Abstract

This article reviews the evolution of startup ecosystem development in Thailand from the early 2010s to the beginning of 2020s. We summarise our findings and provide critical analyses about the innovation development in Thailand, using internal and external sources of information about Thailand’s innovation strategies, policies, and case studies. We also include macro-level national policies and changes in the government that affect the foundation of Thailand’s startup ecosystem, including the mechanisms that drive the growth of the ecosystem. We argue for the decentralisation of innovation policies and ecosystems to help navigate through new challenges and uncertainties, for the recovery of socio-economic factors. Different types and examples of startups that are key to the decentralisation of innovations in Thailand are also explained and illustrated. Impediments and caveats of innovation ecosystem development in Thailand are discussed, pointing the directions for future research.

Introduction

In the beginning of the current millennium, a national innovation system was fragmented, leading to poor economic performances as the country would not be able to catch up and benefit from the development of new innovations (Intarakumnerd et al., 2002). The 1997 financial crisis originated from Thailand and negatively affects such a fragile system. However, the country rebounded rapidly in the first decade of 2000s, whilst in the early 2010s it could be seen as a new chapter of tech startup development and large national corporations (LNCs) investment. Henceforth, since early 2016, the Thai government started to perceive startups as New Economic Warrior (NEW), as a means to liberate the Thai economy from the middle-income trap.

During the early 2000s, the National Innovation System (NIS) of Thailand could be characterised as a slow and passive firm with lacking technological capabilities, non-cohering innovation and industrial promoting policies, unsatisfactory research quality, capability (to produce enough graduates to suit industrial demands), and lack of overall linkage and incentives for the innovation stakeholders in the ecosystem (Intarakumnerd et al., 2002). However, with structural and policy changes as outlined later in the manuscript, Thailand has made significant progress to shift from the economic-output focus to innovation-output promoting schemes. For example, the total number of higher education institutions almost tripled in the early 2000s, as of 2022 there are 185 public and private institutions in Thailand according to the Ministry of Higher Education, Science, and Education (

In the rest of this article, we further elaborate on the evolution of the Thai startup ecosystem in the past 10 years, chronologically in section ‘Evolution of Startup Ecosystem in Thailand’. Then, in section ‘Startup as the New Ingredient for Decentralisation of Innovation’, we illustrate the policies and aspects of a contemporary innovation system that would attain the optimal degree of decentralisation of the innovation system in the Thai context. In section ‘Conclusion’, we provide the conclusion of our article and avenue for future research.

Evolution of Startup Ecosystem in Thailand

The definition of the startup business is not actually about its size. It is more on its purpose to solve problems in the big markets fast with technology and/or innovation; its business model that is scalable and repeatable; and its rapid growth which can be exponential and a game changer in some industries. To be more precise, Forbes, by Jared Hecht, has summarised that the key indicators identifying a business as a startup are its growth intent, funding methods, and end visions (Hecht, 2017). In terms of growth, Paul Graham, a co-founder of Y Combinator, one of the influential startup accelerator and seed capital firms in the world, simply defined a successful startup, is a company that can ‘(a) make something lots of people want, and (b) reach and serve all those people’ (Graham, 2012). Moreover, startups rely on a different kind of business finance than standard loans, such as investments from angel investors and venture capitalists. The amount or size of funds depends on the business’s stage, also known as ‘rounds’. The funding rounds start from a pre-seed or seed round, then Series A, B, C, and beyond. The funding timeline can vary from 3 months to more than 1 year, depending on business sectors (Stephan, 2019). One could argue that the aim of a startup is either an initial public offering (IPO), initial coin offering (ICO), the acquisition by a larger company, or the receiving of strategic investments for the startups to reach its growth potential. According to the ecosystem survey conducted in 2021, 73% of start-ups received seed funding, followed by 15.9% receiving Series A funding, and 6.3% in the pre-seed tier. Although business service areas exhibited the highest number of companies in the survey at 26%, it is noteworthy that the most significant funding was directed towards FinTech. Notably, FinTech secured the highest funding with nine companies and a total of thirty-nine investors, constituting approximately half of the total investment across all fields, with a cumulative value of US$97 million.

In terms of startup development in Thailand, we can classify the evolution into three phases of developmental focus―the startups’ technologies and innovations, investors and venture capitalists, and ecosystem and public policies. The first phase was from the early 2010s until 2015 when mobile-based technologies were growing in Thailand (Aditya, 2017). The second phase was during 2016–2019 when the government started to support startup’s growth through policy reformation. The third phase refers to the decentralisation of technologies and innovations that became the new ingredients of growth for businesses and to adjust to new lifestyles and challenges.

Pioneering Work by Local Young Game Changers (2012–2015)

The evolution of the startup ecosystem in Thailand has been sparked and influenced by Silicon Valley, where many tech-based companies are located. The startup business model has been gaining a lot of interest from technology enthusiasts and innovators since then. The new business and operation models, funding methods, and innovative culture have been inspiring the early adopters and business owners around the world, including those operating in Thailand.

An emergence of the startup business in Thailand became more visible in the market since the early of 2010s. This period could be labelled as a pioneering period for startup enthusiasts. The first group of founders had tech-based knowledge, or work experiences in tech-based companies, particularly those in Silicon Valley. The startup ecosystem in Thailand started its journey from the endeavours of young Thai entrepreneurs returning from Silicon Valley since 2012, in their attempts to establish tech startup companies. Some of which later grown into unicorns, secured record-breaking amounts of funding in the history of Thai startups, or have disrupted the existing business ecosystem at an unprecedented level. Later, all three major telecommunication companies (TELCO); Advanced Info Service (AIS), DTAC, and True Corporation, joined the bandwagon as incubators and investors for tech-startup founders, focusing mainly on software and application building.

