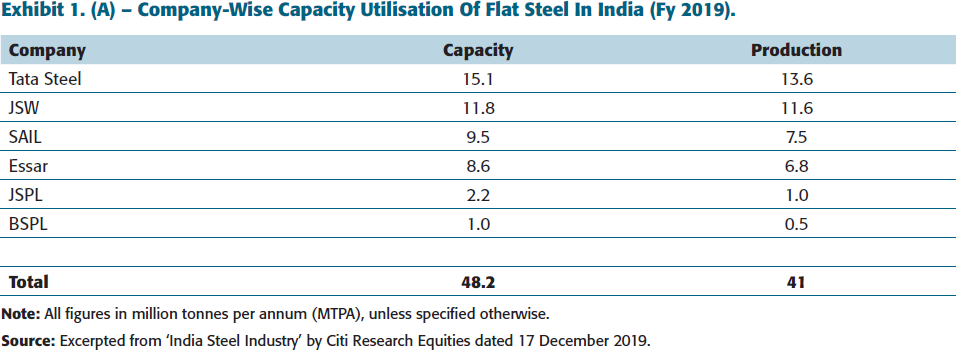

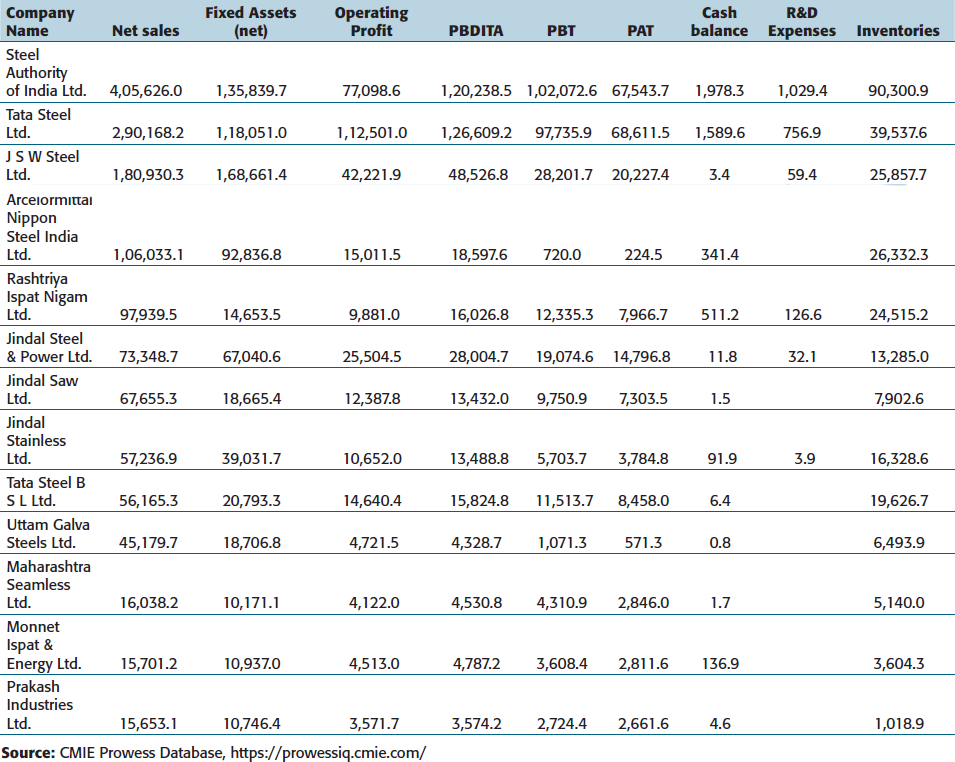

Broadly, there were two categories of players 10 that operated in this space. The first set were the integrated producers, that is, firms that undertook all the activities necessary for converting iron ore to steel. Secondary producers were the mini steel plants that would melt scrap and/or sponge iron to make steel. Steel Authority of India (SAIL), Tata Steel and Rashtriya Ispat Nigam Limited (RINL) were illustrations of the former, and a few big players in the second category were Essar Steel, Ispat Industries and Lloyds Steel. Somewhere in the middle would lie companies like Jindal Steel Works (JSW Steel) 11 with limited backward integration. Exhibit 1(A) tabulates the capacity utilization of the different domestic players for FY 2018–19, and Exhibit 1(B) depicts the industry-wide aggregate trend.

Company-wise Capacity Utilization of Flat Steel in India (FY 2019)

The Indian Steel Industry – A Trend (FY 2019.)

