Abstract

Our study examines the impact of dual leadership on the company’s performance. We also investigate the moderating effects of board independence on duality and firm-performance relationship. The article uses a panel data framework, and the estimation has been carried out using system-generalized methods of moments. The results of our study postulate that dual leadership negatively influences firm performance; however, when the moderator, board independence, is introduced in the empirical model, it affects firm performance positively. We submit that the extensive and complete abolition of CEO duality by Indian regulators may require caution for Indian markets.

1. Introduction

In the context of corporate governance, the dual leadership structure is one of the most well-known and contentious issues (Arora & Singh, 2021; Balinga et al., 1996; Brickley et al., 1994; Finkelstein & D’Aveni, 1994; Pi & Timme, 1993; Yu, 2022). It is the circumstance in which the same person serves as both chairman and managing director (MD)/chief executive officer (CEO). The directive from Securities Exchange Board of India (SEBI) regarding the role split of chairperson and CEO has led to the abolishment of combined leadership structure for about 54% of the top Indian firms. 1 A committee headed by Uday Kotak, CEO of Kotak Mahindra Bank, was constituted by SEBI in 2017 to evaluate the corporate governance guidelines for listed companies. The committee recommended the separation of both roles to have a balanced governance structure, followed by SEBI directives for listed companies to split both the positions in the year 2018. The idea was to separate the decision-making powers between chairperson and MD/CEO to enable more effective and objective management oversight. However later, the mandate was deferred, and companies were required to comply to the same by April 2022. Meanwhile, SEBI decided the separation of roles to be implemented voluntarily, as the companies needed more time for readiness.

The issue of CEO duality (CEOD) is highly contentious for academics, corporate, and policymakers, particularly in a nation like India where there is an ongoing regulatory discussion around CEOD and role-splitting. The management scholars have tried to understand the costs and benefits of CEOD and split. The opponents of duality claim that it may lead to CEO entrenchment creating a unified command structure and elevating the CEO to the position of supreme decision-maker. Duality also has an impact on the board’s capacity for monitoring (Mallette & Fowler, 1992). The agency framework places a strong emphasis on monitoring and opposes entrenchment; as a result, it is opposed to duality since it might lead to an increase in insider control and a reduction in future CEO entrenchment (Khalil & Ozkan, 2016). Maintaining unity of command ensures clarity about decision-making power and reassures stakeholders of clear leadership, according to advocates of CEOD. The organizational theory states that dualism increases the command of unity while focusing on leadership and legitimacy. The board has a contrasting choice between single leadership or avoiding entrenchment. It is apparently difficult to achieve both simultaneously: a unified chain of command at the top and avoiding CEO entrenchment. The stewardship and resource dependency theories of corporate governance support focused and dynamic leadership to enhance company’s efficiency (Dahya et al., 1996; Finkelstein & D’Aveni, 1994). According to Kang and Zardkoohi (2005), both external and internal factors within a company affect board leadership and company performance relationship. This study is more pertinent and compelling for investigation because of the opposing viewpoints of the underlying theories.

The research question for the study is to determine whether CEOD enhances firm performance. The factors which motivated this study are (a) the regulatory force on Indian firms to eradicate CEOD and (b) the inconsistent results on CEOD-performance relationship from past studies (e.g., Krause et al., 2014). Our study uses panel data framework and dynamic estimation methodology to examine the impact of CEOD on firm performance for a sample of the top 500 listed companies. The results of our study postulate that dual leadership negatively influences firm performance; however, when the interaction term of CEOD and board independence is introduced, it is found to have a positive impact on firm performance. We suggest that when an individual wears both hats (chairman and MD), and the company has an independent board, it may help offset CEO influence.

The significant contribution of the study is addition to the scarce empirical Indian literature on the duality-performance relationship. This study is the foremost Indian research to examine this relationship with the interaction of duality and board independence. The prior Indian studies in this field have not considered board independence as a moderator. We emphasize the significance of considering board independence for establishing the relationship between combined leadership structure and firm performance. Thus, we incorporate a moderator, that is, interaction of combined leadership structure and board independence (CEOD*board independence) in our estimation models. The oversight by dual CEO and an independent board may result in a competitive advantage and consequently affect the company’s performance. Next, it is crucial to have a recent evidence on CEOD-performance relationship for Indian firms: (a) triggered by the regulatory push and corporate opposition regarding the mandatory status of splitting the dual roles; (b) more than 50% of top listed firms have already abolished dual leadership structure; in spite of duality having voluntary status in India at present; (c) CEOD is still a controversial topic at the corporate and regulatory level; (d) to the best of our literature review, there is no Indian study conducted to test CEOD-performance relationship, using board independence as the moderating variable.

The study is organized as follows: the next section collates and reviews the literature on CEOD and firm performance and how board independence can affect this relationship, followed by a research gap in the field. The section “Methodology” discusses the methodology adopted, and then, the study shares empirical results along with the discussion. The last section gives conclusion, limitations, and scope for future studies.

2. Review of Literature and Hypotheses Development

This section reviews the literature on CEOD and firm performance, and based on the review, we attempt to identify the research gap. The empirical literature examining the impact of CEOD on firm performance has given ambiguous results, ranging from positive to negative to statistically insignificant coefficients (Daily & Dalton, 1994; Faleye, 2007; Neralla, 2022). This ambiguity in the results could be the outcome of endogeneity issues (Adams et al., 2005; Harrison et al., 1988), posing challenges to find the causal association between duality and performance. However, most Indian literature (Das & Dey, 2016; Uppal, 2020) found no influence of duality on performance. Our study adds to the existing literature by examining the moderating effects of an important dimension of corporate governance, that is, board independence.

The corporate governance theories put forward the following theoretical framework on duality-performance relationship. The agency theory reinforces independence of directors to limit entrenchment and opportunism on the part of management (Jensen & Meckling, 1976). The theory points out that if one person is wearing both the hats of chairperson and MD/CEO, there could be a breach of board independence. The literature (Chen & Nowland, 2010; Jensen, 1993; Singh et al., 2017) suggests that CEOD might adversely affect performance, as it weakens the board’s ability to oversee effectively. On the other hand, many firms support the idea of leadership cohesion that dualism engenders and literature such as Chi and Lee (2010) endorse a positive association between the two. Stewardship theory (Barney, 1990; Donaldson & Davis, 1991) puts forth that when a combined leadership system is in place, shareholders’ interests get a priority in the company, and CEOs enhance firm value through unity of command. According to the resource dependency framework, dual leadership gives CEOs more freedom and authority, improving their capacity to respond and adapt quickly to changes in the business environment and secure performance-critical resources. Consequently, the theories of resource dependency and stewardship suggest a positive correlation between dual roles in the company and its performance. Additionally, research by Macus (2008) argued that board interactions are essential to a board’s success and ultimately affect the company’s bottom line.