Like Silicon Valley, prior to the digital disruption in Thailand, there were some famous websites in the dot-com period pioneering digital startups such as Sanook (launched in 1998) and Kapook (launched in 2003) led by Poramate Minsiri. Sanook, a portal website inspired by Yahoo!, was acquired in 2010 by Tencent, the biggest Chinese internet service portal, with 49.92% control. Tiwa York managed Sanook Online Limited during 2011–2012, while also founded and managed Kaidee.com as a CEO & Head Coach. Sanook was then fully taken over and renamed to Tencent Thailand in 2016 (Tech Wire Asia, 2016). While Poramate Minsiri has continued to manage Kapook.com until today. This shows that there were ample tech-based businesses since before 2010 that were not defined as startups but grew and exited the market in a manner like a startup. Further, most of the founders and people in the startup businesses in this phase completed their education in technology fields and had a good command of English, some had prior work experience or studied aboard, mostly in Silicon Valley.

The pioneering startups in Thailand that caught the attention from investors and corporates and those who successfully raised funds in the early of 2010s were involved mostly in e-commerce, mobile application, and FinTech. These currently operating Thai startups became mentors and key opinion leaders in the next phase are as follows:

Public Policy to Nurture New Economic Warrior (2016–2019)

During this period, we have seen changes in government policy, particularly the establishment of the National Startup Committee (NSC), under the leadership of the Ministry of Science and Technology (later changed to Ministry of Higher Education, Science, Research and Innovation (MHESI)) (Aditya, 2017). One of the goals of NSC was to promote sectoral innovation development; namely, TravelTech, AgriTech, HealthTech, MedTech, and Medical Tourism. In addition, a major reform of the innovation ecosystem resulted in the creation of the Startup Thailand platform in 2017. Startup Thailand aimed to increase the market base of Thai startups, facilitate investments, and improve the capability of the startup stakeholders such as investors, founders, students, innovators, or aspiring entrepreneurs. NSC supported the growth of startups by providing incubation programmes, skill development platforms, financial incentives, and legislation supports to the new development of startup use cases. Furthermore, Thailand’s Board of Investment also provided income tax exemption for a period of 5 years for startups, such as Fin-Tech, and the income tax exemption of Venture Capitalists for a period of 10 years. Lastly, a major reform of the government e-payment system took place around 2016, as the government supported the financial service sector by creating a regulatory sandbox for the multi-national e-payment initiatives such as e-wallets, online payment services, or the iconic electronic payment gateway system ‘PromptPay’. Recently, the government has approved a capital gain tax waiver for startup investment which will drive local startup funding in the country. Twelve target industries approved by the cabinet entail as follows: Smart Automotive, Smart Electronics, Medical Tourism, Agriculture and Biotechnology, Food Processing, Robotics, Aviation and Logistics, Biofuels and Biochemical, Digital Services, Medical Hub, National Defence, and Human Resource Development and Education. The legislation will be effective for 10 years. The investors are required to hold the equity for 24 months before selling the equity.

Establishment of National Startup Committee

The Thai government established the National Startup Committee (NSC) in 2016 to support startups and SMEs, or the tech startups as ‘New Economic Warriors’ (Chundasutathanakul & Chirapanda, 2021), to further propel economic growth. By the second half of 2010s, Thailand developed and deployed various public and private startup policies, and 2022 marks the first decade of Thailand’s startup ecosystem evolution. NSC, which was tasked with the priority mission in developing the Thailand startup ecosystem, led by the Ministry of Science and Technology (MOST), and amalgamated the joint efforts of multiple governmental bodies including the Ministry of Information and Communication Technology, Ministry of Commerce, Ministry of Finance, Ministry of Industry, Ministry of Foreign Affairs, Ministry of Tourism and Sports, Ministry of Education, and Ministry of Agriculture and Cooperatives (Shin & Limapornvanich, 2017).

In 2017, NSC launched national startup policies with the following missions: to increase the awareness of startups (e.g., via Startup Thailand Expo), improve area-based innovation and regulations, incubate startups through multi-agency funding programmes, and devise public policy recommendations to support startups. As the context of the world, technology, and requirements of the consumers change over time, as of 2022, the focus of the NSC comprises of four pivotal strategies. First, is to build awareness of the startup, with the aim to grow the startup community via the establishment of a one-stop service portal and media, to collect public and private data for startup stakeholders in the ecosystem, and promote data-driven innovation. The second strategy is aimed to increase the ease of doing startup businesses, to enhance the startup’s competitiveness and growth. Third, is to strengthen the startup ecosystem, to foster new generations of talents and entrepreneurs. The last strategy focuses on the provision of incentives and supports to stimulate investments and growth in startups domestically and internationally.

National Innovation Agency as the ‘System Integrator’

National Innovation Agency (Public Organization), or NIA, is a special Thai government entity that oversees and promotes the development of innovation and startup ecosystem in Thailand, under the Ministry of Higher Education, Science, Research, and Innovation (MHESI). Since 2003, the NIA has assumed different roles for the amelioration of Thailand’s startup ecosystem at various stages of startup development, as the needs of the startup stakeholders differ according to their progress and the fundamental of their businesses. Under the supervision of NIA, Startup Thailand, acts as the national startup committee and platform for the cooperation between startup stakeholders and evangelists domestically and abroad, this exemplifies some of the projects undertaken by NIA apart from its well-renowned funding agency function.

Corporate-led Innovation and Disruption from COVID-19 (2020–Present)

Rise of Local Venture Capital Community

In the late 2000s, venture capital market of Thailand was underdeveloped, and venture capital firms found it difficult to foster innovations in the local market as compared to the more developed countries (Sun et al., 2019). In the private sector, we observed drastic changes, particularly in large enterprises and startups. On the macro level, many corporates sought or initiated public–private partnership programmes such as ‘Innovation Club’ or ‘Innovation Thailand’, in the attempt to form business alliances, share best practices, and source new research or innovation projects with RTOs, universities, innovation labs, or other startups from different industries. This coincides with the mission of many governmental bodies that support the promotion of innovation ecosystems; for example, NIA, DEPA (Digital Economy Promotion Agency), and the Office of National Higher Education Science Research and Innovation Council (NXPO, 2022).