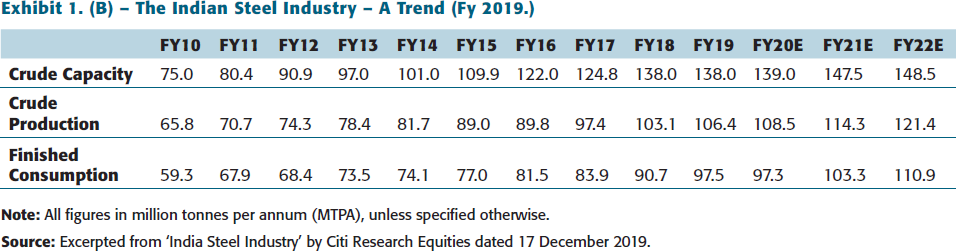

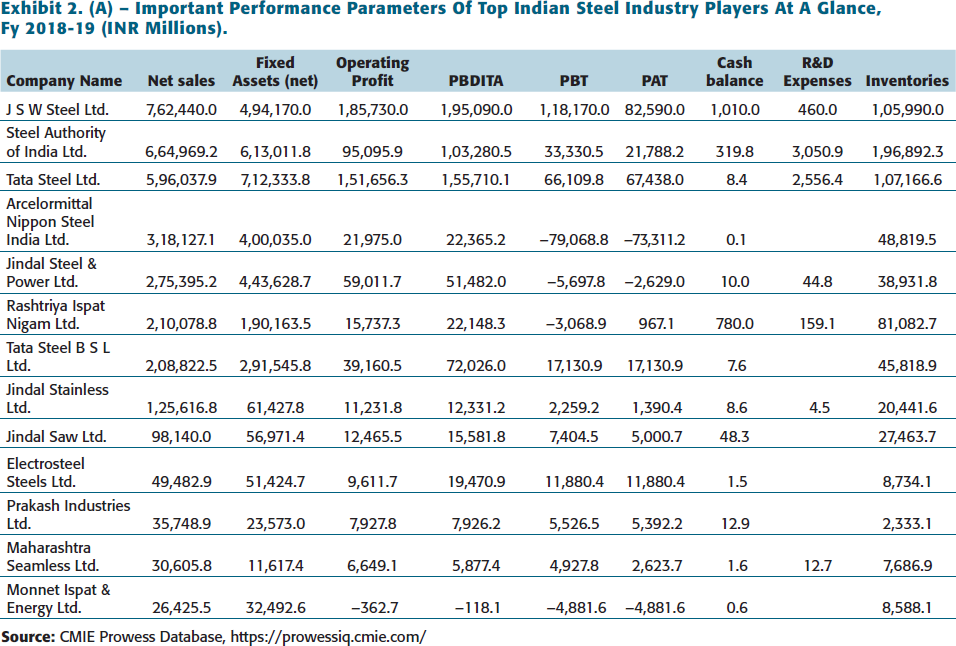

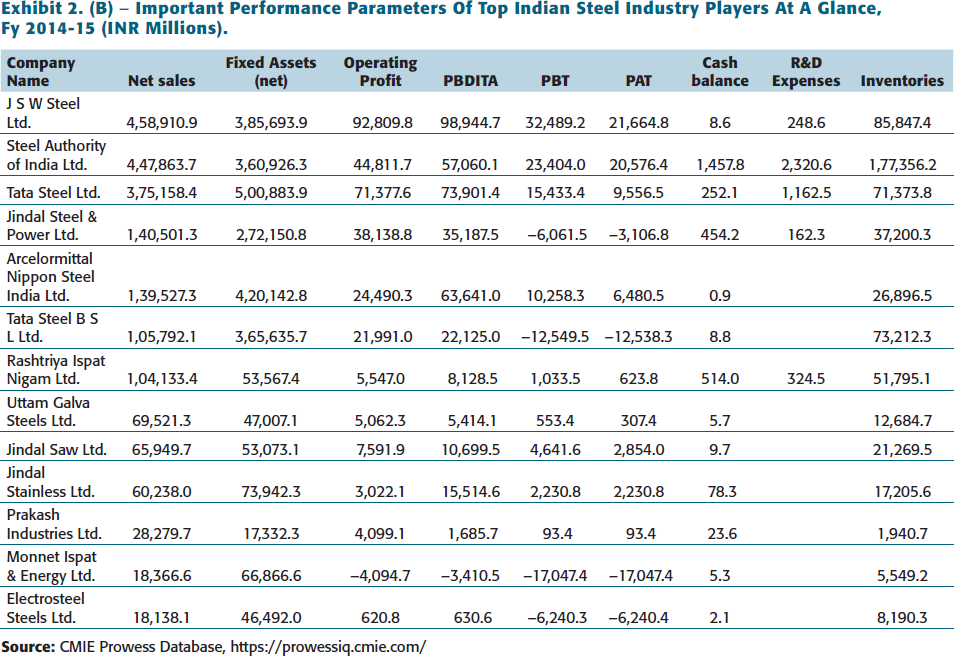

The total number of players in the steel industry in the country in 2018–19 stood at 1,217 {for details of the top players across the past decade, see Exhibit 2(A) through Exhibit 2(C) }. Beyond the first 15 large producers, who control roughly half of the domestic crude steel capacity, scale declines sharply in the industry. A large number of small producers using equipment and technologies of lower capital intensity make up a large part of the 1,200-odd producers, producing either sponge iron (India is the largest producer of sponge iron) or rerolled finished products. The total production of 109.137 million tonnes of crude steel in 2019–20 represented a production decline by 1.6% over 2018–19 and an increase by 5% on a compound annual growth rate (CAGR) basis during the last five years ending 2019–20. Given the nameplate capacity of 142.29 million tonnes, crude steel capacity utilization stood at 77% during 2019–20 compared to 78% of last year. The share of the private sector was consistent with 80%–81%, while the share of public sector companies was close to 20%. However, crude steel production needs to grow at a CAGR of about 7.2% to reach the target for domestic production capacity as set in the National Steel Policy in 2017.

Important Performance Parameters of Top Indian Steel Industry Players at a Glance, FY 2018–19 (INR Millions)

Important Performance Parameters of Top Indian Steel Industry Players at a Glance, FY 2014– 15 (INR Millions)

Important Performance Parameters of Top Indian Steel Industry Players at a Glance, FY 2009– 10 (INR Millions)

The average (retail) market price of iron and steel products displayed significant cyclicity. In March 2020, it showed a decreasing trend compared to March 2019. This pattern was consistent with the previous financial year when the domestic market price also demonstrated similar trends. Considering the average price in the four metro cities, the prices of most steel products displayed a downward trend in December 2019, after which there had been an upturn in the domestic steel markets, with prices increasing for nearly all products.