We rely on agency, stewardship, and resource dependency theories to demonstrate that board leadership structure occurs within the context of other governance mechanisms, such as board independence. Scholars like Hillman and Dalziel (2003), Desender et al. (2013), and Faleye (2007) contend that an independent board enhances the benefits derived from CEOD and mitigates the costs associated with it. It may indicate that a combination of dual leadership and effective monitoring by independent directors may affect firm performance. Further, independent boards have been associated with effective monitoring, lesser information & processing costs, higher transparency, and better disclosures (Guo & Masulis, 2015; Sharma, 2004), and thus enhance shareholders’ value (Brickley et al., 1994). Thus, dual structure boards prefer independent boards for board effectiveness, better monitoring, and reducing costs. This view is also supported by literature such as Bansal and Thenmozhi (2019, 2021) that companies promote independent directors on the board for better oversight in order to offset agency and monitoring cost of CEOD. Thus, a company willing to align its interests with shareholders would encourage independent directors to serve on the board (entrenchment effect), as opposed to a company that wants to control board decisions in order to shield itself from external scrutiny.

The variables of board structure have been investigated in the past, and the findings revealed a dynamic component in determining leadership structure. Studies such as Hermalin and Weisbach (1998) and Wintoki et al. (2012) provided evidence that company-specific traits and prior performance are the dynamic factors influencing firm performance. Additionally, empirical research by Brickley et al. (1997) suggests that CEOD may serve as a motivator for higher-performing companies. This view has been confirmed by Harrison et al. (1988), who demonstrated that better-performing companies give higher authority to CEOs, culminating in dual leadership, but low firm performance leads to the separation of both positions. The benefit of separating CEO-chairman roles is independent checks and better CEO monitoring, which could translate into better performance (Dahya et al., 2009). Although Adams et al. (2010) argue that the impact of previous performance on CEOD may not certainly infer that CEOD influences performance, many review studies (Finegold et al., 2007; Krause et al., 2014; Zahra & Pearce, 1989) and meta-analyses such as Dalton et al. (1998) and Bergh et al. (2016) have also provided evidence of no significant relationship between duality and firm performance.

In a similar research, Duru et al. (2016) contended that understanding the relationship between CEOD and performance is only complete if the mechanics of leadership selection are addressed. A significant inference could be drawn that the static models may provide skewed and erroneous estimates and raise grave difficulties in drawing statistical inferences. On the other hand, the dynamic model may not resolve all endogeneity concerns but may improve the estimate inferences for OLS estimation and fixed-effects method. Apart from testing the impact of CEOD on firm performance, they also examined whether the advantages of a dual leadership system outweigh its costs. Explicitly, they investigated the impact of CEOD on firm performance for UK firms while testing the moderating effects of board independence and drawing inferences from agency and resource dependency theories. We adhered to a similar theoretical viewpoint to investigate the effect of duality on performance while board independence acts as the moderator in the estimation.

Thus, we draw arguments from agency, stewardship, and resource dependency theories of corporate governance for hypotheses development. It is pointed out that the costs and benefits of separate leadership structures vary, and the impact of board characteristics on business performance is contingent on the motivation and powers of directors. Faleye (2007) and Duru et al. (2016) posit that board composition emphasizes the advantages of duality while mitigating its costs, leading to an equilibrium between powerful CEO, leadership system, and efficient oversight. Existing work such as Armstrong et al. (2014) demonstrated that firm disclosures increase with board independence, reducing the processing and acquiring costs of information. As reinforced by prior studies, the financial data quality also gets improved through independent board oversight.

To facilitate the informational needs of independent directors, Duru et al. (2016) provide that the companies should improve their reporting system and disclosures by increasing transparency. Separate leadership has additional costs; however, dual leadership structure is cost-effective for the companies to favor independent boards for monitoring efficacy. This monitoring efficacy that comes from board independence intensifies the impact of duality on performance such that the oversight by independent directors and CEOD may result in competitive advantage and, consequently, better performance. In addition, when there are more independent directors under dual leadership structure, it may help in offsetting CEO influence. A study by Raheja (2005) also found that companies with dual leadership structures may need more independent directors to offset CEO influence. Therefore, we consider board independence and dual leadership structure as crucial corporate governance mechanisms.

The theoretical framework and past academic literature guide us to develop the following hypotheses:

H1: The impact of CEO duality on firm performance is negative. H2: The interaction of CEO duality and the proportion of independent directors has a positive impact on firm performance.

We expect CEOD to have a negative relationship with firm performance for Indian firms. Further, we expect a positive relationship when the dual leadership structure with an independent board is tested against financial performance. We highlight the importance of considering board independence for establishing the relationship between combined leadership structure and firm performance and incorporate the moderator (CEOD*board independence) in our estimation models. The methodology followed to test the above hypotheses has been discussed in the next section.

3. Methodology

This section discusses the research methodology, empirical models, and estimation process.

3.1. Sample

We have estimated the impact of duality on firm performance for a representative sample of Indian firms. The study is secondary data-based, and data have been collected from Centre for Monitoring Indian Economy’s database, ProwessIQ. For the missing data points relating to the board of directors, data have been taken from corporate governance reports. It is one of the popular databases for extracting financial and board data at the firm level. The sample period chosen for the study is 11 years, that is, from 2011 to 2021. First, the sample of the top 500 listed companies at the National Stock Exchange was selected, then the companies from the banking, insurance industry, and companies with incomplete data were removed from the sample, and we reached at our final sample size of 440 firms. Further, we formulate a panel data set for 4840 firm-level observations to estimate the duality-performance relationship.