Many large corporations also found new spin-offs or business units that specialise or responsible for new startup business ventures, new technologies, and innovative business ideas, which attract and/or attain entrepreneurial mindsets into the company, that is, intrapreneurship. Last, we have seen companies replacing their legacy systems and manual labour with automation tools such as, physical robots, Artificial Intelligence (AI), Machine Learning (ML), and Robotic Process Automation (RPA). The pandemic also disrupted the supply chain of human workforces as many chose not to return to their original firms and switched to become smart farmers, entrepreneurs, or online merchants. MK restaurant group, for example, with more than 700 stores under the group brand was particularly affected by the pandemic and lockdown restrictions. The supply chain was adversely affected, and the workers (servers) did not return to their jobs even when the pandemic situation was better. Through swift decision-making and investments in RTOs and startups that specialised in automation robots, the company was able to solve the inadequate workforce issue by employing robot servers at the stores lacking human staff.

Another important trend on the development of innovation is the transition towards Deep Tech innovations. Deep Tech has received more attention amongst academics, researchers, innovators, corporations, startups, and governments around the world as they are distinct from normal innovation and have the potential to disrupt and transform existing ecosystems (BCG and Hello Tomorrow, 2017; BCG and Hello Tomorrow, 2019; Hello Tomorrow and Bpifrance, 2019; SG Innovate, 2019; WIPO, 2021). Deep Tech innovations are research-based and have a low probability of success because the market is yet-to-be-defined (WIPO, 2021). Deep Tech startup, for example, Ricult, underwent a lengthy process of R&D (with extensive patent protection) to address global challenges by offering new solutions usually comprising of a combination of hardware and software. It has come to our attention that many corporations in Thailand have moved towards Deep Tech by internalising innovation units, partner with others using open innovation processes, or by means of merger and acquisition (M&A) or investments using their corporate venture capital arms. More importantly, most of the initiatives in Deep Tech are not limited to the corporation’s original field of expertise or industry, that is, their competitive advantage, but lies outside their business scopes; thereby, expanding their future business opportunities.

COVID-19 and the Decentralisation of Innovation System

The macro-level innovation policy reforms and the changing roles of government agencies paved the ways for the decentralisation of innovation policies as stipulated by the mandates of NSC. However, incidents, such as COVID-19, have brought new challenges and acted as the main catalyst for changes in the innovation ecosystem around the world, let alone in Thailand. Firms needed to reconsider their business value chains and evaluate the new needs of consumers in the New Normal era. The Royal Thai government has inherently shifted the policymaking and adopted the idea of public–private partnerships to both domestic and global stakeholders, in the hope to shorten the innovation creation lifecycle, to create the right innovation just-in-time for its use, that is, opting for decentralisation. Many government agencies assume the role of facilitator and system integrator of the building blocks for the innovation ecosystem; for example, students, innovators, funding agencies, or Research and Technology Organizations (RTOs). Nevertheless, traditional policy planning and understanding of startups might not suffice to provide the adjustments needed in the post-COVID-19 epoch.

In terms of policymaking, Thailand has adopted more integrated approach and aims towards the digitisation of data. The government flagship ‘PaoTung’ (literally translates to ‘wallet’) e-wallet application was built to support economic boosting campaigns such as Kon-La-Krueng (literally translates to ‘each person pays a half’), where the government subsidises half of the shopping expense to the consumers, to ease the cost burdens to the people and business owners affected by the pandemic. This resulted in a vast majority of business owners, street vendors, or online merchants digitising their businesses, open online accounts, and offer electronic and cashless payments to consumers. The government then receives the visibility regarding the cash and tax movements in the economy, where it is estimated only between 10% and 20% of SMEs with tax obligations actually paid their taxes. It is presumed that between 30 and 40 million Thais have experience using PaoTung application. PaoTung application has since progressed to become a Super App, but also has been heavily scrutinised of the lack of stability and transparency in terms of application usability and funding in their early days. Local online shopping platforms took the initiative to adapt their platform and provided the consumers with a better user experience, for example, allowing the Kon-La-Krueng campaign to be used with online food deliveries during the lockdown and travel restriction periods, a feature that the government-backed application was only to provide (by working with the local operators) almost a year after the private sector. These rapid changes and adaptations to government policies could also be found in startups and corporations related to the sector severely affected by the pandemic such as healthcare, logistics, finance, and manufacturing.