BHUSHAN STEEL LTD 12

Bhushan Steel Limited (subsequently rechristened as Tata Steel BSL post-acquisition), with more than 27 years of experience, was one of the leading downstream players in the Indian Steel industry. With an existing steel production capacity of 5.6 MTPA, Bhushan Steel was 3rd largest secondary steel producer in the country. Bhushan Steel’s product portfolio included a variety of products such as hot rolled coil, cold rolled close annealed (CRCA), cold rolled full hard steel (CRFH), galvanized coil and sheet, galume coil and sheet, colour coated coils, colour coated tiles, high tensile steel strips, hardened & tempered steel strips, precision tubes, high-frequency electric resistance welding (HFW)/ electric resistance welding (ERW) pipe (API Grade), 3LP coated pipes, billets and sponge iron.

Armed with technological prowess in the cold rolled steel industry as a secondary producer, Bhushan Steel soon became India’s largest and the only cold rolled steel plant having an independent line for producing 1,700mm width cold rolled coil and sheet and 1,350 mm width galvanized coil and sheet. After succeeding as a high-quality secondary producer, Bhushan Steel integrated backwards in the early 2000s, setting up steel-making capacities through the basic oxygen furnace as well as direct reduced (DRI) route to become an integrated steel producer.

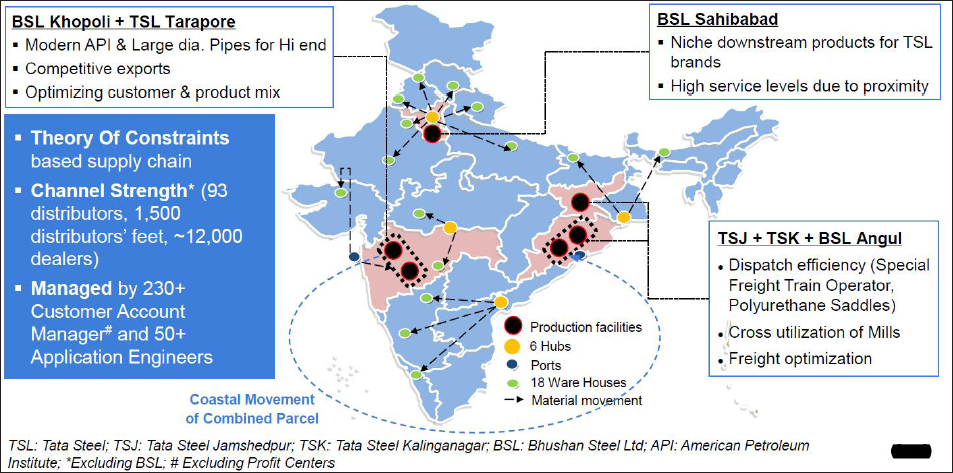

The steelmaker’s facilities were located at Angul in Odisha, Sahibabad in Uttar Pradesh and Khopoli in Maharashtra. Angul boasted of a fully integrated steel facility that included a hot rolled steel facility along with allied facilities such as the induction furnaces, pig caster, oxygen plant, a coke oven plant, sinter plant, a coal washery, two DRI kilns, a captive power plant, and other facilities.