3.2. Regression Models

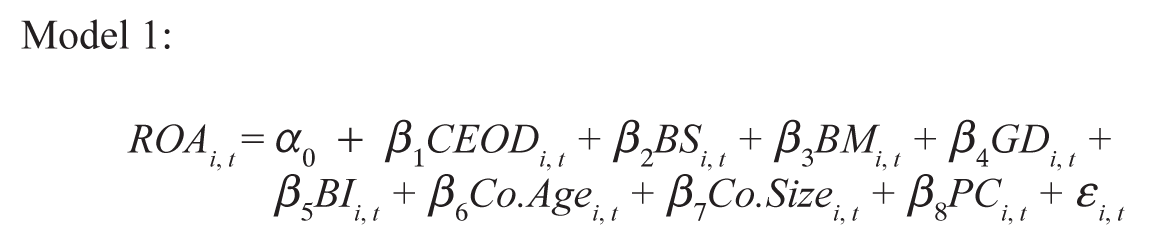

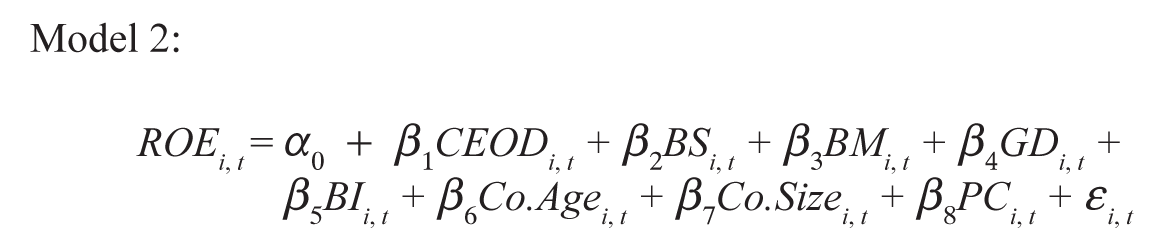

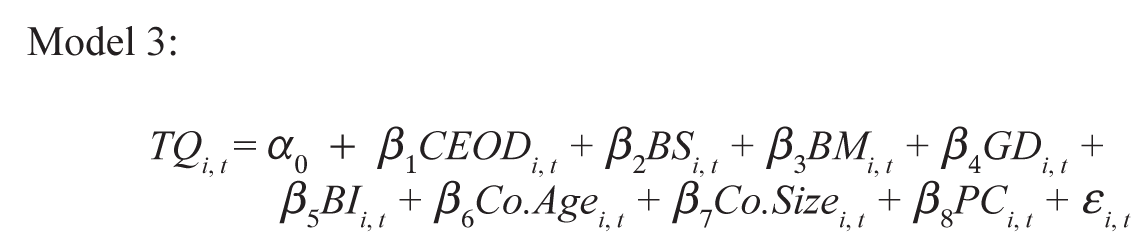

We formulate the following regression models to examine the effects of CEOD on accounting (ROA and ROE) and market (TQ) firm performance measures for firm i in period t:

Model 1:

Model 2:

Model 3:

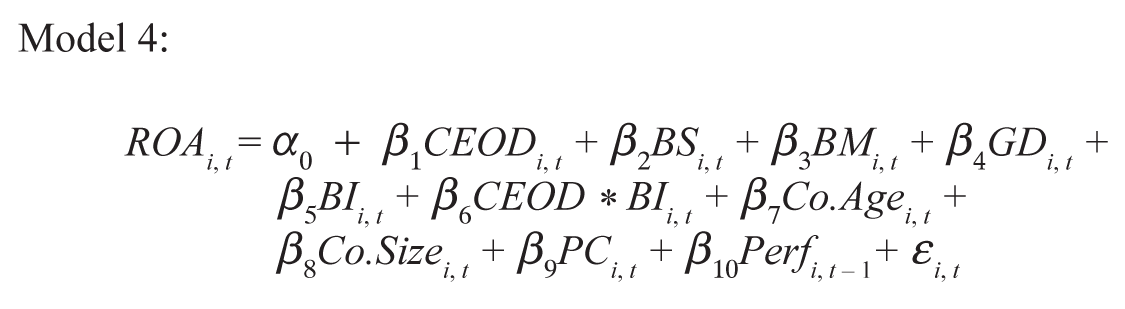

The following three estimation models include the interaction term (CEOD * board independence) while examining the impact of a dual leadership system with independent boards on firm performance.

Model 4:

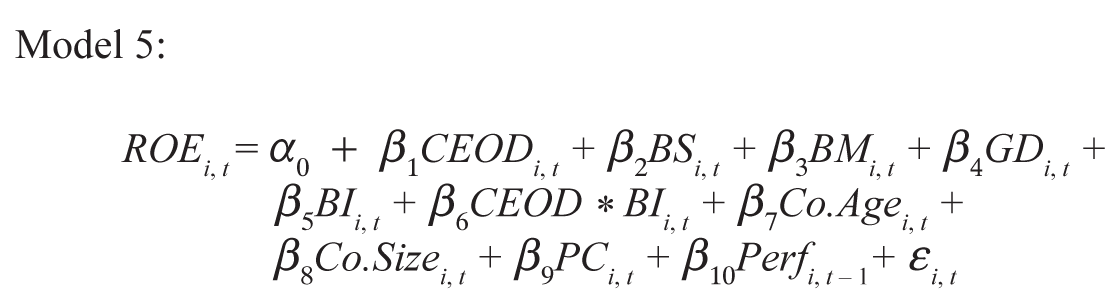

Model 5:

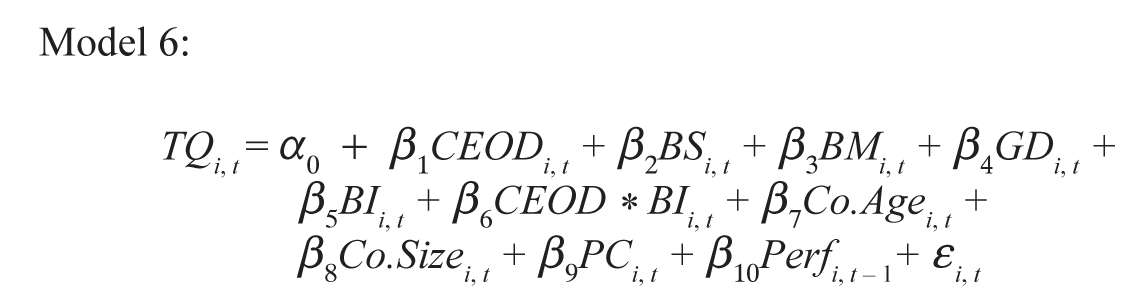

Model 6:

Here, Perft – 1 is previous year’s firm performance and CEOD is CEOD. BS, BM, GD, and BI are board size, board meetings, gender diversity, and board independence, respectively. Co. Age, Co. Size, and PC denote company age, company size, and physical capacity of the company, respectively. €: Error term, i: Firm, and t: Year.