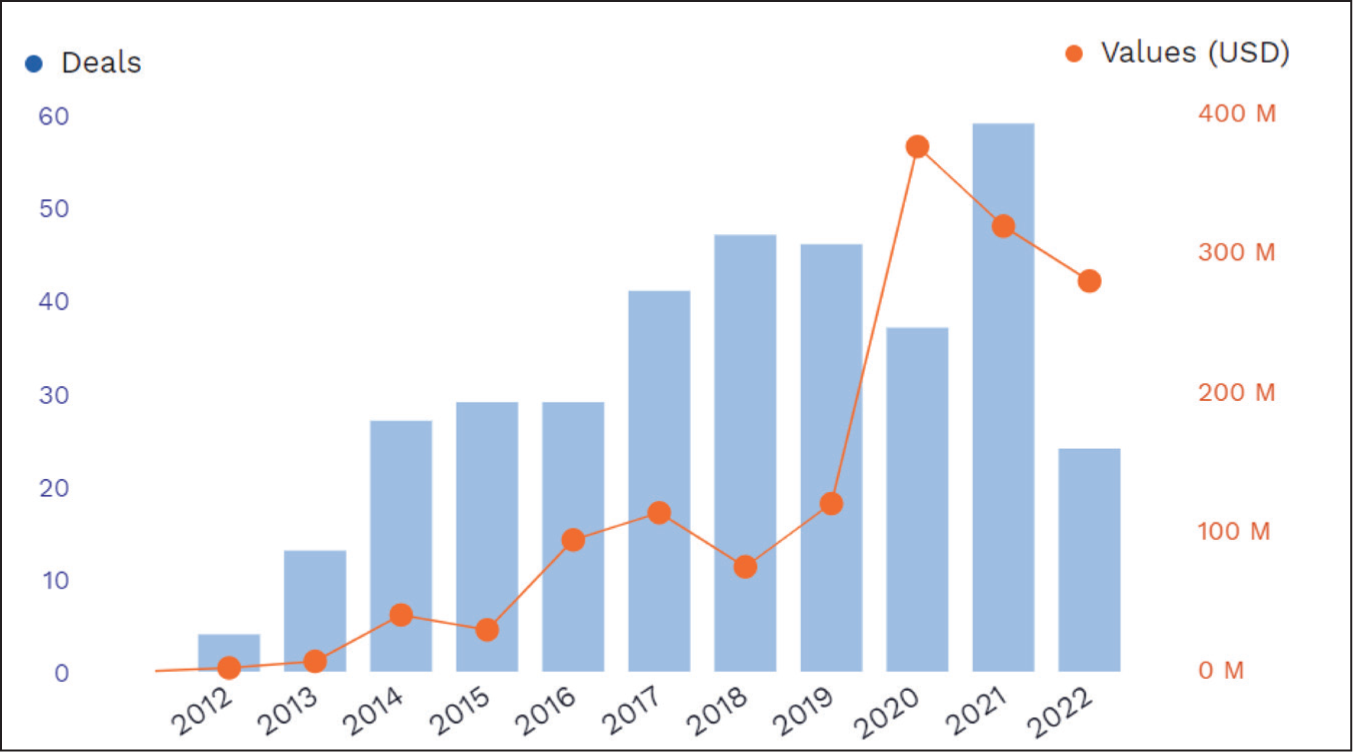

As can be seen from Figure 1, during 2012 to 2016, the deal valuations for startups in Thailand rose sharply from US$2.6 million to US$94 million, an equivalent of approximately 36× growth rate. There were 102 deals during the period totalling to US$175 million, the average deal size rose from US$0.65 million to US$3.25 million in 2016. The year 2017 marked the first time that any startups raised more than US$20 million, aCommerce (e-commerce) at US$65 million, and SYNQA (formerly known as Omise, Fintech) at US$25 million. In 2020, the total disclosed deal value broke through US$300 million for the first time, largely due to Series D funding of Flash Express (logistics), at US$200 million. The Thai startup ecosystem shows resilience despite the post-COVID-19 complications, and the total amount of funding stands around US$280 million during the first half of 2022.

Corporates have significantly contributed to driving Thailand’s startup ecosystem. These contributions can be categorised into distinct waves of industry involvement. The initial wave began in 2012, with a focus on the telecom sector, prominently involving entities like InVent, Trueincube, and DTAC. The subsequent wave emerged in 2016, directing attention towards the banking sector. Key players in the Thai banking industry, such as SCB10X and the Government Savings Bank, actively participated in this wave. Wave 3, in contrast to its predecessors, takes on a different character as it becomes more decentralised and encompasses diverse areas. Notable participants in this wave include PTT, Thai Union, and BDMS. The value of corporate-backed deals in Thailand has consistently increased since 2018, rising from a total of twelve deals worth US$85.8 million to seventeen deals worth US$533.2 million.