With its downstream facilities at Sahibabad and Khopoli, Bhushan Steel was close to Delhi/NCR and Pune, respectively, which conferred the steelmaker a strategic advantage in accessing major white goods and automobile companies. Internally, the Angul facility supplied the principal raw material, that is, hot rolled coils for the production of steel products at the Khopoli and Sahibabad facilities. The plant locations at Angul and Khopoli were also strategic because of their proximity to the major international seaports at Paradeep and Nhava Sheva, respectively ( Exhibit 3 ). This enabled the company to reach the international markets, notably Africa, Middle East, Southeast Asia, and Australia, with minimal inland transportation. Bhushan Steel was the leading supplier to prominent auto players such as Maruti Suzuki, Tata Motors, Honda Cars, Mahindra & Mahindra, Ashok Leyland and consumer durable players such as LG, Samsung, Videocon, and Haier.

THE INSOLVENCY AND BANKRUPTCY CODE, 2016 13

As a major impetus to resolving company bankruptcy, the Insolvency and Bankruptcy Code (IBC), came into being in December 2016. This new code superseded the extant Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest Act (SARFAESI Act) of 2002, and the Reserve Bank of India’s Asset Restructuring Proposals. Further, IBC also repealed the erstwhile piecemeal approach to dealing with commercial insolvency before 2016, including the Sick Industry Companies Act and debt recovery tribunals. To complete the ecosystem, the Insolvency and Bankruptcy Board of India (IBBI) and the chief regulator, the National Company Law Tribunal (NCLT), were instituted to deal with commercial distress.

Consequently, IBC soon became the preferred route for merger and acquisition (M&A) deals in India. According to a report by Bain & Company 14 , acquisitions of stressed assets through the IBC route accounted for 70% growth in deal value on a year-over-year basis in 2018. No wonder Sanjeev Sanyal (the principal economic advisor in India’s finance ministry) wrote 15 : ‘The insolvency & bankruptcy code is the equivalent of the guillotine’. The report further highlighted the closure of seven large deals valued at $23 billion (around INR 1,610 billion) between January 2015 and April 2019. Moreover, several distressed steel companies were among the 70% of the growth that M&A activity saw in 2018, fuelled by the corporate insolvency resolution process under IBC. Global giants ArcelorMittal to Vedanta, and from the Tata group to the fast-rising UK-based Liberty House evinced interests. Though the common thread across these intentions could inorganic growth opportunities, the core of their interest possibly varied from i) acquisitions of stressed assets through a formal market to ii) boosting growth through new market or capabilities (scope deal), to iii) pushing company’s consolidation in its existing business (scale deal), or simply to iv) entering a country through acquisition.

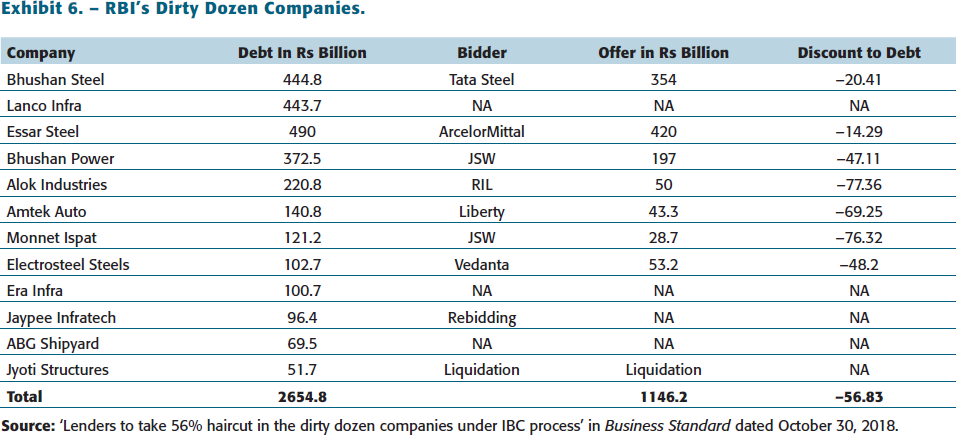

However, like any other nascent law, IBC was also mired with interpretational and implementation challenges. Of the initial 12 large defaulters cherry-picked by the RBI for insolvency proceedings, sarcastically known as the dirty dozen in the popular press, the majority of them were able to draw the attention of reputed and global buyers (see Exhibit 6 for details). Consequentially, the domestic steel sector was heading for consolidation, with a few large players with strong financial and debt-raising capabilities provided an opportunity to expand their market shares by acquiring stressed assets at competitive valuations. After Tata Steel BSL acquisition, the subsequent acquisition of further stressed steel asset of Essar Steel and Bhushan Power and Steel reinforced and legitimized the IBC process to investors looking to acquire debt-laden assets. However, like any new policy intervention, IBC also had its share of highs and lows as it traversed through the byzantine contours of judicial interpretation by the National Company Law Tribunal (NCLT), National Company Law Appellate Tribunal (NCLAT) and the Supreme Court. Notable amongst them were the Supreme Court’s Swiss Ribbons judgement that upheld the constitutionality of IBC and the Supreme Court’s Essar Steel judgement that clarified the pecking order of creditors.