Models 1, 2, and 3 estimate the impact of CEOD on ROA, ROE, and TQ, respectively. The models use other board characteristics and control variables in the regression equations. An interaction term (CEOD * board independence) has been introduced in Models 4, 5, and 6 to know the impact of interaction between duality and board independence on firm performance measures (ROA, ROE, and TQ). Models 1, 2, and 3 test Hypothesis 1, and Models 4, 5, and 6 have been used to test Hypothesis 2.

3.3. Variables

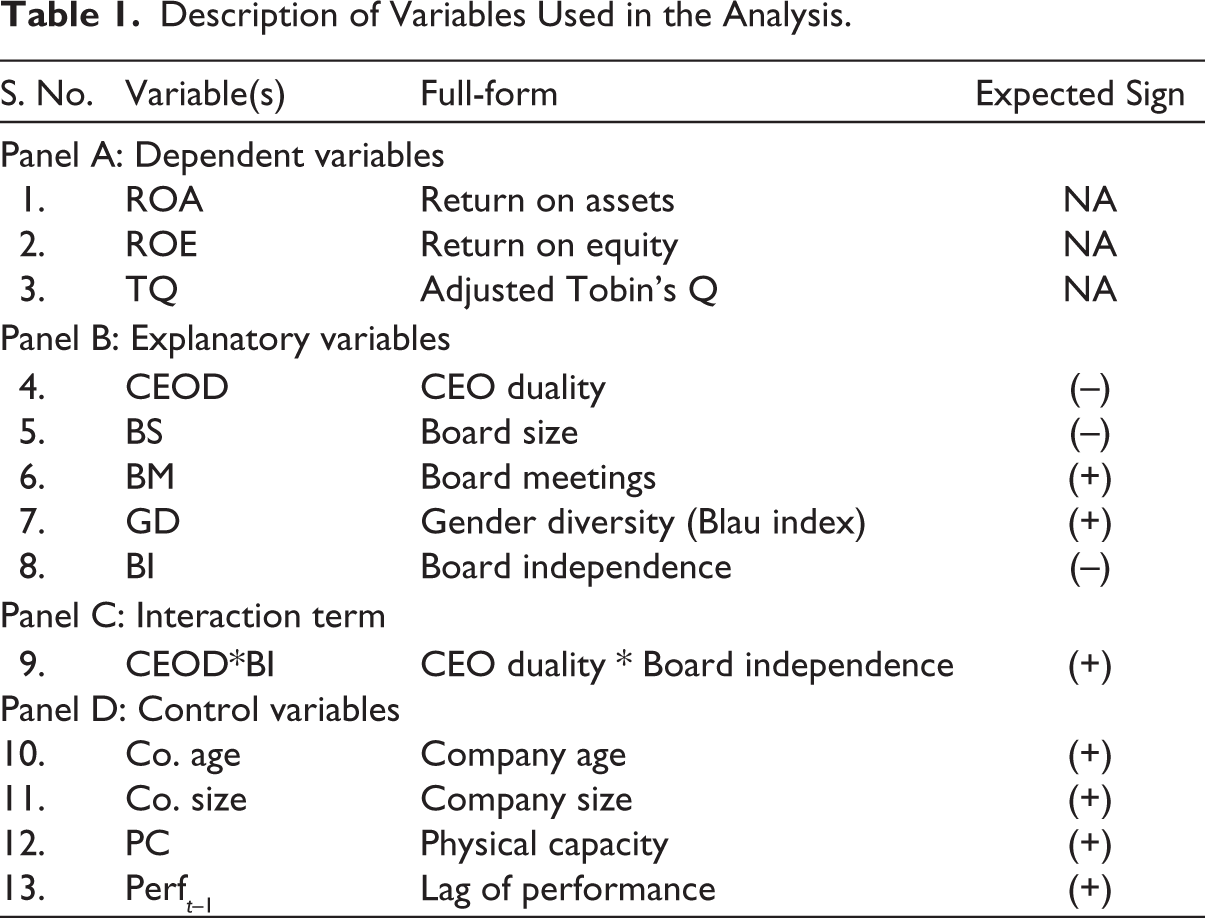

The discussion on dependent, explanatory, and control variables is given in detail below. Table 1 provides a quick peek at the variables list and predicted signs.

Description of Variables Used in the Analysis.

3.3.1. Dependent Variables

We use alternate accounting and market-based firm performance measures as the dependent variables. The accounting firm performance measures used are Return on Assets (ROA) and Return on Equity (ROE), and for the market measure, we use a widely accepted measure of performance, Tobin’s Q (TQ). ROA is computed by dividing profit after taxes with total assets. ROE is the net income for equity shareholders divided by shareholders’ equity. Adjusted TQ is calculated by using the following formula: Total assets plus market capitalization minus book value of equity minus deferred tax liability divided by total assets. In this formula, the book value of equity capital is the sum of paid-up equity and reserves. The accounting performance measures (ROA and ROE) capture the historical events, thus offering a perspective of preceding performance (Soni & Arora, 2016). On the other hand, TQ focuses on future performance (Demsetz & Villalonga, 2001), thus providing a futuristic perspective. Most of the research on corporate governance, particularly CEOD, tends to use both accounting and market performance measures.

3.3.2. Independent Variables

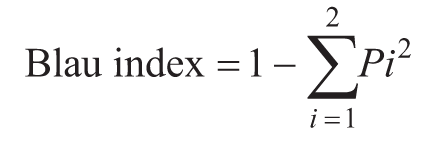

The CEOD is the primary independent variable in the study; we measure it using a dummy variable, which takes the value of 1, when a single individual holds both CEO and board chairman titles, and 0 otherwise. The previous studies which defined CEOD using the same definition are plenty, to cite a few (Gao & Hou, 2019; Lam & Lee, 2008; Wijethilake & Ekanayake, 2018). We also use other board characteristics such as BS, board size (total number of directors on board); BI, board independence (ratio of independent directors divided by board size); and BM, board meetings annually. We have used the natural logarithm of board size and board meetings to improve the model’s fit by converting the data to a further normal bell-shaped curve. For gender diversity (GD) proxy, we used Blau index, which is calculated using the Blau (1977) methodology. It has been replicated by many scholars later (Campbell & Mínguez-Vera, 2008; Nadeem et al., 2017; Nguyen et al., 2015; Vafaei et al., 2015). The calculation of Blau index has been done using the following formula:

Here, i = Number of gender categories (1 or 2, i.e., male or female), and Pi is the proportion of board categories. The minimum and maximum values for Blau index ranges from 0 to 0.5, respectively, indicating that our sample includes homogeneous and heterogeneous boards.