Startup as the New Ingredient for Decentralisation of Innovation

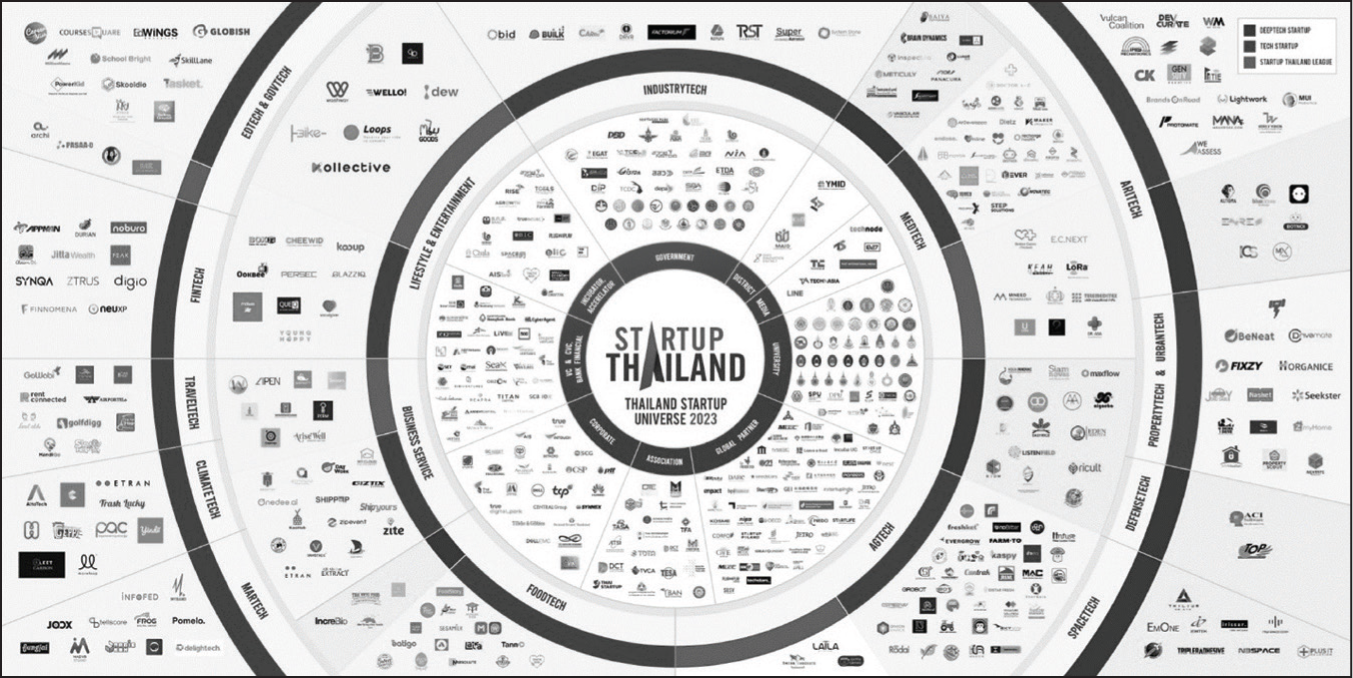

Although there is a dichotomy between centralisation and decentralisation of innovation ecosystem in Thailand, it is undeniable that the main mechanism that has been driving the cogwheel of innovation in the last decade comes from the public–private cooperation; especially, the initiatives led by large conglomerates and corporations. This requires the reformation of legislation, and the way government agencies operate, which are some of the main impediments to the development of the Thai innovation ecosystem. Indubitably, this explains why some of the Thai entrepreneurs chose to incorporate their startups abroad or why foreign startups might not have picked Thailand as the base of their operations. Figure 2 depicts Thailand’s startup ecosystem as of 2023.

The Rise of Corporate Venture and Thai Unicorns

One pivotal player in the decentralisation of innovation is the corporate venture capital (CVC), the investment entity that invests corporate funds directly into startups or businesses, to gain external know-how, customer bases, networks, to expand the corporate’s circle outside of its original ecosystem. Venture capital is an important factor in the innovation creation process, as it funds early-stage businesses that promises high expected returns but still experience high risks and uncertainties (Wonglimpiyarat, 2007). At the time of writing this article, there are at least 34 CVCs in Thailand’s startup ecosystem to date (Techsauce, 2022). Despite the pandemic, Thai CVCs continued to invest in startups, especially, those related to industries that had been transformed or spurred growth using COVID-19 as the catalyst. Krung Sri Finnovate the CVC arm of Bank of Ayudhya or ‘Krung Sri’, for example, closed seven deals in 2021 by investing in startups in different industries that address the global challenges: AppMan (insurance), Builk (construction), Chococard (business solution), Flash Express (logistics), Wisesight (MarTech), and Zipmex (blockchain). InVent, the investment arm of InTouch Holdings PLC., the parent company of Advanced Info Service (AIS), the largest mobile operator in Thailand, concluded four startup deals in business solution, EdTech, and construction. In 2021, we also observed a new cooperation between two large conglomerates SCB10X and Charoen Pokphand (CP) group, one of the largest conglomerates in Thailand with businesses in various industries such as telecommunications, automotive, finance, food/food processing, and retailing and wholesaling. A 50-50 co-ownership fund of approximately US$600–800 million was established, with the aim to invest in startups that specialise in disruptive technologies, for example, digital assets, FinTech, and other high-growth potential global startups. The duo was also related to Thailand’s first three unicorns in 2021―Flash Express (logistics), Bitkub (crypto exchange), and Ascend (digital finance). These three unicorns are currently operating their business. SCB10X directly invested in Flash Express along with other investors and had the plan to acquire 51% shares in Bitkub, potentially increasing its valuation to unicorn tier, but have been cancelled after due diligence investigation has been finished in August 2022. Ascend is the digital finance arm of CP group, that operates the ‘True Money’ e-wallet platform with more than 20 million users, received fundings from Bow Wave Capital Management and Ant group, driving the valuation to US$1.5 billion. Looking ahead, there is an anticipation that emerging high-potential technology sectors, such as BioTech, MedTech, ClimateTech, Generative AI, and FinTech, will consistently garner increasing interest.

From the government sector, there are a few examples of entities that operate as and promote the establishment CVCs. NSTDA Investment Center (NIC) is the investment arm of the National Science and Technology Development Agency (NSTDA) that invests in startups, especially those in the early commercialised stages in scientific and technology-based industries/applications that are deemed beneficial for the advancement of the Thai economy. Internet Thailand Public Company Limited, for example, received support from NIC in their early days, was the first company that provided commercialised internet services in Thailand and now expanding their services to new technologies such as cloud infrastructure, Robotics Process Automation (RPA), and big data analytics. Second, NXPO has provided guidelines for ‘University Holding Company’, UHC, or the idea to create an investment arm for universities governed under MHESI in December 2021. Traditionally, universities in Thailand have mandates and obligations in terms of education, regional developments, or workforce capability improvement, but not mainly focusing on finance or profit-making initiatives. Some universities, for example, Chulalongkorn University, began to incorporate a separate holding company called CU Enterprise as its own investment arm. UHC allows universities to utilise the existing innovation ecosystem, and inflow capital to create startups, spin-offs, and innovation-driven enterprises (IDEs). In addition, this would foster cooperation between researchers and external investors both domestically and abroad. This type of CVC would be beneficial for the innovation ecosystem that relies heavily on natural sciences, deep tech, and frontier research because the gap between research and use-case becomes narrower. NXPO, with the cooperation with NIA, is on the process of reviewing and preparing relevant regulation reforms by early 2022 for the interested universities under MHESI to roll out UHC by the first half of 2022, and plausibly expanding to other universities in the rest of the country later.