TATA’S ACQUISITION OF BHUSHAN STEEL—THE PROCESS

With an outstanding debt of around INR 570 billion, Bhushan Steel was led to insolvency resolution by the State Bank of India in July 2017 for owing INR 440 billion. Consequently, under the corporate insolvency resolution initiated by the Committee of Creditors of Bhushan Steel, Tata Steel emerged as the highest bidder on 6 March 2018. As per the approved resolution plan, Bamnipal Steel Limited (BNL), a wholly owned subsidiary of Tata Steel, acquired a majority stake of 72.65 through a mix of equity capital of INR 1.5889 billion and debt/convertible debt of INR 350.7369 billion. Existing shareholders and the financial creditors of Bhushan Steel held the balance 27.35 % of Tata Steel BSL’s share capital in lieu of the debt owed to them. Tata Steel BSL used the funds to reconcile debts of INR 352.3258 billion against the existing financial creditors, corporate insolvency resolution process (CIRP) costs and employee dues. Despite best efforts, an amount INR 252.8551 billion remained as unsustainable debts, which the financial creditors to BNL novated for a consideration of INR 1.00 billion. By waiving off the unsustainable debts less the cost of novation, BNL recognized this as an equity contribution during the financial year that ended 31 March 2019. Financing of the acquisition was managed through a combination of external bridge loans by BNL and investment by Tata Steel in BNL. The bridge loan of INR 165.00 billion by BNL was expected to be substituted by debt to be raised by BSL over time 16 .

When Tata Steel completed the takeover, the first step Singhal and the team took was to spend an endless amount of time communicating, sitting with people and understanding the challenges. Attention to ailing key performance indicators (KPIs), the bequeathed centralized management structure, non-uniform organization policies, and recurring on-job accidents were stacked up as the next management challenge to be resolved.

On the acquisition, Singhal recalled

17

:

Overall, the steel industry has been growing at a rate of 6%–7% YoY. Our share in the market would have remained the same, or might have increased slightly historically. There were two ways for us to grow – Greenfields and brownfields…the former is often riddled with delays.

Bhushan used to be one of our biggest customers during 1995–2005, and we knew they never compromised on assets. They already had a capacity of 5MT, and it would have taken us 5 years to develop this capacity through Greenfield. Further, they had the most ‘marky’ customers such as Maruti, Mahindra & Mahindra, LG, Samsung and so on. Additionally, they had good equipment. Since they were also our customers, they were a part of the Tata Steel ecosystem, and we were comfortable about it.

Of their 5 million ton capacity, only 3.5 was being used. The remaining was lying idle due to poor maintenance and imbalanced facilities. Also, there was lack of focus on Safety and Environment. Safety is not only behavioural, but is also technology driven.

We walked into and acquired the Bhushan Steel plants within 48 hours of getting the bid – all the planning was done ex ante. We actually transferred the entire money within couple of hours of getting the bid… all these demonstrated complete agility.

Previously, Bhushan Steel had a centralized structure, but we moved to delegation of power. After taking over, we were hard on cost cutting, but not on the employees. We took a stand that the decisions will be based on data mining and not only basis the ‘intuitive mind’.

While we do not believe in being fixated to targets such as ‘topmost’ or ‘top 3 players’ in the steel industry, we want to be leaders (and have respectable market share) in certain segments. Two of those are automobiles and appliances.

In the steel business, 80% of the value is added in upstream activities (such as the Angul facility) and only 20% is contributed by downstream activities. Since we were already in the business of steel, we succeed in creating synergy. E.g., there was no longer a need for stockpile of raw material in all the plants.

Subodh Pandey, Chief Operating Officer, Tata Steel BSL (Angul) shared four major areas as part of integration challenges: agile-ness under earlier ownership versus complacency under the new ownership; developing a new function-based organogram with clear roles and responsibilities; streamlining contract to ensure compliance with norms; and instilling a safe environment with ethics as the core-culture. Once the steelmaker was confident of setting the ground rules on non-operational parameters, next came the refinement of the KPIs in areas such as improving blast furnace productivity, improving the coke oven rate, or achieving the desired parameters.

Sanjib Nanda, Chief Financial Officer, Tata Steel BSL played a pivotal role in the takeover process. Some of the key challenges he anticipated during and post-takeover were establishing the entire governance system—board, financial operating, capital, etc.; institutionalizing the systems and processes for effective financial control and reporting; prudent working capital & cash management; and dealing with a large number of legal cases. He realized that bringing about the mindset change towards these elements across the organization will put his professional experience to test.

With all-around efforts, the company’s operational parameters significantly improved. Because of mill availability, better maintenance practices, and uninterrupted supplies of raw material, TSBSL achieved a crude steel output of 4.14 MTPA in FY2019, which was higher by 10 % year-over-year. Consequently, sales too grew by 6.5 % year-over-year.