3.3.3. Control Variables

We use company age, size, and physical capacity as control variables, which have a bearing on the accounting and market firm performance. The company age is the number of years since the company’s incorporation. The company age (Age) affects firm performance, as older firms carry higher experience with them, thus significantly affecting firm performance. The company size (Size) also affects economies of scale and bargaining power; therefore, we use it as the control variable. Further, past scholars (e.g., Pal & Soriya, 2012; Weqar et al., 2020) have also used physical capacity (PC) as the control variable while determining the factors affecting firm performance. We posit that fixed assets positively impact firm performance. The measurement of control variables has been done as follows:

Age = Natural log (number of years of firm since incorporation) Size = Natural log (total assets) Physical capacity = Natural log (fixed assets/total assets)

3.3.4. Statistical Models

Previous literature such as Faleye (2007) and Hermalin and Weisbach (1998) have reported the possibilities of potential endogeneity and unobservable heterogeneity while estimating duality-performance relationship. In our case, there can be possibilities that companies with dual leadership structures have better financial performance and vice versa. Although literature such as Linck et al. (2008) provides evidence on both the perspectives and found that performance may not influence CEO duality, on the other hand, there are studies such as Wintoki et al. (2012) giving evidence that CEO duality gets affected by the lag of firm performance and, thus, not strictly exogenous. Panel data permit us to remove unobserved heterogeneity at the firm level from the sample. If unobserved heterogeneity is correlated with independent variables, there could be chances of biased coefficients; thus, we undertake the estimation using dynamic panel data methodology. However, when the coefficients are not correlated with the independent variables, it would be better to draw inference through fixed effects model.

The present levels of independent variables depend on the company’s prior performance and could be related to unobserved heterogeneity. As a result, traditional pooled OLS and panel fixed effects estimators may produce biased and inconsistent outcomes. Thus, the analysis has been conducted using dynamic panel methodology to control the possibility of potential endogeneity and inconsistent biased coefficients. We observed in our literature review that the past empirical research on duality-performance relationship is based on static analysis. However, the static panel data models may not consider the effect on choices in future time periods. The dynamic panel data involves the specification of including lags of the dependent variable on the right-hand side of the regression equation. The firm performance variables are likely to get influenced by the company’s past performance; thus, we model dynamics and consider the previous values of firm performance in our analysis to determine the possibilities of the influence of past performance.

Against this backdrop, we use system generalized method of moments (System-GMM) to take into account the endogeneity as well as heterogeneity issues in our panel data set (Arellano & Bover, 1995; Blundell & Bond, 1998). This method accounts for unobservable firm heterogeneity by incorporating firm-fixed effects. In addition to going beyond the fixed effects model, the method permits the independent and control variables to be affected by the lag of the dependent variable. This method is robust to the firm-level heteroscedasticity and multicollinearity. Also, if there is the dynamic relationship within explanatory variables, it is appropriate to employ a set of internal instruments, such as prior values of explanatory variables and company performance, to solve endogeneity concerns, to eliminate the requirement to discover external instruments.

The data have been modeled using system-GMM method to investigate the impact of duality on firm performance. We use lag of firm performance variables as the instruments in this method. This methodology allows us to overcome the possible endogeneity and unobserved heterogeneity concerns. The next section shares the results and provides a discussion thereof.

4. Estimation Results

This section gives the empirical results for descriptive statistics, correlation matrix, and system-GMM method examining the impact of dual board structure on firm performance.

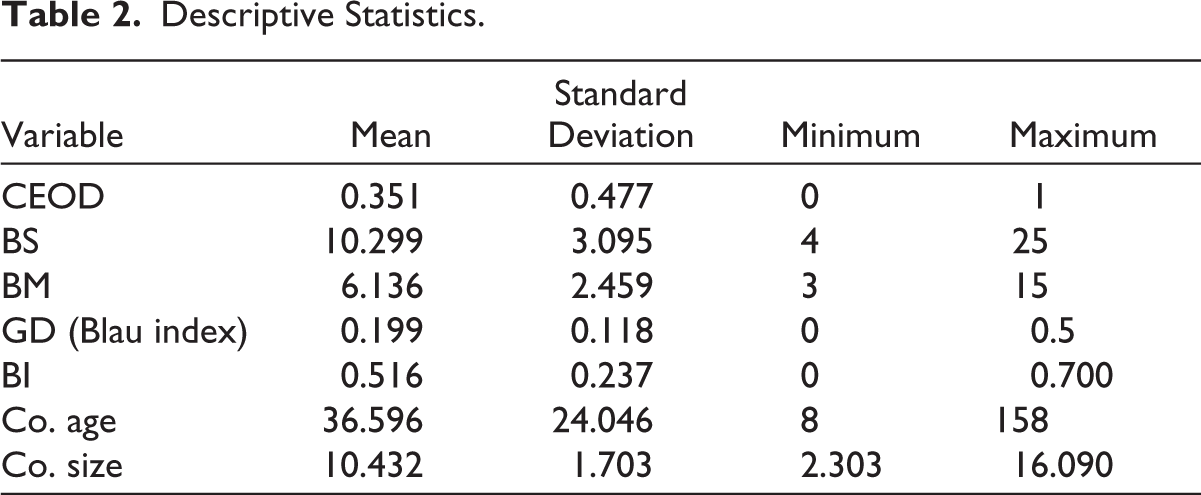

We report descriptive statistics for the variables in Table 2. We have used the original calculated variables for descriptive statistics, instead of the natural logarithm. The mean statistic for our primary explanatory variable, CEOD, is 0.351, and since it is a dummy variable, the minimum and maximum values are 0 and 1, respectively. The minimum and maximum board members in our sample are 4 and 25, respectively, and, on an average, the board size is 10 members and the proportion of independent directors is 51%. Also, the sample companies conduct six meetings, on an average. The gender diversity proxy, Blau index, ranges between 0 and 0.5. In our sample, the mean age of the company is 36 years, with a minimum of 8 and a maximum of 158 years.