Innovation District and Corridor

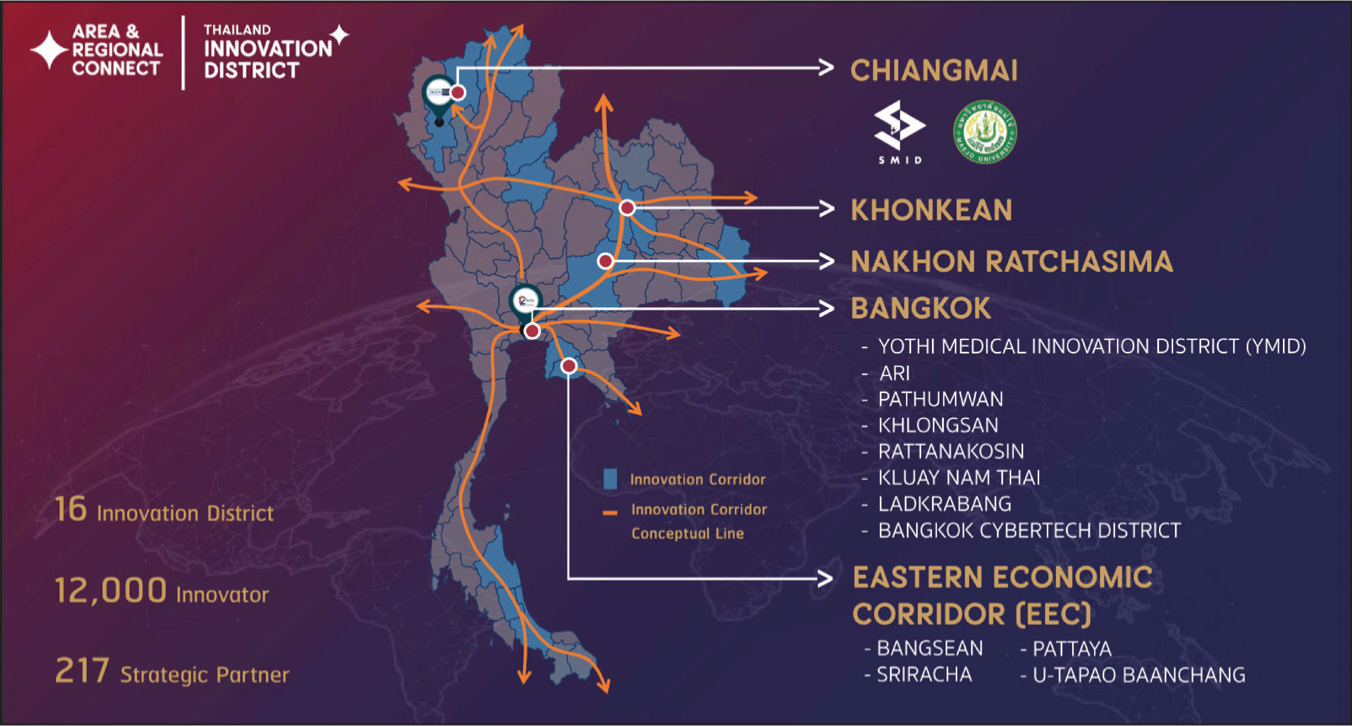

The innovation district is the area where there is extensive use of innovations, with innovators aiming to add value, allocate resources, and actively participate in activities to bring about changes (Katz et al., 2017). The innovation district has three dimensions: the network of innovation developers, the actual service and innovation business, and the physical infrastructure and innovations that facilitate business or the centre of product development (VoiceTV, 2018). Recognising the importance of spatial innovation and the involvement of various sectors (Markman, 2012), NIA has adopted the innovation district concept to create and promote innovative businesses that focus on the development of the area and create activities to attract research to commercialisation and investment, from inside and outside the country through financial and non-financial tools that facilitate business promotion and improve quality of life following the context of the area (Guillen, 2013). To create a framework for developing innovation districts that align with the identity and context of potential innovation districts, NIA has conducted a pilot project to develop eighteen innovation districts in Thailand (see Figure 3).

In NIA’s Innovation District Framework, an innovation district is an area that has anchored research institutions, clusters of businesses, startups, business incubators and accelerators, and infrastructure suitable for innovation ecosystem development. NIA’s Innovation District also incorporates sustainable development, smart city, and transit-oriented development (TOD) concepts during the design of the district blueprint, and subsequent support or promotions from relevant agencies. By integrating networking, economic, and physical assets, the innovation ecosystem can be attained. The location of execution of this concept can play a vital role in developing a successful innovation ecosystem. The ideology can be conceptualised in a matrix as depicted below. Currently, there are fifteen innovation districts in Thailand which consisted of the Yothi Medical Innovation District, Ari, Pathum Wan, Khlong San, Rattanakosin, Kluai Nam Thai, Ladkrabang, Bangkok CyberTech District, four areas in EEC, Chiangmai, Khon Kaen, and Nakhon Ratchasima.

Each innovation district has different goals and contexts: medical and health technology area (Yothi, Suan Dok), robotics–artificial intelligence–immersive technology area (Ari, Punnawithi), agriculture technology area (Mae Jo), creative economy technology area (Rattanakosin and Si Chan), and so on. Investments and grants are the financial mechanisms that drive the development of innovative business projects in the area. The following are examples of non-financial mechanisms that are svital to the success of the innovation district development. First, there are incubation activities that allow for the collaboration between agencies involved in research and development, the private sector, in the form of a consortium cooperation network to develop skills and knowledge to create innovative businesses for entrepreneurs in the preliminary stages to create a transparent business and rapid growth. Second, are the accelerator programmes that focus on cooperation and networking at the global level. The objective is to accelerate the creation of startup enterprises to be ready and commercially capable, capable of expanding business in Thailand and growing in the international market. Programmes that allow the platform to connect startups from different countries to access the Thai startup ecosystem and be a catalyst for creating a new generation and more diverse. Last, the City Lab and Hackathon event allows local regulators to use Thai startup services, reducing the restrictions on government procurement and increasing opportunities or experiences to benefit the city and the local people.