‘Tata’s culture is built around value systems that are non-negotiable. Our concern was how we institutionalise these values into BSL. That is where we spent a lot of time’, reminisced Singhal.

TATA STEEL’S RATIONALE FOR THE ACQUISITION 18

Products

Finished steel production was classified into two broad categories—long and flat products. The flat product was hot-rolled, cold-rolled, galvanized coated, and was primarily used for the construction, appliances and automotive industries. The automotive space happened to be a big play for Tata Steel, especially in the cold rolled and hot rolled, where they enjoyed a 50% market share. This segment was technology-intensive, and most rerollers were not able to produce for this market, making the segment less fragmented. All the major auto producers, Ford, Toyota, Maruti, Tata Motors and Mahindra, were customers of Tata Steel. The long products segment included bars & rods, steel structural and railway materials.

Broadly, the three segments in which Tata Steel operated were automotive & special products, branded products & retail, and industrial products, projects & exports 19 . Of the automotive product categories included hot-rolled, cold-rolled, and galvanized. Hot rolled were used for chassis of the body of the truck, for the chassis of body of the car, or heavy, medium vehicles. The cold-rolled, went into the external bodies, and the components were made by the formation of the shape.

The second vertical that Tata Steel operated was the branded products segment, which was managed through the distribution network with a mix of retail consumers. For a villager who wanted to buy galvanized corrugated sheet (GC sheet) for a roofing requirement, the sheet went through the distributor dealer network and then reached the individual buyer. The other buyers included small and medium enterprises in the automotive business, small proprietary firms who were regular buyers, and finally, individual house builders or the villagers who were not a frequent buyer. The small and medium enterprises labelled emerging customer (EC) account, were the regular customers. Both those segments were served through the distributor network since transaction sizes were small and often required credit support (Tata Steel maintained that they would avoid direct exposure to credit).

The third segment was Industrial Projects (also called the industrial product and projects). This included companies that would make tubes, pipes and pulp. Those were the business-to-business (B2B) buyers directly served by Tata Steel.

For Bhushan Steel, the automotive segment was an important contributor to the portfolio. In fact, they were the first to supply to Maruti Suzuki, a segment that was not part of Tata Steel’s portfolio at one point. Bhushan Steel had the widest cold rolling mill available in the country, imported from Sumitomo and set up at the company’s Sahibabad plant, which supplied to Maruti Suzuki and their ancillaries. Consequently, although Bhushan Steel did not have the product spread of Tata Steel, it dominated high-quality segments, and they were considered a step ahead of other suppliers by automotive customers, especially in the automobile hub in the NCR region.

Like Tata Steel, Bhushan Steel also branded its products in the retail market. However, its products would not fetch as much premium as Tata Steel’s. Bhushan Steel also did not have a planned organization for distribution in terms of its commitment to distributors. In a sense, Bhushan Steel was opportunistic, and if exports were getting a better price, they exported rather than supplied material to the domestic distributors.

Bhushan Steel also specialized in a niche product that Tata Steel did not have in its portfolio. The product medium carbon—high carbon grid, used for blade or saw-making, were made at the Sahibabad and Khopoli plants and were very specialized in application. Market demand for such products was less; hence, not many players fought it out in this space.

Bhushan Steel also had a colour-coated product (not the normal galvanized zinc-coated GC sheets) that Tata Steel did not directly have in its portfolio but was offered through Tata Steel BlueScope joint venture in Pune.

In terms of product specifications, Bhushan Steel made products with a thickness much lesser than what Tata Steel made. Tata Steel had exited the thin sheet segment, the requirements of which were mostly in appliances space like the refrigerator. In Tata Steel Jamshedpur (TSJ), the mill was designed more for mass production, lower set-up time and bigger minimum order quantity(MOQs). For Tata Steel knew that the moment it would get into these segments (i.e., lesser thicknesses), issues of productivity losses and MOQs would kick-in as the appliance segment did not a large quantity. But for Bhushan, the mills used for cold rolling were not as big. Its Sahibabad facility had three rolling mills, Khopoli facility had three rolling mills, and Angul had three rolling mills so that each one could meet the small MOQ requirements and give the desired thicknesses.

While Bhushan Steel supplied 0.33, 0.25, 0.18 mm thickness in the cold roll segment, Tata Steel operated at 0.5mm + segment. So, there was indeed a market need that Tata Steel did not cater to. But Tata Steel could never supply those because they were not making these products in the current facilities at Tata Steel. For appliance makers like Whirlpool and Godrej, the outer door was only meant to provide an aesthetic look. So, the thinner it was, the better it was for the appliances. It did not matter if the sheet was 0.35, 0.3 or 0.27 mm as it was generally the inner structure, that is, the foam, which provided strength to the refrigerator.