Descriptive Statistics.

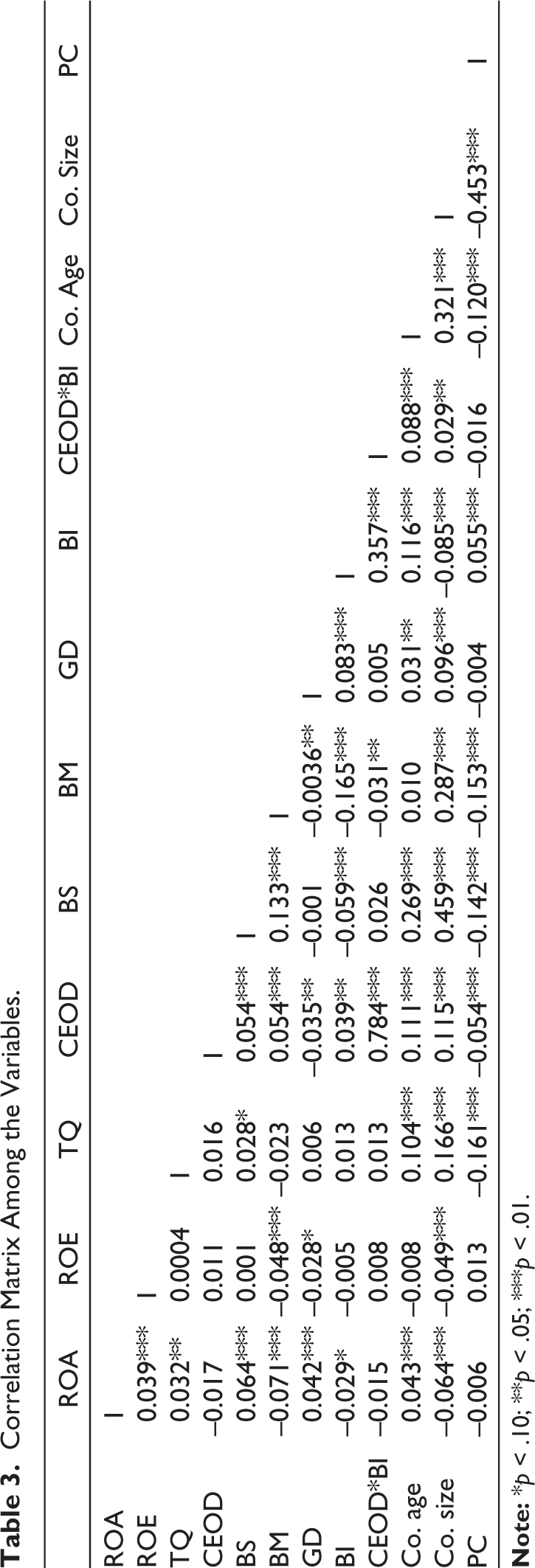

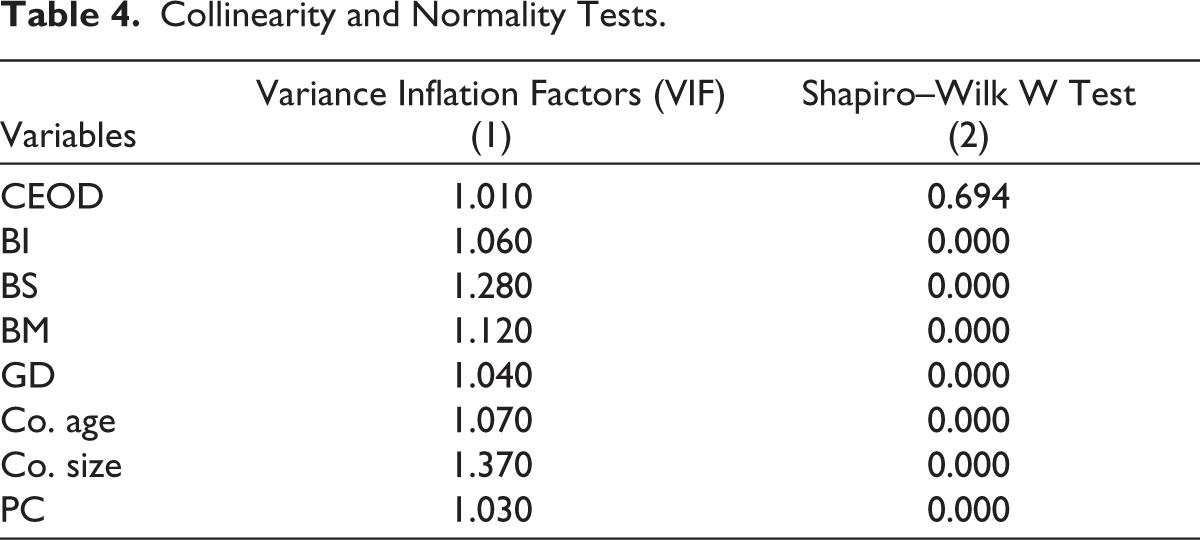

Further, in the correlation matrix in Table 3, it is worth noting that all correlation coefficients among the variables are below 0.70, implying that multicollinearity is not an issue for our data set. The variance inflation factors (VIFs) in Column (1) of Table 4 show that the values for all independent variables are less than 10, confirming no collinearity problems in the models (Gujrati & Porter, 2003). To test whether the data are normally distributed, the Shapiro–Wilk parametric test has been used in Column (2) of Table 4. The null hypothesis is that the population is normally distributed. When we look at the p values, we observed all p values except for CEOD are less than .05; thus, the null hypothesis is rejected implying that the data are not normal. However, data not being normally distributed may not influence the reliability of the results, as the large sample size may not distribute the data normally.

Correlation Matrix Among the Variables.

Collinearity and Normality Tests.