On a larger scale, the Eastern economic corridor (EEC) is another special economic and innovation promotion zone, covering the perimeter of three provinces in the eastern part of Thailand: Chachoengsao, Chonburi, and Rayong, which occupies around 13,266 km2 of land. The goal of EEC aims to achieve: Sustainable area-based development, Comprehensive Infrastructure and Connectivity, and the promotion of advanced technology and innovation. EEC has devised seven promotion zones for different schemes – EECh (High-Speed Rail), EECi (Innovation Platform), EECtp (Tech Park Ban Chang), EECa (Eastern Airport City), EECmd (Medical Hub), EECd (Digital Park), and EECg (Genomic Thailand). As the EEC model requires highly skilled labour which is estimated to be around 475,668 FTE (full-time equivalence). The EEC model not only innovates ideas but also focuses on human capital development at two levels: Vocational levels (Long term course) and type B (Short course).

From Digital Economy to Data Economy

Digital economy refers to the incorporation of digital technologies in socio-economic activities. The interconnectedness of people resulting from digital transformation, online commerce, and New Normal lifestyles are some of the enablers of digital economy. In Thailand, the concept of digital economy has been reflected in the NESDB plans and other ministerial notifications since mid-2010s. Two governmental organisations that have direct responsibility in building digital economy ecosystem are Digital Government Development Agency (DGA) and Electronic Transactions Development Agency (ETDA). With the plan to fully digitalise all state agencies by the end of 2022, DGA oversees the digital transformation of government agencies services and ensures that there would be no service loopholes or transgressions during the change. EDTA, on the other hand, is focused on practical issues; for example, ease of doing electronic transactions, the prevention of frauds or cyber-related crimes, and digital rights and governance. Nevertheless, many of the recent notable digital transformation journeys are related to the pandemic and megatrends such as increasing health consciousness. ‘Samitivej Virtual Hospital’ from Samitivej Hospital, part of Bangkok Dusit Medical Services (BDMS) group, for example, enables home vaccination, medicine delivery, blood collection, and 24–7 online medical consultation. Panacura is a Thai startup that specialises in precision health. It combines high-tech medical diagnostics and techniques such as DNA scanning, genome scanning, and immune systems scanning, to deliver medical consultation and awareness to customers, corresponding to the need for illness/health prevention manoeuvres rather than health curing.

The backbone of the digital economy lies a plethora of data―private, non-private, and data arisen from the analytics of user data obtained with or without the consumers’ consents. Cashless society, touch less society, and the switch to online transaction behaviour of consumers are some of the drivers of the so-called data economy, the economy revolving around the valuation and monetisation of consumers’ personal data. In this regard, Thailand has drafted its own Thailand’s Personal Data Protection Act (PDPA), which would be enforced in mid-2022 (postposed from mid-2021 to allow businesses affected by COVID-19 to adjust themselves). Thailand’s PDPA resembles EU General Data Protection Regulation (GDPR) but consists of additional protection coverage on several topics such as for historical, research, scientific, or statistical analyses. Large private corporations in Thailand particularly those in the banking and online retail sectors, have prepared and enforced their own equivalent PDPA practices long before the enactment of Thailand’s PDPA. This symbolises that the private sector has been researching and preparing for the PDPA implementation beforehand, to fully reap the benefits of data economy. 7-Eleven Thailand, for example, is the largest convenient store chain in Thailand with more than 12,000 stores (as of the time of writing) enforced data protection practices for their transactions (online and offline) since before the enactment date of Thailand’s PDPA in mid-2022. The government ‘PaoTung’ (Thai word for a wallet) super app has also implemented relevant data protection practices several months after its initial launch to comply with the PDPA and ease the public’s scepticism about the government’s private information misuse. The decentralisation of innovations in the realms of data privacy and management provided the insights to the relevant agencies in managing data in the age of the data economy.

Entrepreneurial University and New Generation’s Mindset

Universities have been an important engine in economic development. Traditionally, the university’s major role was to supply research and development capabilities and academic research (Mowery, 2022). Presently, universities came up with a University Business incubator (UBI) to further support entrepreneurial development by providing mentoring services, venture formation, and equipment similar operating model of an incubator programme. Leading universities in Thailand operating in this model like Mahidol University, Chulalongkorn University, and King Mongkut’s University of Technology, which report to the Ministry of Higher Education, Science, Research, and Innovation (MHESI), have shown that this type of programme has proved to be successful in supporting innovation (Wonglimpiyarat, 2016). Besides, a specialised university that provides entrepreneurship education also helps generate entrepreneurial attitudes among graduates to in turn promote the entrepreneurship industry (Karimi et al., 2010).

With the rise of young entrepreneurs in Thailand, new generations in Thailand have a high tendency to pursue entrepreneurship compared to the previous generations. The demographics studied in the literature prove this with a high percentage of attitude towards entrepreneurship in the age of 21–30 at 66.3% compared to the data of the previous generations in Thailand (Soomro et al., 2021). Entrepreneurship has been the new generation’s choice of career as people are more well-informed and aware of the startup industry and venture capital has been now more approachable to the public, and an infrastructure that supports entrepreneurial mindset from the triple helix system and specialised government agencies. Track records from new generations founded by startups in this era also motivated the new generation to take this path.

Thus, the entrepreneurial university concept has been adopted more widely in the ASEAN’s community, let alone Thailand, to adapt to the rise of neo-liberalisation of the world order and increasing capitalism structure in nations. The entrepreneurial university concept aims to create a structure that can survive in complex and unpredictable situations by liberating the university to conduct teaching, research, and dissemination of knowledge. The university will undertake higher education policy as a subset of the economic policy as the university has to deal with the market directly hence it is expected to behave accordingly (Chao, 2019). There are 48 universities in Thailand that have been categorised as entrepreneurial universities.

To drive the growth of national GDP, innovation, and market competitiveness, the Thai government focused on the development of the entrepreneurial university in Thailand which spans all the regions in Thailand, that is, Northern, Northeastern, Eastern, Centre, Southern-most. Moreover, to boost young entrepreneurs, the Startup Thailand League (STL) programme was created with the goal of instilling entrepreneurship spirit among students. The programme includes mentorship to help the students develop a feasible business model innovation. The programme comprises two main leagues which are U-League and R-League. U-League is designed for university students while R-League is exclusively for vocation studies. At the time of writing, there are thirty-five universities in Thailand that have joined the entrepreneurial university ecosystem in across the country.

Previously, the university mandates did not approve universities to undertake investment initiatives nor to establish spin-offs or own startups. Some entrepreneurial universities in Thailand have improved their own flexibility and agility, in terms of startup and innovation investment, through the University Holding Company (UHC) mechanism. Under UHC, the universities can properly manage their investment in high-risk entities, that is, startups and spin-offs, while maintaining their original role as educators, and unsure that entrepreneurial scientists have the option to resume their tenure should the spin-off they ventured into did not go as planned. The holding company allows them to work with startups directly to effectively commercialise innovation and utilise funding. Examples of Thai universities that have adopted the UHC model include Chulalongkorn University’s Chula Enterprise. The structure of the holding company will enable the country to drive tech companies in Thailand, that is, startups, smart SMEs, and IDEs to the next level. There are also concerns about technology transfer fees and return on investment from the university holding company as some might not be familiar with the risk appetite and risk structure of innovation investment projects. At the time of writing leading Thai university with UHC or equivalent structure includes Chiang Mai University (Chiang Mai) Chulalongkorn University (Bangkok), and Khon Kaen University (Khon Kaen). In terms of operating model, these universities often embody departments that are specialised in venture creation such as Innovation Hub at Chulalongkorn University and Regional Science Park, which is a one-stop-service structure to promote innovation in a specific region. These universities often partner up with government agencies and medium-to-large corporations to initiate and execute activities to support young entrepreneurs. These networks of collaboration create a complete loop for students to experience and nurture their skills as well as create opportunities for each venture.

Deep Tech Startup

As we elaborated above, Deep Tech has received many attentions from both public and private sectors in recent years. For our context, NIA defines a Deep Tech startup prerequisite as follows: (1) is based on arduous scientific research and development (>5 years from ideation stage), (2) utilises multidisciplinary technologies to tackle global challenges and megatrends, (3) is protected by intellectual property and hard to be imitated, and (4) creates new market breakthrough and business disruption domestically or abroad. By using these definitions, Deep Tech startups could be easily distinguished from normal tech startups as the probability of research success of Deep Tech is considerably lower than normal tech startup. This is because the market for the applications, products, or services derived from Deep Tech research could not be concretely determined during the R&D phases hence the more uncertainty. Further, the requirements and needs of the stakeholders in the Deep Tech startup ecosystem are different than traditional startups. As Deep Tech solutions often utilise multidisciplinary concepts and techniques, researchers in the ecosystem are encouraged to share their knowledge across fields, that is, adopt open innovation approach. Many of the Deep Tech startups combine the use of software, hardware, and advanced scientific research know-how, thus promoting the collaboration and decentralisation of innovative ideas and concepts into different parties involved in the ecosystem.

Furthermore, Deep Tech research and solutions pave the way for decentralisation of innovations rather than abiding to the traditional centralisation of innovation-related policies and support schemes. Deep Tech startup journey often starts by bridging urgent global challenges with fundamental research in RTOs. This is more resilient and adaptive to changes in the environments than following solely on National Strategy or other long-range plans that would take time to adjust to new challenges. For example, the metaverse and the forthcoming industrial applications were not included in any of the long-range plans but have urgency and direct impact to the development of innovations now. Only by decentralising innovation development would allow us to design the right innovations to address global challenges at the right moments. Tokenine, DomeCloud, Metaverse Thailand, and Jenosize are some of the metaverse experts in Thailand’s startup ecosystem that have cooperation with NIA that provide recommendations for the designing of relevant metaverse policies in Thailand. Lastly, the decentralisation of innovations resulting from the development of Deep Tech opens the opportunities for Thai startups or corporations to address the global value chain of innovation issue. As Deep Tech is highly rooted in the open innovation and innovation sharing paradigm, the stakeholders in the Deep Tech ecosystem would have a clearer supply chain visibility of the ecosystem. The bottleneck of Deep Tech research, for example, components, machines, and cell solutions, that are in high demand could be identified and domestic startups could fill in the country’s capability gap to mitigate future global supply chain problems.

Conclusion

Thailand’s startup ecosystem, like any organisms, undergoes the evolution process. During the past decade, we have seen the shift from founder-led innovation journey, centralisation of public policy, to large corporation-led innovation movements during the pandemic. We argue that, for the Thai economy to be resilient and recover from the economic downturn after COVID-19 or future challenges, decentralisation of innovation propelled by startups is needed. This could be in the forms of CVCs promotion, innovation district establishments, Deep Tech startup supports, or the transformation to data economy as earlier presented. Decentralisation, open innovation, and ‘open’ ecosystem are more advantageous than centralisation because the collective ideas and perspectives outperform internal innovation processes and respond to external changes better than the longer-term innovation policies set by the central government. In addition, the pivotal takeaway of the startup ecosystem development in Thailand is that without public–private (and civil society) participation, we could not have shaped the ecosystem into its current form today.

From the perspectives of NIA as the startup ecosystem integrator and supporter in Thailand, there are a few challenges and avenue for improvements and research. First, to respond to unexpected changes or disruptions such as the emergence of an unknown epidemic, sudden breakthroughs in STI, or paradigm shifts of consumer behaviours, we need to find a system that consistently build firm and human resources capability, in such a way that the startup ecosystem would not be susceptible for such changes. Second, we need to ensure that the innovation infrastructure that we are designing, offer sufficient and right support for those needed. Particularly, during the post-COVID era, new forms of collaboration activities are needed such as regionalisation or internalisation of innovation systems. Third, we need to constantly monitor any legislation requirements that would hinder the development of innovation processes or services, and reform them to create innovation-friendly regulatory ecosystem that would ease the innovation journeys of all the stakeholders.

Footnotes

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.