The second illustration is of a house buyer, in particular a hut. Traditionally, the lesser the thickness, the cheaper the sheet, allowing the house maker to cover more surface area as per price. So, people belonging to the low-income category desired thinner sheets. For example, Ethiopia’s market in Africa bought very, very thin, 0.15 mm-kind of sheets. Tata Steel was not targeting this segment as they could not make such thin products, and it was believed that it made more commercial sense to roll more. Ultimately, in a steel company, volume was the biggest driver. By adding value to the steel, the incremental contribution would translate to only about INR 1,000–2,000/tonne, but a volume increase would enhance the contribution by INR 10,000 a tonne.

Technology

An important factor for Tata Steel in deciding on the acquisition was the kind of assets that Bhushan Steel owned. Bhushan had sourced assets from the best of the suppliers in the world. The world’s best technology suppliers supplied the hot rolling mill, the cold rolling mill, the steel-making shop, and the blast furnaces (e.g., Paul Wurth, SMS, CMI for cold rolling mill or the Sinter Plant, etc.). The assets were believed to be the best in class in the country amongst all the operating private players. It was a new asset because the plant had been set up recently.

Location

The Bhushan Steel plants were located keeping in mind the proximity to the market, customers and raw materials. The imported raw materials could be easily brought in due to the geographical proximity to Paradeep port. The facilities were very close to the iron ore belt in the eastern part of country. The two downstream units at Sahibabad and Khopoli were close to the main market of the National Capital Region, Delhi and Mumbai. All in all, the downstream facility, supposed to provide better service to the customer and also required to interact closely with the customer on a daily basis, was close to the customers. The upstream facility was supposed to be close to the raw material, and the port was ideally located in the eastern part of the country.

Other Value Chain Commonality and Complementarity

Tata Steel Global Procurement (TSGP), the centralized vertical responsible for coal buying for Tata Steel Europe and Tata Steel India also took control of the procurement activity for Tata Steel BSL. This resulted in favourable credit terms, and also volume discounts. Further, iron ore transactions slowly started moving from intermediaries to the end supplier Odisha Mining Corporation (OMC)e. Over the last year, Tata Steel BSL had started procuring from the Tata Steel captive mines in Noamundi, Joda and in associated belts. It gave the steelmaker the much-needed stability in operations and also helped Tata Steel monetize its iron ore assets that were otherwise lying there (for a pictorial depiction of the joint benefits of the acquisition, see

To optimise logistics, the acquired company started using some of the existing Tata Steel facilities, and simultaneously started closing down the idle ones occupied by BSL. This resulted in achieving synergies and cost savings. For example, to serve a particular customer, Tata Steel facility at Jamshedpur (TSJ), Tata Steel Kalinga Nagar (TSK), and Angul examined the least cost pathway to serve and accordingly allocated.

With Tata Steel’s experience and expertise available in Kalinga Nagar and Jamshedpur, Tata Steel BSL addressed problems and rejections in their grids. The technology experts would fly in to resolve such issues. Similar spillover benefits, such as uniformity in customer dealings and pricing mechanisms, were observed even in marketing and sales. Tata Steel BSL even launched branded products that Tata Steel made. Pandey commented, ‘So, there is huge synergy, and I think we did quantify a figure of around INR 10.00 billion, potential synergy that is there between the two (Tata Steel and BSL)’.

Analyst Views

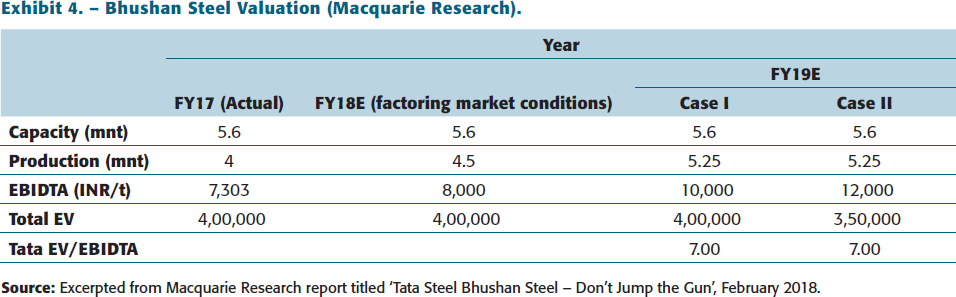

Macquarie Research 20 took a bullish view of the acquisition (see Exhibit 4 for details) as soon as the news of the transaction emerged in the media. While dispelling any concern around the bid to be about 15% higher than expected, the report argued on the upsides of brownfield expansion, proximity to raw material sources, and value addition in certain downstream activities. The lack of the much-desired working capital, and other safety issues, capped BSL’s capacity utilization at 60%–70%. A simple working capital infusion, with Tata’s expertise of the steel business, was argued to be sufficient to jack up the utilization to about 90%. The promoters of erstwhile Bhushan Steel had also submitted a scope of a brownfield expansion at a rate of USD 450–500/ton (that translated to about 50% of the cost of Greenfield scale-up). The proximity of the BSL plant to the iron ore mines owned by Tata was also a boon. And finally, Tata’s dominance in automobile steel would be reinforced through Bhushan Steel’s high-grade auto steel (through its 2.2 MTPA cold rolled mills). Typically, land acquisition-related challenges resulted in the Greenfield projects extending up to a decade, and the quantum of challenges was evident from the successful completion of only two such projects in about the past two decades.