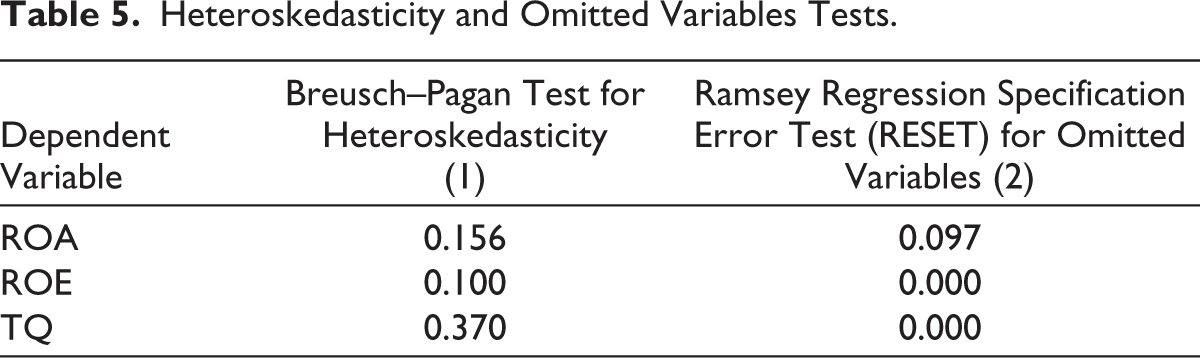

Further, we check for the presence of homoskedasticity using Breusch–Pagan test. The results can be seen in Column (1) of Table 5, showing that p values in all three models are more than .05. It implies that homoscedasticity is present, and the models do not suffer from heteroskedasticity, thus accepting null hypothesis. Lastly, in Column (2) of Table 5, Ramsey regression specification error test for omitted variables has been conducted to test the null hypothesis that the model has no omitted variables. The p value for our F-statistic is less than 10%. Thus, at 10% significance level, we fail to reject the null hypothesis of Ramsey RESET test, implying that our models do not have the problem of omitted variables.

Heteroskedasticity and Omitted Variables Tests.

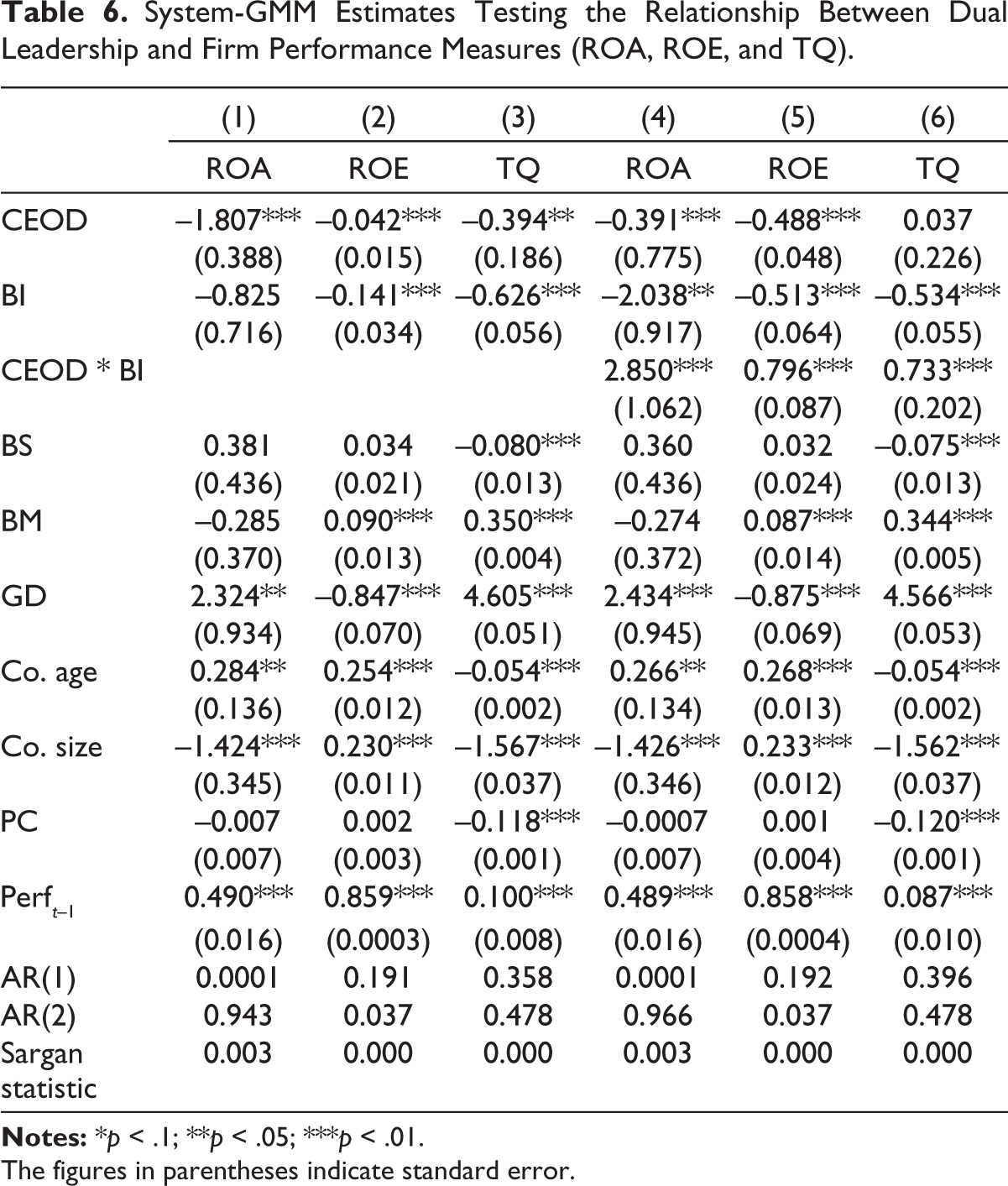

The model has been initially estimated using pooled OLS, fixed-effects approach, and difference-GMM method. 2 The derived difference-GMM coefficients are lower than the fixed effects estimates, suggesting that the former are downward biased due to poor instrumentation. Additionally, the stationarity tests revealed that the firm performance variable displays random walk; in such a situation, the difference-GMM may provide biased and inefficient coefficients. We employed system-GMM to evaluate the duality-performance relationship after taking into account the advantages of system-GMM in such a scenario. Using this technique, Table 6 shows the effects of CEO duality on several firm performance indicators (ROA, ROE, and TQ). The results for Models 1, 2, and 3 are presented in Columns (1), (2), and (3), respectively, and Models 4, 5, and 6 have been estimated in Columns (4), (5), and (6), respectively, of Table 6.

System-GMM Estimates Testing the Relationship Between Dual Leadership and Firm Performance Measures (ROA, ROE, and TQ).

The figures in parentheses indicate standard error.

It can be seen from System-GMM results that when CEOD has been independently assessed against firm performance (columns 1, 2, and 3), it has a significant negative impact on all performance measures, supporting Hypothesis 1. Then, we introduce the interaction term (CEOD * BI) in the analysis in columns 4, 5, and 6; this interaction implies that the impact of CEOD on performance varies for different values of BI. Therefore, the effect of CEOD on performance is not just dependent on its individual coefficients. Additionally, it depends on the values of β6 and BI. β1 is now interpreted as the unique effect of CEOD on firm performance only when BI equals 0. Our research demonstrates that when there are no independent directors, CEOD has a negative correlation with ROA, ROE, and TQ.

When we added the interaction term in the model, it has changed the coefficient values of CEOD. The effect of CEOD on ROA is now –3.391 + 2.850*BI. When BI = 0, the effect of CEOD is –0.391 + 2.850*0 = –0.391. When the proportion of independent directors is 100%, the effect of CEOD is –0.391 + 2.850*1 = 2.459. Similarly, the effect of CEOD on ROE when BI = 0 is –0.488 + 0.796*0 = –0.488. When BI is 100%, the effect of CEOD is –0.488 + 0.796*1 = 0.308. The impact of having more independent directors on a company’s performance varies depending on the extent of board independence as a result of this interaction. This indicates that for each level of BI, there are differences in the slopes of the regression lines between CEOD and performance.

The positive coefficient of interaction term implies that when the proportion of independent directors rises, the impact on firm performance is greater. Furthermore, it can indicate that having more independent directors overseeing a dual leadership system assists in balancing the power of the CEO. The independent directors’ control and monitoring, together with the dual-role CEOs, may provide businesses a competitive edge and, as a consequence, improve performance. Therefore, we accept our second hypothesis. We concur with the findings of earlier research (Brickley et al., 1997; Raheja, 2005) that dual CEO companies require extra independent directors to balance the CEO authority and influence since duality may increase the cost of information access for independent directors.

Our findings demonstrate that board independence favorably moderates the statistically significant negative impact that duality has on company performance (ROA, ROE, and TQ). It implies that independent board members act as efficient monitors, minimize management opportunism, and act in disciplinary capacity while taking advantages of the decisive leadership connected to a joint board leadership structure. Our results are consistent with the contentions made by Aguilera et al. (2008) that the interdependence of corporate governance systems determines their efficacy and by Davidson et al. (2004) and Finkelstein and D’Aveni (1994) that board independence determines the performance–duality relationship.

Additionally, BS has a negative influence on TQ (columns 3 and 6), suggesting that larger boards may not always result in greater market performance, as they may cause more conflicts or delayed decision- making. For instance, the agency theory arguments along with the past studies such as Lipton and Lorsch (1992) and Mori et al. (2013) conjectures that smaller boards help in improving firm’s performance. A higher frequency of board meetings may result in a more fruitful exchange of ideas since BM has a positive impact on ROE and TQ, in line with Vafeas (1999). The board independence, BI, has a negative relationship with firm performance measures, which may be due to the need for independent decision-making powers with independent directors (see Arora & Singh, 2021). Further, when a firm has a gender-diverse board, it boosts operating and market performance as well. The gender diversity, assessed by Blau index, has a favorable influence on ROA and TQ. Our findings demonstrate that the regulatory need for having one woman on board would also improve the company’s performance. The returns (ROE) to equity owners may not, however, increase with GD on board.

Furthermore, the company age and TQ have a negative relationship, contrary to our expectations, which suggests that younger firms have better market performance for our sample set; however, experienced firms have better ROA and ROE. The company size impacts ROA and TQ negatively, but larger companies offer higher returns to equity shareholders (ROE). PC has a negative impact on TQ, implying that fixed assets may not have been optimally utilized to influence market performance metrics. The performance of the previous year also has a positive influence on the company’s performance this year.

5. Conclusion

In research, academia, and media, the question of whether a chairman should also serve as the MD is currently open for debate. After Indian authorities mandated the separation of the two positions in listed companies, the issue gained more prominence. However, in 2022, the companies were given a reprieve, and role separation could be implemented voluntarily. However, academics, businesses, and decision-makers are becoming increasingly intrigued by the issue. Therefore, it is crucial to understand the impact of the separation of the two roles, and how they affect company performance. By using dynamic panel data analysis, we have sought to determine the impact of CEO-MD duality on accounting and market performance measurements.

We examine the relationship between dual leadership structure and firm performance while incorporating the moderating effects of board independence in our estimation models. Linking CEO duality and board independence to firm performance fits within the framework of corporate governance, given that CEOs monitor the board in addition to focusing on maximizing shareholder wealth. The findings provide evidence that CEO duality has a negative relationship with firm performance. Moreover, it suggests that when dual leadership structure has an independent board, it may help in offsetting CEO influence. The monitoring efficiency from independent board intensifies the impact of duality on performance, and the dual leadership board may need more independent directors to counterbalance excessive influence from CEOs. Thus, the extensive and complete abolition of CEO duality by the regulators may require caution. Although holding both positions by a single individual may provide him/her excessive influence over the company, however, separating the roles may affect the company’s performance.

Our study is the first Indian article examining this relationship with an interaction of duality and board independence. The study holds high importance when the regulators are in the process of making a critical decision of whether CEOs should be given the dual powers or whether role split is beneficial from the viewpoint of enhancing firm performance. Most of the Indian literature have suggested insignificant CEOD and firm performance relationship. Our study contributes by finding significant results and can be considered an illustration for Indian markets. It serves as a foundation for comparison for studies in relevant fields from developing economies. It could encourage researchers from other countries to examine the CEO-performance link using board independence or other governance criteria as the moderating variable. The governance and leadership structure of Indian companies may also be a factor for business organizations having investments in India, since it has been linked to performance. The study may be utilized as an initial point of reference for regulatory bodies such as SEBI to examine the link between combined leadership and performance in the presence of the interaction between CEOD and board independence. It may be viewed by other nations as the pilot study to design recommendations for their governance structure. However, the generalization of results may require caution, as the legal and civil environment varies in different markets along with the corporate governance mechanisms. Future scholars may work on cross-country comparisons to draw noteworthy results on the duality-performance association. Future research may also consider examining the moderating effects of gender diversity, firm size, or board size within the dynamic framework. Future research should also examine Indian and foreign ownership patterns; group and family holdings to unravel the CEOD impact on firm performance.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.