Bhushan Steel Valuation (Macquarie Research)

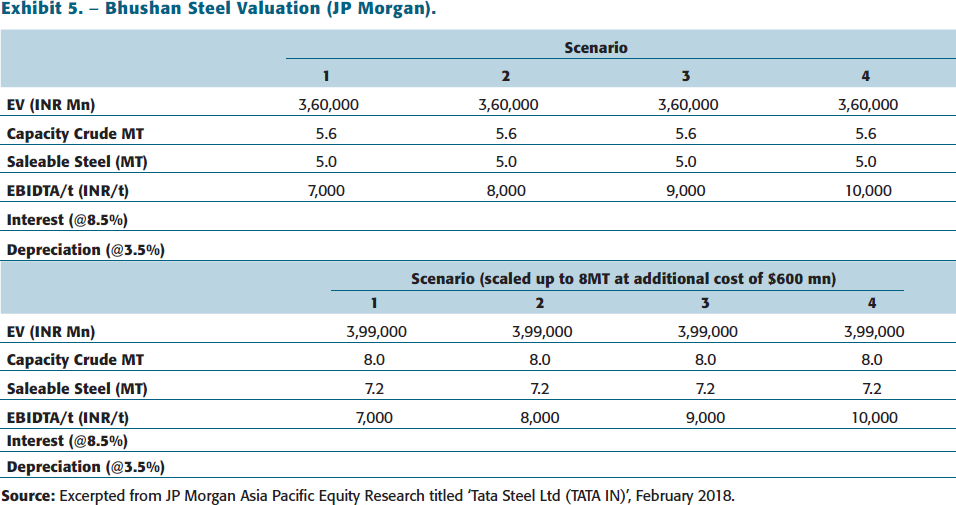

JP Morgan took a similar view, albeit with the underlying assumptions of increasing steel prices, and the acquirer’s presence in raw material sources and downstream value-added businesses. They argued (see Exhibit 5 ) that ‘the bid of Rs. 360bn would translate into an EV/t of $767/t at 8MT and translate into EV/EBITDA of 6.2x at Rs9000/t EBITDA/t on the expanded capacity.’

Bhushan Steel Valuation (JP Morgan)

RBI’s Dirty Dozen Companies

Investec Securities

21

, on the other hand, took a diametrically opposite view of the deal. Excerpts from their report is cited, in-verbatim, below.

As per ET reports, Tata Steel has offered Rs. 352B of upfront cash and 12.2% equity to lenders (vs. JSW at Rs. 280B of cash, no equity) implying EV of ~Rs. 400B. We screen this in three ways – a) trading multiples – assuming Bhushan’s assets clock $1b of EBITDA from day zero, still implies 6x EV/EBIDTA higher vs. Tata’s current trading multiples. Even assuming 10% IDC on the EV implies 5.4x EV/EBIDTA, at par with trading multiples, and not a scenario which excites us. b) asset based valuation – assuming 5.6MT of steel making capacity on derived valuations, EV/T stands at $1278, and, adjusted for IDC at $1151; both variables stand higher vs. blended KPO I and II capex intensity of $900. Even ascribing higher capex intensity to Bhushan’s downstream assets in line with KPO-2 2.2MT CR ill, we fail to find comfort on derived valuations, which stands at par with blended KPO capex. c) incremental expansions – Bhushan had plans to expand from 5.6 to 12.8MT at capex intensity of $424 taking overall capex intensity at $742 (for 12.8MT), a potential bargain then? We do not think so, as incremental land requirement was yet to be tied up. Overall, we find the valuations far from attractive.

Looking forward

With the meeting coming to an end, Singhal’s thoughts were immediately drawn towards the upcoming town hall meeting that he was supposed to address. Understandably, apprehensions werehigh among the legacy employees of Tata Steel BSL, right from the change of the name of the acquired company to our company versus their company to the obvious one—who would stay and who would go? What made a great deal of sense on paper suddenly devolved into a strategic challenge. Would Singhal succeed in putting so many of these concerns to rest?

His thoughts were interrupted by a news alert that popped on his cell phone. The Board of Tata Steel BSL in its meeting had approved merging Tata Steel BSL with Tata Steel. Singhal rushed to his cabin and booted up his laptop while organizing his thoughts on this amalgamation with Tata Steel. His mind was crowded with questions: Would this amalgamation hold promise for Tata Steel BSL? Does it gel well with Tata Steel’s enterprise strategy and earlier M&A pathway? Would this help leverage and unlock potential synergies across the value chain, including procurement, commercial and financing?

Footnotes

ENDNOTES

e-mail:

e-mail:

e-mail: